The Costs of Cancer

2020 Edition

Cancer Acti

on

Network

SM

2 American Cancer Society Cancer Action Network The Costs of Cancer 2020

The American Cancer Society Cancer Action Network

SM

(ACS CAN)

is making cancer—and the affordability of cancer care—a top priority

for public officials and candidates at the federal, state and local levels.

ACS CAN is the American Cancer Society’s nonprofit, nonpartisan advocacy affiliate. ACS CAN

empowers advocates across the country to make their voices heard and influence evidence-based

public policy change, as well as legislative and regulatory solutions that will reduce the cancer burden.

This ACS CAN report focuses specifically on the costs of cancer borne by patients in active cancer

treatment as well as cancer survivors. It examines the factors contributing to the cost of cancer care,

the types of direct costs patients face and the indirect costs associated with cancer. To more fully

illustrate what people with cancer actually pay for care, the report also presents scenario models for

several types of cancer and different types of insurance coverage. Finally, the report presents public

policy recommendations for making cancer treatments more affordable for patients, survivors and the

health care system as a whole.

Published October 2020

For more information regarding the methodology of the modeled patient cost scenarios in this report,

and to view additional materials related to this report, please visit www.fightcancer.org/costsofcancer.

This report was supported in part by grants from the Association for Accessible Medicines and

its Biosimilars Council, AbbVie, the Biotechnology Innovation Organization, Boehringer Ingelheim,

Foundation Medicine, Janssen, Merck, Mylan, Pfizer, Sandoz and Sanofi.

Cancer Acti

on

Network

SM

3American Cancer Society Cancer Action Network The Costs of Cancer 2020

National Cancer Costs Projected to Increase Drastically by 2030

$ 250

B

$ 200 B

$ 150 B

$ 100 B

$ 50 B

$ 0 B

2015

$182.6B

2020

$200.7B

2025

$222.2B

2030

$245.6B

34% increase

Source: Mariotto AB, Enewold L, Zhao J, Zeruto CA, Yabroff KR. Medical Care Costs Associated with Cancer Survivorship in the United States.

Cancer Epidemiol Biomarkers Prev June 10 2020 DOI: 10.1158/1055-9965.EPI-19-1534

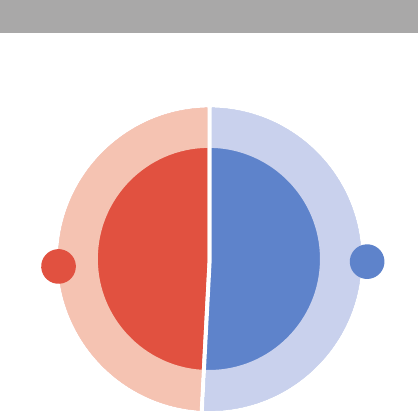

Spending on Cancer Care—in 2019 billions of dollars

4%

5%

10%

33%

49%

Medicaid

Medicare

Other

Patient Out-of-Pocket

Costs = $5.6 billion

Private

Insurance

Everyone Pays the Costs of

Cancer Treatment

Introduction

The American Cancer Society (ACS) estimates that roughly 1.8

million new cases of cancer will be diagnosed in the U.S. in 2020

and that more than 16.9 million Americans living today have a

cancer history.

1

As a leading cause of death and disease in the U.S.,

not only does cancer take an enormous toll on the health of patients

and survivors—it also has a tremendous financial impact.

Patient Costs are Unaffordable

For patients and their families, the costs

associated with direct cancer care are staggering.

In 2018 cancer patients in the U.S. paid $5.6

billion out of pocket for cancer treatments,

2

including surgical procedures, radiation

treatments and chemotherapy drugs.

Overall Cancer Costs are Rising

Cancer also represents a significant portion of

total U.S. health care spending. Approximately

$183 billion was spent in the U.S. on cancer-

related health care in 2015, and this amount is

projected to grow to $246 billion by 2030—an

increase of 34%.

These high costs are paid by people with

cancer and their families, employers, insurance

companies and taxpayer-funded public programs

like Medicare and Medicaid.

Source: Data retrieved from the Agency for Healthcare Research and Quality.

Medical Expenditure Panel Survey, 2018. https://meps.ahrq.gov/mepsweb/

*See reference for category definitions.

3

Percentages in chart have been

rounded.

4 American Cancer Society Cancer Action Network The Costs of Cancer 2020

The Costs of Cancer Do Not Impact

All Patients Equally

Because of high costs, many people with cancer

and those who have survived cancer experience

financial hardship, including problems paying bills,

depletion of savings, delaying or skipping needed

medical care, and potential bankruptcy. These

costs and hardships do not impact all cancer

patients equally—there are certain factors that

make a patient more likely to experience

financial hardship:

60%

70%

50%

40%

30%

20%

10%

0%

Ages 18-54

58.9%

Ages 55-64

48.5%

Cancer patients are more likely to experience financial hardship if they are:

Younger

60%

70%

50%

40%

30%

20%

10%

0%

Other Races/

Ethnicities

63.5%

Non-Hispanic Whites

50.9%

People of Color

60%

70%

50%

40%

30%

20%

10%

0%

Less than high

school graduate

69.5%

52.1%

Some college or

more

High school

graduate

51.8%

Less Educated

60%

70%

50%

40%

30%

20%

10%

0%

Low-income

(≤138% FPL)

60.0%

60.5%

High-income

(>400% FPL)

Middle-income

(139-400%FPL)

47.2%

Lower Income

*

FPL = Federal Poverty Level

S

ource: Han X, Zhao J, Zheng Z, de Moor JS, Virgo KS, Yabroff KR. Medical Financial Hardship Intensity and Financial Sacrifice Associated with Cancer in the

United States. Cancer Epidemiol Biomarkers P

rev. 2020;29(2):308-317. doi:10.1158/1055-9965.EPI-19-0460

Note that similar patterns of disparities e

xist in the over-65 population.

% of Individuals with a History of Cancer Reporting at least 1 Ty pe of Financial Hardship, Ages 18-64

The Costs of Cancer Disparities

Cancer and its costs do not impact all

individuals equally. Look for information about

The Costs of Cancer Disparities throughout

this report.

5American Cancer Society Cancer Action Network The Costs of Cancer 2020

Factors Contributing to the Costs of Cancer

With more than 200 different types of cancer, there is no “one

size fits all” cancer treatment—and therefore the costs of cancer

treatment vary significantly from patient to patient. However, there

are several consistent factors that contribute to patients’ overall

costs for their care.

Insurance Status/Type of Insurance Coverage:

Patients without health insurance are responsible

for all of their treatment costs. Some uninsured

patients may qualify for “charity care,” may be able

to participate in drug discount programs to reduce

their costs or may be able to negotiate discounts

with providers. For patients with insurance, the

kind of health insurance the patient has and

the design of their plan are some of the most

important factors in determining the ultimate costs

for patients. Patient costs are often referred to

as cost sharing or an out-of-pocket requirement.

Following are some of the out-of-pocket

components that determine what patients pay:

■

Premium: The monthly amount the patient

pays to stay covered by the insurance plan (in

some cases an employer pays all or part of a

patient’s premiums). Premiums are determined

by a number of factors that differ depending

on type of insurance and can include: age of

the enrollee, where the enrollee lives, how

generous the benefits are (including cost-

sharing amounts listed below) and how much

the plan anticipates it will pay in health care

claims for enrollees. While many enrollees focus

only on premium prices, the other out-of-pocket

costs listed below offer a

more complete picture of

what patients ultimately pay.

For instance, enrollees who

are high utilizers of care—

including those with cancer—

often face a trade-off of

higher premiums for lower

out-of-pocket costs and vice

versa.

■

Deductible: The amount the patient must first

pay out of pocket for care before the insurance

plan will start covering costs. Some plans have

separate deductibles for medical services,

drugs, and/or out-of-network services. High

deductible health plans—defined in 2020 as

plans with a deductible of $1,400 or higher

for individuals or $2,800 for families—are

becoming more prevalent in the U.S.

