NBER WORKING PAPER SERIES

DESIGNING QUALITY CERTIFICATES:

INSIGHTS FROM EBAY

Xiang Hui

Ginger Zhe Jin

Meng Liu

Working Paper 29674

http://www.nber.org/papers/w29674

NATIONAL BUREAU OF ECONOMIC RESEARCH

1050 Massachusetts Avenue

Cambridge, MA 02138

January 2022

We are grateful to eBay for providing access to the data. None of us has a significant financial

relationship with eBay. The content and analyses in this paper reflect the authors' own work and

do not relate to any institution or organization with whom the authors are affiliated. All rights

reserved. All errors are our own. The views expressed herein are those of the authors and do not

necessarily reflect the views of the National Bureau of Economic Research.

NBER working papers are circulated for discussion and comment purposes. They have not been

peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies

official NBER publications.

© 2022 by Xiang Hui, Ginger Zhe Jin, and Meng Liu. All rights reserved. Short sections of text,

not to exceed two paragraphs, may be quoted without explicit permission provided that full

credit, including © notice, is given to the source.

Designing Quality Certificates: Insights from eBay

Xiang Hui, Ginger Zhe Jin, and Meng Liu

NBER Working Paper No. 29674

January 2022

JEL No. D47,D82,L86

ABSTRACT

Quality certification is a common tool to reduce asymmetric information and enhance trust in

marketplaces. Should the certificate focus on seller inputs such as fast shipping, or include output

measures such as consumer ratings? In theory, incorporating output measures makes the

certificate more relevant for consumer experience, but doing so may discourage seller effort

because outputs can be driven by random factors out of seller control. To understand this tradeoff,

we study a major redesign of eBay's Top Rated Seller (eTRS) program in 2016, which removed

most consumer reports from the eTRS criteria and added direct measures of seller inputs. This

change generates immediate selection on certified sellers, and homogenizes the share of certified

sellers across product categories of different criticalness in consumer ratings. Post the regime

change, sellers improve in the input measures highlighted in the new certificate. These effects are

more conspicuous in categories that had less critical consumer ratings, in part because the new

algorithm automatically removes the potential negative bias for sellers in critical markets and a

clearer threshold motivates sellers to just reach the threshold. The new regime also makes sales

more concentrated towards large sellers, especially in the categories that face more critical

consumers.

Xiang Hui

Washington University in St Louis

Ginger Zhe Jin

University of Maryland

Department of Economics

College Park, MD 20742-7211

and NBER

Meng Liu

Washington University in St Louis

1 Introduction

Since Akerlof (1970), economists view reputation and quality certification as two mechanisms to

address asymmetric information on quality. Many online platforms generate and aggregate buyer

feedback on sellers. Accordingly, a large literature examines how buyers respond to online seller

reputation, what determines the content of online reputation, and how changes in an online repu-

tation system affect buyers and sellers (Tadelis, 2016). In comparison, much less attention is paid

to quality certification, although it is widely used by many online platforms in parallel with online

reputation. In this paper, we study a major redesign of the quality certificate on a leading online

marketplace.

As a pioneer in e-commerce, eBay has become a textbook example of online reputation. In a

nutshell, consumer feedback of past transactions helps to distinguish between reputable and non-

reputable sellers, which in turn motivates sellers to earn and maintain a good consumer rating on

eBay. However, consumer feedback is imperfect, as consumers may not observe all aspects of sellers’

true quality, some reviews may be inauthentic or exaggerated, and many factors out of seller control

could affect consumer experience (e.g., logistic delays due to shipping carriers). Out of retaliation

and other concerns, the distribution of consumer feedback is highly skewed on eBay (on average,

99% of feedback ratings are positive), which could make eBay’s rating system less informative than

an ideal reputation system if consumers interpret the ratings literally.

As well as recording feedback, eBay has accumulated years of other data on seller performance,

including Detailed Seller Ratings (provided by consumers but less visible to most buyers than

percentage positive ratings), consumer claims, consumer returns, seller cancellations, and package

tracking. Some of them, similar to the public-facing consumer feedback, reflect consumer-generated

output, which may be subject to noise out of seller control. However, other metrics such as seller

cancellations and package tracking are more directly related to seller inputs, and could help eBay

identify slacking sellers and address the moral hazard problem.

In 2009 eBay adopted a certification program (eBay Top Rated Sellers, or eTRS), awarding

the eTRS badge to sellers that meet certain criteria. The initial design of eTRS aimed to cap-

ture comprehensive information about a seller’s quality performance (including consumer feedback,

Detailed Seller Ratings, consumer claims, consumer returns, seller cancellations, late shipping),

though consumers can observe both the eTRS badge and consumer feedback on eBay.

Interestingly, in February 2016, eBay narrowed the eTRS criteria to a subset of input measures,

1

and decoupled eTRS from consumer feedback and other output measures that consumers report

to eBay. At the first glance, the decoupling reduces the information contained in the eTRS badge,

which seems to not only defy the common wisdom of the more information the better, but also

deviate further from consumer-reported experience. However, consumer feedback is always visible

to consumers, and thus it is a priori unclear how the decoupling would affect buyers, sellers, and

the whole platform.

Based on the classical principal-agent theory, we develop a model to characterize how sellers

would respond to a new eTRS system that removes consumer-generated noise. The model yields a

few insights: (1) a certificate that no longer conditions on output measures is immediately friendlier

to sellers that operate in a product category with more critical consumers; (2) an emphasis on

input rather than output measures should encourage seller efforts on the focal inputs, and a clearer

threshold may motivate sellers to just reach the threshold; and (3) the algorithmic change and

the resulting effort change may make the proportion of certified sellers more homogeneous across

markets with different output noise.

To test these predictions, we use eBay’s proprietary data from October 2014 to August 2016.

Since the old eTRS system requires badged sellers to satisfy some standards on the output measures

(e.g., consumer feedback, detailed seller ratings, consumer claims), we define consumer criticalness

of a product category as the share of transactions that are considered “bad” based on the old eTRS

system out of all transactions that are considered “good” based on the new eTRS system. By

definition, it captures the noise in the old eTRS system that arises due to criticalness in ratings,

rather than seller misperformance based on the input-based measures according to the new eTRS

requirements.

Since the new regime eliminates most output measures from the eTRS criteria and thus reduces

the noise driven by consumer criticalness, we observe a more homogeneous share of certified sellers

across categories immediately after the introduction of the new eTRS. Six months into the new

regime, sellers demonstrate significant improvement in the input measures highlighted by the new

regime, and the improvement is larger in less critical markets, mostly because the new algorithm

automatically removes the potential negative bias for sellers in critical markets and thus these

sellers have less pressure to reach the new threshold relative to sellers in non-critical markets. For

sellers whose metrics are near the new threshold upon the announcement of the new eTRS criteria,

we observe a significant threshold effect: those just below the threshold improve much more than

those just above it.

2

We also explore seller heterogeneity in seller size. Because the old eTRS system uses metrics

that average across all the qualifying orders of a seller, a seller that completes a smaller number of

orders is subject to greater randomness in each average metric. However, the noise from seller size

could benefit or harm a small seller: a mediocre seller could get badged if his small clientele is too

nice to give negative feedback, but a hardworking seller may not qualify for the badge if his small

clientele is unusually picky. In our data, we find that the new algorithm has a greater negative

selection effect on larger sellers (where seller size is measured by the number of eTRS-qualifying

orders before the regime change), which in turn motivates larger sellers to improve more in the

eTRS-highlighted metrics post the regime change. That being said, the effort improvement of large

sellers is less in critical markets than in non-critical markets, because the new algorithm becomes

friendlier to sellers in critical markets. We also find sales become more concentrated in critical

markets (relative to non-critical markets) after the regime change, probably because large sellers

can gain more from the eTRS status and the average item value is higher in critical markets.

Our results have a few implications for market designers and digital platforms. First, there is

a trade-off between information relevance and noise when deciding whether to use output-based

measures, such as consumer reports, in quality certification. Our study focuses on one design

approach: certifying sellers entirely based on seller input while providing output-based measures as

a separate signal. This design approach can preserve the informativeness of different information

sources and reduce the noise in certification to incentivize seller effort. Second, reducing noise in

certification has two opposing effects on seller effort: it encourages seller effort, as the principle-

agent theory predicts, but also discourages some sellers’ effort, as they can more precisely target

their effort level to just meet the certification threshold. Market designers need to consider these

two forces when choosing the amount of noise in certification requirements. Lastly, if a quality

certification uses input-based criteria, it may result in consumers’ benefiting from a homogenization

of certified sellers across markets if consumers value the ability of interpreting the certification signal

consistently across different markets.

1.1 Literature Review

Our results highlight how noise in consumer reports and the discrete nature of quality certifica-

tion affect seller behavior, thus enriching the classical welfare comparison between reputation and

certification (Shapiro, 1983; Leland, 1979). Specifically, our paper contributes to a few strands of

empirical literature.

3

The first relevant strand of literature studies the design of information disclosure and certi-

fication systems. As summarized in Dranove and Jin (2010), “from cradle to grave, consumers

rely on quality disclosure to make important purchases.” Because consumers value information on

seller quality, well-designed information disclosure can select high-quality sellers into the market

and encourage their quality provision efforts. One of the earliest empirical studies that leverage

abrupt changes in consumer information for identification is Jin and Leslie (2003), who show that

mandatory display of hygiene quality grade cards motivates restaurants to improve hygiene quality.

