Customer Satisfaction

Survey 2022

Banking Industry

FEBRUARY 2023

1962-2022

Fresh Frontiers

‘Building customer experience

does not happen by accident.

It is by design’

CLARE MUSCUTT

The Banking Industry Customer Satisfaction Survey (BICSS) is conducted annually by the Kenya

Bankers Association (KBA) in collaboration with the KBA Customer Service Working Group,

whose membership is drawn from the banking sector. The publication seeks to contribute to the

banking industry’s eorts towards enhancing the quality of customer experience. Since its

inception in 2018, the Survey has continued to inform industry strategies towards

customer-centrism and ensuring access to financial services for all.

The 2022 BICSS coincides with the issuance of the ‘KBA Gold Standard of Bank Services in

Kenya’ report in 2023. The report is based on bank customers’ service feedback since the 2018

inaugural edition of the Survey. The handbook outlines minimum service standard expectations

and provides a comprehensive overview of global best practice recommendations on customer

service. It seeks to channel the banking public’s feedback into clear action points towards

embellishing customer service across banking service points besides informing responsive

product design.

Initiated in 2018, the BICSS is part of eorts being spearheaded by Kenya Bankers Association

(KBA) towards enhancing customer experience in the banking industry. Over the years, the

survey has continued to inform industry strategies towards customer-centrism and ensuring

access to financial services for all. This edition aims to build on these industrywide eorts by

addressing emerging needs.

About

this Survey

i KENYA BANKERS ASSOCIATION

In 2022, the Kenya Bankers Association (KBA) celebrated its 60th Anniversary — a Diamond

Jubilee that presented a fabulous opportunity to take stock of challenges and opportunities in

the economy. The commemoration rearmed the industry’s collective commitment to continue

creating innovative solutions towards enhancing the quality of products and services provided to

the banking public.

Importantly, the celebration also oered an occasion to reflect on strategies that can be

leveraged upon to sustain the banking industry’s longstanding vibrant resilience as part of

collective eorts towards deepening sustainable financial inclusion. In the spirit of the KBA 60

th

Anniversary, this Survey is geared towards sustaining the Kenyan banking industry’s resilience—

dating back to 1962— by informing initiatives designed to optimize the banking industry’s

contribution to the national socio-economic development agenda.

Celebrating

60 Years

1962-2022

Fresh Frontiers

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 II

Contents

The entire content of this publication is protected by copyright laws. Reproduction in part or

whole requires express written consent from the publisher. © Kenya Bankers Association, 2023

About this Survey

Celebrating 60 years

Survey Highlights

Foreword

Sampling Methodology

Demographic Distribution

a. Geographical location

b. Age

c. Gender

Multi-banking Trends

Overall Customer Experience

Customer Banking Channel Preference

Preferred Mode of Interaction when

Accessing Banking Services

Promoting Access to Banking services

for Persons with Special Needs

Customer Complaint Resolution

Industry Net Promoter Score

Acknowledgments

i

ii

2

4

5

6

6

6

7

7

8

9

10

11

12

12

14

Survey

Highlights

The 2022 Banking

Industry Customer

Satisfaction Survey

obtained

33,801

responses

compared to 29,791

responses received in

the 2021 Survey.

The distribution of

responses across the

47 counties

remains comparatively

similar, with slight

variations that suggest

increased participation

in the 2022 survey

compared to 2021.

Majority of respondents

(67.8 percent)

cited mobile banking as

their most preferred

banking channel in 2022

Majority of respondents

in the 2022 Survey were

aged between 26 and

35 years, representing

35 percent

of the total survey

responses.

The 2022 Survey showed

a sustained multiple

relationship with banks,

with two or more bank

account holders

accounting for

48.2 percent

Preference for

human-assisted

customer service

increased to

16 percent

from 12 percent

in 2021

In gender distribution,

males accounted for

65 percent

of the total number

respondents.

Foreword

This issue of the Banking Industry Customer

Satisfaction Survey (BICSS) marks the fifth

instalment of industrywide banking sector

customer service evaluation; the first having been

published in the year 2018. Fortuitously, the Survey

was conducted in 2022, coinciding with the Kenya

Bankers Association (KBA) 60

th

Anniversary

celebrations. The two distinctions make the

current report important— providing an

opportunity to set a fresh pace for an enhanced

quality of banking services.

