August 2007

This publication was produced for review by the United States Agency for International

Development. It was prepared jointly by the USAID-funded TAPR II Project and the

Ministry of Trade and Industry.

Arab Republic of Egypt

Ministry of Trade & Industry

Trade Agreements & Foreign Trade Sector

The Egypt–Turkey Free Trade

Agreement

Potential Economy-wide Effects

The Egypt–Turkey Free Trade

Agreement

Potential Economy-wide Effects

DISCLAIMER

The authors’ views expressed in this publication do not necessarily reflect the views of the United

States Agency for International Development or the United States Government.

Contents

Executive Summary v

1. Background to the Agreement 1

The Euro–Med Context 1

Other Motivations and Benefits 2

2. Main Provisions of Agreement 5

Main Text 5

Schedules of Concessions 6

Rules of Origin 8

3. Egypt–Turkey Trade and Investment 13

Trade 13

Investment 17

4. Global Analysis Using General Equilibrium Approach 19

Tariff Phase Out 19

Welfare Impacts 20

Trade and Production Impact 21

5. Trade Barriers in Turkey 31

Tariffs 31

Tariff Rate Quotas 31

Import Licences 32

Import Surveillance 35

Export Subsidies 35

Domestic Support 36

Appendix. Trade and Investment Data

II

Illustrations

Figures

Figure 3-1. Egyptian Goods Trade with Turkey, 1996-2006 14

Figure 4-1. Change in Egyptian Imports Relative to 2004 Baseline (US$ Millions) 22

Figure 4-2. Change in Egyptian Exports Relative to 2004 Baseline (US$ millions) 22

Tables

Table 2-1.Tariff Phase-out for Egyptian Imports of Industrial Products from

Turkey, 2007–2020 7

Table 2-2. Tariff Concession Schedule for Turkish Exports of Agricultural and

Processed Agricultural Products into Egypt 7

Table 2-3. Tariff Concession Schedule for Egyptian Exports of Agricultural and

Processed Agricultural Products into Turkey 9

Table 3-1. Trade Balance between Egypt and Turkey, 1996–2006 13

Table 3-2. Top 20 Egyptian Exports to Turkey in 2006 and Turkish

Pre-FTA Tariffs on Egyptian Goods 14

Table 3-3. Turkey’s MFN Tariff Schedule Summary 15

Table 3-4. Top 20 Egyptian Imports and Pre-FTA Tariffs on Turkish Goods, 2006 16

Table 3-5. Egypt’s MFN Tariff Schedule Summary 17

Table 4-1. Egyptian Phase-Out Schedule by Sector, 2007–2020 20

Table 4-2.Turkish Phase-Out Schedule, by Sector, 2007–2008 20

Table 4-3. Welfare Impacts, GDP and Income (in 2004 US$) 21

Table 4-4. Egyptian Textile and Apparel Trade as Percent of Production, 2004 24

Table 4-5. Estimated Impacts on Egyptian Textile and Apparel Production

and Trade 24

Table 4-6. Egyptian Motor Vehicles and Equipment Trade as Percent of

Production, 2004 25

Table 4-7. Estimated Impacts on Egyptian Motor Vehicle and Equipment

Production and Trade 25

Table 4-8. Weighted Average Egyptian Tariffs on Mining and Metal Products 26

Table 4-9. Egyptian Mining and Metals Trade as a Percent of Production, 2004 26

Table 4-10. Estimated Impacts on Mining and Metal Production and Trade 27

Table 4-11. Egyptian Chemical, Wood Products and Other Manufactures

Trade as Percent of Production, 2004 28

Table 4-12. Estimated Impact on Chemical, Wood Product, and Other

Manufactures’ Production and Trade 28

Table 4-13. Estimated Impacts on Egyptian Services Production and Trade 30

Table 5-1. Turkey’s Export Subsidies 35

Table 5-2. Turkey’s Market Price Supports, 2001 36

Acknowledgements

This report was made possible through the Central Department for Bilateral and Multilateral

Agreements (CD/BMA), the Trade Policy Analysis Unit (TPAU), and the USAID-funded

Technical Assistance for Policy Reform project (TAPR II). Research for the report was conducted

at the request of and under the guidance of Mr. Abdel-Rahman Fawzy, head of the Trade

Agreements and Foreign Trade Sector (TAS/FTS) at the Ministry of Trade and Industry, and Mr.

Said Abdallah, head of the CD/BMA.

The TPAU team, consisting of supervisor Abir El Anwar and team members Nermeen El Meligy,

Noha Aly, and Noha Nofal, prepared data for the report, carried out much of the analysis in the

report—including GTAP simulations—and was directly responsible for the discussion of trade in

Chapter 3 and for analysis reported in Chapter 4. Mr. Peter Minor, a TAPR II consultant, oversaw

data collection and analysis, and was directly responsible for Chapter 4 and parts of the Chapter 1.

Ms. Sally Shoala from CD/BMA drafted Chapters 1, 2, and 5, the investment section of Chapter 2,

and provided much of insight into the Egypt–Turkey Free Trade Agreement.

The authors are very grateful to Mr. Emre Oztelli, Commercial Counselor at the Turkish Embassy

in Cairo for up to date information on Turkish investments in Egypt and to Rachid Benjelloun, a

TAPR II international trade specialist, who organized and guided report production.

For further information please contact Peter Minor at pminor@nathaninc.com, the TPAU team at

Executive Summary

The Egypt–Turkey Free Trade Agreement (FTA) came into effect on March 1, 2007. The

agreement covers all goods trade, including products in chapters 1 through 97 of the Harmonized

System. The agreement provides for unlimited market access for only a few agricultural products

(chapters 1–24). Agreement partners have instead offered limited product level access in the form

of tariff rate quotas for selected products and agreed to discuss agricultural trade in the future.

Therefore, the agreement’s primary impact is on nonagricultural products in chapters 25-97, with

the exception of certain processed agricultural goods that appear in those chapters. Services trade

will be discussed in future bilateral meetings, taking into account international developments and

progress in the WTO negotiations.

Turkey is to implement its commitments as soon as the agreement comes into effect. Egypt is

provided 12 years to phase out its tariffs for its most sensitive industrial products, with graduated

and briefer phase-outs for other industrial products.

The impacts of the Egypt-Turkey FTA are expected to be modest, adding about 1/10

th

of one

percent to total economic welfare in Egypt. Trade between the two countries has been expanding

from relatively low levels and can be expected to grow as a result of trade liberalization under this

agreement. Egyptian imports from Turkey are expected to increase as a result of the full

implementation of the trade agreement in 2020 by nearly US$ 500 million in 2004 constant dollar

terms. This would equal a doubling of Egyptian imports from Turkey relative to 2004 trade.

However, the rise in Egyptian imports from Turkey will largely come from a decrease in Egypt’s

imports from other countries, resulting in a net total increase in Egyptian imports of US$ 100

million. The trade diversion effect dominates much of Egypt’s trade impacts resulting from the

FTA. Egyptian exports to Turkey are expected to rise by less than US$ 50 million annually but

will be matched by a similar increase in Egyptian exports to other countries.

When tariffs on motor vehicles are eliminated, the Egyptian sector will only be modestly affected

by an expected rise in Turkish imports. Even so, Turkey’s gain will result primarily from trade

diversion and a movement in Egypt away from motor vehicle imports from the rest of the world.

The more significant effects on the mining, minerals, and metals sector will be mitigated by the

fact that current imports from Turkey are less than 1 percent of Egyptian production. The overall

effect of the FTA on the chemical, wood product, and manufactures sector will be less than one

percent of Egyptian production for these products.

Gains in Egypt’s textiles and apparel imports and exports are expected to be modest—a rise in

domestic production of less than 1 percent when the agreement is fully in force in 2020. Gains in

services trade will be an indirect result of tariff reductions in agricultural and nonagricultural

goods, with construction and transportation and communication experiencing by far the greatest

gains. The FTA’s impact on Egypt’s energy sectors is expected to be negligible.

VI E GYPT– T U R K E Y F TA

Although the FTA will have only modest impacts, it offers opportunities for significant gains in

the future, particularly in agricultural trade. Indeed, current Egyptian tariffs on agricultural imports

from Turkey (6.5 percent on a weighted average basis) are significantly lower than Turkey’s tariffs

on agricultural imports from Egypt (37.1 percent). To ensure that trade benefits are captured,

however, Egyptian operators must be instructed in the agreement’s provisions and the demands

and regulatory requirements of the Turkish market.

The extent to which the agreement will be able to remove nontariff barriers (NTBs) is not clear.

The report outlines some known NTBs in Turkey (pre-FTA) and we will, as the agreement is

implemented, report on whether such NTBs are being reduced and what their effect is on Egyptian

exports. The joint committee set up by the agreement is expected to play a major role in resolving

issues related to NTBs and in ensuring a smooth implementation of FTA rules and provisions.

