Support for this study was provided by Apple.

The conclusions and opinions expressed are exclusively those of the authors.

The Continued Growth and Resilience

of Apple’s App Store Ecosystem

Juliee Caminade, Ph.D.

Jonathan Borck, Ph.D.

May 2023

The Continued Growth and Resilience of Apple’s App Store Ecosystem

1

The App Store ecosystem: 2022 at a glance

The App Store ecosystem facilitated a groundbreaking $1.1 trillion in billings and sales worldwide in 2022. More than 90%

of this figure originated from transactions that did not happen through the App Store, meaning that these amounts

accrued solely to developers and other third parties, and that Apple collected no commission on them.

Over the past few years, through the ebbs and flows of the COVID-19 pandemic, the App Store ecosystem grew at a

substantial and remarkably steady rate (between 27% and 29% annually), consistent with a flourishing marketplace.

This steady overall growth hides important variations within app categories that reflect consumers’ changing habits as

the pandemic evolved. For example, some categories grew substantially in 2022 as many people returned to in-person

activities, with travel (up 84%) and ride hailing services (up 45%) leading the way. Other categories, such as grocery sales,

food delivery, and digital goods and services consumed on iOS apps, grew more modestly in 2022 aer booming at the

height of the pandemic. In-app advertising on iOS apps grew at a faster pace in 2022 than 2021, driven by the strong

performance of social media, podcasts, and general retail apps.

Variations across regions were also notable, with a number of factors at play in certain regions in a challenging global

economic environment: Inflation, a stronger US dollar, and regulatory headwinds in the video game industry in China.

These factors should be considered when interpreting our global results and regional variations.

Fieen years of the App Store

The App Store has been a safe and secure home to a large and varied array of apps for 15 years. Users today have

access to over 123 times more apps than they did at the end of 2008, and annual downloads on the App Store

increased 15-fold between 2009 and 2022. Users have downloaded apps more than 370 billion times and developers

have earned more than $320 billion in earnings directly on the App Store since its launch. Over the past 15 years, the

App Store has supported new and growing sectors of the economy and has provided businesses with new ways to

engage with customers and lower costs.

Apple has implemented rules and policies, such as the strict App Review process, to foster user trust. These

policies have prevented billions of dollars in fraudulent transactions. Apple has also supported developers over

the past 15 years through a variety of technical tools, analytics, and education initiatives, all of which have helped

developers add new functionality to their apps, track their performance on the App Store, and receive support from

Apple experts.

$1.1

trillion

ecosystem in 2022

+29%

growth in the

ecosystem in 2022

+84%

in iOS-app-based

travel sales in 2022

+45%

in iOS-app-based

ride hailing sales in

2022

The Continued Growth and Resilience of Apple’s App Store Ecosystem

2

The App Store ecosystem

The App Store ecosystem globally in 2022

We estimate that the App Store ecosystem facilitated more than $1.1 trillion in billings

and sales worldwide in 2022, up from $868 billion in 2021, $643 billion in 2020, and $519

billion in 2019. Of that total, $104 billion, or 9%, originated from billings and sales of digital

goods and services consumed on iOS apps; $910 billion, or 81%, from sales of physical

goods and services made on iOS apps; and $109 billion, or 10%, from in-app advertising on

iOS devices. (See Table 1.)

Apple only collects a commission on app purchases, in-app purchases, and in-app

subscriptions that go through the App Store. No commission is collected on purchases

of digital goods and services that happen outside of apps (e.g., purchasing a subscription

to a newspaper through a web browser), on purchases of physical goods and services

through apps (e.g., when a user pays for a ride on a ride hailing app or buys groceries

online), or on in-app ad revenue. More than 90% of the $1.1 trillion in billings and sales

facilitated by the ecosystem occurred outside the App Store, meaning that these

amounts accrued solely to developers and other third parties and that Apple collected

no commission on them. The share of billings and sales that accrue solely to developers

has continued to increase year-to-year. (See Appendix Table 1 for further methodological

details.)

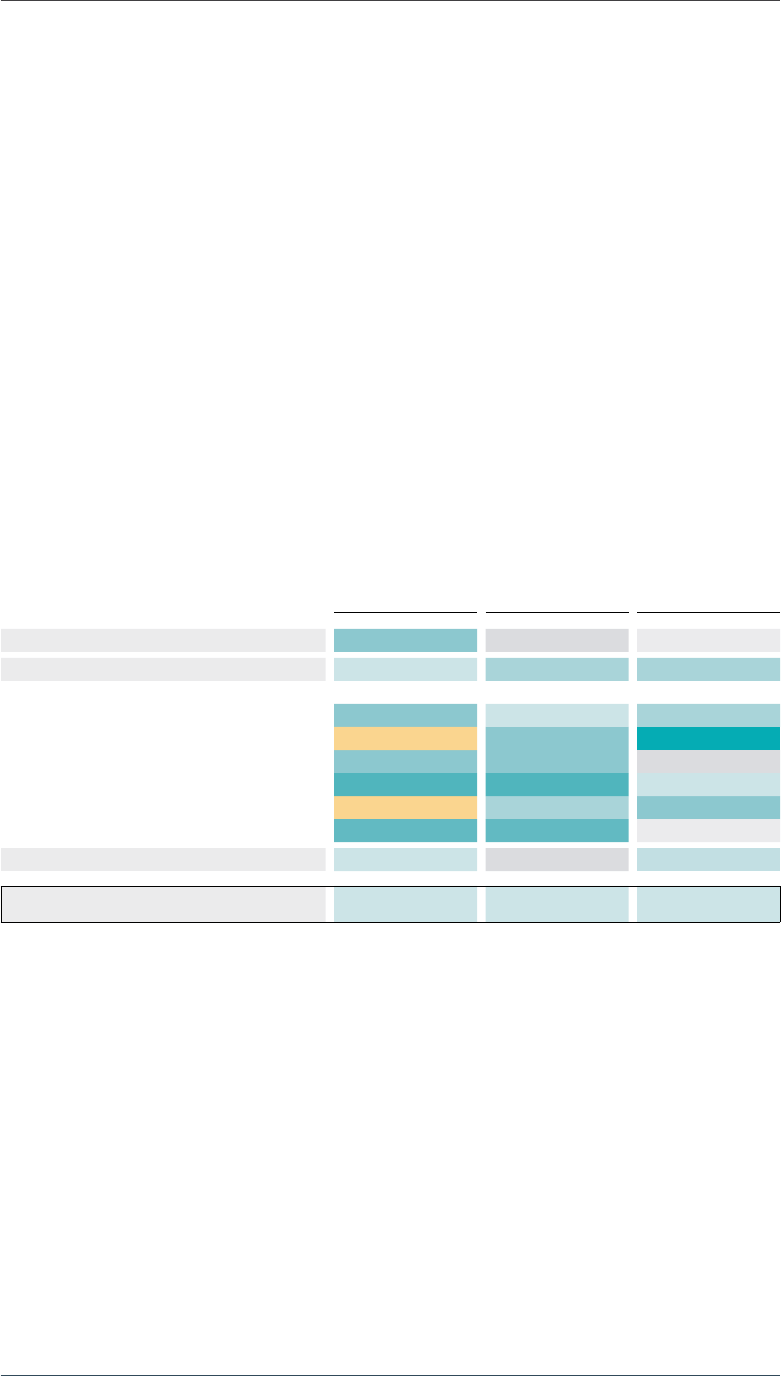

Table 1: Estimated Billings and Sales Facilitated by the App Store Ecosystem, Worldwide,

2019-2022 ($ Billion)*

2019 2020 2021 2022

Digital Goods and Services** $61 $86 $102 $104

Physical Goods and Services $413 $511 $678 $910

M-Commerce

General Retail $268 $383 $471 $621

Travel $57 $38 $56 $102

Food Delivery and Pickup $31 $36 $66 $77

Grocery $14 $22 $43 $52

Ride Hailing $40 $26 $33 $48

Digital Payment $4 $5 $9 $10

In-App Advertising*** $45 $46 $88 $109

Total $519 $643 $868 $1,123

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings. We include sales from digital goods and services purchased elsewhere

but used on apps on Apple devices, and we subtract billings from in-app purchases made via the App Store but used elsewhere. The estimate relies on third-

party sources and Apple data. See Appendix for details.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

In 2022, over

90%

of billings and

sales facilitated

by the ecosystem

occurred outside

the App Store.