In keeping with that expectation, this report is

based on a refreshed questionnaire that covers

new areas, informed by feedback obtained in its

predecessors. The new areas of focus include the

addition of the Net Promoter Score (NPS), an

important metric that assesses the likelihood of

referral. Widely used by organizations globally

across sectors, the metric is considered eective in

measuring overall customer satisfaction. The NPS

is aimed at providing the industry and individual

banks an additional evaluation tool that will inform

strategies towards service excellence.

The past six decades of banking in Kenya have

been marked with groundbreaking developments,

well interspersed with challenges and lessons. At

the forefront of the challenges and learnings was

the COVID-19 disruption which will, without doubt,

continue to have an enduring impact across

sectors. Beyond the negative eects of the health

crisis, it also served as a launchpad for new

possibilities.

In the realm of customer service, the potential of

technology was reawakened at the onset of the

pandemic in 2020. The role of innovation in

preventing the COVID-19 health crisis from

degenerating into a financial crisis in 2020 and

succeeding years cannot be gainsaid. Customers

continued to access banking services without

having to visit banking halls in light of restricted

movement meant to contain the spread of disease.

I would like to commend the banking industry for

the sustained foresighted innovation. Although

COVID-19 was an unanticipated risk, banks’

customer service teams demonstrated responsive

leadership. On behalf of the banking industry, I

take this opportunity to extend gratitude to the

customer service teams for creatively leveraging

on technology to forestall service disruption and at

the same time maintaining service standards.

However, some challenges persist, especially in the

area of facilitating satisfactory experience for

Persons with Disability. Based on this report’s

findings, there is a need to redouble eorts

towards ensuring independent access to banking

services for this important segment of the banking

public. I am pleased to note that out of 93 percent

of customers with special needs were able to

access banking services. However, 13 percent of

the customers surveyed reported having

diculties accessing financial services

independently.

In response to this challenge, it is gratifying to

note that over 30 banks are in the course of

implementing a harmonized banking industry

accessibility roadmap that seeks to address

accessibility challenges. It is the ambition of KBA

to continue supporting member banks to fully

implement the measures by the close of the year

2024.

Customer service is among the most challenging

aspects of banking. This distinction owes to the

fact that the banking public’s needs and

expectations keep evolving. It is, therefore,

incumbent upon the banking industry to keep

abreast with these dynamics as part of eorts to

deepen financial inclusion.

I have no doubt that this report is an important

ingredient to the attainment of the banking

industry’s Strategic Plan, whose aim is to facilitate

access to aordable financial services through

responsive innovation.

Dr. Habil Olaka, EBS

Chief Executive Ocer

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 04

Using a questionnaire developed by the Kenya Bankers Association Customer Service Working

Group, both quantitative and qualitative information was collected. In 2022, a total of 33,801

responses were received, compared to 29,791 responses in the 2021 survey. Out of the sample, 13.8

percent representing 4,677 persons, are those with special needs (i.e., braille, ramp, screen reader,

voiced aid).

This is an annual survey conducted online

using SurveyMonkey© survey tool. Its main

aim is to evaluate the quality of customer

service oered by the banking industry in

Kenya by obtaining feedback from the

banking public on various aspects of

customer experience. The survey is based on

a simple random sampling technique owing

to the approach’s strengths:

i. It reduces the possibility of systemic

errors and minimizes sampling biases.

ii. The approach produces a representative

sample, ensuring generalizability of

inferences drawn therein to population of

bank customers.

Sampling

Methodology

33,801

RESPONSES

IN 2022

01

05 KENYA BANKERS ASSOCIATION

Geographical distribution of the 2022

KBA customer satisfaction survey

responses

Figure 1

Mombasa

Nakuru

Kiambu

Nairobi

44.4%

6.4%

5.7%

4.1%

Age distribution of the survey responsesFigure 2

1%

15%

3%

6%

14%

25%

37%

Under 18yrs

18-25yrs

26-35yrs

65

+

yrs36-45yrs

46-55yrs

56-65yrs

Demographic

Distribution

02

A) GEOGRAPHICAL LOCATION

Access to banking services remains

geographically concentrated. In 2022, those

accessing most of their banking services in

Nairobi stood at 45 percent compared to 50.7

percent in the 2021 Survey while those

accessing them from Mombasa stood at 6.4

percent, and those accessing banking services

in Kiambu and Nakuru stood at 5.7 percent and

4.1 percent respectively (Figure 1). These

trends mirror the distribution of financial touch

points, especially the branch network of the

banking sector

1

. That said, the distribution of

the responses across the 47 counties remains

comparatively similar to the trends observed in

the 2021 Survey, however, slight variations in

the number of responses exist, suggesting that

there has been increased participation by the

banking public in the survey across the

counties.