In the past few years, inward investment has increased substantially as a result of these and other

FTAs signed by Egypt. Though investment in Egypt is still impeded by institutional and other

constraints—regional political instability, bureaucracy, and shortages in skilled labor in certain

sectors—recent policy reforms contributed to a fifteen-fold increase in foreign direct investment

from 2001 to 2006: FDI reached US$9 billion in the first three quarters of Egypt’s 2007 fiscal

year, compared with US$6.1 billion for all of 2006. On July 11, 2007, Egypt became the first Arab

and first African country to sign the Organisation for Economic Co-operation and Development

(OECD) Declaration on International Investment and Multinational Enterprises. With this

promising development, the positive impact of the Egypt–Turkey FTA on investment could easily

surpass its impact on trade.

1. Background to the Agreement

Egypt and Turkey began the first of six rounds of trade negotiations in 1998, signing a final draft

of the Egypt–Turkey Free Trade Agreement on December 27, 2005. The ratified FTA came into

effect on March 1, 2007 in a context governed by the Euro-Med process.

THE EURO–MED CONTEXT

In November 1995, European and Mediterranean countries signed the Barcelona Declaration,

agreeing to establish a free trade area by 2010 and

regional as well as bilateral partnerships on trade,

economic, and security matters. Thus, in 2001, Egypt

and the EU signed the Egypt-EU Association

Agreement, providing each reciprocal market access

in industrial and selected agricultural products; and

Egypt and Turkey recently signed their own FTA. In

addition, trade between the EU and Turkey is

governed by a Customs Union, and Turkey is seeking

to become a full member of the EU.

In part, bilateral trade agreements within the context

of the Euro–Med partnerships, such as that between

Egypt and Turkey, are motivated by Pan-Euro Med

rules of origin that permit three-way or diagonal

cumulation. Most agreements provide for two-way or

bilateral cumulation, which permits the reciprocal use

of inputs from countries party to an agreement.

Diagonal cumulation allows partners to count inputs

of third-parties—countries not party to an

agreement—in meeting the rule of origin. Thus, Egypt

may use inputs from Turkey in its exports to the EU

and still retain market access benefits under the

Egypt–EU Association Agreement. Likewise, Turkey

may use inputs from Egypt and still claim duty free

access to the EU.

In this manner, Pan-Euro Med rules of origin enable a regionwide market that goes beyond simple

bilateral trade flows, leveraging the industrial infrastructure of neighboring countries and others in

the region. To participate in diagonal cumulation with the EU, partners must (1) have concluded an

FTA with the EU and with each other, though the agreements need not be identical; (2) follow

Egypt-Turkey FTA and the Egypt-EU

Association Agreement

Many aspects of the Egypt-Turkey FTA

resemble the Egypt–EU Association

Agreement, with entire sections adopted

from it. Its rules of origin are identical to

those governing each country’s agreements

with the EU (e.g., the ―one list‖ is included),

allowing them both to benefit from Pan-Euro

Med rules of origin. In addition, the tariff

phase period out for Egypt’s nonagricultural

goods is nearly identical to that granted to

Egypt by the EU in recognition of Egypt’s

developing country status. The Association

Agreement specifies four categories of

goods at the product level, delineating a

phase-out period of 3 years, 9 years, 12

years, and 15 years. These schedules have

been largely incorporated, and on a product-

specific basis, into the Egypt-Turkey FTA

with specified years—2008, 2014, 2017, and

2020—to phase out tariffs on the four

categories of goods. (The only differences

between the Egypt-EU and Egypt-Turkey

agreement lists are three HS codes related

to electrical engines and generators, which

were moved from the third to the fourth list.)

2 E GYPT– T U R K E Y F TA

identical rules of origin in the cumulation process; and (3) notify the EU of intent to cumulate with

other free trade partners, and obtain EU approval.

Although these rules of cumulation offer more trade opportunities, seizing these opportunities will

require that Egypt and its partners implement a regional integration strategy. Diagonal cumulation

provisions will provide benefits only to the extent that governments and industry take the final

steps. Egypt and Turkey have significant work ahead to leverage the full advantages of the Pan-

Euro Med rules of origin. These include the following:

Raising producers’ awareness of the advantages and documentation requirements of diagonal

cumulation.

Improving customs cooperation between partner countries.

Reducing nontariff barriers by simplifying standards and testing rules and procedures.

Spreading knowledge of regional materials and sourcing.

Standardizing and automating verification procedures, including certificates of origin.

Enabling local legislation and regulations to encourage investment in new cost-competitive

capacities.

Should Egypt choose not to pursue a regional strategy, industries and governments in neighboring

countries might still very well do so themselves. If so, Egypt’s exports to the EU would face

heightened competition as other preferential suppliers in the Pan-Euro Med area gain from

productivity and specialization efficiencies (costs, services, and quality) and new investments.

Exhibit 1-1. Rules of Origin: The Fine Print of Trade Agreements

Rules of origin are a pivotal part of preferential trade

arrangements and agreements in restricting the use of

inputs used in goods. In apparel trade, for example, EU

rules of origin require double or triple transformation

necessitating the spinning, knitting, weaving, dyeing,

finishing, and making up of garments by the parties to the

agreement. Similarly, to be eligible for preferential

treatment fabrics and yarns must consist of fibers that

originate from the parties to the agreement. Many

exceptions exist, reflecting diverse industrial production

processes. The EU maintains a ―One List‖ of

requirements. Rules of origin are not limited to textiles

and apparel and are often significant in any good with

multiple levels of value added, such as autos or

machinery and equipment manufactures.

Many producers face difficulty meeting rules of origin so

the actual benefits of preferential access vary by country

and product. Egyptian apparel producers interviewed in

2003 indicated that many do not benefit much from

arrangements with the EU because they use cheaper,

higher quality imported yarns and fabrics in their

exported apparel rather than inputs from the EU.

Rules of origin can hinder Egypt’s indirect exports to

the EU. If Turkey wanted to claim preferential access

for its apparel destined for the EU, it would generally be

prohibited from buying Egyptian yarns and fabrics. But

now that Egypt and Turkey implemented the

requirements of the Pan-Euro Med Protocol of Origin,

Egypt’s fabrics and yarns could receive indirect market

access to the EU (assuming Egypt’s products were

competitively priced and met quality standards). And

Turkish fabrics and yarns could be converted to apparel

in Egypt, which would enjoy relief from duties when

they are shipped to the EU.

OTHER MOTIVATIONS AND BENEFITS

In addition to the obligation of the Barcelona Declaration, the Egypt–Turkey FTA was motivated

by a number of factors. The FTA not only provides Egyptian industrial exports with total and

immediate free access to the large Turkish market, but also facilitates access to the EU market.

B A C K G R O U N D T O T H E AG R E E M E N T 3

Egyptian exporters face stiff challenges in accessing that market even with the Egypt–EU

Partnership Agreement. The Egypt–Turkey FTA is expected to help exporters meet the EU’s strict

regulations and standards by integrating Turkish and Egyptian industries and by enabling Egyptian

exporters to benefit from Turkey’s experience in the EU. Just as important, the FTA is expected to

increase confidence in the Egyptian economy and further position it as a hub to other African,

European, and Arab countries. It is expected to generate substantial investments in Egypt and

Turkey, which will help generate additional employment opportunities in the two countries. And

most generally, the heightened competition of freer trade usually boots productivity and improves

standards of living.

In Chapter 2 we summarize the main provisions of the Egypt–Turkey FTA. Chapter 3 describes

trade and investment between Egypt and Turkey. Chapter 4 describes the potential economy-wide

impact of the FTA on Egypt’s economy, covering exports and imports, employment, and overall

welfare, using the GTAP Computable General Equilibrium Model. It also examines the FTA’s

impact on specific sectors. The report concludes by examining trade barriers facing Egyptian

exporters in the Turkish market (Chapter 5).

2. Main Provisions of Agreement

The Egypt–Turkey FTA has four major components: the main text, Protocol I, Protocol II, and

Protocol III. Protocol I relates to the abolition of customs duties and charges having equivalent

effect on imports between Egypt and Turkey. Protocol II relates to the exchange of concessions in

basic agricultural, processed agricultural, and fishery products between Egypt and Turkey.

Protocol III relates to the definition of the ―originating products‖ and methods of administrative

co-operation. The full text of the agreement, including attachments, can be accessed through the

Trade Agreements Sector website (http://www.tas.gov.eg/English/Trade%20Agreements/

Countries%20and%20Regions/Europe/turkey).

MAIN TEXT

The main text of the Agreement consists of 39 articles. Its key provisions include the following:

Articles 4 and 6 abolishes Customs duties and charges having equivalent effect on imports,

and all quantitative restrictions on imports and measures having equivalent effect in

accordance with the provisions of the Agreement, and stipulates that no new measures on

imports may be introduced and that those already applied may not be increased in trade

between the parties.

Articles 7 and 8 abolishes customs duties and charges having equivalent effect on exports, and

all quantitative restrictions on imports and measures having equivalent effect in accordance

with the provisions of the Agreement, and stipulates that no new measures whatsoever on

exports may be introduced, and that those already applied may not be increased in trade

between the parties.

Article 20 lays down the system of Pan-Euro-Med cumulation of origin, which governs the

application of the harmonized preferential rules of origin between the two countries.

Article 23 governs the rights and obligations of the parties with respect to subsidies to be

administered by Articles VI and XVI of the GATT 1994, the WTO Agreement on Subsidies

and Countervailing Measures, and the WTO Agreement on Agriculture.