Billings and Sales

“Billings” refers to app

purchases and in-app

purchases, including

subscriptions, which use

Apple's in-app payment.

“Sales” refers to money

spent by customers

purchasing goods and

services in general. We use

the term “facilitated” to

include the various ways

in which apps contribute

to generating billings and

sales.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

3

As in previous years, most of the billings and sales facilitated by the App Store ecosystem

came from the sales of physical goods and services through iOS apps. Of those, general

retail remained the largest category by far. Two other categories jockeyed for the next

two spots: In 2021, food delivery and pickup temporarily surpassed travel as the second-

largest category, while in 2022, travel once again was number two, with $102 billion in sales

through the App Store. (See Figure 1.) The consistently high amount of sales of physical

goods and services demonstrates that the App Store ecosystem continues to provide

a trusted platform for developers to sell such products. For example, Apple Pay is an

important tool that supports developers in this segment: Apple Pay offers a standardized,

secure, and seamless way for customers to pay for physical goods and services in-app.

Figure 1: Estimated Billings and Sales Facilitated by the App Store Ecosystem by App

Category, 2019-2022 ($ Billion)*

Digital Goods and Services**

Physical Goods and Services

Digital Payment

Ride Hailing

Grocery

Food Delivery and Pickup

Travel

General Retail

In-App Advertising***

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

$519

2019

$45

$57

$31

$40

$61

$14

$4

$268

$36

$86

$22

$5

$643

2020

$46

$38

$26

$383

$868

2021

$88

$38

$56

$66

$102

$43

$33

$9

$471

$1,123

2022

$109

$38

$102

$77

$104

$52

$48

$621

$10

Methodology

“iOS apps” include apps on

iPhone and iPad devices.

Apps developed by Apple,

such as Apple Music, as

well as mobile browser

apps, such as Google

Chrome, are excluded from

this analysis. Third-party

apps featured within Apple

TV are included in our

analysis of video streaming.

Categories as presented in

this report do not reflect

App Store categories.

In-App Ad Sales

Estimates of in-app ad

sales for iOS apps include

revenue generated

from the publishing of

advertisements within

apps only. Estimates do

not include advertising on

mobile web (such as on

mobile browser apps) or

search advertising, such as

Apple Search Ads.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

4

Estimating the size of the App Store ecosystem

The direct monetization of apps represents a small fraction of the overall commerce

the App Store facilitates, because developers can monetize their apps in several

ways that do not involve payments through the App Store, such as:

1. Selling digital goods and services outside of the App Store for use within apps

on Apple devices (e.g., news and magazine subscriptions, music and video

streaming)

2. Selling physical goods and services through apps on Apple devices (e.g., food

and grocery delivery or ride hailing)

3. Offering ad-supported content within apps (e.g., ad-supported games)

While our analysis captures the major app monetization strategies, we do not capture

all of the ways in which the App Store ecosystem facilitates sales or all of the benefits

created by apps. For example, we do not include benefits that companies derive from

“companion apps” that raise the value of their goods and services, including smart

home apps (e.g., Nest, Ring) and health apps, among many others.

A complete description of our methodology is included in the Appendix.

To read about our estimates of billings and sales facilitated by the App Store in

2019 and 2020, please see our previous reports: How Large Is the Apple App Store

Ecosystem? and A Global Perspective on the Apple App Store Ecosystem.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

5

Global trends (2019-2022)

The App Store ecosystem grew 27% between 2020 and 2021 and 29% between 2021 and

2022, in line with the 27% growth from 2019 to 2020.

1

Overall, such growth is a sign of a

flourishing marketplace, where apps innovate, grow, and compete.

i

Each of the three top-level ecosystem categories grew each year, but at somewhat

different rates. (See Table 2.) Specifically, iOS-app-based sales of physical goods and

services accelerated, growing 30% from 2020 to 2021 and 34% from 2021 to 2022. In-app

advertising in iOS apps continued to grow at high rates: Increasing 10% from 2020 to 2021

and 24% from 2021 to 2022.

The size of digital goods and services facilitated by the App Store grew by 19% from 2020

to 2021 before plateauing (up 2%) in 2022. These changes reflect a period of rapid growth

in 2020 as people shied to a more digital world during the pandemic, followed by a

gradual transition through 2022 to a new normal, with sustained higher levels of digital

billings and sales.

Digital goods and services: Within digital goods and services consumed on iOS apps,

we saw large increases in 2020 in enterprise, education, and fitness apps, following a

shi toward remote work, online schooling, and online fitness due to gym closures.

Enterprise apps have continued to grow in popularity since the pandemic, and in 2022

represented one of the fastest growing digital goods and services categories in our

ecosystem estimate of billings and sales, only behind app-based entertainment. In 2022,

business-oriented apps represented five of the top 25 most downloaded apps in the

US (Zoom, Microso Teams, Microso Outlook, Microso Intune Company Portal, and

Authenticator). Billings and sales continued to increase significantly for all categories

of digital goods and services in 2021 and then stabilized in 2022, as people had largely

adapted to remote and hybrid models of work and school, and were returning to in-person

activities in many regions of the world. Online dating services, for example, grew faster in

2021, as many people got vaccinated against COVID-19 and returned to in-person dating,

and continued to grow in 2022.

ii

One exception to the stabilization seen in other categories in 2022 was app-based

entertainment services, a category that includes live-streaming apps, horoscope apps,

and group chat apps, which saw the largest growth among digital goods and services

categories. One notable trend within app-based entertainment services is the growth of

apps supporting the creator economy in recent years; examples of these apps include live-

streaming apps Twitch and BIGO LIVE, and chatroom app Discord.

1 All changes in this report are calculated using the most current figures for 2019 and 2020. We updated some

of the estimates from our previous reports to account for (1) methodological improvements and refinements

developed over time, and (2) retroactive changes made by third-party data sources. We rely on the updated

numbers, rather than our original estimates, to calculate changes compared to 2019 and 2020, as they will more

accurately reflect underlying trends, rather than methodological improvements or updates in third-party data.

See Appendix for more details.

Mobile general

retail sales on

iOS apps have

increased by

64%

since 2020.

Billings and sales

of digital goods

and services

consumed on

iOS apps have

increased by

21%

since 2020.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

6

Physical goods and services: Looking at iOS-app-based purchases of physical goods

and services, the consistent and substantial growth in 2021 and 2022 reflects multiple

factors: A continued shi to buying goods and services through apps – in particular, for

general retail, grocery, and travel; the dramatic growth of categories such as food delivery

and pickup, and grocery delivery; the strong recovery of categories negatively affected

by the pandemic, such as ride hailing and travel, following a return to in-person activities

as vaccines were rolled out and pandemic restrictions were relaxed in many countries

and regions in 2021 and throughout 2022; and global macroeconomic impacts, including

inflation in some regions, changing interest rates, and foreign exchange headwinds from a

strong US dollar.

The category that experienced the largest growth in both 2020 and 2021 was iOS-app-

based grocery sales.

2

The pandemic led many people to change their grocery shopping

habits, buying groceries online – particularly on their iPhone – using delivery services or

ordering ahead and picking them up at the store. These changes in habits were reflected

in 67% growth from 2019 to 2020 and 74% growth from 2020 to 2021. iOS-app-based

grocery sales stabilized in 2022, still increasing at a substantial rate of 20%, suggesting

that this shi in consumer habits is here to stay. For the second year in a row, iOS-app-

based grocery sales remained larger than ride hailing in the App Store ecosystem in 2022,

making it the fourth largest m-commerce category.

