1

Table of Contents

I. EXECUTIVE SUMMARY ................................................................................................... 3

1. Overview ............................................................................................................................. 3

2. Summary of Committee Staff Findings ........................................................................... 4

3. Broader Implications ......................................................................................................... 5

d. Recommendations ............................................................................................................ 11

II. COMMITTEE RESPONSE TO MEME STOCK MARKET EVENT .......................... 14

III. COMMITTEE STAFF FINDINGS ................................................................................... 15

Key Finding #1: Robinhood exhibited troubling business practices, inadequate risk

management, and a culture that prioritized growth above stability during the Meme Stock

Market Event. ............................................................................................................................ 15

Key Finding #2: Broker-dealers facing the greatest operational and liquidity concerns took the

most expansive trading restrictions, although multiple broker-dealers introduced trading

restrictions for a variety of risk management reasons during the Meme Stock Market Event. 70

Key Finding #3: Most of the firms the Committee spoke to do not have explicit plans to change

their policies for how they will meet their collateral requirements during extreme market

volatility or adopt trading restrictions when market volatility may warrant their introduction.96

Key Finding #4: The Depository Trust & Clearing Corporation (DTCC) waived $9.7 billion of

collateral deposit requirements on January 28, 2021. The DTCC lacks detailed, written policies

and procedures for waiver or modification of a "disincentive” charge it calculates for brokers

that are deemed to be undercapitalized and has regularly waived such charges during periods of

acute volatility in the two years before the Meme Stock Market Event. ................................ 101

IV. POLICY RECOMMENDATIONS .................................................................................. 108

1. Understanding the Influx of Retail Traders ................................................................ 109

2. Enhancing Supervision of Retail Facing “Superbrokers” ......................................... 110

3. Strengthening Capital and Liquidity Requirements and Oversight ......................... 114

2

APPENDIX I: GLOSSARY ..................................................................................................... 118

APPENDIX II: HEARINGS AND LEGISLATION IN RESPONSE TO MEME STOCK

MARKET EVENT .................................................................................................................... 121

1. Introduction .................................................................................................................... 121

2. Hearing Series Overview ............................................................................................... 121

3. Key Issues ....................................................................................................................... 124

4. Proposed Legislation ...................................................................................................... 130

APPENDIX III: THE U.S. GOVERNMENT ACCOUNTABILITY ORGANIZATION

(GAO) FOUND SIGNIFICANT GAPS IN THE SEC’S OVERSIGHT OF FINRA IN

CONGRESSIONALLY MANDATED REPORTS ............................................................... 133

3

I. EXECUTIVE SUMMARY

1. Overview

GameStop Corporation (GME), AMC Entertainment Holdings, Inc. (AMC), and other

“meme stocks” became extraordinarily popular on social media leading into January 2021.

Institutional investors bet against these stocks, predicting they would fall in price, while retail

traders took the other side of that bet, purchasing the stocks en masse.

1

This trading frenzy,

collectively referred to in this report as the “Meme Stock Market Event,” drove historic market

volatility, which reached a crescendo on January 28, 2021, when the gross market value of GME

cleared in the stock market was 21,318% greater as compared to January 4, 2021.

2

At the height of the Meme Stock Market Event, several stock trading platforms restricted

trading on meme stocks as an emergency risk management tactic. Others suffered outages in their

technology systems due to the order volume in their trading systems. These restrictions and outages

placed downward pressure on meme stocks. The total dollar amount of GME held by Robinhood

Markets, Inc. (Robinhood)

3

customers decreased from a peak of $2.6 billion before the firm

enacted trading restrictions on January 28, 2021, down to $1.2 billion the next day. The total dollar

amount of AMC held by Robinhood customers decreased from $1.3 billion to $411 million in the

same time frame.

4

Ultimately, these trading restrictions and outages limited market access for

ordinary retail investors and undermined confidence in market integrity.

The House Financial Services Committee (Committee) held a full Committee hearing

shortly after the Meme Stock Market Event with key industry players, including the CEOs of

Robinhood and Citadel Securities, and followed up with two more full Committee hearings,

multiple pieces of legislation, and a full investigation of the Meme Stock Market Event.

5

The

Committee’s thorough response to the Meme Stock Market Event uncovered structural

1

As used in this report, the term “meme stocks” refers to several stocks that surged in popularity due to social media

discourse (See Appendix I

: Glossary for terms highlighted in this report).

2

In this report, we refer to the volatility experienced in the pricing and trading of meme stocks during January and

February of 2021, and the related actions taken by various broker-dealers, as the “Meme Stock Market Event.” DTCC,

NSCC Equity Clearing & Settlement Overview: Presentation to House Staff, at slide 7 (Jun. 17, 2021) (on file with

the Committee).

3

Robinhood Markets is the parent company of Robinhood Financial, Robinhood Securities, and Robinhood Crypto.

As used in this report, “Robinhood” most often refers to Robinhood Markets. Occasionally, taken in context,

“Robinhood” refers to Robinhood Markets and / or its affiliates in a collective sense.

4

Email and attachments to email from Counsel for Robinhood to Committee staff (May 20, 2021) (on file with the

Committee).

5

House Committee on Financial Services, Virtual Hearing - Game Stopped? Who Wins and Loses When Short Sellers,

Social Media, and Retail Investors Collide (Feb. 18, 2021); House Committee on Financial Services, Virtual Hearing

– Game Stopped? Who Wins and Loses When Short Sellers, Social Media, and Retail Investors Collide, Part II (Mar.

17, 2021); House Committee on Financial Services, Virtual Hearing - Game Stopped? Who Wins and Loses When

Short Sellers, Social Media, and Retail Investors Collide, Part III (May 06, 2021).

4

deficiencies exploited by a new generation of “superbroker” retail trading platforms that have

grown in popularity amidst a surge in retail trading.

The stock market has changed significantly in recent years. Robinhood pioneered a new

business model marked by commission-free trading supported by payment for order flow (PFOF),

in which trading platforms route their customers’ orders to market making firms like Citadel

Securities for a fee.

6

In this business model, brokers can profit from volatility in the stock market

as increased trading activity generates more PFOF rebates. Accordingly, Robinhood and other

retail-oriented brokers are incentivized to push their customers to make as many trades as possible

through digital engagement features that include “game-like features and celebratory animations,”

lenient extension of margin trading to their customers, and increased access to fractional shares,

enabling retail traders to purchase dollar increments of expensive stocks like Amazon and

Berkshire Hathaway.

7

This “superbroker” business model has proliferated quickly.

The Meme Stock Market Event raises questions about how retail trading market

infrastructure currently operates and whether it is appropriately designed and regulated to

accommodate new developments. The events of January 28, 2021 exposed inadequacies in the risk

management practices of broker-dealers, concerns about the ways in which PFOF increases

complexity and potential fragility in the securities markets, and the ability of the regulators charged

by Congress to oversee financial markets to assess and correct for liquidity and operational risks.

2. Summary of Committee Staff Findings

Key Finding #1: Robinhood exhibited troubling business practices, inadequate risk management,

and a culture that prioritized growth above stability during the Meme Stock Market Event.

Examples of the firm’s problematic response to the Meme Stock Market Event include:

• Robinhood’s disproportionately high order flow and unique formula for calculating PFOF

rebates strained several market makers and introduced risk to the stock market.

Robinhood’s PFOF formula became a point of contention between Robinhood and Citadel

Securities during the Meme Stock Market Event.

• Robinhood asserted to the public and testified to the Committee that the company was

“always comfortable with [its] liquidity” leading up to its historic trading restrictions,

despite the actions undertaken by Robinhood’s executive leadership to respond to liquidity

issues it faced in the days leading up to the Meme Stock Market Event.

• Robinhood relied on incomplete statistical models for calculating its collateral obligations

leading into the Meme Stock Market Event. The company did not incorporate “best

practices” observations from the Financial Industry Regulatory Authority (FINRA) for

6

In this report, unless otherwise specified, references to “Robinhood” are to Robinhood Markets, Inc., and its

consolidated subsidiaries.

7

SEC, Staff Report on Equity and Options Market Structure Conditions in Early 2021 (Oct. 14, 2021).

5

improving its stress tests nor did it utilize publicly available guidance from the Depository

Trust and Clearing Corporation (DTCC) for calculating collateral obligations.

• Robinhood received a waiver of the largest component of its deposit requirement from the

DTCC. Without this waiver, which Robinhood had no control over, the company would

have defaulted on its regulatory collateral obligations. Robinhood’s Chief Legal Officer

notified senior officials at the DTCC that Robinhood could not meet its collateral

obligations before the market opened on January 28, 2021.

Key Finding #2: Broker-dealers facing the greatest operational and liquidity concerns took the

most extensive trading restrictions, although multiple broker-dealers introduced trading

restrictions for a variety of risk management reasons during the Meme Stock Market Event.

Key Finding #3: Most of the firms the Committee spoke to do not have explicit plans to change

their policies for how they will meet their collateral requirements during extreme market volatility

or adopt trading restrictions when market volatility may warrant their introduction.

