CONTENTS

1

CONTENTS

PART ONE

Executive Summary

3

PART TWO

International Use of the RMB in 2020

5

I. Cross-border Use of the RMB

5

II. Use of the RMB in Current Account Transactions

9

III. Use of the RMB in Capital Account Transactions

12

IV. RMB-denominated Commodity Trading and Transactions

17

V. Use of the RMB in Foreign Exchange Market

17

VI. RMB as an International Reserve Currency

19

VII. Cross-border Circulation of RMB Banknotes

19

VIII. Cross-border Interbank Payment System

19

IX. Central Bank Cooperations

21

X. Interest Rates and Exchange Rates

23

PART THREE

Policies and Relevant Reforms

26

I. New Policies on the Cross-border RMB Settlements

26

II. Further Opening-up of the Capital Market

27

III. Exchange Rate Formation Regime

29

PART FOUR

Offshore RMB Market

30

I. Interest Rate and Exchange Rate

30

II. Offshore RMB Deposits

32

III. Offshore RMB-denominated Financing

34

IV. Issuance of RMB-Denominated Central-Bank Bills

34

V. The RMB in Global FX Market

35

VI. Offshore RMB Clearing

36

PART FIVE

Prospect

37

I. The cross-border Use of the RMB in Current Account Transactions

Will Be Further Expanded

37

2

2021 RMB INTERNATIONALIZATION REPORT

II. The Channels of the RMB Cross-border Investment and

Financing Will Be Further Facilitated

38

III. The Bilateral Monetary Cooperation Will Proceed Steadily

38

IV. The RMB Internationalization Infrastructure Will Be

Further Improved

38

PART SIX

Highlights of RMB Internationalization

41

Afterword

76

Boxs

Box 1

Use of the RMB in ASEAN Countries

8

Box 2

Trade in Goods Settled in RMB (2012-2020)

11

Box 3

Foreign Demand for RMB-denominated Financial Assets

16

Box 4

Use of the RMB in the Commodities Sector Grows Steadily

17

Box 5

Cross-border Interbank Payment System (CIPS) Participants

and RMB Clearing Services

20

Box 6

Overseas RMB Clearing Banks

22

Box 7

New Cross-border RMB Settlement Policies to Preserve

Foreign Trade and Investment

26

Box 8

The Launch of the Cross-Boundary Wealth Management

Connect Pilot Scheme in the Guangdong-Hong Kong-Macao

Greater Bay Area

28

Box 9

Market Survey on the International Use of the RMB

39

Figures

Figure 2-1

Monthly Cross-border RMB Settlement during 2019-2020

5

Figure 2

-

2

Yearly Cross-border RMB Settlement during 2010-2020

6

Figure 2

-

3

Geographical Distribution of the Cross-border RMB

Settlement in 2020

7

CONTENTS

3

Figure 2-4

Monthly RMB Settlement under the Current Account

9

Figure 2-5

Share of RMB Settlement under the Current Account

10

Figure 2

-

6

Monthly RMB Settlement under the Capital Account

13

Figure 2-7

Direct Investment Settled in RMB

13

Figure 2-8

Cross-border Cash Pooling Business Settled in RMB

14

Figure 2-9

The Issuance of Panda Bonds

15

Figure 2-10

Average Daily Cross-border RMB Clearing Statistics

20

Figure 2-11

Shanghai Interbank Offered Rate (1)

23

Figure 2-12

Shanghai Interbank Offered Rate (2)

24

Figure 2-13

Movements in Exchange Rate of CNY/USD

25

Figure 4-1

Movements in HK Offshore RMB Lending Rate

in 2020 (1)

31

Figure 4-2

Movements in HK Offshore RMB Lending Rate

in 2020(2)

31

Figure 4-3

Movements in Exchange Rate of CNH/USD

32

Figure 4-4

RMB-denominated Deposits and Loans in HK

33

Figure 4-5

Offshore RMB-denominated Deposits

33

Figure 5-1

Share of Respondents Considering Increasing

Use of the RMB

39

Figure 5-2

Share of Respondents Using RMB-denomination

during FX Fluctuation

40

Figure 5

-

3

Share of Respondents Considering RMB-denominated

Financing

40

Tables

Table 2-1 Cross-border RMB Settlement by Province in 2020

6

Table 2-2 Domestic RMB Financial Assets Held by Non-residents

16

Table 2-3 Trading Volume of the RMB against Foreign Currencies

in Interbank Foreign Exchange Spot Market in 2020

18

KEY ABBREVIATIONS

1

KEY ABBREVIATIONS

B&R The Belt and Road

BBGA Bloomberg Barclays Global Aggregate Index

BIS Bank for International Settlements

BMI Broad Market Index

CDs Certificates of Deposits

CFETS China Foreign Exchange Trade System

CIBM China

’

s Interbank Bond Market

CIPS Cross-border Interbank Payment System

CMU Central Moneymarkets Unit

COFER Currency Composition of Official Foreign Exchange Reserves

ETF Exchange Trade Fund

FAB First Abu Dhabi Bank

FTSE Financial Times Stock Exchange Group

FX Foreign Exchange

HIBOR Hong Kong Interbank Offered Rate

HKEX Hong Kong Exchange and Clearing

HKMA Hong Kong Monetary Authority

IMF International Monetary Fund

MOU Memorandum of Understanding

MSCI Morgan Stanley Capital International

NDFs Non-Deliverable Forwards

NEER Nominal Effective Exchange Rate

ODI Outward Direct Investment

OTC Over-the-Counter

PBC People

’

s Bank of China

PTA Pure Terephthalic Acid

QFII Qualified Foreign Institutional Investors

REER Real Effective Exchange Rate

2021 RMB INTERNATIONALIZATION REPORT

2

REITs Real Estate Investment Trusts

RMB Renminbi

RQDII Renminbi Qualified Domestic Institutional Investors

RQFII Renminbi Qualified Foreign Institutional Investors

RTGS Real Time Gross Settlement

SAFE State Administration of Foreign Exchange

SAR Special Administrative Region

SDR Special Drawing Right

SGX Singapore Exchange

SHIBOR Shanghai Interbank Offered Rate

SWIFT Society for Worldwide Interbank Financial Telecommunication

TSR Technically Specified Rubber

UAE United Arab Emirates

PART ONE

Executive Summary

3

PART ONE

Executive Summary

I

n the face of a complicated and grim economic environment at home and abroad

in 2020, especially the serious impact of COVID-19 pandemic, the People’s Bank

of China (the PBC) adhered to the guidance of Xi Jinping Thought on Socialism with

Chinese Characteristics for a New Era, and resolutely implemented the decisions

and arrangements of the CPC Central Committee and the State Council. The PBC

responded proactively to ensure stability on six fronts and maintain security in six

areas, thereby contributing to the establishment of a new development paradigm

with domestic circulation as the mainstay and domestic and international circulations

reinforcing each other. The PBC steadily and prudently promoted the international

use of the RMB, with the aim to advance the facilitation of cross-border trade and

investment and serve the real economy with adequate cross-border settlement policies

and infrastructure. The RMB has been well used in cross-border trade and investment

transactions. More foreign central banks held RMB-denominated assets as reserves,

and the RMB as an invoicing currency witnessed new progress.

In 2020, there was a relatively rapid growth in the cross-border use of the RMB. The

total amount of cross-border payments and receipts settled in RMB was RMB 28.39

trillion yuan, with a year-on-year (yoy) increase of 44.3% and a net outflow of RMB

185.79 billion yuan, reaching a record high in terms of volume. In the first half of

2021, the amount of cross-border payments and receipts settled in RMB totaled RMB

17.57 trillion yuan, with a yoy increase of 38.7%. The statistics from SWIFT (Society

for Worldwide Interbank Financial Telecomm) showed that RMB ranked 5th among

the main international payment currencies with a share of 2.5% in June 2021, 0.7

percentage point higher than that in June 2020. By the end of the first quarter of 2021,

the share of the RMB in globally disclosed holdings of foreign exchange reserves

remained a slightly upward trend, ranking 5th with a share of 2.5%, 1.4 percentage

points higher than that of 2016 when the RMB was officially included in the Special

Drawing Right (SDR) currency basket.

2021 RMB INTERNATIONALIZATION REPORT

4

The growth in the cross-border use of the RMB was partly due to the facilitation

of cross-border RMB settlement under the current account and direct investment,

and progress was made in such real economy sectors as commodities trade and

surrounding areas such as ASEAN. The RMB exchange rate moved in both directions

with enhanced flexibility based on market supply and demand and remained basically

stable at an adaptive and equilibrium level. More market entities chose to use RMB

in cross-border trade and investment with respect to avoid exchange rate risk. The

streamlined policies for cross-border RMB settlement was also a major concern for

businesses regarding international trade and direct investment.

Another important factor promoting the international use of the RMB upward was the

increasing foreign demand for RMB-denominated assets. The rapid growth of cross-

border RMB use in portfolio investment suggested that foreign investors actively

allocated RMB assets. With its economy recovering steadily, China was the only major

economy to register positive growth in 2020 and one of the few major economies

staying on a normal path. Considering the interest rate spread between the RMB

and the major convertible currencies, the attraction of the RMB financial assets for

global investors has been expected to persist. By the end of June 2021, the amount of

RMB-denominated financial assets such as stocks, bonds, loans, and deposits held by

overseas entities totaled RMB 10.26 trillion yuan, with a yoy increase of 42.8%.

In the next stage, the PBC will continue to follow the guidance of Xi Jinping Thought

on Socialism with Chinese Characteristics for a New Era, and firmly implement the

decisions and arrangements of the CPC Central Committee and the State Council.

