1

A STUDY ON COGNITIVE BIASES IN GAMBLING:

HOT HAND AND GAMBLERS' FALLACY

by

Juemin Xu

Thesis submitted to UCL

for the degree of Doctor of Philosophy in Experimental Psychology

2

I, Juemin Xu, confirm that the work presented in this thesis is my own. Where

information has been derived from other sources, I confirm that this has been

indicated in the thesis.

3

Abstract

People who appear to believe in the hot hand expect winning streaks to continue

whereas those suffering from the gamblers’ fallacy unreasonably expect losing

streaks to reverse. 565,915 sports bets made by 776 online gamblers in 2010 were

used for analysis. People who won were more likely to win again whereas those who

lost were more likely to lose again. However, selection of safer odds after winning

and riskier ones after losing indicates that online sports gamblers expected their luck

to reverse: they suffered from the gamblers’ fallacy. By following in the gamblers’

fallacy, they created their own hot hands. Some gamblers consistently outperformed

their peers. They also consistently made higher profits or lower losses. They show

real expertise. The key of real expertise is the ability to control loss.

4

Publications associated with this thesis

Xu, J., & Harvey, N. (2014). Carry on winning: the gamblers’ fallacy creates hot

hand effects in online gambling. Cognition, 131(2), 173–80.

http://doi.org/10.1016/j.cognition.2014.01.002

Xu, J., & Harvey, N. (2015). Carry on winning: No selection effect. Cognition, 139,

171–173. http://doi.org/10.1016/j.cognition.2015.02.008

Xu, J., & Harvey, N. (2014). The Hot Hand Fallacy and the Gambler’s Fallacy: What

are they and why do people believe in them? In F. Gobet & M. Schiller

(Eds.), Problem Gambling: Cognition, Prevention and Treatment (pp. 61–73).

London: Palgrave Macmillan UK.

http://doi.org/10.1057/9781137272423_3

Xu, J., & Harvey, N. (in press). The economic psychology of gambling. In Ranyard,

R. (Eds.), Economic Psychology: The Science of Economic Mental Life and

Behaviour. Wiley- Blackwell

5

Table of Contents

Chapter 1. Introduction .............................................................................................................. 9

1.1 Classical economic theory about values. .......................................................................... 9

1.2 Behavioural economic theory about values. ................................................................... 10

1.3 Gamblers' theories about uncertainty: the hot hand and gamblers' fallacies. ................. 11

Chapter 2. Gambling games and biases, fallacies, and real skills ............................................ 14

2.1 Lotteries .......................................................................................................................... 16

2.2 Scratch cards ................................................................................................................... 20

2.3 Roulette .......................................................................................................................... 21

2.4 Fruit machines ................................................................................................................ 24

2.5 Sports betting .................................................................................................................. 26

2.6 Card games ..................................................................................................................... 30

2.7 Summary ........................................................................................................................ 32

Chapter 3. Problem gambling .................................................................................................. 34

Chapter 4. The gamblers' fallacy creates the hot-hand effect .................................................. 39

4.1 Data set ........................................................................................................................... 39

4.2 Methodology and results ................................................................................................ 41

4.3 Do gamblers with long winning streaks have higher payoffs? No. ................................ 47

4.4 The effects of winning and losing streaks on level of odds selected. ............................ 48

4.5 The effects of winning and losing streaks on stake size ................................................. 51

4.5 Hot hands exist because of a belief in the gamblers’ fallacy ........................................ 53

6

4.6 Gamblers became safer or riskier after winning or losing streaks, not the other

way round. ............................................................................................................................ 54

Chapter 5. A roulette experiment ............................................................................................. 60

5.1 Methodology .................................................................................................................. 60

5.2 Results ............................................................................................................................ 62

5.4 Discussion ...................................................................................................................... 67

Chapter 6. Real expertise in gambling .................................................................................... 69

6.1 Is there real expertise? Yes. ............................................................................................ 70

6.2 What is real expertise? The ability to control loss. ........................................................ 78

Chapter 7 Discussion and summary ......................................................................................... 84

7.1 Evidence for the hot hand but not for the gamblers’ fallacy. ......................................... 84

7.2 Gamblers behave differently in roulette and in sports gambling. .................................. 85

7.3 There is real expertise in sports gambling: it is loss control. ......................................... 85

References ................................................................................................................................ 87

7

List of Figures

Figure 1. Probability of winning after obtaining winning streaks of different lengths

(o) and after not obtaining winning streaks of those lengths (Δ). .............................. 42

Figure 2. Probability of winning after obtaining losing streaks of different lengths (o)

and after not obtaining losing streaks of those lengths (Δ). ....................................... 45

Figure 3a. Mean preferred odds after winning (o) and losing (Δ) streaks of different

lengths. ....................................................................................................................... 49

Figure 3b. Median preferred odds after winning (o) and losing (Δ) streaks of

different lengths. ........................................................................................................ 50

Figure 4. Median stake size after winning (o) and losing (Δ) streaks of different

lengths. ....................................................................................................................... 52

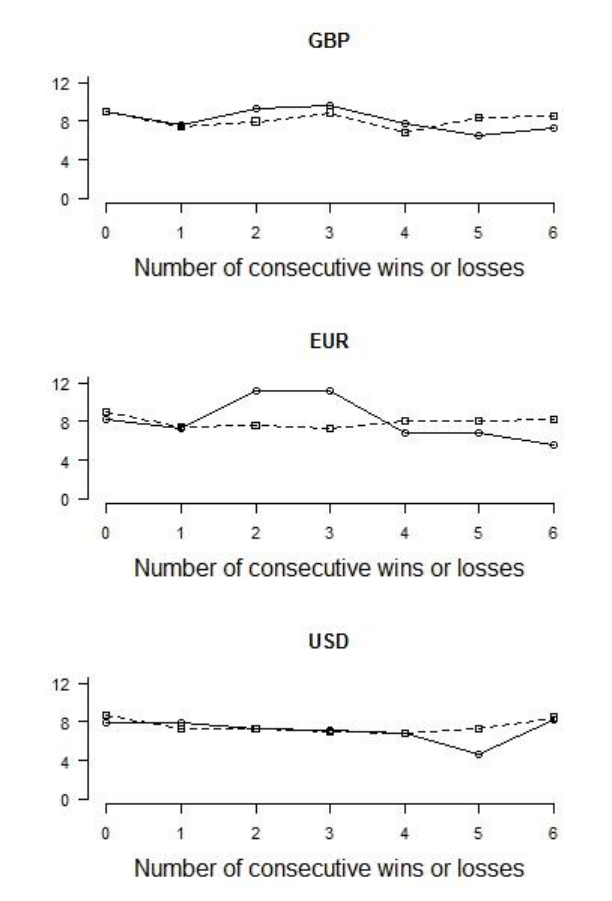

Figure 5. Mean odds plotted against streak length. The continuous line with the “o”

symbol shows data for consecutive wins and the dotted line with the “▢” symbol

shows data for consecutive losses. ............................................................................. 57

Figure 6. Median odds change in always win (o) and always lose (Δ) rounds. ......... 63

Figure 7. Median stake change in always win (o) and always lose (Δ) rounds. ........ 65

8

List of Tables

Table 1. Common forms of gambling ........................................................................ 15

Table 2. Sample characteristics for sports bets placed in each of three currencies for

the year 2010. ............................................................................................... 40

Table 3. Regressions for length of streaks predicting the probability of winning. .... 47

Table 4. Regression for length of streaks predicting the odds. .................................. 64

Table 5. Regression for length of streaks predicting the stake. ................................. 66

Table 6. Binary regression of winning and losing amounts predicting change of

chosen slot. ................................................................................................... 67

Table 7. Monthly median and mean returns in horse racing and football. ................ 71

Table 8. The performance ranking in horse racing in each month was correlated with

the rankings in the other months. ................................................................. 72

Table 9. Positive returns in horse racing in one month were correlated with returns in

other months................................................................................................. 75

Table 10. Performance ranking in football in each month was correlated with the

rankings in the other months. ....................................................................... 77

Table 11. Positive returns in football in one month was correlated with returns in

other months................................................................................................. 78

Table 12. Profitable gamblers were less likely to chase loss. .................................... 81

9

Chapter 1. Introduction

Gambling, being a game of money, gives us a peep into the psychology of

value. Gambling has a long history. It typically involves winning or losing money

with uncertainties. It is one of the earliest behaviours studied in scientific research

into probability (Bernoulli, 1738/1954).

