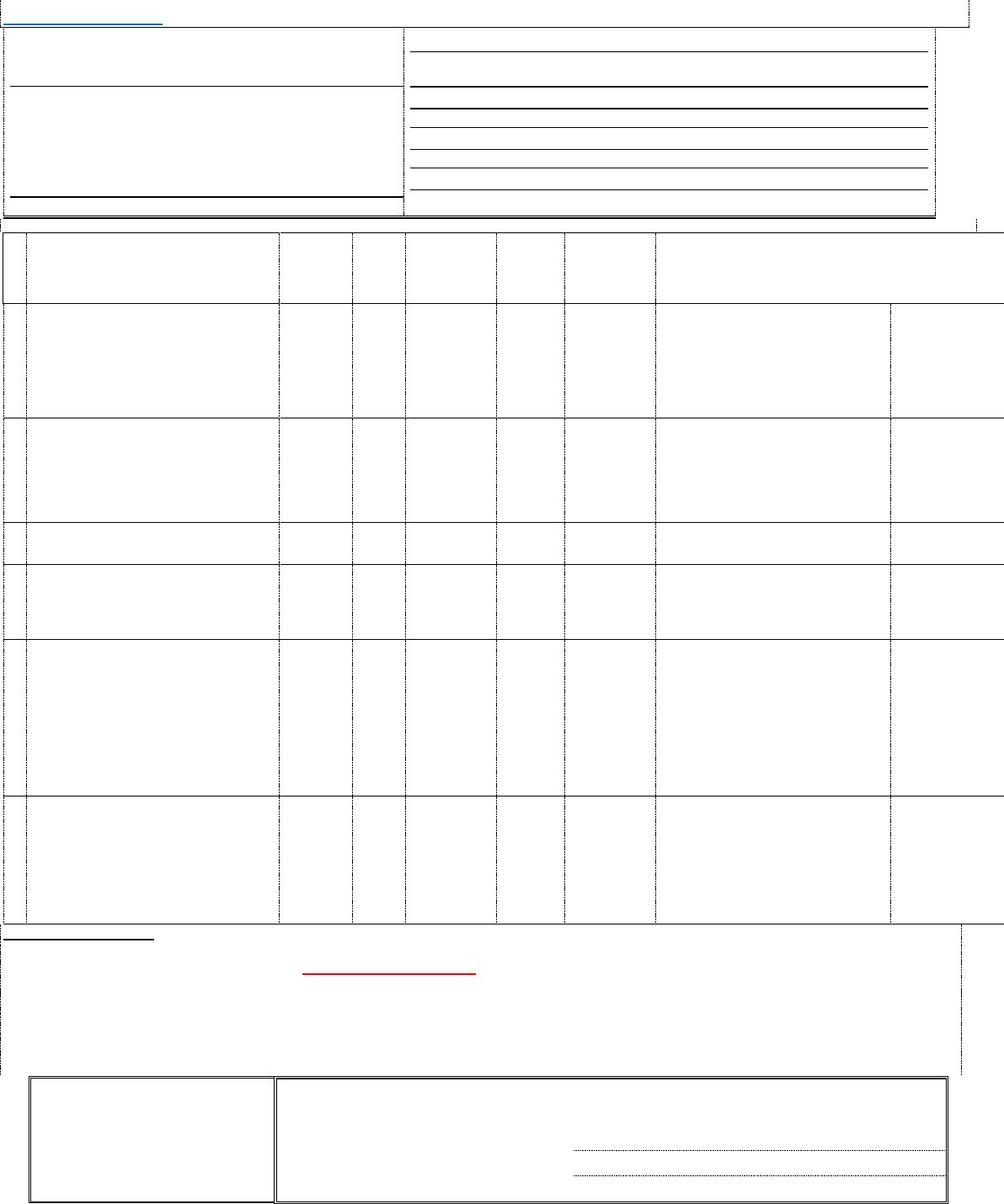

Fax: 1-866-277-8529 Email: [email protected]

HAMPTON INN, HILTON GARDEN INN, HOMEWOOD SUITES, HOME2 SUITES, TRU

HILTON WORLDWIDE – 3 - FOCUSED SERVICE FRANCHISED - REQUIREMENTS

DOMESTIC ONLY Certificate of Insurance

NAME AND ADDRESS OF AGENCY:

E-Mail & Fax

NAME AND ADDRESS OF INSURED:

Insured

Address

City, State, Zip

COMPANIES AFFORDING COVERAGES

INSURANCE COMPANY’S DESIGNATED MUST HAVE A MINIMUM OF A- VII AM BEST

RATING

COMPANY A Must List All Carriers/Insurers (A-/VII Required)

COMPANY B Must List WC/EL Insurers (B++/VII Required)

COMPANY C

COMPANY D

COMPANY E

This Certificate of Insurance neither affirmatively nor negatively amends, extends or alters the coverage afforded by the polices listed on this certificate of insurance.

C

O

.

L

T

R

TYPE OF INSURANCE

ADDL

INSR

WOS

POLICY

NUMBER

EFFECTI

VE

DATE

EXPIRATION

DATE

LIMITS OF LIABILITY

(Below Limits are required minimums)

COMMERCIAL GENERAL LIABILITY

[X] Occurrence (REQUIRED)

_____________________________

[] Gen’l Aggregate Limit Applies:

[X]Per Location

Y

Y

REQUIRED

REQ.

REQUIRED

GENERAL AGGREGATE

PRODUCTS-COMP/OP AGG

PERSONAL & ADV INJURY

EACH OCCURRENCE

DAMAGE RENTED PREMISES

MED. EXP. (Any one person)

$10,000,000

$10,000,000

AUTOMOBILE LIABILITY

[ X ] ANY AUTO

[] ALL OWNED AUTOS

[ ] SCHEDULED AUTOS

[] HIRED AUTOS

[] NON-OWNED AUTOS

Y

REQUIRED

REQ.

REQUIRED

BODILY INJURY & PROPERTY

DAMAGE

BODILY INJURY (Per person)

BODILY INJURY (Per accident)

PROPERTY DAMAGE (Per

accident)

$10,000,000

EXCESS / UMBRELLA LIABILITY

[] Occurrence

Y

EACH OCCURRENCE

AGGREGATE

WORKERS’ COMPENSATION AND

EMPLOYERS’ LIABILITY

N/A

REQUIRED

REQ.

