Sports Tourism:

State of the Industry Report (2019)

W W W . T O U R I S M E C O N O M I C S . C O M

Supported by:

Prepared for:

2

1 | Introduction

3

2 | Key Findings

4

3 | Sports

-Related Travel Volume & Spending

5

4 | Economic Impacts

10

5 | COVID

-19 Impacts

22

6 | Destination Profiles

25

TABLE OF CONTENTS

3

Sports tourism* is an integral part of local and national economies

across the US. Travelers attending sports tournaments, races, and

other events – either as a participant or spectator – generate

significant economic benefits to households, businesses, and

governments alike and represent a critical driver of the overall

economy.

By monitoring the sports tourism economy, policymakers can

inform decisions regarding the funding and prioritization of the

sector’s development. They can also carefully monitor its

successes and future needs. And by establishing a baseline of

economic impacts, the industry can track its progress over time.

To quantify the economic significance of the sports tourism sector

in the U.S., Tourism Economics prepared a comprehensive model

using multiple primary and secondary data sources to quantify the

economic impacts arising from sports-related travel spending.

Impact modeling is based on an IMPLAN Input-Output (I-O) model

for the U.S. The results of this study show the scope of the sports

tourism sector in terms of direct sports-related travel spending, as

well as total economic impacts, including employment, household

income, and tax impacts in the broader economy.

*For purposes of this report, “sports tourism” includes adult and youth

amateur events and collegiate tournaments. The economic impact

analyses conducted within the report exclude professional sports and

collegiate regular season games.

In addition to estimating the economic benefits generated by

sports tourism in 2019 – a critical benchmark year as 2019

establishes the high watermark – the State of the Industry (“SOTI”)

Report also estimates the losses in 2020 due to COVID-19 and

provides an overview of the key characteristics for the Sports

Events & Tourism Association’s (“Sports ETA”) destination

members (i.e. local sports commission, convention and visitors

bureau, chamber of commerce).

The analysis draws on the following data sources:

• Sports ETA: membership survey data

• Longwoods International: traveler survey data, including

spending and visitor profile characteristics for sports tourism

nationwide

• Bureau of Economic Analysis and Bureau of Labor Statistics:

employment and wage data, by industry

• U.S. Travel Association: domestic travel data

• STR: lodging data

• Sports attendance data

INTRODUCTION

4

Sports Travelers

Nearly 180 million people traveled to a sports event in

the U.S. in 2019 either as a participant or spectator,

which generated 69 million room nights.

Sports-Related Travel Spending

Sports travelers, event organizers, and venues spent

$45.1 billion in 2019, which generated $103.3 billion in

business sales when including indirect and induced

impacts.

Fiscal Contributions

Sports tourism generated $14.6 billion in tax revenues in

2019, with $6.8 billion accruing to state and local

governments.

Employment Generator

A total of 739,386 jobs were sustained by sports tourism

in 2019. This included 410,762 direct and 328,624

indirect and induced jobs.

KEY FINDINGS

The sports tourism sector is a driver

of the U.S. economy

SPORTS-RELATED TRAVEL

VOLUME & SPENDING

6

169

171

174

176

179

2015 2016 2017 2018 2019

Sports traveler counts

2.0%

0.8%

1.8%

1.2%

The number of travelers attending sports events in

the U.S. increased by more than 10 million since

2015.

Sports traveler levels and annual growth

Amounts in millions of travelers and year-over-year percentage growth

In 2019, the number of sports travelers grew 2.0%, capping

5.9% cumulative growth over the five-year period.

Sport traveler counts for adult and youth amateur events

were estimated using visitor data from Longwoods

International and Sports ETA SOTI survey results.

The following methodology was used to estimate the

number of collegiate tournament sports travelers:

1) Professional and collegiate sports travelers: Longwoods

International and Sports ETA SOTI survey results provided

the total number of professional and collegiate sports

travelers

2) Removed professional sports: Attendance data from the

NCAA and the five major professional sports leagues was

used to remove professional sports from the analysis

3) Removed collegiate regular season: NCAA regular season

and tournament attendance data was then used to remove

the collegiate regular season attendance, which resulted in

the total number of collegiate tournament sports travelers

SPORTS-RELATED TRAVEL

VOLUME & SPENDING

5.9%

Source: Sports ETA, Longwoods International, US Travel Association, NBA, NCAA, NFL,

NHL, MLB, MLS, Tourism Economics

7

$38.7

$39.4

$41.4

$42.9

$45.1

2015 2016 2017 2018 2019

Sports-related travel spending

Spending by sports travelers, event organizers, and

venues increased by $2.2 billion to $45.1 billion in

2019.

Sports travelers, event organizers, and venues

spent $6.4 billion more in 2019 than in 2015.

Over the five years through 2019, sports tourism

spending increased 16.7%.

Sports-related travel spending and annual growth

Amounts in billions of nominal dollars and year-over-year percentage growth

5.2%

3.6%

5.2%

1.8%

16.7%

Source: Sports ETA, Longwoods International, US Travel Association, Tourism Economics

SPORTS-RELATED TRAVEL

VOLUME & SPENDING

8

Sports travelers, event organizers, and venues spent

$12.5 billion on transportation, $9.2 billion on lodging,

and $8.6 billion on food and beverages. Entertainment,

retail, and tournament operations rounded out

spending, registering $5.7 billion, $5.1 billion, and $3.9

billion, respectively.

The lodging sector accounted for 20% of all sports-

related travel spending. In 2019, sports-related travel

generated 69 million room nights, which is an important

factor given that hotel taxes are a primary funding

source for many entities (refer to pages 28 and 37 for

additional information).

Sports travelers, event organizers, and venues

spent $45.1 billion across a wide range of sectors

in 2019.

