Cook County Board of Review Annual Report 2022 1

2022

COOK COUNTY

BOARD OF REVIEW

Commissioner Larry R. Rogers, Jr.

Commissioner Tammy Wendt

Commissioner Michael M. Cabonargi

ANNUAL REPORT

ASSESSMENT YEAR 2021

FISCAL YEAR 2022

AN INDEPENDENT OFFICE

PROVIDING FAIRNESS

FOR

COOK COUNTY PROPERTY TAXPAYERS

Cook County Board of Review Annual Report 2022 2

1

3

2

Chicago

Orland Park

Palatine

Glenview

Schaumburg

Skokie

Alsip

Des Plaines

Niles

Northbrook

Barrington Hills

Tinley Park

Hoffman Estates

Elgin

Matteson

Arlington Heights

Lansing

Wheeling

Cicero

Lemont

Oak Lawn

Harvey

Evanston

Dolton

Inverness

Elk Grove Village

Park Ridge

Chicago Heights

Bartlett

Streamwood

Wilmette

Markham

Calumet City

Lynwood

South Holland

Oak Forest

Burbank

Homewood

Glencoe

Hillside

Winnetka

Palos Hills

Riverdale

Worth

Morton Grove

Justice

Lyons

Northfield

Bedford Park

Steger

Mc Cook

Summit

Barrington

Bellwood

Lincolnwood

Burnham

Mount Prospect

Berwyn

Oak Park

South Barrington

Franklin Park

Bridgeview

Blue Island

Flossmoor

Rolling Meadows

Park Forest

Northlake

Melrose Park

Glenwood

Sauk Village

Richton Park

Westchester

Brookfield

Palos Heights

Crestwood

Midlothian

Hazel Crest

Country Club Hills

Maywood

Willow Springs

Hodgkins

Thornton

Prospect Heights

Burr Ridge

Countryside

Stickney

La Grange

Hickory Hills

Palos Park

Riverside

Forest Park

Schiller Park

Evergreen Park

Norridge

River Forest

Olympia Fields

River Grove

Hanover Park

Posen

Rosemont

Broadview

Western Springs

Robbins

Buffalo Grove

Chicago Ridge

Berkeley

Ford Heights

La Grange Park

Dixmoor

Elmwood Park

North Riverside

Golf

Roselle

Orland Hills

Calumet Park

South Chicago Heights

Hinsdale

Forest View

Deerfield

Kenilworth

Indian Head Park

Phoenix

Harwood Heights

East Hazel Crest

Hometown

Stone Park

Frankfort

Merrionette Park

East Dundee

Bensenville

University Park

Elmhurst

Deer Park

Oak Brook

Homer Glen

Cicero

Harlem

Tri-State

95th

87th

Golf

Archer

Sauk

1st

Kedzie

159th

Wolf

167th

Rand

Touhy

I 290

Northwest

Oakton

Edens

Ogden

Milwaukee

Higgins

Torrence

La Grange

Palatine

111th

127th

Western

Kennedy

Euclid

Devon

Dixie

Roosevelt

103rd

135th

Lake Cook

147th

Ela

Cermak

Irving Park

Ashland

47th

Leg Dan Ryan

25th

5th

Eisenhower

Lake Shore

Elston

Roselle

143rd

Willow

31st

Mannheim

Lake

175th

Dan Ryan

River

104th

Adlai Stevenson

Bartlett

Dempster

Joliet

C

entral

183rd

Barrington

Halsted

Sheridan

Moline

Foster

80th

115th

Waukegan

Vollmer

Chicago

State

Michigan

55th

123rd

Bishop Ford

Lee

231st

Calumet

Hintz

Sibley

108th

Joe Orr

107th

Wood

Main

Schaumburg

Bell

Ridgeland

Bode

Penny

Roberts

88th

Grand

Skokie

Pulaski

Otis

Quentin

84th

26th

94th

California

Glenview

Oak Park

Arlington Heights

Meacham

Talcott

170th

Church

63rd

17th

138th

Washington

130th

119th

Lincoln

179th

Addison

Sanders

Morgan

Pratt

Techny

Busse

Pfin

gsten

Wise

76th

Flossmoor

Will Cook

Caldwell

Sutton

162nd

86th

Steger

Elmhurst

Peterson

Garfield

Nerge

Hibbard

Wentworth

Shermer

Cottage Grove

Cumberland

Tower

Doctor Martin Luther King Jr

Wilke

Stony Island

Hill

Diversey

82nd

Nagle

Clybourn

Bateman

Ridge

Kingery

Kensington

Augusta

Mc Cormick

Lawrence

Belmont

College

Shoe Factory

Dundee

Southwest

Edens Expy

Montrose

Landwehr

New

West

Ballard

Walters

79th

Pershing

Franklin

Colfax

South Chicago

Howar

d

Lehigh

Asbury

Jackson

Il 171

Crawford

Calumet Sag

100th

106th

Plainfield

North

Midlothian

Des Plaines River

Wagner

Green Bay

Glenwood-Dyer

Hicks

Summit

La Salle

Sunset Ridge

Brainard

Taft

Canal

Hawthorne

Schoenbeck

139th

Bradwell

Gifford

Columbus

Greenwood

Harms

Winnetka

142nd

River Oaks

Plum Grove

Us 20

Landmeier

171st

65th

Old Sutton

Vincennes

Center

Drexel

Happ

Jeffery

51st

Burnham

Dolton

Canfield

I 57

Thacker

151st

Cork

Donlea

South Shore

131st

I

90

Ewing

Cornell

Freeman

Smith

West Lake

Walker

91st

Randolph

Rogers

Kimball

Avondale

Park

Congdon

Kean

Clark

County Line

Algonquin

Fullerton

German Church

Huntington

Weber

Rohlwing

Riegel

Elgin

39th

Harts

Noble

150th

Indiana

Oakwood

Springinsguth

Broadway

177th

Narragansett

South

North

Hicks

Ela

Central

Lincoln

47th

Lincoln

115th

Lincoln

Ridgeland

State

127th

Wolf

Ashland

Central

Central

Dempster

Kedzie

111th

135th

Southwest

Busse

Stony Island

Chicago

Ke

dzie

Central

Central

Central

Sutton

Archer

West Lake

Cermak

Augusta

Dundee

Crawford

State

Wolf

Pershing

Grand

Algonquin

80th

Wolf

Addison

Central

123rd

31st

Chicago

Halsted

Western

151st

26th

Ridgeland

Lehigh

79th

Higgins

Ashland

Lincoln

Kean

183rd

Skokie

Burnham

151st

Northwest

Devon

Higgins

231st

Tri-State

115th

Golf

Pulaski

Lawrence

Grand

76th

Steger

Central

River

Lake

131st

131st

Wolf

Foster

Elmhurst

Irving Park

State

Sheridan

State

Plum Grove

Western

104t

h

Main

Crawford

Lake

Bartlett

Central

State

103rd

Board of Review Districts 2012

Cook County, IL

1 - Dan Patlak

2 - Michael Cabonargi

3 - Larry R. Rogers, Jr.