REQUIRED

[X] WC STATUTORY LIMITS

E.L. EACH ACCIDENT

E.L. DISEASE - POLICY LIMIT

E.L. DISEASE - EACH EMPLOYEE

$1,000,000

$1,000,000

$1,000,000

PROPERTY INSURANCE

[X] All Risks (Special)

[X] Terrorism (BI, Building, Contents)

[X] Business Income

[X] Boiler & Machinery

[X] Property - Building

[X] Property - Contents

BI - Y

REQUIRED

REQ.

REQUIRED

AMOUNT

100% Building

& Contents

Liquor Liability - Y

GL - Terrorism - Y

Crime / Employee Dishonesty - Y

Worldwide Jurisdiction - Y

Cyber Liability - Y

N/A

N/A

REQUIRED

REQ.

REQUIRED

No specific amount for Crime is required

Cyber - $3,500,000 per claim (only for

non-Hilton system platforms)

SPECIAL PROVISIONS:

- Additional Insured Entity Required: With the exception of Commercial Property, Boiler & Machinery and WC, all policies obtained by Franchisee/Owner must name the

Franchisee/Owner as named insured and must name Hilton Worldwide Holdings Inc. and its owners, subsidiaries, and affiliates now or hereafter existing as additional

insured including their employees, officers and directors.

- Coverage must indicate Primary & Non-Contributory

- AUTO Acceptable Configurations: (i) Any-Auto (ii) All+Hired+Non (iii) Sched+Hired+Non

- Garagekeepers’ liability required unless Property has no parking operations

- EX can be combined w/ GL & Auto policies if provided. Assume Follow Form. Need specifically stated if EX covers EL

CERTIFICATE HOLDER:

Hilton Worldwide Holdings Inc.

7930 Jones Branch Drive

McLean, VA 22102

CANCELLATION:

ACORD Language

AUTHORIZED SIGNATURE:

MUST BE SIGNED

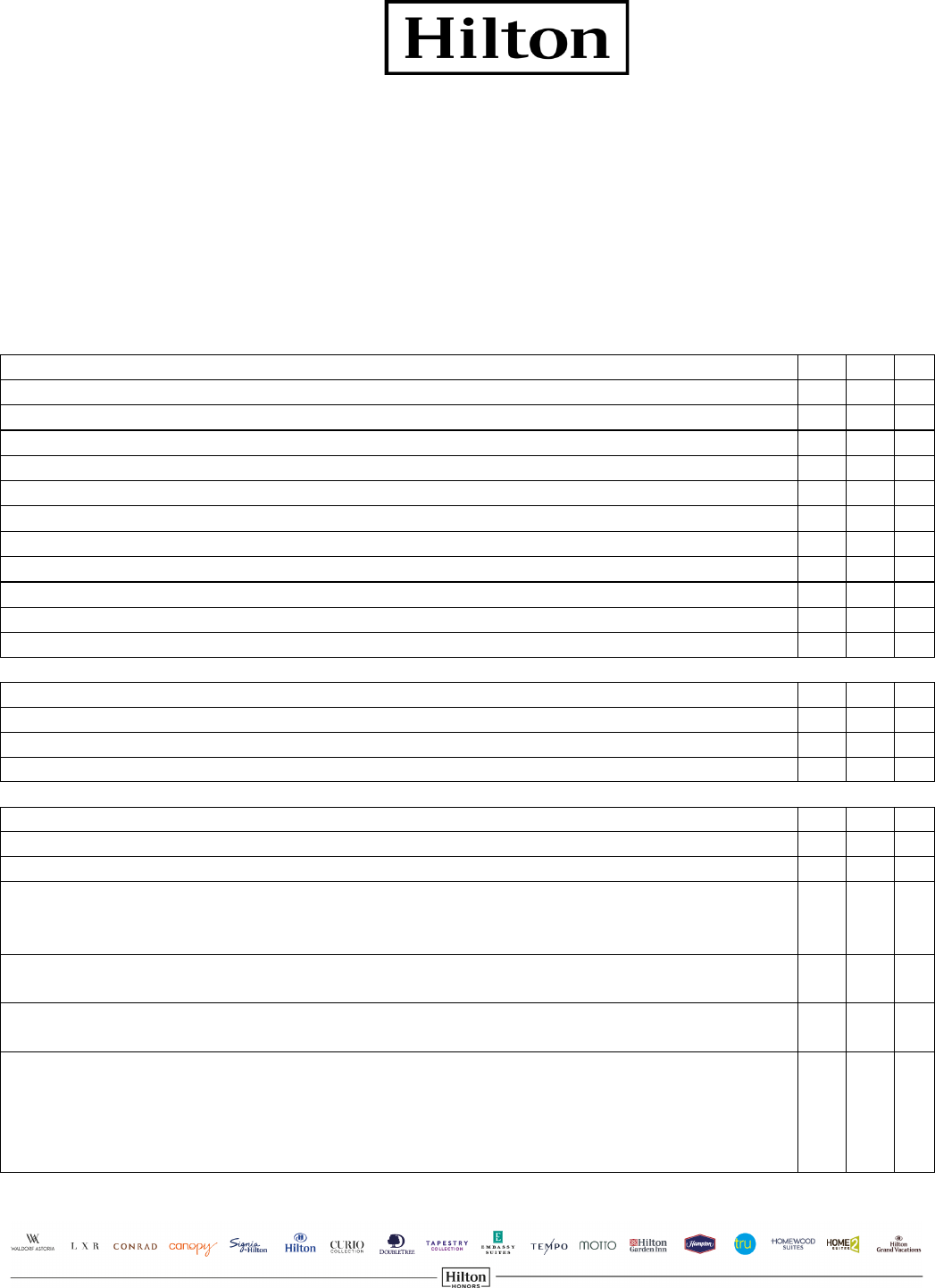

INSURANCE CHECKLIST – FRANCHISE HOTELS (US)

HAMPTON, HILTON GARDEN INN, HOMEWOOD SUITES, HOME2, TRU

INSURANCE REQUIRED DURING OPERATIONS

Location Name (including Brand) ________________________________________________________

Full Address of Location _______________________________________________________________

