Basics of Transfer

Pricing

Amith A Prabhu

October 14, 2016

News on TP : Year 2015

Source Date Title

Economic Times May 21, 2015 CBDT is looking to settle 120 TP disputes – Signing

of APA’s

Economic Times Feb 28, 2015 SDT threshold raised from Rs. 50mn to Rs. 200mn

Business Standard May 21, 2015 Release of draft norms for “range concept”

Economic Times Jan 26, 2015 APAs to draw investments from major

US companies

Times of India Jan 24, 2015 India is ready to commit to sign bilateral advance-

pricing agreements with US companies

Business Standard Mar 16, 2015 Finance Ministry notifies the rollback rules for

TP cases

TP is clearly a focus area of Indian Tax Department!

Basics of Transfer Pricing

Basics of Transfer Pricing

Other highlights…

• Constitution of special benches for TP cases in major cities.

• Independent specialized bench set up for disposing DRP appeals.

• Introduction of Roll back mechanism in APA.

• Aggressive TP audits (assessments).

• Introduction of guidelines for application of range concept and use of

multiple year data.

• Increase in Specified Domestic Transactions (‘SDT’) threshold from

INR 5CR to INR 20 CR.

• India ranked #1 on TP Week’s Top 10 Toughest Tax Authorities for TP.

• India contributes to more than 70% of the TP global disputes

(in numbers).

With so much happening in India important to understand why TP!

Basics of Transfer Pricing

Why TPWhy TP

• More than 60% of the world trade takes place within

multinational enterprises leading to complex issues emerging from

transactions entered between enterprises belonging to same Group;

• General tendency to control profits and transfer the same to low tax

heavens Need for regulation to monitor the possible erosion of

tax base;

• Introduction of legislation felt essential by Governments for protection

of their respective tax base;

• OECD issued TP guidelines for MNEs and Tax Administrations in 1979

(amended in 1995 and then in 2010);

• Base Erosion and Profit Shifting Action Plans introduced

in October 2015

• Need for ‘arm’s length’ pricing principle.

