By Nate Hausman, Project Manager, Clean Energy States Alliance

With New York additions by Max Joel, Jason Mangione,

and Lillie Ghobrial, New York State Energy and Research and

Development Authority (NYSERDA)

2016

New York State

Homeowner’s Guide to

Solar

Leases, Loans,

and Power Purchase

Agreements

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 1

Acknowledgments

Clean Energy States Alliance (CESA) prepared this guide through the New England Solar Cost-Reduction Partnership, a

project under the U.S. Department of Energy (DOE) SunShot Initiative Rooftop Solar Challenge II. The U.S. Department

of Energy SunShot Initiative is a collaborative national eort that aggressively drives innovation to make solar energy fully

cost-competitive with traditional energy sources before the end of the decade. Through SunShot, the DOE supports eorts

by private companies, universities, and national laboratories to drive down the cost of solar electricity to $0.06 per

kilowatt-hour. Visit energy.gov/sunshot to learn more.

The New York State Energy Research and Development Authority (NYSERDA) added New York-specific financing and

incentive programs for solar electric systems into CESA’s ‘Homeowner’s Guide to Solar Financing.

Special thanks to Lise Dondy for her help conceptualizing, preparing, and reviewing this guide. Thanks to the following individuals for their review of the guide:

Maria Blais Costello (Clean Energy States Alliance), Bryan Garcia (Connecticut Green Bank), Janet Joseph (NYSERDA), Max Joel (NYSERDA), Jason Mangione

(NYSERDA), Lillie Ghobrial, (NYSERDA), Elizabeth Kennedy (Massachusetts Clean Energy Center), Emma Krause (Massachusetts Department of Energy Resources),

Suzanne Korosec (California Energy Commission), Warren Leon (Clean Energy States Alliance), Jeremy Lewis (New Mexico Energy, Minerals & Natural Resources

Department), Le-Quyen Nguyen (California Energy Commission), Anthony Vargo (Clean Energy States Alliance), Marta Tomic (Maryland Energy Administration),

Selya Price (Connecticut Green Bank), and David Sandbank (NYSERDA).

U.S. Department of Energy Disclaimer

This material is based upon work supported by the U.S. Department of Energy under Award Number DE-EE0006305.

The information contained within is subject to change. It is intended to serve as guidance and should not be used as a substitute for a thorough analysis of

facts and the law. The document is not intended to provide legal or technical advice.

This report was prepared as an account of work sponsored by an agency of the United States Government. Neither the United States Government nor

any agency thereof, nor any of their employees, makes any warranty, express or implied, or assumes any legal liability or responsibility for the accuracy,

completeness, or usefulness of any information, apparatus, product, or process disclosed, or represents that its use would not infringe privately owned rights.

Reference herein to any specific commercial product, process, or service by trade name, trademark, manufacturer, or otherwise does not necessarily constitute

or imply its endorsement, recommendation, or favoring by the United States Government or any agency thereof. The views and opinions of authors expressed

herein do not necessarily state or reflect those of the United States Government or any agency thereof.

NYSERDA Disclaimer

This document is for informational purposes only. The New York State Energy Research and Development Authority makes no warranties, expressed or implied,

and assumes no legal liability or responsibility for the accuracy, completeness, or usefulness of any information provided within this document. The views and

opinions expressed herein do not necessarily state or reflect those of the State of New York, any agency thereof, or any of the organizations and individuals

that have oered comments as this document was being drafted.

The website addresses provided in this document were accurate as of the date of publication. However, website addresses are subject to change by website

administrators. Therefore, some website addresses may become invalid over time.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 2

Introduction

Are you thinking about installing a solar electric system on your house and

trying to figure out how to pay for it? Solar electric systems are also known

as solar photovoltaic or PV systems. Perhaps you are debating whether

to purchase the system outright or take advantage of a financing option.

Perhaps you are still learning about the financing options available to you.

If you own a home and are thinking about going solar, there is good news. The price of a solar electric system has

come down dramatically in recent years, and there are more ways to pay for it. But with so many solar financing

options now available, the marketplace for these products has become increasingly complex. It can be hard to

choose among the dierent packages and vendors. The dierences between them may not be readily apparent.

Some contracts are filled with confusing technical jargon, and key terms can be buried in the fine print of a

customer contract.

This guide is designed to help homeowners

make informed decisions about financing solar.

This guide is designed to help homeowners make informed decisions and select the best option for your needs

and finances. It describes three popular residential solar financing choices—leases, power purchase agreements or

PPAs, and loans—and explains the advantages and disadvantages of each, as well as how they compare to a direct

cash purchase. It attempts to clarify key solar financing terms and provides a list of questions you might consider

before deciding if and how to proceed with installing a solar electric system. Finally, it provides a list of other

resources to help you learn more about financing a solar electric system.

The guide does not cover technical considerations related to solar electric system siting, installation, and

interconnection with the electricity grid, nor does it cover all of the particular local market considerations that

may impact financing a solar electric system.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 3

Financing Options for Homeowners

The size of a residential solar electric system installation can vary dramatically but is generally between 2 and

20 kilowatts (kW) depending on a variety of factors, including the available roof space (or ground space if it is a

ground-mounted system); site conditions such as roof orientation, azimuth, and shading; the electricity usage of the

home; and available financing. To put these system sizes into context, a 7-kW system in New York State produces

enough electricity for an average New York household in a year.