4

■

Co-payment or Co-pay: A flat fee patients

pay per health care service, procedure or

prescription.

■

Co-insurance: A percentage patients pay

of the total cost of a prescription, service or

procedure. Co-insurance can be unpredictable

because the patient often cannot determine the

total cost of the treatment until arriving at the

pharmacy or receiving a bill after the treatment.

■

Out-of-Pocket Maximum or Out-of-Pocket

Cap: The limit on what a patient must pay each

year before the health plan starts to pay 100%

for covered, in-network benefits. This amount

excludes premiums. Current law establishes

these caps in most private insurance plans.

Caps provide a crucial protection to patients

with high health care costs.

■

In-Network vs. Out-of-Network: Many health

insurance plans have “networks” of doctors,

hospitals, and pharmacies. If a patient goes to

an “in-network” provider, cost sharing is usually

lower because the insurer has negotiated

rates with the provider. Some insurance plans

Current law requires many private

insurance plans to limit annual patient

out-of-pocket spending. The 2020 limit

is $8,150 for an individual plan and

$16,300 for a family plan.

Survivor Views: The Costs of Cancer in

Their Own Words

“I had good insurance through my husband’s

work, but our deductibles were always

high. We met our deductible twice with my

cancers, we have never met it otherwise.

The benefits after meeting the deductible

were nice, but we had to put all of our bills

on payment plans and most would go into

collections even though we were paying

them. When you are paying 8 different bills

for thousands of dollars, and one person is

working with the cost of living and food,

there is little to go around.”

Ovarian Cancer Survivor, Ohio

6 American Cancer Society Cancer Action Network The Costs of Cancer 2020

charge more cost sharing for “out-of-network”

providers, while other plans do not cover out-of-

network providers at all. Out-of-network costs

do not always count towards the patient’s out-

of-pocket maximums.

■

Balance Billing and Unexpected Costs:

Patients may also encounter unanticipated

costs. Their plan may not cover a treatment

they received, they may have used a provider

who was not in-network, or their plan did not

reimburse the provider for the full amount billed

and the patient has to pay the difference (this is

sometimes called “balance billing” or “surprise

billing”). The amount of these surprise bills often

does not count toward the patients’ out-of-

pocket maximum.

Other factors contributing to

costs variations are:

Treatment Plan: The type of treatment (surgery,

radiation, chemotherapy, etc.) and how much

treatment (duration, number of drugs, number

of surgeries, etc.) the patient receives causes

costs to vary significantly. Note that the stage

at which a patient is diagnosed is an important

factor in determining a patient’s treatment plan,

the potential outcome and the treatment costs. In

some cases, doctors and patients have choices

between treatment regimens and can consider

costs in their decision. In other cases, there is only

one treatment option.

Geographic Location: Costs vary based on

where the patient lives and how many providers

are available in that area. Areas that generally

have high costs of living also tend to have higher

treatment costs.

Treatment Setting: Treatment charges are based

on many factors, and the costs to the patient may

differ depending on whether care is delivered in a

hospital, clinic or physician’s office (for example,

many hospitals charge facility fees that increase

costs for patients). Sometimes patients may have

a choice where they receive treatment, but other

times they do not have a choice and must incur

additional cost. Regardless of setting, it is difficult

for patients to obtain price information in order to

make comparisons.

7American Cancer Society Cancer Action Network The Costs of Cancer 2020

Key Terms

■

Medical Benefit: the benefits covered by a health plan. Generally, medical benefits include

coverage for hospital visits, doctor visits and various kinds of tests. In some cases, a health plan

has a separate pharmacy benefit that provides coverage for outpatient prescription drugs

■

Formulary: the list of drugs and pharmacological therapies covered by a health plan.

Formularies often sort drugs into tiers, which are groups of drugs assigned a certain co-pay or

co-insurance.

■

Medicare: the federal government program providing health coverage to Americans age 65

and older, as well as some individuals with disabilities. Medicare has several parts: Part A covers

hospitalization, Part B covers physician and outpatient services (including physician-administered

drugs), and Part D covers oral drugs.

Part C offers private plans that cover hospitalizations, physician and outpatient services. Some

individuals also have a Medigap plan (otherwise known as a Medicare Supplemental plan), which

reduces cost sharing required in Parts A and B.

■

Medicaid: Joint federal-state government program that provides health insurance coverage to

qualifying people with low-incomes, people who are pregnant, children, seniors, and people with

disabilities.

■

Employer-Sponsored Insurance: Health insurance provided through an individual’s employer.

This type of insurance is also usually provided to the individual’s spouse and/or dependents

■

Individual Marketplace Insurance: Insurance purchased by individuals, not offered by

employers or other groups. All individuals have access to either a state-based or federal

Exchange that sells these plans which meet Affordable Care Act standards.

■

Short-Term, Limited-Duration Plan: A private health insurance plan that provides coverage

to policyholders for a period of as little as a month to as long as three years. These plans offer

limited coverage and benefits and are not required to implement the same consumer protections

as other plans.

8 American Cancer Society Cancer Action Network The Costs of Cancer 2020

“Surprise medical billing” or “balance billing” is when an insured

patient is unknowingly treated by an out-of-network provider and is then

billed the difference between what the provider charged and what the

insurer paid. Surprise bills can be significantly higher than the consumer’s

standard in-network cost sharing. They occur most often with ancillary

providers—like anesthesiologists and emergency room physicians.

In an October 2019 survey, ACS CAN asked cancer patients and

survivors about their experiences with surprise bills through its Survivor

Views panel.

5

■

24% of respondents reported having received a surprise bill as a

result of their cancer care.

■

28% of these surprise bills were for $2,000 or higher.

Types of Cancer Treatment Costs

There are traditionally three primary approaches to treating

cancer: surgery, radiation and pharmacological therapy

(including chemotherapy, targeted therapy, hormone therapy

and immunotherapy). Some patients receive all three treatment

modalities, while others receive one or two types. Costs to the

patient vary depending on the type and extent of the treatment.

Surgery: Surgery can be used to remove tumors,

diagnose cancer and/or to find out how far

a cancer has spread. Many people who have

cancer have surgery at least once as part of their

treatment. Surgery can involve multiple medical

providers, hospitals or specialized facilities and

other elements that result in multiple charges

to patients and health insurers. Patients may

be assessed additional facility and other fees

associated with where the surgery is performed.

If a provider is not in-network, a plan may not

cover as much (or any) of the cost for the out-

of-network provider or service. This can lead

the patient to receive unexpected medical bills,

sometimes known as “balance bills” or “surprise

medical bills.” Some insurance plans may require

the patient to pay co-insurance for each service

or a bundle of services, and others have a flat

co-pay per day or per hospital admission. Covered

surgery and associated care are generally

included under a plan’s medical benefit.

Radiation: Radiation therapy uses waves or

high energy particles to destroy or damage

cancer cells. Most patients who receive radiation

treatments do so at a hospital or cancer treatment

facility. Radiation treatment requires complex

equipment and a team of health care providers.

Treatment protocols vary, but some cancer

patients receive radiation daily or several times

a week for many weeks, which contributes to

relatively high patient costs. Patients who have

not yet met their out-of-pocket maximum will

likely be required to pay co-pays per visit or co-

insurance based on the total cost of treatment.

Covered radiation is generally included under a

plan’s medical benefit (or, in the case of Medicare,

under Part B).

Pharmacological Therapy: Medication is a

very common part of cancer treatment. This

can include chemotherapy, targeted therapy,

immunotherapy, hormone therapy and/

or supportive care like pain or anti-nausea

medication. Some of these drugs can be taken as

pills obtained through mail-order or at a pharmacy,

and some are administered intravenously (IV) in

a doctor’s office, clinic or hospital. In most cases,

covered IV drugs are included under a plan’s

medical benefit; while covered drugs taken as

pills or orally and obtained at a pharmacy are

included under a plan’s pharmacy benefit. This

difference is important because cost sharing

is often different for these benefits, and some

plans have separate medical and pharmacy

deductibles. Co-pays and co-insurance are both

common forms of patient cost sharing for drugs.