Key Finding #4: The Depository Trust & Clearing Corporation (DTCC) waived $9.7 billion of

collateral deposit requirements on January 28, 2021. The DTCC lacks detailed, written policies

and procedures for waiver or modification of a "disincentive” charge it calculates for brokers that

are deemed to be undercapitalized and has regularly waived such charges during periods of acute

volatility in the two years before the Meme Stock Market Event.

3. Broader Implications

a. The Meme Stock Market Event revealed how rapid growth and innovation in

retail trading presents novel issues for market stability and orderliness that

neither the industry nor regulators have satisfactorily anticipated or addressed.

By some estimates, retail investors accounted for roughly 20% of stock market activity on

average through the first half of 2021 and up to 25% on peak trading volume days, up from 10%

over the prior year.

8

A significant proportion of this market activity was generated by first-time

investors.

9

In recent years, the number of total trading accounts has risen sharply at retail trading

focused trading platforms such as Robinhood and Apex Clearing Corporation.

8

Bloomberg Markets: European Open, Citadel Securities’ Mecane Says Volatility Behind Rise in Retail

Investing, Bloomberg (July 9, 2021).

9

Between January 1, 2015 and March 31, 2021, over half of the customers who funded accounts on Robinhood said

that it was their first broker-dealers account. A June 2021 survey from Charles Schwab found that 15% of all retail

investors who were active in 2021 began trading in 2020.

A February 2021 FINRA report found that new investors–

—those who did not own a taxable investment account prior to 2020–—were younger, more racially diverse, and had

lower incomes than the established stock market investors. FINRA reported that nearly two-thirds of the new investors

were under 45, and approximately one-third of this same group held account balances of $500 or less. Among the top

6

Figure 1: Total Open Accounts for Select Clearing Brokers

10

reasons new investors cited for opening investor accounts in 2020 were to save for retirement and the ability to invest

with a small amount of money. SEC, Form S-1 for Robinhood Markets Inc. (July 01, 2021); Charles Schwab,

The

Rise of the Investor Generation:15% of U.S. Stock Market Investors got their start in 2020, Schwab Study shows

(accessed Jun. 30, 2021); FINRA, Investing 2020: New Accounts and the People Who Opened Them (Feb. 2021);

Letter from counsel for Robinhood to Chairwoman Waters and Chairman Green (Sept. 20, 2021). According to

Robinhood as of September 20, 2021 27% of its customers are “racially and ethnically diverse”; FINRA,

Investing

2020: New Accounts and the People Who Opened Them (Feb. 2021).

10

Total open account information compiled from email correspondence and various attachment with counsels for

Apex Clearing Corporation, E*TRADE, Charles Schwab / TD Ameritrade, and Robinhood Markets. Data is non-

public information compiled specifically for the Committee and is not kept in the ordinary course of business. In this

instance, the Committee uses total open accounts rather than active accounts because different companies use different

methodologies to calculate the number of “active accounts” they list publicly. Charles Schwab and TD Ameritrade

merged in October 2020 and began integrating their customer base shortly thereafter. The number of accounts shown

here reflect the pro forma combined number of total open accounts for these companies for the periods shown. Apex

Clearing Corporation clears for hundreds of firms, primarily stock trading apps which focus on retail investors. The

0

5

10

15

20

25

30

35

40

45

4Q21

3Q21

2Q21

1Q21

4Q20

3Q20

2Q20

1Q20

4Q19

3Q19

2Q19

1Q19

4Q18

3Q18

2Q18

1Q18

4Q17

3Q17

Total Open Accounts for Select Clearing Brokers (millions)

7

This surge in retail trading has provided retail investors with greater access to the market.

But it also carries risks. The “superbroker” business model pioneered by Robinhood—marked by

commission-free trading, fractional investing,

11

gamification,

12

and the ability to create an account

and start trading within minutes—makes it easier than ever to participate in the stock market for

entertainment value, akin to a “high-stakes multiplayer game.”

13

The trends developing with new

generations of investors will most likely continue. Apex Clearing estimates that within the next 25

years, $70 trillion of wealth is expected

to transfer from Baby Boomers to

younger generations, including

Millennials and Generation Z, who are

more likely to favor stocks that are

popular on social media.

14

When asked about the Meme

Stock Market Event in early 2021, Apex

Clearing Corporation’s CEO, Bill

Capuzzi commented to Committee staff,

“We’ve lowered the barriers to entry.

There’s great content. We’re helping

people invest in their future. And we see

it. There’s millions more people that are

able to invest that never had a chance to

before. That is great. And that’s going to

continue and, frankly, accelerate, right? I

think the impact of social media, I think,

is going to continue to evolve. And so, if

the question is, do I think it’s going to

happen again, the answer is, yes, for

dip in Apex Clearing accounts shown beginning in early 2019 occurred after Robinhood Securities came online and

began migrating customer accounts from Apex to its own clearing broker subsidiary. Robinhood had previously

contracted with Apex to clear its trades. Total open account numbers for Charles Schwab dropped in 4Q 2021 when

its subsidiary, TD Ameritrade closed approximately 1 million accounts deemed to be inactive based upon having a $0

account balance and no transfers for 12 months prior to closing (briefing with counsel for Schwab/TDA (Feb. 14,

2022)).

11

Modern stock trading platforms have popularized the ability of retail investors to portion a fractional share. A

fractional share is any portion of a stock less than a complete share. Offering investing in fractional shares has allowed

retail investors to purchase a modest dollar figure in stocks like Berkshire Hathaway and Amazon, which can cost

thousands of dollars per share.

12

Many modern stock trading platforms such as Robinhood, Webull, and others use app designs intended to increase

consumer engagement, time spent on an investment platform, and number of trades through gamification. The

amalgamation of these features has led to criticism that gamified online trading platforms promote user engagement

by encouraging trading behavior similar to a gambling addiction. Cyrus Farivar,

Gambling addiction experts see

familiar aspects in Robinhood app, NBC (Jan. 30, 2021).

13

Farhad Manjoo, Can We Please Stop Talking About Stocks, Please?, The New York Times (Feb. 3, 2021).

14

Apex Clearing, Apex Next Investor Outlook: Q2 2021 Top 100 Stocks (accessed on Jun. 21, 2022).

A

ND SO

,

IF THE QUESTION IS

,

DO

I

THINK

IT’S GOING TO HAPPEN AGAIN, THE

ANSWER IS, YES, FOR SURE. NO DOUBT

ABOUT IT. HOW IT’S GOING TO MANIFEST

ITSELF, I’M NOT SURE, BUT FOR SURE

IT’S GOING TO HAPPEN AGAIN.

- BILL CAPUZZI,

CEO, APEX CLEARING CORPORATION

8

sure. No doubt about it. How it’s going to manifest itself, I’m not sure, but for sure it’s going to

happen again.”

15

Retail investor trends, like stocks gaining popularity on social media, increasingly affect

the price and trading volume of securities.

16

This has implications for market activity, trading

infrastructure, and regulation. The full range of market participants, infrastructure providers, and

regulators that Committee staff spoke with during its investigation acknowledged this new reality.

Financial services companies that introduce new practices and innovations must carefully

assess and prepare for the potential impact and risk that such innovations pose to market integrity

and stability. Specifically, firms must rigorously evaluate how innovations will affect their ability

to meet existing regulatory requirements before introducing them and be mindful of new problems

that such innovations may cause so that they can engage in adequate and proactive risk

management.

Moreover, regulators must ensure broker-dealers properly assess and prepare for the full

implications of such new innovations. The Meme Stock Market Event demonstrated the need for

the modernization of our retail market regulatory architecture and the ways in which it anticipates,

detects, and corrects for capital, liquidity, and operational risks associated with the rapid growth

of retail trading and the technological and business model innovations facilitating such growth.

This report highlights some of these shortcomings to ensure that regulators and market participants

can address regulatory gaps and better hold individual firms to account.

b. The Meme Stock Market Event demonstrates the need for modernization of

certain key aspects of the self-regulatory framework for retail facing

“superbrokers.”

The regime of Self-Regulatory Organizations (SROs), overseen by the Securities and

Exchange Commission (SEC), will need to further evolve to fully address the risks generated by a

new generation of retail-facing, self-directed broker-dealers referred to throughout this report as

“superbrokers.” Based on the Committee’s investigation, FINRA could more adequately respond

to current market dynamics with a modernized liquidity rule. In addition, the Committee’s

investigation revealed that DTCC’s subsidiary, the National Securities Clearing Corporation

(NSCC)—which sets and enforces rules for clearing equities—engaged in insufficient monitoring

of its membership and has regularly waived certain clearing fund obligations prior to the Meme

Stock Market Event. Collectively, these regulatory shortcomings may have contributed to the lack

15

Interview with W. Capuzzi (Apex Clearing Corporation), at 31 (Jun. 24, 2021) (emphasis added).

16

Erin Gobler, What Is a Meme Stock?, The Balance (Oct. 13, 2021).

