2014 Erie Indemnity Company Annual Report

39679.indd 1 3/16/15 7:59 AM

This year’s cover represents who we are as a company. It features veteran Employees dedicated to ERIE’s

promise of protection and new Employees excited to begin a career in service. They are Employees who

best represent ERIE’s Values in Practice and have been selected by their peers as this year’s VIPs. And

they are Employees who have been giving their above all to celebrate ERIE’s important milestone—

our 90th anniversary. Learn more on page 21.

From Left to Right:

Michael Filipski, Premium Audit - Eileen Polito, Total Rewards - Nick Schneider, Actuarial - Deborah Beck, Commercial Underwriting -

Alicia Aldridge, Service Delivery - Jishnu Sasi, Claims Technology - Maria Carney, Actuarial - Crystal Walters, Personal Lines Underwriting -

Bryan Morphy, Strategic Communications - Vineetha Jaju Babu, Total Rewards - Donna Mushrush, Personal Lines Product Services -

Jae Aoh, Creative Services - Karen Skarupski, Law

39679.indd 2 3/16/15 7:59 AM

39679.indd 3 3/16/15 7:59 AM

As ERIE Employees and Agents,

we are successful because

we are, above all, together in

our drive to always be better.

We are, above all, together in

our

mission to provide the very

best products and services.

And we are, above all, together in

our promise to always be

there for our Customers.

39679.indd 4 3/16/15 7:59 AM

1

Erie Insurance Property

& Casualty Company

Flagship City

Insurance Company

Erie Insurance

Company

Erie Insurance

Company of New York

Management Operation Property/Casualty Insurance Life Insurance

Erie Indemnity Company

Erie Insurance Exchange

(A Reciprocal Exchange)

Denotes ownership

(wholly owned unless otherwise noted)

Denotes attorney-in-fact

relationship to reciprocal exchange

Erie Family Life

Insurance Company

ORGANIZATIONAL STRUCTURE

Erie Indemnity Company (Indemnity) is a publicly held Pennsylvania business corporation that

has been the managing attorney-in-fact for the subscribers (policyholders) at the Erie Insurance

Exchange (Exchange) since 1925. The Exchange is a subscriber-owned Pennsylvania-domiciled

reciprocal insurer that writes property and casualty insurance.

Indemnity’s primary function is to perform certain services for the Exchange relating to

the sales, underwriting and issuance of policies on behalf of the Exchange. This is done in

accordance with a subscriber’s agreement (a limited power of attorney) executed by each

subscriber (policyholder), who appoints Indemnity as their common attorney-in-fact to

transact business on their behalf and manage the affairs at the Exchange.

The property and casualty and life insurance operations are owned by the Exchange, and

Indemnity functions as the management company. Indemnity, the Exchange, and its

subsidiaries and affiliates, operate collectively as the “Erie Insurance Group” (The ERIE

®

).

ERIE INSURANCE GROUP ORGANIZATIONAL CHART

39679.indd 5 3/16/15 7:59 AM

ANNUAL REPORT 2014

SHAREHOLDERS’ LETTER

To our Shareholders:

It’s our 90th anniversary this year. That’s a big deal for any company, especially in today’s

churning business environment. Economic disruptions, rapid-fire innovations in technology

and shifting demographics are presenting challenges like never before. Companies that can

reach this kind of milestone have figured something out. At The ERIE, we have always

stayed true to our mission and have never been intimidated by a changing marketplace or

larger, more visible competitors.

We are the competition.

That’s one of the iconic ERIE mantras that describes how we work. We are the only thing

that stands between good and great, failure and success. We stay focused on our values, our

strategy and our execution. Our success now and into the future depends on how well we

engage our Employees and Agents to uphold our time-honored commitment to do the right

thing and find new and better ways to run a business for our Customers.

This has not changed in over nine decades, and it’s what enables us to keep growing.

Today, The ERIE boasts nearly 5,000 dedicated Employees and almost 2,200 highly

loyal independent agencies across our footprint. In 2014, our property and casualty

business achieved record results, and we expanded into a 12th state. We continue to earn

consecutive honors from J.D. Power and Associates and Ward Group, and we climbed 39

spots on the Fortune 500 list. At the same time, we’re exploring new technology tools like

drones to support underwriting and claims. And among our new products, we introduced a

first-of-its-kind coverage that meets emerging Customer needs in the new sharing economy.

Over the years and through every economic condition imaginable, we continue to thrive

when others fight to survive. That’s because our co-founders, H.O. Hirt and O.G. Crawford,

established a firm foundation and an inspiring legacy of service. In the nine decades since,

generations of dedicated Employees and Agents have remained grounded in that vision,

building upon it in new and inspiring ways all their own.

That’s why the theme for our 90th anniversary is “Above All Together.” It combines

two cherished values: The ERIE Family Spirit of Employees and Agents working together

for the good of our Customers and our forever promise to be Above all in

S

ER

V

I

C

E

SM

.

To me, there’s no better way to describe our 90 years in business.

2

39679.indd 6 3/16/15 7:59 AM

As ERIE Employees and Agents, we are successful because we are, above all, together in our

drive to always be better. We are, above all, together in our mission to provide the very best

products and services. And we are, above all, together in our promise to always be there for

our Customers.

STRONG PERFORMANCE

The ERIE’s consistently strong results are tied to the interdependent relationship H.O. Hirt

created in two organizations working together to succeed—the Erie Insurance Exchange

and Erie Indemnity Company. The Exchange is a reciprocal insurance exchange. Indemnity

is the dedicated management company for the Exchange. Indemnity’s primary source of

revenue is the fee it earns by providing management services to the Exchange.

As a result, Indemnity’s success is directly related to the health and growth of the Exchange.

With direct written premium of over $5.5 billion, 2014 marked our seventh straight year of

premium growth for the Exchange. Direct written premium in the property/casualty lines

grew 8.6 percent, year-over-year. This is well over the 4.6-percent anticipated growth that

researchers at Conning & Co. predicted for the industry in 2014.

Driving overall premium growth was a 4.3-percent increase in total policies in force and

a 4.2-percent increase in average premium per policy. We ended the year with a statutory

combined ratio of 100.6 percent. That’s an uptick from the 97.2 percent we recorded during a

3

Lauren Laws,

Property Adjuster, Hagerstown Claims O ce

39679.indd 7 3/16/15 7:59 AM

relatively calm weather year in 2013. Our retention rate remained solid at 90.3 percent at the

close of 2014—a metric that affirms our Agents’ and Employees’ commitment to do right by

our Customers.

Ensuring that we’re well-capitalized to absorb the ebbs and flows of severe weather and

other catastrophic experiences remains a fundamental strength of the Exchange. Our

exceptional on-the-ground service is backed by a solid balance sheet and a growing

policyholder surplus that exceeded $6.8 billion at year-end.

The Exchange’s 2014 premium performance benefitted Indemnity’s management operations,

generating revenue of $1.4 billion. That’s an increase of more than 8 percent over 2013.

Indemnity finished the year with a net income of $3.18 per diluted Class A share, compared

to $3.08 per diluted Class A share in 2013. The net income increased $5 million, from $163

million in 2013 to $168 million in 2014. This increase was driven by the results of our

management operations.

Indemnity’s financial performance and the strength of our overall balance sheet in 2014

enabled us to return almost $119 million in dividends to Shareholders. Indemnity has paid

steadily increasing dividends since 1933. Additionally, we maintained a share repurchase

program in 2014, repurchasing approximately 276,000 Class A shares at a cost of almost

$20 million.

In December 2014, our Board of Directors agreed to increase Indemnity’s regular quarterly

cash dividend from $0.635 to $0.681 on each Class A share and from $95.25 to $102.15 on

each Class B share. This represents a 7.2-percent increase in payout per share over the prior

dividend rate.

CLEAR PRIORITIES

In 2014, we updated our long-term strategic plan and enrolled our Employees in a deeper

understanding and connection between what they do day-to-day and how it impacts our

Agents, Customers, co-workers and ERIE’s long-term success.

Our strategic focus centers on engaging our Employees, empowering our Agents and

better understanding our Customers. We’re also aimed at supporting future growth and

differentiation by broadening our product portfolio, refreshing our Claims function and

expanding our geographic reach.

Attracting and retaining Employees

The ERIE has long been an esteemed employer with a strong corporate culture. Shifting

demographics and evolving processes and tools are creating high demand for talented

4

39679.indd 8 3/16/15 8:00 AM

Employees. We have a strategic approach to ensure we attract and retain the right skillsets

and values to grow and develop our work force. New Employees, as well as those new to

leadership, go through a robust onboarding experience that shapes them in ERIE’s culture

and business. It also connects them with others in the organization with whom they can

network and share ideas and experiences.

ERIE also maintains a broad array of learning and development opportunities, a recognized

wellness program, and varied communication channels to build and sustain the kind of

trusted environment that leads to Employee satisfaction and engagement.

Our recruiting process is also targeted at bringing in a diversity of talent, with a passion

for service—that’s a given at The ERIE. In 2014, we hired nearly 50 U.S. military veterans.

It’s a means to provide opportunity to those who have served our country, as well as

recognition of the proven assets service men and women often have to effectively solve

problems and lead the way.

Enhancing the Agent experience

ERIE’s business model is built on a strong and

trusted relationship with the independent

Agents who represent us. That goes back as far

as 1927, when our longest running independent

agency signed with The ERIE. The Ralph C.

