Userid: CPM Schema: tipx Leadpct: 100% Pt. size: 10

Draft Ok to Print

AH XSL/XML

Fileid: … ations/p15/2024/a/xml/cycle06/source (Init. & Date) _______

Page 1 of 57 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Department of the Treasury

Internal Revenue Service

Publication 15

Cat. No. 10000W

(Circular E),

Employer's

Tax Guide

For use in 2024

Get forms and other information faster and easier at:

• IRS.gov (English)

• IRS.gov/Spanish (Español)

•

IRS.gov/Chinese (中文)

•

IRS.gov/Korean (한국어)

• IRS.gov/Russian (Pусский)

• IRS.gov/Vietnamese (Tiếng Việt)

Contents

What's New ............................... 1

Reminders ............................... 2

Calendar ................................. 9

Introduction ............................. 11

1. Employer Identification Number (EIN) ....... 12

2. Who Are Employees? .................... 12

3. Family Employees ...................... 15

4. Employee's Social Security Number (SSN) ... 15

5. Wages and Other Compensation ........... 17

6. Tips .................................. 21

7. Supplemental Wages .................... 22

8. Payroll Period .......................... 23

9. Withholding From Employees' Wages ....... 24

10. Required Notice to Employees About the

Earned Income Credit (EIC) .............. 29

11. Depositing Taxes ...................... 30

12. Filing Form 941, Form 943, Form 944, or

Form 945 ............................ 36

13. Reporting Adjustments to Forms 941, Form

943, or Form 944 ...................... 39

14. Federal Unemployment (FUTA) Tax ........ 42

15. Special Rules for Various Types of Services

and Payments ......................... 44

16. Third-Party Payer Arrangements .......... 51

17. Federal Agency Certifying Requirements of

Federal Income Taxes Withheld From U.S.

Government Employees Working in, or

Federal Pension Recipients Residing in,

American Samoa, the CNMI, and Guam ..... 52

How To Get Tax Help ....................... 54

Index .................................. 57

Future Developments

For the latest information about developments related to

Pub. 15, such as legislation enacted after it was

published, go to IRS.gov/Pub15.

What's New

Pub. 15 is now for all employers. Pub. 15 can now be

used by all employers, including agricultural employers

and employers in the U.S. territories. Pub. 51, Agricultural

Dec 19, 2023

Page 2 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Employer's Tax Guide; Pub. 80, Federal Tax Guide for Em-

ployers in the U.S. Virgin islands, Guam, American Sa-

moa, and the Commonwealth of the Northern Mariana Is-

lands; and Pub. 179, Guía Contributiva Federal para

Patronos Puertorriqueños, have been discontinued. If you

prefer Pub. 15 in Spanish, there is a new Pub. 15 (sp)

available for 2024.

Unless otherwise noted, references throughout this

publication to Form W-2 include Forms W-2AS, W-2CM,

W-2GU, W-2VI, and Form 499R-2/W-2PR; references to

Form W-2c include Form 499R-2c/W-2cPR; references to

Form W-3 include Form W-3SS and Form W-3PR; and

references to Form W-3c include Form W-3C (PR).

Social security and Medicare tax for 2024. The rate of

social security tax on taxable wages is 6.2% each for the

employer and employee. The social security wage base

limit is $168,600.

The Medicare tax rate is 1.45% each for the employee

and employer, unchanged from 2023. There is no wage

base limit for Medicare tax.

Social security and Medicare taxes apply to the wages

of household workers you pay $2,700 or more in cash wa-

ges in 2024. Social security and Medicare taxes apply to

election workers who are paid $2,300 or more in cash or

an equivalent form of compensation in 2024.

The COVID-19 related credit for qualified sick and

family leave wages is limited to leave taken after

March 31, 2020, and before October 1, 2021, and may

no longer be claimed on Form 941. Generally, the

credit for qualified sick and family leave wages, as enac-

ted under the Families First Coronavirus Response Act

(FFCRA) and amended and extended by the COVID-rela-

ted Tax Relief Act of 2020, for leave taken after March 31,

2020, and before April 1, 2021, and the credit for qualified

sick and family leave wages under sections 3131, 3132,

and 3133 of the Internal Revenue Code, as enacted under

the American Rescue Plan Act of 2021 (the ARP), for

leave taken after March 31, 2021, and before October 1,

2021, have expired. However, employers that pay qualified

sick and family leave wages in 2024 for leave taken after

March 31, 2020, and before October 1, 2021, are eligible

to claim a credit for qualified sick and family leave wages

in 2024. Effective for tax periods beginning after Decem-

ber 31, 2023, the lines used to claim the credit for qualified

sick and family leave wages have been removed from

Form 941, Employer’s QUARTERLY Federal Tax Return,

because it would be extremely rare for an employer to pay

wages in 2024 for qualified sick and family leave taken af-

ter March 31, 2020, and before October 1, 2021. Instead,

if you’re eligible to claim the credit for qualified sick and

family leave wages because you paid the wages in 2024

for an earlier applicable leave period, file Form 941-X, Ad-

justed Employer's QUARTERLY Federal Tax Return or

Claim for Refund, after filing Form 941, to claim the credit

for qualified sick and family leave wages paid in 2024. Fil-

ing a Form 941-X before filing a Form 941 for the quarter

may result in errors or delays in processing your Form

941-X.

New Forms 941 (sp), 943 (sp), and 944 (sp). If you

prefer your form and instructions in Spanish, you can file

new Form 941 (sp), new Form 943 (sp), and Form 944

(sp).

Reminders

Qualified small business payroll tax credit for in-

creasing research activities. For tax years beginning

before January 1, 2023, a qualified small business may

elect to claim up to $250,000 of its credit for increasing re-

search activities as a payroll tax credit. The Inflation Re-

duction Act of 2022 (the IRA) increases the election

amount to $500,000 for tax years beginning after Decem-

ber 31, 2022. The payroll tax credit election must be made

on or before the due date of the originally filed income tax

return (including extensions). The portion of the credit

used against payroll taxes is allowed in the first calendar

quarter beginning after the date that the qualified small

business filed its income tax return. The election and de-

termination of the credit amount that will be used against

the employer’s payroll taxes are made on Form 6765,

Credit for Increasing Research Activities. The amount

from Form 6765, line 44, must then be reported on Form

8974, Qualified Small Business Payroll Tax Credit for In-

creasing Research Activities.

Starting in the first quarter of 2023, the payroll tax credit

is first used to reduce the employer share of social secur-

ity tax up to $250,000 per quarter and any remaining

credit reduces the employer share of Medicare tax for the

quarter. Any remaining credit, after reducing the employer

share of social security tax and the employer share of

Medicare tax, is then carried forward to the next quarter.

Form 8974 is used to determine the amount of the credit

that can be used in the current quarter. The amount from

Form 8974, line 12 or, if applicable, line 17, is reported on

Form 941, Form 943, or Form 944. For more information

about the payroll tax credit, see IRS.gov/

ResearchPayrollTC. Also see the line 16 instructions in the

Instructions for Form 941 (line 17 instructions in the In-

structions for Form 943 or line 13 instructions in the In-

structions for Form 944) for information on reducing your

record of tax liability for this credit.

Disaster tax relief. Disaster tax relief is available for

those impacted by disasters. For more information about

disaster relief, go to IRS.gov/DisasterTaxRelief.

Payroll tax credit for certain tax-exempt organiza-

tions affected by qualified disasters. Section 303(d) of

the Taxpayer Certainty and Disaster Tax Relief Act of 2020

allows for a payroll tax credit for certain tax-exempt organi-

zations affected by certain qualified disasters not related

to COVID-19. This credit is claimed on Form 5884-D (not

on Form 941, Form 943, or Form 944). Form 5884-D is

filed after the Form 941 for the quarter, Form 943 for the

year, or Form 944 for the year for which the credit is being

claimed has been filed. For more information about this

credit, go to IRS.gov/Form5884D.

2024 withholding tables. The Percentage Method and

Wage Bracket Method withholding tables, the employer in-

structions on how to figure employee withholding, and the

amount to add to a nonresident alien employee's wages

2 Publication 15 (2024)

Page 3 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

for figuring income tax withholding are included in Pub.

15-T, Federal Income Tax Withholding Methods, available

at IRS.gov/Pub15T.

Moving expense reimbursement. P.L. 115-97 sus-

pends the exclusion for qualified moving expense reim-

bursements from your employee's income for tax years

beginning after 2017 and before 2026. However, the ex-

clusion is still available in the case of a member of the U.S.

