I

STUDY OF CUSTOMER SATISFACTION IN THE

BANKING SECTOR IN LIBYA

BY

HAITHAM AHMED AKGAM

808834

A thesis submitted to Othman Yeop Abdullah Graduate School of Business in

partial fulfillment of the requirement for the degree of Master of Science Banking

Universiti Utara Malaysia

brought to you by COREView metadata, citation and similar papers at core.ac.uk

provided by Universiti Utara Malaysia: UUM eTheses

II

PERMISSION TO USE

In presenting this thesis in partial fulfillment of the requirements for a postgraduate

degree from Universiti Utara Malaysia, I agree that University Library may make it

freely available for inspection. I further agree that permission for copying of this the-

sis in any manner, in whole or in part, for scholarly purpose may be granted by my

supervisor or in his absence, by the Dean of Othman Yeop Abdullah Graduate School

of Business. It is understood that copying or publication or use of this thesis or parts

of it for financial gain shall not be allowed without my written permission. It is also

understood that due recognition shall be given to me and to the Universiti Utara Ma-

laysia for any scholarly use which may be made of any material from my thesis. Re-

quests for permission to copy or make other use of materials in this thesis, in whole or

in part should be addressed to:

Dean

Othman Yeop Abdullah Graduate School of Business

Universiti Utara Malaysia

06010 UUM Sintok

Kedah Darul Aman

Malaysia

III

ABSTRACT

The purpose of this paper is to evaluate the customer satisfaction of the banks sector

in Libya, based on customer perception regarding service quality. This is an empiri-

cal study using mainly primary data collected through a well-structured questionnaire.

The method of the study Validity and reliability testing of questionnaire using SPSS

program for windows version 19The questionnaire has been personally administered

on a sample size of 204 bank customers. This paper makes a useful contribution as

there are only a few studies dealing with the assessment of service quality in banking

sector of Libya. The findings based on three different independent variables (service

quality, customer loyalty and security) showed that all these variables influenced con-

sumers satisfaction in Libyan banking sector. There is a positive impact and signifi-

cant relationship between the customer satisfaction and two variables (service quality

and customer loyalty), and also there is a negative relationship between security and

customer satisfaction

IV

ACKNOWLEDGEMENT

In the Name of Allah, the Most Gracious and the Most Merciful, I give thanks to my

creator, the able and powerful Almighty Allah for his help in seeing me through my

master program. It would not have been an easy achievement if not for His love and

mercy on me.

Firstly and foremost, I am grateful to Allah the Almighty for everything He has

granted me, the Most Merciful who has granted me the ability and willing to start and

complete this study. I do pray to His Greatness to inspire and enable me to finish this

dissertation on the required time. Without his permission, for sure I cannot make it

possible.

My most profound thankfulness goes to my supervisor, Dr. Logasvathi a/p Murugiah

for all his patience, scientifically proven, creativity encouraging guidance, and many

discussions that made this study to what it is. Without his understanding, considera-

tion and untiring advice, this dissertation would not have been completed successfully

My thanks and gratitude goes to all my dearest family members especially my moth-

er for being by my side since I left home.

Lastly, I am thankful to my dignified university (UUM) for giving me the opportunity

to carry out this research in a very conducive environment. Thank you.

V

Table of Contents

PERMISSION TO USE ............................................................................................................ II

ABSTRACT ............................................................................................................................. III

ACKNOWLEDGEMENT ....................................................................................................... IV

Table of Contents ...................................................................................................................... V

CHAPTER ONE ....................................................................................................................... 7

BACKGROUND OF STUDY .................................................................................................. 7

1.1 INTRODUCTION .................................................................................................... 7

1.2 RESEARCH PROBLEM ........................................................................................ 10

1.3 RESEARSH OBJECTIVE ...................................................................................... 13

1.4 RESEARSH QUESTIONS ..................................................................................... 13

1.5 SIGNIFICANT OF STUDY ................................................................................... 14

1.6 STUDY LIMITATION ........................................................................................... 15

CHAPTER TWO .................................................................................................................... 16

LITERATURE REVIEW ....................................................................................................... 16

2.1 INTRODUCTION .................................................................................................. 16

2.2 CUSTOMER SATISFACTION ............................................................................. 16

2.3 CUSTOMER SATISFACTION AND BANKING SECTOR ................................ 18

2.4 CUSTOMER SATISFACTION AND CUSTOMER LOYALTY ......................... 20

2.5 CUSTOMER SATISFACTION AND SERVICE QUALITY ............................... 21

2.6 CONSUMER PERCEPTIONS AND BEHAVIOUR: RELATIONSHIPS

BETWEEN SERVICE SATISFACTION, QUALITY AND LOYALTY ......................... 24

2.7 BANK SELECTION CRITERIA ........................................................................... 26

CHAPTER THREE ................................................................................................................ 30

RESEARCH METHODOLOGY ............................................................................................ 30

3.1 INTROUCTION ..................................................................................................... 30

VI

3.2 SAMPLE SELECTION .......................................................................................... 30

3.3 DATA COLLECTION ........................................................................................... 31

3.4 VARIABLES .......................................................................................................... 33

3.4.1 CUSTOMER SATISFACTION ............................................................................. 33

3.4.2 CUSTOMER LOYALTY ............................................................................. 34

3.4.3 SERVICE QUALITY ................................................................................... 35

3.4.4 SECURTY ..................................................................................................... 35

3.5 THEORETICAL FRAMEWORK .......................................................................... 36

3.6 HYPOTHESIS DEVELOPMENT .......................................................................... 37

3.7 STATISTICAL AND ANALYSIS ......................................................................... 37

3.8 DATA ANALYSIS TECHNIQUE ......................................................................... 38

3.8.1 Description analysis ................................................................................................ 38

3.8.2 Correlation analysis ................................................................................................ 41

3.9 REGRESSION ANALYSIS ................................................................................... 44

CHAPTER FOUR ................................................................................................................... 45

FINDINGS .............................................................................................................................. 45

4.1 INTRODUCTION .................................................................................................. 45

4.2 DESCRIPTION ANALYSIS .................................................................................. 45

4.3 CORRELATION ANALYSIS AND LINEARITY ................................................ 49

4.4 ANOVA ANALYSIS ............................................................................................. 51

4.5 COEFFICIENTS ANALYSIS ................................................................................ 54

4.6 DISCUSSION OF RESULT ................................................................................... 54

CHAPTER FIVE .................................................................................................................... 57

CONCLUSIONS AND RECOMMENDATION .................................................................... 57

5.1 INTROUCTION ..................................................................................................... 57

5.2 IMPLICATION OF THE STUDY ......................................................................... 58

5.3 SUGGESTION FOR FUTURE RESEARCHES .................................................... 59

7

CHAPTER ONE

BACKGROUND OF STUDY

1.1 INTRODUCTION

The present chapter contains the research background, problems statement, objectives

of the research, research questions, and justification of the study. The chapter also

shed a light on the significance of the study and the final section provides the study

limitations.

The issue of service quality is a critical one throughout service industries as business-

es attempt to sustain their competitive advantage in the marketplace. Owing to the

financial services like banks’ competition in the marketplace through undifferentiated

products, this highlights service quality as the basic competitive tool (Stafford, 1996).

In other words, a banking organization may attract customers through the provision of

high quality services. As such, structural modifications have led to banks being

enabled to carry out various activities which in turn, allow them to be more competi-

tive even against non-banking financial institutions (Angur et al., 1999).

In addition, technological advancements are helping banks develop their service strat-

egies being offered to individual as well as commercial customers. Moreover, banks

offering quality services own a distinctive marketing edge because enhanced quality

service is associated with higher revenue, customer retention and higher cross-sell

8

ratios (Bennett & Higgins, 1988). Banks are also well aware of the fact that custom-

er’s loyalty lies in the banks’ production of greater value compared to their competi-

tors (Dawes & Swailes, 1999).

