PENNSYLVANIA

Transportation Revenue Options Commission

July 30, 2021

FINAL REPORT

AND

STRATEGIC FUNDING

PROPOSAL

intentionally blank

PA Transportation Revenue Options Commission Final Report – July 30, 2021

3

July 30, 2021

Governor Wolf,

The Transportation Revenue Options Commission (TROC) is pleased to submit its

strategic funding proposal, in accordance with Executive Order 2021-02, to ad-

dress the acute transportation funding challenge facing the Commonwealth now

and into the future.

TROC was established with the expectation that now is the time to fundamentally

change transportation funding strategies for the Commonwealth—to bring revenue

back in sync with the costs of sustaining our essential multimodal transportation

system, and to fairly distribute those costs to those who directly and indirectly ben-

efit from the system.

Inaction is not an option. The Commonwealth must modernize and restructure its approach to transporta-

tion funding for the long term, while rapidly adopting near- and medium-term changes. Properly addressing

the full range of transportation system needs will require unprecedented federal-state-local partnership.

Over the five months in which TROC deliberated, the following became clear:

• While the gas tax that funds Pennsylvania highways and bridges is eroding as a revenue source, the

Mileage-Based User Fee (MBUF) approach presents the most promising long-term solution in Penn-

sylvania and nationally for aligning transportation revenue with the needs of the system.

• However, a full MBUF solution could be far in the future. In the meantime, we need bold action to meet

the system’s improvement and maintenance needs, and to prepare the way for MBUF.

• Other equally critical challenges include the need for adequate and sustainable funding for public

transportation as well as freight and passenger rail, water ports, aviation, and bicycle and pedestrian

accommodation.

• Pennsylvania is not alone in having to address these problems. Other states have taken varied and

innovative measures to broaden their revenue base. They have done so to ensure the continued in-

tegrity of their transportation systems and to provide the mobility and access necessary for individuals

and businesses. Pennsylvania’s particularly heavy reliance on declining gas tax revenues makes the

need for action on this proposal urgent.

The mix of revenue sources in TROC’s strategic proposal represents a feasible, phased approach that

is designed to address the most critical shortfalls in funding levels in the near-, medium-, and long-term

phases. Ultimately, future implementation of MBUF fully aligns revenues with identified needs.

This proposal will position Pennsylvania to benefit from the long-term mobility and access necessary to

support economic prosperity, public safety, and a high quality of life for individuals and communities across

Pennsylvania. The proposed investments will produce significant benefits across the state.

I thank the Majority and Minority Chairs of the Senate and House Appropriations and Transportation Com-

mittees and their sta for their time attending TROC meetings and listening to discussions by TROC work

group members on potential revenue options. We commend all the Commission members for their en-

gagement and hard work, which is captured in this report.

On behalf of the entire Commission, I strongly encourage Pennsylvania’s policymakers to consider and

then act on this proposal as a necessity of bold leadership and responsible stewardship.

Respectfully,

Yassmin Gramian, P.E.

Chair, Transportation Revenue Options Commission

Secretary, Pennsylvania Department of Transportation

Yassmin Gramian, P.E.

intentionally blank

PA Transportation Revenue Options Commission Final Report – July 30, 2021

5

Contents

Introduction

66

Proposed Commonwealth Transportation Funding Strategy

1818

Modernizing Federal and Local Transportation Funding

3232

Proposed Next Steps

3636

Conclusion

3737

Commission Members

3838

PA Transportation Revenue Options Commission Final Report – July 30, 2021

6

Introduction

The Commission’s Assignment and Approach

Modernizing how we pay for Pennsylvania’s multimodal transportation system is a complex and urgent im-

perative. Previous transportation funding studies and initiatives have established the need and addressed

significant parts of the problem. Now, those eorts must be extended and expanded with a comprehen-

sive reassessment and updated approaches to securing long-term, sustainable transportation funding.

Pennsylvania Governor Tom Wolf established the Governor’s Transportation Revenue Options Commis-

sion (TROC, pronounced “TEE-rock”) in March 2021 by Executive Order 2021-02. The Governor tasked

TROC with developing a comprehensive, strategic proposal for addressing the multimodal transportation

funding needs of Pennsylvania. This document presents TROC’s proposal.

The TROC members, listed at the end of this report, represent a cross-section of Pennsylvania’s geograph-

ical areas, transportation modes, local and state governments, and environmental, energy, and industry

interests. TROC was chaired by Pennsylvania Secretary of Transportation Yassmin Gramian. None of its

other members were PennDOT employees.

TROC convened (virtually, due to COVID-19) nine times over the five-

month Commission duration to develop these proposed solutions.

Members also participated in targeted work groups to examine the

transportation funding problem through various lenses. Work group

leaders met several additional times to sharpen the proposed strategy.

TROC was supported by PennDOT’s Bureau of Fiscal Management,

which oered expertise in existing and projected revenue streams.

Tools included advanced spreadsheets allowing work groups to run if-

then scenarios and project the results of diversified funding strategies.

Given its short schedule, TROC largely relied on existing analyses of

transportation funding need along with updated cost estimates where

possible. The existing estimates were vetted with TROC. Many TROC

members deemed the estimates of need to be conservative.

How did a group of more than 40 appointees—with widely ranging

points of view on public investment—come to substantial agreement

on the strategic funding proposal? Despite a great variety of interests

and perspectives, all members recognized the urgent need to update the state’s obsolete and declining

transportation funding approaches. Members agreed on guiding principles (presented on page 18) and

engaged in discussions on which options would produce the best overall results for Pennsylvanians. In

short, TROC members generally put the Commonwealth’s transportation needs above individual interests.

Governor Wolf

established the

Transportation Revenue

Options Commission

(TROC) to propose a

strategic, comprehensive

Commonwealth

transportation funding

scenario.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

7

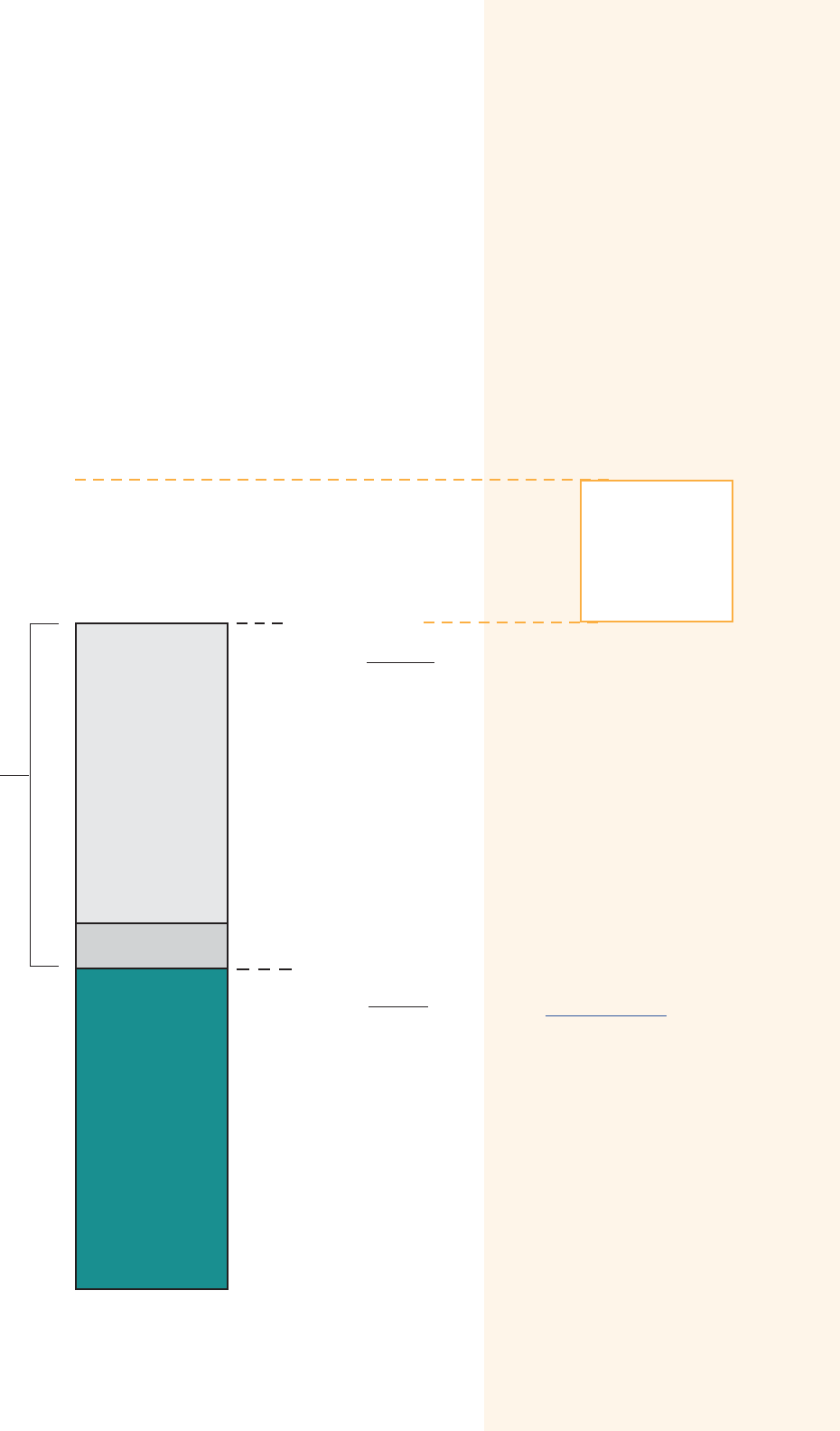

Fiscal Year 2021-22

$9.35 billion

state-level

funding gap

(growing each year)

$8.8 billion

PennDOT’s current

annual budget

(approximately 75%

state funding and 25%

federal funding)

$18.15 billion

PennDOT’s needed

annual budget

(with increases for

inflation) to keep

the state-owned

transportation system

in a state of good

repair

Local transportation funding

is also inadequate.