Mehler Insurance Agency is now led by the

family’s third generation. This kind of loyalty

is not unusual for ERIE, and it’s something we

never take for granted.

Over the last several years, we’ve enhanced the

collaboration with our Agents through a number of Agent task forces that help ensure our

mutual success. These task forces promote increased communication and strategic alignment

between ERIE and the Agents who represent us.

Our Agents face relentless competitive pressures and changing consumer expectations, and

we’re committed to their success in advising and servicing ERIE Customers while attracting

new ones. This year, we spent a great deal of effort enhancing our Agents’ online presence

by developing new mobile-friendly websites hosted on erieinsurance.com. We also continue

to provide expertise to help Agents better leverage rapidly evolving digital and social

media channels.

These improvements strengthen ERIE’s strategic marketing alliance with our Agents, using

our buying power and marketing expertise to advance our Agents’ efforts and allow them

to better compete at the local level.

5

ERIE’s

business model

is built on a

strong and trusted

relationship

with the independent Agents

who represent us.

39679.indd 9 3/16/15 8:00 AM

Furthermore, we’ve improved the sales workflow with Agents. Our online system for

personal lines has evolved to further streamline the process from quote through down

payment and online signature, saving Agents time and effort. Billing-related platforms

and applications are now consolidated with a consistent look and feel and more intuitive

functionality. And we also began to restructure our Agent website, making it easier for

Agents to perform common transactions. These enhancements combine to free up Agents to

be more attentive to their Customers and bring in new business.

Matching product to opportunity

We helped Agents in other ways as well. In 2014, we expanded product offerings by

bringing our industry-leading Rate Lock protection to Maryland and completing the

rollout of ErieSecure Home

®

in North Carolina. We’ve added more customized homeowner’s

protection and even enhanced our personal auto coverage for Customers providing

rideshare services like Lyft and Uber. In our Commercial Division, we rolled out new

restaurant-specific coverages and data breach protection. And the Life Division revamped

its portfolio to offer more competitively priced, consumer-friendly products.

Better serving our Customers

Agents are our valued, front-line connection to the Customer, but the direct customer

experience is, itself, a significant focus of our strategy. In 2014, we launched a

comprehensive upgrade to our Claims capabilities and began exploring emerging

technology tools to more quickly and effectively handle Customer claims.

This forward-thinking mindset is also well represented in ERIE’s state-of-the-art Technical

Learning Center, just completed at year-end. It is an advanced, interactive training

6

Nathan Eades,

IT Intern

39679.indd 10 3/16/15 8:00 AM

destination for our claims adjusters and risk control consultants throughout our territories.

The 52,000-square-foot training center features 14 fully equipped auto bays and a three-

story home. This house is constructed using hundreds of different building materials

so that Claims personnel can learn how to better serve Customers living in homes of all

different styles, periods and values.

With this new facility, Employees experience hands-on training to prepare them for the

complexities of accurate underwriting, claims adjusting and risk control. It also creates

greater consistency and uniformity across our footprint. In an era when nearly every

insurer touts superior service, the Technical Learning Center is a concrete example of

ERIE’s continued investment, action and commitment to be Above all in

S

ER

V

I

C

E

.

Growing inside and out

Expansion has always been an important part of our strategy. We believe if you’re going to

give great service, you have to meet people where they live. In 1953, ERIE opened its first

branch office outside Pennsylvania—in Silver Spring, Maryland, and this year, Kentucky

became our 12th state.

Our strategic entry into the Bluegrass State also serves as a template for future growth.

Specifically, we looked to ERIE’s existing agencies to expand into Kentucky—and not

just those in close proximity. We tapped strong, entrepreneurial agents from throughout

our footprint to import their expertise, service commitment and knowledge of ERIE to a

promising new consumer base. The first Kentucky policy was issued in early November and

by year-end, nearly 40 Agents had committed to representing ERIE in our newest territory.

We’re driving growth within our existing footprint as well, providing resources and

support for our best Agents to grow their business through prudent acquisition. This has

proved to be an efficient way to quickly increase our penetration and market share in

communities where the ERIE name and reputation are already well established. And its

impact is evident in our ability to gain market share in each of our product lines and in

every state in which we do business.

SOUND MANAGEMENT, SUPERIOR SERVICE

Beyond strides in growing our business, in 2014 we continued to receive accolades for our

financial performance and service standard.

From a service perspective, The ERIE was once again recognized by consumer research

firm J.D. Power and Associates. ERIE was highest in customer satisfaction with the Auto

Insurance Purchase Experience in 2014. And for the second year running, ERIE ranked

highest in J.D. Power’s U.S. Small Business Commercial Study. The ERIE also finished

7

39679.indd 11 3/16/15 8:00 AM

among high customer satisfaction groups in

J.D. Power and Associates’ studies of auto

and homeowners insurers and in handling

property claims.

For the seventh straight year—and 17th time

overall—the Ward Group named ERIE to its

Ward’s 50 list of top-performing property and

casualty companies. Erie Family Life Insurance

was also named to this year’s Life/Health list,

marking the second time the life company

was recognized by Ward. Meanwhile, A.M.

Best again affirmed our A+ (Superior) rating

for ERIE’s Property/Casualty Group and the A

(Excellent) rating for Erie Family Life Insurance.

Particularly satisfying was the fact that the

recognition acknowledged so many aspects of our business for both the Exchange and

Indemnity. We were named to the Forbes’ list of America’s 100 Most Trustworthy Financial

Companies. The list is based on data from GMI Ratings, a proprietary ratings provider and

investment advisor.

Indemnity was also named to the Barron’s 500 Index, which collects the most

fundamentally sound and attractively priced stocks from all industries and corners

of the market. Only 6 percent of all publicly traded companies are included on the list.

Our recognition from respected organizations helps Customers, prospects and investors

clearly see what sets The ERIE apart from other insurers. Those external indicators also

provide us with useful benchmarks to track our progress and challenge our performance.

After all, we are the competition.

HONOR THE PAST, SECURE THE FUTURE

The ERIE has always been a company that frames its future upon the bedrock values,

principles and successes of its past. It’s a tribute to the key architect of this company,

H.O. Hirt, who led ERIE for more than half a century. His vision and perseverance have

allowed us to build a company that delivers consistent value to all of our stakeholders—

our Customers and communities, our Agents and Employees, and you, our Shareholders.

8

For the

seventh straight

year–and

17th time overall

–

the Ward Group

named

ERIE

to its

Ward’s 50 list

of top-performing

property and casualty

companies.

39679.indd 12 3/16/15 8:00 AM

Seven years into my tenure, I feel honored to be a part of the ERIE Family as we celebrate

our 90th anniversary. We reached this milestone as a result of our founders’ great vision—

as well as the dedicated leadership of some extraordinary men and women through the past

nine decades. I’m excited to be building on our legacy of service and success, and creating

an even more powerful and productive future.

It’s exhilarating to think about what’s ahead for us. We have the right business model

to weather any economic storm. We have a loyal and engaged agency force, and a rock-

solid balance sheet. Most importantly, we have dedicated and highly knowledgeable

Employees and an engaged and aligned leadership team that will move this company

forward and make it strong for the next 90 years.

That’s our intent, our plan and our commitment. And we’ll make it happen,

above all, together.

Terrence W. Cavanaugh

President and Chief Executive Officer

Sarah Pierce,

Sales Promotions &

Agency Relations

9

TW

C

h

39679.indd 13 3/16/15 8:00 AM

ERIE FOOTPRINTS—1925 TO 2015

Extraordinary People and Pivotal Moments

that Made a Lasting Impression on Erie Insurance

On the heels of the 19th century’s world-changing industrial

revolution, America grew flush with wealth and opportunity.

Rail lines, mass production—and a little something called the

automobile—forever altered a once frontier nation. For young

entrepreneurs with vision and gusto, this was the time to act.

H.O. Hirt and O.G. Crawford were two such men.

Having transformed a failing grocery store into a thriving

business, H.O. Hirt became known in the business community

as a strategic thinker. His friend and partner, O.G. Crawford,

proved himself to be an aggressive and savvy salesman.

Together they were unstoppable. In 1925, they took a big risk.

They quit their jobs at the Pennsylvania Indemnity Exchange

and launched their own kind of insurance company—named

after the city they called home.

H.O. and O.G. founded the Erie Insurance Exchange, a

Policyholder-owned reciprocal exchange, and the Erie

Indemnity Company, a company to manage its operations. In

creating “The ERIE,” the two shaped a company based on an

important principle: Insurance shouldn’t just be for the rich,

but for all the hard-working people around them who had no

way to shelter their families from unpredicted loss and keep

secure what they worked so hard to achieve. In H.O.’s words,

“Insurance is the most important thing a person buys because it protects him against the loss of

everything he has in the world.”

His vision became the founding principle for ERIE—to provide the people of their community

with “as near perfect protection, as near perfect service as is humanly possible, and to do so at the

lowest possible cost.” As we celebrate our 90th anniversary, ERIE remains true to these words.

ERIE Employees and Agents are, as our anniversary theme says, Above All Together in our

united and unshakeable purpose to deliver our promise to be Above all in

S

ER

V

I

C

E

.

Following are some of the extraordinary people and the pivotal moments—from 1925 to 2015—

that helped make The ERIE what it is today.