Armed Forces on active duty who moves because of a

permanent change of station due to a military order. The

exclusion applies only to reimbursement of moving expen-

ses that the member could deduct if they had paid or in-

curred them without reimbursement. See Moving Expen-

ses in Pub. 3, Armed Forces' Tax Guide, for the definition

of what constitutes a permanent change of station and to

learn which moving expenses are deductible.

Withholding on supplemental wages. P.L. 115-97 low-

ered the withholding rates on supplemental wages for tax

years beginning after 2017 and before 2026. See section

7 for the withholding rates.

Backup withholding. P.L. 115-97 lowered the backup

withholding rate to 24% for tax years beginning after 2017

and before 2026. For more information on backup with-

holding, see Backup withholding, later.

Certification program for professional employer or-

ganizations (PEOs). The Stephen Beck, Jr., Achieving a

Better Life Experience Act of 2014 required the IRS to es-

tablish a voluntary certification program for PEOs. PEOs

handle various payroll administration and tax reporting re-

sponsibilities for their business clients and are typically

paid a fee based on payroll costs. To become and remain

certified under the certification program, certified profes-

sional employer organizations (CPEOs) must meet vari-

ous requirements described in sections 3511 and 7705

and related published guidance. Certification as a CPEO

may affect the employment tax liabilities of both the CPEO

and its customers. A CPEO is generally treated for em-

ployment tax purposes as the employer of any individual

who performs services for a customer of the CPEO and is

covered by a contract described in section 7705(e)(2) be-

tween the CPEO and the customer (CPEO contract), but

only for wages and other compensation paid to the indi-

vidual by the CPEO. To become a CPEO, the organization

must apply through the IRS Online Registration System.

For more information or to apply to become a CPEO, go to

IRS.gov/CPEO. Also see Revenue Procedure 2023-18,

2023-13 I.R.B. 605, available at IRS.gov/irb/

2023-13_IRB#REV-PROC-2023-18.

Outsourcing payroll duties. Generally, as an employer,

you’re responsible to ensure that tax returns are filed and

deposits and payments are made, even if you contract

with a third party to perform these acts. You remain re-

sponsible if the third party fails to perform any required ac-

tion. Before you choose to outsource any of your payroll

and related tax duties (that is, withholding, reporting, and

paying over social security, Medicare, FUTA, and income

taxes) to a third-party payer, such as a payroll service pro-

vider or reporting agent, go to IRS.gov/

OutsourcingPayrollDuties for helpful information on this

topic. If a CPEO pays wages and other compensation to

an individual performing services for you, and the services

are covered by a CPEO contract, then the CPEO is gener-

ally treated as the employer, but only for wages and other

compensation paid to the individual by the CPEO. How-

ever, with respect to certain employees covered by a

CPEO contract, you may also be treated as an employer

of the employees and, consequently, may also be liable for

federal employment taxes imposed on wages and other

compensation paid by the CPEO to such employees. For

more information on the different types of third-party payer

arrangements, see section 16.

Aggregate Form 941 or Form 943 filers. Approved

section 3504 agents and CPEOs must complete Sched-

ule R (Form 941), Allocation Schedule for Aggregate Form

941 Filers, or Schedule R (Form 943), Allocation Schedule

for Aggregate Form 943 Filers, as applicable, when filing

an aggregate Form 941 or Form 943. An aggregate quar-

terly Form 941 or annual Form 943 is filed by an agent ap-

proved by the IRS under section 3504 of the Internal Rev-

enue Code. To request approval to act as an agent for an

employer, the agent files Form 2678 with the IRS unless

you're a state or local government agency acting as an

agent under the special procedures provided in Revenue

Procedure 2013-39, 2013-52 I.R.B. 830, available at

IRS.gov/irb/2013-52_IRB#RP-2013-39. An aggregate

quarterly Form 941 or annual Form 943 is also filed by

CPEOs approved by the IRS under section 7705. To be-

come a CPEO, the organization must apply through the

IRS Online Registration System at IRS.gov/CPEO. CPEOs

file Form 8973, Certified Professional Employer Organiza-

tion/Customer Reporting Agreement, to notify the IRS that

they’ve started or ended a service contract with a client or

customer. CPEOs must generally file Form 941 or Form

943 and the applicable Schedule R electronically. For

more information about a CPEO's requirement to file elec-

tronically, see Revenue Procedure 2023-18.

Other third-party payers that file an aggregate quarterly

Form 941 or annual Form 943, such as non-certified

PEOs, must complete and file the applicable Schedule R if

they have clients that are claiming any employment tax

credit (for example, the qualified small business payroll tax

credit for increasing research activities).

Aggregate Form 940 filers. Approved section 3504

agents and CPEOs must complete Schedule R (Form

940), Allocation Schedule for Aggregate Form 940 Filers,

when filing an aggregate Form 940, Employer's Annual

Federal Unemployment (FUTA) Tax Return. Aggregate

Forms 940 can be filed by agents acting on behalf of

home care service recipients who receive home care

services through a program administered by a federal,

state, or local government. To request approval to act as

an agent on behalf of home care service recipients, the

agent files Form 2678 with the IRS unless you're a state or

local government agency acting as an agent under the

special procedures provided in Revenue Procedure

2013-39. Aggregate Forms 940 are also filed by CPEOs

approved by the IRS under section 7705. CPEOs file Form

8973 to notify the IRS that they’ve started or ended a serv-

ice contract with a client or customer. CPEOs must gener-

ally file Form 940 and Schedule R (Form 940)

Publication 15 (2024) 3

Page 4 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

electronically. For more information about a CPEO's re-

quirement to file electronically, see Revenue Procedure

2023-18.

Work opportunity tax credit for qualified tax-exempt

organizations hiring qualified veterans. Qualified

tax-exempt organizations that hire eligible unemployed

veterans may be able to claim the work opportunity tax

credit against their payroll tax liability using Form 5884-C.

For more information, go to IRS.gov/WOTC.

Medicaid waiver payments. Notice 2014-7 provides

that certain Medicaid waiver payments are excludable

from income for federal income tax purposes. See Notice

2014-7, 2014-4 I.R.B. 445, available at IRS.gov/irb/

2014-04_IRB#NOT-2014-7. For more information, includ-

ing questions and answers related to Notice 2014-7, go to

IRS.gov/MedicaidWaiverPayments.

No federal income tax withholding on disability pay-

ments for injuries incurred as a direct result of a ter-

rorist attack directed against the United States. Disa-

bility payments for injuries incurred as a direct result of a

terrorist attack directed against the United States (or its al-

lies) aren't included in income. Because federal income

tax withholding is only required when a payment is includi-

ble in income, no federal income tax should be withheld

from these payments. See Pub. 907, Tax Highlights for

Persons With Disabilities; and Pub. 3920, Tax Relief for

Victims of Terrorist Attacks.

Voluntary withholding on dividends and other distri-

butions by an Alaska Native Corporation (ANC). A

shareholder of an ANC may request voluntary income tax

withholding on dividends and other distributions paid by

an ANC. A shareholder may request voluntary withholding

by giving the ANC a completed Form W-4V. For more in-

formation, see Notice 2013-77, 2013-50 I.R.B. 632, availa-

ble at IRS.gov/irb/2013-50_IRB#NOT-2013-77.

Definition of marriage. A marriage of two individuals is

recognized for federal tax purposes if the marriage is rec-

ognized by the state or territory of the United States in

which the marriage is entered into, regardless of legal resi-

dence. Two individuals who enter into a relationship that is

denominated as marriage under the laws of a foreign juris-

diction are recognized as married for federal tax purposes

if the relationship would be recognized as marriage under

the laws of at least one state or territory of the United

States, regardless of legal residence. Individuals who

have entered into a registered domestic partnership, civil

union, or other similar relationship that isn't denominated

as a marriage under the law of the state or territory of the

United States where such relationship was entered into

aren't lawfully married for federal tax purposes, regardless

of legal residence.

Differential wage payments. Qualified differential wage

payments made by employers to individuals serving in the

U.S. Armed Forces are subject to income tax withholding

but not social security, Medicare, or FUTA tax. See section

5 for more information.

Severance payments. Severance payments are wages

subject to social security and Medicare taxes, income tax

withholding, and FUTA tax.

You must receive written notice from the IRS to file

Form 944. If you’ve been filing quarterly Forms 941 and

believe your employment taxes for the calendar year will

be $1,000 or less, and you would like to file an annual

Form 944 instead of quarterly Forms 941, you must con-

tact the IRS during the first calendar quarter of the tax

year to request to file Form 944. You must receive written

notice from the IRS to file Form 944 instead of quarterly

Forms 941 before you may file this form. For more infor-

mation on requesting to file Form 944, including the meth-

ods and deadlines for making a request, see the Instruc-

tions for Form 944.