Sports-related travel spending

$45.1B SPORTS-RELATED TRAVEL SPENDING (2019)

LODGING

$9.2B

FOOD &

BEVERAGE

$8.6B

ENTERTAINMENT

$5.7B

RETAIL

$5.1B

TRANSPORTATION

$12.5B

TOURNAMENT

OPERATIONS

$3.9B

Source: Tourism Economics

SPORTS-RELATED TRAVEL

VOLUME & SPENDING

9

2015 2016 2017 2018 2019

Total travelers 169.3 171.4 174.4 175.9 179.3

Day 79.6 80.6 82.5 80.9 83.0

Overnight 89.6 90.7 91.9 95.0 96.4

Total traveler spending $35,217 $35,817 $37,726 $39,100 $41,174

Day $5,472 $5,700 $6,138 $6,137 $6,574

Overnight $29,745 $30,118 $31,587 $32,963 $34,600

Per traveler spending $208 $209 $216 $222 $230

Day $69 $71 $74 $76 $79

Overnight $332 $332 $344 $347 $359

Total sports travelers and sports-related travel spending

Amounts in millions of sports travelers and millions of nominal dollars

Sports traveler counts and sports-related

travel spending

The number of individual sports travelers that stayed

overnight grew by 1.4 million to reach 96.4 million in

2019.

An estimated 54% of all sports travelers spent the

night in the event destination, which generated 69

million room nights in 2019.

Sports travelers that stayed overnight spent $359 per

person trip, an increase of $12 year-over-year, while

day trippers spent $79 per person trip in 2019.

Sports travelers that stayed overnight supported

overall sports tourism growth.

Note: event organizer and venue spending on tournament operations is excluded from above

table. In 2019, this amounted to $3.9 billion.

Source: Tourism Economics

SPORTS-RELATED TRAVEL

VOLUME & SPENDING

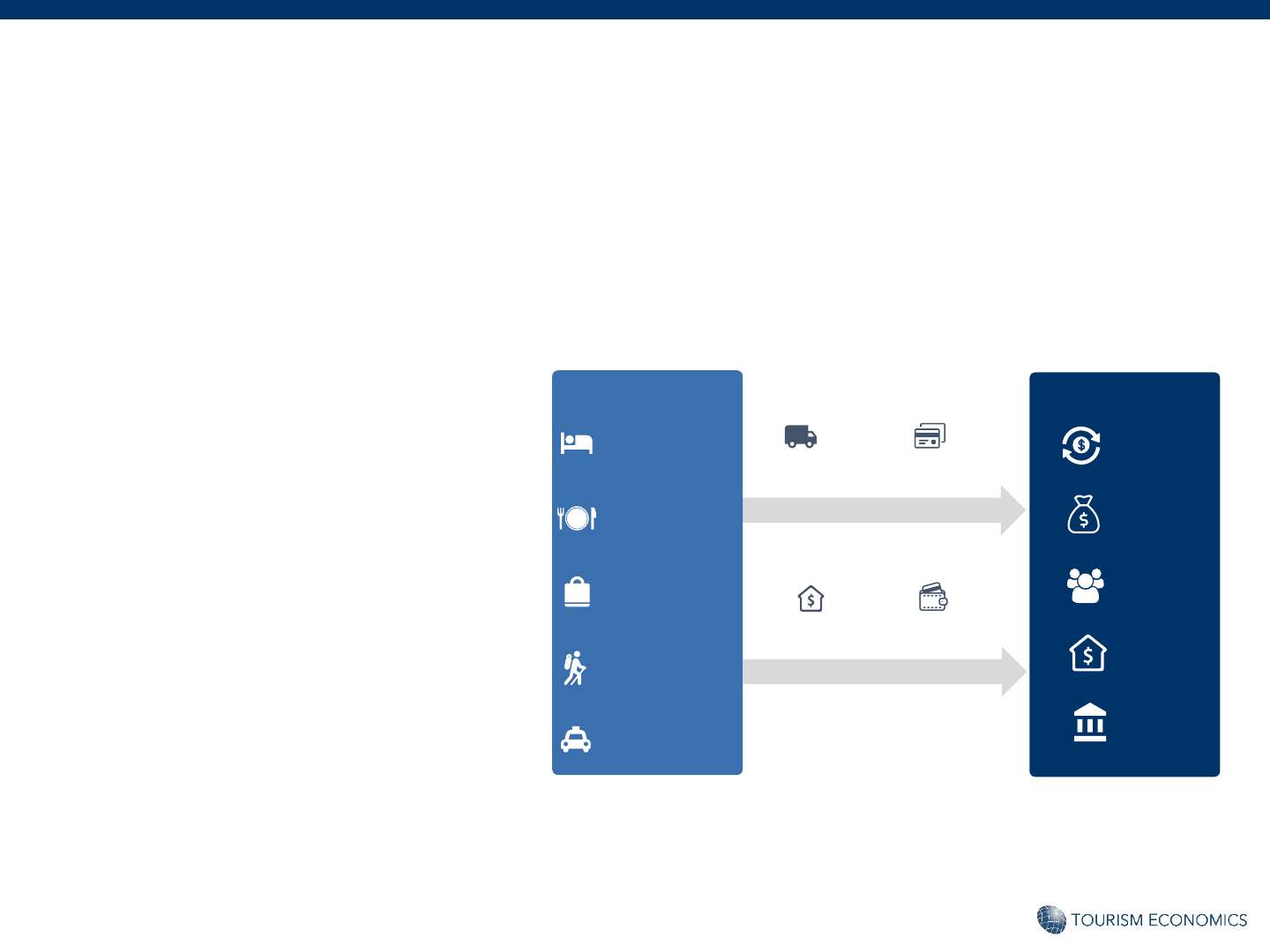

ECONOMIC IMPACTS

11

Our analysis of spending attributable to sports

tourism in the U.S. begins with actual sports-

related travel spending by sports travelers,

event organizers, and venues, but also

considers the downstream effects of this

injection of spending into the local and

national economy. To determine the total

economic impact of sports tourism, we input

the spending into a model of the national U.S.

economy in IMPLAN. This approach calculates

three distinct types of impact: direct, indirect,

and induced.