Banks are more likely to earn higher profits if they are able to position themselves in

a superior way to their competitors in a particular market (Davies et al., 1995). There-

fore, it is imperative for banks to concentrate on service quality as their primary com-

petitive strategy (Chaoprasert & Elsey, 2004). Additionally, both customer satisfac-

tion and service quality have been highlighted by all banking institutions throughout

the world (Hossain & Leo, 2009) with the inclusion of the Libyan banking sector.

Libya is a country extending over an area of 1,759,540 square kilometers and is

ranked 17

th

nation in the world according to size. In the context of land area, Libya is

smaller compared to Indonesia and approximately akin to the size of Alaska, U.S. To

the north, it is bound by the Mediterranean Sea, to the west by Tunis and Algeria, to

the southwest by Niger, to the south by both Chad and Sudan and finally to the east

by Egypt. The Libyan economy is primarily dependent on oil sector revenues which

makes up almost all export earnings and around a quarter of the GDP (gross domestic

product).

In Libya, the discovery of oil and natural gas reserves back in 1959 resulted in the

shift in the country from a poor economy to Africa’s richest. According to the World

Bank, Libya is an Upper Middle Income Economy with seven other African coun-

tries. As a result, Libya used to the among the wealthiest countries in the world in the

9

earlier years of 1980s with a GDP per capita greater compared to developed countries

such as South Korea, Italy, Singapore, New Zealand, and Spain.

The Libyan banking sector has experienced significant developments particularly fol-

lowing the issuance of laws concerning banks and money by the Central Bank of

Libya. In 2005, the Central Bank of Libya played a key role in organizing banks and

restructuring capitals inducing them to look for investment opportunities in order to

compete in the provision of services akin to that of international banking services and

in order to attract depositors and investors to increase the equities and complete the

capital. These laws urged banks to have a capital not less than 30 million Libyan di-

nars. Consequently, banks initiated their new marketing services that used to be lack-

ing in Libya including the Visa Card, Electronic Bank Services, Mobile bank, West-

ern Union and Money Gram. In addition, top financial institutions looked to satisfy

the customers’ needs and demands for their survival and successful competition in the

current dynamic corporate marketplace.

Financial institutions generally believe that customers are the aim behind their servic-

es and hence their activities depend on their customers. This is why financial institu-

tions are more concerned with customer satisfaction, customer loyalty and their reten-

tion (Zairi, 2000). In fact, customer loyalty stems from the organization’s creation of

benefit for customers so they will be retained and continue doing business with the

organization (Anderson & Jacobsen, 2000).

10

1.2 RESEARCH PROBLEM

The main issue being faced by the Libyan banks is that most of them are still being

driven under the operation of the outdated programs. Another issue is the lack of

qualified and experienced workforce which eventually explains the low quality ser-

vice delivery to their customers (Ahmida Ali, 2011).

Owing to this reason, most banks have developed a method to tackle customer prob-

lems. This includes the provision of a suggestion box at the banks’ foyer or entrance

and the carrying out of a survey with the aims of realizing customer satisfaction. This

indicates that to hold the customers’ attention and loyalty, it is imperative for banks to

set up suggestion and complaint sections like hotlines, 24-hour call services as well as

online services (Ahmed Freed, 2012).

In the present study, study factors including service quality, security, and customer

loyalty are adopted from prior literature. Customer satisfaction is referred to as the

feeling or attitude of the customer towards a certain product or service after using

such product or service. It is the major result of marketing activity and it serves as a

connection between different phases of customer buying behavior; for example, when

customers are satisfied with a specific service following its use, they are more likely

to repeat their purchase and attempt at trying out the service line extensions (East,

1997).

11

In addition, although customer satisfaction has long been the focus of the local press,

there is little evidence revealing that it plays a key role in Libyan local banking mar-

ket. The significance of customer satisfaction in banks vary from one country to

another owing to reasons such as social, economic, political and technological envi-

ronmental factors. Factors relating to customer satisfaction are significant in some

countries but are not in others and this relates to the banking services in Libya.

This research is conducted in the context of Islamic Banks customers in Libya in an

attempt to examine the impact of customer loyalty and customer intention through

service quality moderated by customer satisfaction.

In sum, the problem that the present study is attempting to address is whether any re-

lationship exists between service quality, customer satisfaction and customer loyalty

in the context of Libyan Islamic Banks customers.

In the Islamic finance system, business operations and investment have their basis on

the Islamic principal and this differs from the investment concept existing in conven-

tional financial system. The difference lies in the fact that in the former, there is abro-

gation in the benefit rate (riba), and the procedures and finance covenant are accord-

ing to Islamic business principal. The Islamic finance system enables profit sharing in

investments (Othman & Owen, 2000). Moreover, the research concerning service

quality in the conventional financial system has been carried out by academicians in

the past and hence, it is not a new aspect (Le Blanc & Nguyen, 1999).

According to Parasuraman, Berry and Zeithaml (1985), several researches reveal that

service quality is an important strategy in gaining success and excellence in every or-

12

ganization. Similarly, Othman and Owen (2001) stated that good service quality is the

basis of every organization’s success and this includes the service sector such as the

Islamic financial institutions. Hence, these institutions are not only facing strong

competitions from their Islamic counterparts but also from conventional financial in-

stitutions (Naser, Jamal & Al-Khatib, 1999).

Moreover, banking institutions are facing the challenge of customer satisfaction of in

light of their service in several situations; impolite service at the counter, no enough

employees to attend customers, busy telephone lines and limited banking times (Ab-

dullah, 1996). This is particularly true in Libya, a developing country where the bank-

ing culture lacks structure. Therefore, the Libyan banking institutions are required to

expend more efforts and to carry out research to direct banking services in the attain-

ment of customer satisfaction.

13

1.3 RESEARSH OBJECTIVE

The present research aims to achieve the following objectives;

1. To examine the needs of Libyan Islamic banks.

2. To determine the main factors influencing the level of customer satisfaction in

Libyan commercial banking.

3. To assess the level of customer loyalty in Libyan banking services.

4. To assess the level of customer satisfaction of the quality of service provided

by the Libyan banks.

5. To assess the level of safety perception of the customers in Libyan banks.

1.4 RESEARSH QUESTIONS

On the basis of the aforementioned problem statement and the study objectives, the

research attempts to answer the following questions;

1. What are the needs of the Libyan banking sector?

2. What are the main factors influencing the level of customer satisfaction in Li-

byan commercial banking?

3. What is the level of customer loyalty to Libyan banking services?

4. What is the level of customer satisfaction to the quality of services offered by

Libyan banks?

5. What is the level of customer’s safety perception towards Libyan banks?

14

1.5 SIGNIFICANT OF STUDY

The Libyan banking system is highly dependent on the government banks; an ap-

proach not often associated with customer satisfaction. For this reason, the present

study offers practitioners with the incentive to find novel ways in improving their

services to customers and to modify the services currently provided; for instance, to

substitute traditional/conventional services by Islamic financial services and to pro-

vide timely and efficient services. The present research contributes to individual or

institutions and parties desirous of obtaining knowledge concerning bank customers’

behaviors.

The current political changes in Libya has a key role in the attempts to improve the

country’s banking system where all the financial systems were previously controlled

by dictatorship whose only aim is to accumulate individual wealth while disregarding

the country’s economic development. Such a system continued for over four decades

(1969-2011) which culminated in digression in social, economic and administrative

sectors of the country. In order to prevent the return to the previous regime, Libyan

banks are attempting to engage in investment activities by overseeing their dealings

and minimizing competition among financial institutions. They have also denied em-

ploying Islamic transactions within commercial banks with the exception of what has

been addressed in Law of banking and monetary Act No.1 of 2005. The current situa-

tion in the country is a consequence of political repression and economic deprivation

and social digression prior to the revolution on February 17, 2011 which was sup-

ported by the opposition to the old regime.

