1

Ensuring Customer Satisfaction in Banking Sector through Service Quality –

A Study with Reference to Select Branches of State Bank of India

Sangita Maji

Guest Lecturer

Sarojini Naidu College for Women

e-mail: maitysangita090@gmail.com

Bappaditya Biswas

Assistant Professor

Department of Commerce

University of Calcutta

e-mail:aditya_2582@rediffmail.com

Abstract: The banking industries are facing a rapidly changing market, new technologies,

economic uncertainties, increasing competition, and especially more demanding customers. The

income and business growth of the banks depends on loyal and satisfied customers. As a result,

in today‟s competitive environment, banks are continuously trying to retain their existing

customer and attract new customers by providing better quality services. The objectives of the

study are (i) to understand the concept of service quality and customer satisfaction, and to

examine the relationship between them and (ii) to appraise the level of service quality and

customer satisfaction in select branches of State Bank of India. Primary data have been collected

through a structured questionnaire by direct interacting with 110 banking customers of SBI from

different areas of Burdwan district. Bar chart, cross tabulation, Chi-square test, etc. have been

used for interpreting the data. The study found that the service quality of SBI bank is not so

satisfactory in Burdwan district. The study suggests that the banks should increase their number

of ATMs, cash counting machines, and number of front desk employees to improve their quality

of services.

Key-words: Service Quality, State Bank of India, SERVQUAL Model, Tangibility, Reliability.

2

1. Introduction

Banking, an important segment of the service sector, plays a very crucial role in the economic

development of every country. In these days of intense competition, the banks are very

particular in identifying the needs of their customer and how effectively that can be met. They

continuously struggle and develop new strategies to differentiate

themselves from their competitors by providing their customers with high

quality banking services and high technology innovative products.

Although, banking sector of India has been improved gradually for the last two decades. But it is

also facing lot of challenges and difficulties such as, increasing customer‟s demand and

awareness, increasing competition, growing population, etc. Beside these, another important

challenge that the sector is facing is technological changes. As the sector is growing fast, a

number of new private banks have emerged. Therefore customers are getting many options for

selecting their suitable financial service provider. Due to increasing customer awareness, they

would select those particular banks that can provide standard services and fulfill their

expectation. In the Indian scenario, where all banks offer almost similar products and services,

need based efficient customer service and the service quality can differentiate a bank.

So, to ensure customer satisfaction the banks have to improve their service quality, as service

quality and customer satisfaction are interrelated to each other. It means if banks provide

service as per customer‟s expectation then only the customers will be satisfied. As a result, to

cope up this changing market condition banks have to retain old customers and have to attract

new customers by providing better quality of services.

2. Review of Literature

Several studies have been conducted by the academicians and researchers on different aspects

of service quality and customer satisfaction of banking sector. Few of them are summarized

below:

Oppewal and Vriens (2000) used SERVQUAL model to find out the dimension which yield

maximum improvement in bank‟s utility among different dimension such as different service

attributes, strategically important service dimensions, and overall preference for banks or

banking products. Chinwuba (2013) measured the customer perceived service quality and their

3

satisfaction level by using SERVQUAL model through the help of 117 respondents. They found

that assurance, empathy and responsiveness dimensions have positive relationship between them

and no significant effect on customer satisfaction and there was a negative relationship and no

significant impact between reliability and customer satisfaction. But the dimension tangibility

has significant positive relationship with customer satisfaction.

Sheetal et.al (2004) attempted to examine the role of nature of service in knowing the order of

importance of service quality dimension and found out that tangibility is least important and

empathy is second least important in banking service marketing. Agarwal (2009) observed that

the customers are influenced in their usage of e-banking services by the kind of account they

hold, age, profession, etc. The study clearly emphasizes the need for banks to understand that

the financial products and services supplied over the Internet must not only be tailored to fulfill

wants, preferences, security and quality expectations of customers at the present time, but also be

required to induce customers to demand and use e-banking on a wider scale in the future. Siddiq

(2011) attempted to identify the interrelationships and critical factors between service quality,

customer satisfaction and customer loyalty in retail banking sector in Bangladesh. He found that

all the service quality attributes are positively related to customer satisfaction and customer

loyalty in the retail banking sector. Empathy demonstrates the highest positive correlation with

customer satisfaction and tangibility shows the least positive correlation with customer

satisfaction. Jani (2012) identified relative important factors affecting the areas of strength and

weaknesses of public and private sector banks in terms of different technologies offered to

customers and future growth of e-channels in retail banking. The result revealed that use of

technology inferred a positive perception of customers of public sector and private sector banks.