9

of preparedness that certain retail broker-dealers exhibited in their ability to navigate the capital

and liquidity challenges of the Meme Stock Market Event.

17

The Committee’s investigation found that FINRA and the SEC have limited rules focused

on liquidity management practices of retail customer-focused broker-dealers. While FINRA has

previously issued guidance on this topic, its guidance is non-binding and does not require

systematic liquidity reviews of broker-dealers. Liquidity and capitalization issues are assessed

regularly by FINRA for broker-dealers through risk monitoring policies and procedures that

inform exam planning. However, FINRA’s routine cycle examinations review capitalization and

liquidity on a case-by-case basis for individual broker-dealers and are not mandatory.

Neither FINRA nor the SEC have a standalone liquidity rule. FINRA can only require

compliance with the SEC’s net capital rule during cycle examinations, which many industry

experts whom the Committee spoke to during its investigation considered outdated. Outside of

requiring compliance with SEC rules, FINRA issues nonbinding observations relating to liquidity

during examinations. Without an updated liquidity rule from the SEC, and because FINRA does

not have its own capital and liquidity rule, FINRA lacks an adequate foundation to more fully

police the liquidity of its member firms.

Similarly, there are opportunities for the NSCC to modernize and improve how it oversees

member firms. While the NSCC maintains a system to assess the credit risk posed by its members,

including both a “Watch List” and an “Enhanced Surveillance List,” the latter category is not

clearly defined and member firms that are placed on Enhanced Surveillance are not notified of

17

FINRA has recognized shortcomings in this regard, including in testimony provided to the Committee by FINRA’s

CEO and President. FINRA has made preliminary efforts to address such liquidity risk management concerns by

proposing new liquidity related reporting and has indicated to Committee staff that it is considering further potential

reforms. FINRA,

Proposed Rule Change to Adopt a Supplemental Liquidity Schedule, and Instructions Thereto,

Pursuant to FINRA Rule 4524 (Supplemental FOCUS Information) (accessed on Jan. 27, 2020); FINRA briefing with

the Committee (Jan. 26, 2021); House Committee on Financial Services, Testimony of Robert W. Cook, Game

Stopped? Who Wins and Loses When Short Sellers, Social Media, and Retail Investors Collide, Part III, 117

th

Cong.

(May 06, 2021).

10

their inclusion on the list.

18

This lack of transparency misses an opportunity for the NSCC to

communicate to relevant member firms the need to adopt remedial measures.

19

Furthermore, the Committee’s investigation revealed how the NSCC has regularly waived

certain clearing fund requirements in the two years before the Meme Stock Market Event. The

NSCC regularly waives or reduces its Excess Capital Premium charges, which are the component

of a broker’s collateral charge intended to incentivize member firms to maintain an adequate

capital cushion. Excess Capital Premium charges rise exponentially the less capitalized a broker is

relative to how risky its uncleared portfolio is. The NSCC’s regular waiver and/or modification of

Excess Capital Premium charges most often benefit member firms that regularly attract these

charges.

20

The apparent repeated failure of Excess Capital Premium charges from deterring such

firms from accumulating excessive risk is concerning.

Furthermore, based on the Committee’s review of NSCC data, over the two years prior to

the Meme Stock Market Event, the higher the aggregate Excess Capital Premium charges assessed,

the more likely the NSCC was to waive them. While NSCC rules permit discretion in waiving or

reducing Excess Capital Premium charges, the rules contain only limited guidance detailing how

or when it is appropriate to waive or modify such charges.

21

This lack of detailed guidance

undermines the predictability of NSCC decision-making during exigent market circumstances,

such as during the Meme Stock Market Event, which, in turn, leads to confusion and uncertainty

amongst NSCC member firms.

18

Member firms are placed on the “Watch List” if their credit rating, as measured by a credit rating system specified

in NSCC rules, is assessed at a 5, 6 or 7 or if the NSCC otherwise considers that other relevant factors make a particular

member firm pose a heightened risk to the clearinghouse. See NSCC, Rules and Procedures – Rule 1

, at 21 (Jan. 24,

2022). NSCC’s credit rating system considers both “(i) quantitative factors, such as capital, assets, earnings and

liquidity and (ii) qualitative factors, such as management quality, market position/environment, and capital and

liquidity risk management.” See Id. at 5 (Jan. 24, 2022). Members placed on the Watch List may also be required to

maintain a clearing fund deposit over and above the amounts otherwise determined by NSCC procedures to safeguard

the clearinghouse from excessive risk posed by such member to the NSCC itself See Rule 2(B)€ of Id.€at 38 (Jan. 24,

2022). The Enhanced Surveillance List consists of a smaller subset of firms that are on the Watch List. See DTCC

briefing with the Committee (Sept. 14, 2022). With respect to both the Watch List and the Enhanced Surveillance List,

NSCC rules state that: “a Member or Limited Member being subject to enhanced surveillance or being placed on the

Watch List shall result in a more thorough monitoring of the Member’s or Limited Member’s financial condition

and/or operational capability, which could include, for example, on-site visits or additional due diligence information

requests from the Corporation [i.e., NSCC]. In addition, the Corporation may require a Member or Limited Member

placed on the Watch List and/or subject to enhanced surveillance to make more frequent financial disclosures,

including, without limitation, interim and/or pro forma reports. Members and Limited Members that are subject to

enhanced surveillance are also reported to the Corporation’s management committees and regularly reviewed by a

cross-functional team comprised of senior management of the Corporation. The Corporation may also take such

additional actions with regard to any Member or Limited Member (including a Member or Limited Member placed

on the Watch List and/or subject to enhanced surveillance) as are permitted by the Rules and Procedures. See NSCC,

Rules and Procedures – Rule 2(B)(e), at 38 (Jan. 24, 2022).

19

Committee staff recognize that NSCC has proposed rule changes to address certain redundancies in the Watch List

and Enhanced Surveillance List system.

20

DTCC briefing with the Committee (Jun. 17, 2021).

21

NSCC briefing with the Committee (Jan. 21, 2022); NSCC, NSCC Rules and Procedures - Procedure XV I.(B)(2)

(Jan. 01, 2021). Footnote 7 to Section I.(B)(2) of Procedure XV (Clearing Fund Formula and Other Matters).

11

c. The Meme Stock Market Event exposed weaknesses in capital and liquidity

planning and in the robustness of the technology platforms of financial services

institutions upon which the orderly functioning of the stock market relies.

Over the course of the Committee’s investigation, interviews with multiple broker-dealers

revealed considerable confusion, inconsistency, and lack of awareness amongst retail-oriented

broker-dealers as to how the NSCC collateral requirements are calculated. Many member firms

lack a full understanding of how the NSCC’s Excess Capital Premium charges are assessed.

Prominent firms, such as Robinhood, did not model for Excess Capital Premium charges as part

of their capital and collateral planning processes prior to the Meme Stock Market Event, and there

are no industry-wide best practices on how firms can ensure that they have adequate capital and

liquidity to meet NSCC margin requirements.

More worrisome, according to the NSCC, certain broker-dealers that are familiar with

Excess Capital Premium charges have decided to remain thinly capitalized and consciously risk

attracting these charges on a regular basis.

22

Given that the NSCC often waives these charges,

these firms may feel that they are unlikely to be seriously penalized for such risky behavior.

Finally, the Committee’s investigation discovered evidence of multiple broker-dealers,

third party clearing operations, market makers, public stock exchanges, and others suffering

technology outages during the Meme Stock Market Event. Outages are particularly concerning

among market makers, who are, by many accounts, lightly regulated and play an increasingly

significant role in executing retail trades.

23

There is currently no FINRA or SEC requirement for

broker-dealers to be active members of a public exchange, and on January 28, 2021, Robinhood

was not connected to the New York Stock Exchange, Nasdaq, or any other public exchange where

it could have routed customer trades for execution. Instead, Robinhood was solely reliant on its

market maker firms to execute trades, most of whom were struggling under significant operational

stress in the face of historic volume and volatility. Had the market makers Robinhood routinely

routed orders to been unable to accept its order flow, the company would have been unable to

execute trades for its customers.

d. Recommendations

Pursuant to its oversight authority, the Committee has provided a list of recommendations

for possible regulatory reforms at the SEC, FINRA, and the DTCC to increase resiliency,

transparency, oversight of, and access to, the equity markets. These recommendations reflect

recent developments in the stock market, including the influx of retail investors and the rise of

prominent “superbrokers” with millions of retail customer accounts. These potential reforms

include greater attention to the identification of potential problems that may be caused by

22

DTCC briefing with the Committee (Jul. 06, 2021).

23

Members of Congress, consumer advocates, and regulators discussed the risks associated with the concentration of

retail trading in market making firms during the Committee’s three hearings on the meme stock market event. SEC

Chair Gary Gensler raised concerns that such concentration could lead to market fragility. For additional detail, see

Appendix II

: Hearings and Legislation in Response to Meme Stock Market Event.