15

Following this revolution, Libya attempts to activate all the financial institutions in

the country along with the non-financial ones in order to achieve the country’s aims

of improving its level in all aspects.

The present research is invaluable for reference of future studies particularly those

related to service quality, customer satisfaction, customer loyalty and customer inten-

tion to switch.

1.6 STUDY LIMITATION

The present study collects relevant data from various sources relating to the respon-

dents’ view and for content analysis. In addition, some of the sub-samples are quite

small in number while the overall sample is confined to the Libyan banks customers.

These findings should be generalized in providing a description of customer satisfac-

tion of Libyan banks to the rest of the population. However, the findings cannot be

generalized to other types of bank customers

Moreover, another limitation to the study is the time required to complete the study

with the inclusion of analysis and the findings which are all confined to 14 weeks. A

study of this caliber required more effort and timely delivery of results.

16

CHAPTER TWO

LITERATURE REVIEW

2.1 INTRODUCTION

In this chapter we define some concepts which related to this study such as: Customer

Satisfaction, Customer Satisfaction and Banking Sector, Customer Satisfaction and

Customer Loyalty, Customer Satisfaction and Service Quality, Consumer Perceptions

and behavior: relationships between service satisfaction, quality and loyalty and bank

selection criteria

2.2 CUSTOMER SATISFACTION

A significant level of customer satisfaction is among the most critical indicators of

the business’s future. Customers who are satisfied are also loyal and this ensures a

consistent cash-flow for the business in the future. In addition, satisfied customers are

often characterized as less-price sensitive and they are more partial to spend more on

the products they have tried and tested before. Moreover, stability in business rela-

tions is also beneficial where the positive quality image minimizes the cost for a cur-

rent customer (Matzler, Hinterhuber, Bailom & Sauerwien, 1996).

According to Hom (2000), satisfaction refers to a feeling or a short term attitude that

can change owing to various circumstances. It exists in the user’s mind and is unlike

17

observable behaviors like product choice, complaint or repurchase. In a related study,

John and Linda (1976), investigated the relationship between expectations, perfor-

mance and satisfaction. The findings revealed that when a customer judges the per-

formance of a product, he usually compares a set of performance outcomes that are

expectations. The product is then likely to be considered as dissatisfactory or satisfac-

tory.

In another related study, Johnson, Anerson and Fornell (1995) developed and tested

alternative models of market-level expectations, perceived product performance, and

customer satisfaction. They revealed that in a particular period, satisfaction is posi-

tively impacted by performance and expectations where performance effects reveal

the impact that experiences of the product or service have upon satisfaction and ex-

pectation effects reveal the impact that past performance information has upon satis-

faction. They stated that managers inclined to maximize market satisfaction for the

purpose of enhancing future profitability is better off investing in long-run quality

improvement strategies and methods as short-term techniques only leads to temporary

performance or benefits per customer and will be negligible in the long-run.

Similarly, Anderson and Sullivan (1993) examined the antecedents and outcome of

firms’ customer satisfaction and found that quality falling short of expectations have

higher impact on satisfaction and retention compared to those exceeding expectations.

They also revealed that satisfaction positively affects repurchase intentions and both

positive and negative disconfirmations increase with the ease of quality evaluation.

18

2.3 CUSTOMER SATISFACTION AND BANKING SECTOR

Among the many studies in literature dedicated to customer satisfaction in banks, Al-

bro’s (1999) study in the context of Washington, U.S., utilized a benchmark involving

bank customers from all geographic areas and bank assets. The study involved asking

customers various questions concerning their satisfaction with the banks. Data col-

lected was utilized to benchmark customer satisfaction scores of banks participating

in the financial client satisfaction index. The findings revealed that the most signifi-

cant attributes that results in satisfaction include human interaction issues like ‘cor-

recting errors promptly’, ‘courteous employees’ and ‘professional behavior’. Moreo-

ver, the findings also revealed that the provision of good, personal service is consi-

dered by the clients as more important more than convenience or products.

The above findings were consistent with Wan, W.W., Luk C.L and Chow (2005)

findings. The latter study was also conducted in Washington and it revealed that cus-

tomers taking the customer satisfaction survey bought more products compared to the

control group that were not participants to the survey. According to the authors, sur-

vey participation is what led the customers to develop more positive perceptions to-

wards the company and it convinced them that the firm values and cares about its cus-

tomers and their feedback.

In another study, Bennett (1992) claimed that the key to obtaining competitive advan-

tage in the banking business is to be customer-driven. In other words, the entire as-

pects of the institution should concentrate on the factors that the customers hold dear

and it should be willing to exceed customer expectations. Several studies evidenced

19

that by concentrating on and delivering excellent customer satisfaction outcome,

firms achieve superior profitability. Hence, improving customer service may entail

training procedure or enhancement of computer information systems of the bank.

While improving customer service may lead to increased tangible accounting costs, it

may also steer clear of the occurrence of intangible costs. Bankers can develop quan-

titative data through researching customer satisfaction, in the hopes of stressing that

the emphasis and delivery of exceptional customer satisfaction can lead to improved

revenues that are higher than increased costs.

Similarly, Anwyll (2005) stated that customer service and satisfaction are the factors

differentiation a firm from its large, national competitors. Moreover, the banks brand-

ing message reads, “Great Rates. Friendly Service” and through ongoing sales and

service training, it attempts to deliver what it promises to.

Also, Mothey (1994) revealed that in order to achieve customer satisfaction, it is im-

perative for banks to make use of different tools that varies from re-engineering of

service to focusing on specific tasks. In addition, Albro’s (1999) study involved a na-

tional survey of the customers patronizing 814 banks in an attempt to determine cus-

tomer satisfaction. He revealed that cross selling hinges on high level of customer sa-

tisfaction. The study also revealed a very high correlation between satisfaction scores

and customer’s predisposition to repurchase. In short, for happy customers to provide

recommendations through word-of-mouth to others, they must be satisfied.

20

On the contrary, if the firm is derelict in serving the customer, they will not hesitate to

switch to another financial institution. According to Aldisert (1994), customer satis-

faction is not becoming significant in a way that some banks view it as a main ele-

ment in their marketing strategies. The term ‘after marketing’ has also been common-

ly utilized to reflect the concentration on expending effort to cater to current custom-

ers in an attempt to increase their satisfaction and to retain them (Vavra, 1995).

This section stressed on the importance of customer satisfaction which is considered

to be the basis of banks’ development of strategies. As such, it is important for cur-

rent financial institutions to shift towards customer management for their satisfaction

of the services provided. It is also imperative for banks to develop a system that con-

tinuously measures customer satisfaction (Chitwood, 1996).

2.4 CUSTOMER SATISFACTION AND CUSTOMER LOYALTY

Customer loyalty is defined as “the market place currency of the twenty-first century”

(Singh & Sirdesh, 2005). Similarly, Foss and Stone (2001) related customer loyalty to

the customer’s thoughts and actions. Several customer loyalty experts describe loyal-

ty as a state of mind and a set of beliefs. Among the main elements of loyalty are the

information exchange and the relation between the state of mind and behavior. For

instance, loyal customers often provide information to service providers because of

their sense of trust in them and they expect the service providers to utilize the pro-

21

vided information to their advantage. Moreover, customer satisfaction leads to cus-

tomer loyalty which in turn, leads to profitability (Hallowell, 1996).

