S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L

We have a consistent set of strategic priorities

Growing and deepening relationships by

engaging customers

1

with products and

services they love and expanding our distribution

Delivering financial performance that is

consistently best-in-class

Leveraging data and technology to drive speed

to market and deliver customer value

⚫

Grow our customer base through new-to-bank relationships in Consumer Bank and Card

⚫

Engage customers with improved experiences across human and digital channels

⚫

Deepen relationships with a focus on Business Banking, Wealth Management, and Commerce

⚫

Operate resilient businesses with best-in-class returns

⚫

Scale core businesses and invest for long-term growth

Protecting our customers and the firm through a

strong risk and controls environment

Cultivating talent to build high-performing,

diverse teams where culture is a competitive

advantage

⚫

Optimize channels, products, and platforms to deliver customer and business value

⚫

Modernize applications, infrastructure, and data to future-proof the business

⚫

Drive disciplined risk, controls, and governance processes

⚫

Leverage our risk platforms as responsible growth engines

⚫

Create a culture where our people come to work with heart, curiosity, and courage

⚫

Be known as a company that serves customers, communities, and each other in a first-

class way

Strategy

Enablers

Outcome

1

5

2

3

4

1

“Customer” includes both consumers and small businesses and reflects unique individuals and business entities that have financial ownership or decision-making power with respect to accounts

2

We have delivered against our commitments

Added net ~3mm customers to the CCB franchise

Continued to scale distribution by opening 114 branches, while adding 240+ Business Relationship Managers and 300+ Advisors

Launched Personal Advisors and Wealth Plan for Chase clients and advisors

Launched Ink Business Premier, Pay in 4 on debit to select customers, and ChaseTravel.com for cardholders

Targeted and delivered ~$8B in volume through Travel platform – on track for ~$15B by 2025

Migrated nearly 30% of data to the public cloud – on track for 50% by end of 2023

Delivered $500mm+ in value from AI/ML programs

Continued to operate in a strong risk and controls environment

Attracted top talent and reduced attrition

Generated ~$40B in net interest income vs. ~$38B guidance from last year

Incurred ~$31B in adjusted expense

1

vs. ~$32B guidance from last year

Delivered 29% ROE on net income of $14.9B

Extended #1 position in retail deposit share

2

by 60bps

Extended #1 position in card by outstandings

3

by 74bps

Strategy

Enablers

Outcome

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

STRATEGIC PRIORITIES AND COMMITMENTS

For footnoted information, refer to slide 73

3

73.6

74.3

76.3

79.0

4.6

4.9

5.3

5.7

2019 2020 2021 2022

Small businesses

Consumers

We continue to drive significant customer growth – the catalyst for the franchise

Retail deposit share

2

9.1% (#3) 9.6% (#3) 10.3% (#1) 10.9% (#1)

Business Banking primary bank share

3

9.4% (#1) 9.5% (#1) 9.2% (#1) 9.3% (#1)

Card sales share

4

22.4% (#1) 22.3% (#1) 22.4% (#1) 22.4% (#1)

Card O/S share

4

16.6% (#1) 16.6% (#1) 16.5% (#1) 17.3% (#1)

CCB customers (mm)

Since 2019, we have grown our overall customer base by 8% and multi-LOB relationships

5

by ~20%

8%

1

For footnoted information, refer to slide 74

4

We strive to make it easy to do business with us by engaging customers across channels

In 2022, we achieved record high satisfaction across channels

5

active digital

customers

3

63mm+

digital logins

4

>15B

mobile logins per

user per month

>20

unique visitors to

branches per day

~900k

U.S. population

within a 10-min.

drive to a branch

60%

customers met

with a banker

>20mm

#1 Digital banking platform

1

1

st

Retail bank in all lower 48 states

2

Enabling customers to manage their full financial lives through

our digital banking, lending, and investing capabilities

Our branch network is a local storefront for customers who

want to engage with our bankers and advisors

Increasing branch

density

For footnoted information, refer to slide 75

5

We are investing across our lines of business to serve more of our client needs

CONNECTED COMMERCE

Customers (mm)

1.6

2.2

2.3

2019 2021 2022

45%

Relationships

2

(mm)

2.9

3.5

3.8

2019 2021 2022

>75%

of Business Banking clients

also have a Consumer

Banking relationship

>85%

of first-time investors come

from banker referrals

3

BUSINESS BANKING

Clients

5

(mm)

WEALTH MANAGEMENT

1

Enabled by recent

acquisitions

>$3

~$4

~$8

2019 2021 2022

Chase Travel sales volume ($B)

4

>2x 30%

For footnoted information, refer to slide 76

6

We generate tremendous franchise value from operating our businesses within CCB and the broader firm

World-class capabilities across the firm

100%

of J.P. Morgan Wealth Management investments

through Asset & Wealth Management

Solutions throughout customers’ lifecycles

>15%

of new Middle Market relationships came

from Business Banking last year

Unmatched omnichannel distribution

Scale of our franchise

Leading financial services brand

#1

in prospect consideration

across peer institutions

1

$7B+

in investments to drive sustained growth

while delivering industry leading returns

CCB JPM

Customer Value Employee Value Enterprise Value

~50%

of Commercial & Private Banking clients

visit our branch network

5

Branch network as a storefront for JPMC

#

1

#

1

#

1

Consumer Banking

Business Banking

Card

Wealth

Merchant

Mortgage

#

1

#

1

#

2

For Chase clients

3

In the industry

2

75%+

of mortgage originations

4

, Business Banking clients,

and wealth relationships from existing customers

For footnoted information, refer to slide 77

7

2019 2021 2022

Average deposits ($B)

$698 $1,055 $1,163

Average loans ($B)

$478 $434 $439

Average Card outstandings ($B) $156 $140 $163

Revenue ($B)

2

$55.0 $49.9 $54.8

Deposit margin

3

2.48% 1.27% 1.71%

Expense ($B)

2

$28.1 $29.0 $31.2

ROE

31.0% 41.0% 29.0%

$21.7

$18.1

$20.9

We continue to deliver strong financial performance

CCB Pretax Income ex. LLR ($B)

1,2

For footnoted information, refer to slide 78

8

$49.9

$54.8

$3.5

$1.9

($0.7)

($0.7)

$1.0

2021 Macro rate Volume Overdraft changes Margin MSR / Other 2022

We continue to drive core growth in the business: 2021-2022

▲ Deposit growth

▲ Card loan and spend growth

▼ Increase in Card acquisition costs

▼ Home Lending production volumes

▼ Auto leases

1

In the first quarter of 2023, the allocations of revenue and expense to CCB associated with a Merchant Services revenue sharing agreement were discontinued and are now retained in Payments in CIB. Prior-period amounts have been revised to conform with the current presentation

2

Totals may not sum due to rounding

Net Interest Income ($B)

2022

Actual

~$40

2023

Outlook

ex. FRC

~$50

(

▲

~$10 vs. ‘22)

▲ Card loan yield

▼ Home Lending production margin

▼ Card renewals and refreshes

2

CCB REVENUE ($B)

1

9

$49.1

$54.8

($5.1)

$13.0

($1.0)

($0.3)

($0.9)

2012 Macro rate Volume Overdraft changes Margin MSR / Other 2022

Revenue walk: 2012-2022

Net Interest Income ($B)

2022

Actual

~$40

2023

Outlook

ex. FRC

~$50

(

▲

~$10 vs. ‘22)

Deposit Margin

2

2.57%

Deposit Margin

2

1.71%

1

In the first quarter of 2023, the allocations of revenue and expense to CCB associated with a Merchant Services revenue sharing agreement were discontinued and are now retained in Payments in CIB. Prior-period amounts have been revised to conform with the current presentation

2

Banking & Wealth Management

CCB REVENUE ($B)

1

10

$1,173

$1,134

$80

($47)

($118)

$46

1Q22 Customer growth Customer activity Yield-seeking outflows Yield-seeking inflows 1Q23

We are retaining and growing primary bank relationships and capturing money in motion

▼ JPM WM investments

▼ Internal migration

3

▼ External brokerages

▼ Online banks

▲ Internal migration

6

▲ Net new money

$35

JPM WM investments

$81

retention of yield

seeking flows

7

~60%

of banking customers outflow to

an online bank with no change

in primary bank %

5

~5%

YoY customer

growth

2

>3%

Total yield-seeking inflows

4

52% checking

52% checking

Core

Drivers

~4%

For footnoted information, refer to slide 79

decline in deposit

balances driven by

higher taxes and spend

BANKING & WEALTH MANAGEMENT DEPOSIT BALANCES ($B)

1

11

23.9

24.2

We are maintaining expense discipline while we continue to invest for the future

$23.8

$24.0

~$25

$29.0

$(0.8)

$0.9

$0.1

$31.2

~$(0.1)

~$1.1

~$0.3

~$33

$1.9

~$0.7

2021 Volume- &

revenue-related

Structural Investments Other 2022 Actuals Volume- &

revenue-related

Structural Investments Other 2023 Outlook

Investments

▲ Wage inflation

▲ Higher headcount

▲ Technology

▼ Auto lease depreciation

▲ Core volume growth

▲ Salesforce incentives

$7.0

$5.2

2022

▲ FDIC base

assessment

CCB ADJUSTED EXPENSE ($B)

1,2,3

For footnoted information, refer to slide 80

ex. FRC

12

2021 2022 2023

Outlook

~3% CAGR

$23.8B

~$25B

~30%

Customers per branch

6

>15%

Tenured Advisors

7

>15%

Sales productivity per branch

8

BRANCH NETWORK & FIELD COST PER ACCOUNT

$24.0B

2019 2022 2023

Outlook

(5%)

For footnoted information, refer to slide 81

>20%

Servicing calls per customer

3

>50%

Total transaction volume

4

~5%

Fraud loss rate per transaction

5

OPERATIONS & FRAUD COST PER ACCOUNT

2019 2022 2023

Outlook

(11%)

We are realizing benefits of scale and efficiencies across our business

ADJUSTED EXPENSE

1,2

(EX. INVESTMENTS)ARE GROWING MODESTLY

Other volume-

related

Other structural

Tech production

Operations &

fraud

Branch network

& field

13

$7.1

~$7.9

$2.7

$3.1

$3.2

$3.9

$1.2

$0.9

2022 2023 Outlook

From 2022-2023, we will continue to invest in growing the franchise

Wealth

Management

Connected

Commerce

2

Branch

Network

Marketing

⚫ Roll-off of travel platform operating expenses

⚫ Deal integration & amortization (cxLoyalty, FROSCH)

⚫

Advisor hiring

⚫ New builds in expansion and mature markets

⚫ Banker hiring

⚫ Acquisitions & deepening

⚫ Branding

6 year

payback

4 year

break-even

4 year

break-even

2 – 3x ROI

Growth

businesses

$0.5

$0.4

$1.4

$2.5

Note: marketing investments

are part of ~$8B total gross

marketing spend

3

Technology

& product

⚫ Channels, products, and platform development

⚫ Infrastructure, applications, and data modernization

~50% pays

back in <5

years

4

Disciplined investment process – focus on long-term growth and profitability

$0.7

1

2023

Status

2022 Return

Profile

✓

✓

✓

✓

✓

Distribution

For footnoted information, refer to slide 82

14

CCB INVESTMENTS REPRESENT ~$7.9B OF ~$15.7B IN TOTAL FIRMWIDE INVESTMENTS ($B)

We continue to deliver customer and business value as we modernize our technology

$1.2

$1.4

$1.1

$1.3

$0.3

$0.4

2022 2023 Outlook

~$3.1

Tech

modernization

Product &

design org

Tech modernization: Improve speed and quality to help future-proof the business

Tech product development: Deliver experiences customers love

Tech product

development

$2.7

Channels

Evolve our self-service and

digital capabilities

Products

Offer new products and features

Platforms

Continuously improve to

meet customer needs

Digital channels

Improved self

-service capabilities to

reduce

call volumes by 20% per

customer since 2019

Engagement

Total active digital users up 20%

vs. 2019 as we continue to launch

new features and products

Account opening

~11mm accounts opened digitally, up

37%

vs. 2019

$0.4

Infrastructure

Increase resiliency, scalability,

and delivery

Applications

Faster speed to market

Data

Transform our data housing and

consumption

New data centers & public cloud

~50

%

of applications have migrated out

of legacy data centers, on track to

migrate

~95% by YE 2024

Interoperability

~65%

of customer digital account

opening flows moved to target platform,

on track to reach

99% goal by YE 2023

Cloud migration

~30%

of data is in the public cloud, on

target to reach

50% by YE 2023

Looking forward we expect total CCB investment spend growth to moderate – consistent with a profitable growing franchise

IMPACT BEING DRIVEN BY OUR TECHNOLOGY INVESTMENTS (SELECT EXAMPLES)

1

Note: Totals may not sum due to rounding

15

TECHNOLOGY AND PRODUCT INVESTMENTS ($B)

1

We closely monitor the health of our consumers’ balance sheets (1 of 2)

Median balances are down from their peak but

remain up from pre-pandemic levels

Historical avg. Pandemic high Mar '23

Median deposit balances

Total population

Historical avg. Pandemic high Mar '23

Median operating cash buffers

3

(days)

Total population

Jan ‘20

Mar ‘23

17%

19%

Median nominal income growthvs. inflation

Inflation rate

Nominal income growth (Stable cohort - all incomes)

Nominal income growth (Stable cohort - lowest incomes)

Operating cash buffers remain above pre-pandemic levels

and continue to slowly normalize

Nominal incomes are up but inflation

has impacted real wage gains

All incomes

+84% +21%

Lowest incomes

2

+115% +31%

All incomes

+126%

+75%

Lowest incomes

2

+183%

+92%

31%

4

Stable cohort

1

Stable cohort

1

5

6

For footnoted information, refer to slide 83

16

98%

54%

84%

21%

We closely monitor the health of our consumers’ balance sheets (2 of 2)

39%

11%

9%

36%

4%

3%

FY22 vs. FY19 Apr YTD ('23 vs. '22) Apr ('23 vs. '22)

Total credit and debit spend growth

1

Total population

Change in credit spend Change in debit spend

Overall, spend remains solid as our portfolio is growing

We also track the same customers’ spend over time and see

they have recently started to trade down

$169

$180

4Q19 1Q23

Period-end card outstandings ($B)

3

7%

O/S ($) per

account

Revolve O/S

($) over

same time

period up

~3%

While the number of customers who revolve continues to

normalize, those that do revolve have higher balances

10%

O/S ($) per revolving account

Driven by…

14%

% of revolvers (#)

5

17%

2.4%

-

0…

20%

3.5%

0.3%

FY22 vs. FY19 Apr YTD ('23 vs. '22) Apr ('23 vs. '22)

Credit spend growth

1

Stable cohort

2

All incomes Lowest incomes

(1.2%)

Total population

(9%)

Stable cohort

4

(All incomes)

(5%)

All

incomes

+15%

/ +23% +3% / +2% (2%) / 0%

Lowest

incomes

+19%

/ +23% +4% / +2% 0% / 0%

Stable credit cohort discretionary and non-discretionary spend mix

Total

population

+38%

/ +38%

+10%

/

+8%

+7% / +6%

Credit and debit discretionary and non-discretionary spend mix

For footnoted information, refer to slide 84

17

We’ve maintained a prudent risk profile while we continue to grow the business (1 of 2)

Card

1

Issuer

Sub-Prime Mix Sub-Prime Mix 30+ DQs

Net Credit

Losses

3

4Q19 4Q22

4Q22 as a % of

4Q19

4Q22 as a % of

4Q19

Peer 1 N/D N/D 63% 46%

Chase 16% 13% 78% 54%

Peer 2 18% 16% 77% 56%

Peer 3 20% 18% 97% 70%

Peer 4 23% 20% 79% 59%

Peer 5 32% 20% 79% 70%

Peer 6 28% 26% 82% 68%

Peer 7 33% 31% 87% 75%

Auto

1,2

Issuer

30+ DQs Net Credit Losses

3

4Q22 as a % of 4Q19 4Q22 as a % of 4Q19

Peer 1 82% 87%

Chase 89% 80%

Peer 2 99% 111%

Peer 3 103% 137%

INDUSTRY RISK PERFORMANCE METRICS

1

Peer information sourced from public disclosures

2

Chase Auto excludes Wholesale (DCS) & Lease

3

Represents net charge-offs

18

We’ve maintained a prudent risk profile while we continue to grow the business (2 of 2)

2012 2019 2022

Card

% of portfolio

<660 FICO score

1

16% 16% 13%

% of outstandings from balance

parker segment

2

20% 9% 5%

Auto

3

% of portfolio

<660 credit score

4

22% 18% 16%

% of portfolio

<660 FICO score and

LTV >120

5

1.6% 2.1% 1.3%

Home

Lending

6

Owned

-portfolio avg. FICO

1

692 758 769

Owned

-portfolio avg. CLTV 79% 55% 51%

2019 2022 ∆

Card

% of originations <660 credit score

Industry

7

10% 13% 3ppts

Chase 3% 3% -

Auto

3

% of originations with term ≥84 months

Industry

7

12% 18% 6ppts

Chase 5% 5% -

Home

Lending

% LTV >80 HFI jumbo origination mix

Industry

8

11% 13% 2ppts

Chase 9% 10% 1ppt

ORIGINATION RISK METRICSPORTFOLIO RISK METRICS

For footnoted information, refer to slide 85

19

Credit continues to return to pre-pandemic levels

⚫

Consumer balance sheets and credit remain healthy,

continuing a path of normalization

⚫

Leading credit indicators – notably early delinquency roll-rates

– remain below pre-pandemic levels

⚫

Card entry to delinquency rates are ~80% of pre-pandemic

levels, up from the low point in 2Q21

⚫

Chase Auto loan portfolio loss performance has normalized

to pre-pandemic levels

2019 2020 2021 2022 2023 Outlook

Card

3.10% 2.93% 1.94% 1.47% ~2.6%

Auto

0.33% 0.20% 0.05% 0.21% ~0.5%

Retail only 0.44% 0.25% 0.04% 0.24% ~0.55%

Home Lending

(0.05%) (0.09%) (0.17%) (0.14%) ~0.0%

Business

Banking

1

0.58% 0.57% 0.53% 0.40% ~0.6%

ex. Overdraft 0.47% 0.48% 0.41% 0.17% ~0.35%

< 3.5%

2024 Outlook

> 3.5%

2025 Outlook

CREDIT RISK OUTLOOK NET CHARGE-OFF GUIDANCE

1

Excludes Paycheck Protection Program loans

20

⚫ Primary driver of stress scenario is unemployment rate (UER)

⚫ Losses typically lag UER, and will vary depending on when UER peaks and shape of recovery

⚫ Table on the right shows annualized average losses over the two-year period 1Q24-4Q25, and cumulative losses over the same period

Annualized avg. (%) Cumulative ($)

Central case ~3.5% ~$15.5B

Moderate

recession scenario

~4.8% ~$18.8B

Incremental

+130bps +$3.3B

Estimated 2-Year net credit losses (2024-2025)

Unemployment rate

0%

1%

2%

3%

4%

5%

6%

7%

8%

4Q22 1Q23 2Q23 3Q23 4Q23 1Q24 2Q24 3Q24 4Q24 1Q25 2Q25 3Q25 4Q25 1Q26 2Q26 3Q26 4Q26

Moderate recession (peak 3Q24) Central case

5.1%

7.1%

KEY ASSUMPTIONS – NOT AN OUTLOOK

1

Stress scenario analysis for Card

1

Federal Reserve's 2022 DFAST Results and Methodology Disclosure remains instructive data point for more severe recession

21

Our Home Lending portfolio is in a position of strength with low delinquencies and strong LTVs

Our business is well-positioned given current

levels of equity and portfolio quality

Home Lending portfolio by CLTV

1,2

30+ Delinquency % (based on $)

Financial Crisis Pre-Covid Current

2010

3

Mar ‘20 Mar ‘23

13.5% 1.5% 0.8%

We continue to prepare for a variety of

stress scenarios

30+ delinquency rate at 0.2% if vintages prior to

2010 are excluded

~5% of portfolio resides in 80%+

HPI trough

(5%) (15%)

Peak UER

5.1% 7.1%

Central

case

Moderate

recession

Estimated 2024-2025 NCOs ($mm)

< 100

< 300

47%

21%

16%

11%

4%

1%

<50% 50-60% 60-70% 70-80% 80-90% >=90%

Home prices remain elevated but have begun to

decline from recent peaks

Major markets with >10% forecasted HPI

4,5

declines from peak to YE 2023

▪ Additional expected decline (current to Dec’23)

▪ Actual decline (2022 peak to current)

▪ % HFI 2022 originations

6

-13%

-11%

-10%

-9%

-11%

-6%

-9%

-7%

-9%

-6%

-8%

-6%

-7%

-7%

-7%

-8%

-6%

-8%

-5%

-7%

-4%

-7%

-5%

-3%

9%

6%

2%

3%

3%

1%

1%

3%

1%

1%

4%

11%

-20%

-18%

-17%

-17%

-16%

-14%

-14%

-14%

-13%

-13%

-13%

-10%

San Francisco-Oakland-Hayward, CA

Seattle-Tacoma-Bellevue, WA

Austin-Round Rock, TX

Phoenix-Mesa-Scottsdale, AZ

San Jose-Sunnyvale-Santa Clara, CA

Portland-Vancouver-Hillsboro, OR-WA

Las Vegas-Henderson-Paradise, NV

Denver-Aurora-Lakewood, CO

Sacramento-Roseville-Arden-Arcade, CA

Nashville-Davidson-Murfreesboro-Franklin, TN

San Diego-Carlsbad, CA

Los Angeles-Long Beach-Anaheim, CA

For footnoted information, refer to slide 86

22

We run our business for the long-term and manage through cycles

Forward-looking guidance of 25%+ ROE through the cycle

Current outlook is

uncertain

as macro factors may pressure

short term returns

Benefits of

reprice lags

Deposit outlook Credit trends

We leverage the power

of the CCB franchise

remaining confident in our

strategies through cycles

Scale of our

customer

relationships

Strength and

diversification of

our businesses

Operational

excellence and

discipline

Investment

through cycles

with unmatched

capacity

23

We have consistently driven core growth and strong returns over the long term

For footnoted information, refer to slide 87

$11.7

$12.3

$13.4

$14.4

$15.2

$15.0

$19.4

$21.7

$18.8

$18.1

$20.9

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

$1,066 $2,249

7.1% (#3) 10.9%

(#1)

20.5% (#2)

22.4%

(#1)

17.7% (#1)

17.3%

(#1)

6.2% (#3) 9.3% (#1)

Fed Funds effective rate

6

CCB pretax income ex. LLR ($B)

5

CCB ROE ex. LLR

5

Client balances ($B)

7

: 8% CAGR

Retail deposit share (%)

8

: +380bps

Card sales market share (%)

9

: +190bps

BB Primary bank share (%)

10

: +310bps

0.14%

0.11%

0.09%

0.13%

0.40%

1.00%

1.83%

2.16%

0.38%

0.08%

1.68%

16%

15%

15%

17%

18%

18%

28%

31%

26%

26%

31%

Card O/S share (%): (40bps)

Card O/S share is

up >200bps since

2012 when

adjusting for risk-

appetite

CONSUMER & COMMUNITY BANKING – 10-YEAR PERFORMANCE

1,2,3,4

24

25

We are making strong progress against our strategy

#1

retail bank based on

deposits

1

Consumer

Banking

Branch

Network

⚫ Grow: ~40mm customers, up 14% since 2019

2

⚫ Engage: ~80% primary bank

⚫ Deepen: ~50% of primary customers are multi-LOB

3

1

st

bank in all lower

48 states

⚫ Grow: #1 deposit share in 11 of top 50 markets

4

⚫ Engage: >75% of balances held by regular branch visitors

5

⚫ Deepen: ~20% increase in banker productivity since 2019

Optimize and extend our

branch network to reach and

gain trust in more local

communities

Strengthen and tailor our

customer value propositions

to extend leadership

position

Consumer Banking Branch Network Business Banking Card & Connected Commerce

WE’RE THE MARKET LEADER OUR STRATEGY IS WORKING AND WE WILL EXTEND OUR LEAD

For footnoted information, refer to slide 88

26

We have continued to drive core growth in our business

Consumer Banking Branch Network Business Banking Card & Connected Commerce

27

1

“Consumer Banking customer” reflects unique individuals that have financial ownership or decision making power with respect to Consumer Banking accounts

14%

11%

35.4

37.9

39.2

40.4

2019 2020 2021 2022

14%

We added 1.6mm

net new checking

accounts in 2022

4.5%

CAGR

Consumer Banking customers (mm)

1

Average deposits ($B)

$535 $629 $772 $848

Debit card sales ($B)

$314 $339 $414 $431

18.3%

11.3%

10.1%

Our core customer growth has driven significant outperformance

9.1%

9.9%

9.8%

10.9%

10.3%

9.8%

2019

2022

2019

2022

2019

2022

#3 #1 #1 #2 #2 #3

Rank

4

+180bps +40bps flat

Chase Peer 1 Peer 2

Chase Large Banks

2

Industry

(ex. Chase)

3-year deposit CAGR

1

WE OUTPERFORMED PEERS IN DEPOSIT GROWTH SINCE 2019…

National retail deposit share

3

…WHICH HAS LED TO ~180BPS OF DEPOSIT SHARE GAIN

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 89

28

Satisfied

Loyal

Engaged

Our primary bank customers are satisfied, loyal, and engaged

~80%

of primary bank customers

would recommend Chase

2

of Consumer Banking checking customers

partner with us as their primary bank

1

~80%

of Consumer Banking Gen Z and Millennial

consumer checking customers are primary bank

retention rate among

primary bank customers

4

>95%

>75%

>75% >75%

of customers are

mobile active

7

of balances held by customers

who regularly use branches

6

customer satisfaction across

branch and digital channels

3

Record high

of primary bank customers choose

Chase for other financial needs

5

~50%

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 90

29

Our customers engage with Chase to make payments and manage their finances

2019 2022

Cash & check

Debit

Digital

~40%

(25%)

~26mm

active Zelle

customers

2

>35

monthly debit transactions

per active debit customer

3

2019 2022

Mobile-active

>75%

+9ppts

Not mobile-active

~50%

of mobile-active Consumer

Banking users engage with

our financial health tools

5

~9B

digital logins by

Consumer Banking

users

6

Transactions by method of payment

1

CUSTOMERS ARE SHIFTING TO DIGITAL PAYMENTS…

Mobile engagement

4

…AND USING THE CHASE APP TO MANAGE THEIR FINANCES

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 91

30

Wealth

Management

Business

Banking

Credit

Card

Home

Lending

>75%

of retail volume is from

Consumer Banking

customers

>75%

of Business Banking clients

also have a Consumer

Banking relationship

>45%

of Branded Card members

are also Consumer

Banking customers

1

~90%

of Wealth Management

relationships also have a

Consumer Banking relationship

2

~50% of Consumer Banking primary customers are engaged across products

Increases relationship value

Strengthens banking relationship

Lowers cost of acquisition

Consumer

Banking

CONSUMER BANKING SERVES A HIGH PROPORTION OF CUSTOMERS ACROSS EACH LOB AND GENERATES TREMENDOUS VALUE FOR THE FIRM

Consumer Banking Branch Network Business Banking Card & Connected Commerce

31

1

Excludes small business customers

2

Consumer and small businesses with Wealth Management relationships with balances >$0

We continue to strengthen our value proposition to meet the needs of customers across segments

2019 2022

2019 2022

Products &

Services

Advice

⚫ Launched Early Direct Deposit on Secure

Banking

⚫ Launching Freedom Rise for new-to-credit

⚫ Scaled Community Centers and branches

to build trust and financial health locally

⚫ Developing Credit Journey features for

credit building and new-to-credit

⚫ Deployed higher yield options for cash

management

⚫ Improved payments experiences

⚫ Launched Wealth Plan to help clients plan

for the future

⚫ Adding banker and advisor capacity to

serve more client needs

Low-cost entry to banking with tailored

solutions to build financial health

Relationship proposition to meet

banking, lending, and investing needs

2019 2022

⚫ Strengthened Overdraft Assist with next day

no fee / $50 buffer

⚫ Launched Pay in 4 to select customers

⚫ Launched Personal Advisors for mass

affluent clients looking for low-cost advice

⚫ Continuing branch expansion to serve more

communities

Full-service banking solution to meet

spend, save, and liquidity needs

Emerging segments Affluent segmentsMass market segments

~75%

~5%

~20%

% of accounts

4

# OF LOW-COST

CHECKING ACCOUNTS

1

# OF MASS MARKET

CHECKING ACCOUNTS

2

# OF PRIVATE CLIENT RELATIONSHIPS

WITH DEPOSITS AND INVESTMENTS

3

Consumer Banking Branch Network Business Banking Card & Connected Commerce

~40%

~10%

~30%

For footnoted information, refer to slide 92

32

33

5,293

4,831

2017 2022

We have accelerated our growth as we have extended and optimized our branch network

$119

$227

2017 2022

Chase Large banks

2

(ex. Chase)

% of current network opened

in the last five years

4

15% 3%

% of network consolidated in

the last five years

5

22% 24%

(1.8%) CAGR

Large Banks

2

(ex. Chase)

(4.7%) CAGR

13.8% CAGR

Large banks

2

(ex. Chase)

$165mm

3

Chase Large banks

2

(ex. Chase)

Deposits per branch

(10+ years cohort)

4

$259mm $170mm

Deposits per branch

(5

-10 years cohort)

4

$154mm $97mm

BRANCH COUNT

1

DEPOSITS PER BRANCH ($mm)

1,6

Consumer Banking Branch Network Business Banking Card & Connected Commerce

We have increased the number of consumer and small business customers per branch by ~30% from 2019 to 2022

7

For footnoted information, refer to slide 93

34

Network expansion creates an unparalleled growth engine

Meaningful contribution:

7%

3%

15%

5%

3%

6%

79%

88%

94%

ChaseLarge banks

2

(ex. Chase)

0-5 years

10+ years

~$85B

in deposit growth since

2017 from branches

<10 years old

3

5-10 years

~4 year

break-even on

new builds

4

More upside:

~$160B

in incremental deposits as our

branches mature to look like our

seasoned network

5

<5%

branch share in 19 of the top 50

markets, including 3 of the top 10

(DC, Boston, Philadelphia)

1,6

Industry

Branch network by age cohort

1

WE HAVE INVESTED IN NEW BRANCHES FASTER THAN PEERS

THESE INVESTMENTS ARE CONTRIBUTING MEANINGFULLY

TO OUR PERFORMANCE, WITH MORE UPSIDE

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 94

35

We have a demonstrated ability to grow in different starting positions and markets

11.6%

14.8%

20.4%

2012 2017 2022

1.6%

4.2%

6.3%

2012 2017 2022

0.8%

2012 2017 2022

Out of footprint

8.8ppts

111

new builds from

2012-2022

4

~$9B

deposit growth from

2012-2022

1

~$2B

deposit growth from

2017-2022

1

4.7ppts

13.7% 16.5% 16.9%

Branch

share

2

5.7% 6.7% 8.7%

Branch

share

2

0.0% 0.0% 2.6%

Branch

share

2,3

~$86B

deposit growth from

2012-2022

1

42

new builds from

2017-2022

4

35

new builds from

2012-2022

4

0.8ppts

Deposit share

1

LOS ANGELES

Deposit share

1

ATLANTA

Deposit share

1

BOSTON

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 95

36

Branches are an important part of our omnichannel service and engagement model

2019 2022

Branch-

centric

Multi-

channel

Digitally-

centric

2019 2022

>75% of balances are held by customers

who regularly use branches

(~25%)

~20%

Everyday branch transactions

1

WE ENABLE CUSTOMERS TO SELF-SERVE

Balance by customer channel engagement behavior

2

CUSTOMERS CONTINUE TO VISIT BRANCHES

Productivity per banker

3

WE ARE MEETING MORE CLIENT NEEDS

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 96

37

Wealth

Management

Business

Banking

Credit

Card

Home

Lending

Our branches are the storefront for JPMC across lines of business

~50%

of mortgages are

originated in branches

2

~85%

of business checking accounts

are opened in branches

~25%

of Branded credit cards are

opened in branches

>85%

of first-time investors come

from banker referrals

1

Branch team

of experts

OUR BRANCH TEAMS GENERATE TREMENDOUS VALUE FOR THE FIRM ACROSS CCB AND JPMC MORE BROADLY

Creates a talent pipeline

Serves a wide range of client needs

Drives acquisitions across channels

Consumer Banking Branch Network Business Banking Card & Connected Commerce

38

1

Represents first-time investors with full-service relationships through Chase Wealth Management

2

Represents mortgage originations from branch Home Lending Advisors

We are extending our network to cover more Americans and gain trust in local communities

5,293

Branches

1

4,831

~60%

U.S. population coverage

by market

3

~80%

50%

U.S. populationcoverage

within a 10-minute drive time

4

60%

68%

Small business coverage

5

87%

$4.4T

Addressable deposits

6

$7.9T

~85%

coverage

by market

Looking ahead:

~70%

coverage within a

10-minute drive time

2017 CHASE BRANCH NETWORK COVERAGE BY STATE

1

2022 CHASE BRANCH NETWORK COVERAGE BY STATE

1

Consumer Banking Branch Network Business Banking Card & Connected Commerce

Increasing branch share

2

For footnoted information, refer to slide 97

39

40

41

585

The small business ecosystem remains healthy despite economic headwinds

Monthly small business formations (#k)

1

Small business formations are elevated vs. pre-pandemic…

40

140

240

340

440

540

640

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

Consumer Banking Branch Network Business Banking Card & Connected Commerce

Small business optimism index

2

…and while optimism remains low…

80

85

90

95

100

105

110

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

Cash buffers (# of days of reserves, indexed to start of period)

3

…our clients are healthy, with strong cash buffers…

30-day delinquency rates (relative to start of period)

3

…and relatively low delinquencies

60%

80%

100%

120%

140%

160%

180%

200%

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

-0.8%

-0.4%

0.0%

0.4%

0.8%

615

355

101

90

100%

187%

130%

Start

91

Pandemic peak

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

+46bps

-13bps

-80bps

-40bps

0bps

+40bps

+80bps

1

Source: U.S. Census – Business and Industry Time Series, Monthly Business Formation Statistics; not seasonally adjusted

2

Source: NFIB: Optimism Index

3

Cash buffers data based on fixed cohort of clients active in both January 2020 and November 2022, with balances/outflows tracked from January 2019–March 2023; delinquency rates based on both Business Banking line/loan and Chase Small Business Card – excl. PPP loans, overdrafts

42

We serve ~6mm small- and medium-sized businesses (SMBs) across Chase for Business

1

Consumer Banking

Entrepreneurs who start businesses

Chase for Business

<$20mm sales size

Commercial Banking

~$20mm-$2B sales size

2

Corporate & Investment Bank

>$2B sales size

Business Banking Business Card Payments Services

#1

Primary bank market share

3

Today’s focus

#2

SMB credit card spend

3

#1

Payment provider for Business

Banking clients

1

Consumer Banking Branch Network Business Banking Card & Connected Commerce

1

6MM client count as of December 2022; payment provider rank as of April 2023

2

Annual sales size thresholds are directional and do not apply to select core segments and specialized industries within Commercial Banking

3

Primary bank market share sourced from Barlow Research Associates as of 4Q22. Rolling 8-quarter average of small businesses with sales size between $100k-$25mm; SMB credit card spend share based on internal estimates of Nilson (only 2021 available) and 2022 actuals if available

43

We help businesses of all sizes start, run, and grow with Chase

WE SERVE ALL TYPES OF SMALL- AND

MEDIUM-SIZED BUSINESSES…

~65%

of BB clients start in

Consumer Banking

~30%

of large BB clients

started as small clients

2

>15%

of new Middle Market

relationships come

from BB

1

Start Run Grow

~40%

~50%

~10%

<$100k $100k-$1mm >$1mm

(1) Professional Services

(2) Real Estate

(3) Construction

(4) Retail

(5) Healthcare

(6) Transportation

(7) Other

6.2%

9.3%

2012 2022

#3 #1

+310bps

Primary bank market share and rank

3

Annual sales size and industry mix of BB clients

Consumer Banking Branch Network Business Banking Card & Connected Commerce

1

2

3

4

5

6

7

…HELPING THEM START,

RUN, AND GROW…

…EARNING US THE RIGHT TO BE THE

TOP BUSINESS BANK IN THE U.S.

1

Data reflects FY2022

2

Large clients defined as businesses with an annual sales size of $1mm or greater; Small clients defined as businesses with an annual sales size of under $1mm; captures client sales size growth between 2020 and 2022

3

Primary bank market share sourced from Barlow Research Associates as of 4Q22. Rolling 8-quarter average of small businesses with sales size between $100k-$25mm

44

Our business is growing rapidly and delivers strong economics

Business Banking clients (mm)

2.9

3.2

3.5

3.8

0

0.5

1

1.5

2

2.5

3

3.5

4

2019 2020 2021 2022

Average deposits ($B)

$136 $175 $226 $259

Average loans

ex. PPP ($B)

$24 $24 $22 $20

Primary bank rank

1

#1 #1 #1 #1

30%

OUR BUSINESS HAS GROWN SIGNIFICANTLY…

~3x

higher balances per average BB

account vs. average Consumer

Banking account

~80%

of balances in noninterest-

bearing checking accounts

~9% CAGR

+ 90%

since ‘19

We originated >340k

net new checking

accounts in 2022

Consumer Banking Branch Network Business Banking Card & Connected Commerce

…THESE RELATIONSHIPS

HAVE STRONG ECONOMICS

1

Primary bank market share sourced from Barlow Research Associates as of 4Q22. Rolling 8-quarter average of small businesses with sales size between $100k-$25mm

45

The key to our success is continuing to win clients’ primary bank relationships

Are satisfied

~70%

digital and

~85%

branch satisfaction

Are loyal

~95%

retention rate

1

Are engaged

~75%

use multiple channels

2

Have higher balances

~4x

higher balances vs. non-primary

Have multiple products

~10ppts

higher SMB card ownership

2 of 3

Chase Business Banking clients choose us for

their primary operating account

These clients:

2. An industry-leading

omnichannel service model

anytime, anywhere, in the channel

of their choice

1. A complete suite of products and

services that make Chase the

best place to start, run, and grow a

small business

PRIMARY CLIENTS ARE SATISFIED, LOYAL, AND ENGAGED

Consumer Banking Branch Network Business Banking Card & Connected Commerce

WE EARN PRIMARY BANK RELATIONSHIPS THROUGH

BEST-IN-CLASS SOLUTIONS AND EXPERIENCES

1

Excluding businesses <2 years old from formation

2

Both digital and branch active in 2022

46

Our comprehensive suite of financial products and services makes Chase the best place to start, run, and

grow a small business

✓ Entry-level and premium checking

✓ LegalZoom partnership

✓ Payments services including Zelle, Wires, Bill Pay

✓ Coming soon: Digitizing more customer activities

✓ Coming soon: Invoicing

Banking and Cash Management

Invoicing

✓ Entry-level, premium, and co-brand credit cards

✓ SBA

1

, small- and large-dollar lending, digital lending

✓ Coming soon: Expanding Credit Journey

Credit Card / Lending

Lending platform modernization

⚫

6 app inputs

(vs. 50+)

2

⚫

<5 mins to

complete

⚫

Automated

post-app

tasks

✓ Merchant Services integrated with core banking

✓ Everyday 401(k)

✓ Fraud Hub

✓ Coming soon: Tap To Pay

✓ Coming soon: Payroll

Merchant and Adjacent Services

Everyday 401(k)

Consumer Banking Branch Network Business Banking Card & Connected Commerce

1

Small Business Administration

2

Comparison reflects comparable product on modernized platform vs. legacy

47

Our best-in-class omnichannel offering allows us to serve our clients anytime, anywhere, in the channel of

their choice

Multi-

channel

~80%

of clients are

digitally active

~65%

of clients are multi-

channel active

Deliver more omnichannel experiences:

⚫ Interactive demos for prospects

⚫ Video meetings for bankers and clients

⚫ Schedule a banker meeting online

Amplify our digital channels with:

⚫ Enhanced merchant offers

⚫ Expanded Credit Journey

⚫ Enhanced customer insights

>1B digital log-ins

in 2022

~85% branch satisfaction,

~70% digital satisfaction

Serving our

clients anytime,

anywhere, in the

channel of their

choice

Digital

People

Physical

Network

~90%

of assigned

clients met with a

Relationship Manager

2

~80%

of clients visit a

branch

Continue to leverage our expanding branch

footprint which currently covers 87% of U.S.

small businesses

1

Hire ~1,000 Relationship Managers by 2025,

given assigned clients have:

⚫ Higher retention

⚫ More multi-product relationships

⚫ Higher customer satisfaction

~4,800 Chase branches,

>15,000 ATMs

~12,000 Consumer Bankers &

~2,300 Business Relationship

Managers

Consumer Banking Branch Network Business Banking Card & Connected Commerce

1

Small business coverage by CBSA based on Dun and Bradstreet Small Business locations. Small business defined as <$20mm in annual sales size

2

180-day contact rate for clients assigned to either a remote or in-person Business Relationship Manager

48

The value of Business Banking relationships extends to the rest of CCB and JPMC

>15%

of new Middle Market

relationships came from

BB last year

~40%

of total CCB deposits held

by BB clients

1

>5ppt

higher share of Private

Bank client wallet when

they have BB relationship

2

~50%

more Business Card

clients with a BB

relationship vs. 2019

>75% >2x

of accounts opened by existing CCB

clients are originated without a

marketing offer

higher average BB client revenue when

clients have multiple CCB relationships

(vs. BB-only)

Increased revenue per clientLower cost of acquisition

Business Banking

generates

tremendous value

for the Firm…

…and benefits

significantly from

CCB and JPMC

Card

Banking &

Wealth

Private

Bank

Commercial

Banking

Business

Banking

Consumer Banking Branch Network Business Banking Card & Connected Commerce

1

Includes deposits held by Business Banking clients in business and personal accounts; as of January 2023

2

Excludes Private Bank clients who are only associated with Business Banking clients generating <$100k sales size, and client records that do not have wallet share data available; as of May 2023

49

We have a compelling opportunity for continued growth

Industry-leading share of a

rapidly-growing market

✓ ~450k small businesses formed each month

1

✓ #1 primary bank share

2

✓ ~9% annual client growth since 2019

✓ ~80% of balances in noninterest-bearing checking accounts

✓ ~40% of CCB deposits are held by BB clients

✓ ~2,300 Business Relationship Managers held 1.4mm

3

client meetings

✓ ~4,800 branches that reach 87% of U.S. small businesses

4

✓ ~80% of clients are digitally active, with >1B total log-ins in 2022

Unparalleled scale with a

localized service model

Strong unit economics and

contribution to the Firm

Consumer Banking Branch Network Business Banking Card & Connected Commerce

For footnoted information, refer to slide 97

50

4.8

2.7

2.4

2019 2021 2022

5.9

6.4

6.5

2019 2021 2022

11.5

12.1

13.7

2019 2021 2022

31%

35%

32%

2019 2021 2022

Our Card franchise continues to be the industry leader in sales and outstanding balances

43

47

52

2019 2021 2022

16.4

14.8

16.1

2019 2021 2022

156

140

163

2019 2021 2022

763

893

1,065

2019 2021 2022

Active accounts (mm)

2

Average outstandings ($B)

Sales volume ($B)

Revenue ($B)

3

21%

40%

4%

Risk-adjusted revenue ($B)

3,4

19%

Net charge-offs ($B) ROE ex. LLR

4

(50%)

Pretax income ex. LLR ($B)

4

10%

3.10% 1.94% 1.47%

NCO Rate

(2%)

#1

in card sales volume since 2017

1

#1

in card outstandings for more than a decade

1

98%

customer retention in 2022

WE CONTINUED TO SCALE ACTIVE ACCOUNTS AND SALES – AND HAVE SEEN AVERAGE OUTSTANDINGS REBOUND FROM PANDEMIC LOWS

WE MAINTAINED OUR POSITION OF STRENGTH

1Q23 EOP O/S of $180B

Consumer Banking Branch Network Business Banking Card & Connected Commerce

51

For footnoted information, refer to slide 99

Our strategy will drive sustained success while making our business more resilient over time

STRATEGY

Create deeper

customer

relationships

Grow our card

member base across

key segments

Engage through

experiences

customers love

WHAT WINNING LOOKS LIKE

>$30B

volume through our Commerce

platforms in 2025

70 NPS

across Card and Commerce

experiences

⚫ Drive sticky relationships with customers through best-in-class experiences

⚫ Deepen relationships with customers across CCB and merchants across JPMC

⚫ Launch new, tailored products to win in key segments, including SMB and Starter

⚫ Fuel continued growth through our world-class marketing and distribution engine

⚫ Build out our two-sided platform through Connected Commerce

⚫ Continue to expand on our core enablers: payments and lending capabilities

20%

share of industry outstandings

in Card

ACTIONS WE ARE TAKING

Consumer Banking Branch Network Business Banking Card & Connected Commerce

52

10.7%

12.0%

21.8%

22.4%

20.4%

20.4%

2017 2018 2019 2020 2021 2022

We continually launch and refresh Card value propositions to deliver industry leading engagement

sales share

3

#1

Peer 1

Peer 2

10.0%

10.8%

16.2%

17.3%

7.0%

8.8%

2017 2018 2019 2020 2021 2022

outstandings share

3

#1

Peer 1

Peer 2

24 products launched or refreshed

since 2019

97% of co-brand sales contractually

extended to at least 2027

1

CARD HIGHLIGHTS

Continually launching and refreshing our world-class card products

while building stronger partnerships to expand our reach

Investing in new lifestyle benefits and experiences to differentiate

our products, and grow engagement with our customer base

3 airport lounges launched, with 2

more coming later this year

~70% of fee-based card demand

driven by Millennial and Gen Z

2

Consumer Banking Branch Network Business Banking Card & Connected Commerce

MARKET PERFORMANCE

53

For footnoted information, refer to slide 100

We are investing in products and experiences for key segments to drive growth

Strategic Focus Progress

Starter

Launching Freedom Rise in select channels this year

Leveraging the strategic advantage

of our branches to help new-to-

credit prospects

Affluent

Differentiating with investments in

travel and dining assets and

capabilities

Closely integrating key assets with the Sapphire brand

Small

Business

Expanding our product suite to

better serve the full continuum of

SMB needs

Launched Business Premier in all channels in October 2022

Lounges

Concierge

Services

Dining

Addressable Market

U.S. consumers

1

>25mm

U.S. SMBs

2

>40mm

U.S. consumers

3

>40mm

Consumer Banking Branch Network Business Banking Card & Connected Commerce

54

For footnoted information, refer to slide 101

$3.1

$2.1

$3.8

$4.0

$4.3

$1.3

$1.1

$1.4

$1.7

$1.6

2019 2020 2021 2022 ID Outlook 2022 Actuals

Product Benefits

(incl. co-brand)

Acquisition,

Distribution & Media

Our marketing engine fuels our scale and distribution

CARD GROSS CASH MARKETING SPEND ($B)

1

KEY DRIVERS AND PERFORMANCE METRICS

$4.5

$5.9

Revenue

Outlook from 2022 ID Revised Outlook

>30%

2

>50%

2

New accounts – 2022 vintage vs. 2019

New accounts

14% 23%

Active accounts

Outlook from 2022 ID 2022 Actuals

16% 21%

Total portfolio – 2022 vs. 2019

Sales volume

33% 40%

Annual fee

revenue

20% 28%

$3.2

$5.2

$5.7

Our disciplined approach to marketing enables us to generate predictable returns

Lifetime value

>1.5x

3

>1.7x

3

Consumer Banking Branch Network Business Banking Card & Connected Commerce

55

For footnoted information, refer to slide 102

We are improving productivity to better acquire and serve customers, and optimize expense

⚫ Our channels are getting more productive

Of new Branded card accounts acquired

through owned-channels in 2022 (+3ppts YoY)

1

85%

⚫ Our discipline drives more efficient account production

Decrease in customer call-in rates

since 2019

2

3ppts

Increase in accounts originated from pre-

qualified offers in 2022 vs. 2021

4ppts

⚫ Our investments drive a more seamless experience

Increase in digital active card customers

as % of total card base since 2019

5ppts

Improvement in Card fraud loss rate

since 2019

~1.5bps

Increase in new account production in 2022

vs. 2021

21%

⚫ Our ecosystem is serving customers more efficiently

WE ARE MORE PRODUCTIVE AT ACQUIRING CUSTOMERS… …AND SERVING THEM MORE EFFICIENTLY ONCE ACQUIRED

Consumer Banking Branch Network Business Banking Card & Connected Commerce

56

1

Owned channels include phone, chase.com, refer a friend, retail, and direct mail

2

Call-in rate is defined as the number of customer calls to specialists relative to annual customer statements

Our two-sided platform delivers unmatched value for consumers and brands

BrandsConsumers

>63mm

Digital active customers

2

>20

Monthly mobile logins per user

Digital Ecosystem

#1

Credit card issuer with >$1T in sales

>$5.6T

Payments volume

1

Consumer Payments

#1

Consumer bank based on deposits

#1

Most visited banking portal in U.S.

3

Base Beyond Card

Airlines

Hotels

Offers & Shopping

Dining

And >650 Luxury Hotel & Resort Collection partners

And >500 merchants on Chase Offers in 2022

Benefits

Scale of our assets Breadth of our solutions Richness of our data

No provider can match the:

Connected

Commerce

~300k hotel properties including…

>200 airline partners including…

Consumer Banking Branch Network Business Banking Card & Connected Commerce

57

For footnoted information, refer to slide 103

We are on-track to become a household name in premium leisure travel

>$3B

~$8B

~$15B

2019 2022 2025 Outlook

Chase Travel sales volume ($B)

3

✓ On track to hit ~$10B in Chase Travel sales this year

Chase Travel

Creating an end-to-end journey that delivers curated content,

unique experiences, and elevated servicing while operating as

a self-sustaining business

Booking platform that enables end-

to-end control over the experience

Highly-tenured agents that deliver

unique, customized trips

High Tech High Touch

1 in 4

Leisure travel dollars spent

on Chase cards

24%

YoY growth in transactions

through Chase Travel

2

Top 5

Consumer leisure

travel provider

1

~40%

YoY growth in customers

purchasing travel on Chase

2

PERFORMANCE HIGHLIGHTS CHASE TRAVEL VISION

Consumer Banking Branch Network Business Banking Card & Connected Commerce

58

For footnoted information, refer to slide 104

We are applying our consistent playbook to expand beyond Travel to win in Shopping and Dining

Where we are on our strategy

Identify high value experiences

that resonate with card members

Our strategy will migrate category spend to our platforms – driving >$30B in volume and ~$2B in revenue in 2025

Acquire capabilities to create

differentiated on-us journeys and

own the economics

1 3

Accelerate engagement in

existing channels and products

with benefits, rewards, and content

2

Key success metrics

1

Addressable spend

Travel

Reaching new customers through

premium servicing and content

in Chase Travel

sales volume

3

~$8B

Chase Travel visits

~40mm

Category spend on

Chase cards

2

>$140B

Shopping

Integrating our platform and data to enable

better targeting and personalization

in attribution spend

volume

5

>$6B

Offers served to

customers

4

>9B

Category spend on

Chase cards

2

>$470B

Dining

Expanding access to curated content and

experiences to accelerate engagement

Unique monthly

visitors

7

>5mm

Venues covered

6

>25k

Category spend on

Chase cards

2

>$90B

Journey

Make Chase the best platform to

book travel, explore shopping, and

discover new dining experiences

HOW WE’RE APPLYING OUR PLAYBOOK:

OUR COMMERCE PLAYBOOK:

Consumer Banking Branch Network Business Banking Card & Connected Commerce

59

For footnoted information, refer to slide 105

Payments and lending innovation are core enablers of our Connected Commerce strategy

>$5.6T

Payments volume

1

Installments at POSCard-linked installments

>27B

Payment transactions

1

2022 HIGHLIGHTS

Pay in 4 Paze

Card-based Pay-over-time solutions Checkout

Credit and debit

Highly engaged payments

4

customers have higher average NPS and higher likelihood to have multi-LOB relationships

>67mm

Payments active

customers

2

>25mm

Customers transacting >1

times a day

>$1.5T

Credit and debit spend

volume

Live today Live today Launching soon Launching soon

3

My Chase Plan originations

scaled 3x faster than BNPL

competitor outflows YoY

SM

Consumer Banking Branch Network Business Banking Card & Connected Commerce

$260.42 $130.21 $86.81

60

For footnoted information, refer to slide 106

We are investing in critical capabilities and experiences to better serve customers across all segments

“Best hotel co-brand

credit card”

– The Points Guy

1

“Best hotel travel

card”

– CNN

7

“Best cash-back

credit card”

– CNBC Select

6

“Best airline

credit card”

– Forbes Advisor

5

“Best overall

business card”

– CNET

3

70 NPS

On our path to achieving

NPS for select segments, 2022

Usage of machine learning to understand drivers of dissatisfaction

Investments in servicing innovation (e.g., dispute tools, chatbots)

Value of NPS: satisfied customers spend >30% more and attrite ~2x less

8

Customer complaints, 2019-2022

“Best card for small

businesses”

– Money.com

2

“Best travel rewards

credit card”

– The Points Guy

1

“Best premium card

for travel and dining”

– Business Insider

4

WE ARE BEING RECOGNIZED FOR THE WORK WE ARE DOING… …AND ARE TAKING ACTION TO BUILD UPON THIS MOMENTUM

Reduction in customer complaints

19%

+3 NPS

for Mass

vs. 2021

+1 NPS

for SMB

vs. 2021

+2 NPS

for Affluent

vs. 2021

Consumer Banking Branch Network Business Banking Card & Connected Commerce

61

For footnoted information, refer to slide 107

Consumer

Bank

Corporate &

Investment

Bank

~25%

of Chase Offers merchants

sourced through our B2B

franchises in 2022

2

>45%

of Branded Card members

are also Consumer Banking

customers

1

~40%

of SMB Card members

have a Business Banking

relationship

~17ppts

higher Card approval rate

when customer has a

deposit account

Being part of the JPMC ecosystem broadens our scale and distribution

Card

Card contributed ~50% of new CCB customers in 2022 – providing a significant deepening opportunity to the franchise

1

Consumer Banking Branch Network Business Banking Card & Connected Commerce

Business

Bank

62

1

Excludes small business customers

2

Reflects offers sourced through J.P. Morgan Payments and Business Banking

63

Our competitive advantages will enable sustained outperformance for decades to come

Forward-looking guidance of 25%+ ROE through the cycle

The scale of our

customer relationships is

the catalyst for everything

We operate with

excellence and execute

with discipline

We run this franchise for

the long term, with

unmatched capacity

to invest

The strength and

diversification of our

businesses create

resilience of returns

The Power of the CCB Franchise

64

65

Expert advice

and guidance

Premium

service

Value for

relationship

Elevated service and seamless experiences

⚫

Cross-product priority servicing experience

⚫

Higher limits and enhanced authorizations

⚫

Proactive client servicing

Easy access to a team of experts

⚫

Banker or advisor as a relationship quarterback

⚫

Financial planning, investment, and borrowing advice

⚫

Expanded banker and advisor capacity

Access to our best products and benefits

⚫

Expanded banking and investment services

⚫

Relationship-based pricing across products

⚫

Exclusive lifestyle benefits

First Republic provides capabilities to accelerate our existing affluent strategy

First Republic model CCB affluent strategy

High-touch servicing model

with industry-leading NPS and high client

and employee retention

Team of experts

to serve affluent client needs with a primary

relationship quarterback

Relationship-based lending

to acquire and deepen affluent relationships

Single family Multi-family CRE C&I Capital Call

RMs Business Bankers Preferred Bankers Wealth Managers

Preferred Banking Preferred Banking Offices WealthLending

66

First Republic value to Chase

Deepening opportunity

serving affluent client

lending needs

High quality loan

portfolio

strong LTVs, high FICO

scores

Relationship manager-

led acquisition

to drive firm value beyond

lending

First Republic has a unique operating model and strong loan portfolio

First Republic Portfolio Risk Metrics

1

Avg. CLTV

59%

Avg. FICO

774

Avg. Debt-to-

Income

30%

% CA or NY

77%

Avg. Balance

Outstandings

3

~$1.1mm

Loan Portfolio

2

~$100B

1

First Republic residential loan portfolio; funded loans only; CLTV and DTI reported as of time of origination

2

Prior to fair value marks

3

Average mortgage balance outstanding reflects unpaid principal balance

67

We provide advice across the wealth continuum and continue to grow our channels

Global

Private Bank

Advice-driven platform across

wealth, lending, and banking

Target client:

HNW / UHNW

Private Client Advisors

4,500+

Client investment assets

~$410B

Advisors

450+

Client investment assets

~$190B

Personal

Advisors

Lower-cost

remote advice

Target client:

Mass Affluent

Full-Service Wealth Management

Chase Wealth Management J.P. Morgan Advisors

CCB

AWM

Target client: Affluent Target client: Affluent / HNW

1

/ UHNW

2

Added 300+ Advisors in 2022

and on-track to scale

to 6k by 2025

✓

Launched Personal Advisors

to offer lower cost

advice (4Q22)

✓

Rolled out Wealth Plan

to Chase clients and

advisors (4Q22)

✓

Wealth Management Advised Channels

Added ~400 Client Advisors

and on-track to scale

to 4k by 2025

✓

We have invested to strengthen and scale our advised channels

1

High net-worth

2

Ultra high net-worth

68

First Republic Private Wealth Management adds scale to our office-based model

Global

Private Bank

Advice-driven platform across

wealth, lending, and banking

Target client:

HNW / UHNW

Private Client Advisors

4,500+

Client investment assets

~$410B

Advisors

450+

Client investment assets

~$190B

Personal

Advisors

Lower-cost

remote advice

Target client:

Mass Affluent

Full-Service Wealth Management

Chase Wealth Management J.P. Morgan Advisors

CCB

AWM

Target client: Affluent

Wealth Management Advised Channels

First Republic Private Wealth

Management

Private Wealth Advisors

~200

Client investment assets

~$200B

Target client: Affluent / HNW

1

/ UHNW

2

1

High net-worth

2

Ultra high net-worth

69

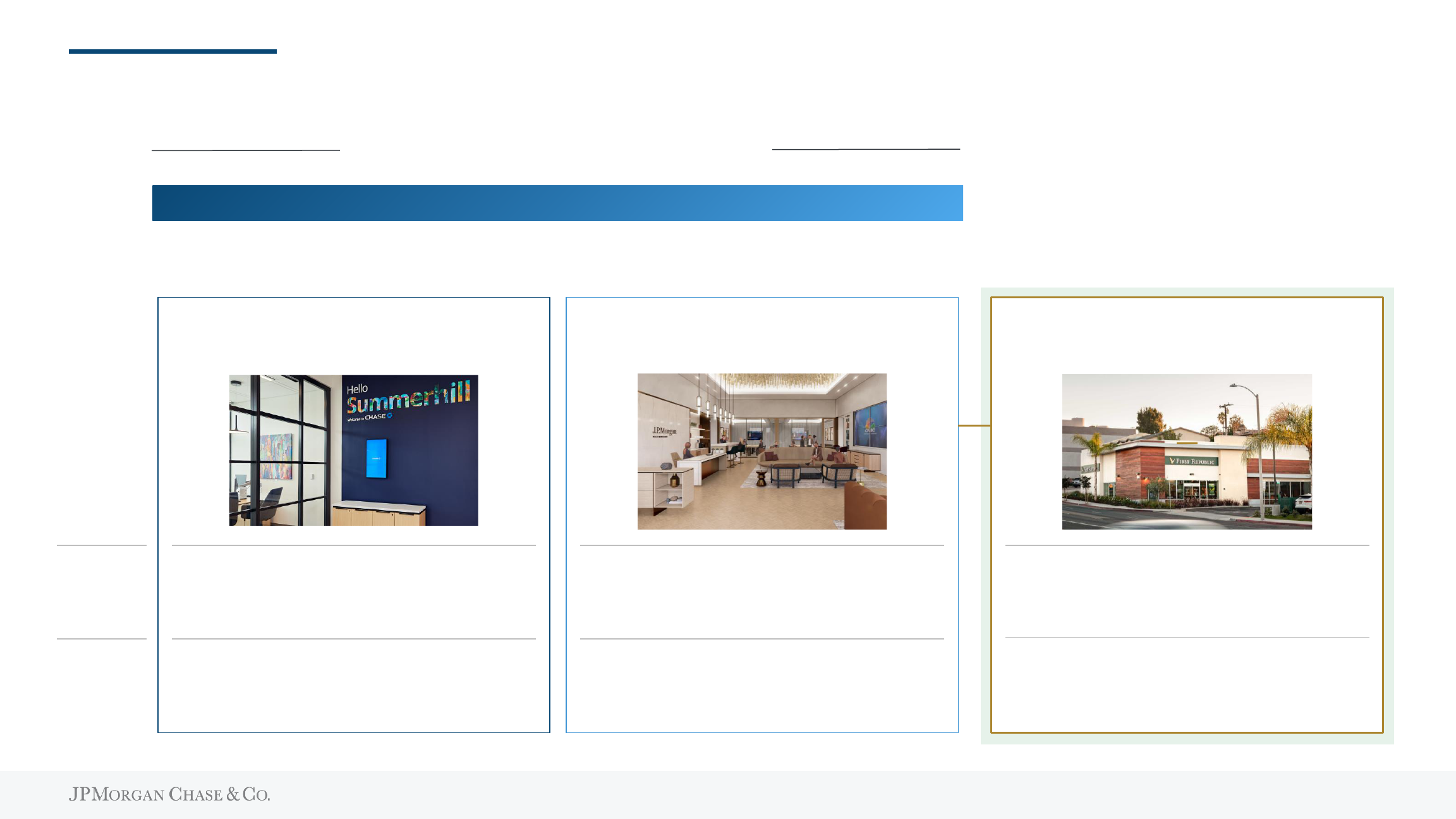

First Republic branches will support our affluent branch segmentation strategy

Formats

Emerging segments Affluent segments

Community Center

(in market)

Private Client Center

(under development)

First Republic

Preferred Banking Offices

Premium locations including SF, NYC, Boston

covering 50% of JPM WM balances

Roles

Community Centers to build trust locally and

promote financial health in underserved communities

Private Client Centers to build wealth brand and

provide exclusive spaces to engage with an

integrated team of experts

Preferred Bankers manage relationships and

provide service

Adapt proven integrated model with dedicated

Community Manager, Small Business Consultant,

and Community Home Lending Advisor roles

Deploy a senior team of experts with Private Client

Bankers & Advisors, Business Relationship

Managers, and Home Lending Advisors

Engagement

High-touch servicing model with industry-

leading experience

Tailored local objectives and engagement

methods to meet the distinct needs of underserved

communities

Serve clients across banking, lending and wealth

and curate financial planning and wealth-focused

experiences

Chase Branch Segmentation Strategy

70

71

Notes on non-GAAP financial measures

1. Adjusted expense excludes CCB legal expense and is a non-GAAP financial measure. For 2021, reported noninterest expense was $29,028 million and legal losses

were $55 million; for 2022, reported noninterest expense was $31,208 million and legal losses were $47 million. Management believes this information helps investors

understand the effect of certain items on reported results and provides an alternate presentation of the Firm’s performance

2. Income before income tax expense (pretax income) excluding the change in loan loss reserves (“pretax income ex. LLR”) and return on equity excluding the change in

loan loss reserves (“ROE ex. LLR”) are non-GAAP financial measures. These metrics reflect the exclusion of the portion of the provision for credit losses attributable

to the change in allowance for credit losses. ROE ex. LLR is calculated as net income excluding LLR divided by average common stockholders’ equity. For CCB

average common stockholders’ equity for the full years 2022, 2021 and 2020, refer to page 65 of JPMorgan Chase’s Annual Report on Form 10-K for the year ended

December 31, 2022. For all other periods presented, refer to the CCB Business Segment Results in JPMorgan Chase’s Annual Report on Form 10-K for each

respective year. The table below provides a reconciliation of reported results to these non-GAAP financial measures

Year ended December 31,

(in millions, except ROE)

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

(1) Pretax income

Reported pretax income

17,236

17,808

14,689

15,472

15,053

14,637

19,399

21,950

11,034

27,840

19,793

Adjustments:

Change in loan loss reserves

(5,506)

(5,490)

(1,253)

(1,023)

150

320

42

(299)

7,809

(9,750)

1,125

Pretax income ex. LLR

11,730

12,318

13,437

14,449

15,203

14,957

19,441

21,651

18,843

18,090

20,918

(2) Net income

Reported net income

10,522

10,715

8,840

9,546

9,418

9,254

14,744

16,575

8,268

20,957

14,916

Adjustments:

Change in loan loss reserves

(3,337)

(3,300)

(742)

(632)

93

207

32

(226)

5,843

(7,356)

879

Net income ex. LLR

7,185

7,415

8,098

8,914

9,511

9,462

14,776

16,350

14,111

13,601

15,795

(3) ROE

Reported ROE

24%

23%

17%

18%

17%

17%

28%

31%

15%

41%

29%

ROE ex. LLR

16%

15%

15%

17%

18%

18%

28%

31%

26%

26%

31%

72

Notes on slide 3

1. See slide 72

2. Federal Deposit Insurance Corporation (“FDIC”) 2022 Summary of Deposits survey per S&P Global Market Intelligence. Applies a $1B deposit cap to Chase and

industry branches. Includes all commercial banks, savings banks, and savings institutions as defined by the FDIC. Prior periods have been revised to conform to the

current period presentation

3. Based on 2022 sales volume and loans outstanding public disclosures by peers (C, BAC, COF, AXP, DFS) and JPMorgan Chase estimates. Sales volume excludes

private label and Commercial Card. Loans outstanding exclude private label, AXP Charge Card, and Citi Retail Cards

73

Notes on slide 4

1. Businesses and legal entities with decision making rights

2. Federal Deposit Insurance Corporation (“FDIC”) 2022 Summary of Deposits survey per S&P Global Market Intelligence. Applies a $1B deposit cap to Chase and

industry branches. Includes all commercial banks, savings banks, and savings institutions as defined by the FDIC. Prior periods have been revised to conform to the

current period presentation

3. Barlow Research Associates, Primary Bank Market Share Database as of 4Q22. Rolling 8-quarter average of small businesses with revenue of more than $100,000

and less than $25 million

4. Based on 2022 sales volume and loans outstanding public disclosures by peers (C, BAC, COF, AXP, DFS) and JPMorgan Chase estimates. Sales volume excludes

private label and Commercial Card. Loans outstanding exclude private label, AXP Charge Card, and Citi Retail Cards

5. Refers to customers with two or more relationships within the following sub-LOBs: Consumer Banking, Business Banking, Wealth Management, Credit Card, Home

Lending, and Auto

74

Notes on slide 5

1. #1 in active users among digital banking mobile apps based on Data.ai and #1 most-visited banking portal in the U.S. (Chase.com) based on Similarweb

2. 2022 Chase branch network coverage by state. Federal Deposit Insurance Corporation (“FDIC”) 2022 Summary of Deposits survey per S&P Global Market

Intelligence. Includes all commercial banks, savings banks and savings institutions as defined by the FDIC. Prior periods have been revised to conform to the current

period presentation. Numbers do not foot to Form 10-K as FDIC represents branch counts as of June 30th, 2022

3. As of 4Q22. Users of all web and/or mobile platforms who have logged in within the past 90 days