Basics of Transfer Pricing

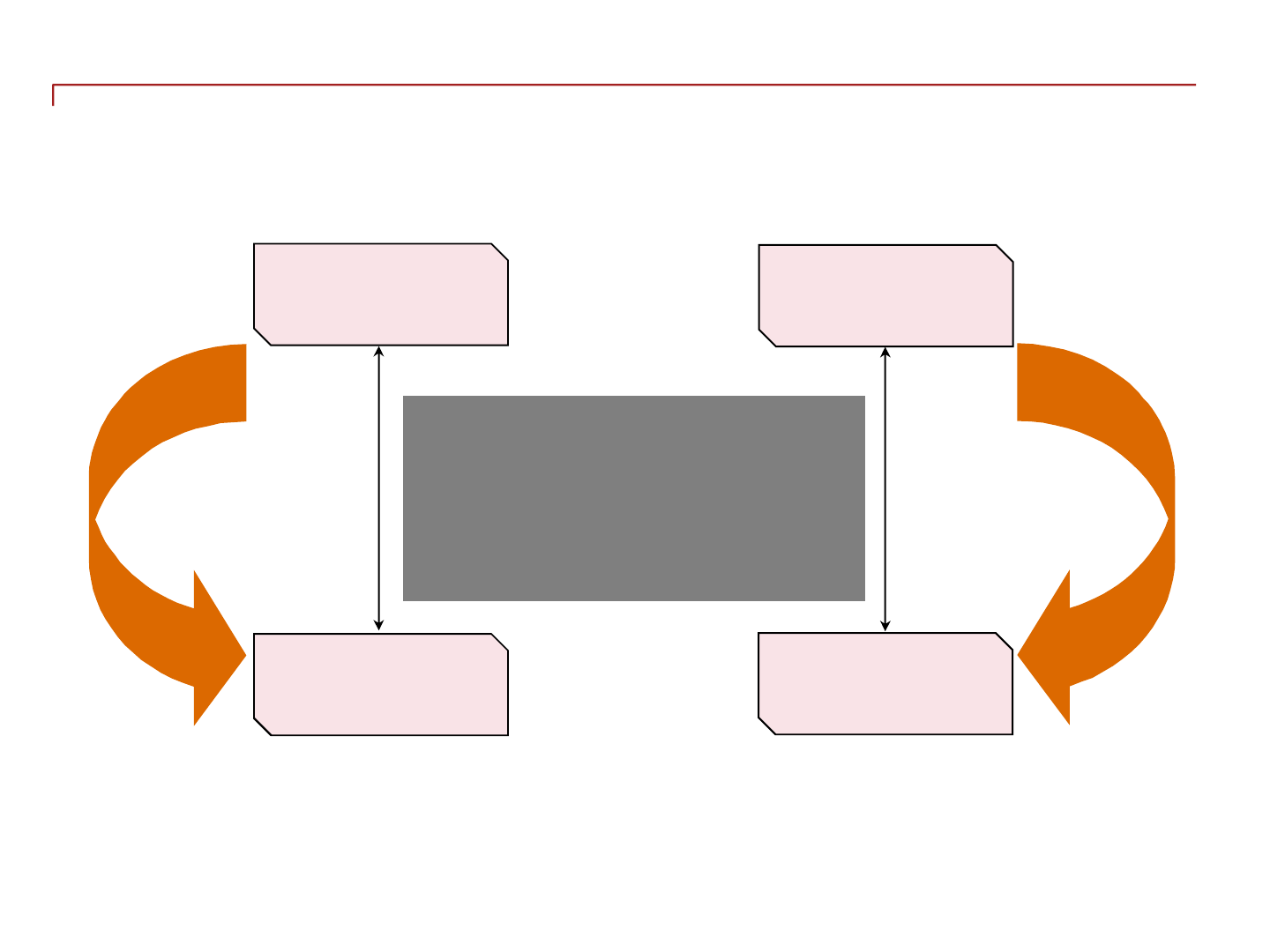

Arm’s length principleArm’s length principle

International transactions

• goods

• services

• intangibles

• loans

Independent

entity

Resident

Associated

enterprise

Resident

Transfer

price

Arm’s length

price

Slide 6

Basics of Transfer Pricing

India

Need for Transfer Pricing Legislation

US

India

US

Singapore

Selling Price 120

Purchase Cost 100

20

Selling Price 100

Total Cost 50

50

Selling Price 120

Purchase Cost 100

20

Selling Price 100

Purchase Cost 60

40

Selling Price 60

Total Cost 50

10

Slide 7

Basics of Transfer Pricing

What do you think about this situation??What do you think about this situation??

Multinational

Country A Country B

Assets

Functions

Risks

Profits

$$ $$$$$$$$$$

Slide 8

Basics of Transfer Pricing

Transfer Pricing – The Genesis

Slide 9

Transfer pricing

refers to the pricing of

cross-border

transactions between

two associated

entities.

When two related

entities enter into any

cross-border

transaction, the price at

which they undertake

the transaction is

‘transfer price’.

Due to the

special relationship

between related

companies, the transfer

price may be different

than the price that

would have been agreed

between unrelated

companies.

Price between

unrelated parties in

uncontrolled

conditions is known

as the “arm’s length”

price (ALP).

Basics of Transfer Pricing

Indian TP Regulations …

• Erstwhile Section 92 of the Income-tax Act, 1961 (‘the Act’) :

- was general in nature and had a limited scope

- did not allow adjustment to income of non-residents

- referred to ‘close connection’ which was undefined and vague

- had provisions for adjustment of profits and NOT PRICES

- the relevant rule 11 for estimating profit was not scientific

- did not apply to individual transactions like payment of royalty

- no rules prescribing documentation requirements were in existence

• India introduced Chapter X in the Income-tax Act (‘the Act’) , 1961

from April 2001 for TP provisions : Based on OECD guidelines

• Indian TP legislation aimed at computation of reasonable, fair & equitable

profits & tax in India

Slide 10

Basics of Transfer Pricing

… Indian TP Regulations

• Sections 92 to 92F of the Act read with rules 10A to 10E referred to as

framework of Indian TP legislation.

• Various circulars, notifications and administrative instructions issued

by CBDT.

• Is still in evolving stage taxpayers seek clarity on various matters.

• Subject to interpretation by Tribunals : reports state that virtually one

case per day churned out by ITAT 500+ case laws by ITAT, High

Court and Supreme Court (maximum by ITAT).

• Key ruling in the case of Vodafone on issue of shares.

• Domestic TP, Safe harbour and APA introduced.

• E-filing of Form 3CEB introduced.

