TRANSFER PRICING

- to be AWARE or BEWARE ?

E-Venue:

The Institute of Cost Accountants of India – Webinar

( 10.01.2018 )

By

CMA Chiranjib Das, FCMA, ACA, M.Com

Presentation Plan

(1) Transfer Pricing – an Overview

(2) Transfer Pricing Laws

(a) – Under Direct Taxation

(i) Specified Domestic Transactions

(ii) International Transactions

(b) – Under Indirect Taxation

(i) as per Customs

(ii) as per Pre-GST Laws

(iii) as per GST Laws

(3) CMAs – role under Transfer Pricing

3

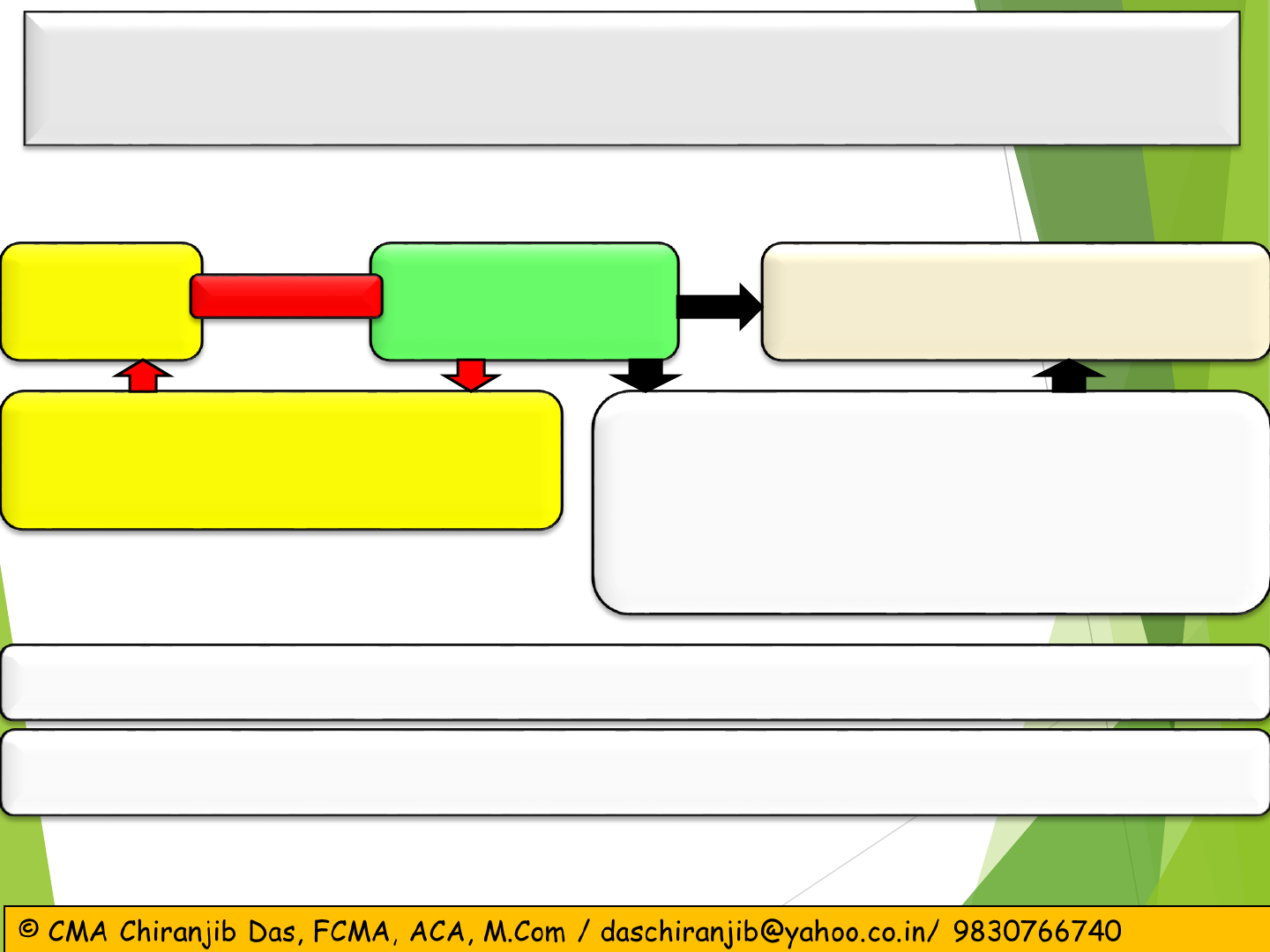

Transfer Pricing - at a glance

Transfer Pricing

Indirect

Taxation

Pre-GST Laws

Central

Taxes

Customs

Central Excise

Service Tax

GST Laws

Sec.15 of the CGST Act

- Valuation Rules

Direct

Taxation

Specified

Domestic

Transactions

International

Transactions

TRANSFER PRICING – under Direct Taxation

Definition:

as per OECD

“Prices at which an enterprise transfers physical goods and

intangibles or provides services to associated enterprises”

Definition:

as per Sec.92 of the Income Tax Act,1961

“Any income arising from an international transaction shall be

computed having regard to the arm's length price”