The column graph only depicts

need for the state-owned system.

The current local unmet

funding need is estimated to be

$3.9 billion per year, growing to

$5.1 billion per year by 2030.

Although addressing local needs

was not part of TROC’s core

assignment, local infrastructure

is a vital part of the statewide

transportation system. See

the Local Solutions section for

additional discussion on local

options.

MULTIMODAL

NEED $1.20B

HIGHWAY &

BRIDGE NEED

$8.15B

LOCAL NEED

$3.9B

Pennsylvania’s Transportation Funding Needs

The stark reality is that PennDOT’s $8.8 billion annual budget must more

than double—to approximately $18.15 billion—to adequately address

transportation system needs.

Figure 1: Pennsylvania’s Transportation Funding Gap

PA Transportation Revenue Options Commission Final Report – July 30, 2021

8

Highways: Interstate and Other

National Highway System Repairs

($1.9 billion)

Highways:

Interstate and Other

National Highway System

Modernization

(Modest Improvements)

($2.1 billion)

Highways:

Maintenance & Operations;

Repairs to the Non-National

Highway System

($4.1 billion)

Highways:

Facilities Improvements

($50 million)

Multimodal

($1.2 billion)

Multimodal detail:

• Freight Rail ($10 million)

• Water Ports ($20 million)

• Bicycle & Pedestrian ($18 million)

• Aviation ($10 million)

• Public Transportation &

Passenger Rail ($1.1 billion)

Figure 2: Breakdown of the $9.35 Billion Annual Unfunded Need

ESTIMATING PUBLIC TRANSPORTATION AND OTHER MULTIMODAL NEEDS

While highway and bridge assets are owned by the Commonwealth, multimodal assets are owned by a range of

entities. Estimates are based on PennDOT programming and reflect long-deferred state-of-good-repair capital and

maintenance needs.

It is recognized that the estimates in this report may not reflect the full extent of multimodal need. For example, the

public transportation stakeholders involved in this eort place the need at closer to $1.65 billion (vs. the stated $1.1

billion). In terms of bicycle and pedestrian need (listed at $18 million in this report), note that the cost to close the top

10 trail gaps is approximately $45 million. Closing all trail gaps would total more than $200 million.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

9

As shown in Figure 2, unfunded needs include:

• $1.9 billion in unmet needs for the National Highway System (NHS) –

» $700 million in unmet basic annual Interstate highway funding needs. To meet federal as-

set condition requirements, PennDOT must gradually increase Interstate funding over the next

few years. Currently, PennDOT invests between $450 and $500 million per year on the Inter-

state Highway System. The amount needed per year

to meet cyclical asset management requirements is

$1.2 billion. PennDOT expects to increase Interstate in-

vestment by approximately $150 million in Federal Fiscal

Year (FFY) 2021 and increase the investment by $50 mil-

lion per year until it reaches $1 billion in FFY 2028.

» $1.2 billion in annual unmet needs for the balance of the

NHS (i.e., non-Interstate NHS roadways). The need for

funding on roads that are not part of the Interstate system

was a common plea from the members of the General As-

sembly during 2021 appropriations hearings. The situation

will become worse because the previously mentioned in-

crease in funding to the Interstates to meet federal perfor-

mance measures will divert funding from the non-Interstate

system, thus expanding the unmet needs for the remainder of the NHS. This underinvestment is

untenable and cannot continue.

• System Modernization and Upgrades of the NHS (including Interstates) – There is an unmet annual

need of $2.1–$3.2 billion for congestion, safety, and modernization projects for the Interstate system

and modest upgrades to the remainder of the NHS system. Examples include adding lanes in key lo-

cations, improving roadway geometry, constructing more ecient interchanges, upgrading guiderail,

expanding Intelligent Transportation System (ITS) capabilities, and making other operational improve-

ments that improve eciency and safety.

• Non-National Highway System and Maintenance and Operations – Although the NHS generally car-

ries higher trac levels, the non-NHS and “low-trac” routes comprise more than three-quarters of

the state-maintained mileage. Similar to the NHS, funding is needed to meet basic asset cycles. Addi-

tionally, standard maintenance, including winter services, crack sealing, line painting, etc., is needed

on all networks. In addition to approximately 40,000 miles of highway and 25,400 bridges, PennDOT

owns and maintains numerous other assets across Pennsylvania (e.g., buildings and maintenance

sheds). Each asset follows a life cycle of build, maintain, preserve, and then reconstruct when the

asset reaches the end of its useful life. All of these assets have relatively predictable required main-

tenance cycles to extend their useful life.

• Public transportation, aviation, rail freight, ports, and bicycle and pedestrian facilities – Multimodal

annual unmet needs exceed $1.2 billion. Freight transportation uses all modes of transportation to

serve businesses, consumers, and the global marketplace. Pennsylvania is a strategic gateway for

goods movement nationally. System investment across the modes is vitally important from this eco-

nomic perspective, as transportation supports our economy and job formation.

Currently, PennDOT invests

between $450 and $500

million per year on the

Interstate Highway System.

The amount needed per

year to meet cyclical asset

management requirements

is $1.2 billion.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

10

The funding gap increases each year, as costs rise and funding levels

remain static. Or, for some revenue sources—such as those derived from

the gas tax—funding decreases. Figure 3 presents additional funding

needs (amounts needed in addition to PennDOT’s current budget) over

the next 10 years.

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

National Highway System $1,900 $1,995 $2,095 $ 2,199 $2,309 $2,425 $2,546 $2,673 $2,807 $2,948

System Modernization

and Upgrades

$2,100 $2,205 $2,315 $2,431 $2,553 $2,680 $2,814 $2,955 $3,103 $3,258

Non-NHS and Maintenance

and Operations

$4,100 $4,305 $4,520 $4,746 $4,984 $5,233 $5,494 $5,769 $6,058 $6,360

Facilities $50 $53 $55 $58 $61 $64 $67 $70 $74 $78

Multimodal $1,200 $1,260 $1,323 $1,389 $1,459 $1,532 $1,608 $1,689 $1,773 $1,862

Total State-Level

Transportation

Funding Need

$9,350 $9,818 $10,308 $10,824 $11,365 $11,933 $12,530 $13,156 $13,814 $14,505

Figure 3: State-Level Transportation Unmet Funding Need Forecast (in millions)

The state-level funding gap

in Year 10 is projected to be

$14.5 billion.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

11

How Did We Get to This Point?

All states struggle with how to pay for transportation infrastructure

and services. The problem is particularly pronounced in Pennsylva-

nia, where our transportation system is larger and older than most.

The average age of the state’s 25,400 bridges, for example, is 55

years—in many cases, nearing or exceeding their design life. Similarly,

the Southeastern Pennsylvania Transportation Authority (SEPTA) op-

erates the oldest rail vehicle fleet in the nation, and replacing aging

vehicles represents one-half of SEPTA’s $4.6 billion State of Good Re-

pair project backlog. Our state and federal governments made major

investments when transportation infrastructure was originally built, but

investments have not kept pace with the needs of an aging system.

There are many factors contributing to this problem:

• Gas tax revenue continues to shrink. Approximately 75% of PennDOT’s highway and bridge funding

comes from federal and state gas tax revenue, which continues to decline. Fuel economy improve-

ments and the transition to alternative fuels and electric vehicles—positive trends in themselves—will

continue to reduce gasoline and diesel consumption, and, therefore, the revenue from the Liquid

Fuels tax. In recent months some major vehicle manufacturers have announced their complete con-

version to electric vehicles by the next decade (in fact Pennsylvania is home to some of the leading

companies pioneering the transition, including Mack Trucks). The current projected growth in elec-

tric-powered vehicles is steep, with corresponding declines in gas tax revenue.

• Act 44 and Act 89 didn’t solve the whole problem. PA Act 44 of 2007 and PA Act 89 of 2013 provided

urgently needed infusions of predictable funding to shore up transportation statewide, particularly our

public transportation systems. However, these acts only addressed part of the funding need. In fact,

Act 44 and Act 89 created a debt of $14 billion for the Pennsylvania Turnpike Commission by diverting

toll revenue to PennDOT. The Turnpike has consequently been forced to raise tolls every year. In July

2022, the $450 million annual Turnpike payment to PennDOT drops to $50 million. To replace that

amount, $450 million per year in vehicle sales tax revenue is to be transferred from the General Fund

to PennDOT. The preservation of Act 89 transportation investment levels is crucial in order to meet

service demands and address multimodal infrastructure maintenance and rehabilitation issues.

