The 2023 Long-Term Outlook

for the Federal Budget

Each year, the Congressional Budget Office provides the

Congress with its projections of what the federal budget and the

economy would look like over the next 30 years if current laws

generally remained unchanged.

Those projections show the estimated effects of demographic

trends, economic developments, and health care costs on federal

spending, revenues, deficits, and debt.

For details about the projections in this section, see Congressional Budget Office, The 2023 Long-Term Budget Outlook (June 2023), www.cbo.gov/publication/59014 .

2

Total Deficits, Primary Deficits, and Net Interest

Primary deficits, which

exclude net interest costs,

equal 3.3 percent of gross

domestic product (GDP) in

both 2023 and 2053.

Combined with rising

interest rates, those large

and sustained primary

deficits cause net outlays for

interest to almost triple in

relation to GDP.

3

Federal Debt Held by the Public

In CBO’s projections, debt

rises in relation to GDP over

the next three decades,

exceeding any previously

recorded level—and it is on

track to continue growing

after 2053.

4

Size of the Population Ages 20 to 64

in Relation to the Population Age 65 or Older

In CBO’s projections, the

number of people ages 20 to

64 measured in relation to

the number of people age 65

or older declines.

In particular, the number of

people in the younger age

group—who are more likely

to work and who generally

pay more in taxes—grows

more slowly than the

number of people in the

older age group—who are

less likely to work, generally

pay less in taxes, and are

generally eligible for Social

Security and Medicare.