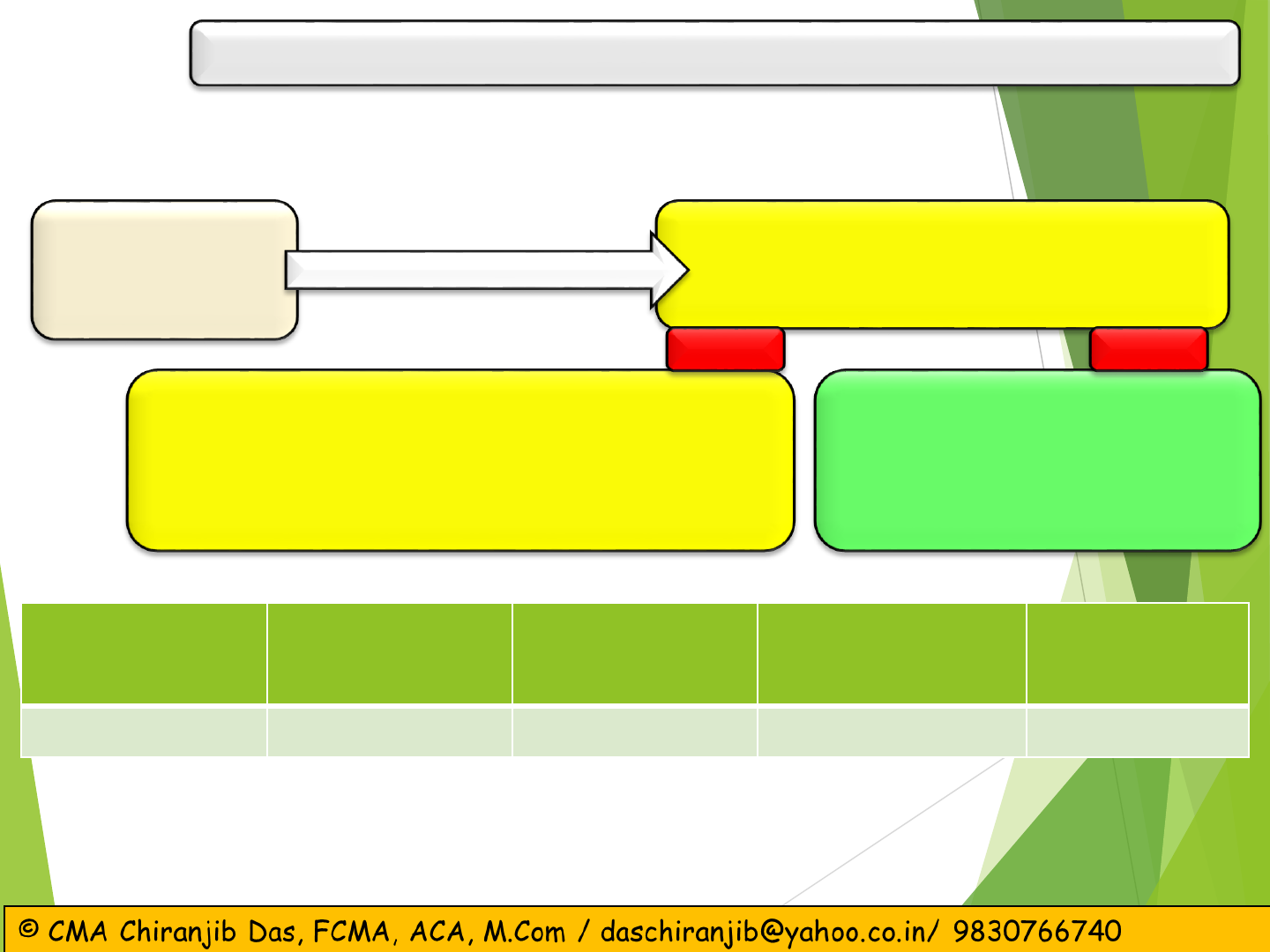

TRANSFER PRICING – International Transactions

Key Elements

Determination of Arm’s Length Price (ALP) as per Sec.92C of IT Act,1961

Associated Enterprises (AE)

International Transaction

Permanent Establishment (PE)

Determination of Arm’s Length Price as per Sec.92C(1) of the Income

Tax Act,1961

(framed as per the OECD Guidelines)

TRANSACTION BASED

METHODS

COMPARABLE UNCONTROLLED PRICE METHOD

(CUP)

RESALE PRICE METHOD (RPM)

COST PLUS METHOD (CPM)

PROFIT BASED METHODS

PROFIT SPLIT METHOD (PSM)

TRANSACTION NET MARGIN METHOD (TNMM)

Is there an

International

transaction

At least

One (1) AE is

Non-Resident

Are

International

Transactions at

ALP?

Between the

AE’s

Transfer pricing regulations not

applicable to the transactions. Hence,

ALP is not to be determined

Yes

Yes

Yes

No

No

No

No

Adjustment is made to the Total

Income

Comply Transfer Pricing

Regulations

Yes

Yes

Stop Assessment Proceedings

Is there a

transaction ?

No

TRANSFER

PRICING –

International

Transactions

Relevant factors Explanation

(a)

The nature and class

of

international

transactions

e

.g., if a product is sold in controlled transactions is identified to have a close similarity

to

the

product in uncontrolled transactions, the CUP method may be useful. Similarly, if

a

transaction

concerns a retailer or distributor, the resale price method would

be

appropriate

.

(b)Assets

employed or risks assumed

The

class or classes of associated enterprises entering into the transaction and

the

functions

performed by them taking into account assets employed or to be employed

and

risk

assumed by such enterprises.

(c)Availability,

coverage and

reliability

of

data necessary for application

of

the

method

e