• Emergency repair needs have increased dramatically. PennDOT budgets $30 million per year for

emergency repairs, such as landslides and washouts. In Fiscal Year 2018-19 alone, the state experi-

enced severe flooding that caused $120 million in road and bridge damage. Although PennDOT in-

corporates practices proven to make infrastructure more resilient to natural disasters, severe weather

events combined with aging infrastructure have resulted in emergency repairs becoming more fre-

quent and more costly. These cost pressures require that more resources be used for maintenance,

which in turn constrains the ability to make other improvements, including those that add system

capacity. Responsible investment levels are necessary to prevent such downward spirals.

• Federal pavement condition requirements for Interstates are more stringent. Interstate highways,

which carry 26% of all vehicle-miles traveled in Pennsylvania, must meet rigorous pavement stan-

dards and be maintained proactively to lower overall costs. Although PennDOT supports this “asset

management” approach, keeping our Interstates in compliant condition requires diverting funds from

other state and local needs (as noted previously: $150 million diverted in FFY 2021, increasing $50

million per year until Interstate investment reaches $1 billion in FFY 2028). Federal policy, understand-

Our state and federal

governments made

major investments

when transportation

infrastructure was

originally built, but

investments have not

kept pace with the

needs of an aging system.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

12

ably protective of the Interstate Highway System, underscores the importance of committed invest-

ment in transportation assets—including more federal funding (see next item) to align with the policy

and regulatory requirements imposed on states.

• Federal transportation gas tax funding hasn’t increased since 1993. When federal funding does not

keep pace with the nation’s needs, federal mandates, and inflation, state governments must fill the

void. However, the Commonwealth does not have the financing tools of the U.S. government. State

government, as the responsible operator of the transportation system, has no choice but to continue

to provide the most-critical funding while advocating for a fresh federal vision and the investment that

goes with that vision.

• Deferred maintenance costs more in the end. When there isn’t enough funding to cover needs,

PennDOT must delay repairs. When we as Pennsylvanians choose not to invest in preventative main-

tenance—year after year—small problems escalate into major reconstruction projects. PennDOT’s

maintenance program has been constrained to a troubling extent for more than a decade. History

teaches us that the “Maintenance First” policy of the late 1970s and 1980s restored Pennsylvania

transportation. That dicult lesson need not be repeated.

• Inflation erodes purchasing power. As shown in Figure 4, inflation alone costs PennDOT more than

$100 million per year as the costs of construction materials and labor continue to sharply increase.

Transportation revenue is not currently indexed to or regularly adjusted for inflation.

billions

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

Buying Power

Revenue - Projected

Revenue - Flat

FY 30-31FY 29-30FY 28-29FY 27-28FY 26-27FY 25-26FY 24-25FY 23-24FY 22-23FY 21-22FY 20-21FY 19-20FY 18-19

$7.6 billion cumulative loss in buying power

FY 2021-22 through FY 2030-31

Figure 4: PennDOT Loss in Buying Power

Impact of Inflation and Reduced Consumption on Motor Fuels Revenue

Buying power loss calculated using the PennDOT Composite Index

value of 3.19% per year—the 10-year average price increase for the

period 2010-2020. The PennDOT Composite Index factors in the

Bid Price Index, Construction Cost Index, and Consumer Price Index.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

13

PennDOT Eciencies and Innovation

PennDOT continuously evaluates its operations to find opportuni-

ties to enhance eciency and save money. The Department has

saved nearly $100 million over the past five years and is a leader in

Lean organizational eciency practices. Department stang levels

continue to trend downward. PennDOT is also applying the 2012

law that made public-private partnerships (P3) an option in deliver-

ing new or improved transportation services.

PennDOT’s 2021 Eciencies Report provides 90 examples of how

the Department uses technology to improve customer service

and enhance projects while streamlining costs. The report is avail-

able at: https://www.penndot.gov/about-us/funding/Documents/

TROC-Meeting_04-15-21/TROC_4-15-21_PennDOT-Eciencies-Re-

port.pdf.

The Department launched PennDOT Pathways in November 2020

to analyze new future-focused sources of funding for our trans-

portation system that could better serve our communities and all

Pennsylvanians for the next generation. Public input was sought

and nearly 6,000 people participated online. As part of PennDOT

Pathways, PennDOT has undertaken a Planning and Environmental

Linkages (PEL) study to identify near- and long-term funding solu-

tions and establish a methodology for their evaluation. PennDOT is

advancing the Major Bridge P3 Initiative as part of PennDOT Path-

ways. See PennDOT.gov/funding for more on PennDOT Pathways.

$38.5 million

saved over three years

by using lower-cost materials

for secondary roads

$10 million

saved over five years

by implementing

eciency improvements

identified by

PennDOT employees

(WorkSmart and IdeaLink

programs)

P3

A Public-Private

Partnership to replace

558 bridges was part of

PennDOT’s reduction in

poor-condition bridges

from more than 6,000 in

2008 to 2,500 today.

$49 million

saved over four years

through the

County Accreditation

Program

PennDOT continuously

evaluates its operations

to find opportunities to

enhance eciency and

save money.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

14

Consequences of Insucient Funding

PennDOT has been forced to steadily reduce the size of its construction program, from $2.5 billion in 2015

to $1.6 billion in 2020. The current value of anticipated construction lettings for 2021 is $1.9 billion. The

significant decline in annual lettings directly translates to a serious shortfall in maintaining our roads and

bridges and causes real impacts to the thousands of private-sector jobs that are supported by engineer-

ing, construction, maintenance, and services performed for PennDOT.

The consequences of insucient investment in transportation infrastructure are varied and compounding.

Among the direct and indirect consequences:

• Greater congestion and the cost associated with travel delay

• Potential closures of bridges and lane reductions

• Potential impacts on the safety and reliability of travel

• Longer-term costs associated with deferred maintenance

and other improvements

• Decreased economic competitive position—transportation

often ranks high in companies’ decisions about facility lo-

cations

• Diminished quality of life

Inadequate capital investment can have a troubling domino eect. For example, a lack of investment in

public transportation can decrease the number of transit vehicles available to provide service. This can re-

sult in decreased levels of service, including frequency, service span, and access for riders. Lack of service

means diminished access to jobs, education, medical appointments, and other important trips provided by

transit. It can also decrease the number of transit jobs.

