i

Trinity Health,

one of the largest faith-based health care organizations in the nation, reports

excess of revenue over expenses growth of 47.3 percent or $404.9 million to $1.3 billion for the

first nine months of fiscal year 2024; net margin of 6.6 percent

Summary Highlights for the First Nine Months of FY2024 (Nine Months Ended March 31, 2024)

Trinity Health reported significant improvements in operating performance, with operating income before other

items of $69.8 million (operating margin of 0.4 percent and cash flow margin of 5.3 percent) for the nine months

ended March 31, 2024, compared to operating losses before other items of $263.1 million (operating margin

of [1.6] percent and cash flow margin of 3.7 percent) for the nine months ended March 31, 2023. Improvements

were attained in payment rates, same facility patient care volume growth and as a result of several revenue

and cost management initiatives.

Trinity Health continues to take various actions to address current challenges facing the health care industry

in fiscal year 2024. The Corporation is focused on clinical optimization and access; continued focus on the

alignment of operating costs (both labor and non-labor) with revenue; labor stabilization through expansion of

its FirstChoice internal staffing agency, recruitment efforts and clinical prioritization; optimizing revenue

realization utilizing a multifaceted payer strategy to address a challenging payer environment and obtain fair

payment rate increases; and capital prioritization and reallocation of resources to focus on investments

supporting attainment of Mission-critical initiatives. To address labor shortages, the Corporation launched a

new innovative, virtual connected care delivery model using a 3-person team with on-site and virtual nursing

named “TogetherTeam Virtual Connected Care” that is being implemented system-wide and is already active

in 22 hospitals and 58 nursing units, with additional sites slated to go live in the fourth quarter of fiscal 2024.

From these actions, the Corporation is experiencing improvements in patient and employee safety, access to

care, employee retention and patient satisfaction that are helping to improve results of operations. On a same

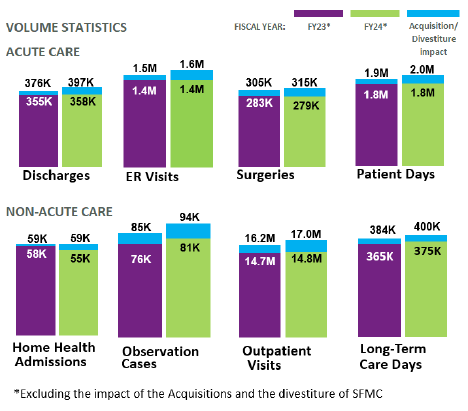

facility basis, volumes as measured by case mix adjusted equivalent discharges (“CMAEDs”) increased 0.5

percent during the nine months ended March 31, 2024 compared to the same period in the prior fiscal year.

The majority of the Corporation’s revenue is comprised of outpatient and other non-patient revenue. The

Corporation continues to diversify its business segments to gain better position for balanced performance when

individual segments are challenged.

Trinity Health reported growth in operating revenue of 11.4 percent or $1.8 billion to $17.8 billion in the first

nine months of fiscal year 2024 compared to the same period in the prior fiscal year. Revenue growth was

driven by the acquisitions of MercyOne in Iowa on September 1, 2022, North Ottawa Community Health System

(“Grand Haven”) in Michigan on October 1, 2022, and Genesis Health System in Iowa and Illinois on March 1,

2023, (collectively the “Acquisitions”) which contributed $1.0 billion of the increase. This increase was partially

offset by the divestiture of St. Francis Medical Center (“SFMC”) on December 22, 2022, that reduced operating

revenue by $59.3 million compared to the prior year. Excluding the Acquisitions and divestiture of SFMC,

operating revenue increased $863.8 million or 5.8 percent over the prior fiscal year. Net patient service revenue

grew $1.6 billion, or 11.7 percent, or $748.7 million and 5.8 percent excluding the Acquisitions. Same facility

net patient service revenue was positively impacted by improvements in payment rates (inclusive of $146.2

million in new Medicaid provider funding in Iowa and Medicaid rate changes in Michigan, and a $102.8 million

340B remedy lump sum settlement received from CMS under the November 8, 2023 Final Rule), same facility

patient volumes and to a lesser extent case mix.

ii

Other revenue increased $108.1 million, or 8.7 percent, compared to the prior fiscal year on a same facility

basis, primarily driven by $86.9 million of pharmacy revenue, and to a lesser extent gainshare revenue, and

equity in earnings of unconsolidated affiliates. In addition, premium and capitation revenue increased $10.0

million, primarily within the Corporation’s health plans and PACE programs.

Operating expenses increased $1.5 billion to $17.7 billion, or 9.1 percent, for the nine months ended March

31, 2024 compared to the prior fiscal year, with the Acquisitions accounting for $902.9 million of the overall

increase. Excluding the impact of the Acquisitions and divestiture of SFMC, operating expenses for the nine

months ended March 31, 2024, increased $653.0 million, or 4.3 percent. Total operating costs per case (as

measured by CMAEDs) increased 2.7 percent compared to the prior year as the Corporation continues to

tightly manage operating costs amid inflation. On a same facility basis, salaries and wages rose $380.1 million,

or 5.6 percent, inclusive of a 3.7 percent increase in salary rates and a 1.9 percent increase in FTEs, as the

Corporation continues to implement initiatives to address industry wide staffing shortages and wage inflation.

Same facility fiscal year 2024 salary rate increases include a $65 million one-time compensation award

program. Same facility employee benefit costs increased $100.2 million or 8 percent, including a $64.7 million

or 16.9 percent increase in employee health plan costs. Supply costs increased $141.4 million, or 5.3 percent,

on a same facility basis compared to the prior fiscal year, primarily due to increased pharmacy volume.