The impacts on business sales, jobs, wages,

and taxes are calculated for all three levels of

impact.

How sports-related travel spending

generates employment and income

1. Direct Impacts: Sports-related travel

creates direct economic value within a

discreet group of sectors (e.g.

entertainment, transportation). This

supports a relative proportion of jobs,

wages, taxes, and GDP within each sector.

2. Indirect Impacts: Each directly affected

sector also purchases goods and services

as inputs (e.g. food wholesalers, utilities)

into production. These impacts are called

indirect impacts.

3. Induced Impacts: Lastly, the induced

impact is generated when employees

whose wages are generated either

directly or indirectly by sports tourism,

spend those wages in the local economy.

ECONOMIC IMPACTS

12

DIRECT TOURISM

INDUSTRY

Introduction and definitions

Tracking the impact of sports-related travel

spending on the broader economy

IMPLAN calculates these three levels of impact –

direct, indirect, and induced – for a broad set of

indicators. These include the following:

• Spending

• Wages

• Employment

• Federal Taxes

• State Taxes

• Local Taxes

Production

Jobs

Wages

Taxes

Accommodation

Food & beverage

Retail

Entertainment

Local transportation

B2B goods &

services purchases

Income

effect

DIRECT SPENDING

INDIRECT IMPACTS

INDUCED IMPACTS

TOTAL IMPACTS

Supply chain

effects

Household

consumption

Sales

GDP

Jobs

Wages

Taxes

13

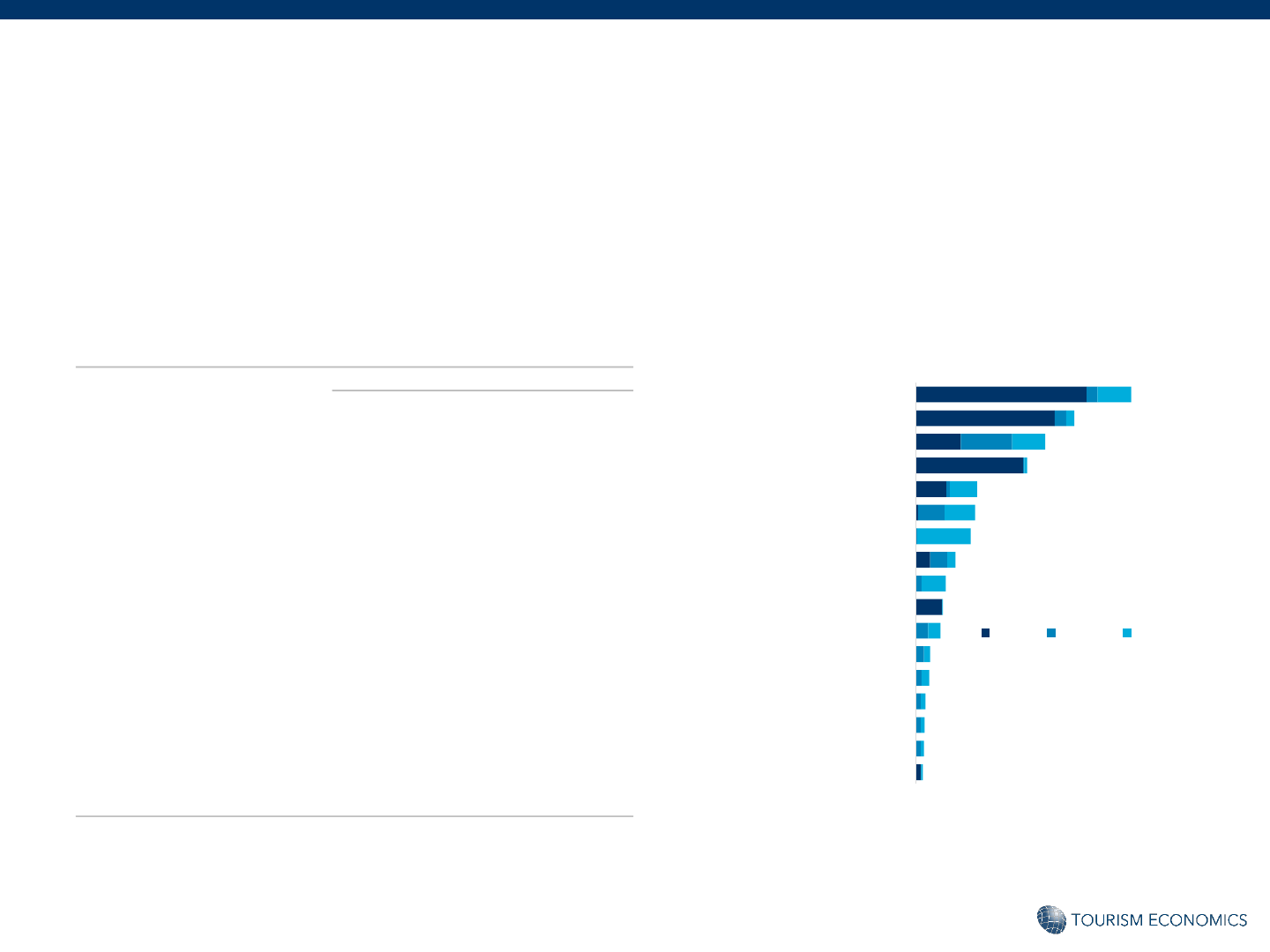

The estimated direct impact of $45.1 billion produced $103.3

billion in business sales including indirect and induced impacts.

While most sales are in industries directly serving travelers (as

presented on the following page), $13.8 billion in business sales

accrued to the finance, insurance, and real estate (“FIRE”)

industry as a result of selling to tourism businesses.