A system’s size is also a key determinant of its cost. Although the price of systems varies considerably, a residential

solar electric system usually costs between $15,000 and $35,000, roughly the same as a new car. But just as buying

a car outright can be financially burdensome for many automobile customers, so too can paying upfront for a solar

electric system. That’s where solar financing comes into play.

Financing innovations have helped fuel the exponential

growth of the solar market in the United States.

Financing innovations have helped fuel the exponential growth of the solar market in the United States and fall into

two broad categories based on ownership of the solar electric system: third-party ownership and homeowner

ownership via a loan. A later section of this report explicitly compares the types of financing.

Some solar companies will arrange for the installation of a solar electric system and provide financing for it. These

companies are often called full-service solar developers. In other cases, the installer is a dierent entity than the

financial lender. A solar financing lender might be a bank, a solar company, a credit union, a public-private partnership,

a green bank, or a utility.

Third-party ownership of residential solar electric systems allows homeowners to avoid high, upfront system costs and

instead spread out their payments over time. It also often puts some or all of the responsibility for system operation

and maintenance on the third-party owner. Currently, approximately 65 percent of homeowners in New York State who

install solar take advantage of third-party ownership. The two most common third-party ownership arrangements are

solar leases and power purchase agreements (PPAs).

Under a solar lease arrangement, a homeowner enters into a service contract to pay scheduled, pre-determined payments

to a solar leasing company, which installs and owns the solar electric system on the homeowner’s property. The homeowner

consumes electricity produced by the leased solar electric system; however, if the system provides excess electricity to the

grid, the homeowner may get credit for that generation from the electrical utility. As with all types of solar financing options,

under a solar lease arrangement the homeowner pays the regular utility rate for any electricity consumed beyond what

credits the solar electric system generates through excess production sent onto the grid.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 4

Solar leases can

be attractive to

homeowners

because of their

relative simplicity

compared to PPAs.

With a residential solar PPA, a homeowner contracts with a project developer who installs, owns, and operates a solar

electric system on the homeowner’s site. The developer agrees to provide all of the electricity produced by the system to the

homeowner at a fixed per-kilowatt-hour rate, typically competitive with the homeowner’s electric utility rate.

Loan financing is becoming another popular to way for homeowners to pay for solar. Similar to leases and PPAs, solar

loans allow customers to spread the system’s cost over time, but they enable customers to retain ownership of the system,

thereby repaying greater benefits over the lifetime of the system. Solar loans have the same basic structure as other kinds

of loans and are being oered by an increasing number of lending institutions—from banks and credit unions to utilities,

solar manufacturers, state green banks and financing programs, housing investment funds, and utilities. Unlike third-party

solar ownership, a solar loan arrangement enables a customer to own a solar electric system outright and benefit directly

from state and federal incentives. However, the customer also incurs the liabilities associated with ownership.

What You Need to Know

about Solar Leases, PPAs, and Loans

First, you should be aware that solar purchase agreements, solar leases, power

purchase agreements and solar loans are all legally binding documents. It is

recommended that you have any agreement reviewed by an attorney with

experience in the solar marketplace before you sign.

Solar Leases

A solar lease involves a scheduled payment, which is usually monthly. With a solar lease, a developer installs and

owns the solar electric system on the home. In return, the homeowner pays a series of scheduled lease payments

to the developer. A typical lease term is 15-20 years.

Because a lease agreement can deal with system maintenance in a variety of ways, it is important to clarify who is

responsible for maintenance costs as a solar electric system may require maintenance or replacement of parts during

the lease contract term. Most solar leases cover maintenance, but may not cover the cost of replacing equipment

such as the inverter. One common option for the homeowner is to make a single payment toward operations and

maintenance upfront. That approach could reduce the third-party owner’s incentive to provide good maintenance

service. The maintenance risk can be reduced if the solar lease contains a minimum performance guarantee or the

contract clearly states that operations and maintenance are covered by the third party. Such guarantees help ensure

that the third-party owner properly maintains the system.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 5

In New York, for

leases and PPAs,

any applicable

state personal tax

credits go to the

homeowner. However,

under a lease or

PPA arrangement

you would not own

the system, and any

applicable federal tax

credits would go to

the system owner.

The benefits of a solar lease include elimination of most or all of the upfront cost of a system and, if indicated in

the contract, transferring operations and maintenance responsibilities to a qualified third-party owner. Although

homeowners who enter into a lease pay a set price for the equipment (and sometimes maintenance), they do not know

for sure how much electricity the solar panels will produce, so cannot know exactly how much money they will save

on their electric bills. Ideally, monthly electric bill savings will be greater than the lease payments, making for a cash-

positive transaction. Many solar leases come with an escalating (meaning increasing) payment schedule, described

in more detail below. Homeowners should thoroughly scrutinize escalating payment schedules when assessing the

desirability of a particular lease.