BOARD OF REVIEW DISTRICTS

COOK COUNTY, IL

BOARD OF REVIEW DISTRICTS

COOK COUNTY, IL

Tammy Wendt

Michael Cabonargi

Larry R. Rogers, Jr.

1

1

2

2

3

3

Cook County Board of Review Annual Report 2022 3

TABLE OF CONTENTS

COOK COUNTY

BOARD OF REVIEW

RESPONSIBILITIES

OFFICE

WHY DOES IT

MATTER TO COOK

COUNTY RESIDENTS

IF THE TAX BILLS GO

OUT ON TIME?

COOK COUNTY BOARD OF REVIEW

RESPONSIBILITIES

LETTER FROM COOK COUNTY

BOARD OF REVIEW

DIGITAL ASSESSMENT PROCESSING

SYSTEM

BUDGET HIGHLIGHTS

EMPLOYEES AND APPEALS

OPERATIONAL HIGHLIGHTS

APPEALS RESULTING IN REDUCTIONS

ASSESSMENT YEARS 2008 2021

PTAB APPEALS

EXEMPT PROPERTIES AND THE BOR

2021 TAX YEAR OUTREACH EFFORTS

When the tax bills are delayed, schools, libraries

and other essential district services are forced into

budget gaps. To fill those gaps, reserves may be

tapped, which means that money is not earning

interest, or, money is borrowed, and loan costs

and interest fees are incurred at the cost of the

taxpayer. The cost to local government can be in

the MILLIONS OF DOLLARS.

The Cook County Board of Review (formerly the Board of Tax Appeals)

was created by the 89th General Assembly in 1998 under statutory

changes that established a three-member Board of Commissioners

elected from three electoral districts.

The Cook County Board of Review (hereinafter “BOR”) is vested

with quasi-judicial power to adjudicate taxpayer complaints and

recommend exempt status of real property, which includes residential,

commercial, industrial, condominium property, and vacant land.

Responsibilities of the BOR include the following:

1. Order the Assessor to revise and correct the assessed

value of property;

2. Review Certificates of Error;

3. Correct factual mistakes;

4. Recommend property for tax exempt status; and

5. Defend assessment decisions for properties appealed at

the Illinois Property Tax Appeal Board (PTAB).

The BOR deals only with assessed valuations before equalization, not

with the tax rate or the amount of the tax bill.

County Building

118 N. Clark St., Room 601

Chicago, IL 60602

Ph: 312/603-5542

www.cookcountyboardofreview.com

1

1

1

1

1

1

1

1

1

1

Cook County Board of Review Annual Report 2022 4

Your Cook County Board of Review Continues to Rise to the Challenge

The 2021 Assessment appeal year was one of the most challenging in the history of the Board of Review. The Board

of Review received the first re-assessed townships in February 2022, seven months late, from the Cook County

Assessor’s Oce. To mitigate the detrimental impact this delay would have on taxpayers, our oce maximized

eciency and our sta worked 22,974 overtime hours to allow tax bills to be payable before the year end. This “all

hands-on deck” approach is demonstrative of the Board of Review’s commitment to ensuring that taxpayers have an

opportunity to have their appeals heard so that the Assessor’s errors can be corrected. This ensures that taxpayers

pay no more than their fair share of property taxes and allows taxpayers to avail themselves of mortgage interest

deduction tax advantages.

We continued to support that mission by conducting over 150 community outreach seminars countywide. At these

outreach seminars the Board of Review brought its services directly into communities to educate property owners

on the property tax system and how to ensure when taxpayers appealed, Assessor errors could be corrected before

tax bills were issued. Also, while our analysts were working overtime on Board of Review appeals, the Property

Tax Appeal Board (PTAB) appeals continued to send prior year files for the Board of Review to defend before its

agency. Fortunately, under the leadership of the Commissioners, the Board’s PTAB Defense Unit – created in 2017

– continued to defend the budgets of school districts and other local taxing bodies from unnecessary refunds.

This PTAB Defense Unit consists of dedicated sta assigned to prepare evidence and represent the county at PTAB

hearings where taxpayers who overpaid property taxes based upon Assessor errors in their assessments, seek

refunds from the county and other taxing districts. With a half billion dollars of refunds requested through appeals

at PTAB, preparing evidence and representing the taxing districts at PTAB for those cases is a major responsibility of

the Board of Review. Eliminating or mitigating exposure through reduced refunds at PTAB has a large impact on the

budgets of all the taxing districts in Cook County, including the County’s budget itself. The taxpayers of every school

district, city, and the whole County benefit from these savings and the Board’s PTAB defense work.

The Commissioners are pleased to report the Board of Review finished adjudicating 248,899 appeals. Once again,

in anticipation that our appeal volume would rise due to increased assessments across the County, we opened the

Board on July 6, 2021. Opening the Board earlier allows us the additional time needed to do our part to get tax bills

out on time. Unfortunately, because the Assessor’s Oce was late certifying townships and transferring them to our

oce, the Board was not able to begin its work until February 2022 due to data integrity issues from the Assessor’s

December 2021 township transmittal. Most significantly, the Board received 71% of its work from March 24, 2022, to

April 23, 2022. The Assessor’s delay in the transmission of townships to the Board coupled with the Board receiving

71% of the volume between March and April 2022 placed immense pressure on the Board of Review and other

property tax stakeholders. However, the Board fulfilled its commitment to use all resources to complete its work

and successfully finished its session at the beginning of October. It is important to note the dedication of the sta

at the Board of Review. To achieve the October completion, many sta members were working seven days/ fifty-

sixty hours a week to ensure the Board was successful and tax bill were payable in 2022. We cannot thank the sta

enough for the dedication, professionalism, and sacrifice they showed to get the job done in the most challenging

circumstances.

Summary

Every session brings dierent challenges. However, despite these challenges, the Board was able to complete its session by late April for the prior

decade to ensure tax bills were payable by August 1st. However, under this Assessor, this 2021 session brought unique challenges due to the Cook

County Assessor’s failure to timely transmit townships to the Board of Review and the unsupported exponential increases in values of residential

and commercial properties. By receiving the initial townships five months late and then having data integrity delays, the Board of Review began this

session under the most challenging circumstances. In spite of the Assessor’s failure to timely complete his assessments of Cook County properties

and transmit townships those assessments to the Board of Review, the Commissioners and sta were committed to complete our work and ensure

that the property tax bill delay caused by the Assessor did not ultimately impact taxpayers beyond their property tax liability. We achieved our goal

and successfully completed the session while defending PTAB and executing our other duties.