5

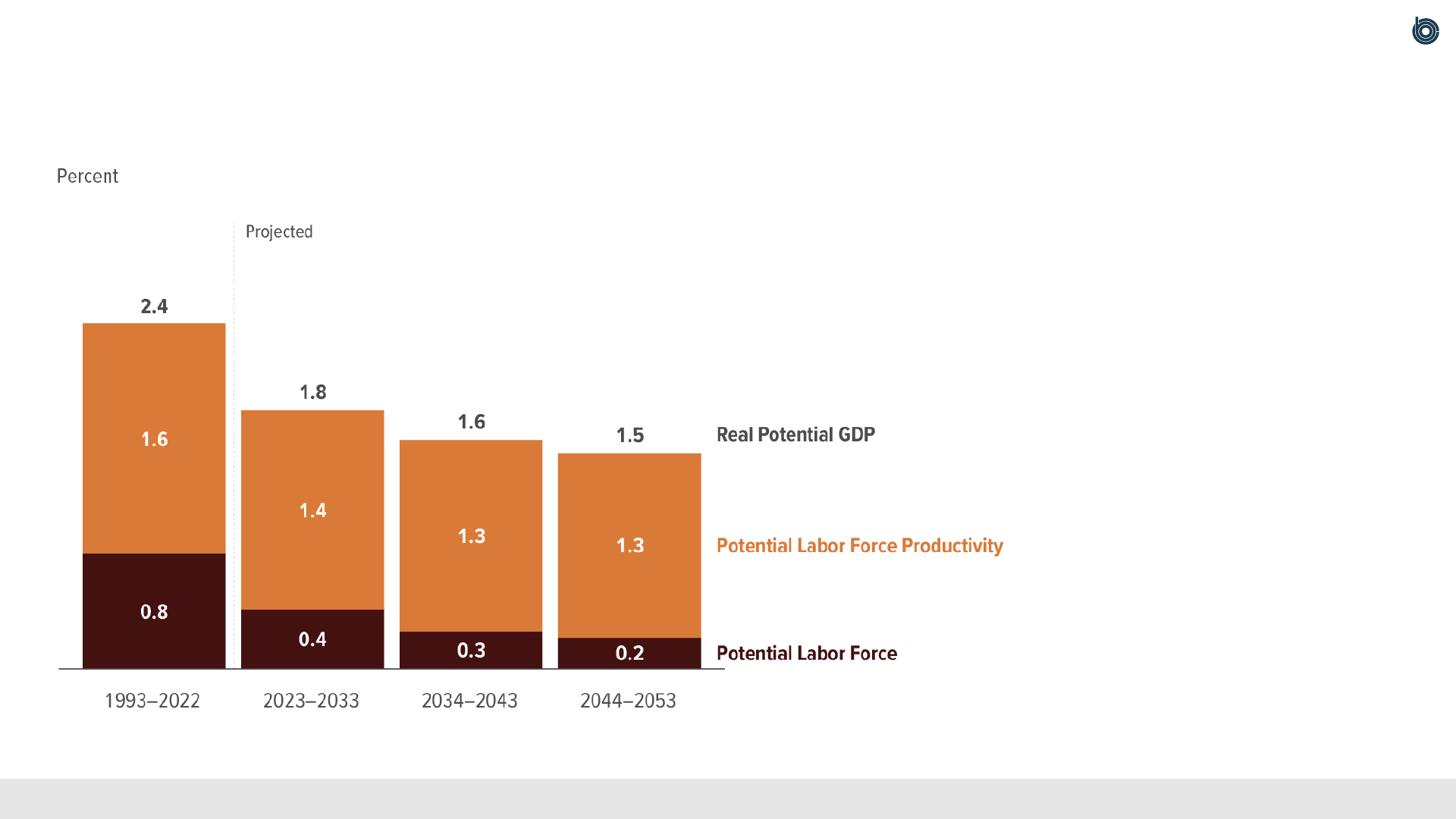

Real potential GDP is the maximum sustainable output of the economy, adjusted to remove the effects of inflation.

Average Annual Growth of Real Potential GDP

and Its Components

In CBO’s projections, real

potential GDP grows more

slowly throughout the

2023–2053 period than it

has, on average, over the

past 30 years.

That slower growth is

explained by slower growth

in the potential labor force

and in potential labor force

productivity.

6

Total Outlays and Revenues

In most years, growth in

outlays is projected to

outpace growth in revenues,

resulting in widening budget

deficits.

7

Outlays for major health care programs consist of spending on Medicare (net of premiums and other offsetting receipts), Medicaid, and the Children’s Health Insurance Program, as

well as outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and related spending. “Other Mandatory” consists of all

mandatory spending other than that for Social Security and the major health care programs. It includes the refundable portions of the earned income tax credit, the child tax credit, and

the American Opportunity Tax Credit.

Outlays, by Category

Rising interest rates and

mounting debt cause net

outlays for interest to

increase from 2.5 percent

of GDP in 2023 to

6.7 percent in 2053.

Outlays for the major

health care programs rise

from 5.8 percent of GDP to

8.6 percent as the average

age of the population

increases and health care

costs grow.

The aging of the population

also pushes up outlays for

Social Security, which

increase from 5.1 percent

of GDP to 6.2 percent.

8

Average Interest Rates

Interest rates—which, along

with primary deficits, help

determine net outlays for

interest—rise through 2053

but remain lower than they

have been, on average, over

the past three decades.

Projected interest rates

remain below that average

for several reasons,

including slower growth of

the labor force, an increase

in savings available for

investment, and slower

growth of total factor

productivity.

