May 20, 2020

Anamaria Pieschacon, PhD

Director

Model Validation

Assessing Model Risk with Effective Validation

Olga Loiseau-Aslanidi , PhD

Director

Business Analytics

Petr Zemcik, PhD

Senior Director

Economics & Business Analytics

Effective Validation Webinar – May 2020 2

Moody's Analytics operates independently of the credit ratings activities of Moody's Investors

Service. We do not comment on credit ratings or potential rating changes, and no opinion or

analysis you hear during this presentation can be assumed to reflect those of the ratings agency.

Effective Validation Webinar – May 2020 3

Presenters

Olga Loiseau-Aslanidi PhD, Director

Head of APAC Risk Modelling

Economics & Business Analytics | Singapore

Petr Zemcik PhD, Senior Director

Head of EMEA Risk and Economics

Economics & Business Analytics | UK

Anamaria Pieschacon PhD, Director

Global Head of Model Validation

Economics & Business Analytics | USA

Effective Validation Webinar – May 2020 4

1. Model Risk in Spotlight

2. Effective Model Validation

3. Application to IFRS 9 Model

4. Key Takeaways

Agenda

1

Model Risk in Spotlight

Effective Validation Webinar – May 2020 6

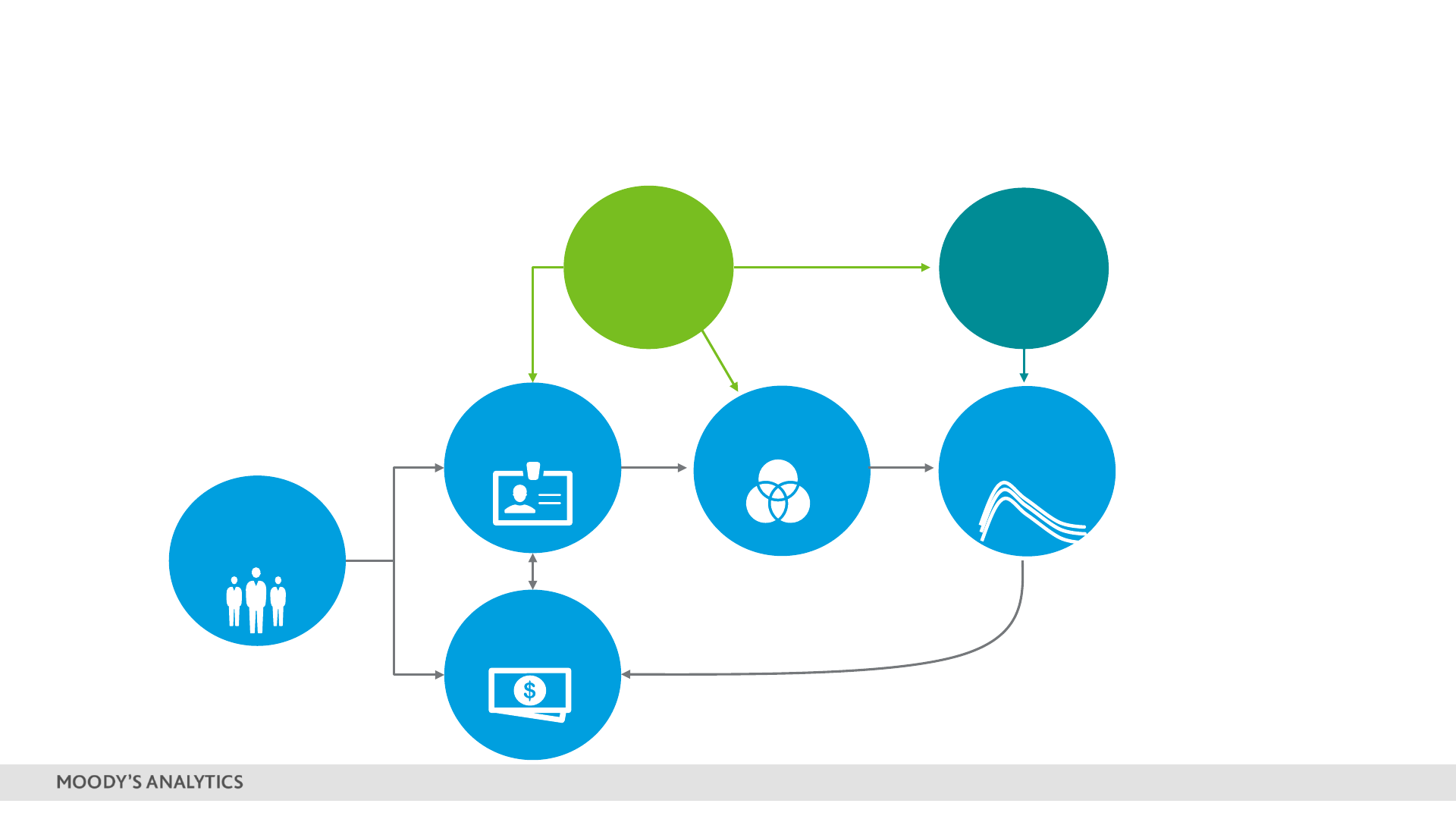

Institutions Rely on Models to Guide Decisions

Manage risk, identify opportunities and comply with regulation

Collection &

Recovery

Business

&

Strategic Planning

Application Scorecards

Credit Policies

Risk Based Limit Management and Pricing

Risk and Profitability Based Decisioning

Credit Line Assignment

Risk Appetite Framework

Behavioral Scorecard

Credit Transition Matrix

Credit Line Management

Fraud Detection

Loss Forecasting

Scenario Generation

Stress Testing

Early Warning Indicators

Propensity and Churn Modeling

Scenario Generation

Stress Testing

Reverse Stress Testing

IFRS 9 Impairment Modeling

ICAAP with IRRBB

Credit Risk Concentration

Economic and Regulatory Capital

Collection Scorecard

Optimal Workout

Credit Policies

Roll Rate Analysis

Tracking Collectors Efficiency

Regulatory

Reporting

Origination

Portfolio

Management

Collection &

Recovery

Effective Validation Webinar – May 2020 7

Assess models’ stability and

validity

Timely and consistent model

adjustments such as recalibration

using most recent data, overlays

Incorporate regulators’ mitigating

actions

Enhance model monitoring

Identify most vulnerable

exposures

Planning for vulnerable

exposures and portfolios

under stress

Optimize capital