The Solar Access to Public Capital (SAPC) working group, convened by the National Renewable Energy Laboratory,

has developed a standardized solar lease template (https://financere.nrel.gov/finance/solar_securitization_public_

capital_finance). This template can be modified to include dierent terms and has not been adopted by all solar

developers. You should closely examine a solar lease contract before executing it or consider having a lawyer read it

before you sign it because terms vary.

Solar Power Purchase Agreements (PPAs)

Under a residential solar PPA, a solar financing company buys, installs, and maintains a solar electric system

on a homeowner’s property. The homeowner purchases the energy generated by the system on a per-kilowatt-

hour basis through a long-term contract at rates competitive with the local retail electricity rate. This allows the

homeowner to use solar energy at a prescribed per-kilowatt-hour rate while avoiding the upfront cost of the solar

electric system and steering clear of system operations and maintenance responsibilities. Because the homeowner

knows how much the solar electricity will cost for the entire term of the PPA, the homeowner is insulated from

possible increases in utility electricity rates. However, it is also notable that if the electricity rates go down, the

homeowner may lose some of the savings.

Ideally, a homeowner’s PPA per-kilowatt-hour payments will be less than the retail electricity rate, making the

transaction cash-flow positive from day one. If you consider this option, you should look carefully at your electricity

bill to see how your current rate compares with the rate proposed by the company oering the PPA. You can ask your

contractor to calculate the projected per-kilowatt-hour rate and annual savings. For PPAs with an escalating rate, you

should consider how any increase in local electricity rates would change your payment.

Visit https://financere.nrel.gov/finance/solar_securitization_public_capital_finance for a SAPC working group

standardized PPA contract. As with all solar financing contracts, you should closely scrutinize a PPA contract before

executing it or have a lawyer read it before you sign it because terms vary.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 6

Solar Loans

Solar loans allow customers to borrow money from a lender or solar developer to install a solar electric system.

With this approach, the homeowner owns the installed system. A wide variety of loan oerings are available with

dierent monthly payment amounts, interest rates, lengths, credit requirements, and security mechanisms. Some

solar loan products oer bundling of energy eciency improvements along with the solar electric installation or

allow for inclusion of roof replacement or energy-related improvements.

Some loans require an asset to serve as collateral to secure the loan. When the lender takes a security interest in the

solar customer’s home, it is called a home equity loan. Unsecured loans do not require an asset to collateralize the loan

other than perhaps the solar electric system itself.

With many solar loans, the solar electric system can start saving the homeowner money right away by structuring the

repayment terms so that the monthly loan payments are less than the resulting reduction in the amount on your home

electricity bill. Alternatively, paying o the loan sooner and over a shorter duration may delay immediate positive cash

flow, but will shorten the time needed to enter the post-loan period when monthly savings will be much greater.

Lenders for solar loans can be banks, credit unions, state programs, utilities, solar developers, or other private solar

financing companies. In New York State, NYSERDA’s Green Jobs – Green New York loan program oers both a Smart

Energy Loan and an On-Bill Recovery Loan. More information on the loans oered, as well as current interest rates, can

be found at http://www.nyserda.ny.gov/All-Programs/Programs/NY-Sun/Customers/Solar-Financing-Options. Private

loans that cover solar may also be available.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 7

Common Terms in Solar Financing

It is important to scrutinize the contractual elements in a solar lease, PPA, or loan.

Here are explanations of some common contract terms.

Buyout Options:

Many third-party financing contracts allow the homeowner to buy out or

pay o the remainder of the payments in one lump sum at any time after a

designated period of time. Some contracts provide for an option to buy out

at the fair market value of the system. Look to see if there is a buyout option

in the contract, under what circumstances a homeowner can buy out of a

contract, and how the buyout price is calculated. Contracts may dier in how

they approach this issue, and methods of calculating buyout prices can vary.

If a clear buyout option is not included in the oer, the homeowner can

always try to request one.

Contract Term:

Contract term, duration, and payback period all refer to the period of time

under which a homeowner’s solar financing agreement is operative. Most

residential financing contracts last for between 5 and 20 years, and some

last even longer. By way of comparison, solar panels typically come with

a 20- to 25-year warranty and their productive lifespan can exceed that

period. Inverters have separate warranties, which are typically 5-10 years,

though some are longer. At the end of a solar lease or PPA term, the

homeowner will often have several options: 1) renew the contract and

continue the monthly payments, 2) purchase the system at a designated price

or the fair market value of the system, which may or may not be negligible

after the term of a contract, or 3) have the third-party lender arrange for

system removal. In the case of a solar loan, the homeowner will continue to

own the system after the contract term concludes and the loan is fully paid o.

Credit Requirement:

As a prerequisite to entering into most third-party financing contracts, third-party

lenders require a credit (or FICO) score. Many third-party financing arrangements

are only available to homeowners who have a credit score of 680 or higher. Some

financing arrangements may be available to homeowners with credit scores lower

than 680, but they may come with higher interest rates. Knowing a credit score

at the outset can be a useful way to determine eligibility for third-party financing.

A credit score below 650 will preclude most homeowners from most third-party

financing options. Some states have developed special loan programs for lower

income or lower FICO score customers. Solar loan programs and other state solar

incentive programs can be found on the DSIRE website at www.dsireusa.org, or

by checking with NYSERDA.

Down Payment:

Many third-party lenders oer options for initial customer down payments.