1.1 Classical economic theory about values.

Economics is a science about values (e.g. money, probability). One common

value is money. In microeconomics, the value of money is ultimately defined by

utilities. Utility is subjective. This means that microeconomics is usually implicitly

based on psychology. Classical economics assumes people want to maximize their

utility and their own utility only, and that they know how to maximize this utility

with minimum cost. Through self-interest, people can trade with each other to

maximize their own utility. Their preferences are stable: in other words, they have a

stable utility function. Their behaviours are consistent with their utility functions. A

large group of people or one person over time, given enough resources to gather

information, should demonstrate, or at least approach, rational decision making.

People are assumed to prefer more money than less money. Money has

diminishing marginal return of utility: all else being equal, every additional unit of

money brings less pleasure. This view is partially derived from the law of

diminishing marginal returns (Smith, 1776). For example, when a person is thirsty,

drinking the first cup of water quenches the thirst most; drinking the second cup of

water may still be nice but may not be as wonderful; a third cup may be OK;

drinking a fourth or fifth cup will eventually bring misery. Many other products may

10

not have such a steep decrease of marginal utility but the pleasure of owning one

more unit of the same product almost always decreases after more units have been

acquired. Money provides the payment method for products and has a similar

diminishing marginal utility.

1.2 Behavioural economic theory about values.

When an economic decision involves uncertainty, the option with the highest

expected value has been assumed to be the preferred choice. If the same decision is

repeated many times, the mean value will approach the expected value. However,

questions have been raised by economists about the validity of using expected value

as the only indicator of preferred choice. In many situations, people consistently

prefer a lower expected value. For example, in insurance, the very fact that the

organizers make profit from the business is a sign that the expected value of the

potential loss is lower than the insurance premium; and in lotteries, the expected

value of the jackpot is almost always lower than the lottery ticket. So why do the

buyers accept a loss? This is likely to be because they have a risk preference that is

different from what is assumed by expected value maximization. Specifically, some

people may prefer to lose a small amount of money for sure rather than a large

amount with small probability. A person who prefers a sure option over a risky

option that has an equal or greater expected value is, for that particular choice at least,

risk averse. Conversely, a person who prefers a risky option over a sure option that

has an equal or greater expected value is risk seeking.

Prospect theory says people value same amount of loss more than same

amount of gain (Kahneman and Tversky, 1979). What's more, people tend to have

different risk preferences for different probabilities (Tversky and Kahneman, 1992;

11

Tversky and Fox, 1995) and for different amounts of money (Markowitz, 1952;

Levey, 1994). Generally speaking, when the decision is about receiving money,

people are risk seeking when probabilities of the largest possible outcome are low

but risk averse when they are high. Thus, Tversky and Fox (1992) re-analysed

Tversky and Kahneman’s (1992) data to show that the certainty equivalent of 5%

chance of receiving $100 was a gain of $14 (risk seeking) but that the certainty

equivalent of a 95% chance of receiving $100 was a gain of $78 (risk aversion). This

pattern was reversed when the decision was about losing money: the certainty

equivalent of a 5% chance of losing $100 was a loss of $8 (risk aversion) whereas

the certainty equivalent of a 95% chance of losing $100 was a loss of $84 (risk

seeking). This fourfold pattern of risk taking is overlaid by effects of the amount of

money to be gained or lost. Thus the risk aversion with gains increases with the size

of the stake (Binswanger, 1981; Levy, 1994).

When people make a decision that involves both a gain and a loss, they tend

to display loss aversion. For example, people who are offered a bet, which has 50%

chance of winning £10 and 50% chance of losing £10, will often refuse it

(Kahneman and Tversky, 1979). This implies that they anticipate that their pain from

losing £10 will be greater than the pleasure from winning £10. Hence, for people to

take the risk of losing £10, their potential gain needs to be bigger than that amount.

In this chapter, I will discuss the economic psychology of gambling in terms of these

three concepts: risk aversion, risk seeking, and loss aversion.

1.3 Gamblers' theories about uncertainty: the hot hand and gamblers' fallacies.

To gamblers, uncertainty is intertwined with luck. When luck is with you,

you can win in spite of low chance of winning; when luck is not with you, you could

12

fail even with a good chance of winning. The hot-hand fallacy and gamblers’ fallacy

are assumed to be common among gamblers because it is thought that they have a

strong tendency to believe that outcomes for future bets are predictable from those of

previous ones. In chapter 4, a mechanism of the gamblers' fallacy creating the hot-

hand effect will be revealed.

Belief in a hot-hand is “If you have been winning, you are more likely to win

again.” The term “hot hand” was initially used in basketball to describe a basketball

player who had been very successful in scoring over a short period. It was believed

that such a player had a “hot hand” and that other players should pass the ball to him

to score more. This term is now used more generally to describe someone who is

winning persistently and can be regarded as “in luck”. In gambling scenarios, a

player with a genuine hot hand should keep betting and bet more.

There have been extensive discussions about the existence of the hot hand

effect. Some researchers have failed to find any evidence of such an effect (Gilovich,

Vallone and Tversky, 1985; Wardrop, 1999; Koehler and Conley, 2003; Larkey,

Smith & Kadane, 1989).

Others claim there is evidence of the hot hand effect in games that require

considerable physical skill, such as golf, darts, and basketball (Gilden and Wilson,

1995; Arkes, 2011; Yaari and Eisenmann, 2011).

People gambling on sports outcomes may continue to do so after winning

because they believe they have a hot hand. Such a belief may be a fallacy. It is,

however, possible that their belief is reasonable. For example, on some occasions,

they may realize that their betting strategy is producing profits and that it would be

sensible to continue with it. Alternatively, a hot hand could arise from some change

in their betting strategy. For example, after winning, they may modify their bets in

13

some way to increase their chances of winning again.

The gamblers’ fallacy is “If you have been losing, you are more likely to win

in future.” People gambling on sports outcomes may continue to do so after losing

because they believe in the gamblers’ fallacy. This is the erroneous belief that

deviations from initial expectations are corrected even when outcomes are produced

by independent random processes. Thus, people’s initial expectations that, in the

long run, tosses of a fair coin will result in a 50:50 chance of heads and tails are

associated with a belief that deviations from that ratio will be corrected. Hence, if

five tosses of a fair coin have produced a sequence of five heads, the chance of tails

on the next toss will be judged to be larger than 50%. This is because the coin “ought

to” have a 50:50 chance of heads and tails in the long run and, as a result, more tails

are “needed” to correct the deviation from that ratio produced by the first five tosses.

There is a conflict between belief in a hot hand and the gambler’s fallacy.

Betting strategies are often based on the previous betting results (Oskarsson, Van

Boven, McClelland, and Reid, 2009). The strategies based on a belief in a hot hand

and gamblers’ fallacy may conflict. For example, when trying to decide what odds to

select in the next round, a belief in the gamblers’ fallacy would result in betting on

higher odds and with more money after losing than after winning. A believer in the

hot hand would do the opposite. In this way, the hot hand and the gamblers' fallacy

give contradictory predictions. They cannot both be true. It is worth investigating

which strategy the gamblers use.

There are many biases, fallacies, and even real skills in gambling, which will

be described in the next chapter.

