BUREAU OF CONSUMER FINANCIAL PROTECTION | MARCH 202 1

Consumer Response

Annual Report

January 1 – December 31, 2020

1 CONSUMER FINANCIAL PROTECTION BUREAU

Message from

the Acting Director

I am pleased to present the Bureau of Consumer Financial

Protection’s (CFPB or Bureau) Consumer Response 2020 Annual

Report, as required by Section 1013(b)(3)(C) of the Dodd-Frank

Wall Street Reform and Consumer Protection Act (Dodd-Frank

Act).

The year 2020 was unprecedented. While that word may be overused lately, it is accurate,

nonetheless. The global pandemic was perhaps the most disruptive long-term event we will see

in our lifetimes. Not surprisingly, the shockwaves it sent across the planet were felt deeply in the

consumer financial marketplace.

In March 2020, state and local governments implemented stay-at-home orders, businesses

closed, and millions of Americans were suddenly out of work. They needed help navigating their

new financial reality and turned to the CFPB. This is reflected in 2020’s complaint volume.

Before the pandemic, the Bureau handled approximately 300,000 consumer complaints

annually. In 2020, the Bureau received more than 540,000 consumer complaints. For seven of

the nine months since March 2020, the Bureau managed record complaint volume and

continued to route consumers’ complaints to financial companies in less than one day.

Companies provided timely responses to 99% of complaints received from the Bureau.

Although the increased volume is primarily attributed to credit and consumer reporting

complaints, this report includes an extended discussion of COVID-19 related complaints to help

readers better understand how the pandemic impacted consumer’s financial lives. In addition,

this report contains an overall analysis of complaint data to inform the marketplace and to

empower consumers to take more control over their financial lives.

This report also includes information about how the Bureau handles complaints to help the

public understand the complaint analyses in context. Finally, it describes trends seen this year,

and highlights notable deviations from the prior year’s trends.

Of course, this report can only provide a point-in-time snapshot of an ongoing situation. That’s

why it’s so important that the Bureau has delivered on its earlier promise to make more

sophisticated analytical tools available to the public. In 2020 the Bureau completed its work to

2 CONSUMER FINANCIAL PROTECTION BUREAU

add data visualization and trend analytics tools to the Consumer Complaint Database. Now,

during this especially critical time, it is easier for consumers, researchers, advocates, and other

stakeholders, including financial companies, to explore the data in near-real-time in a flexible

and powerful interface.

As the nation continues to move through this challenging period, I am confident that the Bureau

will remain a place where consumers can turn for help navigating challenges they face in the

financial marketplace. One of my top priorities is ensuring that consumers who submit

complaints receive substantive responses to the issues described in their complaints, and that

companies provide relief consumers deserve.

To supplement this Annual Report to Congress and in support the goals set forth in the

Executive Order on Advancing Racial Equity and Support for Underserved Communities

Through the Federal Government, the Bureau continues to analyze complaint data to

understand and detail disparities observed in complaints submitted by consumers from Black,

Brown, and Indigenous communities and will publish these analyses to inform the marketplace.

Complaints will continue to play an integral and central role in informing the Bureau’s policy

priorities and day-to-day work on behalf of consumers.

Going forward, the Bureau will work to amplify consumer voices so that they are heard at every

level of this organization. From rulemaking to COVID education to increasing racial equities to

punishing bad actors, the Bureau will seek out, listen to, and integrate consumer voices via

complaints into Bureau priorities.

Sincerely,

David Uejio

Acting Director

3 CONSUMER FINANCIAL PROTECTION BUREAU

Table of Contents

Message from the Acting Director .................................................................................1

Table of Contents .............................................................................................................3

1. Introduction ................................................................................................................4

2. Complaint Numbers ..................................................................................................7

3. Complaint Resolution .............................................................................................16

4. Complaint Types ......................................................................................................18

4.1 Credit or consumer reporting.................................................................. 20

4.2 Debt collection ......................................................................................... 27

4.3 Credit cards .............................................................................................. 37

4.4 Checking or savings account ...................................................................44

4.5 Mortgages................................................................................................. 50

4.6 Money transfers, money services, and virtual currencies ...................... 58

4.7 Vehicle loans or lease...............................................................................64

4.8 Prepaid cards ...........................................................................................69

4.9 Student loans ........................................................................................... 73

4.10 Personal loans .......................................................................................... 79

4.11 Payday loans ............................................................................................ 83

4.12 Credit repair ............................................................................................. 87

4.13 Title loans .................................................................................................89

5. Conclusion................................................................................................................92

4 CONSUMER FINANCIAL PROTECTION BUREAU

1. Introduction

One of the primary functions of the Bureau of Consumer Financial Protection (CFPB or Bureau)

is collecting, investigating, and responding to consumer complaints.

1

Created by the Bureau,

under the Dodd-Frank Wall Street Reform and Consumer Protection Act, the Office of

Consumer Response (Consumer Response)

2

maintains procedures to provide timely responses

to consumer complaints.

3

Consumer Response also analyzes and shares complaint data to

inform the marketplace and to empower consumers to take more control over their financial

lives.

In 2020, the Bureau received approximately 542,300 consumer complaints.

4

The Bureau

receives consumer complaints through its website, by referral from the White House,

congressional offices, and other federal and state agencies, and by telephone,

5

mail, email, and

fax.

6

Consumers submitted approximately 89% of complaints by visiting the CFPB’s website and

5% by calling the CFPB’s toll-free telephone number. The remaining 6% were submitted via

postal mail, fax, or referral.

When consumers submit complaints online

or over the phone, the Bureau asks them to identify

the consumer financial product or service with which they have a problem, as well as the type of

problem they are having with that product or service. This provides information that the Bureau

can use to analyze complaints. The Bureau’s complaint form also requires consumers to affirm

that the information provided in their complaint is true to the best of their knowledge and belief.

1

See Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, Pub. L. No. 111-203 (Dodd-Frank Act),

Section 1021(c)(2). See also § 1002(4) (“The term ‘consumer’ means an individual or an agent, trustee, or

representative acting on behalf of an individual.”).

2

Id. § 1013(b)(3)(A).

3

Consumer complaints are submissions that express dissatisfaction with, or communicate suspicion of wrongful

conduct by, an identifiable entity related to a consumer’s personal experience with a financial product or service.

4

This report covers complaints submitted in calendar year 2020 about a variety of consumer financial products and

services: credit or consumer reporting; debt collection; mortgages; credit cards; checking or savings accounts;

student loans; money transfers, money services, and virtual currencies; vehicle loans or leases; personal loans;

payday loans; prepaid cards; credit repair; and, title loans.

5

In addition to taking consumers’ complaints and providing complaint status updates over the telephone via a toll-

free number, the Bureau also provides consumers with answers to frequently asked questions about consumer

financial products and services over the telephone. Representatives at the Bureau’s U.S.-based contact center

answer consumers’ inquiries, providing clear, unbiased answers and pointing them to CFPB-created tools like

Ask

CFPB and “Protecting your finances during the coronavirus p an de mi c.” The Bureau provides services to consumers

in more than 180 languages and to consumers who are deaf, have hearing loss, or have speech disabilities. In 2020,

the Bureau received an average of more than 17,200 tel ephone calls per month.

6

See Dodd-Frank Act § 1013(b)(3).

5 CONSUMER FINANCIAL PROTECTION BUREAU

The Bureau encourages consumers to submit complaints through its website whenever possible.

The online complaint form helps to ensure completeness of information and enables the Bureau

to send the complaint to the named company quickly—on average, in one day or less. The online

complaint form allows consumers to attach supporting documentation to their complaint, which

often helps companies assess issues raised by consumers. Consumers can also check on the

status of their complaint and access relevant educational resources in the web-based Consumer

Portal.

The Bureau routes consumers’ complaints about financial products and services—and any

documents they provide—directly to financial companies, and works to get consumers a timely

response, generally within 15 days. Secure, web-based Company and Consumer Portals protect

consumer privacy and the confidentiality of companies’ responses to consumers. Where

appropriate, the Bureau routes complaint referrals to other federal agencies through the secure,

web-based Government Portal.

7

After a consumer receives the company’s response to their complaint, the consumer can provide

feedback on the company’s response by completing an optional survey. This optional survey

invites consumers to provide feedback to three prompts:

The company's response addressed all of my issues;

I understand the company's response to my complaint; and

The company did what they said they would do with my complaint.

In addition to answering yes or no to these three statements, consumers can provide narrative

text in support of their answers. Consumers have 60 days from the date the company responded

to complete the survey. This information is made available to companies via the Company

Portal.

Consumers’ complaints and companies’ responses provide the Bureau with important

information about the types of challenges consumers are experiencing with financial products

and services and how companies are responding to consumers’ concerns. The Bureau used a

variety of approaches to identify trends and possible consumer harm in the more than 540,000

complaints received in 2020. Examples include:

7

Dodd-Frank Act § 1013(b)(3)(A) (“The Director shall coordinate with the Federal Trade Commission or other

Federal agencies to route complaints to such agencies, where appropriate.”).

6 CONSUMER FINANCIAL PROTECTION BUREAU

Reviewing cohorts of complaints and company responses to assess the accuracy,

timeliness, and completeness of an individual company’s responses to complaints sent to

them for response

Conducting text analytics to identify emerging trends and statistical anomalies in large

volumes of complaints

Visualizing data to highlight geographic and temporal patterns and using tools to filter,

sort, and search complaints

These analyses support the Bureau’s work to supervise companies, enforce federal consumer

financial laws, propose rules, spot and assess emerging issues, and develop tools that help

empower consumers to make informed financial decisions. The Bureau also shares consumer

complaint information with prudential regulators, the Federal Trade Commission, other federal

agencies, and state agencies using the Government Portal.