Generally, initial down payments range from zero dollars to $3,000. By putting

some money down upfront toward the cost of a solar electric system, the

homeowner will likely receive a lower monthly payment, a shorter duration

contract term (in the case of a solar lease or loan), or get a lower per-kilowatt-

hour rate (in the case of a PPA). With a down payment, some third-party

lenders will waive or reduce the escalation clause.

Escalation Clause:

Many third-party financing options contain a clause that increases a

homeowner’s monthly payment on an annual basis to account for inflation and

projected annual increases in electricity rates. This concept is often referred to

as an annual “escalation clause,” “escalator clause,” or simply an “escalator.”

In many solar lease and PPA contracts, payments escalate at an annual rate

between 1-3 percent. Escalation clauses are not problematic per se—keep in

mind that the average annual increase in U.S. residential electricity rates over

the past decades was over 3 percent and the average annual rate of inflation

was 2.4 percent —but they should be understood and closely examined for

reasonableness. The escalator is a compounding rate, meaning that it applies

not just to the initial payment rate but to the increases added after each year

due to the escalation charges. For example, if the payment rate for a PPA is

12 cents per kilowatt hour in the first year, with an annual escalator of 3 percent,

the customer will be paying 18.2 cents per kilowatt hour in year 15. But if the

escalator is only 1 percent, the customer will only be paying 13.8 cents in

year 15. It is good to calculate or ask for a table of what each year’s payment

rate will be.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 8

Homeownership Transfer Provisions:

It is important to look for contract terms that clarify the allocation of obligations

in the case of a transfer of home ownership. Under a third-party ownership

model, the homeowner can usually transfer the solar lease or PPA to the next

home owner for the remainder of the contract term, provided the new owner

is approved (usually a credit score qualifying a person for a mortgage also

meets the criteria to take over the third-party lending agreement obligations).

Solar panels can add significant value to a home, but third-party solar

ownership can also be a complicating factor during the sale of a home. Some

homebuyers may be wary of purchasing a house with a solar electric system.

If a solar electric system is third-party owned, a seller may have to buy the

system outright before transferring the home, so the system can be removed

upon transfer. With a relatively scant history of solar home sales data, it can be

dicult to calculate the value of a residential solar electric system during the

home sales process, especially when a system is third-party owned and the

buyer would like to assume the remaining lease or PPA payments. Examine

the provisions of a contract that relate to ownership transfer to determine

what the options would be if the home is sold before the end of the contract

term, and have a clear understanding of those conditions with the installer.

Minimum Production Guarantees:

Many lease and PPA arrangements oer solar production or output

guarantees, usually in terms of a certain number of kilowatt-hours of electricity

produced per year. With such a guarantee, if an installed system fails to

meet the minimum level of production output guaranteed, the third-party

owner will compensate the homeowner on a per-kilowatt-hour basis for the

electricity production shortfall. Prospective solar lease or PPA homeowners

should check to see if a minimum production guarantee is included in the

terms of their contact and what accommodations are provided in the case

of a production shortfall, including whether compensation is based on a

wholesale or retail per-kilowatt-hour price. When a homeowner directly owns

a solar electric system, production shortfall risks are incurred by the owner. In

this case, no production guarantees are provided unless oered by a panel

manufacturer or installer.

Net Metering:

Net metering, sometimes referred to as “net energy metering,” enables solar

electric system owners to use their solar electricity generation to oset their

electricity consumption. Simply put, the customer’s meter runs backward

for the amount of solar electricity produced by the solar electric system and

added to the grid. In some cases, homeowners can receive a credit on their

electric bills from the utility for the excess electricity they produce and add to

the grid over the course of a certain billing period. It is important to note that

a residential, grid-tied solar electric system will not function in the case of an

electricity outage unless the home has an accompanying electricity storage

system and the ability to “island” (disconnect from the grid). The reason is

that stand-alone solar electric systems are designed to shut down when the

grid goes down, to prevent the system from feeding power back into the

grid and causing injury to utility employees working on the power lines. Visit

nyserda.ny.gov/Cleantech-and-Innovation/Power-Generation/Net-Metering-

Interconnection for more information on net metering.

Shared Solar:

A shared solar project, also known as community distributed generation

(CDG), allows multiple residences and/or businesses to jointly benefit from

one solar electric installation. Shared solar oers an alternative for people

who cannot install solar on their property. A shared solar project is hosted

by a sponsor with a suitable roof or parcel of land, who is responsible for the

installation and operation of the system. Participants, also known as members

or subscribers, purchase the electricity generated in the form of net metering

credits which are assigned to their utility bill, osetting their electricity usage.

If you chose to participate in a shared solar project, you would enter into an

agreement with the system owner and would pay the system owner for the

net metering credits received. Similar to a PPA for rooftop solar, the price you

pay for the net metering credits should be lower than the price you pay per

kwh to your utility. Visit nyserda.ny.gov/All-Programs/Programs/NY-Sun/

Communities/Shared-Solar for more information about shared solar in New

York State.

