gsk.com

31 January 2024

Full-year and Q4 2023 results

Conference call and webcast for investors and analysts

2

This presentation may contain forward-looking statements. Forward-looking statements give the Group’s current expectations or forecasts of future events. An investor can identify these

statements by the fact that they do not relate strictly to historical or current facts. They use words such as ‘anticipate’, ‘estimate’, ‘expect’, ‘intend’, ‘will’, ‘project’, ‘plan’, ‘believe’, ‘target’ and

other words and terms of similar meaning in connection with any discussion of future operating or financial performance. In particular, these include statements relating to future actions,

prospective products or product approvals, future performance or results of current and anticipated products, sales efforts, expenses, the outcome of contingencies such as legal

proceedings, dividend payments and financial results.

Other than in accordance with its legal or regulatory obligations (including under the Market Abuse Regulations, UK Listing Rules and the Disclosure Guidance and Transparency Rules of

the Financial Conduct Authority), the Group undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

Investors should, however, consult any additional disclosures that the Group may make in any documents which it publishes and/or files with the US Securities and Exchange Commission

(SEC). All investors, wherever located, should take note of these disclosures. Accordingly, no assurance can be given that any particular expectation will be met and investors are

cautioned not to place undue reliance on the forward-looking statements.

Forward-looking statements are subject to assumptions, inherent risks and uncertainties, many of which relate to factors that are beyond the Group’s control or precise estimate. The

Group cautions investors that a number of important factors, including those in this presentation, could cause actual results to differ materially from those expressed or implied in any

forward-looking statement. Such factors include, but are not limited to, those discussed under Item 3.D ‘Risk factors’ in the Group’s Annual Report on Form 20-F for the full year (FY) 2022.

Any forward-looking statements made by or on behalf of the Group speak only as of the date they are made and are based upon the knowledge and information available to the

Directors on the date of this presentation.

A number of adjusted measures are used to report the performance of our business, which are non-IFRS measures. These measures are defined and reconciliations to the nearest IFRS

measure are available in the Q4 2023 earnings release and Annual Report on Form 20-F for FY 2022.

All guidance, outlooks and expectations regarding future performance and the dividend should be read together with the section “Guidance and outlooks, assumptions and cautionary

statements” on pages 54 to 55 of GSK’s full year and Q4 2023 stock exchange announcement and “Guidance and outlooks, assumptions and basis of preparation related to 2024

guidance, 2021-26 and 2031 outlooks" in the appendix of this presentation.

Basis of preparation: On 18 July 2022, GSK plc separated its Consumer Healthcare business from the GSK Group to form Haleon, an independent listed company. Comparative figures

have been restated on a consistent basis. Earnings per share, Adjusted earnings per share and Dividends per share have been adjusted to reflect the GSK Share Consolidation on 18 July

2022.

Cautionary statement regarding forward-looking statements

3

Agenda

Delivering commitments and upgrading outlooks

Emma Walmsley

2023 performance and guidance for 2024

Luke Miels, Deborah Waterhouse and Julie Brown

Outlooks for 2026

-2031

Emma Walmsley and Julie Brown

Q&A

Emma Walmsley, Tony Wood, Luke Miels, Deborah Waterhouse,

Julie Brown, and David Redfern

4

Delivering commitments and upgrading outlooks

Emma Walmsley, Chief Executive Officer

5

Sales growth

1

•

2021: 1%

•

2022: 10%

•

2023: 14%

Launches since 2021

1

• Arexvy

• Apretude

• Cabenuva

• Jemperli

• Ojjaara

Vaccines and Specialty

1

•

2021: 58% of sales

•

2022: 62% of sales

•

2023: 66% of sales

Significant delivery and improved performance since 2021

commitments

Business Development

7

Adj. operating margin

1

•

2021: 25.6%

•

2022: 28.5%

•

2023: 28.6%

Acquisitions:

Affinivax

Aiolos Bio

8

BELLUS Health

Sierra Oncology

Alliances:

Alector

Arrowhead

Halozyme

Hansoh Pharma

Ideya

Janssen Pharma

Mersana

Scynexis

Spero Therapeutics

Springworks

Vir Biotechnology

Wuxi Biologics

2023 Sales

£2.3bn

>16

Acquisitions

& Alliances

R&D late-stage pipeline

2021 Investor Update

Arexvy

MenABCWY

gepotidacin

Apretude

depemokimab

Jemperli

−

Zejula

−

Blenrep

−

Jesduvroq

x otilimab

Progressed/acquired since 2021

MAPS

2

24v/30+v

mRNA

3

influenza

TH HSV

4

bepivirosen

Brexafemme

tebipenem

HIV LA

5

camlipixant

Jemperli LCI

6

CD226

Absolute values at AER; changes at CER, unless stated otherwise

1. All values excl. COVID-19 solutions and on a continuing basis 2. Multiple Antigen Presenting System 3. Messenger RiboNucleic Acid 4. Therapeutic herpes simplex virus 5. Long acting 6. Lifecycle

innovation 7. Select publicly announced acquisitions or alliances that GSK has entered into since June 2021 8. Subject to customary conditions, including applicable regulatory agency clearances under the Hart-

Scott-Rodino Act in the US

6

Strong 2023

performance

Sales

£30.3bn, +5%

+14%

1

Delivered 14%

1

sales growth,

16%

1

adj. operating profit growth

Profitable growth across portfolio:

• Vaccines 24%

1

• Specialty Medicines 15%

1

• General Medicines 5%

New products launched since 2017

2

delivered £ 11 billion sales

Trust/ESG progress sustained:

• Sector leadership recognised by S&P

3

• Low-carbon Ventolin inhaler

programme advances

• Leadership diversity ambitions

achieved

4

Adj. operating profit

£8.8bn, +12%

+16%

1

Adj. EPS

155.1p, +16%

+22%

1

Dividend per share

58p

Highlights

Absolute values at AER; changes at CER, unless stated otherwise 1. Excluding COVID-19 solutions 2. Products include: Zejula, Trelegy, Shingrix,

Juluca, Dovato, Duvroq, Rukobia, Blenrep, Cabenuva, Jemperli, Apretude, Arexvy, Ojjaara 3. S&P Global, The Sustainability Yearbook - 2023

Rankings 4. Ambition to increase female representation at VP level and above roles to at least 45% by 2025 and target at least 30% and 18%

ethnically diverse leaders by the end of 2025 is the US and UK, respectively

7

Delivering on our commitments and upgrading our outlooks

2024 Guidance

•

Sales growth: 5-7%

•

Adj. OP growth: 7-10%

•

Adj. EPS growth: 6-9%

2021-2026 New Outlook

• >7% Sales CAGR

1

• >11% Adj. operating profit CAGR

1

• >31% Adj. operating profit

margin

• >£10bn CGFO

2

2026-2031 New Outlook

• >£38bn sales by 2031

• Continued focus on margin

improvement, with broadly

stable OP

4

margin through

dolutegravir loss of exclusivity

5

2031 Previous Ambition

3

• >£33bn sales

2021-2026 Previous Outlook

3

• >5% Sales CAGR

• >10% Adj. operating profit CAGR

• 30% Adj. operating profit margin

• >10bn CGFO

All guidance, outlooks and expectations regarding future performance should be read together with the section “Guidance and outlooks, assumptions and cautionary statements” on pages 54 to 55 of GSK’s full-year

and Q4 2023 stock-exchange announcement. 2024 guidance growth at CER, unless stated otherwise. All outlook statements are given on a CER basis and use 2023 average exchange rates as a base. All values

excluding COVID-19 solutions 1. Compound annual growth rate 2. Cash flow generated from operations 3. Investor Update June 2021 4. Adj. operating profit excl. COVID-19 solutions.

5. Loss of exclusivity in the US and EU is expected in 2028-2030

8

2023 performance and guidance for 2024

Luke Miels, Chief Commercial Officer

Deborah Waterhouse, CEO, ViiV Healthcare and President, Global Health

9

Strong growth in 2023 for all product areas and regions

Absolute values at AER; changes at CER, unless stated otherwise

1. Excluding COVID-19 solutions

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY 2022 FY 2023

Sales (£m)

Sales contribution by product area

1

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

FY 2022 FY 2023

Sales (£m)