Slide 11

Basics of Transfer Pricing

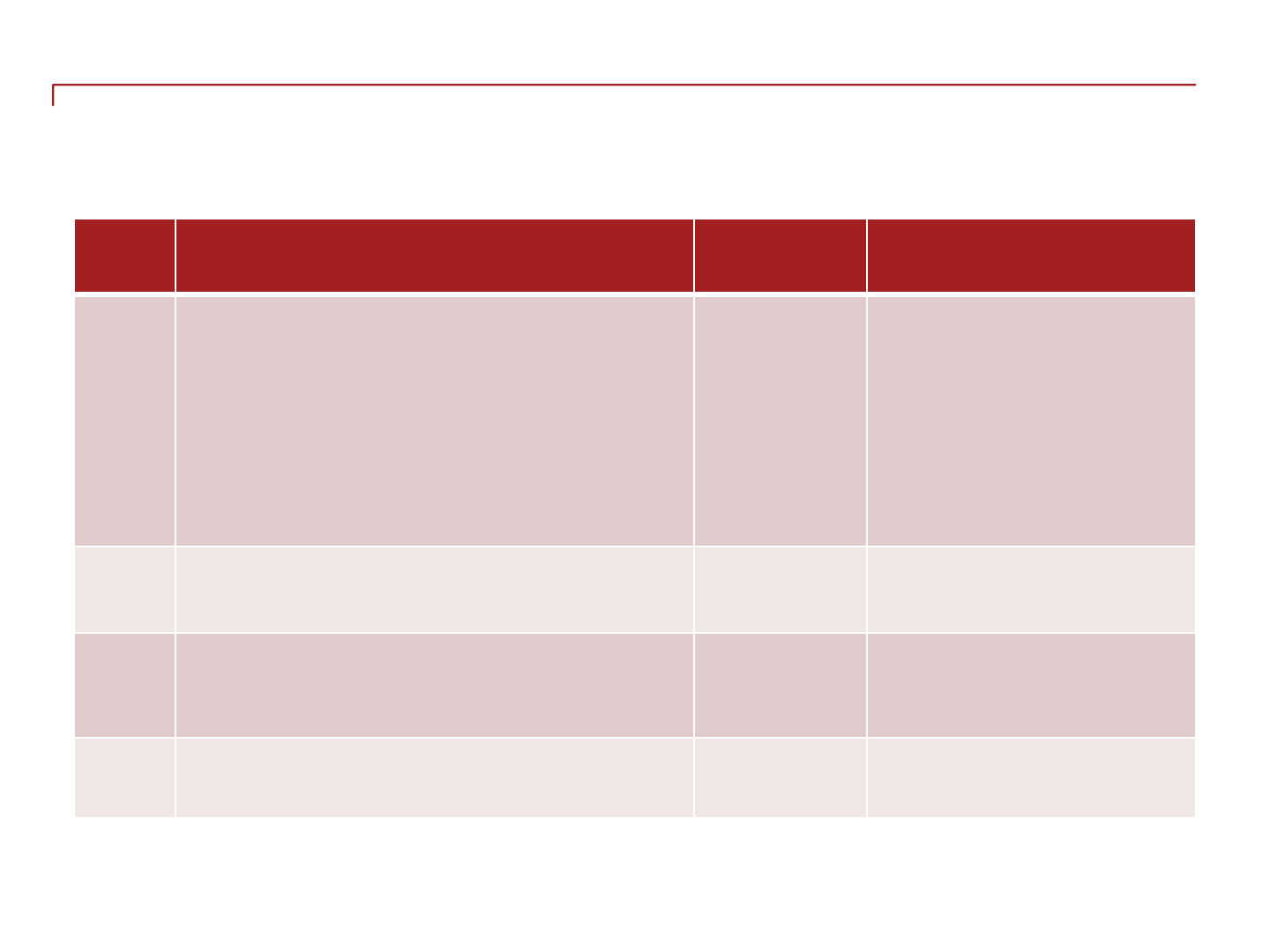

Compliance requirements

Requirement Reference Particulars

Documentation Section 92D read

with Rule 10D

Tax payers required to maintain prescribed

information & documentation

mandatory updation essential

Accountant’s Report Section 92E read

with Rule 10E

In the prescribed Form 3CEB to be filed

along with the return of income

irrespective of value of international

transactions

Stringent penalties for non-compliances…

Slide 12

Basics of Transfer Pricing

Penal consequences

Sr.

No.