14

Chapter 2. Gambling games and biases, fallacies, and real skills

In what follows, I discuss the six popular forms of gambling listed in Table 1

and indicate how they illustrate the way that people reason about money and

probability. After that, I discuss the economic, psychological and neurological roots

of problem gambling in chapter 3.

15

Table 1. Common forms of gambling

Game

Characteristics

Prevalence as a percentage

of all UK adults (Wardle,

Moody, Spence, Orford,

Volberg, Jotangia, 2011)

Biases, fallacies, and

other reasons to gamble

Lottery

Low frequency,

fixed odds,

pure chance.

National lottery 59%;

Other lotteries 25%.

Overestimation of low

odds; The availability

heuristic; Entrapment;

The endowment effect;

The representativeness

heuristic;

Illusions of control;

The gamblers' fallacy;

The hot hand effect;

Superstitious

behaviour;

The near miss effect;

Mental accounting;

Loss chasing;

High testosterone

levels; Abnormal levels

of neurotransmitters;

Abnormal brain

activity;

Card counting (a real

skill).

Scratch

cards

High frequency,

fixed odds,

pure chance.

24%

Roulette

High frequency,

fixed odds,

pure chance.

In a casino 5%;

Online games that include

roulette13%.

Fruit

machine

s

High frequency,

fixed odds,

pure chance.

18%

Sports

betting

High frequency,

flexible odds,

may involve real

skills.

Horse racing 16%;

Football 4%;

Dog racing 4%;

Other sports events 9%.

Card

games

High frequency,

flexible odds,

may involve real

skills.

Poker (pub or club) 2%;

Casino card games 5%;

Online games that include

card games 13%.

16

2.1 Lotteries

A lottery is a common form of gambling. There are at least 180 lotteries

worldwide and the total size of lottery industry is estimated to be $284 billion

according to La Fleur's 2015 World Lottery Almanac (Markel, La Fleur and La Fleur,

2015). In the UK, 59% of adults purchased National Lottery tickets in 2009 (Wardle

et al, 2011). Typically, a lottery gambler chooses a series of numbers and pays a

small fixed price for the lottery ticket. The winning numbers are announced

periodically, usually a couple of times a week. The chance of winning the jackpot is

typically extremely low.

As an example, consider Lotto, one of the games offered by the UK National

Lottery. With a £2 lottery ticket, the buyer chooses six numbers from a range

between one and 59 or, alternatively, they take the Lucky Dip option and a machine

picks the six numbers for them. There are two draws every week, one on Wednesday

and one on Saturday. To win the jackpot, all six numbers on the lottery ticket must

match the six winning numbers.

There are 45,057,474 combinations of six winning numbers. In 2015, the

jackpot size fluctuated from £886,754 to £43 million (Camelot, 2015).

Apart from the jackpot, there are smaller prizes for people with tickets that

have fewer than six numbers that match those selected. For those with five matching

numbers, the prize is estimated to be £1000. However, if the number that fails to

match one of the six that are selected does match the number on the bonus ball, then

winnings can rise to around £50,000. There is also £100 for those with four matching

numbers, £25 for those with tickets with three, and a free Lotto ticket for those with

two. There is also a complimentary Millionaire Raffle included with each £2 ticket.

17

A particular combination of colour and an eight-digit number wins a £1 million

prize; there are also twenty £20,000 prizes in every draw.

Every time a person buys a £2 lottery ticket, they are expected to lose half of

the money. The chance of winning any prize is 1 out of 9.3. Clearly, buying a lottery

ticket is not an efficient way to make money. Other lotteries in the world are also

fairly similar to the lottery games organised the UK National Lottery and have

similar returns. For example, the expected return from participating in Powerball in

the USA is about $0.90 for a $2 ticket and 1 in 24.87 buyers win a prize. It is clear

from these odds that buying lottery tickets does not earn money. So why do people

do it?

Lottery buyers may miscalculate and believe they can make money.

According to prospect theory, people tend to overestimate low odds of winning

(Tversky and Kahneman, 1992). Because the extremely low odds of winning the

jackpot are far lower than what people experience in everyday life, they may not be

able to estimate just how tiny they actually are.

Our understanding of the environment comes from experience. According to

Decision by sampling theory (Stewart, Chater and Brown, 2006), each of our

experiences is saved as a sample in memory. It is extremely rare to encounter an

event with a miniscule chance of occurring. Therefore it is unlikely that the chance

of such an event is represented in memory. As a result, it is really difficult to imagine

a chance of this sort. Consequently, people are likely to use a small chance that they

have retained in memory as a substitute for a minuscule chance that they have never

encountered before. The small chance they think of could be a lot bigger than the

miniscule chance.

18

Another way that people may overestimate the chance of winning a lottery is

by using the availability heuristic (Tversky and Kahneman, 1973). In other words,

they may estimate the probability of winning by recalling how many lottery winners

they have heard of. For example, their attention may have been drawn to news

coverage of a number of highly impressive jackpot wins and, as a result, they over-

estimate their chances of winning (Bordalo, Gennaioli and Shleifer, 2010). The

bigger the jackpot, the more jackpot winners are reported and the more people buy

lottery tickets (Cook and Clotfelter, 1991; Matheson and Grote, 2004). When an

event is sufficiently important (for example, involving a life changing amount of

money), people may neglect the actual probability and decide that the event’s

occurrence is all or none (Loewenstein, Weber, Hsee, and Welch, 2001;

Rottenstreich and Hsee, 2001).

People may play a lottery together with friends as a social activity. They may

also buy lottery ticket to experience excitement. In other words, they buy a short

"dream" of winning the jackpot and may be "entrapped" by the thought that, if they

stop buying tickets, they will miss the jackpot (Beckert and Lutter, 2013; Binde,

2013; Forrest, Simmons and Chesters, 2002). These motivations all focus on what

winning lottery would be like rather than on the expected value of buying a ticket.

After people have concluded that the lottery is a good way of making money,

they invent methods to increase their chances of winning. The randomness of the

lottery is closely monitored by its organisers, the regulation bodies, lottery machine

engineers, independent researchers, and millions of buyers (Camelot, 2016a;

Gambling Commission, 2012; Konstantinou, Liagkou, Spirakis, Stamatiou and Yung,

2005). However, this does not stop people trying to increase their chances of

19

winning. Searching online using keywords such as "predict lottery" and "lottery tips"

produces numerous suggestions for doing so.

These tips for increasing the chances of winning can often be traced back to

well-known cognitive biases. For example, people using the representativeness

heuristic are likely to expect that the winning numbers should look random. As a

result, they avoid numbers that do not look random enough, such as those with

regular intervals or those that do not distribute sparsely across the whole range of

possible numbers (Holtgraves and Skeel, 1992; Hardoon, Barboushkin, Derevensky

and Gupta, 2001). Also, given their susceptibility to the illusion of control (Langer,

1975; Rudski, 2004), people overestimate their ability of choosing winning numbers.

This is likely to be why they prefer numbers that they have chosen themselves (Wohl

and Enzle, 2002). In addition, there is evidence that people are affected by the

gamblers' fallacy. If certain numbers have recently appeared among the winning

ones, people tend not to bet on them whereas, if particular numbers have not

appeared for a long time, they are more likely to bet on them (Clotfelter and Cook,

1991; Terrell, 1994). People may also be affected by a belief that certain numbers are

lucky. As a result, they make efforts to find out which those lucky numbers are by

visiting temples, observing candle tears, examining incense ashes, and so on

(Ariyabuddhiphongs and Chanchalermporn, 2007). People also display the

endowment effect: they value things they own more than the same things if they do

not own (Kahneman, Knetsch and Thaler, 1991). Cognitive biases of the sort

outlined above have also been exploited within the commercial advertising to sell

lottery tickets (McMullan and Miller, 2009). I have recently come across a hand-

written lottery advertisement on the Chinese website, weibo.com. It says "You

already have 10 million Yuan in your bank account. You have only forgotten the

20

password. It costs 2 Yuan to try out a password. Once you have got the right

password, the money is yours. No rush, don't give up. Your heart is here, your dream

is here. Chinese Lottery." This is a good example of the endowment effect.