Sales contributions by region

1

+16%

+8%

+15%

+24%

+15%

+5%

+14% +14%

+10% +10%

Vaccines Specialty Medicines General Medicines

US Europe International

10

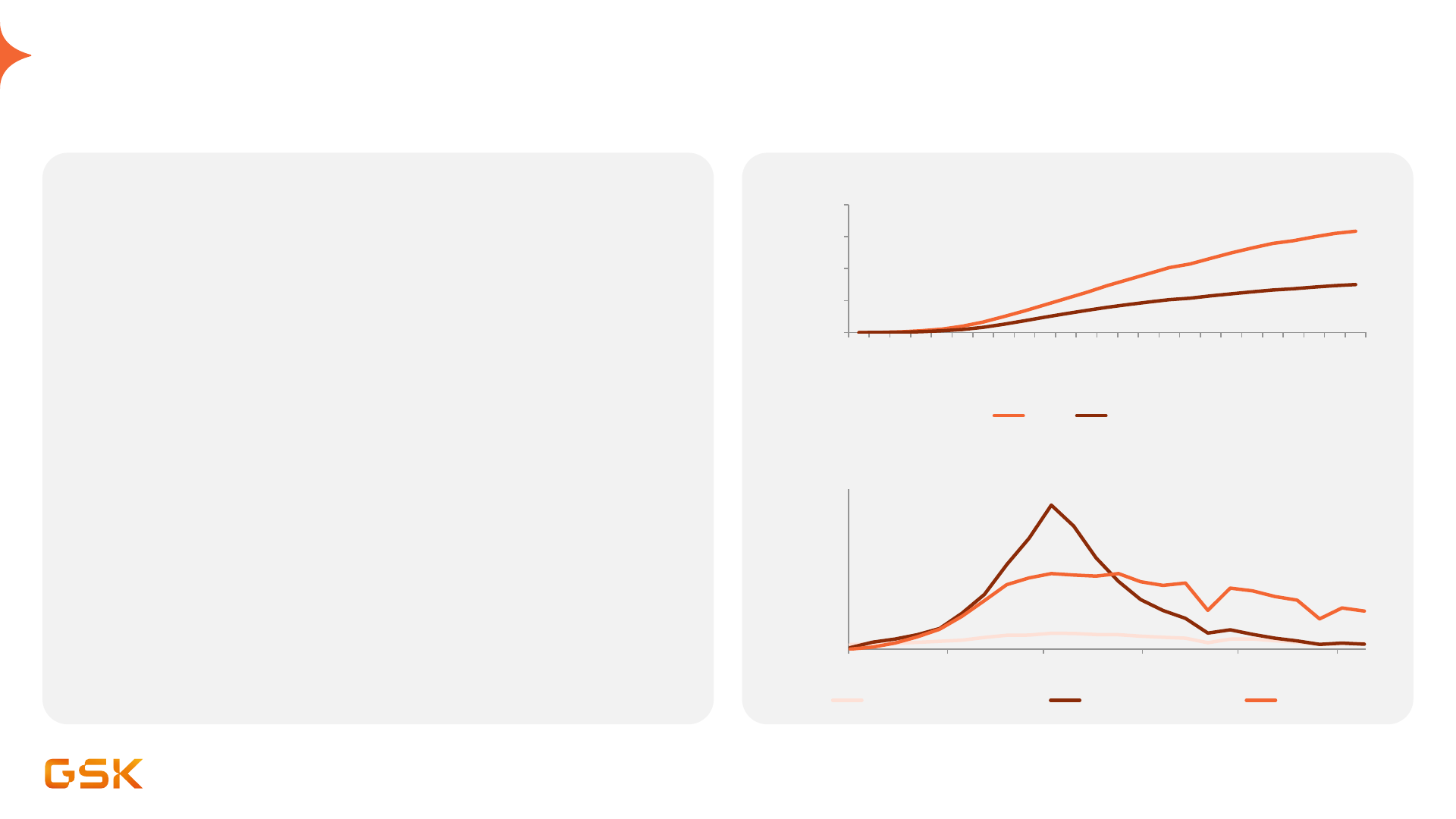

Vaccines: +24%

1

with outstanding

Arexvy

launch

Absolute values at AER; changes at CER for full year, unless stated otherwise

1. Excluding COVID-19 solutions 2. Messenger ribonucleic acid 3. Multiple Antigen Presenting System 4. FY 2023 global sales 5. United States Census Bureau, International Database, Year 2023

6. 9 October 2023: GSK and Zhifei announce exclusive strategic vaccine partnership in China 7. Centers for Disease Control and Prevention

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2022 FY 2023

Sales (£m)

Sales contribution by disease area

1

Further progress expected for mRNA

2

, MAPS

3

, HSV, MenABCWY and Arexvy in 2024

+17%

+7%

+14%

-29%

+24%

+17%

n/a

RSV Shingles Meningitis Influenza Established vaccines

RSV (

Arexvy

) £1,238m

4

• 11% of 60+ population in US vaccinated against RSV; 68% vaccinated

with Arexvy

Shingles (

Shingrix

) +17%

• 35% of >120m US adults

5

recommended to receive Shingrix now

vaccinated

• In 40 countries with <4% penetration in majority of markets

• Partnership with Zhifei

6

in China progressing well

• Confident in delivering >£4bn in peak year sales

Meningitis +14%

•

Bexsero

+14% driven by strong growth in Europe and International

•

Menveo

+12% driven by US CDC

7

replenishment and Brazil performance

Influenza (

Fluarix/FluLaval

) -29%

• Performance in line with expectations of decreased demand and

commoditised market

Established vaccines +7%

2024: expect increase high-single digit to low-double digit %

1

11

Arexvy

launch dynamics

Success in 2023, continued growth in 2024

1. GSK respiratory syncytial virus healthcare professional awareness trial and usage study, December 2023 2. 2023 US Census population data 3. Note: This information is an estimate derived from the use of

information under license from the following IQVIA information service: IQVIA – NPA for the period August 2023 – January 2024. IQVIA expressly reserves all rights, including rights of copying, distribution and

republication

US sets up success for global expansion

• 94.6% efficacy in comorbid population resonating well

• ~2/3 of healthcare professionals prefer Arexvy

1

• Strong position in all major pharmacies

Approved in 39 countries in 2023

• 1

st

entrant in US, Canada, EU and Japan

• Expect additional market approvals and reimbursements in 2024

Continued evidence generation

• 3

rd

year efficacy data in H1 2024

• Expand the market for at risk individuals aged 50 to 59

• 15m people 50-59 with high-risk comorbidities for more severe

RSV infections in the US

2

0.0

2.0

4.0

6.0

8.0

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Total prescriptions (millions)

Number of weeks

Weekly TRx since launch

3

Arexvy Competitor

0.0

0.4

0.8

1.2

Aug/2023 Sep/2023 Oct/2023 Nov/2023 Dec/2023 Jan/2024

Total prescription (millions)

Vaccine seasonality by weekly US TRx

3

Pneumococcal vaccine brand HD QIV flu vaccine brand RSV Total

12

Specialty: +15%

1

with double-digit growth in all product areas

Absolute values at AER; changes at CER for full year, unless stated otherwise

1. Excluding COVID-19 solutions 2. Chronic obstructive pulmonary disease 3. Severe eosinophilic asthma 4. national reimbursement drug list 5. Eosinophilic granulomatosis with polyangiitis

6. Kidney Disease Improving Global Outcomes 7. Lupus nephritis 8. FY 2023 global sales 9. First line 10. 11 December 2023: Jemperli plus chemo approved as first and only frontline IO

treatment in EU for dMMR/MSI-H primary advanced or recurrent endometrial cancer

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2022 FY 2023

Sales (£m)

Sales contribution by disease area

1

+13%

+18%

+15%

+15%

+23%

Depemokimab and Nucala COPD

2

data in 2024

HIV Respiratory/Immunology Oncology

HIV +13%

• 2023 growth driven by oral two-drug regimen and long-acting portfolio

Respiratory/Immunology +18%

•

Nucala

+18%: strong growth in all geographies and indications driven

by new patient growth and US performance. China SEA

3

approval,

launching in private markets; NRDL

4

submission planned for

H2 2024 based on experience with EGPA

5

•

Benlysta

+19%: growth in major markets and continued market

expansion; updated KDIGO

6

guidelines in LN

7

now recommend use at

initial therapy driving further penetration with only ~25% use in the class

Oncology +23%

•

Ojjaara

£33m

8

: strong launch building momentum, first and only

treatment indicated for myelofibrosis patients with anaemia in US

•

Jemperli

£141m

8

: continued momentum and growth in 1L

9

endometrial

cancer in the US; EU 1L endometrial cancer approval in Dec 2023

10

•

Zejula

+15%: driven by US tablet introduction, global expansion and

new patient starts

•

Blenrep

-69%: positive phase III interim analysis of DREAMM-7 head-to-

head with daratumumab, DREAMM-8 phase III data expected H2 2024

2024: expect increase low-double digit %

1

13

General Medicines: +5% driven by

Trelegy

in respiratory

Absolute values at AER; changes at CER for full year, unless stated otherwise

IQVIA MIDAS® monthly data, since launch up to (and including) August 2023, reflecting estimates of real-world activity

1. Chronic obstructive pulmonary disease 2. GSK Annual Reports 2020-23; FactSet major competitor sales in GBP 3. Single inhaler triple therapy 4. Inhaled corticosteroid 5. Long-acting beta-agonists

6. Global Initiative for Chronic Obstructive Lung Disease 7. Average Manufacturer Price

0

2,000

4,000

6,000

8,000

10,000

12,000

FY 2022 FY 2023

Sales (£m)

Sales contribution by disease area

+6%

+2%

+5%

+1%

Respiratory Other General Medicines

Respiratory +6%

•

Trelegy

+29%: Top-selling brand in asthma and COPD

1

market

worldwide; delivering >£2bn in 2023

• Benefit of Arexvy co-promotion and prevention/treatment approach

leading to longer sales calls

• SITT

3

Class displacing ICS

4

/LABA

5

with GOLD

6

guidelines and early

optimisation message accelerating growth

Other General Medicines +2%

•

Augmentin

+17%

• Emerging Markets +15%

• Up to $700m sales exposure related to US AMP

7

Cap removal; Q4 2023

accrued $150m related to rebates and inventory burn

2024: expect decrease mid-single digit %

0

500

1,000

1,500

2,000

2,500

2020 2021 2022 MAT SEPT 23 MAT DEC 23

Sales (£m)