10

“Insurance is themost important

From top left to right: Patrick Duda, Corporate Marketing Services - Patrick Murphy, Claims Refresh - Sandra Smialek, Customer Service Program

Management - Norma Upperman, Commercial Underwriting - Gretchen Clorley, Corporate Services - Darrell Thorpe, Diversity & Inclusion -

Evonne Hanson (retired), IT Software Development - Lee’a Thigpen, IT Service Management - Naveen Davala, Commercial Lines Technology

39679.indd 14 3/16/15 8:00 AM

11

39679.indd 15 3/16/15 8:00 AM

Eileen Polito,

Total Rewards

12

1926

Salesman of the Year

In 1926, just 40 days shy of its

first anniversary, Erie Insurance

was already about to close its

doors because it needed $67,000 to

comply with a recently legislated

guarantee-fund requirement of

$100,000. But a 90-day extension,

two $25,000 loans from local

banks and a super salesman in

O.G. Crawford saved the company.

O.G. is said to have sold 243 auto

policies in just 30 days! His heroic

efforts remain an inspiration to all

of us working to help ERIE reach

an extraordinary milestone in

2015—5 million policies in force.

1927

The Agent Advantage

The Ralph C. Mehler Insurance Agency was founded

in 1925 in Sharpsville, Pennsylvania. Two years

later, the agency signed on to represent The ERIE.

Mehler remains ERIE’s longest-running independent

agency, now led by the family’s third generation.

This kind of enduring trust comes from a tradition

of collaboration and cooperation between The ERIE

and its independent Agents. It’s represented not only

through strong day-to-day business relationships

but through ERIE’s ongoing Agent task forces and

combined annual meeting. ERIE leaders and Agents

from throughout the footprint gather to talk about

how to improve business operations and make Erie

Insurance a sought-after brand in the marketplace.

Each year, we also gather to celebrate our Agents’

success at Branch Recognition Meetings throughout

our territories.

1927

Above all in

S

ER

V

I

C

E

SM

Samuel P. Black joined Erie

Insurance in 1927 as the

company’s first full-time adjuster

and claims manager and worked

closely with H.O. Hirt to respond

to ERIE’s Customers. H.O. believed

that it was the responsibility

of ERIE adjusters and claims

Employees to be “ambassadors

of good will” even during the

most difficult or inconvenient

times. Sam embodied this. He

installed a phone extension in his

room at the nearby YMCA. He

was 24/7 well before it became

a customer service “strategy.”

This extraordinary attention to

ERIE Customers emphasized the

powerful and enduring ERIE

motto H.O. set out at the start:

“Above all in

S

ER

V

I

C

E

.”

39679.indd 16 3/16/15 8:00 AM

Nettie Johnson,

Mail & Document Services

13

1928

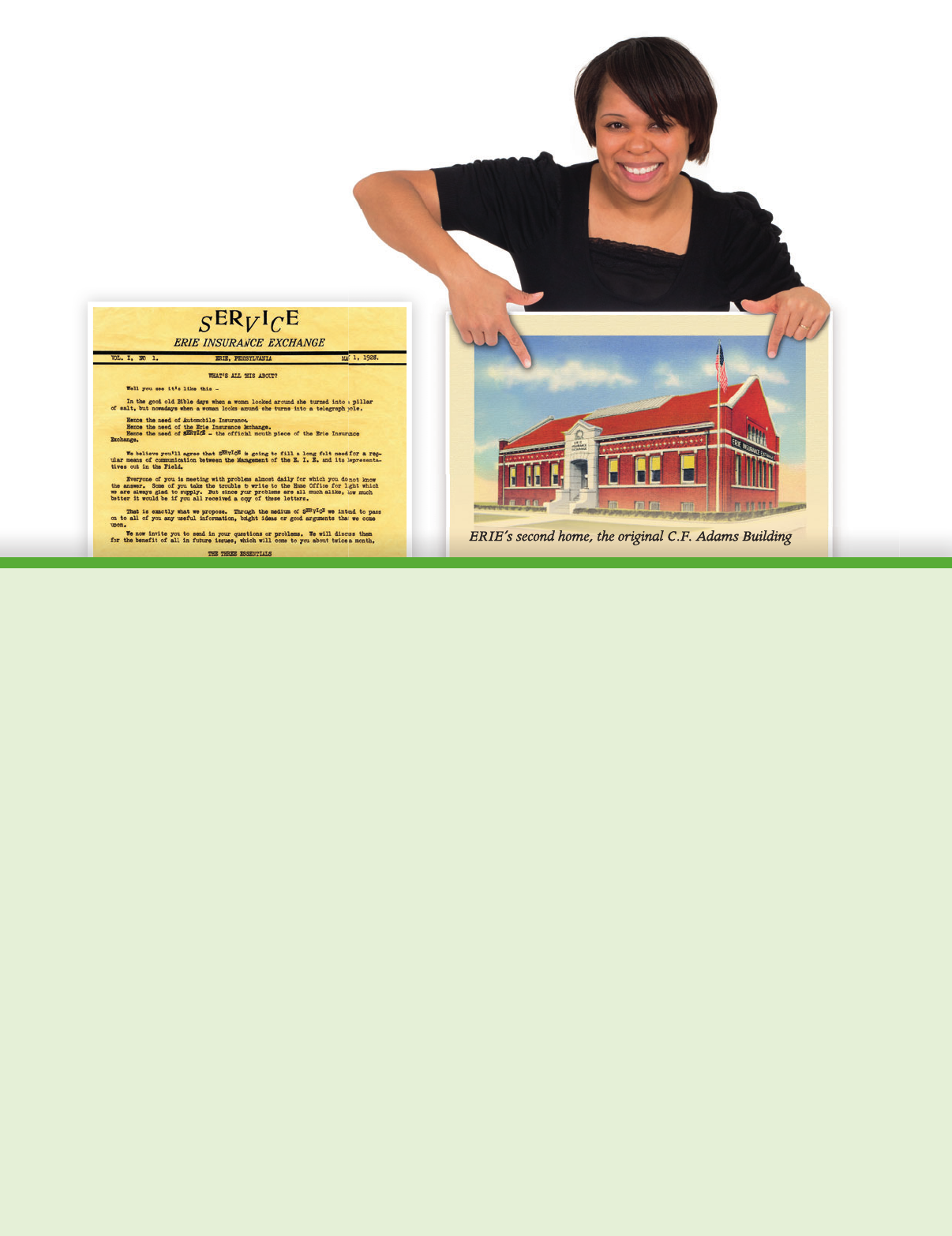

The Write Stuff

H.O. Hirt was prolific, and when he put pen to

paper, his words resonated beyond his corner office.

On May 1, 1928, he published his first newsletter,

called

S

ER

V

I

C

E

, as a way to regularly communicate

with the field and quickly address common business

questions and issues.

S

ER

V

I

C

E

set the stage for the

weekly Bulletin, which started on Aug. 1, 1931. The

Bulletin continues to be published today in the same

purposeful and plain-spoken spirit as H.O.’s first

columns and helps keep both Agents and Employees

close to ERIE’s business strategy.

1934

Super Security

As America recovered from the Great Depression, The ERIE lived up to its promise to provide “as near perfect protection” by

introducing a brand-new Super Standard Auto Policy in 1934. Like its forward-thinking founders, the product and its “Xtra

features” were ahead of its time. Erie Insurance offered much more protection than what people could normally afford and

showed consumers it was a company that cared. ERIE’s Super Standard Auto Policy later became “the standard” auto policy

in the United States. Today, The ERIE continues to develop industry-leading insurance products like ERIE Rate Lock

®

for

more stable insurance premiums and ErieSecure Home

®

with guaranteed replacement costs.

1938

You Can Go Home Again

Nearing its 13th anniversary, ERIE moved its Home Office

from the original office space in the Scott Block Building at

10th and State Streets to the C.F. Adams Building at Sixth

and French. H.O. Hirt described the building, constructed

in 1910, as “magnificent…the most cheerfully daylight place

we have ever worked in.” The company remained there until

the mid-1950s, when it moved across the street into a newly

constructed Georgian colonial-style headquarters. After

decades of service as a center for the developmental needs

of children, the former C.F. Adams Building will return to

active duty as part of ERIE’s campus in 2015, housing the

Erie Insurance Heritage Center.

39679.indd 17 3/16/15 8:00 AM

Tesha NesbitArrington,

Diversity & Inclusion

1940

Fire Starter

Because ERIE started out insuring

automobiles exclusively, ERIE Agents

looked to other companies to meet

their Customers’ non-auto needs. In

1940, The ERIE began closing that

gap, offering fire insurance protection

for homes, followed by casualty

and liability in subsequent years.

Expanding insurance coverages was

a critical business move for The ERIE

through the decades. Today, Erie

Insurance Group is a full-service

insurer offering life, home, auto and

commercial coverage with popular

products such as ErieSecure Home

®

,

Ultraflex

SM

, Ultrapack

SM

, and the

recently released Custom Collection

SM

.

1941

Sharing in Success

H.O. Hirt never forgot that he was

in the relationship business and that

its success depended on satisfied

Employees serving satisfied Customers.

As he once said, “If you give your

Policyholders the proper service that

they have a right to expect, you will grow

and you will prosper.” To that end, H.O.

was again ahead of his time when, in

1941, he led the industry by offering

a profit-sharing bonus to all of his

Employees, not just executives. The

ERIE quickly developed a reputation

for being a great place to work and

became a sought-after place for

employment. Today, ERIE has nearly

5,000 Employees in its footprint from

all over the globe, and continues to

attract prospective hires, with tens

of thousands of unsolicited resumes

received each year.