REQUIREMENTS COMPLIANT

YES NO N/A

GENERAL LIABILITY

$10,000,000 per occurrence

Aggregate limits apply per location (CG2504 or broader)

Innkeepers liability – per statutory requirements

Liquor liability (if hotel serves/sells alcoholic beverages)

Contractual liability

Independent contractors

Premises/operations coverage

Products/Completed operations coverage

Worldwide Jurisdiction (per CG2422 10/01 or broader)

Named Perils Pollution coverage (per CG2165 or equivalent)

Terrorism

AUTOMOBILE LIABILITY

$10,000,000 per occurrence CSL

Aggregate limits apply per location

Garagekeepers (if hotel includes parking operations)

WORKERS COMPENSATION

Workers Compensation coverage in compliance with local law

Employers Liability coverage $1M/$1M/$1M

If EL limits are satisfied through use of the Umbrella/Excess Liability, does your certificate

of insurance clearly indicate that the Umbrella/Excess Liability affords coverage for

Employers Liability?

If insured through a State Fund, Stop Gap or equivalent coverage must be purchased in

an amount no less than $1,000,000 limit per occurrence

If a qualified Self-Insurer, excess Workers Compensation and Employers Liability must be

purchased in an amount no less than $1,000,000 per occurrence

If the hotel participates as a Non-Subscriber (e.g., TX and OK) participation must be

evidenced by submitting to the Brand a copy of the Employers Notice of No Coverage or

Termination of Coverage and an ERISA-compliant Occupational Injury Benefit Plan that

covers substantially the same work-related injuries as WC. Non-Subscribers must carry EL

with limits of no less than $5M.

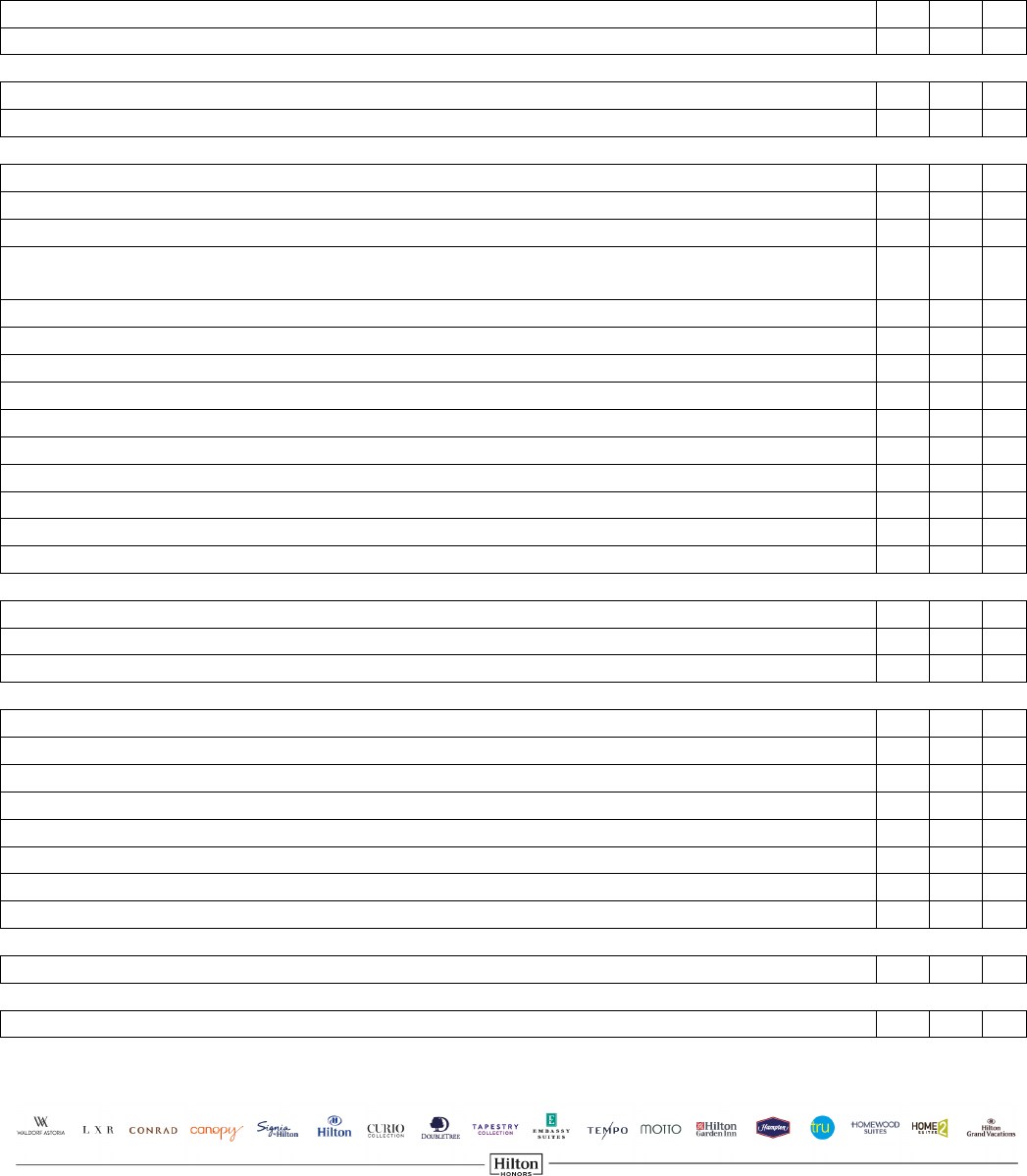

REQUIREMENTS

COMPLIANT

YES NO N/A

EMPLOYMENT PRACTICES LIABILITY (EPLI)

$1,000,000 per claim

CYBER LIABILITY

$3,500,000 per claim (only for non-Hilton system platforms)

COMMERCIAL PROPERTY

Building covered at 100% replacement cost

Contents covered at 100% replacement cost

Business income limit adequate to cover full recovery of the net profits and continuing

expenses of the Hotel (including rental income) for a 12 month period

Continuing expenses specifically include license fees and/or other fees payable to Brand

Special/All Risks coverage form

Peril of windstorm included

Building ordinance coverages included

Flood coverage included

Flood Zone verified (please provide copy of flood zone determination)