.g., if the comparable data is not available in the public domain, in respect of

comparable

prices

of uncontrolled transactions, the selection can be made from other methods.

(d)Degree

of comparability

The

degree of comparability existing between the international transaction and

the

uncontrolled

transaction and between the enterprises entering into such transactions.

(e)Reliability

and accuracy

for

adjustments

The

extent to which reliable and accurate adjustments can be made to account

for

differences,

if any, between the international transaction and the

comparable

uncontrolled

transaction or between the enterprises entering into such transactions.

Selection of Most Appropriate Method (MAM)

Computation of Arm’s length Price (ALP)

Availability, coverage and reliability of data

Comparability between controlled and uncontrolled

transactions

Possibility to make reliable and accurate adjustments

Issues when value added services are provided

Arm’s length Price (ALP)

- Comparability based on FAR Analysis

F = Functions

A = Assets

R = Risk Analysis

Why Arm’s Length Pricing?

Total

Income as disclosed by an Assessee

XXX

Add

: Understatement of profit due to overstatement of purchase price

Add

: Understatement of profit due to understatement of selling price

XXX

XXX

Total

Income after Assessment

XXX

The basic object of determining Arm’s Length Price is to find out whether any addition

to income is warranted or not, if the following situations arises:

•Selling Price of the Goods < Arm’s Length Price

•Purchase Price > Arm’s Length Price

Transfer Pricing :- Compliance Regulations

Accountants Report Documentation

Sec. 93E read with Rule 10E

Form 3CEB is to be filed at the

time of submission of Return of

Income

Sec.92D read with Rule 10D

•Maintain relevant prescribed

documents.