1945

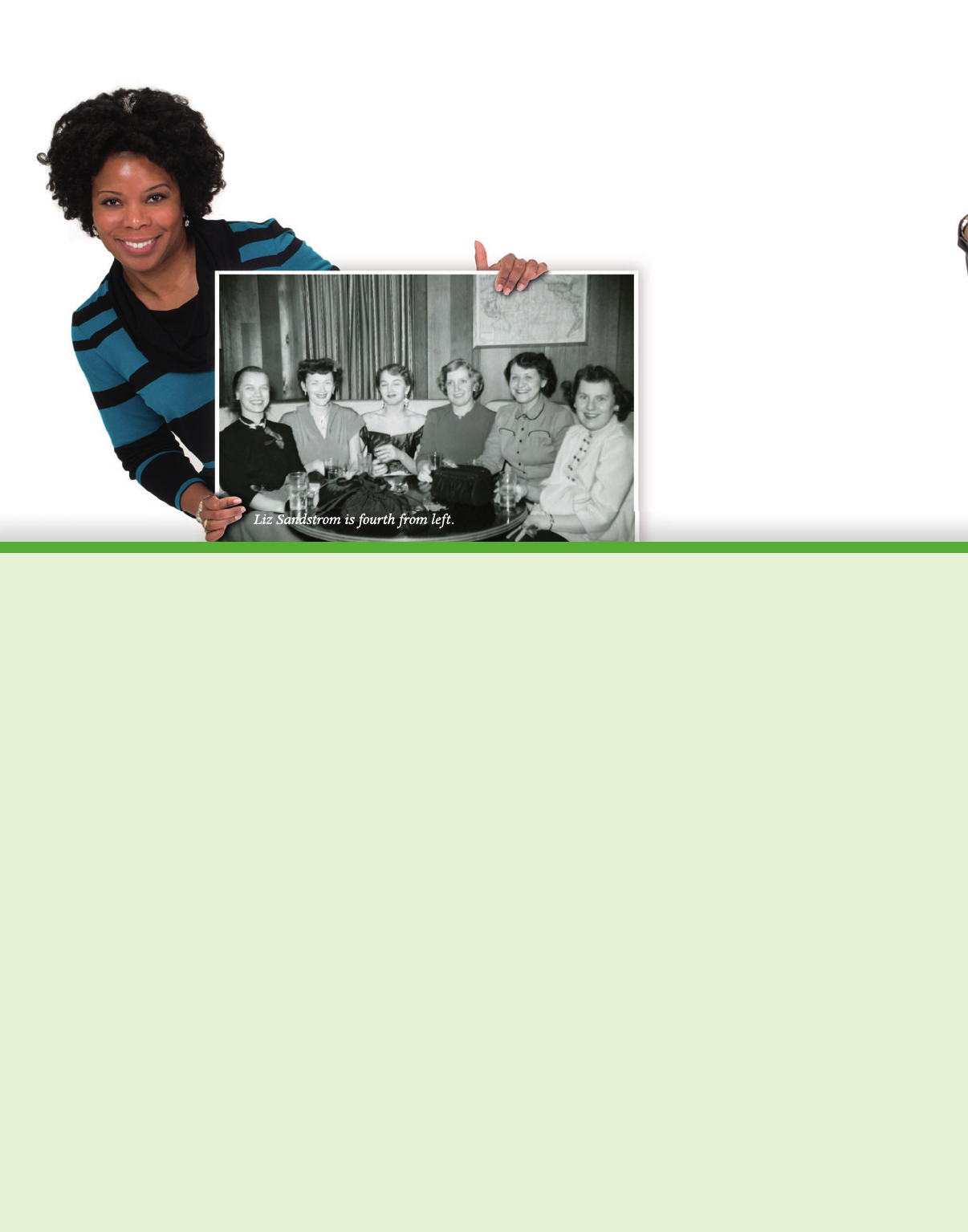

First Lady of Rate

Elizabeth “Liz” Sandstrom was a trail

blazer. Shortly after being hired to

manage the Filing Department in 1945,

Liz’s analytic capability led her up the

corporate ladder where she eventually

headed ERIE’s first Statistics Department

and established consistent practices for the

company. She went on to lead the Statistical

& Pricing Department—the forerunner

of today’s Actuarial Division. Liz became

the first woman in Erie County to earn a

Chartered Property Casualty Underwriter

designation. Her imprint endures not only

in ERIE’s strong actuarial discipline, but

in the organization’s focus on learning and

development for all Employees. In 2014,

Employees completed over 35,000 training

courses, more than 100 Employees obtained

insurance designations and over 100

Employees participated in ERIE’s tuition-

reimbursement program.

1946

A Children’s Story

Following World War II, H.O. became

very interested in the plight of children

orphaned by the war. He began

privately donating to a nationally

established War Orphans Fund, and

wrote numerous columns about the

fund and the status of newly adopted

orphans in The Bulletin, his weekly

newsletter to Agents. In 31 years

following his first donation in 1949,

ERIE Employees and Agents adopted

50 children and donated an average of

$12,000 annually. This set in motion

our deeply-rooted culture of giving and

support for children’s development—

most recently, providing financial

and advisory support to Erie’s public

Pfeiffer-Burleigh School. The ERIE

also reaches communities throughout

its footprint by matching Employees’

generous donations to local and

national charities. Its community

outreach is also embodied in the ERIE

Service Corps, which allows Employees

to devote a full work-day to local

volunteer efforts.

14

39679.indd 18 3/16/15 8:01 AM

Nick Schneider,

Actuarial

1949

Like Father, Like Son

Although he started working for ERIE part time in 1937

when he was just 12 years old, F. W. “Bill” Hirt officially

joined the company in 1949, after serving as a Naval

officer in World War II, finishing college and receiving

an MBA from the Wharton School at the University

of Pennsylvania. He was responsible for bringing The

ERIE into the automation age by converting handwritten

records to the then latest punch-card technology.

During his 41-year career, he held a variety of positions,

including Secretary, Treasurer (CFO) and Executive Vice

President. In 1976, he succeeded his father in leading The

ERIE and went on to become the second longest tenured

CEO in ERIE’s history. Under Bill’s leadership, ERIE’s

premiums increased nearly sevenfold, topping $1.1 billion

at his retirement in 1990. Also, among Bill’s lasting

imprint is ERIE’s first subsidiary, the Erie Family Life

Insurance Company (EFL), which he organized in 1967

and managed. Today, ERIE’s life business is an integral

part of the Erie Insurance Group’s book of business and

our commitment to serving the coverage needs of our

Customers. Bill was active in leadership positions for a

number of charitable and community organizations, and

was a longtime board member of the National Association

of Independent Insurers (NAII), now the Property

Casualty Insurers Association of America (PCI).

1953

Making History

On September 15, 1953, a 17-year-old recent high school

graduate, Tom Hagen, joined The ERIE as a part-time file

clerk just before entering college. He continued to work at

The ERIE throughout college and summers in underwriting

and on special projects. After graduating from The Ohio

State University and serving as an active-duty Naval officer,

Tom became H.O. Hirt’s Assistant to the President in 1960,

serving him for a dozen years. Tom also served as Secretary

to the Board for 20 years, and as the number two executive

(Executive Vice President and then President) for over 14 years.

During that time he founded The ERIE’s first stock property/

casualty subsidiary, Erie Insurance Company, in 1972 and later,

Flagship City Insurance Company in 1992. He followed Bill

Hirt as Chairman of the Board and CEO from 1990 to 1993 and

later, succeeded Bill as non-executive Chairman of the Board,

since 2007. Tom retired from the Navy Reserve as a Captain

and has since served as Pennsylvania Secretary of Commerce

and Secretary of Community & Economic Development.

Tom takes an active role in many business and community

activities, including past Chairman of the Pennsylvania

Chamber of Business and Industry. A student of history like

his father-in-law, H.O. Hirt, Tom has taken an active role in the

revitalization of Erie’s historic neighborhoods and restoration of

some of the city’s treasured homes and public buildings.

15

39679.indd 19 3/16/15 8:01 AM

1953

Spring Forward

In the early 1950s, the post-war boom was bringing in more

business than even H.O. Hirt could have predicted. The ERIE was

growing so quickly that it knew it was time to expand outside of

Pennsylvania. In 1953, ERIE opened its first out-of-state branch

office in Silver Spring, Maryland. The branch, which started in

the living room of founding Branch Manager Frank Yarian, earned

$1 million in premium in just five years. Geographic expansion

has been a key strategy for The ERIE ever since. In addition to

Maryland, ERIE also began writing in Washington, D.C., in 1953 and

then in Virginia in 1955. In the 1960s, The ERIE opened branches in

West Virginia and Ohio, followed by Indiana in 1978 and Tennessee

in 1987. ERIE began selling insurance in North Carolina, New York

and Illinois in the 1990s and then opened a branch in Wisconsin in

2000. In 2014, The ERIE entered its 12th state, Kentucky.

Alicia Aldridge,

Service Delivery

16

1956

The Spirit of America

The post-war boom caught H.O. by

surprise when his original prediction

of a $50,000 per year growth was

actually $50,000 per month between

1945 and 1955. ERIE’s extraordinary

market success resulted in Employees

working elbow to elbow in the

company’s latest office location, the

C.F. Adams Building. So in 1956,

ERIE erected a bold new building

that would symbolize ERIE’s

patriotic spirit and its leader’s respect

for American history. What is now

called the H.O. Hirt Building, was

inspired by our country’s famed

Independence Hall in Philadelphia.