Type of penalty Section Penalty quantified

1

• Failure to maintain prescribed

documentation,

• Failure to report transactions, or

• Maintenance or furnishing of

incorrect information or document

271AA 2% of transaction value

2

Failure to furnish information/

documents during assessment

271G 2% of transaction value

3

Adjustment to taxpayer’s income

during assessment

271 (1) (c)

100% to 300% of tax on

adjustment amount

4 Failure to furnish accountant’s report 271BA INR 100,000

Slide 13

Basics of Transfer Pricing

Relevant provisions

• 92: Computation of income from

international transaction as per ALP

• 92(2A): Domestic TP: allowance for

expenditure, interest, cost or expense or

income in relation to SDT to be computed

having regard to ALP

• 92A: Meaning of associated enterprise

• 92B: Meaning of international transaction

Amended by Finance Bill 2014 to apply

TP rules to transactions with a

domestic unrelated party under

specified conditions

• 92BA: Meaning of Specified Domestic

Transaction

• 92C: Computation of arm’s length price

• 92CA: Reference to Transfer Pricing Officer

• 92CB: Power to make Safe Harbor Rules

• 92CC: Advance Pricing Agreement (APA)

Amended by Finance Bill 2014 to

include roll back provisions

• 92CD: Effect to Advance Pricing Agreement

• 92D: Maintenance of information &

documents

• 92E: Accountant’s report

• 92F: Definition section

Rules

• 10A:Meaning of expressions used in

computation of arm’s length price

• 10AB: Other method for determination of

arm’s length price

• 10B: Determination of arm’s length price u/s

92C

• 10C: Most appropriate method

• 10D: information and documents to be kept

and maintained u/s 92D

• 10E: Report from an accountant to be

furnished u/s 92E

• 10F to 10T – APA Rules

Slide 14

Basics of Transfer Pricing

Section 92

• Any income arising from an international transaction shall be computed

having regard to the arm’s length price [Section 92 (1)]

• Following transactions also require compliance with Arm’s Length Principle:

- allowance for any expense or interest arising from an international

transaction [Explanation to Section 92 (1)]

- costs or expenses allocated/apportioned under mutual

agreement/arrangement for provision of benefit or service or facility by

one enterprise to other [Section 92 (2)]

• Base erosion is the important principle for attraction of TP provisions

• Provisions not to apply where ALP computation has effect of reducing income

chargeable to tax or increasing loss

• No deduction available for TP adjustments after scrutiny by the AO under Sec. 10A,

10AA, 10B or Chapter VI-A

Charging Section or

machinery Section?

Slide 15

Basics of Transfer Pricing

Enterprises

• any activity relating to production, storage, supply, acquisition or control of articles,

goods or specified intangibles.

• any activity pertaining to provision of services or carrying out any work in pursuance

of a contract

• any investment or financing activity

Section 92F (iii) defines enterprise as any person (including PE) engaged in:

The term PE has been defined to be an inclusive term to include a fixed place of

business through which the business of the enterprise if wholly or partly carried

on [S.92F(iiia)]

Slide 16

Basics of Transfer Pricing

Section 92A: Associated EnterprisesSection 92A: Associated Enterprises

A

C

B

Both A and B are associated

enterprises of C

D and E are also associated

enterprises of C since they have a

common ultimate parent (A)

A

C

B E

D

Outside India

In India

Outside India

In India

Direct or indirect participation

(through one or more

intermediaries) in

management, control or capital

– Sec 92A(1)

Slide 17

Basics of Transfer Pricing

The above section is further supplemented by 13 clauses which enlist various

situations under which two enterprises shall be deemed to be AEs –

Sec 92A(2)

Deemed to be AEs: Section 92A(2) …

Slide 18

Basics of Transfer Pricing

Equity / Debt

1. >= 26% direct /

indirect holding

by enterprise OR

2. By same person

in each

enterprise

3. Loan >= 51% of

Book value of

Total Assets

4. Guarantees > =

10% of total

borrowings

5. > 10% interest in

Firm / AOP /

BOI

Management

6. Appointment >

50% of Directors

/ one or more

Executive

Director by an

enterprise OR

7. Appointment by

same person in

each enterprise

Activities

8. 100%

dependence on

use of

intangibles for

manufacture /

processing /

business

9. Direct / indirect

supply of >=

90% Raw

Materials under

influenced prices

and conditions

10. Sale under

influenced prices

and conditions

Control

11. One enterprise

controlled by an

individual and

the other by

himself or his

relative or jointly

12. One enterprise

controlled by

HUF and the

other by a

member or his

relative or jointly

… Deemed to be AEs Section 92A(2)

• The deeming fictions may cover genuine third party transactions:

- Joint Ventures [Section 92 A (2) (a)]

- Extensive financing by Bank to an enterprise [Section 92 A (2) (c)]

- Global arrangements for supply of bulk material [Section 92 A (2) (h)]

- Use of exclusive technology by an enterprise on which it is

fully dependent

[Section 92 A (2) (g)]

Slide 19

Basics of Transfer Pricing

Case Studies

X Inc

(USA)

Y Ltd

(India)

Z Ltd

(India)

52%

49%

Whether the entities

are associated

enterprises?