These tiers are groupings of drugs—like “generic,”

“preferred,” “non-preferred,” and “specialty,” and

sometimes combinations thereof. Each tier has

its own co-pay or co-insurance, which makes

understanding patient out of pocket costs more

complex. Covered pharmacological therapy is

generally included in insurance policies as a

separate pharmacy benefit.

New Therapies: Fortunately, oncology treatment

is a very active area of research and development

for government agencies—such as the National

9American Cancer Society Cancer Action Network The Costs of Cancer 2020

Cancer Institute—as well as for academic and

industry researchers. Decades of significant

investment is resulting in a steady stream of new

treatments becoming available to cancer patients

and their providers. Many of these new treatments

are pharmacological. Some innovations—like

chimeric antigen receptor therapy (CAR-T), which

takes a patient’s own immune system cells and

changes them in a laboratory to attack cancer

cells before re-infusing them

6

—belong in their

own unique category. Some new personalized

therapies require biomarker testing (sometimes

called “genomic testing”) to determine if the

patient has the particular type of cancer the

personalized therapy treats.

Because of the way industry recoups costs for

research and development, a newer treatment

is likely to be more expensive than when it has

been used for many years and competitors

have developed generic or biosimilar versions

of the drug. This often results in higher out-of-

pocket costs for a patient using a new treatment,

especially if they must pay co-insurance, cannot

use copay assistance, or are uninsured. Also, if a

treatment is very new, a patient’s insurance plan

may not have added it as a covered benefit yet or

may consider it ‘experimental.’ In these situations,

a patient may be able to appeal to their insurance

plan for coverage of the treatment–otherwise

their out-of-pocket costs will likely be very high

for an uncovered treatment or a patient may opt

to go without the treatment.

Other Types of Cancer Care Costs: While

surgery, radiation and pharmacological therapy

are the three most common approaches to cancer

treatment, patients may utilize other regimens like

stem cell transplants, hyperthermia, photodynamic

therapy and blood transfusions. Cancer patients

also often need treatments such as supportive or

palliative care, rehabilitative therapy, mental health

services, nutrition counseling and cardiology

consultations as a result of their cancer or

treatments.

7

It is also important to note that these various

forms of treatment require multiple types of health

care personnel. It is very common for people

with cancer to see multiple health care providers

during the course of their treatment, including

primary care doctors, specialists for diseases and

side effects developed as a byproduct of cancer

treatment (like cardiologists, neurologists and

endocrinologists), medical oncologists, radiation

oncologists, surgeons, palliative care specialists,

rehabilitation specialists, physical therapists and

nutritionists. The complexity of cancer treatment

and the necessity of multiple specialists are

large drivers of cancer patient costs. Many health

insurance plans charge higher co-pays or co-

insurance amounts for specialist visits compared

to primary care. Additionally, very specialized

providers are often in short supply, and patients

are sometimes forced to go out-of-network to see

a specialist. This is especially likely for patients

who live in more rural areas.

Rural residents are more likely than their

urban counterparts to have higher rates of

unemployment and lack of health insurance.

10

Survivorship Care Costs: It is also important

to note that even when a person with cancer

has completed their surgery, radiation and/

or chemotherapy, the costs of care do not end

immediately. Many cancer survivors deal with

cancer symptoms and side effects of treatment

months to years after finishing treatment—

sometimes for the rest of their lives. Some cancer

survivors also must take treatments long-term, like

a 10-year regimen of hormone therapy to prevent

breast cancer recurrence. This means many of

the costs discussed in this section, including

for seeing specialist providers like rehabilitation

therapists and psychotherapists, can continue

for years for cancer survivors. In fact, research

shows that annual health care expenditures for

cancer survivors are significantly higher than for

individuals who have never had cancer.

11

Indirect

costs of cancer—explored on the next page—also

often continue into survivorship.

Survivor Views: The Costs of Cancer in

Their Own Words

“One of the most surprising things is the cost

of care AFTER active cancer treatment. I have

lymphedema and the costs are significant,

including various equipment, DME [durable

medical equipment], compression clothing,

and physical therapy. I didn’t realize the costs

would continue after active treatment.”

Breast Cancer Survivor, Arizona

The Costs of

Cancer Disparities

■

Urban areas have

approximately 5

times the number

of oncologists

compared to rural

areas.

8

■

Rural patients have

to travel nearly

twice as long one-

way as urban and

suburban patients

in order to see their

cancer doctor.

9

10 American Cancer Society Cancer Action Network The Costs of Cancer 2020

The Indirect Costs of Cancer

This report focuses on the direct costs of cancer—health care

expenses directly for or related to cancer treatment—but there

are other indirect costs that are just as significant and potentially

problematic for people with cancer and their families.

Survivor Views: The Costs of Cancer in Their Own Words

“ Being diagnosed with cancer six years ago has caused me financial difficulties,

stress, and anxiety. Although I am in remission, I continue to have adverse effects

from my treatment. I spend 2-4 days per week in a doctor’s office and also had to

be treated out of state twice in 2019. Each time I go out of state I am spending a

minimum of $1500. While we are fortunate my husband is well enough to work which

helps pay for my medical bills and expenses, it’s still a financial strain on us.

I am still not able to return to work so we are a one-income family. I don’t know how

others who don’t have a moderate salary are able to afford it. If the ACA [Affordable

Care Act] goes away, I will likely be penalized for my preexisting conditions. I am so

nervous that my medications, physical therapy, treatments, and diabetic supplies will

not be covered.”

Leukemia Survivor, Alaska

Transportation

Some patients have to travel significant distances to

medical appointments and the pharmacy

Lodging

Some cancer patients must travel to receive

treatments, like specialized surgeries, and need a

place to stay near their treatment site

Lost wages or income

Some cancer patients must stop working temporarily

or permanently, or reduce their work schedules

Secondary Effects

Some patients must treat or deal with secondary effects

of cancer or treatment, like fertility treatments, wigs and

cosmetic items, or the cost of special food

Caregiving costs

Some patients may need to pay for help at home to

care for themselves, or for their children

As these are indirect costs, most of them are difficult to quantify and track. But these costs are

significant for people with cancer and their families, adding to the overall costs of cancer care

and also contributing to the “financial toxicity” of cancer.

11American Cancer Society Cancer Action Network The Costs of Cancer 2020

Patient Profiles: Cost Scenarios

Because of the complexity and variation in cancer treatment, it

is difficult to predict the full costs for any individual with cancer

at the time of diagnosis. The following illustrative patient profiles

and associated data represent the typical costs for several

cancer scenarios. The patients are hypothetical, but the treatment

regimens are typical treatments for each specific cancer with the

corresponding actual costs.

Experts at ACS and ACS CAN constructed

profiles of several typical cancer patients. The

types, stages, and details of cancer represented

in these profiles were chosen based on cancer

incidence rates and the need to represent

a diverse set of people with cancer and

experiences. Clinical experts determined the

usual course of treatment for these patients

based on the National Comprehensive Cancer

Network (NCCN) treatment guidelines for each

of the cancers. Estimates for patient out-of-

pocket costs for each of these patients were

based on common insurance scenarios. Note that

some patient profiles were used to run multiple

insurance scenarios for comparison and analysis

purposes—combinations of profiles and insurance

design scenarios that are not reflected in this

section will be discussed in future sections.

All prices and insurance designs are based

on 2020 data. See methodology appendix for

more details, published at www.fightcancer.org/

CostsofCancer.

These patient profiles represent typical scenarios

and timelines. They help illustrate the costs that

cancer patients and health care payers incur for

an individual’s cancer treatments. Note that these

scenarios do not include costs for other health

care treatments unrelated to cancer (for example,

if a patient has asthma, the costs to treat asthma

are not included). Also note that these scenarios

are unable to incorporate all the problems people

with cancer face, including tests that have to be

repeated and delayed timelines.