Adhering to the general principle of pursuing progress while ensuring stability,

the PBC will conform to market-driven principles and respect the choices of market

entities while further improving the policies and infrastructure for the cross-border

use of the RMB, namely, promoting the two-way opening-up of financial markets,

supporting the offshore RMB market development, thereby contributing to a

conducive environment for more convenient use of the RMB and managing to strike a

balance between development and security. Meanwhile, the PBC will further improve

the macro-prudential management framework for the cross-border capital flows, and

firmly safeguard the bottom line that no systemic risk should occur.

PART TWO

International Use of the RMB in 2020

5

PART TWO

International Use of the RMB in 2020

I

n 2020, the cross-border use of the RMB increased steadily with its share in the

total cross-border settlement reaching a record high. The cross-border receipts and

payments were generally balanced with a small net outflow.

I. Cross-border Use of the RMB

In 2020, cross-border RMB settlement totaled RMB 28.39 trillion yuan, increasing by 44.3%

on a yearly basis. The total receipt reached RMB 14.10 trillion yuan, with an increase of

40.8% yoy while the total payment was RMB 14.29 trillion yuan, increasing by 48.0% on a

yearly basis. With a receipt to payment ratio of 1

∶

1.01, the cross-border RMB settlement

demonstrated a net outflow of RMB 185.79 billion yuan compared with a net inflow of

RMB 360.53 billion yuan in 2019. In 2020, the cross-border RMB settlement accounted

for 46.2% of the total cross-border settlement, reaching a record high in history, which

was 8 percentage points higher than that of 2019. In the first half of 2021, the cross-border

RMB settlement was 17.57 trillion yuan, accounting for 48.2% of the total cross-border

settlement in the same period, which was 2.4 percentage points higher yoy.

Figure 2-1

Monthly Cross-border RMB Settlement during 2019-2020

Source: The People’s Bank of China (PBC).

2021 RMB INTERNATIONALIZATION REPORT

6

Figure 2

-

2

Yearly Cross-border RMB Settlement during 2010-2020

Source: PBC.

In 2020, Shanghai, Beijing and Shenzhen continued to rank the top 3 in terms of the

provincial or regional cross-border RMB settlement volume, with a share of 51.5%,

18.2% and 8.7% respectively of the total cross-border RMB settlement. Nation-widely,

9 provinces (autonomous regions and municipalities directly under the central

government) enjoyed a cross-border RMB settlement volume over RMB 200 billion

yuan. Meanwhile, the 8 border provinces (autonomous regions included) reached an

aggregate amount of RMB 552.56 billion yuan, up 14.3% yoy.

Table 2-1

Cross-border RMB Settlement by Province in 2020

Unit: billion yuan, %

Ranking Region Current Account Capital Account Total Share

1 Shanghai 1,542.79 13,087.99 14,630.77 51.5

2 Beijing 837.72 4,339.70 5,177.41 18.2

3 Shenzhen 1,062.59 1,398.47 2,461.06 8.7

4 Guangdong (excluding Shenzhen) 915.80 739.10 1,654.89 5.8

5 Jiangsu 581.58 364.08 945.66 3.3

6 Zhejiang 431.41 357.32 788.73 2.8

7 Shandong 152.64 154.58 307.22 1.1

8 Fujian 65.87 227.37 293.24 1.0

9 Tianjin 129.56 85.30 214.86 0.8

Others 1,047.44 866.12 1,913.59 6.8

Total 6,767.4 21,620.03 28,387.43 100.0

Source: PBC.

PART TWO

International Use of the RMB in 2020

7

In 2020, the amount of cross-border RMB settlement between Chinese Mainland and

Hong Kong accounted for 46.0% of the total cross-border RMB settlement, which was

the highest. Singapore (12.9%), United Kingdom (5.4%) and Macao (3.7%) ranked

2nd, 3rd and 4th respectively. The shares of Hong Kong SAR of China, Singapore, the

United Kingdom, Macao SAR of China, Taiwan province of China all witnessed an

increase compared with 2019.

Figure 2

-

3

Geographical Distribution of the Cross-border RMB Settlement in 2020

Source: PBC.

In 2020, the amount of cross-border RMB settlement between mainland China and

countries along the Belt and Road (B&R) exceeded RMB 4.53 trillion yuan, a yoy

increase of 65.9%, accounting for 16.0% of the total cross-border RMB settlement

during the same period. Among them, the settlement in goods trade was RMB 870.10

billion yuan, a yoy increase of 18.8%, and the settlement in direct investment was

RMB 434.12 billion yuan, a yoy increase of 72.0%. By the end of 2020, the PBC has

signed has signed bilateral local currency swap agreements with 22 central banks or

monetary authorities along the B&R, and established the RMB clearing arrangements

in 8 countries along the B&R.

2021 RMB INTERNATIONALIZATION REPORT

8

Box 1

Use of the RMB in ASEAN Countries

In recent years, the economic and trade cooperation between China and ASEAN has been

continuously deepening and their bond have been increasingly strong. For most ASEAN

countries, China is the largest trading partner and the important source of investment

fund. In 2020, China’s total imports and exports with ASEAN countries increased by 7%

yoy. ASEAN has become China’s first largest trading partner.

China’s monetary and financial cooperation with ASEAN has been deepening

incessantly. In recent years, China and ASEAN have initially established a multi-

level monetary and financial cooperation framework in a broad range of areas, thereby

contributing to multiple occasions for the cross-border use of RMB. The PBC signed

bilateral local currency swap agreements with the central banks of Indonesia, Malaysia,

Thailand, Singapore and Laos, and signed a local currency cooperation agreement

with Bank of the Lao P.D.R.. The PBC and Bank Indonesia signed the Memorandum

of Understanding on the Framework for Cooperation to Promote the Settlement of

Current Account Transactions and Direct Investment in Local currencies, so as to

meet the market and economic development need and advance bilateral cooperation

under the Local Currency Settlement Framework (LCS), and promote convenience

for the use of local currency with respect to the settlement of bilateral trade and direct

investment. RMB clearing arrangements have been established in Malaysia, Thailand,

Singapore and the Philippines, and Cross-border Interbank Payment System (CIPS)

as well as Chinese banks have been operating in all the 10 ASEAN countries. Direct

trading between RMB against Singapore dollar, Thai baht, Malaysian ringgit and

Cambodian riel has been realized. The Bank of the Lao P.D.R launched RMB/Kip direct

trading in Laos.

Driven by the above favorable factors, use of the RMB in ASEAN has gained positive

progress in 2020, the total amount of RMB cross-border settlement between China and

ASEAN was RMB 4.15 trillion yuan, with a yoy increase of 72.2%, which accounted

for 14.6% of the total amount of cross-border RMB settlement, 2.4 percentage points

higher than that of 2019. Between China and ASEAN, the cross-border RMB settlement

of goods trade totaled RMB 745.90 billion yuan, a yoy increase of 20.2%, and direct

investment was RMB 425.10 billion yuan, a yoy increase of 70.8%.

PART TWO

International Use of the RMB in 2020

9

II. Use of the RMB in Current Account Transactions

In 2020, the total amount of the cross-border RMB settlement under the current

account was RMB 6.77 trillion yuan with a yoy increase of 12.1%, among which the

receipts amounted to RMB 2.91 trillion yuan, increasing by 9.8% yoy, the payments

amounted to RMB 3.86 trillion yuan, increasing by 14.2% yoy, and the net payments

amounted to 0.95 trillion yuan, increasing by 31.5% yoy. The total amount of the cross-

border RMB settlement under the current account accounted for 17.8% of the total

cross-border settlement, 1.7 percentage points higher compared with 2019.

Figure 2-4

Monthly RMB Settlement under the Current Account

Source: PBC.

2021 RMB INTERNATIONALIZATION REPORT

10

Figure 2-5

Share of RMB Settlement under the Current Account

Source: PBC.

1. Trade in Goods

In 2020, the total amount of the cross-border RMB settlement of trade in goods

reached RMB 4.78 trillion yuan, increasing by 12.7% yoy with a share of 14.8% of the

total cross-border settlement in goods trade, 1.4 percentage points higher than that in

2019. Among them, the cross-border RMB settlement under the general trade totaled

RMB 3.02 trillion yuan, increasing by 13.5% yoy, and that of the imported materials

processing trade totaled RMB 762.54 billion yuan, increasing by 2.1% yoy.

2. Trade in Services

In 2020, the cross-border RMB settlement of trade in services summed up to RMB

923.86 billion yuan, decreasing by 2.9% yoy and accounting for 25.5% of total cross-

border settlement in service trade during the same period, 1.7 percentage points

higher compared with the last year.

3. Income and Current Transfers

In 2020, the income payments settled in RMB totaled RMB 1,004.57 billion yuan,

increasing by 24.8% yoy, while the current transfer settled in RMB aggregated RMB

53.99 billion yuan, increasing by 45.0% yoy. The share of the cross-border RMB

settlement accounted for 54.8% in the cross-border income and current transfers, 5

PART TWO

International Use of the RMB in 2020

11

percentage points higher compared with the last year.

Box 2

Trade in Goods Settled in RMB (2012

-

2020)

In 2009, starting from the perspective of serving the real economy, China launched

the cross-border RMB settlement of the trade in goods based on the economic ties

with neighboring countries and regions. In 2012, the access of the cross-border RMB

settlement of the trade in goods was extended to the whole nation. The total amount of

cross-border RMB settlement of trade in goods hit another RMB 4 trillion yuan in 2020,

second only to the early highs of 2014 and 2015.