Since then, there have been a plethora of papers that use natural experiments to study the effect of

information disclosure on seller behavior. A summary of these papers can be found in Dellarocas

(2003), Dranove and Jin (2010), and Einav et al. (2016).

In our context, quality disclosure takes the form of the eTRS program. Previous work has

shown that consumers value the eTRS certificate, and that it is equivalent to a 7% increase in

buyer willingness to pay on eBay’s U.K. site (Elfenbein et al., 2015) and a 3% increase in sales

price on eBay’s U.S. site (Hui et al., 2016). Additionally, certification requirements can have a large

impact on seller selection and behavior: In the context of eBay, Hui et al. (2017) show that the

stringency of the eTRS certificate affects the quality distribution of entering sellers, and Hui et al.

(2020) show that adding an intermediate certification tier can mitigate the reputation “cold-start”

problem of young, high-quality sellers. Outside eBay, Farronato et al. (2020) show that occupational

licensing adds little information value above and beyond consumer ratings on a platform that offers

home services. In comparison, Jin et al. (forthcoming) find that partial and mandatory licensing of

food sellers on Alibaba, following the 2015 Food Safety Law of China, improved the average quality

of surviving food sellers.

Our paper contributes to this literature by studying how different content in certification re-

quirements, namely input-based or output-based information, affects seller incentives and market

outcomes. We find that the dichotomous nature of certification matters, because rational sellers

will target their effort to just meet the threshold — a behavior that has also been documented in

contexts where ratings are rounded to half a star (Hunter, 2020).

The certification in our context is partially based on consumer reports. Therefore, our paper also

relates to a big literature that studies the value of consumer feedback, both as an informational

device for buyers and as a motivational device for sellers. Regarding consumer feedback as an

informational device, researchers have shown that higher reputation leads to higher prices and

sales in various contexts, including e-commerce (Chevalier and Mayzlin (2006), Vana and Lambrecht

4

(2021) and Park et al. (2021)), online labor markets (Barach et al. (2020)), review websites (Luca

(2016)), the hotel industry (Hollenbeck et al. (2019)), and eBay (Dewan and Hsu (2004), Resnick

et al. (2006), and Saeedi (2019)). Ratings also improve consumer welfare (e.g., Wu et al. (2015),

Lewis and Zervas (2016), and Reimers and Waldfogel (2021)). See Dellarocas (2003) and Tadelis

(2016) for summaries of this line of work.

Regarding consumer feedback as a motivational device, Cabral and Hortacsu (2010) have shown

that eBay sellers change their effort in response to negative feedback. Recently, a growing empirical

literature shows that the design of rating systems can have profound effects on market outcomes.

For example, many marketplaces use bilateral rating where both buyers and sellers can rate each

other. However, bilateral rating gives sellers an opportunity to retaliate on buyers who leave them

negative feedback and, therefore, dilutes the value of ratings (Dellarocas and Wood, 2008; Bolton

et al., 2013; Fradkin et al., 2019). Moving from bilateral to unilateral rating systems — where only

buyers can rate sellers, increasing market transparency — can further increase seller effort (Klein

et al., 2016) and improve the pool of surviving sellers in the marketplace (Hui et al., 2018). Besides

its impact on the distribution of quality in the market, rating systems can also affect other market

outcomes such as innovation (Leyden, 2021).

Our paper contributes to this line of work by studying the benefits and costs of using consumer

reports in the eTRS certificate. Specifically, our results suggest that the noise borne in consumer

reports can demoralize sellers, and that the market designer needs to weight the informational

benefit of incorporating consumer reports against its negative effect on effort incentives. These

results shed light on the optimal aggregation of input- and output-based quality measures, such as

the first steps taken by Dai et al. (2018).

2 Background

In this section, we describe eBay’s reputation and certification systems. In 1995, eBay began using a

reputation system where buyers and sellers can rate their experience as positive, neutral, or negative

after each transaction. eBay then aggregates this feedback into two metrics on the item listing page:

percent positive (number of positive ratings divided by the sum of positive and negative ratings)

and feedback score (count of positive ratings minus count of negative ratings). Later, in 2008,

eBay switched to a unilateral feedback system in which only buyers are allowed to leave negative

feedback to sellers. In addition, buyers can choose to give Detailed Seller Ratings (DSR) to a seller

5

Table 1: Misperformance measures included in eBay’s eTRS criteria

Before After

1. Negative or neutral feedback (/)

2. Low DSR on item as described (/)

3. Buyer claims (/) Unresolved buyer claims (*)

4. Seller cancellation (*) Seller cancellation (*)

5. Low DSR on shipping time (/) Late delivery based on tracking information (*)

Notes: (*) denotes input-based measures; (/) denotes output-based measures; DSR means Detailed Seller Ratings.

in four dimensions: item as described, communication, shipping speed, and shipping charge. Unlike

the classical feedback system, DSR use a 5-star scale and are anonymous in that the seller cannot

tell the identity of the reviewer.

Besides feedback and DSR, eBay introduced the eBay Top Rated Seller (eTRS) certification

program in September 2009. The goal was to endorse sellers who meet a quality threshold based

on consumer feedback, DSR, and the platform’s internal data. In particular, sellers are evaluated

on the 20th of each month against a set of requirements. The eTRS requirements during the

sample period before the regime change (from October 2014 to January 2016) consist of two parts.

First, a seller needs to have a minimum of $1,000 in sales and 100 transactions in the past 12

months. Second, a seller cannot have a defect rate greater than 2%, where defect includes negative

or neutral feedback (measure 1 in Table 1), 1- or 2-star rating on item-as-described DSR (measure

2), buyer claims due to item being not as described or not received (measure 3), seller cancellations

(measure 4), and 1- or 2-star rating on shipping speed DSR (measure 5). The evaluation period

for the defect rate is the past three months if a seller has at least 400 transactions in the past three

months; otherwise, it is based on the transactions in the past twelve months.

In September 2015, eBay announced a change in eTRS requirements, effective February 2016.

1

The goal of the policy change was to create a simpler and more objective standard. Specifically,

defects in the new criteria are limited to two measures: unresolved buyer claims where eBay finds

the seller at fault (a subset of previous measure 3) and seller cancellation (same as previous measure

4).

2

Because of this change, eBay reduced the maximum defect rate from 2% to 0.5% for eTRS

eligibility.

3

In addition, eBay introduced a new measure for shipping performance, namely whether

1

See the cached (historical) announcement page on 09/11/2015 at http://bit.ly/3t93hPm.

2

When a buyer files a claim on an order and the seller cannot resolve it in three days, the case is escalated to

eBay. It is counted as a defect if eBay decides the seller is at fault.

3

This adjustment was made so that there would be no significant change in the number of eTRS sellers, according

to eBay’s policy announcement.

6

the seller ships out the item on time according to the tracking information.

4

In comparison, the old

system measured shipping time by buyer-reported DSR only. This change places more emphasis

on seller effort toward timely shipping rather than the realized delivery time and, therefore, shields

the seller from potential delay of the shipper. Accordingly, eBay sets the maximum late delivery

rate as 5% in the new eTRS criteria and takes late delivery out of the defect counts.

In short, the new certification regime moves from output-based to input-based measures. Out-

puts such as non-positive feedback (measure 1), low DSR on item-as-described (measure 2), and

resolved buyer claims (part of measure 3) no longer count towards seller defects, and the metric on

shipping time is based on tracking information rather than consumer reports (measure 5). These

changes reduce the noise embedded in consumer-reported outputs, which could arise because of

third-party faults (e.g., shipper delay) or subjective evaluation. As a result, sellers may find it

easier to manage and predict future eTRS eligibility. For example, a seller eager to earn the eTRS

badge may refund the buyer when there is a claim, refrain from cancellation, and ship the item as

soon as possible.

In theory, many measures mentioned above are visible to an attentive buyer familiar with

the eBay system. In reality, the visibility of the metrics used varies and depends on how they

are aggregated and presented by eBay. Figure 1 shows two example listings of Apple iPad: the

upper one is from a non-badged seller with 100% positive feedback and a total feedback score of

3093. Clicking on the seller’s name leads to the seller’s profile page, which has more details about

the seller’s positive, neutral, and negative feedback as well as his star ratings in the four DSR

dimensions. Using clickstream data from eBay, Nosko and Tadelis (2015) show that less than 1%

of buyers ever go to the seller’s profile page. This implies that DSR are much less visible to buyers

than aggregate consumer feedback metrics (positive feedback and feedback score).

The lower example in Figure 1 is from another seller with 98.4% positive feedback, a total

feedback score of 1556, and a Top Rated Plus badge on the upper right corner of the page. This

badge is shown on the listing page when the seller is qualified for the eTRS and offers one-day

handling plus 30-day return for this particular listing.

5

A buyer can also click on the seller’s profile

page for more detailed seller status such as “Top Rated”, “Above standard”, or “Below standard.”

However, since less than 1% of buyers visit the seller profile page, the visibility of the eTRS badge

largely depends on whether an eTRS seller offers fast handling and easy return on a particular

4

If tracking information is not available, eBay will ask the buyer if the item was delivered on time when she leaves

feedback and the delivery will be considered late if the buyer indicates late delivery.