Shonda—

Pancreatic Cancer

Medicare

Carla—

Breast Cancer

Small Employer, High Deductible Health Plan

Kathy—

Lung Cancer

Individual Market Plan

Brian—

Lymphoma

Short-term Limited Duration Plan

Franklin—

Prostate Cancer

Large Employer Plan

Tom—

Colorectal Cancer

Medicare

12 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Tom—Colorectal Cancer

Medicare

Case Study: Colorectal Cancer—

Medicare Coverage

In January, Tom’s fecal immunochemical test (FIT) test was positive indicating that he might have colon

cancer. His primary care doctor sent him to a gastroenterologist (GI) specialist, who ordered a colonoscopy.

Tom received his colonoscopy at a hospital outpatient center. During the colonoscopy his doctors

discovered 2 adenomatous polyps, which were removed, and a lesion suspicious for colon cancer. The lesion was

biopsied, and Tom was diagnosed with Stage IIB colon cancer.

In February, Tom had blood tests and a CT scan to check for possible spread of the disease.

In March, Tom had colectomy surgery to remove the lesion and surrounding tissue, and a lymphadenectomy to

test if the cancer had spread. Tom’s cancer tissue was also tested to see if he had any biomarkers that

would point his doctors towards the right drug regimen.

In April and May, Tom received chemotherapy to treat his cancer and prevent reoccurrence, and supportive

care drugs, like anti-nausea medication, to ease side effects.

Tom finished his treatments in May and began post-treatment follow-up, including regular doctor’s visits

and blood tests.

Throughout his treatment, Tom met with several practitioners and specialists, including his primary care

doctor, a GI specialist, a surgeon, oncologists, and oncology nurses.

Tom had health insurance coverage through

Medicare and Medigap. His premiums were:

Medicare Part A - $0/month

12

Medicare Part B - $145/month

13

Medigap (Policy G) - $236/month

Medicare Part D - $25/month

Tom’s highest total spending came in April and

May ($767 in April and $612 in May) when some

of his chemotherapy and supportive care drugs

were paid for through his Medicare Part D plan.

Otherwise, Tom’s Medigap plan protected him

from high fluctuating out-of-pocket costs. In total

Tom paid $405 in premiums every month. At the

end of his plan year, he had paid a total of $4,864

in premiums and $568 in cost-sharing—a total

of $5,432—for his cancer care.*

The total health care costs for Tom’s

colorectal cancer treatment in 2020 were

$38,035. Medicare and Tom’s Medigap and

Part D plans paid the vast majority of these

costs—$37,467. If Tom had been uninsured, he

would have been responsible for all of these

costs,** and may have been required to pay them

up-front before treatment.

Even though Tom is no longer in active treatment,

he will still require regular follow-up visits with his

oncologist and primary care physician which add

to his costs in future years.

* Note that these costs only include cancer treatment, and do not include

treatment for other conditions that may have developed as a result of the

cancer treatments and/or any other treatments unrelated to cancer care or

other preventive services.

** Costs for an uninsured patient may be higher than this estimate because

uninsured patients do not benefit from a plan’s negotiated discount rate.

However, some uninsured patients are also able to receive charity care,

which discounts or forgives certain treatment costs.

13American Cancer Society Cancer Action Network The Costs of Cancer 2020

Case Study: Breast Cancer—

Small Employer, High Deductible Health Plan

Year One: Carla has her first mammogram in January to screen for breast cancer. Her doctor sees

something suspicious on the images and sends her for several follow-up tests including blood tests, a

breast MRI, CT scans of her chest and abdomen, ultrasounds of her breasts and lymph nodes, and a diagnostic mammogram.

She then has a core needle biopsy in February, and is diagnosed with stage III breast cancer, with a large

tumor and cancer present in her lymph nodes. Molecular tests reveal her cancer is hormone receptor

negative and human epidermal growth factor receptor 2 (HER2) positive.

Carla’s doctors recommend she start neo-adjuvant (before surgery) chemotherapy right away given the

aggressive nature of her cancer. Before she starts this treatment, she consults with a cardiologist about

the way her treatment can impact her heart and has a chemotherapy port installed.

Carla receives multiple cycles of chemotherapy from March through August, along with supportive care

drugs to address symptoms and side effects like nausea. These treatments are successful in shrinking

her tumors but do not fully eliminate them.

In September Carla has local excision and lymphadenectomy surgery to fully remove the tumors, and then begins

adjuvant (post-surgery) radiation therapy to maximize local control of the cancer. In October she also continues

her HER2-targeted therapy infusions, which started before surgery and will continue for one full year. During these

treatments she continues to have blood tests and visits with her oncologist to monitor her treatment progress.

Year Two: January brings the one-year anniversary of the mammogram that caught her breast

cancer—and Carla continues to receive her HER2-targeted therapy treatments, monitoring blood tests, and visits

with her oncologist. She continues these treatments through June, when she completes a full year of

post-surgery HER2-targeted therapy. In the remaining months of her second year, Carla is tested for

lymphedema—a common side effect of breast cancer treatment—and continues to be monitored by her

oncologist. Because Carla still has most of her breast tissue, she must still have a mammogram every year

to look for cancer recurrence or new cancers.

Throughout her two years of cancer treatments, Carla met with several doctors and specialists,

including her primary care doctor, a medical oncologist, radiation oncologist, cardiologist, and a breast surgeon.

Carla is enrolled in a high-deductible health plan

through her small employer. Carla pays $143 per

month in premiums. Note that Carla’s employer

does not offer an accompanying health savings

account.

Carla is required to pay the full amount of her

high deductible—$6,000—and other cost-

sharing in February, when she undergoes most

of her diagnostic tests. Paying these big bills

the same month she received a serious cancer

diagnosis was a struggle. Fortunately, she hits

her maximum out-of-pocket limit of $8,150 in

February and her expenses level off. At the end of

her first plan year, she had paid a total of $1,712

in premiums and $8,150 in cost-sharing for

her cancer care: an annual total of $9,862.*

Carla’s costs continued in the second year after

her diagnosis: in year two she once again paid

a total of $1,712 in premiums and $8,150 in

cost-sharing for her cancer care.

The total health care costs for Carla’s breast

cancer treatment were $222,981 (over two

years). Carla’s insurance plan paid the vast

majority of these costs—$206,681. If Carla had

been uninsured, she would have been responsible

for all of these costs,** and may have been

required to pay them up-front before treatment.

* Note that these costs only include cancer treatment, and do not include

treatment for other conditions that may have developed as a result of the

cancer treatments and/or any other treatments unrelated to cancer care or

other preventive services.

** Costs for an uninsured patient may be higher than this estimate because

uninsured patients do not benefit from a plan’s negotiated discount rate.

However, some uninsured patients are also able to receive charity care,

which discounts or forgives certain treatment costs.

Carla—Breast Cancer

Small Employer, High Deductible Health Plan

14 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Franklin is enrolled in health insurance through

his large employer. Franklin’s employer

contributes $618 per month towards the

premium, and Franklin pays $169 per month.

Franklin has a relatively small deductible ($500)

and maximum out-of-pocket limit ($3,000),

and he reaches that limit by February, when his

out-of-pocket costs level off. At the end of the

year, he had paid a total of $2,030 in premiums

and $3,000 in cost-sharing for his cancer care—

for an annual total of $5,030.*

The total health care costs for Franklin’s

prostate cancer treatment were $100,557.

Franklin’s employer/insurance plan paid the vast

majority of these costs—$97,557. If Franklin had

been uninsured, he would have been responsible

for all of these costs,** and may have been

required to pay them up-front before treatment.

By the end of the year, Franklin had found a

treatment that seemed to be working to fight his

prostate cancer. He will need to continue taking

this medicine for several years and monitoring his

cancer with blood tests and extra doctor’s visits.

Franklin will continue to pay costs related to his

prostate cancer for years to come.

* Note that these costs only include cancer treatment, and

do not include treatment for other conditions that may have

developed as a result of the cancer treatments and/or any

other treatments unrelated to cancer care or other preventive

services.

** Costs for an uninsured patient may be higher than this

estimate because uninsured patients do not benefit from a

plan’s negotiated discount rate. However, some uninsured

patients are also able to receive charity care, which discounts

or forgives certain treatment costs.