Even as more structures have been

added to the ERIE campus, the

H.O. Hirt Building stands apart as

a reminder of one man’s American

dream—and its cupola remains

a symbol of ERIE’s stability and

uniqueness captured in our logo.

1963

Pioneer Spirit

Not satisfied with its new and generic

homeowners policy, H.O. hired a

one-man product development

department in Don Eagan. Don was

charged with creating a new and

improved homeowners policy that

would be true to the mission of The

ERIE: “To provide our policyholders

with as near perfect protection, as near

perfect service as is humanly possible,

and to do so at the lowest possible

cost.” Eagan first created ERIE’s

popular Pioneer Home Protector

policy and then launched a whole

new commercial sales strategy with

the Pioneer Business Protector policy.

Today, Eagan’s legacy lives on in

ERIE’s thriving commercial business,

which is leading the industry with

innovative new products such as

data breach protection.

39679.indd 20 3/16/15 8:01 AM

Sydney Cassidy,

Financial Planning

& Analysis

17

1977

House Proud

In 1977, The ERIE joined other bayfront area businesses and institutions to form a nonprofit called the Bayfront East Side TaskForce (BEST).

A $7.3 million federal grant to the City of Erie made it possible for The ERIE to expand its footprint and build the F.W. Hirt Perry Square

Building—a major addition to the Home Office campus. The Urban Development Action Grant included restoration of local neighborhoods,

as well as a row of historic townhomes on East Fifth and Holland Streets. ERIE Chairman Tom Hagen has personally been involved in

much local revitalization. He led the restoration of the Charles M. Tibbals House, an 1842 Greek Revival home on ERIE’s campus and the

100-year-old C.F. Adams Building.

1973

Fast Forward

H.O. once wrote in The Bulletin, “From that first day—April 20,

1925—ERIE has never taken a backward step.” He then continued

to write that ERIE “has progressed from a tiny, purely local insurer

of autos only, to a 10-million dollar, four-state insurer of nearly all

lines.” By 1973, Erie Insurance became the largest Pennsylvania-

based auto insurer in the state and today, Erie Insurance

policies are available in 12 states and the District of Columbia.

1980

A Family Affair

Upon H.O.’s retirement in 1980, his daughter, Susan Hirt Hagen,

was named a director of the Erie Indemnity Company. The first

woman to hold that office at The ERIE, Susan is also the longest

serving active ERIE Board Member. H.O’s grandson, Jonathan

Hirt Hagen, joined the board in 2005, today serving as Vice

Chairman. H.O’s eldest grandchild (and Bill Hirt’s daughter)

Elizabeth (Betsy) Hirt Vorsheck also serves on the ERIE board,

having joined in 2007. The ERIE was and continues to be family-

focused, with friends, family and neighbors working side by side

across the footprint. It reflects one of our longstanding values—

the ERIE Family Spirit of Employees and Agents working together

for the good of our Customers.

39679.indd 21 3/16/15 8:01 AM

Jishnu Sassi,

Claims Technology Services

18

1985

First Responders

The ERIE faced a great many weather events since it was

founded, but its commitment to service was truly put

to the test when an F4 tornado hit the town of Albion,

Pennsylvania, on May 31, 1985. ERIE moved in fast and

quickly responded by cleverly spray-painting debris to

deliver messages to policyholders and claimants when

communications were down. Since then, ERIE has developed

a reputation as first responders to catastrophic events that

impact our Customers. More recently, this was, again, evident

in November 2013 when the town of Washington, Illinois,

was hit by a tornado with the same velocity as Albion. In

May 2014, a devastating hail storm enveloped Harrisburg,

Pennsylvania. ERIE quickly responded to thousands of

Customers’ claims in what would be the largest weather-

related auto claims event in ERIE’s history.

1992

Claims to Be the Best

In 1992, The ERIE implemented a new technology called the Claims Management System (CMS). This bold technological

achievement not only improved overall efficiency and helped reduce the need for paper claims, it set in motion ERIE’s focus on

technology as a way to better serve our Customers and help Agents run their business. Today, Claims Refresh, one of our top

strategic initiatives, is enabling the next generation of technology and customer-focused processes to further advance quick and

efficient response to The ERIE‘s Customers and claimants.

1993

Above and Beyond

The late Bob Marrion started at Erie Insurance in 1966

as a claims adjuster and quickly became an inspiration

to his peers for his ability to connect and form lasting

relationships with Customers and claimants. It was not

unusual to see Bob burning the midnight oil to make sure

a Customer’s question was answered or claim was settled.

Bob became a vice president in 1984 and died in 1992.

The following year, Bob’s commitment to ERIE Customers

was immortalized in one of The ERIE’s most prestigious

awards, the Robert H. Marrion Award—setting the

standard for exceptional service. Each year, a Claims

Employee is recognized for delivering a new level of

customer service in each state of our footprint as a way to

celebrate and reinforce The ERIE’s long-standing promise

to be Above all in

S

ER

V

I

C

E

.

39679.indd 22 3/16/15 8:02 AM

Maria Carney,

Actuarial

Donna Mushrush,

Personal Lines Product Services

19

1993

On the Market

The early 1990s were an exciting

time financially for ERIE. In 1993—

nearly 70 years after the Company’s

founding—Erie Indemnity Company

Class A stock became available to

the public. In 1994, Erie Indemnity

registered with the Securities and

Exchange Commission (SEC), and

was listed on the NASDAQ as “ERIE”

a year later. The ERIE has paid a

dividend to its stockholders every

year since 1933, and has repeatedly

earned recognition from A.M. Best,

Fortune and Ward Group for its robust

financial performance.

2000

Many Milestones

The ERIE celebrated its 75th

anniversary as it approached 3 million

policies in force and added Wisconsin

to its footprint with the opening of

the Waukesha Branch. In 2015, The

ERIE marked its 90th anniversary,

and approached another important

milestone: 5 million policies in force.

2001

Power Position

In 2001, ERIE received its first J.D.

Power award, ranking highest in

overall satisfaction for homeowners

insurance in the inaugural J.D. Power

Homeowners Insurance Study. Since

then, The ERIE has received 11 J.D.

Power awards, including highest in

the Collision Repair Satisfaction Study,

highest in Customer Satisfaction

with the Auto Insurance Purchase

Experience and top honors in the

Small Business Commercial Insurance

Study. J.D. Power is just one way

that Erie Insurance is recognized as a

service leader throughout the industry.

39679.indd 23 3/16/15 8:02 AM

2011

Future-Focused Service

Ever since Sam Black installed an ERIE phone

extension in his YMCA room in 1927 to quickly

respond to Customers’ claims, The ERIE has done

whatever it takes to provide reliable and quick

claims response. In 2011, ERIE launched a fleet of

Sprinter

TM

vans to immediately respond to areas

in our footprint hit by natural disaster. With

fully equipped work stations directly connected

to ERIE’s service network, these vans continue

to provide on-the-ground claims service and

emergency supplies such as food and water to

ERIE Customers and other affected residents.

Today, The ERIE is experimenting with the latest

technology, including airborne drones, to more

quickly and effectively handle insurance claims.

Jae Aoh,

Creative Services

2013

The 500 Club

In 2013, The ERIE hit a decade mark on the

Fortune 500 list (and, again, making it in 2014).

The company also earned a seventh consecutive

year on the Ward’s 50 listing and reached a

financial milestone—$5 billion in direct written

premium. In 2014, ERIE’s consistent performance

and transparent operations also earned it a spot

on Forbes magazine’s 50 Most Trustworthy

Companies in America. The ERIE is proud to be

an insurer that, for 90 years, has succeeded in a

competitive marketplace while maintaining the

highest of ethical standards.

2014

Above All in Training

H.O. Hirt once wrote an instruction booklet to help Agents and Employees in the field understand and promote The ERIE’s

way of doing business. The spirit of that noteworthy document—called the “Yellow Book”—lives on in an extraordinary

new building on the ERIE campus called the Technical Learning Center (TLC). Opened in January 2015, it’s a state-of-the-art

training facility for ERIE claims handlers and risk control consultants. The TLC encompasses a three-story house constructed

from hundreds of different building materials and 14 high-tech auto bays. The facility propels ERIE ahead of its competition

with its advanced and comprehensive learning technology. More importantly, it promotes to a new generation of ERIE

Employees and Agents what it means to be Above all in

S

ER

V

I

C

E

.

20

39679.indd 24 3/16/15 8:02 AM

Crystal Walters,

Personal Lines Underwriting

2014

Thinking Ahead

During the early 20th century, IBM CEO

Thomas Watson, Sr., used “Think” as a quick

slogan for his then fledgling technology

company. This simple message resonated

with H.O. who placed a “THINK” plaque

in his office, but added an ERIE twist.

He said, “Thinking—yes, thinking—plus

compassion put The ERIE where it is today.”

Through the following decades, The ERIE has

developed a tradition of thinking creatively

to provide the highest level of service to

our Customers. In 2014, ERIE’s President

and CEO Terry Cavanaugh started a new

digital arena of creative collaboration and

innovation called ThinkAhead: A CEO

Challenge that sparked hundreds of new

process efficiencies and product ideas. That

same year, The ERIE launched a first-of-

its-kind coverage to protect drivers who

participate in online ridesharing services.

