Introduction to online

payments

Introduction to online payments 2

Introduction

This guide covers the basics of online payments and explains the dierences for common business

models: online retailers, SaaS and subscription companies, and platforms and marketplaces. Start

by reading about payment fundamentals and what all businesses need to know about online

payments, and then go directly to the section about your business model.

We’ve also put together a list of the most common industry terms and their definitions, so if

you’re unfamiliar with any phrases in this guide, refer to the glossary.

Payments fundamentals

Before diving into payment details for dierent business models, it’s helpful to have a high-level

understanding of how payments work: how money moves from a customer to your business,

how banks facilitate these payments, and the costs involved in the system. Learning about these

fundamental building blocks of online payments will help you better understand the nuances of

the payments setup for your own business model.

Online payments flow

There are four major players involved in each online transaction:

Cardholder: The person who owns a credit card

Merchant: The business owner

Acquirer: A bank that processes credit card payments on behalf of the merchant and

routes them through the card networks (such as Visa or Mastercard) to the issuing bank.

Sometimes acquirers may also partner with a third party to help process payments.

Issuing bank: The bank that extends credit and issues cards to consumers.

To accept online card payments, you need to work with each one of these players (either via a

single payments provider or by building your own integrations).

First, you’ll need to set up a business bank account and establish a relationship with an acquirer

or payment processor. Acquirers and processors help route payments from your website to

card networks, such as Visa and Mastercard. Depending on your setup, you may have a separate

If you want to start accepting online payments right away, read our docs to get started.

1

2

3

4

Introduction to online payments 3

acquirer (oen a bank that maintains network relationships) and processor (which partners with

the acquirer to facilitate transactions), or a single relationship that includes both services.

In order to securely capture payment details, you may also need a gateway, which helps properly

secure information. Gateways frequently use tokenization to anonymize payment details and keep

sensitive data out of your systems, helping you meet industry-wide security guidelines called

PCI standards.

A single provider can oer gateway, processing, and acquiring services, which can help streamline

your online payments. Sometimes, the payments provider will build direct integrations with the

card networks, helping to reduce third-party dependencies.

When you accept a payment online, the gateway will securely encrypt the data to be sent to the

acquirer, and then to the card networks. The card networks then communicate with the issuing

bank, which either confirms or denies the payment (bank rules or regulatory requirements may

sometimes require additional card authentication, like 3D Secure, before accepting a payment).

The issuing bank will relay the message back to the gateway or acquirer so you can confirm the

payment with the customer (by displaying a “payment accepted” or “payment declined” message

on your site, for example).

This describes the online payment flow for one-time payments using U.S. dollars in the U.S. If

you want to expand internationally, you may need to find a bank partner and set up relationships

locally. Or, if you introduce a new product and want to start charging customers on a recurring

basis, you would need to not only accept the credit card number, but also accurately initiate

and collect payments at a set time interval. You would also need to build logic to accommodate

dierent pricing models, figure out how to recover failed payments, manage prorations when

customers switch plans, and more.

Costs involved in online payments

There are a variety of fees that accompany each transaction processed through this four-party

system. Visa, Mastercard and other card networks set the fees, referred to as interchange and

scheme fees.

CARDHOLDER ACQUIRER

MERCHANT ISSUING

BANK

CARD

NETWORK

PAYMENT

GATEWAY

Online payment flow

Introduction to online payments 4

Interchange typically represents the bulk of the costs involved in a transaction. This amount is

given to the issuing bank because it takes on the greatest amount of risk by extending credit or

banking services to the cardholder.

Scheme fees are collected by the card networks themselves and can include additional

authorization and cross-border transaction fees. Fees can also be assessed for refunds and other

network services.

Together, these fees make up the network costs. These vary depending on the card type,

transaction location, channel (in-person or online), and Merchant Category Code (MCC). For

example, a transaction made with a rewards credit card would incur higher network fees than a

transaction with a non-rewards card since banks oen use these fees to subsidize the cost of the

rewards program.