Vasantha and Rani (2011) have analyzed the practicality of determining the retail service quality

opinions and its effect on demographic aspects in Bangalore city. Findings of this study

delivered guidelines regarding enhancement of service offerings by various organizations and

effort to provide a primary understanding on the direction of the customer‟s opinion about the

service quality in retail banking.

Haidar and Islam (2011) determined the importance of perceived service quality factors of

private commercial banks (PCB) in Bangladesh. Sample size of this study was 300.The results

revealed that tangibility is the most important factor in determining the service quality followed

4

by reliability, empathy, accessibility and assurance. Rahaman et al. (2011) conducted the study

on Bangladesh to measure service quality of PCBs on expectation and perception of customers

regarding the services on diverse five dimensions. Authors concluded that three factors were

responsible in determining service quality gaps viz. reliability, responsiveness, and assurance.

The results revealed that the gap existed between perceived services and customers‟ expectation

in PCBs which implies that customers were not satisfied with the services provided by private

sector banks.

Shanka (2012) made an on working mechanism of private banks on Ethiopia. By using

SERVQUAL model, author found out that empathy and responsiveness play a important role in

customer satisfaction level and the author also concluded that providing excellent service

increases the customer satisfaction and customer loyalty. Muyeed (2012) conducted a study in

Bangladesh to examine the service quality in retail banking by taken the sample size 250

respondents of public and private sector banks. The author found that customers are highly

satisfied in prompt and accuracy in transaction but less satisfied in the service of modern

equipment of the bank. Mary (2014) conducted a study in Chennai city and the study found out

that the customers in private sector banks are more satisfied than customers of public sector

banks. There exists a strong relationship between expectation level of the customer and level of

satisfaction and customer loyalty in banking sector.

3. Objectives of the study

The main objectives of the study are as follows:

To understand the concept of customer satisfaction and service quality, and to examine

the relationship between them.

To appraise the level of service quality in select branches of State Bank of India.

4. Database and methodology

Database

The study is both exploratory and empirical in nature. The explorative part of the study is

based on the existing literature on the subject including books, journal, articles, etc. The

empirical analysis in the study has been done on the basis of primary data which have been

collected through field survey as mentioned below.

Methodology

5

For appraisal of service qualities and customers satisfaction in the banks, SBI bank has been

selected as it is the largest public sector bank in India. Three semi-urban branches of SBI

bank from different area of Burdwan district have been considered for collection of primary

data on the basis of convenient sampling method. The selected branches of SBI are; CAC

Burnpur Branch, Rupnarayanpur Branch and Niyamatpur Branch.

The information related to quality of services has been collected through a structured

questionnaire by direct interaction with 110 customers of SBI bank from the three selected

semi-urban branches. The questionnaire is based on SERVQUAL Model which was

developed by Zeithmal, Parsuraman and Berry in the year of 1988. For appraising the service

quality of the selected banks, five parameters of service quality have been used from this

model. The parameters are; tangibility, reliability, responsiveness, assurance and empathy.

Simple percentage, cross tabulation, bar charts, pie charts and Chi Square tests have been

used to present and interpret the data.

5. Customer Satisfaction

The dictionary meaning of „customer‟ is a person who buys goods and services. So, customer

services involve three entities i.e., seller, buyer and goods/services. Customer service is,

therefore, encapsulation of all these entities for the mutual benefits so as to increase the value of

all the participants in the process of buying and selling.

As per Reserve Bank of India‟s (RBI) definition, the customer of a bank may include:

A person or entity that maintains an account and/or has a business relationship with a

bank;

One on whose behalf the account is maintained (i.e. the beneficial owner);

Beneficiaries of transactions conducted by professional intermediaries, such as, stock

brokers, Chartered Accountants, solicitors, etc., and

Any person or entity concerned with a financial transaction, which can pose significant

reputational or other risk to the bank, e.g., issue of a high value demand draft as a single

transaction.

The Talwar Committee (1977) deserved that the main purpose of banking is “to create and

deliver customer – needed services in a customer satisfying manner”. This implies that there are

two elements that are required for the banking services, viz., creating and delivering services.

6

While creation indicates the creation/introduction of new technology in services, carrying out

these services effectively constitutes the delivering of services. These two elements greatly

determine the level of satisfaction of the customers.

According to Kotler and Keller (2009), “customer satisfaction is a person‟s feeling of pleasure or

disappointment resulting from comparing a products perceived performance in relation to his or

her expectation.” Rao (2008) draws the basic formula of customer satisfaction,

Customer satisfaction = Customer perception of the service received - Customer expectation of

service.