These sorts of effects may have consequences beyond financial loss. People

who believe that there are ways of winning the lottery and who act in ways

consistent with those beliefs exhibit the sort of flawed judgement and decision

making that can make them prone to problem gambling.

Does winning the jackpot make people happy? From the huge smiles of the

lottery winners, it is obvious that jackpots bring instant ecstasy. Surprisingly,

however, Brickman, Coates and Janoff-Bulman (1978) found that winning a jackpot

does not produce longer term happiness. They attributed this to the stresses

associated with the large changes in life style and the increased responsibilities

arising from such a win. Consistent with this, winning a relatively small amount, e.g.

£5000, which is insufficient to lead to a change in life style or to increase financial

responsibilities does make people happier (Gardner and Oswald, 2007).

2.2 Scratch cards

Twenty-four percent of all the adults in UK played scratch cards in 2010

(Wardle et al, 2011). A scratch card is typically a paper card coated with a layer of

black silver ink. The ink can be scratched off to reveal winning numbers or symbols

underneath. The UK National Lottery sells them for prices ranging between £1 and

£10. There can be more than one game on one card. Each game has its own rules.

For example, one scratch card sold for £10 is called £4 Million Blue. It is a blue card

claiming to have four top prizes of £4 million each. It contains a number of games.

The first one requires a purchaser to find the UK National Lottery logo to win.

21

Suppose that, after the ink has been scratched off, a bank symbol showing £4 million,

a vault symbol showing £5000, a suitcase symbol showing £50, and a cash symbol

showing £10,000 are revealed. In this case, the purchaser does not win. If the Lotto

symbol appears, the purchaser wins 4 million. Other games are similar, though some

top prizes are smaller than £4 million.

The odds of winning after purchasing a scratch card range from a 1 in

4,347,890 chance of winning £4 million to a 1 in 6 chance of winning £10 (Camelot,

2016b). The expected return at the start of the game is £7. As the cost of the card is

£10, the buyer is expected to lose £3 for every purchase.

The main difference between scratch cards and the lottery is that results from

scratch cards are instant. In fact, one of the scratch cards sold by the UK National

Lottery is called Instant Lotto. Because the result of the gamble is revealed within

seconds after buying the scratch card, people can quickly buy another one if they so

wish. This makes it easier for people to become addicted to purchasing scratch cards:

if they win, they may feel lucky and buy another scratch card; if they lose, they may

display the gamblers' fallacy and decide to have another try (Griffiths, 2000).

Another difference is that, after the initial print run of the scratch cards, the winning

chance changes after winning cards have been claimed.

People display "near miss" effects with scratch cards, which we will discuss

in detail in section 2.4 in the context of fruit machines.

2.3 Roulette

In 2010, 9% of the adult population in UK played casino games, including

roulette, whereas 13% gambled online, again including roulette (Wardle et al, 2011).

22

Roulette requires no skill. It is a game of pure chance. The odds are completely clear

and transparent. The rules are simple. There are 37 slots on the European roulette

wheel (38 on the American one). Numbers range from 0 to 36 (with an extra 00 slot

on the American roulette wheel). Half are red, half are black, and 0 and 00 are green.

Gamblers can choose to bet on a single slot or a selection of slots. For example, they

could select even or odd, red or black, the first 12 numbers, the second 12 numbers,

the third 12 numbers, and so on. The pay-out for a single number is 35 to 1, the pay-

out for even or odd and for red or black is 1 to1, and the pay-out for any selection of

12 numbers is 2 to 1. It is easy to see that the odds against winning for a single

number are 36 to 1 (37 to 1 on the American roulette). The return is the profit a

gambler can expect based on the pay-out. The expected return divides the expected

profit by the investment (Flood, 2017). In the case of roulette, the expected return is

the expected pay-out divided by the wager. The expected return in European roulette

is -1/37 for a single number. For other choices, when the pay-out decreases, the

chances of winning increases correspondingly and so the expected return is the same.

For American roulette, similar principles hold but the expected return is -2/38.

The result of the roulette game is available immediately and gamblers can

play again immediately. Because of this, roulette is a good game to discuss loss

chasing. Loss chasing is characteristic of problem gamblers according to Diagnostic

and Statistical Manual of Mental Disorders, 5th edition (DSM-5) (American

Psychiatric Association, 2014). To normal people, if something brings pleasure, they

do more of it; if something brings pain, they do less of it. Losing money is certainly

painful, or least unpleasant. However, it is quite common for gamblers to gamble

more after losing. They chase their loss in an attempt to get their money back.

Gamblers may have a mental account for each session of gambling (Shefrin and

23

Statman, 1985; Thaler and Johnson, 1990). When they are still gambling, the book is

not yet closed. They have not "lost". When gamblers are losing, they would face a

sure loss if they stopped. However, if they continued to gamble, then their final loss

would not yet be confirmed. In other words, they would be facing an uncertain loss

with some possibility of winning back their money.

According to prospect theory, people tend to be risk seeking when choosing

between a large uncertain loss and a smaller sure loss (Kahneman and Tversky,

1979). For example, the vast majority of people prefer an 80% chance of losing 4000

Israeli Shekels to a sure loss of 3000 Shekels (the median family net income).

Furthermore, once they have lost, they somehow believe that their luck will turn;

they cannot always lose; god must be fair. This is the gamblers' fallacy (Croson and

Sundali, 2005). It leads to loss chasing. In order to catch the anticipated forthcoming

good luck, they must continue gambling. It is possible that, by chasing loss,

gamblers make themselves even more likely to lose. Because they think good luck is

about to arrive after a losing streak, they bet on longer odds to win more money back

and to make most out of the forthcoming good luck. However, longer odds, by their

very nature, mean a higher likelihood of loss. So, unfortunately, gamblers bring back

luck upon themselves by believing that good luck is on its way.

There is even a betting strategy based on the gamblers' fallacy. It's called the

martingale (Snell, 1982; Wagenaar, 1988). It claims to guarantee winning in a

gambling session. The original model of the martingale strategy is based on coin flip

but it "works" in roulette as well. Here is an example of what it involves. Your first

stake is £1 on red. If you win, you stop. If you lose £1, you double your next stake to

£2. If you win, you stop. If you lose again, you double your third stake again to £4. If

you win, you stop. If you lose again, you double the stake again to £8. And so on.

24

Now suppose that you have lost three times but, finally, won. You will get £8 - £4-

£2 - £1 = £1, if you bet on the 1:1 pay-out choice. (In fact, the expected value on a

£1 stake is 36/37 or 36/38). You could win more if you bet on other higher pay-out

slots. This sounds like a brilliant strategy because, no matter how many times you

lose, you can always win in the end.

Unfortunately, there is a catch: it is quite possible that a gambler will run out

of funds after a losing streak. The roulette ball does not remember its history. Thus,

that gambler is no more likely to win after losing streak than in any other round. Of

course, for gamblers who have an infinite amount of money, the martingale is a

reasonable strategy. Most of them, however, do not have an infinite amount of

money to continue the game. In a limited number of rounds, the return could deviate

far away from the expected value. With erroneous beliefs, people can be trapped in

loss chasing and become problem gamblers. Though it is difficult to ascertain how

many people use the martingale strategy, there are written records of it covering

hundreds of years at least (Scarne, 1961). One vivid story is by Casanova

(1822/2013): "Playing the martingale, continually doubling my stake, I won every

day during the rest of the carnival. I was fortunate enough never to lose the sixth

card … I still played the martingale, but with such bad luck that I was soon left

without a sequin".