5

During the sample period, the Top Rated Plus badge resembles a gold medal, the same as the one in Figure 2.

7

Figure 1: Example Listing Pages

(a) Example 1: A listing without an eTRS plus badge

(b) Example 2: A listing with an eTRS plus badge

listing. Around 70% of listings from eTRS sellers have the Top Rated Plus badge, partly because

of the rule on badge visibility and partly because an eTRS seller will receive a 10% discount off the

commission fees on any of her listings with the eTRS badge.

Another difference in visibility is on the search page. Figure 2 shows how two listings appear

together on a search page. This page is loaded when buyers search for products, which usually

occurs before buyers click on a listing page. The badge is highlighted on the search page, but

consumer feedback and DSR do not appear on this page.

In combination, Figures 1 and 2 imply that the eTRS certification is more salient to buyers

than aggregate consumer feedback metrics, which are in turn more salient than DSR on the seller

profile page that consumers rarely visit. If we define reputation as consumer perception of a seller

based on consumer reports of the seller’s past behavior, the eBay setting suggests that aggregate

consumer feedback metrics — namely percent positive and total feedback score — contribute much

8

Figure 2: Example Search Page

more to seller reputation than DSR do.

In comparison, some measures in the eTRS system — for example, buyer claims (measure

3 in Table 1) and seller cancellation (measure 4) — are not shown to buyers anywhere but are

incorporated in the eTRS certificate. While buyer claims are still a form of consumer-reported

output, the new system excludes resolved buyer claims and thus puts more emphasis on seller

effort to resolve buyer claims. This change does not completely rule out consumer-driven noise,

because consumers decide whether, when, and how to file a claim.

3 Model

3.1 Model Setup and Predictions

In this section, we present a stylized model describing the impacts that the new eTRS regime

could have on individual sellers. Consider one period in a market of many sellers and even more

homogeneous buyers. Each seller offers one unit of a standard product with zero production cost.

Each buyer may purchase at most one unit. We assume the product on sale is good enough relative

to the buyer’s outside option, and thus every product is sold at a price that is equal to its expected

quality given the buyers’ information set.

Suppose the true quality of seller j (q

j

) solely depends on seller effort e

j

. We assume that

buyers do not observe e

j

directly, but observe a binary certificate signal provided by eBay. The

key question for eBay is how to construct the certificate signal in order to motivate seller effort to

maximize the platform’s interest. This is a classical principal-agent problem: eBay is the principal

9

that cares about the overall sales revenue (because its commission is a fixed fraction of sales), while

each seller wants to maximize his own sales minus effort costs.

Here we model seller effort as one dimension. In reality, seller effort can be multi-dimensional,

for example, one on shipping and handling and one on answering customer questions about the

product. In that case, consumers may perceive seller quality as a sum of seller efforts in all

dimensions, and eBay may provide multiple signals for multi-dimensional efforts, for example a

summary of consumer feedback (“reputation”) and the eTRS (“certificate”). Even if the signals

are not orthogonal, as long as their definition is known to the public, rational consumers can

redefine them so that each signal captures one dimension of effort independent of other dimensions.

In this sense, our model can be thought as a model of one-dimensional effort conditional on other

dimensions of effort already being covered by other signals.

Let us assume eBay observes a noisy proxy s

j

for e

j

, where the noise

j

conforms to a normal

distribution with mean zero and standard deviation σ:

s

j

= e

j

+

j

j

∼ N (0, σ).

In the old system, eBay defines a binary certificate signal eT RS

old

= 1 if the sum of the proxy s

j

and another noise (

R

j

) is above a minimum threshold κ. We introduce

R

j

to reflect noisy consumer

opinion not captured in seller reputation, not directly observable to consumers, but embodied in

the old eTRS, for example DSRs and resolved buyer claims.

eT RS

old

j

= 1 if s

j

+

R

j

= e

j

+

j

+

R

j

≥ κ

The new eTRS system simplifies the certificate signal based on s

j

only. This is equivalent to

excluding

R

j

:

eT RS

new

j

= 1 if s

j

= e

j

+

j

≥ κ.

Because the eTRS is calculated by an absolute threshold, whether a seller can qualify for the

eTRS depends on not only his effort but also the mean and dispersion of the noises. We assume

R

conform to a normal distribution with mean µ

R

and standard deviation σ

R

:

R

j

∼ N (µ

R

, σ

R

).

10

We allow

R

j

to be biased in the mean because the seller may operate in a product category in

which consumers are known to be harsh (µ

R

< 0) or lenient (µ

R

> 0). As a result, sellers in a

harsh category were subject to a higher eTRS standard in the old system than in the new system

(i.e. s

j

≥ κ − µ

R

vs. s

j

≥ κ). This leads to an algorithmic selection effect:

Prediction 1: The change in eTRS requirements will immediately improve the certificate signal

for seller j if j operates in a category subject to more consumer criticism on average (µ

R

< 0) and

consumer opinion is removed from the new certificate.

The more negative µ

R

is, the more improvement there should be in the new certificate signal.

By definition, these changes are driven by the eTRS algorithmic change before seller j adjusts

efforts.

To complete the model, we assume eBay’s payoff is proportional to total sales on the platform:

π

eBay

∝

X

j

E(q

j

|eT RS

j

)

but seller j must incur effort costs that are increasing and convex in e

j

. Hence seller j’s problem is

choosing e

j

to maximize his expected revenue net of eBay commission (at rate r) and effort costs:

π

j

= (1 − r) · E(q

j

|eT RS

j

) − C(e

j

).

Apparently, moral hazard arises because the principal (eBay) does not observe seller effort

and would like all sellers to exert maximum effort despite their private effort costs. In a classical

principal-agent model (for example Baker (1992)), the principal would set the agent’s wage con-

ditional on an observable outcome that depends on agent effort. Here, eBay does not pay wages

to sellers directly but seller revenue depends on buyer perception of seller quality, which in turn

depends on the certificate signal provided by eBay. In this sense, the eTRS signal can be translated

into signal-based revenue to sellers. The strength of the incentive depends on the noises in the

signal, and how the signal affects consumer belief of seller quality.

Because the certificate signal is binary, we have:

π

j

= (1 − r) · E(q

j

|eT RS

j

) − C(e

j

)

= (1 − r) · {prob(eT RS

j

= 1) · E(e

j

|eT RS

j

= 1) + prob(eT RS

j

= 0) · E(e

j

|eT RS

j

= 0)} − C(e

j

)

= (1 − r) · {E(e

j

|eT RS

j

= 0) + prob(eT RS

j

= 1)

| {z }

P rob of eT RS

· [E(e

j

|eT RS

j

= 1) − E(e

j

|eT RS

j

= 0)]

| {z }

quality premium for eT RS=∆q

} − C(e

j

)

11

Let F(.) represent the CDF of standard normal, we have

prob(eT RS = 1) = prob(e

j

+

j

+

R

j

≥ κ)

= 1 − F

κ − e

j

− µ

R

q

σ

2

+ σ

2

R

At the optimal choice of e

j

, the marginal cost of effort should be equal to the marginal benefit

of effort, which depends on how e

j

affects the probability of reaching the eTRS threshold and how

consumers perceive the average e

j

conditional on the seller’s eTRS status. However, consumer’s

quality expectations are not specific to seller j’s actual effort, they are only conditional on seller

j’s eTRS status. Hence, the quality premium for badged sellers, denoted as ∆q, is a constant from

seller j’s perspective if the seller is only one of many sellers in the same market. Consequently, let

f(.) denote the pdf of standard normal, we can derive seller j’s first order condition with respect

to e

j

:

(1 − r) ·

∂prob(eT RS

j

= 1)