2021 ASSESSMENT YEAR ANNUAL

REPORT LETTER FROM COMMISSIONERS

TAMMY WENDT

COMMISSIONER

LARRY

ROGERS JR.

COMMISSIONER

MICHAEL

CABONARGI

COMMISSIONER

Cook County Board of Review Annual Report 2022 5

• The Assessor failed to implement its “future state” Tyler modules in “parallel” with the fully functioning “legacy” Cook County Property Tax

mainframe as required by the 2015 Tyler contract

1

, recommended by Cook County Bureau of Technology

2

and contrary to industry “best practices.”

• The Cook County Assessor failed to initially transmit “Building Permit” assessment data for 20 of the 38 townships after certifying and

transmitting the data to the Cook County Board of Review. This failure to transmit the bulding permit data directly impacted key

characteristics of properties, such as the age and size of many residential improvements situated in Cook County.

• The Cook County Assessor changed “detail” data of parcels after it no longer posessed jurisdiction over parcels and had already certified and

transmitted the townships to the Cook County Board of Review. The changes made to the data by the Cook County Assessor after it no longer

possesses jurisdiction, included “occupancy” factors, “building permit” data and related characteristics data. Per statute, if the Cook County

Assessor discovers a “mistake” or “error” other than a “mistake or error of judgment post certification and transmission of the assessment roll

data to the Cook County Board of Review, the only remedy available to the Cook County Assessor is the “Certificate of Correction.” See 35 ILCS

200/14-10 (2022). In addition, “an internal Cook County Assessor policy document described the justification for a “Certificate of Correction”

as to correct “an error due to keypunch, or factual error, and the B/R is still open for that specific town, a Certificate of Correction can be used

to correct the problem even if an appeal has not been filed at the Board.”

3

• The noted “detail data” issues plagued the entire Cook County Board of Review 2021 tax session due to the obvious uncertainty and lack of

confidence in the accuracy of the Cook County Assessor data which directly impacted the Cook County Board of Review’s valuation processes.

Also, on occasion, the data would change in between the first and second reviews of the file causing the entire file to need to be reset to achieve

consistent data for all analysts to use on any given property.

THE COOK COUNTY ASSESSOR’S

IMPLEMENTATION OF THE TYLER

PROJECT DELAYED THE 2021 TAX YEAR

2ND INSTALLMENT TAX BILLS

The Cook County Boar

d of Review opened the 2021 tax year Appeal session on July 6, 2021. Unfortunately, because the Assessor had not

completed and transmitted his assessment of any Cook County properties until December 2021 and the 1st City of Chicago township until February

2022, there was an unprecedented delay which drastically affected the schedule for all property tax stakeholders. The Assessor’s delay resulted in

the Cook County Board of Review not finalizing its work until 466 days later on or about October 9, 2022. During the 2021 Session, the Cook County

Board of Review adjudicated 248,899 complaints that comprised 537,618 parcels (“PINs”), all of which alleged errors in the assessment of their

properties. The 2021 tax year session included a 12% increase in Commercial complaints when compared to the last reassessment of the City of

Chicago for the 2018 tax year. The unsupported substantial increases in Commercial/Industrial assessments by the Assessor, (particularly, during a

global pandemic) that ranged from 33% in Hyde Park township to 115% in West Chicago township this significant increase and nearly 9,000 hearing

requests for reassessed City of Chicago properties. However, the fact that the 2021 session spanned 466 days can be traced back to the Assessor’s

decision not to implement its Tyler application pursuant to the 2015 IPTS contract, recommendation of the Bureau of Technology, and industry

“best practices.” 2021 implementation of its Tyler application caused significant data integration and integrity issues for the Board due to its

dependency on Assessor assessment roll data. Despite the Board’s July 6, 2021, opening, it did not receive the first townships from the Assessor

until December 2021 and due to the aforementioned data integrity issue, analytical work did not commence until February of 2022. The first

hearings began March 21, 2022. In addition, from March 24th to April 23rd , the Assessor transmitted 1,323,581 of the total 1.863,980 parcels

situated in Cook County or 71% of the Board’s total workload. Thus, backloading the Board ‘s schedule with the highest number of parcels, as well

as, presenting the Board with the City reassessment and its complex valuation issues.

It is important to note that the delayed finalization of the Board’s 2021 tax year session, caused by the Assessor’s failure to timely transmit townships

to the Board, also delayed the timely distribution of over $16 billion in real estate tax revenue to Cook County cities, towns, villages as well as

fire, police, library and school districts. Another impact of the Assessor’s delay was that some taxing bodies were forced to seek “tax anticipation

notes.” In addition, a number of taxing bodies have bond payments due December 2022; therefore, without distribution in December, the noted

payments would potentially be “late.” Also, this ‘timeliness” issue presented a critical potential federal income tax issue for all Cook County residents.

Specifically, if the 2021 tax bills are not paid in the 2022 calendar year, taxpayers could forfeit taking a deduction for their federal income tax filings

for “settled” state and local taxes, costing residents thousands of dollars in deductions.

Causes for and the Impact of the Delayed 2021 2nd Installment Tax Bill

1

2015 Cook County Bureau of Technology and Tyler Technologies, inc. (Contract No. 1490-13787)(4.11 “Go-Live and Rollout Support.”)

2

Finance and Technology and Innovation Committees Joint Meeting, April 25, 2022.

3

Oce of the Independent Inspector General, Quarterly Report, 3rd Quarter 2022 (October 14, 2022).

Cook County Board of Review Annual Report 2022 6

• The PTAB and Circuit Court refund exposure will directly increase due to the delayed distribution of over $16 billion in real estate tax revenue,

the additional stang resources demanded of all members of the Cook County Property Tax Group (Cook County Assessor, Cook County

Board of Review, Clerk and Treasurer) and Cook County Bureau of Technology which also includes overtime compensation, the probable

increased Cook County Board of Review “error rate” due to the expedited and compressed 2021 schedule and combined with the substantial

2021 Cook County Assessor.

• For City of Chicago condominium properties, the Cook County Assessor failed to comply with the Illinois Condominium Property Act which

requires the Cook County Assessor to assess condominiums while applying the “owner’s corresponding percentage of ownership in the

common elements as a tract, and not upon the property as a whole.” (765 ILCS 605/10a)(2022). The Cook County Assessor’s failure to

comply with the Illinois Condominium Property Act directly resulted in inconsistent underlying market values or “reproduction cost” values

when, per the “Condo Act,” there should be one (“1) underlying market for the entire building with each individual unit prorated or assessed per

its ownership interest.

