Fund

Transfer

Pricing

KPMG d.o.o. Beograd

Financial Services Team

2016

F

T

P

2

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Contents

Introduction to IFRS 9 3

The Journey 4

Why now? 5

Case study 6

Why KPMG? 7

Our approach 9

KPMG gCLAS 10

Would you like to see more and

further than others in terms of

your profitability?

3

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Contents

Page

Introduction to Fund Transfer Pricing (FTP) [4]

• What is FTP? [4]

• Internal transfer and ALM risks centralization [5]

Main targets of FTP [6]

Potential consequences of not having FTP [7]

Exemplary scope of work, timeline and modules [9]

Appendices

Why KPMG? [11]

4

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

- The FTP system groups together the nancial risks generated by commercial transactions with in

a Central Finance Unit (CFU). CFU is generally managed by the ALM/Treasury department, which

has the necessary expertise and resources to assess and hedge the nancial risks.

- This centralization of risks is done thanks to a system of internal transfers between the commercial

(business) lines and the CFU. These internal transfers are made via the theoretical “purchase” of

customer deposits from deposit centers and the theoretical “sale” of funds to loan centers. The

pricing terms of such transfers constitute FTPs.

Introduction to Fund Transfer Pricing (FTP)

Banks have realized the need for an effective transfer pricing

system in order to manage funding, the balance sheet structure

(financial or ALM risks), and risk adjusted profitability.

Taking into account

decreasing market

rates environment

and the fact that

majority of Banks

NBI comes from Net

interest income, the

FTP system is crucial.

Source: National Bank of Serbia.

Note: Annualized data.

Net Banking Income of Serbian Q3

banking sector 2015

Net interest income 73%

Net fee and commission income 19%

Net income from n. transactions 5%

Other income 3%

Total 100%

What is FTP?

- Fund Transfer Pricing (FTP) is a well known

practice in nance. It is a part of the overall

management information, accounting and

control system which includes: pricing, bud-

geting and prot planning, ex-post protabil-

ity measurement (prot ability controlling)

and ALM.

- It is a widely used and comprehensive tool in

overall nancial management. Some would

say it’s crucial for effective and efcient not

only nancial but banking business manage-

ment.

- FTP system serves as main tool for expost

protability measurement, i.e. protabili-

ty follow-up and controling per various axis

(business units, products, branches, relation-

ship managers etc.).

5

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Introduction to Fund Transfer Pricing (FTP)

Internal (theoretical) fund transfer and ALM risk centralization

could be presented as follows

Figure 2 – ALM risks cantralization

Management Board

ALCO

ALM

Liquidity portfolio

income

Liquidity mismatch

Interest rate

mismatch

Funding cost

Reference rate

Reference rate

Liquidity premium

Liquidity premium

Other

Other

Interest

rate gap

Liquidity

gap

FX

gap

$

€

¥

£

FTP rate

FTP rate

Risk

Risk

Assets Liabilities

Market Market

Figure 1 – Theoretical internal transfers

ALM center

FTPFTP

Deposits

Process of commercial products

internal pricing

Commercial

loans

Notional

investments /

Replacement

yield for

deposits

Commercial margin on loans

calculated on the basis of FTPs

cost of funds

Commercial margin on deposits

calculated on the basis of FTPs

replacement rates

Notional

funding / Cost

of funds for

loans

Commercial

deposits

Funding

6

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member fi rm of the KPMG network of independent

member fi rms affi liated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Strategic

goals of FTP

• To de ne funding cost for

the assets and to calculate

NIM for asset items

• To de ne reinvestment

yield for the liabilities and

to calculate NIM for liability

items

• To stabilize NIM for all

commercial deals by

transferring (isolating)

interest rate, liquidity and

FX risk from BUs to CFU

• To de ne pricing benchmark

for clients’ deals (pricing

tool) and thus ex-ante

pro tability measurement

• To establish ef cient ex-post

pro tability measurement

per various axis and thus

to link budgeting and

controlling activities

• To impact BUs sales

strategy through concept

of incentives (subsidies) via

Management FTP

• To signalize a real, existing

market conditions in terms

of market prices of sources

and alternative placements,

and thus infl uence

commercial lines to “ ne

tune”the prices of their

products

• FTP should align risk-taking

initiatives of BUs with

liquidity and interest rate

risk exposure they create for

the whole Bank

• BUs take risk they can

control and manage

• BUs are responsible for

clients pricing

• Fair assessment of

economic performance of

every BU, i.e. commercial

margin then becomes the

sole result of negotiations

by BU with customers

• Business people shall

understand how the

pro tability is measured

and shall be motivated by

pro tability indicators

• FTP requires reliable IT

system and support

• FTP requires comprehensive

FTP Policy and Methodology

Integration of FTP

into general Bank’s

management system

What are main targets of FTP?

