Counterpoint Global Insights

Categorizing for Clarity

Cash Flow Statement Adjustments to Improve Insight

Investing

CONSILIENT OBSERVER | October 6, 2021

Introduction

You can think about a business using some simple ideas. A

company spends money on investments that are expected to

generate good returns relative to the capital’s opportunity cost. It

then sells a good or service to customers that generates revenues

and incurs expenses. The difference between revenues and costs

is operating income, and after financing costs and taxes a company

is left with net income. When income exceeds investments, the

company generates cash that it can return to the capital providers.

When investments exceed income, the company has to raise

capital, usually by issuing debt or equity.

The objective of financial statements is to help investors, creditors,

and other interested parties understand the business. Financial

statements are intended to be relevant and to have predictive

value.

1

In standard finance, discounted cash flow (DCF) models

are based on free cash flow, the difference between net operating

profit after taxes (NOPAT) and investment in future growth. The

analyst projects cash flows and then discounts them to estimate

today’s value.

Public companies are required to disclose an income statement, a

balance sheet, and a statement of cash flows. The income

statement starts with revenue and shows the costs and expenses

that lead to net income for a given period. The balance sheet

provides a snapshot of a company’s assets as well as the liabilities

and equity used to finance them.

The statement of cash flows classifies cash inflows and cash

outflows into three categories: cash flow from operating activities,

cash flow from investing activities, and cash flow from financing

activities. The sum of the three categories reconciles a company’s

cash and cash equivalents from one period to the next. The

statement of cash flows is a relatively recent accounting statement,

having been required in its current form only since 1988.

2

AUTHORS

Michael J. Mauboussin

michael.mauboussi[email protected]om

Dan Callahan, CFA

dan.callahan1@morganstanley.com

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

2

Most financial statement analysis is focused on the income statement and balance sheet, and the statement of

cash flows is often treated as “an after-thought.”

3

But the statement of cash flows appears to match the basic

activities of a business. Cash flow from investing activities tells you how much money the company spent to

generate future growth. Cash flow from operating activities goes beyond net income to reveal the cash in and

out associated with activities based on the customer. And cash flow from financing reveals how the company

addresses gaps between the cash flows associated with investments and operations.

A company is in a position to return cash to capital providers when the operations generate more cash than

investment needs. When investment needs exceed cash from the operations, the company must raise capital

to plug the gap. To be clear, negative free cash flow is not only fine but desirable when the return on investment

is attractive.

4

The point of this report is that today’s accounting creates a huge gap between financial statements and what an

investor needs to understand a business. This is despite the conceptual match between categories on the

statement of cash flows and how businesses work.

We will show how moving certain items from one category to another improves relevance without affecting the

essential task of cash reconciliation.

5

A clearer understanding of the cash in, cash out, and financing activities

provides relevance and predictive value beyond the current standards. This analysis is important because an

accurate measure of the magnitude of investment and profitability is essential to understanding the business.

We use Amazon as our case study, but the analysis is relevant for nearly all companies. We limit the discussion

to historical numbers to illustrate the concepts without implying anything about future results or the stock price.

The main takeaway is that Amazon’s cash flow from operating activities and cash flow from investing activities

are both substantially higher than what the company reports based on accepted accounting principles.

The definition of free cash flow that investors and companies commonly use is cash from operating activities

minus capital expenditures.

6

This is inconsistent with finance theory and can be a very misleading heuristic. To

Amazon’s credit, they provide multiple definitions of free cash flow. The company starts with the popular one but

includes alternative calculations that better reflect the magnitude of investment. Our adjustments do not change

a company’s free cash flow, properly defined, but do change the composition.

7

Adjustments to Improve Insight

We suggest moving the location of stock-based compensation (SBC), leases, and intangible investments within

the statement of cash flow. Removing the purchases and sales of marketable securities from investing activities

may also be appropriate.

Stock-based compensation. Using equity to pay employees is relatively new. As recently as the mid-1980s,

fewer than one-half of the chief executive officers (CEOs) of publicly-traded companies in the United States were

paid in stock or stock options. By 2000, equity was about two-thirds of the median annual pay for CEOs.

8

We

can attribute this large shift to a number of factors. First, the median percentage direct ownership of stock by

CEOs of the top 120 public companies in the U.S. was 8 times higher in 1938 than it was in 1988. The amount

of skin in the game for CEOs had been trending lower for decades.

9

A vibrant market for corporate control arose in the 1980s, encouraging many boards to try to reduce agency

costs by aligning the interests of executives and shareholders. Paying with equity helped with this alignment.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

3

But there is an essential distinction between incentive compensation, where pay is linked to performance, and

equity compensation as a pay delivery mechanism.

Another factor behind the increase in SBC was the rising stock market in the 1990s. For example, for the 10

years ended in 1997, total shareholder returns were positive for each of the top 100 companies in the U.S. That

means that all CEOs who had SBC made money, even if their relative performance was poor.

10

Finally, for a long time SBC did not show up as an expense on the income statement. Not until 2006 was

expensing compulsory under U.S. generally accepted accounting principles (GAAP). The details of employee

stock options were disclosed in the footnotes, but that an obvious expense was not included in the calculation

of earnings encouraged their profligate use.

The Financial Accounting Standards Board (FASB) clearly believed that employee stock options were a cost

that should be on the income statement. But accounting firms and companies, especially in the technology

industry, lobbied heavily against including the expense. The misguided reasoning was that lower earnings would

translate into lower stock prices. Dennis Beresford, then chairman of the FASB, recalls: “People said to me, ‘If

we have to record a reduction in income by 40%, our stock will go down by 40%, our options will be worthless,

we won't be able to keep employees. It would destroy all American business and Western civilization.’”

11

Academic research shows that these concerns came to naught.

12

But even as the issue of expensing SBC on the income statement has long been resolved, accountants still add

back SBC expense in the calculation of cash flow from operations. SBC is a legitimate expense that should not

be reversed.

13

Small companies, which generally have fewer financial resources than large ones do, rely heavily

on SBC. Employees provide both a source of financing and a service.