» In some instances, it appears that the percentage of interest (POI) values, as established in the subject’s Condo Declaration, were not used

to allocate the fair market value (FMV) when tcondominiums were re-assessed.

» The reproduction cost issue presented significant valuation issues at the Cook County Board of Review which included forcing condo

analysts to manually enter reproduction costs line by line for multiple PIN condo complaints which can range from 6 to over 1,000 lines.

This additional manual work directly impacted Condo analysis workflow.

» The Cook County Board of Review addressed the reproduction cost issue by continuing to apply its historical valuation methodology for

residential condominiums based on recent sales and their corresponding POI in the building when establishing the overall FMV.

» In addition, in the interest of equity and to ensure the accurate allocation of the FMV for the subject, the Cook County Board of Review also

continued its practice of using the POI for each unit as established by the subject’s Condo Declaration.

» Due to theoccasional varying Reproduction Costs found in the same building, the Cook County Board of Review’s methodology of relying

on the POI when allocating the FMV may have resulted in assessment decreases for some units and assessment increases for other units

within the subject building while maintaining the underlying FMV.

» To ensure the equitable allocation of the FMV, and not compound the Reproduction Cost errorscaused by the Cook County Assessor,

the Cook County Board of Review may have issued increases, when deemed appropriate, to accurately allocate the FMV throughout the

building based on the per unit POI as established in the Condo Declaration.

› This enabled the Cook County Board of Review to reach its two primary goals when valuing condominiums;

› Established an accurate overall FMV with a singular reproduction cost for the entire condominium building; and

› Equitably allocated that FMV for the subject based on individual unit’s percentage of interest as established in the Condo Declaration.

» Cook County Board of Review Reproduction Cost “Repro” Condo Tool

› In addition, the Cook County Board of Review committed considerable IT, Administrative, and Analytical resources to develop, test, and

implement a valuation application to assist the Cook County Board of Review to fairly and accurately value Condo properties based on

the sales evidence and more importantly, pursuant to the Condo Act.

› This Excel based application considers a “Target Market” value determined by the analyst based on the sales approach. The “Target

Market Value,” determines whether the individual “reproduction costs” are either a “decrease” or “increase.”

• Backloading of the Cook County Board of Review Schedule

» The Cook County Assessor transmitted 71% of the parcel volume to the Cook County Board of Review from March 24th to April 23rd

2022. See Cook County Assessor 2021 Tax Year Publication Dates Townships (18) and related Parcel volume (1,323,581) (71% of all Cook

County parcels) (1,863,980))

› In sum, in a 30-day time span, the Cook County

Board of Review assumed jurisdiction over 71% of all

parcels situated in Cook County.

» The Re-assessment of the City of Chicago represented

over 52% of the 1.8M plus parcels located in Cook

County.

› Seven (7) City Triennial Townships represented

858,884 total parcels.

2021 CCAO Filing Volume versus 2021 CCBOR Filing Volume

Group 1

5,868 vs 8,541 (+46%)

Group 2 2,437 vs 4,423 (+81%)

Group 3 11,592 vs 18,787 (+62%)

Group 4 23,273 vs 26,977 (+16%)

Group 5 9,490 vs 16,480 (+71%)

Group 6 6,510 vs 10,937 (+67.5%)

Group 7 18,683 vs 27,170 (+45%)

Group 8 26,967 vs 40,175 (+49%)

Group 9 24,123 vs 39,772 (+64%)

Group 10 40,512 vs 55,147 (+36%)

TOTAL 169,455 vs 248,899 (+47%)

Cook County Board of Review Annual Report 2022 7

THE COOK COUNTY BOARD OF

REVIEW’S ROLE IN THE IPTS PROJECT

Background

The 2015 assessment appeal year (2015-16) marked the culmination of four (4) years of preparation a re-engineering of the Cook County Board

of Review’s (hereinafter “Board”) operations from a 100% paper-based process to a 100% digital workflow. Against the background of significant

increases in appeals volume, the 2015 session marked a monumental advance in eciency at the Board, leading the way in County government

with the launch its “enterprise content management” (“ECM”) application, Digital Appeals Processing System (hereinafter “DAPS”) which leverages

OnBase software. It should be noted that the Board went live with DAPS during the reassessment of the City of Chicago which, at that time, yielded

a historical number of complaints filed at the Board.

DAPS provided the Board an unprecedented ability to track and process complaints; achieve greater transparency; enhance the access and ease of

use for taxpayers; improve overall management; and save over two million pieces of paper.

In addition, DAPS allowed taxpayers to electronically to submit evidence via its portal instead of in person or via the mail. The complaints and

related valuation evidence is accessible by the taxpayer via the DAPS portal.

This historic change in the appeals processing system was a blueprint that captures how to make significant changes in a cost-eective manner in a

relatively short period of time. With the streamlined system in place, the Board adjudicated a then record number of complaints without increasing

sta and timely finalizing its session which allowed a July mailing of the 2nd Installment tax bill. The July mailing of the 2nd Installment tax bill

assures an uninterrupted revenue stream for local education, police and fire protection and multiple other local services and projects.

The Cook County Board of Review’s analytical workflow is NOT a mainframe process

The Cook County Board of Review’s analytical workflow has never been a mainframe-based process, however, it does solely depend upon

mainframe assessment roll data created and transmitted by the Assessor. More importantly, the frequent inquiries regarding “when is the Board

of Review transitioning o the mainframe” are grossly misplaced. Particularly, when the Cook County Board of Review modernized its analytical

processes in 2015 which the Assessor has yet to achieve at this time.

No Cook County Board of Review specific software modules in the 2015 IPTS contract

Due the Cook County Board of Review’s successful implementation of its future state application, the Digital Appeals Processing System (“DAPS”),

Tyler was not contracted to develop and implement any software modules exclusively for the Cook County Board of Review. Specifically, Tyler was

contracted to provide the following modules

4

:

Tyler Solution and Specific Software Fuctionality Required by Cook County

Tyler shall provide, install, configure and customize the Tyler Solution (software) as necessary to meet the County’s Property Tax needs. Tyler shall

provide at least the following software modules to meed the County’s requirements:

1. CAMA;

2. Exemptions;

3. Tax Billing and Collection;

4. Inquiry and Appeals;

5. Field Mobile;

6. E-file;

7. Public Access;

8. Cashiering;

9. Content Management;

10. Analyze;

11. Activity Center;

It is important to note that in the 2015 IPTS contract Tyler acknowledged that the Cook County Board of Review and Assessor appeals processes are

separate and distinct, stating the following:

5

• The Board of Review (Cook County Board of Review) appeals process is currently being automated via Hyland OnBase Software. This is not

the same as the Assessor’s Appeals process or 2nd pass. Tyler shall automate the Assessor’s Appeals process, or 2nd pass. Tyler shall build the

appropriate interfaces to the Cook County Board of Review OnBase implementation.

