SECTOR REPORT

21 JUN 2018

Indian Gems & Jewellery

HDFC securities Institutional Research is also available on Bloomberg HSLB <GO>& Thomson Reuters

In the (Gold)ilocks zone

What’s VISIBLE to investors?

Durable growth, anchored to wedding demand

A huge trust deficit in unorganised retail POS

Pro-organised regulatory push, incl. demonet + GST

Tightening credit lines for jewellers

What’s LESS visible?

We visited players across the Indian jewellery value chain

in six cities to validate the ‘visible’ and to discover some of

the ‘not so visible’ moving parts. Our findings:

1. India’s jewellery story is mostly about the SUPERPACK

(17 organized jewellery chains that will grab ~42%

share in the next five years). The SUPERPACK has

significant diversity – in current operations as well as

growth strategies.

2. Battle for market share will be played in North an

d

We

st India, away from the largest market (South).

Only one SUPERPACK player is choosing to opt out.

3. Our India visit suggests jewellery may have some legs

(~6% CAGR built over FY18-23E). However, as

a

category, jewellery could so easily have an ‘alternative

history’ - may not

grow apace with demographic (and

income) tailwinds, despite the ‘anchor’ weddin

g

segment, and may even slip down the discretionary

spending ladder. For us, this is the biggest ‘invisible’

that investors must recognise.

4. Street folly: RoCEs are overstated in proforma

a

ccounts. We prefer to see gold on lease and Gold

schemes as debt!

Titan looks like the big winner right now, but ‘DEFENCE’

will be the operating word as SUPERPACK closes in.

Business gains are priced in. Initiate coverage with

NEUTRAL. Thangamayil is evolving in tandem with

regulatory tailwinds. It is poised to drive up return ratios

significantly over the next few years, flowering in its core

markets. Initiate coverage with BUY.

What’s inside?

SUPERPACK to corner 42% of the market by FY23:

India’s jewellery market has actually remained flat at

Rs 2.7tn over FY14-18 as both volume and price have

remained stable. However, the SUPERPACK is

estimated to have grown at ~11% CAGR, implying a

c

lear shift of business towards the organized trade as

the latter aggressively expanded its footprint by an

estimated 2mn sq feet. We expect the SUPERPACK to

corner ~42% of the domestic market by FY23E (vs ~29%

c

urrently) underpinned by their aggressive expansion

drive, design might and increasingly competitive

pricing vis-à-vis family jewellers.

Design to separate the men from the boys: Market

share battle will be fought with the breadth/depth of

designs as pricing premium, gold scheme offerings,

repurchase/exchange commission across the

SUPERPACK are converging. ~3/4 of the combined top-

line of key South jewellers comes from the 5 souther

n

states, where customer purchasing behavior is largely

homogenous in terms of designs. 67-100% of thei

r

stores are South-based too, implying weaker artisans

tie-ups in rest of India. Our interactions with

management of major south jewellers suggested that

t

hey are proactively fixing this gap and increasing the

ir

non-south ‘Karigar’ pool. Hence, the design arbitrage

will dwindle in the medium-term. Based on our store

visits, we reckon jewellers like Joyalukkas, Kalyan

J

ewellers and PCJ may be closer to catching up wit

h

Titan on the design curve vis-à-vis others.

Every record should

be considered in

light of the other

outcomes that could

have occurred just

as easily as the

‘visible histories’

that did.

- Nassim Nicholas Taleb,

Fooled by Randomness

Company Reco TP

Titan NEU 820

Thangamayil BUY 650

J

ay Gandhi

jay.gandhi@hdfcsec.com

+91-22-6171-7320

Rohit Harlikar

+91-22-6639-3036

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 2

North and West - the bone of contention: The

SUPERPACK accounts for a measly 4% of the BIS-listed

jewellery stores in North and West (vs ~8% stor

e

share/~40% revenue share down South). Scope for

penetration, coupled with higher profitability from

impulse purchases and studded jewellery off-take,

make North and West the bone of contention. Key

south jewellers concur that north and west is where

the battle will be fought. While Titan remains a distant

leader in terms of national presence, able contenders

are visible across all zones. These include PC Jewelle

r

(

North), Kalyan Jewellers, Malabar Gold, Joyalukkas

(South) and Senco (East). GRT (one of the biggest,

leanest and most efficiently managed organized

jewellers in India) believes there is enough scope down

South and will remain there for the next 2-3 years.

Different strokes for different folks: Most South-based

players prefer the owned store route vs. the franchise

e

r

oute for expansion (barring Malabar). While this

decision may be inconsequential, as major investments

are towards inventory (93-95%), the unencumbered

cash levels and leverage position of select big-box

jewellers warrant a capital infusion for geographical

e

xpansion. However, this advantage for Titan can

dwindle over the next couple of years as select

jewellers are either expected to hit capital markets or

a

re tying up more debt over FY18-20E.

Exchange schemes – SSSG booster: The up-selling

opportunity presented by an attractive gold exchange

scheme can help the SUPERPACK grow SSSG. ~50-70%

of their customer base are repeat customers who are

ideal candidates for exchange schemes. Titan and PCJ

account for ~5% & ~2% respectively of the total gol

d

exchange market. Across zones, big-box jewellers have

re

vised their exchange programme (more lucrative for

consumers now) to capture the up-selling opportunity.

Titan wins, but peers closing in. Given the current

design/capital arbitrage, we believe Titan will have

a

h

ead-start on the customer acquisition race over FY18-

21E. Co is confident on achieving its aspired 25%

jewellery revenue growth in FY19E. However, peer

gaps will reduce post FY21 (Phase 2 of our medium

term view) and Titan will find itself defending turf

ag

ainst very strong and able challengers across India

.

T

his may impact Titan’s long-term growth and

profitability.

Stocks :

o T

itan remains the best business, albeit it’s no

See’s Candy given the industry’s ‘put-up-more-to-

earn-more’ business model. The 2-3 year head-

start on designs and capital provides healthy

growth visibility. Expect revenue/EBITDA/PAT

CAGR of 20/25/23% over FY18-21E and

improvement in ROICs by ~200bps to ~20% (in our

restated format).

Despite baking in all plausible tailwinds in Phase 1,

current valuations keep us at bay. We have a

NEUTRAL recommendation with a DCF-based TP of

Rs 820/sh (implying 42x FY19 EPS). Our FY19/FY20

EPS estimates are 5/9% below consensus.

o Thangamayil is a classic turnaround story with

multiple levers to pull. We expect Thangamayil to

deliver a revenue/EBITDA/PAT CAGR of 18/24/31%

and economic spread (RoIC-WACC) to improve by

~490bps to 4% by FY21. Recommend a BUY with a

DCF-based TP of Rs 650/sh.

Wait, there’s more (1) Key takes from management

interactions at SUPERPACK, store visits across India, (2)

Key districts across India which could potentially be

(gold)mines for customer acquisition.