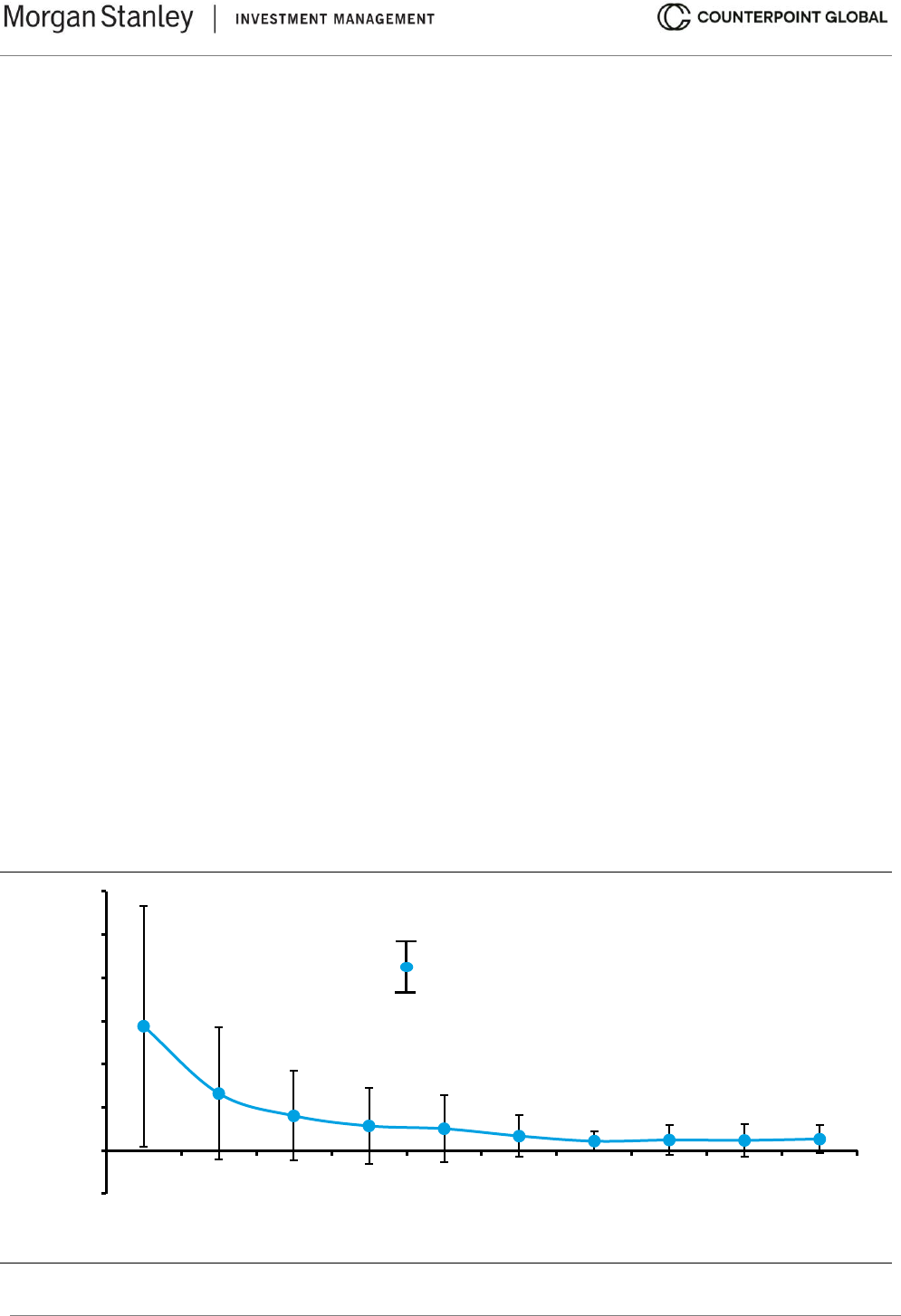

Exhibit 1 shows SBC as a percentage of sales for companies in the Russell 1000 Index based on size. The

index is the top thousand companies in the U.S. measured by market capitalization. The ratio of SBC to sales is

about 15 percent for the smallest companies and declines steadily to about 1 percent for the largest companies.

Further, SBC is strongly correlated with intangible investment.

14

Exhibit 1: Stock-Based Compensation as a Percentage of Sales by Size, Russell 1000, 2020

Source: FactSet.

Note: Russell 1000 as of 12/31/20; Data for calendar year 2020; Companies with minimum sales of $10 million.

-5

0

5

10

15

20

25

30

<0.75 0.75-1.25 1.25-2 2-3 3-4.5 4.5-6.5 6.5-10 10-15 15-30 >30

Stock

-Based Compensation

as a Percentage of Sales

Sales, Latest Fiscal Year ($ Billions)

-1 Standard Deviation

Mean

+1 Standard Deviation

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

4

You can think of SBC as one number that reflects two transactions.

15

The company first sells shares (financing)

and then uses the proceeds to pay employees (compensation for service). Combine these ideas and it makes

sense to move SBC from the cash flow from operating activities section to the cash flow from financing activities

section. This portrays the cash flow statement more accurately.

Amazon’s SBC was $9.2 billion in 2020, or 14 percent of its cash flow from operating activities and 30 percent

of its primary measure of free cash flow, cash flow from operating activities minus net purchases of property and

equipment. Reclassifying their SBC reduces that measure of free cash flow from $31.0 billion to $21.8 billion.

Exhibit 2 shows median and aggregate SBC as a percentage of cash flow from operating activities for sectors

in the Russell 1000. SBC was most significant for technology companies. For this sector, the median ratio of

SBC to cash flow from operating activities was 25 percent and the aggregate was 15 percent.

Exhibit 2: Median and Aggregate Stock-Based Compensation Relative to Cash Flow from

Operating Activities for Sectors, Russell 1000, 2020

Sector

Median

Aggregate

Information Technology

25.0%

14.7%

Health Care

8.1%

6.4%

Consumer Discretionary

5.1%

8.2%

Industrials

4.7%

8.0%

Energy

4.5%

5.2%

Consumer Staples

3.4%

3.5%

Telecommunication Services

3.1%

4.4%

Materials

2.9%

2.6%

Utilities

1.6%

2.0%

Total

5.7%

8.6%

Source: FactSet.

Note: Russell 1000 excluding financial and real estate sectors as of 12/31/20; Data for calendar year 2020.