Similarly, owing to pandemic restrictions on indoor dining and changes in consumer

habits, sales of food delivery and pickup on iOS apps grew substantially throughout the

pandemic (up 40% and 41% in 2020 and 2021, respectively), and continued to grow in 2022

though at a somewhat more modest clip (up 17%). This strong growth led food delivery

and pickup to briefly become the second-largest m-commerce category in the App Store

ecosystem (behind general retail) in 2021 before returning to third (behind general retail

and travel) in 2022. The pandemic also continued to drive an increase in digital payments

in 2021 (up 59%, compared to 54% in 2020) as contactless payment methods replaced

cash, a shi that appears to reflect a longer-term change in payment methods (9% growth

in 2022).

2 Grocery refers to purchases of food and beverages for pickup or delivery from the online stores of large

supermarkets (e.g., Walmart), internet retailers (e.g., Amazon Fresh), dedicated grocery delivery services (e.g.,

Instacart), and subscription-based services (e.g., HelloFresh). Food delivery and pickup refers to orders of

prepared meals from restaurants directly or through platforms (e.g., JustEat) for direct consumption.

iOS-app-based

grocery sales

increased nearly

3.5x

since 2019.

iOS-app-based

food delivery

and pickup sales

increased nearly

2.3x

since 2019.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

7

General retail sales on iOS apps – the largest m-commerce component of the ecosystem

– showed strong growth in 2021 (up 24%) and grew even more in 2022 (32%). This increase

in general retail was partially driven by an increase in the share of iOS device usage in

China,

iii

which has historically been the largest contributor to the general retail category.

As vaccines became available and pandemic restrictions were relaxed in 2021, travel and

ride hailing reversed their pandemic-related declines. These two categories grew 47% and

30%, respectively, in 2021, and an impressive 84% and 45% in 2022. iOS-app-based sales in

both categories in 2022 exceeded their pre-pandemic levels.

In-app advertising: Ad spend was substantially higher in 2022 compared to 2021. This was

consistent with broader macro trends in the ad space, which had a strong year overall

despite challenges from some individual players. The ad market saw strong growth for

certain short-video apps, retail (e.g., Amazon), and podcasts, driving the overall increase

in in-app advertising. The increase in iOS usage shares in China also drove some of this

growth.

Table 2: Yearly Changes in the App Store Ecosystem, Worldwide, 2019-2022

2019 to 2020 2020 to 2021 2021 to 2022

Digital Goods and Services*

,

** +41% +19% +2%

Physical Goods and Services +26% +30% +34%

M-Commerce

General Retail +42% +24% +32%

Travel -33% +47% +84%

Food Delivery and Pickup +40% +41% +17%

Grocery +67% +74% +20%

Ride Hailing -33% +30% +45%

Digital Payment +54% +59% +9%

In-App Advertising**

,

*** +23% +10% +24%

Total +27% +27% +29%

* Billings and sales from digital goods and services are not the same as App Store billings.

** Changes between both 2019 to 2020 and 2020 to 2021 are based on updated numbers. See Appendix for more details.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

8

Regional dynamics on the App Store ecosystem

The App Store ecosystem by region in 2022

In 2022, roughly as in previous years, the US accounted for almost 25% of the billings and

sales facilitated by the App Store ecosystem, China

3

accounted for 51%, and Europe 11%.

Physical goods and services were the largest category in each region. (See Table 3, as well

as Appendix Table 2 for the analogous 2021 table.) Within physical goods and services,

general retail dominated in all regions, with slight differences in the ordering of the other

m-commerce subcategories.

Table 3: Estimated Billings and Sales Facilitated by the App Store Ecosystem,

Large Regions, 2022 ($ Billion)*

US China Europe****

Rest of the

World Total

Digital Goods and Services** $41 $21 $11 $30 $104

Physical Goods and Services $182 $523 $93 $111 $910

M-Commerce

General Retail $96 $411 $51 $63 $621

Travel $27 $32 $21 $22 $102

Food Delivery and Pickup $21 $36 $9 $11 $77

Grocery $13 $25 $6 $8 $52

Ride Hailing $22 $14 $6 $6 $48

Digital Payment $4 $6 - - $10

In-App Advertising*** $50 $25 $15 $19 $109

Total $273 $570 $119 $160 $1,123

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

**** Europe includes countries in Western, Central, and Eastern Europe (including the UK and the Nordic Region, not including Russia).

3 Throughout the report, China refers to Greater China.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

9

The UK remained the largest contributor to the App Store ecosystem in Europe, in part

thanks to its large m-commerce sector and relatively high iOS market share. In most

countries, general retail, travel, and food delivery and pickup remained the three largest

subcategories within m-commerce. (Italy is an exception; see Table 4.)

Table 4: Estimated Billings and Sales Facilitated by the App Store Ecosystem,

Select European Countries, 2022 ($ Billion)*

UK Germany France Italy Spain

Digital Goods and Services** $3.2 $2.1 $1.3 $0.5 $0.3

Physical Goods and Services $40 $15 $8.9 $3.4 $3.4

M-Commerce

General Retail $23 $7.1 $5.4 $1.6 $1.7

Travel $6.3 $4.8 $2.1 $1.3 $1.2

Food Delivery and Pickup $5.1 $1.7 $0.5 $0.2 $0.2

Grocery $2.7 $0.7 $0.5 $0.3 $0.2

Ride Hailing $2.2 $0.5 $0.5 $0.1 $0.2

In-App Advertising*** $4.8 $2.1 $1.8 $0.9 $0.5

Total $48 $19 $12 $4.9 $4.2

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

We find that general retail remained the largest stream of iOS-app-based sales in both

Japan and South Korea in 2022, while in Australia and New Zealand, travel became the

largest m-commerce category within physical goods and services, ahead of general retail.

Travel was the second largest category in Japan, while food delivery and pickup remained

the second largest category in South Korea. (See Table 5.)

Table 5: Estimated Billings and Sales Facilitated by the App Store Ecosystem,

Select Countries and Regions, 2022 ($ Billion)*

Japan South Korea

Australia and

New Zealand

Digital Goods and Services** $14 $1.8 $1.9

Physical Goods and Services $25 $26 $10

M-Commerce

General Retail $14 $17 $3.6

Travel $5.1 $2.6 $4.1

Food Delivery and Pickup $1.8 $4.5 $0.7

Grocery $3.4 $1.7 $0.9

Ride Hailing $0.7 $0.5 $1.2

In-App Advertising*** $7.1 $1.1 $2.1

Total $46 $29 $14

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

10

Regional trends (2019-2022)

In the US, China, and Europe, billings and sales of digital goods and services facilitated

by the App Store ecosystem stabilized between 2021 and 2022 as categories that initially

grew during the onset of the pandemic plateaued in 2022, due in part to regulatory

headwinds in the video game industry in China.

iv

In 2021 and 2022, by contrast, iOS-app-

based sales of physical goods and services increased steadily in the US (up 26% and 20%),

while growth in China almost doubled due to an increase in the adoption of iOS relative to

Android (24% in 2021 compared to 52% in 2022). While the digital goods and services and

physical goods and services categories were stable in Europe between 2021 and 2022, this

is at least partially aributable to the strong US dollar compared to the euro and British

pound. In local currency, the eurozone grew comparably to the United States. Over the

longer, three-year time frame, the size of the ecosystem doubled in Europe and China and

grew by more than 80% in the US. (See Table 6.)