Employers can request to file quarterly Forms 941 in-

stead of an annual Form 944. If you received notice

from the IRS to file Form 944 but would like to file quarterly

Forms 941 instead, you must contact the IRS during the

first calendar quarter of the tax year to request to file quar-

terly Forms 941. You must receive written notice from the

IRS to file quarterly Forms 941 instead of Form 944 before

you may file these forms. For more information on request-

ing to file quarterly Forms 941, including the methods and

deadlines for making a request, see the Instructions for

Form 944.

Correcting Form 941, Form 943, or Form 944. If you

discover an error on a previously filed Form 941, make the

correction using Form 941-X. If you discover an error on a

previously filed Form 943, make the correction using Form

943-X. If you discover an error on a previously filed Form

944, make the correction using Form 944-X. Forms 941-X,

943-X, and 944-X are filed separately from Forms 941,

943, and 944. Forms 941-X, 943-X, and 944-X are used

by employers to claim refunds or abatements of employ-

ment taxes, rather than Form 843. See section 13 for more

information.

Zero wage return. If you haven't filed a “final” Form 940

and "final" Form 941, Form 943, or Form 944, or aren't a

“seasonal” employer (Form 941 only), you must continue

to file a Form 940 and Forms 941, Form 943, or Form 944,

even for periods during which you paid no wages. The IRS

encourages you to file your “zero wage” Form 940 and

Form 941, Form 943, or Form 944 electronically. Go to

IRS.gov/EmploymentEfile for more information on elec-

tronic filing.

Federal tax deposits must be made by electronic

funds transfer (EFT). You must use EFT to make all fed-

eral tax deposits. Generally, an EFT is made using the

Electronic Federal Tax Payment System (EFTPS). If you

don't want to use EFTPS, you can arrange for your tax

professional, financial institution, payroll service, or other

trusted third party to make electronic deposits on your be-

half. Also, you may arrange for your financial institution to

initiate a same-day wire payment on your behalf. EFTPS is

a free service provided by the Department of the Treasury.

Services provided by your tax professional, financial insti-

tution, payroll service, or other third party may have a fee.

For more information on making federal tax deposits,

see How To Deposit in section 11. To get more information

about EFTPS or to enroll in EFTPS, go to EFTPS.gov or

call 800-555-4477, 800-244-4829 (Spanish), or

303-967-5916 (toll call). To contact EFTPS using

4 Publication 15 (2024)

Page 5 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Telecommunications Relay Services (TRS) for people who

are deaf, hard of hearing, or have a speech disability, dial

711 and then provide the TRS assistant the 800-555-4477

number or 800-733-4829. Additional information about

EFTPS is also available in Pub. 966.

Residents of the Philippines working in the Common-

wealth of the Northern Mariana Islands (CNMI). Em-

ployers must withhold and pay social security and Medi-

care taxes on wages and other compensation paid to

residents of the Philippines who don't hold an H-2 status

for services performed as employees in the CNMI unless

those workers are eligible for exemption from social secur-

ity and Medicare taxes under an exception listed in sec-

tion 15. For more information, see Announcement

2012-43, 2012-51 I.R.B. 723, available at IRS.gov/irb/

2012-51_IRB#ANN-2012-43.

Federal employers in the CNMI. The U.S. Treasury De-

partment and the CNMI Division of Revenue and Taxation

entered into an agreement under 5 U.S.C. section 5517 in

December 2006. Under this agreement, all federal em-

ployers (including the Department of Defense) are re-

quired to withhold CNMI income taxes (rather than federal

income taxes) and deposit the CNMI taxes with the CNMI

Treasury for employees who are subject to CNMI taxes

and whose regular place of federal employment is in the

CNMI. For more information, including details on complet-

ing Form W-2, go to IRS.gov/5517Agreements. Federal

employers are also required to file quarterly and annual re-

ports with the CNMI Division of Revenue and Taxation. For

questions, contact the CNMI Division of Revenue and Tax-

ation.

Pub. 5146 explains employment tax examinations

and appeal rights. Pub. 5146 provides employers with

information on how the IRS selects employment tax re-

turns to be examined, what happens during an exam, and

what options an employer has in responding to the results

of an exam, including how to appeal the results. Pub. 5146

also includes information on worker classification issues

and tip exams.

Electronic Filing and Payment

Businesses can enjoy the benefits of filing and paying

their federal taxes electronically. Whether you rely on a tax

professional or handle your own taxes, the IRS offers you

convenient and secure programs to make filing and

payment easier.

Spend less time worrying about taxes and more time

running your business. Use e-file and EFTPS to your

benefit.

•

For e-file, go to IRS.gov/EmploymentEfile for

additional information. A fee may be charged to file

electronically.

•

For EFTPS, go to EFTPS.gov or call EFTPS Customer

Service at 800-555-4477, 800-244-4829 (Spanish), or

303-967-5916 (toll call). To contact EFTPS using TRS

for people who are deaf, hard of hearing, or have a

speech disability, dial 711 and then provide the TRS

assistant the 800-555-4477 number or 800-733-4829.

•

For electronic filing of Forms W-2, Wage and Tax

Statement, including Forms W-2AS, W-2CM, W-2GU,

and W-2VI, and Forms 499R-2/W-2PR, go to

SSA.gov/employer. You may be required to file Forms

W-2 electronically. For details, see the General

Instructions for Forms W-2 and W-3. If you experience

problems filing electronically, contact the Social

Security Administration (SSA) at 800-772-6270. To

speak with the SSA's Regional Employer Services

Liaison Officer, go to the SSA's Regional Employer

Services Liaison Officers website at SSA.gov/

employer/wage_reporting_specialists.htm. The

Regional Employer Services Liaison Officers are

available to provide assistance with all questions

about the SSA's payroll reporting processes and

applications. Employers in the CNMI should contact

their local tax department for instructions on

completing Form W-2CM. You can get Form W-2CM

and its instructions by going to Finance.gov.mp/

forms.php, or by calling 670-664-1000.

If you’re filing your tax return or paying your fed-

eral taxes electronically, a valid employer identifi-

cation number (EIN) is required at the time the re-

turn is filed or the payment is made. If a valid EIN isn't

provided, the return or payment won't be processed. This

may result in penalties. See section 1 for information

about applying for an EIN.

Electronic funds withdrawal (EFW). If you file your em-

ployment tax return electronically, you can e-file and use

EFW to pay the balance due in a single step using tax

preparation software or through a tax professional. How-

ever, don't use EFW to make federal tax deposits. For

more information on paying your taxes using EFW, go to

IRS.gov/EFW.

Credit or debit card payments. You can pay the bal-

ance due shown on your employment tax return by credit

or debit card. Your payment will be processed by a pay-

ment processor who will charge a processing fee. Don't

use a credit or debit card to make federal tax deposits. For

more information on paying your taxes with a credit or

debit card, go to IRS.gov/PayByCard.

Online payment agreement. You may be eligible to ap-

ply for an installment agreement online if you can’t pay the

full amount of tax you owe when you file your employment

tax return. For more information, see the instructions for

your employment tax return or go to IRS.gov/OPA.

Forms in Spanish

Many forms and instructions discussed in this publication

have Spanish-language versions available for employers

and employees. Some examples include Form 941 (sp),

Form 944 (sp), Form SS-4 (sp), Form W-4 (sp), and Form

W-9 (sp). Although this publication doesn't reference

Spanish-language forms and instructions in each instance

that one is available, you can see Pub. 15 (sp) and go to

IRS.gov to determine if a Spanish-language version is

available.

CAUTION

!

Publication 15 (2024) 5

Page 6 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Hiring New Employees

Eligibility for employment. You must verify that each

new employee is legally eligible to work in the United

States, including American Samoa, Guam, the CNMI, the

U.S Virgin Islands (USVI), and Puerto Rico. This includes

completing the U.S. Citizenship and Immigration Services

(USCIS) Form I-9, Employment Eligibility Verification. You

can get Form I-9 at USCIS.gov/Forms. For more informa-

tion, go to the USCIS website at USCIS.gov/I-9-Central, or

call 800-375-5283 or 800-767-1833 (TTY).

You may use the Social Security Number Verification

Service (SSNVS) at SSA.gov/employer/ssnv.htm to verify

that an employee name matches an SSN. A person may

have a valid SSN but not be authorized to work in the Uni-

ted States. You may use E-Verify at E-Verify.gov to confirm

the employment eligibility of newly hired employees.

