1

CHAPTER 7

SOVEREIGN DEFAULT

Julianne Ams

*

, Reza Baqir

†

, Anna Gelpern

‡

and Christoph Trebesch

§

The views expressed in this paper are those of the authors and do not necessarily represent the views

of the IMF, its Executive Board, or IMF management.

*

Counsel, Legal Department, International Monetary Fund

†

Senior Resident Representative to Egypt, International Monetary Fund

‡

Georgetown Law and Peterson Institute for International Economics

§

Kiel Institute for the World Economy and Kiel University

2

This chapter reviews the phenomenon of sovereign default. We first define default, beginning

with an overview of existing definitions, highlighting their problems and limitations. Section

7.2 considers the sovereign’s decision to default, first, by creditor type, second, by the manner

of default (debtor action). We illustrate these with case studies of crises in Jamaica, Ukraine,

Uruguay, and Russia. Section 7.3 reviews the economic determinants of default, including

domestic and external shocks, and considers the legal determinants, which merit further

systematic study. Section 7.4 surveys the economic, financial and legal costs of default. Section

7.5 concludes with ideas for reducing the incidence and the cost of default.

7.1. Defining Default

7.1.1. The Definition Challenge: An Overview and Proposed Solution

1. It is surprisingly hard to define sovereign default. Default at its simplest is a broken promise,

or a breach of contract. For sovereign debt, such a breach could include a missed payment,

involuntary subordination, or data misreporting. The problem with defining default as a breach

of contract is that this is both too broad and too narrow to be useful. It is too broad because the

definition includes events that many would view as unimportant, such as minor delays in

transmitting paperwork. It is too narrow because it ignores the economic context of events such

as the Greek debt exchange in March of 2012, where no payments were missed and no

contracts were breached—they were modified instead—but creditors still faced deep losses in

a distressed debt restructuring.

2. When searching for a formal legal definition of sovereign default it is useful to start with those

listed under the heading “Events of Default” (EoD) in English- and New York-law debt

contracts

5

and their analogues in official bilateral and multilateral credit agreements. These

contractual EoD terms are designed to be observable, cover a broad range of factors that could

affect payoff, specify the consequences of breach, and are generally understood to be legally

binding for debtors and creditors.

6

For this reason, we first discuss the definitions of default

found in market instruments (bond and loan contracts) in Section 7.1.2, before considering

parallel definitions in official agreements in Section 7.1.3. We then examine domestic debt

instruments, which often fail to specify a clear-cut contractual definition of default, in Section

7.1.4.

3. Beyond debt contracts, we review definitions of default used by influential third parties, such

as the credit rating agencies S&P and Moody’s, and definitions used in the credit derivatives

market, where default covers both missed payments (breach of contract) and distressed debt

restructurings that involve losses for creditors. Third-party definitions are often pithier than

those found in debt contracts, and focus on economic substance (payoff). Third-party

5

Sovereign debt loans and bonds are private contractual obligations, enforceable in national courts to the extent

consistent with sovereign immunity.

6

In contrast, because official creditors do not normally sue sovereign debtors in national courts, the parties might

reasonably expect disputes to be resolved through diplomatic or administrative channels.

3

definitions of default can have major economic consequences, for instance, when they are used

to trigger credit rating downgrades or credit default swap (CDS) payouts. Many economists,

and the most widely used datasets on sovereign default, use rating agencies’ definition of

default (e.g., Reinhart and Rogoff 2009). We will discuss the definitions by rating agencies

and those guiding CDS payouts in sections 7.1.5 and 7.1.6, respectively. We do not cover other

potentially useful third-party markers, such as index inclusion, collateral eligibility, or

regulatory treatment, which may merit further consideration.

4. In practice, neither formal contractual nor substantive economic definitions are fully

satisfactory. For example, it is not obvious how to treat minor, short-lived contractual breaches,

such as administrative mishaps, brief payment delays and episodes of credit deterioration that

may entitle lenders to some contractual remedies, but are unlikely to bring about principal

acceleration or expose the debtor to successful lawsuits. Moreover, the rise in domestic-law

debt complicates matters for lack of clear contractual definitions of default, diversity of

background law, and sovereign authority over the law. On the other hand, purely economic

definitions entail drawing bright lines on a continuum of creditor losses; in some cases, creditor

losses are combined with judgments about sovereign debtors’ posture towards the creditors,

which can appear arbitrary or subjective.

5. To address some of these shortcomings, we propose an analytical approach that would

distinguish among technical default, contractual default and substantive default, as follows:

Technical Default includes any contractual EoD occurrence or equivalent for domestic

and official debt that does not also constitute default under third-party definitions, such

as those used by rating agencies and in standardized derivatives contracts.

Administrative errors and some covenant defaults viewed as minor by market

participants would fit under this heading.

Contractual Default includes the occurrence of any EoD or equivalent that also

constitutes default under specified reputable third-party definitions. As we will see,

virtually all definitions of default include payment default, subject to a grace period. At

a minimum, it is reasonable to consider missed payments and payment shortfalls that

persist for longer than 30 days (a typical grace period) as contractual default, regardless

of debt form and creditor identity. However, preemptive (pre-default) debt exchanges

and restructurings that follow contractual modification provisions would not fit this

definition.

Substantive Default includes debtor actions that would count as default in third-party

documentation and practice (in particular, a distressed debt exchange, or a restructuring

using local law or Collective Action Clauses (CACs), if it results in less favorable terms

for the creditor), but would not constitute an EoD under the underlying debt contracts.

Of course, restructuring also presents special process and policy challenges, further

explored in Chapter 8.

4

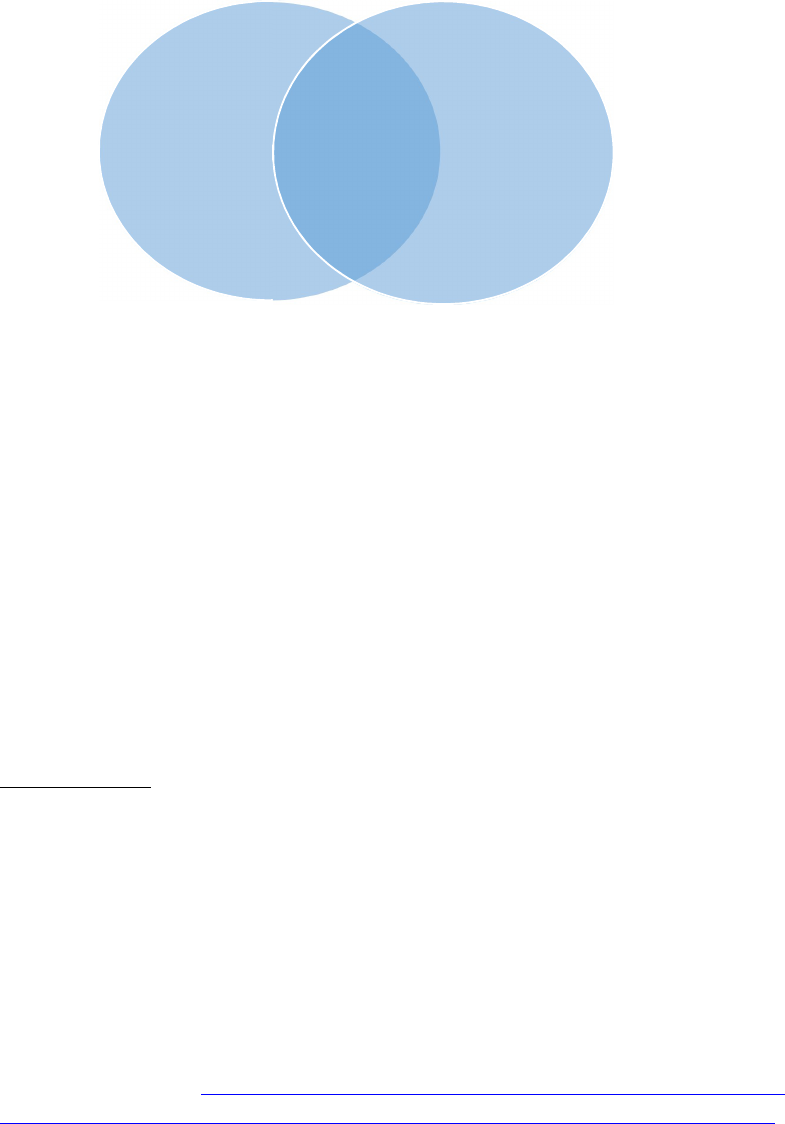

Figure 1 illustrates.