2015

Above All Together

The theme for the 90th anniversary—“Above All Together”—combines two cherished values: The ERIE Family Spirit of

Employees and Agents working together for the good of our Customers and our forever promise to be Above all in

S

ER

V

I

C

E

SM

.

Pictured above are ERIE VIPs—Employees selected by their peers as models of our company’s “Values in Practice”—and

dedicated Employees who volunteered to make a memorable 90th anniversary celebration. The anniversary year is being marked

by company-wide festivities, a social media tribute to ERIE Employees, retirees, Agents and community leaders, and the grand

opening of campus additions, including the Erie Insurance Heritage Center. Thoughtfully renovated, it will contain treasured

archives as a way to remember the significant contribution The ERIE has made to the communities it serves and the insurance

industry at large.

21

39679.indd 25 3/16/15 8:02 AM

CORPORATE DIRECTORY

BOARD OF DIRECTORS

J. RALPH BORNEMAN JR.,

CIC, CPIA

1, 5, 7C, 8

President, Chief Executive Officer and

Chairman of the Board, Body-Borneman

Insurance & Financial Services, LLC

TERRENCE W. CAVANAUGH

5, 6, 7

President and Chief Executive Officer,

Erie Insurance Group

JONATHAN HIRT HAGEN, J.D.

2, 3, 4C, 7, 8

Vice Chairman of the Board of

Erie Indemnity Company;

Vice Chairman, Custom Group Industries

SUSAN HIRT HAGEN

1,

4, 5, 8C

Co-Trustee, H.O. Hirt Trusts

THOMAS B. HAGEN

1C,

9

Chairman of the Board, Erie Indemnity Company;

Chairman, Custom Group Industries

C. SCOTT HARTZ, CPA

6, 7

Chief Executive Officer,

TaaSera, Inc. and Hartz Group

CLAUDE C. LILLY III,

Ph.D., CPCU, CLU

2C, 6, 7, 8

President, Presbyterian College

THOMAS W. PALMER, ESQ.

2, 3C, 4, 7

A member of the law firm of Marshall & Melhorn, LLC

MARTIN P. SHEFFIELD, CPCU

1, 2, 7, 8

Owner, Sheffield Consulting, LLC

RICHARD L. STOVER

2, 6C

Managing Principal, Birchmere Capital, L.P.

ELIZABETH HIRT VORSHECK

1, 4, 5C, 7, 8

Co-Trustee, H.O. Hirt Trusts

ROBERT C. WILBURN, Ph.D.

3, 5, 6

President and Chief Executive Officer,

Medal of Honor Museum Foundation;

Principal, Wilburn Group

1

Member of the Executive Committee

2

Member of the Audit Committee

3

Member of the Executive Compensation

and Development Committee

4

Member of the Nominating and

Governance Committee

5

Member of the Charitable Giving Committee

6

Member of the Investment Committee

7

Member of the Strategy Committee

8

Member of the Exchange Relationship Committee

9

Ex-officio non-voting member of Audit Committee

and Executive Compensation and Development

Committee and voting member of all

other committees

C

Denotes Committee Chairperson

22

39679.indd 26 3/16/15 8:03 AM

EXECUTIVE OFFICERS

TERRENCE W.CAVANAUGH

President and Chief Executive Officer

RICHARD F. BURT JR., FCAS, MAAA

Executive Vice President, Products

MARCIA A. DALL,CPA, CPCU

Executive Vice President and

Chief Financial Officer

GEORGE D. “CHIP” DUFALA, CPCU

Executive Vice President, Services

ROBERT C. INGRAM III

Executive Vice President and

Chief Information Officer

JOHN F.KEARNS,FCII

Executive Vice President, Sales and Marketing

SEAN J. McLAUGHLIN,ESQ.

Executive Vice President, Secretary

and General Counsel

SENIOR OFFICERS

JEFFREY W. BRINLING, CPCU

Senior Vice President, Corporate Services

MARC CIPRIANI, CIC

Senior Vice President, Commercial Lines

LOUIS F. COLAIZZO,CIC

Senior Vice President, Sales and Agency

BRADLEY C. EASTWOOD, FCAS, MAAA

Senior Vice President, Actuarial, and Chief Actuary

RUBEN F. FECHNER III

Senior Vice President, Business Applications and Support,

Information Technology

LORIANNE FELTZ, CPCU, CIC,CPIW

Senior Vice President, Customer Service

GREGORY J. GUTTING, CPA

Senior Vice President and Controller

JAYASHREEISHWAR

Senior Vice President, Chief Underwriting Officer -

Commercial Lines

KEITH E. KENNEDY

Senior Vice President, Strategic and

Integrated Services, Information Technology

CHRISTINA M. MARSH, CPA

Senior Vice President, Services

MATTHEW W. MYERS, CPCU, CIC, SCLA, AIC,

AIM, AIS, AAM

Senior Vice President, Claims Refresh Program Sponsor

TIMOTHY G. NECASTRO,CPA, CIC

Senior Vice President and Regional Officer, West Region

RANDALL T.PETERMAN

Senior Vice President, Financial Planning and Analysis,

Investor Relations and Capital Management

MICHAEL A. PLAZONY,FLMI

Senior Vice President, Erie Family Life Insurance Company

BRADLEY G. POSTEMA

Senior Vice President and Chief Investment Officer

SHERRI A.SILVER, CPCU

Senior Vice President, Strategic Marketing

DOUGLAS E. SMITH, FCAS,MAAA

Senior Vice President, Personal Lines

GARY D.VESHECCO,ESQ.

Senior Vice President and Deputy General Counsel, Law

DIONNE WALLACE OAKLEY

Senior Vice President, Human Resources

ANN H.ZAPRAZNY

Senior Vice President and Regional Officer, East Region

CHRISTOPHER J. ZIMMER, CIC,LUTCF

Senior Vice President, Field Claims

23

39679.indd 27 3/16/15 8:03 AM

The F. W. Hirt Quality Agency Award is the highest honor bestowed on an ERIE agency. Itrecognizes

long-term profitability and growth, thorough and responsible underwriting practices, and continuing

commitment to education.

NEW Y

O

RK BRAN

CH

2014 T

h

e R

y

an A

g

enc

y

2012 Qu

i

nton Insurance Protect

i

on Team

2011 Jo

h

n J. Petruzzi Agenc

y

2010

Lon

g

A

g

enc

y

, Inc

.

PITT

S

B

U

R

G

H BRAN

CH

201

4 Bruner Insurance A

g

enc

y

, LL

C

2013 H

all

m

a

n In

su

r

a

n

ce

2012 Hutton-Blews Insurance

,

LL

C

2011 Madia Insurance A

g

enc

y

, Inc

.

2010 Wi

ll

iam S. E

b

er Insurance A

g

enc

y

RALEI

G

H BRAN

CH

2012 Bree

d

en Insurance Services

,

Inc

.

RI

C

HM

O

ND BRAN

CH

2014 Cascade Insurance Grou

p

, LLC

2013 G.L. Hern

d

on Insurance A

g

enc

y

, Inc

.

2010 L

ewis

In

su

r

a

n

ce

A

ssociates

R

O

AN

O

KE BRAN

CH

2013 The Winchester Grou

p

S

ILVER

S

PRIN

G

BRAN

CH

2014 Wa

lk

er Poo

l

e Insurance, Inc

.

2013 Stat

l

an

d

an

d

Katz

,

LT

D

2012 McCabe Insurance Associates

,

Inc

.

2011 Brownin

g

-Rea

g

le Insurance A

g

enc

y

2010 O

ld

e Towne Insurance A

g

enc

y

, Inc

.

WE

S

T VIR

G

INIA BRAN

CH

201

4 Insurance

C

enters

,

Inc

.

2012 H

ott

In

su

r

a

n

ce

a

n

d

Fin

a

n

c

i

a

l S

e

r

v

i

ces

2011 Unite

d

Securit

y

A

g

enc

y

2010 Assure Amer

i

ca Cor

p

orat

i

o

n

WI

SCO

N

S

IN BRAN

C

H

2013 S

p

arks Insurance

A

LLENT

O

WN BRAN

CH

2014 Bo

dy

-Borneman Associates, Inc

.

2013 Kone

ll

Insurance A

g

enc

y

2012 Ro

b

ert S. Mase

y

c

h

i

k

A

g

enc

y

, Inc

.

2011 Paciotti Insurance A

g

enc

y

2010 Ce

ll

ucci-Foran Insurance A

g

enc

y

C

ANT

O

N BRAN

CH

2013 M

i

nor Insurance A

g

enc

y

, LL

C

C

HARL

O

TTE BRAN

CH

2013 Stan

b

err

y

Insurance A

g

enc

y

2010 En

l

oe Insurance A

g

enc

y

, Inc

.

CO

L

U

MB

US

BRAN

CH

2014 Mitchell Insurance A

g

enc

y

, Inc

.

2012 John W. Nei

g

hbar

g

er Insurance A

g

enc

y

, LL

C

ERIE BRAN

CH

201

4 Turner Insurance A

g

enc

y

, Inc

.

2013 B

o

r

t

In

su

r

a

n

ce

S

e

r

vice

2012 Pfeffer Insurance A

g

enc

y

, Inc

.

2011 Milliren-Hoak A

g

enc

y

2010 H

i

stor

i

c Square A

g

enc

y

HARRI

S

B

U

R

G

BRAN

CH

201

4

C

RS Insurance

,

Inc

.