Franklin—Prostate Cancer

Large Employer Plan

The Costs of Cancer Disparities

Compared with white men, African American

men are more likely to develop prostate cancer

and are twice as likely to die from the disease.

14

Case Study: Prostate Cancer—

Large Employer Plan

Franklin has a family history of prostate cancer. As part of his annual physical in January, Franklin receives

a digital rectal exam and his primary care doctor orders a PSA blood test. Franklin’s PSA score from this test

is over 10, indicating possible prostate cancer. Franklin’s doctor orders more blood tests, an MRI, bone scan

and CT scan; and refers him to a medical oncologist.

After having a core biopsy in February, the tests determine that Franklin has locally advanced prostate cancer.

Since Franklin has a life expectancy of more than 10 years, and he has an intermediate risk of his

cancer growing quickly, Franklin chooses to have a radical prostatectomy surgery to remove his prostate and

test his lymph nodes. The cancer is found in his lymph nodes, so his treatment continues with a goal of

stopping its spread to other parts of his body.

In March he begins androgen deprivation therapy (ADT), or hormone therapy, which are pills he takes daily.

Because Franklin also has diabetes, his doctor wanted to prescribe a certain drug for his treatment.

However, Franklin’s insurance coverage requires he try a different drug first.

In April he begins radiation treatments, and regular PSA blood tests and doctor’s visits to monitor his progress.

After 4 months of these treatments, he has a new round of blood tests and a bone scan. These tests

find that his PSA level has already doubled, indicating the treatments are not working, and Franklin is

diagnosed with ‘castration-resistant’ prostate cancer. In August he begins taking the hormone therapy his doctor

originally wanted to prescribe, which stabilizes his cancer and he continues this therapy through the

end of the year.

Throughout the course of his treatment, Franklin saw several doctors and specialists, including his

primary care doctor, a medical oncologist, surgical oncologist, and a radiation oncologist.

15American Cancer Society Cancer Action Network The Costs of Cancer 2020

Shonda—Pancreatic Cancer

Medicare

The Costs of

Cancer Disparities

African Americans

are more likely

to be diagnosed

with cancer at an

advanced stage

compared to white

Americans, and they

also have lower

survival within each

stage—further

reflecting inequalities

in access to and

receipt of high-

quality cancer care.

15

Case Study: Pancreatic Cancer—

Medicare Coverage

Shonda is retired and lives in a rural area near her family. In January she has her annual Medicare

wellness exam with her primary care doctor, where she shares that she has been having stomach pains

and digestive issues. Her doctor recommends some diet changes and schedules a follow-up appointment

in March to see if these changes help.

Unfortunately Shonda is still experiencing symptoms in March, so her doctor orders several

blood tests, followed by a CT scan of her pancreas, an endoscopic ultrasound, and an endoscopic retrograde

cholangiopancreatography (ERCP) procedure. The tests continue in April, when she has a biopsy, and CT scans of

her chest and pelvis. After consulting with a medical oncologist and gastroenterologist, Shonda is diagnosed with

metastatic pancreatic cancer. Surgery is not an option because the cancer has spread, so she prepares to

start systemic therapy. Her tumors are tested for biomarkers, but none are found.

Her doctor tells her that she would be a good candidate for a clinical trial, which would be her choice

for first-line treatment. However, the trial is only offered in a major city that is a 5-hour drive from her

home, and her family is not able to travel that far and care for her while receiving treatment.

Shonda must choose a treatment that is available near her home, so she opts to receive chemotherapy

from her local oncologist. In April she has a port installed and is tested for jaundice in preparation for

her treatment. She also consults with a palliative care specialist to discuss her options for symptom and

side effect control during her upcoming treatments.

In May Shonda begins her chemotherapy treatment at her local hospital that her children must drive her to

a few times a month. Treatment includes supportive care drugs, blood tests, and regular CT scans of her pancreas

to monitor progress. She also meets with her oncologist regularly.

After three months of chemotherapy, a scan shows that the treatment is not working to shrink her

cancer. Shonda and her doctor decide to try another drug, so she begins a 2nd-line chemotherapy treatment.

However, her cancer also does not respond to that treatment, and by November, Shonda’s level of pain

and symptom burden is increasing. She develops blockages in her bile ducts and stomach. In consultation with

a palliative care specialist who has been monitoring her treatment, Shonda decides to choose care that is

focused on her comfort, including regular doses of pain medication and the placement of a gastronomy tube

to allow her to receive nutrition directly.

Shonda had health

insurance coverage

through Medicare

and Medigap. Her

premiums for both were:

Medicare Part A - $0/month

16

Medicare Part B - $145/month

17

Medigap (Policy G) - $236/month

Medicare Part D - $25/month

Shonda’s Medigap plan covered all of her cancer

treatment expenses until May, when she began

taking drugs covered through her Part D plan,

which required cost-sharing. In total Shonda paid

$405 in premiums every month. At the end of

her plan year, she had paid a total of $4,864 in

premiums and $1,767 in cost-sharing for her

cancer care, for an annual total cost of $6,631.*

The total health care costs for Shonda’s

pancreatic cancer treatment in 2020 were

$27,911. Medicare and Shonda’s Medigap and

Part D plans paid the vast majority of these

costs—$26,144. If Shonda had been uninsured,

she would have been responsible for all of these

costs,** and may have been required to pay them

up-front before treatment.

She and her family may decide to move her to

hospice care in the future—which will change how

her cancer and supportive care are paid for.

* Note that these costs only include cancer treatment, and do not include

treatment for other conditions that may have developed as a result of the

cancer treatments and/or any other treatments unrelated to cancer care or

other preventive services.

** Costs for an uninsured patient may be higher than this estimate because

uninsured patients do not benefit from a plan’s negotiated discount rate.

However, some uninsured patients are also able to receive charity care,

which discounts or forgives certain treatment costs.

16 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Kathy—Lung Cancer

Individual Marketplace Plan

Case Study: Lung Cancer—

Individual Marketplace Plan

Kathy smoked previously and met high risk criteria for lung cancer, so she had an annual low-dose CT scan

in January to screen for lung cancer. Her primary care doctor told her the scan was positive for a large

mass in her left lung and referred her to a pulmonologist.

Her pulmonologist ordered a CT scan to confirm the first scan’s results. In February, Kathy had several

blood tests and a lung function test. She then had a lung needle biopsy to test cells from the mass in her lung,

a PET/CT scan, a brain MRI, and was referred to a medical oncologist.

Kathy’s oncologist diagnosed her with an adenocarcinoma of the lung. She was told the cancer was Stage

IV, and it had metastasized to her bones. Because the cancer was too widespread, surgery and

radiation were not treatment options. She also had special biomarker tests on her tumor which showed

she was not a candidate to start with targeted therapy.

In March, Kathy began chemotherapy with an immunotherapy treatment at her doctor’s office. She also had a

consultation with a palliative care specialist to discuss her goals and treatment impact on her work and

family and received supportive care drugs to ease side effects. She also began regular PET scans and blood

tests to monitor the progress of the treatment.

In May, Kathy went to the emergency room and was hospitalized for trouble breathing. She stayed in

the hospital for three days. Kathy and her doctor decided to try a second-line treatment, as her

chemotherapy was not working.

In June, Kathy began receiving a second immunotherapy treatment at her doctor’s office. She continued PET

scans and blood tests to monitor progress. The immunotherapy worked to keep her cancer from spreading

and maintained her quality of life, so Kathy continued the treatment and monitoring through the end of

the year.

Throughout the course of her treatment, Kathy saw several doctors and specialists, including her primary

care doctor, a pulmonologist, a medical oncologist, a palliative care specialist, and the doctors who treated her in

the emergency room.

Kathy bought an

individual health

insurance plan through

her state’s marketplace,

which started in January. The premium for plan

was $840 per month, but she qualified for tax

credits which helped reduce these costs. Kathy

ended up paying $325 per month in premiums.

Kathy finished paying her high deductible

($6,500) in February and hit her out-of-pocket

maximum of $8,150 in March. These costs were

challenging to afford in the span of three months.