2

Trelegy Seretide/Advair Major competitor

14

HIV: 13% growth in 2023 driven by oral two-drug regimen (2DR) and

long-acting (LA) portfolio

Strong execution across portfolio

Growth driven by oral 2DR and LA

injectables

• FY 2023 sales of £6.4bn driven by oral 2DR and LA

injectable regimens

• Oral 2DR and LA regimens >50% of total HIV portfolio

• Dovato sales of £1.8bn - leading oral 2DR

• Cabenuva sales of £708m - growing >100% vs 2022

• Apretude sales of £149m - potential to transform PrEP

1

• Pipeline: Data to be presented at CROI

2

in March

Target dosing intervals for LA regimens extended to

every four months in treatment and prevention with

roadmap to reach every six months by end of decade

1. Pre-Exposure Prophylaxis 2. Conference on Retroviruses and Opportunistic Infections

25%

26%

28%

33%

36%

39%

42%

46%

47%

51%

53%

55%

0%

10%

20%

30%

40%

50%

60%

0

200

400

600

800

1,000

1,200

Q1

2021

Q2

2021

Q3

2021

Q4

2021

Q1

2022

Q2

2022

Q3

2022

Q4

2022

Q1

2023

Q2

2023

Q3

2023

Q4

2023

HIV Innovation sales as a % of total HIV sales

Sales (£m)

Dovato Cabenuva Juluca Apretude Oral 2DR & LA

15

2023 performance and guidance for 2024

Julie Brown, Chief Financial Officer

16

Delivered a step-change in financial performance in 2023

2022 2023 AER CER Key commentary on CER basis

Adjusted results

£m £m % %

Sales

29,324 30,328 3 5

Sales grew +14% (excl. COVID

-19

solutions) with strong growth in

Vaccines (

Arexvy

and

Shingrix

) and HIV

Cost of sales (8,741) (7,716) (12) (11) Benefit from lower sales of lower margin Xevudy and favourable mix

Gross profit

20,583 22,612 10 12

Gross profit margin 70.2% 74.6% +440 bps +460 bps Improved +20 bps (excl. COVID-19 solutions)

SG&A (8,128) (9,029) 11 13 Increased investment for growth in Vaccines and HIV

Research and development (5,062) (5,750) 14 14 Increased investment in late-stage Vaccines and new product launches

Royalties 758 953 26 26 Benefit from Gardasil, Kesimpta and Biktarvy

Operating profit

8,151 8,786 8 12

Grew +16% (excl. COVID

-19 solutions)

Operating profit margin 27.8% 29.0% +120 bps +180 bps Improved + 60 bps (excl. COVID-19 solutions)

Earnings per share

139.7p 155.1 11 16

EPS grew +22% (excl. COVID

-19 solutions)

2022 2023 AER CER

Total results

£m £m % %

Total operating profit 6,433 6,745 5 10

Total operating profit margin 21.9% 22.2% +30 bps +100bps

Total earnings per share 110.8p 121.6p 10 16

Adjusted results for continuing operations unless stated otherwise; some figures may not sum due to rounding. See page 20 of GSK’s full-year and Q4 2023 stock-exchange announcement for a full reconciliation of

Total to Adjusted results

Improved 2023 adjusted operating margin

0.2%

0.2%

0.3%

0.6%

COGS SG&A

0.0%

R&D Royalties FY 23

Margin

at 22 FX

Currency FY 23

margin

at 23 FX

28.5%

29.1%

28.6%

FY 22

Margin

+60bps

Including COVID-19 solutions +180 bps CER

Excluding COVID-19 solutions +60 bps CER

4.6%

1.9%

1.4%

0.5%

0.6%

FY 22 margin COGS SG&A R&D Royalties FY 23

margin at

22 FX

Currency FY 23

margin at

23 FX

27.8%

29.6%

29.0%

+180bps

Margin benefit driven by decline in lower margin

Xevudy and increased royalties

Margin benefits driven by improved productivity

and increased royalties

1

1

Note: Chart may not sum due to rounding

1. The dilutive effect of Covid-19 solutions reduced from 2022 to 2023 due to decreasing Covid-19 sales and a favorable product mix towards higher margin pandemic sales

18

2023 free cash flow of £3.4bn

Cash generated from operations of £8.1bn

£m £m

2022 2023

Adj. operating profit 8,151 8,786

Decrease/(Increase) in working

capital

67 (1,233)

Gilead Science, Inc. settlement

income

927 -

Other CGFO

1

(1,201) 543

Cash generated from operations

7,944 8,096

Taxation paid (1,310) (1,328)

Net capex

2

(1,916) (2,304)

Other

3

(1,370) (1,055)

Free cash flow

3,348 3,409

Net debt

17,197 15,040

Key drivers of cash flow

Full year

Cash generated from operations increased despite annualising the

Gilead Science, inc settlement in 2022 (£0.9bn) due to:

• Higher Adjusted Operating profit

• Favourable timing of Xevudy cashflows

• Lower UK special pension contributions

• Partly offset by higher receivables from Arexvy sales

Net capital investment increased primarily due to lower proceeds from

asset disposals than in 2022

Q4 2023

Extremely strong quarter, delivering £3.7bn cash from operations versus

£2.1bn in 2022, including benefit from Arexvy collections from Q3

launch

1. Cash generated from operations, including changes in returns and rebates, significant legal payments and operating contingent consideration liability payments 2. Net Capex includes purchases less disposals of

property, plant and equipment and intangibles 3. Other includes net interest paid and dividends to Non-Controlling Interests

19

Capital deployment supports business growth and shareholder

returns

1. Free Cash Flow (FCF) is £3.4bn, including the capital expenditure net of disposal proceeds for plant, property & equipment and intangibles of £1.3bn and £1.0bn, respectively (included in targeted business

development above) 2. Targeted BD in the above chart includes net intangible capex, net purchase of businesses, and net equity investment 3. Other includes dividend and distribution income, exchange on net

debt and other financing items

5.7

1.3

2.5

2.2

0.7

1.8

2022

Net debt

FCF ex-Capex Capex - PP&E Targeted BD Dividends to

shareholders

Other Haleon stake

monetisation

2023

Net debt

17.2

15.0

-£2.2bn

Invest for growth

Shareholder

distributions

£bn

1

2

3

Sales

• Vaccines: high single- to low double-digit % increase

• Specialty Medicines

1

: low double-digit % increase

• HIV: high single- to low double-digit % increase

• General Medicines: mid-single digit % decrease

P&L

• SG&A: low single-digit increase

• R&D: increase broadly in line with sales to support growth of pipeline

• Royalties: £500-£550m; minimal Gardasil royalties (2023: £472m)

• Net finance expense: slightly lower than 2023

• Adjusted Tax rate: around 17%

20

2024 guidance at CER (excl. COVID-19 solutions)

2024 modelling considerations

Guidance

Sales: 5% to 7% growth

Adj. operating profit: 7% to 10% growth

Adj. earnings per share: 6% to 9% growth

All guidance, outlooks, and expectations should be read together with the guidance, outlooks, assumptions, and cautionary statements in GSK’s full-year and Q4 2023 stock-exchange announcement.

1. including HIV.

21

Outlooks for 2026-2031

Emma Walmsley, Chief Executive Officer

Julie Brown, Chief Financial Officer

22

Delivering profitable growth 2026-2031

2026 2031

Build from existing strong performance momentum

With upside opportunity from:

• Early-stage pipeline data

readouts

• Targeted business development

Early-stage pipeline with key inflections and launches

+ targeted business development

Phase II: 30 vaccines and medicines in development

10

Phase I: 23 vaccines and medicines in development

10

>£38 billion RA

9

Innovation-led growth

• Significant growth portfolio with

increasing sales from Vaccines and

Specialty medicines

• >12 major product launches from

2025

Sales >£38bn RA

9

Planned launches ≥£2bn

5

PYS

1

Marketed Growth Drivers ≥£2bn PYS

1

Sales >7% CAGR

4

Arexvy

Shingrix

Meningococcal

vaccines

2

Cabenuva/Apretude

Nucala

Benlysta

Oncology

3

Meningococcal

vaccines

2

mRNA influenza

HIV PrEP

6

depemokimab

camlipixant

Anti-infectives

7

MAPS 24v/30v+

TH HSV

bepirovirsen

HIV treatment

6

Jemperli LCI

8

CD226

All outlook statements are given on a constant currency basis and use 2023 average exchange rates as a base. Pipeline sales are risk-adjusted and include anticipated sales of new products and lifecycle innovation. COVID therapeutic and vaccines solutions sales and profits (2021-

2023) are excluded from the above. See "Guidance and outlooks, assumptions and basis of preparation related to 2024 guidance, 2021-26 and 2031 outlooks" in Appendix of this presentation. 1. Peak year sales 2. Meningococcal vaccines (Bexsero and MenABCWY) 3. Includes

Zejula, Jemperli, and Ojjaara 4. Compound annual growth rate 5. Does not include Blenrep 6. Every-four-month ultra long-acting dosing. ≥£2bn applies to the aggregation of sales of PrEP and treatment. 7. Includes gepotidacin, tebipenem HBr and Brexafemme 8. Lifecycle

innovation 9. Risk-adjusted sales 10. See the appendix for a full list of vaccines and medicines in clinical development.