Table 6: Yearly Changes in the App Store Ecosystem, Large Regions, 2019-2022

US China Europe****

‘19 to ‘20 ‘20 to ‘21 ‘21 to ‘22 ‘19 to ‘20 ‘20 to ‘21 ‘21 to ‘22 ‘19 to ‘20 ‘20 to ‘21 ‘21 to ‘22

Digital Goods and Services*

,

** +51% +17% +7% +30% +18% +6% +44% +28% +1%

Physical Goods and Services** +26% +26% +20% +23% +24% +52% +54% +49% +2%

M-Commerce

General Retail +69% +15% +12% +30% +20% +50% +101% +41% -15%

Travel -37% +76% +54% -27% +7% +158% -33% +77% +79%

Food Delivery and Pickup +52% +24% +5% +4% +56% +37% +96% +50% -0%

Grocery +128% +77% +52% +65% +69% +21% +54% +88% +4%

Ride Hailing -41% +27% +32% -21% +8% +108% -13% +53% +18%

Digital Payment +186% +57% -9% +10% +60% +24% - - -

In-App Advertising**

,

*** +28% +4% +22% +19% +15% +49% +21% +22% +8%

Total +30% +20% +18% +23% +24% +50% +47% +43% +2%

* Billings and sales from digital goods and services are not the same as App Store billings.

** Changes from both 2019 to 2020 and 2020 to 2021 are based on updated numbers. See Appendix for more details.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

**** Europe includes countries in Western, Central, and Eastern Europe (including the UK and the Nordic Region, not including Russia).

The Continued Growth and Resilience of Apple’s App Store Ecosystem

11

Between 2019 and 2022, the categories of iOS-app-based purchases of physical goods and

services saw large changes across regions.

Sustained increases in general retail, grocery, and food delivery categories in the US

and China; slower growth or decreases in Europe. In 2020, we saw large increases in the

general retail, grocery, and food delivery and pickup categories in the US and Europe, a

trend that continued in 2021 as more consumers used apps for purchases. Food delivery

apps such as DoorDash (US) and Deliveroo (Europe) expanded their reach.

v

Grocery

delivery startups such as Weee (US) are launching and growing as a result of these shis,

vi

and major grocery retailers such as Tesco (UK) are moving to in-app ordering. Some of

these trends slowed in 2022, particularly food delivery in both regions and general retail in

Europe.

In 2021, grocery and food delivery and pickup increased the most in China, with growth

rates of 69% and 56%, respectively. The lockdowns and strict quarantine measures in

China that followed the rise of new coronavirus variants and outbreaks were likely the

drivers of these changes.

vii

In 2022, the growth rates for grocery and food delivery remained

high (21% and 37%). (See Sidebar.)

iOS-app-based

general retail

sales increased

more than

2x

in all regions

since 2019.

iOS-app-based

grocery sales in

the US increased

6x

since 2019.

iOS-app-based

food delivery and

pickup sales in

Europe and China

increased more

than

2x

since 2019.

US

Europe

China

Rest of World

150

200

250

300

100

2019 2020 2021 2022

General Retail

200

300

400

600

500

100

2019 2020 2021 2022

Grocery

150

200

250

300

100

2019 2020 2021 2022

Food Delivery and Pickup

The above figures show sales

between 2019 and 2022, indexed on

2019 (i.e., 2019=100). The underlying

data behind sales of physical

goods and services categories were

retroactively updated from previous

reports. Figures are produced based

on updated numbers for 2019 and

2020.

Categories with Sustained

Increases in Sales,

2019-2022

The Continued Growth and Resilience of Apple’s App Store Ecosystem

12

A continuing rebound in travel and ride hailing. The travel and ride hailing categories

declined in all major regions in 2020, as mobility and tourism halted worldwide. In 2021,

these categories rebounded in the US and Europe, with both categories rising above pre-

pandemic levels in Europe. China followed suit in 2022, reflecting the differing impact of

the pandemic and restrictions on travel in different regions. The increase in travel-related

in-app spend reflects the changing consumer m-commerce trends towards one-stop-

shop convenience. Major airlines now have dedicated apps to help plan and book travel.

In 2022, travel was well above pre-pandemic levels in all regions; ride hailing was as well,

except in the US, where it was back to its pre-pandemic level. (See Sidebar.)

A rebound in in-app ad revenue in the US and China. In-app advertising revenue was

substantially higher in both the US and China in 2022 compared to 2021 (up 22% in the

US in 2022 compared to 4% in 2021, 49% in China in 2022 compared to 15% in 2021). This

growth was driven by ad spend in non-gaming apps such as video apps, retail apps, and

podcasts.

Looking ahead

While the world in 2021 began to adjust to a “new normal” in which hybrid models and

in-app purchases became increasingly prevalent, COVID-19 pandemic-driven restrictions

gradually relaxed or phased out across regions throughout 2022. 2022 also came with

global and economic challenges, such as the war in Ukraine, regulatory headwinds in the

video game industry in China, higher gas prices, supply chain disruptions, inflation, higher

interest rates, and foreign exchange headwinds. On the App Store ecosystem, in-app

purchases of digital goods and services stabilized, while the growth in in-app purchases

of physical goods and services and in-app advertisement was strong. We anticipate that

the App Store ecosystem will continue to evolve and adapt to the dynamic needs of

customers across regions.

In the US,

iOS-app-based

travel-related

sales increased

54%

since 2021.

In Europe

iOS-app-based

ride hailing sales

increased

58%

since 2019.

The above figures show sales

between 2019 and 2022, indexed on

2019 (i.e., 2019=100). The underlying

data behind sales of physical

goods and services categories were

retroactively updated from previous

reports. Figures are produced based

on updated numbers for 2019 and

2020.

Categories with

Rebounding Sales,

2019-2022

US

Europe

China

Rest of World

100

150

200

250

50

2019 2020 2021 2022

Travel

100

150

200

50

2019 2020 2021 2022

Ride Hailing

The Continued Growth and Resilience of Apple’s App Store Ecosystem

13

Fieen years of the App Store

By the Numbers

iOS APPS AND

USER CHOICE

370+ billion

downloads since 2008

123x more apps available

now compared to the end of

2008

15x more annual

downloads in 2022 than 2009

650+ million average

weekly visitors to the App Store

TRUST AND

SAFETY

1.7 million App Store

submissions rejected in 2022

$5+ billion

in

fraudulent transactions

prevented since 2020

SUPPORT FOR

DEVELOPERS

40+ SDKs & 250,000 APIs

Education

Developer Academies, Apple-

certified trainings, Entrepreneur

Camps, and learn to code programs

More ways

to process payments:

50 storefronts with carrier billing

20+ storefronts with third-party

electronic wallets

40+ billion average weekly

automatic app updates

DEVELOPER

GROWTH

$320+ billion

developer earnings since 2008

126x more earnings in

2022 than 2009

200+ countries with active

developers in 2022

(vs 69 in 2008)

54% downloads from outside

developers’ home country

By the Numbers

The Continued Growth and Resilience of Apple’s App Store Ecosystem

14

An explosion of opportunities and choices

The App Store was the first of its kind when it opened in 2008. For the past 15 years, it has

offered a seamless and trusted way for users to download apps and new technologies.

In doing so, the App Store has supported an explosion of opportunities for developers of

various types of apps, leading to a proliferation of app-based products and services across

app categories for consumers.

Users can now choose from tens of thousands – sometimes hundreds of thousands – of

apps across more than 20 categories that they can download. Users today have access

to over 123 times more apps than they did at the end of 2008. Annual downloads on the

App Store have increased 15-fold between 2009 – the first full year the App Store was in

operation – and 2022. Since the launch of the App Store, users have downloaded apps

more than 370 billion times.

Developers of all sizes from all over the world have found opportunities on the App

Store. At the end of 2008, developers who published apps on the App Store hailed

from 69 countries; today, they come from nearly every country in the world. The share

of developers from regions other than the US and Europe has grown from 18% to 48%

between the end of 2008 and 2022, with the share of developers from China climbing from

1% to 12%. The App Store provides opportunities for developers to distribute their apps

globally: In 2022, 54% of downloads occurred in storefronts outside of developers’ home

countries.