• ABC Inc does not hold any shares

in ABC India

• Transactions between ABC India and

ABC Inc – covered under TP?

ABC Inc

(USA)

ABC India

Mr. P

Mr. Q

Provision of services – cost

plus mark - up

Slide 20

Basics of Transfer Pricing

Section 92B(1)

• International transaction is

- Transaction between the Group companies : either or both of whom are

non-residents

- for purchase, sale, lease of : tangible property or intangible property

- for provision of services or lending or borrowing money

- other transactions having bearing on profits / income / losses or assets of an

enterprise

- also to include cost allocations/apportionments for benefits/ services or facility

provided by one to other

• Transaction includes arrangement, understanding or action in concert:

- whether formal or in writing

- whether intended to be enforceable with legal proceedings or not

[Section 92F (v)]

• Transaction also includes number of closely linked transactions [Rule 10A (d)]

Slide 21

Basics of Transfer Pricing

Explanation by Finance Act 2012 to widen definition transactions in tangible and intangible

property, capital financing, provision of services, business restructuring included !

Explanation to Section 92B

• Introduction of an explanation to Section 92B of the Income-tax Act, 1961

• Intention of Legislation

- Previous definition leaves scope for misinterpretation - Taxpayers did not report

several international transactions

- Clarification on present scheme of transfer pricing provisions - It does not

require that international transaction should have bearing on profits or income of

current year

• Explanation (i)(a) to 92B(1) – No dispute

• Explanation (i)(b) to 92B(1) – Whether all intangibles to be reported?

• Explanation (i)(c) to 92B(1) – reporting of advances, deferred payments and

receivables

• Explanation (i)(d) to 92B(1) – Whether excess AMP needs to be reported?

• Explanation (i)(e) to 92B(1) – Whether all business restructuring / reorganizations

to be reported?