Fortunately, after her maximum was met she only

had to pay premiums for the rest of the year. At

the end of her plan year, she had paid out-of-

pocket $3,896 in premiums and $8,150 in cost

sharing for her cancer care,* a total of $12,046.

The total health care costs for Kathy’s

cancer treatment were $140,247. Kathy’s

insurance plan paid the vast majority of these

costs—$132,097. Kathy’s out-of-pocket costs

were significant but if she had been uninsured,

she would have been responsible for all of these

costs,** and may have been required to pay them

up-front before treatment.

At the end of the year, Kathy had found an

immunotherapy that had stabilized her cancer.

Kathy will likely continue to take this treatment

for several more months or years—however long

it works—as well as being monitored for further

cancer spread. Kathy will continue paying costs

for cancer treatments into future years.

* Note that these costs only include cancer treatment,

and do not include treatment for other conditions

that may have developed as a result of the cancer

treatments and/or any other treatments unrelated to

cancer care or other preventive services.

**Costs for an uninsured patient may be higher than this

estimate because uninsured patients do not benefit

from a plan’s negotiated discount rate. However, some

uninsured patients are also able to receive charity

care, which discounts or forgives certain treatment

costs.

17American Cancer Society Cancer Action Network The Costs of Cancer 2020

Brian—Lymphoma

Short-term Limited Duration Plan

Case Study: Lymphoma—

Short-term Limited Duration Plan

Brian works several part-time and freelance jobs and buys the cheapest plan he could find through an

insurance broker website, not understanding that this short-term limited duration plan does not cover a

comprehensive set of benefits or have to follow other patient protections.

Brian noticed that his lymph nodes were swollen and that he was frequently getting unexplained

bruises. In January he went to his primary care doctor, and after ruling out an infection, his doctor ordered

several blood tests followed by a whole-body PET/CT scan, and CT scan of his chest, abdomen and pelvis.

In February, Brian underwent a bone marrow biopsy, and was diagnosed with Stage II diffuse large B-cell

lymphoma, which is a form of Non-Hodgkin Lymphoma. Because Brian may want to father children in the

future, he opts to take fertility preservation measures, which are not covered by his insurance plan. He also

has a chemotherapy port inserted to prepare for his treatments.

In March, Brian begins several cycles of chemotherapy infusions. He also receives supportive care drugs to

treat side effects like nausea.

In April, after his 3

rd

cycle of chemotherapy, Brian has another full body PET/CT scan to check if the

treatment is working. Fortunately, his cancer has shrunk, and he is able to complete treatment in June

without incident and does not require radiation.

Follow-up blood tests show no evidence of cancer, but Brian and his doctors must continue to monitor

for cancer recurrence through imaging and blood tests every 3-6 months for the next 5 years.

Throughout the course of his treatment, Brian saw several doctors and specialists, including his primary

care doctor, a medical oncologist, a hematologist, and a fertility specialist.

Brian is enrolled in a short-term limited duration

(STLD) plan that lasts 12 months. He pays

$156 in premiums every month for this non-

comprehensive coverage. Note that his plan can

also engage in post-claims underwriting, which

means that once he is diagnosed with cancer,

they will likely try to classify it as a pre-existing

condition, not cover any of these costs, or rescind

his coverage entirely.

Brian must pay an extremely high deductible

($12,500—which he meets in February) before

his plan will begin covering part of his cancer

care costs. Once his plan begins covering some

costs, he still must pay multiple thousands of

dollars every month until he completes his active

treatment in June. At the end of the year, he had

paid a total of $1,878 in premiums and $49,782

in cost sharing and costs for uncovered

services, for an annual total of $51,660.*

The total health care costs for Brian’s

Non-Hodgkin’s Lymphoma treatment were

$97,849. While Brian’s STLD plan did pay some

of these costs, it did not cover nearly as many

of the costs that a comprehensive, Affordable

Care Act (ACA)-compliant plan would have paid.

Despite being marketed as an insurance plan,

STLD plans are not considered comprehensive

insurance coverage, and Brian was responsible

for 51% of his cancer costs.

While Brian has finished his active cancer

treatment, he will continue to have tests and

imaging for the next 5 years, so his out-of-pocket

will likely continue to be higher than before he

had cancer. If/when he chooses to have children,

he will likely also have to pay out-of-pocket for

fertility services because of his treatments.

* Note that these costs only include cancer treatment, and do not include

treatment for other conditions that may have developed as a result of the

cancer treatments and/or any other treatments unrelated to cancer care or

other preventive services.

18 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Data Analysis & Key Findings

Comparing Patient Out-of-Pocket Costs—Key Findings

■

Insurance coverage is critical. In each of the

scenarios, patients paid a considerable sum

out-of-pocket for their care but would have paid

significantly higher amounts if they had not had

insurance coverage.

■

The type of insurance a person with cancer

has is an important factor in how much they

will pay out-of-pocket. The type of insurance

a patient has, and that insurance benefit design,

determines how much the patient pays, and in

what form they pay it—e.g. in premiums that

are a fixed monthly amount, in deductibles and

cost sharing that are less predictable, or in

uncovered costs that can be unlimited.

●

In these scenarios, the patient with the large

employer plan pays the least out-of-pocket,

with relatively affordable premiums and cost-

sharing amounts, and a smaller out-of-pocket

maximum that is met early in the year.

●

Patients with a small-employer, high deductible

health plan or individual marketplace plan have

much higher deductibles and maximum out-of-

pocket limits and pay more overall.

●

Patients with Medicare (including Medigap

coverage) pay a high amount every month

in premiums, but lower amounts in co-pays

and co-insurance. In these scenarios, the

patients’ supplemental Medigap plan requires

the highest premiums, but also protects the

patients from paying 20% co-insurance on

many treatments. The majority of Medicare

enrollees have similar supplemental coverage,

but patients who do not have this coverage

pay much higher cost-sharing amounts.

●

The patient with a short-term limited duration

(STLD) plan must pay a much higher

deductible—almost twice as high as any other

deductible in the model—and must pay the

full price for many expenses that are not even

covered by the insurance plan.

■

Out-of-pocket limits help protect cancer

patients. Cancer patients are super-utilizers

of their insurance benefits, and each patient

in the scenarios who had an out-of-pocket

limit reached their maximum quickly. Once the

maximum is reached, patients do not have

to pay cost sharing for in-network, covered

services. This is an important protection for

many privately-insured patients.

The Dangers of Non-Comprehensive Coverage

Brian, who bought a short-term limited duration plan, paid over 4 times as

much as any of the other cancer patients profiled in out-of-pocket costs.

He did not realize that his plan had huge gaps in coverage (for instance it

doesn’t cover any prescription drugs) and now has to go into serious debt

to pay for his cancer treatments.

19American Cancer Society Cancer Action Network The Costs of Cancer 2020

$ 6

0,000

$ 5

0,000

$ 4

0,000

$ 3

0,000

$ 20,000

$ 1

0,000

$ 0

Colorectal

Cancer–

Medicare

Breast Cancer–

Small Employer

High Deductible Plan*

Prostate Cancer–

Large Employer Plan

Pancreatic Cancer–

Medicare

Lung Cancer–

Individual Marketplace

Plan

Lymphoma–

Short-term Limited

Duration Plan

*Annual costs for year 1 of breast cancer treatment

$318

$250

$4,864

$2,150

$6,000

$1,712

$2,500

$2,030

$1,517

$4,864

$1,650

$6,500

$3,896

$36,447

$12,500

$1,878

$500

$835

$250

Total:

$5,432

Total:

$9,862

Total:

$5,030

Total:

$6,631

Total:

$12,046

Total:

$5 1, 660

Uncovered Services

Co-pays & Co-insurance

Deductible

Premiums

Patient Out-of-Pocket Costs Vary Widely, Particularly for

Deductibles and Uncovered Services

20 American Cancer Society Cancer Action Network The Costs of Cancer 2020

$6

0,000

$5

0,000

$4

0,000

$3

0,000

$20,000

$10,000

$0

ACA-Compliant or

Comprehensive Plans

$8,684

$10,747

$6,446

$12,931

$5 1, 660

Medicare Small Employer,

High Deductible

Health Plan

Large Employer

Plan

Short-term Limited

Duration Plan

Individual

Marketplace Plan

Total Annual Costs Paid by Brian, Lymphoma Patient in Each Plan Type

Patient Out-of-Pocket Costs Vary Widely,

Even for the Same Patient

Brian’s out-of-pocket

costs vary from over

$6,000 to almost

$13,000 amongst the

ACA-compliant plans

we included in our

analysis.