8

In keeping with the Bureau’s statutory responsibilities and its commitment to accountability,

this report provides information and analysis about complaints received by the Bureau from

January 1 through December 31, 2020, including information and analysis about complaint

numbers, complaint types, and, where applicable, information about the resolution of

complaints.

9

8

Id. § 1013(b)(3)(D).

9

This report fulfills the reporting requirements of Dodd-Frank Act Section 1013(b)(3)(C), which instructs the Bureau

to report on the complaints received by the Bureau in the prior year regarding consumer financial products and

services. “Complaints received” include those sent to companies for a response and those routed to other federal

agencies as required by Section 1013(b)(3)(A).

7 CONSUMER FINANCIAL PROTECTION BUREAU

2. Complaint Numbers

The Bureau received approximately 542,300 consumer complaints in 2020.

10

As of February 1,

2021, the Bureau sent approximately 456,100 (or 84%) of these complaints to companies for

review and response, referred 9% of complaints received to other regulatory agencies, and found

7% to be incomplete. Additionally, 0.2% of complaints were pending with the consumer and

0.1% were pending with Bureau (see Figure 1A, Routing Outcomes).

FIGURE 1: COMPLAINT OUTCOMES IN 2020

A. Routing Outcomes B. Company Responses

Approximately 3,300 companies responded to complaints sent to them for review and response

by the Bureau in 2020. Companies categorize their response to consumers’ complaints.

Response category options include “Closed with monetary relief,” “Closed with non-monetary

relief,” “Closed with explanation,” “In progress,” and administrative options. Companies provide

an administrative response when further review by the Bureau may be needed. This includes

complaints submitted by unauthorized third parties, complaints that are the result of fraud,

10

This report excludes some complaints that the Bureau received, including multiple complaints submitted by a given

consumer on the same issue (i.e., duplicates), whistleblower tips, and complaints the Bureau found were submitted

without the consumer’s authorization. Complaint data in this report is current as of February 1, 2021. Complaint

numbers are rounded throughout the report; therefore, numbers and percentages may not sum to sub-totals or

100%.

8 CONSUMER FINANCIAL PROTECTION BUREAU

scams or business identity theft, and complaints where a company cannot confirm a commercial

relationship with the consumer.

Companies confirmed a commercial relationship with the named consumer and provided a

substantive response to the consumer and the CFPB (i.e., “Closed with monetary relief,” “Closed

with non-monetary relief,” “Closed with explanation,”) to approximately 436,400 complaints

(see Figure 1B, Company Responses). Companies provided an administrative response to

approximately 11,100 complaints. As of February 1, 2021, approximately 3,900 complaints were

being reviewed by companies. In 2020, approximately 4,600 complaints did not receive a timely

response from companies. Section 3 of this report (Complaint Resolution), provides more

details about types of company responses.

The remainder of this section analyzes complaints received in 2020 by:

Product and service

Geographic region

Mention of coronavirus or related keywords

11

Special population (servicemembers and older consumers)

12

11

For this report, “Mention of coronavirus or related keywords” is based on a search of complaint narratives using the

following search string: “covid OR coronavirus OR pandemic OR (corona AND virus) OR (global AND virus) OR

Stimulus OR PPP OR ‘paycheck protection’”. Use of this string enables the Bureau to identify a sub-population of

complaints for analysis.

12

“Older consumers” and “servicemembers” are b oth self-identified. Servicemembers refers to servicemembers,

veterans, and military families. “Ol de r consume rs” refers to consumers who voluntarily reported their age as 62 or

older.

9 CONSUMER FINANCIAL PROTECTION BUREAU

Products and Services

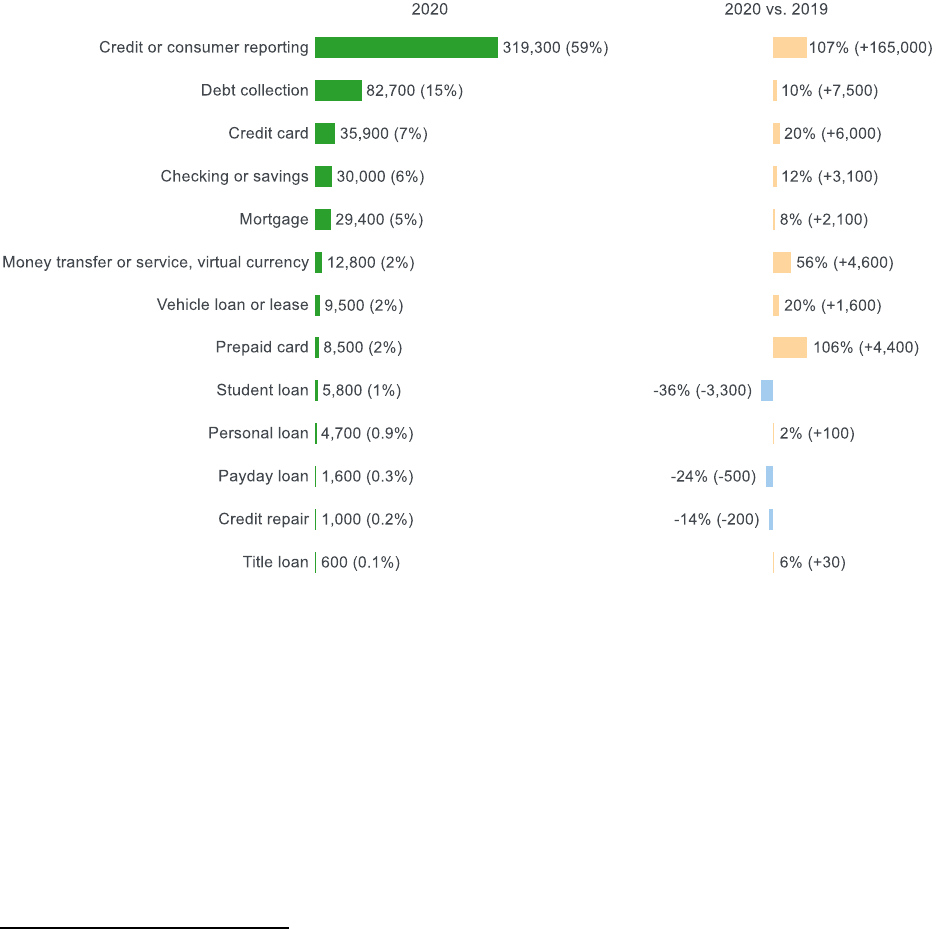

As shown in Figure 2, credit or consumer reporting, debt collection, credit card, checking or

savings accounts, and mortgage were the most complained about consumer financial product

and service categories in 2020. Collectively, these products comprised approximately 92% of all

complaints the Bureau received in 2020.

FIGURE 2: COMPLAINT VOLUME BY FINANCIAL PRODUCT OR SERVICE

13

13

The volume of complaints is not equal to the volume of consumers who submitted complaints to the Bureau (see

e.g., Credit or consumer reporting, Section 4.1). This figure excludes approximately 300 complaints where the

consumer did not indicate a specific consumer financial product or service.

10 CONSUMER FINANCIAL PROTECTION BUREAU

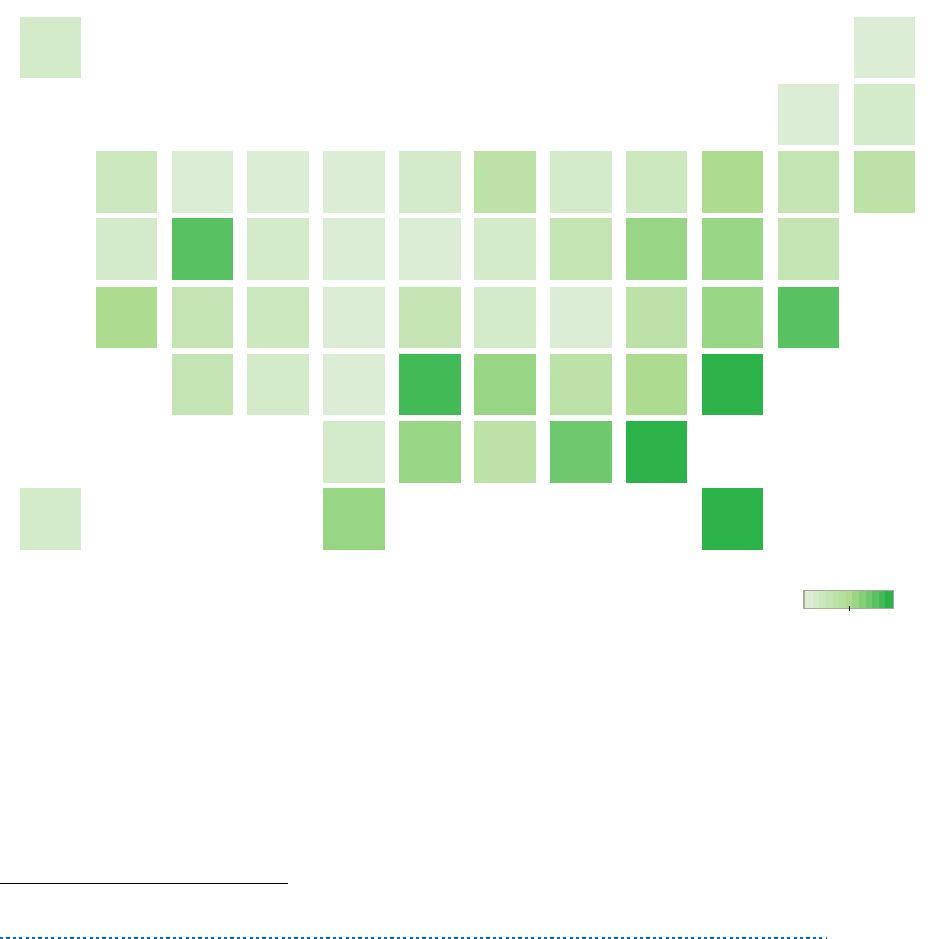

Geographic Region

Consumers from all 50 states and the District of Columbia submitted complaints to the Bureau.