12

technological or other changes to market entry that lead to broader participation by individual

investors. Potential reforms also include alternatives to how the NSCC assesses and applies margin

charges, enhanced risk management, liquidity management and reporting requirements for

clearing brokers, and other similar measures. In summary, these recommendations include the

following:

Understanding the Influx of Retail Traders

Congress should adopt legislation mandating key regulators, including the SEC and

FINRA, to study how existing market rules and supervision will need to evolve to

address new technological developments, including the possibility of social media

driven market activity.

The SEC should consider ways to implement trading halts tailored to respond to

concentrated volatility in a limited number of stocks.

Enhancing Supervision of Retail Facing “Superbrokers”

Congress should adopt legislation requiring broker-dealers that execute above a

pre-determined threshold of customer orders to establish and maintain a connection

to a public market.

Congress should adopt legislation requiring broker-dealers that make markets and

provide liquidity to other broker-dealers, which process above a pre-determined

threshold of order flow, to be subject to Regulation SCI.

The SEC and FINRA should enhance large, retail facing broker-dealer

examinations and mandate stress tests that focus on liquidity management,

including to account for the prospect of social media driven market volatility.

The SEC and FINRA should introduce a requirement for clearing brokers to

establish written contingency plans to address extreme market volatility and fully

disclose both the contingency plans and any trading restrictions to the market in

real time. Such written contingency plans should be reviewed regularly by the SEC

and FINRA.

Congress should adopt legislation that directs FINRA to conduct more thorough

supervision of the broker-dealer industry, and the SEC should conduct more

thorough oversight of FINRA’s activities and any corrective actions FINRA may

propose.

When individual firms introduce trading restrictions, they should be required to

notify the SEC and FINRA. Once introduced, FINRA should engage in enhanced

13

monitoring to ensure that such trading restrictions are appropriate, tailored, and in

place no longer than necessary.

Strengthening Capital and Liquidity Requirements and Oversight

The SEC should introduce capitalization requirements for clearing brokers.

The SEC should introduce a liquidity rule for clearing brokers. FINRA should

establish a rules-based framework governing liquidity planning for clearing

brokers.

The DTCC and its subsidiary, the NSCC, should revisit how it conducts

surveillance of member firms that may pose a greater risk, and FINRA should also

focus more systematically on assessing the sufficiency of clearing brokers’ liquidity

planning.

The DTCC and its subsidiary, the NSCC, should introduce clear written policies

and procedures and establish transparency around the circumstances under which

the DTCC may waive an Excess Capital Premium charge; such decisions should be

subject to review by the SEC.

The DTCC, its subsidiary the NSCC, the SEC, and Congress should introduce an

emergency backstop funding facility for NSCC member firms that provide

emergency liquidity to the NSCC.

14

II. COMMITTEE RESPONSE TO MEME STOCK MARKET

EVENT

In the week after the Meme Stock Market Event, the Committee sent document request

letters to several broker-dealers on February 4, 2021, for records and communications related to

trading restrictions, as well as each firm’s policies and procedures to respond to market volatility.

24

On February 18, 2021, the Committee held the first in a series of three full Committee hearings to

gather information on the Meme Stock Market Event. The first hearing featured testimony from

the CEOs of major financial services institutions involved in the Meme Stock Market Event,

including Robinhood, Citadel Securities, and Melvin Capital. The second hearing, held on March

17, 2021, featured testimony from market experts and advocacy organizations. The final full

Committee hearing on May 6, 2021, featured testimony from the SEC Chair, the CEO of FINRA,

and the CEO of the DTCC.

In addition to the three full Committee hearings on the Meme Stock Market Event, the

Committee engaged on market oversight with hearings on credit rating agencies on May 11, 2022,

and July 16, 2021, and oversight of public exchanges, including the New York Stock Exchange

and Nasdaq on March 30, 2022.

The Committee investigated the Meme Stock Market Event over the course of

approximately 18 months, conducting more than 50 interviews with 20 institutions and reviewing

more than 95,000 pages of responsive material received from stock trading platforms, clearing

brokers, regulators, social media companies, and other related parties in response to our numerous

information requests. This report comprises one part of the Committee’s response to the Meme

Stock Market Event, which included hearings and consideration of legislation addressing issues

such as gamification, short sale disclosure, payment for order flow, and other related issues (See

Appendix II: Hearings and Legislation in Response to Meme Stock Market Event).

Committee staff prepared this report to highlight the structural issues that the Meme Stock

Market Event exposed. Experts that Committee staff spoke to agreed that while aspects of the

Meme Stock Market Event were idiosyncratic, they expect market volatility driven by retail

investors empowered by technology to be a recurrent trend.

25

24

Letter from Chairwoman Waters to Walter W. Bettinger, II, CEO of The Charles Schwab Corporation (Feb. 04,

2021); Letter from Chairwoman Waters to Karl A. Roessner, CEO of E*TRADE Financial Corporation (Feb. 04,

2021); Letter from Chairwoman Waters to Milan Galik, CEO of Interactive Brokers LLC (Feb. 04, 2021); Letter from

Chairwoman Waters to Vladimir Tenev, CEO of Robinhood Markets, Inc. (Feb. 04, 2021); Letter from Chairwoman

Waters to Steve Boyle, CEO of TD Ameritrade (Feb. 04, 2021); Letter from Chairwoman Waters to Anthony Denier,

CEO of Webull Financial LLC (Feb. 04, 2021).

25

See Section III(3); Robinhood briefing with the Committee (Sept. 14, 2021); Letter from counsel for Robinhood to

Chairwoman Waters and Chairman Green (Sept. 20, 2021); Interview with W. Capuzzi (Apex Clearing Corporation),

at 31 (Jun. 24, 2021).

15

III. COMMITTEE STAFF FINDINGS

Key Finding #1: Robinhood exhibited troubling business practices, inadequate

risk management, and a culture that prioritized growth above stability during

the Meme Stock Market Event.

a. Robinhood experienced conditions that limited its customers’ ability to access the

stock market prior to the Meme Stock Market Event.

Robinhood’s unpreparedness to meet its regulatory capital obligations and the ensuing

trading restrictions on January 28, 2021,

was not the first time the company

experienced conditions that limited its

customers’ ability to participate in the

stock market. Robinhood suffered several

technological outages through 2018 and

2019 affecting millions of its

customers.

26

Most notably, on March 2–

3, 2020 Robinhood’s website and mobile

app shut down, locking its entire

customer base out of their accounts

during a time of historic market volatility amidst the onset of the COVID-19 pandemic.

27

On June

30, 2021, FINRA issued the largest fine in its history to Robinhood for the company’s March 2020

outages and for systemic supervisory failures (the “March 2020 Fine”).

28

Among FINRA’s

findings in the June 2021 settlement, FINRA found that Robinhood failed to supervise technology

critical to providing its customers with “core” broker-dealer services and failed to create a

reasonably designed business continuity plan.

29

b. Prior to the Meme Stock Market Event, Robinhood did not update its stress test used

to predict collateral obligations to clearing agencies after FINRA made an

observation to Robinhood Securities’ Chief Financial Officer that the company may

want to take a more conservative “best practices” approach to conducting stress tests.

Prior to the COVID-19 pandemic, FINRA conducted a 2019 Cycle examination of

Robinhood Securities.

30

FINRA’s examination program conducts periodic firm examinations,

often referred to as “cycle exams,” to ensure compliance with FINRA rules and federal securities

laws and regulations. FINRA’s cycle exams are risk-based and can vary in focus, and thus tailored

26

FINRA, Letter of Acceptance, Waiver, and Consent (No. 202006971201) (Jun. 30, 2021).

27

Id.

28

Maggie Fitzgerald, Robinhood to pay $70 million for outages and misleading customers, the largest-ever FINRA

penalty, CNBC (Jun. 30, 2021); Email from FINRA to Committee staff (Mar. 03, 2022).

29

FINRA, Letter of Acceptance, Waiver, and Consent (No. 202006971201) (Jun. 30, 2021).

30

Email from FINRA to Committee staff (Mar. 03, 2022).

Robinhood exhibited troubling

business practices, inadequate

risk management, and a culture

that prioritized growth above

stability during the Meme Stock

Market Event.

16

to the individual broker-dealer that is the subject of the examination. These examinations are

designed in coordination with the risk monitoring analysts assigned to the broker-dealer.

31

Risk

analysts review liquidity and capital issues as a matter of regular practice, however there is no

mandatory liquidity or capitalization review as part of routine cycle examinations; rather, such

areas may be subject to closer scrutiny if related business or financial practices, characteristics,

history, or other factors unique to the broker-dealer are identified as a source of concern.

32

As part of FINRA’s 2019 cycle examination of Robinhood, FINRA evaluated Robinhood

Securities’ stress tests as part of its review of the firm’s liquidity management practices. Stress

tests are simulations that broker-dealers run to approximate how they might respond in a crisis

considering any difficulty the firm might have meeting its financial obligations during periods of

severe stress. FINRA encourages firms to make use of stress tests to prevent failure of the firm

and guard against widespread systemic failure of the stock market during market turbulence.

FINRA provides limited guidance on how firms should conduct stress tests.