allocation

Beware of potential model

failures and model

interdependencies

Quantify what COVID-19

means for the economy

Generate multiple future

paths to revise existing

adverse scenarios

Which models I should be

most worried about?

Which aspects of models

are most affected?

Credit risk and liquidity

risk models are most

vulnerable

COVID-19 Calls for Model Revision

Mitigating model risk is a basis for effective crisis management

Affected Models in Scope

Changes in Market Conditions

Validation and Benchmarking

Portfolio Management

Understand Identify Enhance Act

Proactive Overhaul of Model Risk Management

Effective Validation Webinar – May 2020 8

Credit Risk Models Are Among Most Vulnerable

Need to improve model resilience during pandemic and beyond

Application,

behavioral,

transactional,

alternative data

Scorecards

Dynamic models

IFRS9, stress testing

PD | LGD | EAD

PD | LGD | EAD

IRB models

Pricing

Macroeconomic

Scenarios

COVID-19

Impact

2

Effective Model Validation

Effective Validation Webinar – May 2020 10

Robust Model Governance as a Precondition for

Effective Model Risk Management

Greater Model

Complexity

Amplified

Supervision

Significant

Financial Impact

Increased Data

Availability

More

Models

Effective Validation Webinar – May 2020 11

Effectiveness depends on a

combination of incentives,

competence, and influence

Managing Model Risk Involves Effective Challenge of Models

Effective Model Validation

Critical analysis

by objective

Identify

model

limitations

Effective Validation Webinar – May 2020 12

Intensity should be proportional to the materiality of the portfolio

Depth of Validation

Complexity

Materiality

Internal

Validation

External

Validation

In all cases,

» MRM team should establish model performance

thresholds for periodic monitoring.

» MRM team should run periodic performance tests

and perform formal annual validation.

MRM team can hire external validation

if they lack in-house expertise

Effective Validation Webinar – May 2020 13

3 Pillars for Effective Model Validation

Independence

Purposeful

Rigor

Expertise

Effective Validation Webinar – May 2020 14

Expertise & Purposeful Rigor

Other Advisory

Services

Gap Analysis, Best Practices

and Model Governance

Regulatory Capital &

Stress Testing

Models

Basel, CCAR, PRA, EBA etc.

Financial

Reporting

IFRS 9 and CECL

Business &

Strategic Planning

Models

Credit Policy, Marketing,

etc.