For all businesses accepting online payments

This section covers two important topics for all businesses accepting payments: how the online

payments funnel can increase your conversion, and how adding the right payment methods can

expand your pool of potential customers.

Online payments funnel

Transactions go through three steps to make a purchase: checkout completion, fraud protection,

and network acceptance. Conversion happens when a transaction is successfully completed.

Through each stage of the funnel, your pool of potential customers can gradually shrink. If you

have a long or complicated checkout process, a fraction of customers will fall o. Then, when you

factor in fraud and average transaction acceptance rates, the pool shrinks even more.

INTERCHANGE FEE

A fee paid to the

issuing bank

SCHEME FEE

Fees collected by

the card network

NETWORK COSTS

The total of interchange

and scheme fees

Online payment fees

Stripe’s standard pay-as-you-go pricing oers a single, transparent rate for all card payments,

helping give you more predictability over your payment costs. Learn more.

Introduction to online payments 5

Understanding the interaction between these steps is important to optimizing your entire funnel.

This is especially true for businesses that have separate teams owning checkout, fraud, and

network acceptance, with each one optimizing for their own metrics. For example, if the team

working on checkout completion solely focuses on reducing cart abandonment rates, they may

ask for less customer information to reduce friction. However, this can result in more fraud since

you’re not always capturing details like the full billing address and ZIP code to help validate the

transaction.

In this section, we’ll give you an overview of the online payments funnel and share best practices

to increase conversion.

Designing the best checkout forms

The online payments funnel starts with the checkout experience, where customers enter their

payment information to purchase goods or services. At this stage, you want to collect enough

details to be able to verify that customers are who they say they are, but avoid adding too much

friction to the checkout process—which can cause customers to abandon it altogether.

If your checkout form is too complicated, you risk losing sales from the most likely buyers—

customers with items in their cart and every intention to make a purchase. In fact, 87% of

customers abandon a purchase if the checkout process is too dicult.

To improve your checkout completion rate, the first step is to go through your own checkout

process from the customer’s point of view and look for any friction that could lead to drop o.

Pay attention to how long the site takes to load, how many fields are in your form, and if your

checkout process supports autofill.

The best checkout forms adapt to the customer’s experience. For example, it’s best practice to

oer responsive checkout forms that automatically resize to the smaller screen of a mobile device

and oer a numerical keypad when customers are prompted to enter their card information. You

should also consider supporting mobile wallets, such as Apple Pay or Google Pay, to bypass manual

data entry.

If you choose to expand internationally, your checkout form should cater to each market. Allowing

customers to pay in their local currency is a start, but you also need to support local payment