Figure 1: Defining Default

We find this approach appealing for its relative simplicity, as well as for its ability to account

simultaneously for internal contractual and outside market views of what matters in default.

The remainder of Section 7.1 will explore aspects of this definition—what are contractual EoD,

and how do third parties define default? Because the economic literature is rife with alternative

definitions, some of which conflate whether a debtor has defaulted with how that debtor goes

about restructuring, we consider the prevailing approaches to default and review of the relevant

literature in Section 7.2.

7.1.2. Contractual Events of Default: Market Instruments

6. The following categories of contractual EoD are typical in the sovereign debt markets in

London and New York:

Payment Default is failure to pay principal, interest, or other amounts (such as tax gross-

up) when due, after the expiration of any applicable grace period. Interest payments

typically enjoy grace periods ranging from 10 to 30 days. Grace periods are slightly less

common, and may be shorter, for principal payments (e.g., Gooch & Klein 1992,

Buchheit 2000 for loans; see Box 1 for examples from tradable securities).

The precise timing of payment default is significant and can be hard to ascertain.

Contracts typically say that payment is made when the debtor has transferred funds to

the paying agent, trustee, or clearing system (e.g., Gooch & Klein 1992, United Mexican

States 2012). However, some contracts do not consider a payment to be made until each

creditor has received the funds. For instance, Argentina’s 2005 and 2010 exchange

bonds specified that “the Republic’s obligation to make payments hereunder … shall

not have been satisfied until such payments are received by the Holders of this Security”

(Republic of Argentina 2005). The distinction between the debtor’s payment and the

Technical

Default:

e.g., minor

covenant

default

Substantive

Default:

e.g.,

distressed

restructuring

with haircuts

Contractual

Default:

e.g.,

nonpayment

for 30+ days

5

ultimate creditor’s receipt became salient when a U.S. federal court blocked Bank of

New York Mellon as trustee for Argentina’s exchange bonds from distributing the

government’s interest payment to the bondholders.

7

Repudiation happens when the sovereign rejects its obligation to pay, which could

happen before or after any payment is due. Governments typically avoid questioning

the validity of their debts, or announcing their intention not to pay before missing a

payment, since in practice, repudiation carries all the traumatic consequences of

payment default discussed in Section 7.4. Repudiation may go hand in hand with

governments questioning the legitimacy of one or more obligations. The literature on

“Odious Debt” includes a handful of examples (King 2016, Lienau 2014). In 2008,

Ecuador claimed that two bonds issued by a previous government were illegitimate and

pledged not to pay them. It launched a buyback offer the following year in the shadow

of the illegitimacy claim, and ultimately secured nearly 2/3 debt relief with more than

90 percent of the creditors participating.

Moratorium is a unilateral payment stop on one or more debt obligations. The sovereign

might announce a moratorium—as Mexico did in 1982 (Kraft 1984)—as an interim

measure before launching a debt restructuring; it might also stop payments indefinitely.

A moratorium entails a public act, such as an announcement or legislation, apart from

the missed payment, which can come before or after the payment default. However, it

need not contest the validity of the underlying obligation. A moratorium is distinct from

a negotiated payment suspension: if the creditors agree to a stop, they can waive the

payment default.

Policy-Related EoD may include loss of IMF membership or ineligibility to draw on

IMF resources. Such EoD have the practical consequence of incorporating elements of

the IMF Articles of Agreement and policies, and amplify the effect of its sanctions (e.g.,

Choi, Gulati & Posner 2012). Other policy-related EoD, such as maximum debt ratios,

are widespread in corporate debt but unusual among sovereigns. Notable exceptions

include Ukraine’s borrowing from Russia in 2014, which included a number of unusual

EoD designed to maximize creditor control and make it easy to trigger acceleration.

Because policy conditions are often at the heart of official lending, some forms of

multilateral policy conditionality are indirectly incorporated in contractual EoD by

reference to membership and sanctions.

Covenant Default is a residual category that captures breach of all other express

promises under the debt agreement (Box 1), ranging from clerical omissions to material

violations. The latter category might include effective subordination of creditors without

their consent, such as violations of the pari passu or negative pledge clauses. Covenant

defaults also include false representations, which could range from data misreporting to

7

Argentina had paid Bank of New York Mellon in violation of the court’s injunction designed to compel ratable

payment to holdout creditors whenever the exchange bondholders were paid.

6

lack of borrowing authority at the time the contract was made.

8

Subsequent loss of

borrowing authority is usually a separate EoD.

Cross-Default terms link two otherwise-unrelated debt contracts, so that default under

one becomes default under the other (Box 1). The theory behind cross-default is a mix

of early warning and inter-creditor equity. All else equal, missing payments to other

creditors points to debt distress. Without cross-default, a creditor may have no recourse

as others sue and divide up the debtor’s scarce assets among themselves.

Cross-default clauses vary in two important ways: trigger and scope. With hair-trigger

cross-default, creditors may exercise their default remedies in response to a minor

infraction under someone else’s contract. At the other extreme, they might have to wait

until creditors under the other contract have demanded immediate repayment in full.

Some versions of the clause excerpted in Box 1 include minimum thresholds for missed

payments on other debts. The scope of cross-default can range from a narrow sliver of

similar debt (e.g., foreign-law bonds cross-defaulting to foreign-law bonds) to all

sovereign and quasi-sovereign obligations, which is rare.

7. Four additional observations should help situate contractual EoD in the sovereign default

context:

First, EoD only give creditors the right to invoke contractual remedies; creditors are

under no obligation to do so. In prominent cases of selective default (see Section 7.2.2),

including most recently Venezuela, bond holders chose not to exercise their rights long

after the governments defaulted on other debt, preferring instead to get paid as long as

possible. If creditors do not act, the debtor may have an opportunity to “cure” the

default.

Second, a debt restructuring may not constitute a contractual EoD, regardless of creditor

losses. A market-based debt exchange, a voluntary renegotiation, or a majority vote to

change debt terms using collective action clauses (CACs) would either follow the

contract or circumvent it. Neither would breach it.

Third, EoD in sovereign bond contracts are increasingly subject to collective action

requirements. For instance, even if the government fails to make a scheduled interest

payment and the grace period expires, bond holders may have to muster a vote of at

least 25% of the principal to instruct the Trustee to accelerate. If the debtor later makes

up the payment, holders of at least 50% of the principal could instruct the Trustee to

reverse the acceleration (Buchheit & Gulati 2002).

Fourth, minor differences in EoD wording and procedural requirements, such as

notices, can lead to different consequences for the same debtor actions.

8

If there is no authority to borrow at the time the original debt contract was made, the contract could be void. In

the absence of an enforceable contract, creditors may still be able to sue for fraud.

7

8. It bears emphasis that contractual EoD found in London and New York do not supply a

complete definition of default for at least three reasons.

First, even “standard-form” debt contracts are not fully standardized. EoD vary over

time, between markets, across borrowers and across bonds and loans within a single

borrower’s debt stock.

Second, obligations governed by the law of the issuing sovereign, which make up the

bulk of the global sovereign debt stock and a growing portion of emerging market debt,

may not spell out EoD at all. Default and its consequences are a matter for background

law, which varies among legal systems (Addo Awadzi 2015; Austin 2015).

Third, as noted earlier and elaborated below, acts and omissions that are not specified

among EoD can have consequences functionally similar to those of EoD, and are widely

understood as default in the markets, and among the relevant domestic and international

official stakeholders.