Article 28 outlines means of promoting investment and technology flows between the two

countries to achieve economic growth and development.

Article 29 establishes a framework for achieving gradual liberalization in trade in services in

accordance with the provisions of the WTO General Agreement on Trade in Services (GATS).

Articles that outline preventive and defensive measures include the following:

Article 14 allows Egypt to take exceptional measures to protect infant industries or sectors that

face difficulties in the form of increased customs duties. In this case Customs duties applicable

on imports from Turkey into Egypt may not exceed 25 percent ad valorem and must maintain

an element of preference for products originating in Turkey. The total value of imports of

6 E GYPT– T U R K E Y F TA

products subject to these measures may not exceed 20 percent of total imports of industrial

products from Turkey, as defined in Article 3, during the last year for which statistics are

available. These measures can be applied for a period not exceeding five years.

Articles 15 and 16 allow parties to take measures against dumping or to apply safeguard

measures in accordance with WTO Agreements.

Article 17 allows both parties to take measures in case of serious shortage in an essential

product to the exporting country that leads to serious difficulties.

Article 19 allows either party to take measures in case of balance of payments difficulties in

accordance with relevant WTO and IMF articles.

Through Articles 30 and 31, the FTA establishes an Egyptian–Turkish Joint Committee with

representatives to administer the FTA, resolving problems arising during implementation and

discussing the possibility of further concessions.

SCHEDULES OF CONCESSIONS

Protocols I and II attached to the main text provide the schedules of concessions. Protocol I covers

the abolition of customs duties and charges having equivalent effect on imports between Egypt and

Turkey; Protocol II covers the exchange of concessions in basic agricultural, processed

agricultural, and fishery products.

Industrial Products

Industrial products (HS 25 to HS 97) are treated in accordance with Protocol I. One part covers

Egypt’s exports to Turkey and the other covers Egypt’s imports from Turkey. Industrial products

originating in Egypt shall enjoy an immediate removal of all customs duties and other charges

having equivalent effect, when the FTA enters into force. Therefore, all Egyptian exports of

industrial products will enjoy free access to Turkey.

1

Customs duties on industrial products

originating in Turkey shall be gradually abolished according to the four lists attached to the

protocol.

List 1 covers raw materials that are important as inputs for most industries. This list enjoys 75

percent reduction from the Most Favored Nation (i.e. non-preferential) duty from the day of

entry into force of the agreement. Products on the list will enter Egypt duty-free in the second

year of entry into force of the agreement (i.e., 2008). The list consists of about 2,070 HS tariff

lines, including aluminum ores, sodium chloride, sulphur, wood, parts of machines, aluminum

oxide, and copper alloys. Egypt’s MFN duties on those products are 0, 2, 5, or 10 percent.

List 2 covers intermediate goods. Tariff phase-out for these products will start in 2008.

Egyptian imports will enjoy duty-free access starting in 2014.The list consists of about 1,204

HS tariff lines, including carbon, chemical preparations, papers, glasses fibers, tubes and

pipes of vulcanized rubber, insecticides, and vacuum flask. Egypt’s MFN duties on those

products are 2, 5, 10, 20, or 30 percent.

List 3 covers final goods for which tariff phase-out will begin in 2010 and end with complete

liberalization in 2017. The list consists of nearly 1,650 HS lines, including apparel, textiles,

1

Products in Annex I of the FTA are treated as agricultural or processed agricultural products and are not

considered industrial products even though some are classified between chapters 25 and 97 of the HS.

M AIN P R O V I S I O N S 7

shoes, iron and steel, and electrical equipments and machines. Egypt’s MFN duties on those

products are 2, 5, 10, 20, or 30 percent.

List 4 includes mainly vehicles and some electrical engines and generators. Tariff phase-out

will occur from 2011 to 2020. The list includes only 23 HS lines. Egypt’s MFN duties on those

products are 10, 30, 40, or 135 percent.

Tariff reductions for Egyptian imports are summarized in Table 2-1.

Table 2-1.Tariff Phase-out for Egyptian Imports of Industrial Products from

Turkey, 2007–2020

List

07

08

09

10

11

12

13

14

15

16

17

18

19

20

1

75%

100%

-

-

-

-

-

-

-

-

-

-

-

-

2

-

10%

25%

40%

55%

70%

85%

100%

3

-

-

-

5%

10%

25%

40%

55%

70%

85%

100%

4

-

-

-

-

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Agricultural, Processed Agricultural, and Fishery Products

Concessions on agricultural, processed agricultural, and fishery products are outlined in Protocol

II. The two parties have agreed to grant each other concessions either as tariff rate quotas (TRQs)

or tariff reductions on agricultural, processed agricultural, and fishery products. The two parties

exchanged the same concessions on processed agricultural products.

Protocol II has two tables of concessions. Table A includes agricultural and processed agricultural

products originating in Turkey that will be subject to TRQs and/or reduced duties when exported

to Egypt. Table B includes agricultural, processed agricultural, and fishery products originating in

Egypt that face TRQs and/or reduced duties when exported to Turkey. Thus, Egyptian exports of

agricultural products have better market access opportunities into the Turkish market than Turkish

exports of similar products into the Egyptian market. Moreover, Egyptian fishery exports, except

HS 0301, face a 50 percent MFN duty reduction when entering the Turkish market, while some

live plants will access the Turkish market on a duty-free basis. Although limited, the products

listed in Tables A and B (Tables 2-2 and 2-3) are important for both countries. Nevertheless, the

two countries may discuss expanding those concessions at a later date through the joint committee.

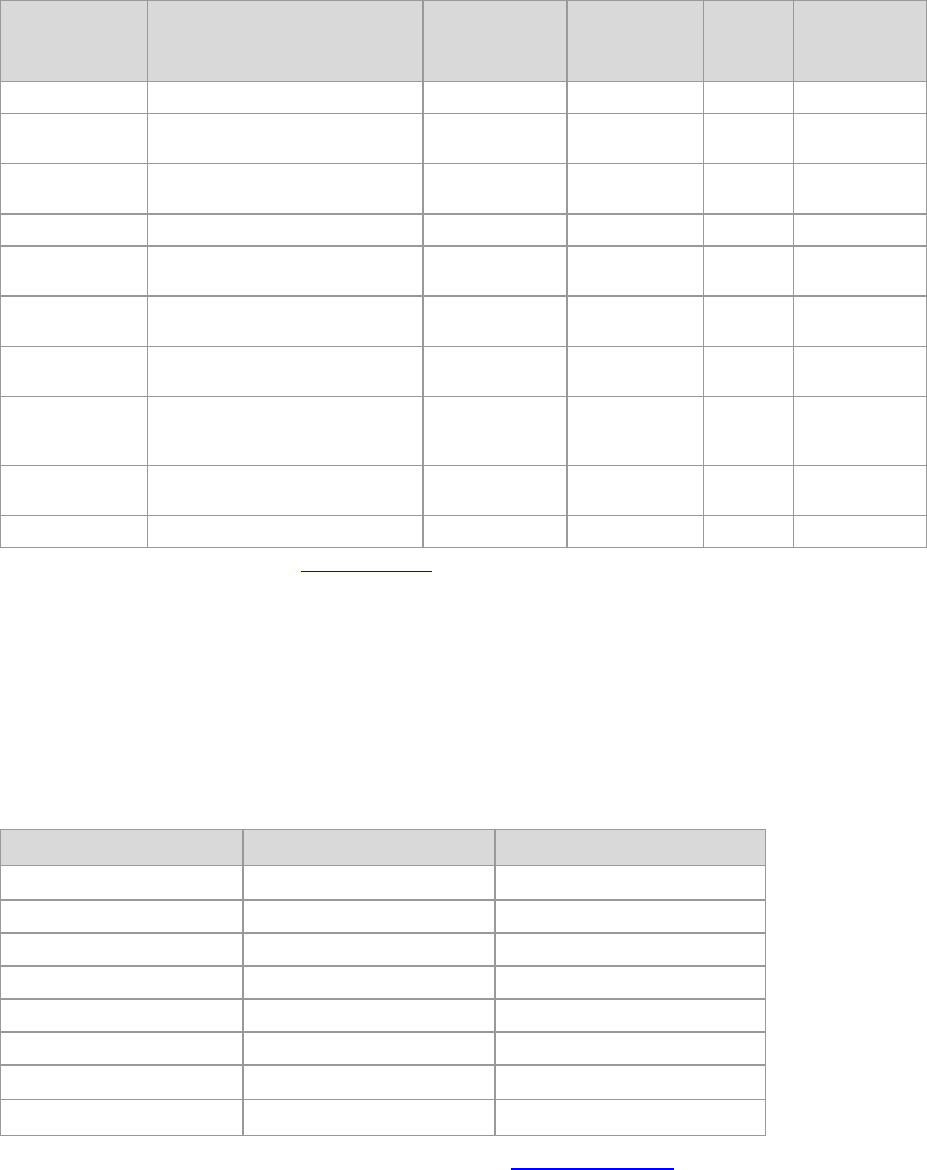

Table 2-2. Tariff Concession Schedule for Turkish Exports of Agricultural and

Processed Agricultural Products into Egypt

CN Code

Product Description

Quantities (tons)