Flood Zone (please provide location’s flood zone) ____________________

Earthquake coverage included

Earthquake Zone (please provide location’s earthquake zone) _________________

Terrorism coverage on Building, Contents and Business Income

BOILER & MACHINERY

Broad form coverage included at 100% replacement value

Coverage includes Business Interruption

CRIME COVERAGE

Limit commensurate with risk – to include:

Employee Dishonesty

Forgery & Alteration

Money & Securities

Money & Securities (outside)

Computer Fraud

Counterfeit paper currency

WATERCRAFT COVERAGE – if exposure present (limit commensurate with risk)

AIRCRAFT COVERAGE - if exposure present (limit commensurate with risk)

REQUIREMENTS

COMPLIANT

GENERAL REQUIREMENTS YES NO N/A

Add as additional insured “Hilton Worldwide Holdings Inc. and its subsidiaries and

affiliates (including their respective directors, officers and employees), now or hereafter

existing” on the General Liability, Auto Liability and as Loss Payee or Additional Insured

on the Business Interruption (form CG2029 11/85, CG2010 11/85 or broader for

operations or CG2010 11/85 for construction and renovation)

Insurance companies are rated A-VII or higher by A.M. Best Company

Policies are endorsed to be primary insurance with no recourse to or contribution from

any other similar insurance, if any, carried by Hilton Worldwide Holdings Inc., its owners,

subsidiaries, and affiliates now or hereafter existing

Certificate(s) and/or Evidence of insurance, completed Checklist and additional insured

endorsements have been submitted via email to [email protected] or via fax to (866)

277-8529

Certificate Holder: Hilton Worldwide Holdings Inc. 7930 Jones Branch Drive, McLean, VA

22102

As designated representative of location’s Owner, or licensed agent/broker for the insurance policies noted above, I affirm

and attest that this Checklist is an accurate representation of insurance maintained on behalf of the above-named location.

______________________________ _______________________________ __________________________

Printed Name Signature Date

If completed by Insurance Agent/Broker:

Name of Agency/Brokerage: ________________________________________________

and Broker License Number: ________________________________________________

Address: ________________________________________________

________________________________________________

912.00-

INSURANCE

912.00 - INSURANCE

912.01 INSURANCE REQUIRED DURING CONSTRUCTION ..............................................................................................912.00-2

912.02 INSURANCE REQUIRED DURING OPERATION ......................................................................................................912.00-5

912.00 - INSURANCE

912.00-1 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

INSURANCE

NOTE: The following Insurance Requirements section is written with U.S. Dollars used for coverage types and minimum limits. The insurance obtained must meet or

exceed these brand standards based on current currency conversions.

Franchisee/Owner must meet or exceed the insurance requirements specified in this Hilton Holdings Inc., Brand Standards Manual (“Manual”), unless specifically

indicated to the contrary in the Management Agreement (“Agreement”). Insurance requirements are split into TWO areas:Insurance required during Construction (or

Significant Renovation); and Insurance required during Operation.

Wherever possible, global standards have been provided. To the extent requirements differ for hotels located within the U.S. and those located outside the U.S.,

specific standards are provided

912.01

INSURANCE REQUIRED DURING CONSTRUCTION

912.01.A

OCCUPATIONAL INJURY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: As required by local law

NOTE: Occupational Injury insurance, as required by law or regulation, must be in force prior to the hiring of any Team Members.

United States:

Minimum Required Limit: Statutory

NOTE: WC, as required by law or regulation, must be in force prior to the hiring of any Team Members.

912.01.B

EMPLOYERS LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: $1M per occurrence or as required by local law

NOTE: The EL limits can be satisfied by any combination of Occupational Injury Scheme, EL, and/or PL policies. However, the certificate of insurance must

clearly indicate that PL insurance affords coverage for EL.

United States:

Minimum Required Limit: $1M each accident, $1M each disease, $1M each Team Member

NOTE: The EL limits can be satisfied by any combination of WC, EL, and/or Excess/Umbrella policies. However, the certificate of insurance must clearly

indicate that Excess/Umbrella liability insurance affords coverage for EL.

912.01.C

GENERAL LIABILITY / PUBLIC LIABILITY

Minimum Required Limit: $10M each occurrence

NOTE: Coverage must include Products-completed operations, Personal and advertising injury, Protective liability, Independent contractors, and Liability

assumed under an insured contract (including the tort liability of another assumed in a business contract) on an "occurrence basis.” This insurance may not

have any restrictions, modifications or exclusions for explosion, collapse, underground property damage, earth movement or damage to work performed by

a subcontractor. Contractor must carry completed operations insurance for a period of not less than 5 years after the completion of the project.

912.01.D

AUTO LIABILITY

912.00 - INSURANCE

912.00-2 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: As required by local law

NOTE: As required by local law

United States:

Minimum Required Limit: $2M per occurrence

NOTE: Including, but not limited to: owned, hired, and non-owned vehicles.

912.01.E

POLLUTION LEGAL LIABILITY

Minimum Required Limit: (if exposure exists) $1M

NOTE: If the Contractor's policy is on a claims-made form, the retroactive date of the policy must be on or before the date of the commencement of

services by Contractor.

Insurance must be maintained and evidence of insurance must be provided for at least three (3) years after completion of the work. If the coverage is

canceled or not renewed, and it is not replaced with another policy with a retroactive date that precedes the date of Contractor’s agreement, the Contractor

must provide extended reporting coverage for a minimum of three (3) years.

912.01.F

UMBRELLA / EXCESS LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: See Underlying Requirements

NOTE: Insurance requirements for PL, EL and AL may be satisfied with a combination of primary umbrella and/or excess policies.

United States:

Minimum Required Limit: See Underlying Requirements

NOTE: Insurance requirements for GL, EL and AL may be satisfied with a combination of primary, umbrella / excess policies.

912.01.G

PROFESSIONAL ERRORS AND OMISSIONS

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Limits Commensurate with risks

NOTE: The Architect and all other professionals must carry E&O. Such policy shall cover claims arising out of negligent errors or omissions during the

performance of professional services and include coverage for attorney fees. The retroactive date of the policy must be shown on the certificate of

insurance and must be before the date of the agreement. If the coverage is canceled or not renewed and it is not replaced with another policy with a

retroactive date that precedes the date of this agreement, all professionals must provide extended reporting coverage for a minimum of two (2) years after

completion of the agreement or the work on the former policy. Professionals shall keep such insurance in force during the course of this Agreement for a

period of not less than two (2) years after the date of completion.