4

2015 Cook County Bureau of Technology and Tyler Technologies, inc. (Contract No. 1490-13787 (3.3 “Tyler Solution and Specific Software Functionality Required by

Cook County.”)

5

Id. at L.

Cook County Board of Review Annual Report 2022 8

In sum, there are no Cook County Board of Review specific software modules outlined in the subject contract. with the Cook County Board of

Review singular but vital role of having the ability to “PULL” and “PUSH” assessment data from the proposed “future state” application. The Tyler

solution “IASWorld” as it had from the “legacy” “mainframe” which is a data source shared by all members of the Cook County Property Tax Group

which includes the Cook County Assessor, Cook County Board of Review, CC Clerk and CC Treasurer.

Tyler was contracted to develop interfaces with the Cook County Board of Review’s DAPS application

However, due to the gross mischaracterization of the Cook County Board of Review’s role/involvement in the IPTS, and more importantly, the

impact on the 2021 2nd Installment Tax Bill, it must be noted that the “2015 IPTS Contract” explicitly states that “THE BOARD OF REVIEW IS

CURRENTLY AUTOMATING ITS PROCESSES VIA ONBASE SOFTWARE, THUS TYLER SHALL IDENTIFY AND BUILID ALL COOK COUNTY BOARD OF

REVIEW INTERFACES WITH ONBASE AND DOCUMENT SAID INTERFACES IN THE INTERGRATION PLAN.”

6

In addition, Tyler stated that the Cook County Board of Review’s OnBase solution was compatible with iasWorld application.

7

System Requirements

Tyler shall provide all functionality in-scope. The functionality listed below corresponds to the requirements identified by business process owners in

the Uses Case, which Tyler shall validate.

No. Requirements

Module or

Solution Name

In-scope?

5.011

Systems can capture credit card and e-check payments

through the receipt of an interface file from external source

(i.e. banks, credit card processors)

iasWorld Yes

5.012

Systems can access Board of Review (BOR) review process

finalized results from Onbase software.

iasWolrd Yes

5.013

System can interface with OnBase to present all relevant BOR

PIN information for an analysist to make a decision.

iasWorld Yes

5.014

System can associate (link) location of document in OnBase

to a PIN.

iasWorld Yes

5.015

System inferfaces with the BOR OnBase system to pull the

PTAB data and update the refunds values.

iasWorld Yes

Concerning the “integration” of the Cook County Board of Review’s DAPS application, the 2015 contract clearly states the following

8

:

Integration

Upon completing its initial assessment of the County’s Technology environment, Tyler shall document a plan that at minimum documents the

required interfaces with sucient detail to understand the data that will be pushed and/or pulled from each date source, including comprehensive

diagrams. This plan should also outline the approach and timeline to build, test and accept interfaces. Tyler shall also discuss with the County the

recommended interfacing approach such as web services, batch file processing, direct database integration via APIs, and/or the County’s Enterprise

Service Bus (ESB) prior to finalizing any decisions or making any assumptions. The County shall review and approve the Integration Plan.

Tyler shall at minimum provide:

1. An Integration;

2. An updated integrations/interface model/diagram;

3. Planned interfacing methods (real-time/batch, etc.);

4. Estimated phased timeline for interfaces to go live;

5. Approach to build and test each of the interfaces/integration;

6. For each identified interface, Tyler shall alert the County to work with its vendors to estimate indirect level of eort by resources other

than Tyler’s resources.

7. Tyler shall at minimum build interfaces to the following existing technologies:

6

Id. at 3.3.1.8

7

Id. at 3.3.2

8

Id. at 3.7

OnBase Software.

OnBase is used in various Property Tax Oces including the BOR, Treasurer’s Oce and

Assessor’s Oce. Tyler shall validate OnBase data feeds with all Oces.

Cook County Board of Review Annual Report 2022 9

Therefore, pursuant to the “2015 IPTS Contract,” the vendor, Tyler, shall document an integration plan that, at a minimum, that documents the

REQUIRED INTERFACES with sucient detail to understand the data that will be PUSHED and/or PULLED from each data source which specifically

includes NOT excludes OnBase. To date, such a plan does not exist nor contractually is it the responsibility of the Cook County Board of Review

to create such a plan. See Section 3.6. However, the Cook County Board of Review has proactively secured capital project approval and funding

to build an interface between the Cook County Assessor’s Oce and the Cook County Board of Review. This capital project will complement

Tyler’s eorts to establish this interface. Due to the well-known data dependencies of all members of the Cook County Property Tax Group, but

particularly the numerous exchanges between the Cook County Assessor and Cook County Board of Review, the Cook County Board of Review’s

ability to “PUSH” and “PULL” data to and from the future state application, “IASWorld” is critical to not only the entire Cook County Property Tax

Group, but ultimately to all Cook County residents.

It should be noted that the Cook County Board of Review has actively participated in the IPTS eorts, producing “file layouts;” “process maps;” and

“workflow maps” dating back to, at least February 2016, clearly pre-dating the current Cook County Assessor administration, however, this data has

been saved and shared on the “Integrated Property Project Team” site.

It should be noted that the Cook County Assessor informed the Cook County Board of Review in late June of 2021 of its inability transmits

assessment data via its future state application, “iasWorld” despite having launched Phase 1 of assessment “Go Live.” Nonetheless, Cook County

Assessor, Cook County Board of Review, Bureau of Technology and Tyler all collaborated on a solution that relied on the mainframe for the

2021 tax year. Presently, for the 2022 tax year, until an interface between the Cook County Board of Review’s OnBase application and “iasWorld”

as contracted for is developed and tested, the Cook County Property Tax Group will again rely on the mainframe “workaround” solution. This

“interface” issue was identified and addressed in the “2015 IPTS Contract,” therefore, it is far from a “newly discovered” issue.

THE ASSESSOR’S INTENTIONAL SHIFT OF THE TAX BURDEN

BASED ON FLAWED ASSESSMENT METHODOLOGY

Majority View

In considering the income and expenses of a property, a decision must be made on how to treat the property taxes. When property is valued for ad

valorem tax purposes, taxes should not be considered an expense item. Because any deduction from gross income directly aects the indicated

property value through the income approach, only typical and reasonable expenses can be used.

When property is valued for ad valorem tax purposes, therefore, property taxes cannot be shown as an operating expense because the actual taxes

are not known as of the assessment date. Indeed, the appraisal is often done to estimate the amount of tax. The problem can be resolved by

developing an eective tax rate and including it in the capitalization rate for the subject property.

To avoid circularity, however, property taxes are accounted for in valuations for assessment purposes by adjusting the capitalization rate.