In this way it is easy to generalize that if the perception of the service received exceeds the

expectation of the service, customer‟s satisfaction will be positive. On the other hand if the

perception of the service received is less than the level of expectation of the service, it would

lead to customer dissatisfaction. But customer satisfaction is highly effected by the other factors

like experience, purchase decision, service provider, price, etc. There is a substantial body of

empirical literature that establishes the benefits of customer satisfaction for firms. It is well

established that satisfied customers are key to long-term business success. Companies that have a

more satisfied customer base also experience higher economic returns. Consequently, higher

customer satisfaction leads to greater customer loyalty; which in turn leads to higher future

revenue.

Indian banking industries is facing various kind of ups and downs in the current scenario. There

are some specific reasons like lowering of entry barriers, increasing product line of banks and

non-banks, etc. Since the financial reforms, bank are also facing huge competitive pressure

therefore it is inevitable for the banks to maintain loyal customers based, besides banks are trying

to make strategies towards customers satisfaction and loyalty through improved service quality

to achieve and improve their marker and profit position.

6. Service Quality and its Different Models

A service is an act or performance offered by one party to another. They are economic activities

that create value and provide benefits for customers at specific times and places as a result

bringing desired change. It can be said that service is a transaction where no physical goods are

transferred. Service quality means a form of an attitude, related but not equivalent to satisfaction

that results from the comparison of expectation with performance. The customers generally use

7

certain criteria to evaluate service quality by examining reliability, responsiveness, assurance,

empathy and physical aspects. The aim of providing quality services is to satisfy customers.

Measuring service quality is a better way to dictate whether the services are good or bad and

whether the customers will or are satisfied with it.

According to business dictionary “Service quality means an assessment of how well a delivered

service conforms to their client‟s expectation”. Reeves and Bednar (1994) defined service quality

as excellence, value, conformance to specifications and meeting or exceeding customers‟

expectations. Service quality is defined as the degree of discrepancy between customers‟

normative expectations for service and their perceptions of service performance (Parasuraman et

al., 1985). Customer always wants good services from their service provider. But from above

definition we can say that delivered service will become as the quality service if it meets the

customer expectation. But customer expectation depends on his perception which varies from

person to person. So service quality is a comparison between perceived expectation of a service

and perceived performance of a service. As per Parasuraman, Zeithmal and Berry (1985) the

service quality may be expressed as:

Service quality=Perception - Expectation

Therefore if the customer gets same services as they expect then difference will be zero, we can

say service quality is very good. If the customer does not get the expected services then service

quality is bad. Customer perception depends on various factors like age, gender, occupation,

technological changes, etc. which again influence the service quality.

Service Quality Models

Numbers of service quality model have been developed by different researchers around the

world like Gronroos model, GAP Model, Attribute Service Quality Model (Haywood-Farmer,

1988), Alignment Model (Berkley and Gupta 1994), SERVPERF Model, and SERVQUAL

Model. Among these SERVQUAL model is one of the popular model that has been used

globally for measuring service quality of different institutions including banking sector. In this

study we have applied SERVQUAL model for measuring the service quality and customer

satisfaction among the selected customers of State Bank of India.

SERVQUAL is a well-known multidimensional research instrument for measuring and

evaluating service quality in any service sector. This model perfectly covers the dimensions that

8

are considered by a customer in evaluating quality of service in a service sector. The objective of

this survey instrument is to determine the value that the service sector is currently delivering to

the customers and the value that the customer expects. The SERVQUAL model of measuring

the scale of quality in service was developed by Valerie Zeithaml, Parasuraman and Len

Berry in 1985. In this method data are collected via surveys of a sample of customer. In

these surveys the customer responds to series of questions based around a number of key

service dimensions .The methodology was originally based around 5 key dimensions. The

questionnaire consists of matched pairs of items; 22 expectation items and 22 perceptions items,

organized into five dimensions which are believed to align with the consumer‟s mental map of

service quality dimension. The 5 dimensions that are used in this model are:

Reliability: The ability to perform the promised service dependably and accurately.

Assurance: The knowledge and courtesy of employees and their ability to convey

trust and confidence.

Tangibles: The appearance of physical facilities, equipment, personnel and

communication materials.

Empathy: The provision of caring, individualized attention to customers.

Responsiveness: The willingness to help customers and to provide prompt service.