New hire reporting. All 50 states, and most of the territo-

ries, have a new hire registry. You’re required to report any

new employee to a designated state new hire registry. A

new employee is an employee who hasn't previously been

employed by you or was previously employed by you but

has been separated from such prior employment for at

least 60 consecutive days.

Many states accept a copy of Form W-4 with employer

information added. Go to the Office of Child Support En-

forcement website at acf.hhs.gov/programs/css/employers

for more information. Employers in American Samoa,

Guam, the CNMI, the USVI, and Puerto Rico should con-

tact their local government for information on their new

hire registry.

W-4 request. Ask each new employee to complete the

2024 Form W-4. See section 9.

Name and social security number (SSN). Record

each new employee's name and SSN from their social se-

curity card if it is available. If an employee can't provide

their social security card, you should verify their SSN and

their eligibility for employment as discussed under Verifi-

cation of SSNs. Any employee without a social security

card should apply for one. See section 4.

Information Returns

You must file Forms W-2 to report wages paid to

employees. You may also be required to file information

returns to report certain types of payments made during

the year. For example, you must file Form 1099-NEC,

Nonemployee Compensation, to report payments of $600

or more to persons not treated as employees (for

example, independent contractors) for services performed

for your trade or business. For details about filing Forms

1099 and for information about required electronic filing,

see the General Instructions for Certain Information

Returns for general information, and the separate, specific

instructions for each information return you file (for

example, the Instructions for Forms 1099-MISC and

1099-NEC). Generally, don't use Forms 1099 to report

wages and other compensation you paid to employees;

report these on Form W-2. See the General Instructions

for Forms W-2 and W-3 for details about filing Form W-2

and for information about required electronic filing.

Technical Services Operation (TSO). The IRS oper-

ates the TSO to answer questions about reporting on

Forms W-2, W-3, and 1099, and other information returns.

If you have questions related to reporting on information

returns, call 866-455-7438 (toll free) or 304-263-8700 (toll

call). The center can also be reached by email at

[email protected]v. Don't include taxpayer identification num-

bers (TINs) or attachments in email because email isn't

secure.

Federal Income Tax

Withholding

References to federal income tax withholding

don't apply to employers in American Samoa,

Guam, the CNMI, the USVI, and Puerto Rico, un-

less you have employees who are subject to U.S. income

tax withholding. Contact your local tax department for in-

formation about income tax withholding.

Withhold federal income tax from each wage payment

or supplemental unemployment compensation plan

benefit payment according to the employee's Form W-4

and the correct withholding table in Pub. 15-T. Farm

operators and crew leaders must withhold federal income

tax from the wages of farmworkers if the wages are

subject to social security and Medicare taxes. If you're

paying supplemental wages to an employee, see section

7. If you have nonresident alien employees, see

Withholding federal income taxes on the wages of

nonresident alien employees in section 9.

See section 8 of Pub. 15-A, Employer’s Supplemental

Tax Guide, for information about withholding on pensions

(including distributions from tax-favored retirement plans),

annuities, and individual retirement arrangements (IRAs).

Nonpayroll Income Tax

Withholding

Nonpayroll federal income tax withholding (reported on

Forms 1099 and Form W-2G, Certain Gambling Winnings)

must be reported on Form 945, Annual Return of Withheld

Federal Income Tax. Separate deposits are required for

payroll (Form 941, Form 943, or Form 944) and nonpayroll

(Form 945) withholding. Nonpayroll items include the

following.

•

Pensions (including distributions from tax-favored

retirement plans, for example, section 401(k), section

403(b), and governmental section 457(b) plans),

annuities, and IRA distributions.

•

Military retirement.

•

Gambling winnings.

CAUTION

!

6 Publication 15 (2024)

Page 7 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

Indian gaming profits.

•

Certain government payments on which the recipient

elected voluntary income tax withholding.

•

Dividends and other distributions by an ANC on which

the recipient elected voluntary income tax withholding.

•

Payments subject to backup withholding.

For details on depositing and reporting nonpayroll

income tax withholding, see the Instructions for Form 945.

Distributions from nonqualified pension plans and

deferred compensation plans. Because distributions to

participants from some nonqualified pension plans and

deferred compensation plans (including section 457(b)

plans of tax-exempt organizations) are treated as wages

and are reported on Form W-2, income tax withheld must

be reported on Form 941, Form 943, or Form 944, not on

Form 945. However, distributions from such plans to a

beneficiary or estate of a deceased employee aren't wa-

ges and are reported on Forms 1099-R, Distributions

From Pensions, Annuities, Retirement or Profit-Sharing

Plans, IRAs, Insurance Contracts, etc.; income tax with-

held must be reported on Form 945.

Backup withholding. You must generally withhold 24%

of certain taxable payments if the payee fails to furnish you

with their correct TIN. This withholding is referred to as

“backup withholding.”

Payments subject to backup withholding include inter-

est, dividends, patronage dividends, rents, royalties,

commissions, nonemployee compensation, payments

made in settlement of payment card or third-party network

transactions, and certain other payments you make in the

course of your trade or business. In addition, transactions

by brokers and barter exchanges and certain payments

made by fishing boat operators are subject to backup

withholding.

Backup withholding doesn't apply to wages, pen-

sions, annuities, IRAs (including simplified em-

ployee pension (SEP) and SIMPLE retirement

plans), section 404(k) distributions from an employee

stock ownership plan (ESOP), medical savings accounts

(MSAs), health savings accounts (HSAs), long-term-care

benefits, or real estate transactions.

You can use Form W-9 to request payees to furnish a

TIN. Form W-9 must be used when payees must certify

that the number furnished is correct, or when payees must

certify that they’re not subject to backup withholding or are

exempt from backup withholding. The Instructions for the

Requester of Form W-9 include a list of types of payees

who are exempt from backup withholding. For more infor-

mation, see Pub. 1281, Backup Withholding for Missing

and Incorrect Name/TIN(s).

CAUTION

!

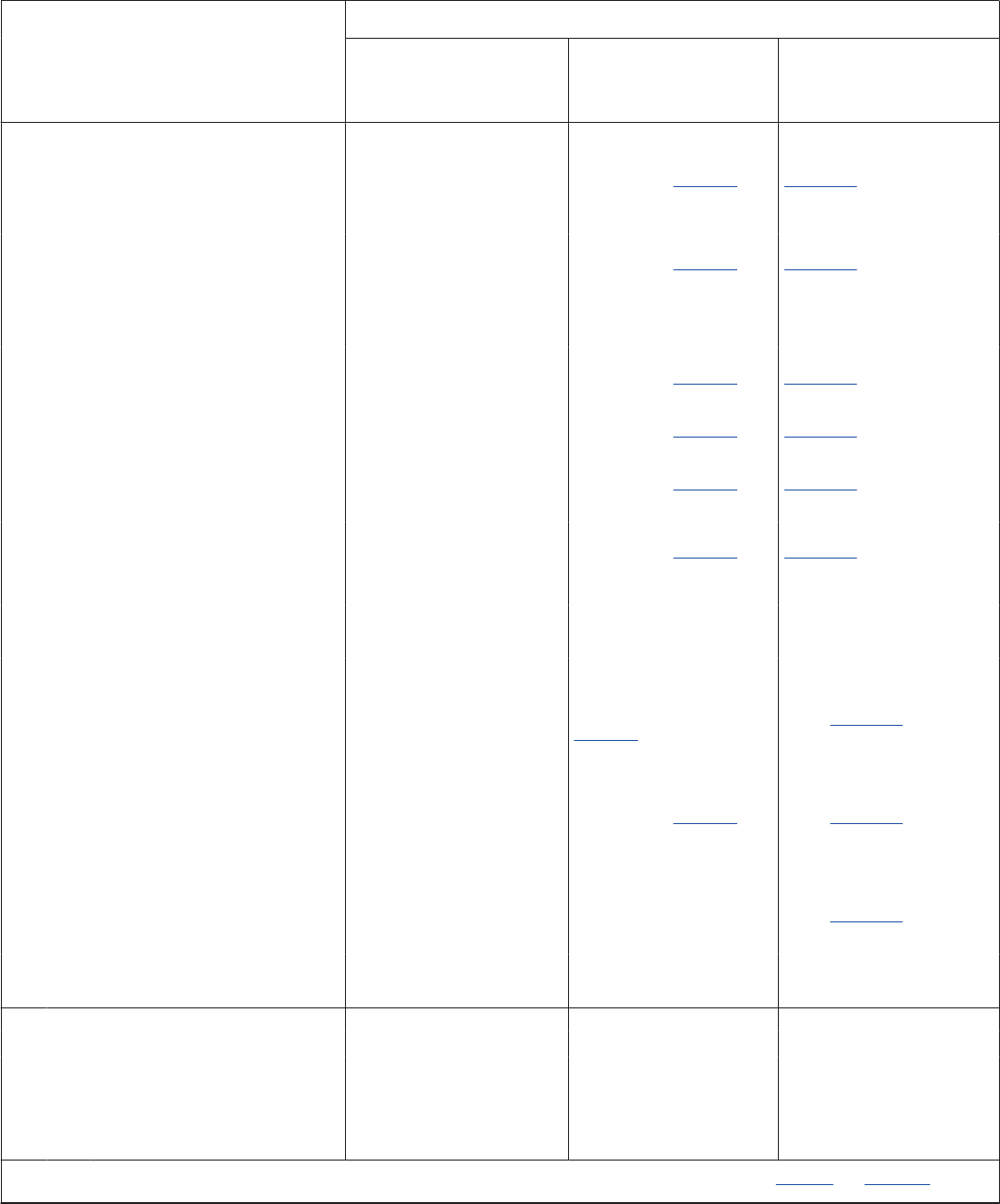

Employer Responsibilities

The following list provides a brief summary of your basic responsibilities. Because the individual circumstances for each employer

can vary greatly, responsibilities for withholding, depositing, and reporting employment taxes can differ. Each item in this list has a

page reference to a more detailed discussion in this publication.