9

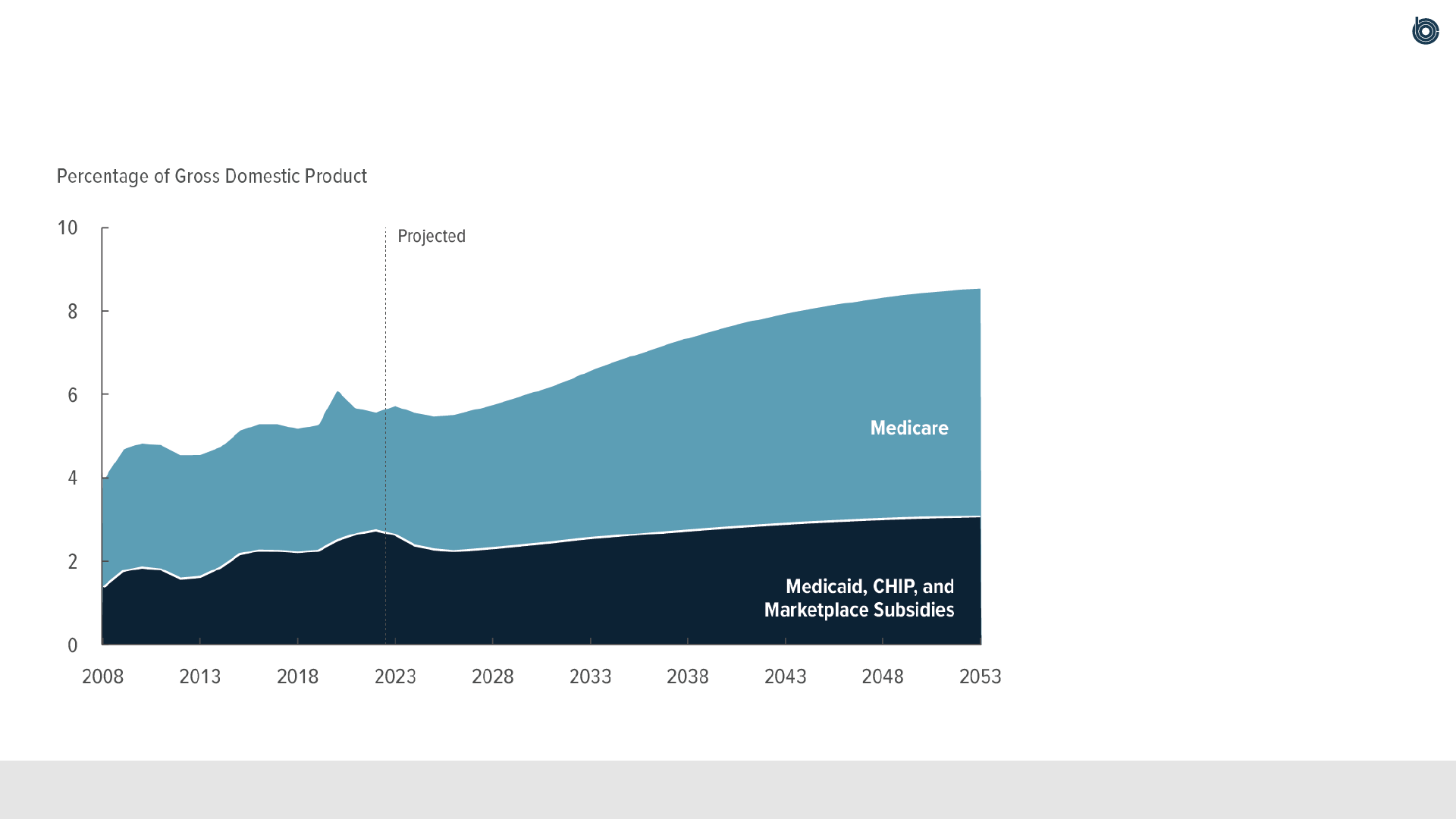

Outlays for Medicare are net of premiums and other offsetting receipts. “Marketplace Subsidies” refers to outlays to subsidize health insurance purchased through the marketplaces

established under the Affordable Care Act and related spending. CHIP = Children’s Health Insurance Program.

Composition of Outlays for the Major Health Care Programs

Spending on Medicare is

projected to account for

more than four-fifths of the

increase in spending on the

major health care programs

over the next 30 years.

10

The spending on the major health care programs examined here consists of gross spending on Medicare (which does not account for premiums or other offsetting receipts), Medicaid,

and the Children’s Health Insurance Program, as well as outlays to subsidize health insurance purchased through the marketplaces established under the Affordable Care Act and

related spending. Additional cost growth is the extent to which the growth rate of nominal health care spending per person (adjusted for demographic changes) exceeds the growth

rate of potential GDP per person. Potential GDP is the maximum sustainable output of the economy.

Composition of Growth in Outlays for the

Major Health Care Programs and Social Security

Growth in spending on the

major health care programs

is largely driven by cost

growth above and beyond

that accounted for by

demographic changes or the

growth of potential GDP per

person. Spending on those

programs, as well as

spending on Social Security

benefits, is also boosted by

the aging of the population.

11

Revenues, by Source

From 2023 to 2053, total

revenues, measured as a

percentage of GDP, grow by

about 1 percentage point.

Individual income taxes

account for nearly all of

that growth.

Receipts from payroll and

corporate taxes decline by

small amounts in relation to

GDP over the 30-year

period.

12

Key Factors Contributing to Changes in Revenues

The largest source of growth

in revenues is real bracket

creep: As income rises

faster than prices, a larger

proportion of income

becomes subject to higher

tax rates.

After 2025, another source

of growth in revenues is the

scheduled expiration of

certain provisions of the

2017 tax act.

Other factors partially offset

those effects. In 2023 and

2024, for example, revenues

fall in relation to GDP as a

temporary boost to tax

receipts observed in recent

years abates.

13

CBO’s economic projections are subject to a high degree of uncertainty. For

instance, the possibility that growth in the labor force or in productivity could be

faster or slower than expected makes CBO’s projections of labor market

conditions and economic output uncertain. Other key sources of uncertainty are

future monetary policy and the path of interest rates.

CBO’s long-term demographic projections are subject to significant uncertainty

because, compounded over many years, even small changes in rates of fertility,

mortality, or net immigration could greatly affect outcomes later in the projection

period.

Uncertainty of CBO’s Long-Term Projections

14

Alternative Scenarios

CBO analyzed eight scenarios that differ from those underlying its

long-term baseline budget projections—six that vary economic

outcomes and two that vary spending or revenues.

For details about the analysis in this section, see Congressional Budget Office, The Long-Term Budget Outlook Under Alternative Scenarios for the Economy and the Budget

(July 2023), www.cbo.gov/publication/59233

.