Aging transit vehicle fleets

threaten the ability to

provide reliable service

connecting Pennsylvanians

to jobs, medical care, and

community life.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

15

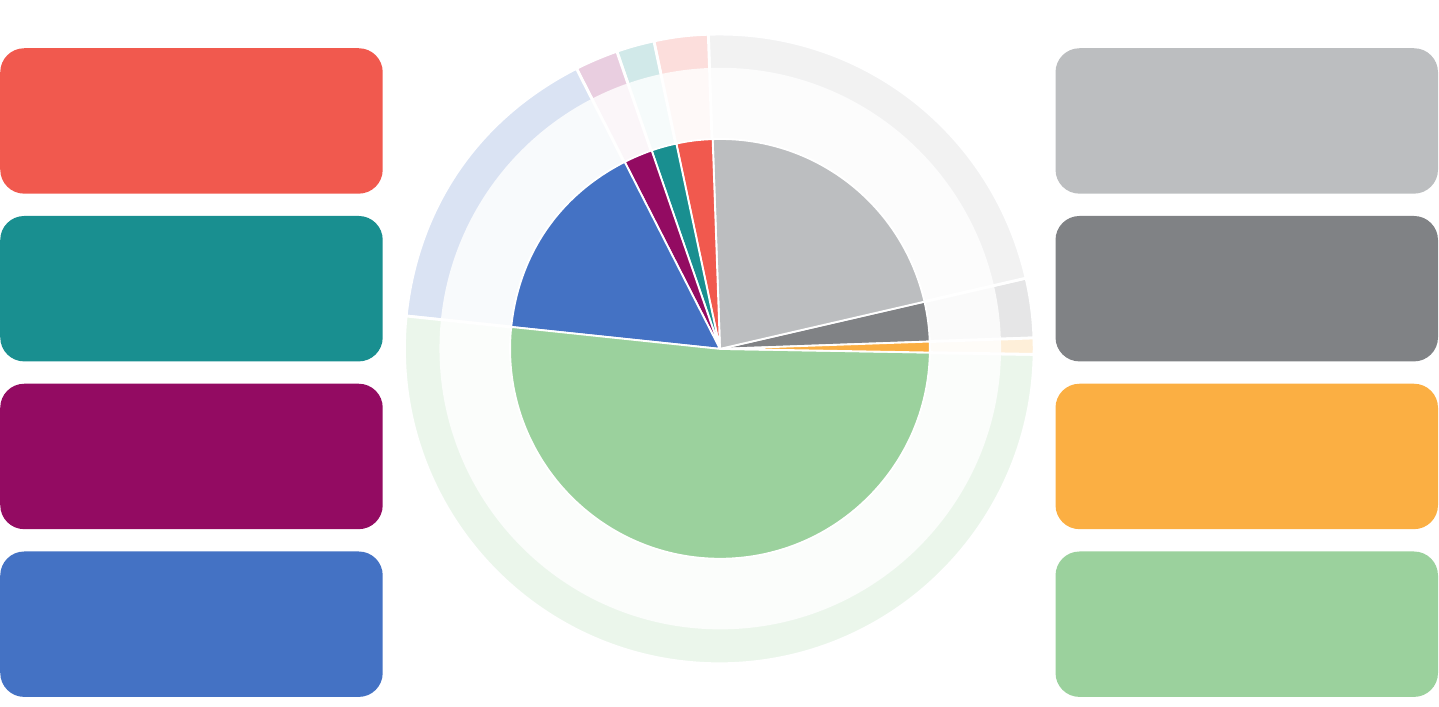

1%

Other Funds

52%

PA Motor

License Fund

3%

Federal Funds –

Multimodal

21%

Federal Funds –

Highway & Bridge

3%

PA Public

Transportation

Assistance Fund

2%

PA Lottery Fund

2%

PA Multimodal

Transportation

Fund

16%

PA Public

Transportation

Trust Fund

$8.8 billion annual budget

(Fiscal Year 2021-22)

The Commonwealth provides approximately 75% of PennDOT's annual

budget; 25% comes from federal funds. State and federal fuel taxes are

the revenue source for three-quarters of PennDOT's highway and bridge

funding (via the federal Highway Trust Fund and the PA Motor License

Fund). Fuel tax revenue continues to decline as improved fuel eciency

and alternative fuels (including electric vehicles) reduce demand for gaso-

line and diesel.

PennDOT’s Current Funding Sources and Restrictions

Figure 5: PennDOT’s Current Funding by Source

$280M

$170M

$150M

$1.41B

$4.59B

$70M

$250M

$1.92B

PA Transportation Revenue Options Commission Final Report – July 30, 2021

16

Motor License

Fund Accounts &

Liquid Fuels Tax

Fund

Capital Facilities

Fund

Public

Transportation

Trust Fund & Public

Transportation

Assistance

Fund

Motor License Fund

Aviation Restricted

Account

General Fund

Multimodal

Transportation

Fund

$

$

$

$

$

$

● Sales Tax Transfers to Dedicated Transit Funds

● PA Turnpike Commission Contributions

● Lottery Fund Payments and Transfers

● Motor Vehicle Fees and Civil Penalties/Fines

● Federal Capital/Operating Grants (Non-Urban)

● Capital Facilities Fund Bonds (General Fund)

● Treasury Investment Earnings

● Jet Fuel and Aviation Gasoline Taxes

● Federal Airport Development Capital Grants

● Capital Facilities Fund Bonds (General Fund)

● Treasury Investment Earnings

● Unconventional Gas Well Fund

● Capital Facilities Fund Bonds (General Fund)

● Motor Vehicle Fees

● PA Turnpike Commission Contribution

● Oil Company Franchise Tax Transfer

● Treasury Investment Earnings

● General Fund Non-Restricted Revenues

● Oil Company Franchise Tax

● Driver and Vehicle Fees

● Federal Project Reimbursement

(State Projects)

● Federal Project Reimbursement

(Local Projects)

● Treasury Investment Earnings

★ Fixed-Route Operating Assistance Grants

★ Fixed-Route Asset Improvement Grants

★ Older Pennsylvanians Fixed-Route/Shared-

Ride Subsidies

★ Intercity Passenger Rail and Bus Subsidies

★ Persons with Disabilities Transportation

Subsidies

★ State Match for Federal Access Programs

★ Airport Development Grants for Facilities

and Equipment

★ Real Estate Tax Rebates

★ Aviation Safety and Licensing

★ Grants for Track Improvements, Land

Acquisition, and Facilities Construction

★ Reimbursement for Collection of Vehicle

Sales Tax and Processing Voter Registration

★ Debt Service for Multimodal (TAP) Bonded

Projects

★ Public Transportation Infrastructure Projects

★ Act 89-Directed Freight Rail, Ports/

Waterways, Passenger Rail, Aviation, and

Bicycle/Pedestrian Grants

★ Commonwealth Financing Authority Grants

★ PennDOT Statewide Program Grants

★ Highway and Bridge Reconstruction/

Construction

★ Highway Maintenance, Repair, Operations,

and Safety

★ Local Maintenance and Improvement Grants

★ Driver and Vehicle Services

★ Welcome Centers

★ State Police Highway Patrol

HIGHWAYS & BRIDGES

AVIATION

RAIL FREIGHT

ALL MODES

VARIOUS MODES

PUBLIC TRANSPORTATION

Figure 6: PennDOT Revenue Sources and Uses by Mode

PA Transportation Revenue Options Commission Final Report – July 30, 2021

17

A New Funding Approach is Essential

The gas tax, once a fair and sustainable way to pay for roads and bridges, is antiquated and inadequate.

Pennsylvania relies to a much greater extent than other states on this eroding revenue source (Figure 7).

Together we need to find fair, feasible, future-oriented solutions to pay for all transportation modes.

Figure 7: Gas Tax as a Percentage of Total Transportation Revenue, by State

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Pennsylvania

West Virginia

Ohio

Maryland

New Jersey

Virginia

Delaware

New York

22%

26%

32%

41%

52%

60%

78%

18%

The gas tax, once a fair and sustainable way

to pay for roads and bridges, is antiquated

and inadequate. Pennsylvania relies to a

much greater extent than other states on this

eroding revenue source.

See page 31 for more detail on the composition of other states’ transportation revenue sources.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

18

Proposed Commonwealth

Transportation Funding Strategy

Principles

As part of its evaluation, TROC followed several guiding principles to shape the strategic funding proposal:

• User Pays – Direct users of the transportation system should generally bear most of the burden of

funding that system. Historically this has been an overarching principle, as reflected in the gas tax.

• Be Fair – Equitable solutions aim for a fair balance, considering how each revenue source impacts

various segments of the population, specifically around the ability-to-pay concern as well as urban vs.

rural issues.

• Diversify the Revenue Base – This principle complements the “user pays” concept, recognizing that

even those not owning a vehicle or directly traveling on the transportation system benefit from it and

should contribute.

• Build in Predictability and Stability – Gas tax revenue continues to decline and therefore is not a sta-

ble revenue source. The funding proposal must have a reasonable degree of predictability and stabil-

ity over the long term to allow multi-year planning, design, and construction projects to move forward.

• Index to Inflation – The cost of improving and maintaining our multimodal transportation system is

impacted by inflation in the same way that price increases aect other industries, products, and ser-

vices. New revenue sources must keep pace with inflation.

• Reduce Funding Restrictions – Many of PennDOT’s current funding sources can only be spent on

certain modes or on certain parts of the system (e.g., state vs. local roadways). New sources that oer

greater flexibility to meet the various modal and local network needs are more beneficial than ear-

marked sources.

• Ensure Near-Term Feasibility – Pennsylvania’s funding problem is particularly challenging because it

cannot wait for a long-term solution. Until a long-term fix such as a Mileage-Based User Fee is feasible

nationally (and there is no guarantee of that), Pennsylvania’s funding package must be implemented

rapidly to address immediate needs and to sustain the system over the next decade and beyond.

• Simplify Administration – Burdensome administrative or enforcement requirements could pose a

serious barrier for some potential revenue sources and reduce their net value to the Commonwealth.

• Learn from Other States – All states face transportation funding challenges similar to Pennsylvania’s,

and most are actively modernizing their funding strategies, providing experience that can inform our

eorts.

TROC referred to these principles throughout its analysis of funding options, and the funding proposal

meets these principles to the extent practicable.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

19

$0

$2

$4

$6

$8

$10

$12

$14

Funding Gap

PHASE 3PHASE 2PHASE 1

billions

Years 1 and 2 Years 3 and 4 Year 5 and beyond

$9.35

$10.31

$11.37

Funding Target

$3.5

$6.6

$11.5

Phases and Funding Targets

The state-level need for additional funding, as described in the previous chapter, is $9.35 billion, increasing

each year. TROC recognizes that fully closing that gap will require several years due to the time needed to

implement new revenue sources. However, we must begin to systematically close that gap and generate

near-term and medium-term revenue while working toward longer-term solutions.

TROC therefore developed a three-phased approach to its proposal and established target levels for

additional funding by phase (Figure 8). The proposed totals by phase are responsible and feasible levels

of annual additional revenue for necessary transportation improvements:

• Phase 1 (Years 1 and 2): $3.5 billion

• Phase 2 (Years 3 and 4): $6.6 billion

• Phase 3 (Year 5 and beyond): $11.5 billion

There is a general consensus that although the funding need is not fully

met until Phase 3, the funding targets represent substantial, systematic

progress, moving Pennsylvania in the right direction. As the TROC propos-

al is acted upon it is of paramount importance that the revenue targets by

phase not become diluted.