New Employees: Page Annually (see Calendar for due dates): Page

Verify work eligibility of new employees ....... 6

File Form 944 if required (pay tax with return if

Record employees' names and SSNs from not required to deposit) ..................... 36

social security cards ....................

6

Remind employees to submit a new Form W-4

Ask employees for Form W-4 ..............

6

if they need to change their withholding .......... 24

Each Payday: Ask for a new Form W-4 from employees

Withhold federal income tax based on each

claiming exemption from income tax

employee's Form W-4 ................... 24 withholding .............................. 25

Withhold employee's share of social security Reconcile Forms 941 (Form 943 or Form 944) with

and Medicare taxes .................... 27 Forms W-2 and W-3 ....................... 38

Deposit: Furnish each employee a Form W-2 ............ 10

• Withheld income tax, File Copy A of Forms W-2 and the transmittal

• Withheld and employer social security taxes,

and

Form W-3 with the SSA ..................... 10

• Withheld and employer Medicare taxes ......

30

Furnish each payee a Form 1099 (for example,

Note. Due date of deposit generally depends Form 1099-NEC) ......................... 10

on your deposit schedule (monthly or File Forms 1099 and the transmittal Form

semiweekly). 1096 .................................. 10

Quarterly (By April 30, July 31, October 31,

File Form 940 ............................

10

and January 31):

File Form 945 for any nonpayroll income tax

Deposit FUTA tax if undeposited amount

withholding .............................. 10

is over $500 .......................... 43

File Form 941 (pay tax with return if not

required to deposit) ..................... 36

Publication 15 (2024) 7

Page 8 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

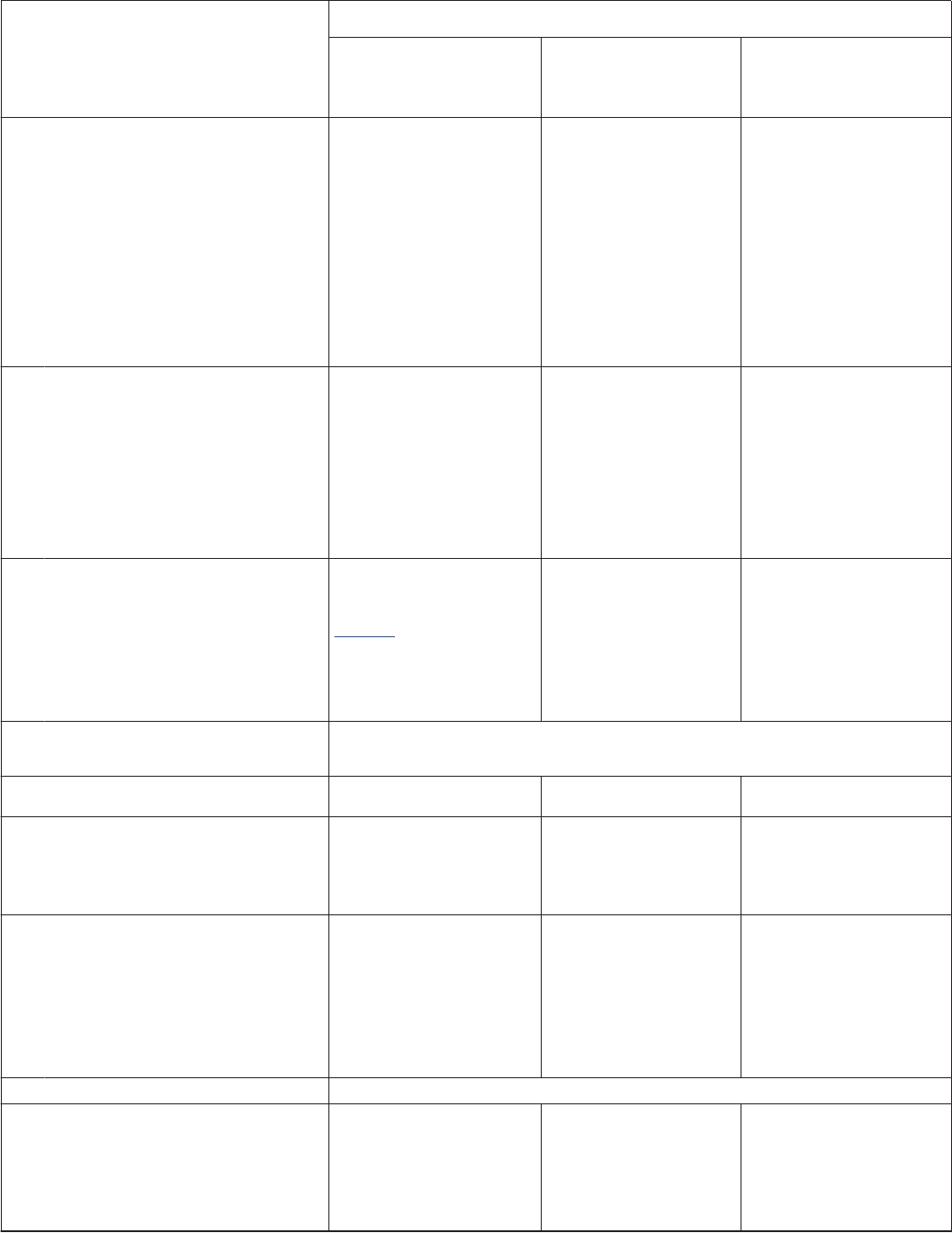

Recordkeeping

Keep all records of employment taxes for at least 4 years.

These should be available for IRS review. Your records

should include the following information.

•

Your EIN.

•

Amounts and dates of all wage, annuity, and pension

payments.

•

Amounts of tips reported to you by your employees.

•

Records of allocated tips.

•

The fair market value (FMV) of in-kind wages paid.

•

Names, addresses, SSNs, and occupations of

employees and recipients.

•

Any employee copies of Forms W-2 and W-2c

returned to you as undeliverable.

•

Dates of employment for each employee.

•

Periods for which employees and recipients were paid

while absent due to sickness or injury and the amount

and weekly rate of payments you or third-party payers

made to them.

•

Copies of employees' and recipients' income tax

withholding certificates (Forms W-4, W-4P, W-4R,

W-4S, and W-4V).

•

Dates and amounts of tax deposits you made and

acknowledgment numbers for deposits made by

EFTPS.

•

Copies of returns filed and confirmation numbers.

•

Records of fringe benefits and expense

reimbursements provided to your employees,

including substantiation.

•

Documentation to substantiate any credits claimed.

Records related to qualified sick leave wages and

qualified family leave wages for leave taken after

March 31, 2021, and before October 1, 2021, and

records related to qualified wages for the employee

retention credit paid after June 30, 2021, should be

kept for at least 6 years. For more information on

substantiation requirements, go to IRS.gov/PLC and

IRS.gov/ERC.

•

Documentation to substantiate the amount of any

employer or employee share of social security tax that

you deferred and paid for 2020.

If a crew leader furnished you with farmworkers, you

must keep a record of the name, permanent mailing

address, and EIN of the crew leader. If the crew leader

has no permanent mailing address, record their present

address.

Change of Business Name

Notify the IRS immediately if you change your business

name. Write to the IRS office where you file your returns,

using the Without a payment address provided in the

instructions for your employment tax return, to notify the

IRS of any business name change. See Pub. 1635 to see

if you need to apply for a new EIN.