His out-of-pocket costs

were over 4 times

higher when he had a

STLD plan that was not

ACA-compliant.

Patient Costs Throughout the Year—Key Findings

■

Out-of-Pocket cancer costs spike quickly.

Almost all of our cancer patients had to pay

several thousands of dollars in the first one to

three months after the

first suspicion of cancer.

Note that many of these

costs were before the

patient was officially

diagnosed—as some

diagnostic tests can be

quite expensive. High

amounts of spending

are required until the

cancer patient meets his

or her deductible and

maximum out-of-pocket

limit (if applicable).

■

Costs spike higher for patients with higher

deductibles and maximum out-of-pocket

limits. Patients with a high deductible or

maximum out-of-pocket limit experience higher

spikes and more uneven month-to-month

spending patterns because a higher amount

of spending is required up-front before the

plan begins covering expenses. This can cause

significant financial hardship for patients who

cannot afford to pay large medical bills all at

once, and can also cause patients to delay tests

or treatments.

19

■

Medicare patients see different spending

patterns. Because a majority of Medicare

enrollees purchase supplemental coverage,

most Medicare patients pay lower cost-sharing

amounts. For the Medicare patients in our

scenarios, their spending did not spike until

they started taking pharmacy drugs—which are

covered through Medicare Part D rather than

their Medigap plan and require cost sharing,

which can often be significant and is not capped.

■

STLD plans play by their own rules (or lack

thereof). Because STLD plans are not required

to have particular maximum out-of-pocket

limits or cover specific services, the spending

pattern under this plan is vastly different. Brian’s

spending spikes much higher, and for a longer

amount of time, than the other patients. This is

because his plan requires a very high deductible,

has a high maximum out-of-pocket limit (note:

some STLD plans do not have such a limit at

all), and does not cover important services like

prescription drugs. Therefore, Brian’s high out-

of-pocket costs never relent until he finishes his

active cancer treatment in July.

The Costs of Cancer Disparities

Could YOUR monthly budget accommodate

a $5,000 (or higher) medical bill? These

spending spikes are hard to afford even for

middle-and high-income people with cancer.

An annual survey shows that 37% of

Americans would NOT be able to cover a one-

time unexpected expense of $400 without

borrowing money or using a credit card that is

not paid off in full at the end of the month. The

survey found that people of color and those

with less education are more likely to have

trouble covering an unexpected expense.

18

21American Cancer Society Cancer Action Network The Costs of Cancer 2020

$ 1

6,000

$ 14,000

$ 12,000

$ 1

0,000

$ 8,000

$ 6,000

$ 4,000

$ 2,000

$ 0

January

February

March

April

May

June

July

August

September

October

November

December

*Monthly costs for year 1 of breast cancer treatment

Brian–Lymphoma–Short-term Limited Duration Plan

Carla–Breast Cancer–Small Employer High Deductible Plan*

Kathy–Lung Cancer–Individual Marketplace Plan

Franklin–Prostate Cancer–Large Employer Plan

Tom–Colorectal Cancer–Medicare

Shonda–Pancreatic Cancer–Medicare

Monthly Patient Out-of-Pocket Spending Spikes Within

1-3 Months of Diagnosis

22 American Cancer Society Cancer Action Network The Costs of Cancer 2020

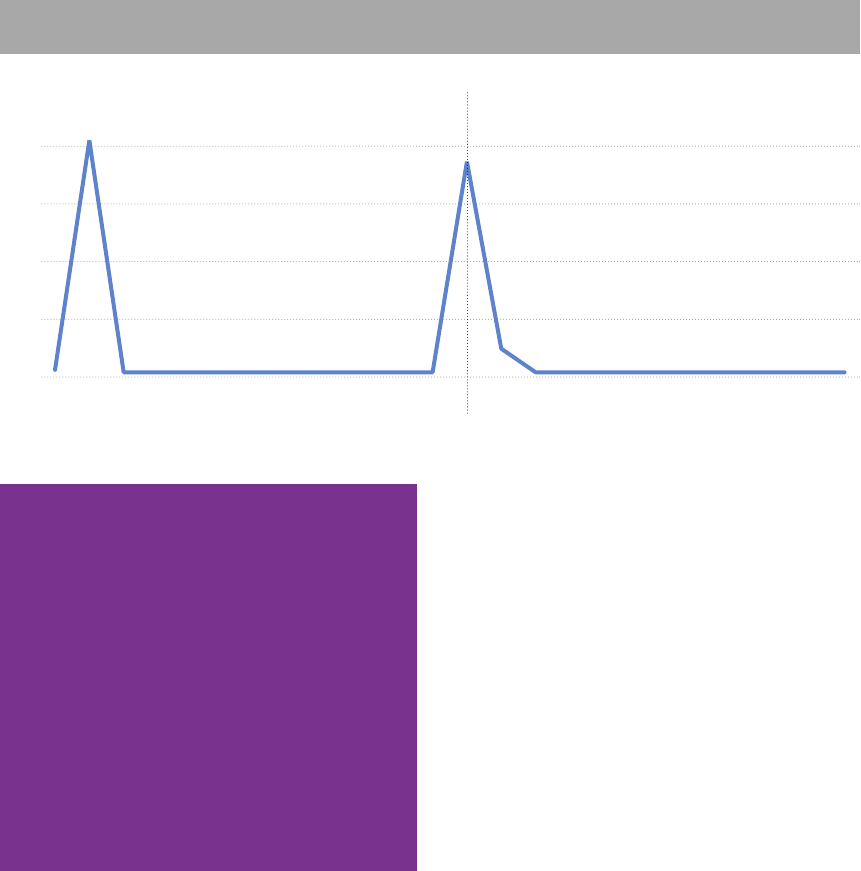

Patient Out-of-Pocket Spending Over Multiple Years—Key Findings

■

The higher costs of cancer can span

multiple years. Carla had an aggressive form

of breast cancer that required several months of

chemotherapy before surgery, and many months

of drug therapy after surgery. Her cancer

experience—and therefore her spending on

cancer treatments—did not fit neatly into a one-

year timeline. Most patients’ cancer treatments

cross plan years. Over the two years we tracked

Carla’s spending on cancer treatments, she

paid her full maximum out-of-pocket amount

twice—resulting in two spending spikes. As

she continues to need follow-up care after her

treatments, she will continue to pay higher costs

for multiple years into survivorship.

Januar

y

April

July

October

Januar

y

April

July

October

Year

1Y

ear 2

$8,000

$6,000

$4,000

$2,000

$0

Two Years of Monthly Out-of-Pocket Costs for Carla, Breast Cancer Patient

When Cancer Treatments Span Multiple Years, Patient Out-of-Pocket

Spending Spikes Multiple Times

The Costs of Cancer Disparities

■

Breast cancer is the most commonly

diagnosed cancer in Hispanic women, and is

also the leading cause of cancer death in this

population.

■

Breast cancer is less likely to be diagnosed

at a local stage in Hispanic women compared

to non-Hispanic white women. Lower rates of

mammography screening and delayed follow-

up on abnormal test results or self-discovered

abnormalities likely contribute to this disparity.

■

Hispanic women are less likely than non-

Hispanic whites to receive appropriate and

timely breast cancer treatment.

Source: American Cancer Society.