7.1.3. Contractual Defaults on Official Debt—Suspension, Refund,

Acceleration

9. Official bilateral and multilateral credits resemble contractual EoD, but are structured

differently in important ways, reflecting the creditors’ mandates and, for multilateral creditors,

their character as membership organizations. We use the General Conditions of IBRD and IDA

(together, World Bank) loans, revised in July of 2017, to illustrate (World Bank Group 2017).

The General Conditions make a useful point of comparison to contractual EoD because the

World Bank is the largest multilateral creditor, because it has a global policy mandate, because

IBRD and IDA lend only to sovereigns or backed by sovereign guarantees, and because today’s

General Conditions have been revised many times to reflect the World Bank’s experience in

sovereign lending, including interaction between official and market finance.

10. The General Conditions are incorporated by reference in transaction-specific “legal

agreements” between the World Bank and its borrowing member; unlike the legal agreements,

General Conditions do not vary by borrower or by transaction.

9

Article VII of General

Conditions contains three potential analogues to contractual EoD: (i) events that would allow

the World Bank to suspend or cancel disbursements, (i) events that would require a refund

from the sovereign, and (iii) events that could trigger acceleration (immediate repayment). The

last category, “Events of Acceleration,” comes closest to EoD in private contracts, and can

trigger cross-default under private contracts.

9

For the first time, the 2017 revision introduced distinct General Conditions for three World Bank lending

instruments: Investment Project Financing, Development Policy Financing, and Program-for-Results Financing.

The instrument-based distinctions are unimportant for purposes of this chapter; we draw primarily on the

development policy instrument conditions as the closest to general purpose market borrowing by the

government.

8

Suspension and Cancellation. The World Bank may suspend disbursements and, in

some cases, may cancel the loan in response to any of the following: “payment failure,”

“performance failure” (referencing transaction-specific terms), fraud, corruption,

misrepresentation, unauthorized assignment of obligations, ineligibility to draw,

withdrawal from membership in the World Bank or the IMF, “cross-suspension” of

other World Bank loans, or any of a series of events that convince the lender that the

program is unlikely to be carried out. The latter include material financial, policy, and

legal changes. Suspension and even cancellation are distinct from default under market

instruments. The focus is on the policy objectives and the use of proceeds consistent

with the lender’s mandate. Ideally, the prospect of suspension of all World Bank

disbursements across the board should bring the authorities to the negotiating table and

fix the underlying problem. However, it is not meant to bring about the collapse of the

sovereign’s debt structure through cross-default.

Refund. The World Bank can require sovereigns to refund past disbursements if it

determines that they were used in a manner inconsistent with its loan agreement,

typically due to fraud or corruption. The 2017 revision made clear that the refund

requirement was not intended, and was not perceived in the market, as a cross-default

trigger for bonds and loans.

Acceleration. The World Bank can demand immediate repayment of a disbursed loan

in the event of a payment default on any of its exposure to the sovereign, subject to a

30-day grace period, and in the event of a performance default, subject to a 60-day grace

period. Unauthorized assignment, material adverse change, failure of co-financing, and

events specified in transaction-specific agreements may trigger acceleration under some

circumstances. Of all the sanction triggers specified in Article VII of General

Conditions, the term “default” is only used in the third category, “Events of

Acceleration,” which is understood to interact with cross-default terms in loan and bond

contracts.

7.1.4. Domestic Debt—No Definition, No Default?

11. Debt governed by the sovereign issuer’s domestic law typically has few express terms. For

example, it is not customary for domestic-law debt to include a litany of EoD. As a result, it

can be difficult to identify a clear contractual definition of default on domestic debt. The

relevant contractual terms may be incorporated by reference to statutes and administrative

regulations, which vary in form and substance among different countries (Addo Awadzi 2015).

For instance, the Uniform Offering Circular is a U.S. federal regulation that sets out terms and

conditions for most tradable U.S. Treasury securities. Out of its 34 sections, 30 spell out

auction procedures; one tells when the creditors are paid, and none address substantive

modification or default (31 C.F.R. 356 and 356.30).

12. This does not mean that governments cannot default on domestic debt. Instead, default and

remedies for default are a matter of background law—contract, constitutional, and

administrative, among others. For instance, in most jurisdictions, a debtor that simply fails to

pay as promised would be in default. However, as Austin (2015) illustrates with examples of

payment disruptions on U.S. Treasury securities in 1814, 1933, and 1979, missing domestic

9

debt payments sometimes has no discernible domestic or international consequences for the

sovereign. He suggests that of the three incidents, the failure to pay in 1814 on account of a

“bankrupt” Treasury comes closest to the widely shared contemporary understanding of

default. There is no agreement in the literature or jurisprudence on the default status of the

other two episodes, which involved retroactive removal of indexation and administrative

delays, respectively.

13. The power to change domestic law—so that default is either excused, or no longer counts as

default—is inherent in sovereignty, subject only to constitutional constraints as interpreted and

enforced by domestic courts. In some legal systems, governments have express additional

flexibility under domestic law to respond to economic emergencies (e.g., Gross & Ni Aiolan

2006).

10

14. In sum, even something as simple as payment default on domestic debt requires context for a

meaningful definition. It is not clear that an event with no discernible legal or economic

consequences should be called a default.

15. Although domestic-law sovereign debt may be less vulnerable to formal default, it is more

vulnerable to unilateral modification by the debtor designed to lower its payment burden and

reduce payoff for the creditors (e.g., Beers and Mavalwalla 2018; Moody’s 2011; Cruces and

Trebesch 2013; S&P 2017; Fitch 2018). If debt is denominated in local currency, sovereigns

can use monetary policy to reduce its value.

11

They can also use fiscal policy, such as

withholding taxes, to recapture at least in part payments that would otherwise go to creditors.

12

Reinhart and Sbrancia (2015) group these policies under the rubric of modern-day “financial

repression.”

7.1.5. Rating Agency Criteria for Default

16. Rating agency definitions of default matter because they inform ratings actions. A sovereign

downgrade may lead to rapid sell-off of its debt, since some investors would be barred from

10

For a recent illustration, see e.g., Mamatas and Others v. Greece ECHR 256 (2016), 21.07.2016.

11

Currency reforms to reduce debt payments include Cuba 1961; Myanmar, 1964, 1985, and 1987; Nigeria,

1967 and 1984; Laos, 1976; Vietnam, 1978 and 1985; Ghana, 1979 and 1982; Mozambique, 1980; Nicaragua,

1988; Angola, 1990; Sudan, 1991; Russia/Soviet Union 1991, 1993; North Korea, 1992 and 2009; Iraq, 1993;

Rwanda, 1995; and Venezuela, 2016 (Beers and Mavalwalla 2018).

However, inflation in general is not normally considered default (Moody’s 2011). According to Fitch (2002),

“Sovereign borrowers usually enjoy the very highest credit standing for obligations in their own currency. If they

retain the right to print their own money, the question of default is largely an academic one. The risk instead is

that a country may service its debt through excessive money creation, effectively eroding the value of its

obligations through inflation.”

12

For example, in 1999, the government of Turkey imposed a retroactive withholding tax of between four and 19

percent on interest income from domestic currency bonds. Note, however, that many bond contracts include

explicit language fixing bondholders’ tax liability; imposition of a tax in such a case could constitute a

contractual EoD.

10

holding it by regulation, contract, or mandate (Böninghausen and Zabel 2015). It may also

trigger downgrades of other borrowers in the country, particularly financial institutions that

benefit from sovereign guarantees, becoming a source of contagion.

17. As information intermediaries, credit rating agencies have developed distinct methodologies

for evaluating sovereign default, which inform their analysis and ratings. Their criteria focus

overwhelmingly on payoff. They reference underlying credit agreements but are both far more

streamlined and broader than EoD. For example, Moody’s definition of default includes three

kinds of events:

(i) failure to pay interest or principal within the grace period under the debt agreement,

(ii) a distressed debt exchange that reduces the sovereign’s financial obligation to avoid

payment default, and

(iii) unilateral change in payment terms “imposed by the sovereign that results in a

diminished financial obligation, such as a forced currency re-denomination … or a

forced change in some other aspect of the original promise, such as indexation or

maturity

.”