United States:

Minimum Required Limit: Limits Commensurate with risks

NOTE: The Architect and all other professionals must carry E&O.

The policy must cover negligent errors or omissions during performance of professional services and include attorney fees. Retroactive date must be

before the date of the agreement.

912.00 - INSURANCE

912.00-3 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

Professionals shall keep such insurance in force during the course of this Agreement for a period of not less than two (2) years after the date of

completion.

912.01.H

BUILDER'S RISK

Minimum Required Limit: 100% Completed Value (Full Replacement Cost) or limits sufficient to avoid co-insuranceEarthquake and Flood (not less than

75% of the replacement cost or full probable maximum loss (PML) if in an earthquake and/or flood hazard area Windstorm – 75% Replacement Cost or

PML

NOTE: “All Risk” form and including the following: cold testing, windstorm, flood (if in a 100 year zone), earthquake (if in high hazard zone) and collapse,

including collapse resulting from design error This insurance must apply to: property intended for incorporation into the work for the entire duration of the

contract including: Property in the course of construction, reconstruction, or repair;Property while in transport to the site;Property stored at the site or off

premises;Scaffolding, staging, shoring, formwork, fences, false work, and temporary buildings and any similar items commonly referred to as construction

equipment located at the site;Furniture, fixtures, andOther personal property typical to a hotel located on premises or in storage or at any other temporary

location.The policy must cover the cost of removing debris, including demolition as may be made legally necessary by the operation of any applicable law,

ordinance or regulation.Permission to occupy or a partial occupancy clause or definition must be included and allow occupancy without qualification. This

insurance must include Business Interruption coverage including the Brand's interest for full recovery of net profits and continuing expenses of the hotel

projected for 12 months following a covered loss (including Rental Value and payments that would have been owed the Brand in the absence of a loss).

This insurance must be maintained in effect until the earliest of either the date on which all persons and organizations who are insured under the policy

agree that it may be terminated or as provided for in the contract documents. This insurance must name all Franchisees/Owners of the premises, agents of

the Franchisee/Owner, and Contractors of any tier as insured. The policy must include a waiver of subrogation stating that all Franchisees/Owners and

Contractors waive their rights of subrogation against one another with respect to losses covered by this policy.

912.01.I

GENERAL REQUIREMENTS

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

NOTE: Franchisee/Owner must defend, indemnify and hold Hilton Holdings, Inc., its owners, subsidiaries and affiliates now or hereafter existing, harmless

from any and all damages or claims arising out of the failure of any Contractor, supplier or vendor doing business with the hotel to maintain adequate

insurance. Contractors must not be allowed on the site or within the premises until the stated insurance requirements are evidenced.

Contractor's insurance, with the exception of an Occupational Injury Scheme, must name Franchisee/Owner, Hilton Holdings, Inc., and each of their owners,

subsidiaries and affiliates (including their respective directors, officers and Team Members), now or hereafter existing as additional insured, and copies of

these endorsements or their equivalent must be provided to Franchisee and the Brand.

Franchisee/Owner, at its option, may purchase an "Owner controlled insurance program" or "wrap up."

United States:

NOTE: Franchisee/Owner must defend, indemnify and hold Hilton Holdings, Inc., its owners, subsidiaries and affiliates now or hereafter existing, harmless

from any and all damages or claims arising out of the failure of any Contractor, supplier or vendor doing business with the hotel to maintain adequate

insurance. Contractors must not be allowed on the site or within the premises until the stated insurance requirements are evidenced.

Contractor's insurance, with the exception of WC must name Franchisee/Owner, Hilton Holdings, Inc., and each of their owners, subsidiaries and affiliates

(including their respective directors, officers and Team Members), now or hereafter existing as additional insured on terms no less broad than forms ISO CG

912.00 - INSURANCE

912.00-4 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

20 10 11 85 or a combination of ISO forms CG 20 10 10 01 and CG 20 37 10 04 (or a substitute form providing equivalent coverage), and copies of these

endorsements or their equivalent must be provided to Franchisee/Owner and the Brand.

Franchisee/Owner, at its option, may purchase an "Owner controlled insurance program" or "wrap up."

912.02

INSURANCE REQUIRED DURING OPERATION

912.02.A

PUBLIC LIABILITY AND EXCESS LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Participation in Brand insurance program is mandatory.

NOTE: The Brand or its designee will, at Franchisee/Owner’s cost, provide upon the commencement of operation of the hotel and maintain at all times

during the term of the Agreement, third-party PL in such amounts as the Brand may deem necessary. Franchisee/Owner will be named as an additional

insured. The Brand may elect to maintain all or part of such policies under an arrangement insuring one or more hotels operated by the Brand or its

affiliates or subsidiaries, in which event the cost of such insurance to Franchisee/Owner will be allocated by the Brand on the same basis as other hotels of

the Brand.If the Brand cannot obtain coverage, Brand will advise Franchisee/Owner of acceptable insurance requirements.

912.02.B

WORKERS COMPENSATION / OCCUPATIONAL INJURY SCHEME

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: As required by local law or regulation

NOTE: Occupational Injury insurance, as required by local law or regulation, must be in force prior to the hiring of any Team Members.

United States:

Minimum Required Limit: Statutory

NOTE: To be obtained by statutory employer WC must be extended to cover ""All States,"" Voluntary Workers' Compensation, and Longshore and Harbor

Workers’ Compensation Act on an ""if any"" basis, unless the hotel is insured under a state operated fund.

Participation in a State Fund shall satisfy the requirements hereunder. If hotel participates in a State Fund, Stopgap coverage is required in an amount not

less than $1M.If the hotel self-insures WC, a copy of the license granting authority to self-insure must be furnished to the Brand and excess workers’

compensation coverage should be purchased in an amount no less than $1M. If the hotel participates as a Non-Subscriber (e.g., TX and OK) participation

must be evidenced by submitting to the Brand a copy of the Employers Notice of No Coverage or Termination of Coverage and an ERISA-compliant

Occupational Injury Benefit Plan that covers substantially the same work-related injuries as WC. Non-Subscribers must carry EL with limits of no less than

$5M.