CHECKOUT

COMPLETION

FRAUD

PROTECTION

NETWORK

ACCEPTANCE

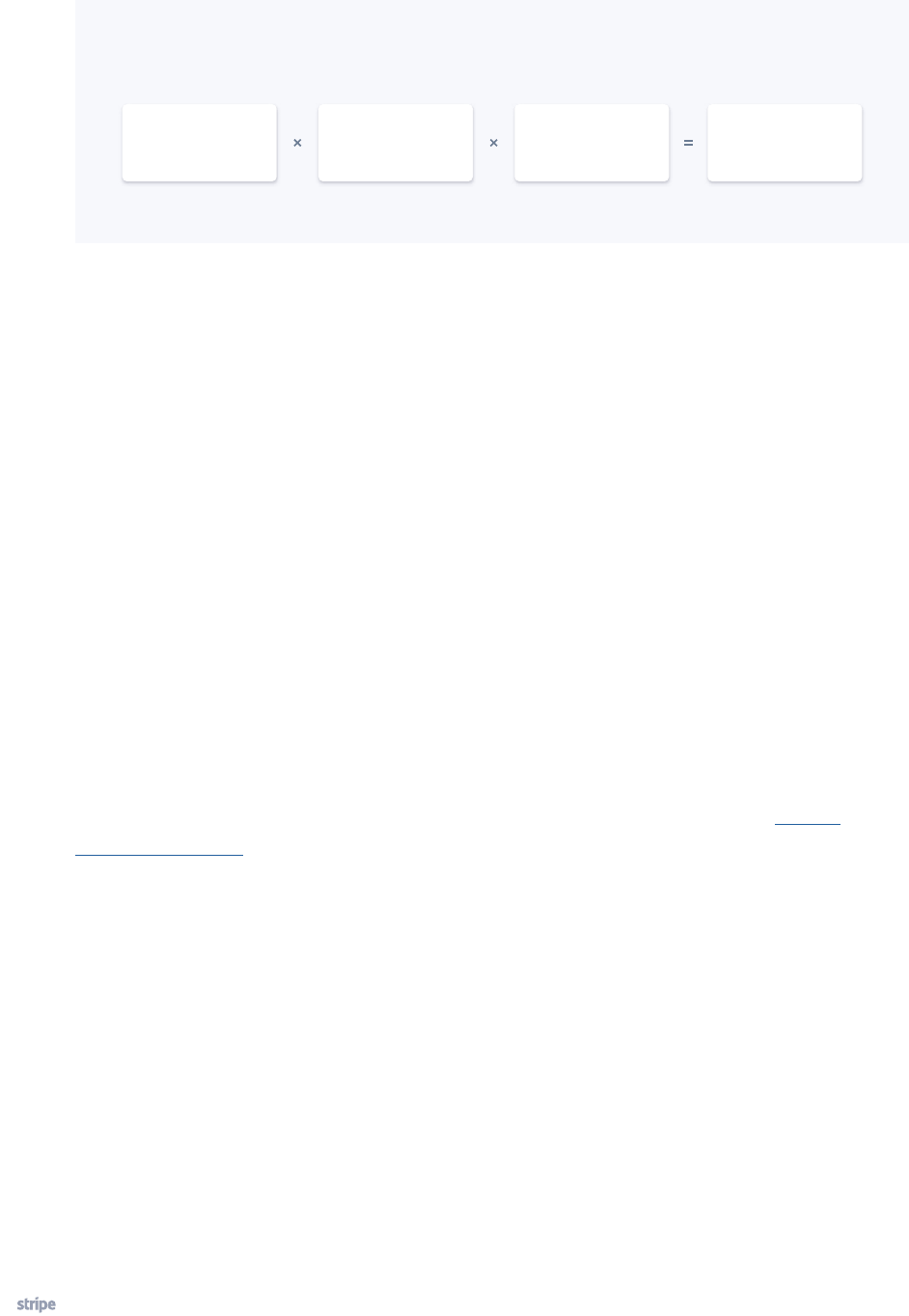

CONVERSION

The conversion equation

Introduction to online payments 6

methods to provide the most relevant experience. For example, more than half of customers in

the Netherlands prefer to pay with iDEAL, a payment method which directly transfers funds from

a customer’s bank account to the business.

The card number can also indicate where a customer is located geographically, allowing you to

dynamically change the form fields to capture the right information for each country. For example,

if your form recognizes a U.K. card, you should add a field to capture the postcode. If your form

recognizes an American card, you should change that field to ZIP code.

Managing risk online

The next step is to evaluate whether a transaction is fraudulent. The majority of illegitimate

payments involve fraudsters pretending to be legitimate customers by using stolen cards and

card numbers.

For example, if a fraudster makes a purchase on your website using a stolen card number that

hasn’t been reported, it’s possible the payment would be processed successfully. Then, when the

cardholder discovers the fraudulent use of the card, he or she would question the payment with

his or her bank by filing a chargeback. While you have the chance to dispute this chargeback by

submitting evidence about whether the payment was valid, card network rules tend to favor the

customer in most disputes. If your business loses a dispute, your business would lose the original

transaction amount. You, as the business owner, would also have to pay a chargeback fee, the cost

associated with the bank reversing the card payment.