Since 2012, the cross-border RMB settlement of the trade in goods has been characterized

by the following features: First, the general trade is the main stay, the imported materials

processing trade settled in RMB fluctuates a bit more, and the cross-border e-commerce

business settled in RMB sees a rapid growth. The RMB settlement volume in general

trade has grown steadily since 2012. It registered RMB 3.02 trillion yuan in 2020,

accounting for 63.2% of the RMB settlement of the trade in goods. From 2012 to 2020,

the ratio of receipts to payments in RMB settlement of imported materials processing

trade was 2.91

∶

1, and the net RMB cross-border settlement volume was significantly

correlated with the RMB exchange rate and relatively volatile. Among which, it

registered RMB 762.54 billion yuan in 2020. Meanwhile, the RMB settlement in cross-

border e-commerce amounted to RMB 258.41 billion yuan, increasing by 50.0% yoy.

Second, the cross-border RMB settlement of the trade in goods is highly concentrated

in the wholesale industry

a

and manufacture of computers, communication and other

electronic equipment. From 2012 to 2020,it involved a total of 96 industries with

wholesale industry and manufacture of computers, communication and other electronic

equipment consistently ranking the top two. In 2020, the cross-border RMB settlement

in the wholesale industry amounted to RMB 1,273.73 billion yuan with a yoy increase

of 11.6%; RMB settlement in the manufacture of computers, communication and other

electronic equipment amounted to RMB 997.27 billion yuan with a yoy increase of 8.4%.

a

Wholesale industry here refers to: (1) activities of selling household goods and production materials in

bulk to other wholesale or retail units (including self-employed individuals) and other enterprises, institutions

and organizations, etc; (2) activities of engaging in import and export trade, trade brokerage and agency; (3) wholesale

activities at fixed stalls in various wholesale markets, and acquisition activities for the purpose of sales.

2021 RMB INTERNATIONALIZATION REPORT

12

Third, the cross-border RMB settlement of the trade in goods in the eastern regions

accounts for 90%. From 2012 to 2020, it amounted to RMB 31.57 trillion yuan,

2.03 trillion yuan and 1.58 trillion yuan in the eastern, central and western regions

respectively, of which the eastern region accounted for a share of 89.7%. In 2020, its

proportion in the settlement both in domestic and foreign currencies reached 15.6%,

9.3% and 9.6% for the eastern, central and western regions respectively, 5.1, 2.7 and 0.8

percentage points higher compared with 2012.

Fourth, Hong Kong has always been the largest overseas counterparty of RMB settlement

of the trade in goods, While the use of the RMB in goods trade between China and

European Union (EU) as well as other places has increased significantly. The proportion

of RMB settlement with Hong Kong SAR of China in the total RMB settlement of goods

trade was 42.2% in 2020, and Hong Kong maintained the largest counterparty among

overseas regions. In 2020, the proportions of the goods trade settled in RMB with EU

and ASEAN were 18.1% and 15.3% respectively, which made them rank the 2nd and

3rd in terms of the cross-border RMB settlement of the trade in goods.

The cross-border RMB settlement of the trade in goods has increased substantially from

a low base. It has played a role in helping businesses avoid foreign exchange rate risks

and reduce financial costs. In recent years, business areas such as commodities and

cross-border e-commerce have become a new pillar of growth. In the future, the PBC will

adhere to the orientation of serving the real economy, further enhance the facilitation

of the cross-border RMB settlement of the trade in goods, and ensure a high-quality

development of international use of the RMB.

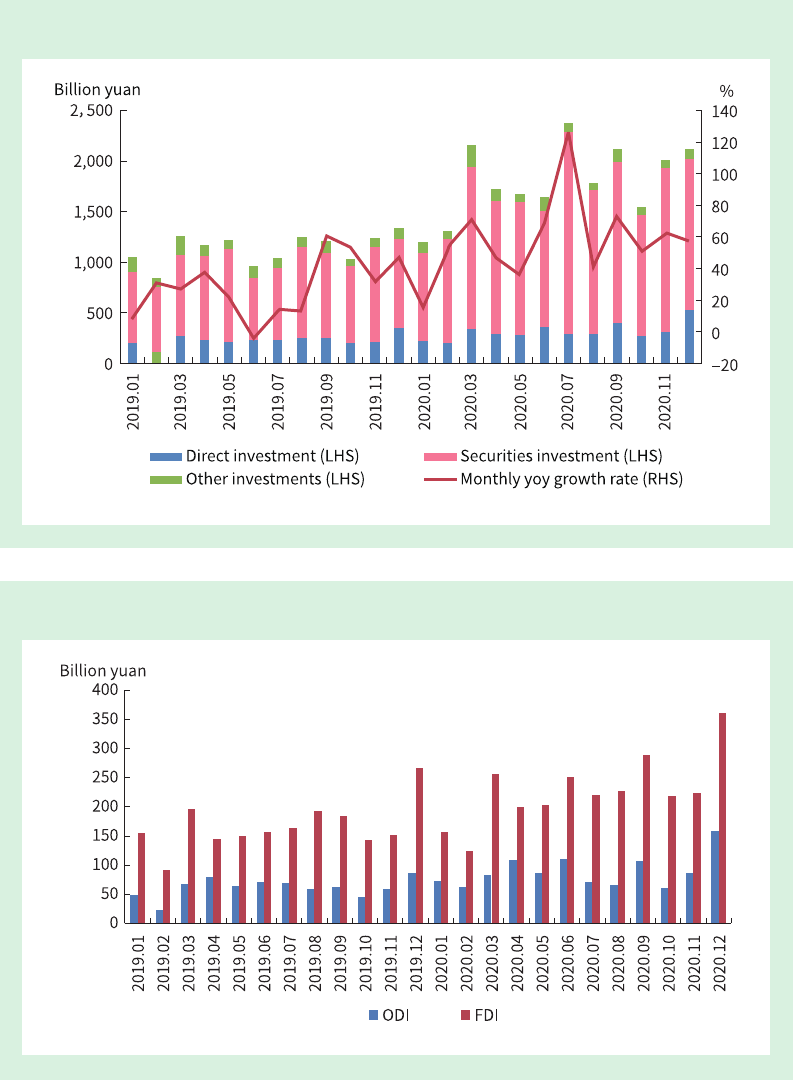

III. Use of the RMB in Capital Account Transactions

In 2020, the cross-border RMB settlement under the capital account totaled RMB

21.61 trillion yuan with a yoy increase of 58.7%, of which receipts and payments

stood at RMB 11.19 trillion yuan and RMB 10.42 trillion yuan respectively. The direct

investments, portfolio investments and cross-border financing accounted for 17.7%,

76.4% and 4.3% of the total settlement under the capital account respectively.

PART TWO

International Use of the RMB in 2020

13

Figure 2

-

6

Monthly RMB Settlement under the Capital Account

Source: PBC.

Figure 2-7

Direct Investment Settled in RMB

Source: PBC.

1. Direct Investment

In 2020, the amount of cross-border direct investment settled in RMB totaled RMB

3.81 trillion yuan, up 37.1% yoy. Among them, the amount of the Outward Direct

Investment (ODI) transactions settled in RMB stood at RMB 1.05 trillion yuan,

increasing by 39.1% yoy. In 2020, the amount of RMB settlement in the Foreign Direct

2021 RMB INTERNATIONALIZATION REPORT

14

Investment (FDI) transactions hit RMB 2.76 trillion yuan, increasing by 36.3% yoy.

2. The Cross-border RMB Cash Pooling Business

By the end of 2020, 2611 cross-border RMB cash pools had been established

nationwide. In 2020, cross-border RMB cash pools had outflows of RMB 1.30 trillion

yuan and inflows of RMB 1.24 trillion yuan, totaling RMB 2.54 trillion yuan, with an

increase of 39.6% yoy.

Figure 2-8

Cross-border Cash Pooling Business Settled in RMB

Source: PBC.

3. Panda Bonds

The issuers of the Panda Bonds comprise government institutions, international

development institutions, financial institutions and non-financial enterprises. By the

end of 2020, the cumulative registration or approval (filed) quota of the Panda Bonds

reached RMB 1 trillion yuan, with the issuance amount totaling RMB 433.72 billion

yuan. In 2020, there were a total of 42 Panda Bonds issued in both CIBM and security

exchange markets, reaching the amount of RMB 58.65 billion yuan.

PART TWO

International Use of the RMB in 2020

15

Figure 2-9

The Issuance of Panda Bonds

Source: PBC.

4. Portfolio Investment

In 2020, the cross-border portfolio investment settled in RMB totaled RMB 16.50

trillion yuan with a yoy increase of 73.6%, and the net inflow reached RMB 578.39

billion yuan.

Bond Investment. In 2020, 905 foreign institutions entered the interbank bond market,

468 of which entered directly, 625 accessed through the Bond Connect, and 188 used

both channels mentioned above. In 2020, the total amount of the inflow hit RMB 6.44

trillion yuan in contrast to the outflow of RMB 5.48 trillion yuan, making a net inflow of

RMB 963.02 billion yuan. The net inflow that directly entered the bond market hit RMB

472.37 billion yuan, while that via the Bond Connect stood at RMB 490.65 billion yuan.

Stock Investment. In 2020, the cross-border settlement via both of the Shanghai-Hong

Kong Stock Connect and the Shenzhen-Hong Kong Stock Connect totaled RMB 1.70

trillion yuan with a yoy increase of 65.3%, making a net outflow of RMB 413.29 billion

yuan in contrast to the net inflow of RMB 122.17 billion yuan in 2019. The net inflow via

Shanghai Stock Connect and Shenzhen Stock Connect reached RMB 178.05 billion yuan,

while the net outflow via Hong Kong Stock Connect reached RMB 591.34 billion yuan.