TROC’s deliberations about proposed revenue sources occurred in the context of ensuring that the total

funding targets by phase were maintained. Throughout the process the combinations and dollar values

of proposed revenue sources were refined numerous times, always with an eye toward preserving the

bottom-line revenue total for each phase.

Figure 8: Funding Targets by Phase

Feasible funding

targets by phase

aim to close the

funding gap

over time.

As the TROC proposal

is acted upon it is of

paramount importance

that the revenue

targets by phase not

become diluted.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

20

Proposed Revenue Sources Overview

TROC members collaborated in eight work groups followed by subsequent deliberations of the work-

group leaders. Work groups followed a systematic process for evaluating the various revenue options

using detailed scenario spreadsheets, developing several draft proposals, and refining the proposal to

arrive at the recommended set of revenue options. The Strategic Funding Proposal (Figure 10) is the heart

of this document. It provides a brief description and rationale for each proposed revenue source, along

with assumptions and the basis for the revenue estimate.

This section briefly highlights each of the six proposed revenue categories. The overall mix of revenue

sources proposed is:

• A balanced, reasonable, and responsible approach.

• Generally similar to other states that have broadened their transportation revenue bases.

• Largely aligned with the “user-pays” principle rather than calling for corporate, personal, or other

general taxation sources.

• Flexible enough to address the needs of all modes of transportation.

• Structured to provide a foundation for more funding for local needs.

• Future-focused, with revenue sources that prepare for long-term solutions while addressing immedi-

ate needs.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

21

Road User Charges

The proposed Road User Charges consist of two sources: Mileage-Based User Fees (MBUF) and an Elec-

tric Vehicle (EV) MBUF Pilot. MBUF presently appears to be the best long-term funding solution for Penn-

sylvania, and likely for all or most states. As Figure 10 shows, MBUF is not assumed to yield revenue until

Phase 3 (which would not likely be year 5 but possibly year 10 or beyond). The proposed Electric Vehicle

MBUF Pilot is a major step toward preparing for MBUF by charging on a per-mile basis for vehicles for

which the operator is not paying the gas tax. Overall, road user charges are considered to be both feasible

and fair.

Revenue Category: Road User Charges

Strengths/Benefits Potential Concerns

• MBUF nationally is assumed to be the

long-term likely direction for the nec-

essary restructuring of transportation

funding.

• Provides the ultimate replacement for

the phasing-out of the gas tax.

• Leverages technology, which is a great

driver of change for all of transporta-

tion.

• Is a revenue mechanism based directly

on the use of the transportation system.

• Could encourage some carpooling to

lower the cost-per-passenger per mile.

• Assumed to be flexible across transpor-

tation modes.

• MBUF is not yet a certainty, even for

Phase 3 (which is why other proposed

sources should be implemented and

could stay in place if MBUF does not

occur).

• A perception of public resistance to the

tracking associated with MBUF.

• Depends extensively on federal leader-

ship and implementation coordinated

with neighboring states.

Considering MBUF strategically, TROC proposes a long-term Commonwealth commitment to positioning

and preparing for MBUF by vigorously encouraging supportive federal action, raising public awareness

and support, and beginning to lay the groundwork for the technological and other implementation com-

ponents.

Such commitment is essential, but it does not address Pennsylvania’s immediate funding problem. There-

fore, it is vital to identify and implement multiple near- and medium-term funding sources, as highlighted

on the following pages.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

22

Tolling

The two proposed tolling sources are corridor tolling and managed lanes (limited lane tolling). Corridor toll-

ing of Interstate highways and expressways based on distance traveled is both feasible and fair (especially

as the gas tax phases out). Recognizing that the Interstate Highway System is aging and in great need of

repair and modernization, some believe that tolling of such higher-volume highways may be inevitable.

A managed lane is a lane on a highway on which the trac is regulated by charging a toll or by encourag-

ing carpooling. A managed lane can take the form of either an express lane in which all users are charged

a toll for use, or a high-occupancy-toll (HOT) lane that allows high-occupancy vehicles (HOV) free passage

while single-occupancy vehicles (SOV) are charged a toll. PennDOT has the authority to implement man-

aged lanes, so managed lanes are a near-term solution. More planning and studies are needed to identify

candidate roadways where managed lanes would be appropriate.

TROC believes that corridor tolling and some use of managed lanes in high-volume corridors represent

a medium-term approach to meeting part of the transportation funding need. No revenues are assumed

until Phase 2 (years 3 and 4) based on policy clearances, physical set-up of tolling infrastructure, and other

technical considerations.

Revenue Category: Tolling

Strengths/Benefits Potential Concerns

• Provides significant revenue in the

medium term.

• Based on the “user pays” principle.

• Helpful in transitioning to MBUF.

• Uses existing technology.

• Could create diversion to lower-volume

routes (this concern was expressed by

the PA Motor Truck Association and the

PA Bus Association, which also stated

that toll and registration fee increases

disproportionately impact commercial

vehicles).

• Raises ability-to-pay issues that are

associated with almost any tolling

strategy.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

23

Redirection of Funding

This category includes one proposed revenue source: eliminating transfers from the Motor License Fund

(MLF) to the Pennsylvania State Police, assuming replacement of that budgetary item from the General

Fund. The rationale has been substantially vetted not only by TROC but by the State Transportation Advi-

sory Committee (TAC) and others.

The proposition is that policing, whether state or local, is a general function of government and that the

Motor License Fund’s revenue sources are more aligned with transportation system use. The PA State Po-

lice obviously carry out an essential responsibility and one that is stretched by having to police some com-

munities that do not have municipal police forces. That challenge also necessitates a broader approach to

police funding outside of the Motor License Fund. The feasibility of this proposed redirection is high and

is deemed to be fair.

Revenue Category: Redirection of Funding

Strengths/Benefits Potential Concerns

• Provides needed funding for transpor-

tation in all three phases.

• The General Assembly’s actions to date

begin to move in this direction.

• Places further pressure on the General

Fund.

View the TAC study on

PA State Police funding sources:

https://www.talkpatransportation.com/perch/resources/documents/

pspfundingoptionswhitepaper.pdf

PA Transportation Revenue Options Commission Final Report – July 30, 2021

24

Fees

Various new or increased fees are proposed:

• Vehicle Registration Fee

• Electric Vehicle Fee

• Vehicle Lease Fee

• Vehicle Rental Fee

• Transportation Network Company (rideshare) Fee

• Aircraft Registration Fee

• Goods Delivery Fee

Taken together, these fees represent reasonable pricing in step with transportation system needs. They

also yield stable revenue in all three phases. It is possible that the electric vehicle fee might yield more

revenue than TROC’s conservative estimate as some forecasters are projecting a sharper increase in the

number of electric vehicles within a few years.

Revenue Category: Fees

Strengths/Benefits Potential Concerns

• Provides needed funding for transpor-

tation in all three phases.

• Electric vehicles are projected to pro-

gressively be a larger percentage of the

vehicle fleet.

• Provides a means for operators of elec-

tric vehicles to pay for their use of the

system as they do not pay gas tax.

• Aircraft may be the only form of trans-

portation that does not yet have Penn-

sylvania registrations. This fee would

be an important source for airport

improvements that would also benefit

airplane owners.

• The Goods Delivery Fee represents a

sensible adjustment to the changing

nature of package delivery, especially

since the pandemic. Generally this fee

is more than oset by cost savings

associated with the reduction of travel

expense and time to purchase goods.

• The Vehicle Registration Fee adjust-

ment is a large change in terms of per-

centage, but the dollar amount better

aligns the pricing with system needs.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

25

Taxes

Three proposed tax adjustments comprise this revenue source category—increases to the present vehicle

sales tax and the jet fuel tax, as well as indexing the gas tax to inflation.

Revenue Category: Taxes

Strengths/Benefits Potential Concerns

• The proposed increase in the vehicle

sales tax provides substantial revenue

over each phase—this is especially

important as a Phase 1 and Phase 2

revenue source.

• Use of the vehicle sales tax is not

restricted, allowing use for the various

modes.

• Corrects a fundamental flaw with the

gas tax that it is not fully inflation-ad-

justed (this will be especially important

to the overall revenue picture even as

the gas tax is being phased out).

• The jet fuel tax proposed increase is

modest, particularly in light of being

essentially unchanged for several

decades.

• Jet fuel tax proceeds would be invest-

ed in PA airports, providing needed

improvements that benefit the industry

and the communities they serve.

• Allegheny and Philadelphia counties’

vehicle sales tax would be 9% and 10%,

respectively, as compared to the 8%

level for the rest of the state (all rates

would increase by 2% as detailed on

Figure 10).

• Possible impact on dealers’ vehicle

sales.

Other

Other proposed revenue sources include an Ad Valorem Vehicle Tax (for passenger vehicles only) based

on the value of the vehicle. Also in this category are two revenue osets, one that reflects the reduction in

registration fees associated with those paying the Ad Valorem instead, and the other reflecting the Phase

3 elimination of the gas tax.