•Submit with the tax authorities

during the time of TP AUDIT

COMPARABLE UNCONTROLLED PRICE METHOD

(CUP)

Case Study:

(i) J Inc.(Korea) & CD Ltd (India) are Associated Enterprises ; (ii) CD

Ltd. supplied 2,50,000 cell phones to J Inc. @ Rs.3,000 per unit ( on

FOB basis ) and 35,000 units to A Ltd. Nepal @ Rs.5,800 each (on CIF

basis); (iii) Freight & Insurance paid by J Inc. @ Rs.700 per unit; (iv)

Sale to A Ltd.(Nepal) under two year warranty but no such warranty to

J Inc. Korea, estimated cost of each warranty Rs.500; (v) Quantity

discount offered to J Inc. Rs.200 per unit

Cont…

J Inc. Korea

CD Ltd. India

(Mfg. of Cell Phones)

2,50,000 UNITS SOLD @ Rs.3,000 each

A.E.

A Ltd. Nepal

( Un related Buyer)

35,000 UNITS SOLD @ Rs.5,800 each

Less: Adjustments for:

Freight Rs. 700

Warranty Rs. 500

Qty.Discount Rs. 200

ARM’S LENGTH PRICE Rs. 4,400

Difference in Price = Excess of ALP over Sale Price to A.E.= Rs.(4,400-3,000) =Rs.1,400 per unit

Undisclosed Income = Units Sold to A.E. x Difference in Price

= 2,50,000 units x Rs.1,400 per unit = Rs.35 crores

COMPARABLE UNCONTROLLED PRICE METHOD

(CUP)

RESALE PRICE METHOD (RPM)

Case Study:

(i) Mega Inc.(France) & R Ltd (India) are AEs; (ii) R Ltd. imports 3,000

compressors from Mega Inc.@ Rs.7,500 per unit and sold to Pleasure

Cooling Solutions @ Rs.11,000 p.u. (iii) R Ltd. also imported similar

products from Cold Inc. Poland and sold outside @ 20% G.P. on sales.

(iv) Quantity Discount : Mega Inc.(France) @ Rs.1,500 per unit; Cold

Inc. @ Rs.500 p.u. (v) Freight Charges paid by R Ltd -imports from

:Mega Inc. Rs. 1,200 p.u.; Cold Inc. Rs.200 p.u.

Cont…

RESALE PRICE METHOD (RPM)

Mega Inc. France

R Ltd. India

(Mnf. Of Compressor)

Cold Inc. Poland

Sale Price to Pleasure Cooling @ Rs.11,000

Less: Gross Profit @ 20% of Rs.11,000 Rs. 2,200

Less: Savings in Freight Cost (Rs.1,200 – Rs.200) Rs. 1,000

Less: Diff.in Qty.Disc (Rs.1,500 – Rs.500) Rs. 1,000

ARM’S LENGTH PRICE Rs. 6,800

3,000 units of compressor imported @ Rs.7,500 per unit

(paid by R Ltd)

Price Comparable to ALP = Rs.7,500 per unit

Foreign Supplier of Compressors to R Ltd.

Difference in Price = Excess of Price paid to A.E. & ALP = Rs.(7,500 -6,800) =Rs.700 per unit

Undisclosed Income = Units Purchased from A.E. x Difference in Price

= 3,000 units x Rs.700 per unit = Rs.21 lakhs

COST PLUS METHOD (CPM)

Case Study

(i) Branco Inc.(UK) & C Ltd. (India), a software development company, are AEs;

(ii) C Ltd. spent 2,400 man hours in Branco Inc. and billed @ Rs.1,300 per man-hr

, actual cost incurred Rs.20 lakhs; (iii) C Ltd. also provided service to Harsha Ltd

@ Rs.2,700 per man-hr and made a gross profit of 60% ; (iv) Branch Inc. provides

technical support to C Ltd., valued at 8% of normal gross profit (v) Quantity

Discount to Branco Inc. @ 14% of normal gross profit; (vi) C Ltd. also offered 90

days credit to Branco Inc. which is equal to 2% of normal gross profits.

Cont…

COST PLUS METHOD (CPM)

Branco Inc. ( UK)

C Ltd. India

(Software Developer)

A.E.