2.5 CUSTOMER SATISFACTION AND SERVICE QUALITY

In the current dynamic and competitive business world, sustainable competitive ad-

vantage is driven by the delivery of high quality service that will result in customer

satisfaction. In other words, customer satisfaction is a condition to achieving custom-

er retention and loyalty and it can assist in boosting profitability, market share and

return on investment. In a related study, Suresh chandar, Rajendran and Anantharman

(2002) conducted an in-depth investigation of the relation between service quality and

customer satisfaction. They concluded by identifying five factors of service quality

that are considered by customers as critical. They are enumerated as follows;

1. Core service or service product – service content,

2. The human elements of the service delivery including reliability, responsive-

ness, assurances, empathy, and service recovery – all a part of the human ele-

ment when delivering the service,

3. Service delivery systemization which refers to the processes, procedures, sys-

tems and technology that helps in making the provision of service in a seam-

less manner,

22

4. Service tangibles which refers to equipment, signage, employees’ appearance

and the man-made physical environment characterizing the service – com-

monly called the ‘service space’, and finally,

5. Social responsibility which is the service provider’s ethical behavior and ac-

tivities.

The above study indicated the close relation between service quality and customer

satisfaction in a way that an increase in one factor leads to the increase in the other.

Viewed from another perspective, Johnston (1995) investigated the relation between

the determinants of service quality and outcomes of the zone of tolerance. He re-

vealed that there are some determinants that are more likely to be a source of dissatis-

faction while others to be a source of satisfaction. He demonstrated the following;

1. Some determinants of quality are superior to others,

2. The key sources of satisfaction of the bank’s customers include attentiveness,

responsiveness, care and friendliness while the key sources of dissatisfaction

include issues pertaining to integrity, reliability, responsiveness, availability

and functionality,

3. The sources of satisfaction enumerated above are not necessary the opposite

of the sources of satisfaction,

4. The intangible aspects of the staff-customer relation significantly impact ser-

vice quality in a negative and positive way,

23

5. Responsiveness is a key determinant of quality and is a key element in the

provision of satisfaction while the lack of it is a main source of dissatisfaction,

and

6. Issues of reliability are a source of dissatisfaction as opposed to satisfaction.

From the above, it is evident that satisfaction can be achieved by providing the ser-

vice in a timely and efficient manner. The presence of satisfying factors may also lead

to positive, virtuous circles, supporting contact staff-customer relationship.

Another study related to customer satisfaction in business service is the one by Na-

wak and Washburn (1998). They revealed that service quality has a highly significant

relationship with overall customer satisfaction. First, they revealed that product quali-

ty is a critical element of presentation. Second, the significant relation between time-

liness and cost management could support the saying “time is money” in the context

of business response to market changes. The third most critical contributor to overall

customer satisfaction was revealed to be service quality.

Moreover, Rod, Ashill, Carruthers and Shao (2009) stated that overall internet bank-

ing service quality is significantly related to overall customer satisfaction in New

Zealand banks. They added that the delivery of high quality online service is called

for, for the maintenance or enhancement of the banks’ customer satisfaction.

24

Also, Maddern (2007) revealed that the role of staff satisfaction and service quality

are both main drivers of customer satisfaction of the technical service quality (TSQ)

in the U.K. In addition, TSQ was revealed to be a key determinant of customer satis-

faction. In a related study, Isa and Amin (2008) claimed that most of the Islamic

Bank’s customers were satisfied with the banks’ overall service quality. The findings

also indicated that the standard model of Islamic banking service quality dimensions

should include the following six dimensions; tangible, reliability, empathy, respon-

siveness, assurance and compliance along with the good determinants of satisfaction.

They also revealed a significant relationship between service quality and customer

satisfaction.

2.6 CONSUMER PERCEPTIONS AND BEHAVIOUR: RELATION-

SHIPS BETWEEN SERVICE SATISFACTION, QUALITY AND

LOYALTY

Widespread support has been dedicated to the general notion that customer satisfac-

tion is a key variable for evaluating and controlling bank marketing management

(Moutinho & Bronwlie, 1989; Howcroft, 1991; Moutinho, 1992). Additionally, the

main role of service quality in the realm of financial service delivery has been

stressed by authors (e.g. Smith & Lewis, 1989; Avkiran, 1994). Despite the fact that

the constructs of both service quality and satisfaction are often interchangeable, the

significant body of research has attempted to clarify the nature of the relationship be-

25

tween them (e.g. Bitner, 1990; Cronin and Taylor, 1992; Parasuraman et al., 1994).

Moreover, based on Oliver’s (1993) review of the issues, service quality is an antece-

dent to satisfaction and it is by nature, non-experiential, which is not unlike attitude in

nature that can be developed from other sources like word of mouth. Despite the ac-

knowledgement of the multi-attribute nature of both constructs, over the years, re-

searchers have been focusing on the identification of the attributes and expansive di-

mensions of service quality. Prior works in the topic differentiated between technical

and functional quality (GroEnroos, 1984) and stressed on the significance of the func-

tional or service delivery as an element of consumer evaluations. This distinction has

influenced later works where researchers (e.g. Parasuraman, et al., 1988, 1991, 1994;

Babakus & Boller, 1992; Mels et al., 1997; Carman, 1990) investigated the dimensio-

nality of service quality. Other later works like Smith (2000), provided the following

three elements of the service process in addition to outcome; access/convenience,

human elements comprising of the combination between instrumental and expressive

qualities and finally, tangibles.

The effect of consumer’s service evaluation (implicit or explicit) in service quality

and satisfaction literature indicates the relation between the constructs and consumer

behavior. Researchers have attempted to define the relationship between behavioral

intentions and satisfaction (e.g. Oliver, 1980; Mittal et al., 1999) and between beha-

vioral intentions and service quality (Parasuraman et al., 1994; Boulding et al., 1993).

Meanwhile other researchers investigated the antecedent relation between all three

constructs with conflicting findings (e.g. Cronin & Taylor, 1992; Liljander & Strand-

26

vik, 1992; Taylor & Baker, 1994). Moreover, the relationship between intentions and

actual behavior is still unconfirmed (Keaveney, 1995) as research has mostly concen-

trated on studying the relationships between customer satisfaction and loyalty (Hal-

lowell, 1996; Yi, 1990). Loyalty is defined as repeat purchase intention, attitudes or

other alternative measures of actual behavior like repeat purchase, recommendation

among others. The complex relation between consumers various degrees or condi-

tions of loyalty (Dick & Basu, 1994) and their shift or ‘exit’ behavior has been exten-

sively studied (see Stewart, 1998).

2.7 BANK SELECTION CRITERIA

Several studies have been dedicated to customer bank selection decision. Most of

these studies made use of the questionnaire method of data collection to evaluate the

relative importance of specific selection attributes.

Among these studies is Che Wel and Mohd. Noor’s (2003) study whose sample com-

prised of 578 bank customers to determine the impact of personal and sociological

factors upon customer bank selection criteria in the context of Malaysia. The findings

revealed that personal factors are more influential compared to sociological factors.

Hence, to attract a customer over, banks must employ a strategy to satisfy the needs

of the target market and they can do this by focusing on personal factors but also

keeping the sociological factors in mind. In addition, convenience was revealed to be

an important factor in bank selection.

27

In a related study, Anderson, Cox III and Fulcher (1976) attempted to determine the

bank selection decision and market segmentation. They revealed that bank selection

decisions are carried out based on conscious deliberation with convenience being a

dominant factor in customer patronage. They added that image of bank and financial

consideration are principal determinants of bank patronage among customers who are

service-oriented and it is a significant criterion for both market segmentation and de-

sign of patronage attraction.

On the other hand, in the context of Hong Kong, Wan, Luk and Chow (2005) investi-

gated the factors influencing bank customers’ adoption of four major banking chan-

nels namely branch banking, ATM, telephone banking and Internet banking. Their

study specifically focused on the impact of demographic variables and psychological

notions concerning positive attributes characterizing the channels. They revealed that

ATM was the most often adopted channel followed by Internet banking and branch

banking. Telephone banking was the least often utilized channel.