Loan Lifecycle

Management

Models

Application, Pricing,

Origination, Monitoring, Loss

Mitigation, Disposition

Credit Portfolio

Management

Models

Risk Appetite, Concentration

Risk, Counterparty,

Operational, etc.

Effective Validation Webinar – May 2020 15

» Model developers and owners

should coordinate all stages of

model lifecycle, including

implementation.

» Validators should provide

effective challenge to existing

models, based on purpose and

materiality.

» To avoid conflicts of interest,

validation should be performed

by a team independent from

model development.

Independence

Board

Board Risk Committee

Model Risk Committee

1

st

Line

Model Owner Modeler

Implementation

Manager

2

nd

Line

Validation and

Ongoing

Monitoring

3rd Line

Internal Audit

Effective Validation Webinar – May 2020 16

Our Validation Process

Qualitative

Replication and outcomes

analysis

Validation Report

Comparison of inputs and

outputs of estimates from

alternatives allows to assess

and manage model risk

Evaluation of conceptual soundness

Assessment based on the

qualitative, quantitative and

benchmarking analysis

Benchmarking

Quantitative

Effective Validation Webinar – May 2020 17

Model Evaluation – Action Ratings

Satisfactory

The model has no critical

findings and is suitable for

deployment.

Satisfactory with

Recommendations

The model’s performance is

satisfactory and is suitable

for deployment.

Nevertheless, the validators

have identified areas where

the model could undergo

improvements that may

improve its overall

performance.

Needs Improvement

The validators have

identified multiple critical

findings that have a negative

impact on the model’s

performance. The current

model provides at least a

minimally adequate level of

performance and can be

used in its present form.

Unsatisfactory

There are important flaws in the

model’s underlying data,

conceptual framework, or

development process. Either i)

the model cannot perform its

intended function and should

not be used in any decision-

making capacity, or ii) there is

not enough evidence to show

that the model can perform its

intended function and it should

not be used in any decision-

making capacity until such

evidence becomes available.

Effective Validation Webinar – May 2020 18

Issues Identified and Recommended Actions – Generic Example

Final Assessment: Model Ratings by Category

Risk Category Rating Comments

Documentation The documentation needs to include XYZ.

Data Cleaning and Treatments …

Variable Selection Process …

Model Selection …

Model Performance …

Sensitivity Analysis

Model Replication …

Monitoring and Performance Tracking …

Overall Rating

The report will explicitly describe that the above risk categories do not hold equal weighting. The categories

shown may not reflect actual categories used.

Effective Validation Webinar – May 2020 19

Our Validation Process

Model document

review/understanding

Evaluate

» Purpose, scope, materiality

» Model selection process

» Data, conceptual soundness

» Assumptions & limitations

» Uncertainty & mitigating controls

» Review model governance,

ongoing monitoring/tests

Replication

Review and verify additional

analysis submitted by model

owners

In-sample and out-of-sample

performance evaluation

Push documents and scripts to

production

Discussion with model

owners/stakeholders

Stability and robustness

Sensitivity Analysis

Identify and discuss any gaps with

stakeholders

Initial model assessment

» Qualitative commentary on

possible model deficiencies,

implementation errors

» Categorize by severity and

issue recommendations

» Independent analysis

» Independent implementation

» Commentary on identified

shortcomings

» Final document with action

ratings

» Recommendations and

summary

of findings

COMPONENTS

DELIVERABLES

Qualitative

Validation

Quantitative

Validation

Consolidation

Preliminary

Model Review

01 02 03 04

Benchmarking*

Document and categorize the

findings by severity, issue

recommendations

Effective Validation Webinar – May 2020 20

We Measure Model Risk by Benchmarking

3

Application to IFRS 9

Models

Effective Validation Webinar – May 2020 22

Impairment Model

Macroeconomic Scenario Forecast

Scenario Probability Weights

Probability of

Default

Survival Probability

Loss Given

Default

Exposure at

Default

Discount Factor

Expected

Credit Loss

X X X =

Behavioral

Component

Probability of Cure

Effective/contractual

Interest Rate

Unbiased Point-in-Time Estimates

Stage

1, 2 or 3

IFRS 9: Macroeconomic Scenarios & Expected Credit Loss Calculation 23

An Integrated Process

Credit Risk Models

Credit Risk

Models

Macro-

economic

Scenarios

Data

Expected

Credit Loss

Model

Sensitivity

Analysis

Implementation

Results and

Reports

Portfolio Data

Macroeconomic

Scenarios

IRB Models / Basel

Models

Stress Testing

Models

IFRS 9 Models

April 2020 24

Scenario Severity Shift

Source: Moody’s Analytics

BL Apr

S3 Apr

BL FebS3 Feb

S1 Feb

S1 Apr

Effective Validation Webinar – May 2020 25

PD Modelling Approaches

Segment level

Account level

PD= f

Lifecycle

Quality of Vintage

Forward-looking Indicator

Dynamic evolution of vintages as they mature

Variable capturing the heterogeneity across cohorts:

vintage dummies, portfolio characteristics and/or

economic conditions at origination

Sensitivity of performance to the evolution of

macroeconomic and credit series

Modelling approach with three key factors influencing vintage

segment performance:

PD is forecasted using customer and loan characteristics,

and macroeconomic indicators using panel data

econometric techniques

PD= f

Customer and Loan Level Characteristics

Macroeconomic Drivers

Characteristics such as LTV, score, months on book,

education, etc.

Select pre-macro model using single factor and

multifactor analysis

Variable selection algorithm to select macroeconomic

drivers.

1. Segmentation

» Switch to bucketing based on DPD & LTV

» No further segmentation

» Internal portfolio

» Macro data

» Initial estimation

» Smoothing

» Scaling

Transition Matrix Approach

2. Data Inputs

3. TTC Matrix Creation

Effective Validation Webinar – May 2020 26

Looking at Forecast Properties

» Policy variables, e.g. CPI

» Changes in past correlations

» Non-cyclical sectors

» Growth rates:

– Low range level variables,

e.g. RMM

– QoQ growth rate

PD & Driver

Correlation

Driver

Forecasts

PD

Forecasts

Issue

Inconsistent

Volatile

No

convergence

» Long-term forecast property

of transformation

Downside

Upside

Upside

Downside

Upside

Upside

Upside

Upside

Downside

Downside

Downside

Downside

Driver

PD

Time

Time

Time

Time

Time

Time

Driver

PD

Driver

PD

Macro Driver

Macro DriverMacro Driver

PD

PD

PD

Effective Validation Webinar – May 2020 27

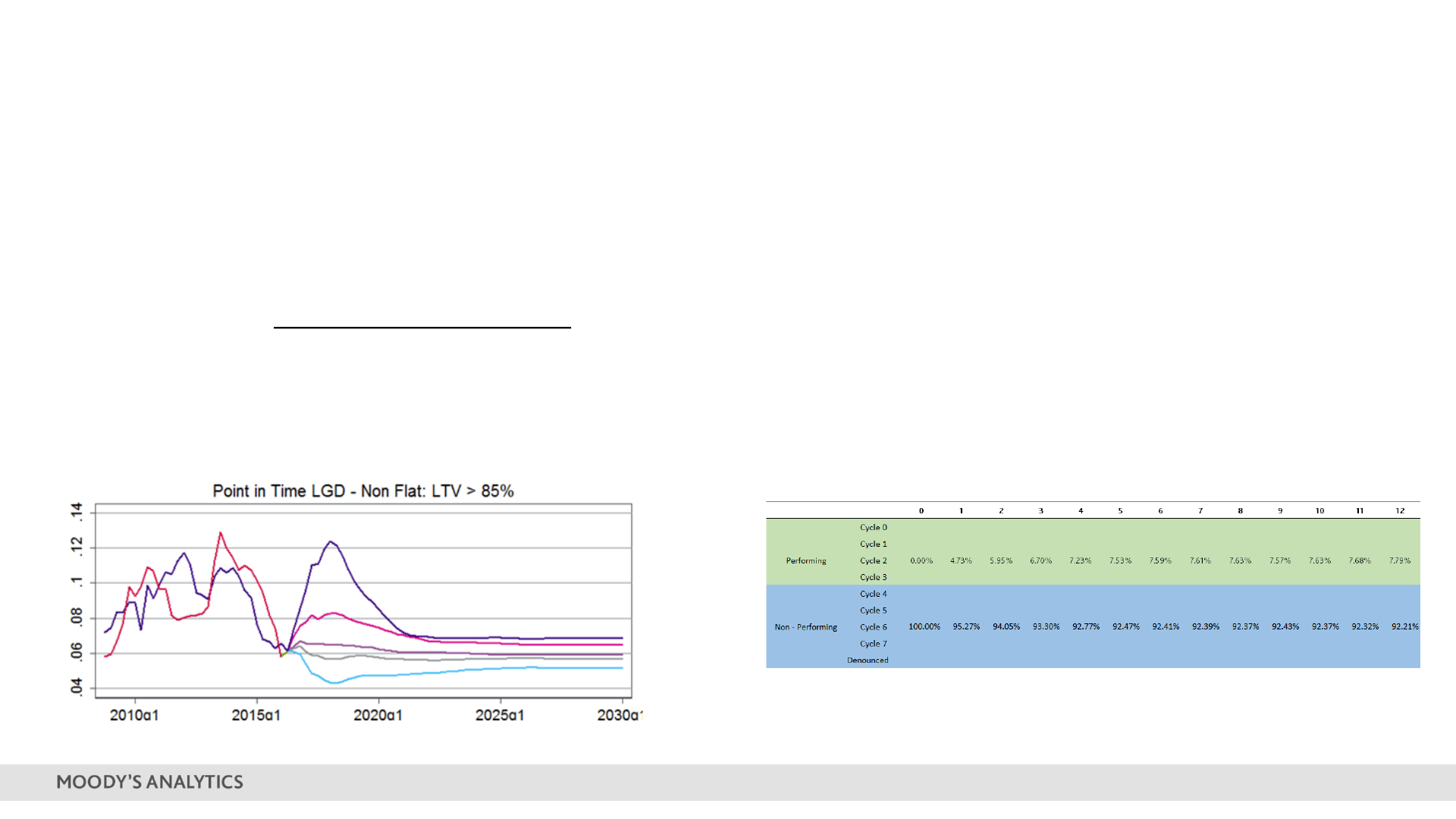

LGD Design Approaches

Balance and Recoveries

For a facility i, time t and workout period w:

= 1 −

,

−

,+

,

By Assumption

LGD of 50-60% for PF, 30-40% for RE and

65-75% for CC; fully insured products usually

get LGD of 5-10%.

Estimates of recovery costs range from 1-2%.