This discussion has no bearing on the merits of SBC. Using stock for compensation can make sense because

it provides a source of capital and aligns the interests of employees and shareholders. The crucial point is to

think of SBC properly in the context of how a business creates value.

Leases. A company that invests in a physical asset can generally buy it or lease it. A lease is a contract by

which the lessor agrees to allow the lessee the use of an asset for a specific period in return for a periodic

payment. For example, say you are at an airline and are in charge of acquiring aircraft. You would analyze the

pros and cons of a purchase versus a lease and select the one that makes the most sense financially. Airlines

in fact buy and lease, as do many companies making the investments required to create value.

Investors need to understand the magnitude of investment. The problem is that the assets a company purchases

show up in cash flow from investing activities, while assets that are leased are reflected in cash flow from

financing activities. The adjustment here is to move the property and equipment acquired with leases into the

section that captures cash flow from investing activities.

For Amazon, $10.7 billion moves from the financing to the investing category, taking the company’s cash flow

from investing activities from an outflow of $59.6 billion to an outflow of $70.3 billion, an 18 percent increase. It

also reduces the company’s secondary definition of free cash flow, cash flow from operating activities minus net

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

5

purchases of property and equipment less principal repayments of finance leases and financing obligations, from

$31.0 billion to $20.3 billion. Remove the SBC addback and free cash flow drops to $11.1 billion.

To be clear, Amazon adheres to all accounting standards and provides this modified definition of free cash flow.

They specifically disclose that, “In this measure [of free cash flow], property and equipment acquired under

capital leases is reflected as if these assets had been purchased for cash.”

16

While we focus here on capturing the large adjustment from the financing to the investing sections, further

modifications are necessary to properly calculate net operating profit after taxes in order to build an unlevered

discounted cash flow model.

17

Intangible Investments. The most significant adjustment deals with intangible investments. An investment is

an outlay today with the expectation of an attractive return based on the present value of future cash flows. Until

the 1990s, tangible investments exceeded intangible ones. Further, the basic structure of financial statements

was developed to reflect a world of tangible assets and has not changed much in a century.

18

Companies now invest much more in intangible assets than in tangible assets.

19

Intangible assets are not

physical and include employee training, brand building, and software code. Tangible assets are physical, such

as factories, airplanes, and machines. We estimate that companies in the Russell 3000 made $1.8 trillion in

intangible investments in 2020 and spent $900 billion on capital expenditures.

20

Accountants record most intangible investments on the income statement. The essential adjustment is to move

intangible investment from cash flow from operating activities, where it is hidden, to cash flow from investing

activities.

The analytical challenge is to separate selling, general, and administrative (SG&A) expenses into what is an

investment and what is necessary to maintain the business. In recent years, academics have developed

techniques to do this. The split between discretionary and maintenance SG&A spending is different based on

the industry and the company.

21

We use these techniques to estimate Amazon’s investment in intangible assets. We assume that fulfillment

costs, about 45 percent of total SG&A, are linked to current sales and hence have no investment component.

These are predominately the expenses to operate fulfillment centers, stores, and customer service centers.

Estimating intangible investment for the remaining SG&A requires two significant assumptions: the percentage

of an expense item that is deemed an investment and the appropriate amortization period. We designate three-

quarters of technology and content expense, one-half of marketing expense, and one-fifth of general and

administrative expense as investment in intangible assets. This suggests that 62 percent of eligible SG&A, and

34 percent of total SG&A, are discretionary investments. Exhibit 3 shows the relevant components of SG&A in

2020 multiplied by the percent allocated to intangible investment.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

6

Exhibit 3: Estimate of Amazon’s Intangible Investments, 2020

Item

Amount

Percent

Allocated to

Intangible

Intangible

Investment

Technology and content

$42.7 billion

75%

$32.1 billion

Marketing

22.0

50

11.0

General and administrative

6.7

20

1.3

Total

$71.4 billion

$44.4 billion

Source: Amazon.com and Counterpoint Global estimates.

We assume a useful life of five years for investments in technology and content and three years for investments

in marketing and general and administrative. We create a schedule to capitalize and amortize these estimates

through time. The amortization of past intangibles in 2020 equaled $25.4 billion.

The adjustment to cash flow from operating activities is in two parts. First, net income increases by $19.0 billion,

the $44.4 billion of intangible investment minus the $25.4 billion in amortization. Second, depreciation and

amortization rises by $25.4 billion. The sum of $19.0 billion and $25.4 billion is $44.4 billion, the figure we want

to reflect in cash flow from operating activities and cash flow from investing activities. Exhibit 4 summarizes the

net result of these category changes.

Exhibit 4: Summary of Category Changes for Amazon, 2020

Cash Flow from:

Operating

Activities

Investing

Activities

Financing

Activities

Reported total

$66.1 billion

-$59.6 billion

-$1.1 billion

Stock-based compensation

-9.2

9.2

Leases

-10.7

10.7

Intangible investments

44.4

-44.4

Adjusted total

$101.2 billion

-$114.7 billion

$18.8 billion

Source: Amazon.com and Counterpoint Global estimates and adjustments.

Cash flow from operating activities increases 53 percent, from $66.1 billion to $101.2 billion. Adding intangible

investment net of amortization results in a near doubling of net income, from $21.3 billion to $40.3 billion.

Cash flow from investing activities goes from an outflow of $59.6 billion to an outflow of $114.7 billion. This is an

essential insight for an investor who is trying to get a clear sense of the magnitude of investment in order to

make an intelligent forecast about future profits.

Cash flow from financing activities goes from -$1.1 billion to $18.8 billion, suggesting the company raised capital

to finance its operations. Note that the sum of the three sections is identical whether you use the as reported or

the adjusted figures. Exhibit 5 summarizes the statement of cash flows before and after the adjustments.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

7

Exhibit 5: Summary of Adjustments to Amazon’s Statement of Cash Flows

As Reported With Adjustments

Source: Amazon.com, Form 10-K, December 31, 2020, Counterpoint Global estimates and adjustments.

Note: *D&A=depreciation and amortization.