B) AGE

Most of the bank customers surveyed were

aged between 26 – 35 years, which accounted

for 37.3 percent survey responses, 24.8 percent

were aged between 36 – 45 years, 14.6 percent

were 18-25 percent, while those aged 46-55

accounted for 13.8 percent while those aged

55-65 years accounted for 6.15 percent of the

responses. Under 18 and those above 65 years

accounted for 0.7 percent and 2.5 percent

respectively. While there are slight variations in

the distribution of responses by age in the

2022 Survey, it mirrors the trends observed in

2021.

2

CBK Annual Bank Supervision Report 2021

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 06

03

Multi-banking

Trends

Multiple bank relationships, herein referred to as

the maintenance of more than one bank account

in dierent banks is becoming a predominant

feature. In 2022, one-bank account holders

stood at 45.3 percent which is in line with the

findings of the 2021 FinAccess survey which

revealed that 44.1 percent of Kenyans use

banking services. The ownership of two or more

accounts stood at 48.2 percent which is a

reduction from the 62 percent in 2021. Those

holding between four and five accounts

accounted for 5.8%, while only 0.7 percent of the

respondents held more than six bank accounts.

The multiple bank relationships are not unique

though to the Kenyan context but is a consistent

feature across the globe where it is observed

that customers deal with more than one bank.

Gender distribution of the survey

responses

Figure 3

Trends in multi-bank account

ownership

Figure 4

C) GENDER

In terms of the distribution by gender, males

accounted for 65. 2 percent while females

accounted for 35 percent of the responses, a

trend that compares with the 2021 survey,

where 65.6 percent of the respondents were

male, and 34.4 percent were female.

1%

6%

48%

45%

1 bank account

2-3 bank accounts

4-5 bank accounts

6

+

bank accounts

Female

Male

65%

35%

KENYA BANKERS ASSOCIATION07

ABC Bank

Overall Customer

Experience

04

Based on customer experience ranking, respondents were asked to rank on a scale of 1 to 5 their

overall experience with the main bank, and the respondents’ views are resoundingly positive. For

instance, ninety-six (96.5) percent of the respondents rated their customer experience with their

banks above three (3). For instance, 50.70 percent of the respondents rated their customer

experience with their main banks at five (5), being the highest rating. In addition, 35.4 percent

rated it at four (4) and 10.4 percent rated their customer experience at three (3).

Top Overall

Tier 01 Tier 02 Tier 03

In the 2022 Survey, respondents were asked to rank which bank oers the best overall

customer experience and the feedback is as tabulated below.

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 08

Customers’ rating of their bank’s customer experience

Figure 5

50.70%

of respondents

rated their customer experience

with their main banks at five, being the

highest rating

05

Customer Banking

Channel Preference

Channels leveraging on technology are emerging to be the most preferred banking channels with

mobile banking emerging top. In 2022, 67.8 percent of the Survey respondents preferred mobile

banking, a trend that gained traction with onset of COVID-19 and continues to stay elevated

which is consistent with the 2021 FinAccess survey findings that found mobile banking usage

also increased between 2019 and 2021. Preference for Internet or online banking is also on the

rise with 23.3 percent of the respondents expressing preference for it. Moreover, the preference

for branch banking came in third at 17.6 percent and ATMs fourth at 16.9 percent while both

agency banking and card payments or touchpoints came in fifth at 6.1 percent . only 2.1 percent

of the respondents expressed preference for cash depositor machines. Compared to 2021,

preference for digital channels has accelerated; for instance, in the 2021 Survey, 58.7 percent of

the respondents preferred mobile banking, and 20.3 percent expressed preference for internet or

online banking.