Default Vintages & Macro Drivers

Roll Rate Modelling

= 1 −

Effective Validation Webinar – May 2020 28

EAD Design Approaches

Fixed Term Products - Amortization Revolving Products - CCF

,+ℎ

=

,+ℎ

+ ∗

,

Credit Limit

Time

Balance

EAD

Undrawn amount x CCF

Drawn Amount

Effective Validation Webinar – May 2020 29

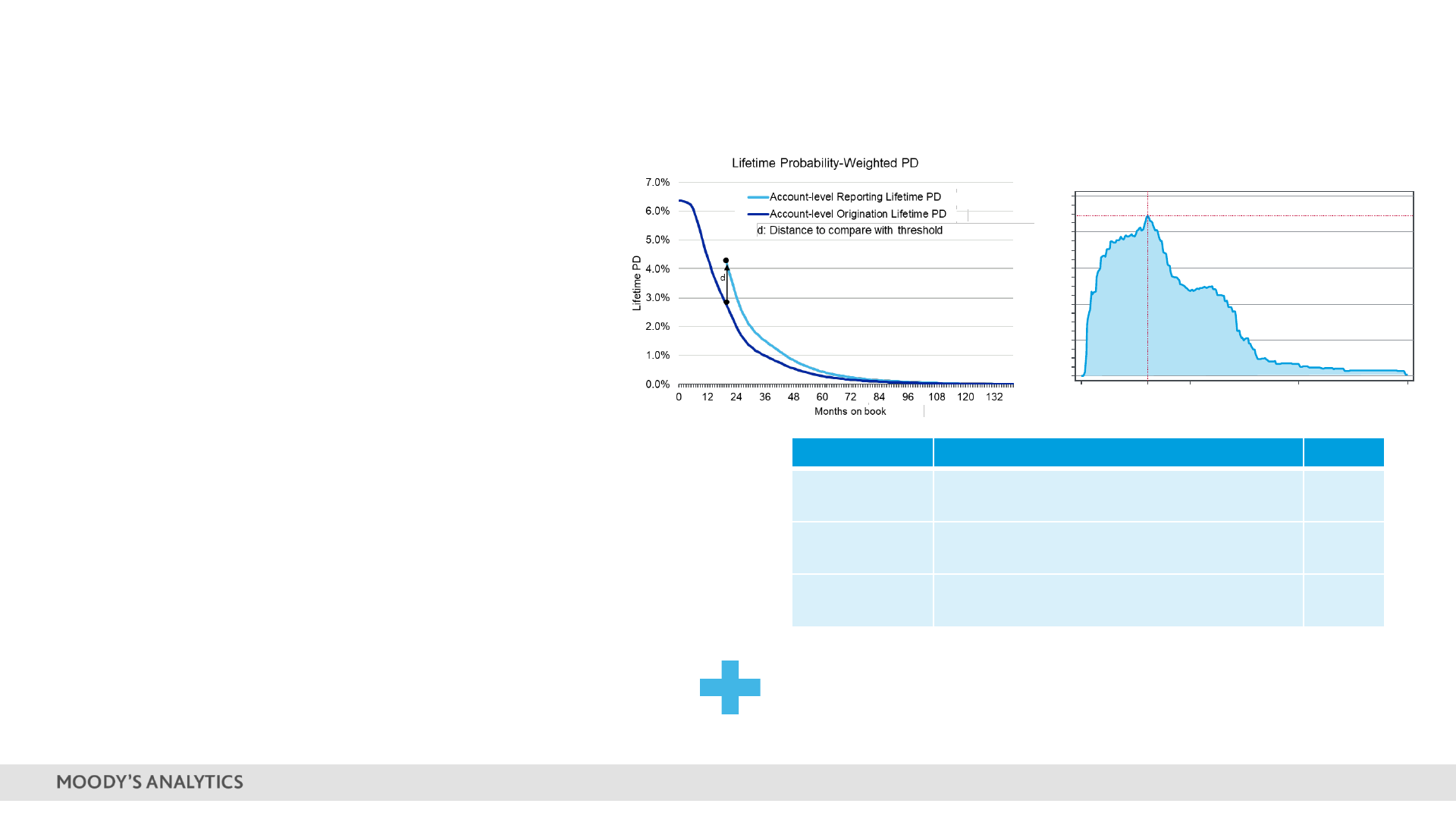

Evaluation of SICR

Quantitative Approach

Characteristics of the metric:

» Forward-looking (scenarios)

» Capture risk of default

» Lifetime information

» Available at origination and at reporting date

Status Criteria Stage

Non-Default Lifetime PD(T) ≤ Lifetime PD

0

(T) + Buffer 1

Non-Default Lifetime PD(T) > Lifetime PD

0

(T) + Buffer 2

Default 3

What is the optimal d to identify SICR?

» Buffer is the optimal value of d that maximizes an

accuracy ratio from good:bad odds analysis

» We examine differences (in logit) between

– the lifetime PD at the reporting date Lifetime PD(T)

– the lifetime PD at the same age as the reporting date

forecasted at origination Lifetime PD

0

(T)

for different historical reporting dates

Qualitative Approach

» DPD

» Forbearance

» Watch list

» …

.5

.55

.6

.65

.7

.75

Accuracy Ratio

0 .61 1 2 3

Buffer Size (logit)

Effective Validation Webinar – May 2020 30

= �

, ∗ , ∗ , ∗ ,

=

1

,

1

+

2

2

+ … +

(|

)

Probability-Weighted ECL by instrument:

ECL by scenario (s) & instrument (i):