In millions of U.S. dollars 2020 In millions of U.S. dollars 2020

Operating Activities Operating Activities

Net income 21,331 Net income 21,331

Intangible investment 44,393

Amortization of intangible investment (25,410)

Adjusted net income 40,314

Adjustments to reconcile net income to net cash from

operating activities

Adjustments to reconcile net income to net cash from

operating activities

D&A* of property and equipment and capitalized

content costs, operating lease assets, and other

25,251

D&A* of property and equipment and capitalized

content costs, operating lease assets, and other

25,251

Amortization of intangible investment 25,410

Stock-based compensation 9,208

Other operating expense (income), net (71) Other operating expense (income), net (71)

Other expense (income), net (2,582) Other expense (income), net (2,582)

Deferred income taxes (554) Deferred income taxes (554)

Changes in operating assets and liabilities Changes in operating assets and liabilities

Inventories (2,849) Inventories (2,849)

Accounts receivable, net and other (8,169) Accounts receivable, net and other (8,169)

Accounts payable 17,480 Accounts payable 17,480

Accrued expenses and other 5,754 Accrued expenses and other 5,754

Unearned revenue 1,265 Unearned revenue 1,265

Net cash provided by (used in) operating activities 66,064 Net cash provided by (used in) operating activities 101,249

Investing Activities Investing Activities

Purchases of property and equipment (40,140) Purchases of property and equipment (40,140)

Proceeds from property and equipment sales and

incentives

5,096

Proceeds from property and equipment sales and

incentives

5,096

Principal repayments of finance leases (10,642)

Principal repayments of financing obligations (53)

Acquisitions, net of cash acquired, and other (2,325) Acquisitions, net of cash acquired, and other (2,325)

Sales and maturities of marketable securities 50,237 Sales and maturities of marketable securities 50,237

Purchases of marketable securities (72,479) Purchases of marketable securities (72,479)

Intangible investment (44,393)

Net cash provided by (used in) in investing activities (59,611) Net cash provided by (used in) in investing activities (114,699)

Financing Activities Financing Activities

Proceeds from short-term debt, and other 6,796 Proceeds from short-term debt, and other 6,796

Repayments of short-term debt, and other (6,177) Repayments of short-term debt, and other (6,177)

Proceeds from long-term debt 10,525 Proceeds from long-term debt 10,525

Repayments of long-term debt (1,553) Repayments of long-term debt (1,553)

Principal repayments of finance leases (10,642)

Principal repayments of financing obligations (53)

Stock-based compensation 9,208

Net cash provided by (used in) financing activities (1,104) Net cash provided by (used in) financing activities 18,799

Foreign-currency effect on cash and cash equivalents 618 Foreign-currency effect on cash and cash equivalents 618

Net increase (decrease) in cash and cash equivalents 5,967 Net increase (decrease) in cash and cash equivalents 5,967

Cash, cash equivalents, and restricted cash, beginning

of period

36,410

Cash, cash equivalents, and restricted cash, beginning

of period

36,410

Cash, cash equivalents, and restricted cash, end of

period

42,377

Cash, cash equivalents, and restricted cash, end of

period

42,377

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

8

Marketable securities. The Statement of Financial Accounting Standards No. 95 specifies where particular

cash receipts and cash payments are classified within the statement of cash flows. It notes that cash outflows

from investing activities include payments “to acquire debt instruments of other entities (other than cash

equivalents)” and “to acquire equity instruments of other enterprises.”

22

The standard also says that a “statement of cash flows shall explain the change during the period in cash and

cash equivalents” where cash equivalents are “short-term, highly liquid investments” with original maturities of

three months or less.

The analytical question is whether Amazon’s marketable securities should be treated as a cash equivalent. This

issue is also relevant for other large companies that are rich in cash. The reasoning is that marketable securities

are straightforward to value, non-essential to operations, and designated as current assets, which means they

are expected to be converted to cash within a year.

An analyst who concludes that marketable securities and cash are equivalent can remove the purchases and

sales of marketable securities from the cash flows from investing activities. The statement of cash flows would

then explain the change during the period to reconcile cash, cash equivalents, and marketable securities.

Exhibit 6 shows this additional adjustment for Amazon. As compared to exhibit 5, adjusted cash flow from

operating activities is unchanged at $101.2 billion as is the adjusted cash flow from financing activities of $18.8

billion. But now the revised cash flow from investing activities goes from an adjusted -$114.7 billion to -$92.5

billion. This is the result of reclassifying the net purchase of $22.2 billion of marketable securities in 2020 as a

component of the change in cash, cash equivalents, and marketable securities.

We believe that this adjustment is more open to debate than the other ones but makes sense for certain

businesses, including Amazon.

Impact on Traditional Multiples

Free cash flow, properly defined as net operating profit after taxes (NOPAT) minus investment in future growth

(I). NOPAT and I are both appropriately adjusted up by $19.0 billion. Free cash flow is unchanged, but the path

to get there is markedly different than without the adjustments.

While free cash flow is unaffected, traditional measures of income change dramatically. As a result, common

valuation methods based on multiples can be very misleading. One example is enterprise value-to-earnings

before interest, taxes, depreciation, and amortization (EV/EBITDA). Enterprise value is the sum of the market

value of the company’s debt and equity minus excess cash. At year-end 2020, Amazon’s enterprise value was

just under $1.7 trillion and its 2020 EBITDA was $48.2 billion, for an EV/EBITDA multiple of 35.0.

These adjustments add $44.4 billion to EBITDA ($19.0 billion to EBIT and $25.4 billion to DA), more than a 90

percent increase from the unmodified sum. As a result, the EV/EBITDA multiple falls to 18.2. If these adjustments

make economic sense, the EV/EBITDA multiple is off by a factor of nearly two.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

9

Exhibit 6: Summary of Adjustments to Amazon’s Statement of Cash Flows, Including Treating

Marketable Securities as Cash and Cash Equivalents

As Reported With Adjustments

Source: Amazon.com, Form 10-K, December 31, 2020; Counterpoint Global estimates and adjustments.

Note: *D&A=depreciation and amortization.