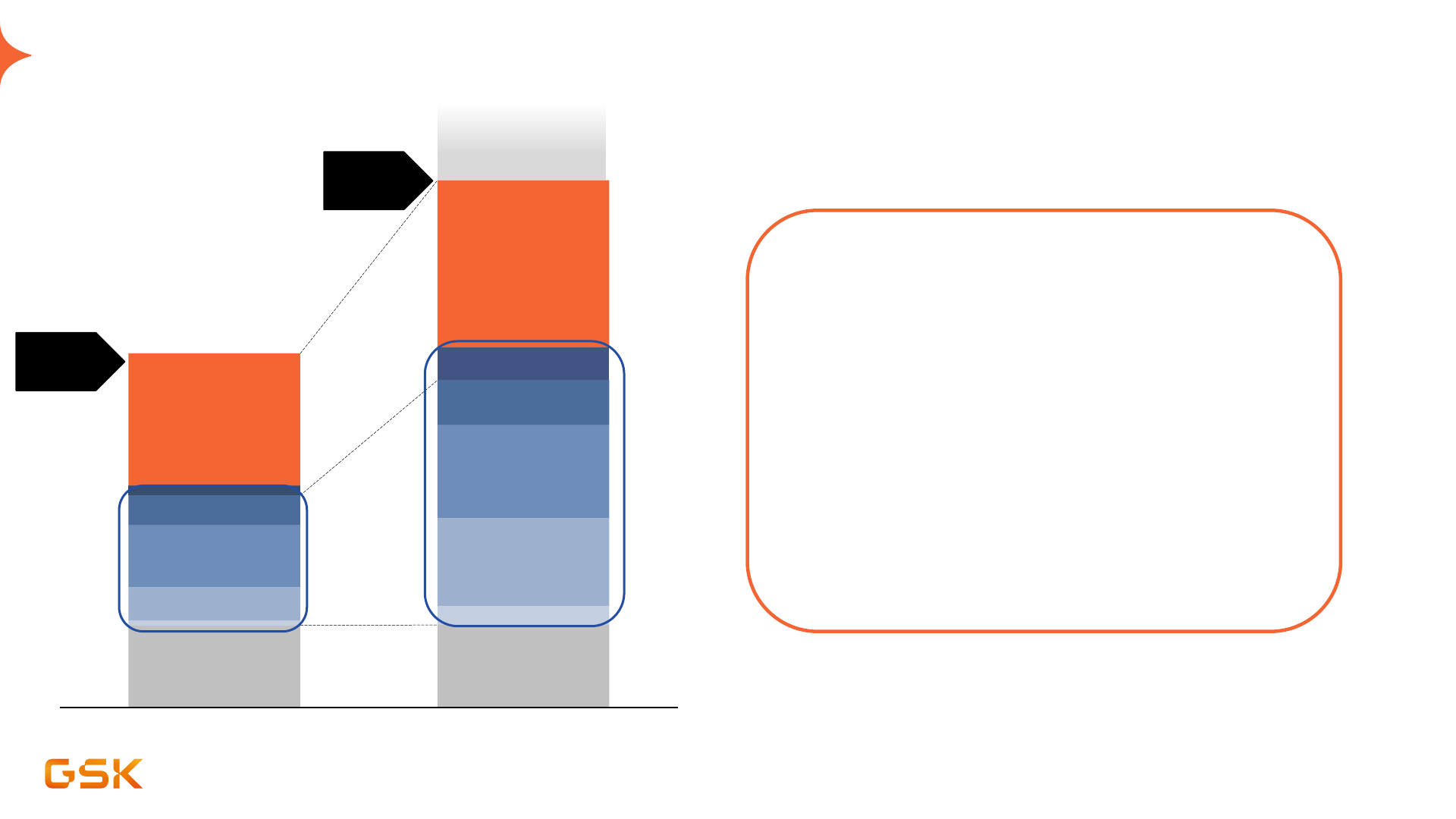

2031 sales outlook: high potential and attractive risk profile

2031 risk adjusted sales 2031 non risk adjusted sales

HIV

Vaccines

General

Medicines

Other Spec

Oncology

1

Respiratory/

Immunology

Vaccines

Respiratory/

Immunology

Oncology

1

Other Spec

General

Medicines

Sales risk

adjusted

> £38bn

Infectious Diseases

Infectious Diseases

23

HIV

Early-stage pipeline +

targeted BD

Sales

Non risk

adjusted

Marketed

• 2031 sales outlook of >£38bn provided on risk

adjusted basis

• More than 90% of sales supporting 2031

outlook of >£38 bn come from products

already approved, or from planned launches

≥£2bn, with majority planned for launch in

next four years

• Significant potential upside with successful

development outcomes and targeted BD

Pipeline opportunity

Charts are schematic and not to scale. All outlook and ambition statements are given on a constant currency basis and use 2023 average exchange rates as a base. Pipeline sales are risk-adjusted and include

anticipated sales of new vaccines and medicines and life cycle innovation. See "Guidance and outlooks, assumptions and basis of preparation related to 2024 guidance, 2021-26 and 2031 outlooks" in appendix.

1. Does not include Blenrep

General Medicines

Significant future pipeline value "unlocks" in 2024-2026

24

Launch year and NRA PYS

1

potential of major launches 2026-31

2025+ Anti-infectives

2

~£2bn

in peak year sales

1

Vaccines

2026+ mRNA seasonal flu

and combinations –

Influenza

>£3bn

in peak year sales

1

2027+ MAPs -

pneumococcal disease

24/30+

>£4bn

in peak year sales

1

2026 camlipixant -

refractory chronic cough

>£2.5bn

in peak year sales

1

Specialty Medicines

2025+ depemokimab / IL5

–

Nucala

COPD

>£4bn

in peak year sales

1

2026+ HIV Q4M ULA

prevention and treatment

>£3bn

in peak year sales

1

2027 bepirovirsen -

hepatitis B virus

>£2bn

in peak year sales

1

2031 CD226 – exploratory

oncology indications

>£2bn

in peak year sales

1

2025+

MenABCWY/

Bexsero

–

Meningococcal vaccines

~£2bn

in peak year sales

1

2028 TH HSV

3

– suppress

recurrence of genital

herpes

>£2bn

in peak year sales

1

2027+

Jemperli

LCI - lung,

colorectal and head &

neck

>£2bn

in peak year sales

1

Scale opportunities in all core product areas

All outlook statements are given on a constant currency basis and use 2023 average exchange rates as a base. See "Guidance and outlooks, assumptions and basis of preparation related to 2024 guidance, 2021-26

and 2031 outlooks" in appendix. 1. Non-risk adjusted peak year sales potential 2. Anti-infectives includes gepotidacin, tebipenem HBr and

Brexafemme

3. Therapeutic herpes simplex virus

25

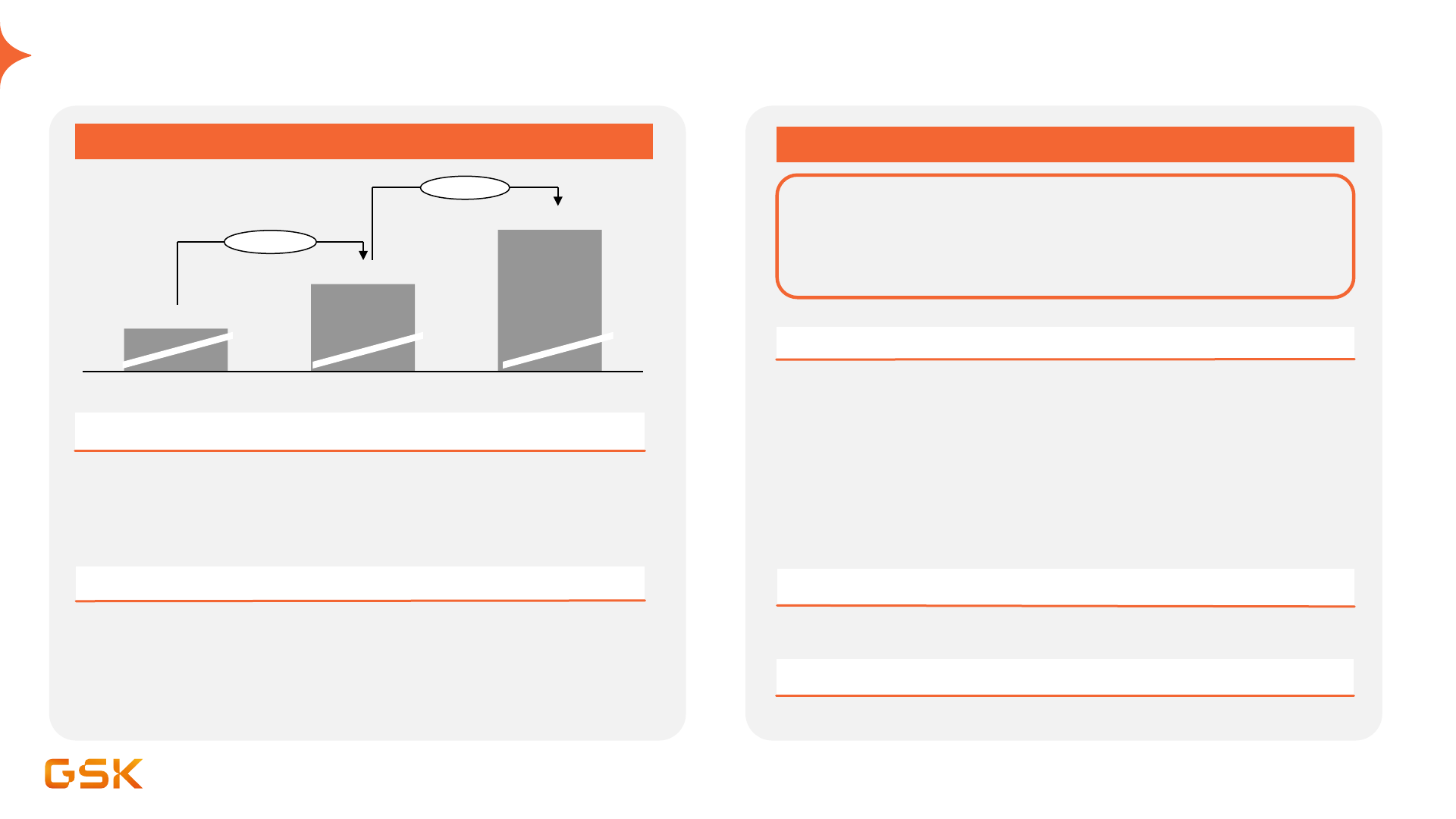

Sustained focus on operating margin improvement

2021 – 2026

• Gardasil royalties end in 2023

Headwinds

• Sales mix shift to Vaccines and Specialty Medicines

• Productivity across supply chain, commercial and functions

• Major restructuring complete

Key drivers

2026 – 2031

Continued focus on margin improvement,

with broadly stable OP margin through

dolutegravir loss of exclusivity (2028-2030)