Change of Business Address

or Responsible Party

Notify the IRS immediately if you change your business

address or responsible party. Complete and mail Form

8822-B to notify the IRS of a business address or

responsible party change. For a definition of “responsible

party,” see the Instructions for Form SS-4.

Filing Addresses

Generally, your filing address for Form 940, 941, 943, 944,

945, or CT-1 depends on the location of your residence or

principal place of business and whether or not you’re

including a payment with your return. There are separate

filing addresses for these returns if you’re a tax-exempt

organization or government entity. See the separate

instructions for Form 940, 941, 943, 944, 945, or CT-1 for

the filing addresses.

Private Delivery Services

(PDSs)

You can use certain PDSs designated by the IRS to meet

the “timely mailing as timely filing” rule for tax returns. Go

to IRS.gov/PDS for the current list of PDSs.

The PDS can tell you how to get written proof of the

mailing date.

For the IRS mailing address to use if you're using a

PDS, go to IRS.gov/PDSstreetAddresses. Select the

mailing address listed on the webpage that is in the same

state as the address to which you would mail returns filed

without a payment, as shown in the instructions for your

employment tax return.

PDSs can't deliver items to P.O. boxes. You must

use the U.S. Postal Service to mail any item to an

IRS P.O. box address.

Dishonored Payments

Any form of payment that is dishonored and returned from

a financial institution is subject to a penalty. The penalty is

$25 or 2% of the payment, whichever is more. However,

the penalty on dishonored payments of $24.99 or less is

an amount equal to the payment. For example, a

dishonored payment of $18 is charged a penalty of $18.

CAUTION

!

8 Publication 15 (2024)

Page 9 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

E-News for Payroll

Professionals

The IRS has a subscription-based email service for payroll

professionals. Subscribers will receive periodic updates

from the IRS. The updates may include information

regarding recent legislative changes affecting federal

payroll reporting, IRS news releases and special

announcements pertaining to the payroll industry, new

employment tax procedures, and other information

specifically affecting federal payroll tax returns. To

subscribe, go to IRS.gov/Newsroom/E-News-

Subscriptions.

Telephone Help

Tax questions. You can call the IRS Business and Spe-

cialty Tax Line with your employment tax questions at

800-829-4933.

Help for people with disabilities. You may call

800-829-4059 (TDD/TTY for persons who are deaf, hard

of hearing, or have a speech disability) with any employ-

ment tax questions. You may also use this number for as-

sistance with unresolved tax problems.

Additional information. Go to IRS.gov/

EmploymentTaxes for additional employment tax informa-

tion. For general tax information relevant to agricultural

employers, go to IRS.gov/AgricultureTaxCenter. For infor-

mation about employer responsibilities under the Afforda-

ble Care Act, go to IRS.gov/ACA. For information about

COVID-19 tax relief, go to IRS.gov/Coronavirus.

Ordering Employer Tax Forms,

Instructions, and Publications

You can view, download, or print most of the forms,

instructions, and publications you may need at IRS.gov/

Forms. Otherwise, you can go to IRS.gov/OrderForms to

place an order and have them mailed to you. The IRS will

process your order as soon as possible. Don't resubmit

requests you've already sent us. You can get forms,

instructions, and publications faster online.

Instead of ordering paper Forms W-2 and W-3,

consider filing them electronically using the SSA's free

e-file service. Go to the SSA's Employer W-2 Filing

Instructions & Information webpage at SSA.gov/employer

to register for Business Services Online (BSO). You’ll be

able to create Forms W-2 online and submit them to the

SSA by typing your wage information into easy-to-use

fill-in fields. In addition, you can print out completed

copies of Forms W-2 to file with state or local

governments, distribute to your employees, and keep for

your records. Form W-3 will be created for you based on

your Forms W-2.

The SSA's BSO is an independent program from the

Government of Puerto Rico electronic filing system.

Employers in Puerto Rico must visit Hacienda.gobierno.pr

for additional information.

Photographs of Missing

Children

The IRS is a proud partner with the National Center for

Missing & Exploited Children® (NCMEC). Photographs of

missing children selected by the Center may appear in

this publication on pages that would otherwise be blank.

You can help bring these children home by looking at the

photographs and calling 1-800-THE-LOST

(1-800-843-5678) if you recognize a child.

Calendar

The following is a list of important dates and

responsibilities. The dates listed here haven’t been

adjusted for Saturdays, Sundays, and legal holidays (see

the TIP next). Pub. 509, Tax Calendars (for use in 2024),

adjusts the dates for Saturdays, Sundays, and legal

holidays. See section 11 for information about depositing

taxes reported on Forms 941, 943, 944, and 945. See

section 14 for information about depositing FUTA tax. Due

dates for forms required for health coverage reporting

aren't listed here. For these dates, see Pub. 509.

If any date shown next for filing a return, furnishing

a form, or depositing taxes falls on a Saturday,

Sunday, or legal holiday, the due date is the next

business day. The term "legal holiday" means any legal

holiday in the District of Columbia. A statewide legal holi-

day delays a filing due date only if the IRS office where

you’re required to file is located in that state. However, a

statewide legal holiday doesn't delay the due date of fed-

eral tax deposits. See Deposits Due on Business Days

Only in section 11. For any filing due date, you’ll meet the

“file” or “furnish” requirement if the envelope containing

the return or form is properly addressed, contains suffi-

cient postage, and is postmarked by the U.S. Postal Serv-

ice on or before the due date, or sent by an IRS-designa-

ted PDS on or before the due date. See Private Delivery

Services (PDSs) under Reminders, earlier, for more infor-

mation.

Fiscal year taxpayers. The due dates listed next apply

whether you use a calendar or a fiscal year.

By January 31

File Form 941 or Form 944. File Form 941 for the

fourth quarter of the previous calendar year and deposit

any undeposited income, social security, and Medicare

taxes. You may pay these taxes with Form 941 if your to-

tal tax liability for the quarter (Form 941, line 12) is less

than $2,500. File Form 944 for the previous calendar

year instead of Form 941 if the IRS has notified you in

writing to file Form 944. Pay any undeposited income,

social security, and Medicare taxes with your Form 944.

TIP

Publication 15 (2024) 9

Page 10 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

You may pay these taxes with Form 944 if your total tax

liability for the year (Form 944, line 9) is less than

$2,500. For additional rules on when you can pay your

taxes with your return, see Payment with return in sec-

tion 11. If you timely deposited all taxes when due, you

may file by February 10.

File Form 943. Agricultural employers file Form 943

for the previous calendar year and deposit any undepos-

ited income, social security, and Medicare taxes. You

may pay these taxes with Form 943 if your total tax liabil-

ity for the year (Form 943, line 13) is less than $2,500. If

you timely deposited all taxes when due, you may file by

February 10.

File Form 945. File Form 945 to report any nonpayroll

federal income tax withheld. If you deposited all taxes

when due, you may file by February 10. See Nonpayroll

Income Tax Withholding under Reminders, earlier, for

more information.

File Form 940. File Form 940 to report any FUTA tax.

However, if you deposited all of the FUTA tax when due,

you may file by February 10. See section 14 for more in-

formation on FUTA tax.

Furnish Forms 1099 and W-2. Furnish each em-

ployee a completed 2023 Form W-2. Furnish a 2023

Form 1099-NEC to payees for nonemployee compensa-

tion. Most Forms 1099 must be furnished to payees by

January 31, but some can be furnished by February 15.

For more information, see the Guide to Information Re-

turns chart in the General Instructions for Certain Infor-

mation Returns.

File Form W-2. File with the SSA Copy A of all 2023

paper and electronic Forms W-2 with Form W-3, Trans-

mittal of Wage and Tax Statements. Forms W-2AS,

W-2CM, W-2GU, and W-2VI are filed with Form W-3SS.

Forms 499R-2/W-2PR are filed with Form W-3PR. For

more information on reporting Form W-2 information to

the SSA electronically, go to the SSA’s Employer W-2

Filing Instructions & Information webpage at SSA.gov/

employer. If filing electronically, via the SSA's Form W-2

Online service, the SSA will generate Form W-3 data

from the electronic submission of Form(s) W-2.

Send Copy 1 of Forms W-2AS, W-2CM, W-2GU, and

W-2VI, and Form W-3SS to your local tax department at

the address shown on Form W-3SS. For more information

on Copy 1, contact your local tax department. Employers

in the CNMI should contact their local tax department for

instructions on how to file Copy 1. For additional informa-

tion on how to file Forms 499R-2/W-2PR with the Puerto

Rico Department of Treasury, go to Hacienda.gobierno.pr

or call 787-622-0123.