13

(Moody’s 2018)

This definition relies on the underlying agreements for payment default parameters and includes

two additional elements beyond payment default: a debt restructuring, even if it is preemptive

and consensual (discussed in Chapter 8), and domestic law measures that target and adversely

affect payoff, whether or not they amount to default under the terms of domestic debt

instruments.

7.1.6. Credit Default Swaps—Credit Events and Default

18. Sovereign credit default swaps (CDS) are tradable contracts under which “protection sellers”

take on sovereign credit risk for a fee from “protection buyers.” The buyers enter into CDS

contracts either to hedge existing exposure to the sovereign, or to bet against the sovereign

credit. If the sovereign defaults—in CDS parlance, if a “credit event” occurs—the seller must

compensate the buyer for the loss in value of a “reference obligation” specified in the CDS

contract. Since protection buyers are not required to hold any sovereign debt, in theory, market

participants can use CDS to create unlimited synthetic sovereign risk exposure. Sovereign CDS

have grown as a share of the CDS market (primarily attributable to contracts referencing

European sovereign credits), reaching 16% at the end of 2017. However, the aggregate notional

amount of all sovereign CDS outstanding, approximately $1.5 trillion, is still small relative to

the $40 trillion bond market (Aldasoro & Ehlers 2018).

19. CDS definitions of sovereign credit events matter because CDS contracts transmit credit

risk and can become a source of financial market contagion in a sovereign debt crisis. CDS

contracts are highly standardized. They are drafted by a trade group, the International Swaps

13

A fourth event of default, bankruptcy or receivership, does not apply to sovereigns.

11

and Derivatives Association (ISDA), which takes copyright in its standard terms. A single CDS

contract might comprise the ISDA Master Agreement in effect between the two counterparties,

a product-specific Definitions Booklet (here, CDS Definitions), a Credit Support Annex, which

includes any collateral arrangements, and a transaction-specific confirmation.

20. The term “Credit Event” is included in the Definitions Booklet, periodically revised by ISDA

in response to market and legal developments. Parties to a CDS contract incorporate the

definitions by reference in particular transactions. To enhance CDS liquidity, definitions do

not normally vary across parties or transactions. CDS could trigger independently of any

definition of default in a sovereign debt contract. As a result, ISDA definitions can have a

homogenizing effect in a world of incompletely standardized debt contracts.

21. The definition of sovereign credit events that trigger protection sellers’ payment obligation

reflect the objectives of the CDS instrument: to isolate and transfer credit risk, as distinct from

“legal” risks, economic conditions, or policy performance. In addition, CDS are meant to be

actively traded, which implies that credit event attributes should be observable and verifiable.

22. Credit events for sovereign CDS can include

(i) failure to pay,

(ii) obligation acceleration,

(iii) obligation default,

(iv) repudiation/moratorium, and

(v) restructuring (ISDA 2003, 2014).

Failure to pay incorporates any applicable contractual grace periods. Obligation default is an

EoD or similar event, other than failure to pay, that entitles creditors to accelerate under their

debt contracts, subject to an additional minimum threshold for outstanding amounts affected.

The definition of restructuring is the most challenging and controversial of the lot, since it

captures a wide range of consensual and involuntary outcomes (e.g., Gelpern & Gulati 2012).

It includes principal and interest reductions, payment date extensions, subordination, and

redenomination into currencies other than those of the G-7 or top-rated OECD member

countries, provided any such change is related to deteriorating creditworthiness or financial

condition of the sovereign and is effected in a way that “binds all holders” of the reference

obligation. Protection sellers and buyers can select which of the credit events would apply to

their transaction.

23. Interpretation and application of credit event definitions is the province of five regional

Determinations Committees (DCs), each comprising ten dealers (typically large financial

institutions that buy and sell CDS) and five non-dealers, such as smaller hedge funds.

Declaring a credit event requires 80% supermajority vote of the appropriate regional DC

(ISDA 2015). An auction to determine how much protection sellers must pay protection buyers

follows the determination.

12

24. CDS credit events would make an attractive template for defining sovereign default because

ISDA definitions reflect a common research objective: linking breach of contract, payoff, and

creditworthiness using transparent, observable criteria. However, drafting ambiguities persist,

and the DC process has attracted its share of criticism. Moreover, some participants in the

corporate, but not sovereign, CDS market were recently exposed for structuring their choice

of CDS triggers to get paid in the absence of underlying credit deterioration—contrary to the

stated goal of the instrument (ISDA 2018). Despite widespread concern, CDS have not been

associated with significant disruptions or delays in sovereign debt crises.

7.2 Variants of Default: Who is Affected? How Is It Done?

25. Default or its threat is among a sovereign debtor’s most powerful tools to achieve the goal of

sufficient relief to put debt on a sustainable path. While the literature has traditionally treated

debt default as binary—the country is either in default or not (e.g., Eaton and Gersovitz 1981;

Arellano 2008)—more recent work has begun to delve more deeply into the different ways a

sovereign can default. In order to explore the different considerations a debtor must weigh, we

examine this decision from two angles: default by creditor type (i.e., on whom to default) and

default by debtor action (i.e., how to default).

7.2.1 Default by Creditor Type

26. Given that a default on different creditor groups will result in different consequences for a

debtor, a debtor may choose to discriminate, often by using different categories of debt as a

proxy. One key underlying concern in differentiating among creditors is that selective default

may give rise to inter-creditor equity concerns and complicate the restructuring task down the

road if the debtor’s actions are widely perceived as unfair. Whenever a debtor chooses to

differentiate, therefore, it becomes important to justify that choice on relevant grounds.

Default on Official and Private Creditors

27. Among multilateral, bilateral, and private creditors, multilateral creditors are least likely to

face sovereign default (Schlegl, et al. 2017), and even less likely to participate in a

restructuring.

14

It has been generally accepted by official and private creditors that IMF

financing, in particular, should be excluded from sovereign debt restructurings, as the IMF’s

lending during crisis situations (just when all other creditors are exiting) constitutes a public

good that helps resolve a country’s balance-of-payments problems (Lastra 2014; Steinkamp

14

For example, Reinhart and Trebesch (2015) show 23 instances of members running arrears to the IMF over the

institution’s 70-year history.

At the start of the 21

st

century, international pressure prompted some of the largest multilateral creditors,

including the World Bank and the IMF, to provide conditional debt relief to a group of low-income countries

through the Heavily Indebted Poor Countries Initiative and the Multilateral Debt Relief Initiative, with

assurances from the G-8 countries that such debt relief would jeopardize neither the multilaterals’ ability to

continue to provide financial support nor the multilaterals’ own finances.

13

and Westermann 2014; IMF 2009; Rieffel 2003).

15

Other multilaterals are also generally

considered senior creditors (cf. Roubini and Setser 2004), though that status has occasionally

been called into question (Gelpern 2004).

28. By contrast, official bilateral creditors restructure frequently—pre- or post-default, formally

and informally—either through the provision of new financing or the restructuring of existing

debt. Indeed, because of the long-standing track record of official creditors giving concessional

treatment to distressed sovereign debtors (see Chapter 8), credit rating agencies generally do

not consider a failure to pay debt owed to another government a default (e.g., S&P Global

Ratings 2017; Fitch 2018).

16

29. Conventional wisdom has been that, despite the lack of de jure seniority rankings among

creditors, private creditors generally face a higher risk of default and steeper haircuts than

official bilateral creditors (e.g., Roubini and Setser 2004).

17

In line with this, Steinkamp and

Westermann (2014) note that 65% of experts responding to the 2013 World Economic Survey

indicated that they expected bilateral loans extended during the Eurozone crisis to be treated

as senior debt. However, recent research challenges whether this perceived seniority holds true

in practice. Schlegl, et al. (2017) and Moody’s (2018) both find that Paris Club restructurings

outnumber defaults on private creditors and often result in larger haircuts on the official

creditors.

18

Moreover, when focusing on the start of default, Schlegl, et al. (2017) find that

sovereigns are more likely to accumulate arrears towards official creditors than towards private

creditors. The speed and scope at which payments are missed suggests that government-to-

government loans are to junior to private bank loans and bonds, even after controlling for

country characteristics and the size and composition of the debt outstanding.