∂e

j

· ∆q =

∂C

∂e

j

(1 − r) · f

κ − e

j

− µ

R

q

σ

2

+ σ

2

R

·

∆q

q

σ

2

+ σ

2

R

=

∂C

∂e

j

(1 − r) · ∆q · f

κ − e

j

− µ

R

q

σ

2

+ σ

2

R

=

∂C

∂e

j

·

q

σ

2

+ σ

2

R

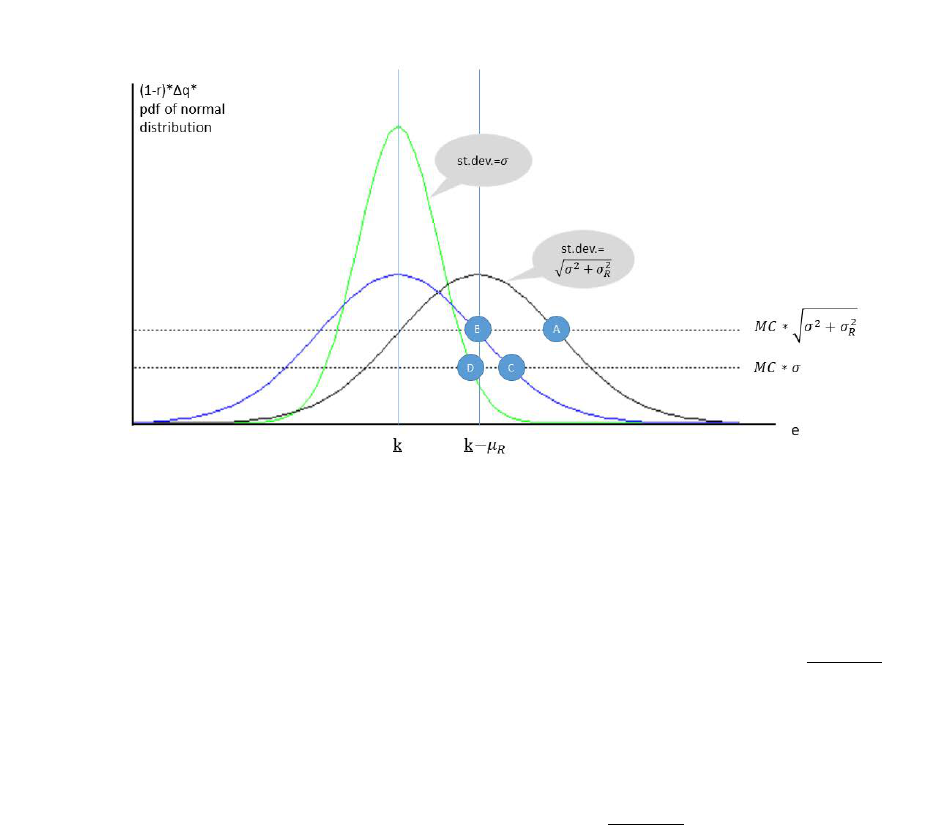

Figure 3 plots the two sides of the equation respectively as a function of e

j

, for a seller that

operates in a critical market (µ

R

< 0) and has constant marginal cost of effort (MC). Their

intersection denotes the optimal e

j

, if we assume seller j takes ∆q as given. As shown in Figure 3,

the impact of the new eTRS regime on e

j

can be decomposed into three parts:

• Effect 1 on e

j

|∆q: Reduce overshooting (undershooting) in the categories with

µ

R

< 0 (µ

R

> 0). In the old regime, sellers in a category with harsh consumer criticism

(µ

R

< 0) must exert extra efforts to reach the eTRS threshold, as indicated by point A. This

overshooting is no longer necessary in the new regime, as indicated by point B. The effort

change from A to B is a reduction in overshooting. This effect is reversed in a lenient product

category (µ

R

> 0), because, sellers in that market were closer to the threshold in the old

regime but this institutional help is no longer available in the new regime, and thus they

12

Figure 3: Decomposition of the Impact of the New Regime on Individual Seller Effort (assume

µ

R

< 0)

must exert more efforts to reach the same threshold. This is a reduction of undershooting.

• Effect 2 on e

j

|∆q: Motivate more effort to target a more precise goal: because the

standard deviation of the noise in the new eTRS certificate is reduced from

q

σ

2

+ σ

2

R

to σ,

sellers can better predict how their effort affects the probability of reaching the eTRS thresh-

old. Following the standard principal-agent theory, reducing noise in performance outcome

can translate effort into outcome more effectively, thus motivating effort. In Figure 3, this

amounts to a reduction of the right hand side from MC ·

q

σ

2

+ σ

2

R

to MC ·σ, which implies a

move from point B to point C. Note that this change is independent of µ

R

regardless whether

the seller operates in a harsh or lenient category. Moreover, illustrated in Figure 3 is a seller

whose marginal cost is low enough so that he has tried to reach the eTRS even in the old

regime. If the seller’s marginal cost is sufficiently high, he may have given up on eTRS in the

old regime but finds it worthwhile to aim for eTRS in the new regime. In that case, Effect 2

would be greater than what is shown in Figure 3 because point B in that case should denote

zero effort in the old regime.

• Effect 3 on e

j

|∆q: Sharpen the classical threshold effect. Reduced noise in the new

13

eTRS also makes the marginal benefit of effort more sensitive to the distance to the threshold.

When the effort is below but close to the threshold, the gain from extra effort increases sharply

in the new regime; but when the effort exceeds the threshold or is far away from the threshold,

the gain from extra effort drops sharply. In Figure 3, this effect is represented by moving the

bell curve from blue to green, resulting in a reduction of effort from point C to point D. Like

Effect 2, this effect is sensitive to the magnitude of σ

R

but independent of µ

R

.

The above three effects assume individual sellers take the market-wide quality premium ∆q as

given. However, when every seller adjusts his effort in the new regime, consumers will update ∆q

accordingly. This brings:

• Effect 4: Consumers update the quality premium for badged sellers (∆q). When

sellers adjust e

j

because of the above three effects, the adjustment on ∆q tends to go to the

opposite direction: for example, sellers in a harsh category (µ

R

< 0) were known to face a

higher threshold in the old system (κ − µ

R

), thus consumers had reason to believe that those

badged in the old system were of higher quality. When the new system restores the threshold

to κ, sellers in the harsh category find it easier to reach the new threshold, which also implies

that rational consumers should lower the quality premium for badged sellers. This market-

wide adjustment counters Effect 1. Conversely, if the new eTRS motivates most sellers to

barely pass the threshold, consumers should believe that the average quality of badged sellers

is barely above the threshold. This market-wide adjustment counters Effect 3. Furthermore,

if everyone is motivated to exert more effort because the certificate signal is more precise

(Effect 2), it may be cancelled out in the relative difference between badged and non-badged

sellers.

In combination, we have:

Prediction 2: The new eTRS system has ambiguous effects on e

j

, depending on how the above

four effects play out in sum.

Later on in the empirical section, we will present evidence on the overall effort changes before

and after the eTRS regime shift (a sum of the four effects), the relative effort changes in critical

versus non-critical categories (Effect 1), seller efforts around the new eTRS threshold (Effect 3),

and the change in the average quality premium for eTRS-certified sellers (Effect 4).

The above two predictions focus on individual seller incentives in a product category with

specific µ

R

and σ

R

. Assuming the distribution of seller’s marginal cost of effort (M C) is the same

14

across categories, we can compare the effect of the new eTRS regime across categories. In particular,

Effects 1, 2 and 3 imply that individual seller’s effort choice will become more homogenized across

categories because the new system eliminates the incentive differential driven by category-specific

µ

R

and σ

R

. Effect 4 speaks to the quality premium of eTRS within each category, which depends

on µ

R

and σ

R

as well. If seller efforts are more homogenized across categories, ∆q should also be

more homogenized because it reflects consumer expectation of average effort conditional on eTRS

status. This implies:

Prediction 3: The new eTRS system may homogenize the probability of getting eTRS certified

across categories, if every product category has the same distribution of marginal cost of effort

among individual sellers.

We will provide evidence for Prediction 3 by studying temporal changes in the distribution of

certified sellers across product categories.

3.2 Numerical Simulation in eTRS

The model clarifies that the new regime eliminates µ

R

and σ

R

from eTRS criteria. Later on, we

will compute average consumer criticalness across categories, which corresponds to a distribution

of µ

R

and will naturally lead to variations in σ

R

.

A less obvious source of variation for σ

R

is seller size. Sellers of different size are subject to

different amount of noise because all eTRS-relevant metrics are averaged across a seller’s qualifying

orders. Assuming draws of

R

are independent across orders, the mean of this random noise (µ

R

)

may be the same for different sellers in the same category, but a seller with more qualifying orders

will have a more precise average metric relative to his true quality (and thus a lower σ

R

).

To illustrate how µ

R

and σ

R

affect the certificate signal in the old eTRS system, we conduct

a numerical simulation where every seller makes maximum effort in the actual performance (say,

sellers always describe the item perfectly, always ship immediately, and never cancel), but a seller

earns an eTRS certificate if and only if the defect rate observed by eBay is no higher than 2%.

The signal reflects an average of previous consumer reports on the seller, and each consumer report

conforms to a Bernoulli distribution with probability p for value 1 (i.e., a bad consumer report)

and 1 − p for value 0 (i.e., a good consumer report). One can think of these binary signals as

low DSR ratings on the seller-profile page, or claims that consumers file to eBay. Given this, the

seller’s probability of getting eTRS badge follows a binomial distribution. To fit in our model,

the simulation is equivalent to setting µ

R

= −p (negative because DSR and consumer claims are

15

criticism by definition) and σ

R

=

q

p(1−p)

n

where n is the seller’s total number of qualifying orders.

To reflect different consumer criticalness in different product markets, we assume p is fixed in

each category but ranges from 0 to 1 across categories. On seller size, we consider two types of

sellers in each product category: a small seller has only 20 orders qualified for eTRS calculation,

while a big seller has 2000 qualified orders. For each type of sellers in a category with criticalness

p, we simulate the probability of being certified for a typical small seller and a typical big seller in

that category. Figure 4 presents the simulated results. The horizontal axis is consumer criticalness

p. The vertical axis is the probability that a seller satisfies the old eTRS requirement. The vertical

line indicates the 2% cutoff. We present two curves for small and large sellers respectively.

Figure 4: Seller Size and Rating Criticalness

Notes: This figure plots the probability of being certified against rating criticalness for a typical small seller

and a typical big seller. Sellers always deliver high quality, and rating criticalness is the probability of getting

a negative feedback. The certification bar is at 98% positive feedback, as repented by the vertical line. The

probabilities are calculated using the binomial probability mass function.

Figure 4 demonstrates two patterns. First, the probability of getting certified decreases by

consumer criticalness for all sellers. This reflects Prediction 1: when the draw of the noise is more

negative on average (µ

R

< 0), the certificate signal is more negative. Second, when consumer

reports are more accurate than the certificate cutoff (p < 2%, the left side of the vertical line),

small sellers are more vulnerable to consumer criticalness than large sellers. Essentially, the Law

of Large Numbers guarantees that a perfect-performing large seller will almost always pass the

minimum threshold, but chances play a bigger adverse role for sellers with only a few transactions.