7. Relation between Customer Satisfaction and Service Quality

Customer satisfaction and service quality are inter-related. The higher the service quality, the

higher is the customer satisfaction. Many agree that in the banking sector, there are no

recognized standard scales to measure the perceived quality of a bank service. Thus, competitive

advantage through high quality service is an increasingly important weapon to survive. As a

process in time, service quality takes place before, and leads to overall customer satisfaction.

Service quality has been found to be an important input to customer satisfaction.

Service quality is one of the important areas of business especially for service industries like

bank to retain their customer and to attract new one. Poor customer service could cause a

banking business loss of millions of dollars and also „its credibility‟. Good customer service and

service quality is what attracts people to a business. When customers are pleased they become

long-term assets of the bank. Building strong customer relations can tie a customer and a

business together. When customers are satisfied they feel well treated and are willing to treat the

9

business well. Perfect and smiley customer service definitely improves customer satisfaction.

From the customer‟s perspective service quality significantly influence customer satisfaction and

customer satisfaction has direct influences on purchase intentions.

Some researchers have found empirical supports for the view of the point mentioned above;

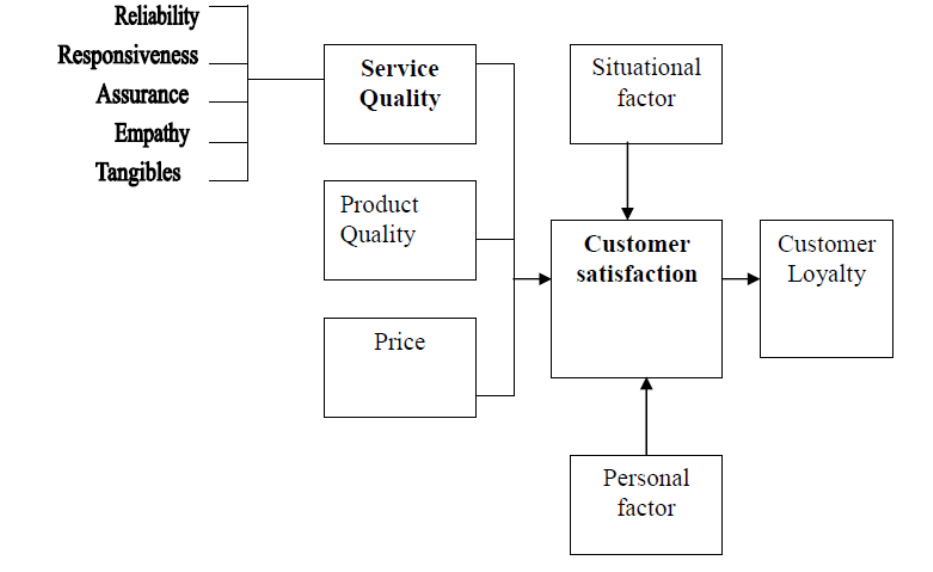

where customer satisfaction came as a result of service quality. As said by Wilson et al. (2008),

service quality is a focused evaluation that reflects the customer‟s perception of reliability,

assurance, responsiveness, empathy and tangibility while satisfaction is more inclusive and it is

influenced by perceptions of service quality, product price and quality, also situational factors

and personal factors. The relationship between service quality and customer satisfaction is

becoming crucial with the increased level of awareness among bank customers.

Exhibit 1: Customer perception of quality and customer satisfaction

(Source: Wilson et al., 2008)

10

8. Appraisal of Service Quality and Customer Satisfaction in SBI Bank

In this section for appraising the service quality, three branches of SBI bank have been

considered from semi-urban areas of Burdwan district. The information related to quality of

services has been collected through direct interview with the 110 customers of SBI by filling up

the questionnaire.

8.1.Demographic Profile of the Respondent

The demographic profile of the respondents are summarized below:

a. Branch wise distribution of the Customers

The Table 1 in below shows that 45.50% respondents are from Rupnarayanpur branch, 32.70%

are from CAC Burpur branch and remaining from Niyamatpur branch.

Table 1

SBI BANK- NAME OF THE

BRANCH

NO. OF CUSTOMER

PERCENTAGE

CAC Burnpur branch

36

32.70%

Rupnarayanpur branch

50

45.50%

Niyamatpur branch

24

21.80%

Total

110

100%

(Source: Field survey by the Researcher)

b. Gender of the Respondents

Exhibit 2: Gender wise distribution of the customers

(Source: Field survey by the Researcher)

Exhibit (2) indicates that for SBI bank (80%) most of the respondents are male.