2.4 Fruit machines

In 2010, 18% of all adults in UK played fruit machines in 2010 (Wardle et al,

2011). Fruit machines are said to be most addictive form of gambling because of

their highly stimulating sounds and colours. According to Turner and Horbay (2004),

25

it takes just over a year to become addicted to them, whereas it takes over three years

with traditional table games, such as roulette.

Fruit machines, like scratch cards, represent a form of gambling that has no

specific odds of winning. They look like vending machines and work like them.

Typically, they have three to five reels on which pictures are depicted. The player

inserts a coin and then pulls down a handle or presses a button. The reels spin. When

they stop, the combination of pictures forms a certain pattern. If the combination

comprises three pictures that are the same (or some other designated pattern), a

reward is given. The most common winning combination is 777. The odds of

winning on fruit machines are unknown. The fact that it is a game of pure chance

and that the owners of the machines make money indicates that luck is unlikely on

the gamblers' side.

One of the main phenomena identified in studies of fruit machine gambling is

the effect of a near miss. This is a losing pattern that is very similar to a winning one.

For example, the three reels may stop at 776, a combination very similar to the

winning 777. In fact, this sort of result should really be labelled a near win.

Occurrence of a near miss makes the gamblers feel that luck is with them and that

success is on its way. As a result, near miss experiences tend to encourage more

gambling (Reid, 1986; Griffiths, 1991).

In natural environments to which we are adapted by evolution, a near miss

may indeed be close to win. For example, almost catching prey clearly indicates that

prey is nearby and your skill levels are probably adequate to make a kill. In these

circumstances, it makes sense to continue to hunt. However, in artificial

environments, this link may no longer hold. A 776 in fruit machine does not indicate

26

that the result of the next spin is likely to be 777. A piece of valid natural reasoning

has been hijacked. In fact, with functional magnetic resonance imaging, it has been

found that the part of brain that responds to real winning also responds to near miss

(Clark, Lawrence, Astley-Jones and Gray, 2009). This supports the notion that a near

miss is a loss that is either mistaken for gain or that is taken to indicate an

expectation that persistence will produce a gain. Any confusion between losses and

gains could lead to problem gambling. This is because near misses that are registered

in the brain as gains will result in gamblers receiving positive reinforcement even

when they are losing money. As a result, they would encourage people to gamble

more.

2.5 Sports betting

In 2010, 16% of adults in the UK gambled on horse races, 4% on football

matches, 4% on dog races, and 9% played on other types of sports betting (Wardle et

al, 2011).

In sports betting, people bet money on the outcome of sports events. Here we

include non-human sports events, such as horse racing and dog racing, as well as

human sports events like football, tennis, and so on. This is because the format of the

gambling is similar and gambling houses include betting on non-human sports as

sports betting. Gamblers can bet against the bookmaker or against each other in a

betting exchange. Traditionally, the bookmaker sets the odds, the gamblers bet that a

certain event will occur (back) and the bookmaker bets that it will not (lay). This

traditional form of gambling can be done in gambling outlets or on the bookmakers’

websites.

27

Betting exchange typically takes place on bookmakers’ websites. Gamblers

bet against each other. They can offer to "back" a certain event, or to "lay" a certain

event. Their counterparts can see the offers and choose the best odds. Bookmakers in

this scenario work as risk-free exchange houses and do not get involved in the price

setting of the odds. They display matches and settle the odds for a small percentage

of commission. In both betting against the bookmaker and in betting exchange, many

different bets can often be made on one event. For example, for a single football

match, there can be bets on the total score, the first half score, the second half score,

the first team or player to score a goal, the number of goals over or under a certain

number, and so on. The range of odds can be wide. For example, they can range

from 4:3 for "both teams to score" to 150:1 for "over 9.5 goals". Hence, gamblers

can choose from many different types of bet and can select from a wide range of

different risk levels.

Gamblers who back a certain event can choose to hedge their position by

laying that event in the exchange. This could reduce or eliminate the risk they are

exposed to. For example, a gambler who has placed £10 on odds of 150:1 for "over

9.5 goals" may find that the prevailing odds for the same event become 50:1 after

four goals in the first half. He may decide to lay 50:1 "over 9.5 goals" for £20

backer's stake. In other words, he now believes the final result will not exceed 9.5

goals and so he accepts a £20 stake from another gambler who believes the final

result will exceed 9.5 goals. If the final score is over 9.5, he will win £1490 from his

first bet, lose £980 from his second bet, and so win £510 overall (minus commission).

If the final score is under 9.5, he will lose the £10 stake in the first bet, win the £20

stake in the second bet, and so win £10 overall (minus commission). At half time,

28

this gambler can guarantee making profit no matter what the final score is. Such

hedging is a real skill that gamblers can learn.

Among gamblers, it is widely believed that there is useful knowledge to be

learned about different sports. There are books, columns and websites that provide

tips for betting. Betting companies also sell past records to people who want to carry

out analyses. However, researchers have not found much evidence of expertise

(Ladouceur, Giroux and Jacques 1998; Cantinotti, Ladouceur and Jacques, 2004).

Ladouceur, Giroux and Jacques (1998) found that experts won more times than

randomly selected betters but did not win any more money. Experts were just being

cautious and chose safe bets, but they still lost money overall. If this is to be called

an expert strategy, then so should the strategy of not gambling at all as this would

have a non-negative return of zero.

Gamblers feel empowered by knowing the past records of sports teams and

the latest updates. Their confidence level is increased, but their performance level is

not (Cantinotti, Ladouceur and Jacques, 2004). Research has shown that experienced

betters make more accurate judgments in complicated tasks, such as the final score

of a game and the ball control time by each team in a game in football. However,

they do not perform any better in simple tasks, such as predicting which teams went

through to t he next round in the World Cup 2006 (Andersson, Memmert and

Popowicz, 2009). It is not clear whether experienced betters can make profits or not.

It is not impossible that some gamblers have inside information (Crafts, 1985).

Superstition is common in sports gambling. Windross (2003) found that a

majority of people betting on horseracing believed in luck and they practiced

superstitious ceremonies to create good luck. The superstitious behaviours include

29

choosing a lucky number or lucky colour, finding a lucky letter combination in horse

names, combining the numbers of the two previous winning horses, and so on.

Gamblers believe luck can be observed and manipulated. Superstitious rituals are the

methods that are used to obtain good luck. Some rituals can appear bizarre and

dangerous. For example, in South East Asia, some people run in front of trucks on

highways to read their number plates. The number plate gives clues of the lucky

number. The closer the gambler runs to the truck, the luckier the number.

When people have no control over uncertainty, they may turn to superstition

in an attempt to feel that they are still in charge. The hot hand fallacy represents one

such illusion of control. This is the belief that winning brings forth more winning. In

skill-based games, people may believe that winning is a signal that a period of

especially good performance has started and that it will continue. As a result, a streak

of winning indicates that the streak will continue. Ayton and Fischer (2004)

discovered that people who were told that a run of the same outcome was the result

of random process predicted the trend would reverse whereas those who were told

that the same sequence was the result of an algorithm predicted that it would

continue. Fischer and Savranevski (2015) obtained a similar result.

This begs an obvious question: do gamblers believe that sports-betting is

skill-based or not? If they believe that it is their skills that give them an edge, they

should predict they are more likely to win after winning and therefore become more

risk seeking. Xu and Harvey (2014) discovered the opposite: in sports gambling,

gamblers predicted the trend in their betting performance would reverse. They were

more risk averse after winning and more risk seeking after losing. They chose safer

odds after winning and riskier odds after losing. Interestingly, this actually produced

a hot hand effect because safer odds are more likely to produce a win and risky odds

30

are more likely to produce a loss. However, safer odds do not have high payoffs.