Revenue Category: Other

Strengths/Benefits Potential Concerns

• Ad Valorem provides a progressive

revenue element linked to the ability to

pay.

• The Ad Valorem rate translates to a rea-

sonable dollar amount at the proposed

level, and provides a sustained annual

revenue source.

• Perception challenge that the value of

a vehicle should not bear on the cost of

registration. However, progressivity has

long been a part of non-transportation

taxation structures.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

26

The TROC proposal

is an integrated

package that

achieves the

funding targets

for each phase of

implementation.

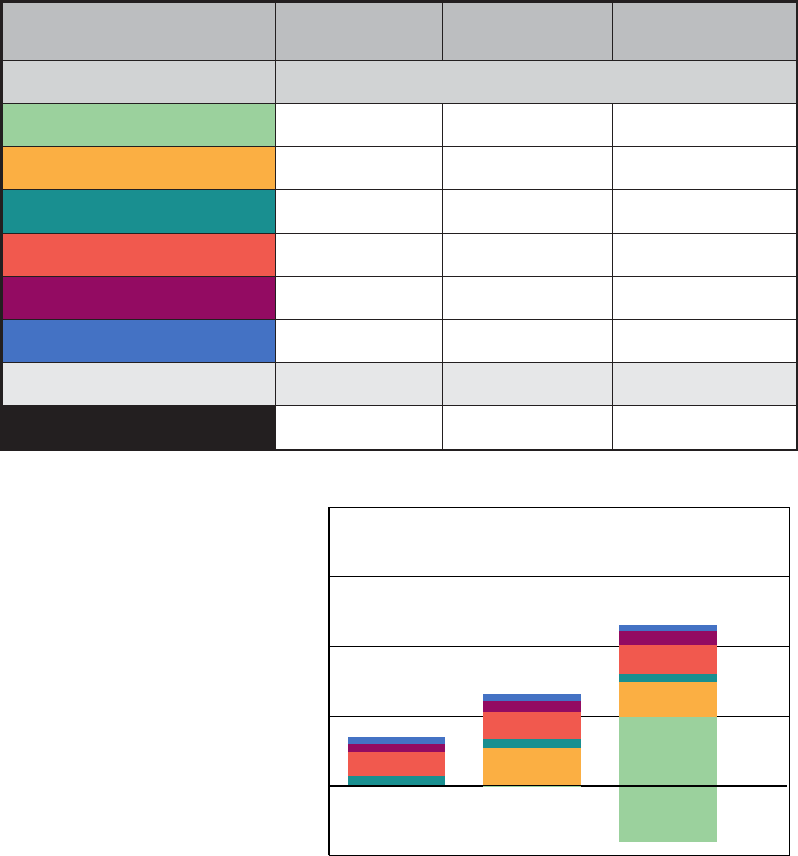

Figure 9: Funding Proposal Summary by Revenue Type

$-5

$0

$5

$10

$15

$20

Other

Taxes

Fees

Funding Redirection

Tolling

Road User Charges (MBUF)

billions

PHASE 3PHASE 2PHASE 1

Years 1 and 2 Years 3 and 4 Year 5+

Portion of MBUF

replaces gas tax

$3.47

$6.56

$11.48

-$4.09

PHASE 1

(Years 1 and 2)

PHASE 2

(Years 3 and 4)

PHASE 3

(Year 5+)

PROPOSED REVENUE TYPE ESTIMATED ADDITIONAL REVENUE

Road User Charges (MBUF) $2,000,000 $2,122,000 $8,932,316,000

Tolling $0 $2,705,040,000 $2,543,716,000

Funding Redirection $673,000,000 $609,000,000 $545,000,000

Fees $1,712,420,000 $1,991,864,000 $2,072,438,000

Taxes $635,167,000 $786,798,000 $992,343,000

Other $450,000,000 $468,180,000 $487,095,000

Eliminate Gas Tax $0 $0 -$4,088,301,000

TOTAL $3,472,587,000 $6,563,004,000 $11,484,607,000

TROC Strategic Funding Proposal

The proposed funding sources are an integrated set of options to address established needs. The dollar

targets for each phase are a step toward addressing the most critical needs and establishing stability and

predictability for PennDOT’s budget. Therefore, if individual components of the proposal are not imple-

mented, the resulting gaps must be closed with other options.

Figure 9 summarizes proposed sources of additional revenue by phase; the detailed proposal table is

presented in Figure 10.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

27

ESTIMATED ADDITIONAL ANNUAL REVENUE

PROPOSED REVENUE SOURCE DESCRIPTION BRIEF RATIONALE

PHASE 1

(Years 1 and 2)

PHASE 2

(Years 3 and 4)

PHASE 3

(Year 5 and Beyond)

ASSUMPTIONS AND

BASIS FOR ESTIMATE USE RESTRICTIONS

ROAD USER CHARGES

Mileage-Based User Fee (MBUF) Implement an 8.1-cents-per-mile MBUF on

all miles traveled in Pennsylvania.

MBUF is the long-range funding solu-

tion for gas tax replacement. National

implementation is expected; PA has the

opportunity to prepare.

$0 $0 $8,930,065,000 8.1 cents per mile would yield the

targeted revenue amount (at 102

billion miles traveled multiplied by

8.1 cents).

No restriction on use.

Electric Vehicle (EV) MBUF Pilot Implement a pilot MBUF for electric

vehicles.

The growing prevalence of electric

vehicles provides a useful pilot to prepare

for MBUF and to capture a fair share of

revenue from those using the system but

not paying gas tax.

$2,000,000 $2,122,000 $2,251,000 Rate determined by the targeted

additional revenue of $2 million.

No restriction on use.

TOLLING

Corridor Tolling Toll Interstates/expressways based on the

distance traveled along that highway.

Corridor tolling supports transition to

MBUF implementation. Trac volumes

support corridor tolling.

$0 $2,444,940,000 $2,543,716,000 Rate determined by the targeted

additional revenue of $2.4 billion.

No restriction on use.

Managed Lanes

(Limited Lane Tolling)

Toll additional lanes on a highway where

the trac is regulated by charging a toll

or by encouraging carpooling.

Managed lanes are a revenue-raising

mechanism suitable for a limited number

of high-volume roads or road segments.

Revenues flow to the improvement and

maintenance of the facility, not to other

purposes.

$0 $260,100,000 $0 Rate determined by the targeted

additional revenue of $260 million.

Restricted to State Highways and

Bridges.

REDIRECTION OF FUNDING

PA State Police Funding Eliminate transfers from the Motor License

Fund (MLF) to the State Police and replace

those amounts from the General Fund.

MLF dollars should be used for transpor-

tation; other more appropriate funding

sources should be used for State Police.

$673,000,000 $609,000,000 $545,000,000 The PSP amount currently to be

paid out of the Motor License Fund

per the Fiscal Code Reduction.

Restricted to State Highways and

Bridges.

FEES

Vehicle Registration Fee Increase all vehicle registration fees

100%.

The proposed increase aligns with the

"user pays" principle and brings the fee

more in line with costs to improve, main-

tain, and operate the system.

$800,000,000 $832,320,000 $865,946,000 The current Department of Reve-

nue (DOR) estimate is $799 million

for FY 2021-22.

Restricted to State Highways and

Bridges.

Electric Vehicle Fee Introduce a $275 fee for electric vehicles

and eliminate the Alternative Fuels Tax on

electric vehicles.

Electric vehicles are a rapidly increasing

percentage of the total vehicle fleet, but

do not pay taxes that are tied to Liquid

Fuels.

$4,650,000 $4,939,000 $5,242,000 Assumes a higher conversion to

electric vehicles in Phases 2 and 3.

Restricted to State Highways and

Bridges.

Vehicle Lease Fee Increase current rate from 3% to 5%. This aligns with the "user pays" principle

for drivers who choose to lease a vehicle

rather than buy.

$67,000,000 $69,707,000 $72,523,000 Calculated by multiplying 1% of the

fee revenue ($32.883 million) by 5.

Restricted to Multimodal–Mass

Transportation.

Aircraft Registration Fee Introduce a $50 registration fee for all

aircraft in Pennsylvania.

Owners of PA-based aircraft should pay

a registration fee as do owners of motor

vehicles, motorcycles, etc.

$320,000 $333,000 $346,000 Calculated by multiplying 6,200

aircraft by a $50 fee.

Restricted to Multimodal–Aviation.

Continued next page

Figure 10. Strategic Transportation Funding Proposal

PA Transportation Revenue Options Commission Final Report – July 30, 2021

28

ESTIMATED ADDITIONAL ANNUAL REVENUE

PROPOSED REVENUE SOURCE DESCRIPTION BRIEF RATIONALE

PHASE 1

(Years 1 and 2)

PHASE 2

(Years 3 and 4)

PHASE 3

(Year 5 and Beyond)

ASSUMPTIONS AND

BASIS FOR ESTIMATE USE RESTRICTIONS

FEES, continued

Transportation Network Company

Fee (Uber, Lyft, taxis, etc.)