Similarly, Jones, Nielsen and Trayler’s (2002) study made use of the Australian

Competition and Consumer Commissions (ACCC) method in an attempt to determine

criteria of bank selection of Australian 2,500 business firms. They revealed that for

large firms, the following factors are the selection criteria (in order of importance);

28

Bank charges competitive prices for both products and services

The bank’s ability to provide long-term business relations

Bank is efficient in its daily activities.

The above factors indicate that larger firms require a range of choices in financial

services. On the other hand, for small firms, the selection criteria include (in order of

importance);

Banks are able to provide long-term business relations

Banks are inclined to provide customer’s credit requirements

Bank charges competitive prices for both products and services.

It is evident from the above that large firms hold competitive prices as the most sig-

nificant factors in their criteria indicating that decisions are made at the level of indi-

vidual product. As such, specialist financial service providers may be able to gain

market share at the expense of full service providers if they can provide competitive

prices.

On the other hand, small firms are more desirous of having long-term business rela-

tions with banks which provides banks the opportunity to make use of customer

loyalty to bundle services. Also, small firms are less swayed by the price and are

hence less inclined to search for the cheapest price of any service.

29

In a related study, Zineldin’s (1996) attempted to determine bank selection and cus-

tomers’ perceptions of a bank and the products it offers. He revealed that the factors

impacting functional quality include friendliness, helpfulness, accuracy in account

transaction management, efficiency in rectifying mistakes, speed of service and deci-

sion making – all of these factors were revealed to be critical determinants of bank

selection.

But based on the above results, functional quality is superior to traditional marketing

activities comprising of location, price and advertising. Price competitiveness was

also a less important criterion than speed of service and decision making. On the oth-

er hand, designing a high quality and effective delivery system mix may impact

bank’s competitive edge both in short and long-term. He also added that performance

of contact personnel, word-of-mouth and technological based services may compen-

sate for overall lower factor scores.

Finally, Dusuki and Abdullah (2007) investigated the pertinent factors that customers

of Islamic banks perceive as affecting their selection criteria of banks. They revealed

that the most important factor is customer satisfaction which hinges on quality of ser-

vice by Islamic banks. This includes factors such as, treating customers courteously

and respectfully, conveying trust and confidence, efficient and effective handling of

transactions and inclination and preparedness to provide solutions and answers con-

cerning the products and services offered by the Islamic Banks.

30

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 INTROUCTION

The literature review in the previous chapter indicates the definition of the key terms

of this research and also the conceptual of the research. This chapter covers the re-

search method employed in this study. Research method is defined as techniques that

are used for conducting research such as in data collection, data analysis, and evalua-

tion of the accuracy of the research results (Sekaran, 2003)

3.2 SAMPLE SELECTION

Data was obtained for this study from a simple random sample of bank customers in

the Most Libyan cities without limited to specific city, or specific branch. Sampling is

taking a fraction of a population to represent the whole population but the researcher

only managed to find 150 people to become respondents. Population is a group of

people that can involve in the research. Selection of the population is depending on

the research conducted by the researcher. Respondents for questionnaire were ran-

domly selected from customer who visited the sampling locations during the chose

time intervals, in order to eliminate the sampling frame errors and ensure the repre-

sentation of the population under the study in the sample units. However, Sampling is

taking a fraction of a population to represent the whole population but the researcher

31

only managed to find 249 people to become respondents. Population is a group of

people that can involve in the research. Selection of the population is depending on

the research conducted by the researcher.

Samples are to be made of groups of research. It is a subset or sub-groups in the

population selected. Sample reflects the population selected. Researcher use conveni-

ence sampling as sampling method. Researcher use this method in order to determine

the sample involve in this research. Through this convenience sampling, each cus-

tomer who makes transaction with Islamic banking has equal opportunity to be se-

lected as respondents. They are representing of the populations research. Purposely

researcher chose this method in order to avoid an imbalance in the selection.

3.3 DATA COLLECTION

In data collection process, the researcher obtained the data in primary design. Primary

data is the data collect own by researcher. Primary data is the original data that

created by researcher through interview, questionnaire, experiments or case study.

In this research, the researcher use questionnaire as medium to collect data. There are

twenty six questions answered by all respondents. The questionnaire is dividing by

five parts/sections. Part one consists of questions about your demographic profile;

continue with part two about the service quality, the third part about customer loyalty,

32

the fourth part trust, and the last part about customer satisfaction, In order to evaluate

the effectiveness of this research, researcher use questionnaire as primary resource.

Forming of the questionnaire is to see the relationship between independent variables

that can influence dependent variable.

The questionnaire distribute to respondent is the result by referring from previous re-

search. However, the discussion with supervisor is done from time to time in order to

make sure the validity of the questions. In this research, researcher distributes hun-

dred set of questionnaire to respondent. To make easier to researcher analyze the data,

the researcher use question that in likert form. The likert 1 scale is for strongly not

agree answer, likert 2 scale for not agree answer, likert 3 scale for not sure answer,

likert 4 scale for agree answer and likert 5 scale for strongly agree answer. Every li-

kert represent own value and from that value the researcher can study about what res-

pondent feel and their valuation towards this research.

In questionnaire distribution process, the researcher explained about the definition of

the questions and the purpose of this research to the respondent. The researcher to-

gether with the respondent while they answering the questionnaire. This is to make

sure the questionnaire return back and respondent answering in good.

33

3.4 VARIABLES

In this study the researcher will examine how the independent variables affect the de-

pendent variable. Hence the dependent variable is customer satisfaction, and the in-

dependent variables are Customer Loyalty, Service Quality, and Security.

3.4.1 CUSTOMER SATISFACTION

Customer satisfaction in this study is a dependent variable, Customer satisfaction is

the term most commonly used in trade and industry. But is an expression of the work

explaining this type of measurement of products and services offered by the company

to meet the expectations of its customers. For some, this may be considered the com-

pany's key performance indicator.

Customer satisfaction is one of the important outcomes to marketing activity (Spreng

et al., 1996). In today’s highly competitive banking industry, customer satisfaction is

considered as the essence of success (Siddiqi, 2011). A lot of studies have dealt with

satisfaction of customers or consumers with products or services. Marketing re-

searchers in general agree that satisfaction is response to consumption related expe-

riences (Anderson et al.,1994).

34

3.4.2 CUSTOMER LOYALTY

The study of customer loyalty has long been a topic of interest in the arena of con-

sumer behavior. A number of constructs of customer behavior related to customer

attachment have been developed and explored in marketing, including source loyalty,

customer loyalty, customer involvement, customer commitment, brand sensitivity and

brand commitment. Customer loyalty is considered an important key to organization-

al success and profit (Oliver, 1997). It is more expensive to recruit new customer than

to keep existing customer (Rosenberg and Czepiel 1983). The matter of expenditures

would not be matter as those consumers that demonstrate the greatest levels of loyalty

toward the product, or service activity, tend to repurchase more often, and spend

money. Consequently, a great deal of research attention has focused on the identifica-

tion of effective methods of enhancing loyalty (Lach, 2000)

Oliver (1999) defined customer loyalty as a deeply held commitment to rebuy a pre-

ferred product/service consistently in the future, thereby causing repetitive same-

brand or same brand-set purchasing, despite situational influences and marketing ef-

forts having the potential to cause switching behavior.

35

3.4.3 SERVICE QUALITY

Service quality can be defined as the difference between customers’ expectations for

service performance prior to the service encounter and their perceptions of the service

received (Asubonteng et al., 1996). Gefan (2000) defined Service quality as the sub-

jective comparison that customers make between the quality of the service that they

want to receive and what they actually get. Service quality is determined by the dif-

ferences between customer’s expectations of services provider’s performance and

their evaluation of the services they received (Parasuraman et al.,1988).