RQFII. In 2020, the amount of receipts and payments via the RQFII reached RMB 1.29

trillion yuan and 1.24 trillion yuan respectively, with a net inflow of RMB 52.63 billion yuan.

2021 RMB INTERNATIONALIZATION REPORT

16

Box 3

Foreign Demand for RMB-denominated Financial Assets

By the end of 2020, the amount of the financial assets held by foreign entities such as

domestic RMB stocks, bonds, loans, and deposits reached RMB 8.98 trillion yuan,

increasing by 40.1% yoy. Among them, the financial market value of stocks was RMB

3.41 trillion yuan, the outstanding amount of bonds under custody, RMB-denominated

deposits and loans were RMB 3.33 trillion yuan, RMB 1.28 trillion yuan, and RMB 0.96

trillion yuan respectively.

Stocks and bonds traded in domestic financial market have become the prominent options

of RMB assets allocated by overseas investors. By the end of 2020, the outstanding

amount of domestically traded RMB stocks and bonds held by foreign investors has

increased significantly by 54.5% yoy, among which bonds under custody accounted for

2.8% of the total bond custody in the CIBM, increasing by 47.4% yoy, and the market

value of stocks accounted for 4.3% of the total market value of A-shares in circulation,

increasing by 62.1% yoy. In 2020, stocks accounted for 54.9% of the amount increment

of the domestic RMB assets held by foreign entities.

Table 2-2

Domestic RMB Financial Assets Held by Non-residents

Unit: billion yuan

Instruments Dec.2019 Mar.2020 Jun.2020 Sep.2020 Dec.2020

Stocks 2,101.88 1,887.38 2,456.76 2,750.91 3,406.56

Bonds 2,262.93 2,319.90 2,572.42 3,015.92 3,335.08

Loans 833.16 887.17 972.05 983.08 963.02

Deposits 1,214.87 1,285.05 1,182.45 1,193.43 1,280.33

Total 6,412.84 6,379.49 7,183.68 7,943.34 8,984.99

Source: PBC.

5. Other Investments

In 2020, the total cross-border settlement amount under other investments such as

the cross-border financing and RMB loans for overseas projects reached RMB 1.30

trillion yuan, which was basically the same as last year, with a net outflow of 86

million yuan.

PART TWO

International Use of the RMB in 2020

17

IV. RMB-denominated Commodity Trading and Transactions

On June 22, 2020, low-sulfur fuel oil futures were listed on the Shanghai Futures

Exchange International Energy Trading Center. On November 19, 2020, international

copper futures were listed on the Shanghai Futures Exchange International Energy

Trading Center. On December 22, 2020, palm oil futures were officially introduced to

overseas traders. So far, seven specific varieties of futures—crude oil, iron ore, purified

terephthalic acid (PTA), TSR20, low-sulfur fuel oil, international copper and palm

oil—have been listed in China. Oversea traders who could access specific varieties of

futures in China can use RMB or USD as margin. By the end of 2020, foreign traders

had totally remitted fund inward equivalent of RMB 71.14 billion yuan as margin

and outward equivalent of RMB 78.00 billion yuan, in which the RMB settlement

accounted for 73.3% and 84.3% respectively.

Box 4

Use of the RMB in the Commodities Sector Grows Steadily

In 2020, the RMB was used in cross-border commodities trade. The cross-border RMB

payments and receipts in crude oil, iron ore, copper, soybean and other commodities trade

during the whole year amounted to 252.57 billion yuan, up 16.4% yoy. In the iron ore

trade, China Baowu Steel Group Co., Ltd made the first cross-border RMB settlement

with the world’s top three iron ore supplier at the beginning of the year, amounting to

more than 500 million yuan in aggregate. In August 2020, An steel Group and Rio Tinto

Group of Australia, one of the three largest iron ore suppliers in the world, made RMB

settlement of imported iron ore with an amount of RMB 100 million yuan. It is a sign

showing that the RMB is gradually being accepted by commodity traders, although the

amount settled in RMB is still at a low base.

V. Use of the RMB in Foreign Exchange Market

More and more trading entities got access to China’s interbank foreign exchange

market, with a total of 735 RMB foreign exchange spot trading members, 266 forward

trading members, 259 foreign exchange swap trading members, 213 currency swap

trading members, 163 option trading member, 30 RMB foreign exchange spot market

makers, and 27 forward swap market makers.

2021 RMB INTERNATIONALIZATION REPORT

18

The domestic interbank foreign exchange market operated smoothly, and the product

structure was generally stable, with annual RMB foreign exchange transaction volume

equivalent of USD 25.40 trillion, up 1.6% yoy, and an average daily transaction

volume of USD 104.53 billion. Among them, the CNY spot transaction volume was

equivalent of USD 8.38 trillion, up 5.6% yoy,and the CNY swap transaction volume

was equivalent of USD 16.32 trillion, down 0.2% yoy, among which the overnight

dollar swap trading volume was equivalent of USD 9.45 trillion, accounting for 57.9%

of total swap turnover. The currency swap transaction volumeamounted to USD 20.20

billion, down 60.6% yoy; RMB forward transaction volume was equivalent of USD

104.36 billion, up 37.4% yoy. The CNY foreign exchange option transaction volume

amounted to USD 566.66 billion, down 2.5% yoy.

In 2020, FX transactions against non-USD foreign currencies fell slightly, and spot

transaction volume against non-USD foreign currencies amounted to RMB 2.18 trillion

yuan, accounting for 3.8% of spot trading in the interbank foreign exchange market,

down 0.4% compared with last year.

Table 2-3

Trading Volume of the RMB against Foreign Currencies in Interbank Foreign

Exchange Spot Market in 2020

Unit: billion yuan

Currency USD EUR JPY HKD GBP AUD NZD

Trading

Volume

55,320.522 1,419.495 273.376 145.662 58.677 58.875 21.439

Currency SGD CHF CAD MYR RUB ZAR KRW

Trading

Volume

84.000 13.480 33.700 0.504 14.369 0.175 6.152

Currency AED SAR HUF PLN DKK SEK NOK

Trading

Volume

0.892 2.168 1.583 1.597 5.466 2.811 1.125

Currency TRL MXN THB

KZT

(regional trade)

KHR

(regional trade)

MNT

(regional trade)

—

Trading

Volume

0.950 0.911 35.888 0.002 0.006 0 —

Source: China Foreign Exchange Trade System (CFETS).

PART TWO

International Use of the RMB in 2020

19

VI. RMB as an International Reserve Currency

According to the quarterly data on the Currency Composition of Official Foreign

Exchange Reserves (COFER) released by the International Monetary Fund (IMF),

RMB-denominated reserves held by reporting entities reached USD 287.46 billion,

accounting for 2.5% of the total amount of official foreign exchange reserves which

had indicated currency composition by the end of the first quarter of 2021 and ranked

5th, which is the highest level since the RMB-denominated reserve was listed by the

COFER survey in 2016. According to incomplete statistics, more than 70 central banks

or monetary authorities incorporated RMB-denominated assets into their foreign

exchange reserves.

VII. Cross-border Circulation of RMB Banknotes

In 2020, the cross-border circulation of RMB banknotes declined significantly due to

the impact of the Covid-19 pandemic as well as some other factors. The total volume

of cross-border RMB banknotes transported by banks was RMB 13.63 billion yuan,

down 87.0% yoy, of which outbound volume was RMB 2.32 billion yuan, and inbound

volume was RMB 11.31 billion yuan, resulting in a net inward volume of RMB 8.99

billion yuan.

VIII. Cross-border Interbank Payment System

In 2020, the Cross-border Interbank Payment System (CIPS) operated steadily,

handling a total of 2.21 million cross-border RMB transactions with an overall

volume of RMB 45.27 trillion yuan, up 17.0% and 33.4% respectively yoy, and an

average daily processing of 8,855 transactions and volume of RMB 181.82 billion

yuan. In 2020, there were 1.67 million customer remittances, with the amount of

RMB 7.81 trillion yuan; 451,900 financial institutions remittances, with the amount of

RMB 32.66 trillion yuan; 26,800 bulk customer remittances, with the amount of RMB

125 million yuan; 57,700 bilateral settlement transactions, with the amount of RMB

4.80 trillion yuan; 250 clearing agency lending transactions, with the amount of RMB

109 million yuan.

2021 RMB INTERNATIONALIZATION REPORT

20

Figure 2-10

Average Daily Cross-border RMB Clearing Statistics

Source: CIPS.

Box 5

Cross-border Interbank Payment System (CIPS) Participants and

RMB Clearing Services

Since its launch in 2015, the Cross-border Interbank Payment System (CIPS) has

maintained a safe and stable operation with an increasing number of domestic and

oversea participants of more diversifying types. The coverage of the CIPS’ network has

continued to expand and its business volume has increased gradually. It has provided

safe, convenient, efficient and low-cost services to participants in the field of cross-border

RMB payment, settlement and clearing.

In 2020, 9 new direct participants (4 of which were overseas RMB clearing banks) and

147 new indirect participants joined the CIPS. By the end of 2020, a total of 1,092

domestic and foreign institutions had linked to the CIPS through direct or indirect

means, including 42 direct participants 23 more compared to the number at the initial

launch in October 2015, and 1,050 indirect participants whose number increased by

about five times from the inital launch in 2015.