912.02.C

EMPLOYER'S LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: $1M per occurrence or as required by local law

NOTE: The EL limits can be satisfied by any combination of Occupational Injury Scheme, EL and/or PL policies. However, the certificate of insurance must

clearly indicate that PL insurance affords coverage for EL.

United States:

912.00 - INSURANCE

912.00-5 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

Minimum Required Limit: Non-Subscribers $5M per occurrence; All others:

• $1M each accident

• $1M each disease

• $1M each Team Member

NOTE: The EL limits can be satisfied by any combination of WC, Employers Liability, and/or Excess/Umbrella policies. However, the certificate of

insurance must clearly indicate that Excess/Umbrella liability insurance affords coverage for EL.

912.02.D

GENERAL LIABILITY / PROPERTY OWNER'S LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Commensurate with Risk

NOTE: Franchisee/Owner must procure and maintain Property Owners Public Liability policy fully protecting Franchisee/Owner for liability arising out of its

ownership, possession and use of the hotel. Exposure will depend on the extent to which Franchisee/Owner is involved in day to day operation of the hotel.

Hilton recommends that Franchisee/Owner consult with a licensed insurance broker to determine appropriate limits.

United States:

Minimum Required Limit: $10M each occurrence

NOTE: The GL insurance must include coverage for the following risks: Damage to property of others and bodily injury including sickness, disease and

death. Personal and advertising injury covering liability for false arrest, libel, slander, defamation, false imprisonment, unlawful detention, wrongful or

malicious prosecution or invasion of privacy. Innkeeper’s Liability - This can be satisfied by any combination of GL or Crime coverage. Liquor Liability (if

hotel serves alcoholic beverages). Contractual Liability. Independent Contractors Liability. Premises/Operation liability. Products and Completed

Operations. Named perils pollution including coverage for liability arising out of heat, smoke or fumes from a hostile fire, or smoke, fumes, vapor or soot

produced by or originating from equipment that is used to heat, cool or dehumidify the building, or equipment that is used to heat water. Terrorism liability

(may be part of the liability policy or a separate policy). Worldwide jurisdiction covering lawsuits brought anywhere in the world from occurrences arising out

of the hotel or the operations connected with the hotel may be satisfied with a combination of GL and umbrella/ excess insurance policies. Aggregate limits,

if any, must be on no less than a “per location” basis

912.02.E

AUTO LIABILITY

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: The greater of US$25,000 and limit required by local law

NOTE: If hotel owns and operates vehicles, Franchisee/Owner must procure and maintain AL as required by local law or regulation subject to a US$25,000

minimum

United States:

Minimum Required Limit: $10M each occurrence

NOTE: Including, but not limited to: owned, hired, and non-owned vehicles

May be satisfied with a combination of AL and umbrella/excess insurance policies.

Aggregate limits, if any, must be on a “per location” basis.

Garage Keeper’s Liability must be included if the hotel’s operations include parking operations. This may be included under GL if there are no hotel

vehicles.

912.00 - INSURANCE

912.00-6 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

912.02.F

WATERCRAFT LIABILITY

Minimum Required Limit: Commensurate with Risk

NOTE: Hilton recommends that Franchisee/Owner consult with a licensed insurance broker to determine appropriate limits

912.02.G

AIRCRAFT LIABILITY

Minimum Required Limit: Commensurate with Risk

NOTE: Hilton recommends that Franchisee/Owner consult with a licensed insurance broker to determine appropriate limits.

912.02.H

COMMERCIAL PROPERTY AND BUSINESS INTERRUPTION

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Full Replacement Cost or limits sufficient to avoid co-insurance

Earthquake and Flood (not less than 75% of the replacement cost or full probable maximum loss (PML) if in an earthquake and/or flood hazard area

Windstorm – 75% Replacement Cost or PML

NOTE: Property Damage on a special causes of loss policy form (""All Risks""), including terrorism (may be part of the liability policy or a separate policy)

covering 100% of the insurable replacement value of the building and its contents. Such limit must be sufficient to avoid a co-insurance penalty, if

applicable. The policy must include coverage for the peril of windstorm and for ordinance and law.

This requirement for Earthquake and Flood only applies to hotels in an earthquake or flood hazard area. Please work with your insurance professional to

determine whether or not your hotel is in a high hazard area.

If a PML study is being used to determine appropriate earthquake, flood or wind limits, the PML must be based on the results of a professional study.

United States:

Minimum Required Limit: Full Replacement Cost or limits sufficient to avoid co-insurance

Earthquake and flood (not less than 75% of the replacement cost or full probable maximum loss (PML) if in an earthquake and flood hazard area

Windstorm – 75% Replacement Cost or full PML

NOTE: Property Damage on a special causes of loss policy form ("all–risks"), including terrorism (may be part of the property policy or a separate policy)

covering 100% of the insurable replacement value of the building and its contents. Such limit must be sufficient to avoid a co-insurance penalty, if

applicable. The policy must include coverage for the peril of windstorm and for ordinance and law.

The requirement for Earthquake and flood only apply to hotels in an earthquake or flood hazard areas. Please work with your insurance professional to

determine whether or not your hotel is in a high hazard area.

If a PML study is being used to determine appropriate earthquake, flood or wind limits, the PML must be based on the results of a professional study.

Continuing expenses must specifically include royalty/license fees and other fees payable to the Brand, its subsidiaries and affiliates. HWI and its owners,

subsidiaries and affiliates now or hereafter existing must be included as an additional insured as respects their interest in Business Interruption insurance.

912.02.I

BOILER AND MACHINERY (EQUIPMENT BREAKDOWN)

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Full replacement cost of items

NOTE: Broad form Boiler and Machinery insurance against loss from accidental damage to, or from the explosion of, boilers, air conditioning systems,

including refrigeration and heating apparatus, pressure vessels and pressure pipes in an amount equal to 100% of the actual replacement value of such

912.00 - INSURANCE

912.00-7 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

items (without taking into account any depreciation) plus full recovery of the net profits and continuing expenses of the hotel. Continuing expenses must

specifically include royalty/license fees and other fees payable to the Brand.