Tariff Reduction

from MFN Duties (%)

0802.21

Hazelnuts or filberts (Corylus spp)

2,000

100

0802.22

0804.20

Figs

500

100

0809.20

Cherries (including sour cherries)

500

100

0813.10

Dried apricots

500

100

1507.90.91

Soya-bean oil, semi-refined in bulk

10,000

100

1512.11

Crude sunflower or safflower oil

20,000

100

1512.19.91

Sunflower seed oil, semi-refined in bulk

8 E GYPT– T U R K E Y F TA

CN Code

Product Description

Quantities (tons)

Tariff Reduction

from MFN Duties (%)

1515.21

Crude maize (corn) oil and its fractions

10,000

100

1517

Margarine; edible mixtures or preparations of animal or

vegetable fats or oils or of fractions of different fats or oils

of this chapter, other than edible fats or oils or their

fractions of heading 1516

1,000

100

1704

Sugar confectionery (including white chocolate), not

containing cocoa

2,000

15

1806

Chocolate and other food preparations containing cocoa

1,000

15

1902

Pasta, whether or not cooked or stuffed (with meat or

other substances) or otherwise prepared, such as spaghetti,

macaroni, noodles, lasagna, gnocchi, ravioli, cannelloni;

couscous, whether or not prepared

1,000

15

1905

Bread, pastry, cakes, biscuits and other bakers’ wares,

whether or not containing cocoa; communion wafers,

empty cachets of a kind suitable for pharmaceutical use,

sealing wafers, rice paper and similar products

1,000

15

2001.10

Cucumber and gherkins, prepared or preserved by vinegar

or acetic acid

1,000

15

2008

Fruit, nuts and other edible parts of plants, otherwise

prepared or preserved, whether or not containing added

sugar or other sweetening matter or spirit, not elsewhere

specified or included

500

15

2009

Fruit juices (including grape must) and vegetable juices,

unfermented and not containing added spirit, whether or

not containing added sugar or other sweetening matter

500

15

2102.10

Active yeasts

3,000

15

RULES OF ORIGIN

Protocol III outlines the rules of origin under the FTA. Both parties will apply the Pan-Euro-Med

rules of origin, which allow goods produced from materials originating in any Euro-Med countries

to enter the EU market with preferences. As the Egypt–Turkey FTA enters into force, Egypt and

Turkey can benefit from cumulation of origin under the Pan-Euro-Med rules of origin, establishing

originating integrated industries and exporting resulting goods into the EU. These cumulation

opportunities will likely expand with the entry into force of other Agreements by both Egypt and

Turkey with other Euro-Med countries under the auspices of the Barcelona Declaration.

2

Definition of Originating Products

Protocol III of the Egypt–Turkey FTA defines originating products as products that are either

wholly obtained in Egypt within the meaning of Article 5 or ―products obtained in Egypt

incorporating materials which have not been wholly obtained there, provided that such materials

have undergone sufficient working or processing in Egypt within the meaning of Article 6.‖ The

definition of these "sufficient" operations is presented in Annex II. The annex contains a complete

list of operations that are considered as conferring origin to a non-originating raw material for all

2

Since the Pan-Euro-Med Rules of Origin are quite complex, we encourage interested readers to read

Protocol III at http://www.tas.gov.eg/English/Trade%20Agreements/Countries%20and%20Regions/

Europe/turkey

M AIN P R O V I S I O N S 9

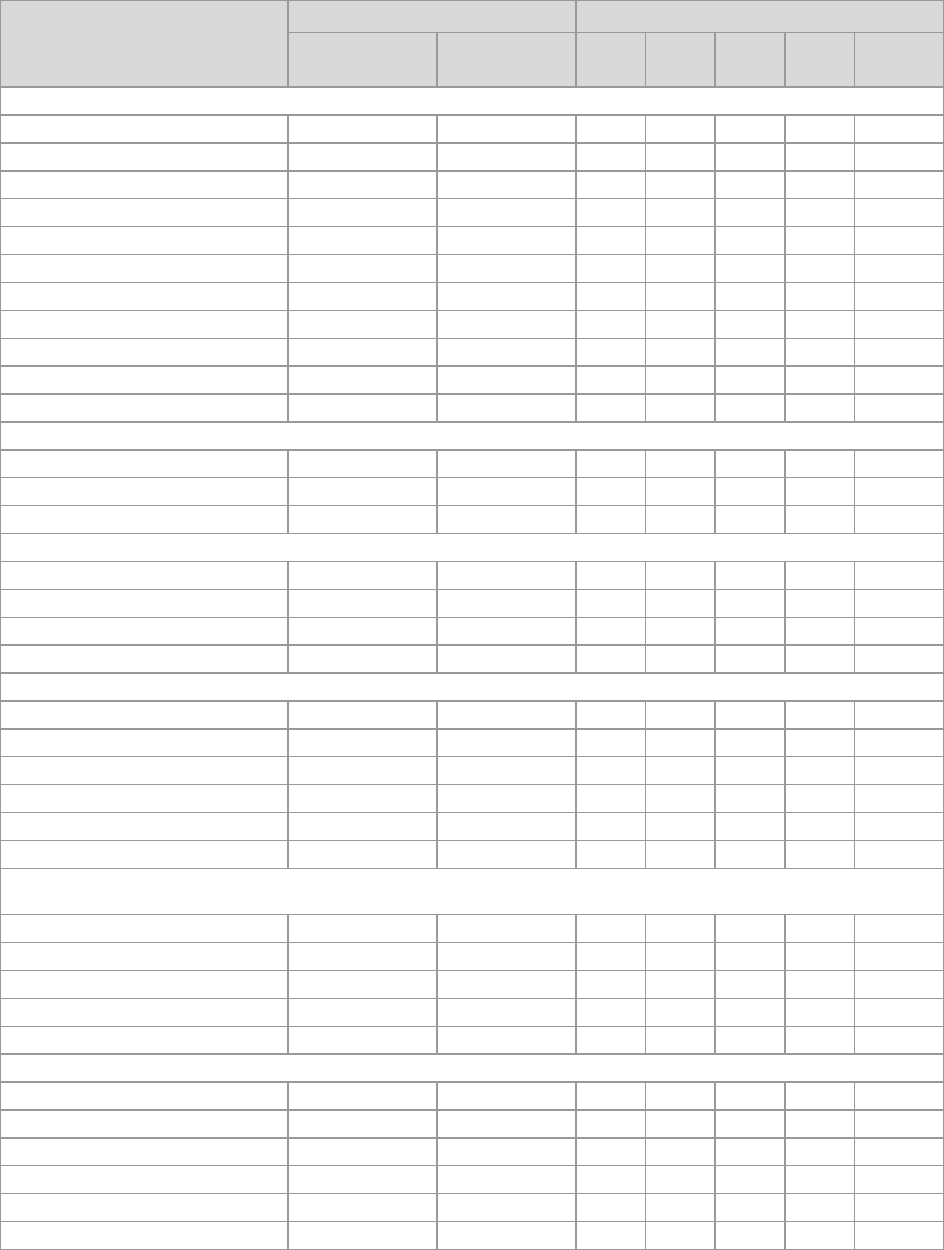

Table 2-3. Tariff Concession Schedule for Egyptian Exports of Agricultural and

Processed Agricultural Products into Turkey

CN

Code

Product

Quantities (tons)

Tariff Reduction

from MFN Duties (%)

Chap. 3

Fish and crustaceans, molluscs and other aquatic invertebrates

(excl. 0301)

Unlimited

50

0602

Other live plants (including their roots), cuttings and slips;

mushroom spawn (excl. 0602.90.91, 99)

Unlimited

100

0603

Cut flowers and flower buds of a kind suitable for bouquets or

for ornamental purposes, fresh, dried, dyed, bleached,

impregnated or otherwise prepared

15

100

0701.90

Other potatoes, fresh or chilled

400

100

0703.20

Garlic, fresh or chilled

100

100

0705

Lettuce (Lactuca sativa) and chicory (Cichorium spp.), fresh or

chilled

600

100

0706

Carrots, turnips, salad beetroot, salsify, celeriac, radishes and

similar edible roots, fresh or chilled

0709

Other vegetables, fresh or chilled (excl. 0709.90.31, 39)

0710

Vegetables (uncooked or cooked by steaming or boiling in

water), frozen (excl. 0710.80.10)

0711

Vegetables provisionally preserved (for example, by sulphur

dioxide gas, in brine, in sulphur water or in other preservative

solutions), but unsuitable in that state for immediate

consumption (excl. 0711.20, 40)