Hence, gamblers who have experienced a winning streak may feel that their

gambling performance has improved even though they have not actually made more

profits. This echoes the observation by Ladouceur, Paquet and Dubé (1996) that

experts did not make more money in spite of higher probability of winning. They

might become experts simply by winning more times rather than winning more

money. They can be expert and problem gamblers at the same time. However, good

moods resulting from previous wins may lead to risk aversion in future bets (Isen &

Patrick, 1984). When people are in a good mood, they may choose safer bets to

maintain that mood by avoiding losses. This is an alternative explanation to Xu and

Harvey (2014). This could also create hot hand phenomenon even if the estimate of

the risk level of the future bets remains unchanged.

2.6 Card games

Wardle et al (2011) reports that, in 2010, 2% of adults in the UK played

poker in a pub or club, 5% went to a casino to gamble on games (including poker

and blackjack), and 13% played online games (including poker and blackjack).

There are many different kinds of card games. Some of them, such as blackjack and

poker, have both elements of luck and of real expertise. In blackjack, which is also

called twenty-one, the players take cards in rounds and the one who wins is the

person who reaches 21 points or who is the closest to 21 without exceeding that

number of points. It is played between the dealer of the house and one or more

gamblers. If players can remember the cards that have already appeared in the game,

they will have a better chance of guessing other people's cards and the cards that are

going to appear.

31

In lottery and roulette, anomalies are rare and when they happen, it is

difficult to profit from them; in card games, there are real cases of sustainable

successes. One of the legends is the MIT blackjack team (Mezrich, 2002). They used

a card counting technique. Cards A, 2, 3, 4, 5, 6, are marked as +1, cards 7, 8, 9 are

marked as 0, cards 10, J, Q, K are marked -1. The gambler keeps adding the value of

the cards as they appear. If the sum is negative, it means there are more small cards

in the undistributed deck. This is advantageous to the house and so gamblers should

decrease their stake. Though the profit level of the MIT blackjack team has not been

verified, statistically it is possible to profit from blackjack, poker and other card

games (Javarone, 2015; DeDonno and Detterman, 2008; Turner, 2008).

It is not easy to make money by playing card games because, after all, the

success is largely influenced by holding good cards and gamblers may not have

enough funds to survive potential losses. Hurley and Pavlov (2011) carried out a

simulation based on the card counting technique. They found that, although the

expected return was positive with the card counting technique, with a minimum

stake of $100, the 95% confidence interval of return ranged between -$59,570 and

$76,044. It is a risky business. The gamblers must be prepared for difficult periods

during their search for positive returns. There are also exogenous risks that are not

related to card games per se. For example, casinos do not welcome card counters and

they may restrict entry for such players. If this happens when the players are losing,

it may be difficult to play enough games to reach the expected value. It is possible

that people become problem gamblers with the belief that they will win their money

back.

Poker games often involve a combination of the suit and the points of the

cards. There are many different kinds of poker games. The rank of the card

32

combinations from low to high normally are: single, pair, three of a kind, straight

(consecutive cards), flush (cards of the same suit), full house (three card of one rank

and two cards of another rank), four of a kind, straight flush (consecutive cards of

the same suit). There are small variations in ranking orders in different games. Texas

Hold’em is a popular variant of poker. It has three to five community cards visible to

all players. Players can use the community cards with their own secret two cards to

form combinations. They can decide to increase the stake or to fold as the games

goes along. Players win either by having the highest rank of the combination or by

being the only person remaining.

In Texas Hold'em, players guess each other's cards by observing their stake

change and other emotional signals. Cards games are available online or in a casino.

There is evidence of real expertise in this game (Hannum and Cabot, 2009; Fiedler

and Rock, 2009). Experts consistently perform better than amateurs. Experts are

better at minimizing loss when they have bad cards (Meyer,von Meduna, Brosowski

and Hayer, 2013). It is also possible to teach neural networks to play Texas Hold 'em

to a professional level based on evolutionary methods (Nicolai and Hilderman, 2009).

The argument that it is a skill-based game may give it a status of sport rather than

gambling. As a sport, it would receive less strict regulation.

2.7 Summary

Gambling is a mixture of biases, fallacies, and real expertise. It provides

terrific opportunities to study monetary decision making. In this chapter, I have

described a variety of phenomena associated with the psychology of gambling and

have shown how they may be explained in different gambling contexts.

33

People tend to overestimate low odds of winning (Tversky and Kahneman,

1992). This overestimation may arise from use of the availability heuristic, from

illusions of control, or from over-inflated confidence associated with acquisition of

knowledge specific to the gambling domain. Gamblers also have techniques that they

believe enhance their chances of winning: these include superstitious practices and

choosing random looking lottery numbers. Some of these techniques are effective:

real skills in some card games and in use of hedging strategies can bring profit.

However, the vast majority of the gamblers are likely to lose money in the long term.

Once it has been lost, many of them become susceptible to loss chasing. They

believe their luck is going to turn and they must bet again to win the money back. As

long as they continue to gamble, the book is still open and losses are not yet realized.

They have to keep gambling to prevent that happening. As a result, they often end up

losing more money. The brain may fail to discriminate adequately between wins and

losses: there is evidence that indicates that near misses activate the same brain region

as wins. Confusion arising from this could also encourage continuation of gambling.

This, in turn, may eventually produce problem gambling, discussed next.

34

Chapter 3. Problem gambling

Problem gambling (gambling addiction, pathological gambling) is a mental

disorder defined by DSM-5 as "persistent and recurrent problematic gambling

behaviour leading to clinically significant impairment or distress'' (American

Psychiatric Association, 2014). Two of the major screening questionnaires for

problem gambling are the South Oaks Gambling Screen (Lesieur and Blume, 1987)

and the Problem Gambling Severity Index (Stinchfield, Govoni and Frisch, 2007).

According to the British Gambling Prevalence Survey in 2010, 1.5% of men,

0.3% of women and 0.9% of the entire adult population are problem gamblers

(Wardle et al, 2011). Problem gambling is a major psychological disorder in the

same league as depression or panic disorder (McManus, Meltzer, Brugha,

Bebbington and Jenkins, 2009). It is positively correlated with being male, young,

having a low level of education, and having a low socio-economic status (Wardle et

al, 2011). Internet gambling, because of its constant availability and convenience,

may exacerbate problem gambling: Researchers found that half of problem gamblers

reported that convenient online payment increased their monetary losses (Gainsbury,

Russell, Hing, Wood, Lubman and Blaszczynski, 2015). The internet gamblers also

gamble in more games because they are offered a wider choice than that offered by

traditional casino or gambling shops.

Blaszczynski and Nower (2002) suggested that there are three kinds of

problem gamblers: gamblers with poor judgment and decision-making skills; those

who gamble in order to satisfy emotional needs; gamblers with neurological or

neurochemical dysfunctions.

35

The first of these do not have any psychopathology before they start

gambling. They embark upon their gambling habit because it represents an easily

accessible or social activity. They may experience excitement from their gambling,

they may experience illusions of control or other kinds of irrational belief, and, for

the reasons we have discussed, they may believe that they can win. After losing, they

may start to chase their losses and, as a result, they may lose even more. Evidence

suggests that this type of gambler can gain control over their habit with minimal

intervention provided by sound economic reasoning (Hodgins, 2005).

The second type of problem gambler often has a family history of problem

gambling, together with emotional and biological vulnerabilities (e.g., depression,

anxiety). Gambling provides an escape from these problems (Jacobs, 1988; Lesieur

and Rothschild, 1989; Gambino, Fitzgerald, Shaffer, Renner and Courtage, 1993).

The third type of problem gambler typically exhibits impulsive or antisocial

behaviours that are independent of their gambling. Such behaviours include

substance abuse, suicidality, irritability, low tolerance for boredom, and criminal

behaviour not related to gambling. In other words, they have problem behaviours

that are manifested not only in gambling but also in other ways (Goldstein,

Manowitz, Nora, Swartzburg and Carlton,1985; Carlton, Manowitz, McBride, Nora,

Swartzburg and Goldstein, 1987).

