Calculating Pay Plan Reserve Requests

GS 143C-4-9 established the Pay Plan Reserve to assist agencies in funding statutory

and experience-based salary schedule pay expenses on an as-needed basis. Per SL

2023-134, Section 39.19, this job aid details the process that agencies will use to verify

their need from the Pay Plan Reserve to OSBM.

1) Assemble Data on Pay Plan Employees

Agency HR staff must compile the following information for employees subject to the Pay

Plan, and send it to agency budget staff:

• Personnel Number

• Position Number

• Budget Fund

• Salary as of July 1, 2023, after Legislative Increase (LI)

• Salary after Adjustment for Step Increase

• Anniversary Date (e.g., date hired in pay plan position, date sworn-in, etc.)

• Month to Receive Step Increase

2) Determine Total Amount of Step Increase

The value of the step increase is equal to the cost of the pay plan in the current year (FY

2023-24) with positions at their new step minus the cost of pay plan in the current year

(FY2023-24) with positions at their prior step.

Agency budget staff will calculate the total funding required to support all step increases,

including benefits (FICA, retirement, longevity), within a budget fund.

Calculation

Step Increase Amount = Salary and benefits after Adjustment for Step increase –

Salary as of July 1 after LI

3) Determine Salary Needed for Remaining Step Increases

To calculate salary needed for remaining step increases in a fiscal year, run the B0149:

Position by Funding Source report in BEACON/Fiori Business Objects. This report

provides a list of employee salaries ‘as of’ a particular month and year. Subtract these

salaries from the “Salary after Adjustment for Step” to determine the “Estimated Salary

Needed for Remaining Step Increases.”

Calculation

Estimated Salary Needed for Remaining Step Increases = Salaries after Adjustment

for Step – B0149 Employee Salaries

If the calculation yields zero, this employee did not experience a step increase and will

not require additional funds. If the calculation yields a dollar amount, this is the amount

required to support the step increase in the new fiscal year or “Estimated Salary Needed

for Remaining Step Increases.”

4) Determining Available Salary Reserves

Agency staff will also verify the salary reserves within a budget fund, as available

reserves will offset the amount requested from the Pay Plan Reserve.

To determine a budget fund’s available salary reserves, agencies must access the IBIS

Salary Control module. First, select the relevant agency. Second, select the previous

fiscal year. Third, review by budget fund. This will display the balance of salary reserves

as of the end of the previous fiscal year.

Finally, using the same parameters, review salary reserve balances at the time of

analysis to determine current reserve levels.

5) Determine Amount of Salary Reserves Allowed to Retain Non-Pay Plan FTE

within the Same Budget Fund as Pay Plan FTE (if applicable)

If the agency has non-Pay Plan employees in the same budget fund as Pay Plan

employees, it must also calculate the amount of salary reserve to retain for those non-

Pay Plan employees.

To do this, run the B0149: Positions by Funding Source report and export this data to

Excel. Summarize Position Number, Position Title, Sum of FTE, and Sum of Budgeted

Salary in a pivot table.

Use the pivot table to determine the total budgeted salary for non-Pay Plan employees

as well as Pay Plan employees. Calculate what percentage non-Pay Plan employees

are of that total budgeted salary amount.

Lastly, multiply the salary reserves at the start of the fiscal year by that percentage to

determine the amount of salary reserves to retain for non-Pay Plan employees.

Calculations

Total Budgeted Salaries = Salaries of Non-Pay Plan FTE + Salaries of Pay Plan FTE

Percentage Non-Pay Plan Salaries = Salaries of Non-Pay Plan FTE / Total Budgeted

Salaries

Salary Reserve Eligible to Retain = Percentage Non-Pay Plan Salaries x Salary

Reserve at Start of FY

6) Determine Total Amount of Pay Plan Reserve Request

To determine the total amount in the Pay Plan Reserve request, add together the

salary reserves in the budget fund (as of time of analysis) and (if applicable) the amount

to retain for non-Pay Plan employees.

Subtract this total from the Estimated Salary Needed for Remaining Step Increases

to get the Total Salary needed from the Pay Plan Reserve.

Calculate the fringe costs by multiplying the retirement and social security rates by the

Total Salary needed from the Pay Plan Reserve.

S.L. 2023-134 appropriated a non-recurring retirement supplement for FY 2023-24.

Therefore, agencies must use the total retirement rate (R+NR) for year 1 (Column D in

the table below) but only use the recurring retirement rate for year 2 (Column C in the

table below).

Finally, add the total salary amount with the total fringe benefits costs to get the total

amount of the pay plan reserve request.