This pattern is reversed when consumer criticalness is larger than the certificate cutoff (p > 2%,

the right side of the vertical line), because it is easier for a small seller to have enough lucky draws

16

to get above the certificate cutoff.

What does the regime change mean in our simulation? Because the new eTRS system excludes

consumer feedback, low DSRs, and resolved buyer claims, it essentially lowers p to p

0

for all markets,

where p

0

reflects other noises that remain in the new system (e.g. cancellation due to factors out

of seller control or traffic jam from the seller’s warehouse to the postal office). This implies that we

should observe less heterogeneity across critical and non-critical markets, conditional on the same

seller performance. However, as long as p

0

is positive, heterogeneity across small and big sellers still

exists, and how that heterogeneity changes depends on where p and p

0

are in reality. If p is to the

left of the certification threshold, say around 1%, then a reduction to p

0

would disproportionately

benefit small sellers, as they were more adversely affected by the old eTRS rules than big sellers. If

p is to the right of the certification threshold, say around 3%, then a reduction to p

0

would benefit

big sellers, because they are almost never certified under the old eTRS rules.

In short, the simulation emphasizes the importance of the interaction between feedback crit-

icalness of a market and seller size on the algorithmic selection effect: the regime change should

immediately benefit all sellers in more critical markets; additionally, it should disproportionately

benefit small sellers in non-critical markets and large sellers in critical markets. These insights are

consistent with Prediction 1. Lastly, small and large sellers may become more homogenized in the

share of certified sellers after the regime change, as (a simple extension of) Prediction 3 indicates.

4 Data

4.1 Sample Construction

We use proprietary data from eBay’s U.S. site. Our starting point is the set of all listings on

eBay from 11 months before to 11 months after the month when eBay announced the eTRS regime

change, excluding the listings in Motors and Real Estate categories. We define three periods based

on the policy announcement date and implementation date: “before” refers to the 11 months

before the policy announcement (October 20, 2014 to September 19, 2015); “interim” refers to

the 5 months between the policy announcement and its implementation (September 20, 2015 to

February 19, 2016); “after” refers to the 6 months after the policy implementation (February 20 to

August 19, 2016).

6

To focus on professional (rather than occasional) sellers, we first condition the

6

The policy announcement date is September 11, 2015. Therefore, the first month in the interim period is the

first full month after the policy announcement.

17

sample construction on sellers who had sold at least $5,000 in the year before the month the policy

was announced. We then keep sellers who listed at least one item in each of the before, interim,

and post periods, to mitigate the potential problem of dynamic entry and exit.

To better understand across-market variations, we remove small markets from a total of 428

markets on eBay, where a market refers to a product category as defined by eBay.

7

Specifically, we

remove all markets with less than $300,000 in sales in the first three months of the sample period,

including one market with missing sales data. This procedure leaves us with a sample of 380,978

sellers in 336 markets, which accounts for 99.7% of the total sales without market restrictions.

Conditional on these sellers, we aggregate transaction data at the seller and seller-month levels for

seller analysis, and at the market-month level for market analysis.

4.2 Summary Statistics

Our goal is to test our model’s predictions of how a regime change from output-based to input-based

certification requirements would affect (1) the algorithmic selection of eTRS certified sellers before

any effort change by sellers; (2) how sellers may respond to the regime change in their effort choice;

and (3) how markets may become homogenized as the new regime eliminates some cross-market

differences from the certification criteria. The first item is an automatic change that immediately

happened when eBay announced the new eTRS algorithm, in September 2015, while the other two

items are endogenous changes that may occur after the announcement date.

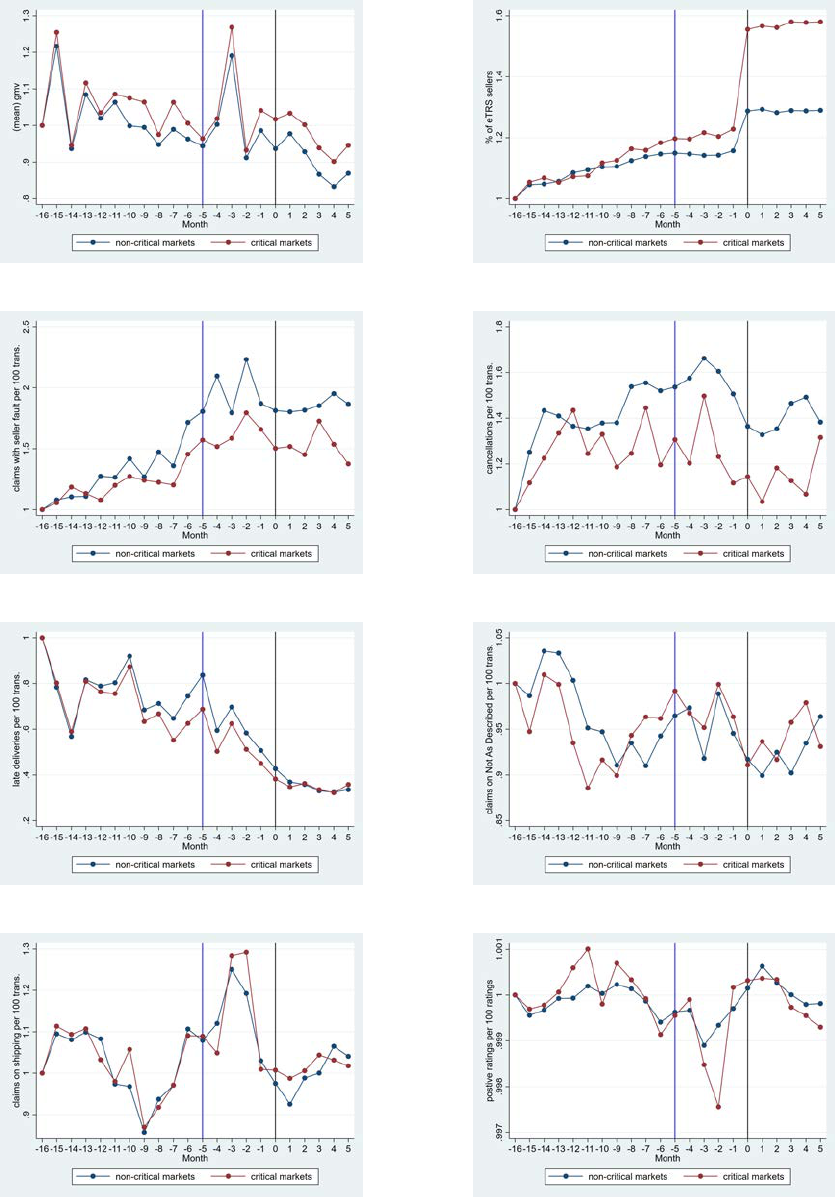

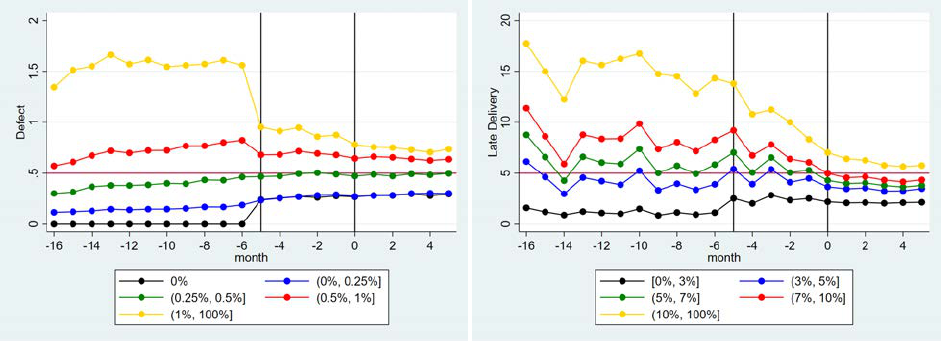

To illustrate market trends, in Figure 5 we plot monthly averages of some key variables from

sellers included in our sample. To get a data point in the figure, we first get a summary statistic

for each market in a month, and then we calculate the average of that summary statistic across

markets. Month 0 refers to the first month of the new eTRS policy implementation (February 2016),

as illustrated by the black vertical lines. eBay announced the then forthcoming eTRS change in

Month -5, as illustrated by the blue vertical lines. All monthly averages are normalized by the value

in the first month of our sample (i.e., October 2014), to keep eBay’s business data confidential.