While chargebacks are a part of accepting payments online, the best way to manage them is to

prevent them from happening in the first place. There are two primary approaches: rules-based

logic and machine learning.

Rules-based fraud detection operates on an “If x happens, then do y” logic created and is managed

on an ongoing basis by fraud analysts. Examples include blocking all transactions from a certain

country, IP address, or above a certain dollar amount. However, because this logic is based on

strict rules, it doesn’t recognize hidden patterns nor does it adapt to shiing fraud vectors by

analyzing information beyond these defined parameters. As a result, analysts are oen playing

catch up—manually creating new rules aer they detect fraud rather than proactively

fighting fraud.

Fraud management based on machine learning, on the other hand, can use transaction data to

train algorithms that learn and adapt. Some machine learning models mimic the behavior of

human reviewers, while others are trained by millions of data points. These models learn how to

Stripe Checkout is a drop-in payments page designed to drive conversion. It dynamically

surfaces mobile wallets when appropriate and supports 15 languages so customers can use

a checkout form that’s personalized and relevant. Learn more.

Introduction to online payments 7

discern legitimate transactions from those that are potentially fraudulent. Some of these models

can even train themselves, making them more scalable and ecient than rules-based logic.

For example, let’s say a customer with normal browsing behavior and a suspicious IP address

wants to purchase something from your site. Machine learning decides how much weight each

of these signals should carry. For example, should the transaction be declined solely based on the

IP address? A rules-based system may block all transactions from that location, but a machine

learning model should be able to distinguish between good and bad transactions from by

weighting the location alongside all the other information available to determine the probability

that a given payment will result in a chargeback.

Combining these two approaches—rules-based logic and machine learning fraud management—

can be a powerful, customizable solution. You are able to leverage the sophistication of machine

learning, but also customize the approach and encode logic that is specific to your business. For

example, you can set custom rules based on the risk level of a subset of your users and what they

are buying.

For more information, read our guide on machine learning for fraud detection.

Risk score assigned

0–100

Charge features

Behavioral

Device fingerprint

Historical

Machine learning fraud detection

LOW

Allow

HIGH

Block

Data points

Stripe Radar is a suite of modern tools for fraud detection and prevention. Its core is powered

by adaptive machine learning, with algorithms evaluating every transaction for fraud risk and

taking appropriate actions. Radar is included for free as part of Stripe’s integrated pricing.

Users can upgrade to Radar for Fraud Teams to set their own rules-based logic, and use other

powerful tools for fraud professionals.

Introduction to online payments 8

Improving network acceptance

The last step in the online payments funnel is card network acceptance: having the issuing bank

successfully process the payment.

When customers make a purchase, a payment request is sent to the issuing bank. Based on a

variety of factors, ranging from your customer’s available balance, the formatting of transaction

metadata, or even system downtime, the issuing bank will either accept or decline the request.

The higher your acceptance rate, the more transactions you’ve been able to successfully process.

You can help reduce unnecessary declines by collecting additional data or passing through

details like CVC, billing address, and ZIP code during checkout. This information gives the issuing

bank extra information about the transaction, helping improve the chances of acceptance for

legitimate transactions.

Global payment methods

While cards are the predominant online payment method in the U.S., 40% of consumers outside

the U.S. prefer to use a payment method other than a credit card, including bank transfers and

digital wallets (such as Alipay, WeChat Pay, or Apple Pay). You may lose sales simply because you

don’t oer the preferred payment methods of a global audience.

To capitalize on a global customer base, you need to oer the payment methods that are most

commonly used in the countries in which you operate. There are the five common types of

payment methods:

Credit cards allow customers to borrow funds from a bank and either pay the balance in full

each month or pay the money back with interest. Debit cards make payments by deducting

money directly from a customer’s checking account, rather than using a line of credit.

Digital wallets, including Apple Pay and Google Pay, let customers pay for products or

services electronically by linking a card or bank account. Digital wallets can also allow

customers to store monetary value directly in the app with top-ups.