Harsha Ltd

( Un-related Buyer)

Service provided for 2,400 man hours @ Rs.1,300

Actual Job Cost incurred by C Ltd Rs.20 lakhs

Rate per Man hr @Rs.2,700

Gross Margin (%) 60.00

Less: Cost not to be taken

Tech. Know How (i) 4.80

Qty.disc. (ii) 8.40

Add: Gain to be further added back:

Credit 1.20

Adjusted Gross Profit Margin (%) 48.00

COST TAKEN IN ACCOUNT(%) [in terms of Harsha Ltd]

(i) Tech. Knowhow- 8% on 60%= 4.8%

(ii) Qty.disc- 14% on 60%=8.4%

(iii) Gain included 2% on 60%=1.2%

COMPUTATION

OF INCREASE IN TOTAL INCOME OF CTL ( for services rendered to

Branco

Inc

. (UK))

%

Amount (Rs.)

Cost

Adjusted

Gross Profit Margin

Arm’s

Length Price ( Billed value at arms length [ cost/(100-arms length mark)]= Rs.20,00,000

/

(

100% -48%)

Less

: Actual Billing to Branch Inc.

52.00

48.00

100.00

20,00,000

18,46,154

38,46,154

31,20,000

Increase

in Total Income of Branco Inc.

7,26,154

PROFIT SPLIT METHOD (PSM)

Case Study:

(i) NBR Inc.(Canada) received order from Healthy Recovery Group of Hospitals (UK) for

rendering of specialised services. Order value Euro 3,00,000; (ii) NBR Inc. joined hands

with its subsidiary PC Inc.(USA) and B Ltd.(India); (iii) PC Inc. holds 30% shares in B Ltd;

(iv) NBR Inc. paid to: PC Inc Euro 90,000 and B Ltd. Euro 1,00,000; (v) Profit earned Euro

1,00,000 (vi) Total Cost of B Ltd for execution of its work in the above contract Euro

80,000; (vii) Relative contribution of NBR, PCI & B Ltd. are 30%, 30% and 40%

respectively.

Cont…

PROFIT SPLIT METHOD (PSM)

PC Inc., USA [ Cont:30%]

Received from NBR Inc. = Euro 90,000

B Ltd.India [ Cont:40%]

Received from NBR Inc:

Euro 1,00,000

NBR Inc.,Canada

Cont: 30%

Healthy

Recovery

Hospitals, UK

Order for 3 lac Euro

Total Cost of B

Ltd

Share of Profit

from NBR Inc.

Canada

Arm’s Length

Price

Receipt of B L td.

from Canada

Undisclosed

Income

80,000 40,000 1,20,000 1,00,000 20,000

A.E. A.E.

TRANSACTION NET MARGIN METHOD(TNMM)

Case Study:

(i) Fox Solutions Inc. (USA) sells laser printer cartridge drum to its Indian subsidiary

“Quality Printing Ltd” @ $ 20 per drum ; (ii) Fox Solutions has other takers in India for @ $

30 per drum (iii) Fox Solutions Inc. supplied 12,000 of such items to Quality Printing Ltd.

(iv) Taxable Income of “Quality Printing Ltd” is Rs.45,00,000 (v) $ = Rs. 45

Cont…

Fox Solutions Inc. (USA) ( seller of laser printer cartridge drums)

Quality Printing Ltd.

Profit Reduced Due to Excess Cost charged in Profit & Loss Account in

Comparable Transaction

=Units Purchased x Difference in Price x Conversion Rate

=12,000 units x $(40-30) x Rs.45= Rs.54 lakhs

Other Un-related Buyers in India

Purchased from Fox Solutions Inc.

@ $ 30 per unit

Quality Printing Ltd (India)

Purchased from Fox Solutions Inc.

12,000 units @ $ 40

TRANSACTION NET MARGIN METHOD(TNMM)

A.E.

Assessed Total Income = Income declared + Increase in income after adjustment of ALP

= Rs.(45 + 54) lakhs = Rs.99 lakhs.

Under Pre-GST regime Vs. Transfer Pricing

Pre

-GST Indirect Tax Regime Vs. Transfer Pricing

( Under Income Tax)

Transaction

Customs/

Service

Tax Valuation

Transfer Pricing

(Income Tax)

Import of Goods

Yes

Yes

Import of

Services

No

Yes

Excise / Service Tax

Valuation

Domestic goods

Yes

Yes (restricted to profit linked

transactions)

Domestic

Services

No

Yes (restricted

to profit linked

transactions)

TRANSFER PRICING – under Indirect Taxation

GST Vs. Transfer Pricing regime

GST Vs.