Otherwise, the amount of tax affects the estimate of value used to calculate the tax.

THE ASSESSOR’S “SHIFT” UNLOADED CAP RATE METHODOLOGY

Unloaded Cap Rate

The Assessor does not use a loaded cap rate becuase the tax rate, and levy, vary from year to year, depending on the municipality and other local

taxing bodies. As such, taxes cannot be predicted down to a precise dollar amount prior to the millage rate being announced after assessments are

certified.

The Assessor uses an unloaded cap rate because it reflects the way transactions and investments are viewed in the open marketplace. The typiacal

tax appeal appraiser will conclude for an unloaded cap rate and then add the tax load to that number and explain that the rates should equal that

same valuation when unwound. Instead of convuluting the cap rate by loading it, we utilize the unloaded rate to compare apples to apples in a clear

and transparent way.

Cook County Board of Review Annual Report 2022 10

CCAO Mass Income Approach

No Tax Load Applied Tax Load Applied

Square Feet 94,134 94,134 $310,642.00

Rent PSF (PGI) $3.30 $310,642.00 $3.30 $292,003

V/C (EGI) 6% $292,003 6% $248,203

Exp (NOI) 15% $248,203 15%

Cap Rate 8.50% 8.50% 2021 Tax Load: 5.59%

Cap Rate + Tax Load 14.09%

Market Value $2,920,037 $1,761,555

Assessed Value $730,009 $440,389

Note: 66% over tax load calculation

2018 Tri TMV 2021 CCAO TMV 2021 CCBOR Relief TMV 2021 Appr.

$841,276 $2,920,028 (+247% over 2018 TMV $1,764,753 (+110% over 2018 TMV) $840,000

2020 RET 2021 CCAO RET Actual 2021 RET

$47,007 $147,280 (+213% over 2020) $89,010 (+89% over 2020)

2021 PTAB Refund Liability

$104,912 $46,643

ILLUSTRATION OF CAPITALIZATION RATE VS.

LOADED CAPITALIZATION RATE CALCULATION

Cook County Board of Review Annual Report 2022 11

Save A Lot

420 S Pulaski

2018 CCBOR Relief 2018 Appr. 2020 RET 2021 CCAO 2021 RET. 2021 Appr.

$1,191,960 $875,000 $66,604 $2,540,908 +113%-No BOR Action $151,746+127% N/A

Subject: “Save a Lot” Grocery Store located at 420 S. Pulaski Road, Chicago, Illinois

Supermarket - Northwest Cit Submarket

Chicago, IL 60624

11,440

SF GLA

1.15

AC Lot

1968/2008

Built/Renov

Family Dollar

2274 N Milwaukee

2018 CCBOR Relief 2018 Appr. 2020 RET 2021 CCAO 2021 RET. 2021 Appr.

$1,064,804 (BOR NC) N/C $59,515 $1,725,620-+62% (BOR NC) $87,035-+46% $830,000

E

XAMPLE OF THE IMPACT OF THE

ASSESSOR’S MISDIRECTED “SHIFT”

METHODOLOGY

Subject: “Family Dollar “ located at 2274 N. Milwaukee Avenue, Chicago, Illinois

Freestanding Retail - Northwest City Submarket

Chicago, IL 60647

10,000

SF GLA

0.63

AC Lot

1956

Built

Single

Tenancy

Cook County Board of Review Annual Report 2022 12

HEARINGS

Residential

The pandemic prompted the Board to be nimble in its operations. The Board,

therefore, undertook a triage system of pro se hearings, having members of our

Clerk’s sta do pre- screening phone calls with taxpayers to see if they wished to

proceed to hearing or simply had questions about the process. The Board is happy

to report that taxpayers and our hearing ocers found this created eciencies and

provided better service to taxpayers.

Commercial

Similarly, Cook County Board of Review commercial hearing ocers reported

eciencies in the hearing process having all hearings conducted via video

conference while maintaining full transparency to the public.

TRANSPARENCY

All information – notes, evidence, and decisions – have been available online for

seven years. Taxpayers may view final decision rendered and any notes by the

analysts. The Board is also proud that it frequently is quicker than the statutory

deadline to respond to FOIA requests.

Number of PINS Appealed

by Property Type

Residential

218,399

Commercial

83,516

Condo

235,703

0

3000

6000

9000

12000

15000

Number of Requested Hearings

20202021 2019 2018

BUDGET HIGHLIGHTS

• The Board continues to maintain a lean operation despite the explosion of cases appealed

• The Board has leveraged technological eciencies to keep up with the massive increase in cases filed and has realized a modest increase in

head count to help maintain its successes

• Moreover, the Board continues to maintain a budget that is overwhelmingly focused on personnel to continue service to the taxpayers

• The Board operates on the tax year; the information below is per the fiscal year

• Improve time to process appeals

• Improved public data access and transparency

• Severance the reliability on the mainframe

• Improved intergovernmental property tax agency data interaction and processes

• Intuitive portal enhancements for a better public user experience

Appropriations ($ thousands)