For example, tourism businesses such as hotels, restaurants,

and attractions purchased goods and services (i.e. financial

services, insurance) from businesses in the FIRE industry

(“indirect sales”). Further, the FIRE employees whose wages

were generated indirectly by sports tourism, spent those

wages in the local economy (“induced sales”).

Similarly, significant benefits accrued to sectors such as

manufacturing ($10.3 billion) and business services ($10.0

billion).

Business sales impacts by industry

ECONOMIC IMPACTS

Source: Tourism Economics

Summary economic impacts ($ billions) – 2019

14

$0 $4,000 $8,000 $12,000 $16,000

Finance, Insurance and Real Estate

Food & Beverage

Manufacturing

Business Services

Lodging

Air Transport

Recreation and Entertainment

Retail Trade

Other Transport

Education and Health Care

Communications

Construction and Utilities

Wholesale Trade

Gasoline Stations

Agriculture, Fishing, Mining

Personal Services

Government

Direct Indirect Induced

Direct Indirect Induced Total

Total, all industries $45,114 $25,393 $32,822 $103,329

By industry

Finance, Insurance and Real Estate $412 $5,008 $8,387 $13,807

Food & Beverage $8,764 $433 $1,673 $10,871

Manufacturing $0 $5,230 $5,107 $10,337

Business Services $2,052 $4,943 $2,975 $9,970

Lodging $9,244 $94 $268 $9,606

Air Transport $8,486 $131 $220 $8,838

Recreation and Entertainment $7,423 $603 $522 $8,548

Retail Trade $5,124 $222 $1,881 $7,227

Other Transport $1,298 $2,011 $876 $4,184

Education and Health Care $0 $34 $4,007 $4,041

Communications $0 $1,796 $1,818 $3,614

Construction and Utilities $0 $1,502 $1,146 $2,648

Wholesale Trade $0 $1,050 $1,420 $2,470

Gasoline Stations $2,312 $17 $100 $2,429

Agriculture, Fishing, Mining $0 $1,186 $705 $1,891

Personal Services $0 $438 $1,146 $1,584

Government $0 $692 $572 $1,264

Business sales impacts by industry

ECONOMIC IMPACTS

Business sales impacts by industry ($ millions) – 2019 Business sales impacts by industry ($ millions) – 2019

Source: Tourism Economics Source: Tourism Economics

15

Sports-related travel spending generated $13.9 billion in direct

labor income, which generated a total of $32.2 billion in labor

income including indirect and induced impacts.

Labor income impacts by industry

ECONOMIC IMPACTS

Source: Tourism Economics

Summary labor impacts ($ billions) – 2019

16

$0 $2,000 $4,000 $6,000

Business Services

Food & Beverage

Lodging

Recreation and Entertainment

Finance, Insurance and Real Estate

Education and Health Care

Air Transport

Other Transport

Retail Trade

Manufacturing

Personal Services

Communications

Wholesale Trade

Agriculture, Fishing, Mining

Government

Construction and Utilities

Gasoline Stations

Direct Indirect Induced

Direct Indirect Induced Total

Total, all industries $13,871 $8,020 $10,332 $32,223

By industry

Business Services $1,393 $2,588 $1,574 $5,555

Food & Beverage $3,217 $231 $661 $4,109

Lodging $3,042 $30 $88 $3,160

Recreation and Entertainment $2,668 $267 $183 $3,117

Finance, Insurance and Real Estate $97 $1,084 $1,353 $2,533

Education and Health Care $0 $21 $2,325 $2,346

Air Transport $2,169 $34 $56 $2,259

Other Transport $482 $831 $343 $1,656

Retail Trade $664 $94 $723 $1,481

Manufacturing $0 $680 $714 $1,394

Personal Services $0 $222 $709 $930

Communications $0 $512 $388 $900

Wholesale Trade $0 $365 $494 $858

Agriculture, Fishing, Mining $0 $422 $224 $647

Government $0 $331 $208 $539

Construction and Utilities $0 $300 $237 $537

Gasoline Stations $140 $9 $52 $201

Labor income impacts by industry

ECONOMIC IMPACTS

Labor income impacts by industry ($ millions) – 2019 Labor income impacts by industry ($ millions) – 2019

Source: Tourism Economics Source: Tourism Economics

17

Sports-related travel spending sustained 739,386 full-time

equivalent jobs* on an annualized basis when indirect and

induced impacts are considered.

Job impacts by industry

ECONOMIC IMPACTS

Source: Tourism Economics

Summary job impacts – 2019

*The full-time equivalent concept converts part-time and temporary jobs to a full-

time equivalent annual basis, based on output and wages.