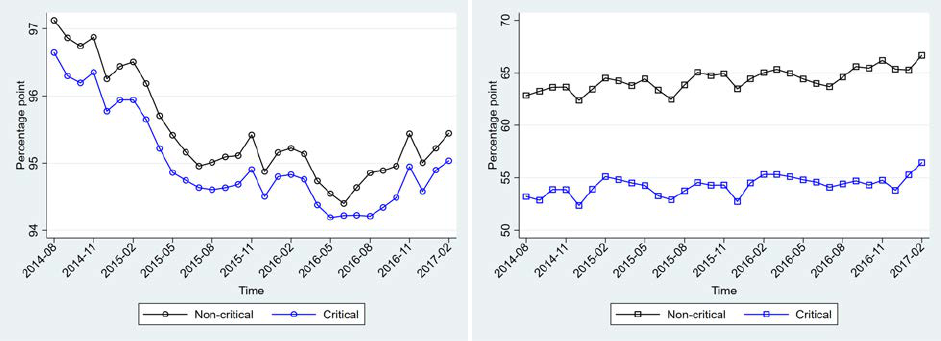

Because a key heterogeneity in our model is consumer criticalness in a market, we plot the series

separately for non-critical and critical markets. We define consumer criticalness in a market by the

share of transactions that were considered defect in the old eTRS system out of all transactions

that are considered good in the new system. For example, these transactions contain packages that

were scanned by the post office on time but received a low DSR on shipping speed. The share of

7

Examples of categories include Video Games, Women’s Clothing, and Cell Phones & Smartphones.

18

these transactions among all transactions that would be good under the new eTRS criteria gives

us a continuous measure of consumer criticalness at the market level. Throughout the paper, we

label a market “critical” if its criticalness is above the median of all 336 sampled markets, and

“non-critical” otherwise. By definition, we have 168 critical markets and 168 non-critical markets.

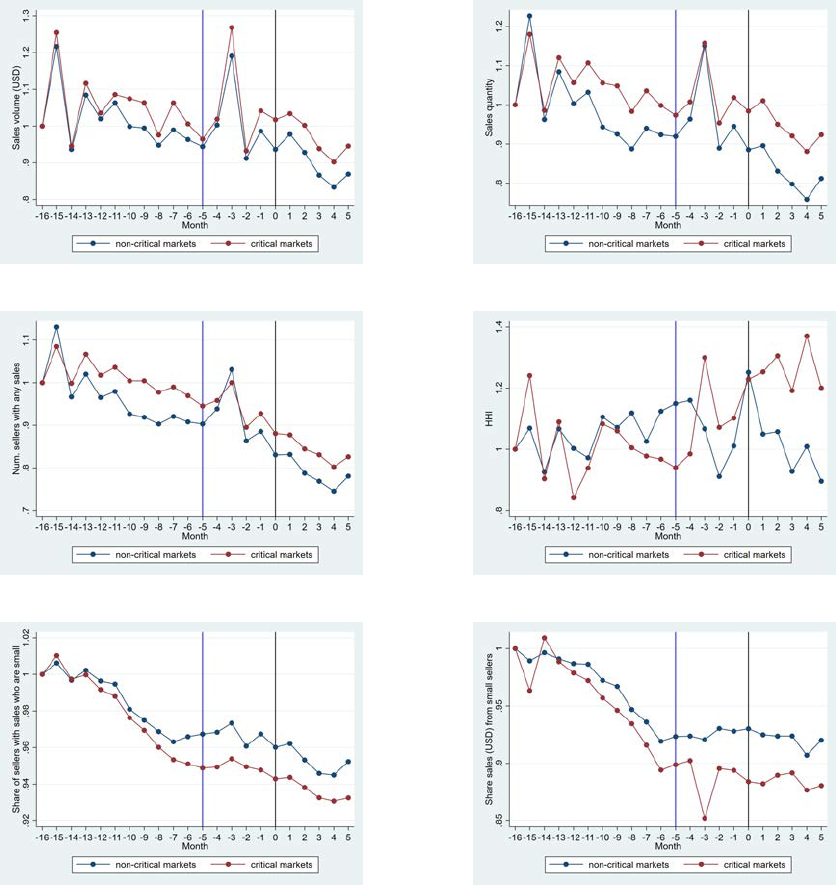

Figure 13a plots the normalized sales volume (in USD) over time. The data points exhibit

strong seasonality, as indicated by large spikes in sales in Month -3 (November 21 to December

20, 2015) and in the same calendar month the previous year (Months -15). There are no obvious

changes in overall sales before and after the policy announcement month for either market type.

Figure 13b shows a clear increase in the number of eTRS-certified sellers after the policy im-

plementation. Moreover, this increase is larger in critical markets than in non-critical markets.

The reason is twofold. First, as stated in Prediction 1, because consumer criticalness is larger in

critical markets (corresponding to µ

R

< 0 in the model), the algorithmic change that eliminates

µ

R

in certification will lead to disproportionately badging more sellers in critical markets. Second,

the algorithmic selection also incentivizes sellers to change their behavior subsequently because of

reasons described in Prediction 2, which can also contribute to a higher share of eTRS sellers after

the policy implementation. Specifically, sellers overall seem to demonstrate better performance in

the input measures highlighted by the new eTRS system: while Figure 13c and Figure 13d show

no clear overall change in unresolved claim rate and seller cancellation, both measures are lower

in critical markets, consistent with the argument that the new regime incentivizes sellers in these

markets to exert more effort (Effect 2 under Prediction 2). In Figure 13e, sellers seem to have

an overall decrease in late delivery after the policy announcement, although this can be partially

driven by the pre-existing trend. However, month-by-month variation in this measure is clearly less

after the regime change, suggesting that sellers may have taken this measure more seriously in the

new eTRS regime.

Lastly, Figures 13f, 5g, and 5h plot three output measures that are no longer included in the new

certification requirements: the share of transactions that have items not as described (as reported

in DSR or buyer claims), the share of transactions that have items not received, and the share of

positive feedback ratings among all consumer feedback. We do not observe any systematic change

in these measures neither across time nor across markets.

19

Figure 5: Normalized Time Series by Rating Criticalness

(a) sales volume (USD) (b) share eTRS sellers

(c) share transactions with unresolved claim (d) share transactions with seller cancellation

(e) share transactions with late delivery (f) share transactions not as described

(g) share transactions not received (h) share of positive feedback if any

Notes: All variables are normalized by the value in the first month of our sample. Rating criticalness is defined as

the share of transactions that are considered “defect” by the old system out of all transactions that are considered

good by the new system. Markets are divided into non-critical and critical based on a median split. Blue and black

vertical lines indicate the policy announcement and implementation months, respectively.

20

4.3 Certification Premium

A necessary condition for sellers to care about certification is that it must benefit certified sellers,

as has been established in previous papers using eBay data (Elfenbein et al., 2015; Hui et al., 2016).

For confirmation, we estimate the eTRS premium in our sample and describe how it changes before

and after the eTRS regime shift. Recall that Effect 4 in Prediction 2 predicts that the badge

premium could go either way.

Because the degree of eTRS certification differs greatly by product, we match transactions from

certified and non-certified sellers by product ID and calendar week of sales.

8

The goal of matching

is to control for unobserved product heterogeneity and temporal demand and supply shocks that

could be correlated with sales price and a seller’s eTRS status. The matching procedure yields

a sample of 101,642 unique sellers in 126 markets, with more than 6 million transactions in our

sample period. We then regress the logarithm of sales price on whether a seller of that listing had

earned the eTRS badge at the sales time, and its interaction with a dummy of the new regime,

controlling for the seller’s percent of positive feedback, product-week fixed effects, and seller fixed

effects.

Estimation suggests that being an eTRS seller is associated with a 1.5% increase in sales price

before the regime change, and 1.8% after, with both estimates and the difference being statistically

significant at the 1% level. These positive premiums imply that sellers should have an incentive to

meet the eTRS requirements both before and after the regime change.

5 Results

5.1 Algorithmic Selection by Market Criticalness and Seller Size

As described in Section 3, the regime change should have two effects: an immediate effect on

which sellers are certified by the new eTRS algorithm, based on their previous performance, and a

subsequent, indirect effect when sellers choose to adjust their efforts in response. We refer to the

former as algorithmic selection, and to the latter as seller behavioral change.

To measure the selection effect, we simulate a seller’s hypothetical eTRS status by applying

the new requirements against the seller’s performance metrics on the policy announcement date

(September 2015, or Month -5). At that time, sellers had not yet had an opportunity to change

8

Product ID is eBay’s finest catalog, which is defined for homogeneous products only. For example, an unlocked

128GB black iPhone 12 has a unique product ID that is different from that of another version of iPhone.

21

their efforts in response to the new policy, so the difference between the seller’s actual and simulated

eTRS status should capture only algorithmic selection.

9

Our model predicts the algorithmic selection effect should differ by consumer criticalness across

markets and by seller size. Figure 6 plots the algorithmic selection effect (subject to measurement

error) across a continuous, market-specific measure of consumer criticalness. Each circle represents

a product subcategory (market) as defined by eBay. On the y-axis is a ratio between the number

of simulated eTRS sellers upon the policy announcement (Month -5) in market m and the actual

number of eTRS sellers at that time in that market according to the old algorithm. Since we may

not report the exact value of the ratio, we normalize it by a constant. Note that this ratio is smaller

than the one in almost all markets in our sample, which means that the algorithm has a negative

selection effect in almost all markets. On the x-axis is the average consumer criticalness of the

market (in percentage points, based on data from the three months before the policy announcement

date (i.e., Month -8 to -6), as defined in Section 4. Circle size corresponds to total dollar sales of

the market in these three months (Months -8 to -6).