MALE, 80

%

FEMALE,

20%

11

c. Educational qualification of the Respondents

Exhibit 3: Educational qualification of the Respondents

(Source: Field survey by the Researcher)

Exhibit (3) shows that most of the customers are „12 th‟ pass (49.50%) and „graduate‟ (30.40%),

and few are „primary level educated‟ and „eight pass‟ and Post Graduate (PG) and Professional.

e. Type of account selected by the Respondents

2.70%

1.80%

10.90%

49.50%

30.40%

4.70%

12

Exhibit 4: Type of account selected by the customers

(Source: Field survey by the Researcher)

From the above Exhibit (4) it can be said that most of the respondents (70.90%) have only

Savings Account with SBI and very few of them have Current Account (0.90%) and Fixed

Deposit Account (1.80%). 16.40% of the respondents have both Saving and Fixed deposit

Account.

8.2.Analysis of the Service Quality and Customer Satisfaction by using SERVQUAL

Model

In this section, we have analysed the primary data collected from 110 customers of three

branches of SBI bank through questionnaire designed on the basis of the five parameters of

SERVQUAL model. We have collected the customer‟s feedback in five point likert scale

regarding their satisfaction level out of the services provided by SBI to examine the customer‟s

satisfaction in regards to the quality of services. Chi-Square tests have been done to compare

between the desired level and perceived level of satisfaction of the respondents regarding the five

parameters. The findings of the analysis have been summarized below:

a) Tangibility

Savings

A/C

Current

A/C

Recuring

deposit

A/C

Fixed

deposit

A/C

Savings

and

Recuring

deposit

A/C

Savings

and

Recuring

deposit

and Fixed

deposit

A/C

Savings

and Fixed

deposit

A/C

70.90%

0.90%

0.0%

1.80%

4.50%

5.50%

16.40%

13

For collecting the information regarding the „Tangibility‟ or physical infrastructure of the bank

eleven (11) sub-parameters or questions were set up. The findings are as follows:

(i) Sub-parameter - 1: Availability of sufficient number of counter in the Banks

Availability of sufficient numbers of counters in the banks is an important factor of service

quality. A Chi-Square test has been done to examine whether there is any significant difference

between the desired level and perceived level of the customers regarding the availability of

sufficient number of counters in the banks.

Chi Square test

Hypothesis -1

Ho – There is no significant difference between desired level and perceived level regarding

sufficient number of counter available in the branches.

H1 – There is a significant difference between desired level and perceived level regarding

sufficient number of counter available in the branches.

Table 3 and 4 describe the table of cross tabulation test and Chi-Square test result.

Table 3 : Cross tabulation table of desired level and perceived level of Sufficient number of

counter available in the branches

Name of the Bank

Desired tangibility

Sufficient number

counter available

Total

Highly

satisfied

Satisfied

SBI

Perceived tangibility

Sufficient number counter

available

Highly

satisfied

Count

27

2

29

% of Total

24.5%

1.8%

26.4%

Satisfied

Count

34

12

46

% of Total

30.9%

10.9%

41.8%

Not Decided

Count

16

7

23

14

% of Total

14.5%

6.4%

20.9%

Dissatisfied

Count

10

2

12

% of Total

9.1%

1.8%

10.9%

Total

Count

87

23

110

% of Total

79.1%

20.9%

100.0%

Table 4 : Chi-Square Tests

Name of the Bank

Value

df

Asymp. Sig.

(2-sided)

SBI

Pearson Chi-Square

5.582

a

3

.134

Likelihood Ratio

6.364

3

.095

Linear-by-Linear

Association

1.693

1

.193

N of Valid Cases

110

In the above table 4, for SBI, Pearson Chi-Square value is 0.134, which is greater than 0.05 at

5% level of significance. So, we accept the Null Hypothesis (Ho). Now we can say that for SBI

there is no significant difference between the desired level and perceived level regarding

sufficient number of counter available in the branches. Hence, we may conclude that SBI bank

has sufficient number of counter available for providing smooth services to the customer and the

bank has met the customer‟s expectation level.

In the same way, we have done Chi-Square tests for the other ten (10) sub-parameters of

„Tangibility”. The findings of the Ch-Square test of all the eleven (11) sub-parameters are

summarized in the following table

Table 5: Summary Table of the Chi Square tests of the parameter ‘Tangibility’

Sl no.

Hypothesis

P

value

Remarks

15

1

Ho= There is no significant difference between desired level

and perceived level relating to sufficient number of counter

available in the bank.

0.134

Ho accepted

2

Ho= There is no significant difference between desired level

and perceived level regarding availability of cash depository

machine in the branch.