15

Total factor productivity growth is the growth of real output (that is, output adjusted to remove the effects of inflation) per unit of combined labor and capital services in the nonfarm

business sector.

Federal Debt Under the Baseline and Two Scenarios

in Which Total Factor Productivity Growth Differs

If the productivity of labor

and capital in the nonfarm

business sector grew

0.5 percentage points per

year faster or slower than

CBO projects, federal debt

held by the public in 2053

would equal 137 percent of

GDP or 228 percent of GDP,

respectively.

16

In the higher-interest-rates scenario, the average interest rate on federal debt is boosted above the rate underlying CBO’s extended baseline by a differential that starts at 5 basis

points in 2023 and increases by 5 basis points each year (before macroeconomic effects are accounted for)—that is, the interest rate is 5 basis points higher than the baseline rate in

2023, 10 basis points higher than the baseline rate in 2024, 15 basis points higher than the baseline rate in 2025, and so on. In the lower-interest-rates scenario, the average interest

rate on federal debt is pushed below the rate underlying CBO’s extended baseline analogously. A basis point is one-hundredth of a percentage point.

Federal Debt Under the Baseline and Two Scenarios

in Which Interest Rates Differ

If the average interest rate

on federal debt was above

or below the baseline

projection by an amount that

started at 5 basis points in

2023 and changed by that

amount in each year

thereafter, federal debt held

by the public in 2053 would

be 231 percent of GDP or

143 percent of GDP,

respectively.

17

Under the greater-sensitivity scenario, the effect of federal borrowing on private investment is twice as large as it is in CBO’s extended baseline. Under the less-sensitivity scenario,

federal borrowing has no effect on private investment.

Federal Debt Under the Baseline and Two Scenarios

in Which Private Investment’s Sensitivity to Deficits Differs

If government borrowing

reduced private investment

by twice as much as it does

in CBO’s long-term

projections or had no effect

on that investment, federal

debt held by the public in

2053 would exceed

250 percent of GDP or

would equal 145 percent of

GDP, respectively.

18

In the first scenario in which spending or revenues differ, discretionary spending

and revenues are at their 30-year historical averages as a percentage of GDP

between 2023 and 2053.

Under that scenario, discretionary spending would equal 7.1 percent of GDP and

revenues would equal 17.2 percent of GDP in every year, 1.4 percentage points

more and 1.2 percentage points less, respectively, than they average in CBO’s

extended baseline projections.

The Historical Rates Scenario

19

CBO’s extended baseline projections reflect the assumption that the Social Security Administration will pay benefits as scheduled under current law regardless of the status of the

program’s trust funds. That approach is consistent with the requirement that CBO’s 10-year baseline budget projections incorporate the assumption that funding for such programs is

sufficient to make all payments required by law. For additional discussion of a scenario in which the program continues to pay benefits as scheduled under current law, regardless of

whether the program’s two trust funds have sufficient balances to cover those payments, see Congressional Budget Office, CBO’s 2023 Long-Term Projections for Social Security

(June 2023), www.cbo.gov/publication/59184

.

In the second scenario in which spending or revenues differ, Social Security

benefits are limited to the amounts payable from dedicated funding sources after

the combined trust funds are exhausted (that is, their balances reach zero) in

fiscal year 2033.

To project the effects of that change, CBO estimated the total reduction in annual

Social Security benefits that would be necessary for the program’s outlays to

match its revenues in each year after 2033.

The Payable Benefits Scenario

20

Social Security Outlays and Revenues,

With Scheduled and Payable Benefits

In CBO’s projections, Social

Security outlays in a payable

benefits scenario are smaller

than in its extended baseline

projections. The required

reduction would amount to

25 percent in 2034 and

would rise gradually to

28 percent in 2053, relative

to the amounts in CBO’s

extended baseline

projections.

21

In the historical rates scenario, discretionary outlays equal 7.1 percent of GDP and revenues equal 17.2 percent of GDP over the entire projection period. In the payable benefits

scenario, Social Security benefits are limited to the amounts payable from dedicated funding sources.

Federal Debt Under the Baseline and Two Scenarios

in Which Revenues and Spending Differ

If, between 2023 and 2053,

discretionary spending and

revenues were at their 30-

year historical averages as a

percentage of GDP, then

federal debt held by the

public in 2053 would exceed

250 percent of GDP.

If, instead, Social Security

benefits were limited to the

amounts payable from

dedicated funding sources

after the combined trust

funds are exhausted in fiscal

year 2033, federal debt held

by the public in 2053 would

equal 132 percent of GDP.