Operations and Maintenance:

If the homeowner chooses a lease or PPA model, the third-party owner owns

the solar electric system and will likely cover operations and maintenance over

the course of the contract term. It is important to check your contract because

some lease contracts may divvy up responsibilities dierently. Under most

third-party ownership arrangements, the third-party owner also incurs accidental

risks associated with panel ownership, including unforeseen destructive

events or panel malfunction. Under the solar loan model, the homeowner owns

the system directly and therefore incurs the liabilities associated with such

ownership. A homeowner who owns a solar electric system outright or finances

through a loan may be responsible for insuring the solar electric system, which

could be added to homeowner’s insurance or an existing property policy.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 9

Because large, third-party financing entities have established relationships

with insurance companies, they often receive more favorable rates than do

residential customers looking for solar property insurance. In some case,

solar leases or PPAs may require homeowners to increase their homeowner’s

insurance to cover risks associated with the system.

Another way to mitigate risk is to purchase an extended warranty. Solar panels

may come with a manufacturer’s production warranty guaranteeing at least

80 percent system performance for 20-25 years. However, homeowners who

directly purchase or finance their system through a loan may want to seek

additional protection. Although panel manufacturers usually oer extended

performance guarantees, other system components such as disconnects,

inverters, racking, and wires may come with relatively short warranties or no

warranties at all. Homeowners may want to purchase an extended warranty

to cover replacement or repair of these components, system installation

workmanship defects, or the risk that a panel manufacturer will have undergone

bankruptcy by the time a homeowner pursues a manufacturer’s warranty claim.

Pre-Payment:

A pre-payment option can be similar to a buyout option and allows

homeowners to pay some or all of the payments for a solar electric system

before the payments become due. Pre-payment can range from zero to full

pre-payment. Full, upfront pre-payment can allow a homeowner to reap some

of the benefits of third-party ownership, such as maintenance coverage, while

avoiding ongoing interest payments.

Production Estimates:

Residential solar electric systems usually come with electricity production

or output estimates. System underperformance of a production estimate

can be costly for a solar homeowner. Under the lease model, system

underperformance can be particularly problematic because a homeowner

owes the solar developer a fixed payment regardless of the amount of

electricity produced by the leased system. On the other hand, the homeowner

gains if the leased solar electric system overproduces. Under a PPA model,

the homeowner only pays for the amount of electricity actually produced by

the solar electric system. Thus, when actual system output falls below the

production estimate, homeowners leasing their solar electric system may be

economically disadvantaged compared to PPA customers.

Solar Incentives:

The federal government provides a 30 percent federal investment tax credit

(ITC) for the purchase of residential solar electric systems. States, too, often

oer incentives for going solar. In New York State, a 25 percent state personal

tax credit is available in addition to the federal investment tax credit. New York

City has a Real Property Tax Abatement Program through the NYC Department

of Buildings. Visit www.nyc.gov/html/gbee/html/incentives/solar.shtml to find

the instructions and forms. NYSERDA also provides direct financial incentives

for the installation of a solar electric system by an approved contractor Visit

nyserda.ny.gov/All-Programs/Programs/NY-Sun/Customers/Available-

Incentives for information on how to find a contractor and current incentives.

It is important to note that the 30 percent ITC is only available to the owners or

purchasers of a solar electric system. In other words, if the homeowner agreed

to a solar lease or PPA with a third-party system owner, the homeowner will

be unable to take advantage of this tax credit. Instead, the third-party owner

will realize the tax benefits. However, the 25 percent New York State personal

tax credit is available for the homeowner and NYSERDA incentives for leases

or PPAs are required to be reflected in the lease or PPA agreement. Under

a loan arrangement where a solar customer owns the solar electric system,

the solar customer will be able to take direct ownership of most incentives.

Solar installers should be able to provide an estimate of the payback period

for a direct purchase, taking into account all of the available incentives. Make

sure they explain all of the payback calculation assumptions. Interest paid

on solar loans that are secured through a home equity loan may also be tax

deductible. It is important to consider the impact of the available incentives on

the economic benefits based on the homeowner’s tax bracket before deciding

whether third-party ownership (such as a solar lease or PPA) or direct ownership

(either through a loan arrangement or through outright purchasing) makes

more sense.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 10

Weighing the Benefits

of Direct Home Ownership vs.

Third-Party Financing

A direct, upfront, cash purchase of a residential solar electric system is typically the least expensive option in terms of

total dollars spent, because no interest costs or finance fees are incurred. In many cases, however, a homeowner will

not have the cash available to pay for a system outright. And, even when a homeowner does have enough cash to pay

for a solar electric system, it may still be financially advantageous to finance the solar electric system and invest the

cash elsewhere.

It is important to note that with a lease, PPA, or loan, homeowners will have an additional monthly bill to pay beyond

their regular monthly electric utility bill. However, the utility electric bill should be greatly reduced.

A homeowner who is financing solar through a lease or PPA generally will

have fewer concerns about maintenance and operation of the system.

A homeowner who is financing solar through a lease or PPA generally will have fewer concerns about maintenance

and operation of the system. Maintenance, monitoring, insurance, and warranties are usually provided through a solar

lease or PPA arrangement. For example, the replacement of most system parts to maintain a solar electric system’s

production performance will be covered by the third-party developer over the term of the contract under a lease or PPA

arrangement. Some homeowners may feel more comfortable knowing that they do not bear these maintenance and

operation responsibilities. Others may prefer to control and manage a system sited on their property.