Bank debits and transfers move money directly from a customer’s bank account. Account

debits collect your customers’ banking information and pull funds from their accounts (for

example, ACH in the U.S.). Credit transfers link to customers’ bank accounts and they push

1

2

3

Stripe helps automatically improve network acceptance for businesses thanks to direct

network integrations and industry partnerships that provide additional data and insights into

the reasons for declines. We use this to build machine learning models that identify the best

ways to update payment metadata to improve the chances of acceptance. Learn more.

Introduction to online payments 9

money to you (like wire transfers). There are also payment methods like Giropay in Germany

and iDEAL in the Netherlands that operate as a layer on top of banks to facilitate transfers,

but look more like digital wallets.

Buy now, pay later is a growing category of payment methods that oers customers

immediate financing for online payments, typically repaid in fixed installments over time.

Examples include Aerpay, Klarna, and Arm.

Cash-based payment methods, from companies like OXXO and Boleto, allow customers to

make online purchases without a bank account. Instead of paying for a product or service,

customers receive a scannable voucher with a transaction reference number that they can

then bring to an ATM, bank, convenience store, or supermarket and make a payment in cash.

Once the reference number for the cash payment is matched to the initial purchase, the

business gets paid and can ship the product.

For more information, read our guide to payment methods.

Online retailers

Read this section if you want to sell goods in-person at retail locations in addition to your website

or mobile app.

Increasingly, retailers that started as online-only operations are finding success in expanding

into the physical world by opening in-person locations. With more than 90% of purchases still

happening in person, this creates the potential for digital businesses to create a new revenue

stream.

The challenge, however, is unifying data across your online and in-person payments. Customers

expect to engage with your business in the same way across channels and, as part of that, how

they make a purchase needs to be consistent and on-brand. For example, users may expect

discount codes and promotions to apply to both online and in-person purchases.

Here are two things you need to know if you want to expand your online business to support in-

person sales:

Leverage existing infrastructure

Retailers oen have to set up two seperate payment providers: one for online and one

for in-person purchases. This requires two integrations and two separate accounts,

doubling the amount of work required to get started, making it hard to manage financial

reconciliation, and oen siloing customer data within each account.

4

5

Stripe lets you support dozens of payment methods with a single integration. Learn more.

1

Introduction to online payments 10

Instead, make sure you leverage your existing payments infrastructure—what you already

set up for online payments—rather than onboarding a new vendor. This not only saves you

time and resources, it also simplifies reporting and helps create a more unified customer

experience.

This creates a seamless payments experience whether customers make a purchase on their

smartphone or walk into your store. For example, customers could start a subscription

in person that continues online. The payment method they used in the store would be

saved to their online profile, where they would be able to update any details or change the

subscription cadence.

Support chip cards and mobile wallets

Magnetic stripe cards increase a business’s exposure to risk because they’re easy for

fraudsters to copy and require additional steps to encrypt customer payment information.

As a result, EMV chip cards—which are more secure and protect businesses from liability in

the event of fraud—have been the global standard for decades.

In 2015, the U.S. began its transition to chip cards and today, they are used for the majority

of credit card transactions. However, there are still businesses that use older card readers

that support magnetic stripe cards. As you’re evaluating hardware to accept in-person

payments, it’s important to pick a newer card reader that allows you to accept chip cards.

You should also consider supporting mobile wallets, such as Apple Pay and Google Pay,

for in-person transactions. Like chip cards, they securely encrypt payment information

and minimize your liability associated with fraudulent transactions. Mobile wallets also

improve the payment experience, making transactions more convenient and streamlined for

customers.

SaaS and subscription companies

Read this section if you charge your customers on a recurring basis or use stored payment

information.

When managing recurring revenue, there’s a lot of complexity around how you initiate and collect

payments, and accommodate dierent pricing models. You must store customers’ payment

information and accurately charge them at set time intervals.