0712

Dried vegetables, whole, cut, sliced, broken or

in powder, but not further prepared

0804.10

Dates, fresh or dried

5000

100

0804.50

Guavas, mangoes and mangosteens, fresh or dried

1000

100

0810.10

Strawberries, fresh

200

100

0909

Seeds of anise, badian, fennel, coriander, cumin or caraway;

juniper berries

100

100

0910

Ginger, saffron, turmeric (curcuma), thyme,

bay leaves, curry and other spices

100

100

1006.20

Husked (brown) rice

30000

100

1006.30

Semi-milled or wholly milled rice, whether or not polished or

glazed

10000

50

1202

Groundnuts, not roasted or otherwise cooked

500

100

1704

Sugar confectionery (including white chocolate), not containing

cocoa

2000

15

1806

Chocolate and other food preparations containing cocoa

1000

15

1902

Pasta, whether or not cooked or stuffed (with meat or other

substances) or otherwise prepared, such as spaghetti, macaroni,

noodles, lasagne, gnocchi, ravioli, cannelloni; couscous, whether

or not prepared

1000

15

1905

Bread, pastry, cakes, biscuits and other bakers’ wares, whether

or not containing cocoa; communion wafers, empty cachets of a

kind suitable for pharmaceutical use, sealing wafers, rice paper

and similar products

1000

15

2001.10

Cucumber and gherkins, prepared or preserved by vinegar or

acetic acid

1000

15

2008

Fruit, nuts and other edible parts of plants, otherwise prepared or

preserved, whether or not containing added sugar or other

sweetening matter or spirit, not elsewhere specified or included

500

15

2009

Fruit juices (including grape must) and vegetable juices,

unfermented and not containing added spirit

500

15

2102.10

Active yeasts

3000

15

10 E GYPT– T U R K E Y F TA

products. Those operations might involve one or a combination of the following types of criteria:

A minimum percentage of value-added that has taken place in Egypt

A specific process that must have taken place in Egypt

Restrictions stating that specific inputs must be wholly obtained in Egypt

Change of tariff heading.

Cumulation Concept

In the context of the Pan-Euro-Med zone, cumulation means that

products that have obtained originating status in one partner country may be used with

products originating in another partner country without prejudice to the preferential

status of the finished product. In the case of cumulation the working or processing

carried out in each partner country on originating products does not have to be

’sufficient working or processing’ within the meaning of Article 6 in order to confer

on the finished product, the origin of the partner country but it must go beyond the

minimal operations in Article 7.

3

As indicated earlier, in bilateral cumulation materials are imported from a country to which the

finished product will be exported (e.g. Turkish materials processed in Egypt for export to Turkey).

But with diagonal cumulation, materials are imported from a country other than the country to

which the finished product will be exported (e.g., Turkish materials processed in Egypt for export

to the EU).

No Draw Back Rule

In the Pan-Euro-Med zone drawback is generally prohibited in diagonal trade. Article 15 in

Protocol III of the Egypt–Turkey FTA provides that non-originating materials used in the

manufacture of products originating in Turkey, Egypt, or in one of the other Euro-Med zone

countries cannot be subject in Egypt or in Turkey to drawback when those manufactured products

are destined for export to the zone. However, Egypt and Turkey may, except for products falling

within HS Chapters 1 to 24, benefit from drawback until December 31, 2009 subject to the

following provisions:

A 5 percent rate of customs charge shall be retained in respect of products falling within

Chapters 25 to 49 and 64 to 97 of the Harmonized System, or such lower rate as is in force in

Egypt or Turkey;

A 10 percent rate of customs charge shall be retained in respect of products falling within

Chapters 50 to 63 of the Harmonized System, or such lower rate as is in force in Egypt or

Turkey.

4

Thus, the protocol allows Egyptian exporters to benefit from drawback in purely bilateral trade

between Egypt and Turkey (until 2009 and not including HS chapters 1-24). In diagonal trade the

Egyptian exporters may apply for preferential proof of origin and pay duties on imported parts or

they may not apply for preferential proof of origin and benefit from drawback on imported parts.

The decision depends on the preferential margin on the exported product and the rate of duty on

imported materials.

3

A User's Handbook to the Rules of Preferential Origin used in trade between the European Community,

other European Countries and the countries participating to the Euro-Mediterranean Partnership, p 10.

4

Egypt-Turkey Free Trade Agreement, Protocol III, Article 15, paragraph 7.

M AIN P R O V I S I O N S 11

Proof of Origin

To benefit from tariff concessions granted in preferential agreements, products must be originating

and exporters must have proof of origin. To enable operators to fully benefit from the system it is

necessary to submit either a movement certificate EUR.1; a movement certificate EUR-MED; or

an invoice declaration given by the exporter on an invoice, a delivery note, or any other

commercial document that describes products in sufficient detail to enable identification. An

invoice declaration may be made out by an approved exporter or by any exporter for any

consignment consisting of one or more packages containing originating products whose total value

does not exceed EUR 6,000.

3. Egypt–Turkey Trade and

Investment

TRADE

Egypt’s trade with Turkey was on an upward if fluctuating trend even before the FTA took effect.

In 2006, Egyptian exports to Turkey had more than tripled since 1996 and imports rose by slightly

less than 50 percent during the same period.

Egypt’s trade with Turkey accounts for 2.6 percent of Egyptian goods exports and 2 percent of

imports. In 2006, exports to Turkey amounted to $363 million, making Turkey the eleventh largest

market for Egyptian exports. Also in 2006, Egyptian imports from Turkey were valued at $367

million, making Turkey Egypt’s fifteenth largest supplier. Egypt’s trade deficit with Turkey

widened from 1998 through 2002, largely because of increased imports from Turkey, then

narrowed substantially in 2003 and 2004 as Egyptian exports increased. In 2005 the deficit again

widened, and, then, in 2006 narrowed dramatically, an improvement that was due mainly to

increased imports of machinery, petroleum oils, motor cars, and iron and steel products (Table 3-

1).

Table 3-1. Trade Balance between Egypt and Turkey, 1996–2006

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Exports to

Turkey

115

97

118

97

85

78

78

144

235

334

362

Change from

1996

100%

84%

102%

84%

74%

67%

67%

125%

204%

290%

313%

Imports from

Turkey

253

174

489

358

202

247

223

178

246

623

391

Change from

1996

100%

69%

193%

141%

80%

98%

88%

70%

97%

246%

155%

Trade Balance

-138

-78

-371

-261

-117

-170

-145

-34

-11

-289

-29

Change from

1996

100%

43%

-169%

-89%

15%

-23%

-5%

75%

92%

-109%

79%

SOURCE: CAPMAS.

Exports

Egyptian exports to Turkey increased over the last three years (Figure 3-1). The top 20 Egyptian

exports to Turkey in 2006 are depicted in Table 3-2, with petroleum oils ranking at the top of the

list with $153 million. Other top Egyptian exports to Turkey consisted mainly of industrial goods

including chemicals, textiles, steel, and cement. Rice is the only agricultural product (within the

agreement definition) on that list with exports to Turkey valued at $39 million. Thirteen percent of

Egyptian rice is exported to Turkey.

14 E GYPT– T U R K E Y F TA

Figure 3-1. Egyptian Goods Trade with Turkey, 1996-2006

The top 20 Egyptian exports to Turkey accounted for 87 percent of Egyptian exports to Turkey in

2006. Sixty-seven percent of these exports entered the Turkish market on a duty-free basis.

Egyptian chemicals exports to Turkey represented a substantial share–21 percent–of all Egyptian

chemicals exports, with the vast majority of Egypt’s exports of polyvinyl chloride (64 percent),

sodium hydroxide (81 percent), and sodium hydroxide in aqueous solution (71 percent) destined

for the Turkish market.

Table 3-2. Top 20 Egyptian Exports to Turkey in 2006 and Turkish Pre-FTA

Tariffs on Egyptian Goods

HS

Subheading

Description

To Turkey

(US$ millions

To World

(US$

millions)

Turkey

Share

(%)

Turkish Pre-

FTA Tariff

(%)

271000

Petroleum oils and oils obtained from

bituminous minerals, other than crude

153.2

3604.8

4%

Free

100630

Semi-milled or wholly milled rice,

whether or not polished or glazed

38.7

287.4

13%

45%

270400

Coke and semi-coke of coal, of lignite

or of peat

21.2

43.4

49

Free

390410

Polyvinyl chloride, not mixed with any

other substances

19.0

29.6

64

3

390110

Polyethylene having a specific gravity

of less than 0.94

13.7

203.8

7

3

390490

Other: Polymers of vinyl chloride or of

other halogenated olefins, in primary

forms.

7.9

23.2

34

281511

Sodium hydroxide (caustic soda)- solid

7.5

9.2

81

1.9

252310

Cement clinkers

6.9

81.2

9

Free

520100

Cotton not carded or combed.

6.5

117.5

6

Free

283429

Other: Nitrites; nitrates.

6.1

16.1

38

Free

T R A D E A N D I N V E S T M E N T 15

HS

Subheading

Description

To Turkey

(US$ millions

To World

(US$

millions)

Turkey

Share

(%)

Turkish Pre-

FTA Tariff

(%)

281410

Ammonia anhydrous ammonia

5.0

12.6

40

Free

281512

Sodium Hydroxide in aqueous

solution (soda lye or liquid soda)

5.0

7.0

71

1.9

390190

Other: Polymers of ethylene, in

primary forms.

4.4

30.4

15

Free

271290

Other: Petroleum jelly

4.2

76.9

5

Free

720824

Flat-rolled products of iron or non-

alloy steel

3.5

24.4

14

5

721911

Flat-rolled products of stainless steel of

a thickness exceeding 10 mm

2.7

207.0

1

2

310230

Ammonium nitrate, whether or not in

aqueous solution

2.4

9.1

27

6.5

250590

Other: Natural sands of all kinds,

whether or not colored, other than

metal-bearing sands of Chapter 26.