To understand state and regional trends, the Bureau analyzes the geographic distribution of

complaints after accounting for population differences. Figure 3 shows that, on a per capita

basis, the Bureau received more complaints from consumers from Florida than anywhere else in

the United States, followed by consumers in Washington, D.C., Georgia, Arkansas, and Nevada.

Consumers in South Dakota submitted the fewest complaints of any state per capita.

FIGURE 3: U.S. COMPLAINT SUBMISSIONS PER 100K POPULATION

14

14

Population data is from 2019 U.S. Census data as of July 1, 2019, available at

https://www2.census.gov/programssurveys/popest/tables/2010-2019/state/totals/nst-est2019-01.xlsx

.

WY

60

WV

40

WI

60

WA

85

VT

50

VA

134

UT

112

TX

197

TN

189

SD

39

SC

173

RI

102

PA

203

OR

69

OK

68

OH

109

NY

184

NV

254

NM

64

NJ

195

NH

62

NE

48

ND

41

NC

142

MT

52

MS

136

MO

104

MN

73

MI

96

ME

50

MD

201

MA

140

LA

190

KY

61

KS

57

IN

71

IL

137

ID

53

IA

45

HI

80

GA

304

FL

309

DE

252

DC

307

CT

115

CO

99

CA

166

AZ

113

AR

274

AL

245

AK

70

39 309

11 CONSUMER FINANCIAL PROTECTION BUREAU

Coronavirus Pandemic

The volume of complaints the Bureau receives each month is influenced by numerous factors,

including changing market conditions. On March 13, 2020, the President declared a national

emergency as a result of the coronavirus (COVID-19) pandemic. Consumer Response began to

monitor and analyze pandemic-related problems and issues reported by consumers. The Bureau

has used these complaint insights to inform its work in response to the pandemic, including its

supervisory and enforcement activities. The Bureau has also shared complaint information with

federal and state agencies to ensure other regulators have useful information to support

consumers. In 2020, consumers submitted approximately 32,100 complaints mentioning

coronavirus or related keywords. As shown in Figure 4, beginning in April 2020, consumers

submitted over 3,000 such complaints nearly every month. While complaints mentioning

coronavirus or related keywords represent just 6% of submissions in 2020, the absence of

coronavirus keywords in a complaint does not necessarily mean the complaint was not related to

the financial impact of the pandemic. Section 4 of this report (Complaint Types) further

analyzes complaints where the keywords were present.

FIGURE 4: COMPLAINTS SUBMITTED MENTIONING CORONAVIRUS OR RELATED KEYWORDS, BY MONTH

Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20

0

1,000

2,000

3,000

4,000

COVID

12 CONSUMER FINANCIAL PROTECTION BUREAU

Servicemembers

Consumer Response and the Bureau’s Office of Servicemember Affairs monitor and analyze

complaints from servicemembers, veterans, and military families (collectively referred to as

“servicemembers” in this report). When submitting a complaint to the Bureau, consumers have

the option to identify their military status (active duty, reserve, guard, veteran, or military

dependent), branch of service, and rank. Consumers provided their servicemember affiliation in

approximately 40,800 complaints, or 8% of all complaints submitted in 2020. As shown in

Figure 5, self-identified servicemembers submitted complaints about debt collection, mortgages,

credit cards, checking or savings, vehicle loans or leases, money transfer or service, and virtual

currency at slightly higher rates than non-servicemembers and about credit or consumer

reporting at much lower rates

15

. Section 4 of this report (Complaint Types) analyzes some of

these differences.

15

Servicemembers are defined as those who self-identify as a “servicemember.”

13 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 5: COMPLAINTS SUBMITTED BY SERVICEMEMBERS AND NON-SERVICEMEMBERS

Servicemember

Non-Servicemember

Credit or consumer reporting

Debt collection

Mortgage

Credit card

Checking or savings

Vehicle loan or lease

Money transfer or service, virtual currency

Prepaid card

Personal loan

Student loan

Payday loan

Credit repair

Title loan

41%

60%

22%

15%

11%

5%

9%

6%

6%

5%

3%

2%

3%

2%

2%

2%

0.8%

2%

1%

1%

0.4%

0.3%

0.3%

0.2%

0.2%

0.1%

14 CONSUMER FINANCIAL PROTECTION BUREAU

Older Consumers

Consumer Response and the Bureau’s Office of Financial Protection for Older Americans

monitor and analyze complaints from consumers who indicated they were 62 years of age or

older at the time of submission. Consumers provided their age in approximately 128,900

complaints, or 26% of all complaints submitted in 2020. As shown in Figure 6, complaints

submitted by self-identified older consumers were less often about credit or consumer reporting,

debt collection, and student loans, and more often about credit cards, mortgages, and checking

or savings accounts than complaints submitted by consumers not self-identifying as 62 years of

age or older. Section 4 of this report (Complaint Types) analyzes some of these differences.

15 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 6: PERCENTAGE OF COMPLAINTS BY PRODUCT AND AGE GROUP

16

16

Consumers who did not provide their age are excluded from this chart. “Under 62” refers to consumers who self-

identified as under the age of 62. When comparing older consumers to their younger counterparts, the Bureau

limits its analysis to consumers who provided their age when submitting a complaint. Therefore, in these analyses,

the Bureau excludes complaints where the consumer opted not to disclose their age.

Credit or consumer reporting

Credit card

Mortgage

Debt collection

Checking or savings

Money transfer or service, virtual currency

Prepaid card

Vehicle loan or lease

Personal loan

Student loan

Credit repair

Payday loan

Title loan

22%

37%

18%

10%

16%

8%

16%

20%

12%

8%

5%

5%

4%

4%

3%

3%

2%

2%

1%

2%

0.4%

0.4%

0.4%

0.6%

0.3%

0.2%

62 or Older

Under 62

16 CONSUMER FINANCIAL PROTECTION BUREAU

3. Complaint Resolution

The Bureau sent approximately 456,100 complaints to approximately 3,300 companies for

review and response in 2020. The Bureau expects companies to provide complete, accurate, and

timely responses tailored to the issues described in each consumer’s complaint. When a

company cannot take action on a complaint because it was submitted by unauthorized third

parties, was the result of fraud, scams or business identity theft, or the company cannot confirm

a commercial relationship with the consumer, the company can provide an administrative

response that includes a statement or other evidence supporting this response.

Complete responses address the issues raised by the consumer, describe communications with

the consumer, and detail follow-up or planned follow-up actions. Accurate responses are those

where the responses narratives and attachments support the response category selected. Timely

responses are those provided within 15 calendar days of receipt and when a company provides a

final response, if applicable, within 60 calendar days.

Response category options include “Closed with monetary relief,” “Closed with non-monetary

relief,” “Closed with explanation,” “In progress,” and administrative options.

The Bureau defines “monetary relief” as objective, measurable, and verifiable monetary relief to

the consumer as a direct result of the steps that have or will be taken in response to the

complaint. The Bureau defines “non-monetary relief” as other objective and verifiable relief to

the consumer as a direct result of the steps that have or will be taken in response to the

complaint. Examples of non-monetary relief to consumers include; stopping unwanted calls

from debt collectors; correcting account information; correcting inaccurate data provided or

reported in consumers’ credit reports; issuing corrected documents; restoring account access;

and, addressing formerly unmet customer service issues.

“Closed with explanation” indicates that the steps taken by the company in response to the

complaint included an explanation that was tailored to the individual consumer’s complaint. For

example, this category is used if the explanation substantively meets the consumer’s desired

resolution or explains why no further action will be taken. Companies should select “Closed with

explanation” category when specific, verifiable monetary or non-monetary relief was not

provided to the consumer in response to issues raised in the complaint.

Consumer Response analyzes consumer complaints, company responses, and consumer

feedback to assess whether companies are providing accurate, complete, and timely responses.

Companies provided a timely response to approximately 99% of the approximately 456,100

complaints that the Bureau sent to them for response in 2020. Table 1 shows how companies

17 CONSUMER FINANCIAL PROTECTION BUREAU

responded. Section 4 of this report (Complaint Types) provides an analysis of patterns and

trends of company responses for each product and service.

TABLE 1: HOW COMPANIES HAVE RESPONDED TO CONSUMER COMPLAINTS

17

Financial Product

or Service

Closed

with

monetary

relief

Closed

with non-

monetary

relief

Closed with

explanation

Admin

response

Company

reviewing

Company

did not

provide a

timely

response

All

3%

6%

87%

2%

<1%

1%

Credit or consumer

reporting

<1% 5% 91% 3% <1% <1%

Debt collection

<1%

9%

85%

1%

<1%

3%

Credit card

17%

9%

70%

2%

1%

<1%

Mortgage

4%

3%

88%

2%

1%

2%

Checking or

savings

16%

4%

76%

2%

2%

<1%

Money transfer or

service, virtual

currency

9%

6%

80%

3%

<1%

2%

Vehicle loan or

lease

3%

8%

86%

<1%

<1%

2%

Prepaid card

10%

12%

64%

2%

4%

8%

Student loan

2%

9%

84%

<1%

1%

3%

Personal loan

5%

6%

80%

2%

1%

6%

Payday loan

1%

1%

83%

5%

<1%

9%

Credit repair

6%

5%

80%

2%

<1%

6%

Title loan

4%

6%

82%

2%

<1%

5%

17

Percentages throughout this report may not sum to 100% due to rounding. The Bureau expects companies to

provide a response to each complaint within 15 calendar days of the complaint being sent to the company. When a

complaint cannot be closed by the company within 15 calendar days, the company may indicate that work to

respond to the complaint is “In progress” and provide a final closure response within 60 calendar days of the

complaint being sent to the company. Responses provided outside the 15- or 60-day timeframe are considered

“u ntimely.”