Slide 22

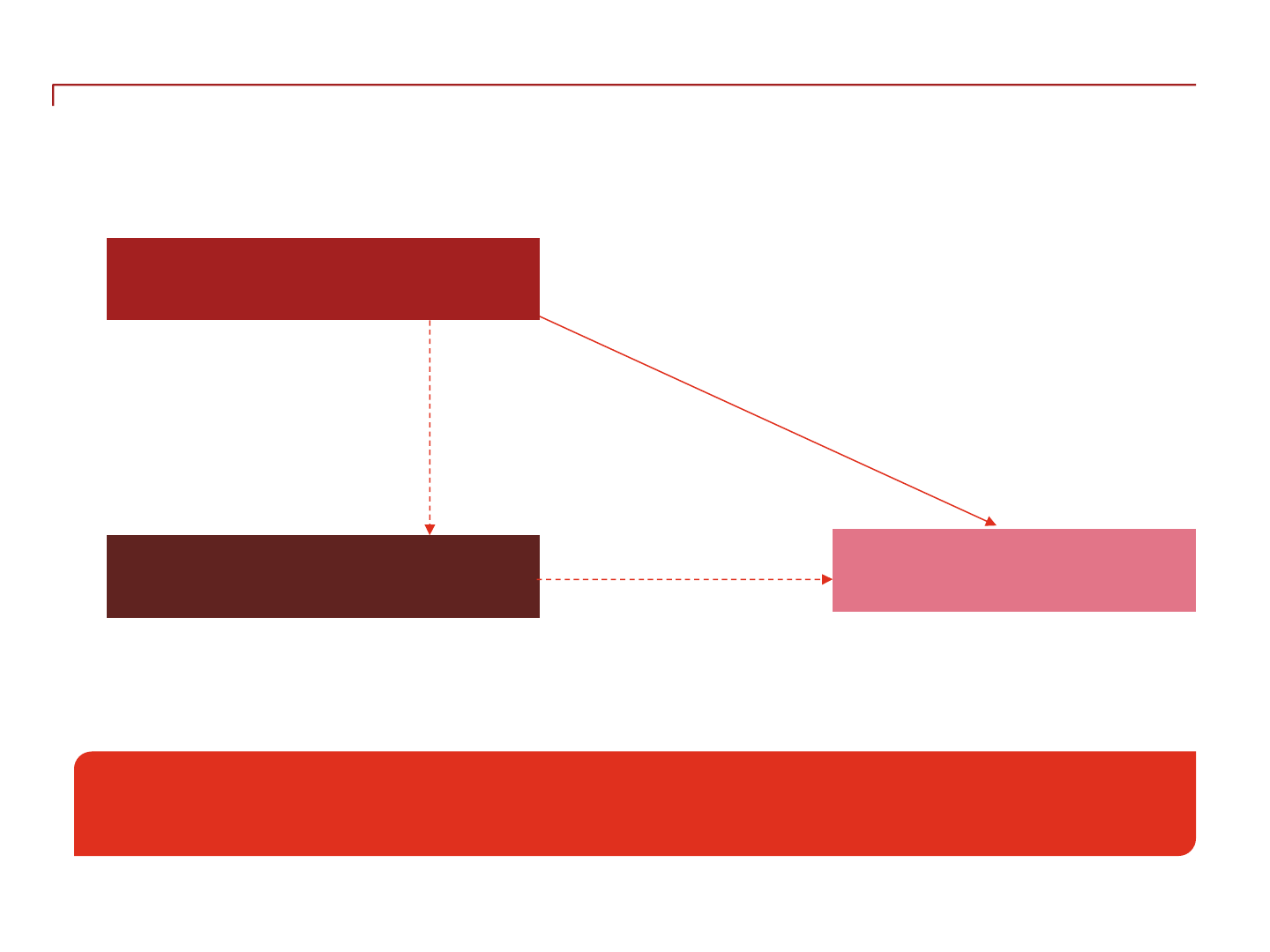

Basics of Transfer Pricing

Deemed International transactions – Sec 92B(2)

ABC AE

XYZ

India

ABC

India

Goods

/Services

Old provision New provision

Not covered under the

ambit of TP provisions

Outside

India

India

ABC AE

XYZ

India

ABC

India

Outside

India

India

Goods

/Services

Slide 23

Will be covered under TP

provisions, if ABC AE:

(i) has prior agreement with

XYZ India; or

(ii) determines the terms in

substance with XYZ India

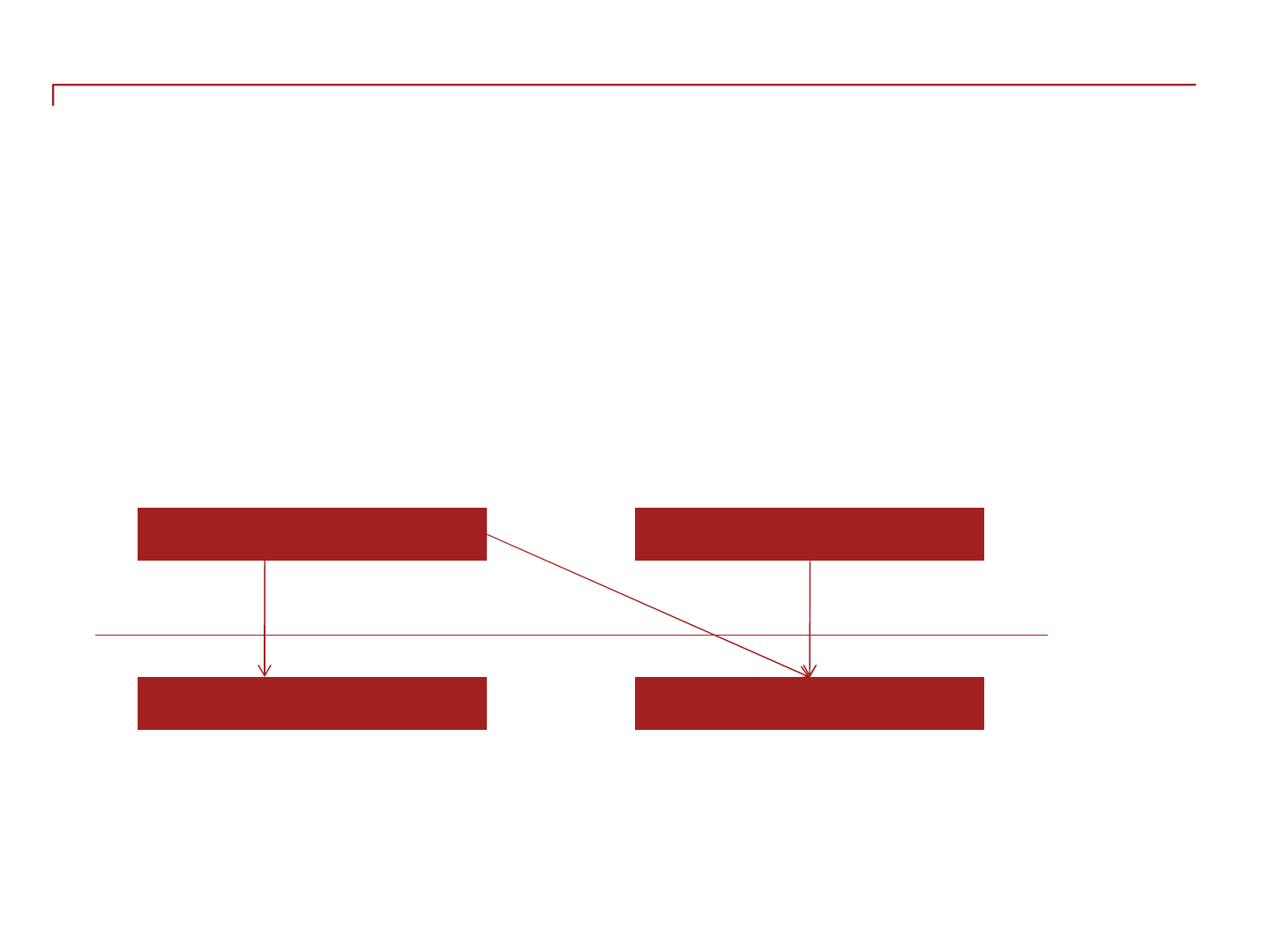

Basics of Transfer Pricing

Deemed International Transaction: Section 92B(2)

Prior agreement

Parent Company

Third party

Subsidiary

Parent Company

Third party

Subsidiary

Determination of terms

Transaction between subsidiary & overseas third party

Prior agreement exists between

parent company and

third party

Terms of transaction are

determined in substance by

parent company and

third party

Overseas

India

Overseas

India

Slide 24

Basics of Transfer Pricing

Deemed International Transaction: Section 92B(2)

Transaction between subsidiary & domestic third party

Prior agreement exists

between parent company and

third party

Terms of transaction are

determined in substance by

parent company and

third party

Overseas

India

Overseas

India

Prior agreement

Parent Company

Affiliate of

Third party

Subsidiary

Services under contract between parent and

third party affiliate

Third party

Determination of terms

Parent Company

Affiliate of

Third party

Subsidiary

Services under contract between parent and

third party affiliate

Third party

Basics of Transfer Pricing

Deemed International Transaction: Section 92B(2)

Parent Company

Third party

Subsidiary

Transaction between subsidiary & domestic third party

Prior agreement exists between

parent company and

third party

Terms of transaction are

determined in substance by

parent company and third party

Parent Company

Third party

Subsidiary

Goods

Overseas

India

Overseas

India

Goods

Slide 26

Basics of Transfer Pricing

Case Studies on applicability of TP

Holding company USA

Indian Branch

Singapore Subsidiary

Hong Kong Branch

Slide 27

Basics of Transfer Pricing

Whether the Indian TP provisions would apply for the above

scenarios?

… Case studies on international transactions

Parent P

Subsidiary S

Customer of P

Sale under contract

Assignment of

contract

Sale at prices

as per contract

Slide 28

Basics of Transfer Pricing

Whether sales by S to the Indian customer would qualify as

International Transaction?

Computation of ALP [Section 92C (1)]

OECD Transfer Pricing Methods

Transaction Methods Transactional Profit Methods

Comparable

Uncontrolled

Price

Resale Price

Method

Cost Plus

Method

Profit Split

Method

Transactional

Net Margin

Method

By use of any of the prescribed methods being

the Most Appropriate Method (‘MAM’)

Slide 29

Basics of Transfer Pricing

Or any other method prescribed by the board

Comparable Uncontrolled Price Method (‘CUP’)…

• Compares price charged for property/ service transferred in controlled transactions

with price charged in comparable uncontrolled transactions

• Requires very high standard of comparability

• Most direct and reliable way to apply the arm’s length principle – but can be used in

case of similarity of product and services

• Conditions for use of CUP

- none of the differences between the transactions can materially affect price in the

open market

- reasonably accurate adjustments can be made to eliminate the material effects of

such differences

Slide 30

Basics of Transfer Pricing

…CUP Method…

• Comparability based on:

- Strong similarity of products and services

- Functions

- Contractual terms

- Risks

- Economic conditions

- Level of market

- Geography catered

- Timing of the transaction

Slide 31

Basics of Transfer Pricing

...CUP Method

• Types of CUPs available

- Internal CUP - The price that the company has charged in a comparable

uncontrolled transaction with an independent party

- External CUP - The price charged in a comparable uncontrolled transaction

between third parties when compared to a price of controlled transactions

Parent Co. Third Party

Subsidiary Co. Third Party

Outside India

India

Internal CUP External CUP

Sale of goods

Slide 32

Basics of Transfer Pricing

CUP Method – Practical Issues and challenges

• Often difficult to obtain identical transaction:

- Difference in volume / geography / end user / contractual terms

• Making reliable / accurate adjustments not always feasible

• Indirect evidences of CUP – Can data from public exchanges / quotations be used?