20

23American Cancer Society Cancer Action Network The Costs of Cancer 2020

Insurance Coverage Transitions—Key Findings

■

Changing insurance plans mid-year or

mid-treatment can cause spending spikes

and higher total costs. If a cancer patient

must change insurance coverage mid-year or

mid-treatment, they will likely be required to pay

the new plan’s deductible and maximum out-

of-pocket amount—resulting in higher annual

costs for the patient and multiple spikes in

monthly spending. Higher costs also may result

from the new plan covering different benefits

and/or providers. A patient may have to change

their insurance plan mid-year or mid-treatment

if they have:

●

Changed jobs

●

Lost their job, or had to reduce hours to

part-time because of their health, cancer

treatments, or external factors

●

Moved to a new state, and did not have

coverage that transferred to the new state or

had providers located in the patient’s new area

●

Were no longer able to afford paying

premiums

$8,000

$1

0,000

$6,000

$4,000

$2,000

$0

January

February

March

April

May

June

July

August

September

October

November

December

Franklin—Switches Plan Mid-Year

Franklin—Stays in Large Employer Plan All Year

Changing Insurance Mid-Year Causes Higher Costs and Multiple Spikes

Monthly Out-of-Pocket Costs for Franklin, Prostate Cancer Patient

Franklin loses his

job and must

switch to an

Individual

Marketplace Plan

Franklin’s total

annual cost:

$14,580

Franklin’s total

annual cost:

$5,030

The Costs of Cancer Disparities

What if Franklin wasn’t able to afford to enroll in a

marketplace plan right away after he lost his job and

employer-sponsored insurance? A recent study

21

showed:

Disruptions in insurance coverage are common among low-

income populations.

Compared to people whose insurance coverage was

continuous, those with disruptions were less likely to receive

cancer prevention, screening, and treatment.

24 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Types of Cancer Costs—Key Findings

■

Type of cancer and treatment plan cause

huge variation in the source of cancer costs.

For all of the patients included in our analysis,

the majority of their cancer treatment costs

came from drugs, hospital costs, and/or surgical

procedures. This amount varied, however,

depending on the patient’s treatment plan.

■

There are many drivers of the costs of

cancer. While much attention tends to focus on

drug costs, and whether they are rising, other

types of treatments and services drive many of

the costs for people with cancer.

0% 10% 20% 30%40% 50%60% 70%80% 90

%1

00%

Percentage of To tal (Patient & Payer) Costs, Per Treatment Type

Tom—Colorectal Cancer

Carla—Breast Cancer*

Franklin—Prostate Cancer

Shonda—P

ancreatic Cancer

Kathy—Lung Cancer

Brian—Lymphoma

Drugs Radiation Treatments Hospital Costs/Surgical Procedures Doctor's Visits Imaging Tests Laboratory Tests

*Percentage of total costs for 2 years of breast cancer treatment

The Drivers of Cancer Costs Vary Widely Among Patients

25American Cancer Society Cancer Action Network The Costs of Cancer 2020

Spotlight on Drug Costs—Key Findings

■

Patients and payers can save when patients

take biosimilars. In our breast cancer scenario,

Carla underwent drug therapy spanning multiple

years. Under the scenario where she was

able to substitute one of her main drugs for a

biosimilar version, total spending on drugs was

reduced by 21%.

$8

0,000

$6

0,000

$70,000

$5

0,000

$4

0,000

$3

0,000

$20,000

$10,000

$0

$58,906

$74,487

Using Brand-name Drug Using Biosimilar

21%

reduction

Patients and Payers Save With the Use of Biosimilars

Carla, Breast Cancer: Total Expenditures Over 2 Years for Targeted Therapy

26 American Cancer Society Cancer Action Network The Costs of Cancer 2020

0% 10% 20% 30%40% 50%60% 70%80% 90

%1

00%

Percentage of To tal (Patient & Payer) Drug Costs, Per Drug Type

Tom—Colorectal Cancer

Carla—Breast Cancer*

Franklin—Prostate Cancer

Shonda—P

ancreatic Cancer

Kathy—Lung Cancer

Brian—Lymphoma

Physician-administered Anti-cancer Drugs Pharmacy Anti-cancer Drugs Pharmacy Supportive Care Drugs

* Percentage of drug costs for 2 years of breast cancer treatment

Drivers of Drug Costs in Cancer Care Vary Widely

■

The drivers of drug costs in cancer care

vary widely based on the patient’s treatment

plan. Anti-cancer drugs meant to kill cancer

cells or keep them from returning—including

chemotherapy, immunotherapy and hormone

therapy drugs—can be delivered intravenously

in a doctor’s office, or via a pill obtained at the

pharmacy. Supportive care drugs—intended

to help patients with side effects like nausea

and pain—are also an important part of cancer

drug treatment and can come in either form.

Insurance plans often treat drugs differently—

including placing them on different tiers and/or

charging patients different amounts—depending

on these distinctions.

27American Cancer Society Cancer Action Network The Costs of Cancer 2020

Unexpected Problems that Add to

Patient Out-of-Pocket Costs

In each of the modeled scenarios included in this report, analysts

assumed that the cancer patients had no problems using their

insurance benefits, and that each insurance plan covered every

treatment.

22

In reality, many people with cancer encounter problems

that cause delays and complications and further increase their costs.

Below are several common scenarios patients encounter that make

their out-of-pocket costs higher than what was modeled in this

report, or what the patient expected.

No Insurance Coverage

While each patient profiled in this report had

insurance coverage (note: Brian’s STLD plan—

which left many treatments uncovered—is not

considered comprehensive insurance), we know

that millions of Americans are still uninsured.

23

Some of these Americans are diagnosed with

cancer every year. While some uninsured cancer

patients are able to negotiate discounts or qualify

for charitable programs to help pay for their

care, they are never guaranteed treatment. An

uninsured cancer patient is responsible for all

costs of their treatment,

and many forego care due

to cost.

Example: what if Kathy

didn’t have insurance

coverage?

In our scenario, Kathy has

insurance coverage through

her state’s individual

marketplace. At the end of the year in which

she is diagnosed with Stage IV lung cancer, she

has paid over $12,000 in premiums and cost-

sharing—not a small amount. However, if Kathy

were uninsured, she would be responsible for the

entire cost of her cancer care—over $140,000

(or likely higher because she would not benefit

from a plan’s negotiated rates). While she might

be able to negotiate discounts with providers or

receive some charity care, these costs and the

uncertainty of how to pay them would likely to

take a huge toll on Kathy’s financial, emotional

and physical quality of life.

Inadequate Coverage

Some consumers struggle to afford health

insurance premiums, and when shopping for

cheaper premiums may unknowingly enroll in a

plan that has inadequate coverage. Plans like

short-term limited duration insurance—which

despite the name, can last the same amount of

time as other insurance plans—and Association

Health Plans do not have to follow all of the

requirements in the ACA and other regulations.

These plans are missing comprehensive patient

protections, and an enrollee who is diagnosed

with a serious illness like cancer while enrolled in

one of these plans will likely discover that it does

not cover what they expected when purchasing

the plan. Because of this, the patient pays

catastrophically high costs.

$1

50,000

$90,000

$120,00

0

$60,000

$30,000

$0

$140,247

$12,046

With Individual

Marketplace Plan

With No Insurance

Costs are Much Higher for

Uninsured Patients

Annual out-of-pocket costs for Kathy,

lung cancer patient

The Costs of Cancer Disparities

■

Most uninsured people are in low-income

families and have at least one worker in

the family.

■

Adults are more likely to be uninsured

than children.

■

People of color are at higher risk of being

uninsured than non-Hispanic Whites.

24

28 American Cancer Society Cancer Action Network The Costs of Cancer 2020

Example: Brian has a short-term limited

duration plan.

As a young adult who works several part-time

and freelance jobs, Brian was left to find health

insurance on his own. He went online and

bought the cheapest plan he could find through

an insurance broker website, not understanding

that this short-term plan does not cover a

comprehensive set of benefits or have to follow

other patient protections. He knew it had a high

deductible, but he did not expect to need many

health care services this year. Unfortunately, Brian

is diagnosed with lymphoma and discovers that

his plan’s coverage is extremely limited. At the

end of his year of cancer treatments, Brian’s plan

has covered less than half of his cancer treatment