18 CONSUMER FINANCIAL PROTECTION BUREAU

4. Complaint Types

Monitoring consumer complaints is one of the Bureau’s primary functions. Complaints provide

insights into problems consumers experience and can serve as an early indicator of issues in the

financial marketplace. Complaint analyses support the Bureau’s work to supervise companies,

enforce federal consumer financial laws, propose rules, and develop tools to empower

consumers to make informed financial decisions.

The Bureau analyzes complaints in several ways to identify trends and possible consumer harm.

For example, the Bureau monitors complaint volume across multiple categories, such as

product, issue, sub-product, sub-issue, company, and company response, among others. The

Bureau analyzes complaint volume across time and by geographic area, as well as by self-

identified characteristics, such as servicemember status and age.

While complaint volume provides important information to the Bureau, it has some limitations.

The Bureau recognizes that complaint data can often be better understood in the context of

other data, such as product or service market size and company share. But providing additional

market context to complaint information requires the Bureau to balance several, sometimes

competing, considerations. For example, a variety of measures may provide useful context (e.g.,

company size, number of accounts, number of transactions, and company market share), but the

availability of this market information varies by financial product and service.

Given these and other considerations, the Bureau has not yet identified a universal approach to

contextualize complaint volume across multiple products, services, and markets for the public

without imposing a significant burden on companies to provide data. From its engagements

with stakeholders, the Bureau is aware that the determination about what data are paired with

complaint information often depends on the question being asked. Nevertheless, because

context is informative, throughout this section the Bureau references market research when it

provides some useful context for complaint information.

While complaint volume and context are important, some of the most valuable information is

found in the narrative text that both consumers and companies provide during the complaint

process. The Bureau analyzes the narrative text consumers provide in their complaints,

frequently augmenting traditional qualitative analysis with automated methods.

18

Similarly, the

Bureau analyzes the text companies provide in their responses to consumers and in the

18

The Bureau uses a variety of tools and approaches to assist staff when reviewing complaints. This i nclu de s

statistical approaches to understanding large volumes of complaints (e.g., topic modeling) and tools to make

complaint data easier to filter, sort, and search (e.g., elastic search-based search application).

19 CONSUMER FINANCIAL PROTECTION BUREAU

documents provided to support their responses. Analyzing text from consumers and companies

provides a more complete understanding of issues and a clearer idea of how companies respond

to those issues.

The following sub-sections provide information and analyses of the types of complaints

consumers submitted to the Bureau in 2020.

19

Each sub-section includes an analysis of

complaints the Bureau received, products consumers complained about, problems they

experienced, and how companies responded.

20

The COVID-19 pandemic has and continues to take a substantial toll on the economy, creating

declines in output and living standards. In March 2020, Congress passed the Coronavirus Aid,

Relief, and Economic Security (CARES) Act that, among other things, provided relief to

consumers who were managing the resulting economic fallout. Even with these efforts to help

the American public, the Bureau continued to receive complaints from consumers about their

experiences during the pandemic. In their complaints, consumers described problems and

issues they experienced as a result of COVID-19. The following sections describe the most

common issues consumers described in their complaints.

Where appropriate, sub-sections include a discussion of how product type and issue selections

differ for older consumers and servicemembers.

21

Figures in this section plot product and issue

selections made by these specialty populations based on a level of confidence.

22

19

Compl ai nt numbers are rounded throughout the report; therefore, numbers and percentages may not sum to sub-

totals or 100%.

20

The Bureau’s online complaint form is dynamic and, therefore, adjusts based on consumer selections. Some issues

are not available for certain sub-products (e.g., the issue unable to get your credit report or credit score is not

available for complaints about other personal consumer reports). A full list of complaint form products, sub-

products, issues, and sub-issues is available at

https://files.consumerfinance.gov/f/documents/201704_cfpb_Consumer_Complaint_Form_Product_and_Issue_

Options.pdf.

21

Supra note 12.

22

Figures in this section display 95% confidence intervals, which estimate the true value for the statistic within the

specialty population. The lines with each mark show the confidence interval, with a shorter line reflecting a

narrower range of likely values and a l onger line reflecting a wider range of likely values.

20 CONSUMER FINANCIAL PROTECTION BUREAU

4.1 Credit or consumer reporting

The Bureau received approximately 319,300 credit or consumer reporting complaints in 2020.

The Bureau sent approximately 292,200 (or 92%) of these complaints to companies for review

and response, found approximately 22,400 (or 7%) to be incomplete, and referred 2% to other

regulatory agencies. As of February 1, 2021, 0.1% of credit or consumer reporting complaints

were pending with the consumer and 0.1% were pending with the Bureau (see Figure 7A,

Routing Outcomes).

Companies responded to approximately 99% of credit or consumer reporting complaints sent to

them for review and response. Companies closed 91% of complaints with an explanation, 5%

with non-monetary relief, and 0.2% with monetary relief. Companies provided an

administrative response for 3% of complaints. As of February 1, 2021, 0.7% of complaints were

pending review by the company. Companies did not provide a timely response for 0.3% of

complaints (see Figure 7B, Company Responses).

FIGURE 7: CREDIT OR CONSUMER REPORTING COMPLAINTS BY OUTCOMES

A. Routing Outcomes B. Company Responses

The remainder of this analysis focuses only on those credit or consumer reporting complaints

for which the company confirmed a commercial relationship with the consumer and responded

with an explanation or relief (i.e., complaints closed with explanation, closed with non-monetary

21 CONSUMER FINANCIAL PROTECTION BUREAU

relief, and closed with monetary relief). In 89% of these complaints, consumers reported first

attempting to resolve their issue with the company before submitting a complaint to the Bureau.

When submitting credit or consumer reporting complaints, consumers specify whether they are

complaining about a credit report or some other personal consumer report (e.g., background

checks, employment screening).

23

In 2020, consumers complained about credit reporting most

frequently (see Figure 8).

FIGURE 8: CREDIT OR CONSUMER REPORTING COMPLAINTS BY TYPE OF REPORT AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Consumers also identify the issue that best describes the problem they experienced. For credit

or consumer reporting complaints, options include: credit monitoring or identity theft

protection services; improper use of report; incorrect information on report; problem with a

credit reporting company’s investigation into an existing problem; problem with fraud alerts

or security freezes; and, unable to get credit report or credit score. The most common issue was

incorrect information on your report (see Figure 9).

Unlike most other products and services, a consumer’s problem with a credit or consumer

report may prompt them to submit multiple complaints about, for example, a data furnisher and

consumer reporting agencies. The complaint form reflects this market feature. When submitting

complaints, consumers identify the company or companies about which they are complaining.

In April 2017, in response to feedback from stakeholders and consumers, the Bureau made

enhancements to improve the user experience when submitting a complaint. Where consumers

had previously had to go through the entire submission process separately for each company

about which they were submitting a complaint, beginning in April 2017 consumers could use

one submission process to submit complaints about up to four companies. The Bureau sends

one complaint to each company the consumer identifies. For example, a consumer may go

through one submission process to submit complaints about the data furnisher and the three

NCRAs.

23

The Bureau publishes an annual list of consumer reporting companies. This list includes the three nationwide

credit reporting companies as well as other companies that focus on certain market areas and consumer segments.

See Consumer Fin. Prot. Bureau, List of Consumer Reporting Companies (Jan. 2020), available at

https://files.consumerfinance.gov/f/documents/cfpb_consumer-reporting-compani es-li st.p df

.

Credit reporting

Other personal consumer report

279,200 (99%)

1,600 (0.6%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

22 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 9: CREDIT OR CONSUMER REPORTING COMPLAINTS BY ISSUES AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Credit or consumer reporting complaint volume increased dramatically in 2020. Companies

responded, on average, to more than 23,400 credit or consumer reporting complaints per

month (compared to a monthly average 11,400 complaints in 2019 and 9,200 complaints in

2018). Complaints about credit reports, rather than other personal consumer reports, had the

greatest change in volume in 2020, increasing 129% from the prior two years’ monthly average

(see Figure 10). Although the increase in credit reporting complaints accelerated around the

time of the COVID-19 national emergency declaration in March 2020, this upward trend

precedes 2020.

Incorrect information on your report

Problem with a company's investigation into an existing issue

Improper use of your report

Unable to get your credit report or credit score

Problem with fraud alerts or security freezes

Credit monitoring or identity theft protection services

191,300 (68%)

66,900 (24%)

1,300 (0.5%)

15,100 (5%)

3,500 (1%)

2,700 (1%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

23 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 10: MONTHLY COMPLAINT VOLUME FOR TYPE(S) OF CREDIT OR CONSUMER REPORTING

COMPLAINTS THAT MAKE UP 80% OF OVERALL PRODUCT VOLUME

24

This substantial increase is concentrated in complaints about inaccurate information and the

three largest Nationwide Credit Reporting Agencies (NCRAs)—Equifax, Experian, and

TransUnion. A significant portion of these complaints are about attempts to address identity-

theft-related issues. Complaints about identity theft take a variety of forms: requests to block

information under Section 605B of the Fair Credit Reporting Act (FCRA); requests for

reinvestigations of inaccurate information resulting from identity theft; and issues arising out of

fraud alerts and security freezes under both the FCRA and state law.