Developers earned over $320 billion in total on the App Store between 2008 and the

end of 2022, and yearly developer earnings have grown 126-fold between 2009 and

2022. Monetization options have expanded: When the App Store started, developers

could only monetize their apps directly via the App Store through app purchases; now,

app purchases are responsible for less than 1% of earnings. In-app purchases account

for the majority of developer earnings (about two-thirds), and subscriptions, which now

account for about one-third of earnings, are growing. Subscriptions have been increasing

globally, and are offered by many different businesses, ranging from physical bookstores,

to e-commerce stores, to streaming platforms.

viii

The App Store is no exception, and

developers have embraced this global trend. The App Store provides features like the

ability to cancel subscriptions easily, as well as a reduced developer commission rate on

revenue from subscriptions aer the first year. Over the years, more and more developers

across different categories have embraced subscriptions as their preferred monetization

strategy.

Many segments have seen an enormous increase in choices for users and opportunities

for developers on the App Store. By the end of 2008, for example, users could choose

from only 3,200 games; by the end of 2022, they could choose from nearly 220,000, more

than a 60-fold increase. Business apps have become more important for users in recent

years, especially during and in the aermath of the COVID-19 pandemic: The App Store

went from hosting only 350 business apps at the end of 2008, to over 190,000 by the end of

Our 2022 study, “The

Success of Third-Party Apps

on the App Store,” provides

more detail on how the

options for developers and

content creators to reach

consumers have changed

over time.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

15

2022. Also, both education and health and fitness are important categories that now offer

consumers tens of thousands of choices.

Figure 2: Number of iOS Apps at the End of 2008 and 2022,

Select App Store Categories

220K

3,200

190K

170K

90K

Games

Business

Education

Health &

Fitness

350

1,000

430

2022 2008

This increase in choices has transformed many aspects of our daily life. As just one

example, consider how the experience of going on a trip has been transformed by apps.

Prior to the App Store, a typical travel experience included printing paper boarding passes

from one’s computer, waiting at a taxi stand or bus stand for a ride from the airport to one’s

destination, using unwieldy folding maps to navigate a new city or expensive and clunky

GPS devices while driving, and waiting to get back home to share photos and videos

with family and friends. Since the advent of the App Store, this experience has been

transformed: Mapping apps make it easier to navigate a new destination and find reviews

of aractions and restaurants, ride hailing apps allow travelers to get around an unfamiliar

city, and communication and social media apps allow travelers to share photos and videos

in real time.

Supporting new and growing sectors of the economy

The ability to distribute soware – specifically, apps – seamlessly through hundreds of

millions of devices, paired with Apple’s hardware and soware advances, made entirely

new types of apps possible and allowed other categories of apps to scale massively.

˿ Mobile gaming: In the early days, mobile games such as Tetris and solitaire offered

a simple experience to pass the time. Since then, advances in hardware, soware,

graphics, and screen quality have led to an explosion of mobile gaming. Games that

use heightened processing capabilities, realistic graphics, and augmented reality

provide a state-of-the-art gaming experience without the need to buy a console.

˿ Transportation platforms and food delivery: Since launching nearly 10 years

The Continued Growth and Resilience of Apple’s App Store Ecosystem

16

ago, ride hailing platforms have revolutionized how people get around worldwide,

leveraging riders’ and drivers’ use of connected devices that can track their

locations. This new paradigm has been extended with the emergence of micro-

mobility apps that offer bike, e-bike, and scooter sharing, and car sharing apps

that allow users to rent a car for a few hours. Similarly, food delivery apps connect

a network of customers, restaurants, and delivery drivers by taking advantage

of mapping and location technology. Apps give users and workers the ability to

complete these transactions without needing to carry cash or credit cards.

˿ Music streaming and video streaming: The ability to stream content at any time and

in any place contributed to the expansion of music and video streaming services.

Improvements in baery life, screen size, and screen quality have made watching

content on iPhone and iPad more enjoyable. Additionally, digital rights management

features, such as technology that prevents users from screen recording while the

video is playing, have helped protect content owners and allowed video streaming

services to flourish.

˿ Education: Education apps are used by teachers, parents, and students to support

learning. Apps can help teachers manage classrooms, communicate with parents

and students, and help students study or explore new topics. The use of education

apps to support learning also increased during the pandemic when in-person

schools were temporarily closed. Outside of the classroom, apps have also helped

people of all ages learn new languages and new skills.

˿ Connected home devices: The App Store has also enabled a new generation of

physical products like smart thermostats, doorbells, locks, baby monitors, and light

bulbs, which make users’ homes more comfortable, functional, and secure. Users’

ability to remotely control these devices or view the data they collect via apps has

greatly improved their utility.

˿ Civic engagement: Governments increasingly rely on apps to facilitate interactions

with citizens. For example, apps allow citizens to report non-emergency issues,

check the schedule of trash pickup, find federally funded health centers, or apply

for assistance aer an emergency. During the COVID-19 pandemic, public health

authorities created apps to track exposure through the Exposure Notifications

APIs developed by Apple and Google, and to provide citizens access to COVID-19

screening tools and information, among other features.

Honkai: Star Rail (China,

2023) is a role-playing

space fantasy game that

was one of the most

highly anticipated and

successful RPG releases

of 2023.

Weee! (US, 2014)

is a grocery delivery app

that allows users to shop

for Asian and Latino food

options.

Ten Percent Happier (US,

2015) is a meditation app

that helps users start and

sustain a mindfulness

practice.

Twinkl (UK, 2017) is an

educational app that

provides teachers access

to a variety of educational

resources, including

worksheets, lesson plans,

educational games, and

more.

Examples of apps

from new and growing

sectors of the economy

The Continued Growth and Resilience of Apple’s App Store Ecosystem

17

Connected home devices

The market for connected home devices has grown quickly over the last five

years.

ix

In 2022, categories of connected home devices that typically rely on apps to

control, and sometimes use, the device and view data generated $49 billion in global

revenue.

x

These devices include security devices like Ring and smart camera, home

entertainment devices like Sonos, energy management tools like Nest, and comfort

and lighting tools like GE’s smart light bulbs controlled by the Cync app.

The growth of connected home devices has been a global phenomenon: For

example, $13 billion in revenue came from Europe in 2022.

xi

Global manufacturers

of connected home devices include Siemens, a multinational corporation

headquartered in Germany that offers a suite of connected home devices controlled

via an app; Arkifi, a Chilean-based company offering smart locks; and tado°, a

German-based company producing smart thermostats.

Supporting users’ everyday health

Users can find thousands of apps on the App Store to help them adopt healthier

lifestyles. Many of these apps take advantage of Apple’s HealthKit API, which allows

the use of sophisticated sensors on iPhone and Apple Watch, while ensuring that

user data is safe according to Apple’s rigorous privacy and data security protocols. In

addition, there are an increasing number of connected devices that work alongside

HealthKit-enabled apps. Popular consumer-targeted health apps include:

̥ Running apps like Nike Run Club

̥ Fitness apps like MyFitnessPal

̥ Sleep apps like Rise: Energy & Sleep Tracker, SnoreLab, and Pillow

̥ Meditation and mindfulness apps like Calm, Headspace, and Ten Percent

Happier

̥ Hearing-related apps like SonicCloud

̥ Nutrition apps like WeightWatchers and Lose It!

̥ Medication and symptom tracking apps like Pt Pal Pro and Medisafe

Medication Management

̥ Apps that work alongside connected devices like Qardio heart health to

measure blood pressure, Withings Health Mate to measure weight, and

ReSound to work alongside hearing aids

The Continued Growth and Resilience of Apple’s App Store Ecosystem

18

New ways to engage with customers and to lower costs

Many traditional businesses have used apps in innovative ways to improve their

customer experiences and/or provide their services more efficiently. For example,

airlines have developed apps that provide an ever-growing array of features for their

customers. Through apps, users can conveniently store and access mobile boarding

passes, check flight status, modify reservations, receive gate and baggage updates, access

the plane’s entertainment system, and more. Some of these features have reduced costs

as well, such as the cost savings from phasing out in-flight entertainment system screens

or printing paper boarding passes.

xii,xiii

Similarly, banks have developed apps that facilitate mobile check deposit using the phone

camera, send fraud alerts, and allow customers to quickly check balances or transfer

money. The extra convenience for consumers has also led to lower costs for banks

from the reduction in in-person visits to physical branches.

xiv

Supermarket apps allow

consumers to order items on the go, check savings and deals, look up store maps and

aisle locations, scan items for prices, and pay directly through the app.