Establish a $1.10 per-trip fee on all TNCs

and taxis in Pennsylvania.

TNC use represents a growing portion of

passenger transportation that relies on

the roadway system.

$0 $210,161,000 $218,651,000 Calculated by an estimated 162.9

million TNC trips and 20.9 million

taxi trips at a rate of $1.10 to reach

the targeted revenue amount.

No restriction on use.

Vehicle Rental Fee Increase current fee per rental from

$2 to $5.

This updates the amount of an estab-

lished fee to a reasonable level.

$60,450,000 $62,892,000 $65,433,000 Calculated by multiplying 1% of the

fee ($20.150 million) by 5.

Restricted to Multimodal–Mass

Transportation.

Goods Delivery Fee Establish a $1 fee on all deliveries to an

end point in Pennsylvania.

Significant increases in package deliv-

ery volumes impose maintenance and

improvement costs on the state and local

road network.

$780,000,000 $811,512,000 $844,297,000 Calculated by multiplying

780 million trips by $1.

No restriction on use.

TAXES

Vehicle Sales Tax

Increase tax from 6% to 8% (Pittsburgh

and Philadelphia rates would increase

from 7% to 9% and from 8% to 10%,

respectively.)

This increase aligns directly with system

use and increased needs.

$550,000,000 $572,220,000 $595,338,000 Estimated vehicle sales for

FY 2021-22 of $1.8 billion,

assuming a 33% increase of

$600 million.

No restriction on use.

Gas Tax Index gas tax to inflation. Remaining gas tax proceeds must be

adjusted to keep pace with inflation.

$75,000,000 $204,000,000 $386,000,000 Calculated as the dierence

between the PA Department of

Revenue (DOR) gas tax revenue

estimate and a 2%* increase per

year in gas tax revenue.

Restricted to State Highways and

Bridges.

Jet Fuel Tax Increase tax from 1.5 cents to 4 cents per

gallon.

This is a modest increase to a tax that has

not been adjusted in nearly four decades.

$10,167,000 $10,578,000 $11,005,000 The latest DOR estimate is $6.1

million at 1.5 cents per gallon.

Raising to 4.0 cents would yield the

calculated additional amount.

Restricted to Multimodal–Aviation.

OTHER

Ad Valorem (Value-Based) Vehicle

Tax

Tax passenger vehicles annually based on

their current value.

Taxing the value of a vehicle better aligns

revenue with users' ability to pay versus a

flat fee. (See reduction to registration fees

in next line item.)

$800,000,000 $832,320,000 $865,946,000 Rate determined by the targeted

additional revenue of $800 million;

assumes same rate for all types of

vehicles.

No restriction on use.

Reduction to Registration Fees with

Ad Valorem

Oset to vehicle registration increases on

passenger vehicles with an Ad Valorem

tax.

An oset of vehicle registration fees with

the associated shift of the passenger

vehicle fleet to Ad Valorem.

-$350,000,000 -$364,140,000 -$378,851,000 Oset to vehicle registration

increases.

Reduces Highways and Bridges in-

crease but still an overall increase.

Elimination of Gas Tax with full

MBUF

Replace most of gas tax proceeds with

MBUF in Phase 3.

This long-range cost adjustment would

reflect the implementation of MBUF.

$0 $0 -$4,088,301,000 Replacing the gas tax with MBUF.

DOR estimate for Year 5 plus the

gas tax indexing increase.

Would reduce multiple areas but

could be oset in MBUF.

TOTAL $3,472,587,000 $6,563,004,000 $11,484,607,000

Continued from previous page

Notes:

Major Bridge P3 – The major bridge projects presently being evaluated as part of PA Pathways are not included in the Strategic

Funding Proposal as revenue sources. These are discrete candidate bridge projects that have already been identified. The reve-

nues would cover the costs of the improvement and maintenance and would not be available for addressing other unmet funding

needs. The Managed Lanes revenue option that is being proposed has not identified discrete projects, yet the same principles

generally apply.

Transition from the Gas Tax – The Pennsylvania Turnpike Com-

mission has issued bonds secured by its portion of the Oil Compa-

ny Franchise Tax (OCFT), and that portion of the tax would need to

remain in place until the OCFT bonds are retired.

*Inflation Rate – 2% annual inflation is used in the projections, however the

rate should be adjusted at least according to the Consumer Price Index.

Given the volatility of construction materials prices, experience suggests

that the actual inflation rate could exceed 2% per year.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

29

Revenue Options Considered but Not Included in the TROC Proposal

Some TROC members have suggested broadening the revenue base to include general taxation sources

such as corporate income tax. However, TROC overall does not favor this revenue option, preferring to

develop a proposed funding package that largely adheres to the “user pays” principle.

Other potential revenue sources as wide-ranging as taxation on marijuana if legalized, sports wagering,

and bicycle fees were discussed but deemed to be less promising or less appropriate for transportation

funding—including the concern over any revenue sources that may be at odds with public safety.

Funding Solutions Must Eectively Address All Modes

The proposed strategic funding proposal would make a substantial positive impact in addressing present

unmet need across the transportation modes. TROC emphasizes to policymakers the importance of the ul-

timate allocations of expanded revenue being flexible to ensure that each mode is eectively addressed.

Although roads and bridges have traditionally formed the framework of our statewide transportation sys-

tem, each transportation mode is essential for the ecient movement of people and goods.

Public Transportation

Public transportation—including fixed-route buses and shared-ride service (for seniors and people with

disabilities), intercity bus, intercity passenger rail (Amtrak), commuter rail, light rail, etc.—plays a critical role

in sustaining our economies, reducing congestion and transportation emissions, and ensuring access to

essential goods and services for millions of residents across the state. Non-motorized transportation facil-

ities that allow pedestrians and bicyclists to safely navigate are a vital link in providing first- and last-mile

connectivity, oering no-emissions travel alternatives that promote health, and expanding options for pop-

ulations who cannot or choose not to drive. Pennsylvania's investments in passenger rail, particularly the

Harrisburg-Philadelphia Keystone Corridor, have made this travel option extremely popular and growing

steadily (before the pandemic). Economic growth around stations has been a result.

Water Ports

Pennsylvania’s ocean, river, and Great Lakes ports in Philadelphia, Pittsburgh, and Erie are major economic

and transportation assets. The Commonwealth has made significant investments in water ports over the

years. TROC emphasizes that water port funding must remain a priority in the implementation of this stra-

tegic funding proposal.

Transportation for Seniors and People with Disabilities

The Commonwealth supports transportation for senior citizens and people with disabilities through various

statewide programs. Public transportation and paratransit (with lifts) provide the pathway to independent living

for people with disabilities and those who support community life (attendants, direct-support professionals, etc.).

Amtrak and other passenger rail systems are also important for both regional and statewide travel, and require

accessibility upgrades for both vehicles and stations. Further, many people with disabilities travel through the

Commonwealth in their own vehicles or are transported by family or support sta who use the roads and bridges

being discussed as part of PennDOT’s tolling initiative.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

30

Aviation

Pennsylvania’s system of commercial and general aviation airports provides an important support for the

economy through business and personal travel, and some smaller airports provide trac relief for larger

airports. Pennsylvania has historically delivered a modest (as compared to other modes) airport develop-

ment program providing grants to airports that provide a matching share on Federal Aviation Administra-

tion (FAA) funding. Moreover, PennDOT aviation funding has often been the primary source of funding for

many improvements that do not qualify for FAA funds.

Rail Freight

Pennsylvania is among the nation’s leaders in advancing public investment in rail freight. This has had

economic benefits as well as helping in many cases to reduce the number of trucks on the road and the

associated wear-and-tear caused by larger vehicles. The PA Transportation Advisory Committee previ-

ously evaluated the economic impacts of freight transportation and found a wide range of benefits (see

https://www.talkpatransportation.com/perch/resources/documents/economic-impact-of-railroads-in-penn-

sylvania-january-2005-execut.pdf).

Further Eciencies

As Pennsylvania modernizes its transportation funding strategy, state agencies and their partners should

continue to look for opportunities to reduce costs through partnerships and innovations. Examples sug-

gested by TROC members include:

• Streamlining the Commonwealth’s bidding and oversight procedures (as feasible while meeting fed-

eral requirements) to reduce a regulatory burden that may add 10% to 20% to project costs.

• Continuing to streamline the design and permitting process for project development to potentially

produce substantial time and cost savings. (Most permitting requirements are imposed on PennDOT

by other agencies, which highlights the need for inter-agency cooperation and coordination.)

• Expanding agency collaborations, such as between PennDOT and the PA Department of Community

and Economic Development for accessible community improvements such as curb ramps, between

PennDOT and the PA Department of Human Services for Medical Assistance Transportation Program

services, and between PennDOT and the PA Department of Aging for the senior shared-ride program.

• Exploring potential eciencies or revenue-sharing opportunities where PennDOT provides stang

support to other agencies to leverage funds and improve services.

• Pursuing branding and new advertising of PennDOT products and services, similar to the PA Depart-

ment of Aging’s use of a mascot (Gus the Groundhog).