3.4.4 SECURTY

In many ways this security of an bank process isn't dissimilar to this security of an

process which usually belongs to help another business corporation. Nonetheless,

people knowing of the requirement permanently computer system security regarding

bank programs can be quite large. Perhaps this consciousness is usually lifted by the

affiliation along with Automated Money Transport, as well as the heavy dependence

and that is located on very large intercontinental personal telecoms systems. Nonethe-

less, seriously isn't the only real programs action throughout bank. Numerous stability

practices tend to be akin to these of another small business corporation. Your security

of bank programs can be incredibly noticeable into a bank customer.

36

3.5 THEORETICAL FRAMEWORK

This study examines the impact of service quality dimensions which are Customer

Loyalty, Service Quality, and Security is stated as independent variables and custom-

er satisfaction is dependent variable. The interaction of variables in the model deter-

mines somehow the effect of service quality on customer satisfaction.

FRAMEWORK OF CUSTOMER SATISFACTION

Figure 3.4 Research Framework

Customer Loyalty

Service Quality

Security

CUSTOMER

SATISFACTION

IV

DV

37

3.6 HYPOTHESIS DEVELOPMENT

Based of framework and the object of study, the hypothesis will be as following:

According to Bidayatul Akmal (2006) who studied the relationship between

customer loyalty and customer satisfaction, it showed that there is a positive

relationship between these variables. Hence this study going to assume:

H1: there is positive relationship between Customer Loyalty and customer sa-

tisfaction in the Banking sector in Libya.

According to Nur Syuhanida (2011) who studied the relationship between ser-

vice quality and customer satisfaction, it showed that there is a positive rela-

tionship between these variables. Hence this study going to assume:

H2: there is positive relationship between Service Quality and customer satis-

faction in the Banking sector in Libya.

According to Abdullah Mohamed (2009) who studied the relationship be-

tween security and customer satisfaction, it showed that there is a negative re-

lationship between these variables. Hence this study going to assume:

H3: there is positive relationship between Security and customer satisfaction

in the Banking sector in Libya.

3.7 STATISTICAL AND ANALYSIS

The basic objective of this study is to test the research hypotheses, based upon the

conceptual framework of this study. This study has used quantitative research ap-

38

proach. The statistical software SPSS version 19 was employed to ensure the relevant

issues is examined in a comprehensive manner.

Both simple and advanced statistical tools and methods are used where appropriate

for analyzing the relationship among the variables in the model. Therefore, usage of

statistical techniques is accordance to commonly accepted research assumptions and

practices. Multivariate statistical analysis is performed to analyze the data of this

study.

The questionnaire divided to four parts. The first part was particular to the DV varia-

ble which “customer satisfaction”, it’s appear six questions which test how the cus-

tomers satisfied with their Banks. The second part was particular to the first IV vari-

able which “customer loyalty”, it’s appear five questions that test the degree of cus-

tomer loyalty for their Bank. The third variable “service quality” has tested by four

questions and the last variable “security” has tested by six questions to determination

its relationship with the customer satisfaction.

3.8 DATA ANALYSIS TECHNIQUE

3.8.1 Description analysis

Descriptive used inferential statistics will be employed. Several statistical validity

tests and analysis will employ such as reliability test, descriptive analysis, correlation

and regressions test to examine the hypothesis in the research framework. The quan-

titative analysis will examine the Customer loyalty related to the service quality.

39

Normality

After looked at the descriptive statistics for the present study data, and before looking

at the coming statistics test, is better to look at whether the data follows a normal dis-

tribution or not, because many of the statistical procedures including correlation, re-

gression, and so on are based on the assumption that the data follows a normal distri-

bution (Zahediasl, 2012). In other words normality test in statistics is used to deter-

mine whether a data set is well-modeled by a normal distribution or not. There are

several tests for the assessment of normality and shape of a data distribution such as

skewness and kurtosis test, which will be used in the present study.

Skewness is the measure of the symmetry of distribution. The normal distribution is

symmetric and has value of zero for skewness. Also has been defined Skewness as a

measure of the symmetry of a distribution. A positive value indicates that the distribu-

tion has a greater tendency to tail to the right (positively skewed or skewed to the

right), and a negative value indicates a greater tendency of the distribution to tail to

the left (negatively skewed or skewed to the left). Skewness is 0 for a normal distribu-

tion (Keller, 2010).

Kurtosis is a measure of the shape of a distribution. A positive value indicates that the

distribution has longer tails than the normal distribution (platykurtosis); while a nega-

tive value indicates that the distribution has shorter tails (leptokurtosis). For the nor-

mal distribution, the kurtosis is 0 (Keller, 2010). As well as kurtosis refers to peaked-

40

ness or flatness of the distribution, so that the high peak data called a Leptokurtic

where the kurtosis value is greater than 3(kurtosis >3). The perfect normal distribu-

tion of the data called Mesokurtic, which as a kurtosis equals 3,while the high flatness

data is called Platykurtic, where the kurtosis value is less than three (kurtosis < 3)

(Bulmer, 1979).

According to Balmer, M.G. if skewness is less than -1 or greater than +1, the distribu-

tion is highly skewed, and if skewness is between -1 and - ½ or between + ½ and +1,

the distribution is moderately skewed, while if skewness is between-½ and +½ the

distribution is approximately symmetric.

Levene's test

Levene’s test are used to check the homogeneity of variances. Levene’s test of homo-

geneity of variances or equality of variances is one of most common, powerful, and

robust tests to non-normality to determine what extent there are significant differenc-

es between different samples. Levene’s test is denoted by the letter F. in other words

the F- test is applied to the absolute deviations of the observation from their group

means (Joseph L. Gastwirth, 2009).

41

Multicollinearity

The F test is used to determine whether there is a significant overall relationship be-

tween the dependent variable and the set of all independent variables, while Multicol-

linearity is used to determine the relationship among the independent variables one

another. In short the multicollinearity refers to the correlation among the independent

variables. Multicollinearity is a problem in multiple regression that develops when

one or more of the independent variables is highly correlated with one or more of the

other independent variables. (David R. Anderson, 2011). The Variance Inflation Fac-

tor (VIF) is widely used measures of the degree of multi-collinearity of the indepen-

dent variable with the other independent variables in regression model. So if the value

of VIF reaches 10 the multi-collinearity regarded as a serious one, if so should reduce

the collinearity by eliminating one or more variables (O’BRIEN, 2007).

3.8.2 Correlation analysis

Correlation, linear and multiple regressions will be use for inferential statistics. The

Pearson correlation will be use to measure the significance of linear bivariate between

the independent and dependent variables thereby achieving the objective of this study.

Multiple regressions will be use to determine the relationship between independent

and dependent variables, the direction of the relationship, the degree of the relation-

ship and strength of the relationship (Sekaran, 2000).

42

Moreover, simple linear regression enables us to find the straight line most appropri-

ate for representing the connection between two sets of observed values. Because the

line that we ‘fit’ to our data can be used to represent the relationship it is rather like

an average in two dimensions, it summarizes the link between the variables (Buglear,

2001)

Basically, a correlation describes a statistical relationship between two variables

based on each observation, in other words, correlation is the extent to which two or

more things are related to one another (C.Reinard, 2006, Mike Allen & Hunt, 2009).

The correlation range is from +1.00 to – 1.00 (both of these values indicate perfectly

correlated variables) thus the values between 0 to – 1.00 which has minus sign indi-

cate to a negative correlation, the meaning of that as one value for a variable increases

the value of the other variable diminishes. On contrast, the positive correlation pre-

sented by the values fall in between 0 to +1.00, the positive correlation indicates that

as one value increases, the value for other variable also increases. Likewise the size of

the correlation value indicates the accuracy of the prediction in the direction indicated

– larger correlations indicate greater accuracy. (C.Reinard, 2006, Mike Allen & Hunt,

2009).

The correlation interpretation guide suggested by Losh (2004) has been used in this

study to describe the relationship between the independent variables and the depen-

dent variables, the association measurements are described as: r =1.0 “Perfect” rela-

43

tionship. 0.76 to 0.99 “Very strong” relationship. 0.51 to 0.75 “Strong” relationship.