15

The de facto nature of the IMF’s “preferred creditor status” means that when a country receives financing from

the IMF, there is no legal subordination of existing debt, and no credit event has occurred. For an example, see

the International Swaps and Derivative Association’s determination regarding Ireland’s IMF financing in 2011.

16

It should be noted that, with a rising proportion of official bilateral financing being extended by sovereigns

outside of the traditional Paris Club process, the extension of this track record is uncertain.

17

Trade creditors are often seen as outside this calculus because interruption of payments would have immediate

implications for trade. Kaletsky (1985), for example, found that nearly all debtors had continued to promptly

service trade debts, even while defaulting on medium-term bank loans, given that “the interruption of trade

finance might turn out to be the heaviest penalty for a defaulter.” More recent work, however, has found that

trade creditors face default more often the previously supposed (Schlegl, et al. 2017).

18

As highlighted by Roubini and Stetser (2004), the differences between Paris Club treatments and private

creditor restructurings—e.g., flow treatments by the Paris Club over a limited period compared with “stock”

restructurings of privately held debt—makes an apples-to-apples comparison difficult. Other complications

include the sequencing of restructurings (the Paris Club assumption is that official creditors will go first,

determining their contribution to the restructuring and leaving the remainder for other creditors) and the lack of

rules for allocating near-term cash flow among creditors.

14

Default on Foreign and Domestic Creditors

30. A debtor may also seek to differentiate between foreign and domestic creditors and favor one

or the other depending on their domestic concerns and their objectives in the ultimate

restructuring (Zettelmeyer and Sturzenegger 2005). Erce and Díaz-Cassou (2010) have found

that considerations that lead to this type of discrimination include the origin of liquidity

pressures, the soundness of the banking system, and the domestic private sector’s reliance on

international markets. Others have identified domestic politics as a key factor (Kohlscheen

2010; Erce 2013). The economic consequences of default will be described in more detail

below. In short, a default on resident creditors can impact the health of the financial system

and will merely reallocate adjustment internally, whereas a default on non-resident creditors

can impair private-sector access to capital markets but also will redistribute the burden partially

outside the issuer’s economy (Erce and Díaz-Cassou 2010; Erce 2013).

31. Domestic creditors can be subject to certain incentives to participate in an exchange. While a

distressed exchange can occur with both domestic and foreign debt, domestic creditors may be

particularly vulnerable to the issuer’s regulatory power over financial institutions and moral

suasion (e.g., appeals to patriotism to increase exposure to government debt).

19

For example,

in the 2003 Uruguay restructuring, the central bank declared the old bonds ineligible for

liquidity assistance, effectively rendering them unmarketable. Failure of a bank to participate

in the exchange would have therefore hurt their provisioning and capital adequacy ratios (IMF

2014).

20

Where the stability of the financial sector was a concern, some restructurings have

included a framework for central bank liquidity provision—Box 2 discusses the case of

Jamaica, and Box 3 presents Uruguay. Russia provides an example of a sovereign default that

had devastating effects on the domestic banks (Box 3).

32. In practice, cleanly separating foreign and domestic creditors is very difficult. The type of debt

can be used as a proxy to some extent, categorizing along different axes, including governing

law and currency.

21

However, as many observers have noted, the move toward liberalizing

capital flows in recent years means that foreign creditors are increasingly holding domestic-

law, domestic-currency instruments, and vice versa, making this distinction—and the resulting

economic predictions—ever more difficult (Gelpern and Setser 2004; IMF 2015; Moody’s

2017).

19

Erce and Díaz-Cassou (2010) provide examples from Uruguay’s and Argentina’s exchanges.

20

IMF (2014), Annex IV.

21

The residence of creditor should be distinguished from whether the debt itself is considered foreign or

domestic. Traditionally, debt governed by local law and/or issued in local currency has been considered

domestic. The governing law plays an important role in determining the issuer’s tools in the context of a

restructuring (see Chapter 8). The currency of issuance determines whether inflation can be leveraged to lessen

the effective debt burden.

15

33. Jamaica’s restructuring in 2013 and Ukraine’s restructuring in 2015 provide an interesting

contrast between debtors that chose to focus on debt held by domestic creditors and foreign

creditors, respectively (See Box 2).

Default on Banks and Bondholders

34. Rieffel (2003) and others have suggested that “there is a general impression that bonds are

senior to bank loans.” This observation has empirical support, with Schlegl, et al. (2017)

finding bank loans more likely to face payment arrears than bonds. Over the past 40 years, it

is also true that bank loans of emerging market sovereigns have been restructured more

frequently than bonds (Cruces and Trebesch 2013); it remains to be seen if the trend continues

in the face of the increasing share of sovereign bonded debt.

35. It is important to note, that a default on bonds does not limit the damage to one type of creditor;

bondholders include investment funds, pension funds, and even official entities like central

banks and sovereign wealth funds. Importantly, banks themselves are fairly large holders of

government bonds, making the distinction between bank loans and bonds artificial when

looking at the effect on banks. For example, Gennaioli, et al. (2014) find that default on bonds

can decrease the liquidity of domestic banks, particularly in countries with better-developed

financial institutions (see below on the cost of default).

7.2.2 Default by Debtor Action

36. Defaults can also be categorized by actions that the debtor takes, irrespective of which creditors

stand on the other side.

Technical Default

37. “Technical default” is not a legal term. As we suggest in the first part of this chapter, the phrase

connotes a formal but ultimately unimportant breach. Which breach is important is in the eye

of the beholder (hence our proposed choice of reputable and impactful third-party definitions).

For example, the European Banking Authority defines a technical default (also called a

“technical past due situation”) as occurring only where the default was the result of (a) a “data

or system error of the institution,” (b) “failure of the payment system,” (c) the time lag between

payment and receipt, or (d) certain specific issues in factoring arrangements (European

Banking Authority 2017). Some others consider a “technical default” a non-payment that is

cured within three months without an announcement of default (e.g., Schwarcz 2014).

22

38. A few examples of historical defaults that some observers consider “technical” demonstrate to

what type of events the term generally applies. In July 1998, Venezuela missed a payment on

a local-currency bond with no grace period. The coupons were paid with a one-week delay,

22

Some have also defined “technical default” in a broader sense, including episodes in which all payments are

actually honored, but a sovereign makes a rescheduling offer on less favorable terms than the original debt

(Reinhart and Rogoff 2009, citing practices by Moody’s and S&P). For a further discussion on such “distressed

exchanges,” see Section 2.1.2, above.

16

and the government claimed the problem was that the check signatory had been unavailable.

The credit ratings agency Moody’s considered this a technical default but, due to a pattern of

similar missed payments, downgraded Venezuela’s rating from B2 to Caa1 (Moody’s 2008).

A longer-running saga—that of Argentina’s payments to exchange bondholders blocked by

court injunction, mentioned above in Section 7.1.1—was also labeled by some observers, such

as the United Nations Conference on Trade and Development, as a “technical” one (UNCTAD

2016).

Repudiation

39. Repudiation, described in Section 7.1.1, is rare in modern times.

23

Repudiations most often

occur after a regime change, and examples of repudiations include those in the wake of

communist revolutions—such as Russia in 1917, China in 1949, and Cuba in 1960; Rhodesia

in 1965, after its unilateral declaration of independence from the United Kingdom; Zaire in

1979; Ghana in 1979 and 1982; and North Korea in 1976.

24

40. Repudiation can go hand-in-hand with the concept of “odious debt,” which posits that a

government is not obligated to pay for those debts incurred by a previous government contrary

to the interests of the public.

25

Though, the concept has strong moral appeal, it is difficult to

define odious debt in a sufficiently limited way to allow its practical application (Reinhart and

Rogoff 2009).

26

The doctrine has not gained traction with arbitrators, courts, or credit rating

23

In an earlier era, the repudiation of a predecessor government’s debt was a common feature in treaties ending

armed conflict—e.g., Treaty of Campo Formio of 1797 (France and Austria); Treaty of Tilsit of 1807 (France

and Prussia); Treaty of Vienna of 1864 (Denmark, Prussia, Austria); 1947 Peace Treaties of Paris (Menon, 1986

at p. 116). Other repudiations followed significant regime changes: Spain in 1824, Greece in 1826, Portugal in

1834, Mexico in 1866, and the Dominican Republic in 1872.