In millions of U.S. dollars 2020 In millions of U.S. dollars 2020

Operating Activities Operating Activities

Net income 21,331 Net income 21,331

Intangible investment 44,393

Amortization of intangible investment (25,410)

Adjusted net income 40,314

Adjustments to reconcile net income to net cash from

operating activities

Adjustments to reconcile net income to net cash from

operating activities

D&A* of property and equipment and capitalized

content costs, operating lease assets, and other

25,251

D&A* of property and equipment and capitalized

content costs, operating lease assets, and other

25,251

Amortization of intangible investment 25,410

Stock-based compensation 9,208

Other operating expense (income), net (71) Other operating expense (income), net (71)

Other expense (income), net (2,582) Other expense (income), net (2,582)

Deferred income taxes (554) Deferred income taxes (554)

Changes in operating assets and liabilities Changes in operating assets and liabilities

Inventories (2,849) Inventories (2,849)

Accounts receivable, net and other (8,169) Accounts receivable, net and other (8,169)

Accounts payable 17,480 Accounts payable 17,480

Accrued expenses and other 5,754 Accrued expenses and other 5,754

Unearned revenue 1,265 Unearned revenue 1,265

Net cash provided by (used in) operating activities 66,064 Net cash provided by (used in) operating activities 101,249

Investing Activities Investing Activities

Purchases of property and equipment (40,140) Purchases of property and equipment (40,140)

Proceeds from property and equipment sales and

incentives

5,096

Proceeds from property and equipment sales and

incentives

5,096

Principal repayments of finance leases (10,642)

Principal repayments of financing obligations (53)

Acquisitions, net of cash acquired, and other (2,325) Acquisitions, net of cash acquired, and other (2,325)

Sales and maturities of marketable securities 50,237

Purchases of marketable securities (72,479)

Intangible investment (44,393)

Net cash provided by (used in) in investing activities (59,611) Net cash provided by (used in) in investing activities (92,457)

Financing Activities Financing Activities

Proceeds from short-term debt, and other 6,796 Proceeds from short-term debt, and other 6,796

Repayments of short-term debt, and other (6,177) Repayments of short-term debt, and other (6,177)

Proceeds from long-term debt 10,525 Proceeds from long-term debt 10,525

Repayments of long-term debt (1,553) Repayments of long-term debt (1,553)

Principal repayments of finance leases (10,642)

Principal repayments of financing obligations (53)

Stock-based compensation 9,208

Net cash provided by (used in) financing activities (1,104) Net cash provided by (used in) financing activities 18,799

Foreign-currency effect on cash and cash equivalents 618

Foreign-currency effect on cash, cash equivalents,

restricted cash

1,721

Net increase (decrease) in cash and cash equivalents 5,967

Net increase (decrease) in cash, cash equivalents,

restricted cash, and marketable securities

29,312

Cash, cash equivalents, and restricted cash, beginning

of period

36,410

Cash, cash equivalents, restricted cash, and marketable

securities, beginning of period

55,339

Cash, cash equivalents, and restricted cash, end of

period

42,377

Cash, cash equivalents, restricted cash, and marketable

securities, end of period

84,651

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

10

Exhibit 7 summarizes all of the recommended adjustments and offers a brief rationale for each.

Exhibit 7: Summary of Recommended Adjustments

Item from Cash Flow Statement

From

To

Rationale

Stock-based compensation

(SBC)

Cash flow from

operating activities

Cash flow from

financing activities

SBC is the sale of shares

to pay employees

Principal repayment of

financing obligations

Cash flow from

financing activities

Cash flow from

investing activities

Consolidate investments by

assuming buy and lease are

equivalent

Intangible investment

Cash flow from

operating activities

Cash flow from

investing activities

Discretionary investments

are capitalized instead of

expensed

Marketable securities

Cash flow from

investing activities

Cash, cash

equivalents, and

marketable

securities

When marketable

securities are deemed to

be the same as cash and

cash equivalents

Source: Counterpoint Global.

Conclusion

Understanding the magnitude and prospective return on investment is the principal task of a business analyst.

Financial statements are designed to contribute to this understanding. The investment analyst and academic

communities tend to focus on the income statement and balance sheet. The statement of cash flows, required

in the U.S. only since the late 1980s, documents the cash flows from operations, investing, and financing that

can provide insight into how a business works.

The challenge is that the accounting has not kept pace with the economics. As a result, we suggest three

adjustments within the statement of cash flows to better categorize activities. The first is stock-based

compensation. Accounting standards prescribe adding back this expense to cash flow from operating activities,

but it is better classified as equity financing and therefore should be in cash flow from financing activities.

A company making a physical investment commonly has a choice between purchasing or leasing the asset. It

is an investment in either case, but a purchase and a lease show up in different parts of the statement of cash

flows. We recommend reflecting all of these expenditures in cash flow from investing activities.

There has been a dramatic change in the nature of investment for companies, from tangible to intangible assets,

in recent decades. Accountants place tangible investments on the balance sheet, as they have done for

centuries. But investments in intangible assets are typically expensed on the income statement. This means that

earnings and investments are understated absent any adjustments.

The proper measurement of the magnitude and useful life of intangible assets is a fast-growing area of research.

Our estimates suggest that intangible investments by public companies in the U.S. are more than twice those of

tangible investments. The central issues are which items within selling, general, and administrative expenses

are reasonably considered discretionary investments, and the length of time over which those investments

should be amortized once capitalized on the balance sheet.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

11

A final potential adjustment is to consider marketable securities as part of cash and cash equivalents. This

affects cash flow from investing activities and means that the statement of cash flows is reconciling larger

beginning and ending sums.

We shared a case study of Amazon for 2020 in an effort to make the concepts more concrete. The adjustments

change the portrayal of the company’s finances, including a 53 percent boost in cash flow from operations and

a 92 percent increase in outflows associated with cash flow from investing activities. Excluding net purchases

of marketable securities, the adjusted cash flow from investing activities still shows a 55 percent gain relative to

the unadjusted one.

We believe these adjustments substantially improve the description of a business. But we would add that free

cash flow, defined properly, does not change at all. The main payoff from reclassifying items is a better

appreciation of the cash flows in and out of the company.

Please see Important Disclosures on pages 14-16

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

12

Endnotes

1

“Statement of Financial Accounting Concepts No. 8: Conceptual Framework for Financial Reporting,” Financial

Accounting Standards Board, September 2010.