1

• Dolutegravir LOE (from 2028-2030 (US/EU) with majority impact

2029-2030

Headwinds

Key drivers

2021 2023 2026

25.6%

28.6%

>31%

+290 bps

>240 bps

• Early-stage pipeline progression and targeted BD

Upside opportunity through additional revenue growth

• HIV portfolio transition (~40% of HIV business in long-acting

therapies anticipated at start of loss of exclusivity in US/EU)

• Operating margin mix benefit from Vaccine and Specialty

Medicines marketed and new pipeline products

• >12 major product launches planned 2026-31

• Expected productivity gains in supply chain and SG&A, with

increased use of AI and analytics

All outlook statements are given on a constant currency basis and use 2023 average exchange rates as a base. See "Guidance and outlooks, assumptions and basis of preparation related to 2024 guidance, 2021-

26 and 2031 outlooks" in appendix. Operating margin bridge excludes COVID-19 solutions; FX: 2021 reported margin at 2021 average exchange rates. 2023 and 2026 at 2023 average exchange rates. Basis point

movement at CER. 1. Anticipated loss of exclusivity from 2028-2030 in US/EU

26

Capital allocation framework to support investment and returns

Priority is to invest for growth, coupled with attractive shareholder returns

+8%

+11%

+17%

+15%

+12%

+8%

Sustainable, profitable growth and cash generation

Attractive and growing shareholder returns

Invest for growth

Pipeline (organic and targeted BD)

New product launches

1

Shareholder distributions

Progressive dividend (40-60% pay-out ratio)

Excess cash returns

2

Underpinned by strong balance sheet with strong investment grade credit rating

2022

1

dividend

2023 dividend

2024 dividend

55p/share

expect 58p/share

expect 60p/share

1. GSK group dividend 2022; GSK related only and excludes dividend related to Consumer in H1-2022; FY 2022 dividend 61.25p/share

27

IR Roadmap 2024 to 2025

H1 2024 H2 2024

*

2025

Execution

• Full year 2023 results

• Guidance 2024

• Q1 2024 results

• Half-year 2024 results

• Q3 2024 results

• Full-year 2024 results

• Guidance 2025

• Q1 2025 results

• Half-year 2025 results

• Q3 2025 results

Pipeline

Phase III and

regulatory decisions

2

Regulatory Decisions

• Ojjaara/Omjjara:

MOMENTUM, myelofibrosis (JP)

• Ojjaara/Omjjara: MOMENTUM,

myelofibrosis (EU)

• Nucala: severe asthma (CN)

• Arexvy, RSV, 50-59 YoA (US, EU, JP)

• Nucala, nasal polyposis (JP)

• gepotidacin: EAGLE

• MenABCWY 1

st

gen

(US, EU)

4

•

Jemperli

RUBY (Part 1) EC

3

1L (US)

•

Blenrep

, DREAMM-7/82 L+ MM

1, 8

(US, EU, CN, JP)

• depemokimab ANCHOR-1/2 CRSwNP

9

, (US)

• depemokimab SWIFT-1/2 SEA

16

(US)

• gepotidacin uUTI

10

, GC

11

(US)

• Nucala MATINEE COPD

12

(EU, CN)

• Nucala CRSwNP

9

(CN)

• Zejula ZEAL, 1L maintenance NSCLC (US)

• linerixibat cholestatic pruritus (US, EU, CN, JP)

Phase III readouts

• gepotidacin EAGLE-1, GC

11

• depemokimab SWIFT-1/2, SEA

16

• Zejula FIRST 1L maintenance OC

•

Jemperli

RUBY, 1L dMMR/MSI-H EC

3

(EU)

•

Jemperli

RUBY Part 1L OS

5

EC

3

•

Jemperli

RUBY Part 2, 1L EC

3

•

Blenrep

DREAMM-7, 2L+MM

1, 8

• depemokimab ANCHOR-1/2, CRSwNP

• Nucala MATINEE, COPD

•

Blenrep

DREAMM-8, 2L+ multiple

myeloma

1

• cobolimab COSTAR, 2L NSCLC

6

• Zejula ZEAL, 1L maintenance NSCLC

6

• linerixibat GLISTEN, PBC

7

• depemokimab OCEAN, EGPA

13

• camlipixant CALM 1/2, RCC

14

• tebipenem PIVOT-PO, cUTI

15

Capital Allocation

• Full-year 2023 dividend declaration

• Dividend expectation 2024

• Full-year 2024 dividend declaration

• Dividend expectation 2025

Investor

engagement

• Meet the management, Oncology • Meet the management, Early pipeline

Roadshows and Medical congresses

* HIV long-acting combination decision 1. Not included in the updated outlook 2. Includes phase III data readouts and regulatory decisions with the applicable geography denoted in brackets 3. Endometrial cancer 4. Regulatory submission and acceptance 5. Overall survival

overall population Phase III data readout ; 6. Non-Small Cell Lung Cancer 7. Cholestatic pruritus in primary biliary cholangitis 8 Multiple Myeloma; 9 Chronic rhinosinusitis with nasal polyps 10 Uncomplicated Urinary Tract Infections 11. Urogenital gonorrhoea 12 Chronic Obstructive

Pulmonary Disease 13 Eosinophilic granulomatosis with polyangiitis 14. Refractory Chronic Cough 15. Complicated urinary tract infection 16. Severe eosinophilic asthma

28

R&D based on science of

the immune system and

use of new platform and

data technologies

Leaders in development of

new Vaccines and

Specialty Medicines, for

Infectious Diseases, HIV

Respiratory/Immunology

and Oncology

Products that improve

the health of millions of

people, and sector

leaders in ESG

performance

Strong momentum and

improving outlook for

sustained growth through

the decade

Focused on prevention and changing the course of disease

Ahead Together

29

30

Appendix

31

2024 full year outlook considerations to support modelling

2023 growth

excl Covid

2024 Guidance 2024 Assumptions

2021 – 2026

BIU 2021

2021 – 2026

BIU 2024

Turnover +14% 5-7% >5% CAGR >7% CAGR

- Vaccines +24% HSD – LDD HSD CAGR LDD CAGR

- Specialty +15% LDD DD CAGR DD CAGR

- HIV +13% HSD – LDD MSD CAGR 6-8%

1

- Gen Meds +5% MSD decr

Largely Amp Cap removal

Broadly Stable Broadly Stable

Adj. Operating Profit +16% 7-10%

SG&A: LSD increase

R&D: increase broadly in line with sales

Royalties: £500-£550m; minimal

Gardasil royalties

>10% CAGR >11% CAGR

Adj. Op. Profit margin 28.6% n/a >30% >31%

Adj EPS + 22% 6-9%

Interest: slightly lower than 2023

Tax rate: around 17%

Non-controlling interest: ViiV is main

ongoing NCI

Dividend 58p 60p

All guidance, outlooks and expectations regarding future performance should be read together with the section “Guidance and outlooks, assumptions and cautionary statements” on pages 54 to 55 of of GSK’s full-

year and Q4 2023 stock-exchange announcement.. 2024 guidance growth at CER, unless stated otherwise. All outlook statements are given on a CER basis and use 2023 average exchange rates as a base. All values

excluding COVID-19 solutions. CAGR is compound annual growth rate. 1. As per HIV Meet The Management event, 28 September 2023

32

2023 Total to adjusted operating profit reconciliation

2022 2023 Key commentary on CER basis

Operating profit

(£m)

Operating profit

(£m)

Total results

6,431

6,745

+10% at CER

Intangible amortisation 739 719

Intangible impairment 296 398

Major restructuring 321 382

~£1.1bn benefits to date

1

Transaction-related 1,750 572

ViiV CCL

2

movements

Divestments, significant

legal and other

(1,388) (30)

Receipt of dividend and distribution income from investments, legal

fees and settlements

Adjusted

results 8,151 8,786

+ 12%

at CER

Table may not sum due to rounding. See page 20 of GSK’s full-year and Q4 2023 stock-exchange announcement for a full reconciliation 1. Separation Preparation restructuring programme initiated in 2020

2. Contingent consideration liabilities

33

Improved adj. earnings per share with +16% growth at CER

2022 2023

Key commentary on CER basis

£m £m

Adj. operating

profit (OP) 8,151 8,786

+12% incl. COVID; +16% excl. COVID

-19 solutions

Net finance expense (791) (669) Lower bond interest costs and higher interest income

Share of associates (2) (5)

Tax (1,138) (1,257)

Tax rate 15.5% 15.5% In-line with guidance

Non-controlling interests (595) (572) Lower net profits in some Group entities

Adj. Profit attributable to shareholders

5,625 6,283

+17% incl. COVID

Adj. earnings per share (EPS)

139.7p 155.1p

+16% incl. COVID, +22% excl. COVID

-19 solutions

Total EPS

110.8p 121.6p

+16% at CER

Weighted average number of shares (millions) 4,026 4,052

Adjusted results and for continuing operations unless stated otherwise.