24

Moody’s (2008) and Sturzenegger and Zettelmeyer (2007) provide examples.

25

For a further examination of this doctrine, see Blair (2014), Gelpern (2007), Buchheit et al. (2007),

Jayachandran and Kremer (2006).

26

To get around the difficult determination of which particular debts should be considered odious, Bolton and

Skeel (2011), for example, propose an “odiousness of the regime” approach rather than the traditional “debt-by-

debt” approach.

17

agencies (Gelpern 2007; Blair 2014) and, the earlier example of Ecuador aside,

27

states tend

not to assert it explicitly.

28

29

Hard vs. Soft

41. Defaults are often categorized as either “hard”/“unilateral” or “soft”/“negotiated,” though the

exact meaning of these terms often depends on the speaker. The key consideration across the

board, however, is whether the debtor is presenting creditors with nonpayment as a fait

accompli, or proactively engaging with its creditors on the terms of a default and restructuring.

As discussed in Section 7.1, this is a set of definitions used in the literature that conflates

default (an event) with actions taken during the restructuring (a process). However, because it

this group of definitions is so widely used, it is important to understand.

42. To measure and define creditor engagement and negotiated defaults it is useful to consider the

IMF’s “good faith” criterion under its Lending Into Arrears Policy.

30

This policy is important

because it outlines the conditions under which the IMF may provide crisis financing when a

debtor is in arrears to its private creditors (IMF 2013). In order to be judged by the IMF to be

acting in good faith toward its private creditors the debtor country should, with due regard to

the circumstances, (1) engage in a dialogue with the creditors at an early stage and throughout

the restructuring process, (2) share relevant non-confidential information on a timely basis, (3)

provide creditors with the opportunity to give input on the design of the restructuring and

individual instruments, and (4) engage with a timely-formed and representative creditor

committee, where warranted by the complexity of the case (IMF 2002).

43. The literature generally depicts a “hard” or “unilateral” default as a combination of payment

default and an aggressive restructuring posture, where the debtor refuses to negotiate with

creditors in good faith (Andritzky 2006; Enderlein et al. 2014; Trebesch & Zabel 2017). Such

cases may be more closely associated with creditor lawsuits, deep net present value reductions,

and capital controls. Debtor-creditor interactions take place against the background of large

information asymmetries.

27

See Feibelman (2010) for an argument that the government’s justification for default does not meet the

traditional definition for “odious debt” in that it did not show that “the citizens did not obtain meaningful

benefits from the underlying transactions.”

28

See, e.g., Reports of the International Arbitral Awards, Aguilar-Amory and Royal Bank of Canada claims

(Great Britain v. Costa Rica), Vol. I pp. 369-399, October 18, 1923 (finding that Tinoco regime’s oil concessions

to a British company and bank notes were binding on successive governments, despite the unconstitutionality of

the contracting and the fact that Tinoco’s government was not recognized by Great Britain).

29

As Blair (2014) notes: “The term ‘odious debt’ may … be one of public international law, but it is not much

used in English law, currently at least, and certainly has no technical meaning… .”

30

The Lending Into Arrears (LIA) policy permits the IMF to lend to a member country in arrears to private

creditors on a case-by-case basis where “(i) prompt Fund support is considered essential for the successful

implementation of the member’s adjustment program, and (ii) the member is pursuing appropriate policies [and]

is making a good faith effort to reach a collaborative agreement with its private creditors” (IMF 2013).

18

44. In a “soft” or “negotiated” default, by contrast, the debtor engages proactively with creditors

to reach a negotiated solution.

31

Generally, a soft default would allow for comprehensive

market soundings and informal negotiations with creditors, information sharing, and an offer

that could take a menu approach with different options. Of course, this classification is

subjective—one man’s market sounding is another’s take-it-or-leave-it offer. In reality,

defaults and restructurings fall somewhere between these two extremes. Examples of defaults

often classified as “hard” include the cases of Argentina in 2001 (see Chapter 8) and Russia in

2000 (see Box 3), while Uruguay’s 2003 restructuring provides an example of a “soft”

approach (see Box 3).

Partial vs. Full

45. The literature has also differentiated between “partial” and “full” defaults, typically by

considering the amount being defaulted on, though there is significant disagreement over

where the boundary lies. Some authors, including Arellano, et al. (2013), consider that

sovereign debtors only ever partially default, as debtors will always continue to pay some

portion of their debt—and often continue to borrow new amounts. Others, such as Eichengreen

(1991), consider countries that miss “more than a small fraction of interest payments” to be

“heavy” or full defaulters.

46. A very related concept is that of “selective default”, where sovereigns default on some creditor

classes while sparing others. For a detailed discussion see Erce (2012) and Schlegl, et al.

(2017).

7.3 Why Do Defaults Occur?

47. What are the drivers of sovereign debt distress and default? To set the stage, one can think of

debt crises as a result of either “mismanagement,” meaning bad financial and macroeconomic

policymaking at home, and/or of “misfortune,” mainly due to external shocks such as a sudden

spike in global interest rates, crises in financial center countries, commodity price swings, or

natural disasters. In practice, a clean distinction between these two causes is difficult. In

particular, it is well-known that countries can implement precautionary macroeconomic and

fiscal policies that help to buffer and manage external shocks when they occur. Despite this, it

is useful to summarize the findings from the early warning literature on defaults by looking at

domestic determinants (Section 7.3.1) and external determinants (7.3.2) separately. This

distinction can also be applied to the Eurozone debt crisis of 2010-2012, which has been

characterized by some as a crisis of economic fundamentals and reckless over-borrowing by

domestic politicians, while others emphasize the role of cross-border contagion, debt runs by

foreign investors, and self-fulfilling default expectations (see Section 7.3.3). In this context,

we will also summarize studies on legal drivers of default in Europe and beyond, in particular

31

Where the debtor continues to abide by the payment and other terms of the contract, this would not constitute a

legal default. For a further discussion of distressed exchanges, see Section 2.1.2, above.

19

the impact of bond clauses and jurisdiction choice for sovereign risk and recovery rates

(Section 7.3.4).

7.3.1. Mismanagement: Domestic Determinants of Default

48. To study the domestic determinants of sovereign default Manasse and Roubini (2009)

distinguish between liquidity and solvency. Simply put, liquidity crises are episodes with roll-

over problems, meaning difficulties in refinancing short-term debt, while solvency crises are

marked by a high debt burden.

32

Their analysis shows that the risk of default due to illiquidity

is especially high if short-term debt exceeds 130% of reserves. Above this threshold, defaults

can even occur at moderate levels of debt to GDP.

49. With a view to insolvency, Manasse and Roubini (2009) find that the risk of default is

particularly high in case of a high stock of external debt (in excess of 50% of GDP), while the

level of total public debt to GDP is a less useful warning indicator. In line with this, Reinhart

et al. (2003) show that a high public debt burden alone is not a good predictor of when and

why countries default. Using long-run data they show that some countries are “debt intolerant”

and have defaulted at debt/GDP ratios of just 20%, while others have tolerated debt stocks

above 100% of GDP for decades without running into distress. At the same time, the authors

show that the credit history of a country is a crucial predictor of default. All else equal,

advanced economies and emerging market countries that have never defaulted are much less

likely to run into debt problems than “serial defaulters”, with a high historical default

probability.

50. The risks of external debt are also studied by Catao and Milesi-Ferretti (2014) who show that

the ratio of net foreign liabilities (NFL) to GDP is an important predictor of sovereign debt

crises, especially if this ratio surpasses 50%. The recent Eurozone crises fits into this picture,

as much of the debt of countries such as Greece or Portugal was owed to foreign, not domestic

creditors. External dependence thus appears as a dominant explanation for serial debt

problems, not just in Europe, but also in Argentina and many other countries that have relied

on foreign debt and defaulted again and again (Reinhart and Trebesch 2016).