2.3

7.0

34

Free

520542

Cotton sewing thread, whether or not

put up for retail sale.

2.3

31.6

7

3.2

281420

Ammonia in aqueous solution

2.3

7.5

31

Free

SOURCE: CAPMAS, Turkish tariff schedule (www.gumruk.gov.tr), and TPAU analysis.

Table 3-3 summarizes Turkey’s Most-Favored Nation (MFN) tariff schedule. These are the tariff

rates that Egyptian goods faced in Turkey before the FTA. More than 85 percent of Turkey’s MFN

tariff lines have duties between zero and 10 percent, with nearly 60 percent of Turkey’s tariff lines

having duty-free status. Only 14 percent of Turkey’s MFN tariff lines have duties exceeding 10

percent.

Table 3-3. Turkey’s MFN Tariff Schedule Summary

Tariff Base Rate (%)

Number of Tariff Lines

Percent of Total Tariff Lines

0

6,837

58.4

>0 to 10

3,241

27.7

>10 to 20

393

3.4

>20 to 35

149

1.3

>35 to 50

197

1.7

>50 to 65

379

3.2

>65

502

4.3

Total

11,698

100

SOURCE: Turkey’s 2007 MFN Tariff Schedule from Turkish Customs website (www.gumruk.gov.tr), and TPAU analysis.

Imports

Egyptian imports of goods from Turkey reached $367 million in 2006, making Turkey Egypt’s

fifteenth largest merchandise supplier with 2 percent market share of the nearly $21 billion

Egyptian import market. Slightly more than 40 percent (by value) of the top 20 Egyptian imports

from Turkey entered the Egyptian market duty free.

Table 3-4 shows the top 20 Egyptian imports of goods from Turkey in 2006, with petroleum oils

ranking first in value($70.5 million) and semi-finished products of iron or non-alloy steel ranked

16 E GYPT– T U R K E Y F TA

second ($47 million). Other top imports from Turkey included textiles, including woven fabric and

cotton yarn, which account for 70 percent and 62 percent, respectively, of total Egyptian imports

of those products.

Egypt’s agricultural imports from Turkey, including durum wheat, lentils, broad beans and horse

beans and hazelnuts or filberts, accounted for 18 percent (by value) of Egypt’s top 20 imports from

Turkey. Most of these products entered the Egyptian market duty-free.

Table 3-4. Top 20 Egyptian Imports and Pre-FTA Tariffs on Turkish Goods, 2006

HS

Subheading

Description

From Turkey

(US%

millions)

From World

(US$

millions)

Turkey

Share

(%)

Egypt Pre-

FTA Tariff

(%)

2710.00

Petroleum oils and oils obtained from

bituminous minerals, other than crude

70.5

1239.0

6

3.5*

7207.19

Other: Semi-finished products of iron or non-

alloy steel.

46.8

502.9

9

Free

5501.30

Woven fabrics of synthetic staple fibers,

containing less than 85% by weight of such

fibers, mixed mainly or solely with cotton, of a

weight not exceeding 170 g/m2.

17.5

25.1

70

10

1001.10

Durum wheat

16.0

964.3

2

Free

0713.40

Lentils

11.0

34.1

32

Free

0713.50

Broad beans and horse beans

8.3

113.1

7

Free

8708.99

Containers

7.4

178.8

4

10

8485.90

Other: Machinery parts

5.9

104.6

6

20

5503.30

Synthetic staple fibers Acrylic or modacrylic

5.9

7.6

77

Free

7612.90

Other: Aluminum casks, drums, cans, boxes and

similar containers

5.0

10.2

49

20

8479.89

Other: Machines and mechanical appliances

having individual functions, not specified or

included elsewhere in this Chapter.

4.9

125.3

4

Free

2401.10

Tobacco, not stemmed/stripped

4.9

164.7

3

L.E 6.1 / net Kg

5402.49

Synthetic filament yarn: other Partially oriented

(p. o. y)

4.6

75.3

6

Free

7228.30

Other bars and rods, not further worked than

hot-rolled, hot-drawn or extruded

4.2

10.1

41

5

4408.90

Other: Sheets for veneering

4.1

15.1

27

5

5205.22

Cotton yarn Measuring less than 192.31 decitex

but not less than 125 decitex

3.9

6.2

62

5

4011.10

New pneumatic tyres, of rubber of a kind used

on motor cars

3.7

40.1

9

20

3906.90

Other: Acrylic polymers in primary forms.

3.7

15.8

23

2

4011.20

New pneumatic tyres, of rubber of a kind used

on buses or lorries

3.6

62.7

6

10

5205.15

Cotton yarn Measuring less than 125 decitex

(exceeding 80 metric number)

2.9

31.6

9

5

0802.22

Hazelnuts or filberts (Corylus spp.). Shelled.

70.5

1239.0

98

5

Average tariff applied to 27.10

SOURCE: CAPMAS , Egyptian tariff schedule, and TPAU analysis

T R A D E A N D I N V E S T M E N T 17

Table 3-5 summarizes Egypt’s MFN tariff schedule, which was issued in February 2007 before the

FTA took effect in March 2007.

Table 3-5. Egypt’s MFN Tariff Schedule Summary

Tariff Base Rate (%)

Number of Tariff Lines

Percent of Total Tariff Lines

0

484

8.8

>0 to 5

2,876

52.4

>5 to 10

1,054

19.2

>10 to 20

254

4.6

>20 to 30

780

14.2

>30 to 40

13

0.2

>40

23

0.4

Total

5,484

100.0

SOURCE: Egyptian Tariff schedule 2007, TPAU analysis.

INVESTMENT

5

Investment promotion is an important objective of the Egypt–Turkey FTA, and a review of past

and current investment information will help detect investment trends. In the FTA the two parties

agreed to promote investment and technology flows by

6

Identifying, through appropriate means investment opportunities and information channels on

investment regulations;

Providing information on measures to promote investment abroad (e.g., technical assistance,

financial support, investment insurance, etc.);

Planning and implementing development projects, including the participation of foreign

investors;

Encouraging joint ventures, especially for SMEs and, when appropriate, concluding

agreements between Turkey and Egypt.

From the Egyptian side the agreement is expected to increase confidence in the Egyptian economy

and make it attractive as a hub for exports to other African, European, and Arab countries. Indeed,

Turkish and other investors may not only benefit from duty-free provisions when importing raw

material and other inputs from Turkey, but also export eligible products on a duty-free basis to

Turkey, EU, and other countries with free trade agreements with Egypt. Inward investment and

expanded trade are, in turn, expected to expand industrial activity and, thus, employment for

skilled and non-skilled labor.

Investment figures are already rising rapidly. Turkish investments in Egypt amounted to about

$ million from 1986 to the first quarter of 2007 and may reach $1 billion during the course of

this year.

7

At the same time, about 66 Egyptian companies are reportedly operating in Turkey,

5

Data used in this section was provided mainly by the Turkish Embassy in Cairo.

6

Egypt-Turkey Free Trade Agreement, Article 28.

7 A True Turkish Delight, Hadia Mostafa, Business Today, February 2007,

http://www.businesstodayegypt.com/

18 E GYPT– T U R K E Y F TA

according to Turkish Trade Minister Kürzad Tüzmen, while several others, particularly in the

service sectors, are considering investing there.

8

,

9

Turkish Investment in Egypt

Before the FTA was signed in 2005, 39 Turkish companies had established operations in Egypt in

diverse sectors and locations (Table A-4). Inward investment particularly picked up beginning in

2001 when FTA preparations were underway. By December 2005, when the agreement was signed

and results widely known among the business community in both countries, 20 more Turkish

companies had invested in Egypt (Table A-5).

Post-FTA, 2006 to April 2007. Once the agreement was signed–and even before its

implementation in 2007—the number of Turkish companies investing in Egypt increased

substantially to take advantage of export opportunities created by the agreement (Table A-6). Most

of the 59 Turkish companies that have invested in Egypt since the signing are involved in textiles

and apparel, again reflecting the opportunities to export into a wide range of African, Arab,

European, and even U.S. markets (through the Qualifying Industrialized Zones). This is reflected

in the 13 memoranda of understanding signed by the Egyptian–Turkish business association and

which aim at enhancing cooperation in various fields with other Turkish associations and the

chamber of commerce.

10

There are 28 Turkish stores, retailers, showrooms, buying offices

currently operating in Egypt. According to the Turkish Embassy another 40 companies are

expected to begin operating in Egypt shortly (Table A-7).

Prospective. More than 90 Turkish companies, 21 shops and buying offices, and 6 Turkish banks

are considering investing in Egypt and are studying the feasibility of doing so. Most investments

being considered are in the textiles, automotive, and chemicals sectors.

11

Minister of Trade and

Industry Eng. Rachid Mohamed Rachid and the Turkish Trade Minister Kürzad Tüzmen have

signed a memorandum of understanding to establish the first private industrial park in Egypt for

Turkish manufacturers. The new 2 million square kilometer industrial cluster in the Sixth of

October City will include Turkish manufacturing operations from a number of sectors.