Solar electric systems generally require little maintenance. They should be inspected periodically and may need to be

cleaned for optimized performance. If a homeowner lives in an area where snow buildup occurs, the panels may need

to be cleared of snow from time to time. Other maintenance issues which can occur over the lifetime of a system may

include loose wiring connections, loss of inverter function, or breaking or cracking of the panels themselves.

When a homeowner directly owns the solar electric system, either through upfront cash purchase or a solar loan, and

the system is not covered under any other insurance policy or covered under a warranty, the homeowner will bear the

risk of system malfunctions, accidents or any other unforeseen circumstances that result in the loss or curtailment of the

solar electric system’s output. Under a solar lease or PPA arrangement, these risks are borne by the third-party owner

rather than the homeowner.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 11

On the other hand, when a homeowner finances his or her solar purchase through a lease or PPA, the financing contract may limit the homeowner’s ability to alter

the property if doing so would negatively impact solar access or solar electric system performance. For example, construction of a chimney could pose a problem if it

would cast a shadow on the solar electric system. When homeowners directly own their solar electric system, they are not bound by a third-party owner’s restrictions.

As noted above, with a third-party ownership arrangement (lease or PPA), a homeowner will not be able to take advantage of federal incentives such as the

ITC and state incentives such as Solar Renewable Energy Certificates (SRECs), where available. However, the fact that the third-party company will receive

these valuable incentive credits should allow it to oer more favorable financing arrangements to the homeowner than would otherwise be the case. Under the

direct-ownership model, whether a system is financed through a loan or purchased outright, the homeowner will be able to realize these incentives directly.

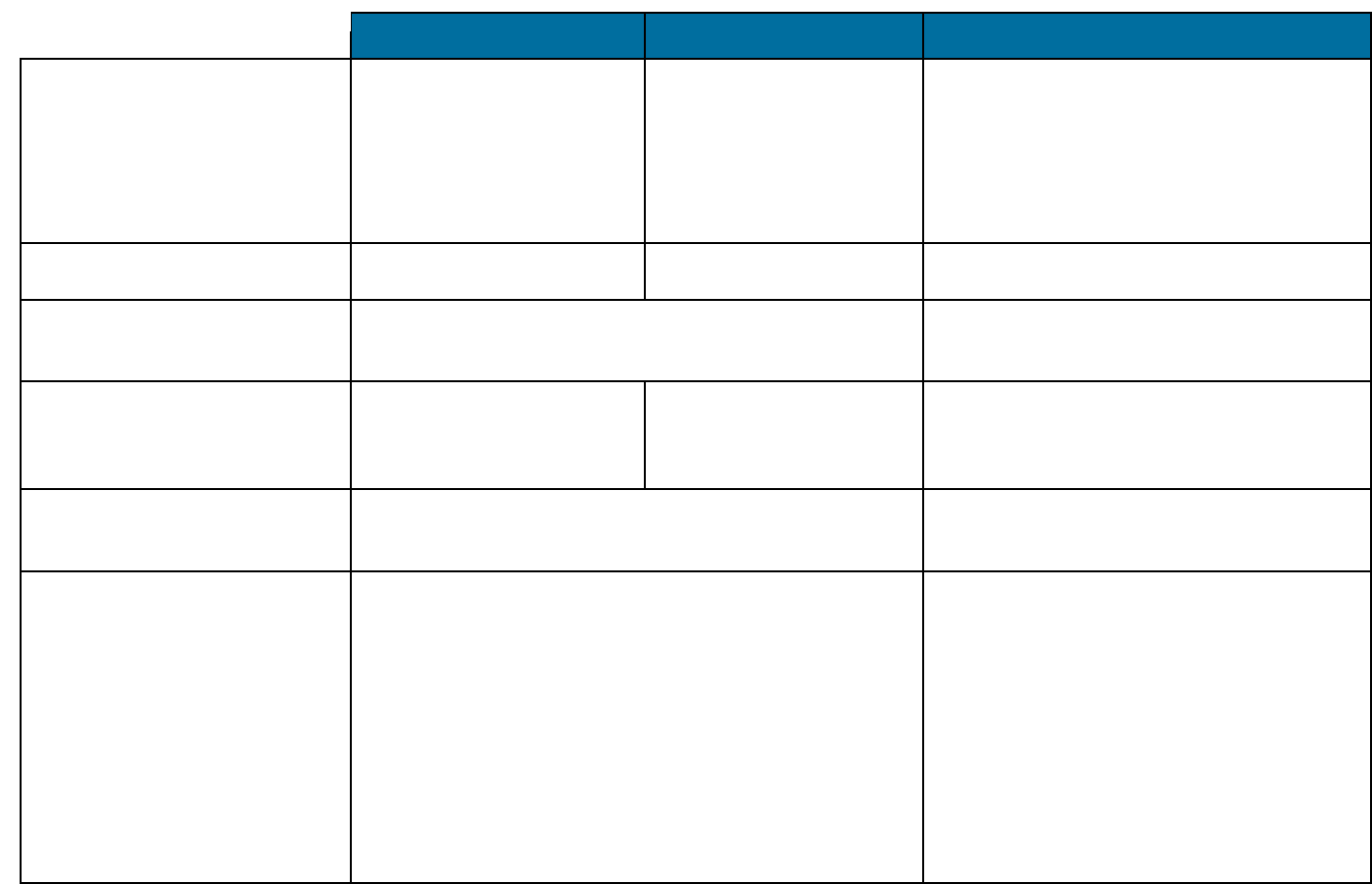

Table 1 summarizes the similarities and dierences between the dierent arrangements.