We have pointed out that most forms of gambling in most situations have

negative expected returns. Why would people be addicted to negative returns?

Neurological research has cast some light on this. When they are viewing gambling

scenarios, problem gamblers show decreased brain activity in regions that control

impulse, emotion, and decision-making (Potenza, 2014; Potenza, Steinberg,

36

Skudlarski, Fulbright, Lacadie, Wiber, Rounsaville, Gore and Wexler, 2003). When

viewing these scenarios, they also have decreased activity in brain regions

responding to loss and increased activity in those regions associated with pleasure

and risk taking (van Holst, van Den Brink, Veltman and Goudriaan, 2010). It is still

unclear whether the brain regions associated with problem gambling overlap with

those related to substance abuse (Potenza et al, 2003; Grant, Brewer and Potenza,

2006). However, some medical treatments used for substance abuse are used to treat

problem gambling and have been found to be effective (Bullock and Potenza, 2013).

There is also some evidence that problem gambling is associated with abnormal

levels of various neurotransmitters, such as serotonin, dopamine, endogenous

opioids and hormones (Grant, Brewer and Potenza, 2006). It is not yet clear whether

these anomalies in neurological function are inherited (Lin, Lyons, Scherrer, Griffith,

True, Goldberg and Tsuang, 1998).

For less severe problem gamblers, brief interventions like warning messages

have been used to reduce the gambling behaviour. This approach appears to be

useful for some of them (Hodgins, 2005) but not for others (Steenbergh, Whelan,

Meyers, May and Floyd, 2004). Courses of cognitive-behavioural therapy (CBT)

typically last longer than brief interventions: in Gooding and Tarrier's (2009) study,

the minimum effective CBT session length was four hours. There are different

variants of CBT. These range from correction of perceptions about gambling,

desensitization to images of gambling, and reduction in motivations to gamble. Some

studies have shown that CBT is effective in reducing gambling behaviours (Sylvain,

Ladouceur and Boisvert, 1997; Gooding and Tarrier, 2009). Psychopharmacological

treatments have also been used, with or without behavioural therapies, to reduce

37

problem gambling and some of these have been found to be effective (Leung and

Cottler, 2009; Bullock and Potenza, 2013).

Research has found that risk preference is related to the level of certain

hormones, particularly testosterone. Men and women who have high testosterone

levels are more risk seeking than their low testosterone level counterparts (Stanton,

Liening and Schultheiss, 2011). Men naturally have higher testosterone levels than

women and they are more risk seeking. Adolescent males and females in different

stage of puberty have different levels of testosterone and their testosterone levels are

positively related to their risk seeking behaviours (Op de Macks, Gunther Moor,

Overgaauw, Güroğlu, Dahl and Crone, 2011). Injecting women with testosterone

results in reduced sensitivity to loss and increased risk seeking (Van Honk, Schutter,

Hermans, Putman, Tuiten and Koppeschaar, 2004; Eisenegger and Naef, 2011).

Furthermore, a low ratio of the length of the index finger to the ring finger, an

indicator of pre-birth testosterone levels inside mother's uterus, is associated with

high levels of risk seeking (Neave, Laing, Fink and Manning, 2003; Stenstrom, Saad,

Nepomuceno and Mendenhall, 2011). All these findings imply that risk preference

has a biological basis and can be influenced by long-term and short-term testosterone

levels.

In summary, people may become problem gamblers because they

overestimate their chances of winning, because they suffer emotional vulnerabilities

that are temporarily offset by gambling, or because they have neurological

abnormalities manifested in various antisocial behaviours that include gambling.

Problem gamblers may have abnormal brain activity or neurotransmitter levels. High

testosterone level predicts high risk preference.

38

In the chapter 6, I will discuss the difference between those who can and

cannot make money from gambling. It seems that limiting loss chasing is the key to

losing less money or even to winning more. Problem gamblers lacks the ability to

control loss.

39

Chapter 4. The gamblers' fallacy creates the hot-hand effect

To date, there is little research on real gambling. The research reported in this

chapter demonstrates the existence of the hot hand effect in gambling, investigates

gamblers’ beliefs in the hot hand effect and the gamblers’ fallacy, and finally

explores the causal relationship between the hot hand effect and the gamblers’

fallacy.

4.1 Data set

A large real online gambling database was used. In this analysis, streaks of

winning and streaks of losing were used to detect the relationship between the hot

hand effect and the gamblers' fallacy.

The complete gambling history of 776 gamblers between 1 Jan 2010 and 31

Dec 2010 was obtained from an online gambling company. The gamblers were

selected randomly from the customer database. In total, 565,915 sports exchange

bets were placed by these gamblers during the year. In sports exchange, gamblers put

or take odds against each other. Characteristics of the samples are shown in Table 2.

40

Table 2. Sample characteristics for sports bets placed in each of three currencies for

the year 2010.

GBP

EUR

USD

Number of bets

371,306

162,077

32,532

Number of gamblers

407

318

51

Mean stake

£145

(1,482)

€395

(5,555)

$50

(321)

Median stake

£14

€18

$15

Maximum stake

£313,900

€1,492,000

$20,500

Mean number of bets placed by a single

account

917

517

641

Median number of bets placed by a single

account

171

88

153

Number of horse racing bets

260,550

34,659

8,290

Number of football bets

69,863

90,415

12,058

Number of greyhound racing bets

28,859

6,660

9,159

Each gambling record included the following information: game type (e.g.,

horse racing, football, and cricket), game name (e.g. Huddersfield v West

Bromwich), time, stake, type of bet, odds, result, and payoff. Each person was

identified by a unique account number. All the bets they placed in the year were

arranged in chronological order by the time of settlement, which was precise to the

minute. The time when the stake was placed was not available. According to the

gambling house, there is no reason to think that the stake was placed long before the

time of the settlement. Each account used one currency, which was chosen when the

account was opened; no change of currency was allowed during the year.

41

4.2 Methodology and results

If there is a hot hand effect, then, after a winning bet, the probability of

winning the next bet should go up. I compared the probability of winning after

different run lengths of previous wins with the probability of winning not following

a winning streak (Figure 1).

42

Figure 1. Probability of winning after obtaining winning streaks of different lengths

(o) and after not obtaining winning streaks of those lengths (Δ).

43

First, we counted all the bets in GBP; there were 178,947 bets won and

192,359 bets lost. The probability of winning was 0.48.

Second, we took all the 178,947winning bets and counted the number of bets

that won again; there were 88,036 bets won. The probability of winning was 0.49. In

comparison, following the 192,359 lost bets, the probability of winning was 0.47.

The probability of winning in these two situations was significantly different (Z =

12.10, p < .0001).

Third, we took all the 88,036 bets, which already had won twice and

examined the results of bets that followed these bets. There were 50,300 bets won.

The probability of winning rose to 0.57. In contrast, the probability of winning did

not rise after gambles that did not show a winning streak: it was 0.45. The

probability of winning in these two situations was significantly different (Z = 60.74,

p < .0001).

Fourth, we examined the 50,300 bets which already won three times and

checked the result of the bets followed them. I found that 33,871 bets won. The

probability of winning went up again to 0.67. In contrast, the bets not having a run of

lucky predecessors showed a probability of winning of 0.45. The probability of

winning in these two situations was significantly different (Z = 90.63, p < .0001).

Fifth, we used the same procedure and again took all the 33,871 bets which

already won four times. We checked the result of bets followed these bets. There

were 24,390 bets won. The probability of winning went up again to 0.72. In contrast,

the bets without a run of previous wins showed a probability of winning of only

0.45. The probability of winning in these two situations was significantly different

(Z = 91.96, p < .0001).