12

Discussions are also underway to create another industrial park for Turkish textiles manufactures

in Borg El-Arab, where a number of Turkish textile and ready-made garments factories have

already set up shop.

13

The Egyptian-Turkish business association announced the start of two

investment projects amounting to 1.8 billion Egyptian Pounds, one in Upper Egypt to produce

paper, and the other in el Areesh to produce glass.

14

Finally, an agreement has been reached to

establish regular marine lines to link Alexandria and Port Said ports with Izmir and Istanbul

ports.

15

Details on investors, locations, and investment amounts are provided in the Appendix.

8

Ibid

Details on Egyptian investment in Turkey are outside the scope of this report.

10

Al Ahram newspaper, Khalifa Adham, 16 July 2007.

11

Data provided by the Turkish Embassy in Cairo

12

Al Ahram newspaper, Abd El Naser Aref, 17 March 2007

13

Business Today, February 2007, http://www.businesstodayegypt.com

14

Al Ahram newspaper, Khalifa Adham, 16 July 2007.

15

Ibid

4. Global Analysis Using General

Equilibrium Approach

In this chapter we model the impact of the Egypt–Turkey FTA on the Egyptian economy. The

model employed is the GTAP Computable General Equilibrium (CGE) model widely used to

analyze the impact of tariff liberalization. The model and its structure are reviewed in an earlier

paper (TPAU 2006) and in international journals and publications (Tsagas and Hertel 1997). To

accurately reflect conditions in Egypt and Turkey, the standard model was modified to include

macroeconomic ―closures‖:

Unemployment in the Egyptian market for unskilled labor.

Balance of payments for Egypt and Turkey constrained to 2004 levels, thus preventing either

country from deviating substantially from its current balance of trade in goods and services

into deficit or surplus (a common assumption for developing countries).

The database employed is the GTAP version 7p1 database reflecting global trade, production, and

tariffs for 2004. Egypt’s tariffs on imports from Turkey have been updated to 2007 rates, reflecting

substantial liberalization of Egypt’s tariff schedule.

TARIFF PHASE OUT

Simulations were carried out in four stages or scenarios reflecting the four major delineations of

Egypt’s tariff phase-out over 12 years. This methodology reveals the magnitude and timing of

sector impacts.

Table 4-1 presents Egyptian tariffs in place on goods from Turkey in 2007 (post-FTA) broken

down by six major sectors ranging from agriculture to services trade.

16

It also shows the phase out

of tariffs from 2008 to 2020 in the four periods that mark major shifts in the phase out schedule.

An analytical incongruity is evident where 2007 tariff data are presented with 2004 trade and

production data. The phase out schedule starts with the tariffs in place at the ratification of the

agreement (February 2007) (using the new 2007 tariff schedule). But trade data for 2007 are not

available before the end of the year. In addition, the global database of production and trade used

here is based on 2004 data. These inconsistencies are not serious and more up to date data are used

whey they are available, such as 2007 tariffs applied to 2004 trade data. Turkey’s tariffs have

changed little since it entered into a customs union with the EU in the 1990s. Rates from a

database for 2004 (see Table 4-2) are therefore applied in the following analysis.

17

16

Details on sector-by-sector tariff phase out for Egypt are presented in Table A-1.

17

Table A-2 provides sector by sector tariff phase out for Egypt.

20 E GYPT– T U R K E Y F TA

Table 4-1. Egyptian Phase-Out Schedule by Sector, 2007–2020

Sector

2004 (US$ millions)

Tariff Phase Out Schedule (Trade

Weighted Average Tariffs, %)*

Production

Imports from

Turkey (%)

Base

2007

2008

2014

2017

2020

Agriculture

27,163.5

50.1

6.5

6.5

6.5

6.5

6.5

Energy

13,945.5

0.3

3.1

1.4

0.0

0.0

0.0

Textiles and apparel

12,518.7

80.9

1.7

1.5

0.3

0.0

0.0

Motor vehicles and equipment

2,705.8

102.2

33.1

30.5

17.2

7.6

0.0

Mining and metals

9,874.0

142.1

9.1

8.7

3.4

0.0

0.0

Chemicals, wood and other manu.

9,310.0

77.0

7.4

5.7

1.3

0.2

0.2

All products

75,517.5

452.5

12.6

12.1

6.7

2.8

0.7

SOURCE: Analysis by Nathan Associates and the Egyptian TPAU based on the Egypt-Turkey Phase out schedules.

*Data reflect weighted averages based on 2004 Egyptian imports from Turkey as reported by CAPMAS and 2007 tariffs.

Table 4-2.Turkish Phase-Out Schedule, by Sector, 2007–2008

Sector

Imports from Egypt

2004 (US$ Millions)*

Tariffs on Imports from Egypt (%)**

2007

2008

Agriculture

46.6

37.1

37.1

Energy

31.9

0.1

0.0

Textiles and apparel

26.3

7.0

0.0

Motor vehicles and equipment

14.5

3.2

0.0

Mining and metals

43.6

2.9

0.0

Chemicals, wood and other man.

69.8

2.6

0.0

All products

232.6

9.8

7.4

SOURCE: Analysis by Nathan Associates and the Egyptian TPAU based on the Egypt–Turkey Phase out schedules.

* GTAP 2004 trade data.

**Data reflect weighted averages based on 2004 Turkish imports from Egypt as reported by GTAP.

WELFARE IMPACTS

Table 4-3 presents estimates of net welfare impacts resulting from market access liberalization

under the Egypt–Turkey FTA. The annualized welfare impact amounts to US$45 million for Egypt

and US$95 million for Turkey at the time of complete implementation of the agreement in 2020.

These impacts are modest, amounting to less than 1/10th of a percent of the GDP of either country.

For Egypt, more than two-thirds of the benefits of the FTA accrue at or before 2014. For Turkey,

benefits are significantly delayed, with more than two-thirds accruing after 2014. This stems from

the long phase out of industrial tariffs granted to Egypt. So, while Egypt’s total welfare benefits

are less than Turkey’s, Egypt starts accruing them much earlier and for a longer period. The

standard GTAP model implemented in this analysis does not capture the dynamic effects of

investments and capital accumulation that might occur as a result of the free trade agreement.

Understanding where welfare benefits and costs arise can provide insight not only into the overall

impact of the FTA, but also into how different stakeholders in an economy are affected. Table 4-3

also presents these manifestations of welfare changes:

G T A P A N A L Y S I S 21

Allocative efficiency—the gain or loss to an economy when scarce resources, such as land,

skilled labor, and capital are used more efficiently;

The endowment effect—the gain from greater utilization of unemployed factors of production,

such as unskilled labor in Egypt;

The terms of trade effect—the change in the ratio of export prices to import prices.

The US$45 million welfare gain for Egypt has three components. Importantly, wage gains from

expanding employment in the unskilled labor market make up US$46 million of the benefits. This

is offset, however, by a loss of US$14 million from deteriorating terms of trade. In contrast, the

gains to Turkey accrue largely from improved terms of trade effect of over US$66 million.

Table 4-3. Welfare Impacts, GDP and Income (in 2004 US$)

Welfare Component

GDP 2004

Impacts (US$ millions)

2008

2014

2017

2020

Total

E GYPT

Total

76,805.0

15.7

17.7

9.0

2.8

45.2

Allocative efficiency

--

1.4

14.6

7.3

-5.1

18.2

Employment gains low skilled

labor (losses)

--

7.2

10.8

12.1

16.6

46.7

Terms of trade

--

5.8

-5.2

-7.4

-7.4

-14.2

T U R K E Y

Total

295,831.0

3.8

26.0

30.2

32.3

92.3

Allocative efficiency

--

1.2

3.1

4.3

7.9

16.5

Employment gains (losses)

--

--

--

--

--

--

Terms of trade

--

2.2

20.0

22.7

21.4

66.3

Note: Impacts do not sum to total because several smaller categories are omitted.

SOURCE: Analysis by Nathan Associates and the TPAU.

TRADE AND PRODUCTION IMPACT

While the FTA’s impact on Egypt’s GDP is modest, differences in trade and production at the

sector level are significant. Sectors of interest here include the following:

Agriculture

Energy

Textiles and apparel

Motor vehicles and equipment,

Mining and metals,

Chemicals, wood and other manufactures

Services

Exports and Imports

The Egypt–Turkey FTA results in an increase in Egyptian imports of just under US$100 million

by 2020. Imports from Turkey increase by nearly US$500 million by that time period, but more

than half of the increase in imports from Turkey occurs after 2017. Imports from the rest of the

world decline significantly, but by somewhat less than the increase in imports from Turkey (Figure

22 E GYPT– T U R K E Y F TA

4-1). The decline in imports from the rest of the world demonstrates the FTA’s strong trade

diversion effect, which limit much of the gains from trade.

Egypt’s exports to both Turkey and elsewhere are estimated to increase. Most of Egypt’s export

gains to Turkey occur in 2008 as a result of Turkey’s immediate elimination of industrial tariffs at

the ratification of the agreement. Exports to the rest of the world decline slightly as Egyptian

industry shifts sales from other export markets to Turkey.