FTP changes the overall commercial mindset of the Bank

• Regulations on liquidity:

ü Minimum liquidity

requirements from local

regulator or from Basel III

in form of NSFR and LCR

requirement

ü Recommendations on

Organizing Effective

Liquidity Management

• BCBS requirements

• FSA requirements

• Best practices

Regulatory

requreiments and

best practice

7

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member fi rm of the KPMG network of independent

member fi rms affi liated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

What are potential consequences of not following/having FTP?

How we can help

Consequences

of not having

FTP system

Volatile result of BUs due to

not transferred and not hedged

liquidity and IR risk

Without FTP top management is not able

to distinguish pro table BUs, segments,

products, branches, front of cers etc.

from non-pro table ones

BUs are unclear on real

margin of their products. Non-

market based FTP overstates

performance of some BUs and

understates that of others and

leads to “unfair” and inef cient

performance-rewards decision

Overstated pro tability of

non-funded products creates

wrong incentives for BUs to

disproportionally grow portfolio

Total level of liquidity and IR risk cannot be measured and managed.

Bank bears hidden risk of maturity and IR transformation

Loosing money on products mispricing.

Without FTP framework, based on actual

maturity, some BUs are charged less than

required rate to cover funding cost

Performance of ALM Unit

cannot be measured and volatile

nancial results of ALM-unit

(realized liquidity risks or

improper liquidity management)

allocated back to BUs and distort

their performance

We offer more than just FTP as is:

ü Comprehensive gap analysis concerning

Bank’s current pro tability management

approach

ü Benchmark analysis vs. best practice

ü Recommendations for improvement of

Bank’s pro tability system

ü Journey beyond just FTP –OPEX

allocation and Cost of Risk incorporation

into products pricing

ü Completely new pro tability approach in

order to reach targeted ROE and EVA

ü PMO in terms of selection and

implementation of new FTP tool (engine)

We have developed the robust and comprehensive

FTP framework in line with Maturity and Cash-

fl ow Weighted Rate Approach (MCWR).

Liability

Price

Term

Rate

[%]

Liability

margin

Market rate based transfer procong method

Asset

margin

Loan

Price

Treasure

margin for

levarage

management

Market curve

What we offer:

8

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Our approach to FTP is flexible and

customized, driven by the specific

needs, culture and strategic goals

of our clients.

9

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member fi rm of the KPMG network of independent

member fi rms affi liated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

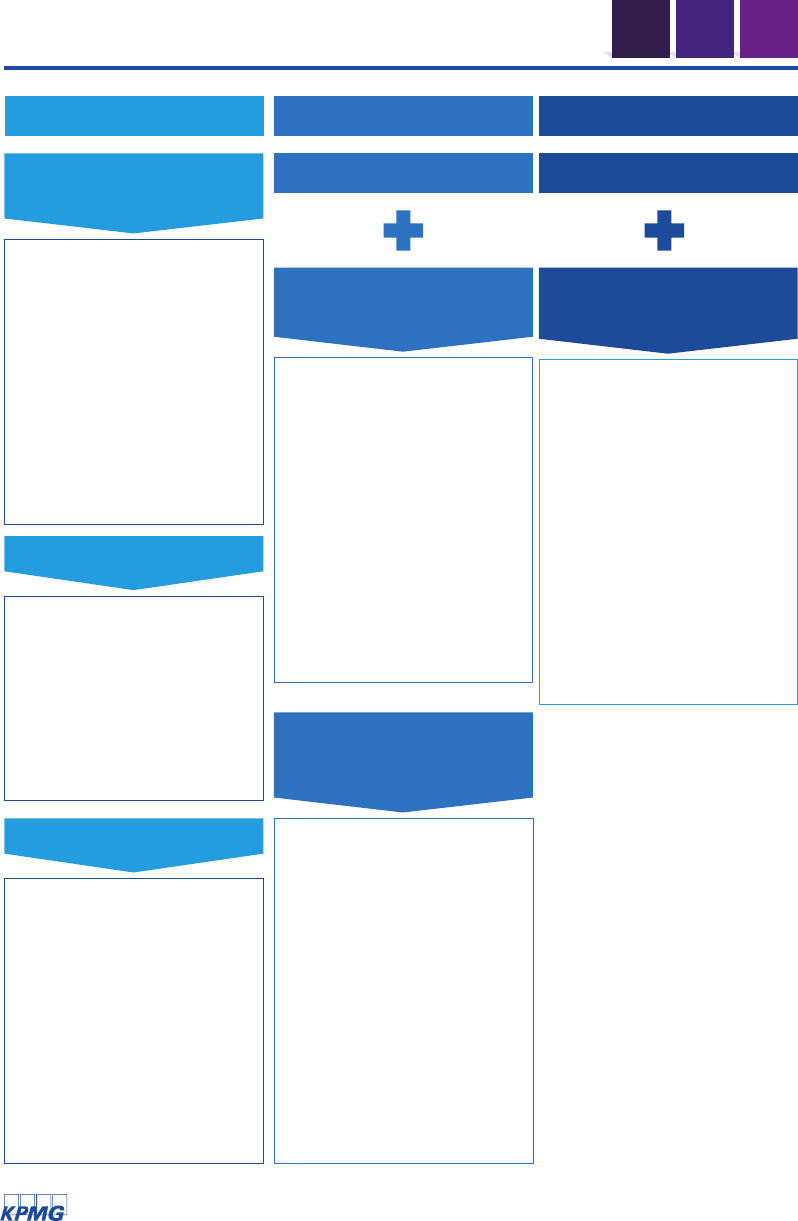

Exemplary scope of work

F

T

P

Basic module Optimal module

Basic module Optimal module

Advanced module

Phase 1: Review of Bank’s

current FTP model and gap

analysis

Review and gap analysis will

be conducted in the following

areas of the FTP model:

• Objectives and principles of

FTP system with taking into

consideration requirements

regarding Bank’s business and

funding strategy

• Scope of FTP model applica-

tion

• Components of FTP rates and

methods for their determination

• Operational processes in

scope of FTP system

Phase 4: Development of

detailed concept of new FTP

model

Development of detailed

performance concept of target

funds transfer pricing model.

Developed solutions will

encompass such aspects as:

• Objectives and principles of

new FTP system

• Components of FTP rates

and methods for their

determination

• Methodology of assigning

FTP rates to particular

products groups

• Scheme of FTP system

and division of task and

competences.

PMO in order to help Bank

to select and implement new

FTP tool (engine)

PMO by KPMG shall help Bank

to select a comprehensive FTP

tool (IT solution), which shall

be used as FTP engine in order

to calculate and store FTP rates,

compute margins and produce

various pro tability reports.

Such tailor made FTP tool shall

meet “state-of-the art” nancial

best practice.

The FTP tool is to be developed

either as in-house solution or

external solution provided by

vendors the KPMG cooperated

with.

Phase 5: Preparation

of written Policy and

Procedures for new FTP

model

Development of formal

documentation for FTP model

based on the concept prepared

by KPMG and accepted by

Bank, including the following:

• Policy –describing new

FTP model methodology,

objectives and principles

for new FTP model,

organizational units involved

in FTP process with division

of task and competences.

• Procedure –description of

methods and rules of tasks

execution by particular unites

involved in the process.

• Training of staff.

Phase 2: Benchmark analysis

• Benchmark analysis of fund

transfer pricing models

used by leading nancial

institutions.

• During the benchmark

analysis KPMG will review

best practice solutions for

selected aspects of FTP

models applied by the leading

nancial institutions.

Preparation of conclusions and

recommendations based on

as-is and benchmark analyses.

The recommendations shall be

divided into two groups:

• Key changes designed to

ensure security and consisten-

cy of the FTP model in its key

functioning aspects.

• Potential improvements with

aim to add new features

and to adapt the model to

application for wider range of

products.

Phase 3: Recommendations

10

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member fi rm of the KPMG network of independent

member fi rms affi liated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Indicative timeline

FTP Project

Week 1 Week 2

Kick-off!

Your comments Your comments

End of Moderate

Module

End of

Advanced PMO

services

End of Basic

Module

Week 3 Week 4 Week 5 Week 6 Week 7 Week 8

Phase 1:

Review and gap analysis

Phase 2:

Benchmark analysis

Phase 3:

Recommendations

Phase 4:

Development of detailed concept

of new FTP model

Phase 5:

Preparation of Policy and

Procedure for new FTP model

Exemplary scope of work

Advanced PMO: Selection and implementation of new FTP engine (tool)

F

T

P

11

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member fi rm of the KPMG network of independent

member fi rms affi liated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

Why KPMG?

KPMG d.o.o. Beograd is the leading consultant of nancial institutions in Serbia.

Currently, we perform audit and consulting for more than 2/3 of the banking

market in Serbia.

The practice in Serbia has rich experience in providing advisory services to the

entire spectrum of nancial institutions: banks, leasing companies, government

bodies, foreign investors, insurance companies and other nancial institutions,

agencies and other companies that operate in Serbia. Our team also covers

Montenegrin nancial sector market.

KPMG d.o.o. Beograd currently has about 210 employees, including 9 partners.

Our FS Team, responsible for clients in the nancial sector, currently has about

30 employees, including one partner, two senior managers and three managers.

12

© 2016 KPMG d.o.o. Beograd, a Serbian limited liability company and a member firm of the KPMG network of independent

member firms affiliated with KPMG International Cooperative (‘KPMG International’), a Swiss entity. All rights reserved

© 2016 KPMG d.o.o. Beograd, a Serbian limited

liability company and a member firm of the KPMG

network of independent member firms affiliated

with KPMG International Cooperative (‘KPMG

International’), a Swiss entity. All rights reserved.

Printed in Serbia.

The KPMG name and logo are registered

trademarks or trademarks of KPMG International.

Dušan Tomi , Partner

T: +381 11 20 50 521

Sanja Ko ovi , Departmental Senior Manager

E: skoco[email protected]

T: +381 11 20 50 518

Ivan Cirkovi , Manager

E: icirko[email protected]

T: +381 11 20 50 649

Contact us:

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity.

Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is

received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a

thorough examination of the particular situation.