25

Complaints related to the

accuracy and completeness of information on consumers’ reports, and complaints about

problems that a consumer encountered in a previous investigation also increased substantially

(see Figure 11). Complaints about incorrect information increased 147% from the prior two

years’ monthly average, whereas problems with investigation increased 139% from the prior two

years’ monthly average.

24

Throughout Section 4, this report highlights changes in the sub-product types and issues selected by consumers.

This report does not include all options that are available to consumers for selection; rather, it highlights those

making up at least 80% of the complaints in each product category.

25

Fair Credit Reporting Act Section 605B, 15 U.S.C § 1681c-2.

24 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 11: MONTHLY COMPLAINT VOLUME FOR ISSUE(S) OF CREDIT OR CONSUMER REPORTING

COMPLAINTS THAT MAKE UP 80% OF OVERALL PRODUCT VOLUME

It appears that some consumers are working with third parties, specifically credit repair

companies, to submit complaints to the Bureau. The Bureau accepts complaints from authorized

third parties

26

but expects those third parties to disclose their involvement in the complaint

process. The complaint process informs third parties that they may not receive a response,

unless they provide authorization, such as a release form signed and submitted by the primary

consumer.

In past years, the NCRAs typically provided substantive and comparatively detailed responses to

the majority of complaints—including providing details of dispute investigations and outlining

steps taken for consumers that are attempting to address identity theft. This year, however,

NCRAs stopped providing complete and accurate responses in many of these complaints.

27

Frequently the NCRAs mentioned suspected third-party activity in their responses to these

complaints, but did not detail steps taken to authenticate consumers or respond to the subject

26

Supra note 1.

27

Consumer Response analyzes consumer complaints, company responses, and consumer feedback to assess wh e ther

companies are provi ding accurate, complete, and timely responses. Accuracy is whether companies select

appropriate response categories based on their narrative text and complete all appropriate fields. Completeness is

whether companies respond to the issues raised by the consumer, describe communications wi th the consumer, and

detail follow-up or planned follow-up actions. And timeliness is whether companies respond to complaints within 15

calendar days of receipt and provide a final response, if appli cable, within 60 calendar days. In 2020, Consumer

Response identified accuracy and completeness issues in the responses received from the NCRAs.

25 CONSUMER FINANCIAL PROTECTION BUREAU

matter raised in the complaints.

28

In other responses, NCRAs closed complaints by noting that a

dispute would be filed on the consumer’s behalf, but failed to provide any details about the

ultimate determinations they made with respect to the subject matter raised in the complaints.

As part of its ongoing complaint monitoring efforts, Consumer Response asked Equifax,

Experian, and TransUnion to review procedures and processes to ensure that complaints are

closed in accordance with the Bureau’s guidelines.

Section 611e of the Fair Credit Reporting Act directs the Bureau to submit an annual report

regarding complaints submitted about the NCRAs that are related to incomplete or inaccurate

information on the consumers’ credit reports.

29

The Bureau typically fulfills this reporting

requirement by including the relevant information it gathers in the Consumer Response Annual

Report. This year, the Bureau received approximately 246,100 complaints about the three

largest NCRAs (Equifax, Experian, and TransUnion). Due in part to the increase in complaint

volume, the Bureau will issue a separate report later this year to provide a more robust analysis

of these complaints and responses.

The Bureau continues to accept credit reporting complaints about other consumer and credit

reporting agencies, as well as furnishers of information. Although the NCRAs experienced the

largest increase in complaint volume this year, both furnishers and smaller credit reporting

agencies also received a greater volume of consumer and credit reporting complaints in 2020.

The Bureau accepts complaints about a number of different types of consumer reports,

including employment, tenant, check and bank screening, as well as reports for specific

industries (e.g., insurance companies and utilities). These complaints frequently involve

disputes of information on consumers’ reports, including personal information, account details,

and public records. Consumers submit furnishing complaints about a variety of different types

of accounts, including credit cards, vehicle loans, mortgages, student loans, as well as debt

collection accounts. The majority of these complaints involve claims of inaccurate account

information (e.g., the date the account was opened or the balance due) and errors in the

consumers’ payment history. In response to these complaints, companies typically responded by

providing a response that included details of actions they took to address consumers’ claims.

28

The Bureau takes steps to identify third parties who may be misusing the Bureau’s complaint process and, when

appropriate, discontinues processing future complaint submissions from those sources. The Bureau expects

companies to authenticate consumers who submit complaints. When a company is unable to authenticate a third

party, they may use administrative response options and describe the steps they took to attempt to authenticate the

third party. Companies also have the ability to respond directly to consumers while securely providing the Bureau

with a copy of their response to the consumer in lieu of using an administrative response. In 2020, none of the

NCRAs availed themselves of this option.

29

Fair Credit Reporting Act Section 611(e), 15 U.S.C. § 1681i(e).

26 CONSUMER FINANCIAL PROTECTION BUREAU

As discussed more extensively in Section 4.9, the (CARES) Act provided relief for borrowers of

federal loans owned by the U.S. Department of Education (ED), including automatic suspension

of payments. When these relief measures went into effect, some student loan borrowers

reported significant drops in their credit scores as a result of how their student loans were

reported. Many of these complaints were regarding a drop in credit scores triggered by a

furnishing issue that affected a subset of borrowers whose government-owned loans were placed

in an administrative forbearance. For this issue, borrowers reported that their servicer was

incorrectly marking their suspended payments as deferred payments instead of as current as

required by the CARES Act, effectively decreasing their credit scores. These consumers learned

of the drop in their score after receiving an alert from their credit monitoring service. In

response to these complaints, their servicer acknowledged the error and stated it was working

with consumer reporting agencies to ensure the accuracy of the information it reported.

As with student loans, consumers with mortgages reported that their credit score declined after

entering into a forbearance plan. This pattern appears to have happened at a number of

servicers. Several consumers mentioned that they were either put into forbearance agreements

without asking their servicer for assistance, or that their account was reported as impacted by

COVID-19 despite being in good standing.

27 CONSUMER FINANCIAL PROTECTION BUREAU

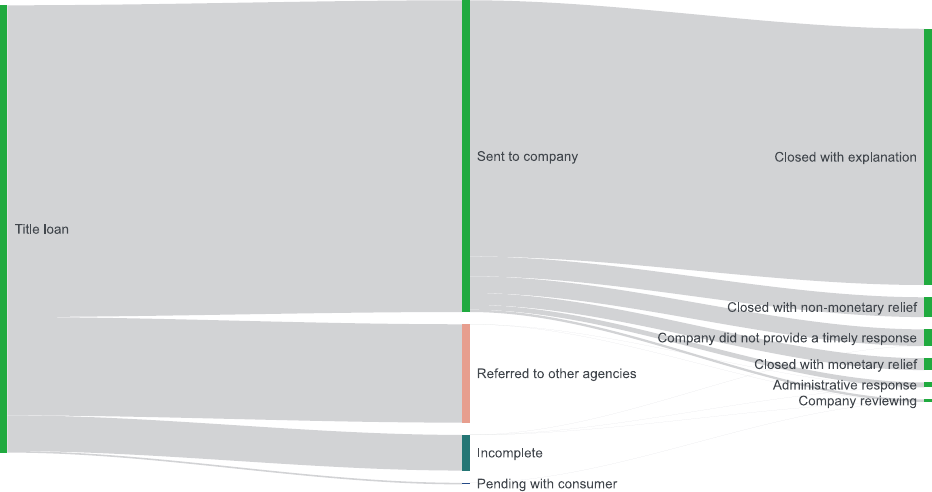

4.2 Debt collection

The Bureau received approximately 82,700 debt collection complaints in 2020. The Bureau sent

approximately 54,700 (or 66%) of these complaints to companies for review and response,

referred approximately 21,500 (or 26%) to other regulatory agencies, and found 8% to be

incomplete. As of February 1, 2021, 0.5% of debt collection complaints were pending with the

consumer and 0.1% were pending with the Bureau (see Figure 12A, Routing Outcomes).

Consumers can submit complaints about creditors collecting their own debts (i.e., first-party

collectors) or companies collecting debt on behalf of others, such as creditors or businesses (i.e.,

third-party collectors).

30

When the Bureau received debt collection complaints about companies

where it was not the primary federal regulator (e.g., a mobile phone or Internet service provider)

or about depository institutions with less than $10 billion in assets, for example, it referred the

complaints to other regulatory agencies (e.g., Federal Trade Commission) or a prudential

regulator.

Companies responded to approximately 97% of debt collection complaints sent to them for

review and response. Companies closed 85% of complaints with an explanation, 9% with non-

monetary relief, and 0.6% with monetary relief. Companies provided an administrative response

for 1% of complaints. As of February 1, 2021, 0.6% of complaints were pending review by the

company. Companies did not provide a timely response for 3% of complaints (see Figure 12B,

Company Responses).

30

See Consumer Fin. Prot. Bureau, Fair Debt Collection Practices Act: CFPB Annual Report 2021 (Mar. 2021) (“[T]he

third-party debt collection market was a $12.7 billion industry that employs nearly 141,000 people across

approximately 6,950 collection agencies in the United States.”) (citations omitted).

28 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 12: DEBT COLLECTION COMPLAINTS BY OUTCOMES

A. Routing Outcomes B. Company Responses

The remainder of this analysis focuses only on those debt collection complaints for which the

company confirmed a commercial relationship with the consumer and responded with an

explanation or relief (i.e., complaints closed with explanation, closed with non-monetary relief,

and closed with monetary relief). In 87% of these complaints, consumers reported first

attempting to resolve their issue with the company before submitting a complaint to the Bureau.