App-based innovations also extend to cultural and recreation activities: Visitors to art

museums can now use mobile apps to take a wide variety of self-guided tours or listen to

audio descriptions of individual artwork that catch their aention. Theme parks have apps

that allow visitors to view wait times for popular rides, navigate the park, and view activity

schedules. Many ski resorts now offer apps that allow visitors to check real-time weather

conditions and forecasts, get updates on li closures, and view trail maps.

United Airlines (US,

2011) United Airlines'

app allows users to book

flights, access in-flight

entertainment, pay for

in-flight snacks and

drinks, check in for flights

and download boarding

passes, track bagages,

and more.

USAA (US, 2009) United

Services Automobile

Association was one of

the first financial service

companies to offer mobile

check deposit using

iPhone’s camera.

John Lewis & Partners

(UK, 2011) is a department

store app that allows

users to browse products,

use augmented reality

features to "try before you

buy," and get notifications

when products are back

in stock.

Examples of apps that

provide new ways to

engage with customers

The Continued Growth and Resilience of Apple’s App Store Ecosystem

19

Innovations from healthcare providers and the medical community

Healthcare providers and the medical community use apps to deliver cuing-edge

care to patients and conduct groundbreaking research. These apps include:

Epic Rover, which helps manage clinical communication by pairing

iPhones with patient charts and has a scanning feature to streamline the

administration of medication.

StrivePD, which uses Apple’s Movement Disorder API to help measure

and record tremors and muscle movements associated with Parkinson’s

disease.

Buerfly iQ+, a handheld ultrasound device that was built using Apple’s

developer tools and has expanded access to ultrasound imaging.

Epic’s MyChart app, which is integrated with HealthKit and paired with

third-party medical devices (for example, blood pressure cuffs and

glucose monitors), and provides digital medicine programs for patients

with hypertension and diabetes.

One Medical, which allows patients to participate in telehealth video

appointments in the app, schedule visits, message with providers via

video or chat, manage prescriptions, and view health records.

Apple Research, built on the ResearchKit framework, which is

broadening the scope of possibilities for researchers while maintaining

complete control over data sharing for participants.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

20

Scholarship in economics and business strategy shows

that digital marketplaces create value by facilitating

interactions between different sets of users.

xv

The

App Store, a digital marketplace, makes it easier for

Apple iOS device owners and developers to interact. This

means that the App Store has the incentive to bring both

sides on board and encourage their interactions.

xvi

Apple

benefits if iOS users have more positive experiences

downloading and using apps, and if developers have the

tools and support from Apple to create beer apps.

To succeed, digital marketplaces need to actively

manage the interactions between developers and iOS

users and create trust to ensure continued participation

from both sets of users.

To do so, digital marketplaces rely on technology,

processes, and policies to improve the quality of

interactions on the platform.

xvii

This is an iterative

process that requires work and investment, adjusting

to changing conditions, and incorporating new

technologies as they become available.

Apple’s focus on device owners and developers

contributes to making the App Store a vibrant

marketplace with over 650 million average weekly

visitors, and over 747 million and 1.5 billion average

weekly downloads and redownloads, respectively.

1.7m

App Store

submissions

rejected in 2022

$5b+

in fraudulent

transactions

prevented since

2020

950,000+

apps rejected for

privacy violations

since 2020

690m+

fraudulent

customer accounts

deactivated since

2020

Apple device owners: Providing a safe, secure, and private

platform for users to discover new apps

Trust and safety have been central to the growth in app downloads and usage

over time. Compared to the early 2000s, when downloading soware always

came with the risk of infecting the device with a virus or becoming victim to

a scam, the App Store has brought peace of mind to users downloading apps.

Apple’s unique approach integrates hardware, soware, and other services, such

as safe payment options, to provide users with a secure and private experience

to discover and enjoy new apps. Apple’s policies and rules, for example for App

Review, ensure the App Store remains a safe marketplace.

Apple has heavily invested in the development of policies to foster user trust

and the deployment of resources to enforce them. Many of these rules apply

even before apps are released on the App Store. Before submiing new apps

for review, Apple requires developers to provide detailed information about

how the apps, and any third-party products integrated into the apps, deal with

privacy and user data. Once developers submit their apps, Apple’s screening

mechanisms ensure that apps and all in-app content meet the App Store Review

Guidelines, are periodically updated, and do not represent a privacy risk for

users. Additionally, automatic app updates make it easy and seamless for users

to have the latest and safest app versions. Apple has also developed multiple

mechanisms to remove bad actors and prevent fraud on the App Store, including

by removing fraudulent reviews, removing fraudulent users and developers, and

preventing payment and credit card fraud.

The need to encourage platform usage on both sides

The Continued Growth and Resilience of Apple’s App Store Ecosystem

21

Serving Developers: Tools to foster success

Apple’s continual investments in the iOS ecosystem facilitates the

development and discovery of new apps, gives developers the ability to add

new functionality to their existing apps, and provides access to metrics to

track app usage.

Since 2008, Apple has released over 40 SDKs and 250,000 APIs for

developers, including HealthKit (2014), which provides a secure option

to create apps based on user health data, and the Metal API, which can

improve running time and be used to create state-of-the art 3D designs

for games. Technical tools like Xcode and Swi (2014) lower the

technical barriers to design, and make it easier to debug and optimize

apps. And testing tools such as TestFlight (2014) connect developers

and users during the app’s testing phase. Apple also provides

developers with the option to collect data on app performance, which

can inform improvements to their apps.

Apple’s App Analytics tools, such as “Peer Group Benchmark,” allow

developers to track the performance of their apps by monitoring

downloads, active sessions, paying users, and in-app content.

The App Store gives developers multiple alternatives to monetize their apps,

including by offering subscriptions and/or employing different business models

(free, freemium, paid, paymium). It also supports many payment methods,

including payments in local currencies, carrier billing (which allows users to pay

developers through their monthly phone bill), Apple Pay, and other methods that

leverage third-party companies.

Support for

students

through programs such

as “Everyone Can Code,”

“Develop in Swift”, and

“Swift Playgrounds”

Support for

new developers

through Developer

Academies and

Apple-certified trainings

Support for iOS

entrepreneurs

through Entrepreneur

Camps, App

Accelerators, and

developer workshops

around the world

Our 2021 study, “A

Global Perspective of

the Apple Ecosystem,”

provides more details

on how Apple supports

developers.

73

storefronts where Apple

offers the option to pay in

local currency

Thanks to the App Store, developers can seamlessly distribute their apps around the world and make sure users

discover their apps. The App Store facilitates on average more than 747 million app downloads, 1.5 billion

redownloads, and 40 billion automatic app updates each week. The App Store’s global marketing team, editors, and the

“Today,” “App of the Day,” and “Game of the Day” features are examples of how Apple helps developers drive discovery of

their apps.