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 3

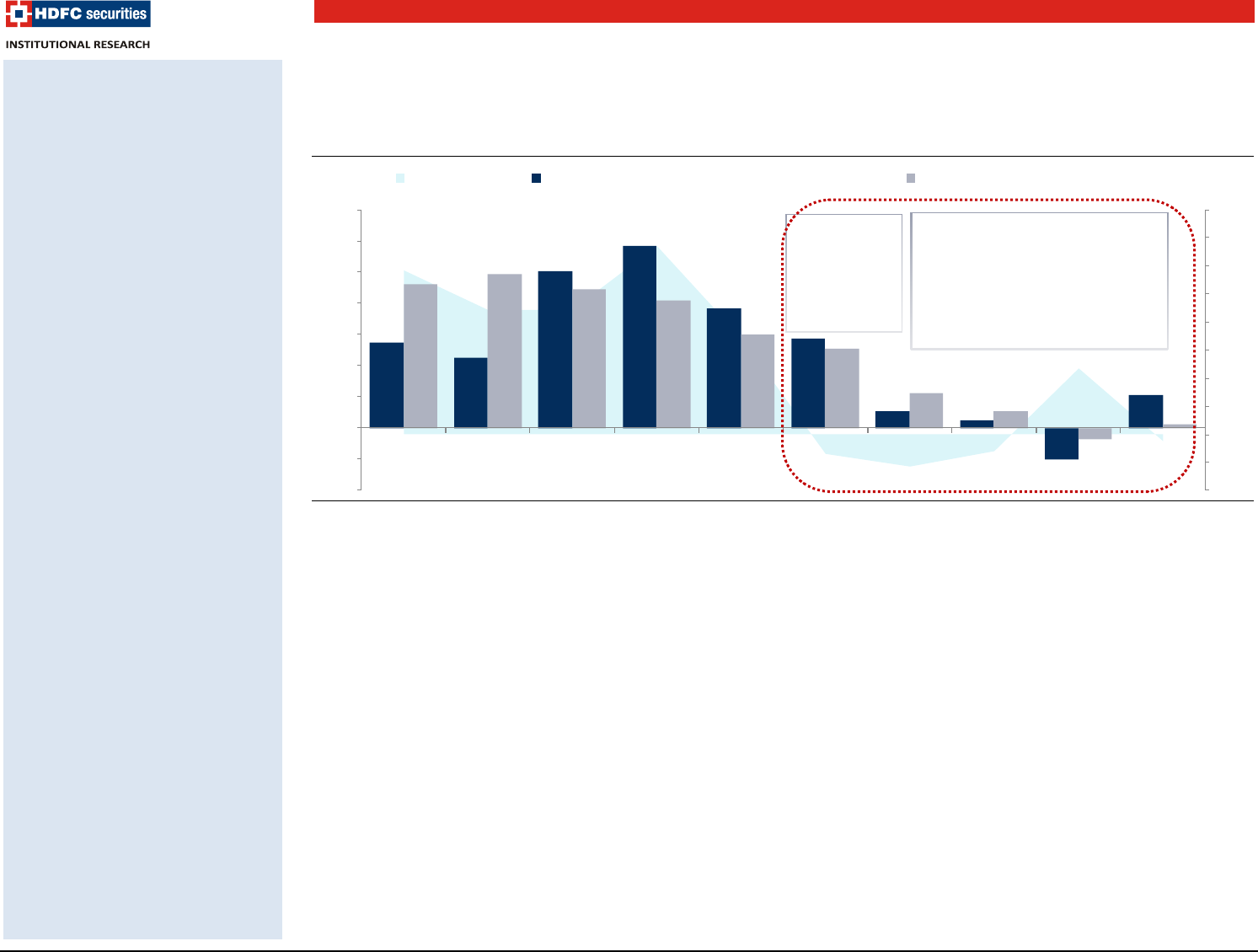

Meanwhile, some Street folly…

Key listed jewellers classify (1) Gold procured on lease from banks as Trade Payables, and (2) ‘Deposits outstanding as a

part of schemes’ under Current Liabilities. As both liabilities are interest bearing, we reclassify them as DEBT, which

knocks up capital employed significantly. Titan has recently started classifying gold loans separately, but the Street

continues to exclude them from debt. As a result, jewelers report optically high return ratios. On the other hand, our

method depicts a more genuine picture of the underlying returns profile of the business.

Titan: Proforma vs underlying RoCE

Titan: ROIC – Proforma vs underlying RoIC

PCJ: Proforma vs underlying RoCE

PCJ: Proforma vs underlying RoIC

Thangamayil: Proforma vs underlying RoCE

Thangamayil: Proforma vs underlying RoIC

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

24.3

29.5

29.4

30.4

30.7

14.2

17.8

19.3

19.7

19.8

0

20

40

FY17

FY18

FY19E

FY20E

FY21E

RoIC - Proforma (%)

Underlying RoIC (%)

16.8

16.6

19.3

22.0

22.1

10.1

9.7

10.6

11.4

11.5

4

8

12

16

20

24

FY17

FY18

FY19E

FY20E

FY21E

RoCE - Proforma (%)

Underlying RoCE (%)

18.7

21.8

23.1

24.5

26.7

10.2

10.8

11.2

11.6

12.2

4

8

12

16

20

24

28

FY17

FY18

FY19E

FY20E

FY21E

RoIC - Proforma (%)

Underlying RoIC (%)

11.5

11.6

12.3

13.8

14.3

7.8

7.6

8.2

9.1

9.5

0

4

8

12

16

FY17

FY18

FY19E

FY20E

FY21E

RoCE - Proforma

Underlying RoCE

11.9

12.3

16.2

23.9

24.8

7.9

7.9

9.4

11.9

12.4

0

7

14

21

28

FY17

FY18

FY19E

FY20E

FY21E

RoIC - Proforma

Underlying RoIC

21.5

25.1

26.2

26.6

26.8

13.5

16.4

18.1

18.3

18.3

0

10

20

30

FY17

FY18

FY19E

FY20E

FY21E

RoCE - Proforma (%)

Underlying RoCE (%)

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 4

Contents

Story in charts .................................................................................................................................................... 5

Competitive positioning of key jewellers ............................................................................................................. 9

Peer Comparison .............................................................................................................................................. 10

Waiting for ‘normal’ times ............................................................................................................................... .11

Mom & Pop jewellers: really squeezed? ............................................................................................................ 15

SUPERPACK to grow at over 12% over FY18-23E ................................................................................................... 16

Weddings : the bedrock of demand ................................................................................................................... 18

Where would jewellery be without brides! ............................................................................................................ 18

Studded jewellery remains healthy ........................................................................................................................ 19

Different strokes for different folks ................................................................................................................... 21

South market is mature, majors will tread out ...................................................................................................... 21

Own store expansion – Mantra down south .......................................................................................................... 22

Phase 1 - Advantage TITAN, Phase 2 - closely fought ............................................................................................. 22

Rising gold prices can drive franchisee throughput ............................................................................................... 24

North & West : The battlegrounds .................................................................................................................... 26

Headroom to penetrate is higher ........................................................................................................................... 26

Able challengers in the fray in North & West ......................................................................................................... 27

Design portfolio : Key factor ............................................................................................................................. 29

Prices converging across the SUPERPACK .............................................................................................................. 29

Tanishq leads on design, peers will catch up .......................................................................................................... 31

Sourcing of gold could be the joker in the pack ..................................................................................................... 31

Expert talk ........................................................................................................................................................ 33

Flagship Store visits .......................................................................................................................................... 37

KPIs : How do top jewellers stack up? ............................................................................................................... 39

Where could the expansion come from? ........................................................................................................... 42

Companies

The Titan Company – Best in class, but no See’s Candy (Initiating Coverage) ................................................ 49

Thangamayil – Turnaround story (Initiating Coverage) ................................................................................. 77

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 5

Story in charts

Indian Bride to keep jewellery demand stable; SUPERPACK accounts for a quarter in weddings

India Consumption Market: ~5% CAGR over

FY18-23E

….jewellery to grow at ~6% CAGR

India Jewellery: Growth drivers over FY18-23

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Weddings to contribute half the growth

Gold/Studded contribution

SUPERPACK’s est. wedding share

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

1.4

3.0

1.1

5.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Gold Volume

CAGR

Gold

realization

CAGR

Mix CAGR

FY18-23E

Domestic

Jewellery

CAGR

2,722

3,570

564

284

FY18 Domestic

Jewellery

Gold Jewellery

Studded

Jewellery

FY23 Domestic

Jewellery

Rs bn

7.4

7.0

-9.6

2.1

-3.3

7.1

6.3

5.7

4.4

4.4

-15.0

-10.0

-5.0

0.0

5.0

10.0

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY14E

FY15E

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

Domestic Jewellery (Rs bn)

Domestic Jewellery YoY (%) - RHS

0.3

-2.6

-10.1

2.1

-3.5

6.8

5.3

4.8

3.6

3.6

-15.0

-10.0

-5.0

0.0

5.0

10.0

0

1,000

2,000

3,000

4,000

5,000

FY14E

FY15E

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

Domestic Jewellery (Rs bn)

Bars & Coins (Rs bn)

Domestic consumption (YoY) - RHS

2,722

3,570

430

195

223

FY18

Domestic

Jewellery

Wedding

Jewellery

Casual

Special

Occasion

FY23

Domestic

Jewellery

Rs bn

Tanishq

2.0

PC Jeweller

3.6

TBZ

0.7

Thangamayil

0.3

GRT

3.3

Joyalukkas

1.9

Kalyan

2.8

Malabar

3.3

PN Gadgil &

Sons

0.5

Others

7.8

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 6

SUPERPACK to corner over 40% of the market; tanishq to double its market share

SUPERPACK’s share to touch 42% by FY23E

Tanishq to nearly double its share by FY23E

Tanishq to lead the SUPERPACK (mkt share)

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Design will be key; as offerings across the SUPERPACK converge with time

Player-wise premium over MCX

Effective interest rate on gold schemes

Old Gold Repurchase/Exchange commissions

Jeweller

Repurchase for Cash

(commission %)

Old Gold Exchange

(commission %)

Own

gold

Other

jewellers

Own

gold

Other jewellers

Titan 3% NA 0%

2%(22k) /

8%(below 22k)

PCJ 3% NA 0% 1%

TJL 3% 3% 0%

TBZ 3% NA 0% 3%

Kalyan 1% NA 0% 6%

P N Gadgil

& Sons

3% NA 0%

GRT 3% NA 0%

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

23.2

24.3

29.2

30.9

33.0

35.6

38.5

41.7

76.8

75.7

70.8

69.1

67.0

64.4

61.5

58.3

0.0

20.0

40.0

60.0

80.0

100.0

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

SUPERPACK

Unorganized

%

4.2

8.1

12.5

2.2

2.0

2.0

1.2

0.8

0.4

0.4

0.4

0.1

1.0

FY18E Tanishq's share

Unorganized …

Malabar Gold

GRT

PCJ (Dom Biz)

Joyalukkas

Kalyan

Thangamayil

Jos Alukkas

PN Gadgil

TBZ

Other organized …

FY23E Tanishq's share

%

14.2

19.5

-

2.7

1.1

0.5

0.6

0.3

0.2

0.2

0.2

0.7

9.3

FY18E Tanishq

PCJ (Dom Biz)

Malabar Gold

Joyalukkas

Thangamayil

PN Gadgil & Sons

GRT

Jos Alukkas

TBZ

Kalyan

Other organized

FY23E Tanishq

8.1

6.5

6.4

5.9

4.6

4.4

4.4

3.9

3.3

2.6

2.3

-

2.0

4.0

6.0

8.0

10.0

Titan

TBZ

Jos Alukkas

P N Gadgil & Sons

Malabar Gold

Thangamayil

GRT

PCJ

Kalyan

Joyalukkas

PNG Jewellers

Premium (%)

12.0

12.0

11.4

11.0

10.9

10.9

7.8

5.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Tanishq

Thangamayil

PC Jeweller

Malabar Gold

GRT

Kalyan

PN Gadgil & Sons

Joyalukkas

Effective Interest rate

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 7

North and West – the bone of contention as South well-entrentched with a cap on profitability

Zone wise revenue split (estimated)

SUPERPACK’s presence <4% in North/West

Top jewellers enjoy ~40% market share

down South

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Top Jewellers expansion strategies

Expansion Route

FY19 Store additions commentary

Tanishq

Mix of Owned & Franchisee

40-45

PC Jeweller Mix of Owned & Franchisee ~25

Malabar Gold

Mix of Owned & Franchisee

~30

Senco Gold Mix of Owned & Franchisee NA

Kalyan Jewellers Owned store ~20-25

Joyalukkas

Owned store

~20

GRT Owned store ~5

Thangamayil

Owned store

~5

TBZ Mix of Owned & Franchisee ~15

Source: HDFC sec Inst Research

North

21

South

40

East

15

West

26

%

2.6

11.3

5.4

3.0

9.6

1.1

2.7

3.6

1.2

0.8

1.0

1.0

1.4

0.5

0.6

0.8

-

2.0

4.0

6.0

8.0

10.0

12.0

Tanishq

GRT

Joy Allukas

Kalyan

Malabar Gold

Thangamayil

Jos Allukas

Khazana

RMS (%)

Store share (%)

74.7%

25.3%

3.7%

standalone jewellers as % of total

chains as % of total

SUPERPACK as % of total

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 8

Capital – The Achilles heel for Titan’s peers; arbitrage to dwindle over the next two-three years

Leverage : Select jewellers

FCFE : Select jewellers

Avg. cost of debt : select jewellers

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

Key vitals of top jewellers remain stable

Key vitals of top jewellers

Player wise average store size

Gold price near its six years peak

Source: Company, ROC, HDFC sec Inst Research; above

universe estimated to account for 20% RMS

Source: HDFC sec Inst Research

Source: HDFC sec Inst Research

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Titan

PCJ

Thangamayil

South

-based A

South

-

based B

South

-based C

South-based D

TBZ

PN Gadgil

Net Debt/Equity

Net Debt/EBITDA

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

-

2.0

4.0

6.0

8.0

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

5,000

Titan

PCJ

Thangamayil

South-based B

South-based C

South-based D

TBZ

PN Gadgil

FCFE (Rs mn)

FCFE yield (%) - RHS

14.6

6.0

3.5

16.5

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Gross Margin

EBIT margin

PAT margin

RoE

Top 9 Jewellers

%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

GRT

Kalyan

Malabar Gold

PC Jeweller

Tanishq

PN Gadgil & Sons

Joyalukkas

TBZ

Thangamayil

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

TBZ

South-based E

South-based C

PN Gadgil

PCJ

Thangamayil

South-based B

South-based D

South-based A

Tanishq

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Gold price (Rs/10 gm)

Avg price

+1 Std dev

-1 Std dev

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 9

Competitive positioning of key jewellers

GRT Joyalukkas Kalyan Malabar Gold PN Gadgil

PCJ (Dom

Biz)

Tanishq TBZ Thangamayil

Design Portfolio

Tonnage

Expansion strategy

Margins

Working capital efficiency

Balance Sheet strength

Return Profile

Presence

Gold sourcing strategy

Wedding share

Geographic reveunue split South - 100%

South - 90%

ROI - 10%

South - 45%

ROI - 55%

South - 90%

ROI - 10%

West - ~98%

South - ~2%

NA South - 100%

Geographic Store split South - 100%

South - 80%

North - 10%

West - 10%

East - Nil

South - 67%

North - 15%

West - 13%

East - 5%

South - 87%

North - 5%

West - 7%

East - 1%

West - 96%

South - 4%

South - 4%

North - 70%

West - 14%

East - 12%

South - 28%

North - 31%

West - 25%

East - 17%

South - 11%

North - 3%

West - 70%

East - 16%

South - 100%

No. of stores (#) 46 78 90 99 25 93 253 37 32

Weakness

Strength

Source: Company, HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 10

Waiting for ‘normal’ times…

Peer Comparison : Premium to global peers justified given the growth and return profile

Company

Market

Cap

(USD

mn)

Revenue (USD mn)

Revenue

CAGR

(FY18 -

FY21E)

EBITDA (USD mn)

EBITDA

CAGR

(FY18 -

FY21E)

PAT (USD mn)

PAT

CAGR

(FY18

-

FY21E)

P/E

ROE (%)

FY19E

FY20E FY21E

FY19E FY20E

FY21E

FY19E FY20E FY21E

FY19E

FY20E FY21E

FY19E FY20E

FY21E

India

Titan

11,711

2,919

3,477

4,118

20.2%

311

385

468

24.6%

208

253

303

22.6%

56.3

46.3

38.6

25.2

25.7

25.9

PCJ

778

1,668

1,951

2,297

17.6%

173

205

250

20.5%

115

134

163

27.3%

7.3

6.2

5.1

19.3

19.7

19.7

Thangamayil

94

243

286

334

18.1%

11

14

17

23.8%

4

6

7

30.7%

21.6

15.3

12.2

16.0

19.5

20.9

TBZ

90

275

301

330

8.7%

12

14

16

12.8%

4

4

6

21.2%

24.3

21.1

16.7

5.3

5.9

7.1

Global

Tiffany

16,601

4,524

4,746

4,998

6.2%

1,066

1,147

1,233

7.2%

583

645

707

11.0%

28.5

25.8

23.5

17.7

19.9

18.4

LUK Fook

Holdings

2,742 1,984

2,119

7.9%

232 255

11.4% 172 189

12.0%

15.9

14.5

13.9 14.2

Signet Jewellers

2,579

6,022

5,896

5,701

-3.0%

512

501

549

-9.1%

232

209

258

-15.1%

11.1

12.3

10.0

9.7

6.1

12.3

Chow Tai Fook

Jeweller

12,548 7,864

8,469

13.2%

987 1,105

15.4% 626 706

15.5%

20.1

17.8

14.9 15.8

Source: Company, Bloomberg estimates, HDFC sec Inst Research

Jewellery -Valuation Table

Company CMP

Mcap

(Rs bn)

Reco TP

EPS

P/E (x)

RoE (%)

RoIC (%)

RoCE (%)

FY19E

FY20E

FY21E

FY19E

FY20E

FY21E

FY19E

FY20E

FY21E

FY19E

FY20E

FY21E

FY19E

FY20E

FY21E

Titan 897 804 NEU 820 15.9

19.4

23.2

56.3

46.3

38.6

25.2

25.7

25.9

19.3

19.7

19.8

18.1

18.3

18.3

PC Jeweller 136 58 NR NA 20.4

23.9

28.9

7.3

6.2

5.1

19.3

19.7

19.7

11.2

11.6

12.2

10.6

11.4

11.5

Thangamayil 483 7 BUY 650 21.0

29.6

37.1

21.6

15.3

12.2

16.0

19.5

20.9

9.4

11.9

12.4

8.2

9.1

9.5

Source: Company, HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 11

Waiting for ‘normal’ times

Industry could use some normal, post the FY14-18 drama

Source: Bloomberg, HDFC sec Inst Research

Industry dynamics have oscillated from being

favorable to unorganized jewellers (FY13-15) to being

favorable for organized jewellers (FY15-till date),

given the spate of regulatory events. The recent

defaults by well-known jewellers (Nirav Modi and

Geetanjali) haven’t helped the industry’s image

amongst lenders, either. With the 5-year drama

behind, the Indian Jewellery industry could use

some ‘normal’.

Multiple unfavorable regulations such as the ban on

gold on lease (Jul-13) and imposition of the 80:20

import rule (Aug-13) had severely impacted the

financial health of organized jewellers as working

capital needs (and consequently debt) increased.

Jewellers had to purchase raw material (gold)

upfront. This bloated up the capital employed and

put the returns profile of jewellers under pressure.

The capping of Gold deposit schemes to 25% of

networth and the interest that can be paid on such

schemes (Apr-14) further added to the woes of

organized jewellers.

Second phase of regulations has decisively been in

favor of organized jewellers – 1. 80:20 import rule

revoked (Nov-14), 2. Ban of Gold on lease was

revoked (Feb-15), 3. The cap on Gold deposit

schemes also have been revised upwards to 35% of

networth (FY17). Mandatory hallmarking (to be

implemented soon) too is expected to aid the

unorganised to organised shift.

14

11

25

29

19

14

3

1

(5)

5

23

25

22

21

15

13

6

3

(2)

1

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

(10)

(5)

-

5

10

15

20

25

30

35

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Gold price growth

YoY growth in bank credit O/S to Gems & Jewellery sector (%)

YoY growth in bank credit to Other Industries (%)

-FY14: 80-20

import rule

-FY14: Gold on

lease ban

-FY14: Restrictions

-FY14: Gold on lease ban lifted

-FY15: 80-20 import rule revoked

-FY16: PAN-card mandatory on

transctions >2 lacs

FY16: -1% excise duty levy on mfg

FY17 - Demonetization

FY18 - GST implemetation

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 12

A road fraught with frauds

Year Scams Description

FY18

Nirav Modi - Mehul Choksi PNB

fraud (Feb 2018)

Nirav Modi and Mehul Choksi acquired fraudulent letters of undertaking from PNB

for overseas credit from other Indian lenders, defrauding a bank of more than Rs

113 bn.

FY18

Nathella Sampath jewellery fraud

(Mar 2018)

Promoters and directors of Chennai-based Nathella Sampath Jewelry Pvt Ltd

(NSJPL) defrauded three banks namely SBI, Union Bank and HDFC Bank of Rs 3.8 bn.

Nathella Sampath Jewelry misrepresented financial statements from 2010 and

liquidated the primary asset kept as security/collateral.

FY18 Kanishk Gold scam (Mar 2018)

Kanishk Gold Pvt Ltd (KGPL) allegedly falsified records and financial statements to

get loans from the banks over a 10 year period beginning 2008, defrauding a

consortium of 14 banks led by the SBI to the tune of Rs 8.25 bn

FY17

Shree Ganesh Jewellery house

(2017)

Shree Ganesh Jewellery House cheated a consortium of 25 banks, including 20

nationalised ones, of over Rs 22 bn. It was alleged that the accused had defrauded

the banks through diversion of funds, fraudulent exports to shell companies in

Hong Kong, Singapore and the UAE.

FY13

Winsome Diamonds and Jewellery

(2013)

Winsome diamonds group defrauded consortium of banks of more than Rs 65 bn.

Hasmukh Shah, an ex-director and authorised signatory of Winsome Diamonds

group was allegedly orchestrating the export-import operations of the company

and was also allegedly liasoning with the banks.

Source: Industry, HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 13

Domestic Jewellery to grow at 6% CAGR (FY18-23E)

5-year drivers for domestic jewellery industry

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

Jewellery volumes to mean revert

Gold prices at 6-year peak

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

Our Industry model pegs the

domestic gems & jewellery

consumption at Rs 3.2tn, of

which the domestic jewellery

market is estimated at Rs

2.7tn (est to have grown at

~6.5% CAGR over FY11-18

largely driven by pricing/mix)

Domestic jewellery pegged to

grow at a similar rate (~6%)

over FY18-23. Gold volume

expected to remain stable

(1.5% CAGR) as unorganized

jewellers increasingly get

marginalized courtesy the

governments push to

formalize the sector.

Gold prices are near its 6-year

peak.

No expert on gold prices,

however, when brent crude

inches up; gold prices follow

suit. Expect gold prices to

remain elevated given the

deteriorating macros.

600

625

650

675

700

725

750

775

FY14E

FY15E

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

Jewellery Volume ex-smuggling (tonnes)

+1 Std Dev

-1 Std Dev

Avg

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Gold price (INR/10 gm)

Avg price

+1 Std dev

-1 Std dev

7.4

7.0

-9.6

2.1

-3.3

7.1

6.3

5.7

4.4

4.4

-15.0

-10.0

-5.0

0.0

5.0

10.0

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY14E

FY15E

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

Domestic Jewellery (Rs bn)

Domestic Jewellery YoY (%)

- RHS

1.4

3.0

1.1

5.6

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Gold Volume

CAGR

Gold

realization

CAGR

Mix CAGR

FY18-23E

Domestic

Jewellery

CAGR

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 14

Gold prices – A high correlation with Brent Crude

Gold imports (USD bn) vs Brent Crude

Source: Bloomberg, HDFC sec Inst Research

Source: Bloomberg, HDFC sec Inst Research

30

50

70

90

110

130

800

1,000

1,200

1,400

1,600

1,800

2QFY10

4QFY10

2QFY11

4QFY11

2QFY12

4QFY12

2QFY13

4QFY13

2QFY14

4QFY14

2QFY15

4QFY15

2QFY16

4QFY16

2QFY17

4QFY17

2QFY18

4QFY18

LBMA Avg gold price ($/oz)

Brent Crude (USD) - RHS

0

5

10

15

20

25

30

35

0

20

40

60

80

100

120

140

2QFY10

4QFY10

2QFY11

4QFY11

2QFY12

4QFY12

2QFY13

4QFY13

2QFY14

4QFY14

2QFY15

4QFY15

2QFY16

4QFY16

2QFY17

4QFY17

2QFY18

4QFY18

Brent Crude (USD) - LHS

CAD (USD bn)

Gold Imports (USD bn)

No expert on gold prices,

however, when brent crude

inches up; gold prices follow

suit. Expect gold prices to

remain elevated given the

deteriorating macros.

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 15

Mom & Pop jewellers: really squeezed?

Beyond demonetisation and GST...

Myth vs reality: It is assumed that GST will inevitably

lead to massive and quick business migration. While

this may be true for many sectors, it may hold less

relevance in jewellery. What matters more is (1) How

long is the supply chain? (2) Does GST really hit

margins and business processes of unorganized

jewellers?

Shorter B2C supply chain helps unorganized play:

The shorter the B2C supply chain the easier it is to

keep the entire transaction outside the organized

trade (as long as gold sourcing is guaranteed through

unofficial channels). The B2C supply chain in jewellery

is relatively short with two (or at most three) levels

(manufacturers who sell jewellery to wholesalers or

retailers) ahead of consumers.

The unorganized sector continues to source gold via

illegal channels. These include smuggling and

exchange/recycling. The ex-SUPERPACK exchange +

smuggling market is ~250-300 tonnes p.a. Multiple

retail invoicing, fake invoicing and other methods are

employed to skip the organized route to business.

Cash is the medium of exchange, obviously.

A part of official imports also find its way into the

informal chain through ‘Bill-to-ship’ mechanism

wherein the delivery of gold happens to one

individual and the transaction is billed to another.

There are two ways to do this: (1) Paper Exports:

exports shown on paper but physical gold enters the

unorganized channel, and (2) Multiple retail

invoicing: to circumvent the PAN card requirement

for transactions > Rs 200k, small jewellers prepare

multiple retail invoices. Our walks through Karolbagh

(Delhi) and Jhaveri Bazaar (Mumbai) gave us enough

evidence of these malpractices!

Easy to manage input-output ratio for Diamonds:

The input-output ratio in converting rough diamonds

into polished ones varies as much as 30-60% of the

input. Also, diamond pricing remains fuzzy, unlike

gold where purity (and hence price) is easy to

establish. This gives diamond polishers and jewellery

makers an opportunity to officially show low output

and sell the rest through the informal chain.

Hence, while the events (GST and demonetisation)

were enablers and may aid in the unorganized to

organized shift in jewellery, the pace of shift may be

more secular.

Domestic gold sourcing routes

Source: HDFC sec Inst Research

Gold Value

Chain

Imports through

formal Channel

Official Trade

Informal trade

using "Bill to

ship to"

Fake exports

Multiple Fake

retail invoices

Smuggling Recycling

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 16

Hallmarking squeezing mom-and-pop jewellers: Our

interactions across jewellery chains and mom-and-

pop jewellers across India suggests that while

hallmarking is yet not mandatory, consumers are

increasingly insisting on hallmarked jewellery. This

has increased the cost of procurement for jewellers

and the ~25-30% pricing arbitrage between jewellery

chains and standalone jewellers is shrinking. A back-

of-the-envelope calculation in the table below gives a

perspective of how the mom-and-pop jeweller is

getting squeezed due to hallmarking.

Back-of-the envelope calculation suggests mom-

and-pop jeweller getting squeezed

Transaction

Without

Hallmarking

Premium

halved

With

Hallmarking

Premium

maintained

With

Hallmarking

Gold Price (Rs/g)

3,100

3,100

3,100

Karat

21.0

22.0

22.0

Purity (%)

87

92

92

Cost-based on

purity (Rs/g)

2,711 2,840 2,840

Pricing Premium

(%)

6 3 6

Board rate for

consumer (Rs/g)

2,873 2,925 3,010

Making Charges

(Rs/g)

150 195 195

Making charges (%)

5.2

6.7

6.5

Retail Price (Rs/g)

3,023

3,120

3,205

Gross Profit (Rs/g)

313

280

365

Gross Margin (%)

10.3

9.0

11.4

Organized Jeweller

Gross margin in

north/west (%)

13-15

Organized Jeweller

Gross margin in

South (%)

8-10

Source: HDFC sec Inst Research

Indian households are getting nuclear: One of the

major shifts underway is that the avg Indian

household is increasingly getting nuclear with

urbanisation, esp. towards tier 1 cities. This remains a

strong catalyst for the shift from family jewellers to

organized chains.

Family Type Distribution – All HHs (%)

IRS 2013

BI 2016

Joint Family

26

22

Nuclear Family with Elders

17

17

Nuclear Family w/o Elders

53

58

Living Alone

4

3

Source: BARC, HDFC sec Inst Research

SUPERPACK to grow at over 12% over FY18-23E:

Given some of the above tailwinds for the organized

jewellers coupled with the design spread they offer,

we expect our SUPERPACK (comprising 17 Top

Jewellers) to grow at over 12% CAGR over FY18-23E.

(est. ~11% CAGR over FY16-18E). They will gain avg

~250bps/year in market share over FY18-23E to hit

~42% (vs ~29% currently)

SUPERPACK’s share to touch 42% by FY23E

Source: BARC, HDFC sec Inst Research

Note: We don’t have a categorical definition of unorganized jewellers

and focus only on how the SUPERPACK performance is expected to

pan out.

23.2

24.3

29.2

30.9

33.0

35.6

38.5

41.7

76.8

75.7

70.8

69.1

67.0

64.4

61.5

58.3

0.0

20.0

40.0

60.0

80.0

100.0

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

Organized

Unorganized

%

Nuclear families on the rise.

This coupled with migration

to tier 1 cities is a strong

catalyst for share gain from

family jewellers.

SUPERPACK to clock 12%

revenue CAGR over FY18-23E

and corner 42% of the

domestic consumption by

FY23

Top 6 jewellers to nearly

corner one-third the market

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 17

Top 6 to corner one-third the market: The top 6

jewellers in India account for 4-5% of the BIS-listed

stores and command ~20% revenue market share

(RMS). Given their ambitious expansion over the next

5 years, RMS-to-store ratio is expected to expand

further. We expect them to account for nearly one-

third of the domestic consumption (Jewellery +

Investment) in India by FY23E.

Gold jewellery is the big chunk of spend: Falling

diamond prices will underpin this trend. We expect

nearly two-thirds of the growth over FY18-23E to

come from plain gold jewellery sales.

…of which the top 6 will have ~1/3 mktshare

Gold/Studded contribution to industry growth

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

Player-wise ad spends (% of sales)

Celebrity endorsements

Jeweller Brand ambassador

Tanishq (Titan) Deepika Padukone

PC Jeweller Akshay Kumar, Twinkle Khanna

TBZ Vaani Kapoor

Kalyan Katrina Kaif, Amitabh Bachchan

PN Gadgil Jewellers Salman Khan

Malabar Gold Manushi Chhillar

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

Launch of new stores in new

regions will keep marketing

investment elevated as top

jewellers focus on brand

building. This however could

be a strong footfall pulling

tool.

0.0

1.0

2.0

3.0

4.0

5.0

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Titan

PC Jeweller

Thangamayil

TBZ

2,722

3,570

564

284

FY18 Domestic

Jewellery

Gold Jewellery

Studded

Jewellery

FY23 Domestic

Jewellery

Rs bn

19.8

32.1

0.3

12.5

FY18E Top 6

jewellers

other

organized

unorganized

FY23E Top 6

jewellers

%

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 18

Weddings : the bedrock of demand

Where would jewellery be without brides! Weddings

remain the bedrock for gold jewellery demand in

India. With an estimated ~8-10mn weddings in India

and an average ticket size of ~Rs 200k, the wedding

market itself is pegged at over Rs ~1.6tn (~58% of

domestic jewellery sales). The age-old concept of

‘Streedhan’ (property/assets given to the bride for

security at the time of her wedding) remains deep-

rooted in India and consequently lends inelasticity to

demand from this segment. We expect the wedding

segment to add over half the incremental industry

growth. As is well known, this is a weak spot for Titan.

However, Titan is putting its best foot forward to

correct this.

Wedding to add over half of incremental growth

Est. wedding share of key jewellers

Source: HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

2,722

3,570

430

195

223

FY18

Domestic

Jewellery

Wedding

Jewellery

Casual

Special

Occasion

FY23

Domestic

Jewellery

Rs bn

Tanishq

2.0

PC Jeweller

3.6

TBZ

0.7

Thangamayil

0.3

GRT

3.3

Joyalukkas

1.9

Kalyan

2.8

Malabar

3.3

PN Gadgil &

Sons

0.5

Others

7.8

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 19

Studded jewellery remains healthy: We believe the

~Rs 40bn studded jewellery market (est. 9-10% CAGR

over FY13-18) is expected to remain healthy as the

SUPERPACK push studded jewellery through an

aggressive sales push, including attractive return

policies. While urban centres (especially in the north

& west) will boost studded jewellery off-take, the

predisposition towards purchasing plain gold

jewellery remains strong in heartland India. Hence

blow-out growth in the studded category is unlikely.

We assume a generous 11% CAGR in aggregate

studded revenues over FY18-23E.

…but falling diamond prices pose risk : Diamond

prices have halved since peaking in Sep-11. This was

largely a function of supply outstripping demand. The

midstream in the value chain ended up with

excessive inventory pile up during the period, which

led to De Beers – the world’s largest diamond miner

recalibrating its production and prices.

Prices have stabilized since FY17. While the motive a

studded jewellery purchase is typically driven by

gifting (thereby insulating it somewhat from diamond

price movement), the category competes with other

hi-ticket consumer discretionary spends such as

automobiles, gadgets, travel, home-décor, etc.

India: Estimated studded ratio trends

…Key jewellers’ studded ratio:

Tanishq 30

PC Jeweller 30

TBZ 23

Joyalukkas 20-22

Kalyan Jewellers 18-20

Malabar Gold 9-12

GRT 3-4

PN Gadgil & Sons 3.2

Thangamayil 0.4

Source: HDFC sec Inst Research

Source: Company, RoC, DRHP, HDFC sec Inst Research

Studded jewellery expected to

grow at 11% CAGR over FY18-

23E as SUPERPACK pushes

through aggressive diamond

activation programmes

Studded jewellery

increasingly competes with

other indulgent

discretionaries. This coupled

with perception of falling

diamond prices may keep the

Indian from loosening her

purse strings in a meaningful

way. We do not factor this

risk yet

-

5.0

10.0

15.0

20.0

25.0

-

200.0

400.0

600.0

800.0

FY16E

FY17E

FY18E

FY19E

FY20E

FY21E

FY22E

FY23E

Studded Jewellery (Rs bn) - LHS

YoY

Studded ratio (%)

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 20

Diamond Prices (USD/carat) for VVS1 diamonds

Diamond Prices (USD/carat) for IF diamonds

Source: Bloomberg, HDFC sec Inst Research

Source: Bloomberg, HDFC sec Inst Research

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

Sep-15

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Diamond 1 Carat D VVS1 ($)

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Sep-13

Mar-14

Sep-14

Mar-15

Sep-15

Mar-16

Sep-16

Mar-17

Sep-17

Mar-18

Diamond 1 Carat D IF ($)

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 21

Different strokes for different folks

South market is mature, majors will tread out

As part of our pan-India jewellery tour, we met

unlisted jewellery chains and visited their flagship

stores to gauge the competitive landscape, growth

strategies and spot winners.

Our findings : (1) Most south-based national/regional

chains concur that incremental market share will be

earned through expansion into the North and West

regions, (2) Most South players prefer the owned store

model vs. the franchisee model. Also pace of expansion

may be slower vs. Titan for a couple of years given

capital constraints, (3) Given the predominantly South-

based footprint of key peers, Tanishq’s national design

width will give it an advantage for now. But it is not a

durable hurdle and will dwindle over time.

South well-entrenched, profitability capped: The

four (now five) southern states in India account for

~41% of the domestic consumption (est Rs 1.25tn)

and ~27% of the BIS-listed stores. Consumer

purchasing behavior gravitates towards traditional

plain gold jewellery where margins are low. Major

jewellers’ EBITDA margins hover in the 4-6% range.

Key players (Tanishq, Malabar Gold, GRT, Joyalukkas,

Kalyan, Jos Alukkas, Khazana, Thangamayil) are well-

entrenched and are estimated to account for ~45-

47% of the South market (in spite of ~10% share in

store count). Given the higher penetration and lower

profitability in South India, most major South-based

jewellers concur that incremental market share gain

will be through expansion in the north and west.

Zone-wise BIS-listed stores

SOUTH: Chains vs Standalone

…top jewellers enjoy ~40% market

share down South

Source: BIS, HDFC sec Inst Research (Note: BIS-listed 21,778 stores used as sample to extrapolate industry behavior and performance)

West

31%

South

27%

East

25%

North

17%

No. of

standalone

stores

75%

Regional/

national

chain

stores

25%

2.6

11.3

5.4

3.0

9.6

1.1

2.7

3.6

1.2

0.8

1.0

1.0

1.4

0.5

0.6

0.8

-

2.0

4.0

6.0

8.0

10.0

12.0

Tanishq

GRT

Joy Allukas

Kalyan

Malabar Gold

Thangamayil

Jos Allukas

Khazana

RMS (%)

Store share (%)

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 22

Own store expansion – Mantra down south: Most

South-based jewellers with national ambition intend

to expand through own stores in the North and West.

While there is little advantage in capital by opting for

the franchisee model (over 95% of investment is

towards inventory), we reckon the decision to go the

owned store way is driven by (1) Most jewellers are

yet to travel Tanishq’s learning curve in franchisee

management, (2) Potential franchisees in the rest of

India may also have limited appetite for tying up with

South based chains as they foray into the North or

West.

We believe key challengers will be better prepared

after the next 2-3 years to push the franchisee

throttle as the current capital and design arbitrage

shrinks. There are exceptions, of course. For example,

Malabar Gold intends to expand via the franchisee

route. PCJ which already has a strong foothold in the

north zone is expected to increasingly focus on

pushing throughput via franchisees in the West.

Note Risks pertaining to franchisee model are: (1) Franchisee

Capital erosion if gold prices decline, as most franchisees

don’t enjoy gold on lease arrangement with banks, (2)

Inventory management and design availability at franchisee

stores, and (3) Standardization of customer experience

Top jewellers : Expansion strategies

Top Jewellers expansion strategies Expansion Route FY19 Store additions commentary

Tanishq Mix of Owned & Franchisee 40-45

PC Jeweller Mix of Owned & Franchisee ~25

Malabar Gold

Mix of Owned & Franchisee

~30

Senco Gold Mix of Owned & Franchisee NA

Kalyan Jewellers

Owned store

~20-25

Joyalukkas Owned store ~20

GRT Owned store ~5

Thangamayil

Owned store

~5

TBZ Mix of Owned & Franchisee ~15

Source: Company, HDFC sec Inst Research

Phase 1 - Advantage TITAN, Phase 2 - closely fought:

Our interactions with lenders also suggest that

unencumbered cash levels and leverage warrant a

capital infusion for some of the unlisted big-box

jewellers, if they have to make any meaningful

investments in the north and west (given their owned

store expansion route. Given that credit flow will be

cautious, Phase 1 (FY19-21E) will see levered

jewellers either raising money through capital

markets or will sit on the fence as less levered

companies gain market share. This is expected to give

Titan a 1-2 year head-start. This is also evident in

Titan’s confidence of achieving its 25% jewellery

revenue growth aspiration for FY19. However, this

capital arbitrage along with the design arbitrage will

narrow down over the medium term. Tanishq will

find itself defending turf against some strong and

able challengers across India, especially those with a

wider national footprint.

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 23

Expected IPOs in the next 1-3 years

Kalyan Jewellers

South

Senco

East

Joyalukkas

South

PN Gadgil & Sons

West

Source: Company, HDFC sec Inst Research

Titan: Leaner vs peers

Player-wise FCFE profile

Source: Company, RoC, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research, FY17 RoC for unlisted data

Player-wise estimated avg cost of funds (%)

Est. rev share amongst top 8 jewellers down South

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

TBZ

South-based E

South-based C

PN Gadgil

PCJ

Thangamayil

South-based B

South-based D

South-based A

Tanishq

Tanishq

2.6

GRT

11.3

Joyalukkas

13.7

Kalyan

3.0

Malabar

Gold

9.6

Thangamayil

1.1

Jos Alukkas

7.0

Khazana

3.6

-

2.0

4.0

6.0

8.0

10.0

Titan

PCJ

Thangamayil

South

-based A

South

-based B

South-based C

South-based D

TBZ

PN Gadgil

Net Debt/Equity

Net Debt/EBITDA

(10.0)

(5.0)

-

5.0

10.0

(4,000)

(3,000)

(2,000)

(1,000)

-

1,000

2,000

3,000

4,000

5,000

Titan

PCJ

Thangamayil

South-based B

South-based C

South-based D

TBZ

PN Gadgil

FCFE (Rs mn)

FCFE yield (%) - RHS

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 24

Rising gold prices can drive franchisee throughput:

Not all franchisees of top jewellers employ the gold

on lease method of sourcing gold (a natural hedge).

Hence, their throughput and store inventory depends

to some extent on their open position on gold. With

deteriorating macros, we believe India has entered a

stable-to-rising gold price environment. This makes it

conducive for stoking up franchisee throughput.

About a third of Titan’s jewellery revenue comes

from its L3 channel (FOFO stores) which could see a

pick-up in throughput. PCJ and Malabar Gold have

kicked off franchisee operations with some

franchisees procuring gold on lease from banks,

thereby hedging their inventory.

MCX Gold price trends (Rs/10g)

Tanishq: Owned vs Franchisee stores (%)

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

L1 + L2

67

L3

33

5,000

15,000

25,000

35,000

Mar-06

Mar-07

Mar-08

Mar-09

Mar-10

Mar-11

Mar-12

Mar-13

Mar-14

Mar-15

Mar-16

Mar-17

Mar-18

Gold price (Rs/10 gm)

Avg price

+1 Std dev

-1 Std dev

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 25

Owned stores vs Franchisee store economics : a rough cut view

Particulars

Owned Stores

Franchisee Stores

Area (Sq ft) 3,500

2,000

Studded Ratio (%) 25

20

Revenue per sq ft 140,000

80,000

Revenue per store (Rs mn)

490

160

Gold Jewellery rev/store 368

128

Studded Jewellery rev/store 123

32

Franchisee margin (%) @ 50% of GM 0

7.5

Attributable Company revenue/store (Rs mn) 490

148

EBIT margin (%)

10

10

Attributable Company EBIT/store (Rs mn) 49

15

Capex per sq ft 4500

0

Capex per store (Rs mn) 15.75

0

Est. WC cycle (Days) 145

60

Working capital requirement

195

26

Total Investment (Rs mn) 210

26

RoCE (%) 23.3

56.3

Company, HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 26

North & West : The battlegrounds

The SUPERPACK accounts for under 4% of the stores in

North and West (over 45% of domestic consumption)

Headroom to penetrate is higher : The SUPERPACK

accounts for a measly 3.5% of the BIS-listed jewellery

stores in North and West (vs ~8% in South). Some of

the key jewellers in the North are Tanishq, PCJ,

Kalyan, Senco. In the West it is Tanishq, TBZ, PN

Gadgil & Sons, PNG Jewellers and Waman Hari Pethe.

SUPERPACK occupy 4% outlet share in North

…even lower at 3% in West Zone

Source: BIS, Company, HDFC sec Inst Research

Source: BIS, Company, HDFC sec Inst Research

State-wise BIS listed jewellery stores in India: surprisingly low nos. in some Southern states

Source: BIS, HDFC sec Inst Research

83.6%

16.4%

4.8%

standalone jewellers as % of total

chains as % of total

SUPERPACK as % of total

69.7%

30.3%

3.1%

standalone jewellers as % of total

chains as % of total

SUPERPACK as % of total

15

719

435

580

61

355

6

10

632

73

2,024

568

179

254

118

864

2,057

429

3,871

5

2

1,132

85

445

809

1,726

439

53

670

131

3,031

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Andaman

Andhra Pradesh

Assam

Bihar

Chandigarh

Chhatisgarh

Dadra and Nagar …

Daman

Delhi

Goa

Gujarat

Haryana

Himachal Pradesh

Jharkhand

JK

Karnataka

Kerala

Madhya Pradesh

Maharashtra

Meghalaya

Nagaland

Orissa

Pondichery

Punjab

Rajasthan

Tamil Nadu

Telangana

Tripura

Uttar Pradesh

Uttarakhand

West Bengal

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 27

Impulse purchases + higher studded = higher profits

in North & West: Consumers in the North & West

region of India are more receptive to studded

jewellery and impulse-led lighter-weight jewellery

purchases (14k, 18k jewellery) viz-a-vis their southern

counterparts. Plain gold jewellery typically enjoys

gross margins ranging from 10-14%, while diamond-

studded jewellery has gross margins of 30-35%.

Consequently as studded ratio (studded

jewellery/total revenue) goes up, profitability

improves.

Retail sales by jewellery type

Category

% of retail

sales

Range of weights

(gm)

Avg. ticket

weight (gm)

Necklaces 15%-20%

25-250

30-60

Bangles 30%-40%

8-25

10-15

Chains 30%-40%

10-50

10-20

Earrings 5%-15%

2-30

3-8

Finger rings 5%-15%

2-15

3-7

Source: WGC, HDFC sec Inst Research

Regional tastes in gold jewellery

South

East

West

North

Market

share

40%

15%

25%

20%

Caratage 22k

22k

22k, 18k,

14k

23k, 22k,

18k, 14k

Important

centres

Chennai,

Hyderabad,

Cochin,

Bangalore

Kolkata

Mumbai,

Ahmedabad

New Delhi,

Jaipur

Source: WGC, HDFC sec Inst Research

Able challengers in the fray in North & West: While

Tanishq remains a distant leader in terms of

presence, it has able challengers in PC Jeweller

(North), Kalyan, Joyalukkas (South) and Senco (East)

given their leading positions vs. other regional

players. This does imply relatively better tie-ups with

‘karigars’. They may thus be closer to catching up

with Tanishq on the design curve vs. other regional

jewellers.

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 28

PCJ, Kalyan & TBZ have better width in presence amongst regional jewellers; South players to play catch up

Jewellers Origin North

East

West

South

Store share in

region of origin

Store share in

region of

non-origin

Presence

(No of

States/UTs)

Presence

(No of

Districts)

Tanishq

National

78

46

59

71

NA

NA

26

156

PCJ

North

65

14

10

4

69.9

30.1

20

77

Kalyan

South

13

4

11

58

67.4

32.6

16

71

Joyalukkas

South

5

0

7

59

83.1

16.9

12

58

Malabar Gold

South

5

1

7

86

86.9

13.1

11

64

GRT

South

0

0

0

46

100.0

-

5

22

Jos Alukkas

South

0

0

0

38

100.0

-

5

30

Thangamayil

South

0

0

0

32

100.0

-

1

16

Khazana

South

0

0

0

49

100.0

-

5

31

TBZ

West

1

7

25

4

67.6

32.4

11

26

PN Gadgil & Sons

West

0

0

24

1

96.0

4.0

3

16

PNG Jewellers

West

0

0

22

0

100.0

-

3

13

Senco

East

9

74

4

4

81.3

18.7

14

48

Source: BIS, HDFC sec Inst Research

PCJ has been the most aggressive in store

expansion: PCJ has been the most aggressive in

network expansion. It has added 282k sq. ft of

retailing space (CAGR ~20%) over FY12-18 vs Titan

(ex-Caratlane) 620k sq. ft (CAGR 15%). The race will

continue over the next 5 years as the SUPERPACK

capitalizes on the weakening position of mom-and-

pop jewellers. We believe PCJ will continue to add

~25 stores per year (75% via franchisee route), while

Titan intends to add ~150 stores over FY18-23E (~85%

through the franchisee route). In the west, TBZ

intends to increase its retail space from ~111k sq ft to

150k sq ft over the next 2-3 years. PN Gadgil & Sons

expects to further deepen its presence in Maharastra

by adding ~15 stores over FY18-20E. The Southern

troika (Malabar Gold, Kalyan and Joyalukkas) are

expected to add ~20-30 stores each in FY19.

PN Gadgil (off a small base), PCJ and GRT have expanded aggressively

Area (sq. ft.) FY13

FY14

FY15

FY16

FY17

FY18

5-yr CAGR

5-yr space

addition

Tanishq (ex-caratlane)

608,628

720,123

812,928

902,928

957,407

1,079,742

12.1%

471,114

PC Jeweller

164,572

238,000

313,296

353,213

386,923

419,963

20.6%

255,391

Thangamayil

46,295

56,724

56,724

57,624

57,624

58,024

4.6%

11,729

TBZ

82,368

88,093

91,000

98,200

108,948

110,666

6.1%

28,298

PN Gadgil

28,412

42,363

53,220

56,256

66,702

100,213

28.7%

71,801

GRT

-

227,000

262,000

297,000

339,000

374,000

13.3%

374,000

Malabar Gold

Joyalukkas

234,000

Kalyan Jewellers

559,000

Source: HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 29

Design portfolio : Key factor

Given that most jewellers are inching towards parity in

terms of gold pricing, monthly scheme offerings and

repurchase/exchange commissions, the battle will

eventually be fought over the breadth and depth of

designs on offer.

Prices converging across the SUPERPACK: A decade

ago, consumers would fork out a premium of 5-15%

over the MCX gold price whilst purchasing from a top

jeweller. Organized players merrily took advantage of

consumers’ ignorance. This is receding now. Titan’s

gold price premium (over MCX) has considerably

shrunk to ~8% (May-18) vs ~15-16% in FY11 and 10%

in Aug-15. As Titan pushes out its wedding collections

over the next 5 years, this spread can only reduce.

Premia for other top jewellers are converging

already, esp. if geographical differences in gold price

are built in.

Monthly gold schemes also converging: Monthly

gold investment schemes by organized jewellers seek

to push market share. These have largely converged

across the SUPERPACK. For jewellers, these are

helpful as (1) Revenues are assured, (2) Working

capital efficiency rises. The obvious trade-off is that

the financing cost is higher than gold on lease (~3-4%

p.a.), typically 6-12%.

Player-wise premium over MCX

…Effective interest rate offered on gold schemes

Source: Company, HDFC sec Inst Research, as per 10

th

Jun 18

Source: Website, Company, HDFC sec Inst Research

8.1

6.5

6.4

5.9

4.6

4.4

4.4

3.9

3.3

2.6

2.3

-

2.0

4.0

6.0

8.0

10.0

Titan

TBZ

Jos Alukkas

P N Gadgil & Sons

Malabar Gold

Thangamayil

GRT

PCJ

Kalyan

Joyalukkas

PNG Jewellers

Premium (%)

12.0

12.0

11.4

11.0

10.9

10.9

7.8

5.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Tanishq

Thangamayil

PC Jeweller

Malabar Gold

GRT

Kalyan

PN Gadgil & Sons

Joyalukkas

Effective Interest rate

Gold realizations, monthly

scheme offerings, repurchase/

exchange discounts

converging across the

SUPERPACK

Hence, battle will be fought

on designs in the medium-to-

long term

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 30

Repurchase/exchange indicate similar trends:

Repurchase commissions are charged by jewellers if

the latter wishes to sell/exchange old jewellery for

cash or new jewellery. The commissions depend on

(1) Type of transaction (repurchase or exchange), (2)

Whether the jewellery is their own or that of other

jewellers. These commissions are largely converging

across key jewellers (see table). With mandatory

hallmarking expected to be a reality soon, this

convergence can only accelerate. Also, with tighter

credit (higher collateral and stricter Debt/Equity

norms), we believe jewellers may focus on procuring

more gold via exchange schemes, further driving

down exchange pricing premia. Titan’s stated

strategy of increasing its exchanged gold mix from

~40% in FY18 to ~50% by FY23 is but an indication of

this trend. Co has revised its old gold exchange

scheme recently.

Player-wise: Old Gold Repurchase/Exchange commissions

Jeweller

Repurchase for Cash (commission %)

Old Gold Exchange (commission %)

Own gold

Against Other jewellers

Own gold

Against Other jewellers

Titan

3%

No repurchase

0%

2%(22k) / 8%(below 22k)

PCJ

3%

No repurchase

0%

1%

Thangamayil

3%

3%

0%

TBZ

3%

No repurchase

0%

3%

Kalyan

1%

No repurchase

0%

6%

P N Gadgil & Sons

3%

No repurchase

0%

GRT

3%

No repurchase

0%

Source: HDFC sec Inst Research

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 31

Tanishq leads on design, peers will catch up: Two

thirds of jewellery manufactured in India today is

hand-crafted. Hence, (1) Strong tie-ups with Karigars

for each region to cater to local tastes, (2) In-house

manufacturing capabilities, (3) In-house design teams

and/or tie-ups with celebrity designers, and (4) Large

inventory at retail outlets are key to gaining market

share.

Our industry/store visits suggest that Tanishq has a

headstart in design offerings as its wider geographic

presence implies better Karigar tie-ups in the regions

targeted for expansion. South is largely a

homogenous market in terms of designs

offered/purchased and accounts for ~75% of the

revenues for major South jewellers. This clearly

suggests that south jewellers have some catching up

to do on their tie-ups with Karigars ergo, on the

design curve. However, we suspect able competitors

such as PCJ, Kalyan are closer in the catch-up phase

given their relative breadth of presence vs other

jewellers (ex-Tanishq). PCJ’s in-house manufacturing

capabilities is expected to hold the company in good

stead as the battle over designs intensifies. Malabar

Gold and Joyalukkas too are fast climbing up the

design curve.

Sourcing of gold could be the joker in the pack:

Jewellers source their raw material through a mix of

(1) Gold on lease through banks, wherein designated

bullion banks charge an interest rate of ~2-4%. This is

the cheapest source of funding inventory and gold

procurement, (2) The (old) gold exchange route is

where consumers exchange their old jewellery for

new jewellery (or for cash), (3) Jewellers also

purchase gold in the domestic spot market.

The mix of sourcing gold varies across jewellers.

Given that banks have tightened the noose on

lending to the industry, we believe jewellers may

have to re-look their sourcing strategies and focus on

procuring more from their gold exchange schemes.

An attractive gold exchange scheme helps jewellers

to (1) De-risk its sourcing dependence on Gold on

lease (2) Up-sell costlier (and more profitable)

jewellery to consumers.

Exchange schemes can drive SSSG for SUPERPACK:

The up-selling opportunity presented by an attractive

gold exchange scheme could help top jewellers stoke

up SSSG as typically the consumer ends up spending

~1.4-1.7x the exchange value. Our industry visit

suggests that top jewellers typically have ~50-70% of

repeat customers who are ideal candidates to push

this too. We estimate Titan and PCJ to account for

~5% & ~2% respectively of the total gold exchange

market. This could nearly double for both over 5

years Across zones, big-box jewellers have revised

their exchange programme (more lucrative for

consumers now) to capture the up-selling

opportunity. .

Tanishq has a 1-2 year head-

start vs peers on designs

given its wider presence

Exchange programme is a

good up-selling tool. Could

push SSSG

INDIAN GEMS & JEWELLERY : SECTOR REPORT

Page | 32

SUPERPACK’s est exchange market share (FY18)

Gold on lease for listed jewellers (FY18)

Source: Company, HDFC sec Inst Research

Source: Website, Company, HDFC sec Inst Research

Bank credit sector and share in exposure

…Credit growth tends to mimics gold prices with a lag

Source: Company, HDFC sec Inst Research

Source: Company, HDFC sec Inst Research

Malabar

Gold

7

GRT

5

Tanishq

5

Joyalukkas

4

Kalyan

3

PCJ (Dom

biz)

2

Khazana

2

Jos Alukkas

1

PNG

Jewellers

1

PN Gadgil

1

Thangamayil

1

TBZ

1

Other

organized

Jewellers

4

251

285

318

397

513

611

699

718

727

690

727

2.30

2.40

2.50

2.60

2.70

2.80

2.90

3.00

200

300

400

500

600