We draw a few insights from Figure 6. First, we find that almost all markets experience negative

selection from the algorithm change. That is, the share of sellers who meet the new certification

requirements is significantly smaller than the share of eTRS under the old regime. A big part of the

drop in the eTRS share is mechanical and a direct outcome of the difference between the old and

the new system — sellers were targeting their behavior towards the old system, which naturally

warrants a lower probability of meeting the new requirements, because we define selection as the

change in the eTRS share by applying the new criteria to the existing behavior of sellers. Secondly,

there is a clear positive correlation between the simulated change in eTRS sellers and consumer

criticalness. This is consistent with Prediction 1 and the corresponding numerical simulation in

Figure 4: sellers are handicapped in markets with harsh criticalness; as a result, the new regime

generates greater positive selection for sellers in these markets. Lastly, the figure suggests that

markets with more consumer criticalness tend to have a larger sales volume.

9

Note that there could be measurement errors when we simulate a seller’s eTRS status. For example, we observe

the number of unresolved claims (or other certification metrics) that a seller received. If eBay first thought the seller

is at fault but reversed the decision after the seller appealed with more evidence, that transaction should no longer

be counted as a defect by eBay. However, we would still label this instance as a defect because we do not observe

metrics revision in our sample. In the presence of measurement errors, we can no longer be certain of the absolute

magnitude of the algorithm selection effect, because the difference between the actual and simulated eTRS status

on the policy announcement date reflects not only algorithmic selection but also measurement error. Despite this

shortcoming, we can still study how the relative selection effect differs by market type and seller size if we assume

that the measurement error is independent of the two variables. Additionally, we can still study changes in seller

behavior by comparing simulated eTRS status over time if we assume that the measurement error is constant over

22

Figure 6: Selection by Rating Criticalness

Notes: Rating criticalness on the x-axis is the share of transactions that are considered defect by the old

system out of all transactions that are considered good by the new system. The ratio on the y-axis is based

on sellers’ simulated and actual eTRS status on the announcement date. We normalize this ratio by a

constant. Circle size corresponds to dollar sales in Month -8 to -6.

Next, our conceptual framework predicts that when consumer criticalness is below the old eTRS

cutoff, removing consumer criticalness from the certification requirements would immediately select

more small sellers into the eTRS certification; on the other hand, the selection should be more

positive for sellers in critical markets where sellers were subject to larger noise in certification. To

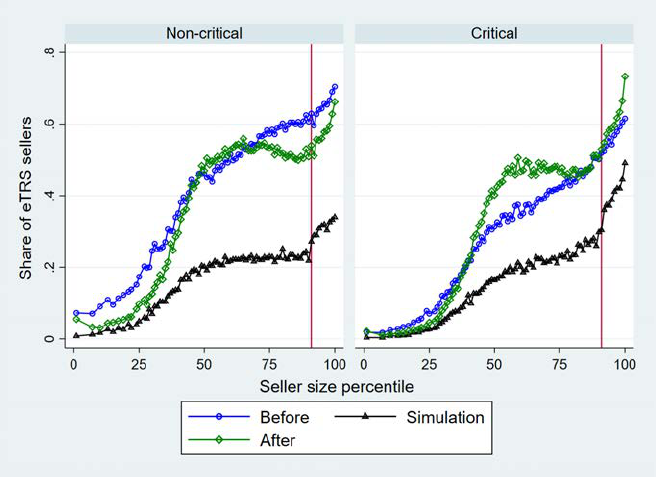

test these patterns using real data, in Figure 7, we plot the “before” (Month -5) and simulated

(at Month -5) shares of eTRS sellers across different percentiles of seller sizes, where seller size

is measured by the number of qualifying orders based on a seller’s historical sales at the time

of the policy announcement (recall that the method for order counts does not change with the

regime shift). We do this separately for critical and non-critical markets. To comply with the

data agreement, the simulated shares of eTRS sellers are normalized by a constant (i.e., the same

constant across time for both sub-figures). The vertical line around the 90 percentile is the cutoff

time.

23

Figure 7: Policy Effect by Seller Size and Rating Criticalness in Markets

Notes: Rating criticalness is defined as the share of transactions that are considered defect by the old system

out of all transactions that are considered good by the new system. Markets are divided into non-critical

and critical based on a median split. Vertical line indicates the percentile cutoff for large sellers. Simulated

share of eTRS sellers (represented by triangles) is normalized by a constant. “Before” refers to Month -5;

simulation is done at Month -5. “After” refers to Month 5.

for large sellers. By both old and new algorithms, sellers that have 400 or more orders in the past

three months are defined as “large”, and their performance metrics are computed based on orders

in the past three months rather than the past twelve months.

Several patterns emerge from Figure 7. First, the share of certified sellers increases in seller size

most of the time, regardless of the type of market and whether the share is actual or simulated.

This makes sense because (1) the certification has requirements on a minimum number of past sales

and (2) seller size may be positively correlated with seller quality.

Second, Figure 7 suggests that the algorithmic selection is more positive (or less negative) in

critical markets than in non-critical markets. This can be seen from a smaller negative distance

between the simulated curve and the “before” curve for all seller sizes. There are two reasons for

this result. First, fixing effort, sellers are less likely to be badged in critical markets because of

more criticism in consumer reports — a key insight shown in our numerical exercise in Figure 4 and

in Prediction 1. The second reason is the behavior incentives induced by the noisier certification

requirements under the old regime. We will elaborate on this point in Section 5.2, where we analyze

sellers’ change in behavior. But the key idea is that in the presence of consumer reports in the

24

certification requirements, on the one hand, sellers that intend to be badged need to overshoot

on quality metrics that they can control in order to overcome consumer criticalness (Effect 1 in

Prediction 2) and to mitigate the uncertainty in consumer reports (Effect 3 in Prediction 2). To

the extent that seller size is a proxy for seller quality, this explains why the black curve (simulated

eTRS at Month -5) is higher for large sellers in critical markets than for large sellers in non-critical

markets. On the other hand, sellers with higher effort costs may be discouraged from exerting effort

because of the noise in certification (Effect 2 in Prediction 2); therefore, the black curve is slightly

lower for the smallest (a proxy for lower-quality) sellers in critical markets.

Third, the difference between the “before” and simulated shares of certified sellers is less negative

for small sellers in both non-critical and critical markets. According to our numerical simulation in

Section 3, this can happen if both types of markets are to the left of the certification threshold (the

red line at 2% in Figure 4).

10

The reason is that small sellers were disproportionately affected by

random noise because of their small number of orders, and a reduction in this noise immediately

helps them gain the eTRS badge.

Fourth, the difference between the “after” and simulated shares of certified sellers, which roughly

represents seller behavioral change (up to some measurement error in simulation and our normal-

ization of simulated shares), suggests more improvement among larger sellers. One can think of

several reasons for this result: first, larger sellers may expect more immediate benefits from their

current behavioral change, because they are subject to a shorter look-back window in the eTRS

algorithm; second, since the eTRS status brings a positive premium to each transaction, sellers

that predict a larger volume of orders should expect more benefits in total; third, larger sellers may

enjoy a greater economy of scale in their effort improvement if such improvement entails some fixed

costs.

Fifth, quality improvement is smaller among sellers that operate in critical markets. This result

is due to the behavior incentive induced by the new regime, as we elaborate in the next subsection.

Lastly, we observe homogenization in the share of certification across seller sizes and across

markets. Specifically, if we ignore the smallest sellers below the 50th percentile, the “before” curve

has a positive slope everywhere from the 50th to 100th percentiles, but the post-curve is almost flat

between the 50th and 90th percentiles and slopes up only beyond the 90th percentile. This suggests

10

This is certainly plausible because many previous papers have shown that negative feedback is rare on eBay

(around 1% among all feedback ratings). Also, sellers can contact eBay’s customer service to remove wrong negative

feedback, such as a negative rating indicating an item was not received by the buyer when tracking information shows

the item was successfully delivered.

25

that the new regime homogenizes the share of certification among sellers in the middle range of the

seller size distribution.

11

Next, to see homogenization in the share of certification across markets,

Figure 7 suggests that fewer sellers are certified in critical markets before the regime change, but

the simulated shares are much more similar across the two types of markets, and the “after” shares

of certification are essentially identical except for the largest sellers. This suggests that the cross-

market homogenization is driven by both algorithm selection and seller behavioral change, in line

with Prediction 3. More analyses on this result are presented in Section 5.3.

Now, we summarize the above findings on heterogeneity in algorithmic selection via the following

seller-level regression:

Y

i

= β

0

+ β

1

∗ Large

i

+ β

2

∗ AvgCriticalness

i

+ β

3

∗ Large

i

∗ AvgCriticalness

i

+

i

, (1)

where i denotes a seller, Y

i

is a categorical variable describing the difference between the seller’s

simulated and actual certification status in Month -5: it is equal to 1 if a non-certified seller gains a

simulated eTRS because of the new eTRS algorithm, -1 if a certified seller loses the eTRS in simu-

lation, and 0 if the simulation does not generate any status change. Moreover, Large

i

is a dummy

indicating whether seller i had at least 400 transactions in Months -8 to -6; AvgCriticalness

i

indi-

cates the degree to which seller i operates in critical markets: it is constructed based on consumer

criticalness in each market that seller i operated in during Months -8 to -6, weighted by the seller’s

sales share in that market in Months -8 to -6. Note that equation 1 is at the seller level because

a seller’s eTRS status is evaluated at the seller level (not product or listing level). Since we focus

on the selection effect at Month -5, it is based on a cross-section of 380,978 sellers, following the

sample construction procedure described in Section 4.1.