0.496

Ho accepted

3

Ho = There is no significant difference between desired level

and perceived level relating to sufficient number cash

counting machine.

0.014

Ho rejected

4

Ho = There is no significant difference between desired level

and perceived level relating to sufficient number of ATM

machine in the bank.

0.121

Ho accepted

5

Ho = There is no significant difference between desired level

and perceived level relating to sufficient space to serve

customer with reasonable comfort in the branch of this bank.

0.015

Ho rejected

6

Ho = There is no significant difference between desired level

and perceived level relating to availability of bank slip,

Challan and pamphlets.

0.000

Ho rejected

7

Ho= There is no significant difference between desired level

and perceived level relating to adequate staff at the bank to

meet customer requirements in the bank

0.024

Ho rejected

8

Ho = There is no significant difference between desired level

and perceived level relating to bank has sufficient passbook

up to date machine.

0.117

Ho accepted

16

9

Ho= There is no significant difference between desired level

and perceived level parking facilities in the bank premises.

0.13

Ho accepted

10

Ho = There is no significant difference between desired

level and perceived level relating to seating facilities,

drinking water and toilet facilities are convenient.

0.357

Ho accepted

11

H0= There is no significance difference between desired

level and perceived level relating to E-corner facilities in the

bank.

0.137

Ho accepted

(Source: Compiled by Researcher)

Table 6: Consolidated result of the Chi-Square tests for Tangibility

SBI Bank

Accept

7

Reject

4

Total

11

(Source: Compiled by Researcher)

The above table (6) shows that regarding tangibility, seven (7) hypotheses have been accepted

and four (4) hypotheses have been rejected. The acceptance of the hypothesis means that there is

no significant difference between the desired level and perceived level among the customers

regarding any particular service. That means, the customers are satisfied with the services if the

hypothesis are accepted and vice-versa. Again, rejection of hypothesis means that there is a

significant difference between the desired level and perceived level among the customer i.e. the

customers are not getting the expected services regarding this parameter of ‘Tangibility’.

a) Reliability

As the same way, we have also done Chi-Square tests for the seven (7) sub-parameters of

„Reliability” also and got the findings which are summarized in the following table:

17

Table 7: Summary Table of the Chi Square tests of the parameter ‘Reliability’

Sl.no

Hypothesis

P value

Remarks

1

Ho= There is no significance difference between

desired level and perceived level relating to bank

renders service as promised.

0.215

Ho accepted

2

Ho = There is no significance difference between

desired level and perceived level relating to

standard time taken to process transaction .

0.004

Ho rejected

3

Ho = There is no significance difference between

desired level and perceived level relating to staffs

are sincere in solving customer problems.

0.483

Ho accepted

4

Ho= There is no significance difference between

desired level and perceived level relating to

level of services are same at all times of day .

0.035

Ho rejected

5

Ho= There is no significance difference between

desired level and perceived level relating to

accurate information are provide on website.

0.000

Ho rejected

6

Ho = There is no significance difference

between desired level and perceived level relating

to banks insist error free records.

0.082

Ho rejected

18

7

Ho = There is no significance difference

between desired level and perceived level relating

to customers can feel a sense of security during

the transaction process.

0.000

Ho rejected

(Source : Compiled by the Researcher)

Table 8: Consolidated result of the Chi-Square tests for Reliability

SBI Bank

Accept

2

Reject

5

Total

7

(Source : Compiled by the Researcher)

The above table (8) shows that for SBI, two (2) hypotheses have been accepted and five (5)

hypotheses have been rejected and for all rejected hypothesis, desire level of the customer is

greater than the perceived level regarding the parameter ‘Reliability’.

c. Responsiveness

In this case, we have also selected six (6) Sub parameter and also have done Chi-Square tests for

that of „Responsiveness” and got the findings which are summarized in the following table.

Table 9: Summary Table of the Chi Square test of the parameter

‘Responsiveness’

sl.no

Hypothesis

P value

Remarks

19

1

Ho = There is no significance

difference between desired level and

perceived level relating to your request

are handle promptly.

0.003

Ho rejected

2

Ho= There is no significance difference

between desired level and perceived

level relating to bank alerts the customer

after their every transaction through

SMS promptly.

0.001

Ho rejected

3

Ho= There is no significance difference

between desired level and perceived

level relating to response in case of

emergency and seriousness.

0.434

Ho accepted

4

Ho = There is no significance difference

between desired level and perceived

level relating to bank delivers the

information and product at proper time.

0.0183

Ho rejected

5

Ho= There is no significance difference

between desired level and perceived

level relating to banks performs the

services right the first time.