0.26 to 0.50 “Moderate” relationship. 0.11 to 0.25” Weak” relationship.0.01 to 0.10

“Very weak” relationship. And 0 “No relationship” (C.Reinard, 2006).

44

3.9 REGRESSION ANALYSIS

The current section will assign for multiple regression test to provide more informa-

tion about the variables relationship whereby the multiple regression can provide it so

that it allows calculating a partial correlation, which is the correlation between a pre-

dictor variable and a dependent variable when holding constant another variable or

variables (Mike Allen & Hunt, 2009). But for multiple regression to work all assump-

tion has already met, in the previous sections.

Multiple regression, is used to analyze relationships between more than two variables,

and non-linear regression, which is used to analyze relationships that do not have a

straight-line pattern (Buglear, 2001).In other word multiple regression analysis is the

study of how a dependent variable Y is related to two or more independent variables

(David R. Anderson, 2011).

45

CHAPTER FOUR

FINDINGS

4.1 INTRODUCTION

The current chapter will be assigned for presenting the findings of the present study,

so that as mentioned earlier; SPSS version 19 will be used to analyze the existing data

using some of the statistics analyses related to the main aim for this study, such as

descriptive statistics, normality, multicollinearity, correlation analysis, linearity and

multiple regression, in order to answer the research objective as well as to test the hy-

potheses that appeared in the chapter three in this study.

4.2 DESCRIPTION ANALYSIS

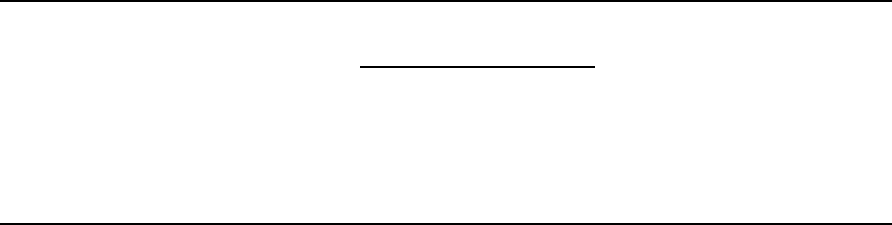

From the Table 4.2 descriptive statistics, the total sample size (n) is 204 respondents.

Customer satisfaction has mean of 3.94 and stander deviation of .25(M= 3.94, SD =

.44). The lowest value was 3.50 and the highest 5.00. Customer loyalty shows mean

of 3.47 and stander deviation of .24 (M=3.47, SD =. 24). The lowest value was 3.00,

and the highest 4.20. Service quality has mean of 3.87 and stander deviation of

.47(M=3.87, SD=.47) the lowest value was 3.00 and the highest 5.00. Security has

mean of 4.08, and stander deviation of .37(M=4.08, SD=.37) the lowest value was

3.00 and the highest 5.00.

46

Table 4.2 Descriptive Statistics

N

Minimum

Maximum

Mean

Std. Deviation

Customer Satisfaction

204

3.50

5.00

3.9469

.25097

Customer Loyalty

204

3.00

4.20

3.4716

.24830

Service Quality

204

3.00

5.00

3.8725

.47180

Security

204

3.00

5.00

4.0843

.37344

From the Table 4.2 the customer satisfaction which represent the independent varia-

ble, it has a highly skewed with 1.588, and highly peak with 3.567 kurtosis as the his-

togram 3.4 shows below. Customer loyalty and service quality which present depen-

dent variables, both of them approximately symmetric with .478 skewness for cus-

tomer loyalty and - .176 skewness for service quality, on the other hand both of them

high flatness (platykurtic distribution) with -.122 kurtosis for customer loyalty and -

.912 kurtosis for service quality as can be seen from the histograms 4.2and 4.4 below.

Whereas the security variable as can be seen from table 4.2 is moderately skewed

with -.758, and high flatness with -.159 kurtosis as shown in the histogram 4.1 Hence,

the assumption of normality has not been violated.

47

Table 4.2 Distribution of data

Variables

N

Skewness

Kurtosis

Customer Satisfaction

204

1.588

3.567

Customer Loyalty

204

.478

-.122

Service Quality

204

-.176

-.912

Security

204

-.758

-.159

Histogram 1.4 Histogram 2.4

Histogram 3.4 Histogram4.4

48

Table 4.3Test of Homogeneity of Variance

Levene

Statistic

df1

df2

Sig.

Customer

satisfaction

Based on Mean

44.935

4

191

.000

Based on Median

18.198

4

191

.000

Based on Median and with adjusted df

18.198

4

73.423

.000

Based on trimmed mean

43.287

4

191

.000

Table 4.3 shows that the significance is smaller than 0.05, which indicates that the

variances are not equal. F (4; 191) = 44.935, 0.000.

Table 4.4: Multicollinearity Analysis

Collinearity

Tolerance

Statistics

VIF

Service Quality

.996

1.004

Customer Loyalty

.433

2.312

Security

.992

1.008

49

As can be clearly seen from the above Table 4.4that there is no multicollinearity is-

sue, whereby the VIF value is less than 10. Hence, the assumption of multicollinearity

has not been violated

4.3 CORRELATION ANALYSIS AND LINEARITY

After checking the present study data by looking at the descriptive analysis then the

normality, homogeneity and multicollinearity, this section will assign for examining

the relationships and linearity between the independent variables and the dependent

variable, using simple linear regression analysis which is the most commonly consi-

dered analysis method, by looking at Pearson Correlation and scatterplot matrix.

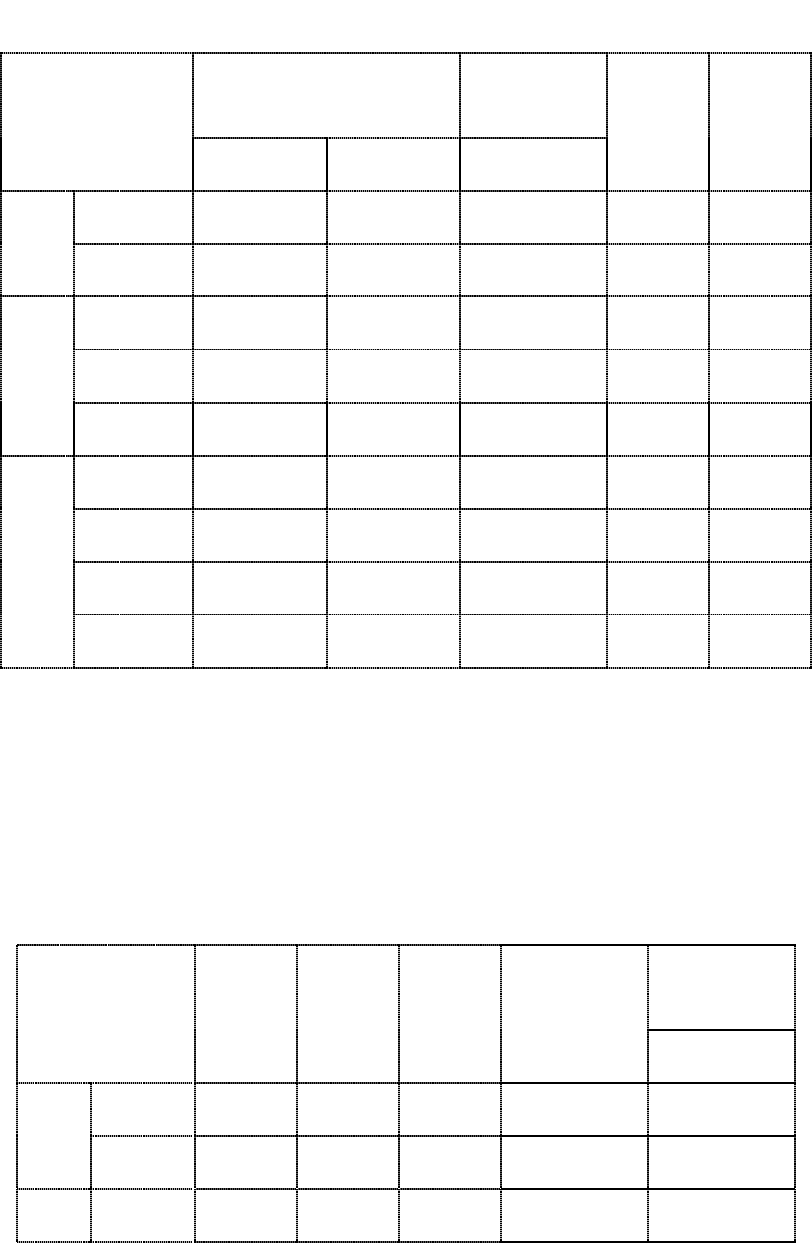

The table 4.5 and figure 4.5 showed that the relationship between customer satisfac-

tion as a dependent variable and customer loyalty as independent variable is a posi-

tive, strong, and linear relationship with a significant statistical correlation(r = .515, p