PA Transportation Revenue Options Commission Final Report – July 30, 2021

31

Aging infrastructure, vast multimodal transpor-

tation networks, and funding shortfalls, while

pronounced in Pennsylvania, are experienced by

other states. The mix of revenue sources varies

greatly among the states. Many states employ

more diversified revenue sources than Pennsylva-

nia does at present. TROC endorses the principle

of broadening the revenue base while maintaining

the primary focus on transportation users. From

the examples below, based on the most recent

figures available for each state, some states have

embraced a direction relying on revenue sources

that are both transportation user- and non-user

based, including general taxation. Note: These

figures provide a general comparison only. Rev-

enues normally fluctuate somewhat year to year

and other states continue to update their funding

strategies.

• Pennsylvania relies on gas-tax-related sourc-

es for approximately 75% of its transportation

revenue, as compared to 26% in Virginia, 41%

in Maryland, 32% in New Jersey, 18% in New

York State, 60% in West Virginia, 22% in Del-

aware, and 52% in Ohio. This comparison un-

derscores Pennsylvania’s highly challenging

situation—being overly reliant on a declining

revenue source.

• Pennsylvania’s per-gallon gas tax is higher

than that of comparable states—57.6 cents per

gallon in Pennsylvania, as compared to Dela-

ware (23 cents), Maryland (39.49 cents), Mich-

igan (37.2 cents), Ohio (47 cents), and Virginia

(21.2 cents).

• Pennsylvania’s diesel tax, at 74.1 cents per

gallon, is also higher than those of the afore-

mentioned states. Delaware and Virginia are at

the low end with 22 cents per gallon and 20.2

cents per gallon, respectively. The closest state

to Pennsylvania in terms of this tax is Ohio, at

47 cents per gallon.

• A motor vehicle sales tax is used by Maryland,

Michigan, and Virginia. In Pennsylvania, no

sales tax revenue is directed into the Motor Li-

cense Fund to pay for highways and bridges.

TROC proposes implementing this revenue

option. Note that portions of Pennsylvania’s

motor vehicle sales tax and non-motor-vehi-

cle sales tax are directed toward multimodal

needs (0.947% of total sales tax revenue goes

into the Public Transportation Assistance Fund;

4.4% of total sales tax revenue goes into the

Public Transportation Trust Fund; and begin-

ning in FY 2022-23, approximately $450-$500

million in motor vehicle sales tax revenue will

go to the Multimodal Deputate).

• Driver’s license fees—on an annualized basis—

are higher in Delaware ($40), Massachusetts

($15), and Michigan ($9-$12.50) than in Penn-

sylvania ($7.87).

• Virginia uses general sales taxes to fund trans-

portation. Virginia generates well over $800

million annually for transportation from retail

sales and use taxes.

• Maryland transportation revenue includes

about $202 million a year from corporate in-

come tax and another $31.6 million from sales

taxes on rental vehicles.

• New Jersey transportation funding sources

include $72 million from a cigarette tax, $338

million from the Casino Revenue Fund, and

$3.7 billion from the Corporation Business Tax.

• New York State’s transportation funding sourc-

es include a corporate franchise tax that yields

$942 million a year, corporation and utilities tax

that produces $145 million in revenue, $237

million from the insurance tax, $22 million from

a bank tax, and $939 million from a sales and

use tax.

The experience nationally shows that reve-

nue-base broadening has been necessary, and

with it a recognition that transportation provides

streams of benefits that extend far beyond the

direct users.

States Broaden Revenue Base to Fund Transportation

PA Transportation Revenue Options Commission Final Report – July 30, 2021

32

Modernizing Federal and Local

Transportation Funding

Intergovernmental Partnership is Essential

TROC strongly emphasizes that its strategic funding proposal is a state government proposal, but that it

cannot address the funding problem in a vacuum. Federal and local roles must be a part of the solution.

Policymakers must recognize that this proposal is based on the essential principle of a federal-state-local

transportation partnership that includes the collaborative implementation of this proposal. There is the

need for a shift in thinking that emphasizes a renewed and robust federal-state-local partnership with ex-

panded funding from each.

Federalism (i.e., the system of shared responsibilities among federal, state, and local governments), as it

relates to transportation, necessitates that all three levels of government function as partners. This is more

than an aspiration. Rather, it is a practical necessity that mirrors the transportation system. Policies, pro-

grams, and facility operations have various intergovernmental dimensions. The pillars of this partnership

include:

• Shared responsibility for funding transportation and doing so at levels to significantly reduce the

backlog of improvement needs;

• Collaborating on policy development and execution; and

• Fostering innovation and flexibility.

Federal policy support and funding is essential, starting with the transportation reauthorization as dis-

cussed below. The federal government must also advance a workable policy and program for making

MBUF a reality as quickly and methodically as possible with state and local government to advance an

eective national implementation.

State government and PennDOT in particular must work to make the intergovernmental partnership as ef-

fective as it possibly can be through expanded statewide funding that includes modal and local resources.

Local government clearly needs greater resources going forward, but also will need to be positioned for

and expect that local share, especially on projects of regional significance, will be more the norm than the

exception going forward. Local funding partnership will also entail broader eorts for including developers

and other private sector sources of funding and in-kind resources as well.

Federal and local roles

must be a part of the

transportation funding

solution.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

33

Federal Considerations

TROC is encouraged by the focus of the Biden Administration and the U.S. Congress on infrastructure. The

federal government has held a vital funding role for the nation’s diverse and multimodal transportation sys-

tem dating back to the Interstate era and earlier. Even as federal funding strategies are being re-evaluated

and modernized, Pennsylvania cannot take a wait-and-see approach and hope that federal investment in

transportation will eventually close its funding gap. In fact, TROC proposes that Pennsylvania take a strong

leadership role in working with other states and the USDOT modal agencies to advance key changes sup-

portive of this strategic funding proposal, including:

• Reauthorizing federal surface transportation funding levels above the current Fixing America’s Sur-

face Transportation Act (FAST Act).

• Establishing a long-term, dedicated, and sustainable source of funding for multimodal transportation.

• Allowing greater flexibility in the use of federal funds.

• Updating and streamlining statutory and regulatory provisions that currently prevent infrastructure

owners (i.e., state DOTs) from leveraging and monetizing their Interstate highway assets to generate

incremental revenue and advance critical policy goals.

• Allowing greater flexibility in the use of right-of-way to address current and future challenges (such as

truck parking, broadband/connectivity, electric vehicle charging, etc.).

• Encouraging federal leadership in partnership with state governments to accelerate MBUF policy,

programs, and other pilot programs.

TROC would urge Congress to approve the transportation reauthorization at funding levels that make sub-

stantial progress in addressing the great need for transportation system improvements. Further, Congress

and the Administration must give priority attention to implementing a federal MBUF, the associated policy

framework, and criteria for its implementation.

TROC strongly emphasizes that federal-state collaboration be even more deliberate, bold, and flexible for

states to eectively address the increasing challenges with the necessary funding flexibility.

Local Solutions

The Need

Although TROC’s funding proposal focuses on the state-level funding gap, the

Commission recognizes that Pennsylvania’s local governments are responsi-

ble for managing an extensive and aging road and bridge network, in addition

to multimodal facilities that are typically owned and operated by regional au-

thorities. Some 2,560 municipalities manage an estimated 78,000 linear miles

of roadway and more than 6,300 bridges longer than 20 feet. Also, 55 local

public transit agencies and providers operate 7,000 buses, rail cars, and para-

transit vans across all 67 Pennsylvania counties, making 393 million passenger

trips and 39 million senior trips annually.

Local road and bridge network needs were estimated for the 2012 Transpor-

tation Funding Advisory Commission (TFAC) report, and the figures have been

updated to reflect inflation. The current local unmet funding need is estimated

The current local

unmet funding

need is estimated

at $3.863 billion

per year, growing

to $5.123 billion

per year by 2030.

PA Transportation Revenue Options Commission Final Report – July 30, 2021

34

Local governments currently receive:

• March 1st payments to municipalities (13.5% of the total gas and diesel tax):

» 20% of 57 mills gas and diesel tax per Act 35 of 1981 and Act 32 of 1983, after $35 million dedicated to

the PA Department of Conservation and Natural Resources and the State Conservation Commission per

Act 89 of 2013.

» 12% of 55 mills gas and diesel tax per Act 26 of 1991.

» 12% of 38.5 mills gas and diesel tax per Act 3 of 1997.

» 20% of 39 mills, after 4.17% to counties, of Act 89 of 2013, previously the 12-cent flat tax.

• Paid December and June of each year:

» 4.17% of 39 mills of the gas tax per Act 89 of 2013, the equivalent of a half-cent prior to Act 89, dedicated

to counties via the Liquid Fuels Tax Fund.

• PennDOT also provides funding to local governments through the Pennsylvania Infrastructure Bank (PIB),

3 mills of the gas tax per the Highway Transfer/Turnback program, dedicated local bridge funding, and other

programs.

to be $3.863 billion per year, growing to $5.123 billion per year by 2030. This is in addition to the $530