2

Income statements and balance sheets have been around for a long time (double-entry bookkeeping, a

powerful innovation, goes back to the 13

th

century). In 1863, Northern Central Railroad summarized its cash

transactions in an early version of a cash flow statement. In 1902, U.S. Steel provided a reconciliation of its

current assets minus accounts payable, a rough proxy for working capital. (See

https://digital.case.edu/islandora/object/ksl%3Auniann00.) In 1971, the Accounting Principles Board (APB)

issued Opinion 19, which required a funds statement. In 1987, the Financial Accounting Standards Board (FASB)

released Statement of Financial Accounting Standards No. 95 to supersede Opinion 19. It specified a cash flow

statement be included in financial reports. There are two noteworthy points about FAS No. 95. First, it

encouraged companies to use the “direct method,” which starts the section on cash flows from operations with

receivables from customers, relative to the “indirect method,” which starts the section with net income. Nearly

all companies use the indirect method today. Second, there was substantial dissension on the FASB board,

which is noted in the release. For a more complete discussion see, Geoffrey Poitras, “History of the Cash Flow

Statement” at www.sfu.ca/~poitras/cash-flow-stmt-history.pdf. For a broader discussion of the history of

accounting, see Gary John Previts and Barbara Dubis Merino, A History of Accountancy in the United States:

The Cultural Significance of Accounting (Columbus, OH: Ohio State University Pres, 1998).

3

Allen G. Arnold, R. Barry Ellis, V. Sivarama Krishnan, “Toward Effective Use of the Statement of Cash Flows,”

Journal of Business and Behavioral Sciences, Vol. 30, No. 2, Fall 2018, 46-62.

4

As we have discussed before, Wal-Mart Stores, Inc. had negative free cash flow each year from 1972-1986.

Its annual total shareholder return was 18 percentage points higher than that of the S&P 500 during that period.

5

For example, see the corporate performance statement in Alfred Rappaport, “The Economics of Short-Term

Performance Obsession,” Financial Analysts Journal, Vol. 61, No. 3, May/June 2005, 65-79.

6

Katharine Adame, Jennifer Koski, Katie Lem, and Sarah McVay, “Free Cash Flow Disclosure in Earnings

Announcements,” Working Paper, June 3, 2020. For example, see Paul Roche and Sid Tandon, “SaaS and the

Rule of 40: Keys to the Critical Value Creation Metric,” McKinsey & Company, August 3, 2021.

7

The standard definition of free cash flow in finance is net operating profit after taxes (NOPAT) minus investment

in future growth. NOPAT equals earnings before interest and taxes (EBIT) plus amortization of acquired

intangibles assets minus cash taxes. Cash taxes reflect the tax provision, deferred taxes, and the tax shield. As

such, NOPAT is the unlevered cash earnings of a company. Investment in future growth includes changes in

working capital, capital expenditures net of depreciation, and acquisitions net of divestitures. Two components

of investment are reflected in cash flow from operating activities: depreciation and amortization and changes in

working capital. In Amazon’s case, changes in working capital have historically been a source of cash because

the company receives cash from its customers sooner than it pays its suppliers. (To be more formal, the company

has a negative cash conversion cycle.) In effect, working capital has been a source of financing for the company.

This is not unique to Amazon but is an important consideration in assessing investment, profit, and financing.

8

Brian J. Hall, “Six Challenges in Designing Equity-Based Pay,” Journal of Applied Corporate Finance, Vol. 15,

No. 3, Spring 2003, 21-33.

9

Michael C. Jensen and Kevin J. Murphy, “CEO Incentives: It's Not How Much You Pay, But How,” Harvard

Business Review, Vol. 68, No. 3, May-June 1990, 138-153.

10

Alfred Rappaport, “New Thinking on How to Link Executive Pay with Performance,” Harvard Business Review,

Vol. 77, No. 2, March-April 1999, 91-101.

11

“Stock Options are Not a Free Lunch,” Forbes, May 18, 1998.

12

Judy A. Laux and Abdou N’Dir, “Employee Stock Options and Market Efficiency,” Journal of Applied Business

Research, Vol. 23, No. 2, Second Quarter 2007.

13

Partha Mohanram, Brian White, and Wuyang Zhao, “Stock-Based Compensation, Financial Analysts, and

Equity Overvaluation,” Review of Accounting Studies, Vol. 25, No. 3, September 2020, 1040-1077.

14

Qi Sun and Mindy Z. Xiaolan, “Financing Intangible Capital,” Journal of Financial Economics, Vol. 133, No. 3,

September 2019, 564-588.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

13

15

Sanjeev Bhojraj, “Stock Compensation Expense, Cash Flows, and Inflated Valuations,” Review of Accounting

Studies, Vol. 25, No. 3, September 2020, 1078-1097.

16

Amazon.com, Form 8-K, February 2, 2021.

17

Building an unlevered DCF model requires an adjustment for operating lease expense. After the FASB

updated its standards for Lease (Topic 842) accounting, which most companies had to implement by early 2019,

companies capitalize operating leases but still expense lease costs. The result is a mismatch that needs to be

corrected.

Consistent with the discussion in the body, think of an airline buying a plane and financing it with debt. The

company records the plane as an asset and the debt as a liability. It would then subtract interest expense, a

financing cost, from operating income. Now consider a lease of the plane. Per the updated standard, the plane

would show up on the asset and liability sides of the balance sheet. But the airline records the lease cost as an

operating, rather than a financing, expense. This means that to calculate net operating profit after taxes (NOPAT)

correctly, you need to reclassify the embedded interest portion of the lease cost from the operating section of

the income statement to the financing section. This is only for U.S. GAAP, as the International Accounting

Standards Board (IASB) properly treats the depreciation and interest expense components of operating lease

payments. See Matthew A. Stallings, “The Potential Impact of Lease Accounting on Equity Valuation:

Implications of Cost of Capital and Free Cash Flow Estimates,” CPA Journal, Vol. 87, No. 11, November 2017,

52-56.