0.011

Ho rejected

6

Ho = There is no significance difference

between desired level and perceived

level relating to sincerity of bank staff

to answer when you have doubts and

queries.

0.025

Ho rejected

20

(Source : Compiled by the Researcher)

Table 10: Consolidated result of Responsiveness

SBI Bank

Accept

1

Reject

5

Total

6

The above table (10) shows that for the bank SBI one (1) hypothesis have been accepted and

five (5) hypothesis have been rejected and as same way all five hypothesis are rejected. It means

SBI have not been able to satisfy the customers regarding the parameter Responsiveness.

d. Assurance

For the parameter Assurance four (4) sub parameter or questions were setup and we have done

Chi-Square tests on that. The findings of the Ch-Square test are summarized in the following

table.

Table 11: Summary Table of the Chi Square test of the parameter ‘Assurance’

sl.no

Hypothesis

P value

Remarks

1

Ho= There is no significant difference

between desired level and perceived level

employee of the bank have knowledge to

answer customer‟s questions.

0.034

Ho rejected

2

Ho = There is no significant difference

between desired level and perceived level

relating to staff behavior with customers are

polite and friendly.

0.026

Ho rejected

21

3

Ho = There is no significant difference

between desired level and perceived level

relating to employees are always willing to

help you.

0.013

Ho rejected

4

Ho= There is no significant difference

between desired level and perceived level

relating to bank can honor their

commitment.

0.006

Ho rejected

Table 12: Consolidated result of the parameter ‘Assurance’

SBI Bank

Accept

0

Reject

4

Total

4

The above table (12) describe that for SBI bank all of the hypothesis have been rejected, it means

that SBI have not been able to satisfy the customers of the parameter of „Assurance‟. So we can

say that for the selected branches of SBI, the customers are not getting better quality of service

regarding the parameter of ‘Assurance’.

d. Empathy

In the same way, we have also set up and done Chi-Square tests for the five (5) sub-parameters

of „Empathy”. The findings of the Ch-Square test of all the five (5) sub-parameters are

summarized in the following table

Table 13: Summary table of chi square test of the parameter ‘Empathy’

sl.no

Hypothesis

P value

Remarks

1

Ho= There is no significant difference

between desired level and perceived level

relating to provisions of financial advice.

0.402

Ho accepted

22

2

Ho= There is no significant difference

between desired level and perceived level

relating to staffs try to determine what are the

clients specific objectives.

0.519

Ho accepted

3

Ho = There is no significant difference

between desired level and perceived level

relating to helpdesk , call center of bank

operate 24 hours.

0.118

Ho accepted

4

Ho = There is no significant difference

between desired level and perceived level

relating to bank‟s operating hour are

convenient to their customer.

0.107

Ho accepted

5

Ho = There is no significant difference

between desired level and perceived level

relating to employees give personal attention

to their customer .

0.426

Ho accepted

(Source: Compiled by the Researcher)

Table 14: Consolidated result of the parameter ‘Empathy’

SBI Bank

Accept

5

Reject

0

Total

5

The above table (14) indicates that for SBI, all and five (5) hypotheses have been accepted and

none (0) of the hypothesis have been rejected. It means that SBI has been able to satisfy the

customers for 100% of the sub-parameters (5 out of 5) of „Empathy‟. So we can say that the

customers of SBI are highly satisfied with the service quality regarding the parameter

‘Empathy’.

23

9. Conclusion

The study found that in today‟s competitive environment, service quality plays an important

role for the long term sustainability of the banks. As a result, to cope up this changing market

condition banks have to retain old customers and have to attract new customers by providing

better quality of services. It has been evident from the study that there is a strong relationship

between the customer satisfaction and service quality. To ensure customer satisfaction the

banks have to improve their service quality as per the customer‟s expectation. The specific

conclusions regarding the five parameters of service quality are as flows:

(i) The appearance of physical facilities, equipment, personnel and communication

materials in relation to „Tangibility’ are not so strong in SBI Bank to satisfy their

customer.

(ii) Service quality of SBI bank is not so reliable, accurate, secured and faithful to

satisfying their customers.

(iii)In case of ‘Responsiveness’ service quality of this bank could not meet their customer‟s

expectation level.

(iv) Regarding ‘Assurance’ the feedback of customers of the banks is not good. Lack of

assurance has been found for the bank.

(v) Regarding ‘Empathy’, SBI provide excellent services which have increased the

customer‟s satisfaction.

10. Recommendations

Some recommendations are given below for betterment of the services in State Bank of India.