United States:

Minimum Required Limit: Full replacement cost of items

NOTE: Broad form Boiler and Machinery insurance, including business interruption coverage, against loss from accidental damage to, or from the explosion

of, boilers, air conditioning systems, including refrigeration and heating apparatus, pressure vessels and pressure pipes.

Must include full recovery of the net profits and continuing expenses of the hotel. Continuing expenses must specifically include royalty/license fees and

other fees payable to the Brand.

912.02.J

TERRORISM

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

Minimum Required Limit: Full replacement cost and business interruption

Third party liability if not covered in the GL policy

NOTE: Terrorism coverage shall be obtained and maintained for both first-party damage and-third party liability either stand-alone, through a government

operated or mandated pool, or as part of the PL coverage and the Property Damage/ Business Interruption coverage.

United States:

Minimum Required Limit: Full replacement cost and business interruption

Third-party liability if not covered in the GL policy

NOTE: May be either stand-alone or through a government operated or mandated pool, or as part of the GL coverage and the Property Damage/Business

Interruption coverage. Must include full recovery of the net profits and continuing expenses of the hotel. Continuing expenses must specifically include

royalty/license fees and other fees payable to the Brand.

912.02.K

CRIME

Minimum Required Limit: Commensurate with risk

NOTE: Please consult with a licensed insurance broker to determine appropriate limits. The Crime insurance must include coverage for the following risks

and consider more than cash on hand: Team Member DishonestyForgery & AlterationMoney & SecuritiesComputer FraudSafe RobberyCounterfeit Paper

912.02.L

GENERAL REQUIREMENTS

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America: NOTE: With the exception of

Property, Boiler & Machinery and Occupational Injury, all policies obtained by Franchisee/Owner must name the Franchisee/Owner as named insured, and

must name Hilton Holdings, Inc., and its owners, subsidiaries and affiliates now or hereafter existing as additional insured including their Team Members,

officers and directors. All policies of Franchisee/Owner must be endorsed to be primary insurance with no recourse to, or contribution from, any other

similar insurance, if any, which may be carried by Hilton Holdings, Inc., and its owners, subsidiaries and affiliates. Evidence of such must be supplied to the

Brand.Any deductibles or self-insured retentions above $50,000 or 5% of the replacement cost of the hotel must be declared to and approved by Hilton

Holdings, Inc., Risk Management Department, at: 7930 Jones Brand Drive, McLean, VA 22102; Email: [email protected] by

Franchisee/Owner to modify requirements for Earthquake, Flood, Windstorm or Terrorism may be submitted to Hilton Risk Management for consideration.

Guidelines for such requests may be requested at [email protected]/Owner must deliver or cause to be delivered to the Brand

912.00 - INSURANCE

912.00-8 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

upon renewal or change in limits or coverage each of the following:Certificates of insurance or documentation acceptable to Hilton Holdings, Inc.,

evidencing the insurance, including applicable endorsements. Where applicable each certificate must specifically identify and/or list: Insured location(s) by

name, address and Facility ID number.Relevant policy numbersRelevant parties as being named additional insured (as specified above)Correct Hilton legal

entity as certificate holder (Hilton Inc., 7930 Jones Branch Dr., McLean, VA 22102)For Property, Boiler & Machinery and Business

InterruptionWindstormEarthquake and/or Flood as appropriateTerrorism (unless provided separately)A signed letter written or translated to English from the

insurance agent or broker who placed the required insurance affirming that he or she has read and understood the insurance requirements contained in this

Manual. This letter must specifically address whether the insurance the agent or broker has placed complies with the insurance requirements set forth in

this Manual.A signed checklist from the insurance agent or broker indicating whether there is coverage for each of the minimum requirements set forth in

this Manual.For samples of these letters and checklists, as well as sample certificates and evidence of property insurance, please request a copy from

Hilton Holdings, Inc., Risk Management department at [email protected] notice purposes the certificate holder is “Hilton Holdings, Inc.,

Attn: Risk Management, 7930 Jones Branch Drive, McLean, VA 22102"All certificates or other documents evidencing insurance must be provided in

English with currency indicated in U.S. dollars. Limits required in this standard may be satisfied in the local currency equivalent at the time the policy is

purchased.All evidence of insurance required herein including certificates must be sent, either by fax, email or upload, to Hilton Holdings, Inc.'s, external

partner as indicated on OnQ’s Risk Management page: Proof of Insurance (Certificates).Hilton Holdings, Inc.'s, external partner will review and audit each

certificate of insurance in line with requirements as set out in this Manual.If Franchisee/Owner does not obtain or maintain the required insurance or policy

limits, the Brand can (but is not obligated to) obtain and maintain the insurance or such portion of the insurance (Difference in Limits”/”Difference in

Conditions”) needed to bring Franchisee/Owner’s insurance in line with the requirements herein for Franchisee/Owner without first giving Franchisee/

Owner notice. If the Brand does so, then Franchisee/Owner must immediately pay the Brand upon request, the premiums and costs incurred by Brand.The

Brand makes no representation, implied or express, that the foregoing insurance requirements are adequate to protect Franchisee/Owner.The insurance

coverage requirements contained in this Manual are only minimum requirements. These requirements do not relieve Franchisee/Owner from responsibility

for any loss or claim for damages arising out of the Agreement. Franchisee/Owner must indemnify the Brand for any claim for damages due to failure of

Franchisee/Owner or any Contractor, supplier or vendor doing business with Franchisee/Owner to maintain adequate insurance.To ensure compliance, the

Brand strongly recommends that Franchisee/Owner reproduce all insurance requirements in this Manual in full and submit it to a licensed agent or broker

experienced in writing insurance for hotels.Failure of the Brand to demand evidence of compliance with the insurance requirements in this Manual or failure

of the Brand to identify a deficiency from evidence that is provided shall not be construed as a waiver of Franchisee/Owner's obligation to maintain such

insurance.At the request of the Brand, Franchisee/Owner must deliver a copy of each policy bearing certification of the insurance company underwriter(s),

that the policy is a complete copy of the policy issued with all endorsements to the Brand.The Brand may increase or decrease the minimum amount of

insurance, require additional or different types of insurance, or otherwise change the requirements to make them comparable to the amount and kinds of

insurance carried by other properties or hotels, taking into account the size and location of the hotel and changing circumstances in the law and insurance

marketplace.Franchisee/Owner must obtain and maintain any other insurance required by local or national statute or law.