When submitting debt collection complaints, consumers specify the type of debt. Options

include: auto debt, credit card debt, federal student loan debt, medical debt, mortgage debt,

payday loan debt, private student loan debt, other debt (e.g., phone bill, health club

membership, utilities), and debt that is not known.

31

In 2020, other debt and credit card debt

were the most complained about debt types (see Figure 13).

31

The Bureau’s complaint form requires consumers to select the type of debt from a list of options, including “I don’t

know.” See supra note 19.

Debt collection

Pending w ith CFPB

Pending w ith consumer

Incomplete

Ref erred to other agencies

Sent to company

Administrative response

Company did not provide a timely response

Company review ing

Closed w ith monetary relief

monetary relief-Closed w ith non

Closed w ith explanation

29 CONSUMER FINANCIAL PROTECTION BUREAU

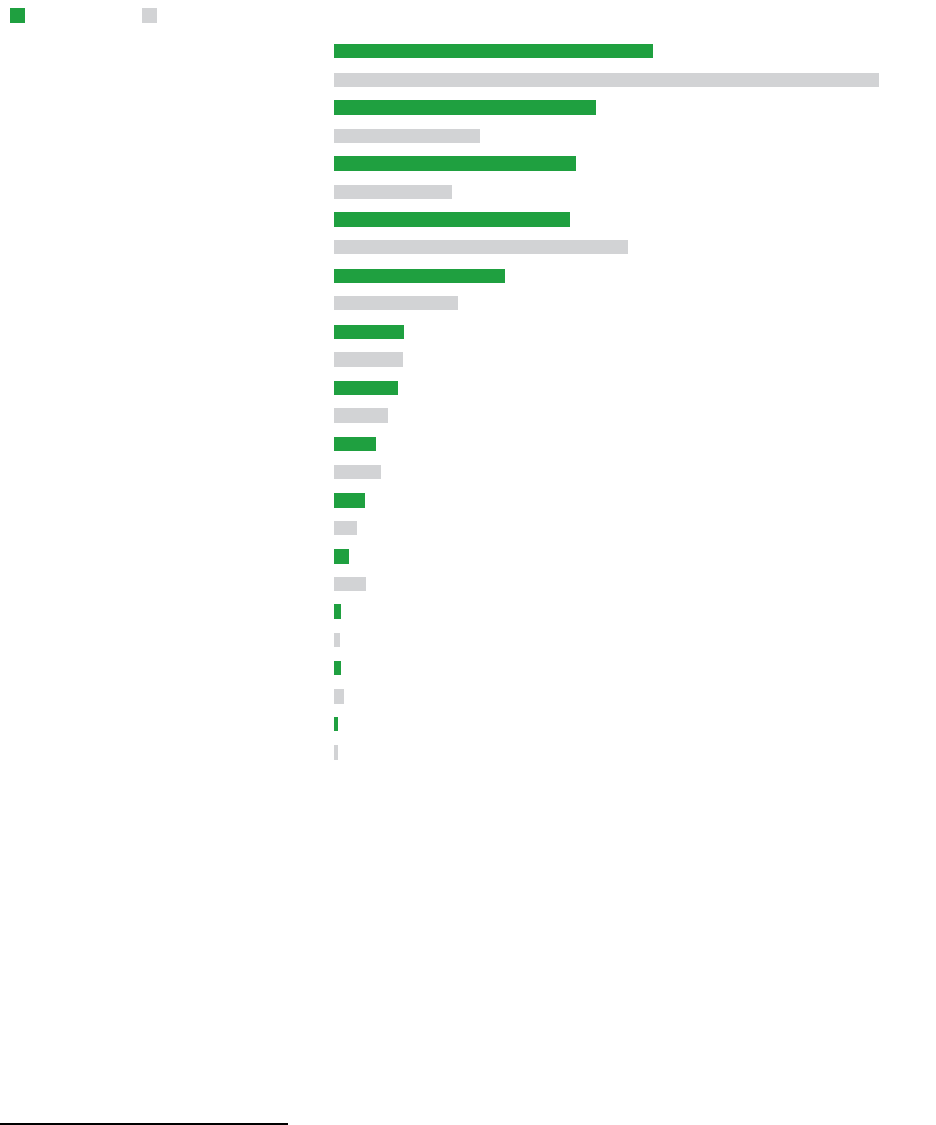

FIGURE 13: DEBT COLLECTION COMPLAINTS BY TYPE OF DEBT AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Consumers also identify the issue that best describes the problem they experienced. For debt

collection complaints, options include: attempts to collect debt not owed; communication

tactics; false statements or representation; threatened to contact someone or share

information improperly; took or threatened to take negative or legal action; and, written

notification about debt. The most common issue was attempts to collect debt not owed (see

Figure 14).

FIGURE 14: DEBT COLLECTION COMPLAINTS BY ISSUES AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Debt collection complaint volume increased in 2020. Companies responded, on average, to

more than 4,300 debt collection complaints per month (compared to a monthly average 3,700

complaints in 2019 and 4,100 complaints in 2018). Among the types of debt consumers

1 square = 1%

Other debt

Credit card debt

I do not know

Medical debt

Auto debt

Payday loan debt

Mortgage debt

Private student loan debt

Federal student loan debt

13,800 (27%)

13,000 (25%)

12,600 (24%)

7,500 (14%)

1,900 (4%)

1,400 (3%)

400 (0.8%)

900 (2%)

500 (1%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

1 square = 1%

Attempts to collect debt not owed

Written notification about debt

False statements or representation

Took or threatened to take negative or legal action

Communication tactics

Threatened to contact someone or share information improperly

27,200 (52%)

12,300 (24%)

4,300 (8%)

3,900 (7%)

3,500 (7%)

800 (2%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

30 CONSUMER FINANCIAL PROTECTION BUREAU

identified in their complaint, credit card debt increased 22% from the prior two years’ monthly

average (see Figure 15). Debt the consumer did not recognize also continued to be a common

debt type, increasing 25% in 2020 from the prior two years’ monthly average.

FIGURE 15: MONTHLY COMPLAINT VOLUME FOR TYPE(S) OF DEBT COLLECTION COMPLAINTS THAT

MAKE UP 80% OF OVERALL PRODUCT VOLUME

The most common debt collection complaint was about attempts to collect a debt that the

consumer reports is not owed. This has been the predominant issue selected by consumers since

the Bureau began accepting debt collection complaints in 2013. In 2020, this issue increased

24% compared to the prior two years’ monthly average (see Figure 16). In these complaints,

consumers described a range of topics, such as being called about debts they do not recognize,

attempts to collect a debt that belongs to someone else, and being in collections for services or

products they did not receive.

31 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 16: MONTHLY COMPLAINT VOLUME FOR ISSUE(S) OF DEBT COLLECTION COMPLAINTS THAT

MAKE UP 80% OF OVERALL PRODUCT VOLUME

Consumers also often reported that a debt in collection was the result of identity theft.

Complaints about debt resulting from identity theft have been increasing for several years. In

these complaints, consumers often reported that they first learn of the existence of the debt after

reviewing their credit reports. Many of these consumers described completing an identity theft

report and contacting the collectors listed on their credit report in an attempt to remove the

debt. In response to these complaints, third-party collectors often provided copies of validation

notices and detailed information about where the debt originated. Some debt collectors

discontinued collection efforts entirely.

Complaints involving written notifications about debt is also a common issue reported by

consumers. The Fair Debt Collection Practices Act (FDCPA) requires collectors within five days

after the initial communication with a consumer, to provide the consumer with a written notice

informing them, among other things, of their right to dispute, unless this information is

contained in the initial communication or the consumer has paid the debt. Most consumers who

complained about written notifications report they have not received enough information to

verify the debt. These consumers often complained of notices being vague or not having

sufficient information to identify the account in question; therefore, in their complaints,

consumers often asked for additional information, including supporting documentation.

Additionally, similar to complaints about identity theft, many consumers reported first learning

32 CONSUMER FINANCIAL PROTECTION BUREAU

of the debt after reviewing their credit report. These consumers often stated that the limited

amount of information furnished on their credit report made it difficult to understand details

about the source of the debt.

In their complaints about collection activities, consumers often expressed difficulty in making

payments or meeting existing agreements because of a loss in income.

There were several examples of tenants who reported vacating, voluntarily or otherwise, their

apartments following the onset of the pandemic. These consumers were later referred to third-

party collections because of outstanding balances or insufficient security deposits. Some of these

consumers reported having entered into modified lease agreements and settling their accounts

prior to departure. In response to these complaints, companies typically provided a detailed

ledger of charges or discontinued collection of the account.

Complaints about communication tactics and threatening to contact someone or sharing

information improperly decreased in 2020. This may be explained, in part, by restrictions on

debt collectors imposed by states. For example, many states imposed temporary restrictions on

debt collection practices in order to protect consumers including prohibiting certain

communications from collectors and banning debt collection altogether.

32

Consumer complaints suggest that ordinary collection practices (e.g., calls to consumers, wage

garnishment, etc.) resumed during the summer months. In complaints about communication

tactics, consumers reported a variety of issues: frequent or repeated calls; ignored requests to

stop calling; and interactions where the collector was rude and aggressive.

In 2020, consumers more frequently described receiving text messages concerning debts that

they purportedly owed. Complaints about this issue, however, remain small in number. In

complaints where consumers describe receiving a text, they often express suspicion of the text or

concern that it is scam. It appears that few third-party collectors are attempting to collect a debt

via text message. Indeed, in the company responses of some of the largest third-party collectors,

collectors stated that they do not use text messages to currently collect debts. For those

collectors that do employ text messaging to collect a debt, some responded to the consumers

complaint stating that they removed the consumers’ number from further collection efforts.