• Can CUP include “pricing basis”?

Slide 33

Basics of Transfer Pricing

Resale Price Method (‘RPM’)…

• Method used in case of purchase of

goods or services from related parties

for resale to unrelated parties

without substantial value

addition

• The price is reduced by the normal

gross margins earned by unrelated

party for same or similar products or

services

• Need for similarity of functions

performed and risks undertaken

• Gross margins used as the profit level

indicator

Group Manufacturer

in US

Related

Distributor

in India

Unrelated

Retailer

An Indian related distributor

Purchases goods from its US

Manufacturer for resale to

unrelated retailers in India.

Indian distributor earns a gross

margin of 25%

$ 75

$ 100

25% resale margin earned by Indian distributor, if lies

within arm’s length range of margins earned by

similar Indian distributors – substantiates arm’s

length nature of the purchase from the group

company

Slide 34

Basics of Transfer Pricing

RPM – Practical Issues and challenges…

• Gross margins are affected by minor functional differences

• Difficulties in proper application, particularly in determination of costs

- Difficult to find accurate data disclosing gross margins of independent resellers in

public domain

- Categorization of expenses as operating expenses or cost of goods sold may be

subject to manipulation

- Differences in accounting policies, operational efficiency, economies of scale, etc

would be difficult to adjust

- Difficulties in benchmarking limited risk distributor / net losses

- Lack of guidance for reliable adjustments

- Difficulty in applying RPM in case segmental data of comparable company is

considered

Slide 35

Basics of Transfer Pricing

Cost Plus Method…

• Method using the costs incurred by the supplier of property (or services) in a

controlled transaction for property or services provided to an associate purchaser.

• An appropriate cost plus mark-up is added to the above cost in light of the FAR

ALP = Direct and Indirect Cost of Production (“DICOP”)

(+) gross profit mark-up of entity selling goods to AE

Governing conditions for use of CPM

• none of the differences between the transactions can materially affect cost plus

margin in the open market

• reasonably accurate adjustments can be made to eliminate the material effects of such

differences

• Tolerant to Product Differences unlike the CUP method

• Focuses on gross profit margins, which are heavily influenced by the scope, intensity of

functions performed and accounting methods

Slide 36

Basics of Transfer Pricing

Profit Split Method (PSM)…

PSM is applied, where:

• Both the entities have unique intangibles

• Operations of both the entities are so integrated that identifying the

tested party is very difficult

PSM is contribution analysis rather than

comparability analysis

Slide 37

Basics of Transfer Pricing

Profit Split Method – Strengths and weakness

Strengths

• Offers solutions for integrated

operations not offered by one-sided

methods

• Helps share profits for unique

intangibles contributed

• Less dependant on comparables

• Less likely to leave any party to the

transaction with extreme profitability

as both parties are evaluated

Weakness

• Difficulty in application

• Necessitating application of similar

accounting policies and standards

• Allocation of costs

• Reluctance of tax authorities to accept

Slide 38

Basics of Transfer Pricing

Transactional Net Margin Method (‘TNMM’)

• Comparison at operating margin level

• Comparison at transactional level, where possible

• Broad level of similarity of FAR

• Selection of the right comparables and PLI are critical factors

• Most preferred and practical method

Slide 39

Basics of Transfer Pricing

Other Method

Any method which takes into account :

• the price which has been charged or paid,

• or would have been charged or paid,

• for the same or similar uncontrolled transaction, with or between

non-associated enterprises, under similar circumstances, considering

all the relevant facts

Slide 40

Basics of Transfer Pricing

Transfer Pricing Methods and Comparability

Methods

Comparability

Requirements

Approach

Practical

Applicability

CUP Very High Prices are benchmarked Low

RPM High

Gross margins are

benchmarked

Low

CPM High

Gross margins are

benchmarked

Low

PSM Medium

Operating margins are

benchmarked

Medium

TNMM Medium

Operating margins are

benchmarked

High

Other High

Prices charged /

proposed to be charged

For selected

transactions

Slide 41

Basics of Transfer Pricing