United States: NOTE: All required insurance must be purchased from insurance companies with a financial rating acceptable to Hilton, which shall be no

less than A - VII if rated by the company A.M. Best.

Any deductibles or self-insured retentions above 50,000 USD or 5% of the replacement cost of the hotel must be declared to and approved by Hilton

Holdings, Inc.'s, Risk Management Department, at: 7930 Jones Branch Drive, McLean, VA 22102; Email: [email protected].

Evidence shall be provided via certificate upon renewal or change in limits or coverage and shall be provided to Hilton or their designee and must include

the following:With the exception of Commercial Property, Boiler & Machinery and WC, all policies obtained by Franchisee/Owner must name the

Franchisee/Owner as named insured, and must name Hilton Holdings, Inc., and its owners, subsidiaries and affiliates now or hereafter existing as

912.00 - INSURANCE

912.00-9 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

additional insured including their Team Members, officers and directors.

All policies of Franchisee/Owner must be endorsed to be primary insurance with no recourse to, or contribution from, any other similar insurance, if any,

which may be carried by Hilton Holdings, Inc., and its owners, subsidiaries and affiliates. Evidence of such must be supplied to the Brand. Requests by

Franchisee/Owner to modify requirements for Earthquake, Flood, Windstorm or Terrorism may be submitted to Hilton Risk Management for consideration.

Guidelines for such requests may be requested from [email protected].

Franchisee/Owner must deliver or cause to be delivered to the Brand upon renewal or change in limits or coverage each of the following:

Certificates of insurance or documentation acceptable to Hilton Holdings, Inc., evidencing the insurance, including applicable endorsements. Where

applicable each certificate must specifically identify and/or list: Insured location(s) by name, address and Facility ID number Relevant policy numbers

Relevant parties as being named additional insured (as specified above) Correct Hilton legal entity as certificate holder (Hilton Holdings, Inc., 7930 Jones

Branch Dr., McLean, VA 22102) For GL:

Terrorism (unless provided separately)Garage Keeper’s Liability Liquor Liability Worldwide Jurisdiction Policies as being primary and non-contributoryFor

Property, Boiler & Machinery and Business Interruption

Windstorm Earthquake and/or Flood as appropriate Terrorism (unless provided separately) All evidence of insurance required herein including certificates

must be sent, either by fax, email or upload, to Hilton Holdings, Inc., external partner as indicated on OnQ’s Risk Management page: Proof of Insurance

(Certificates).

Hilton Holdings, Inc.'s, external partner will review and audit each certificate of insurance in line with requirements as set out in this Manual. If Franchisee/

Owner does not obtain or maintain the required insurance or policy limits, the Brand can (but is not obligated to) obtain and maintain the insurance or such

portion of the insurance (Difference in Limits”/”Difference in Conditions”) needed to bring Franchisee/Owner’s insurance in line with the requirements herein

for Franchisee/Owner without first giving Franchisee/Owner notice. If the Brand does so, then Franchisee/Owner must immediately pay to the Brand, upon

request, the premiums and costs incurred by Brand.

The Brand makes no representation, implied or express, that the foregoing insurance requirements are adequate to protect Franchisee/Owner.

The insurance coverage requirements contained in this Manual are only minimum requirements. These requirements do not relieve Franchisee/Owner from

responsibility for any loss or claim for damages arising out of the Agreement. Franchisee/Owner must indemnify the Brand for any claim for damages due

to failure of Franchisee/Owner or any Contractor, supplier or vendor doing business with Franchisee/Owner to maintain adequate insurance.

To ensure compliance, the Brand strongly recommends that Franchisee/Owner reproduce all insurance requirements in this Manual in full and submit it to a

licensed agent or broker experienced in writing insurance for hotels.

Failure of the Brand to demand evidence of compliance with the insurance requirements in this Manual or failure of the Brand to identify a deficiency from

evidence that is provided shall not be construed as a waiver of Franchisee/Owner's obligation to maintain such insurance.

At the request of the Brand, Franchisee/Owner must deliver a copy of each policy bearing certification of the insurance company underwriter(s), that the

policy is a complete copy of the policy issued with all endorsements to the Brand.

The Brand may increase or decrease the minimum amount of insurance, require additional or different types of insurance, or otherwise change the

requirements to make them comparable to the amount and kinds of insurance carried by other properties or hotels, taking into account the size and location

of the hotel and changing circumstances in the law and insurance marketplace.

Franchisee/Owner must obtain and maintain any other insurance required by local or national statute or law.

912.02.M

BUSINESS INTERRUPTION

Asia Pacific | Canada | Central America | Europe | Mexico | Middle East and Africa | Puerto Rico | South America:

912.00 - INSURANCE

912.00-10 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021

Minimum Required Limit: Full recovery of net profits and continuing expenses for 12 months

NOTE: Full recovery of the net profits and continuing expenses of the hotel (including rental value) for a 12 month period must be carried. Such limit must

be sufficient to avoid a co-insurance penalty, if applicable.

Continuing expenses must specifically include royalty/license fees and other fees payable to the Brand, its subsidiaries and affiliates. The policy must

include coverage for all perils identified for Commercial Property Insurance and Boiler & Machinery above.

Hilton Holdings, Inc., and its owners, subsidiaries and affiliates now or hereafter existing must be included as an additional insured as respects their

interest in Business Interruption insurance.

912.02.N

UMBRELLA / EXCESS LIABILITY

United States:

Minimum Required Limit: See Underlying Requirements.

NOTE: Umbrella or other excess policies may be utilized in conjunction with primary policies to achieve the required insurance limits for GL, AL and EL.

Aggregate limits must be per location.

912.02.O

CYBER LIABILITY

United States:

Minimum Required Limit: $3.5M per occurrence and In the aggregate

NOTE: This coverage is only required for non-Hilton computer systems. Coverage must include the following:

Security and Privacy Liability Event Management Cyber Extortion Crisis Fund Event

912.02.P

EMPLOYMENT PRACTICES LIABILITY INSURANCE

United States:

Minimum Required Limit: $1M per occurrence

NOTE: Such insurance shall include coverage for class action multi party claims

912.00 - INSURANCE

912.00-11 CONFIDENTIAL

Hampton - Brand Standards - Global

Generated On April 16, 2021