Transfer Pricing ( Under Income Tax)

Transactions

Customs

Valuation

(BCD)

GST

Valuation

(IGST)

Transfer Pricing

(Income Tax)

Import of Goods

Yes

Yes

Yes

Import of

Services

No

yes

Yes

Domestic Goods

Yes

Yes

Yes (restricted to profit

linked

transactions)

Domestic

Services

No

Yes

Yes (restricted to profit

linked transactions)

GST and Transfer Pricing – Expectation of Taxpayers

Harmonisation –

GST framework governing arms’ length standard would

need to be aligned with the Income Tax Provisions

Methodologies to be adopted

Nature of documentation to be maintained

Process to identify comparable data

Reliance to be placed on the comparable data

Section 15 of the CGST Act, 2017 – Valuation

Read with Valuation Rules

( as prescribed in Rules 27 – 35 of the CGST Rules, 2017)

APA (Advanced Pricing Agreement) & Transfer Pricing

Is the TP Study or an APA alone viewed by the

Customs Authorities as sufficient to support the use

of the transaction value method of customs valuation?

- APA/ TP may contain useful information for

supporting the transaction value method.

Transfer Pricing – Issues & Concerns

Is it possible to get the customs and tax authorities

agree on the same price

( = the price paid or payable, exclusive of freight,

insurance and other additions to the price) for

corporate tax and customs duties purposes ?

Transfer Pricing – Issues & Concerns

In practice, what evidence do the customs authorities

require to substantiate that the related party price is

acceptable from a customs perspective ? Is it

recommended to conduct a test and/ or analysis under

the customs rules ( which would be a separate test/

analysis from the transfer pricing analysis) ?

Customs Valuation – Post importation changes & its

impact on Transfer Pricing

Are importers required to report to Customs

Authorities on any post-importation change in the

reported customs value (e.g. due to a retroactive

transfer pricing adjustment) that increases the price

paid / payable by the importer ?

If yes, is there an exception to report when the duty

rate is zero ?

If no, is there still a risk of fines or penalties ?

Customs Valuation – Post importation changes & its

impact on Transfer Pricing

Are importers required to report to Customs

Authorities on any post-importation change in the

reported customs value (e.g. due to a retroactive

transfer pricing adjustment) that increases/

decreases the price paid / payable by the importer ?

If yes, is there an exception to report when the duty

rate is zero ?

If no, is there still a risk of fines or penalties ?

Inventory Valuation & Transfer Pricing

Does the income tax laws or practices in the country

require (for corporate income tax purposes)

consistency between a tax payer’s inventory basis

( cost of goods sold) and values reported for customs

purposes ?

If such amounts are not consistent, what are the

potential risks ?

Anti Dumping… a quick look….

Anti Dumping takes its reference and powers from Customs Laws

It is similar to determining the Arm’s Length Price which is applied in case

of

both International and Specified Domestic Transactions

With the Assessed Value/ Value as determined, the difference over the

normal

value is considered to be the quantum of dumping

on the quantum of dumping - duty of customs is imposed under the title ‘Anti

-

dumping’

This provides a relief to the domestic industry from being affected by injury

due

to price of imports which are at a price lower than the normal value of

identical

/like goods in the domestic market

Trade Remedy Measures

– Relief to Domestic Industries

Relief to Domestic

Industries

Trade Remedy Measures (Imposing

duties of customs )

Anti-dumping Duty Countervailing Duty Safeguard Duty

Price Undertakings

Comparative Analysis – AD/CD/SD

Anti Dumping Countervailing Duty Safeguard Duty

Product

specific

and

Exporter

Specific Duty

Product

specific

and

Country

specific duty

Product

specific

duty

imposed

against

imports

coming

from all

sources

irrespective

of

exporter

and

country of origin

Continue

forever as long

as

dumping

continues

Continue

forever as long

as

subsidy

continues

Continue

only for

a

temporary

period

not

exceeding

10 years

There

is an alleged foul

play

on

the part of the exporter

There

is an alleged foul

play

on

the part of

the

exporting

country

No

alleged foul play on

the

part

of exporter

or

exporting

country in case

of

safeguards

duty

Cost Accounting Standards – relevance in AD Study

Anti-dumping Application

Proforma

Reference to Para prescribed under Cost Audit

Report Rules,2011

Reference to relevant Cost

Accounting Standards

Format A

- Statement of Raw

Materials and Packing Materials

Consumption and Reconciliation

Para 5 :