Stripe Terminal helps you unify your online and oine channels with flexible developer tools,

pre-certified card readers, and cloud-based hardware management.

2

Introduction to online payments 11

There are two ways to set this up: build your own payments system or buy existing soware.

Either way, you need to make sure your billing system can accept orders from a web or mobile

checkout, correctly bill the customer based on the pricing model (flat-rate billing or tiered pricing,

for example), and collect payments using whichever payment methods customers prefer to use.

You also need the ability to surface insights that are important for recurring businesses, including

churn, monthly recurring revenue, and other key subscription metrics—or integrate with your

customer relationship management system or account system.

As you decide whether to build your own soware from scratch or buy an existing one, think

about the opportunity costs. Consider the ongoing engineering resources required to build and

maintain your billing soware versus the other needs of your business.

Here are three considerations for SaaS and subscription payments:

Set flexible subscription logic

Subscription logic is made up of time-based and price-based rules that, together, accurately

charge your customers on a predetermined cadence. When you only have one product and

simple pricing, like $25 per month for a soware subscription, setting up this logic in your

billing system is easy because the dollar amount doesn’t change from month to month.

Over time, you may expand your business to add new products and promotions. You need

to ensure that your subscription logic can handle this growth with the ability to experiment

with dierent pricing models, like flat-rate, per-seat, or metered subscriptions, tiered pricing,

freemium, and free trials. You may also want the ability to oer bundles or discounts.

Your subscription logic should also be flexible enough to account for customers changing

plans at any time. If someone wants to switch to a cheaper plan mid-month, you have to

prorate the costs of both plans and ensure that the customer will be charged for the right

amount going forward.

Think about your invoicing needs

Customers usually prefer to receive an invoice if you’re charging them for a large amount

or sending a one-o bill (both of which are common for SaaS companies that have other

businesses as their customers).

To send invoices, think about what the creation process should look like: do invoices

have the same line items or does each one need to be customized? Depending on which

countries you are operating in, you also have to follow dierent invoice requirements. For

example, you may have to follow sequential invoice numbering or set invoice prefixes at

either the customer or account level.

Then, you need a way to send the invoices to your customers. Think about whether you

want to manually send them via email or if your billing solution can automate this process

for you.

2

1

Introduction to online payments 12

Minimize involuntary churn

Most SaaS and subscription companies face involuntary churn issues, where customers

intend to pay for a product but their payment attempt fails due to expired cards, insucient

funds, or outdated card details (9% of subscription invoices fail on the first charge attempt

due to involuntary churn).

When you only have a handful of failed payments a month, it’s easy to call or email each

customer and ask him or her to remedy the situation (whether that’s by using a new

payment method or updating payment information). However, as your business grows and

you have to manage hundreds of customers with failed payments, this approach becomes

less manageable.

A more scalable way to communicate with your customers is to send automated failed

payment emails whenever a payment is declined.

In addition to outbound communication, you can also retry payments directly. Many

businesses will retry failed transactions on a set schedule, like every seven days (this process

is known as dunning). Experiment with dierent cadences to learn what is most eective for

your business or find a payments provider that automates the dunning process and allows

you to adapt it based on your customers’ preferences.

Platforms and marketplaces

Read this section if you are a soware platform and enable other businesses to accept payments

directly from their customers (like Shopify) or if you are a marketplace, where you collect payments

from customers and then pay them out to sellers or service providers (like Ly).

Platforms and marketplaces have some of the most complex payment requirements because

they accept money on behalf of sellers or service providers and issue payouts to them. As a result,

there are many unique considerations, including verifying sellers’ identities, compliantly managing

money transmission, taking a service fee from each payment, and filing 1099s with the IRS

when applicable.

However, providing payments functionality to your customers allows you to dierentiate your

platform or marketplace and add value for your sellers or service providers. You can help them

launch businesses faster without having to worry about lengthy merchant account applications or

writing code to be able to accept payments.

Stripe Billing oers an end-to-end billing solution. You can create and manage subscription

logic and invoices, accept any supported payment method, and reduce involuntary churn

with smart retry logic.