2013 Saleme Insurance Services

,

Inc

.

2012 Michael A. Starr Insurance, Inc

.

2011 Fisc

h

er Insurance A

g

enc

y

2010 S.M. Smit

h

& Compan

y

ILLIN

O

I

S

BRAN

CH

2011 Y

ae

k

e

l

&

A

ssoc

i

ates

In

su

r

a

n

ce

S

e

r

v

i

ces

INDIANA BRAN

CH

2014 A

ld

ri

dg

e Insurance, Inc

.

2013 Reliance Insurance A

g

enc

y

2012 Masters Insurance A

g

enc

y

2011 Mart

i

n Insurance A

g

enc

y

2010 Nic

h

o

l

s Insurance A

g

enc

y

F. W. HIRT QUALITY AGENCY AWARD WINNERS 2010–2014

24

39679.indd 28 3/16/15 8:03 AM

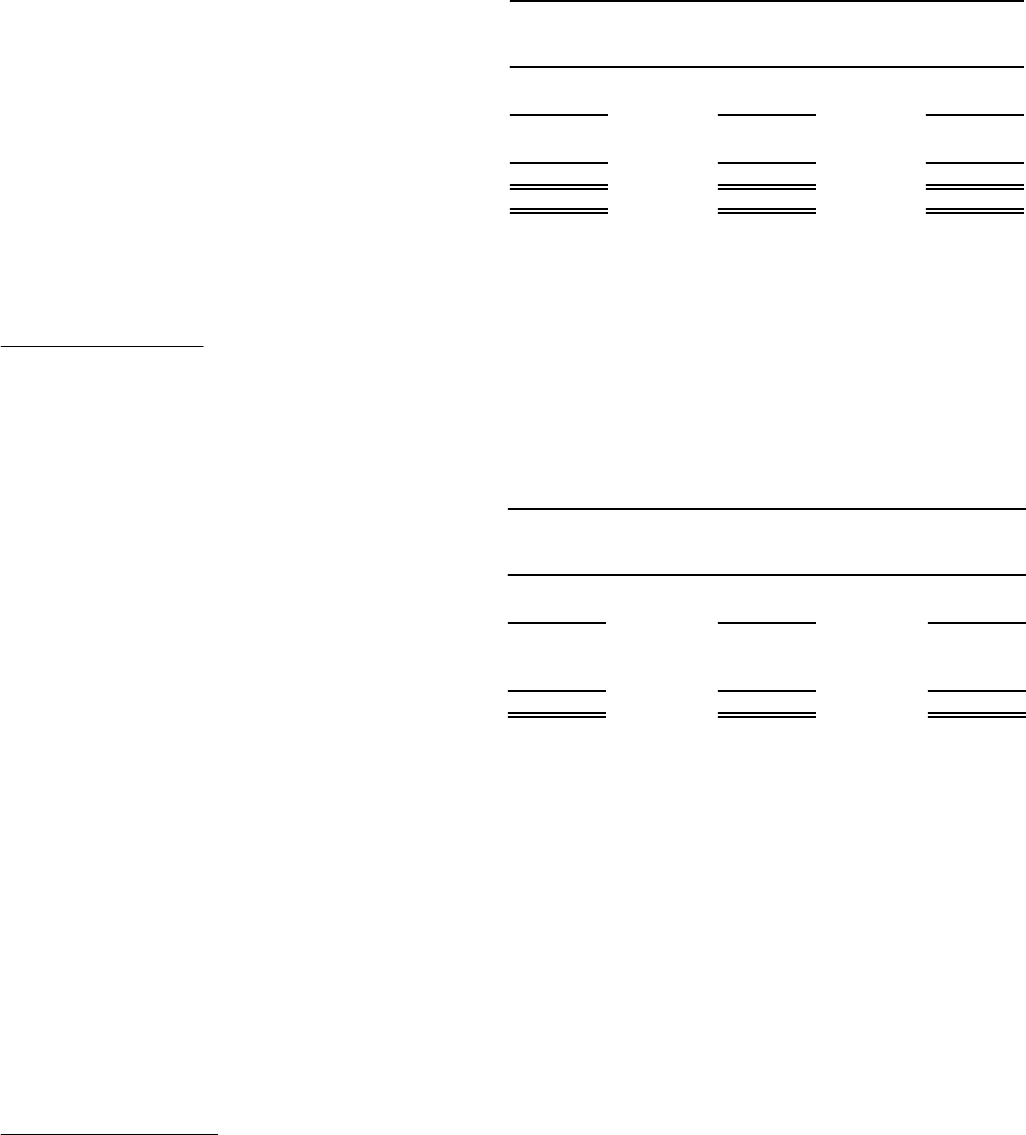

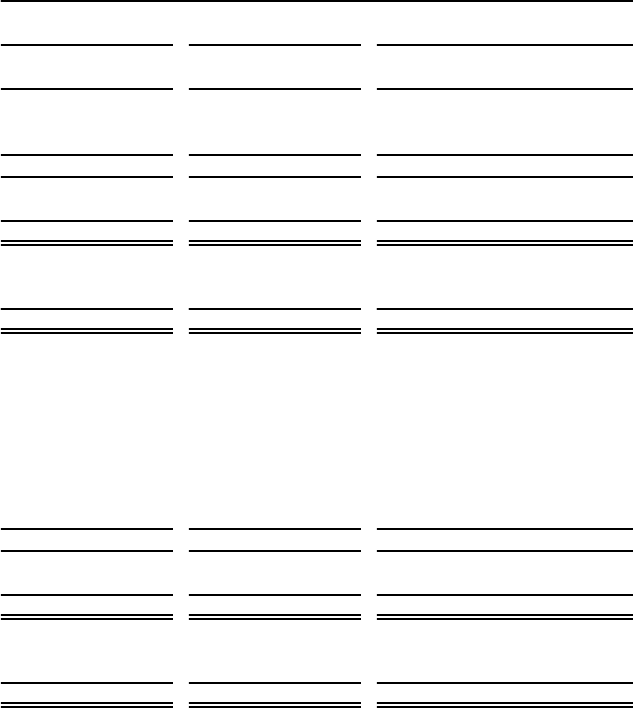

(1) Before income taxes

(2) In addition to the regular quarterly dividend declared in November 2012, Indemnity’s Board of Directors also declared a special one-time cash dividend of

$2.00 on each Class A share and $300.00 on each Class B share.

Net income per Class A share - diluted

Dividends declared per Class A share

(2)

2012

$4.25

2013

$2.4125

2014

$2.586

2013

$3.08

2012

$2.99

2014

$3.18

25

ERIE INDEMNITY COMPANY FINANCIAL HIGHLIGHTS

(dollars in millions, except share data)

PROPERTY & CASUALTY GROUP

Direct written premium $ 4,631 $ 5,076 $ 5,514

Statutory combined ratio 103.8 97.2 100.6

INDEMNITY SHAREHOLDER INTEREST

FINANCIAL OPERATING DATA:

Management fee rate 25% 25% 25%

Revenue from management operations $ 1,188 $ 1,297 $ 1,407

Income from management operations

(1)

205 209 223

Gross margin from management operations 17.3% 16.1% 15.8%

Income from investment operations

(1)

36 38 28

Net income 160 163 168

Return on equity 22.5% 23.6% 23.3%

PER SHARE DATA:

Net income per Class A share - diluted $ 2.99 $ 3.08 $ 3.18

Dividends declared per Class A share

(2)

4.25 2.4125 2.586

Dividends declared per Class B share

(2)

637.50 361.875 387.90

FINANCIAL POSITION DATA:

Total assets $ 1,160 $ 1,213 $ 1,319

Total equity 642 734 703

Weighted average Class A common and equivalent Class B shares

outstanding - diluted 53,547,833 52,855,757 52,616,234

2012 2013 2014

Return on equity

2012

22.5%

2013

23.6%

2014

23.3%

Revenue from management operations

2012

$1,188

2013

$1,297

2014

$1,407

39679.indd 29 3/16/15 8:03 AM

39679.indd 30 3/16/15 8:03 AM

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2014

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 0-24000

ERIE INDEMNITY COMPANY

(Exact name of registrant as specified in its charter)

Pennsylvania 25-0466020

(State or other jurisdiction (I.R.S. Employer

of incorporation or organization) Identification No.)

100 Erie Insurance Place, Erie, Pennsylvania 16530

(Address of principal executive offices) (Zip code)

(814) 870-2000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Class A common stock, stated value $0.0292 per share, listed on the NASDAQ Stock Market, LLC

(Title of each class) (Name of each exchange on which registered)

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes X No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No X

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes X No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data

File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period

that the registrant was required to submit and post such files). Yes X No ___

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be

contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this

Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange

Act. (Check one):

Large Accelerated Filer X Accelerated Filer Non-Accelerated Filer Smaller Reporting Company

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No X

Aggregate market value of voting and non-voting common stock held by non-affiliates as of the last business day of the registrant’s most

recently completed second fiscal quarter: $1.8 billion of Class A non-voting common stock as of June 30, 2014. There is no active market for

the Class B voting common stock. The Class B common stock is closely held by few shareholders.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

46,189,068 shares of Class A common stock and 2,542 shares of Class B common stock outstanding on February 20, 2015.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Part III of this Form 10-K (Items 10, 11, 12, 13, and 14) are incorporated by reference to the information statement on Form 14

(C) to be filed with the Securities and Exchange Commission no later than 120 days after December 31, 2014.