33

In April 2020, shortly after the onset of the COVID-19 pandemic, FINRA concluded its

2019 cycle examination of Robinhood Securities and communicated deficiencies and observations

to the firm. Based upon FINRA’s internal review, FINRA records show on-site and pre-exit

meetings related to the 2019 cycle exam where FINRA officials shared an observation with

Robinhood Securities regarding the company’s stress test.

34

Specifically, FINRA examiners made an observation regarding Robinhood’s methodology

for calculating its required collateral deposits for clearing agencies like the NSCC, the Options

Clearing Corporation (OCC), and the Depository Trust Company (DTC) used in its stress tests.

35

At the time, Robinhood’s stress tests used a “day zero” assumption for the firm’s collateral charges

with its clearing agencies, using whatever firm’s collateral charge from the last day of the previous

quarter and doubling that number. FINRA examiners communicated an oral observation that from

a conservative “best practices” standpoint, the company would be better served by using the peak

collateral charges and doubling that number instead.

36

According to FINRA’s records, Robinhood

Securities officials, including the Chief Financial Officer and the Regulatory Inquiries Manager

for Robinhood Securities, were present for discussions of Robinhood Securities incorporating their

peak clearing deposits for stress tests.

37

Robinhood had difficulty finding any evidence of feedback

that FINRA may have provided regarding collateral charge assumptions the company used in their

31

Id.

32

In contrast, risk monitoring analysts generally review liquidity and capital issues as a matter of regular practice.

Email from FINRA to Committee staff (Mar. 03, 2022).

33

FINRA, Guidance on Liquidity Risk Management Practices (Sept. 2015).

34

Email from FINRA to Committee staff (Jun. 21, 2022).

35

Email and attachments to email from representatives for FINRA to Committee staff (Jun. 20, 2022).

36

Email and attachments to email from Counsel for Robinhood to Committee staff (Jun. 20, 2022).

37

Email from FINRA to Committee staff (Jun. 19, 2022).

17

stress test, and commented to Committee staff that it cannot corroborate FINRA’s documentation

of these discussions.

38

In any event, Robinhood did not update its stress tests according to FINRA’s observation

before the Meme Stock Market Event.

39

In fact, Robinhood conducted a quarterly stress test

exercise in mid-January of 2021, prior to the Meme Stock Market Event using its collateral charges

from the prior quarter end rather than the peak collateral charges as FINRA staff had suggested.

FINRA’s observation would have led Robinhood to adapt a more conservative method for

conducting a stress test than the standard FINRA guidance on this matter. Taking the approach

outlined in FINRA’s observation would have been a more accurate measure of the actual highest

collateral charges the firm would be likely to be charged during periods of heightened volatility.

As a result, the stress test that Robinhood ran in January 2021, mere days before the Meme Stock

Market Event, did not more fully reflect the collateral charges with clearing agencies the firm

should have anticipated.

Any increase in Robinhood’s capital position could have had a significant impact. For

example, Robinhood’s NSCC collateral charges on December 31, 2020, the most recent quarter

end before January 28, 2021, which the firm actually used in its January 2021 stress test, was as

follows:

Figure 2: Robinhood’s NSCC collateral charges (Dec. 31, 2020)

Date

Deposit Requirement (Start of Day)

12/31/2020 $72,774,074.93

40

The company’s top NSCC collateral charge for 2020, a level more than four times higher,

which FINRA observed would be a more “best practices,” conservative approach

41

for modeling

Robinhood’s stress test, was as follows:

Figure 3: Robinhood’s highest NSCC collateral charges (2020)

Date

Deposit Requirement (Start of Day)

6/10/2020 $299,855,653.27

38

FINRA conducted an accuracy review of this sub-finding and confirmed that the Committee’s descriptions of events

are correct. Email from FINRA to Committee staff (Jun. 21, 2022); Briefing with counsel for Robinhood (Jun. 21,

2022); Robinhood briefing with the Committee (Nov. 03, 2021).

39

Email from Robinhood to Committee staff (Feb. 08, 2022)

40

Letter from counsel for Robinhood to Chairwoman Waters and Chairman Green (Dec. 15, 2021).

41

Email and attachments to email from Counsel for Robinhood to Committee staff (Jun. 20, 2022).

18

The difference between the two numbers when doubled in a stress test is nearly half a

billion dollars (approximately $140 million versus $600 million). Consider the fact that Excess

Capital Premium charges (the main contributor to Robinhood’s NSCC clearing fund requirement

on January 28, 2021) rise exponentially the less well capitalized a broker-dealer is relative to the

volatility in their unsettled portfolio. When Committee staff inquired why FINRA would

communicate its observations regarding Robinhood’s stress tests orally without making an official

written finding, FINRA responded that its practice is to only memorialize deficiencies in writing

to the firm. In this case, there was no liquidity rule, no rule violation, and the firm was in

compliance with the SEC’s net capital rule (which many experts the Committee spoke with during

its investigation considered to be outdated).

42

This rule framework illustrates a gap in the current supervision of liquidity planning

practices and a need to modernize the supervisory framework that applies to a new generation of

retail broker-dealers, particularly at the time of the Meme Stock Market Event.

43

Lacking a more

updated rule framework governing liquidity, a more conservative approach to the assumptions

used to model their clearing fund obligations at the NSCC and other clearing agencies in

Robinhood’s stress tests could have alerted the company to the need to raise additional capital

prior to January 28, 2021.

c. Robinhood relied on incomplete internal models without fully utilizing the NSCC’s

publicly available resources for modeling collateral charges, leaving Robinhood

unprepared to accurately calculate its collateral charges on January 28, 2021.

Robinhood’s CEO, Vlad Tenev, represented in Congressional testimony before this

Committee that January 28, 2021, was an “unmodellable,” “Black Swan event.”

44

While it is

impossible to know how the company could have reacted to the Meme Stock Market Event with

different internal processes and controls, the Committee’s investigation found that Robinhood’s

models used for calculating its clearinghouse collateral obligations in the days before the Meme

Stock Market Event were incomplete, and therefore grossly underestimated how much the

company would owe in collateral obligations on January 28, 2021.

The DTCC and the National Securities Clearing Corporation (NSCC)—the DTCC’s

subsidiary for clearing equities—serve as a central counterparty clearinghouse for the stock

42

FINRA has taken several actions to respond to both the volatility from the onset of COVID-19 and the Meme Stock

Market event, which includes new and revised protocols and procedures including the adoption of a Supplemental

Liquidity Schedule. However, the Committee’s investigation has also identified multiple areas in which FINRA could

conduct more thorough oversight of broker-dealers. For instance, during the course of the investigation, Committee

staff learned that the SEC and FINRA do not require firms to notify them of trading restrictions, to maintain written

plans for emergency capital raisings or liquidity arrangements, or to conduct stress tests to specifically determine

broker-dealers’ ability to offer market access to customers during periods of peak volatility.

42

43

The SEC reviewed 69 FINRA examinations from fiscal year 2021 and found numerous. Related reports have

demonstrated the SEC has been slow to implement programs that might increase the effectiveness of FINRA

supervision. For further discussion of various shortcomings with the SEC’s oversight of FINRA, see Appendix III:

The U.S Government Accountability Organization (GAO) Found Significant Gaps in the SEC’s Oversight of FINRA

in Congressionally Mandated Reports.

44

House Committee on Financial Services, Virtual Hearing - Game Stopped? Who Wins and Loses When Short

Sellers, Social Media, and Retail Investors Collide (Feb. 18, 2021).

19

market.

45

As a central counterparty, the NSCC is at the heart of processing trades in the U.S.

equities market and reduces settlement risk for both buying broker-dealers and selling broker-

dealers, each of which are NSCC member firms.

46

Customers execute trades through their broker,

and those brokers match trades through a public exchange like Nasdaq, a market making firm like

Citadel Securities, or another trading venue, but those venues ultimately direct all securities trades

through the NSCC for clearing.

47

If an NSCC member firm defaults on its obligations, the NSCC stands in the defaulted

firm’s place and delivers cash and securities to the non-defaulting members.

48

The NSCC requires

individual member firms to deposit collateral, or margin, to protect against the risk of a member

firm’s default.

49

Following the outages that occurred on Robinhood’s platform in March of 2020 (which

ultimately led to FINRA levying the March 2020 fine), Robinhood was placed on the NSCC’s

Enhanced Surveillance List.

50

However, in keeping with existing NSCC practices, the NSCC did

not notify Robinhood that it had been placed on this list and was now subject to greater scrutiny.

Moreover, Robinhood’s incomplete liquidity planning practices were neither detected by the

clearinghouse nor remedied despite the company being subject to enhanced surveillance.

Specifically, in addition to the problematic assumptions that Robinhood used in its stress

tests in mid-January 2021, Robinhood’s internal models used to predict its NSCC collateral

charges leading into the week of January 28, 2021, did not account for the prospect of Excess

Capital Premium charges—a significant component of the NSCC’s collateral charge regime that

applies when a broker-dealer is deemed to be undercapitalized.