ECL Calculation

Effective Validation Webinar – May 2020 31

IFRS 9 Validation Process

0

2

4

6

8

200 0m1 2005m1 2010m1 2015m1 2020m1 202 5m1

MA Baseline

0

2

4

6

8

200 0m1 2005m1 2010m1 2015m1 2020m1 202 5m1

MA St re ss

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0.1

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

PD

Time

Robustness & Sensitivity Analysis Report

Portfolio Behavior to Changing

Macroeconomic Conditions

Qualitative Quantitative

Final

Assessment

Methodology

Data use,

description &

treatment

Regulatory

compliance

Model

governance

Data analysis

Model

replication

Model

performance

Benchmark

model

development

Written report

Observation,

findings and

recommendati

ons and or

remedial

actions

Effective Validation Webinar – May 2020 32

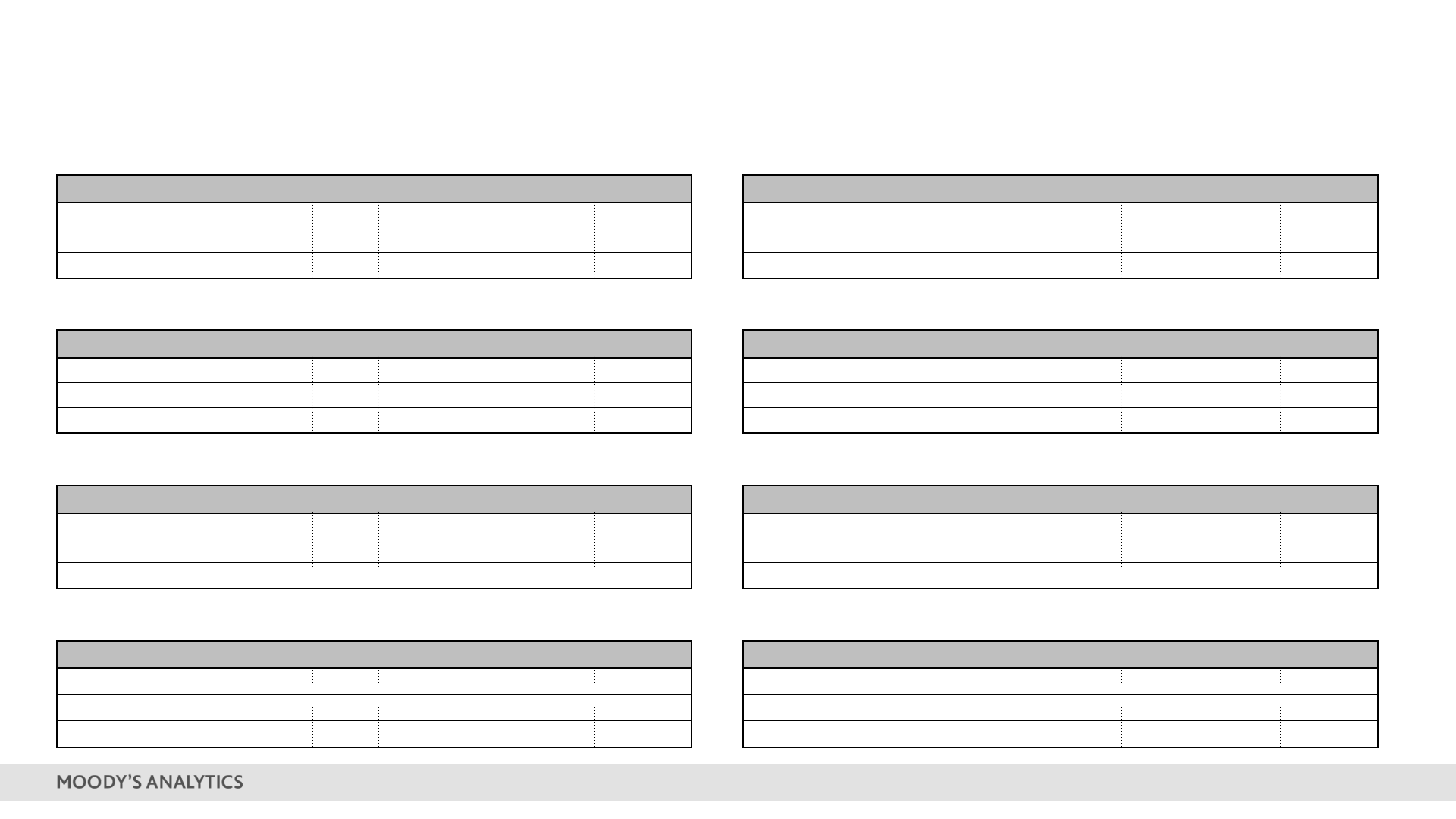

IFRS 9 Case Study – Impact of COVID-19

Baseline Feb 2020

Baseline Apr 2020

IFRS 9 Stage # % Exposure ECL=0.03 IFRS 9 Stage # % Exposure ECL=0.05

1

92,090

99.00

8,275,327,246

0.00

1

92,047 98.90 8,266,730,875 0.01

2

717

0.83

69,352,356

0.89

2

760 0.93 77,948,726 1.68

3

146

0.17

13,986,747

12.21

3

146 0.17 13,986,747 12.82

Upside Feb 2020

Upside Apr 2020

IFRS 9 Stage # % Exposure ECL=0.03 IFRS 9 Stage # % Exposure ECL=0.04

1

92,093

99.01

8,275,597,498

0.00

1

92,082 98.99 8,273,841,624 0.01

2

714

0.83

69,082,104

0.79

2

725 0.85 70,837,977 1.31

3

146

0.17

13,986,747

12.21

3

146 0.17 13,986,747 12.82

Downside Feb 2020

Downside Apr 2020

IFRS 9 Stage # % Exposure ECL=0.04 IFRS 9 Stage # % Exposure ECL=0.07

1

92,079

98.97

8,272,959,874

0.01

1

91,770 98.34 8,219,603,740 0.02

2

728

0.86

71,719,727

1.35

2

1,037 1.50 125,075,861 1.88

3

146

0.17

13,986,747

12.21

3

146 0.17 13,986,747 12.81

Prob-weighted Feb 2020

Prob

-weighted Apr 2020

IFRS 9 Stage # % Exposure ECL=0.03 IFRS 9 Stage # % Exposure ECL=0.05

1

92,086

99.00

8,274,895,046

0.01

1

92,020 98.84 8,261,408,180 0.01

2

721

0.83

69,784,556

1.00

2

787 1.00 83,271,421 1.76

3

146

0.17

13,986,747

12.21

3

146 0.17 13,986,747 12.81

4

Key Takeaways

Effective Validation Webinar – May 2020 34

Proactive Overhaul of Model Risk Management

Understand Identify Enhance Act

Affected Models in Scope

Changes in Market Conditions

Validation and Benchmarking

Portfolio Management

moodysanalytics.commoodysanalytics.com

West Chester, EBA-HQ

+1.610.235.5299

121 North Walnut Street, Suite 500

West Chester PA 19380

USA

New York, Corporate-HQ

+1.212.553.1653

7 World Trade Center, 14th Floor

250 Greenwich Street

New York, NY 10007

USA

London

+44.20.7772.5454

One Canada Square

Canary Wharf

London E14 5FA

United Kingdom