Fund Category 2020 Adopted 2021 Adopted 2022 Adopted 2023 Adopted

Corporate Fund 13,473 14,073 14,924 17,834

Special Purpose Funds 0 0 1,084 0

Total Funds 13,473 14,073 16,008 17,834

Expenditures by Type

Personnel 12,820 13,466 15,162 16,699

Non Personnel 653 607 846 1,135

Total Funds 13,473 14,073 16,008 17,834

FTE Positions 142.0 142.0 151.0 156.0

Cook County Board of Review Annual Report 2022 13

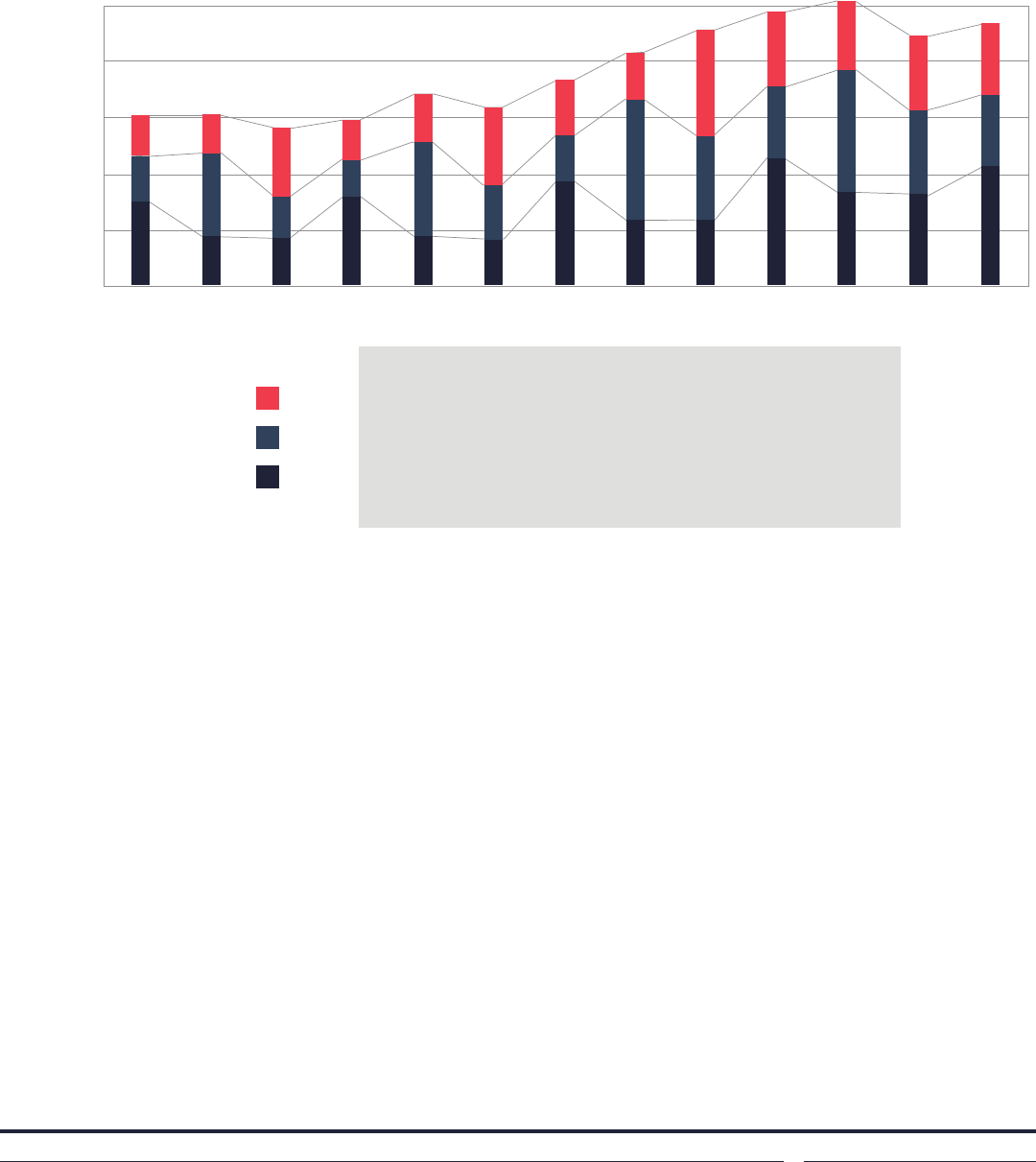

EMPLOYEES AND APPEALS

Appeals have held relatively consistent from 2009 to 2015, at which point they have been steadily rising year over year. In the decade from 2009-

2021, the BOR has seen a 59% increase in the volume of appeals. While we cannot say with certainty why appeals are increasing, we attribute it to

a combination of our oce’s increased community outreach eorts to inform and assist property owners with the appeals process, as well as to

changes in assessment practices by the Cook County Assessor.

While the volume of appeals has more than doubled, BOR sta (measured in Full Time Equivalent employees, or FTEs) has barely kept pace.

Nevertheless, we have increased the number of appeals reviewed exponentially by modernizing and professionalizing the oce with our digital

appeals system. The Board also increased outreach capabilities to match the need and access given the ongoing pandemic to ensure residents

are still reached when in person outreaches have been paused. Also, an increased measure of analysts available to help residents over video

conferencing and walk them through each step on how to file an appeal with the Board. In addition to increasing access to resources available in

other languages than English to reach more communities

In 2015, the BOR moved from an arcane paper-based system to an award-winning digital system that also made the Board’s functions more

transparent and more easily accessed by the public. Over twelve years, the number of BOR appeals has risen by 103%, but the investment in

the technology allowed the BOR to do its job much more eciently: eliminating the cumbersome paper-based system, making it easier for

management to find and clear chokepoints in the process, and making the data transfer between oces (the Board, the Assessor, the Treasurer,

etc.) much more seamless and faster. These eciencies have saved weeks in each session and created eciencies in downstream oces.

SOUTH TRI S

NORTH TRI N

CITY TRI C

2009 Appeal Session Volume ....................... 159,000 dockets

2015 Appeal Session Volume (DAPS) ................. 184,088 dockets

2017 Appeal Session Volume (May 10) ............... 228,389 dockets

2019 Appeal Session Volume ....................... 253,425 dockets

2020 Appeal Session Volume ....................... 223,276 dockets

2021 Appeal Session Volume ....................... 248,899dockets

Historic BOR APPEAL Data

Number of Appeals

0

50,000

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

100,000

150,000

200,000

250,000

Cook County Board of Review Annual Report 2022 14

EMPLOYEES AND APPEALS CONTINUED

Employees Appeals* Pins* Filed

2009 122 159 439

2010 118 158 386

2011 119 146 342

2012 124 152 423

2013 125 175 403

2014 125 162 319

2015 125 184 476

2016 130 208 422

2017 111 228 361

2018 126 245 540

2019 142 253 466

2020 142 223 387

2021 151 249 537

*in thousands

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

122 118 119 124 125 125 125 130 111 126 142 142 151

159 158 146 152 175 162 184 208 228 245 253 223 249

Sum of Number of FTEs

Sum of Appeals Reviewed

(in Thousands)

260

240

220

200

180

160

140

120

100

122

118

119

124

125

125

125

130

111

126

253

159

158

146

152

175

162

184

208

228

245

14 142 2

2009-2021 FTEs vs Appeal Volume

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

223

249

151

Cook County Board of Review Annual Report 2022 15

OPERATIONAL HIGHLIGHTS

Tri/Assessment Year PINs (in thousands) Dockets (in thousands)

2009 439 135

2012 426 152

2015 475 184

2018 540 245

2021 537 249

2010 386 158

2013 403 174

2016 422 208

2019 466 253

2011 342 146

2014 319 162

2017 360 228

2020 366 224

Total PINS and Appeals Filed

Although the Board continues to see a large increase in the volume of appeals year over year, the 2021assessment was a nominal increase over the

2018 assessment, however, there was a notable 12% increase in Commercial/Industrial filings due to the significant Assessor increases.