51

As the market becomes more

volatile, and particularly as an individual broker-dealer’s uncleared portfolio becomes riskier, the

NSCC collateral deposit requirements for that individual broker-dealer increases.

52

In particular,

45

Wyatt Wells, Certificates and Computers: The Remaking of Wall Street, 1967 to 1971, Business History Review,

74 (2): 193–235 (Jan. 1, 2000); House Committee on Financial Services, Testimony of Michael C. Bodson

, Game

Stopped? Who Wins and Loses When Short Sellers, Social Media, and Retail Investors Collide, Part III, 117th Cong.

(May 06, 2021).

46

“Clearing brokers,” who are responsible for executing and processing trades, are members firms of clearinghouses.

“Introducing brokers,” who interface with individual clients and assist them in opening accounts, are not themselves

members of clearinghouses. Certain brokers only act as introducing brokers and contract with a third-party clearing

broker to provide clearing services. Webull is an example of a broker-dealers that acts as only an introducing broker

and, in its case, relies on a contractual arrangement with Apex to clear and process trades initiated by Webull’s

customers on its platform.

47

DTCC briefing with the Committee (Jun. 17, 2021).

48

Id.

49

DTCC briefing with the Committee (Jun. 17, 2021). This is also referred to as a member firm’s “clearing fund

requirement.”

50

DTCC briefing with the Committee (Jul. 22, 2021).

51

See Appendix I: Glossary for definition of “Excess Capital Premium charge”; SEC, Self-Regulatory Organizations;

Fixed Income Clearing Corporation and National Securities Clearing Corporation; Notice of Filing and Order

Granting Accelerated Approval of Proposed Rule Changes to Institute a Clearing Fund Premium Based Upon a

Member’s Clearing Fund Requirement to Excess Regulatory Capital Ratio (Sept. 15, 2006) (Release No. 34-54457);

House Committee on Financial Services, Testimony of Michael C. Bodson, Game Stopped? Who Wins and Loses

When Short Sellers, Social Media, and Retail Investors Collide, Part III, 117th Cong. (May 06, 2021); DTCC briefing

with the Committee (Jul. 06, 2021).

52

DTCC briefing with the Committee (Jun. 17, 2021); DTCC briefing with the Committee (Oct. 28, 2021).

20

the Excess Capital Premium charge Increases exponentially based upon how risky a broker-

dealer’s uncleared portfolio is deemed to be relative to its capitalization.

53

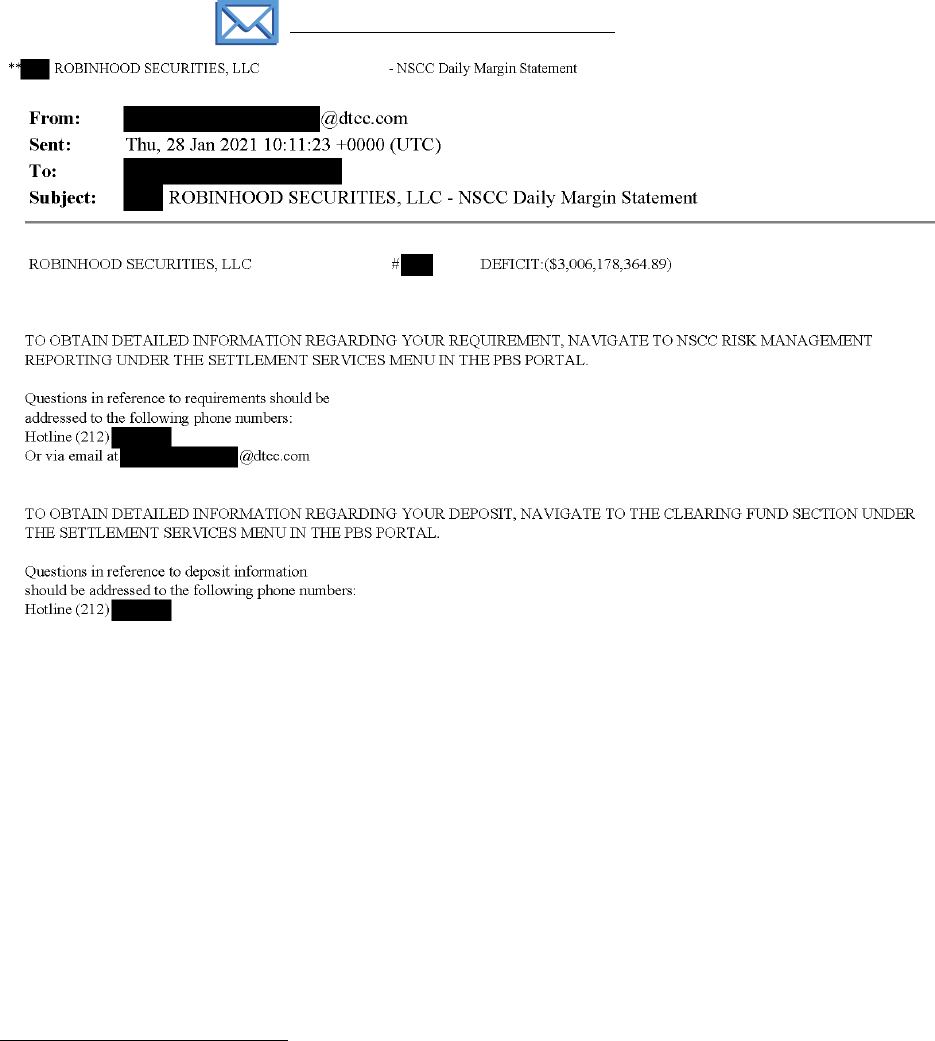

The NSCC assessed a $3.7 billion collateral charge to Robinhood on January 28, 2021,

based on the risk in Robinhood’s uncleared portfolio relative to the company’s capitalization. This

charge, which ultimately prompted Robinhood’s trading restrictions, had several components. The

two largest components were the Value-at-Risk charge, which totaled $1.3 billion, and the Excess

Capital Premium charge, which totaled $2.2 billion.

54

During interviews with Committee staff,

Robinhood officials confirmed that the company was only modeling for its potential Value-at-Risk

charge for the week of January 25, 2021.

55

In other words, Robinhood had no visibility into the

possibility of, much less the precise level of, Excess Premium Capital charges that it could be

required to pay during the Meme Stock Market Event.

On January 28, 2021, after learning of its collateral charge for the day, Robinhood

operational staff first accessed and utilized the publicly available formula that the NSCC uses to

calculate Excess Capital Premium charges.

56

Three weeks after the Meme Stock Market Event, on

February 18, 2021, the company first incorporated the Excess Capital Premium charge into a

mathematical model used to estimate when such a charge could be assessed.

57

Then, on May 27,

2021, four months after the Meme Stock Market Event, the firm began regularly modeling what

its Excess Capital Premium charge would be if it exceeded its net capital.

58

Robinhood’s Head of

Data Science confirmed that updating the models is relatively straightforward as the company uses

Excel spreadsheets to model its NSCC collateral charge rather than more sophisticated machine

learning algorithms.

59

Despite the acknowledged simplicity of its model and the NSCC’s public release of its

formula for calculating collateral charges, Robinhood’s Head of Data Science commented

internally that Robinhood’s collateral charges were a “black box” to him the day before Robinhood

received its historical collateral charge.

60

Furthermore, the NSCC neither notified Robinhood that

the firm was under Enhanced Surveillance, nor conducted any form of supervision that would have

uncovered the incompleteness of Robinhood’s calculations for modeling collateral obligations.

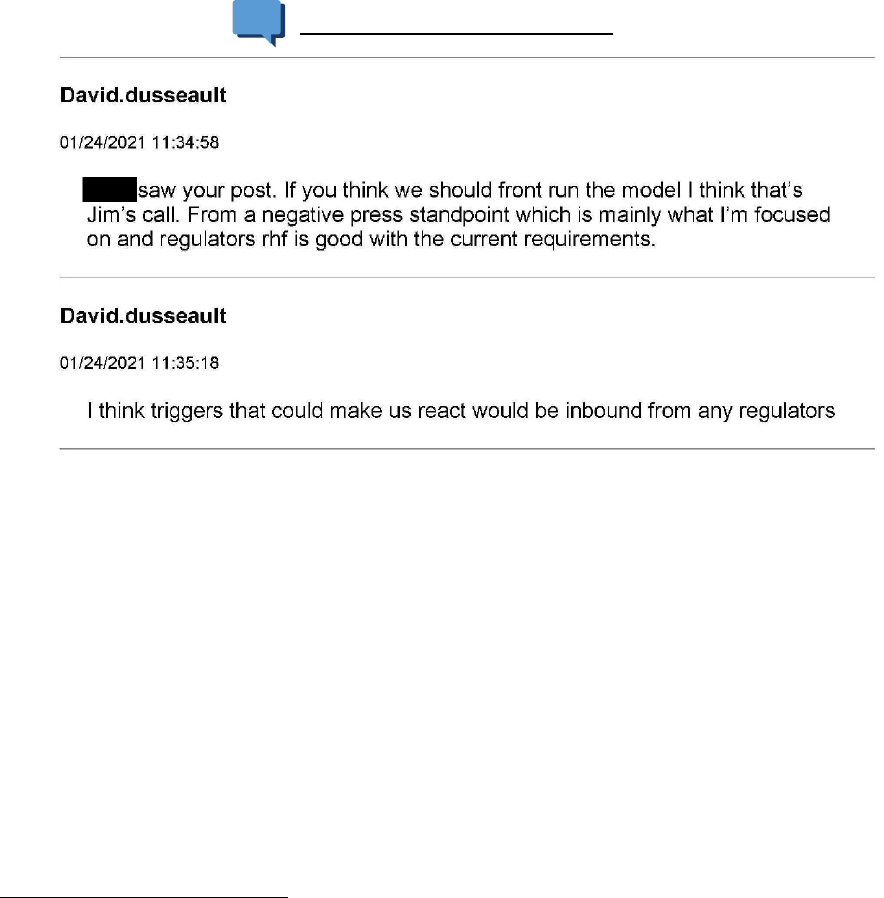

d. On Sunday, January 24, 2021, Robinhood leadership hesitated to model volatility