18

Baruch Lev and Feng Gu, The End of Accounting and the Path Forward for Investors and Managers (Hoboken,

NJ: John Wiley & Sons, 2016). For the case against capitalizing intangible investments, see Stephen Penman,

Accounting for Value (New York: Columbia Business School Publishing, 2011). Penman writes,

“This view [that accounting is remiss if it does not get the balance sheet right] is shared by those who maintain

that accounting fails by not putting intangible assets on the balance sheet. They ask: How can accountants leave

important assets off the balance sheet, assets such as a firm’s ‘knowledge capital,’ its ‘human capital,’ the

organizational capital’ in its customer and supply-chain relationships, and its R&D assets? Why in the

‘information age’ do we still have a balance sheet more suited for the ‘industrial age’ when value came primarily

from tangible assets rather than intangible assets? Let’s get value back on the balance sheet!

This is an alluring proposal. The fundamentalist, of course, shudders. He or she see the term ‘intangible asset,’

as an excuse for speculation, for putting water on the balance sheet. . . . Anyone drilled in the methods of

accounting for value sees the fallacy in the notion that the balance sheet is remiss if it does not indicate asset

values; there is also an income statement and accounting for value employs both the income statement and the

balance sheet. If value is missing from book value, it can be plugged with earnings from the income statement.”

(179-180).

19

For example, see Carol A. Corrado, Charles Hulten, and Daniel Sichel, “Measuring Capital and Technology:

An Expanded Framework,” in Carol A. Corrado, John Haltiwanger, and Daniel Sichel, eds. Measuring Capital in

the New Economy (Chicago: University of Chicago Press, 2005); Carol A. Corrado, Charles Hulten, and Daniel

Sichel, “Intangible Capital and U.S. Economic Growth,” Review of Income and Wealth, Vol. 55, No. 3, September

2009, 661-685; and Jonathan Haskel and Stian Westlake, Capitalism Without Capital: The Rise of the Intangible

Economy (Princeton, NJ: Princeton University Press, 2017).

20

Michael J. Mauboussin and Dan Callahan, “Market-Expected Return on Investment: Bridging Accounting and

Valuation,” Consilient Observer: Counterpoint Global Insights, April 14, 2021.

21

Aneel Iqbal, Shivaram Rajgopal, Anup Srivastava, and Rong Zhao, “Value of Internally Generated Intangible

Capital,” Working Paper, September 2021 and Luminita Enache and Anup Srivastava, “Should Intangible

Investments Be Reported Separately or Commingled with Operating Expenses? New Evidence,” Management

Science, Vol. 64, No. 7, July 2018, 3446-3468.

22

“Financial Accounting Standards No. 95: Statement of Cash Flows,” November 1987, item 17.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

14

IMPORTANT INFORMATION

The views and opinions and/or analysis expressed are those of the author as of the date of preparation of this

material and are subject to change at any time due to market or economic conditions and may not necessarily

come to pass. Furthermore, the views will not be updated or otherwise revised to reflect information that

subsequently becomes available or circumstances existing, or changes occurring, after the date of publication.

The views expressed do not reflect the opinions of all investment personnel at Morgan Stanley Investment

Management (MSIM) and its subsidiaries and affiliates (collectively “the Firm”), and may not be reflected in all

the strategies and products that the Firm offers.

Forecasts and/or estimates provided herein are subject to change and may not actually come to pass.

Information regarding expected market returns and market outlooks is based on the research, analysis and

opinions of the authors or the investment team. These conclusions are speculative in nature, may not come to

pass and are not intended to predict the future performance of any specific strategy or product the Firm offers.

Future results may differ significantly depending on factors such as changes in securities or financial markets or

general economic conditions.

Past performance is no guarantee of future results. This material has been prepared on the basis of publicly

available information, internally developed data and other third-party sources believed to be reliable. However,

no assurances are provided regarding the reliability of such information and the Firm has not sought to

independently verify information taken from public and third-party sources. The views expressed in the books

and articles referenced in this whitepaper are not necessarily endorsed by the Firm.

This material is a general communications which is not impartial and has been prepared solely for information

and educational purposes and does not constitute an offer or a recommendation to buy or sell any particular

security or to adopt any specific investment strategy. The material contained herein has not been based on a

consideration of any individual client circumstances and is not investment advice, nor should it be construed in

any way as tax, accounting, legal or regulatory advice. To that end, investors should seek independent legal

and financial advice, including advice as to tax consequences, before making any investment decision.

Charts and graphs provided herein are for illustrative purposes only. Any securities referenced herein are solely

for illustrative purposes only and should not be construed as a recommendation for investment.

The Russell 3000® Index measures the performance of the largest 3,000 U.S. companies representing

approximately 98% of the investable U.S. equity market. The Russell 3000 Index is constructed to provide a

comprehensive, unbiased, and stable barometer of the broad market and is completely reconstituted annually

to ensure new and growing equities are reflected. The index is unmanaged and does not include any expenses,

fees or sales charges. It is not possible to invest directly in an index. The index referred to herein is the intellectual

property (including registered trademarks) of the applicable licensor. Any product based on an index is in no

way sponsored, endorsed, sold or promoted by the applicable licensor and it shall not have any liability with

respect thereto.

This material is not a product of Morgan Stanley’s Research Department and should not be regarded as a

research material or a recommendation.

The Firm has not authorised financial intermediaries to use and to distribute this material, unless such use and

distribution is made in accordance with applicable law and regulation. Additionally, financial intermediaries are

required to satisfy themselves that the information in this material is appropriate for any person to whom they

provide this material in view of that person’s circumstances and purpose. The Firm shall not be liable for, and

accepts no liability for, the use or misuse of this material by any such financial intermediary.

The whole or any part of this work may not be directly or indirectly reproduced, copied, modified, used to create

a derivative work, performed, displayed, published, posted, licensed, framed, distributed or transmitted or any

of its contents disclosed to third parties without MSIM’s express written consent. This work may not be linked to

unless such hyperlink is for personal and non-commercial use. All information contained herein is proprietary

and is protected under copyright and other applicable law.

Eaton Vance is part of Morgan Stanley Investment Management. Morgan Stanley Investment Management is

the asset management division of Morgan Stanley.

This material may be translated into other languages. Where such a translation is made this English version

remains definitive. If there are any discrepancies between the English version and any version of this material

in another language, the English version shall prevail.

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

15

DISTRIBUTION

This communication is only intended for and will only be distributed to persons resident in jurisdictions

where such distribution or availability would not be contrary to local laws or regulations.