18

0 50,000 100,000 150,000 200,000

Food & Beverage

Recreation and Entertainment

Business Services

Lodging

Retail Trade

Finance, Insurance and Real Estate

Education and Health Care

Other Transport

Personal Services

Air Transport

Manufacturing

Agriculture, Fishing, Mining

Wholesale Trade

Communications

Construction and Utilities

Government

Gasoline Stations

Direct Indirect Induced

Direct Indirect Induced Total

Total, all industries 410,762 129,649 198,975 739,386

By industry

Food & Beverage 130,169 8,315 25,581 164,066

Recreation and Entertainment 105,861 8,699 6,016 120,575

Business Services 34,130 39,228 25,151 98,510

Lodging 81,674 805 2,377 84,856

Retail Trade 23,168 2,701 20,741 46,609

Finance, Insurance and Real Estate 1,541 20,369 23,246 45,156

Education and Health Care 801 40,918 41,719

Other Transport 10,729 13,200 6,176 30,105

Personal Services 4,277 18,372 22,648

Air Transport 19,822 307 515 20,644

Manufacturing 9,215 9,484 18,699

Agriculture, Fishing, Mining 6,071 4,638 10,709

Wholesale Trade 4,262 5,765 10,027

Communications 3,819 3,367 7,185

Construction and Utilities 3,649 2,919 6,567

Government 3,698 2,341 6,039

Gasoline Stations 3,668 234 1,368 5,271

Job impacts by industry

ECONOMIC IMPACTS

Job impacts by industry – 2019 Job impacts by industry – 2019

Source: Tourism Economics Source: Tourism Economics

19

Direct

Indirect /

Induced

Total

Total Tax Revenues $7,371 $7,196 $14,568

Federal $3,361 $4,429 $7,790

Personal Income $1,124 $1,494 $2,618

Corporate $366 $737 $1,103

Indirect Business $352 $263 $615

Social Insurance $1,519 $1,935 $3,454

State and Local $4,010 $2,767 $6,778

Sales $1,383 $1,033 $2,416

Bed Tax $703 $0 $703

Personal Income $280 $372 $651

Corporate $57 $115 $172

Social Insurance $25 $32 $57

Excise and Fees $320 $289 $610

Property $1,242 $927 $2,169

Sports-related travel spending generated $14.6 billion

in total tax revenues. State and local tax revenues alone

accounted for $6.8 billion.

Fiscal (tax) total impact

ECONOMIC IMPACTS

Source: Tourism Economics

Tax impacts ($ millions) – 2019

20

The $14.6 billion in federal,

state, and local taxes generated

by sports tourism would cover

the average salaries of nearly

228,000 public school teachers.

ECONOMIC IMPACTS IN CONTEXT

Spending, jobs, and income impacts in context

$45.1

BILLION

The $45.1 billion in sports-

related travel spending

means that nearly $124

million was spent EVERY

DAY by sports travelers,

event organizers, and

venues.

The $32.2 billion in total

income generated by sports

tourism is the equivalent of

$269 for every household in

the U.S.

If the number of total jobs

sustained by sports tourism

was the population of a U.S.

city, it would rank as the

19

th

largest city in the U.S.,

behind Seattle, Washington.

$32.2

BILLION

739,386

JOBS

$14.6

BILLION

SPORTS –RELATED TRAVEL SPENDING PERSONAL INCOME TAXESEMPLOYMENT

21

Employment

Motor vehicles, bodies and trailers, and parts manufacturing (3361/2/3) 999

Offices of certified public accountants (541211) 490

Furniture and home furnishings stores (442) 473

Barber shops and beauty salons (812111/2) 453

Motion picture and sound recording industries (512) 444

Sports tourism 411

Wood product manufacturing (321) 409

Highway, street, and bridge construction (2379) 351

Pharmaceuticals and medicines (3254) 306

Credit unions and other depository credit intermediation (52213/9) 290

Oil and gas extraction (211) 150

The sports tourism sector supports more direct jobs

than many large sectors including wood product

manufacturing, pharmaceuticals, and oil and gas

extraction.

Industry comparisons

ECONOMIC IMPACTS

Note: Numbers indicate three- to five-digit North American Industry Classification System (NAICS) code

corresponding to such industry sector.

Source: Bureau of Labor Statistics

Direct employment (thousands) – 2019

COVID-19 IMPACTS

23

Sports tourism represents a substantial value to the U.S. economy.

However, this economic value has been severely limited by the

coronavirus pandemic that has especially damaged the sports

events and tourism industry.

Estimates of COVID-19 Impact on U.S. Economy

COVID-19 quickly impacted the U.S. economy during the first

quarter of 2020 and will continue to have profound impacts

throughout the remainder of the year. The U.S. entered the early

stages of a deep recession with steep employment and income

losses.

Nearly all industries are impacted by COVID-19, but to varying

degrees. Given that sports are considered non-essential services

and typically involve many participants and spectators which

increases the risk of transmission, it is expected that the sports

tourism industry will be significantly impacted for much of 2020.