before the start of the trading week

On January 24, 2021, the Sunday before Robinhood experienced a liquidity crisis and had

difficulty in meeting its NSCC collateral requirements, a senior manager in Robinhood’s treasury

department advocated modelling the company’s collateral obligations in an abundance of

53

DTCC briefing with the Committee (Jul. 06, 2021).

54

Letter from counsel for Robinhood to Chairwoman Waters and Chairman Green (Sept. 20, 2021).

55

Letter from counsel for Robinhood to Chairwoman Waters and Chairman Green (Dec. 15, 2021).

56

Letter from counsel for Robinhood to Chairwoman Waters and Chairman Green (Dec. 15, 2021).

57

Id.

58

Id.

59

Robinhood briefing with the Committee (Nov. 03, 2021).

60

RH_HFSC_00029119 (on file with the Committee).

21

caution.

61

Note that even with this cautious approach, its models did not account for Excess Capital

Premium charges. However, David Dusseault, President and Chief Operating of Robinhood

Financial, the subsidiary of Robinhood that operates the company’s brokerage through its app and

website, suggested that “triggers” that would make the firm react more fully to the surging

volatility going into the trading week would be “inbound from… regulators.”

62

Figure 4: RH_HFSC_00020687

63

The senior manager in Robinhood’s treasury department sent an internal message, urging

the company to not wait to run the models until trading opened the next day.

64

She also responded

to Dusseault, saying that she was “thinking about this from a risk perspective though you guys are

balancing many other concerns.”

65

e. On Monday, January 25, 2021, Robinhood focused its efforts on accommodating

rapid growth, even as it faced severe operational strain in its internal systems and

nearly missed a deadline to its options clearinghouse that would have prompted a

liquidity crisis within Robinhood.

The next day, Monday, January 25, 2021, Robinhood executives observed a sharp increase in

meme stock activity.

66

Gretchen Howard, Robinhood’s Chief Operating Officer commented,

“VERY high volume coming in today… Possibly Gamestop trending on twitter and wall street

bets.” Robinhood CEO, Vlad Tenev and Robinhood’s Head of Data Science agreed.

67

61

RH_HFSC_00020687 (on file with the Committee).

62

Id.

63

RH_HFSC_00020687 (on file with the Committee).

64

Id.

65

Id.

66

RH_HFSC_00006682 (on file with the Committee).

67

Id.

22

At the same time, Robinhood employees noticed operational concerns within the company

relative to the sharp rise in volume and warned that volume would most likely increase.

68

The

company’s Head of Data Science commented that the “success of GME short squeeze and people

knowing more about other short squeezes WSB (wallstreetbets) is talking about may lead to a ton

of volume in the next few weeks.”

69

In response, a Robinhood engineering manager responded,

“today was a huge day. There are internal things that are starting to buckle under pressure.”

70

As market activity increased, the company faced challenges as various systems became

overwhelmed. For example, the firm’s Automated Customer Account Transfer Service (ACATS),

which is used to transfer securities from one trading account to another, and various files and

reports, such as Robinhood’s Automated Clearing House (ACH) file, faced operational strain.

71

Robinhood’s Head of Data Science and his team worked throughout the week to make sure the

company’s systems remained operational.

72

As Jim Swartwout, President and Chief Operating

Officer for Robinhood’s clearing operation commented to his employees, the increasing volume,

to the extent it created longer delays in processing for internal systems, was unsustainable.

73

Figure 5: RH_HFSC_00006803

74

Robinhood employees were particularly worried about submitting a critical file to the

Options Clearing Corporation (OCC) on a timely basis. The OCC is a clearinghouse that provides

central counterparty clearing and settlement services for the securities derivates market.

75

The

OCC serves a similar role for the derivatives market as the NSCC serves in the equities market.

When calculating daily broker-dealer dealer margin requirements, the OCC permits broker-dealers

68

RH_HFSC_00005965 (on file with the Committee).

69

RH_HFSC_00005965 (on file with the Committee).

70

Id.

71

RH_HFSC_00006803 (on file with the Committee)

72

Robinhood briefing with the Committee (Nov. 03, 2021).

73

RH_HFSC_00006803 (on file with the Committee).

74

RH_HFSC_00006803 (on file with the Committee).

75

OCC, What is OCC? (accessed Jan. 27, 2021).

23

to offset long and short positions in the same security so as to lessen the total margin owed for the

day.

76

To obtain such an offset, broker-dealers must submit a file to the OCC that includes all of

its long and short positions by 9:00 p.m. EST each day.

77

If the broker-dealer does not submit a

request to offset securities, the OCC assumes there is no offset for each security and charges the

maximum margin. In other words, rather than long positions offsetting short positions in

calculating margin requirements, the OCC charges the full margin obligations for all the securities

in a broker-dealer’s uncleared portfolio.

78

On January 25, 2021, Robinhood faced operational strain on its systems used to calculate

its OCC spread file.

79

Given the historic volume and volatility in the markets, the OCC extended

the deadline for all broker-dealers to submit their spread file on January 25, 2021. Robinhood ran

various models to estimate its OCC obligations if it missed the extended deadline to submit its file

to the OCC.

80

On the night of January 25, 2021, Robinhood Securities’ Senior Director of Clearing

Operations estimated the OCC’s requirement to be approximately $1.6 to $1.9 billion if the

company was unable to submit its spread file by the deadline. He also advised that missing the

OCC deadline would almost certainly prompt a regulatory investigation of the firm.

81

Figure 6: RH_HFSC_00029036

82

Robinhood employees continued to work throughout the day to address the delays in its

systems used to calculate its OCC spread files. The company’s executive leadership, including Jim

76

Interview with J. Swartwout (Robinhood) (Oct. 22, 2021).

77

Id.

78

OCC, OCC Rules - Rule 1306 (accessed Jan. 27, 2022).

79

Interview with J. Swartwout (Robinhood) (Oct. 22, 2021).

80

Id.

81

RH_HFSC_00029036 (on file with the Committee).

82

The original chat message was edited by its author to change the word “shorts” to “spreads” in the second sentence

of the message. Id.

24

Swartwout and Gretchen Howard, expressed concerns about the impact of missing the OCC

deadline for submitting the spread file would have on the firm’s liquidity.

83

Figure 7: RH_HFSC_00006804

84

As Robinhood operational staff raced to meet the OCC’s deadline to avoid a liquidity crisis,

Robinhood’s executive leadership held an all-hands meeting and asked operational staff to discuss

ways to handle Robinhood’s rapid growth during the rising volatility, which many in the company

saw as a commercial opportunity.

85

Prior to the meeting, Jim Swartwout commented to a Clearing

Operations Manager at Robinhood Securities that perhaps instead of discussing ways to facilitate

the company’s rapid growth at the upcoming meeting, he should instead discuss all of the things

his team was doing to “keep the lights on” amidst the week’s spiking volatility.

86

Figure 8: RH_HFSC_00006669

87

83

RH_HFSC_00006804 (on file with the Committee).

84

Id.; RH_HFSC_00007056-57 (on file with the Committee).

85

RH_HFSC_00006669 (on file with the Committee); RH_HFSC_00028837 (on file with the Committee);

RH_HFSC_00029126 (on file with the Committee).

86

RH_HFSC_00006669 (on file with the Committee).

87

Id.

25

In response, the Clearing Operations Manager commented that Robinhood doesn’t handle

scale well, to which Jim Swartwout responded, “That is probably the biggest understatement of

the day….”

88

Figure 9: RH_HFSC_00006669

89

The Clearing Operations Manager further commented that she was struggling to understand

why the company should be discussing how to absorb further growth when “things are barely being

held together. Is there a focus I’m missing here?” She felt the company’s product team might be

better able to put a positive spin on the situation, but from an operational perspective, Robinhood

had failed its obligation to fully service its customers by struggling to complete its operational

obligations.

90

Figure 10: RH_HFSC_00006669

91

88

Id.