By the end of 2020, direct participants in the CIPS consisted of 37 domestic and

foreign banks (5 of which are overseas RMB clearing banks) and 5 financial market

infrastructures. Besides, there had been 1,050 indirect participants in CIPS covering

99 countries and regions worldwide, about half of which were foreign participants. By

PART TWO

International Use of the RMB in 2020

21

the end of 2020, the RMB clearing business of CIPS reached out to more than 3,300

corporate bodies of banks in 171 countries and regions around the world through direct

and indirect participation, with more than 1,000 institutions from countries along the

B

&

R (excluding Mainland China, Hong Kong SAR of China, Macao SAR of China and

Taiwan Region). From its launch to the end of 2020, the CIPS had processed a total of

7,513,500 transactions, amounting to RMB 125.04 trillion yuan.

IX. Central Bank Cooperations

1. Bilateral Local Currency Settlement

On January 6, 2020, the PBC signed the Bilateral Local Currency Cooperation

Agreement with the Bank of Lao P.D.R. On March 1, 2021, the PBC signed the Bilateral

Local Currency Cooperation Agreement with the National Bank of Cambodia. The

agreements expanded the covering business of local currency settlement to all current

and capital transactions that had been allowed by the two countries, which was

conducive to the fully application of bilateral local currencies and promoting trade

and investment facilitation.

On September 6, 2021, the PBC and Bank Indonesia formally launched cooperation

framework for Local Currency Settlement (LCS), so as to promote the facilitation of

local currencies used in settlement of bilateral trade and direct investment.

2. Bilateral Local Currency Swap

In 2020, the PBC signed a new bilateral currency swap agreement with the Bank of Lao

P.D.R, renewed the bilateral local currency swap agreements with the central banks or

monetary authorities in Egypt, Switzerland, Mongolia, Argentina, New Zealand, the

Republic of Korea, Iceland, Russia, Hong Kong SAR of China and other countries and

regions, and lifted the amount of bilateral local currency swap agreements with the

central banks of Pakistan, Chile, Hungary and other countries. By the end of 2020, the

PBC has signed bilateral currency swap agreements with the central banks or monetary

authorities of 40 countries and regions, totaling more than RMB 3.99 trillion yuan.

3. Overseas Clearing Arrangements of the RMB

By the end of 2020, the PBC has designated 27 overseas RMB clearing banks in 25

countries or regions.

2021 RMB INTERNATIONALIZATION REPORT

22

Box 6

Overseas RMB Clearing Banks

In recent years, the RMB clearing business of overseas clearing banks has steadily

increased, with an average RMB clearing amount of 344.76 trillion yuan and an average

annual growth rate of 8.2% in the past three years. By the end of December 2020,

altogether 907 participating banks and other institutions opened clearing accounts in

overseas RMB clearing banks. In 2020, the RMB clearing amount of overseas RMB

clearing banks totaled RMB 369.49 trillion yuan, increasing by 6.1% yoy.

The overseas RMB clearing banks are mainly concentrated in the Asia-Pacific region,

followed by Europe. At present, 13 of the total 27 RMB clearing banks are located in the

Asia-Pacific region, which have opened clearing accounts for a total of 612 participating

banks and other institutions, accounting for 67.5% of the total number of clearing

accounts at the clearing banks. In 2020, the RMB clearing amount of these 13 banks

totaled RMB 354.29 trillion yuan, accounting for 95.9% of the clearing amount of

all clearing banks. Among them, Hong Kong SAR of China and Singapore took the

dominant place, with a total RMB clearing amount of RMB 336.42 trillion yuan in

2020, accounting for 95.0% of the total RMB clearing amount of the clearing banks in

the Asia-Pacific region. The second was Europe, where currently 7 RMB clearing banks

were located and had opened clearing accounts for 225 participating banks and other

institutions, with a total RMB clearing amount of RMB 15.02 trillion yuan in 2020.

The RMB clearing banks have played an active role in the process of RMB

internationalization. The RMB clearing banks connect the onshore and offshore RMB

markets, and mostly took the initiative to provide RMB clearing services in international

market. In terms of RMB clearing, the RMB clearing banks have greatly improved the

efficiency of RMB clearing through continuing system construction. The RMB clearing

banks of Hong Kong SAR of China can provide 7×20.5 hours of RMB clearing services

for global customers. Besides, clearing banks have the responsibility to let more foreign

entities know the convenience of using the RMB when conduct business with Chinese

partners, such as Bolstering China-Japan Financial Cooperation Forum organized by the

RMB Clearing bank in Tokyo, RMB/RRW Drived Exchange Marbet Seminar organized

by the RMB clearing bank in Seoul. The cross-border RMB settlement volume between

the countries (regions) where overseas RMB clearing banks are located with mainland

PART TWO

International Use of the RMB in 2020

23

China accounted for 86.4% of the total in 2020. In terms of nurturing the offshore

market, the RMB clearing banks provide adequate RMB liquidity support for the offshore

market, relying on the policy advantages of obtaining RMB liquidity from China.

X. Interest Rates and Exchange Rates

1. Interest rates

In 2020, the overall RMB interest rate pivot in domestic money market depreciated

first and then appreciated, which reached a low point in May and then rebounded,

with a slight decline at the end of the year. By the end of 2020, the overnight, 7-day,

1-month, 3-month, 6-month and 1-year Shanghai Interbank Offered Rate (SHIBOR)

dropped by 35, 5, 20, 24, 18 and 9 basis points respectively from the beginning of the

year to close at 1.09%, 2.38%, 2.70%, 2.76%, 2.84% and 3.00%.

Figure 2-11

Shanghai Interbank Offered Rate (1)

Source: CFETS.

2021 RMB INTERNATIONALIZATION REPORT

24

Figure 2-12

Shanghai Interbank Offered Rate (2)

Source: CFETS.

2. Exchange rates

In 2020, RMB experienced both appreciation and depreciation based on market supply

and demand with enhanced resilience, and remained basically stable at a reasonable

level of equilibrium. At the end of the year, the China Foreign Exchange Trade System

(CFETS) RMB exchange rate index was 94.84, up 3.8% from the end of 2019.

In 2020, the domestic RMB exchange rates fluctuated in both directions with

significantly greater flexibility. The RMB had appreciated and depreciated against

the US dollar and other major global currencies, with the central parity rate of the

RMB appreciating 6.9%, 1.3% and 2.9% against the US dollar, the Japanese yen and

the British pound respectively, and depreciating 2.6% against EUR at the end of

2019.

In 2020, the central parity rate of the RMB/USD was as high as 6.52 and as low as

7.13, with a fluctuation range of 6,080 basis points and an annualized volatility of

4.5%. During 243 trading days, RMB appreciated on 140 days and depreciated on 103

days. The biggest intraday appreciation was 1.0% (670 bps) and the biggest intraday

depreciation was 0.8% (530 bps). At the end of the year, the central parity rate of the

RMB/USD exchange rate was 6.52, an appreciation of 6.9% compared with the end of

PART TWO

International Use of the RMB in 2020

25

the last year, and the closing rate against the USD stood at 6.54, an appreciation of 6.5%

compared with the previous year-end.

Figure 2-13

Movements in Exchange Rate of CNY/USD

Source: PBC, CFETS.

2021 RMB INTERNATIONALIZATION REPORT

26

PART THREE

Policies and Relevant Reforms

I

n 2020, new policies to enhance the facilitation of the cross-border RMB use were

lauched, and the opening-up of financial market continued to progress and the

RMB exchange rate formation regime was further improved.

I. New Policies on the Cross-border RMB Settlements

In February 2020, the PBC together with MOF, CBIRC, CSRC and SAFE jointly issued

the Notice on Further Strengthening Financial Support for Containing COVID-19 Outbreak

(PBC Document [2020]No.29), which streamlined the procedures of cross-border RMB

businesses related to pandemic containment, and supported the financial services for

more efficient cross-border RMB businesses.

In December 2020, the PBC together with NDRC, MOFCOM, SASAC, CBIRC and

SAFE jointly issued the Notice on Further Optimizing the Cross-border RMB Policies

to Stabilize Foreign Trade and Investment (PBC Document [2020] No.330), further

improving the fundamental operational policies to sovle the problems market entities

met when using the RMB to settle the internation trade and investment.

Box 7

New Cross-border RMB Settlement Policies to Preserve Foreign

Trade and Investment

In December 2020, the PBC together with NDRC, MOFCOM, SASAC, CBIRC and

SAFE jointly issued the Notice on Further Optimizing the Cross-border RMB Policies to

Stabilize of Foreign Trade and Investment (PBC Document [2020] No.330, hereinafter

referred to as the Notice). The Notice closely focused on the needs of the real economy

and proposed a series of facilitation measures.

Firstly, it promoted a higher level of RMB settlement facilitation in trade and

investment, including expanding the pilot program of a higher level of trade and

investment facilitation to nationwide, supporting cross-border RMB settlement for

PART THREE

Policies and Relevant Reforms

27

e-commerce trade, and requiring banks timely to adjust business processing and review

request in line with the latest reform.

Secondly, it simplified the cross-border RMB settlement process, including improving

the creation of the supervisory watch list for cross-border RMB transactions, supporting

electronic review of documentation, optimizing the centralized cross-border RMB

payments and receipts under current account for multinational enterprise groups, and

piloting cross-border RMB settlement facilitation nationwide for qualified contractors

engaged in international engineering services.

Thirdly, it optimized the management of cross-border RMB investment and financing,

including relaxing restrictions on the use of certain RMB capital-account receipts,

facilitating domestic reinvestment by foreign-invested enterprises, canceling the requirement

of special account management for foreign direct investment, improving and simplifying the

management of overseas RMB borrowing and lending by domestic enterprises.

Fourthly, it facilitated the use of RMB remittances from Hong Kong and Macao. Hong Kong

and Macao residents could enjoy a more convenient payment and employment of the funds

when traveling or living in mainland China.