COVID-19 IMPACTS

24

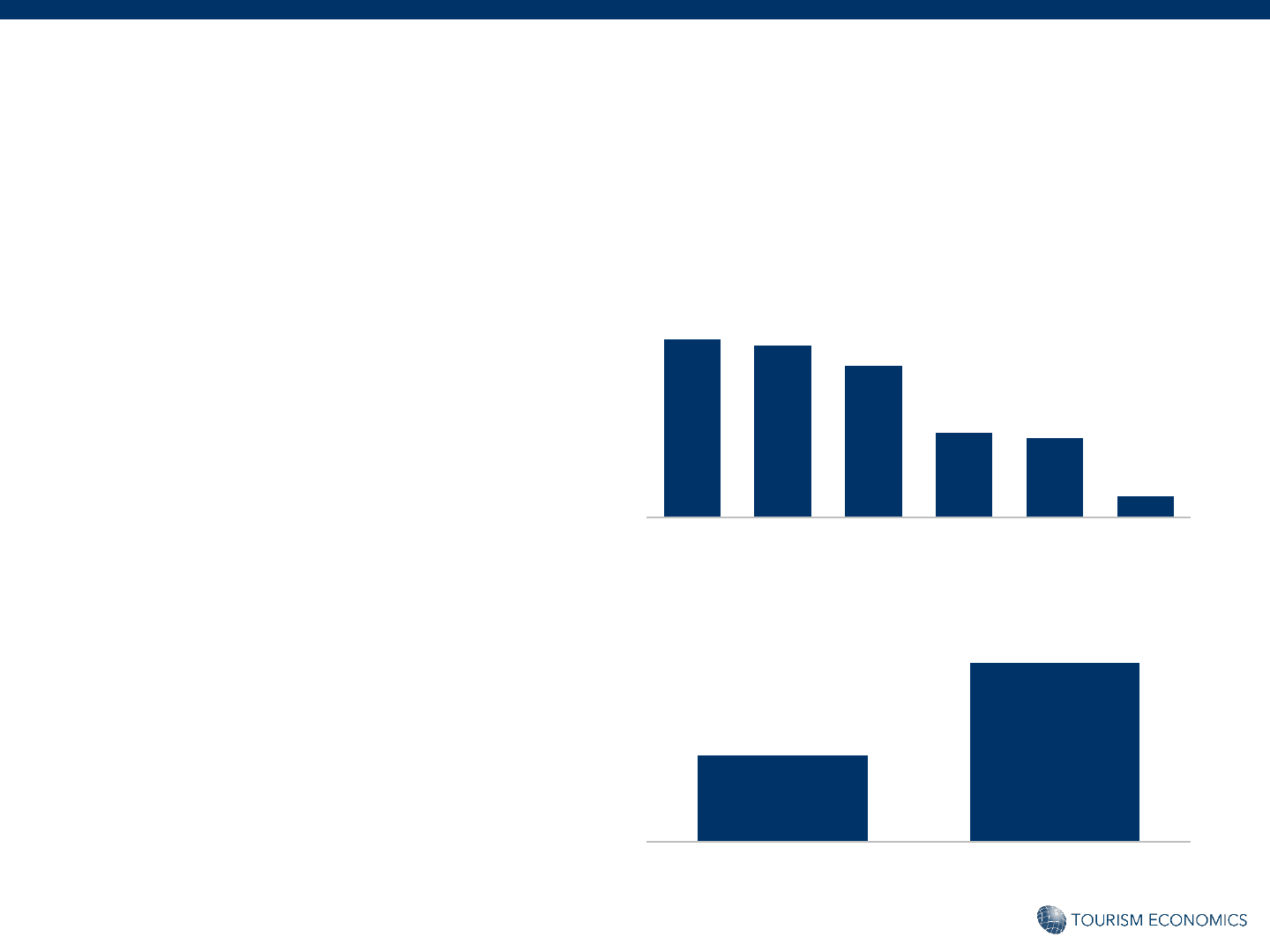

Estimates of COVID-19 Impact on Sports Tourism

Given the event cancellations / postponements, travel restrictions,

and ensuing job losses and budget cuts resulting from COVID-19,

the sports tourism industry has been hard hit.

In March 2020, approximately 9.9 million fewer people traveled to

participate in or watch a sports event compared to March 2019,

which translates into a loss of approximately $2.5 billion in direct

spending.

April fared worse as all sports events were cancelled or postponed

resulting in a loss of 14.9 million travelers and $3.8 billion in direct

spending. Similar losses occurred in May, but then losses are

expected to shrink as the year progresses.

Over the ten-month period from March to December 2020, we

expect that over 75 million fewer people will travel to sports

events compared to 2019, resulting in a loss of $20.0 billion in

direct spending in 2020.

As the economy begins to recover, it will likely take longer for the

sports tourism industry to reach 2019 levels than it will for the

overall U.S. economy.

COVID-19 IMPACTS

Monthly sports tourism spending loss ($ billions)

Monthly sports traveler volume loss (millions)

Source: Tourism Economics

DESTINATION PROFILES

26

In February 2020, Sports ETA electronically distributed the

State of the Industry survey to its membership. The survey

remained in the field for approximately five weeks and

garnered responses from 149 destinations.

The objective of the survey was to develop an understanding

of the key characteristics for Sports ETA destination

members, including convention & visitors bureaus (CVBs),

destination marketing organizations (DMOs), sports

commissions, and chambers of commerce.

Data throughout the remainder of the report present the

results of the destination survey.

OVERVIEW

Participation by Destination Type (2019)

54%

26%

15%

1%

5%

CVB / DMO

Sports Commission as a Department within a CVB / DMO

Stand-Alone Sports Commission

Chamber of Commerce

Other

149

Destination

Participants

27

Approximately 55% of all destination organizations operated

with a budget of $500,000 or less. Approximately 7% of

destinations operated with a budget exceeding $5 million.

More than 40% of destinations experienced a budget increase

in 2019 with an average increase of 13% year-over-year.

Only 6% of destinations experienced a decline in their budget

in 2019 with an average decrease of 9%. However, moving

forward destination budgets will be re-evaluated due to the

impacts of COVID-19.

BUDGET

Destination Budget (2019)

23%

32%

14%

14%

11%

3%

4%

$100,000 or less

$100,001 – $500,000

$500,001 – $1,000,000

$1,000,001 – $2,000,000

$2,000,001 – $5,000,000

$5,000,001 – $10,000,000

$10,000,001+

41%

6%

53%

Increased Decreased Remained the Same

Destination Budget Change (2018 to 2019)

28

Hotel taxes fund the majority of destination organizations.

Destinations with a budget of $1 million or less had a larger

percentage of their budget (76%) funded by hotel taxes,

compared to those destinations with a budget over $1 million

(64%).

Destinations with a budget over $1 million had a larger

percentage of their budget funded by the general fund (8%),

grants (5%), and other sources (14%). Other funding sources

included event revenue, sponsorships, partnership co-ops,

and private funding.

ORGANIZATION

FUNDING

Organization Funding (2019)

76%

6%

5%

6%

1%

7%

64%

8%

4%

6%

5%

14%

Hotel Tax General

Fund

BID / TID Membership Grants Other

$1M budget or less Greater than $1M budget

29

1.6

3.0

3.7

7.8

10.3

21.8

5.0

7.5

4.0

7.2

$100K or

less

$100K –

$500K

$500K –

$1M

$1M – $2M $2M – $5M $5M+

Full-Time Staff Part-Time Staff Seasonal Staff

Annual Interns Seasonal Interns

The number of staff employed by a destination directly relates

to the overall budget. The number of full-time staff at

destinations ranged from 1.6 at destinations with a budget

less than $100,000 to 21.8 at destinations with a budget over

$5 million.

When part-time staff and interns are considered, the total

number of employees ranged from 4.8 to 45.4 depending on

budget.

The average destination, regardless of budget, employed 5.3

full-time staff and 13.6 total staff when including part-time

staff and interns.

STAFFING

4.8

8.4

7.0

19.8

21.1

45.4

Destination organization staffing (2019)

30

Nearly all destinations hosted youth events (97%) – either

competitive or recreational – in 2019. Less than half of the

destinations hosted senior or United States Olympic &

Paralympic Committee (USOPC) events.