51. Beyond solvency and liquidity indicators, recent years have brought to the fore another

domestic trigger of sovereign distress, namely banking crises and sovereign-financial “doom

loops” (Fahri and Triole 2012). Using 200 years of data, Reinhart and Rogoff (2011) show

that domestic banking crises are often followed by a sovereign debt crisis, partly due to the

large fiscal costs associate with a financial crash. Negative spillovers from bank balance sheets

to the sovereign also played a major role during the Eurozone crisis, as documented by

Acharya, Drechsler and Schnabl (2014). Announcements of large financial bailouts between

2010 and 2012 were followed by a strong and immediate increase of sovereign risk measures

such as CDS spreads. Similarly, Ang and Longstaff (2013) show that systemic sovereign risk

is highly related to financial sector distress, rather than macro fundamentals. Finally,

32

For sovereign debtors, the distinction between illiquidity and insolvency is blurry, as liquidity crises can result

in a situation of insolvency, while crises of insolvency are often triggered by refinancing problems.

20

economists have also identified domestic macroeconomic volatility (Catao and Kapur 2006)

or domestic political and institutional factors as relevant drivers of sovereign risk (Kohlscheen

2007; van Rickeghem and Weder 2009; Enderlein et al. 2012; Trebesch forthcoming).

7.3.2 Misfortune: External Determinants of Default

52. External shocks are a main reason why countries default on their debt, especially during

systemic debt crises that occur in multiple countries simultaneously (Kaminsky and Vega

Garcia 2016). Sturzenegger and Zettelmeyer (2006, p. 6) study the main sovereign default

clusters of the last 200 years and find external factors to be decisive, in particular (i) a

worsening of the terms of trade; (ii) a recession in the core countries that acted as providers of

capital; (iii) an increase in international borrowing costs, e.g., due to tighter monetary policy

in creditor countries; and (iv) a crisis in an important country that causes contagion across trade

and financial markets.

These findings are in line with Reinhart et al (2016, 2018) who show

that a collapse of international capital flows and commodity markets are a powerful predictor

of default. Five of the six main waves of external default since 1815 were preceded by such a

“double bust”, meaning a sudden stop in global capital flows that coincides with a collapse in

global commodity prices. Kaminsky and Vega Garcia (2016) further show that terms of trade

and export shocks have typically preceded defaults in Latin America, while Hilscher and

Nosbusch (2010) show the volatility of terms of trade shocks to be a main driver of sovereign

bond spreads. The role of sudden stops in capital flows is further examined by Mendoza (2010),

while the link between commodity prices and sovereign risk is studied in a more granular way

by recent work of Mendoza and Restrepo-Echavarria (2018) and Dominguez et al. (2018).

7.3.3 Can Debt Crises Be Self-Fulfilling?

53. The idea that debt crises could be self-fulfilling goes back to Calvo (1988) and Cole and Kehoe

(2000), among others. They show that the probability of default largely depends on investor

expectations and that there can be multiple equilibria in crisis times. During the Eurozone

crisis, this notion has regained new prominence. De Grauwe and Li (2013), for example, show

evidence that, at the peak of the crisis, sovereign spreads were mostly driven by market

sentiment and had decoupled from macroeconomic fundamentals or risk indicators such as

debt/GDP. Beirne and Fratzscher (2013) also find that a large part of the increase in the level

and dispersion of bond spreads during the Eurozone crisis cannot be explained by

fundamentals. They distinguish between “pure contagion” or herding panics and

“fundamentals contagion,” meaning a crisis-induced increase in market sensitivity to

fundamentals, which was the main contagion channel during the Eurozone crisis according to

their results (see Dell’Arriccia et al 2006 for a similar result for emerging markets after the

Russian crisis). Bocola and Dovis (2016) provide a more theory-driven assessment on the role

of fundamentals versus self-fulfilling crisis expectations. They find that rollover risks (or self-

fulfilling crisis risk) can explain only a small part of the Italian bond spreads during the crisis,

while economic fundamentals play the dominant role.

54. The overall take away from recent research is that there can indeed be more than one

equilibrium in crisis episodes and that excessive debt accumulation and weak fundamentals

can therefore “leave sovereign borrowers at the mercy of self-fulfilling increases in interest

rates” (Lorenzoni and Werner 2016). Precautionary policies ex-ante can help countries to avoid

21

entering this “crisis zone” in the first place, e.g. via a fiscal rule (e.g. Conesa and Kehoe 2016;

Lorenzoni and Werner 2016), while cross-border bailouts or central bank interventions can

prevent or mitigate self-fulfilling dynamics ex-post (e.g. Corsetti and Dedola 2016; Corsetti,

Erce and Uy 2018; Roch and Uhlig 2018). Furthermore, Chamon (2007) suggest relying on

state-contingent debt (such as GDP-linked bonds) to reduce the likelihood of self-fulfilling

runs.

7.3.4 Legal Determinants of Default: Do Contract Terms Matter?

55. Policy and academic debates about sovereign debt contract reform occasionally imply that

contract terms which make debt restructuring more orderly, such as Collective Action Clauses,

should also make default easier, more attractive, and therefore more likely. However, studies

have failed to find consistent evidence that terms described by market participants as “legal”

or “process” terms—capturing all but the core economic bargain— increase sovereign debt

prices at issue (e.g. Becker et al. 2003, Eichengreen and Mody 2004).

56. The puzzle that CACs and related terms have no (or limited) impact on bond pricing has been

occasionally explained as a matter of offsetting effects: default may be more likely, but

recovery values are higher if the subsequent restructuring process goes smoothly. However, if

creditors find smoother restructuring attractive, the “upside” of process terms should become

more salient as the sovereign slides into distress (default probability approaches 100%), so that

contracts with CACs and similar terms that facilitate orderly restructuring should be priced

more favorably (see e.g., Carletti et al. 2017). Instead, studies find growing price penalties for

process terms as default draws near (e.g., Carletti et al. 2016, Chamon, Schumacher &

Trebesch 2018).

57. Future studies could help illuminate the relevance of contract terms for the default probabilities

and recovery values. Interviews with debtors, creditors, and other market participants suggest

that they associate legal or process terms with recovery values, but view their impact on the

probability of default as simply too uncertain at issue (Gelpern, Gulati, & Zettelmeyer 2018).

7.4 The Cost of Default

58. Sovereign defaults can be costly for governments and investors alike and cause collateral

damage to the economy of a defaulting country. This section summarizes these costs.

7.4.1. Loss of Market Access

59. The theoretical literature typically assumes that defaults and distressed restructurings lead to

the exclusion of sovereigns from international capital markets, as well as to an increase in

borrowing costs afterwards (see, e.g. Eaton and Gersovitz 1989 or Arellano 2008). The

empirical results, however, are mixed.

60. Overall, there is a consensus that defaults do hurt the conditions under which governments

can borrow abroad and at home, but there is disagreement around how persistent this effect

is. For example, the survey by Panizza et al. (2009) indicates that defaults increase borrowing

costs (risk spreads) markedly, but only in the first two years post-default. Similarly, Gelos et

22

al. (2011) document that most defaulters regain access to international markets within just one

or two years after a crisis. These findings are in line with older studies

33

and suggests that

investors have short memories. In contrast, more recent work by Cruces and Trebesch (2013)

and Catao and Mano (2017) account for the severity of default, measured by the size of

haircuts or the length of the default, and find evidence for a more persistent, sizeable default

premium, of 200 basis points, and a longer exclusion period from international markets.

61. One channel by which defaults affect market access and borrowing costs are credit rating

downgrades. It is well-known that ratings decrease markedly before and after sovereign

default events (see e.g. S&P 2018). Post-default ratings can also remain low for long periods,

deterring institutional investors from buying and holding these low-rated bonds. Indeed,

defaults and downgrades can result in portfolio relocation effects, also because distressed debt

instruments are often excluded from benchmark indices. JP Morgan’s EMBI index, for

example, drops bonds when they become illiquid and have unreliable pricing, which is often

the case in default, especially in protracted defaults. Give the current boom in index investing,

these types of index exclusions are likely to be increasingly costly for sovereigns in distress.