MSIM, the asset management division of Morgan Stanley (NYSE: MS), and its affiliates have

arrangements in place to market each other’s products and services. Each MSIM affiliate is regulated

as appropriate in the jurisdiction it operates. MSIM’s affiliates are: Eaton Vance Management

(International) Limited, Eaton Vance Advisers International Ltd, Calvert Research and Management,

Eaton Vance Management, Parametric Portfolio Associates LLC, and Atlanta Capital Management LLC.

This material has been issued by any one or more of the following entities:

EMEA

This material is for Professional Clients/Accredited Investors only.

In the EU, MSIM and Eaton Vance materials are issued by MSIM Fund Management (Ireland) Limited (“FMIL”).

FMIL is regulated by the Central Bank of Ireland and is incorporated in Ireland as a private company limited by

shares with company registration number 616661 and has its registered address at 24-26 City Quay, Dublin 2,

DO2 NY19, Ireland.

Outside the EU, MSIM materials are issued by Morgan Stanley Investment Management Limited (MSIM Ltd) is

authorised and regulated by the Financial Conduct Authority. Registered in England. Registered No. 1981121.

Registered Office: 25 Cabot Square, Canary Wharf, London E14 4QA.

In Switzerland, MSIM materials are issued by Morgan Stanley & Co. International plc, London (Zurich Branch)

Authorised and regulated by the Eidgenössische Finanzmarktaufsicht ("FINMA"). Registered Office:

Beethovenstrasse 33, 8002 Zurich, Switzerland.

Outside the US and EU, Eaton Vance materials are issued by Eaton Vance Management (International) Limited

(“EVMI”) 125 Old Broad Street, London, EC2N 1AR, UK, which is authorised and regulated in the United

Kingdom by the Financial Conduct Authority.

Italy: MSIM FMIL (Milan Branch), (Sede Secondaria di Milano) Palazzo Serbelloni Corso Venezia, 16 20121

Milano, Italy. The Netherlands: MSIM FMIL (Amsterdam Branch), Rembrandt Tower, 11th Floor Amstelplein 1

1096HA, Netherlands. France: MSIM FMIL (Paris Branch), 61 rue de Monceau 75008 Paris, France. Spain:

MSIM FMIL (Madrid Branch), Calle Serrano 55, 28006, Madrid, Spain. Germany: MSIM FMIL Frankfurt Branch,

Große Gallusstraße 18, 60312 Frankfurt am Main, Germany (Gattung: Zweigniederlassung (FDI) gem. § 53b

KWG). Denmark: MSIM FMIL (Copenhagen Branch), Gorrissen Federspiel, Axel Towers, Axeltorv2, 1609

Copenhagen V, Denmark.

MIDDLE EAST

Dubai: MSIM Ltd (Representative Office, Unit Precinct 3-7th Floor-Unit 701 and 702, Level 7, Gate Precinct

Building 3, Dubai International Financial Centre, Dubai, 506501, United Arab Emirates. Telephone: +97 (0)14

709 7158).

This document is distributed in the Dubai International Financial Centre by Morgan Stanley Investment

Management Limited (Representative Office), an entity regulated by the Dubai Financial Services Authority

(“DFSA”). It is intended for use by professional clients and market counterparties only. This document is not

intended for distribution to retail clients, and retail clients should not act upon the information contained in this

document.

U.S.

NOT FDIC INSURED | OFFER NO BANK GUARANTEE | MAY LOSE VALUE | NOT INSURED BY ANY

FEDERAL GOVERNMENT AGENCY | NOT A DEPOSIT

ASIA PACIFIC

Hong Kong: This material is disseminated by Morgan Stanley Asia Limited for use in Hong Kong and shall

only be made available to “professional investors” as defined under the Securities and Futures Ordinance of

Hong Kong (Cap 571). The contents of this material have not been reviewed nor approved by any regulatory

© 2023 Morgan Stanley. All rights reserved.

6112950 Exp. 11/30/2024

16

authority including the Securities and Futures Commission in Hong Kong. Accordingly, save where an

exemption is available under the relevant law, this material shall not be issued, circulated, distributed, directed

at, or made available to, the public in Hong Kong. Singapore: This material is disseminated by Morgan

Stanley Investment Management Company and should not be considered to be the subject of an invitation for

subscription or purchase, whether directly or indirectly, to the public or any member of the public in Singapore

other than (i) to an institutional investor under section 304 of the Securities and Futures Act, Chapter 289 of

Singapore (“SFA”); (ii) to a “relevant person” (which includes an accredited investor) pursuant to section 305 of

the SFA, and such distribution is in accordance with the conditions specified in section 305 of the SFA; or (iii)

otherwise pursuant to, and in accordance with the conditions of, any other applicable provision of the SFA.

This publication has not been reviewed by the Monetary Authority of Singapore. Australia: This material is

provided by Morgan Stanley Investment Management (Australia) Pty Ltd ABN 22122040037, AFSL No.

314182 and its affiliates and does not constitute an offer of interests. Morgan Stanley Investment Management

(Australia) Pty Limited arranges for MSIM affiliates to provide financial services to Australian wholesale clients.

Interests will only be offered in circumstances under which no disclosure is required under the Corporations

Act 2001 (Cth) (the “Corporations Act”). Any offer of interests will not purport to be an offer of interests in

circumstances under which disclosure is required under the Corporations Act and will only be made to persons

who qualify as a “wholesale client” (as defined in the Corporations Act). This material will not be lodged with

the Australian Securities and Investments Commission.

Japan

This material may not be circulated or distributed, whether directly or indirectly, to persons in Japan other than

to (i) a professional investor as defined in Article 2 of the Financial Instruments and Exchange Act (“FIEA”) or

(ii) otherwise pursuant to, and in accordance with the conditions of, any other allocable provision of the FIEA.

This material is disseminated in Japan by Morgan Stanley Investment Management (Japan) Co., Ltd.,

Registered No. 410 (Director of Kanto Local Finance Bureau (Financial Instruments Firms)), Membership: the

Japan Securities Dealers Association, The Investment Trusts Association, Japan, the Japan Investment

Advisers Association and the Type II Financial Instruments Firms Association.