File Form 1099-NEC reporting nonemployee compen-

sation. File with the IRS Copy A of all 2023 paper

and electronic Forms 1099-NEC. Paper forms must be

filed with Form 1096, Annual Summary and Transmittal

of U.S. Information Returns. For information on filing in-

formation returns electronically with the IRS, see Pub.

1220, Specifications for Electronic Filing of Forms 1097,

1098, 1099, 3921, 3922, 5498, and W-2G.

By February 15

Request a new Form W-4 from exempt employees.

Ask for a new Form W-4 from each employee who

claimed exemption from income tax withholding last

year.

On February 16

Forms W-4 claiming exemption from withholding ex-

pire. Any Form W-4 claiming exemption from with-

holding for the previous year has now expired. Begin

withholding for any employee who previously claimed

exemption from withholding but hasn't given you a new

Form W-4 for the current year. If the employee doesn't

give you a new Form W-4, withhold tax as if they had

checked the box for Single or Married filing separately in

Step 1(c) and made no entries in Step 2, Step 3, or Step

4 of the 2024 Form W-4. See section 9 for more informa-

tion. If the employee gives you a new Form W-4 claiming

exemption from withholding after February 15, you may

apply the exemption to future wages, but don't refund

taxes withheld while the exempt status wasn't in place.

By February 28

File paper 2023 Forms 1099 and 1096. File Copy A

of all paper 2023 Forms 1099, except Forms 1099-NEC,

with Form 1096 with the IRS. For electronically filed re-

turns, see By March 31, later.

By February 29

File paper Form 8027. File paper Form 8027, Em-

ployer's Annual Information Return of Tip Income and

Allocated Tips, with the IRS. See section 6. For electron-

ically filed returns, see By March 31 next.

By March 31

File electronic 2023 Forms 1099 and 8027. File

electronic 2023 Forms 1099, except Forms 1099-NEC,

with the IRS. Also file electronic Form 8027 with the IRS.

For information on filing information returns electroni-

cally with the IRS, see Pub. 1220 and Pub. 1239, Speci-

fications for Electronic Filing of Form 8027, Employer's

Annual Information Return of Tip Income and Allocated

Tips.

By April 30, July 31, October 31, and

January 31

Deposit FUTA taxes. Deposit FUTA tax for the quar-

ter (including any amount carried over from other quar-

ters) if over $500. If $500 or less, carry it over to the next

quarter. See section 14 for more information.

10 Publication 15 (2024)

Page 11 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

File Form 941. File Form 941 and deposit any unde-

posited income, social security, and Medicare taxes.

You may pay these taxes with Form 941 if your total tax

liability for the quarter (Form 941, line 12) is less than

$2,500. If you timely deposited all taxes when due, you

may file by May 10, August 10, November 10, or Febru-

ary 10, respectively. Don't file Form 941 for these quar-

ters if you have been notified to file Form 944 and you

didn't request and receive written notice from the IRS to

file quarterly Forms 941.

Before December 1

New Forms W-4. Remind employees to submit a new

Form W-4 if their filing status, other income, deductions,

or credits have changed or will change for the next year.

Also remind employees to submit a new Form W-4 if

they made a mid-year change to their Form W-4 based

on their use of the IRS Tax Withholding Estimator availa-

ble at IRS.gov/W4App. Employees that made a

mid-year change may be underwithheld or overwithheld

once their Form W-4 is applied to the next full calendar

year.

Introduction

This publication explains your tax responsibilities as an

employer, including agricultural employers and employers

whose principal place of business is in American Samoa,

Guam, the CNMI, the USVI, or Puerto Rico. It explains the

requirements for withholding, depositing, reporting, pay-

ing, and correcting employment taxes. It explains the

forms you must give to your employees, those your em-

ployees must give to you, and those you must send to the

IRS and the SSA. References to “income tax” in this guide

apply only to federal income tax. Contact your state or lo-

cal tax department to determine their rules. Whenever the

term "United States" is used in this publication, it includes

American Samoa, Guam, the CNMI, the USVI, and Puerto

Rico, unless otherwise noted.

When you pay your employees, you don't pay them all

the money they earned. As their employer, you have the

added responsibility of withholding taxes from their pay-

checks. The federal income tax and employees' share of

social security and Medicare taxes that you withhold from

your employees' paychecks are part of their wages that

you pay to the U.S. Treasury instead of to your employees.

Your employees trust that you pay the withheld taxes to

the U.S. Treasury by making federal tax deposits. This is

the reason that these withheld taxes are called trust fund

taxes. If federal income, social security, or Medicare taxes

that must be withheld aren't withheld or aren't deposited or

paid to the U.S. Treasury, the trust fund recovery penalty

may apply. See section 11 for more information.

This publication also provides employers, including em-

ployers in the USVI and Puerto Rico, with a summary of

their responsibilities in connection with the tax under the

Federal Unemployment Tax Act, known as FUTA tax. See

section 14 for more information.

Additional employment tax information is available in

Pubs. 15-A, 15-B, and 15-T. Pub. 15-A includes special-

ized information supplementing the basic employment tax

information provided in this publication. Pub. 15-B, Em-

ployer's Tax Guide to Fringe Benefits, contains information

about the employment tax treatment and valuation of vari-

ous types of noncash compensation. Pub. 15-T includes

the federal income tax withholding tables and instructions

on how to use the tables.

Most employers must withhold (except FUTA), deposit,

report, and pay the following employment taxes.

•

Income tax.

•

Social security tax.

•

Medicare tax.

•

FUTA tax.

There are exceptions to these requirements. See sec-

tion 15 for guidance. Railroad retirement taxes are ex-

plained in the Instructions for Form CT-1.

Comments and suggestions. We welcome your com-

ments about this publication and suggestions for future

editions.

You can send us comments through IRS.gov/

FormComments.

Or, you can write to:

Internal Revenue Service

Tax Forms and Publications

1111 Constitution Ave. NW, IR-6526

Washington, DC 20224

Although we can’t respond individually to each com-

ment received, we do appreciate your feedback and will

consider your comments and suggestions as we revise

our tax forms, instructions, and publications. Don’t send

tax questions, tax returns, or payments to the above ad-

dress.

Getting answers to your tax questions. If you have

a tax question not answered by this publication, check

IRS.gov and How To Get Tax Help at the end of this publi-

cation.

Getting tax forms, instructions, and publications.

Go to IRS.gov/Forms to download current and prior-year

forms, instructions, and publications.

Ordering tax forms, instructions, and publications.

Go to IRS.gov/OrderForms to order current forms, instruc-

tions, and publications; call 800-829-3676 to order

prior-year forms and instructions. The IRS will process

your order for forms and publications as soon as possible.

Don’t resubmit requests you’ve already sent us. You can

get forms and publications faster online.

Federal government employers. The information in this

publication, including the rules for making federal tax de-

posits, applies to federal agencies.

State and local government employers. Payments to

employees for services in the employ of state and local

Publication 15 (2024) 11

Page 12 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

government employers are generally subject to federal in-

come tax withholding but not FUTA tax. Most elected and

appointed public officials of state or local governments are

employees under common-law rules. See chapter 3 of

Pub. 963, Federal-State Reference Guide. In addition, wa-

ges, with certain exceptions, are subject to social security

and Medicare taxes. See section 15 for more information

on the exceptions.

If an election worker is employed in another capacity

with the same government entity, see Revenue Ruling

2000-6 on page 512 of Internal Revenue Bulletin 2000-6

at IRS.gov/pub/irs-irbs/irb00-06.pdf.

You can get information on reporting and social security

coverage from your local IRS office. If you have any ques-

tions about coverage under a section 218 (Social Security

Act) agreement, contact the appropriate state official. To

find your State Social Security Administrator, go to the Na-

tional Conference of State Social Security Administrators

website at NCSSSA.org.

Indian tribal governments. See Pub. 4268 for employ-

ment tax information for Indian tribal governments.

Disregarded entities and qualified subchapter S sub-

sidiaries (QSubs). Eligible single-owner disregarded en-

tities and QSubs are treated as separate entities for em-

ployment tax purposes. Eligible single-member entities

must report and pay employment taxes on wages paid to

their employees using the entities' own names and EINs.

See Regulations sections 1.1361-4(a)(7) and

301.7701-2(c)(2)(iv).

Useful Items

You may want to see:

Publication

15-A Employer's Supplemental Tax Guide

15-B Employer's Tax Guide to Fringe Benefits

15-T Federal Income Tax Withholding Methods

225 Farmer's Tax Guide

535 Business Expenses

583 Starting a Business and Keeping Records

1635 Employer Identification Number:

Understanding Your EIN

1. Employer Identification

Number (EIN)

If you’re required to report employment taxes or give tax

statements to employees or annuitants, you need an EIN.