7.4.2. Collateral Damage for the Economy

62. The idea that default may cause “collateral damage” to the economy is nothing new. Cole and

Kehoe (1998) develop a model of generalized reputation which suggests that default triggers

reputational spillovers that adversely affect not only the sovereign credit market but also other

fields of the economy. In line with this, a large literature has studied the link between default

and various economic outcome variables.

63. First, sovereign debt crises are accompanied by a significant drop in economic growth, as

shown in more than a dozen studies. Borensztein and Panizza (2009), Furceri and Zdzienicka

(2012), and Kuvshinov and Zimmermann (2014), for example, use cross-country panel data to

show that defaults are associated with two to six percentage points lower growth in the first

years of the crisis. There is also a consensus that the fall in output is particularly large when

defaults are accompanied by banking crises (see e.g. De Paoli et al. 2009; Kuvshinov and

Zimmermann 2014). Furthermore, recent work has zoomed in on the aggregate relationship

between default and growth. Levy-Yeyati and Panizza (2011), for example, use quarterly data

to show that, on average, output contractions precede defaults and that the recovery starts right

after the default. Tomz and Wright (2007) show that the relationship between default and

output since 1820 is unexpectedly weak and that countries have also defaulted in “good times”.

Trebesch and Zabel (2016) show that the output losses are more pronounced in “hard” defaults.

64. Moreover, the literature has documented a negative correlation between default and (i) trade,

(ii) foreign direct investment and (iii) domestic firms in the defaulting country. Regarding

trade, Rose (2005) estimates a gravity panel and shows that, following sovereign debt

33

The influential studies by Lindert and Morton (1989) and Özler (1993) find that the average default penalty is

not sizable, and leads to an average increase in spreads of, at most, 50 basis points in years one or two after the

crisis. Additional evidence, going back farther in history, is provided by Jorgensen and Sachs (1989).

23

restructurings, trade falls bilaterally by about 7 percent per year and for more than 10 years.

Both Martinez and Sandleris (2011) and Mitchener and Weidenmier (2005) show that the

observed drop in trade during debt crises is mostly due to a “general” effect rather than a

bilateral punishment channel. In a similar setup, Fuentes and Saravia (2010) show that

countries that undergo a debt restructuring see their FDI flows drop by up to 2 percent of GDP

per year.

65. Regarding domestic firms, Hebert and Schreger (2017) use data from Argentina to show that

a sovereign default significantly reduces the value of domestic firms on the stock market,

especially for exporters and foreign-owned companies. In earlier work, Arteta and Hale (2008)

and Das et al. (2012) find that sovereign debt crises are accompanied by sizable drop in external

borrowing by domestic firms. This indicates that corporations in defaulting countries face

difficulties in accessing foreign capital markets. Borenzstein and Panizza (2010) and Zymek

(2012) also focus on this credit channel and provide evidence that defaults hurt those sectors

and exporters most that are dependent on foreign financing. These findings are in line with the

theoretical model of Mendoza and Yue (2012) in which defaults increase the cost of borrowing

abroad and, thus, the cost of paying for imported inputs. The resulting shift to domestic inputs

causes efficiency losses in domestic production and lowers growth.

7.4.3. Spillovers on the Domestic Banking Sector

66. Sovereign default can also cause major damage on banks and other systemically relevant

institutions, especially if they hold large amounts of government debt. This type of “top-down”

sovereign-financial spillover has played an increasingly important role in recent years, most

visibly during the Eurozone crisis. Indeed, there is a consensus that heightened sovereign

default risk in economies with a large financial sector can result in an aggregate credit shortage,

less investment and possibly a banking crisis and an output decline (e.g. Acharya et al. 2014;

Perez 2015; Bocola 2016; Sosa-Padilla, forthcoming).

67. A widely cited paper on the link between sovereign default and banks is Gennaioli et al. (2014),

who find that sovereign defaults are followed by large drops in private credit and that this post-

default credit crunch is stronger for countries in which banks hold more government debt. In

follow-up work, the same authors use finer-grained data and again find a strong negative

correlation between a bank's holdings of government bonds and its lending during sovereign

defaults (Gennaioli et al. 2018). Acharya et al. (2018) and Bofondi et al. (2018) come to a

similar result when linking data on a bank’s holdings of sovereign debt and that bank’s lending

activity.

7.4.4. Creditor Lawsuits: The Legal Costs of Default

68. Other important concerns for policymakers in the context of default are legal risks (threat of

litigation) and the costs arising from the so called “holdout problem” (see Chapter 8; Panizza

et al. 2009; Buchheit et al. 2013). Overall, the evidence shows that sovereign immunity has

eroded since the 1970s, strengthening the hands of creditors and raising the legal cost of default

for debtors, with implications for government willingness to repay.

24

69. The Argentine debt crisis after 2001 is the best-known example for how large the legal costs

of default can become. Dozens of hedge funds filed suit against Argentina in New York,

litigated for full repayment, and repeatedly attempted to seize Argentine assets abroad. Fifteen

years later, those holdout creditors achieved a major victory in court, which ultimately forced

the Argentine government into a settlement of more than $10 billion – a multiple of the debt’s

original face value (Cruces and Levy Yeyati 2016; Hébert and Schreger 2017).

70. Argentina is not an exception but is part of a general trend, as shown by Schumacher et al.

(2018). Building on a new dataset on sovereign debt lawsuits, the authors document that the

risk of litigation in the context of a sovereign default has increased greatly since the 1980s.

34

Furthermore, they show that legal disputes can disrupt government access to international

capital markets, as foreign courts impose a financial embargo on defaulting sovereigns. Legal

risks are therefore one possible channel explaining why government loose market access.

71. In recent years, the risks of creditor holdouts and litigation has only continued to increase.

Schumacher et al. (2018) document that, unlike in the 1990s or early 2000s, governments in

distress now frequently point to legal risks when explaining their policy choices, and the same

is true for rating agencies justifying up- or downgrades. In line with this, Gulati et al. (2013)

argue that the fear of a protracted, Argentine-style disputes with creditors was one of the

reasons many Eurozone governments decided to avoid a default or debt restructuring. The one

exception is Greece, but even there legal risks played an important role. Most importantly, the

Greek government decided to repay holdouts on foreign-law bonds in full and on time,

allowing them to escape the haircut imposed on all other creditors. The resulting transfers

amounted to more than 2% of Greek GDP (Zettelmeyer et al. 2013).

7.5 Reducing the Incidence and Costs of Default

72. A country’s decision on whether or not to default and how to restructure its debt is typically

not taken on its own. Very often, such a decision comes about in the context of a lending

program from the official sector, most typically from the IMF. Therefore, the international

financial policy architecture and particularly the policy framework of the IMF that governs

when and how much it can lend materially affects the incidence and cost of default.

73. This section reviews the experience with the incidence and cost of default, though it

necessarily discusses the process of restructuring as well. It is largely based on a series of

analytical and policy papers started by the IMF in 2013 to review its experience with

resolving sovereign debt crises and considering changes to its policy framework governing

its lending and sovereign debt restructuring. The section is organized as follows. Section

7.5.1 documents the “too little, too late” problem: whether or not a country defaults,

restructurings are often delayed and when they do take place they often don’t entail a deep

enough restructuring to definitively restore sustainability. Hence they end up being more

costly. Section 7.5.2 reviews possible factors behind such outcomes, discussing both the

34

The risk of litigation is particularly high for sovereigns imposing a high haircut on large amounts of debt

(Schumacher et al. 2015).

25

incentives of debtors as well as official creditors. Finally, Section 7.5.3 discusses what can be

done and has been done to make default and restructurings less likely and when they do

occur to reduce their associated costs.

7.5.1. Too Little, Too Late: Timing and Depth of Restructuring

74. A prominent example of a delayed restructuring is Greece (2012). As explained in detail by

the IMF’s Independent Evaluation Office (2016), when Greece approached the IMF in May

2010, its debt situation did not meet the bar required by the IMF to lend it large amounts: in

the IMF’s jargon, debt was not considered sustainable with “high probability” to allow