26, 2015

2

INDEX

PART ITEM NUMBER AND CAPTION PAGE

I Item 1. Business 3

Item 1A. Risk Factors 9

Item 1B. Unresolved Staff Comments 19

Item 2. Properties 19

Item 3. Legal Proceedings 19

Item 4. Mine Safety Disclosures 20

II Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases

of Equity Securities

21

Item 6. Selected Consolidated Financial Data 23

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations 24

Item 7A. Quantitative and Qualitative Disclosures About Market Risk 63

Item 8. Financial Statements and Supplementary Data 67

Item 9. Changes In and Disagreements With Accountants on Accounting and Financial Disclosure 123

Item 9A. Controls and Procedures 123

Item 9B. Other Information 123

III Item 10. Directors, Executive Officers and Corporate Governance 125

Item 11. Executive Compensation 126

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

126

Item 13. Certain Relationships and Related Transactions, and Director Independence 126

Item 14. Principal Accountant Fees and Services 126

IV Item 15. Exhibits and Financial Statement Schedules 127

Signatures 128

3

PART I

ITEM 1. BUSINESS

General

Erie Indemnity Company (“Indemnity”) is a publicly held Pennsylvania business corporation that has been the managing

attorney-in-fact for the subscribers (policyholders) at the Erie Insurance Exchange (“Exchange”) since 1925. The Exchange is

a subscriber owned, Pennsylvania-domiciled, reciprocal insurer that writes property and casualty insurance.

Indemnity’s primary function is to perform certain services for the Exchange relating to the sales, underwriting, and issuance of

policies on behalf of the Exchange. This is done in accordance with a subscriber’s agreement (a limited power of attorney)

executed by each subscriber (policyholder), which appoints Indemnity as their common attorney-in-fact to transact business on

their behalf and to manage the affairs of the Exchange. Pursuant to the subscriber’s agreement and for its services as attorney-

in-fact, Indemnity earns a management fee calculated as a percentage of the direct premiums written by the Exchange and the

other members of the Property and Casualty Group (defined below), which are assumed by the Exchange under an

intercompany pooling arrangement.

Indemnity has the power to direct the activities of the Exchange that most significantly impact the Exchange’s economic

performance by acting as the common attorney-in-fact and decision maker for the subscribers (policyholders) at the Exchange.

The Exchange, together with its wholly owned subsidiaries, Erie Insurance Company (“EIC”), Erie Insurance Company of New

York (“ENY”), Erie Insurance Property and Casualty Company (“EPC”), and Flagship City Insurance Company (“Flagship”),

operate as a property and casualty insurer and are collectively referred to as the “Property and Casualty Group”. The Property

and Casualty Group operates in 12 Midwestern, Mid-Atlantic, and Southeastern states and the District of Columbia and writes

primarily private passenger automobile, homeowners, commercial multi-peril, commercial automobile, and workers

compensation lines of insurance.

Erie Family Life Insurance Company (“EFL”), a wholly owned subsidiary of the Exchange, operates as a life insurer that

underwrites and sells individual and group life insurance policies and fixed annuities.

The Property & Casualty Group and EFL began writing private passenger automobile, home insurance, personal excess liability

insurance, and life insurance and annuity products in Kentucky in the fourth quarter of 2014.

All property and casualty and life insurance operations are owned by the Exchange and Indemnity functions solely as the

management company.

The consolidated financial statements of Erie Indemnity Company reflect the results of Indemnity and its variable interest

entity, the Exchange, which we refer to collectively as the “Erie Insurance Group” (“we,” “us,” “our”).

“Indemnity shareholder interest” refers to the interest in Erie Indemnity Company owned by the Class A and Class B

shareholders. “Noncontrolling interest” refers to the interest in the Erie Insurance Exchange held for the subscribers

(policyholders).

Business Segments

We operate our business as four reportable segments – management operations, property and casualty insurance operations, life

insurance operations, and investment operations. Financial information about these segments is set forth in and referenced to

Item 8. “Financial Statements and Supplementary Data - Note 5, Segment Information, of Notes to Consolidated Financial

Statements” contained within this report. Further discussion of financial results by operating segment is provided in and

referenced to Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained

within this report.

Management operations – We generate internal management fee revenue, which accrues to the Indemnity shareholder interest,

as Indemnity provides services to the Exchange relating to the sales, underwriting, and issuance of policies. The Exchange is

the sole customer of our management operations. Indemnity charges the Exchange a management fee, determined by our

Board of Directors, not to exceed 25% of all premiums written or assumed by the Exchange for its services as attorney-in-fact.

Management fee revenue is eliminated upon consolidation.

4

Property and casualty insurance operations – The Property and Casualty Group generates revenue, which accrues to the

noncontrolling interest, by insuring preferred and standard risks, with personal lines comprising 71% of the 2014 direct written

premiums and commercial lines comprising the remaining 29%. The principal personal lines products based upon 2014 direct

written premiums were private passenger automobile (43%) and homeowners (27%). The principal commercial lines products

based upon 2014 direct written premiums were commercial multi-peril (13%), commercial automobile (7%), and workers

compensation (7%).

The members of the Property and Casualty Group pool underwriting results under an intercompany pooling agreement. Under

the pooling agreement, the Exchange retains a 94.5% interest in the net underwriting results of the Property and Casualty

Group, while EIC retains a 5.0% interest, and ENY retains a 0.5% interest.

Historically, due to policy renewal and sales patterns, the Property and Casualty Group’s direct written premiums are greater in

the second and third quarters than in the first and fourth quarters of the calendar year. Property and casualty insurance

premiums earned accounted for approximately 86% of our total consolidated revenue in 2014, 77% in 2013, and 80% in 2012.

The Property and Casualty Group is represented by nearly 2,200 independent agencies comprising over 11,000 licensed

property and casualty representatives, which is our sole distribution channel. In addition to their principal role as salespersons,

the independent agents play a significant role as underwriting and service providers and are fundamental to the Property and

Casualty Group’s success.

The Property and Casualty Group writes business in Illinois, Indiana, Kentucky, Maryland, New York, North Carolina, Ohio,

Pennsylvania, Tennessee, Virginia, West Virginia, Wisconsin, and the District of Columbia. The states of Pennsylvania,

Maryland, Virginia, North Carolina and Ohio made up 74% of the Property and Casualty Group’s direct written premium in

2014.

While sales, underwriting, and policy issuance services are centralized at our home office, the Property and Casualty Group

maintains 25 field offices throughout its operating region to provide claims services to policyholders and marketing support for

the independent agencies that represent us.

The Property and Casualty Group ranked as the 12

th

largest automobile insurer in the United States based upon 2013 direct

premiums written and as the 16

th

largest property and casualty insurer in the United States based upon 2013 total lines net

premiums written according to A.M. Best Company.

Life insurance operations – Our life insurance operations generate revenue from the sale of individual and group life insurance

policies and fixed annuities. These products are offered through our property and casualty insurance agency force to provide an

opportunity to cross-sell both personal and commercial accounts. EFL writes business in 11 states including Illinois, Indiana,

Kentucky, Maryland, North Carolina, Ohio, Pennsylvania, Tennessee, Virginia, West Virginia, Wisconsin, and the District of

Columbia. The state of Pennsylvania made up 46% of EFL’s 2014 premium and annuity considerations, with Maryland,

Virginia, and Ohio making up nearly 10% each.

Investment operations – Our investment operations generate revenue from our fixed maturity, equity security, and limited

partnership investment portfolios to support our underwriting business. The Indemnity and Exchange portfolios are managed

with the objective of maximizing after-tax returns on a risk-adjusted basis, while the EFL portfolio is managed to be closely

aligned to its liabilities and to maintain a sufficient yield to meet profitability targets. We actively evaluate the portfolios for

impairments. We record impairment writedowns on investments in instances where the fair value of the investment is

substantially below cost, and we conclude that the decline in fair value is other-than-temporary, which includes consideration

for intent to sell. Revenues and losses included in investment operations consist of net investment income, net realized gains

and losses, net impairment losses recognized in earnings for our fixed maturity and preferred equity portfolios, and equity in

earnings and losses from our limited partnership investments, which include private equity, mezzanine debt, and real estate

limited partnerships. The volatility inherent in the financial markets has the potential to impact our investment portfolio from

time-to-time. Net revenues from our investment operations accounted for approximately 12% of our total consolidated revenue

in 2014, 21% in 2013, and 18% in 2012.

5

Competition

Property and casualty insurers generally compete on the basis of customer service, price, consumer recognition, coverages

offered, claims handling, financial stability, and geographic coverage. Vigorous competition, particularly in the personal lines

automobile and homeowners lines of business, is provided by large, well-capitalized national companies, some of which have

broad distribution networks of employed or captive agents, by smaller regional insurers, and by large companies who market

and sell personal lines products directly to consumers. In addition, because the insurance products of the Property and Casualty

Group are marketed exclusively through independent insurance agents, the Property and Casualty Group faces competition

within its appointed agencies based upon ease of doing business, product, price, and service relationships.

Market competition bears directly on the price charged for insurance products and services subject to regulatory limitations.

Growth is driven by a company’s ability to provide insurance services and competitive prices while maintaining target profit

margins. Industry capital levels can also significantly affect prices charged for coverage. Growth is a product of a company’s

ability to retain existing customers and to attract new customers, as well as movement in the average premium per policy.