The EIN is a nine-digit number the IRS issues. The dig-

its are arranged as follows: 00-0000000. It is used to iden-

tify the tax accounts of employers and certain others who

have no employees. Use your EIN on all of the items you

send to the IRS and the SSA. For more information, see

Pub. 1635.

15-A

15-B

15-T

225

535

583

1635

If you don’t have an EIN, you may apply for one online

by going to IRS.gov/EIN. You may also apply for an EIN by

faxing or mailing Form SS-4 to the IRS. If the principal

business was created or organized outside of the United

States or U.S. territories, you may also apply for an EIN by

calling 267-941-1099 (toll call). Don't use an SSN in place

of an EIN.

You should have only one EIN. If you have more than

one and aren't sure which one to use, call 800-829-4933

or 800-829-4059 (TDD/TTY for persons who are deaf,

hard of hearing, or have a speech disability). Give the

numbers you have, the name and address to which each

was assigned, and the address of your main place of busi-

ness. The IRS will tell you which number to use. For more

information, see Pub. 1635.

If you took over another employer's business (see Suc-

cessor employer in section 9), don't use that employer's

EIN. If you’ve applied for an EIN but don't have your EIN

by the time a return is due, file a paper return and enter

“Applied For” and the date you applied for it in the space

shown for the number.

Always be sure the EIN on the form you file ex-

actly matches the EIN the IRS assigned to your

business. Don't use your SSN or individual tax-

payer identification number (ITIN) on forms that ask for an

EIN. If you used an EIN (including a prior owner's EIN) on

Form 941, Form 943, or Form 944, that is different from

the EIN reported on Form W-3, see Box h—Other EIN

used this year in the General Instructions for Forms W-2

and W-3. On Form W-3PR for Puerto Rico, “Other EIN

used this year” is reported in box f. The name and EIN on

Form 945 must match the name and EIN on your informa-

tion returns where federal income tax withholding is repor-

ted (for example, backup withholding reported on Form

1099-NEC). Filing a Form 945 with an incorrect EIN or us-

ing another business's EIN may result in penalties and de-

lays in processing your return.

Agricultural employers that have crew leaders. An

agricultural employer must record the crew leader's name,

address, and EIN. See sections 2 and 14.

2. Who Are Employees?

Generally, employees are defined either under common

law or under statutes for certain situations. See Pub. 15-A

for details on statutory employees and nonemployees.

Employee status under common law. Generally, a

worker who performs services for you is your employee if

you have the right to control what will be done and how it

will be done. This is so even when you give the employee

freedom of action. What matters is that you have the right

to control the details of how the services are performed.

See Pub. 15-A for more information on how to determine

whether an individual providing services is an independ-

ent contractor or an employee.

Generally, people in business for themselves aren't em-

ployees. For example, doctors, lawyers, veterinarians, and

CAUTION

!

12 Publication 15 (2024)

Page 13 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

others in an independent trade in which they offer their

services to the public are usually not employees. If the

business is incorporated, corporate officers who work in

the business are employees of the corporation.

If an employer-employee relationship exists, it doesn't

matter what it is called. The employee may be called an

agent or independent contractor. It also doesn't matter

how payments are measured or paid, what they’re called,

or if the employee works full or part time.

Statutory employees. If someone who works for you

isn't an employee under the common-law rules discussed

earlier, don't withhold federal income tax from their pay,

unless backup withholding applies. Although the following

persons may not be common-law employees, they’re con-

sidered employees by statute for social security and Medi-

care tax purposes if the conditions under Tests, later, are

met.

a. An agent or commission driver who delivers meat, veg-

etable, fruit, or bakery products; beverages (other than

milk); laundry; or dry cleaning for someone else.

b. A full-time life insurance salesperson who sells primar-

ily for one company.

c. A homeworker who works at home or off premises by

the guidelines of the person for whom the work is done,

with materials or goods furnished by and returned to that

person or to someone that person designates.

d. A traveling or city salesperson (other than an agent or

commission driver) who works full time (except for sideline

sales activities) for one firm or person getting orders from

customers. The orders must be for merchandise for resale

or supplies for use in the customer's business. The cus-

tomers must be retailers, wholesalers, contractors, or op-

erators of hotels, restaurants, or other businesses dealing

with food or lodging.

Tests. Withhold social security and Medicare taxes

from statutory employees' wages if all three of the follow-

ing tests apply.

1. The service contract states or implies that almost all

of the services are to be performed personally by

them.

2. They have little or no investment in the equipment and

property used to perform the services (other than an

investment in transportation facilities).

3. The services are performed on a continuing basis for

the same payer.

Persons in a or d, earlier, are also employees for FUTA

tax purposes if tests 1 through 3 are met.

Pub. 15-A gives examples of the employer-employee

relationship.

Statutory nonemployees. Direct sellers, qualified real

estate agents, and certain companion sitters are, by law,

considered nonemployees. They’re generally treated as

self-employed for all federal tax purposes, including in-

come and employment taxes. See Pub. 15-A for more in-

formation.

Farmworkers. In general, you're an employer of farm-

workers if your employees:

•

Raise or harvest agricultural or horticultural products

on your farm (including the raising and feeding of live-

stock);

•

Work in connection with the operation, management,

conservation, improvement, or maintenance of your

farm and its tools and equipment, if the major part of

such service is performed on a farm;

•

Provide services relating to salvaging timber, or clear-

ing land of brush and other debris, left by a hurricane

(also known as hurricane labor), if the major part of

such service is performed on a farm;

•

Handle, process, or package any agricultural or horti-

cultural commodity in its unmanufactured state if you

produced over half of the commodity (for a group of up

to 20 unincorporated operators, all of the commodity);

or

•

Do work for you related to cotton ginning, turpentine,

gum resin products, or the operation and maintenance

of irrigation facilities.

For this purpose, the term “farm” includes stock, dairy,

poultry, fruit, fur-bearing animal, and truck farms, as well

as plantations, ranches, nurseries, ranges, greenhouses

or other similar structures used primarily for the raising of

agricultural or horticultural commodities, and orchards.

Farmwork doesn't include reselling activities that don't

involve any substantial activity of raising agricultural or

horticultural commodities, such as a retail store or a

greenhouse used primarily for display or storage. It also

doesn’t include processing services which change a com-

modity from its raw or natural state, or services performed

after a commodity has been changed from its raw or natu-

ral state.

Crew leaders. If you're a crew leader, you're an em-

ployer of farmworkers. A crew leader is a person who fur-

nishes and pays (either on their own behalf or on behalf of

the farm operator) workers to do farmwork for the farm op-

erator. If there is no written agreement between you and

the farm operator stating that you're their employee and if

you pay the workers (either for yourself or for the farm op-

erator), then you're a crew leader. For FUTA tax rules, see

section 14.

If you're a crew leader, you're not considered the em-

ployee of the farm operator for services you perform in fur-

nishing farmworkers and as a member of the crew.

H-2A agricultural workers. On Form W-2, don't

check box 13 (Statutory employee), as H-2A workers

aren't statutory employees.

Treating employees as nonemployees. You’ll gener-

ally be liable for social security and Medicare taxes and

withheld income tax if you don't deduct and withhold these

taxes because you treated an employee as a nonem-

ployee. You may be able to figure your liability using

Publication 15 (2024) 13

Page 14 of 57 Fileid: … ations/p15/2024/a/xml/cycle06/source 14:07 - 19-Dec-2023

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

special section 3509 rates for the employee share of so-

cial security and Medicare taxes and federal income tax

withholding. The applicable rates depend on whether you

filed required Forms 1099. You can't recover the employee

share of social security tax, Medicare tax, or income tax

withholding from the employee if the tax is paid under sec-

tion 3509. You’re liable for the income tax withholding re-

gardless of whether the employee paid income tax on the

wages. You continue to owe the full employer share of so-

cial security and Medicare taxes. The employee remains

liable for the employee share of social security and Medi-

care taxes. See section 3509 for details. Also see the In-

structions for Form 941-X, the Instructions for Form 943-X,

or the Instructions for Form 944-X.

Section 3509 rates aren't available if you intentionally

disregard the requirement to withhold taxes from the em-

ployee or if you withheld income taxes but not social se-

curity or Medicare taxes. Section 3509 isn't available for

reclassifying statutory employees. See Statutory employ-

ees, earlier in this section.

If the employer issued required information returns, the

section 3509 rates are the following.

•

For social security taxes: employer rate of 6.2% plus