34

Quarterly summary of results

2022 2023

Q1 Q2 Q3 Q4 FY Q1 Q2 Q3 Q4 FY

Including COVID

-19 solutions

Sales (£m) 7,190 6,929 7,829 7,376 29,324 6,951 7,178 8,147 8,052 30,328

Operating profit (£m) 1,943 2,008 2,605 1,595 8,151 2,092 2,170 2,772 1,752 8,786

Operating margin 27.0% 29.0% 33.3% 21.6%

27.8%

30.1% 30.2% 34.0% 21.8%

29.0%

Earnings per share (pence) post-share

consolidation

32.3 34.7 46.9 25.8

139.7 37.0 38.8 50.4 28.9 155.1

COVID

-19 solutions impact

Sales (£m) 1,307 466 417 183 2,373 132 41 1 20 194

Operating profit (£m) 194 58 141 69 462 118 57 (4) 9 179

Earnings per share (pence) post-share

consolidation

4.1 1.2 2.9 1.5

9.7 2.5 1.2 (0.1) 0.2 3.8

Excluding COVID

-19 solutions impact

Sales (£m) 5,883 6,463 7,412 7,193 26,951 6,819 7,137 8,146 8,032 30,134

Operating profit (£m) 1,749 1,950 2,464 1,526 7,689 1,974 2,113 2,776 1,743 8,607

Operating margin 29.7% 30.2% 33.2% 21.2%

28.5%

28.9% 29.6% 34.1% 21.7%

28.6%

Earnings per share (pence) post-share

consolidation

28.2 33.5 44.0 24.3

130.0 34.5 37.6 50.5 28.7 151.3

Adjusted results and for continuing operations; some figures may not sum due to rounding.

35

Currency

1. Based on 2023 GSK continuing operations, including COVID-19 solutions 2. The other currencies that each represent more than 1% of GSK sales include Australian Dollar, Brazilian Real, Canadian Dollar, Chinese Yuan and Indian

Rupee. In total, they accounted for 9% of GSK revenues in 2023. 3. If exchange rates were to hold at the closing rates on 24 January 2024 ($1.27/£1, €1.17/£1 and Yen 188/£1) for the rest of 2024, the estimated impact on 2024

Sterling turnover growth for GSK would be -3% and if exchange gains or losses were recognised at the same level as in 2023, the estimated impact on 2024 Sterling Adjusted Operating Profit growth for GSK would be -5%.

2023 currency sales exposure

1

2024 adj. operating profit

3

US $ 52% US $: 10 cents movement in the average exchange rate for full year

impacts adj. operating profit by approx. +/- 9.0%

Euro € 19% Euro €: 10 cents movement in the average exchange rate for full year

impacts adj. operating profit by approx. +/- 0.5%

Japanese ¥ 4% Japanese ¥: 10 Yen movement in the average exchange rate for full

year impacts adj. operating profit by approx. +/- 1.0%

Other

2

25%

2022 2023

Historical average exchange rates

quarterly

Q1 Q2 Q3 Q4 FY 22 Q1 Q2 Q3 Q4 FY 23

US $

1.34 1.26 1.18 1.19 1.24 1.22 1.25 1.26 1.25 1.24

Euro €

1.19 1.18 1.16 1.15 1.17 1.14 1.15 1.16 1.15 1.15

Japanese ¥

156 162 161 165 161 162 173 182 183 175

Historical period end exchange rates

US $

1.31 1.21 1.11 1.20 1.24 1.26 1.23 1.27

Euro €

1.18 1.16 1.13 1.13 1.14 1.17 1.16 1.15

Japanese ¥

160 165 160 159 165 183 183 180

36

Investor roadmap highlights progress of key events

Q2 2023

Q3 2023 Q4 2023

H1 2024

H2 2024

Execution

• Q2 and Half-year

2023 results

• Full-year 2023

upgraded guidance

• Q3 and Year-to-date

2023 results

• Full-year and Q4 2023

results

• Performance vs BIU

2021

1

• Full-year 2024 guidance

• Q1 2024 results

• Q2 and Half-year 2024 results

• Q3 and Year-to-date 2024 results

• Full-year and Q4 2024 results

• Performance vs BIU 2021

1

• Guidance 2025

Pipeline

Phase III and

regulatory

decisions

2

• Therapy Area

Strategy

• R&D priorities

• Arexvy US

regulatory approval

• Arexvy second

season data

• BELLUS Health, Inc.

acquisition

completed

• SCYNEXIS, Inc.

exclusive license

completed

• Arexvy RSV, ≥60 YoA (JP)

• Arexvy, RSV, 50-59 YoA

• Apretude, HIV pre-exposure (EU)

• Vocabria, HIV treatment (CN)

• Ojjaara, MOMENTUM, myelofibrosis (US)

• Jemperli RUBY, 1L dMMR/MSI-H EC

3

(US)

• Jemperli: RUBY, 1L dMMR/MSI-H

EC

3

(EU)

• Ojjaara: MOMENTUM, myelofibrosis

(EU)

• Ojjaara: MOMENTUM, myelofibrosis

(JP)

• Blenrep: DREAMM-7, 2L+ MM

• gepotidacin: EAGLE-1, GC

• depemokimab: SWIFT-1/2, asthma

• Jemperli: RUBY (Part 2), 1L EC

3

• Jemperli: RUBY (Part 1) 1L OS

4

EC

3

• Zejula: FIRST, 1L maintenance OC

ovarian cancer

• Arexvy: RSV, 50-59 YoA (US, EU, JP)

• Nucala: CRSwNP (JP)

• Nucala: severe asthma (CN)

• depemokimab: ANCHOR-1/2,

CRSwNP

• Nucala MATINEE, COPD

• cobolimab: COSTAR, 2L NSCLC

• Blenrep: DREAMM-8, 2L MM

• Zejula: ZEAL, 1L maintenance NSCLC

• linerixibat: GLISTEN, PBC

5

Capital

Allocation

• Capital allocation

• R&D and BD

priorities

• TA priorities

• Full-year 2023

dividend

declaration

• Full-year 2024 dividend declaration

Investor

Engagement

Roadshows

Meet the

management,

Infectious Diseases

Meet the management,

HIV

Meet the

management,

Respiratory

Meet the management, Oncology

Medical congresses

1. June 2021 Investor Update 2. Includes phase III data readouts and regulatory decisions with the applicable geography denoted in brackets 3. Endometrial cancer 4. Overall survival population

5. cholestatic pruritus in primary biliary cholangitis

37

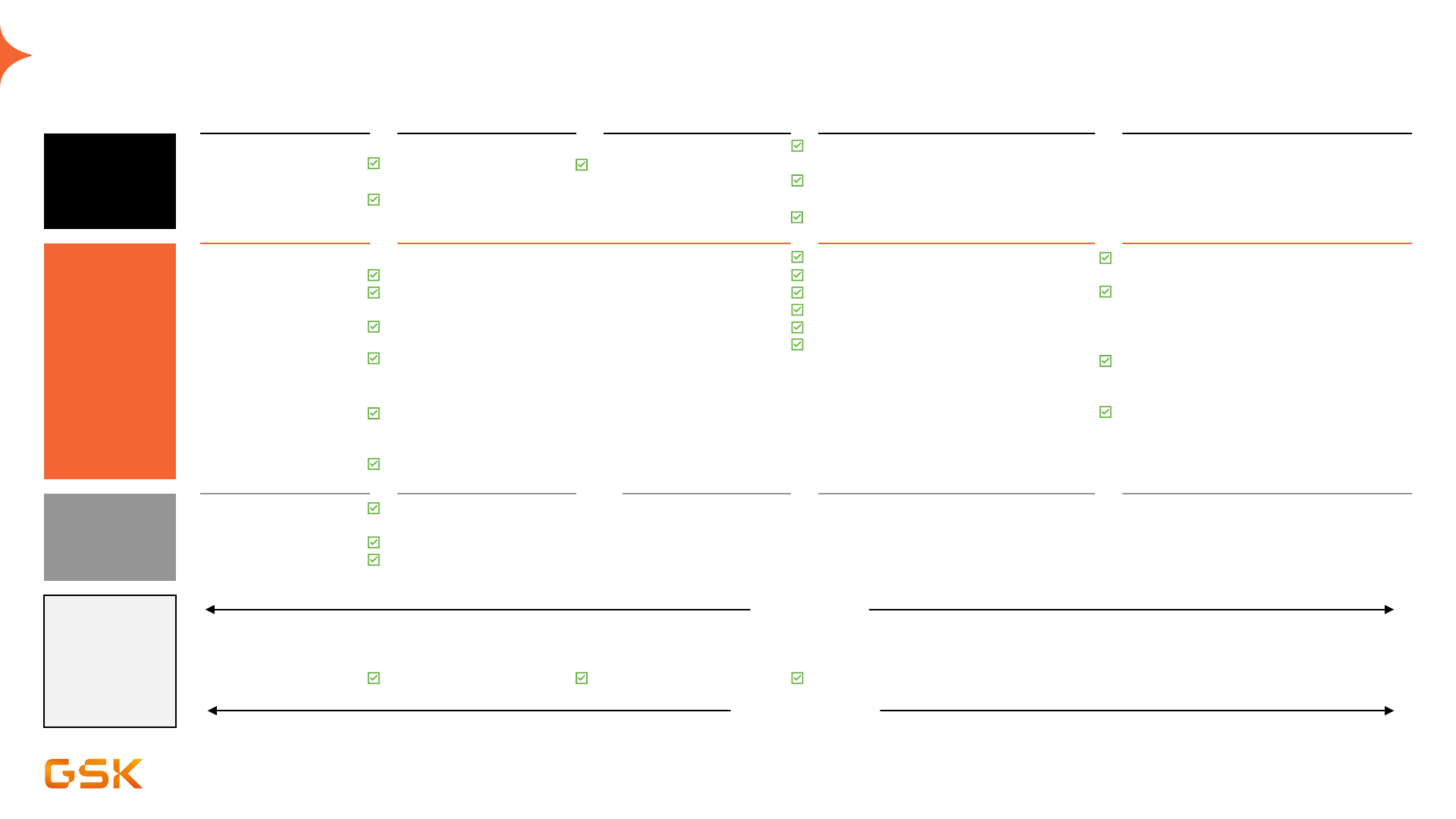

Upcoming pipeline catalysts: 2024 and 2025

H1 2024 H2 2024 2025

Regulatory

decision

Ojjaara/Omjjara: MOMENTUM, myelofibrosis JP Arexvy: 50-59 YoA

10

US, EU, JP

gepotidacin: EAGLE-2/3, uUTI

11

US

Nucala: CRSwNP

1

JP

gepotidacin: EAGLE-1, GC

5

US

MenABCWY vaccine 1st Gen

US, EU

depemokimab: SWIFT-1/2, asthma

US

depemokimab: ANCHOR-1/2, CRSwNP

1

US

Nucala: CRSwNP

1

CN

Nucala: MATINEE, COPD

12

US

Blenrep: DREAMM-7/8, 2L+ MM

7

US, EU, CN, JP

Jemperli

2

: RUBY (Part 1)