Table 1.

Comparing Residential Solar PPAs, Solar Leases, and Solar Loans/Direct Purchases

Solar Leases Residential Solar PPAs Solar Loans/Direct Purchase

Who buys the system? Third-party developer Homeowner

Who owns the system? Third-party developer Homeowner

Who takes advantage of the

federal investment tax credit

for solar?

Third-party developer Homeowner

Who takes advantage of the

state personal tax credit?

Homeowner

Who takes advantage of

NYSERDA incentive?

Although the incentive goes

directly to contractor, the

homeowner may benefit

through reduced costs on the

lease agreement.

Although the incentive goes

directly to contractor, the

homeowner may benefit

through reduced costs on the

PPA agreement.

Homeowner

Who is responsible for operations

and maintenance of the solar

electric system?

Usually the third-party

developer

Third-party developer Homeowner, though some state incentive

programs require installers to provide a

workmanship warranty for a set period of time

such as five years, thereby reducing the risk of

immediate issues related to improper installation.

Who incurs the risk of damage

or destruction

Third-party developer Homeowner

What happens if the homeowner

sells the home where the solar

electric system is located?

Depends on the contract If the homeowner finances the system through a

loan, the homeowner remains responsible for loan

payments after the transfer unless negotiated with

the buyer.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 12

Solar Leases Residential Solar PPAs Solar Loans/Direct Purchase

Are financing payments fixed? Yes, payments are pre-set but

may include an annual escalator,

increasing payments each year.

No. Payments to the third-

party developer/owner are

on a per kilowatt-hour basis

based on electricity generated

by the solar array. Per

kilowatt-hour payments may

include an annual escalator.

If the homeowner finances the system through

a loan, the loan payments will be fixed. If the

homeowner decides to purchase a system

outright, a contractor may sometimes oer several

payment installments instead of one lump sum.

What contract duration terms

are available?

Terms can vary. Terms can vary, but often in

the range of ~20 years.

If the homeowner finances the system through a

loan, the loan terms can vary.

Does this type of financing

arrangement require a down

payment?

Not necessarily; down payment requirements vary. If the homeowner finances the system through a

loan, down payment requirements can vary.

Do contracts provide minimum

production guarantees?

Yes, usually. Solar lease

providers commonly provide

minimum production

guarantees.

Yes, usually. PPA providers

commonly provide minimum

production guarantees.

A loan contract does not include production

guarantees. However, a solar panel manufacturer

or developer/installer may provide a production

guarantee.

Are there escalator clauses

in the contracts?

Sometimes. Check the contract for specific terms. If the homeowner finances the system through

a loan, interest rates may increase over time

depending upon the specific terms of the loan.

Is insurance coverage provided? Ye s No. Homeowners who directly own their solar

electric system and want to be covered will need

to find coverage either through a homeowner’s

existing insurance policy or through the purchase

of a new or expanded policy. Homeowners may

decide to forgo insurance coverage altogether

and bear the risks of solar electric system

ownership. Some state incentive programs require

installers to provide a workmanship warranty for

a set period of time such as five years, thereby

reducing the risk of immediate issues related to

improper installation.

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 13

Questions to Ask

As you go through the process of deciding whether to purchase or finance

solar panels, listed below are some questions to ask yourself and the

companies you are interviewing. Going solar is an exciting option and one that

can give you many years of satisfaction.

Questions Related to Making the Decision to Go Solar

• Have you received quotes from at least three solar installation companies?

• Will the solar developer install the system directly or will that be done by a sub-contracted installer?

• How long has the solar developer and/or installer been in business? What is the solar developer/installer’s

reputation and financial standing? Do you know anyone who has used this solar developer/installer before?

Have you received references?

• Does the solar installer have the proper state certifications and licenses, if required?

• Will an on-site visit be performed to assess whether your house is a viable site for a solar electric system?

• Will you be able to monitor the electrical production of your solar electric system once it is installed?

• Will the electricity produced by your system cover all of your electrical needs at home? On average, will your

system produce excess electricity? How much will you be compensated for excess electricity production

if your state has net metering in place?

Questions Related to Financing

• Have you asked the solar developer to calculate the payback and walk you through the contract and any assumptions?

• Given your personal tax situation, does it make more sense to own (through a loan or direct purchase) your solar

electric system to take advantage of all the federal and state tax incentives?

• What is the interest rate and duration (in years) of the financing agreement? Have you shopped around to compare

other financing packages?

• Will you have to make a down payment? Do you have the option to make a down payment to reduce monthly fixed

payments (lease) or kilowatt-hour rate (PPA)?