< 0.01), while the relationship between customer satisfaction and service quality is

positive weak and nonlinear, with a significant statistical correlation(r = .256, p <

0.01). As for the relationship between customer satisfaction and security is positive

very weak and nonlinear also statistically it is not significant (r = .041, p > 0.01).

50

After looked at the correlation between the dependent and independent variables in

the above section, the current section will be assign to look at the relationship among

the independent variables one another.

From the table 4.5 and the figure 4.5 showed that the relationship between the cus-

tomer loyalty service quality and security is negative, very weak and nonlinear with

non-significant statistical correlation (r = -.067; -.091, p > 0.01). While the relation-

ship between service quality and security is positive, strong and linear relationship

with significant statistical correlation (r = .753, p < 0.01).

Table 4.5 Correlations Analysis

Variables

Customer

Satisfaction

Customer

Loyalty

Service

Quality

Security

Pearson

Correlation

Customer Sa-

tisfaction

1.000

.515

.256

.041

Customer

Loyalty

.515

1.000

-.067

-.091

Service Quali-

ty

.256

-.067

1.000

.753

Security

.041

-.091

.753

1.000

Sig. (1-tailed)

Customer Sa-

tisfaction

.

.000

.000

.280

Customer

Loyalty

.000

.

.171

.098

Service Quali-

ty

.000

.171

.

.000

Security

.280

.098

.000

.

51

Figure 4.5 Dependent and independent variables relationships

4.4 ANOVA ANALYSIS

The ANOVA (Analysis of Variance) table below provides us with the inferential test

of each model. In particular, the F and its df (degrees of freedom) are indicators of

how good the model is, as can be seen that all models (1,2 ,3) have a statistical signi-

ficance, which means that every single predictor variable has a significant predictor

of the outcome of the customer satisfaction, with a different degree, but the compen-

sation of all of them it has more effect on the dependent variable which presented as

follow (F=42. 462, df =3, p< .05). Sig. (statistical significance) is a measure of how

52

likely it is that an F this high or higher could have arisen if there was no relationship

in the whole population from which the sample analyzed was drawn.

Table 4.6 ANOVA

d

Sum of Squares

df

Mean Square

F

Sig.

Regression

4.975

3

1.658

42.462

.000

c

Residual

7.811

200

.039

Total

12.786

203

c. Predictors: (Constant), Customer Loyalty, Service Quality, Security

d. Dependent Variable: Customer Satisfaction

Table 4.6 of the multiple regression test lists the variables that used as a predictors.

As can be clearly seen that there are three predictors’ variables (customer loyalty,

service quality and security), and one dependent variable or outcome variable (cus-

tomer satisfaction).

Table 4.7 Model Summary

R

R-square

Adjusted R-

square

.624

c

.389

.380

c. Predictors: (Constant), Customer Loyalty, Service Quality, Security

53

Table 4.7 shows regression model summary includes the R, R-squared and adjusted

R-squared for the model, and the standard error of the estimate. R is the multiple cor-

relation coefficients, its present all the variable together (R = .624). R-squared is a

measure of how much of the variation in the dependent variable is accounted for by

the model, as can be clearly seen from Table 4.7 that R

2

in the model 3 equals

.389(R

2

= .389) explains approximately 38% of variance in customer satisfaction

,which predicted by the combination of the three independent variables . Adjusted R-

squared attempts to adjust this for the complexity of the model. More complex mod-

els will explain more variance than simpler models. Table 4.7 shows the adjusted R

square is 0.38. The adjusted R square shows that 38% of the variance in Customer

Satisfaction has been significantly explained by 1% change in the three independent

variables. The almost same value between R square and the adjusted R square indi-

cates high model fit.

54

4.5 COEFFICIENTS ANALYSIS

Table 4.8 Coefficients

a

Analysis

Standardized Coef-

ficients

t

Sig.

Beta

(Constant)

7.269

.000

Customer Loyalty

.522

9.401***

.000

Service Quality

.519

6.178***

.000

Security

-.303

-3.595***

.000

Note: ***, ** and * denotes significantly at 1%, 5% and 10% level of significant respective-

ly. Dependent Variable: Customer Satisfaction.

a. Dependent Variable: Customer Satisfaction

Table 4.8 shows the coefficients for each model tested. Notice that all models are sta-

tistically significant with p-value less than .05(p < .05) the meaning of that every sin-

gle predictor variable has contribution in the outcome variable.

4.6 DISCUSSION OF RESULT

Table 4.8 shows coefficients analysis to the variables influencing customer satisfac-

tion. The result indicates that a 1% change in customer loyalty leads to 52.2% in-

crease in customer satisfaction. This result suggests that customer loyalty is the major

factor in influencing customer satisfaction. There is a significant and positive rela-

tionship between customer loyalty and customer satisfaction (t- statistic = 9.401,

P<0.01). The positive relationship indicates that the higher the customers loyal are

expected that the bank provide a higher customer satisfaction in respective banks..

Hence, the null hypothesis stated in HX is failed to accept or reject? Customer loyal-

ty as a major determinant has been supported by past studies such as Luiz Moutinho,

Anne Smith(2002). The first hypotheses H1 assume that there is positive relationship

55

between customer Loyalty and customer satisfaction in the banking sector in Libya.

And this hypothesis is accepted.

Customer loyalty refers to the extent of the customer's desire to continue to deal with

the bank and not dealing with the alternatives offered by other banks. This study

shows that there is positive correlated between customer loyalty and customer satis-

faction. The bank customers in Libya prefer transaction with the banks which they

feel it's they belongs.

Likewise, as for service quality the result indicates that 1% change in service quality

leads to 51.9% increase in customer satisfaction. Almost same with customer loyalty,

this result suggests that service quality also has a big influence on customer satisfac-

tion. There is a significant and positive relationship between service quality and cus-

tomer satisfaction (t- statistic = 6.178, p<0.01). The positive relationship indicates

that the higher the service quality is expected that the bank provide a higher customer

satisfaction in respective banks. The second hypothesis assumed that there is positive

relationship between service quality and customer satisfaction in the banking sector in

Libya, so this hypothesis has accepted too.

The hypotheses test of this study confirms that there is positive relationship between

service quality and customer satisfaction. These results imply that when service quali-

56

ty is high, the customer satisfaction will be also high. The results also show that the

customers are satisfied with the quality of service that is provided by banks’ staff.

While security represents that 1% change in security leads to 30.3% decrease in cus-

tomer satisfaction. This result suggests that security has a little influence on customer

satisfaction. There is a negative relationship between security and customer satisfac-

tion with a statistical significant (t-statistic= -3.595. The negative relationship indi-

cates that less security is expected that the bank provide less customer satisfaction in