50

storefronts that offer carrier billing,

including O2 in Germany (2015), BYT

in France (2017), Optus in Australia

(2019), and WOM Nextel in Chile (2022)

26

storefronts that offer third-party

electronic wallets including Alipay in

China (2016), Kakaopay in Korea (2019),

and Dana in Indonesia (2020)

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A1

Appendix

Appendix Table 1: Breakdown of Where Apple Collects a Commission on Billings and

Sales Facilitated by the App Store

Apple does not collect a commission on:

Q Digital goods and services that are purchased outside of the

App Store, for example:

* Subscriptions to multiplatform video streaming apps like Hulu

* Subscriptions to audiobook apps like Audible

* Subscriptions to music streaming apps like Spotify

* Subscriptions to news and magazine apps like the NY Times

Q Physical goods and services ordered within-app, for example:

* Ordering a ride through the Uber app

* Placing an order on the Amazon app

* Ordering grocery delivery through Instacart

* Transaction fees on digital payments occurring through apps

Q In-app advertising for apps that make money through in-app

advertising, for example:

* Non-gaming apps like Pinterest and YouTube

* Gaming apps like Rolly Vertex and Helix Jump

Apple collects a commission on:

Q Digital goods and services that are

purchased in or through the App Store,

for example:

* In-app subscriptions to multiplatform

video streaming apps like Hulu

* In-app subscriptions to education

apps like Duolingo

* In-app purchases of a game's bonus

features

* In-app subscriptions to news and

magazine apps like the NY Times

Billings and Sales Facilitated by the App Store Ecosystem: $1,123 Billion

No commission: More than 90%

Commission: Less than 10%

Appendix Table 2: Estimated Billings and Sales Facilitated by the App Store Ecosystem,

Large Regions, 2021 ($ Billion)*

US China Europe****

Rest of the

World Total

Digital Goods and Services** $38 $20 $11 $33 $102

Physical Goods and Services $153 $344 $91 $90 $678

M-Commerce

General Retail $86 $273 $60 $52 $471

Travel $17 $13 $12 $14 $56

Food Delivery and Pickup $20 $26 $9 $11 $66

Grocery $8 $21 $5 $8 $43

Ride Hailing $17 $7 $5 $5 $33

Digital Payment $4 $5 - - $9

In-App Advertising*** $41 $17 $14 $16 $88

Total $232 $381 $116 $139 $868

* Totals may not sum due to rounding.

** Billings and sales from digital goods and services are not the same as App Store billings.

*** iOS in-app ad revenue; does not include mobile web, search ads, and Apple Search ads.

**** Europe includes countries in Western, Central, and Eastern Europe (including the UK and the Nordic Region, not including Russia).

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A2

Methodological approach

To arrive at our results, we distinguish among three primary app monetization strategies

that developers use:

˿ The first monetization strategy is to sell and distribute digital goods and services.

Sales and distribution of digital goods and services can occur through the

App Store in the form of paid app downloads and in-app purchases, or through the

sale of digital content and subscriptions from multi-platform apps that allow for the

use and consumption of the app, both on the App Store ecosystem and elsewhere.

Examples of apps using this monetization strategy include those for gaming, dating,

video and music streaming, fitness and health, and news and magazines.

˿ The second monetization strategy is to sell physical goods and services through

the app. Apps using this monetization strategy are m-commerce apps generally,

including apps for ride hailing, food delivery and pickup, grocery delivery and pickup,

general retail, and travel, as well as digital payment apps.

˿ The third monetization strategy is to sell in-app advertising. Examples of apps

using in-app advertising as their primary monetization strategy are social media and

short video sharing apps.

We employ different methodologies to estimate billings and sales facilitated by the

App Store ecosystem for each of these monetization strategies. In so doing, we rely on

a variety of data sources, including data from Apple, app analytics companies, market

research firms, and individual companies. To ensure the reliability and robustness of our

estimates, we validate and compare key inputs from different data sources.

4

We are continually working to improve on our methodology and to adjust for changes

in underlying third-party data. As a result, estimates and changes seen throughout

this report may differ from those presented in previous years’ reports. Where and when

applicable, we have made note of reliance on updated estimates.

Sales and distribution of digital goods and services

Apps used to sell and distribute digital goods and services fall into two subcategories:

˿ Certain app developers choose to monetize their iOS apps only through the

App Store, and those apps can only be used on the iOS platform.

5

Most billings from

these apps come from games, which involve a one-time payment or, more oen,

in-app payments that allow app users to remove ads, unlock bonus levels, or access

premium features.

6

This category also includes most photo-editing apps and dating

4 This methodological approach is consistent with the one used in our 2019 and 2020 App Store ecosystem

studies.

5 Developers may also offer the same digital goods and services through apps on other platforms, such as

Android.

6 Our analysis does not include billings generated from the Apple Arcade gaming service. Apple Arcade provides

participating developers with an additional business model – distinct from the App Store – in which Apple

supports the development costs of Apple Arcade games. Many small and independent developers with games

in Apple Arcade also monetize with other free-to-play or paid games on the App Store.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A3

apps, as well as apps for short video, among others.

˿ Other apps allow for the consumption of digital goods and services both within the

App Store ecosystem and elsewhere. These so-called multi-platform apps allow

consumers to pay through either the App Store or another platform or device. In

other words, consumers use non-device-specific subscriptions or purchases to

enjoy the digital goods and services provided. Multi-platform apps can be further

divided into consumer apps and enterprise apps.

- Consumer apps typically offer paid digital content – such as movies, music,

audiobooks, news, meditation courses, and fitness classes – that can be

consumed within the app. Moreover, they may offer paid digital services obtained

on the app, such as educational services, password management, job search,

and access to job platforms.

- Enterprise apps allow businesses and organizations to provide tools and

capabilities through smartphones and tablets. These include communication

and collaboration apps, mobility management solutions, cloud-based business

apps, and file hosting services. These apps usually make money by selling

subscriptions to corporations and institutions outside of the App Store.

To distinguish between these two subcategories of apps, we manually review the

most popular apps in each App Store category, focusing on their business models and

monetization strategies. We use this information to ascertain (1) whether the app can be

used on mobile or computer browsers, or on a different app platform; and (2) whether an

app on an Apple device can be used through a subscription or purchase made outside the

App Store.

Methodology for iOS apps that sell only through the App Store

For iOS apps that sell digital goods and services only through the App Store, we count

total billings, which include Apple’s commission.

7

We use billings because they represent

the total amount customers pay.

7 In 2022, Apple’s commission rate was 30% for the sale of digital goods and services; for subscriptions, it was

30% for the first year and 15% for any subsequent years. Developers who made up to $1 million in 2021 for all

of their apps, as well as developers new to the App Store, qualify for the Small Business Program and pay a

reduced commission of 15%.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A4

Methodology for multi-platform apps

Background. For multi-platform apps, estimating the volume of sales facilitated by the

App Store is complex because subscriptions and purchases associated with them are not

device specific. The lack of device-specificity creates a dual challenge:

˿ First, consumers can pay to access multi-platform digital goods and services in

different ways, regardless of where they consume those goods and services. In

some cases, consumers pay through the App Store, but sometimes they do not.

˿ Second, multi-platform apps allow users to access content and services across

different devices, including non-Apple devices. For example, consumers can

stream videos through smart TVs, connected TV devices, video game consoles,

smartphones, tablets, and web browsers, and across different platforms (Apple,

Android, etc.).

Because of these two characteristics of multi-platform apps, billings that flow through the

App Store are not necessarily a reliable indication of Apple users’ engagement with multi-

platform apps. Consequently, we must be deliberate about aributing the appropriate

share of billings and sales to the App Store ecosystem.

Example. To illustrate these challenges, consider the video streaming service Hulu. The

Hulu app is free to download, but a subscription is necessary to watch content on the

iPhone, iPad, and Apple TV apps. A Hulu subscription can be purchased in one of two

ways:

˿ Through the Hulu app on an Apple device, in which case the purchase happens

through the App Store. But a subscription purchased through the App Store can

also be used to watch Hulu on other platforms. Consequently, it would be incorrect

to aribute all of the App Store billings (the full subscription amount) to the

App Store ecosystem because it would overstate the value of the Hulu product

enjoyed on Apple devices specifically.

˿ Outside of the app (on a Mac or PC via web browser, for example), in which case

the purchase does not happen through the App Store, and there are no App Store

billings. However, the subscription can be used to watch content on Hulu using

apps on Apple devices. Consequently, it would be incorrect to use the App Store

billings (which are zero) as an input to our App Store ecosystem results, because

it would understate the value of the Hulu product enjoyed through apps on Apple

devices.