50.70%

1.46%

2.04%

10.42%

35.39%

09 KENYA BANKERS ASSOCIATION

Bank Agent/

Agency Banking

6.06%

Bank Branch

17.64%

ATM

16.85%

Mobile Banking

67.83%

Internet Banking/

Online Banking

23.33%

Cash Depositor

Machines

2.04%

Card Payments

(Online/Point of Sale)

6.14%

Customers’ preferences of banking channels

Figure 6

67.83%

of respondents

cited Mobile

Banking

as their

topmost preferred

banking channel

45%

06

Preferred Mode of Interaction

When Accessing Banking Services

There has been a steady growth in the last

four years of bank customers preferring fully

automated or self-service modes (including

Mobile, Internet and Chatbots), when

accessing banking services. In 2022, 45.6

percent preferred this mode of interaction,

compared to 46.7 percent in 2021 and 43

percent in 2020. Some 15.5 percent of the

respondents preferred human-assisted

service (including Call Centers and

Branches), compared to 12.8 percent in 2021

and 16 percent in 2020, denoting a reversal

of the downward trajectory. Those who are

indierent to the use of either slightly

declined to 38.9 percent in 2022 compared

to 40.5 percent in 2021 and 40 percent in

2020.

Preferred Mode of Interaction

When Accessing Banking Services

Figure 7

39%

16%

Either is fine

Human-Assisted Service

(including Call Centers and Branches)

Fully Automated / Self-service

(including Mobile, Internet, Chatbots)

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 10

Access to bank services for Persons with Special Needs

Figure 8

Promoting Access to Banking services

for Persons with Special Needs

07

Banking services must be adaptable to the

needs of all, and customers with special needs

should be able to access the same financial

services as customers without special needs.

From the 2022 survey, 13.8 percent of the

respondents needed special accommodation

(e.g., braille, ramp, screen reader, voiced aid)

to access banking services. Out of the

respondents’ 93.5 percent were able to use

the banking services (e.g. Mobile banking and

online banking) independently, a significant

improvement from the 2020 and 2021 level

where 78 percent and 81 percent, respectively,

could access services independently. However,

6.5 percent of customers with special needs

reported requiring support in accessing

banking services. This highlights the need for

the banking industry to enhance eorts

towards ensuring independent access to

banking services for customers with special

needs.

That said, majority (70.1 percent) of customers

do not intend to switch to another bank that

provides them with accessible services

independently compared to 29.9 percent that

do. These findings are inspiring and

demonstrate the commitment of the banking

industry to improve the financial services and

ensure inclusion of all customers regardless

their conditions, which aligns with the

industry’s commitment to making banking

work for everyone as envisioned in the report

on “A Roadmap for Digital Accessibility and

Financial Inclusion of People with Disabilities.”

YES

NO

13.8%

86.2%

Need Special Accommodation to Access Banking Services

(e.g. braille, ramp, screen, reader, voiced aid)

YES

NO

93.5%

6.5%

Able to Use the Banking Sevices Independently

(e.g. mobile banking and online banking independently)

YES

NO

29.9%

70.1%

Intent to Switch to Another Bank that Provides you with Accessible Services Independently