3,

1L EC

4

US

linerixibat: GLISTEN, cholestatic pruritus in PBC

14

US

Regulatory

submission and

acceptance

MenABCWY vaccine 1st Gen

US

gepotidacin: EAGLE-2/3, uUTI

11

US

gepotidacin: EAGLE-1, GC

5

US

Nucala: CRSwNP

1

CN

MenABCWY vaccine 1st Gen

EU

tebipenem pivoxil: PIVOT-PO, cUTI

15

US

Jemperli

2

: RUBY (Part 1)

3

, 1L EC

4

US

depemokimab: SWIFT-1/2, asthma

US

camlipixant: CALM-1/2, RCC

16

US, EU

depemokimab: ANCHOR-1/2, CRSwNP

1

US

Nucala: MATINEE, COPD

12

EU, CN

Nucala: MATINEE, COPD

12

US Blenrep: DREAMM-7/8, 2L+ MM

7

US, EU, CN, JP

cobolimab

2

: COSTAR, 2L NSCLC

13

US, EU

linerixibat: GLISTEN, cholestatic pruritus in PBC

14

US, EU, CN, JP

Late

-

stage phase

III and phase II

readouts

gepotidacin: EAGLE-1, GC

5

depemokimab: ANCHOR-1/2, CRSwNP

1

tebipenem pivoxil: PIVOT-PO, cUTI

15

depemokimab: SWIFT-1/2, asthma Nucala: MATINEE, COPD

12

camlipixant: CALM-1/2, RCC

16

Blenrep: DREAMM-7

6

, 2L+ MM

7

Blenrep: DREAMM-8, 2L+ MM

7

depemokimab: OCEAN, EGPA

17

Zejula

2

: FIRST, 1L maintenance OC

8

cobolimab

2

: COSTAR, 2L NSCLC

13

Zejula

2

: ZEAL, 1L maintenance NSCLC

13

mRNA Seasonal flu

9

linerixibat: GLISTEN, cholestatic pruritus in PBC

14

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

1. Chronic rhinosinusitis with nasal polyps 2. Tesaro asset 3. Overall population 4. Endometrial cancer 5. Urogenital gonorrhoea 6. Overall survival 7. Multiple myeloma 8. Ovarian cancer 9. Phase II 10. Years of age 11. Uncomplicated urinary tract infection 12. Chronic

obstructive pulmonary disorder 13. Non-small cell lung cancer 14. Treatment of cholestatic pruritus in primary biliary cholangitis 15. Complicated urinary tract infection 16. Refractory chronic cough 17. Eosinophilic granulomatosis with polyangiitis

38

12 major planned launches

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

MenABCWY

mRNA influenza

Anti-infectives (gepotidacin, tebipenem and Brexafemme)

MAPs 24v/30+v

TH HSV (herpes simplex virus)

bepirovirsen

HIV PrEP

HIV treatment

depemokimab

camlipixant

Jemperli LCI

CD226

1. Every-four-month ultra long-acting dosing

39

71 potential new vaccines and medicines in pipeline

Phase III / Registration – 18 assets

Arexvy (RSV vaccine) Recombinant protein, adjuvanted* RSV older adults (50-59 YoA)^

gepotidacin (2140944) BTI inhibitor* Uncomplicated UTI**

bepirovirsen (3228836) Antisense oligonucleotide* Chronic HBV infection**

Bexsero (MenB vaccine) Recombinant protein, OMV Meningitis B (infants US)

MenABCWY vaccine (3536819) Recombinant protein, OMV, conjugated vaccine MenABCWY, 1

st

Gen

tebipenem pivoxil (3778712) Antibacterial carbapenem* Complicated UTI

ibrexafungerp (5458448) Antifungal glucan synthase inhibitor* Invasive candidiasis

Nucala (mepolizumab) Anti-IL5 antibody COPD

depemokimab (3511294) Long-acting anti-IL5 antibody* Asthma**

latozinemab (4527223) Anti-sortilin antibody* Frontotemporal dementia

1

**

camlipixant (5464714) P2X3 receptor antagonist Refractory chronic cough

Low carbon version of MDI

2

, Ventolin (salbutamol)

Beta 2 adrenergic receptor agonist Asthma

3

Ojjaara/Omjjara (momelotinib) JAK1, JAK2 and ACVR1 inhibitor* Myelofibrosis^

4

Jemperli (dostarlimab) Anti-PD-1 antibody* Endometrial cancer^**

Zejula (niraparib) PARP inhibitor* Ovarian cancer**

Blenrep (belantamab mafodotin) Anti-BCMA ADC* Multiple myeloma

cobolimab (4069889) Anti-TIM-3 antibody* Non-small cell lung cancer

linerixibat (2330672) IBAT inhibitor Cholestatic pruritus in primary biliary cholangitis

*In-license or other alliance relationship with third party ** Additional indications or candidates also under investigation ^ In registration

1. Phase III trial in patients with progranulin gene mutation 2. Metered dose inhaler 3. Phase III start expected in 2024 4. Approved in US and EU 5. In phase I/II study 6. Phase II study start imminent 7. Transition activities

underway to enable further progression by partner 8. GSK has an exclusive global license option to co-develop and commercialise the candidate

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

*In-license or other alliance relationship with third party ** Additional indications or candidates also under investigation ^ In registration

1. Phase III trial in patients with progranulin gene mutation 2. Metered dose inhaler 3. Phase III start expected in 2024 4. Approved in US and EU 5. In phase I/II study 6. Phase II study start imminent 7. Transition activities

underway to enable further progression by partner 8. GSK has an exclusive global license option to co-develop and commercialise the candidate

40

71 potential new vaccines and medicines in pipeline

3437949 Recombinant protein, adjuvanted* Malaria fractional dose

4406371 Live, attenuated MMRV new strain

3536852 GMMA* Shigella

3528869 Viral vector with recombinant protein, adjuvanted* Chronic HBV infection

5

**

4023393 Recombinant protein, OMV, conjugated vaccine MenABCWY, 2

nd

Gen

5

4178116 Live, attenuated Varicella new strain

5101956 MAPS* Adult pneumococcal disease, 24-valent

5101955 MAPS* Paediatric pneumococcal disease, 24-valent

4106647 Recombinant protein, adjuvanted* Human papillomavirus

5

4348413 GMMA Gonorrhoea

5

4382276 mRNA* Seasonal flu

4396687 mRNA* COVID-19

3993129 Adjuvanted recombinant subunit Cytomegalovirus

5

3943104 Recombinant protein, adjuvanted* Therapeutic herpes simplex virus

5

5637608 Hepatitis B virus-targeted siRNA* Chronic HBV infection

4077164 Bivalent GMMA Invasive non-typhoidal salmonella**

3036656 Leucyl t-RNA synthetase inhibitor* Tuberculosis

sanfetrinem cilexetil (GV118819) Serine beta lactamase inhibitor* Tuberculosis

BVL-GSK098 Ethionamide booster* Tuberculosis

3810109 Broadly neutralizing antibody* HIV

3739937 Maturation inhibitor HIV

4004280 Capsid protein inhibitor HIV

4011499 Capsid protein inhibitor HIV

4524184 Integrase inhibitor* HIV

6

Benlysta (belimumab) Anti-BLys antibody Systemic sclerosis associated interstitial lung disease

3858279 Anti-CCL17 antibody* Osteoarthritis pain**

1070806 Anti-IL18 antibody Atopic dermatitis

4527226 (AL-101) Anti-sortilin antibody* Alzheimer’s disease

6

belrestotug (4428859) Anti-TIGIT antibody* Non-small cell lung cancer**

4532990 HSD17B13 siRNA* Non-alcoholic steatohepatitis

Phase II – 30 assets

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

41

71 potential new vaccines and medicines in pipeline

Phase I – 23 assets

*In-licence or other alliance relationship with third party ** Additional indications or candidates also under investigation ^ In registration

1. Phase III trial in patients with progranulin gene mutation 2. Metered dose inhaler 3. Phase III start expected in 2024 4. Approved in US and EU 5. In phase I/II study 6. Phase II study start imminent 7. Transition activities

underway to enable further progression by partner 8. GSK has an exclusive global license option to co-develop and commercialise the candidate