Similar to last year, debt collection was the second-most complained about product by

servicemembers and made up a greater share of complaints for servicemembers than for non-

32

See e.g., FDCPA 2021 Annual Re port, supra note 30 (“Some states instituted pandemic measures that impacted the

debt collection industry and consumers. These measures include prohibitions on new wage garnishments or bank

attachments, and a requirement that consumers be offered the option to defer scheduled payments.”) (citations

omitted).

33 CONSUMER FINANCIAL PROTECTION BUREAU

servicemembers (see Section 2, Figure 5). On average, servicemembers submitted 10% of debt

collection complaints with a greater percentage complaining about debts relating to mortgage

and auto debt (see Figure 17).

FIGURE 17: PROPORTION OF SERVICEMEMBER COMPLAINTS FOR DEBT COLLECTION TYPES

34 CONSUMER FINANCIAL PROTECTION BUREAU

A greater share of complaints about communication tactics and debt collectors taking or

threatening to take negative or legal action were submitted by servicemembers (see Figure 18).

FIGURE 18: PROPORTION OF SERVICEMEMBER COMPLAINTS FOR DEBT COLLECTION ISSUES

35 CONSUMER FINANCIAL PROTECTION BUREAU

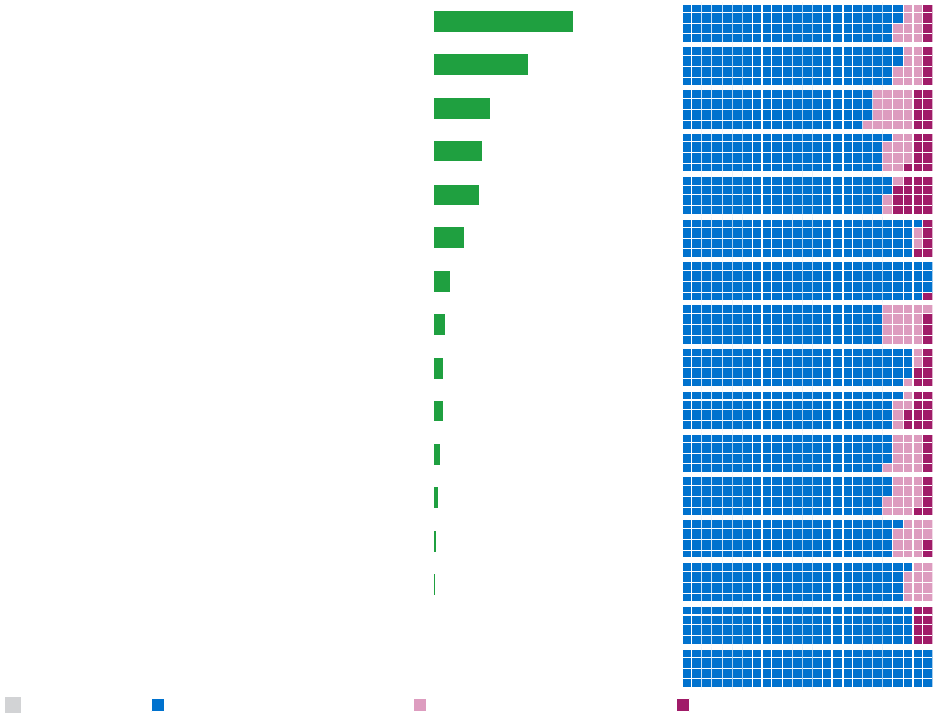

Debt collection comprised a smaller percentage of complaints for older consumers than for

consumers under 62 years old. Within these complaints, a greater percentage of older

consumers complaints about debts related to mortgage and credit cards (see Figure 19).

FIGURE 19: PROPORTION OF OLDER AMERICANS COMPLAINTS FOR DEBT COLLECTION TYPES

36 CONSUMER FINANCIAL PROTECTION BUREAU

Similar to servicemembers, a greater share of complaints about communication tactics were

submitted by older consumers (see Figure 20).

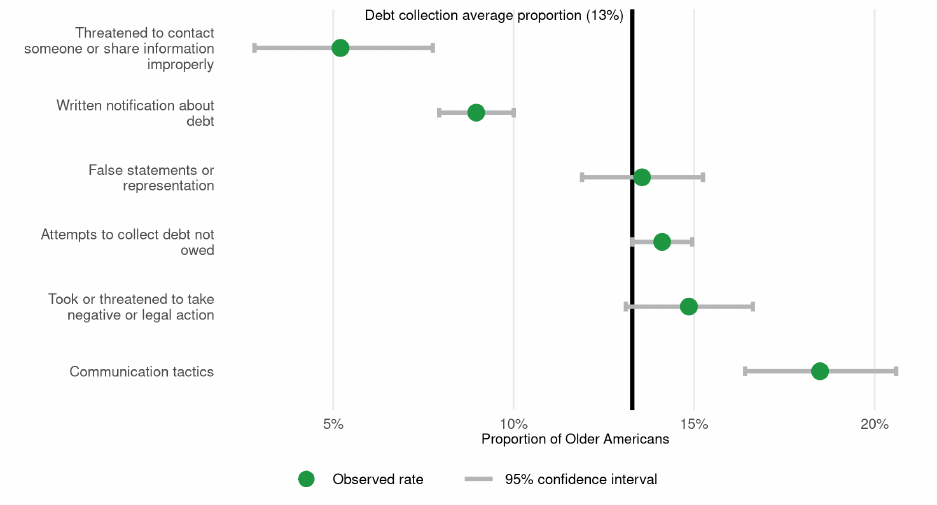

FIGURE 20: PROPORTION OF OLDER AMERICANS COMPLAINTS FOR DEBT COLLECTION ISSUES

37 CONSUMER FINANCIAL PROTECTION BUREAU

4.3 Credit cards

The Bureau received approximately 35,900 credit card complaints in 2020. The Bureau sent

approximately 29,000 (or 81%) of these complaints to companies for review and response,

referred approximately 5,400 (or 15%) to other regulatory agencies, and found 4% to be

incomplete. As of February 1, 2021, 0.2% of credit card complaints were pending with the

consumer and 0.01% were pending with the Bureau (see Figure 21A, Routing Outcomes).

Companies responded to approximately 99% of credit card complaints sent to them for review

and response. Companies closed 70% of complaints with an explanation, 17% with monetary

relief, and 9% with non-monetary relief. Companies provided an administrative response for 2%

of complaints. As of February 1, 2021, 1% of complaints were pending review by the company.

Companies did not provide a timely response for 0.6% of complaints (see Figure 21B, Company

Responses).

FIGURE 21: CREDIT CARD COMPLAINTS BY OUTCOMES

A. Routing Outcomes B. Company Responses

The remainder of this analysis focuses only on those credit card complaints for which the

company confirmed a commercial relationship with the consumer and responded with an

explanation or relief (i.e., complaints closed with explanation, closed with non-monetary relief,

and closed with monetary relief). In 95% of these complaints, consumers reported first

attempting to resolve their issue with the company before submitting a complaint to the Bureau.

38 CONSUMER FINANCIAL PROTECTION BUREAU

When submitting credit card complaints, consumers specify whether they are complaining

about a general-purpose credit card (or charge card) or a store credit card. In 2020, consumers

complained about general-purpose credit cards more frequently than store credit cards (see

Figure 22).

FIGURE 22: CREDIT CARD COMPLAINTS BY TYPE AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Consumers also identify the issue that best describes the problem they experienced. For credit

card complaints, options include: advertising and marketing, including promotional offers;

closing credit card account; fees or interest; getting a credit card; other features, terms, or

problems; problem when making payments; problem with a credit report or credit score;

problem with a purchase shown on a statement; trouble using card; and, struggling to pay bill.

The most common issue was problem with a purchase shown on your statement (see Figure

23).

1 square = 1%

General-purpose credit card or charge card

Store credit card

23,600 (84%)

4,500 (16%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

39 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 23: CREDIT CARD COMPLAINTS BY ISSUES AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

The volume of credit card complaints increased in 2020. Companies responded, on average, to

more than 2,300 credit card complaints per month (compared to a monthly average 1,870

complaints in 2019 and 1,900 complaints in 2018). Complaints about general purpose credit

cards had the greatest change in volume, increasing 24% from the prior two years’ monthly

average (see Figure 24). This increase accelerated around the time of the COVID-19 national

emergency declaration.

1 square = 1%

Problem with a purchase shown on your statement

Other features, terms, or problems

Fees or interest

Problem when making payments

Getting a credit card

Closing your account

Problem with a credit report or credit score

Trouble using your card

Advertising and marketing, including promotional offers

Struggling to pay your bill

8,500 (30%)

3,300 (12%)

3,200 (11%)

2,700 (10%)

2,500 (9%)

2,200 (8%)

2,200 (8%)

1,400 (5%)

1,300 (4%)

800 (3%)

Closed with explanation Closed with monetary relief Closed with non-monetary relief

40 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 24: MONTHLY COMPLAINT VOLUME FOR TYPE(S) OF CREDIT CARD COMPLAINTS THAT MAKE UP

80% OF OVERALL PRODUCT VOLUME

Similar to 2019, consumers who complained about purchases on their statements described card

issuers not resolving disputes. These consumers often raised concerns about refund requests

and purchases resulting from fraud or identity theft. Some consumers reported receiving a

security alert and declining fraudulent transactions, but later receiving a billing statement with

the fraudulent charges still included.

Consumers often reported problems with purchases on their statements (see Figure 25). Many

of these consumers complained about difficulties in obtaining refunds as their travel plans,

sporting events, concerts, and other bookings were cancelled around the time of the COVID-19

national emergency declaration. Both consumers who had their purchases cancelled by service

providers and consumers who proactively cancelled their purchases reported difficulties in

obtaining refunds. Consumers attempting to invoke chargeback rights reported communication

and customer service issues with their card issuers, including not being able to reach

representatives via phone. In response to these complaints, card issuers typically apologized for

long wait times, explaining that they were attempting to adapt to new working conditions.