Results are reported in Table 2, and we do not report the constant term, to comply with eBay’s

data policy. From column (1), we see that on average, the net selection effect is 0.149 more negative

for large sellers, and 0.138 more positive for sellers in critical markets (relative to the scale of the

dependent variable from -1 to 1). The two coefficients correspond to the second and third points

when discussing Figure 7. In column (2), we further include an interaction of large seller and critical

markets. The positive coefficient on this interaction suggests an extra positive selection for large

11

The curvature on the first half of these curves may be an artifact of the eTRS algorithm: because sellers below the

50th percentile sold fewer than 10 orders in Months -6 and -4, many of them may not meet the minimum threshold for

eTRS inclusion (i.e., 100 orders and $1000 sales in the past 12 months). The part of the curve for these smaller sellers

tends to slope up, probably because those in a higher percentile have a greater chance of meeting the eTRS threshold

on minimum sales. This mechanical effect exists in both the old and new regimes, as the minimum threshold does

not change.

26

Table 2: Seller Selection

(1) (2)

net selection net selection

Large -0.077*** -0.091***

(0.002) (0.003)

Avg. Criticalness in operation markets 0.152*** 0.149***

(0.001) (0.001)

Large* Avg. Criticalness in operation markets 0.030***

(0.005)

Observations 424,607 424,607

R-squared 0.030 0.030

Notes: Seller-level cross-sectional regressions. Outcome is the difference between a seller’s simulated and actual

certification status on the policy announcement date. Large is a dummy for having sold at least 400 transactions

in the three months before the policy announcement. Critical is a sales-weighted measure of rating criticalness

in the markets that a seller operates in. We also control for the constant term in the regression. Standard

errors in parentheses. *** p<0.01, ** p<0.05, * p<0.1.

sellers, relative to small sellers, in critical markets. This positive coefficient is consistent with the

second point on behavior incentives in the discussion of Figure 7.

5.2 Changes in Seller Effort

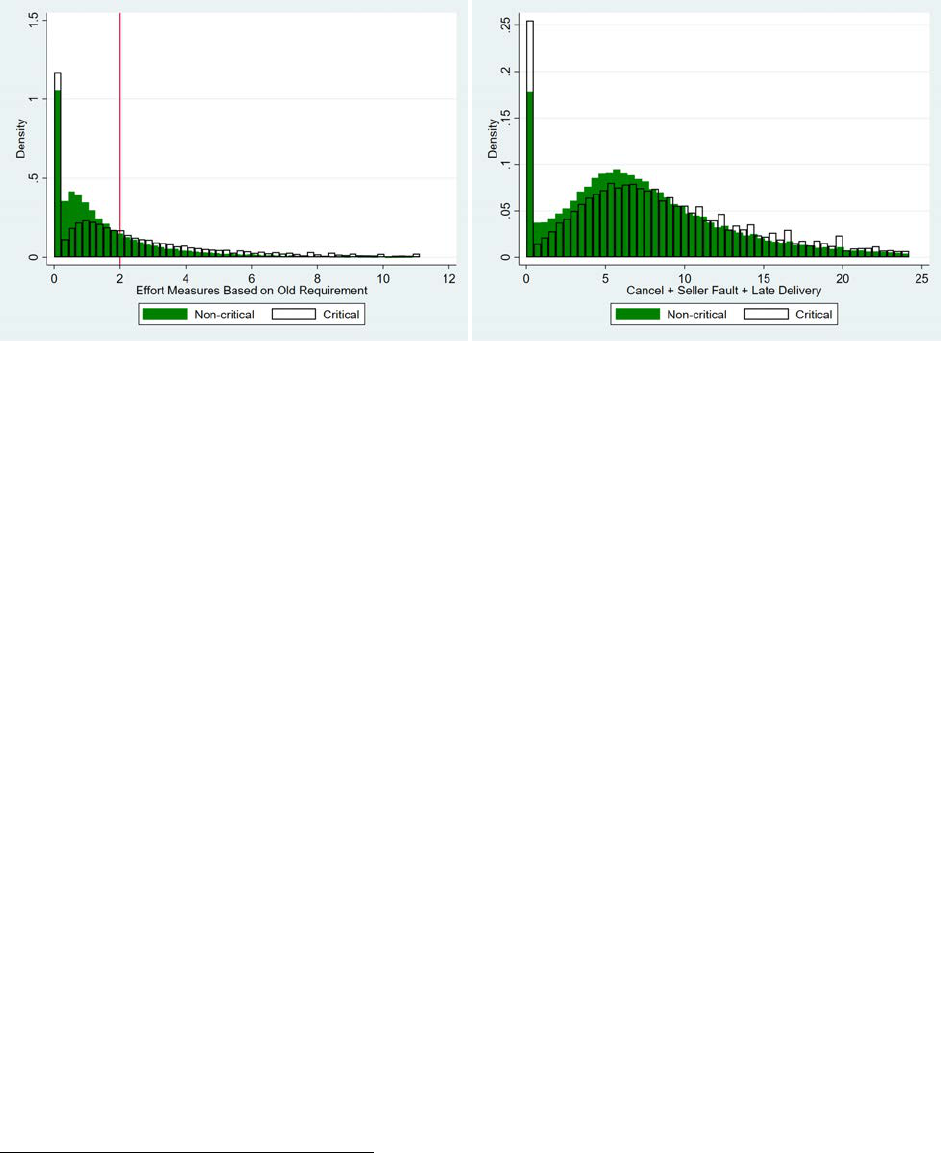

5.2.1 Old Regime Induces Bimodal Effort

We start by illustrating the behavior incentive induced by the old regime, which is based on both

output- and input-based measures. Facing negative µ

R

in critical markets, sellers need to overshoot

on the input-based measures, to overcome the more critical consumer reports (Prediction 2, Effect

1). In the meantime, critical markets may also have a higher σ

R

if the random noise

R

is binary

as in our numerical simulation in Figure 4. In that case, sellers with sufficiently high effort costs

may give up on exerting effort (Prediction 2, Effect 2). Therefore, if we compare the distribution

of seller quality in critical versus non-critical markets before the policy announcement, we should

see that it has fatter tails in critical markets.

We test this hypothesis in Figure 8. In the left graph, the effort measure is based on the

old certification requirements, and is calculated based on the “before” data. The vertical line at

2% indicates the certification threshold under the old regime. The quality distribution in critical

markets (represented by hollow bars) indeed has fatter tails than that in non-critical markets

(represented by solid bars). Note that because we proxy effort by the old requirements, which

contain consumer reports, there will be larger (negative) noise in this proxy in critical markets;

27

Figure 8: Quality Distribution of Sellers in Different Markets

Notes: The effort measure is based on the old certification requirements in the left graph, and based on

the new certification requirements in the right graph. Both effort measures are calculated using data from

the “before”period. Markets are divided into non-critical and critical based on a median split. Vertical line

indicates the certification threshold under the old regime.

therefore, the distribution of true effort could have even fatter tails in critical markets. To see this,

in the right graph, we use another effort measure based on new certification requirements, again

using the “before” data.

12

Here we see a clearer pattern of fatter tails in the distribution of seller

quality in critical markets. Both graphs are consistent with the behavior incentive induced by the

old certification requirements, which are in turn consistent with the shape of the black curve on

the selection effect described in Figure 7.

13

5.2.2 New Regime Induces Threshold Effect

To examine the behavior incentive induced by the new regime, we start by analyzing how seller

behavior changes over time. In Figure 9, each line corresponds to sellers’ simulated badge status

in a month. The simulation is based on seller performance evaluated in that month against the

new certification regime. We interpret the vertical distances between lines as changes in seller

effort as measured by metrics in the new eTRS requirements. As before, the evaluation is based

on transactions in the past three months if a seller has at least 400 transactions in that period, or

the past twelve months if otherwise. To preserve eBay’s data confidentiality, the values in Figure

9 are normalized by one constant so that they can be compared across time and across markets.

14

12

We do not draw a vertical line here because there are two thresholds for seller defects and late delivery rate.

13

Note that another explanation for the fatter tails is survival bias, which we discuss in Appendix A.

14

As mentioned in footnote 9, we do not observe revisions in consumer reports in our dataset; therefore, the

simulation is based on the initial consumer reports. This can explain the difference in the shape of the curve

28

Figure 9: Policy Effect on Seller Performance by Seller Size and Rating Criticalness

Notes: A seller’s eTRS status in a month is simulated based on the new requirements. Rating criticalness

is defined as the share of transactions that are considered defect by the old system out of all transactions

that are considered good by the new system. Markets are divided into non-critical and critical based on a

median split. Vertical line indicates the percentile cutoff for large sellers. Simulated shares in the two types

of markets are normalized by a constant.

A few patterns are worth noting in Figure 9. First, all sellers except the very small ones increase

their effort, as indicated by an upward shift of the curve over time. Very small sellers do not increase

their efforts, probably because they are too small to be eligible for certification. Second, the sellers

that improved their efforts improved the most in the month right after the policy announcement

(between Month -5 and Month -4).

Third, we see that effort improvement is smaller in critical markets than in non-critical markets.

This result may seem prima facie counterintuitive, because classical agent theory would predict a

higher effort incentive when the observability of effort increases (Prediction 2, Effect 2). However,

this argument ignores the binary nature of certification: once a seller has reached the certification

threshold, there is no benefit of exerting additional effort. This gives rise to the threshold effect,