Methodology. To address these challenges, we generally do not rely on App Store billings

for multi-platform apps. Instead, we rely on the proportion of use that occurs on apps in

the App Store ecosystem to estimate how much of the total sales of multi-platform apps

(App Store plus non-App Store) is facilitated by the App Store ecosystem.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A5

Consider, for example, not just Hulu but the entire video streaming industry, a market

with more than $30 billion in total annual sales in the US in 2022.

xviii

Users consume video

streaming content over a mix of smartphone apps, tablet apps, desktop browsers, smart

TVs, connected TV devices, and video game consoles. To estimate the volume of sales

facilitated by the App Store ecosystem, we first take the portion of hours streamed on

smartphone apps, tablet apps, and smart TVs of all types. We then apportion this share to

Apple devices specifically, using the Apple market share for each device category.

Using this framework and approach, we estimate the volume of sales facilitated by the

App Store ecosystem for several categories of apps offering similar types of goods and

services. The app categories for which we estimate sales facilitated by the App Store

are video and music streaming, e-books and audiobooks, newspapers and magazines,

and enterprise. We use third-party research to account for the variation in users’ app

consumption habits across categories and countries. For example, consumers oen listen

to music and audiobooks through apps on mobile devices, while they are more likely

to stream videos on smart TVs. Those consumption habits may also vary by geography.

Additionally, when the data are available, we take into account any variation in the

consumption paerns of iOS (and non-iOS) users by app type and geography.

For each app category, we estimate total sales by geography by relying on inputs from

third-party sources, typically market research firms.

xix

We then apportion those sales

using the share of content consumed on apps on any platform by geography, based

on information collected from marketing surveys, company reports, or data on usage

paerns.

xx

Finally, we apportion usage to Apple iOS devices specifically by using the iOS

market share for each device category in each geography.

xxi

We use a more tailored approach for enterprise apps for a number of reasons. First, usage

paerns are more heterogeneous for enterprise apps. Second, app-based usage and

desktop-based usage of enterprise products tend to be more integrated. Third, the pricing

of enterprise products is less transparent and more complex than for consumer apps.

With these complexities in mind, we individually estimate sales from 10 major enterprise

apps or families of apps; Microso Office 365, Google Workspace (i.e., enterprise versions

of Google productivity tools such as Gmail and Google Docs), Adobe (Acrobat), WPS

Office, Dropbox, Box, Baidu Drive, Webex, Zoom, and Slack. We also include an aggregate

market-level estimate for mobility management apps, which allow employees to securely

access business content.

Finally, for some categories of apps, we use billings from the App Store as a proxy for

sales facilitated by the App Store ecosystem. We do this for categories of apps, such as

education or fitness apps, for which consumers typically consume the content within

the app but may purchase it outside of the App Store. This methodology likely results in

a conservative (or lower) estimate compared with an estimate relying on usage-based

apportionment.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A6

Sales of physical goods and services through the app

Many developers monetize their apps by selling physical products through their apps.

These include:

˿ Apps that let customers purchase physical goods and services. We broadly refer to

these as m-commerce apps. The group includes apps for general retail, ride hailing,

food delivery and pickup, grocery delivery, and travel.

˿ Apps that enable digital payments or transfers, such as mobile point-of-sale apps

that rely on QR codes and peer-to-peer transfer apps.

M-commerce

Globally, mobile apps are an increasingly important e-commerce channel due to

their convenience. This growth has been most pronounced in China, the leader in

m-commerce.

8

Apps of retailers such as Amazon and Target allow consumers to browse

and purchase physical goods directly in the app and offer in-store pickup or delivery. In

addition, mobile apps – including those for ride hailing, food delivery and pickup, grocery

delivery and pickup, and mobile pickup ordering – have been central to the creation or

expansion of certain business models.

Sales on m-commerce apps do not flow through the App Store.

9

We therefore use

third-party data to estimate the volume of sales of physical goods and services from

transactions on mobile apps.

10

We provide results for several categories of apps: general

retail, food delivery and pickup, travel, grocery, and ride hailing.

For many of our m-commerce categories, we rely on Statista’s Digital Market Outlook and

Mobility Market Outlook data for online sales revenue. In 2022, Statista updated their

methodology to estimate industry revenues to use current exchange rates, rather than

fixed exchange rates, with the goal of being more accurate. As a result, their 2019, 2020

and 2021 estimates were retroactively updated.

For each app category, we estimate the total volume of e-commerce or m-commerce

sales by geography, relying on estimates of third-party sources, typically market research

firms.

xxii

We then apportion the volume of sales, if necessary, to purchases that occur via

smartphone and tablet apps. For example, for online food delivery and pickup, customers

may place orders via an app, a mobile browser, or a desktop browser. We estimate the

share of each app category’s sales that occur via mobile apps, within each geography,

8 In China, more than 80% of online retail is mobile. Additionally, most mobile commerce occurs through apps

and to a lesser – but increasing – extent through “mini-programs” on platforms such as WeChat, Baidu, and

Alipay. See, eMarketer; QuestMobile, "China Mobile Internet 2019 Half Year Report"; Aladdin, "2019 Mini-

Programs White Papers," January 2, 2020.

9 Since the launch of the App Store, Apple’s policy has been to not charge a commission on sales of physical

goods and services or advertising.

10 The sales associated with purchases made on mobile browser apps are excluded.

The Continued Growth and Resilience of Apple’s App Store Ecosystem

A7

using information collected from marketing surveys or data on usage paerns.

xxiii

Finally,

we apportion usage to Apple platforms based on the overall iOS share market share.

11,xxiv

Digital payments

Digital payment apps have become increasingly popular worldwide, although the

landscape differs substantially across countries. In China, currently the largest market for

digital payments, two QR code-based payment apps, Alipay and WeChat Pay, dominate

both online and brick-and-mortar points of sales. These apps charge merchants a fee on

purchases paid for with their apps. In the US, app-based payment systems are a relatively

nascent market

xxv

while peer-to-peer transfer apps such as Venmo and Cash App are

already popular and have grown significantly in recent years.

xxvi

In this year's study, we also

consider India’s growing digital payment market driven by PhonePe; however, they remain

significantly smaller than the US and China.

We estimate the transaction fees collected by developers from customers or merchants

for payments and transfers occurring through apps on the iOS platform.

12

For QR code-

based payment apps in China, we start with an estimate of total payment volume (TPV)

from a third-party research firm.

xxvii

We then estimate WeChat Pay and Alipay total

transaction fees using their published fee rates and deductible policies. For peer-to-peer

transfer apps in the US, we use the ratio of total transaction fees to TPV from Venmo and

Cash App to estimate the transaction fees collected by the apps. For digital payment

apps in India, we start with a third-party estimate of total transaction value of digital

payments,

xxviii

as well as PhonePe’s revenue and market share to back-out the total fees

and average fee rate generated from digital payments. Finally, we apportion usage to Apple

platforms based on data on the overall iOS share in each region.

xxix

In-app advertising

In-app advertising is a frequently used and effective method of monetizing apps whereby

developers publish advertisements within their apps. Prominent examples of apps that

primarily make money through in-app advertising are Instagram, Twier, YouTube, and

Pinterest, and Sina Weibo in China. Examples of games are Rolly Vortex and Helix Jump.

These apps tend to be free to download and use, but in-app advertising can also be a

complementary monetization strategy for paid apps or apps with in-app purchases.

Users have been spending more and more time on their mobile devices, particularly using

apps, which has led to an increased share of digital marketing expenditures going toward

in-app advertising. Given that apps are used frequently throughout the day – for example,

during commutes or moments of downtime – in-app advertising allows advertisers to

reach users in ways that other marketing channels cannot. Compared with mobile web,

11 Apportioning by iOS market share almost certainly results in a conservative estimate because owners of iOS

devices tend to spend relatively more than owners of Android devices. See, e.g., Comscore.

12 Our study excludes digital payment apps and services based on near-field communication, such as Apple

Pay. Mobile commerce transactions that occur within an app and are paid with Apple Pay are included in

m-commerce sales.