89

Id.

90

Id.

91

Id.

26

The OCC extended its deadline on the night of Monday, January 25, 2021 for Robinhood

and others, and extended the deadline by 60 to 90 minutes every other night of that week due to

the heightened volatility.

92

Robinhood was ultimately able to work through its system issues and

submitted its spread file to the OCC shortly before the extended deadline.

93

In communication

with Robinhood’s Head of Engineering after the company successfully submitted its file to the

OCC, Gretchen Howard commented, “Made it with 1 minute to spare!!!”.

94

Robinhood’s OCC collateral requirement was $92 million on January 25, 2021, rather than

the estimated $1.6 to $1.9 billion charge.

95

Robinhood employees ended the day aware that further

market volatility was likely,

96

Throughout the evening and into the night, Jim Swartwout remained

wary of regulatory scrutiny.

97

While Robinhood employees were relieved to have submitted their

OCC spread file on time, Swartwout remained cognizant of other operational difficulties that might

concern regulators and communicated such concerns to Gretchen Howard, including FINRA’s

concerns with Robinhood’s ability to continue processing fractional shares.

98

On the evening of

January 25, 2021, the company’s Head of Data Science warned that the company should not rule

out higher volume days for the rest of the week and suggested considering contingencies if

Robinhood missed the OCC’s deadlines in the future.

99

f. On Tuesday, January 26, 2021, Robinhood employees observed a historic spike in

trading activity on their platform following a tweet about GameStop posted by Tesla

CEO Elon Musk.

On Tuesday, January 26, 2021, employees at Robinhood continued to monitor market

activity and observe volume and volatility.

100

Popular momentum behind meme stocks continued

to increase, and at 4:08 p.m. EST, Tesla CEO Elon Musk tweeted “Gamestonk!!” with a link to

the wallstreetbets subreddit.

101

92

Interview with J. Swartwout (Robinhood) (Oct. 22, 2021).

93

RH_HFSC_00007056-57 (on file with the Committee).

94

Id.

95

Letter from counsel for Robinhood to Committee staff (Nov. 04, 2021).

96

RH_HFSC_00005969 (on file with the Committee).

97

RH_HFSC_00011695 (on file with the Committee).

98

Id.

99

RH_HFSC_00005969 (on file with the Committee).

100

Id.

101

Elon Musk (@elonmusk), Twitter post (Jan. 26, 2021, 4:08 p.m.) (accessed Jan. 27, 2022).

27

Figure 11: Twitter post from Elon Musk (@elonmusk)

102

As Robinhood employees monitored the number of customers applying to open an account

on their trading platform, they observed a historical spike directly following Mr. Musk’s tweet.

103

A product manager flagged the acute increase in activity internally.

104

102

Id.

103

RH_HFSC_00028836 (on file with the Committee); RH_HFSC_00028837 (on file with the Committee).

104

RH_HFSC_00028836 (on file with the Committee).

28

Figure 12: RH_HFSC_00028836

105

The same product manager commented, “we could probably interact with this movement

to promote RH growth,” to Robinhood’s Head of Data Science as they considered interacting with

the market activity to promote firm growth and reminding Robinhood customers that GME was

one of the stocks the company gave away as a free referral stock earlier in the company’s history.

106

105

Id.

106

RH_HFSC_00028837 (on file with the Committee).

29

Figure 13: RH_HFSC_00028837

107

On Tuesday, January 26, 2021, Robinhood once again faced system delays that threatened

its ability to submit its OCC spread file before the deadline. As Robinhood employees implored

the OCC for another extension of the deadline, senior leadership grew increasingly worried about

the impression the company’s recurring systems delay would leave with the clearinghouse. Jim

Swartwout texted Gretchen Howard on the afternoon of January 26, 2021, to say that if OCC

granted Robinhood another extension on submitting its spread file, the clearinghouse “may follow

up with why we needed it though. Which would not be good.”

108

107

Id.

108

RH_HFSC_00011697 (on file with the Committee).

30

g. On Wednesday, January 27, 2021, as Robinhood employees began to create trading

restrictions to slow volatility on their platform, they also sought to conceal the reasons

for implementing such restrictions from their customers and the public, even as they

feared restrictions could cause the market to crash.

On the morning of January 27, 2021, Robinhood employees continued to monitor market

activity and observe volume and volatility.

109

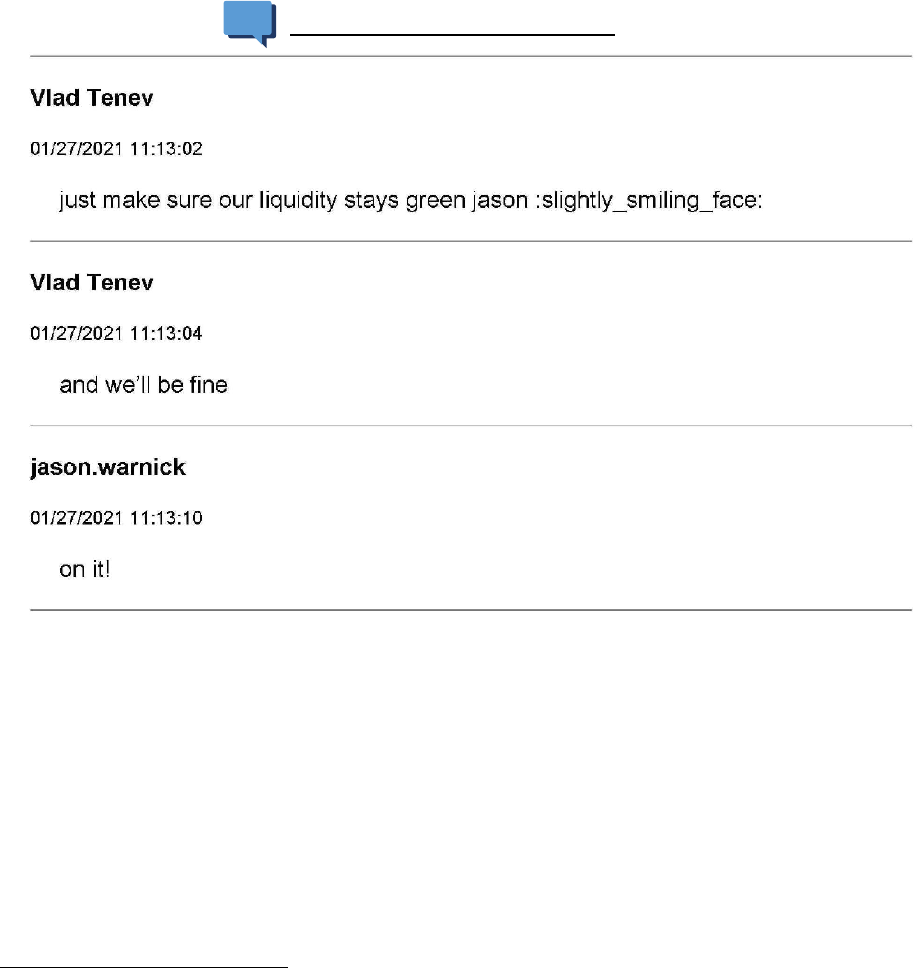

Vlad Tenev was concerned going into Wednesday,

January 27, 2021, about the company’s ability to maintain adequate liquidity as expressed to the

company’s Chief Financial Officer, Jason Warnick.

110

Figure 14: RH_HFSC_00007154

111

In interviews with Committee staff, Robinhood executives could not recall with specificity

when the idea of creating position limits for certain volatile stocks first arose.

112

Robinhood

employees worked to slow the velocity of trading within their platform.

113

Several different ideas

were discussed, but at first, position limits became the favored method to slow trading velocity.

109

Interview with J. Swartwout (Robinhood) (Oct. 22, 2021).

110

RH_HFSC_00007154 (on file with the Committee).

111

Id.

112

Interview with J. Swartwout (Robinhood) (May 05, 2021); Interview with G. Howard (Robinhood) (May 11, 2021).

113

RH_HFSC_00015755-69 (on file with the Committee).

31

Position limits limit the total number of stocks each customer can own in certain volatile stocks,

as compared to position closing only (PCO) restrictions, which prohibit customers from purchasing

certain stocks altogether.

114

Robinhood’s Head of Data Science expressed concerns that PCO

restrictions would look bad for the company, and also raised concerns that given the size of the

company, Robinhood placing PCO restrictions on specific symbols could trigger a market crash

in certain stocks.

115

Robinhood’s Head of Market Operations also expressed concern that PCO

restrictions could move the market given that Robinhood customers accounted for more than 10%

of the market.

116

Figure 15: RH_HFSC_00029118

117

As Robinhood employees worked through Wednesday, January 27, 2021, to code position

limits for meme stocks, they struggled with how to frame the trading restrictions to the public and

seemed to want to avoid giving their own clients the real reasons for imposing restrictions.

118

A

product manager at Robinhood Financial asked, “Do we have a customer facing rational we can

114

RH_HFSC_00015755-69 (on file with the Committee)

115