Sixth, we used the same method to check the 24,390 bets which already won

44

five times in a row. There were 18,190 bets won, giving a probability of winning of

0.75. After other bets, the probability of winning was 0.46. The probability of

winning in these two cases was significantly different (Z = 86.78, p < .0001).

Seventh, we examined the 18,190 bets that had won six times in a row.

Following such a lucky streak, the probability of winning was 0.76. However, for the

bets that had not won on the immediately preceding occasion, the probability of

winning was only 0.47. These two probabilities of winning were significantly

different. (Z = 77.50, p < .0001).

The results showed that gamblers were more likely to win after winning

streaks, i.e. hot hand effects exist. The hot hand also occurred for bets in other

currencies (Figure 1). Regressions (Table 2) show that, after each successive

winning bet, the probability of winning increased by 0.05 (t(5) = 8.90, p < .001) for

GBP, by 0.06 for EUR (t(5) = 8.00, p < .001), and by 0.05 for USD (t(5) = 8.90, p <

.001).

We used the same approach to analyze the gamblers’ fallacy. If the gamblers’

fallacy is not a fallacy, the probability of winning should go up after losing several

bets. I also compared the probability of winning in this situation to to the probability

of winning not following a losing streak.

The first step was same as in the analysis of the hot hand. We counted all the

bets in GBP; there were 178,947 bets won and 192,359 bets lost. The probability of

winning was 0.48 (Figure 2, top panel).

45

Figure 2. Probability of winning after obtaining losing streaks of different lengths (o)

and after not obtaining losing streaks of those lengths (Δ).

In the second step, we identified the 192,359 bets that lost and examined

results of the bets immediately after them. Of these, 90,764 won and 101,595 lost.

46

The probability of winning was 0.47. After the 178,947 bets that won, the probability

of winning was 0.49. The difference between these two probabilities were significant

(Z = 12.01, p < 0.001).

In the third step, we took the 101,595 bets that lost and examined the bets

following them. We found that 40,856 bets won and 60,739 bets lost. The probability

of winning after having lost twice was 0.40. In contrast, for the bets that did not lose

on both of the previous rounds, the probability of winning was 0.51. The difference

between these probabilities was significant (Z = 58.63, p < 0.001).

In the fourth step, we repeated the same procedure. After the 60,739 bets that

had lost three times in a row, there were 19,142 winning bets won and losing 41,595

bets ones, giving a probability of winning of 0.32. For other bets, this probability

was 0.51 (Z = 88.26, p < 0.001).

The fifth, sixth and seventh steps were carried out in an analogous way. They

showed that the probability of winning after four lost bets was 0.27, after five lost

bets was 0.25, and after six lost bets was 0.23.

The pattern was similar for bets in other currencies (Figure 2). Regressions

(Table 2) showed that each successive losing bet decreased the probability of

winning 0.05 (t(5) = 9.71, p < .001) for GBP, by 0.05 for EUR (t(5) = 9.10, p < .001)

and by 0.02 for USD (t(5) = 7.56, p < .001). This is bad news for those who believe

in the gamblers’ fallacy.

47

Table 3. Regressions for length of streaks predicting the probability of winning.

B

SE B

β

t

Sig.(p)

F

𝑅

2

GBP

Win

0.475

0.021

0.053*(0.006)

8.902

<0.001

79.25

0.928

Lose

0.489

0.018

-0.047*(0.004)

9.711

<0.001

94.31

0.940

EUR

Win

0.439

0.026

0.059*(0.007)

8.223

<0.001

67.62

0.917

Lose

0.508

0.021

-0.053*(0.006)

9.100

<0.001

82.8

0.932

USD

Win

0.315

0.025

0.054*(0.007)

7.996

<0.001

63.93

0.913

Lose

0.386

0.010

-0.022*(0.003)

7.560

<0.001

57.15

0.904

Note: The independent variable is the number of bets taken into consideration.

4.3 Do gamblers with long winning streaks have higher payoffs? No.

One potential explanation for the appearance of the hot hand is that gamblers

with long winning streaks consistently do better than others. To examine this

possibility, we compared the mean payoff of these gamblers with the mean payoff of

the remaining gamblers.

Among 407 gamblers using GBP, 144 of them had at least six successive

wins in a row on at least one occasion. They had a mean loss of £1.0078 (N =

279,162, SD = 0.47) for every £1 stake they placed. The remaining 263 gamblers

had a mean loss of £1.0077 (N = 92,144, SD = 0.38) for every £1 stake they placed.

The difference between these two was not significant.

We performed same analysis for bets made in EUR. Among 318 gamblers

using this currency, 111 of them had at least one winning streak of six. They had a

mean loss of €1.005 (N = 105,136, SD = 0.07) for every €1 of stake. The remaining

207 EUR gamblers had a mean loss of €1.002 (N = 56,941, SD = 0.22). The

difference between these two returns was significant (t (162,075) = 4.735, p <

48

0.0001). Those who had long winning streaks actually lost more than others. They

did not win more.

The results in USD also failed to show that those with long winning streaks

won more. Seventeen gamblers had at least one winning streak of six and 34 did

not. For those who had, the mean loss was $1.022(N = 23,280, SD = 0.75); for those

who had not, it was $1.029 (n = 9,252, SD = 0.35). There was no significant

difference between the two ( t(32530) = 0.861, p = 0.389). The gamblers who had

long winning streaks were not better at winning money than gamblers who did not

have them.

4.4 The effects of winning and losing streaks on level of odds selected.

To determine whether the gamblers believed in the hot hand or gamblers’

fallacy, we examined how the results of their gambling affected the odds of their

next bet. Among all GBP gamblers, the mean level of selected odds was 7.72 and the

median odds was 1.11 (N = 371,306, SD = 37.73). After a winning bet, lower odds

were chosen for the next bet. The mean odds dropped to 6.19 and the median odds to

0.61, (N = 178,947, SD = 35.02). Following two consecutive winning bets, the mean

odds decreased to 3.60 and the median odds to 0.32 (N = 88,036, SD = 24.69).

People who had won on more consecutive occasions a person selected less risky

odds. This trend continued (Figure 3a and 3b, top panel).

49

Figure 3a. Mean preferred odds after winning (o) and losing (Δ) streaks of different

lengths.

50

Figure 3b. Median preferred odds after winning (o) and losing (Δ) streaks of

different lengths.

51

After a losing bet, the opposite was found. People who had lost on more

consecutive occasions selected riskier odds. After six lost bets in a row, the mean

odds went up to 17.07 and the median odds to 6.00 (N = 22,694, SD = 50.62). In

comparison, after winning six times in a row, the figure for mean odds was 0.85, and

the median odds was 0.15 (N = 18,252, SD = 9.82). From the odds that they selected,

we can infer that gamblers followed the gamblers’ fallacy but were unaffected by the

hot hand.

The gambling results were affected by the gamblers’ choice of odds. One

point increase in the odds reduced the probability of winning by 0.035 (SD = 0.003, t

(36) = 13.403, p < .001).

4.5 The effects of winning and losing streaks on stake size

Among all GBP gamblers, the median stake was £14 (N = 371,306,

Interquartile Rang = 4.80 - 53.29). After winning once, the median stake went up to

£18.47 (N = 178,947, Interquartile Range = 5.04 - 66.00). After winning twice in a

row, the median stake rose to £20.45 (N = 88,036, Interquartile Range = 8.00 -

80.00) (Figure 4, top panel).

52

Figure 4. Median stake size after winning (o) and losing (Δ) streaks of different

lengths.

For gamblers who lost, the opposite was found. People who had lost on more

consecutive occasions decreased their stakes more. After losing once, the median

53

stake went down to £10.89 (N = 192,359, Interquartile Range = 4.00 - 44.16). After

losing twice in a row, the median stake dropped to £10.00 (N = 101,595,