Additionally, card issuers often directed consumers to work with the merchant to arrange a

refund. In some limited circumstances, some card issuers reversed the charges or credited

consumers’ credit card reward accounts with points and travel vouchers.

41 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 25: MONTHLY COMPLAINT VOLUME FOR TYPE(S) OF CREDIT CARD COMPLAINTS THAT MAKE UP

80% OF OVERALL PRODUCT VOLUME

Some consumers affected by COVID-19 contacted their card issuers to seek alternative

repayment or deferment options, often after experiencing a disruption in income. Some

consumers who took advantage of these options reported that issuers were not implementing

these options as promised (e.g., interest is not being waived as advertised) or expressed

confusion because account statements did not reflect enrollment in these options. In response to

these complaints, companies often explained that they had recently or were in the process of

updating relevant systems to recognize new workout options. Other card issuers assured

consumers that they were enrolled in the deferment program, but monthly statements would

continue to show a balance due. In these complaints, consumers often expressed concern about

potential negative effects on their credit report.

Consumers also described issues with late fees assessed even while enrolled in a deferral

program or after they had contacted their creditor and informed them of a financial hardship. In

response to these complaint types, some companies reimbursed consumers for assessed late fees

42 CONSUMER FINANCIAL PROTECTION BUREAU

and informed them that interest would continue to accrue on their account during the

deferment period.

As consumers responded to the effects of COVID-19, some reported issues with reduced credit

limits. Some consumers stated that when contacting their card issuers regarding the negative

action taken on their account, they were informed that their credit line was decreased or closed

because they had not used enough of the credit line or that the account was closed due to

inactivity.

33

In response to these complaints, companies often stated that the credit card

agreement allows them to investigate consumer credit records and to close an account at any

time, for any reason.

Credit cards were the second-most complained about product by older consumers and made up

a greater share of complaints for older consumers than for their younger counterparts (see

Section 2, Figure 6). Within these complaints, older consumers submitted a greater percentage

complaining about problems with a purchase shown on their statement (see Figure 26). Similar

to 2019, on average, older consumers were less likely to submit complaints related to struggling

to pay their bill and closing their accounts.

34

33

See Consumer Fin. Prot. Bureau, Data Point: The early effects of the COVID-19 pandemic on consumer credit

(Aug. 2020), available at

https://files.consumerfinance.gov/f/documents/cfpb_earl y-effects-covid-19-consumer-

credit_issue-brief.p df.

34

See Federal Reserve Bank of N.Y., Quarterly Report on Household Debt and Credit (Q4 2020) (Feb. 2020),

available at

https://www.newyorkfed.org/medialibrary/interactives/householdcredit/data/xls/HHD_C_Report_2020Q4.xlsx

(credit card users aged 60-69 had the lowest rates of balances transitions to 90 days delinquency in all four quarters

of 2020; credit card users aged 70+ had the second lowest rates).

43 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 26: PROPORTION OF OLDER AMERICANS COMPLAINTS FOR CREDIT CARD ISSUES

44 CONSUMER FINANCIAL PROTECTION BUREAU

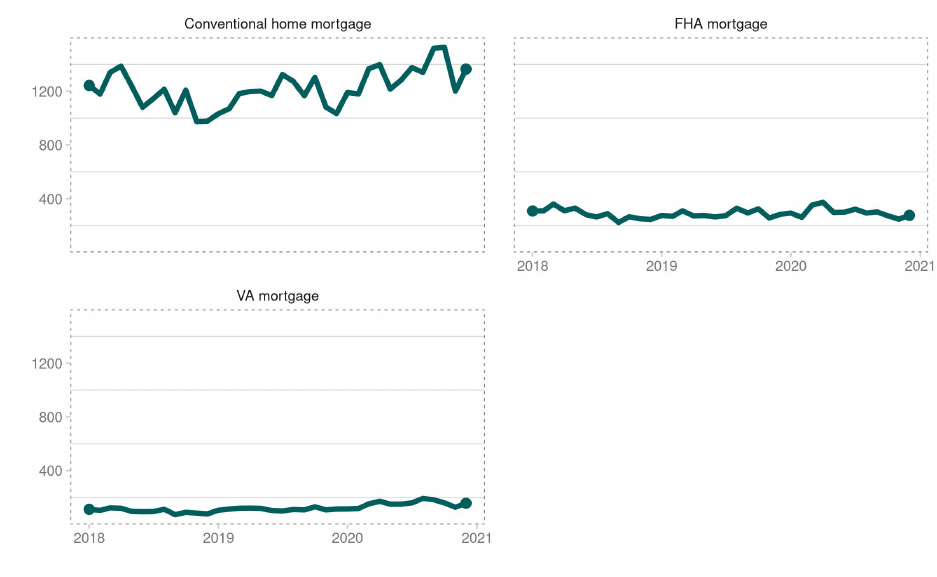

4.4 Checking or savings account

The Bureau received approximately 30,000 checking or savings account complaints in 2020.

The Bureau sent approximately 24,800 (or 82%) of these complaints to companies for review

and response, referred 9% to other regulatory agencies, and found 8% to be incomplete. Of the

9% of checking or savings account complaints referred to other agencies, most were complaints

submitted about credit unions and other depository institutions with less than $10 billion in

assets. As of February 1, 2021, 0.2% of checking or savings account complaints were pending

with the consumer and 0.02% were pending with the Bureau (see Figure 27A, Routing

Outcomes).

Companies responded to approximately 99% of checking or savings account complaints sent to

them for review and response. Companies closed 76% of complaints with an explanation, 16%

with monetary relief, and 4% with non-monetary relief. Companies provided an administrative

response for 2% of complaints. As of February 1, 2021, 2% of complaints were pending review by

the company. Companies did not provide a timely response for 1% of complaints (see Figure

27B, Company Responses).

FIGURE 27: CHECKING OR SAVINGS ACCOUNT COMPLAINTS BY OUTCOMES

A. Routing Outcomes B. Company Responses

The remainder of this analysis focuses only on those checking or savings account complaints for

which the company confirmed a commercial relationship with the consumer and responded

45 CONSUMER FINANCIAL PROTECTION BUREAU

with an explanation or relief (i.e., complaints closed with explanation, closed with non-monetary

relief, and closed with monetary relief). In 94% of these complaints, consumers reported first

attempting to resolve their issue with the company before submitting a complaint to the Bureau.

When submitting checking or savings account complaints, consumers specify the type of

product. Options include; checking account, savings account, certificate of deposit (CD), and

other banking product or service. In 2020, checking account was the most complained about

product type (see Figure 28). Although ownership rates of checking and savings accounts are

similar, it is not surprising that checking accounts are the subject of more complaints as they are

used for everyday transacting—a frequent issue raised by consumers in complaints.

FIGURE 28: CHECKING OR SAVINGS ACCOUNT COMPLAINTS BY TYPE OF PRODUCT OR SERVICE AND

OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses

Consumers also identify the issue that best describes the problem they experienced. For

checking or savings account complaints, options include; closing an account; opening an

account; managing an account; problem caused by funds being low; problem with a lender or

other company charging your account; and, problem with credit report or credit score. The

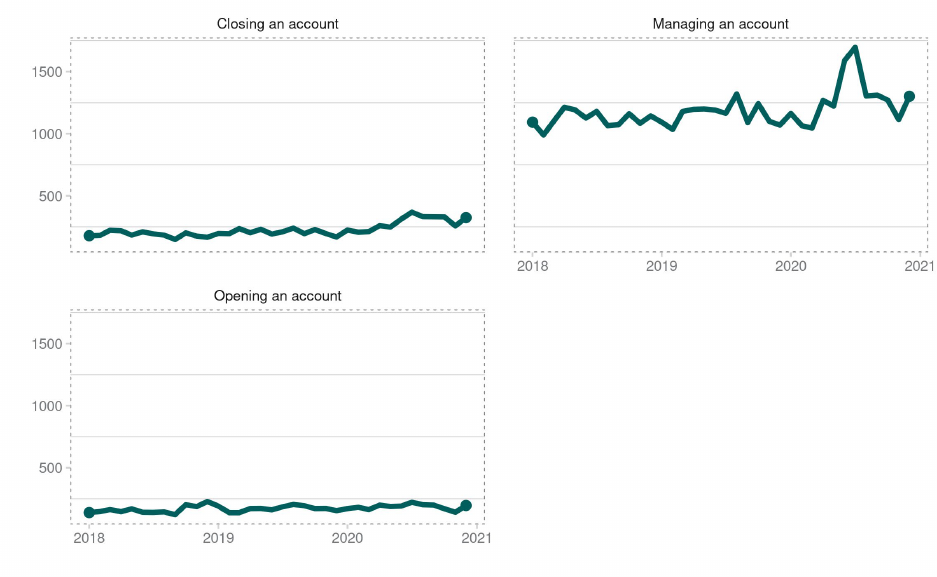

most common issue was managing an account (see Figure 29).

1 square = 1%

Checking account

Other banking product or service

Savings account

CD (Certificate of Deposit)

18,700 (79%)

2,500 (11%)

1,700 (7%)

600 (3%)

Closed with explanation

Closed with monetary relief

Closed with non-monetary relief

46 CONSUMER FINANCIAL PROTECTION BUREAU

FIGURE 29: CHECKING OR SAVINGS ACCOUNT COMPLAINTS BY ISSUES AND OUTCOMES

Complaints closed with explanation or relief in 2020 Company responses