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 14

• Will your monthly loan payments be equal to or less than the savings on your electric bill? (You will want to factor in

how much of your electricity needs will be met by your solar electric system as that will impact the reduction of your

electric bill. If the system doesn’t cover a significant portion of your electricity needs, then your savings may not be

substantial enough to justify the payments for your solar electric system.)

• Is there an escalation clause included in the financing agreement? If so, what is the annual escalation rate?

• If you are financing through a PPA, is the electricity rate you are being oered lower than what you are currently paying?

• If you are financing through a lease or PPA, is there a pre-payment option under which you can pay some or

all of your lease or PPA payments before they become due?

• If you are financing your system through a lease or PPA, what happens at the end of the contract term? Does the

contract require you to buy the system at the end of your term? If so, how is the buyout amount determined?

• Can you buy out your financing contract? Under what circumstances? At what rate? At what point? How is that rate

calculated?

• What happens if you sell your home before the end of your solar contract term? For instance, what happens if the

buyer does not qualify to assume your solar lease or PPA? What if the buyer does not want the solar electric system

included in the property sale?

• If you are financing your system through a lease or PPA, what happens if you need to replace the roof during the

contract term?

• Could the system be removed or repossessed if the lender goes out of business or gets into financial trouble?

• Can the lender sell the contract to a new entity? Will you be notified if that happens?

Questions Related to the Operations of the Solar Electric System

• Who will perform operations and maintenance on the system? If the third-party owner performs operation and

maintenance, who specifically would you contact if there is a problem? Are you obligated to notify someone within a

certain timeframe if there is a problem? How quickly will that person respond to your request for help? Will there be

any charges for parts and labor? What services does the operations and maintenance contract cover?

• Does the contract contain minimum production guarantees? If so, what accommodations are provided in the case of a

production shortfall? Will shortfall compensation be based on a wholesale or retail per-kilowatt-hour price?

• What are the insurance requirements? Who insures the system? Do you have to pay for any damage? Are there damage

reporting requirements? Is there a minimum insurance coverage requirement for the house in order to install a solar

electric system on it? What will your current home insurance policy cover with respect to your solar electric system?

• Who is responsible for warranting the system? If there is a warranty, is it with you or the solar company? Will you

receive a copy of the warranty agreement?

New York State Homeowner’s Guide to Solar Leases, Loans, and Power Purchase Agreements | 15

Solar Financing Resources for Homeowners

• Financing Options for NY-Sun Incentive Program:

http://www.nyserda.ny.gov/All-Programs/Programs/NY-Sun/Customers/Solar-Financing-Options

• Private Sector Lenders for Solar Projects:

http://www.nyserda.ny.gov/All-Programs/Programs/NY-Sun/Customers/Solar-Financing-Options/Residential-Lenders

• Financing Your Solar Electric System, EnergySage: www.energysage.com/solar/financing

EnergySage, an online marketplace that provides price quotes from multiple PV installers, has a webpage dedicated to solar financing.

This webpage provides information homeowners navigate their solar financing options.

• Homeowners Guide to Financing a Grid-Connected Solar Electric System U.S. Department of Energy (DOE) Guide:

www1.eere.energy.gov/solar/pdfs/48969.pdf

DOE’s Homeowners Guide to Financing a Grid-Connected Solar Electric System provides an overview of the financing options that may be

available to homeowners who are considering installing a solar electric system on their house. It explains the benefits of a solar electric system,

key terms, and various options for homeowners financing a solar electric system.

• Introduction to Solar Project Finance Solar Outreach Partnership Solar Training Video:

www.youtube.com/watch?v=fojwEO3zpH8

Under the U.S. Department of Energy’s SunShot Solar Outreach Partnership, the International City/County Management Association, and

Meister Consultants Group produced a video series for local government ocials covering many aspects of installing solar. One of the videos

covers the basics of solar project financing, which may be useful for homeowners interested in financing a residential solar electric system.

• Solar Leasing for Residential Photovoltaic Systems National Renewable Energy Laboratory (NREL) guide:

http://www.nrel.gov/docs/fy09osti/43572.pdf

NREL’s Solar Leasing for Residential Photovoltaic Systems guide examines the solar lease option for residential solar electric systems.

It also describes two lease programs: the Connecticut Solar Lease Program and SolarCity’s program.

• Solar Checklist, Interstate Renewable Energy Council (IREC):

http://www.irecusa.org/consumer-protection/consumer-checklist/

IREC provides a checklist for residential consumers considering solar energy, including preliminary questions and tips for yourself,

safety considerations to ask your contractor, and what to look for in a contract between you and your contractor.

• Additional solar information and resources, IREC:

http://www.irecusa.org/consumer-protection/consumer-resources/

New York State Energy Research and Development Authority (NYSERDA), a public benefit corporation, oers objective information and analysis, innovative programs,

technical expertise, and support to help New Yorkers increase energy eciency, save money, use renewable energy, and reduce reliance on fossil fuels. NYSERDA

professionals work to protect the environment and create clean energy jobs. NYSERDA has been developing partnerships to advance innovative energy solutions in

New York State since 1975. To learn more about NYSERDA’s programs, visit nyserda.ny.gov or follow us on Twitter, Facebook, YouTube, or Instagram.

SUN-GEN-leaseloanppa-br-1-v2 9/21