Calculations

Salary from Pay Plan Reserve = Estimated Salary Needed for Remaining Step

Increases - (Salary Reserve in Budget Fund + Salary Reserve Retained for Non-Pay

Plan FTE)

Social Security = Total Salary Needed from Pay Plan Reserve x 7.65%

Retirement Year 1 = Total Salary from Pay Plan Reserve x Column D

Retirement Recurring Year 2 = Total Salary from Pay Plan Reserve x Column C

Total Pay Plan Reserve Request = Total Salary Needed + Fringe Benefit Cost

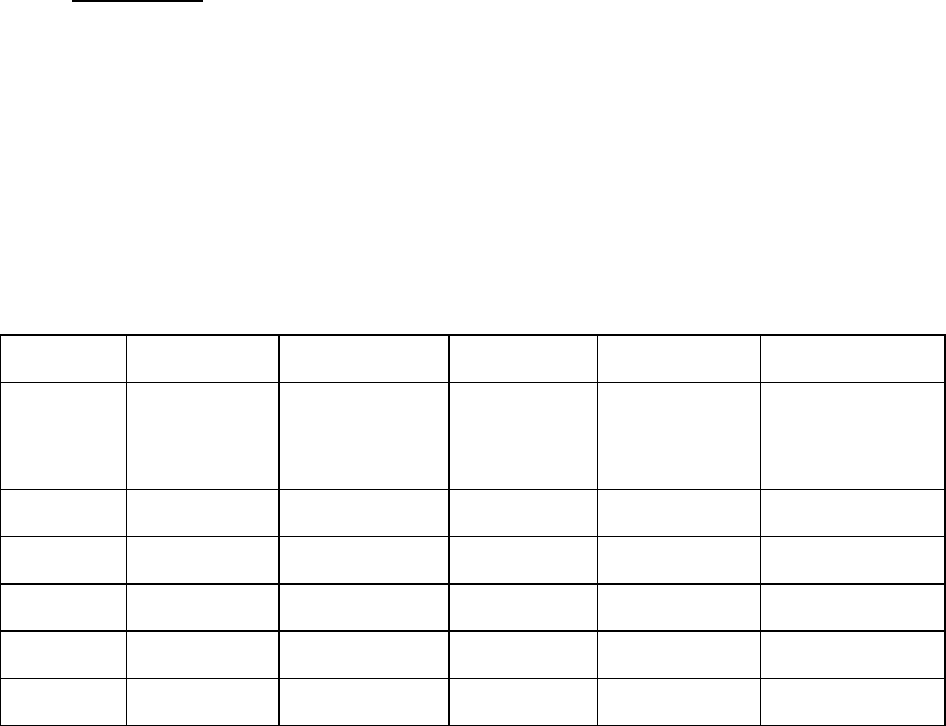

A

B

C

D

E

F

System

FY 2022-23

Recurring

Rate

FY2023-24

Recurring

Rate

FY 2023-24

Total Rate

(R+NR)

FY 2023-24

Recurring

Change

FY 2023-24

Non-recurring

Change

TSERS

22.94%

23.82%

25.02%

0.88%

1.20%

LEO

27.94%

28.82%

30.02%

0.88%

1.20%

CJRS

43.63%

39.98%

42.42%

-3.65%

2.44%

ORP

13.56%

13.96%

14.09%

0.40%

0.13%

LRS

28.67%

25.75%

27.79%

-2.92%

2.04%

Note: Columns E and F are used for calculations, the remaining columns are included for informational

purposes only.

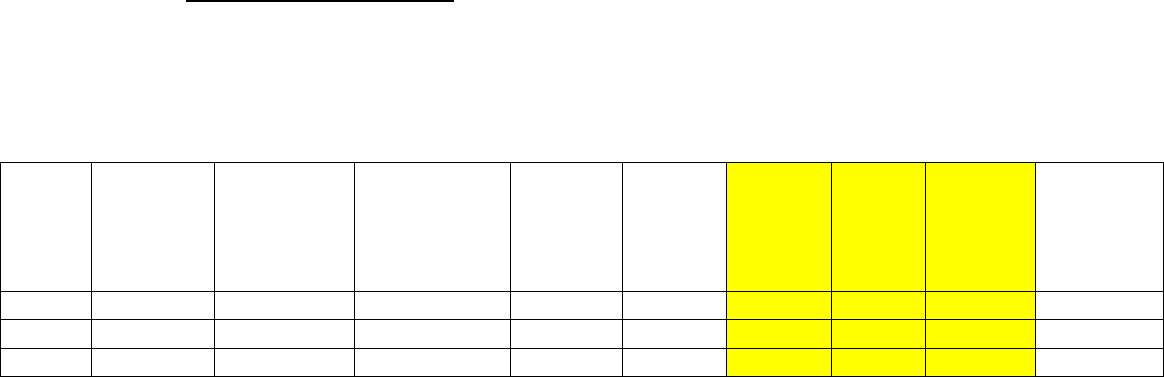

Documentation for OSBM

Agencies should provide appropriate documentation to their OSBM Budget Execution

Analyst with any Pay Plan Reserve request. This includes any relevant data and

calculations, including a summary of the request in the following format.

Budget

Fund

Salary

Reserve as

of

MM/DD/YYYY

Salary Amount

Needed for

Already

Implemented

Step Increases

Salary Reserve

Balance (June 30,

prior SFY)

Salary

Reserve

Retained

for Non-

Pay Plan

FTE (if

applicable)

Estimated

Salary

Needed

for

Remaining

Step

Increases

Salary

from Pay

Plan

Reserve

Social

Security

Retirement

Total Pay

Plan Reserve

Request

1XXXXX $0 $45,374 $45,374 $11,986.00 $81,028 $93,014 $7,116 $22,974 $123,104

1YYYYY ($252,980) $1,547,778 $1,294,798 $0 $357,227 $610,207 $46,681 $150,721 $807,609

1ZZZZZ $63,397 $125,524 $188,921 $73,427.00 $177,701 $187,731 $14,361 $46,370 $248,462