KENYA BANKERS ASSOCIATION11

Customer complaint resolution by banks

Figure 9

Customer Complaint

Resolution

08

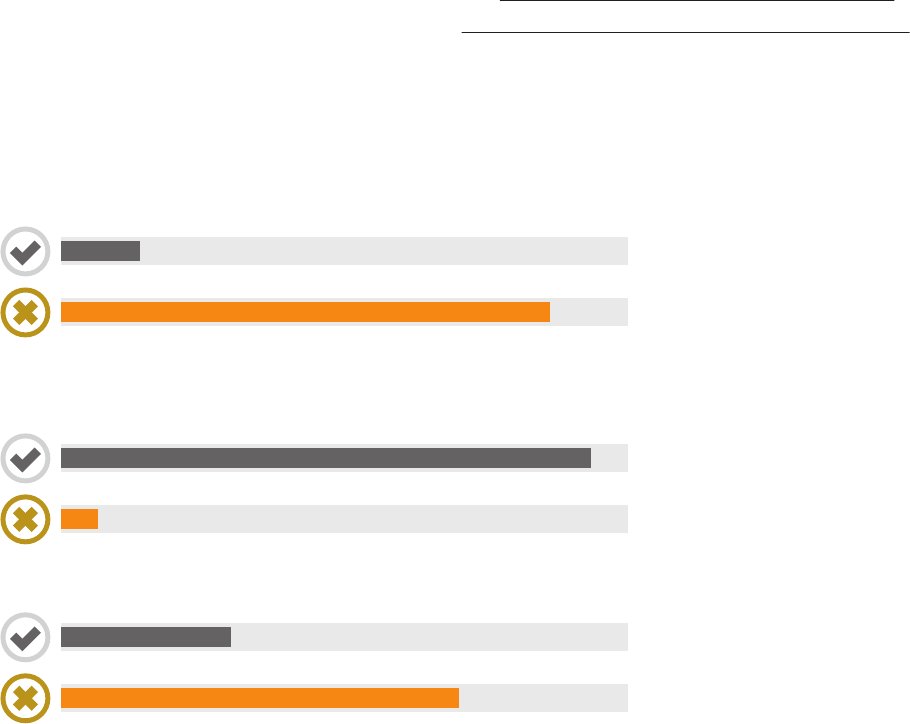

Most of the respondents, at 68.9 percent

indicated that their banks were always able

to respond to complaints within two days of

the complaint being raised. This is against 74

percent recorded during the 2021 Banking

Industry Customer Satisfaction Survey

(BICSS). Some 23.5 percent of the

respondents in 2022, compared to 20

percent in 2021, indicated that their banks

respond to complaints within two days,

sometimes, denoting the need for clear

Service Level Agreements (SLAs) and strict

adherence to the same, among banks that fall

in this category.

Industry Net

Promoter Score

09

In an increasingly competitive banking climate, customer loyalty is more important than ever. As

banks continue to face increased competition among each other and from emerging FinTechs,

the need for customer retention and acquisition, that is the ability of its customers to

recommend it to their close associates has become so important. In the 2022 survey, unlike in

the previous editions of the BICSS, respondents were asked the question “On a scale of 0-10,

with 10 being the highest, what’s the likelihood that you would recommend us (our bank) to a

friend or colleague?” The response to this question is used to compute the Net Promoter Score®

(NPS)

2,3

, a crucial metric of assessing how likely it is for customers to refer others to a given

brand or even products and services.

2

Since its 2003 debut, NPS has been used by companies of all sizes in a variety of industries, and its eectiveness comes

from its ability to measure the overall satisfaction of a customer base.

3

The NPS score is calculated in the following ways. First, the responses are divided into three categories namely

promoter, passive, and detractors. Second, obtain a count of the number of promoters and detractors in the total number

of responses. Third, obtain the proportion of promoters and detractors to the total responses and subtract the

percentage of detractors from the percentage of promoters. The resulting number, whether positive or negative, is your

NPS score. Notably, the passives are left out of the NPS calculation because they are unlikely to recommend or not

recommend.

3.05%

4.49%

68.93%

23.52%

Always

Sometimes

Rarely

Never

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 12

Net promoter score of the banking industry

Figure 10

Based on the responses obtained, 55.8 percent of the respondents are promoters

4

, 27.5 percent

of the respondents are passive

5

while 16.7% are detractors

6

. Given these trends, the industry’s

standing especially from a promoter’s standpoint is impressive as research shows that the

lifetime value of a promoter is 2.5 times higher than that of a detractor, while detractors are 2.3

times more likely to switch to another financial organization compared to a promoter. More

importantly, research has shown that a higher net promoter score (NPS) correlates positively

with revenue. For instance, according to a study published by the London School of Economics

entitled “Advocacy Drives Growth”, an average NPS increase of 7 percent correlates on average

with a 1 percent growth in revenue.

4

Promoters are respondents who answer with a 9 or 10 and are the most loyal of customers whose enthusiasm for the

bank translates into actual recommendations to family and friends.

5

Passives are respondents who answer with a 7 or 8, and are largely indierent, and therefore are disinclined to share

either negative or positive reviews with others.

6

Detractors are those respondents who answer the question with a 6 or lower; these respondents are unsatisfied

customers who could actively harm the bank’s brand by making their complaints public.

Detractor

Passive

Promoter

Promoter

Detractor

Passive

55.8%

39

16.7%

27.5%

13 KENYA BANKERS ASSOCIATION

The Kenya Bankers Association wishes to express its sincere gratitude to

the KBA Customer Service Working Group for playing an important role in

conceptualizing the research upon which this Survey is based. We extend

gratitude to the KBA member banks for sharing the survey across

platforms. We gratefully acknowledge the thousands of bank customers

across the country who continue to provide feedback since the Survey’s

inception in 2018. Data review, analysis and compilation of the report was

led by Palm Consulting Services, supported by Josea Kiplangat,

supported by Christine Onyango, and Hesborn Nyakundi-Nyagaka from

the KBA Secretariat. It has been designed by Sabinga Brand Design Ltd.

Acknowledgements

BANKING INDUSTRY CUSTOMER SATISFACTION SURVEY 2022 14

www.kba.co.ke