On average, 38% of all destinations surveyed owned an event

in 2019 – 58% of destinations with budgets over $1 million

and 28% of destinations with budgets less than $1 million.

Destinations with budgets over $1 million owned an average

of 4.1 events compared to 2.8 events for destinations with

budgets less than $1 million.

Of those destinations that owned an event, approximately

65% owned a team event and 57% owned an individual event.

EVENTS

Event Types (2019)

Owned Events (2019)

97%

94%

82%

46%

43%

11%

Youth Adult /

Amateur

Collegiate Senior USOPC Other

28%

58%

$1M budget or less Greater than $1M budget

31

55%

8%

37%

64%

12%

30%

Increased Decreased Remained the Same

Events Participants

Destinations hosted an average of 70 events in 2019 ranging

from 49 at destinations with a budget less than $100,000 to

88 at destinations with a budget of $1 million to $2 million.

The average number of participants per event correlated to

the destination budget – ranging from 404 participants per

event at destinations with the smallest budget to 1,259

participants per event at destinations with the largest budget.

More than half of the destinations experienced a growth in

the number of events (55%) and participants (64%) year-over-

year.

Only 8% of destinations hosted fewer events and 12% of

destinations hosted fewer participants in 2019 compared to

2018.

EVENTS

Events & Participants (2019)

0

200

400

600

800

1,000

1,200

1,400

0

20

40

60

80

100

$100K or

less

$100K –

$500K

$500K –

$1M

$1M –

$2M

$2M+

Participants per event

Events

Avg. Events Avg. Participants Per Event

Events & Participants Change (2018 to 2019)

32

$69,357

$150,588

$148,708

$259,922

$100K or less $100K – $500K $500K – $1M $1M+

50%

72%

82%

84%

$100K or less $100K – $500K $500K – $1M $1M+

Approximately 73% of destinations paid bid fees in 2019. Half

of the destinations with a budget less than $100,000 paid bid

fees compared to 84% of destinations with a budget over $1

million.

The average bid fee funding pool, regardless of budget, was

approximately $176,000, ranging from over $69,000 at

smaller budget destinations to nearly $260,000 at larger

budget destinations.

The bid fee pool increased for 30% of destinations in 2019 and

remained the same for 70% of destinations. No destinations

decreased its bid fee pool between 2018 and 2019.

The internal budget was the most common source of funding

for the bid pool – 87% of destinations funded a portion of the

bid pool using internal funds, 36% used city or state funds, and

21% used other funding, such as sponsorships or private

donations.

BID FEES

Paid Bid Fees (2019)

Bid Fee Funding Pool (2019)

33

$42,350

$112,153

$218,333

$247,731

$100K or less $100K – $500K $500K – $1M $1M+

Over 60% of destinations, regardless of budget, offered local

event grants in 2019. Nearly 80% of destinations with a

budget less than $100,000 offered grants, compared to less

than 60% for destinations with budgets greater than

$100,000.

The average bid fee funding pool, regardless of budget, was

approximately $145,000, ranging from approximately

$42,000 at smaller budget destinations to nearly $250,000 at

larger budget destinations.

The internal budget was the most common source of funding

for the local grants – 76% of destinations funded a portion of

the local grants pool using internal funds, 33% used city or

state funds, and 12% used other funding, such as sponsorships

or private donations.

LOCAL GRANTS

Offered Local Grants (2019)

Local Grants Funding Pool (2019)

78%

54%

45%

59%

$100K or less $100K – $500K $500K – $1M $1M+

34

Participating at event owner marketplaces, such as

conferences and trade shows, was the most important part of

a destinations marketing strategy – it ranked 4.3 on a 5-point

scale with a range of 4.2 to 4.7 depending on destination

budget.

An organization’s website, exhibiting at conferences and trade

shows, and social media were other important marketing

methods.

MARKETING

STRATEGY

Importance to Marketing Strategy: Average and Range (2019)

0

1

2

3

4

5

Rank

Note: The survey question asked “how important is each element in your marketing strategy”? The red

diamond represents the average rank of importance for all destinations, regardless of budget. The blue

circles present the low and high ranks based on the following destination budget segmentations: $100K or

less, $100K - $500K, $500K - $1M, $1M-$2M, and $2M+.

35

6%

29%

27%

56%

$100K or less $100K – $500K $500K – $1M $1M+

Approximately 33% of all destinations received sponsorships

in 2019, ranging from 6% of destinations with a budget less

than $100,000 to 56% of destinations with a budget over $1

million.

Sponsorship revenue increased at 45% of destinations

between 2018 and 2019, with an average increase of 17%.

Only 10% of destinations decreased sponsorship revenue

year-over-year while the remaining 45% of destinations

maintained the same level of sponsorship revenue.

Nearly 90% of destinations indicated that community

awareness was the key factor for sponsoring their

organization.

SPONSORSHIP

Sponsored Destinations (2019)

87%

61%

58%

35%

13%

Community

Awareness

Youth Philanthropic Product Sales Other

Key Factors for Sponsorship (2019)

36

3%

13%

13%

16%

45%

52%

65%

84%

13%

20%

25%

13%

48%

55%

64%

81%

Destination Demographics

Destination Location

Destination Offerings

Destination Cost

Venue Cost

Bid Fees / Incentives Too High

Lack of Available Dates

Venue Building Program Constraints

$1,000,000 or less $1,000,000+

Venue building program constraints, such as not enough

playing surfaces, were the most prominent reason for lost

business in 2019, followed by lack of available dates, high bid

fees / incentives, and venue cost.

Destination specific factors – such as offerings, location, and

demographics, but excluding cost – accounted for a larger

portion of lost business at destinations with budgets less than

$1 million.