3

Introduction to online payments 13

Traditionally, adding payments functionality required you to become licensed, and register and

maintain status as a payment facilitator with card networks (such as Visa or Mastercard). Since

you are seen as controlling the flow of funds when you move money between buyers and sellers,

the card networks apply strict regulations. This process can take months (sometimes years) and

require millions of dollars in upfront and ongoing costs.

Today, however, several options exist for platforms and marketplaces to add customized payments

capabilities for their customers and earn revenue from payments, without having to register as a

payment facilitator themselves.

Here are two capabilities you need to consider when adding payments to your platform or

marketplace:

Verify users during onboarding

Before you accept any money on behalf of your sellers or businesses, you need to onboard

them to your payment system and verify their identity. This step is complicated due to

stringent laws and regulations including Know Your Customer (KYC) laws and sanctions

screening requirements, which carry penalties and fines for violations. In addition to

government regulations, which can vary from country to country, card networks including

Visa and Mastercard have their own information collection requirements, which are

regularly updated.

Balancing these information requirements with the user experience is delicate. On the one

hand, you want to collect as much information as possible (such as full name, email, date of

birth, last four digits of their social security number in the U.S., phone number, and address)

to ensure your platform isn’t being used for nefarious purposes like money laundering or

terrorist financing. You also want to avoid penalties with regulatory bodies and financial

partners.

On the other hand, you want to make your user experience better than the competition.

That means providing a low-friction onboarding experience, which isn’t always compatible

with detailed information requests.

To help remove friction, consider collecting data in a phased approach and auto-completing

fields for your users when possible. For example, you could only ask for sellers’ or service

providers’ tax information once they pass an IRS reporting threshold. And, you could pre-

populate fields for their legal name and address if you already collected this information.

Support different ways to move money

Paying your users involves more than just moving money from point A to point B. You need

the ability to collect service fees for your platform, split and route funds among sellers, and

control when payouts are sent to your sellers’ bank accounts.

1

2

Introduction to online payments 14

Let’s say you run an e-commerce platform and a customer makes a $50 purchase from a

seller. You need to think about three parties: your platform, your sellers or service providers,

and their buyers or end-users. Before you pay the seller, you need to take your platform

fee. Then, you need to figure out how and when to send the remaining funds to the seller.

Do you send the payout immediately upon receipt of the goods or services, or do you

aggregate the funds and pay out every week? Do you have the correct banking information

to route the payment?

You also need to ensure you’re moving money in a compliant way. For example, in the U.S.,

46 states require their own licenses to move money on behalf of others. In Europe, PSD2

laws require licensing for payment intermediaries. If you are deemed a money transmitter or

payment intermediary by a regulatory body and are not licensed, you can be fined or at risk

of being shut down.

Depending on your business model, you should be able to support a number of dierent

ways of moving money, such as:

- One-to-one: One customer is charged and one recipient is paid out (e.g. a ride-

sharing service).

- One-to-many: One transaction is split between multiple sellers or recipients (e.g.

a retail marketplace where a customer purchases one “cart” with items sourced

from multiple online stores).

- Holding funds: A platform accepts funds from customers and holds them in

reserve before paying out recipients (e.g. a ticketing platform that pays recipients

only aer an event has taken place).

- Account debits: A platform performs a debit or transaction reversal to pull

funds from its sellers or service providers (e.g. an e-commerce platform pulling a

monthly store maintenance fee from its business customers).

- Subscriptions: A platform allows its sellers to collect a recurring charge from

customers (e.g. a SaaS platform enables its nonprofits to accept recurring

donations).

Stripe Connect enables platforms and marketplaces to facilitate payments for their sellers,

service providers, and customers. It supports onboarding and verification, allows you to accept

135+ currencies and dozens of local payment methods around the world with built-in fraud

protection, pay out users, and track the flow of funds

Introduction to online payments 15

Additional reading

We hope this guide gave you a high-level overview of online payments and helped you understand

the nuances of your own payments setup.