Historical filing data before the Board from 2009-2021:

DocketsPINs

0

100

200

300

400

500

600

2012 2010 20112009 2015 2013 20142018 2016 20172021 2019 2020

City North South

Number of Dockets and Last Tri (in the thousands)

Assessment Years

CityNorthSouth

Cook County Board of Review Annual Report 2022 16

APPEALS RESULTING IN A REDUCTION

Assessment Years 2008–2021

Since 2017, the Board’s total reductions of all property types have been well below 60%:

Reductions by Property Type

Residential Commercial Tri

2021 44% 56% City

2020 45% 57% South

2019 57% 34% North

2018 65% 47% City

Appeals Resulting in a Reduction Assessment Years

Average Appeals (PINs)

Resulting in a Reduction

0

10

20202021 2019 2018 2017

20

30

40

50

60

70

Year Docket Resulting in Reductions

2009 77%

2010 67%

2011 62%

2012 64%

2013 62%

2014 59%

2015 64%

2016 64%

2017 63%

2018 52%

2019 54%

2020 55%

2021 47%

RESIDENTIAL NONCONDO

NUMBER OF APPEALS FILED

ATTORNEY VS PRO SE

ATTORNEY VS PRO SE CHANGE

RESIDENTIAL CHANGE COMMERCIAL CHANGE

190,318 vs 58,581

41% vs 51%

44% 56%

Cook County Board of Review Annual Report 2022 17

PTAB APPEALS

The Illinois Property Tax Appeal Board (PTAB) is frequently the next level most taxpayers can choose to appeal the decision of the Cook County

Board of Review. share a symbiotic relationship.

The mandate of each entity is to provide taxpayers with an unbiased forum for appealing assessments at no cost to the property owner. PTAB is a

forum to appeal the Cook County Board of Review’s decision.

PTAB DEFENSE DIVISION

The purpose of the PTAB Defense Division here at the Board is to defend the County’s assessment decisions from the appeals at PTAB. This division

is active year-round defending the dockets by preparing and providing evidence, arguing at hearings, and negotiating settlements from all the

prior years appealed until they are closed. Successfully defending and closing appeals, and reducing the backlog of appeals, given the resources

available at the Board is our task. The current total refund liability is $278 million. The Board has been very successful in defending the taxing

districts. Funding the resources of the Board to defend at PTAB pays o for the County and all the taxing districts. In FY 2022, there was $137

million of savings from the risk of refunds (plus savings on interest) for all taxing districts. Small investments in resources at the Board pay o in

large amounts given the size of the refund liability. The Cook County Board of Review was able to utilize a digital process for our PTAB workflow

for the first full year and improved eciencies with this in place. Each year we improve this process, working with PTAB and our respective

technology teams to coordinate improved digital file processing and workflow. Approximately 7-10% of BOR appeals go to PTAB annually.

INITIAL LIABILITY

$276,187,276

SAVINGS

$137,232,053

2020 PTAB CASELOAD

FISCAL YEAR 2021:

DOCKETS

CLOSED

PTAB

HEARINGS

DOCKETS FOR

HEARINGS28,583

384

10,409

Cook County Board of Review Annual Report 2022 18

EXEMPT PROPERTIES & THE COOK

COUNTY BOARD OF REVIEW

The Cook County Board of Review examines applications from governmental, charitable, and religious organizations that believe they meet

the qualifications for property tax exempt status. The requirements for property tax exempt status can vary. The Cook County Board of Review

examines each case to determine whether the property is specifically exempt by statute and whether the property owner has met the required

burden of proof. The Cook County Board of Review may hold a hearing in cases involving a question of law, an incomplete file, or when a taxing

body objects to an application. In either case, petitioners are notified by mail of their hearing date. Following the hearing, a recommendation on

exempt status is sent to the Illinois Department of Revenue.

While the Cook County Board of Review makes a recommendation, only the State of Illinois can remove property from the property tax roll. In

assessment year 2021, the Cook County Board of Review processed 1,182 exempt parcels requesting exempt status.

0

500

1000

1500

2000

2500

3000

Exempt PINs Filed

Average Total Exempt PINs Filed

20202021 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008

Year PINs

2021 2,058

2020 1,182

2019 1,208

2018 1,527

2017 1,928

2016 1,694

2015 1,017

2014 1,017

2013 1,911

2012 1,246

2011 1,276

2010 1,367

2009 1,946

2008 2,807

2021 Total Exemption Petitions

Governmental 1,123/1,521

Religious/Charitable 256/537

Cook County Board of Review Annual Report 2022 19

2021 TAX YEAR OUTREACH EFFORTS

Through the Cook County Board of Review’s community outreach programs, we bring assessed valuation complaint services to the community.

During the 2021 assessment year, our oce conducted over 150 outreach events (often virtual; some in person) and serviced thousands of

taxpayers throughout Cook County. The main focus of the outreach programs are to educate and inform taxpayers of the Cook County Board of

Review’s services and to explain the assessed valuation appeal process. Our outreach programs have proven to be a viable and eective way to

provide the community with important information and to provide transparent access to this oce.

The Civic Consulting Alliance (CCA) report noted the underserved communities as a whole are over assessed leading to regressivity in the Cook

County Assessor’s Oce assessment model. Per the CCA report, owners of lower value homes contest their assessments at a lower rate than

owners of higher value homes. As it has for many years, the Cook County Board of Review provides transparent access to the assessment appeal

process via its Outreach programs. This has proven to be an invaluable vehicle in bridging the gap between the rich and poor homeowners and

also bringing our services into the community.

The Cook County Board of Review is fortunate to have the continued support for our respective outreach initiatives from elected ocials and

community organizations throughout Cook County. The Cook County Board of Review has partnered with elected ocials and community

organizations whose support has played an integral role in making the Cook County Board of Review more accessible to taxpayers.

Cook County Board of Review Annual Report 2022 20

CCAO TRIENNIAL ASSESSMENT CYCLE

Hyde Park

Jeerson

Lake

Lakeview

North Chicago

Rogers Park

South Chicago

West Chicago

City Tri (2012, 2015, 2018)

70

71

72

73

74

75

76

77

Barrington

Elk Grove

Evanston

Hanover

Leyden

Maine

New Trier

Niles

Northfield

Norwood Park

Palatine

Schaumburg

Wheeling

North Tri (2013, 2016, 2019)

10

16

17

18

20

22

23

24

25

26

29

35

38

Berwyn

Bloom

Bremen

Calumet

Cicero

Lemont

Lyons

Oak Park

Orland

Palos

Proviso

Rich

River Forest

Riverside

Stickney

Thornton

Worth

South Tri (2014, 2017, 2020)

11

12

13

14

15

19

21

27

28

30

31

32

33

34

36

37

39

City Tri

North Tri

South Tri

Area

Sections

Hydroline

Lake Michigan

Interstate Highway

04 81 22

Miles

COOK COUNTY

BOARD OF REVIEW

Commissioner Larry R. Rogers, Jr.

Commissioner Tammy Wendt

Commissioner Michael M. Cabonargi

ANNUAL REPORT

ASSESSMENT YEAR 2021

FISCAL YEAR 2022