Abridged Cost

Statement

Item No.1 & 2

Raw Material Consumption and

Process Materials

CAS 6

– Material Cost

Item No.16 and 23

– Primary

Packing Cost Material and

Secondary Packing Cost

CAS 9

– Packing Material Cost

Format B

– Statement of Raw

Material Consumption

Para 5 : Abridged Cost Statement

– Item Nos.1 & 2

CAS

– 6 – Material Cost

Format CI

– Statement of Cost of

Production

(to be certified by a Cost

Accountant in Practice)

Para 5 : Abridged Cost Statement

– Item No. 21 –

Cost of Production

CAS 2

– Capacity Determination

CAS 6

– Material Cost

CAS 7

– Employee Cost

CAS 8

– Cost of Utilities

CAS 9

– Packing Material Cost

CAS 10

– Direct Expenses

CAS 12

– Repairs & Maintenance

Format CII

– Allocation and

Apportionment of Expenditure

Para 2 : Cost Accounting Policy

CAS 1

– Classification of Cost

CAS 2

– Capacity Determination

CAS 3

- Overheads

Format D

– Statement of

Consumption of Utilities

Para 5: Abridged Cost Statement

– Item No.3 –

Utilities

CAS 8

– Cost of Utilities

Installed Capacity

1,00,000 units

Production in Installed

65,000 units

Capacity Utilization (%)

65%

Production in Investigation Period

56,000 units

Capacity Utilisation in Investigation period

56%

Sales (quantity)

61,000 units

51,000 units

Particulars

Previous Accounting Year Investigating Period

Qty Rate

(Rs.)

Value

(Rs.)

Cost

per unit

(Rs.)

Qty Rate

(Rs.)

Value

(Rs.)

Cost

per unit

(Rs.)

Manufacturing Expenses:

Raw Materials (specify the major raw

materials) (MT)

Utilities

Depreciation

Others (specify nature of expenditure)

10,000

100.00

10,00,000

2,00,000

1,95,000

15.38

3.08

3.00

8,000

120.00

9,60,000

1,90,000

1,75,000

17.14

3.39

3.13

Administrative Expenses

Variable

Fixed

1,30,000

78,000

2.00

1.20

1,12,000

78,000

2.00

1.39

Selling & Distribution Expenses

Variable

Fixed

61,000

40,000

1.00

0.66

56,000

40,000

1.00

0.71

Financial Expenses

Variable

Fixed

1,30,000

21,000

0.70

0.32

35,700

21,000

0.70

0.38

Less: Miscellaneous Income

( from product concerned)

–

Sale of Scrap

raw materials

(25,000)

(20,000)

Total Cost to make and sell

18,34,000

28.22

16,47,700

29.42

Selling Price

35.00

32.00

Profit/Loss

6.78

2.58

Example: FORMAT “CI” - STATEMENT OF COST OF PRODUCTION - Name of the Company: XYZ Limited

37

Role of CMAs in Goods and Services Tax (GST) in India

Role of CMAs in GST – as per Draft Report of Dr. J.P Verma Committee in 2002, CMAs were recommended & recognised to conduct

Transer Pricing Audits

Towards Taxable Persons / Business Entities

- Advising in maintenance of Proper

Records & documents leading to

support TP adjudications

- Determination of Price/ Value for the

purpose of Transfer between related

parties

- Preventing Litigation

- Defending Litigation

Government

Advisory in Advance

Pricing/ Valuation /

Anti-Profiteering

Facilitating in TP

Adjudication & TP

Audits – to serve the

National Interest

Valuation : Anti-Profiteering under GST & Transfer

Pricing

- Nexus between Anti-profiteering under GST

& Valuations involving Transfer Pricing