LOST BUSINESS

Lost Business (2019)

37

54%

29% 29%

15%

10%

Room Nights Economic

Impact

Events Lodging Tax

Revenue

Lodging

Occupancy

FACTORS FOR

SUCCESS

Top 5 Factors for Success – $1M+ Budget (2019)

Destinations utilize many key performance indicators to

monitor success. The top two factors in 2019, regardless of

budget, were room nights and economic impact, used by 49%

and 32% of destinations, respectively.

For destinations with budgets over $1 million, 38% indicated

they used economic impact and room nights as measurements

of success. Other key success factors included earned media,

number of events, and repeat business.

Over half (54%) of destinations with budgets less than $1

million stated that room nights were the biggest factor for

success. Other key factors included economic impact, number

of events, lodging tax revenue, and lodging occupancy.

Top 5 Factors for Success – Less than $1M Budget (2019)

38% 38%

17%

13%

13%

Economic

Impact

Room Nights Earned Media Events Repeat

Business

38

25%

69%

64%

63%

79%

$100K or less $100K –

$500K

$500K – $1M $1M – $2M $2M+

The following are other insights derived from the State of the

Industry survey:

• The Event Impact Calculator offered by Sports ETA in

partnership with Destinations International and Tourism

Economics was the most utilized tool for estimating visitor

spend in 2019 – used by 57% of destinations.

• Approximately 60% of destinations, regardless of budget,

required “stay to play” in 2019.

• Only 27% of destinations calculated or collected

information on earned media estimates in 2019.

• Nearly half of destinations (44%) participated in

community-based health and wellness activities in 2019.

OTHER INSIGHTS

Visitor Spending Estimate Source (2019)

57%

34%

12%

16%

Event Impact

Calculator

Internal Calculator Independent Study Other

Required “Stay to Play” (2019)

Note: “Stay to Play” means that destinations require teams to stay within the established

room block in order to participate in the tournament

39

About Sports ETA

As the only trade association for the sport tourism industry, Sports ETA is the most trusted resource for sports commissions, destination

marketing organizations (DMOs), and sports event owners. Sports ETA is committed to the success of more than 850 member organizations

and 2,400 sports event professionals. Our promise is to deliver quality education, ample networking opportunities and exceptional event

management and marketing know-how to our members - sports destinations, sports event owners, and suppliers to the industry - and to

protect the integrity of the sports events and industry. For more information, visit sportseta.org.

About Northstar Travel Group

Northstar Travel Group is the leading B-to-B information and marketing solutions company serving all segments of the travel industry

including leisure/retail, corporate/business travel, corporate and sports meetings, incentives, hospitality, and travel technology. Northstar is

the owner of well-known brands including SportsTravel, Successful Meetings, Meetings & Conventions, Incentive, M&C China, Business Travel

News, Travel Procurement, The Beat, Travel Weekly US, TravelAge West, Travel Weekly China, Travel42, Axus Travel App, and Web in Travel.

The company produces more than 80 face-to-face and digital events in 13 countries in retail travel, hospitality, corporate travel, travel

technology, sports travel, and the meetings & incentive industry. Leadership events include The Business Travel Show, the largest corporate

travel event in Europe; The Meetings Show, the largest meetings industry event in the UK; Web in Travel; CruiseWorld; Global Travel

Marketplace; the EsportsTravel Summit; and the TEAMS Conference & Expo, the world’s largest gathering of sports-event organizers. In

addition, Northstar owns Phocuswright, the leading research, business intelligence, and event producer serving the travel technology industry.

Northstar Travel Group owns the Burba Hotel Network, the leading producer of hotel investment events globally, including ALIS, the largest

hotel investment conference in the world produced with the American Hotel & Lodging Association in Los Angeles each year. Northstar is also

the majority shareholder in Inntopia, the leading SaaS e-commerce software, CRM database marketing and predictive analytics business

serving the mountain destination, golf, activities, hospitality, and specialty destination travel markets.

Based in Secaucus, NJ, the company has offices in New York, NY; Stowe, VT; Denver, CO; Edwards, CO; Burlington, VT; Los Angeles, CA; Costa

Mesa, CA; Lombard, IL; and global offices in London, Singapore, Beijing, and Shanghai. Northstar Travel Group is owned by funds managed by

EagleTree Capital.

ABOUT SPORTS ETA & NORTHSTAR TRAVEL GROUP

40

Tourism Economics is an Oxford Economics company with a singular objective: combine an understanding of the travel sector

with proven economic tools to answer the most important questions facing our clients. More than 500 companies, associations,

and destination work with Tourism Economics every year as a research partner. We bring decades of experience to every

engagement to help our clients make better marketing, investment, and policy decisions. Our team of highly-specialized

economists deliver:

• Global travel data-sets with the broadest set of country, city, and state coverage available

• Travel forecasts that are directly linked to the economic and demographic outlook for origins and destinations

• Economic impact analysis that highlights the value of visitors, events, developments, and industry segments

• Policy analysis that informs critical funding, taxation, and travel facilitation decisions

• Market assessments that define market allocation and investment decisions

Tourism Economics operates out of regional headquarters in Philadelphia and Oxford, with offices in Belfast, Buenos Aires,

Dubai, Frankfurt, and Ontario.

Oxford Economics is one of the world’s foremost independent global advisory firms, providing reports, forecasts and analytical

tools on 200 countries, 100 industrial sectors and over 3,000 cities. Our best-of-class global economic and industry models and

analytical tools give us an unparalleled ability to forecast external market trends and assess their economic, social and business

impact. Headquartered in Oxford, England, with regional centers in London, New York, and Singapore, Oxford Economics has

offices across the globe in Belfast, Chicago, Dubai, Miami, Milan, Paris, Philadelphia, San Francisco, and Washington DC, we

employ over 250 full-time staff, including 150 professional economists, industry experts and business editors—one of the

largest teams of macroeconomists and thought leadership specialists.

ABOUT TOURISM ECONOMICS

For more information: