TAX

ADMINISTRATION

Opportunities Exist to

Improve Monitoring

and Transparency of

Appeal Resolution

Timeliness

Report to Congressional Committees

September 2018

GAO-18-659

United States Government Accountability Office

United States Government Accountability Office

Highlights of GAO-18-659, a report to

congressional

committees

September 2018

TAX ADMINISTRATION

Opportunities

Exist to Improve Monitoring and

Transparency of Appeal

Resolution Timeliness

What GAO Found

The Internal Revenue Service (IRS) has a standard process to resolve a diverse

array of taxpayer requests to appeal IRS proposed actions to assess additional

taxes and penalties or collect taxes owed. The process begins with a taxpayer

filing an appeal with the IRS examination or collection unit proposing the

compliance action and ends with a decision from the Office of Appeals (Appeals).

Appeals must have staff with expertise in all areas of tax law to review taxpayer

appeals. However, its staffing levels declined by nearly 40 percent from 2,172 in

fiscal year 2010 to 1,345 in fiscal year 2017. Appeals anticipates a continued risk

of losing subject matter expertise given that about one-third of its workforce was

eligible for retirement at the end of last fiscal year.

Appeals monitors the number of days to resolve taxpayer appeals of

examination, collection, and other tax disputes. However, IRS does not monitor

the timeliness of transfers of all incoming appeal requests. GAO analysis showed

that the time to transfer appeal requests from compliance units varied depending

on the type of case (see table below).

Collections workstreams—taxpayer appeals where IRS (1) filed a notice of

federal tax lien or proposed a levy (collection due process) or (2) rejected an

offer to settle a tax liability for less than owed (offer in compromise).

• The Internal Revenue Manual (IRM), IRS’s primary source of instructions to

staff, requires transfer to Appeals within 45 days for the largest collection

workstream. With manager approval, collection staff may have an additional

45 days to work with the taxpayer. Nearly 90 percent of collection appeals

closed in fiscal years 2014 to 2017 were transferred to Appeals within

90 days.

Examination workstreams—taxpayer appeals of additional tax and penalty

assessments IRS proposed based on its auditing of tax returns over a wide

range of examination issues.

View GAO-18-659. For more information,

contact

Jessica Lucas-Judy at (202) 512-

9110 or

Why GAO Did This Study

The Taxpayer Bill of Rights entitles

taxpayers with the right to appeal a

decision of the Internal Revenue

Service (IRS) in an independent

forum. GAO was asked to review this

administrative appeal process within

IRS.

Among other things, this report (1)

describes the IRS appeal process and

staffing; (2) assesses how IRS

monitors and manages the time to

receive and resolve taxpayer appeals

cases; and (3) evaluates the extent to

which Appeals communicates

customer service standards and

assesses taxpayer satisfaction with

the appeal process.

GAO reviewed IRS guidance,

publications, and documentation on

the appeal process. GAO analyzed

IRS data for administrative appeal

cases closed in fiscal years 2014

through 2017 to compare appeal case

resolution time for different types of

cases. GAO interviewed IRS officials

and a non-generalizable sample of

external stakeholders, including

attorneys and accountants,

knowledgeable about the appeal

process. Among other things, GAO

compared IRS actions to federal

standards for internal control and

customer service.

What GAO Recommends

GAO makes seven recommendations

to help enhance controls over and

transparency of the IRS appeals

process (several of the

recommendations are detailed on the

following page).

•

IRS does not have an IRM requirement with guidelines and procedures for

timely transfer for examination appeals. Accordingly, more than 20 percent of

examination appeals closed in fiscal years 2014 to 2017 took more than

120 days to be transferred to Appeals. Delays in transferring appeals can

result in increased interest costs for taxpayers.

Average Days for Compliance Review by Workstream, Fiscal Years 2014-2017

Appeal workstream

Average number of days

Compliance share

of total appeal

resolution time

Compliance transfer

to Appeals

Total appeal

resolution time

Collection workstreams

• Collection due process

59

252

23%

•

Offer in compromise

61

240

26%

Examination workstreams

• Large case examination

108

637

17%

• Examination

105

337

31%

•

Innocent spouse

30

249

12%

• Penalty appeals

100

220

45%

Other workstream

39

101

38%

Source: GAO analysis of Appeals Centralized Database System I GAO-18-659

Although Appeals maintains data on total appeal resolution time—from IRS

receipt to Appeals’ decision—such information is not readily transparent to IRS

compliance units or the public. GAO analysis of IRS data found that, for fiscal

years 2014 to 2017, about 15 percent of all appeal cases closed within 90 days

(see figure below). About 85 percent of all cases were resolved within one year

of when the taxpayer requested an appeal. Total resolution times differed by

case type. However, without easily accessible information on resolution times,

taxpayers are not well informed on what to expect when requesting an appeal.

Total Appeal Resolution Time by Workstream, Fiscal Years 2014-2017

Although Appeals has customer a service standard and conducts a customer

satisfaction survey, its standard and related performance results are not readily

available to the public. Under the GPRA Modernization Act of 2010 (GPRAMA)

and Executive Orders, the Department of the Treasury is responsible for

customer service performance. Appeals conducts outreach to the tax practitioner

community but does not regularly solicit input before policy changes.

Without a

mechanism, such as leveraging existing IRS advisory groups or alternatively

developing its own advisory body, Appeals is missing an opportunity to obtain

public input on policy changes affecting the taxpayer’s experience in the appeal

process.

GAO recommends, among other

things, that the Commissioner of

Internal Revenue

• Establish timeframes and

monitoring procedures for timely

transfer of taxpayer appeals

requests by examination

compliance units to the Office of

Appeals.

• Direct the Office of Appeals to

regularly report and share with

each compliance unit the data on

the time elapsed between when a

taxpayer requests an appeal to

when it is received in the Office of

Appeals.

• Provide more transparency to

taxpayers on historical average

total appeal resolution times.

GAO recommends, among other

things, that the Secretary of the

Treasury, consistent with its

responsibilities under GPRAMA and

Executive Orders for customer service,

ensure that the Commissioner of

Internal Revenue develops a

mechanism to solicit and consider

customer feedback on a regular basis

on current and proposed IRS appeal

policies and procedures.

Treasury and IRS agreed with GAO’s

recommendations, and IRS said it will

provide detailed corrective action

plans.

Page i GAO-18-659 IRS Appeal Process

Letter 1

Background 5

Appeals Has a Standard Process to Resolve Diverse Taxpayer

Cases but Has Not Assessed Critical Skills Gaps in Its

Declining Workforce 13

IRS Does Not Monitor Timeliness of Transfers of All Incoming

Appeal Requests and Appeals Does Not Communicate Total

Resolution Times to Taxpayers 26

Appeals Does Not Make Customer Service Standard Clear to

Taxpayers, and It Does Not Have a Mechanism to Consider

External Customer Input on Policy Changes 40

Conclusions 49

Recommendations for Executive Action 50

Agency Comments and Our Evaluation 51

Appendix I Comments from the Internal Revenue Service 53

Appendix II GAO Contact and Staff Acknowledgements 57

Tables

Table 1: Overview of IRS Business Operating Divisions 6

Table 2: Average Days for Compliance Review and Share of Total

Appeal Resolution Time for Appeal Cases Closed, Fiscal

Years 2014-2017 28

Table 3: Attributes and Internal Measures for Appeals Customer

Service and Taxpayer Rights Standard 41

Figures

Figure 1: Overview of IRS Appeal Workstreams 10

Figure 2: IRS Office of Appeals Funding, Fiscal Years 2010-2018 11

Figure 3: Office of Appeals Inventory, Cases Received and

Pending, Fiscal Years 2010-2017 12

Figure 4: Overview of the IRS Appeal Process 14

Figure 5: Overview of Compliance Review and Transfer 16

Figure 6: Overview of Appeals Case Receipt and Assignment

Process 18

Figure 7: Overview of Appeals Case Review Process 19

Contents

Page ii GAO-18-659 IRS Appeal Process

Figure 8: Appeals Staffing Levels, Fiscal Years 2010-2017 23

Figure 9: Average IRS Collection Case Transfer Time to Office of

Appeals for Appeal Cases Closed, Fiscal Years 2014-

2017 29

Figure 10: Average IRS Examination Case Transfer Time to Office

of Appeals for Appeals Cases Closed, Fiscal Years 2014-

2017 32

Figure 11: Average Examination Case Transfer Time from IRS

Business Operating Divisions to Office of Appeals, Fiscal

Year 2017 33

Figure 12: Average Days for Appeals Review by Workstream for

Cases Closed, Fiscal Years 2014-2017 36

Figure 13: Percentage of Cases Closed by Total Appeal

Resolution Time by Appeals Workstream, Fiscal Years

2014-2017 38

Abbreviations

Appeals Office of Appeals

ACDS Appeals Centralized Database System

AQMS Appeals Quality Measurement System

FTE Full-Time Equivalent

GPRA Government Performance and Results Act

GPRAMA GPRA Modernization Act of 2010

IRM Internal Revenue Manual

IRS Internal Revenue Service

IRSAC Internal Revenue Service Advisory Council

LB&I Large Business and International

OMB Office of Management and Budget

Restructuring Act IRS Restructuring and Reform Act of 1998

SB/SE Small Business/Self-Employed

TE/GE Tax Exempt and Government Entities

Treasury Department of the Treasury

W&I Wage & Investment

This is a work of the U.S. government and is not subject to copyright protection in the

United States. The published product may be reproduced and distributed in its entirety

without further permission from GAO. However, because this work may contain

copyrighted images or other material, permission from the copyright holder may be

necessary if you wish to reproduce this material separately.

Page 1 GAO-18-659 IRS Appeal Process

441 G St. N.W.

Washington, DC 20548

September 21, 2018

The Honorable Orrin Hatch

Chairman

The Honorable Ron Wyden

Ranking Member

Committee on Finance

United States Senate

The Honorable Kevin Brady

Chairman

The Honorable Richard E. Neal

Ranking Member

Committee on Ways and Means

House of Representatives

The Taxpayer Bill of Rights gives taxpayers the right to appeal a decision

of the Internal Revenue Service (IRS) in an independent forum. IRS

expounded further on this right, stating that “taxpayers are entitled to a

fair and impartial administrative appeal of most IRS decisions, including

many penalties, and have the right to receive a written response

regarding the Office of Appeals (Appeals’) decision.”

1

If taxpayers

disagree with IRS decisions to assess additional tax or take collection

action, they can generally bring their disputes before Appeals.

Appeals’ mission is to resolve taxpayer disputes, without litigation, on a

basis which is fair and impartial to both the government and the taxpayer

in a manner that will enhance voluntary compliance and public confidence

in the integrity and efficiency of the IRS.

2

Appeals’ policy is to provide a

prompt conference and decision in each case.

3

Timely appeal decisions

are important for (1) the taxpayer and IRS to know the amount of taxes

owed or outcome of other tax matters in dispute, and (2) the Department

1

26 U.S.C. § 7803(a)(3)(E), and see also, Department of the Treasury, Internal Revenue

Service, Taxpayer Bill of Rights, Pub. 5170, (July 2014), and Department of the Treasury,

Internal Revenue Service, Your Rights as a Taxpayer, Publication 1 (September 2017).

This publication further explains 10 rights for taxpayers and the processes for

examination, appeal, collection, and refunds.

2

Internal Revenue Manual (IRM) Part 8, Chapter 1, Section 1.1.

3

IRM Part 8, Chapter 1, Section 1.1.2.b.

Letter

Page 2 GAO-18-659 IRS Appeal Process

of the Treasury (Treasury) to receive any additional revenue involved at

the earliest practicable date.

4

You asked us to review the IRS administrative appeal process, the time to

resolve taxpayer appeals, and taxpayer satisfaction with the process. This

report (1) describes the steps and staffing levels for the IRS appeal

process and assesses the extent to which Appeals conducts workforce

planning in a time of declining resources; (2) assesses how IRS monitors

and manages the time to receive and resolve taxpayer appeals cases;

and (3) evaluates the extent to which Appeals communicates customer

service standards and assesses taxpayer satisfaction with the appeal

process.

To describe the IRS administrative appeal process, we reviewed Internal

Revenue Manual (IRM) sections that detail how IRS employees are to

process appeal cases. We also reviewed the IRS website and IRS

documents and publications that describe the appeal process and

indicate how taxpayers are to file an appeal. We interviewed senior

Appeals managers to understand how Appeals operates and how cases

are processed when Appeals receives them. To understand the initial IRS

receipt of taxpayer appeals, we interviewed IRS examination and

collection officials in the Small Business/Self-Employed (SB/SE) and

Wage and Investment (W&I) business operating divisions. These two IRS

divisions accounted for 97 percent of appeal cases closed in fiscal year

2017. We interviewed Appeals administrative processing staff who

receive and route cases in Appeals as well as customer service staff who

handle taxpayer inquiries about the status of their appeals. We also

analyzed data from the Appeals Centralized Database System (ACDS)

for 346,038 appeals cases closed in fiscal year 2014 (the oldest complete

year available) through fiscal year 2017 (the last complete fiscal year

available at the time of our analysis).

5

We used the data to calculate the

percentage of taxpayers who had a representative with them through the

process and to determine the percentage of cases that had a conference

with appeals, including those with an in-person conference. We also

conducted observational visits to Appeals locations in Philadelphia,

Pennsylvania and Atlanta, Georgia to interview a non-generalizable group

4

IRM Part 8, Chapter 1, Section 1.1.2.b.

5

ACDS combines various database systems into one centralized web-based system used

to track and document appeals case review, including time and progress of the workload,

within the Office of Appeals. Our analysis excluded 439 cases to suppress small case

counts and avoid disclosure of taxpayer information.

Page 3 GAO-18-659 IRS Appeal Process

of Appeals frontline supervisors and staff who handle a diversity of

appeals cases to better understand how appeals cases are assigned to

staff, as well as the case review process. We selected these locations

because they allowed us to interview Appeals frontline staff who work a

wide variety of taxpayer appeals across all seven Appeals work

categories.

To describe the staffing levels and assess the extent to which Appeals

conducts workforce planning in a time of declining resources, we obtained

and analyzed staffing information and reviewed the IRM section that

explains the Appeals human capital programs and the IRS Strategic

Workforce Planning Team. We interviewed Appeals and IRS human

capital staff to better understand how they conduct workforce planning

and reviewed documentation about the IRS Strategic Workforce Planning

team’s activities and timeframes. We then compared Appeals workforce

planning activities to our key principles of effective workforce planning.

6

We also reviewed a hiring tool Appeals uses to project case inventory

based on historical case data and current staffing levels to determine

workforce needs and interviewed Appeals managers about strategies and

policies for maintaining staff skills.

To assess how IRS monitors and manages the time to receive and

resolve taxpayer appeals cases, we reviewed IRS documents, including

IRM sections, IRS procedures, and quarterly Appeals performance

reports and monthly reports to the Commissioner of Internal Revenue.

We compared the controls identified to federal standards for internal

control.

7

We interviewed IRS officials responsible for managing Appeals’

review process as well as SB/SE and W&I officials managing initial

appeals receipt for those compliance units. We reviewed the measures

IRS uses to describe timeframes to resolve appeals, which quantify case

review time in average days. Overall averages can be a broad measure

and may be affected by outliers. Finally, we analyzed data from the ACDS

for 346,038 appeals cases closed in fiscal year 2014 through fiscal year

6

GAO, Human Capital: Key Principles for Effective Strategic Workforce Planning,

GAO-04-39 (Washington, D.C.: Dec. 11, 2003). Based on GAO reports and testimonies,

review of studies by leading workforce planning organizations, and interviews with officials

from the Office of Personnel Management and other federal agencies, this report

describes the key principles of strategic workforce planning agencies should address

irrespective of the context in which planning is done.

7

GAO, Standards for Internal Control in the Federal Government, GAO-14-704G

(Washington, D.C.: September 2014.

Page 4 GAO-18-659 IRS Appeal Process

2017. We calculated and compared average appeal case resolution time

for different types of cases. For purposes of this review, we determined

that the ACDS data used in our analysis were reliable. Our data reliability

assessment included reviewing relevant documentation, interviewing

knowledgeable IRS officials, and reviewing the data to identify obvious

errors or outliers.

To evaluate the extent to which Appeals has and communicates customer

service standards and assesses taxpayer satisfaction with the appeal

process, we identified federal standards for customer service under the

GPRA Modernization Act of 2010 (GPRAMA), as well as customer

service-related Executive Orders, Office of Management and Budget

(OMB) guidance, and internal control standards and compared IRS

Appeals actions to those standards.

8

We reviewed IRM documentation of

the Appeals customer service standard and related measures from the

Appeals Quality Measurement System (AQMS), as well as AQMS annual

reports for fiscal years 2014 through 2017.

9

To understand how Appeals obtains customer feedback, we reviewed the

methodology for the annual Appeals customer satisfaction survey and

analyzed survey reports for fiscal years 2016 through 2017 as well as

focus group reports from fiscal years 2012 through 2014 (the last year

IRS held these focus groups). We drew on results from the surveys and

focus groups to describe factors that affect Appeals customer satisfaction.

We interviewed Appeals managers and staff who handle cases to

understand their views on factors that affect taxpayer satisfaction and

understand how Appeals communicates service standards and measures

customer satisfaction. We also conducted semi-structured interviews with

13 external stakeholders from law and accounting organizations who

have represented a mix of higher- and lower-income individuals as well

as corporations and other businesses to understand their experiences

with the appeal process. To select interviewees with prior experience with

IRS and its appeal process, we used a snowball sampling technique

based on our review of IRS partner and stakeholder organizations, public

comments about the appeals process, and referrals from initial

8

Pub. L. No. 111-352, 124 Stat. 3866 (Jan. 4, 2011). GPRAMA significantly enhanced the

Government Performance and Results Act of 1993 (GPRA), Pub. L. No. 103-62, 107 Stat.

285 (Aug. 3, 1993). GAO-14-704G.

9

AQMS is a system that uses key output measures from the appeals review process to

assess organizational performance and serves as an internal tool for managers to use in

determining strengths and weaknesses in the appeal process.

Page 5 GAO-18-659 IRS Appeal Process

interviewees. Information from this sample of stakeholders is not

generalizable.

We conducted this performance audit from February 2017 to September

2018 in accordance with generally accepted government auditing

standards. Those standards require that we plan and perform the audit to

obtain sufficient, appropriate evidence to provide a reasonable basis for

our findings and conclusions based on our audit objectives. We believe

that the evidence obtained provides a reasonable basis for our findings

and conclusions based on our audit objectives.

Enforcing tax laws helps IRS collect revenue from noncompliant

taxpayers and, perhaps more importantly, promotes voluntary compliance

by giving taxpayers confidence that others are paying their fair share.

However, every year, taxpayers fail to pay hundreds of billions of dollars

in taxes. This tax gap—the difference between tax amounts that

taxpayers should pay and what they actually pay voluntarily and on

time—has been a persistent problem for decades.

10

In our 2017

High-Risk Report we continued to include Enforcement of Tax Laws as a

high-risk area.

11

Key components of this high-risk area include both

addressing the tax gap and improving tax compliance.

IRS has four business operating divisions responsible for enforcing tax

law and providing taxpayer service to ensure taxpayer compliance, as

shown in table 1. For this report, we refer to these divisions as

compliance units and their staff as compliance staff.

10

In 2016, IRS estimated that taxpayers voluntarily and timely paid about 81.7 percent of

the taxes they should have for tax years 2008 to 2010, resulting in an average annual

gross tax gap of $458 billion for those years. IRS estimated that through late payments

and enforcement actions, it will collect an additional $52 billion annually for tax years 2008

to 2010. The average net tax gap—$406 billion per year for those years—may never be

collected.

11

Every 2 years, we report on agencies and program areas that are high risk due to their

vulnerabilities to fraud, waste, abuse, and mismanagement or are most in need of

transformation. Enforcement of tax laws was designated as a high-risk area in 1990, the

first year we published a High-Risk List. See GAO, High-Risk Series: Progress on Many

High-Risk Areas, While Substantial Efforts Needed on Others, GAO-17-317 (Washington,

D.C.: Feb. 15, 2017).

Background

Page 6 GAO-18-659 IRS Appeal Process

Table 1: Overview of IRS Business Operating Divisions

Business operating

division

Enforcement responsibilities

Taxpayers served

Small Business/Self-

Employed (SB/SE)

Audits individual and business tax returns to detect

misreporting of income, employment, excise, estate,

or gift taxes. SB/SE audits include field examinations

(conducted from field offices) and correspondence

audits conducted through the mail from campus

locations.

Small businesses, self-employed, and

corporations and partnerships with less than

$10 million in assets

Collects delinquent taxes and secures delinquent tax

returns. Automated collection is largely a call center

operation from campus locations that uses

automated calls and letters to remind taxpayers of

their tax delinquency. Field collection contacts

noncompliant individuals and business taxpayers

face-to-face.

Individuals and businesses

Wage and Investment

(W&I)

Audits individual tax returns to detect misreporting of

income tax, primarily for refundable tax credits. All

W&I audits are correspondence audits conducted

through the mail from campus locations.

Individual taxpayers

Large Business and

International (LB&I)

Audits business tax returns to detect misreporting of

income, employment, and excise taxes. These are

field examinations of taxpayer books and records.

Audits income tax returns for individuals with assets

or earnings of tens of millions of dollars or with

international tax issues. These audits include field

examinations and correspondence audits conducted

through the mail.

Large corporations and partnerships with

$10 million or more in assets

Individuals with high wealth or international tax

issues

Tax Exempt and

Government Entities

(TE/GE)

Audits exempt organizations and government

entities to detect misreporting of income,

employment, or excise taxes and to ensure exempt

organizations are operating in accordance with their

exempt purposes. These audits include field

examinations and correspondence audits conducted

through the mail.

Retirement plans and trusts

Tax-exempt organizations, such as charities, civic

organizations, and business leagues

Federal, state, and local governments; Indian

tribal governments; and tax-exempt bond issuers

Source: GAO analysis of Internal Review Service information. I GAO-18-659

Formed in 1927, Appeals is the only administrative function of IRS with

authority to consider settlements of tax controversies and has the primary

responsibility to resolve these disputes without litigation to the maximum

extent possible.

12

IRS states that the appeal process is both less formal

12

IRM Part 8, Chapter 6, Section 2.1.1. This report focuses on the IRS administrative

appeal process. Appeals also offers alternative dispute resolution programs in which an

Appeals staff member trained in mediation techniques serves as an impartial third party

facilitating negotiations between taxpayers and IRS during examination or collection.

Role of the Office of

Appeals

Page 7 GAO-18-659 IRS Appeal Process

and costly than court proceedings and is not subject to judicial rules of

evidence or procedure.

13

The IRS Restructuring and Reform Act of 1998 (Restructuring Act)

specified that IRS must provide an independent appeals function.

14

Appeals carries out this function. Appeals is a separate unit within IRS,

and its chief reports directly to the Commissioner of Internal Revenue.

The Restructuring Act also prohibits communications between Appeals

staff and other IRS functions without the taxpayer or representative being

given an opportunity to participate. In 2016, IRS clarified that Appeals is

separate from the IRS compliance functions, including examination and

collection units, that initially review a taxpayer’s case and that Appeals

may return cases to compliance units when taxpayers provide new

information for consideration.

15

Taxpayers may appeal many IRS decisions, including tax collection

actions and proposed tax assessments, with some exceptions.

16

Taxpayers cannot appeal solely due to moral, religious, political,

constitutional, conscientious, or other similar grounds.

17

Taxpayers

requesting appeals can range from individuals to large multinational

corporations. IRS provides publications that explain taxpayer’s rights for

13

Internal Revenue Service, Appeals – An Independent Organization, accessed Sept. 11,

2018, https://www.irs.gov/compliance/appeals/appeals-an-independent-organization.

14

Pub. L. No. 105-206, title I, § 1001(a)(4), 112 Stat. 685 (July 22, 1998), codified at

26 U.S.C. § 7801 note.

15

Department of the Treasury, Internal Revenue Service, Fact Sheet: IRS Clarifies Office

of Appeals Policies, (Updated October 1, 2016).

16

26 C.F.R. §§ 601.105-106.

17

26 C.F.R. § 601.106(b).

Appeal Eligibility

Page 8 GAO-18-659 IRS Appeal Process

both examination and collection appeals.

18

IRS also developed online

self-help tools to help taxpayers understand what can be appealed.

19

For collection actions, the Restructuring Act created a statutory right for

collection due process appeals and provides an impartial review for

taxpayers facing possible levies for collecting delinquent taxes or who

have had a notice of federal tax lien filed against them.

20

IRS also offers a

collection appeals program for a broader range of collection issues, such

as when IRS rejects or terminates an installment agreement to pay taxes

owed.

21

In contrast, for examination decisions, the tax code does not

provide statutory rights to administrative appeals. In certain

circumstances, IRS will designate an examination issue for litigation and

not offer access to the administrative appeal process.

22

In other

circumstances, IRS may decide not to refer cases docketed in the U.S.

Tax Court to Appeals for settlement if it determines doing so will be in the

best interest of sound tax administration.

23

For example, IRS may decide

not to refer a docketed case to Appeals in cases (1) involving a significant

issue common to other cases in litigation for which it is important that the

IRS maintain a consistent position or (2) related to a case over which the

Department of Justice has jurisdiction.

24

18

Appeals rights for examinations are explained in Department of the Treasury, Internal

Revenue Service, Your Appeal Rights and How To Prepare a Protest If You Don’t Agree,

Publication 5, (Jan. 1999) and Department of the Treasury, Internal Revenue Service,

Examination of Returns, Appeal Rights, and Claims for Refund, Publication 556, (Sept.

2013). Appeals rights for collections are explained in Department of the Treasury, Internal

Revenue Service, Collection Appeal Rights, Publication 1660, (Feb. 2014).

19

The tools can be found on the IRS website at

https://www.irs.gov/compliance/appeals/appeals-online-self-help-tools, accessed Sept. 11,

2018.

20

Pub. L. No. 105-206, § 3401, codified at, 26 U.S.C. §§ 6320 and 6330.

21

IRM Part 8, Chapter 24, Section 1. IRS Publication 1660 explains collection issues that

can be appealed under the collection appeals program.

22

IRM Part 33, Chapter 3, Section 6 lays out the designation procedure. IRS officials told

us that from March 2007 to August 2018, the agency had designated fewer than 10 cases

for litigation.

23

26 C.F.R. §601.106, and IRS Rev. Proc. 2016-22, Sec. 3.03.

24

IRS Rev. Proc. 2016-22, Sec. 3.03.

Page 9 GAO-18-659 IRS Appeal Process

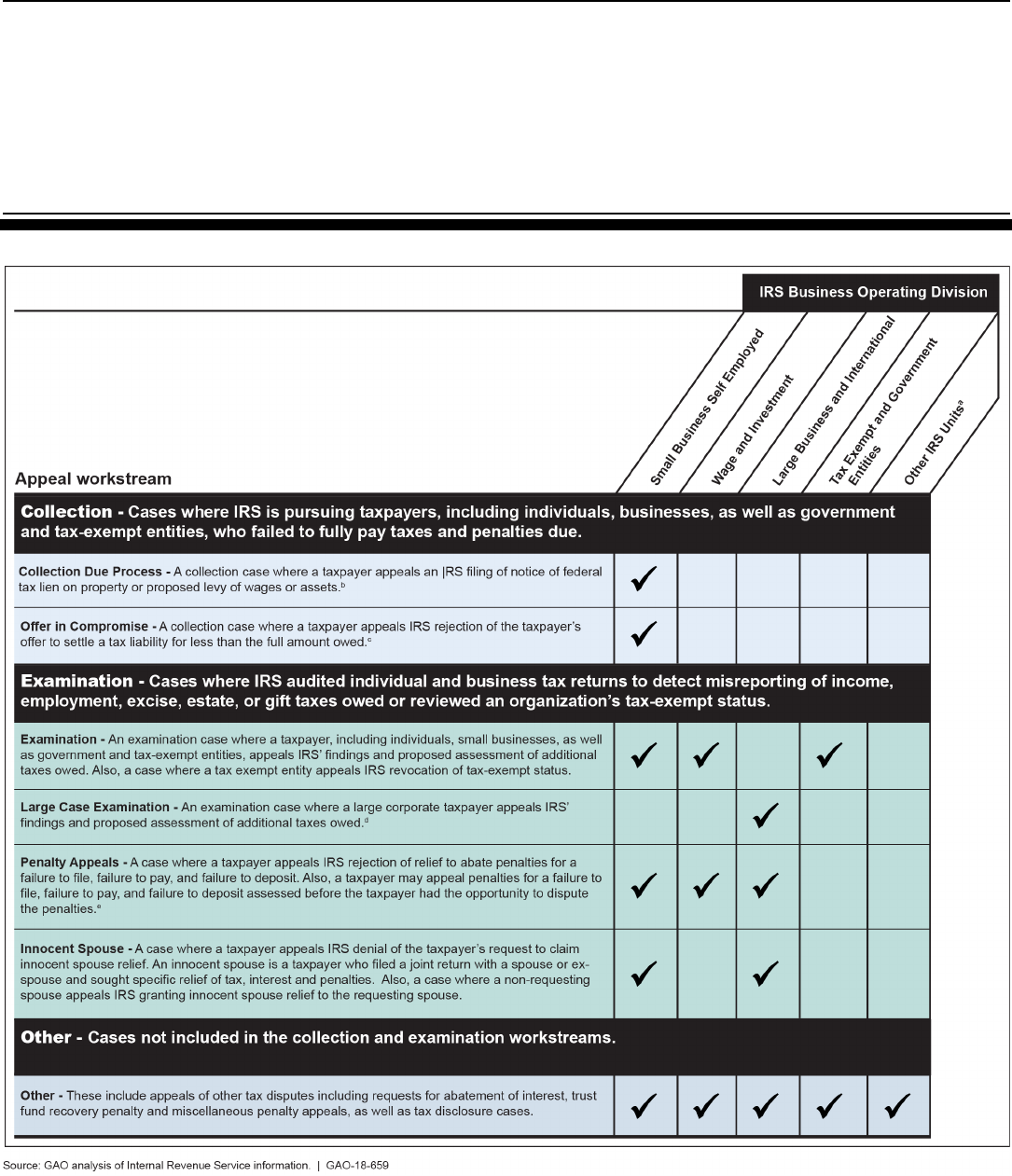

Appeals’ workload is organized into seven workstreams based on

similarities in case characteristics. Two workstreams involve collection

appeals where IRS is pursuing taxpayers who failed to fully pay taxes and

penalties owed. Four workstreams include a wide range of examination

appeals where IRS is proposing additional tax and penalty assessments

based on auditing tax returns. The last workstream covers other cases

that do not fit into the collection and examination workstreams. Figure 1

below provides an overview of the appeal workstreams, including which

IRS business operating divisions transfer the cases to Appeals.

Appeal Workstreams

Page 10 GAO-18-659 IRS Appeal Process

Figure 1: Overview of IRS Appeal Workstreams

a

Other IRS units include the Office of Professional Responsibility and disclosure offices.

b

This workstream excludes collection due process timeliness determination and collection appeals

program cases, which are included in the other workstream.

Page 11 GAO-18-659 IRS Appeal Process

c

This workstream excludes collection appeals program cases, which are included in the other

workstream.

d

For this report, we combined the Appeals industry case and coordinated industry case workstreams

into a large case examination workstream.

e

This workstream contains cases for penalties that have already been assessed.

While Appeals is separate from IRS’s examination and collection

compliance functions, its budget is part of the IRS enforcement budget

appropriation. From fiscal year 2010 to fiscal year 2018, Appeals

represented about 4 percent of the IRS enforcement budget

appropriation. Appeals’ funding has decreased by 29 percent since 2010

to $175 million in 2018 (see fig. 2). Adjusting for inflation, Appeals funding

has decreased 38 percent since 2010.

Figure 2: IRS Office of Appeals Funding, Fiscal Years 2010-2018

Note: Inflation adjustments were made using Bureau of Economic Analysis data for 2010-2017 and

Congressional Budget Office projections for 2018 of the fiscal year chain weighted gross domestic

product price index.

Over this same time period, Appeals received fewer cases as IRS

enforcement activities declined. For example, the individual examination

(or audit) coverage rate declined by about 50 percent from fiscal years

Appeals Funding and

Workload

Page 12 GAO-18-659 IRS Appeal Process

2010 to 2017. Also, the number of notices of federal tax liens filed

declined by nearly 60 percent over the period. Faced with declining

budgetary resources, IRS compliance units can prioritize and select fewer

taxpayers to examine or pursue collection action. Appeals officials said

their office generally must work every case received. Appeals aims to

close approximately the same number of cases each year as it

anticipates receiving during the year. Appeals closure rate—or the

number of cases it resolved divided by the number it received in a

year—improved from 98 percent for fiscal year 2010 to 103 percent for

fiscal year 2017. Annual closure rates for 2017 varied by workstream,

ranging from 72 percent for the innocent spouse workstream to nearly

109 percent for the examination workstream.

25

Figure 3 shows the total

number of cases received and pending at year end since fiscal year 2010.

Figure 3: Office of Appeals Inventory, Cases Received and Pending, Fiscal Years

2010-2017

25

A closure rate greater than 100 percent reflects that Appeals closed more cases in a

year than it received from compliance units and reduced the year end count of cases

pending.

Page 13 GAO-18-659 IRS Appeal Process

Note: Numbers reflect both cases in the IRS administrative appeal process as well as court cases

with Appeals for settlement prior to trial. Data for each fiscal year reflect the number of cases

received during the year and the count of cases pending at year end.

The diverse array of appeal requests across IRS compliance units that

flow into Appeals workstreams follows the same standard process. As

illustrated in figure 4, the appeal process involves multiple steps,

beginning with a taxpayer filing an appeal of a proposed IRS compliance

action and ending with a decision from Appeals. If the taxpayer and IRS

cannot reach agreement through the appeal process, the taxpayer may

have the case reviewed in federal court if eligible. While certain types of

cases must go through the appeal process before review by a court,

others may bypass it and taxpayers may directly petition IRS’s proposed

actions in federal court.

26

26

Collection due process issues under 26 U.S.C. §§ 6320(b) and 6330(d) must be

considered by Appeals before review by a court. 26 C.F.R. §§ 301.6320-1(f)(2) Q&A-F3

and 301.6330-1(f)(2) Q&A-F3.

Appeals Has a

Standard Process to

Resolve Diverse

Taxpayer Cases but

Has Not Assessed

Critical Skills Gaps in

Its Declining

Workforce

IRS Uses a Standard

Process to Resolve

Taxpayer Appeals

Page 14 GAO-18-659 IRS Appeal Process

Figure 4: Overview of the IRS Appeal Process

a

A court case that has not gone through the administrative appeal process generally will go to the

Office of Appeals for possible resolution.

Compliance action. For proposed examination actions to assess

additional taxes and penalties or collection actions, such as filing a notice

of federal tax lien or proposing a levy to collect delinquent taxes, IRS

notifies the taxpayer in writing about the proposed compliance action and

explains their appeal rights. The notification states that the taxpayer has

30 days to file an appeal and includes a list of IRS publications and other

information on how to file an appeal.

Taxpayer action. Within 30 days from the compliance notification,

taxpayers who disagree with the IRS proposed action must send a formal

written request to appeal. The appeal request must include:

• the taxpayer’s name and address, and a daytime telephone number;

• a statement that the taxpayer wants to appeal the IRS findings to the

Appeals Office;

• a copy of the letter showing the proposed changes and findings that

the taxpayer does not agree with;

• the tax periods or years involved;

Page 15 GAO-18-659 IRS Appeal Process

• a list of the changes that the taxpayer does not agree with, and why

the taxpayer does not agree;

• the facts supporting the taxpayer’s position on any issue that the

taxpayer does not agree with;

• the law or authority, if any, on which the taxpayer is relying; and

• a signature on the written protest, stating that it is true, under the

penalties of perjury.

27

Taxpayers may choose to represent themselves or have professional

representation before Appeals. A representative must be a federally

authorized practitioner, who can be an attorney, certified public

accountant, or enrolled agent authorized to practice before the IRS.

28

Low-income taxpayers or those who speak English as a second language

may be eligible for free or low cost representation from a Low Income

Taxpayer Clinic.

29

Based on our analysis of ACDS data for appeal cases

closed from fiscal year 2014 through 2017, 57 percent of taxpayers had a

representative and 43 percent were taxpayers representing themselves.

The share of appeal cases with taxpayers representing themselves varied

significantly across the workstreams, ranging from 18 percent for large

case examination appeals to 95 percent for innocent spouse appeals.

Taxpayers are instructed to send their appeal and supporting material to

the examination or collection compliance unit that proposed the action.

IRS states sending the appeal request directly to the Office of Appeals

will result in delays and may result in the appeal not being considered a

timely request.

Compliance review. Compliance staff work directly with the taxpayer to

try to resolve the issue once they determine a taxpayer is requesting an

appeal. This may involve multiple interactions by telephone or

27

26 C.F.R. § 601.105(d)(1)-(2); Department of the Treasury, Internal Revenue Service,

Your Appeal Rights and How to Prepare a Protest If You Don’t Agree, Publication 5,

(January 1999).

28

An enrolled agent is an individual who has, either through past service and technical

experience at IRS or by demonstrating special competence through a written examination,

earned the ability to represent taxpayers before IRS. An unenrolled preparer may be a

witness at an appeals conference, but not a representative.

29

Low income taxpayer clinics are operated by nonprofit organizations or academic

institutions. Although these clinics receive partial funding from the IRS, clinics, their

employees, and their volunteers are completely independent of the IRS.

Page 16 GAO-18-659 IRS Appeal Process

correspondence. Compliance staff will review any new information

submitted by the taxpayer as they attempt to resolve open collection or

examination matters. Figure 5 illustrates the steps compliance staff are to

follow when they receive an appeal.

Figure 5: Overview of Compliance Review and Transfer

a

Not applicable for collection due process appeal request. If the taxpayer does not request a

collection due process hearing within the 30-day period, the taxpayer may still be entitled to an

equivalent hearing with Appeals but will not have any appeal rights allowing the taxpayer to file for

judicial review of the equivalency hearing determination. 26 C.F.R. § 301.6330-1(i).

b

A taxpayer requesting an offer in compromise appeal does not need to submit additional information.

c

A statute of limitations extension can be for a fixed date or open-ended.

If compliance staff cannot reach agreement with the taxpayer, the

compliance unit forwards the appeal request and documentation from the

taxpayer along with the proposed compliance action documentation to

Appeals. Appeals provides a case routing tool on the IRS intranet with

instructions and addresses for compliance staff transferring appeal

documentation to an Appeals location. In general, taxpayer appeals

Page 17 GAO-18-659 IRS Appeal Process

related to examination and collection campus cases are transferred to an

Appeals campus location.

30

Appeals for field examination and collection

cases are transferred to an Appeals office near the taxpayer’s location.

Compliance staff may not forward an appeal request to Appeals if the

taxpayer did not file the request in time or refuses to sign the appeal

under penalty of perjury, among other reasons.

Appeals receipt and review. Figure 6 provides an overview of how

Appeals receives and assigns cases. Upon receipt of an appeal, Appeals

processing staff log each appeal case into the ACDS used to control and

track cases in Appeals inventory. Most appeal cases arrive from

compliance as paper files, and Appeals is working to receive certain

collection cases electronically.

31

For examination cases, Appeals

processing staff also check that sufficient time remains for Appeals to

complete its review. Generally, examination cases must have at least

365 days remaining on the assessment statute expiration date when the

case is received in Appeals.

32

30

Campuses, formerly called service centers, are facilities where IRS performs various

operations, such as processing tax returns, handling taxpayer calls, and conducting

correspondence audits. Appeals also has staff in those IRS locations.

31

Appeals has coordinated with SB/SE to electronically receive collection appeals

program cases in the other workstream. Since fiscal year 2015, Appeals has had a pilot to

receive a limited number of collection due process cases electronically. In October 2017,

Appeals expanded the pilot to receive an increased number of these collection appeals

electronically.

32

IRM Part 8, Chapter 21, Section 3.1.1. Estate tax appeal cases and certain excise tax

claim appeals must have at least 270 days remaining on the assessment statute

expiration date, and these expiration dates cannot be extended. See, 26 U.S.C. § 6206;

IRM Part 8, Chapter 21, Section 3.1.3.2, IRM Part 8, Chapter 21, Section 3.1.3.22, and

IRM Part 4, Chapter 24, Section 8.1.2.

Page 18 GAO-18-659 IRS Appeal Process

Figure 6: Overview of Appeals Case Receipt and Assignment Process

An Appeals manager is to assess a case’s complexity and difficulty to

determine how to assign the case.

33

The manager is to consider the

factual and legal complexity of the case issues and the level of

conference negotiation skills needed to handle the case. The manager

also is to consider whether the case has industry-wide implications or the

decision would potentially affect other taxpayers and overall voluntary

compliance. Generally, Appeals employees with higher skill levels and

expertise are expected to be assigned more complex cases.

The manager is then to assign the case to an Appeals staff person based

on the employee’s grade level, ability, and case load. The Appeals

employee leading the case may also draw on support from Appeals

technical specialists, such as engineers and economists. For the large

case examination workstream, an Appeals team case leader may

oversee multiple Appeals employees working a large appeal case with

highly complex issues and disputed amounts of $10 million or more.

Figure 7 provides an overview of the Appeals case review process once a

case is assigned to an Appeals employee. First, the Appeals employee

sends a letter to the taxpayer with information about the appeal process

and schedules a meeting. The letter details what additional material is

needed, if any, and explains that a determination will be made on the

information provided if there is no further contact from the taxpayer. The

letter states that Appeals is independent from IRS compliance offices and

refers to Publication 4227—Overview of the Appeals Process. Finally, the

33

IRM Part 1, Chapter 4, Section 28.

Page 19 GAO-18-659 IRS Appeal Process

letter mentions that the taxpayer may be asked to participate in an

Appeals customer satisfaction survey after they have completed the

appeal process.

Figure 7: Overview of Appeals Case Review Process

Appeals offers conferences to provide taxpayers with an opportunity to

present their position (see fig. 7). Based on our analysis of ACDS data for

appeal cases closed, about 87 percent of appeal cases that were closed

in fiscal year 2014 through 2017 had a conference.

34

Most conferences

are held by telephone which can be a quick and efficient means for

taxpayers to resolve their issues. Appeals campus locations conduct

telephone conferences because these locations currently are not

configured to accommodate in-person conferences. Appeals may be able

to resolve some taxpayer appeals with mail correspondence only. For

34

An appeal case may not have a conference if the taxpayer does not respond to

schedule a conference or fails to appear for a scheduled conference, or if IRS determines

that a conference is not necessary. Based on our analysis of ACDS data for appeal cases

closed, the other workstream accounted for about 40 percent of all appeal cases that were

closed without a conference in fiscal years 2014 to 2017.

Page 20 GAO-18-659 IRS Appeal Process

perspective, about 10 percent of appeal cases that were closed and also

had a conference from fiscal year 2014 through 2017 did so only by

correspondence, and the penalty workstream accounted for nearly

two-thirds of those appeal cases.

Appeals also holds in-person conferences, usually at an Appeals office.

Alternatively, under its conference policy as of August 2018, Appeals staff

can meet taxpayers in a mutually convenient location when the taxpayer,

representative, or business is beyond a certain distance from an Appeals

office.

35

In-person conferences may be used, among other things, for

reviews involving substantial books and records, judging the credibility of

witnesses, or accommodating with a taxpayer with a special need, such

as disability or hearing impairment. Based on our analysis of ACDS data

for appeal cases closed, about 6 percent of appeal cases that were

closed from fiscal year 2014 through 2017 had an in-person conference,

although this varied significantly by workstream. About half of the large

case examination appeals closed over the period had in-person

conferences, whereas about 3 percent of appeal cases closed in the

collection due process, innocent spouse, and penalty workstreams had

in-person conferences.

As of August 2018, Appeals had revised its policy on in-person

conferences twice since October 2016. Prior to that, campus appeal

cases were transferred to a field office when taxpayers requested a face-

to-face conference. For fiscal year 2017, Appeals limited in-person

conferences to appeal cases meeting specific criteria, such as involving

those with substantial books and records to review or where the taxpayer

has special needs that can only be accommodated with an in-person

conference. Appeals managers had final approval on granting taxpayer

requests for in-person conferences. In October 2017, Appeals further

revised its policy stating it would attempt to schedule in-person

conferences requested by taxpayers for field appeal cases at a time and

location reasonably convenient for both the taxpayer and Appeals.

Appeals stated it was intending to strike the right balance between

making in-person conferences available to taxpayers and ensuring the

process is efficient and workable for Appeals.

35

As of June 2018, Appeals officials said they had no staff presence in nine states:

Delaware, Idaho, Kansas, Montana, North Dakota, Rhode Island, South Dakota, Vermont,

and Wyoming. They also said Appeals had a small staff presence with three or fewer

employees in eight states: Alaska, Arkansas, Hawaii, Iowa, Maine, Mississippi, Nebraska,

and West Virginia.

Page 21 GAO-18-659 IRS Appeal Process

Appeals also offers virtual technology interaction to potentially allow more

taxpayers, especially those in remote locations, to have an option other

than a phone conference. Using IRS virtual service delivery capacity,

Appeals staff at campus locations can conduct virtual conferences with

taxpayers who schedule to use video terminals at some taxpayer

assistance centers. In August 2017, Appeals began piloting web-based

virtual conferences.

If taxpayers provide Appeals with new information or evidence, or raise a

new issue that requires additional investigation or analysis, Appeals will

return the case to the originating compliance unit for further review. After

a compliance unit transfers a case to Appeals, communication between

compliance staff and Appeals staff is generally restricted without the

taxpayer or representative being given an opportunity to participate.

In line with its mission to resolve cases prior to litigation, Appeals is

authorized to review the facts of the case considering the hazards that

would exist if the case were litigated.

36

Appeals is the only IRS unit

authorized to consider hazards of litigation when deciding whether to

allow taxes and penalties. This means that Appeals may recommend a

fair and impartial resolution somewhere between fully sustaining and fully

conceding the compliance unit’s proposal that reflects the probable result

in the event of litigation.

Appeals decision. Appeals makes a decision on a taxpayer’s case after

weighing evidence from the compliance unit and the taxpayer. Appeals

determines whether IRS compliance decisions correctly reflect the facts,

as well as applicable law, regulations, and IRS procedures. To resolve an

examination appeal case, Appeals may (1) agree with the IRS

examination compliance unit and fully sustain its recommended

assessment, (2) disagree and reduce the recommended assessment to

partially sustain the assessment, or (3) fully concede to the taxpayer’s

position and not sustain the assessment. To resolve a collection appeal

case, Appeals may (1) agree with and sustain the proposed enforcement

action, (2) disagree and modify the proposed action (e.g., propose an

installment agreement rather than a levy) or defer collection, or (3) fully

concede to the taxpayer’s position and not sustain the collection action.

36

26 C.F.R. § 601.106(f)(2). Hazards of litigation are a substantial uncertainty (1) as to

how the courts would interpret and apply the law, (2) about the court’s likely factual

findings, or (3) about the admissibility or weight that would be given to a specific item of

evidence. Hazards of litigation are not considered for collection cases.

Page 22 GAO-18-659 IRS Appeal Process

This is the final decision by Appeals. Once Appeals makes its decision, it

informs the taxpayer in writing and also IRS. Taxpayers dissatisfied with

Appeals’ decision may file a petition in tax court if they are eligible.

37

To handle the diverse array of taxpayer appeals across all workstreams,

IRS relies on an Appeals workforce that must have sufficient numbers of

staff with expertise in all areas of tax law. However, Appeals experienced

nearly a 9 percent annual attrition rate from fiscal year 2015 to fiscal year

2017 and projects a similar attrition rate for fiscal years 2018 and 2019.

As shown in figure 8, Appeals staffing levels have declined from 2,172 in

fiscal year 2010 to 1,345 in fiscal year 2017, nearly a 40 percent

decrease.

38

As previously noted, Appeals workload also decreased over

this period of time as IRS examination and collection enforcement activity

declined.

37

Certain appeal cases are not eligible to petition in tax court. For example, when IRS has

accepted a taxpayer’s offer in compromise, taxpayers waive their right to challenge the tax

debt in court.

38

Appeals reports the total number of Appeals employees in its Business Performance

Review, which is a quarterly review conducted by the IRS for each business unit that

reviews organizational performance, key initiatives, risks, budget, staffing and other

considerations. The number of employees can differ from a full-time equivalent (FTE)

measure. FTEs represent the total number of hours worked based on IRS payroll data

divided by the number of compensable hours applicable to each fiscal year.

Appeals Has Not

Conducted a Skills Gap

Analysis

Page 23 GAO-18-659 IRS Appeal Process

Figure 8: Appeals Staffing Levels, Fiscal Years 2010-2017

Appeals anticipates a continued risk of losing subject matter expertise

given that a large share of its workforce is eligible for retirement.

According to an Appeals report, at the end of fiscal year 2017, about

one-third of the Appeals workforce was eligible for retirement. Moreover,

Appeals officials reported that close to half of the staff who are critical to

Appeals’ mission—including those who handle the most complex

cases—were eligible for retirement. Based on our analysis of ACDS data

for appeal cases closed, these types of cases accounted for about

one-third of appeal cases closed in fiscal years 2014 through 2017.

Gaps in available staff with critical skills and training can result in delays

resolving appeal cases. For example, in fiscal year 2017 Appeals

received an increased number of innocent spouse appeals, and officials

told us they initially lacked sufficient numbers of trained staff ready to

review those cases. As of April 2018, the time from receipt by Appeals to

case closing for the innocent spouse workstream had increased by

39 percent over the same time period in 2017—from 205 days to

285 days. In response, Appeals was training additional staff and is

working to resolve the increased volume of cases.

Page 24 GAO-18-659 IRS Appeal Process

Appeals has taken action to mitigate the risk of having a sufficient number

of staff needed to handle its workload. Appeals has a tool that draws on

historical ACDS case data to project the number of Appeals staff needed

to review the numbers and types of case receipts expected from IRS

compliance units. From fiscal year 2014 through fiscal year 2017,

Appeals requested and received approval to hire 292 employees. In

November 2017, IRS changed its policy to allow business units funded

from IRS’s enforcement budget, including Appeals, to manage their own

staff levels in certain instances provided they do not exceed their fiscal

year staff limits. Under this policy, Appeals will be able to hire staff as its

workforce declines due to attrition. While the steps Appeals has taken can

be useful stopgap measures, they are not substitutes for nor do they

replace the longer-term benefits of strategic workforce planning and

conducting critical skills gap analysis.

We have identified that key principles of effective workforce planning

include that an agency must define the critical skills that it will need to

meet its strategic goals and achieve its mission in the future. An agency

must then develop strategies tailored to address staffing and skills gaps in

its workforce, including how to acquire, develop, and retain staff to meet

its goals.

39

We have previously reported that mission-critical skills gaps

within the federal workforce pose a high risk to the nation and that

individual agencies must take steps to address skills gaps.

40

We have

also reported on the need to close government-wide mission critical skills

gaps and to develop strategies to help agencies meet their missions in an

era of highly constrained resources.

41

Agencies that do not conduct a critical skills gap analysis risk significant

negative effects. We have previously reported that in a time of declining

resources, it is important for top management to take actions that ensure

the agency maintains capacity—including its workforce—in order to

39

GAO-04-39.

40

GAO-17-317.

41

Federal Workforce: OPM and Agencies need to Strengthen Efforts to Identify and Close

Mission-Critical Skills Gaps, GAO-15-223 (Washington, D.C.: Jan. 30, 2015), and Human

Capital: Strategies to Help Agencies Meet Their Missions in an Era of Highly Constrained

Resources, GAO-14-168 (Washington, D.C.: May 7, 2014).

Page 25 GAO-18-659 IRS Appeal Process

achieve its mission.

42

Once skill gaps are identified, strategies should be

tailored to address the gaps.

Appeals has identified knowledge loss and maintaining expertise during a

time of declining staff levels as one of its top risks in its Business

Performance Reviews. Although it has not conducted a skills gap

analysis, Appeals has identified that maintaining expertise in all areas of

tax law is essential because it must have staff trained to work a diverse

array of appeal cases across all workstreams. Many Appeals staff who

review appeal cases, including those who conduct in-person conferences,

are in the appeals officer job series critical to Appeals’ mission. As of July

2018, about 60 percent of the Appeals workforce was in this job series.

As of September 2018, Appeals is participating in a larger IRS effort to

address workforce planning. IRS states that its workforce planning is to

involve an integrated and systematic process for identifying current and

future human capital needs, the competencies that align with future

organizational goals, and the strategies to be implemented to reduce the

gaps.

43

Created in 2017, the IRS Workforce Planning Council is

comprised of representatives from all business units, including Appeals.

The council is to share workforce planning activities and best practices

across IRS and assist in developing the IRS strategic workforce plan. The

council is working to develop an agency-wide workforce plan, which will

include identifying gaps between current and projected workforce needs

and developing strategies to close the gaps.

According to IRS human capital officials responsible for workforce

planning, a service-wide strategic workforce planning effort will include

identifying skills and competency gaps in mission critical occupations.

Initially planned for the middle of fiscal year 2018, the initiative was

delayed as of September 2018, according to IRS human capital officials.

IRS units redirected resources to implementation of Public Law 115-97—

commonly referred to by the President and many administrative

documents as the Tax Cuts and Jobs Act—and requested an extension.

44

42

GAO, Declining Resources: Selected Agencies Took Steps to Minimize Effects on

Mission but Opportunities Exist for Additional Action, GAO-17-79 (Washington, D.C.: Dec.

20, 2016).

43

IRM Part 6, Chapter 250, Section 2.1.

44

To provide for reconciliation pursuant to titles II and V of the concurrent resolution on the

budget for fiscal year 2018, Pub. L. No. 115-97, 131 Stat. 2054 (Dec. 22, 2017).

Page 26 GAO-18-659 IRS Appeal Process

IRS human capital officials also told us the workforce planning team lost

resources due to attrition and anticipated the initiative would be complete

in the third quarter of fiscal year 2019. Appeals officials told us that they

expected to begin their activities once the IRS planning tools are in place.

While the broader Treasury and IRS initiatives will benefit Appeals with

longer-term strategic workforce planning, Appeals faces ongoing

challenges in achieving its goal and may be unable to mitigate the risk of

maintaining staff expertise. Gaps in the Appeals workforce could delay

the timely review of Appeals cases. The large share of its staff who are

critical to the mission who are eligible for retirement underscores the

importance of conducting critical skills gap analysis for Appeals. Given

Appeals’ unique role in ensuring taxpayers’ administrative option to

dispute most IRS decisions, it is important for Appeals to have the tax

expertise necessary to review appeals cases across multiple

workstreams. These factors underscore the importance of Appeals

conducting a skills gap analysis in coordination with Treasury and IRS

human capital efforts to ensure Appeals immediate skill needs are

reflected in broader agency planning.

Within the standard process that all appeal cases follow, Appeals has

developed a series of process measures that use ACDS data to monitor

the amount of time for a case to move through an Appeals workstream.

These measures track the number of days from Appeals receipt through

the appeal review process to when a case is closed in ACDS. Appeals

also measures the amount of time for compliance units to transfer

appeals cases. For the purpose of this report, total appeal resolution time

IRS Does Not Monitor

Timeliness of

Transfers of All

Incoming Appeal

Requests and

Appeals Does Not

Communicate Total

Resolution Times to

Taxpayers

Appeals Has a Data-

Driven Process and

Measures to Track and

Manage Case

Workstreams

Page 27 GAO-18-659 IRS Appeal Process

is the length of time from when a taxpayer submitted the appeal request

to IRS to when the case is closed in ACDS.

Appeals managers use ACDS to monitor progress staff have made

reviewing each case assigned to them, including holding a conference

with the taxpayer and reaching a decision to resolve the appeal. ACDS

inventory reports allow managers to monitor total employee time per case

and determine if a case has not had any activity recorded for 60 days.

Appeals officials explained that the process measures are indicators that

assist in making management decisions and identifying data driven

process efficiencies to control workflow within each workstream. For

example, an Appeals manager may use the ACDS data to address case

review backlogs and offer assistance to help expedite case review.

Appeals reports its review time measure by workstream in its monthly

performance report to the Commissioner of Internal Revenue.

The IRS website states that if a taxpayer has not heard from Appeals and

it has been more than 120 days since the request was submitted, the

taxpayer should contact the IRS office to which they sent their appeal

request. According to IRS examination and collection officials we

interviewed, compliance unit staff attempt to resolve all taxpayer requests

and work with taxpayers to obtain additional information if needed and

answer questions about pending compliance actions. According to

Appeals officials, there are different levels of case complexity across the

workstreams.

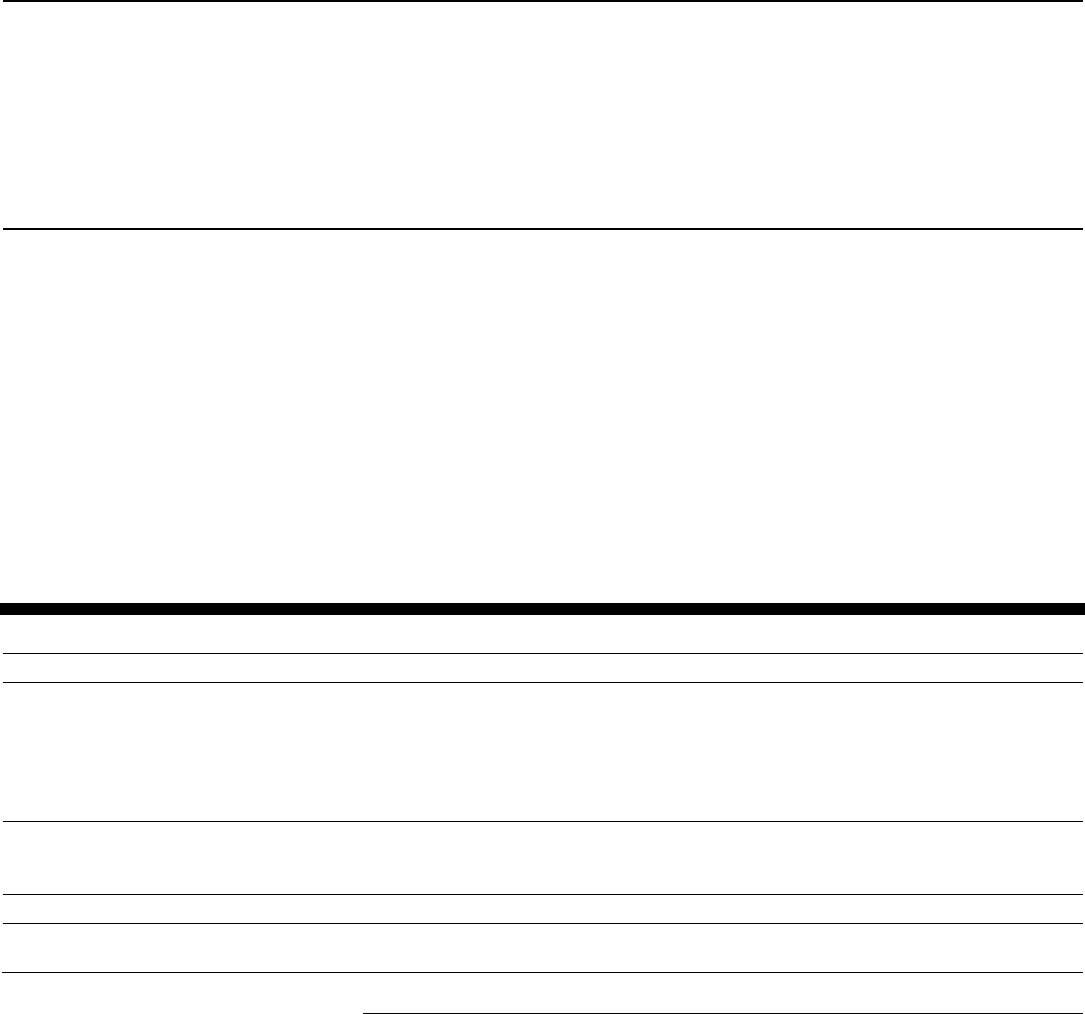

For appeal cases closed from fiscal years 2014 through 2017, table 2

shows the average number of days from when IRS received a taxpayer

appeal to when the compliance unit completed its review and transferred

the case file to Appeals. Across the appeals workstreams, the compliance

review time varied from 30 days for innocent spouse appeals to 108 days

for large case examination appeals. Any delay during compliance review

adds to the total time to resolve an appeal. As shown in table 2,

compliance review accounted for about a quarter of the total resolution

time for collection appeals. Among the examination workstreams, the

compliance review share of total resolution time ranged from 12 percent

for innocent spouse appeals to about 45 percent for penalty appeals.

IRS Does Not Always

Transfer Collection

Appeals on a Timely Basis

and Does Not Monitor

Incoming Examination

Appeals or Time to

Transfer to Appeals

Page 28 GAO-18-659 IRS Appeal Process

Table 2: Average Days for Compliance Review and Share of Total Appeal Resolution Time for Appeal Cases Closed, Fiscal

Years 2014-2017

Workstream

Number of appeal

cases

Average number of days

Compliance share of

total appeal resolution

time

Compliance review and

transfer to Appeals

Total appeal

resolution time

Collection workstreams

•

Collection due process

a

158,057

59

252

23%

•

Offer in compromise

b

36,837

61

240

26%

Examination workstreams

•

Large case examination

3,802

108

637

17%

•

Examination

48,460

105

337

31%

•

Penalty appeals

39,711

100

220

45%

•

Innocent spouse

10,747

30

249

12%

Other

48,424

39

101

38%

Source: GAO analysis of Appeals Centralized Data System data. I GAO-18-659

Note: The average number of days varied from the median number of days, suggesting that outliers

increased the average review time.

a

A collection case where a taxpayer appeals an IRS filing of notice of federal tax lien or proposed levy

of wages or assets.

b

A collection case where a taxpayer appeals IRS rejection of the taxpayer’s offer to settle a tax liability

for less than the full amount owed.

According to the IRM, IRS requires SB/SE collection units to review

collection due process appeals within a 45 day period of receipt of the

taxpayer requests.

45

The 45 calendar days after receipt of an appeal

request includes time to ensure completeness of the request, obtain

additional information if necessary, and transfer the request to Appeals.

Collection unit staff reviewing appeal requests may experience delays

with taxpayers submitting additional material to support their requests.

With management approval, collection units may have an additional

45 days to continue working with the taxpayer to resolve the collection

issue in dispute. The IRM time requirement does not specifically apply to

offer in compromise collection appeals.

According to our analysis of ACDS data for appeals closed in fiscal years

2014 to 2017, the majority of collection due process appeals were

transferred within the IRM time requirements. In fiscal year 2017,

approximately 57 percent of collections due process appeals were

45

IRM Part 5, Chapter 1, Section 9.

Collection Appeals

Page 29 GAO-18-659 IRS Appeal Process

transferred in less than 45 days and approximately 93 percent of these

cases were transferred within 90 days. However, IRS did not always

transfer collection due process appeals in a timely manner. For collection

due process appeal cases closed in fiscal year 2017, approximately

4 percent (1,559) of these collection appeals took more than 120 days to

be transferred to Appeals (see fig. 9).

Figure 9: Average IRS Collection Case Transfer Time to Office of Appeals for Appeal Cases Closed, Fiscal Years 2014-2017

Note: Appeal cases closed by Appeals in a fiscal year may have been transferred from compliance

units in prior fiscal years. The average number of days varied from the median number of days,

suggesting that outliers increased the average review time. Percentages may not total to 100 due to

rounding.

Page 30 GAO-18-659 IRS Appeal Process

As shown in figure 9, the majority of offer in compromise collection

appeals were also transferred within 90 days, even though the IRM time

requirement applies specifically for collection due process appeals.

Approximately 11 percent (995) of these collection appeals took more

than 120 days to be transferred to Appeals in fiscal year 2017.

Delays in transferring collection due process appeals, in turn, affect

prompt resolution for the taxpayer and IRS. Each tax assessment has a

collection statute expiration date of 10 years after the assessment. When

a taxpayer appeals a collection action within 30 days of receiving the

notice, IRS suspends further collection activity until Appeals decides the

case. When the IRS suspends the collection statute for a period longer

than its policy allows, this means that the taxpayer can face a longer

period where IRS can collect the balance owed.

Standards for Internal Control in the Federal Government states that

management should establish and operate monitoring activities to monitor

internal controls. Management should evaluate the results and remediate

any identified deficiencies.

46

SB/SE collection tracks the number of collection due process appeals that

are not transferred to Appeals within 45 days of receipt from the taxpayer.

SB/SE collection officials told us that they do not have reports or tools to

systematically track transfer times for other types of collection appeals.

Although SB/SE has the capacity to identify how long collection due

process appeals have been waiting, collection officials we interviewed

acknowledged that they do not always monitor whether they are meeting

the transfer time requirement. For non-docketed cases closed in fiscal

year 2017, the deficiency in transferring nearly 1,600 collection due

process appeals more than 120 days after receipt points to the lack of

monitoring. Evaluating the existing tracking reports for collection due

process appeals and remediating deficiencies in collection staff following

procedures would be a key step to achieve timely transfer of these

collection appeals.

Unlike the requirements for collection due process cases, the IRM does

not establish timeframes for compliance review and transfer of taxpayer

appeals of examination disputes. According to Appeals officials,

examination cases can have many issues, and the level of review to try to

46

GAO-14-704G.

Examination Appeals

Page 31 GAO-18-659 IRS Appeal Process

resolve examination issues can be significant prior to the taxpayer appeal

request being transferred to Appeals. Review procedures differ across the

business operating divisions.

In its examination quality standards, SB/SE field examination has national

standard timeframes, which include 20 days from the receipt of a

taxpayer appeal request to close the examination case and then 10 days

for SB/SE technical services to transfer the file to Appeals. IRS officials

acknowledged that SB/SE field does not always meet its 30-day

timeframe standard for appeal transfers, in part, because examiners must

review any new information submitted with a taxpayer’s appeal request.

Our analysis of ACDS data showed that about two-thirds of all

examination appeals closed in fiscal years 2014 through 2017 had been

transferred from IRS examination compliance units within 90 days.

However, nearly a quarter of examination appeals took more than

120 days to be transferred to Appeals (see fig. 10).

Page 32 GAO-18-659 IRS Appeal Process

Figure 10: Average IRS Examination Case Transfer Time to Office of Appeals for

Appeals Cases Closed, Fiscal Years 2014-2017

Note: Appeal cases closed by Appeals in a fiscal year may have been transferred from compliance

units in prior fiscal years. The average number of days varied from the median number of days,

suggesting that outliers increased the average review time. Percentages may not total to 100 due to

rounding.

As shown in figure 11, transfer times for examination appeals varied

across IRS examination compliance units. For appeal cases closed in

fiscal year 2017, more than two-thirds of examination appeals originating

in SB/SE and LB&I were transferred by those units within 90 days. For

examination appeals originating in W&I, less than half were transferred

within 90 days, and 37 percent took more than 120 days to transfer.

TE/GE transferred fewer appeals than the other units, but nearly half of

TE/GE appeals took more than 120 days to be transferred to Appeals.

47

47

IRM Part 4, Chapter 75, Section 17 requires mandatory review of all exempt

organization cases before transfer to Appeals.

Page 33 GAO-18-659 IRS Appeal Process

Figure 11: Average Examination Case Transfer Time from IRS Business Operating

Divisions to Office of Appeals, Fiscal Year 2017

Note: Appeal cases closed in a fiscal year by Appeals may have been transferred from compliance

units in prior fiscal years. The average number of days varied from the median number of days,

suggesting that outliers increased the average review time. Percentages may not total to 100 due to

rounding. Small Business/Self-Employed (SB/SE) transfers included appeal cases in the examination,