22

CBO’s Preliminary

2024 Demographic Projections

Each year, CBO provides the Congress with its projections of what

population growth would look like over the next 30 years if current

laws generally remained unchanged. That growth is determined

by births, deaths, and net immigration.

For details about these preliminary projections, see testimony of Julie Topoleski, Director of Labor, Income Security, and Long-Term Analysis, Congressional Budget Office, before the

Joint Economic Committee, CBO’s Demographic Projections (November 15, 2023), www.cbo.gov/publication/59683

.

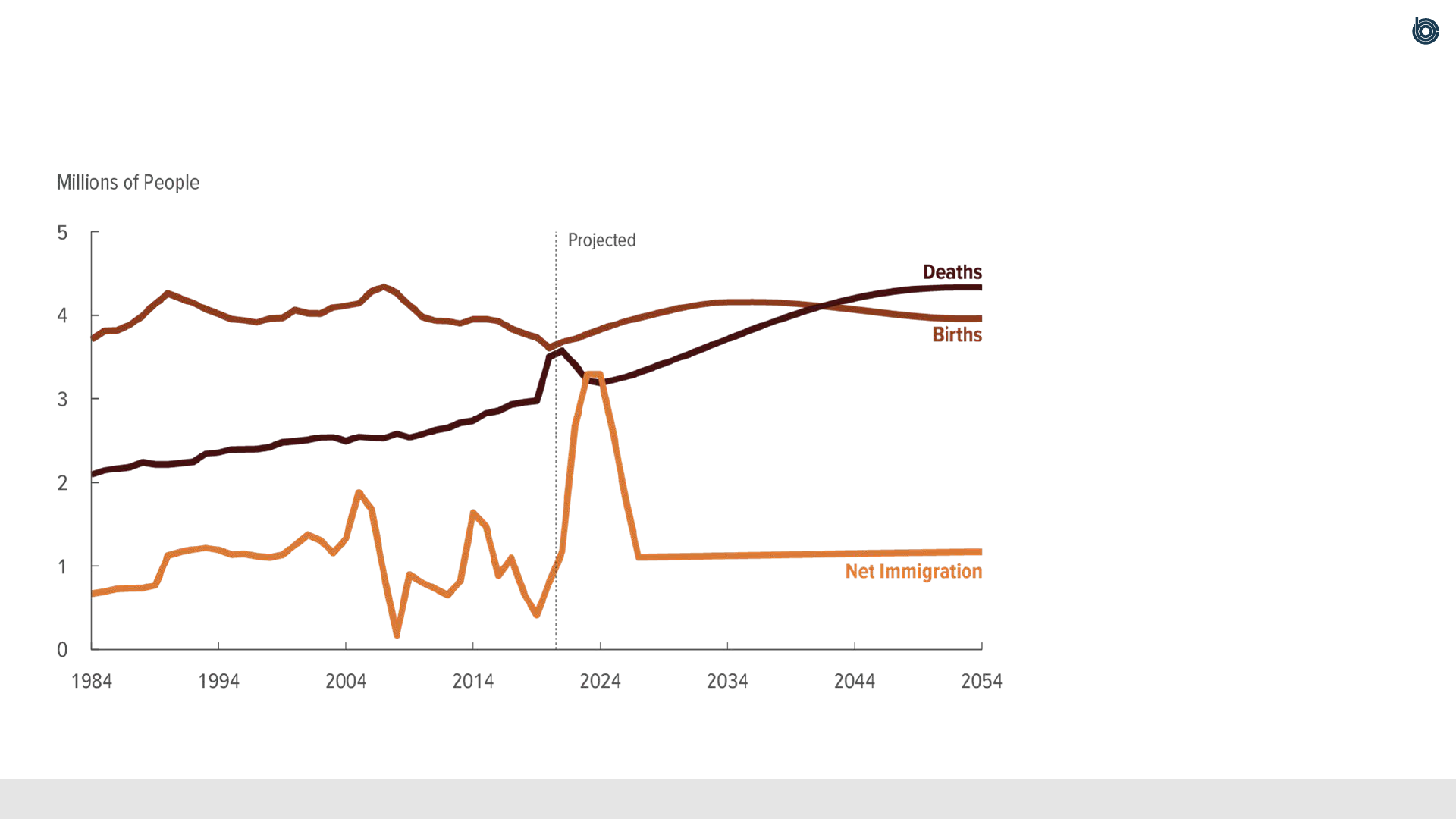

23

In CBO’s preliminary

projections, fertility rates

remain lower than the

replacement rate (the fertility

rate required for a

generation to exactly replace

itself in the absence of

immigration), mortality rates

generally continue to

decline, and immigration

becomes an increasingly

important part of overall

population growth.

Births, Deaths, and Net Immigration