(i) Now a day‟s technology is modernizing day by day therefore SBI Bank have to up to date

there technology as per modern era, and banks have to install sufficient number of cash

counting machine in every branches. The bank should ensure availability of bank slip,

challan and pamphlets to serve customers in a better way.

(ii) The bank should increase its staff to give personal attention to the customers and serve

quickly.

(iii) The bank should ensure that the employees are behaving politely and friendly with the

customers.

24

(iv) There are a huge number of customers in SBI bank. So the bank should increase its

number of staff to serve the customers quickly, should improve seating facility to

customers and increase the space inside the bank for providing smooth services to the

customers.

(v) Better and faster technology, swanky branches and best product/service offering are

necessary but not sufficient for customer satisfaction. Hence, there is a need to transform

the mindset of the staff through greater knowledge and enhanced communication skills.

References

Journals

Agarwal, J. (2009). Customer satisfaction in Indian Banking Services- A Study in Aligarh

District. International Journal of Computing and Business Research, Vol.3 Issue 1, 4-5.

Chinwuba, M. S. and Egene, S. (2013). Evaluating customer – Perceived Service Quality And

Customer Satisfaction in The Nigerian Banking Industry, Far East Journal of Psychology and

Business, Far East Research Center, Vol-11(3), 34- 46.

Gronroos, C (1984). A Service Quality Model and Its Marketing Implications, European Journal

of Marketing, 18, 36-44.

Haidar, M. I, and Islam, M. S. (2011), Determination of Service Quality Factors of Private

Commercial Banks in Bangladesh, ASA University Review, Vol.5, No.2, 129-138.

Jani, A. S. (2012), A study of Customer Perception on the use of E-Technology in the Retail

Banking Sector: A Comparative study of Public Sector and Private Sector Banks, Indian Journal

of Marketing, Vol: 42, No: 1, 46-58.

Mary S. S. (2014). A Comparative Study on the Customer Satisfaction in Private Sector and

Public Sector Banks with Reference to Chennai City, International Journal of Business

Quantitative Economics and Applied Management Research, Vol 2, 42-43.

Muyeed M. A. (2012). Customer perception of service quality in retail banking in developing

countries – A case study, International Journal of Marketing Studies, Vol.4, No.1, pp. 116-122.

Oppewal, H. and Vriens, M. (2000). Measuring Perceived Service Quality Using Integrated

Conjoint Experiment, International Journal of Bank Marketing, Vol.18 Issue: 4, pp.154-169.

25

Parasuraman, A., Zeithaml, V. A. and Berry, L. L. (1988). “SERVQUAL: A Multiple-item Scale

for Measuring Consumer Perception of Service Quality”, Journal of Retailing, Vol.64, No.1, 12-

40.

Rahaman, M. M., Abdullah, M and Ataur (2011). Measuring Service Quality using SERVQUAL

Model: A Study on PCBs (Private Commercial Banks) in Bangladesh, Business Management

Dynamics, 05-11.

Seth, Deshmukh, Vrat (2004). Service quality models: A Review, International Journal of

Quality and Reliability Management Vol. 22, 915-923.

Shanka, M.S. (2012). Bank Service Quality, Customer Satisfaction and Loyalty in Ethiopian

Banking Sector, Journal of Business Administration and Management Sciences Research, 1(1),

001-009.

Sheetal B. Sachdev and Harsh V. Verma (2004). Relative Importance Of Service Quality

Dimensions: A Multi-sectoral Study, Journal Of Service Research, Volume 4, No 1, 93-115.

Siddiqi K. O. (2011). Interrelations Between Service Quality Attributes, Customer Satisfaction

and Customer Loyalty in the Retail Banking Sector in Bangladesh”, International Journal of

Business and Management, Vol. 6, No. 3, 12-36.

Vasantha, H. and Rani, S.S. (2011). Customer Perception of Services Quality in the Retail

Banking Sector, European Journal of Business and Management, 3, 18-23.

Books

Desai, V. (1979). Indian Banking-Nature and Problems, Himalaya Publishing House, Bombay.

Indian Institute of Banking and Finance (2004). Banking Product and Service, Taxman

Publication, New Delhi.

Indian Institute of Banking and Finance (2000). Principle and Practice of Banking,

MACMILLAN Publication, New Delhi.

Jha, S.M. (2007). Services Marketing, Himalaya publishing House, Bangalore.

Kothari, C.R. (2005). Research methodology methods and Techniques, New Age International

publishers, New Delhi.

Report

Report of the RBI Study Group, IBA Publications, 1977.