Toronto

+1.416.681.2133

200 Wellington Street West, 15th Floor

Toronto ON M5V 3C7

Canada

Prague

+420.23.474.7500

Pernerova 691/42

186 00 Prague 8 - Karlin,

Czech Republic

Sydney

+61.2.9270.8111

Level 10

1 O'Connell Street

Sydney, NSW, 2000

Australia

Singapore

+65.6511.4400

6 Shenton Way

#14-08 OUE Downtown 2

Singapore 068809

Shanghai

+86.21.6101.0172

Unit 2306, Citigroup Tower

33 Huayuanshiqiao Road

Pudong New Area, 200120

China

Contact Us: Content Solutions - Economics & Business Analytics Offices

Effective Validation Webinar – May 2020 37

© 2020 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All

rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND/OR ITS CREDIT RATINGS AFFILIATES ARE MOODY’S CURRENT

OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND

MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY, “PUBLICATIONS”) MAY INCLUDE SUCH

CURRENT OPINIONS. MOODY’S INVESTORS SERVICE DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS

CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR

IMPAIRMENT. SEE MOODY’S RATING SYMBOLS AND DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL

FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S INVESTORS SERVICE CREDIT RATINGS. CREDIT RATINGS DO NOT ADDRESS ANY

OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS, NON-

CREDIT ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF

CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK

AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS,

ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS

TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND

PUBLICATIONS DO NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS

CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND

UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS

UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS

AND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER

OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER

PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH

INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED,

REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR

MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A

BENCHMARK AS THAT TERM IS DEFINED FOR REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM

BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or

mechanical error as well as other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all

necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable

including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every instance independently verify or

validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any

person or entity for any indirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information

contained herein or the use of or inability to use any such information, even if MOODY’S or any of its directors, officers, employees, agents, representatives,

licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to: (a) any loss of present or prospective

profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any

direct or compensatory losses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful

misconduct or any other type of liability that, for the avoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the

control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers, arising from or in connection with the

information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY

PARTICULAR PURPOSE OF ANY CREDIT RATING, ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY

FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt

securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc.

have, prior to assignment of any credit rating, agreed to pay to Moody’s Investors Service, Inc. for credit ratings opinions and services rendered by it fees

ranging from $1,000 to approximately $2,700,000. MCO and Moody’s investors Service also maintain policies and procedures to address the independence

of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of MCO

and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publicly reported to the SEC an ownership

interest in MCO of more than 5%, is posted annually at

www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and

Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S

affiliate, Moody’s Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL

383569 (as applicable). This document is intended to be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act

2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or are accessing the document as a

representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to

“retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt

obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is

wholly-owned by Moody’s Overseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating

agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ

are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and, consequently, the rated obligation will not

qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency and

their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and

commercial paper) and preferred stock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or

MSFJ (as applicable) for credit ratings opinions and services rendered by it fees ranging from JPY125,000 to approximately JPY250,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.