This is our first guide in a series about the fundamentals of online payments. We’ll continue to

explore foundational concepts, like in-person and recurring payments, as well as more advanced

topics like declines and payout management, in future guides.

In the meantime, here is some additional reading:

All businesses accepting payments

• A guide to payment methods

• A guide to PCI compliance

• A primer on machine learning for fraud detection

• 3D Secure 2: A new authentication standard

Online retailers

• How to use Stripe Terminal to accept in-person payments

SaaS companies

• How to create and charge for a subscription with Stripe

• A guide to SaaS businesses and how to grow them

• SCA best practices for recurring revenue businesses

Platforms and marketplaces

• How to route payments between multiple parties with Stripe

• How PSD2 impacts marketplaces and platforms in Europe

• A guide to payment facilitation for platforms and marketplaces

Introduction to online payments 16

Payments glossary

This glossary defines the most common terms in the payments industry.

Acquirer

Also referred to as an acquiring bank, an acquirer is a bank or financial institution that processes

credit or debit card payments on behalf of the merchant and routes them through the card

networks to the issuing bank.

Bank transfers

Can refer to an account debit, where you collect your customers’ banking information and pull

funds from their accounts, or a credit transfer, where you link to customers’ bank accounts and

they push money to you.

Cardholder

A person who owns a credit or debit card.

Card networks

Process transactions between merchants and issuers and control where credit cards can be

accepted. They also control the network costs. Examples include Visa, Mastercard, and American

Express.

Chargeback

Also referred to as a dispute, a chargeback occurs when cardholders question a payment with

their card issuer. During the chargeback process, the burden is on the merchant to prove that the

person who made the purchase owns the card and authorized the transaction.

Chargeback fees

The cost incurred by the merchant when the acquiring bank reverses a card payment.

Digital wallet

Lets customers pay for products or services electronically by linking a card or bank account, or

storing monetary value directly in the app. Examples include Apple Pay, Google Pay, Alipay, and

WeChat.

Disputes

See definition for “Chargeback”

Introduction to online payments 17

Four-party system

The four parties involved in processing payments: the cardholder, merchant, acquirer, and

issuing bank.

Fraud

Any false or illegal transaction. It typically occurs when someone has stolen a card number or

checking account data and uses that information to make an unauthorized transaction.

Interchange

A fee paid to the issuing bank for processing a card payment.

Issuing bank

The bank that issues credit and debit cards to consumers on behalf of the card networks.

Merchant Category Code (MCC)

A four-digit number used to classify a business by the type of goods or services it provides.

Network acceptance

The percentage of transactions that are accepted or declined by the issuing bank. A decline can

occur due to outdated credentials, suspicion of fraud, or insucient funds.

Network costs

The total of interchange and scheme fees.

Payment facilitator

Traditionally, adding payments functionality required a platform or marketplace to register and

maintain status as a payment facilitator (or payfac) with the card networks, since it was seen as

controlling the flow of funds between buyers and sellers. Today, it’s easy to add the payments

functionality that most platforms and marketplaces require without becoming a payment

facilitator.

Payment gateway

A piece of soware that encrypts credit card information on a merchant’s server and sends it to

the acquirer. Gateway services and acquirers are oen the same entity.

Introduction to online payments 18

Payment method

The way a consumer chooses to pay for goods or services. Payment methods include bank

transfers, credit or debit cards, and digital wallets.

Payment processor

Facilitates the credit card transaction by sending payment information between the merchant,

the issuing bank, and the acquirer. The payment processor usually gets the payment details from a

payment gateway.

PCI Data Security Standards (PCI DSS)

An information security standard that applies to all entities involved in storing, processing, or

transmitting cardholder data, and/or sensitive authentication data.

Scheme fees

Fees collected by the card network. A single transaction may incur multiple scheme fees, such as

authorization fees or service fees.

Introduction to online payments 19