Figure 4-1. Change in Egyptian Imports Relative to 2004 Baseline (US$ Millions)

Figure 4-2. Change in Egyptian Exports Relative to 2004 Baseline (US$ millions)

G T A P A N A L Y S I S 23

The net long-term impact is overwhelmingly positive. Starting in 2014, Egypt’s tariff liberalization

on imports from Turkey results in Egypt expanding exports to the rest of the world. This continues

to grow with successive phases of tariff phase out as cheaper imports on inputs from Turkey make

Egypt’s exports to the rest of the world more competitive. By 2020, the increase in Egyptian

exports to the rest of the world will be more significant than the increase in Egyptian exports to

Turkey because of continued reductions in tariffs on Turkish imports (Figure 4-2).

Agriculture

The impact of the Egypt–Turkey FTA on Egypt’s agricultural sectors is modest because chapters

1-24 of the Harmonized Schedule were not provided tariff elimination under the agreement.

Liberalization of agriculture sectors is limited to a few tariff rate quotas (TRQs) and an agreement

to continue discussions on agricultural products. TRQs with low quotas result in rents, in the form

of tariff revenue, being diverted to producers in the exporting country. Out of quota tariffs have no

impact on import levels and hence trade patterns.

Still, data in Tables 4-1 and 4-2 show that Egyptian tariffs on agricultural imports from Turkey

(6.5 percent) are significantly lower than Turkey’s tariff on imports from Egypt (37.1 percent).

These data seem to indicate that Egypt has more potential to gain from extending the FTA to

agricultural products then Turkey and Egypt could gain from this liberalization. Egyptian imports

that could benefit the most from further liberalization include rice, sugar and sugar cane, fruits and

nuts, and processed food products (see Table A-2).

Energy

The estimated impact of the Egypt–Turkey FTA on Egypt’s energy sectors (natural gas, oil, coal,

and electric generation) is negligible. Tariffs on energy imports are already low in both countries

(in Egypt, an average 3.1 percent; in Turkey less than 1 percent) .

Textiles and Apparel

Total imports of textile and apparel products, from all countries, are estimated to comprise 10

percent of Egyptian production or US$1.3 billion in imports in 2004 (Table 4-4). Egypt’s imports

of textile and apparel products from Turkey in 2004 are estimated at less than 1 percent of

Egyptian production. In all cases, for imports and exports, textile trade with Turkey surpasses

apparel trade by a wide margin.

On the basis of average tariffs presented in Table 4-1, one can estimate the average tariff to be

eliminated on imports of textile and apparel from Turkey to be 1.7 percent. A detailed examination

of product line trade data reveals that the vast majority of Egyptian imports from Turkey are

manmade fiber textile fabrics and yarns, which draw a zero tariff when entering Egypt, resulting in

a strong downward bias on the weighted average tariff rate. Conversely, Egyptian exports to

Turkey face an average tariff rate estimated to be 7 percent. The model, therefore, estimates only

modest gains for Egyptian imports and exports of textile and apparel products—a change in

domestic production of less than 1 percent when the agreement is fully in force in 2020 (Table 4-

5).

24 E GYPT– T U R K E Y F TA

Table 4-4. Egyptian Textile and Apparel Trade as Percent of Production, 2004

Trade Flow

Total

Apparel

Textiles

Total imports

10.2

4.1

16.1

From Turkey

0.6

0.0

1.3

Total exports

13.6

13.4

13.8

To Turkey

0.2

0.0

0.4

SOURCE: Table 3-5.

Table 4-5. Estimated Impacts on Egyptian Textile and Apparel Production and

Trade

Sector

Base

2004

Impacts (est. US$ millions)

2008

2014

2017

2020

Total

P R O D U C T I O N

Apparel

6,156.2

0.6

1.2

-0.2

-1.5

0.1

Textile fabrics and yarns

6,362.5

15.2

-1.5

0.1

-1.7

12.1

Total

12,518.7

15.8

-0.3

-0.1

-3.2

12.1

I M P O R T S

Apparel

255.0

0.2

0.1

0.3

0.0

0.6

Textile fabrics and yarns

1,024.5

1.3

3.1

0.3

-0.1

4.7

Total

1,279.6

1.5

3.2

0.6

-0.1

5.2

E XPORTS

Apparel

826.9

0.4

0.8

0.6

0.6

2.4

Textile fabrics and yarns

881.1

15.5

0.8

0.6

-0.1

16.8

Total

1,708.0

15.9

1.6

1.2

0.4

19.2

I M P O R T S F R O M TURKEY

Apparel

0.4

0.0

0.4

0.7

0.0

1.1

Textile fabrics and yarns

80.5

1.3

7.0

1.2

-0.1

9.4

Total

80.9

1.3

7.4

1.9

-0.1

10.4

E X P O R T S T O T U R K E Y

Apparel

1.7

1.9

0.0

0.0

0.0

1.9

Textile fabrics and yarns

24.6

15.5

0.0

0.0

-0.1

15.4

Total

26.3

17.4

0.0

0.0

-0.1

17.4

Motor Vehicles and Equipment

Egypt’s motor vehicle, transportation, and heavy equipment sector has high import penetration and

low export competitiveness, as evidenced by trade flows as a percentage of Egyptian production of

these products (Table 4-6). Imports of motor vehicles and transport equipment are estimated to be

slightly less than two-thirds of domestic production. The machinery and heavy equipment market

is dominated by imports, with Egyptian production only achieving a fraction of total import levels

for these products. Meanwhile, motor vehicle imports face some of the highest levels of Egyptian

protection of any manufactured goods sector—tariffs average 65 percent—and tariffs on particular

products can exceed 100 percent.

G T A P A N A L Y S I S 25

Even with high tariffs, Egyptian production of motor vehicles is only modestly affected by rising

Turkish imports resulting from tariff elimination. The impact on Egyptian production is estimated

to be about US$11 million by 2020. Imports from Turkey, however, are expected to surge from

less than 1 percent of Egyptian production to US$282 million or 17 percent of Egyptian

production. Importantly, the large Turkish gain in the Egyptian market primarily results in trade

diversion and a movement away from motor vehicle imports from the rest of the world (Table 4-

7).

Table 4-6. Egyptian Motor Vehicles and Equipment Trade as Percent of

Production, 2004

Trade Flow

Total

Motor

Vehicles

Transportation

Equipment

Machinery and

Equipment

Total imports

188.0

60.7

57.3

622.1

From Turkey

0.1

0.1

0.0

0.2

Total exports

0.1

0.2

2.7

1.6

To Turkey

0.1

0.0

0.0

0.0

SOURCE: Table 3-7.

Table 4-7. Estimated Impacts on Egyptian Motor Vehicle and Equipment

Production and Trade

Sector

Base

2004

Impacts (est. US$ millions)

2008

2014

2017

2020

Total

P R O D U C T I O N

Motor vehicles

1,619

2.5

-2.2

-4.4

-7.7

-11.8

Transportation equipment

471

0.1

0.6

0.6

0.5

1.8

Machinery and equipment

616

1.0

1.5

1.5

0.0

4.0

Total

2705.8

3.6

-0.2

-2.3

-7.2

-6.0

I M P O R T S

Motor vehicles

981.7

1.6

-10.4

-2.8

17.5

5.8

Transportation equipment

270.0

0.0

0.1

0.1

0.3

0.5

Machinery and equipment

3834.6

16.2

0.5

-0.7

-1.6

14.4

Total

5,086.4

17.8

-9.9

-3.4

16.2

20.7

E XPORTS

Motor vehicles

2.7

2.1

0.6

1.0

1.0

4.8

Transportation equipment

12.6

0.0

0.2

0.2

0.2

0.5

Machinery and equipment

10.1

1.1

1.2

1.1

1.1

4.6

Total

25.5

3.2

2.0

2.3

2.3

9.9

I M P O R T S F R O M TURKEY

Motor vehicles

1.9

1.6

47.0

87.6

146.4

282.6

Transportation equipment

0.0

0.0

0.1

0.0

0.0

0.1

Machinery and equipment

1.3

16.2

8.5

3.5

-0.2

28.0

Total

3.3

17.8

55.5

91.2

146.3

310.7

E X P O R T S T O T U R K E Y

26 E GYPT– T U R K E Y F TA

Sector

Base

2004

Impacts (est. US$ millions)

2008

2014

2017

2020

Total

Motor vehicles

0.2

2.1

0.1

0.1

0.1

2.4

Transportation equipment

0.0

0.0

0.0

0.0

0.0

0.0

Machinery and equipment

0.2

1.1

0.0

0.0

0.0

1.2

Total

0.4

3.2

0.1

0.1

0.1

3.7

Mining, Minerals, and Metals

With an estimated US$9.8 billion in sales, mining and metal products are Egypt’s third largest

manufacturing sectors. The largest segment is mineral products, including cement and aggregates,

followed by iron and steel products. These two sectors also enjoy the highest import protection—

15 and 19 percent weighted average tariffs on Turkey (Table 4-8).

While imports as a percentage of Egyptian production often exceed 50 percent in other mining and

metals industrial segments, imports in the two protected sectors are less than 10 percent of

production. This relationship follows through the export side: Egyptian exports of raw minerals

and basic iron and steel exceed 50 percent of estimated domestic production. Meanwhile, exports