Fifthly, it facilitated the use of RMB funds channeled from overseas forforeign entities who

have open non-resident RMB account onshore.

II. Further Opening-up of the Capital Market

In May 2020, the PBC and SAFE jointly issued the Regulations on Funds of Securities and

Futures Investment by Foreign Institutional Investors (PBC, SAFE Public Announcement

[2020] No.2), to standardize and simplify administrative requirements on domestic

funds of securities and futures investment by foreign institutional investors, aiming to

better facilitate foreign investors’ participation in financial market of China.

In September 2020, the PBC, China Banking and Insurance Regulatory Commission

(CBIRC) and State Administration of Foreign Exchange (SAFE) jointly released the

Measures for the Administration of Domestic Securities and Futures Investment by Qualified

2021 RMB INTERNATIONALIZATION REPORT

28

Foreign Institutional Investors and RMB Qualified Foreign Institutional Investors (CSRC,

PBC, and SAFE Decree No.176), which integrated relative institutions and supporting

rules for QFII and RQFII, expanded market access and investing scope, and improved

custodians management.

Box 8

The Launch of the Cross-Boundary Wealth Management Connect

Pilot Scheme in the Guangdong-Hong Kong-Macao Greater Bay Area

The Cross-Boundary Wealth management Connect Scheme (Cross-boundary WMC)

refers to individual residents in the Guangdong-Hong Kong-Macao Greater Bay

Area (GBA) investing in eligible investment products distributed by banks in each

other’s market through a closed-loop funds flow channel established between their

respective banking systems. The Cross-boundary WMC consists of the Southbound

Scheme and the Northbound Scheme, depending on the identity of the investors.

The Southbound Scheme refers to residents in the Mainland GBA cities investing

in eligible investment products distributed by banks in Hong Kong and Macao via

designated channels; the Northbound Scheme refers to residents in Hong Kong and

Macao investing in eligible investment products distributed by Mainland banks in

the GBA cities via designated channels.

In June 2020, the People’s Bank of China, the Hong Kong Monetary Authority,

and the Monetary Authority of Macao jointly announced The Launch of the Cross-

boundary Wealth Management Connect Scheme in the Guangdong-Hong Kong-Macao

Greater Bay Area. In February 2021, the People’s Bank of China, China Banking and

Insurance Regulatory Commission, China Securities Regulatory Commission, State

Administration of Foreign Exchange, Hong Kong Monetary Authority, Securities and

Futures Commission of Hong Kong, and Monetary Authority of Macao jointly signed

the Memorandum of Understanding on the Launch of the Cross-Boundary Wealth

Management Connect Scheme in the Guangdong-Hong Kong-Macao Greater Bay

Area. The authorities had agreed on the principles of supervisory cooperation under

the cross-boundary Wealth Management Connect. In September 2021, the authorities

in Guangdong

,

Hong Kong and Macao simultaneously promulgated Implementation

Arrangements for the Cross-Boundary Wealth Management Connect Pilot Scheme in

the Guangdong-Hong Kong-Macao Greater Bay Area , marking the formal launch of the

Cross-Boundary WMC.

PART THREE

Policies and Relevant Reforms

29

The Cross-Boundary WMC is an important measure to implement the strategic

deployment of the CPC Central Committee and the State Council to support the

development of Guangdong-Hong Kong-Macao Greater Bay Area, as well as the

Outline Development Plan for the Guangdong-Hong Kong-Macao Greater Bay Area.

It is conducive to a quality living environment within the Greater Bay Area, the

advancement of the interconnectivity of financial markets in the Greater Bay Area, the

promotion of the two-way opening-up of the Mainland’s financial markets, and the

development of Hong Kong as the international financial center.

III. Exchange Rate Formation Regime

In 2020, the PBC continued to deepen the market-based reform of the RMB exchange

rates and to improve the managed floating exchange rate regime based on market

supply and demand with reference to a basket of currencies. It maintained the

flexibility of the RMB exchange rates and gave play to the role of the exchange rate as

an automatic stabilizer in adjusting the macro-economy and the balance of payments.

In the first 5 months of 2020, affected by the COVID-19 pandemic, the international

foreign exchange market volatility increased. The RMB exchange rate showed strong

resilience, depreciated against the US dollar, and appreciated slightly against a basket

of currencies. As China among the first to contain the virus, and Chinese economic

fundamentals continued to improve, the RMB exchange rate appreciated against the

US dollar and a basket of currencies after June. In October, the counter-cyclical factor

faded out of the central parity quotation model of the RMB against the US dollar.

The improvement in the transparency, benchmark and effectiveness of the central

parity formation regime after its adjustment was also the embodiment of the role of

market participants in the Foreign Exchange Self-disciplinary Mechanism. Overall, in

2020, the cross-border capital flows and foreign exchange supply and demand were

basically balanced, and the market expectations remained generally stable. Based on

market supply and demand, the RMB exchange rate experienced both depreciation

and appreciation, and remained basically stable at a reasonable and equilibrium level.

2021 RMB INTERNATIONALIZATION REPORT

30

PART FOUR

Offshore RMB Market

I

n 2020, the offshore RMB market maintained a healthy and steady development.

The interest rate spread of RMB between the onshore and offshore markets

narrowed, and the exchange rates of onshore and offshore RMB steadily

appreciated with a generally consistent trend. The offshore RMB-denominated

financial products were increasingly enriched with a constantly widened and

deepened offshore RMB market.The interaction between onshore and offshore

market further strengthened.

I. Interest Rate and Exchange Rate

1. Interest Rate

In 2020, the offshore RMB interest rate remained generally stable, and the differentials

of different maturities tended to be obvious: the fluctuation of short-term interest rates

increased while that of long-term interest rates fell overall. At the end of 2020, Hong

Kong Interbank Offered Rate (HIBOR) for overnight and 7-day lending fixing rate of

RMB were 4.03% and 2.96% respectively, 210 and 56 basis points higher than those at

the end of 2019 respectively, and the 3-month, 6-month and 1-year HIBOR were 2.88%,

2.94% and 3.07% respectively, dropping 38, 34 and 28 basis points from the end of

2019 respectively.

In 2020, the interest rate of offshore market was overall higher than that of the onshore

market with the HIBOR 0.39% higher than the SHIBOR on average. The spread

between the HIBOR and the SHIBOR for 1-month and 3-month periods narrowed

from 48 and 61 basis points in the first half of the year to 27 and 20 basis points in the

second half of the year respectively.

PART FOUR

Offshore RMB Market

31

Figure 4-1

Movements in HK Offshore RMB Lending Rate in 2020 (1)

Source: Hong Kong Association of Banks.

Figure 4-2

Movements in HK Offshore RMB Lending Rate in 2020(2)

Source: Hong Kong Association of Banks.

2. Exchange Rate

In 2020, the exchange rate of the offshore RMB featured significant two-way

fluctuations, generally remaining consistent with the exchange rate of the onshore

RMB, the exchange rate spread between the onshore and offshore RMB was stable

overall. In the first half of 2020, the offshore RMB generally depreciated with the

2021 RMB INTERNATIONALIZATION REPORT

32

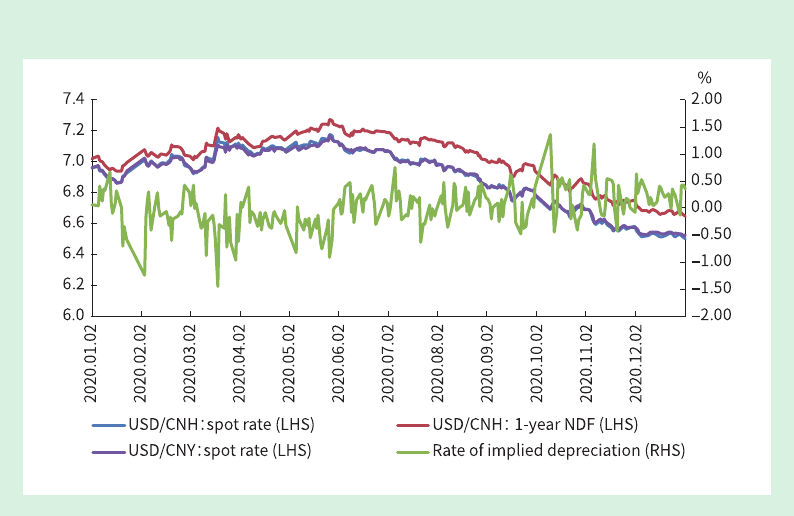

minimum of 7.17. In the second half of the year, the offshore RMB appreciated

gradually, closing at 6.50 at the end of the year, appreciating by 7.1% from the end

of the last year. The 1-year Non-deliverable Forward (NDF) quotation generally

appreciated, with an appreciation of 5.6% for the whole year, and the rate of implied

devaluation fluctuated in two ways during the year, reaching 0.4% at the end of the

year, 30 basis points higher than that at the beginning of the year. The trading days

that the exchange rate of offshore RMB was stronger or weaker than that of onshore

RMB during the year were roughly the same. The average daily exchange rate spread

between offshore and onshore RMB of the year was 114 basis points, increased by 11

basis points from 2019.

Figure 4-3

Movements in Exchange Rate of CNH/USD

Source: PBC, Reuters.

II. Offshore RMB Deposits

In 2020, the offshore RMB deposits steadily increased. By the end of 2020, the RMB

deposits in major offshore RMB markets exceeded 1.27 trillion yuan. Among them, the

RMB deposits in Hong Kong SAR of China was RMB 720.90 billion yuan, ranking 1st

in offshore RMB markets, with a yoy increase of 14.2%, accounting for 5.9% of the total

amount of deposits and 11.9% of foreign currencies deposits in Hong Kong SAR of

China. The RMB deposits in Taiwan province of China was RMB 244.09 billion yuan,

ranking 2nd in offshore RMB markets, with a yoy decrease of 6.5%, accounting for 2.7%

PART FOUR

Offshore RMB Market

33

of the total deposits and 9.8% of foreign currencies deposits in Taiwan province of

China. The RMB deposits in the United Kingdom was RMB 64.56 billion yuan, ranking

3rd in offshore RMB markets.

Figure 4-4

RMB-denominated Deposits and Loans in HK

Source: Hong Kong Monetary Authority (HKMA).

Figure 4-5

Offshore RMB-denominated Deposits

Source: PBC.

2021 RMB INTERNATIONALIZATION REPORT

34

III. Offshore RMB-denominated Financing

In 2020, the overall scale of offshore RMB loans remained generally stable, and the

amount of outstanding RMB loans in major offshore markets was RMB 528.55 billion

yuan. Among them, the amount of outstanding RMB loans in Hong Kong SAR of

China was RMB 152.00 billion yuan, ranking 1st in all offshore markets. Singapore

ranked 2nd with the amount of RMB 118.90 billion yuan and Macao SAR of China

ranked 3rd with the amount of 105.36 billion yuan.

In 2020, the offshore RMB-denominated bond market developed steadily. Incomplete

statistics showed that the total issuance of the RMB-denominated bonds in countries

and regions, where overseas RMB clearing arrangements established, amounted to

RMB 331.96 billion yuan in 2020, with a yoy increase of 14.2%. The RMB-denominated

bonds issued in Hong Kong SAR of China amounted to RMB 270.74 billion yuan,

increasing 11.1% yoy. By the end of 2020, the outstanding amount of the RMB-

denominated bonds in countries and regions with RMB clearing arrangements was

RMB 264.87 billion yuan, with a yoy decrease of 11.9%.The balance of the RMB-

denominated Certificates of Deposits (CDs) amounted to RMB 122.15 billion yuan,

with a yoy increase of 38.2%.

IV. Issuance of RMB-Denominated Central-Bank Bills

In 2020, the PBC issued RMB-denominated central-bank bills in Hong Kong SAR of

China markets regularly, further optimized the issuance structure of central-bank

bills of different maturities, and improved the market vigorousness of offshore RMB-

denominated central-bank bills. The PBC issued 12 batches of RMB-denominated

central-bank bills including maturities of 3-month bills, 6-month bills and 1-year bills,

with total amounts of 155.00 billion yuan in Hong Kong SAR of China. The RMB-

denominated central-bank bills issued in Hong Kong SAR of China were welcomed

by offshore investors, and the total bid-to-cover ratio of each issue tender exceeded

2.1 with the peak of 3.6 in 2020. Foreign investors comprise international financial

organizations, central banks, sovereign funds, commercial banks, funds, insurance

companies and other overseas investors, with geographical distribution covering

Hong Kong SAR of China, Macao SAR of China, Taiwan province of China, Asia-

Pacific, Europe, Africa and other regions.

PART FOUR

Offshore RMB Market

35

On January 27, 2021, Bank of China (Hong Kong) launched the market-making

mechanism for the repurchase of RMB-denominated central-bank bills in Hong Kong

SAR of China, providing quotations for overnight, one-week, two-week, one-month,

two-month and three-month repurchase and reverse repurchase of RMB-denominated

central-bank bills. As of July 2021, Bank of China (Hong Kong) had conducted 284

transactions with a total amount of RMB 73.40 billion yuan. The repurchase market-

making mechanism provides convenience for investors to use RMB-denominated

central-bank bills issued in Hong Kong SAR of China for liquidity management, and

facilitates the development of the offshore RMB currency market in Hong Kong SAR

of China.

The issuance of the RMB-denominated central-bank bills in Hong Kong SAR of

China provides overseas investors with sovereign credit rating of high quality RMB-

denominated investment products. It enriches the liquidity management tools of the

RMB-denominated market in Hong Kong SAR of China, improves the yield curve of

the RMB-denominated bonds in Hong Kong SAR of China, and encourages domestic

and overseas market participants to issue the RMB-denominated bonds and conduct

RMB business in offshore markets, thereby facilitating the sustainable and healthy

development of the offshore RMB market.

V. The RMB in Global FX Market

The RMB ranked fifth in terms of foreign exchange spot transactions, according to a

report released by Society for Worldwide Interbank Financial Telecommunications

(SWIFT) in June 2021, following the US dollar, the Euro, the British pound and the

Japanese yen. The main countries and regions for foreign exchange spot transactions

in RMB included the United Kingdom (with a settlement proportion of 36.7%),

the United States (with a settlement proportion of 14.4%), and China (excluding

Hong Kong SAR of China, Macao SAR of China, Taiwan province of China) (with a

settlement proportion of 11.0%) respectively.

a

According to the SWIFT statistics, RMB

was one of the most active currencies in foreign exchange markets globally. At present,

the RMB trading amount in the United Kingdom, the United States, Hong Kong SAR

a

Most of the transactions in the Chinese market (excluding Hong Kong SAR of China, Macan SAR of

China, Taiwan province of China) use the confirmation service of China Foreign Exchange Trading System,

and only a few of them use SWIFT MT300 message.

2021 RMB INTERNATIONALIZATION REPORT

36

of China and France ranked top four in the offshore markets, accounting for over 80%

of the offshore RMB trading volume in total.

VI. Offshore RMB Clearing

In 2020, the RMB clearing amount of overseas RMB clearing banks had totaled in

RMB 369.49 trillion yuan with a yoy increase of 6.1%, among which the clearing

amount on behalf of clients and for the interbank had been RMB 37.63 trillion yuan

and RMB 331.86 trillion yuan respectively, with each yoy increase respectively at

15.0% and 5.2%. By the end of 2020, 907 participating banks and other institutions

had opened clearing accounts in overseas clearing banks. In 2020, the RMB clearing

amount conducted by Hong Kong Real Time Gross Settlement (RTGS) added up to

RMB 282.48 trillion yuan and continued its rapid growth with a yoy increase of 6.3%.

PART FIVE

Prospect

37

PART FIVE

Prospect

I

n the next phase, the PBC will adhere to the guidance of Xi Jinping Thought on

Socialism with Chinese Characteristics for a New Era, and resolutely implement

the decisions and arrangements of the CPC Central Committee and the State

Council. The PBC will advance the opening-up reform to facilitate the international

use of the RMB in a steady and prudent manner, and strike a balance well between

development and security. The PBC will conform to market-driven principles and

respect the choices of market entities while further improving the policies and

infrastructures for the cross-border use of the RMB. Work will be done to streamline

the procedures of cross-border RMB settlement, to promote the two-way opening-

up of financial markets and to develop the offshore RMB market, thereby creating

a more convenient environment for market entities to use the RMB. Meanwhile,

the PBC will further improve the macro-prudential management framework for

cross-border capital flows, strengthen the work on monitoring, analysis and early-

warning of the cross-border capital flows, and ensure that no systemic risk would be

triggered by regulatory misconduct, so as to better serve the establishment of a new

development paradigm.

I. The cross-border Use of the RMB in Current Account Transactions Will Be

Further Expanded

The cross-border use of the RMB in current account transactions is an important

foundation for the RMB internationalization. The signing of the Regional

Comprehensive Economic Partnership (RCEP) will further enhance the development

of trade in the Asia-Pacific region, and enlarge the room for the use of the RMB in

trade and investment activities. The use of the RMB in commodity trade already had

a good start and is expected to be a growth pillar for the cross-border use of the RMB.

New trade modes such as the cross-border e-commerce will enrich the scenarios of the

use of the RMB and promote the use in foreign trade.

2021 RMB INTERNATIONALIZATION REPORT

38

II. The Channels of the RMB Cross-border Investment and Financing Will Be

Further Facilitated

The PBC will continue to promote the two-way opening of the financial market

and enrich FX risk hedging tools, thus facilitating foreign entities to allocate the

RMB financial assets. Work will be done to support foreign central banks, monetary

authorities and reserve management departments to allocate the RMB reserve

assets. Focusing on the construction of the pilot free trade zone (free trade port), the

Guangdong-Hong Kong-Macao Greater Bay Area and the Shanghai International

Financial Center, the PBC will further promote pilot initiatives to use the RMB in

cross-border investment and financing business.

III. The Bilateral Monetary Cooperation Will Proceed Steadily

The PBC will steadily promote bilateral local currency swap, optimize the framework

of local currency swap, and make the swap play its role in supporting the development

of the offshore RMB market and promoting trade and investment facilitation. The

PBC will strengthen local currency settlement cooperation with other central banks,

especially central banks in the neighboring countries and countries along the B&R,

so as to create a better environment for the use of the RMB abroad. The PBC will

continue to facilitate the direct trading of the RMB against the currencies of relevant

countries when the time is right and support foreign countries to use the RMB in local

foreign exchange markets.

IV. The RMB Internationalization Infrastructure Will Be Further Improved

The PBC plans to make overseas RMB clearing banks fully play the role of facilitating

RMB investment and financing, cultivating offshore RMB markets and offering

adequate RMB liquidity. The PBC will put more strength on the construction of the

CIPS, enhancing the security and efficiency of the RMB clearing and settlement, as

well as the building of the RMB Cross-border Payment and the Receipt Information

Management System (RCPMIS) , so as to do better on the statistics collection and

analysis.

PART FIVE

Prospect

39

Box 9

Market Survey on the International Use of the RMB

In 2020, the Bank of China conducted a market survey on the current status, inclination

and future expectations about the use of the RMB by the industrial and commercial

businesses and financial institutions from home and abroad, with nearly 3,300

participants engaged, of which about 2,500 participants were at home and 800 foreign

participants were from 32 countries and regions abroad. The survey shows that:

Firstly, the role of the RMB as the settlement currency had been further consolidated.

There were about 78.8% of the respondents considering using the RMB in cross-border

transactions or increasing the frequency of the use, and that proportion increased

compared with recent years.

Figure 5-1

Share of Respondents Considering Increasing Use of the RMB

Source: Bank of China.

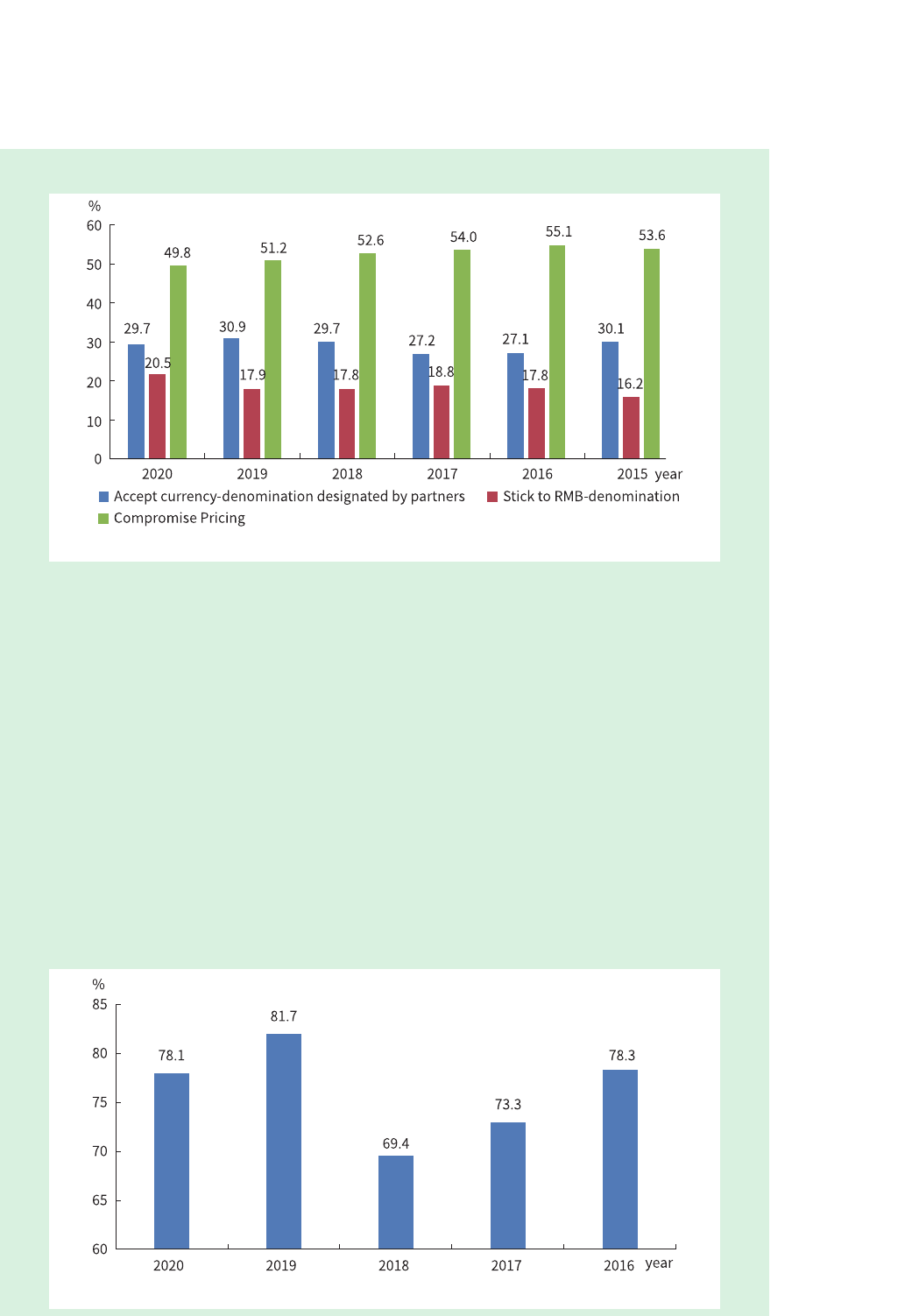

Secondly, the role of the RMB as a denominating currency had been brought into play

at a preliminary level. The survey results showed that 20.5% of domestic respondents

expressed their insistence on using the RMB to denominate in cross-border transactions,

indicating a proportion that had increased slightly from 2019. The share of respondents

that stuck to using the RMB for dominating has increased by 4 percentage point

compared to 2015, while the share of those using compromise pricing to mitigate

exchange rate risk had decreased by 4 percentage point.

2021 RMB INTERNATIONALIZATION REPORT

40

Figure 5-2

Share of Respondents Using RMB-denomination during FX Fluctuation

Source: Bank of China.

Thirdly, the role of the RMB in financing also played a part in international business,

especially under certain tight circumstances. The results of 2020 survey showed that about

78.1% of the foreign industrial and commercial respondents indicated that they would

consider using the RMB for financing while encountering tight liquidity of international

currencies such as the USD and the EUR. Although this ratio had fallen slightly according

to the 2019 survey, it was still maintained at a relatively high level in the past 5 years. The

results of both the 2020 and 2019 surveys demonstrated that the level of interest rates and

the cost of controlling the exchange rate risk of the RMB against domestic currency were

the two main factors that foreign industrial and commercial enterprises most concerned

about when considering whether to use the RMB for trade financing.

Figure 5

-

3

Share of Respondents Considering RMB-denominated Financing

Source: Bank of China.

PART SIX

Highlights of RMB Internationalization

41

PART SIX

Highlights of RMB Internationalization

2009

On January 20, the PBC and the Hong Kong Monetary Authority signed a bilateral

local currency swap agreement of RMB 200 billion yuan/HKD 227 billion.

On February 8, the PBC and the Bank Negara Malaysia signed a bilateral local

currency swap agreement of RMB 80 billion yuan/MYR 40 billion.

On March 11, the PBC and the National Bank of the Republic of Belarus signed a

bilateral local currency swap agreement of RMB 20 billion yuan/BYR 8 trillion.

On March 23, the PBC and Bank Indonesia signed a bilateral local currency swap

agreement of RMB 100 billion yuan/IDR 175 trillion.

On April 2, the PBC and the Central Bank of Argentina signed a bilateral local

currency swap agreement of RMB 70 billion yuan/ARS 38 billion.

On April 20, the PBC and the Bank of Korea signed a bilateral local currency swap

agreement of RMB 180 billion yuan/KRW 38 trillion.

On June 29, the PBC and the Hong Kong Monetary Authority signed the Supplementary

Memorandum III of Cooperation on the Pilot Program of RMB Settlement of Cross-

border Trade Transactions between Mainland and Hong Kong SAR of China.

On July 1, upon the approval of the State Council, the PBC, Ministry of Finance (MOF),

Ministry of Commerce (MOFCOM), General Administration of Customs (GAC),

State Administration of Taxation (SAT) and China Banking Regulatory Commission

2021 RMB INTERNATIONALIZATION REPORT

42

(CBRC) jointly issued the Administrative Rules on the Pilot Program of RMB Settlement

of Cross-border Trade Transactions (PBC, MOF, MOFCOM, GAC, SAT, CBRC Public

Announcement [2009] No.10).

On July 3, the PBC and the Bank of China (Hong Kong) Ltd. signed the revised RMB

Clearing Agreement, to support pilot program of RMB settlement of cross-border trade

transactions.

On July 3, the PBC issued the Regulations for Implementing the Administrative Rules of the

Pilot Program of RMB Settlement of Cross-border Trade Transactions (PBC Document [2009]

No.212).

On July 6, the first transaction of RMB cross-border trade settlement was conducted

in Shanghai, and the RMB Cross-border Payment Information Management System

(RCPMIS) was put into operation.

On July 7, the pilot program of RMB settlement of cross-border trade transactions was

launched in four cities of Guangdong.

On July 14, the PBC, MOF, MOFCOM, GAC, SAT and CBRC jointly issued the notice

to the Shanghai municipal government and Guangdong provincial government the

approval of Enterprises list for the Pilot Program of RMB Settlement of Cross-border

Trade Transactions (PBC General Administration Reply letter [2009] No.472). The first

batch of 365 enterprises was officially approved to conduct RMB settlement of export

transactions.

On September 10, the PBC and the SAT signed the Memorandum on data and

information transmission on the RMB settlement of cross-border trade transactions.

On September 15, the MOF issued the first sovereign RMB-denominated bond in

Hong Kong SAR of China with the amount of RMB 6 billion yuan.

On December 22, the PBC issued Questions & Answers on relevant policies of the pilot

program of RMB settlement of cross-border trade transactions.

PART SIX

Highlights of RMB Internationalization

43

2010

On February 11, the Hong Kong Monetary Authority issued the Elucidation of

Supervisory Principles and Operational Arrangements Regarding the RMB Business in Hong

Kong SAR of China.

On March 8, the PBC issued the Interim Administrative Rules for the RMB Cross-border

Payment Management Information System (PBC Document [2010] No.79).

On March 19, the PBC and the GAC signed the Memorandum of Cooperation on the RMB

Settlement of Cross-border Trade Transactions.

On March 24, the PBC and the National Bank of the Republic of Belarus signed a

bilateral local currency settlement arrangement.