3536867 Bivalent conjugate* Salmonella (typhoid + paratyphoid A)

2556286 Mtb cholesterol dependent inhibitor* Tuberculosis

3186899 CRK-12 inhibitor*

7

Visceral leishmaniasis

3494245 Proteasome inhibitor* Visceral leishmaniasis

3772701 P. falciparum whole cell inhibitor* Malaria

4024484 P. falciparum whole cell inhibitor* Malaria

3882347 FimH antagonist* Uncomplicated UTI

3923868 PI4K beta inhibitor Viral COPD exacerbations

3965193 PAPD5/PAPD7 inhibitor Chronic HBV infection

5

5251738 TLR8 agonist* Chronic HBV infection

cabotegravir (1265744) Integrase inhibitor HIV

3888130 Anti-IL7 antibody* Autoimmune disease

3915393 TG2 inhibitor* Pulmonary fibrosis

3862995 Anti-IL33 antibody COPD

5462688 RNA-editing oligonucleotide* Alpha-1 antitrypsin deficiency

4347859 Interferon pathway modulator Systemic lupus erythematosus

4381562 Anti-PVRIG antibody* Cancer

6097608 Anti-CD96 antibody* Cancer

XMT-2056

9

(wholly owned by Mersana Theraprutics)

STING agonist ADC* Cancer

belantamab (2857914) Anti-BCMA antibody Multiple myeloma

4524101 DNA polymerase theta inhibitor* Cancer

5

5733584 (HS-20089) ADC-targeting B7-H4* Gynecologic malignancies

4172239 DNMT1 inhibitor* Sickle cell disease

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

42

Changes since Q3 2023

Changes on pipeline Achieved pipeline catalysts

Regulatory decisions

Nucala – severe asthma CN

Jemperli

1

– RUBY, dMMR/MSI-H 1L endometrial cancer EU

Omjjara: MOMENTUM, myelofibrosis EU

Regulatory submission acceptances

Arexvy – 50-59 YoA EU, JP

Other events

Blenrep – DREAMM-7, 2L+ MM – Positive headline phase III data

Jemperli

1

– RUBY (Part 2), 1L EC – Positive phase III data readout

New to Phase I

4024484 – P. falciparum whole cell inhibitor, malaria

3862995 – Anti-IL33 antibody, COPD

5462688 – RNA-editing oligonucleotide, Alpha-1 antitrypsin deficiency

4347859 – Interferon pathway modulator, systemic lupus erythematosus

5733584 – ADC targeting B7-H4, gynecologic malignancies

New to Phase II

3943104 – Recombinant protein, adjuvanted, Therapeutic HSV

5637608 – HBV-targeted siRNA sequential combination, chronic HBV infection

4077164 – Bivalent GMMA, Invasive non-typhoidal salmonella**

4524184 – Integrase inhibitor, HIV

New to Phase III

Low carbon version of MDI, Ventolin – Beta 2 adrenergic receptor agonist, asthma

Removed from Phase I

4429016 – Bioconjugated recombinant protein, adjuvanted, K. pneumoniae

4182137 (VIR7832) – Anti-spike protein antibody, COVID-19

Removed from Phase II

VIR2482 – Neutralising monoclonal antibody, influenza

Infectious diseases

HIV (ViiV)

Respiratory/Immunology

Oncology

Opportunity driven

** Additional indications or candidates also under investigation

1. Tesaro asset

43

ADC Antibody drug conjugate EGPA Eosinophilic granulomatosis with polyangiitis NSCLC Non-small cell lung cancer

AE Adverse event FVC Forced vital capacity OMV Outer membrane vesicle

AESI Adverse event of special interest GC Urogenital gonorrhea ORR Overall response rate

AUC Area under curve GMMA Generalised Modules for Membrane Antigens OS Overall surival

BCMA B-cell maturation antigen GSI Gamma secretase inhibitor PBC Primary biliry cholangitis

BICR Blinded Independent Central Review HA Healthy adults PFS Progression-free survival

BRCA Breast cancer HBV Hepatitis B virus PFS2 Time to second disease progression or death

CAE Corneal adverse events HES Hypereosinophilic syndrome PK Pharmacokinetic

CBR Clinical benefit rate Hgb Hemoglobin PMF

Primary myelofibrosis

cCR Complete clinical response hSBA Human serum bactericidal assay Post-PV/ET MF Post-essential thrombocythemia myelofibrosis

CKD Chronic kidney disease HZ Herpes zoster RCC Refractory chronic cough

CfB Change from baseline IC Immunocompromised RL Repeat dose level

CMV Cytomegalovirus ICR Independent central review RRMM Relapsed/refractory multiple myeloma

CN China iNTS Invasive non-typhoidal salmonella RSV Respiratory syncytial virus

COPD Chronic obstructive pulmonary disease ITT Intention-to-treat SAD Single ascending dose

CP Cholestatic pruritus JP Japan SAE Serious adverse event

CRR Complete response rate LLOQ Lower limit of quantitation siRNA Small interfering RNA

CRSwNP Chronic rhinosinusitis with nasal polyps LRTS Lower respiratory tract symptoms SoC Standard of care

cUTI Complicated urinary tract infection MAD Multiple ascending dose SSc-ILD

Systemic sclerosis associated interstitial lung disease

CV Cardiovascular MAE Medical attended events TOC Test of cure

DDI Drug-drug interaction MDI Metered dose inhaler TTBR Time to best response

DFS Disease-freee survival MAPS Mulitple Antigen Presenting System TTD Time to treatment discontinuation

DL Dose level MM Multiple myeloma TTP Time to tumour progression

DLT Dose-limiting toxicity MMR Measles, mumps and rubella TTR Time to treatment response

dMMR Deficient mismatch repair MMRV Measles, mumps, rubella and varicella UTI Urinary tract infection

DoR Duration of response MRD Multiple rising dose uUTI Uncomplicated urinary tract infection

DPNP Diabetic peripheral neuropathic pain MSI-H Microsatellite instability high VGPR Very good partial remission

EASI Eczema Area and Severity Index NASH Nonalcoholic steatohepatitis VSP Vital sign parameters

EGPA Eosinophilic granulomatosis with polyangiitis NRS Numeric Rating Scale YoA Years of age

Glossary

44

In outlining the guidance for 2024 and outlooks for the period 2021-2026 and for 2031, the Group has made certain assumptions about the macro-economic environment, the

healthcare sector (including regarding existing and possible additional governmental legislative and regulatory reform), the different markets and competitive landscape in which the

Group operates and the delivery of revenues and financial benefits from its current portfolio, its development pipeline and restructuring programmes.

2024 Guidance

These planning assumptions as well as operating profit and earnings per share guidance and dividend expectations assume no material interruptions to supply of the Group’s

products, no material mergers, acquisitions or disposals, no material litigation or investigation costs for the Company (save for those that are already recognised or for which provisions

have been made) and no change in the Group’s shareholdings in ViiV Healthcare. The assumptions also assume no material changes in the healthcare environment or unexpected

significant changes in pricing as a result of government or competitor action. The 2024 guidance factors in all divestments and product exits announced to date.

2021-26 and 2031 outlooks

The assumptions for GSK’s updated revenue, operating profit, operating margin and cash flow outlooks, 2031 revenue outlook and margin expectations through dolutegravir loss of

exclusivity assume the delivery of revenues and financial benefits from its current and development pipeline portfolio of drugs and vaccines (which have been assessed for this purpose

on a risk-adjusted basis, as described further below); regulatory approvals of the pipeline portfolio of drugs and vaccines that underlie these expectations (which have also been

assessed for this purpose on a risk-adjusted basis, as described further below); no material interruptions to supply of the Group’s products; successful delivery of the ongoing and

planned integration and restructuring plans; no material mergers, acquisitions or disposals or other material business development transactions; no material litigation or investigation

costs for the company (save for those that are already recognised or for which provisions have been made); no share repurchases by the company; and no change in the

shareholdings in ViiV Healthcare. GSK assumes no premature loss of exclusivity for key products over the period.

The assumptions for GSK’s updated revenue, operating profit, operating margin and cash flow outlooks, 2031 revenue outlook and margin expectations through dolutegravir loss of

exclusivity also factor in all divestments and product exits announced to date as well as material costs for investment in new product launches and R&D. Risk-adjusted sales includes

sales for potential planned launches which are risk adjusted based on the latest internal estimate of the probability of technical and regulatory success for each asset in development.

Potential future sales contribution from Blenrep have not been included.

Notwithstanding these outlooks and expectations, there is still uncertainty as to whether our assumptions, outlooks and expectations will be achieved, including based on the other

assumptions outlined above.

All outlooks statements are given on a constant currency basis and use 2023 average exchange rates as a base (£1/$1.24, £1/€1.15, £1/Yen 175). 2021-2026 outlook refers to the 5 years

to 2026 with 2021 as the base year.

Assumptions and basis of preparation related to 2024 guidance, 2021-26 and 2031 outlooks

45

Use of GSK conference call, webcast and presentation slides

The GSK plc webcast, conference call and presentation slides (together the ‘GSK materials’) are for your personal, non-commercial use only. You may not copy,

reproduce, republish, post, broadcast, transmit, make available to the public, sell or otherwise reuse or commercialise the GSK materials in any way. You may not edit,

alter, adapt or add to the GSK materials in any way, nor combine the GSK materials with any other material. You may not download or use the GSK materials for the

purpose of promoting, advertising, endorsing or implying any connection between you (or any third party) and us, our agents or employees, or any contributors to the

GSK materials. You may not use the GSK materials in any way that could bring our name or that of any Affiliate into disrepute or otherwise cause any loss or damage to

us or any Affiliate. GSK plc, 980 Great West Road, Brentford, Middlesex, TW8 9GS, United Kingdom. Telephone +44 20 8047 5000, www.gsk.com

gsk.com