Although overall supply costs increased, same facility supplies as a percent of net patient service revenue,

excluding the 340B remedy settlement and accrual of the aforementioned Medicaid provider tax changes,

decreased 0.7 percent from prior year. Same facility increases were also reported in interest expense and

other expenses, which includes $55.1M of increased provider tax expense related to the aforementioned

Medicaid provider tax changes.

The Corporation continues to use strong cost controls over contract labor and other operational spending.

Labor stabilization is occurring with investments in its FirstChoice internal staffing agency and TogetherTeam

Virtual Connected Care model. On a same facility basis, contract labor costs decreased $71.3 million, or 25

percent compared to the prior fiscal year. Further expense reductions were seen in purchased services and

medical claims, depreciation and amortization and occupancy.

For the first nine months of fiscal year 2023, other items consisted of $53.9 million in dividend income received

from a cost method investment and an $8.0 million gain for the final settlement from the fiscal year 2022 sale

of Gateway Health Plan, L.P., and Subsidiaries, offset by $82.3 million of restructuring costs related to the

divestiture of SFMC.

The Corporation reported non-operating income of $1.2 billion for the nine months ended March 31, 2024 and

2023. Non-operating income was driven by investment earnings of $853.0 million or 9.1 percent in the first nine

months of fiscal year 2024, compared to earnings of $457.3 million or 5.4 percent during the previous fiscal

year, an increase of $395.7 million. Investment results also drove the $137.7 million improvement in equity in

earnings of unconsolidated affiliates. This was partially offset by a reduction in inherent contributions of $487.7

million primarily related to the fiscal year 2023 acquisitions of Genesis Health System and Grand Haven.

Excess of revenue over expenses for the nine months ended March 31, 2024 was $1.3 billion, net margin of

6.6 percent, compared to excess of revenue over expenses of $856.3 million, net margin of 5.1 percent, for the

nine months ended March 31, 2023.

The Corporation’s balance sheet remains strong after prompt responses to negative impacts from Change

Healthcare’s cyberattack that occurred in February 2024. While the attack did not directly impact the

Corporation’s systems, the event disrupted the billing and collection of patient accounts receivable that grew

$896.8 million as of March 31, 2024 compared to June 30, 2023, or a 19-day use of cash. Responses included

iii

a $600 million draw on liquidity facilities and receipt of Medicare cash advances, amongst others. As of March

31, 2024, days cash of 173 days declined 4 days since June 30, 2023.

Highlights as of and for the nine months ended March 31, 2024, include:

• Total assets of $34.7 billion and net assets of $19.7 billion,

• Operating revenue growth of 11.4 percent to $17.8 billion compared to the same period in the prior

fiscal year, including the impact of the Acquisitions and net of the SFMC divestiture,

• Operating cash flow before other items of $944.8 million, or 5.3 percent operating cash flow margin;

compared to operating cash flow before other items of $596.1 million or 3.7 percent operating cash

flow margin for the nine months ended March 31, 2023,

• Operating income before other items of $69.8 million, or 0.4 percent operating margin; compared to

operating loss before other items of $263.1 million or (1.6) percent operating margin for the nine

months ended March 31, 2023,

• Excess of revenue over expenses of $1.3 billion, net margin of 6.6 percent, compared to excess of

revenue over expenses of $856.3 million, net margin of 5.1 percent for the nine months ended March

31, 2023,

• Unrestricted cash and investments of $10.7 billion; days cash on hand of 173 days compared to 178

days for the year ended June 30, 2023 including the line of credit draws and Medicare cash

advances; excluding these items, days cash on hand is 161 days, or a reduction of 17 days from

June 30, 2023,

• Historical debt service coverage ratio of 3.10x compared to 1.1x required.

TRINITY HEALTH

UNAUDITED QUARTERLY REPORT

As of March 31, 2024, and June 30, 2023, and

For the nine months ended March 31, 2024 and 2023

TRINITY HEALTH

TABLE OF CONTENTS

Page

UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS AS OF

MARCH 31, 2024 AND JUNE 30, 2023 AND FOR THE

NINE MONTHS ENDED MARCH 31, 2024 AND 2023:

Consolidated Balance Sheets (unaudited) 3-4

Consolidated Statements of Operations and Changes in Net Assets (unaudited) 5-6

Summarized Consolidated Statements of Cash Flows (unaudited) 7

Notes to Consolidated Financial Statements (unaudited) 8-26

MANAGEMENT’S DISCUSSION AND ANALYSIS (unaudited) 27-33

LIQUIDITY REPORT (unaudited) 34

FINANCIAL RATIOS AND STATISTICS (unaudited) 35

- 3 -

TRINITY HEALTH

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(In thousands)

March 31, June 30,

ASSETS 2024 2023

CURRENT ASSETS:

Cash and cash equivalents

924,060$

576,308$

Investments

5,184,250

5,266,635

Security lending collateral

358,247

349,985

Assets limited or restricted as to use - current portion

454,787

430,985

Patient accounts receivable

3,372,384

2,475,557

Estimated receivables from third-party payers

544,852

298,946

Other receivables

430,667

422,689

Inventories 399,135

409,193

Prepaid expenses and other current assets

236,140

225,464

Total current assets

11,904,522

10,455,762

ASSETS LIMITED OR RESTRICTED AS TO USE - noncurrent portion:

Self-insurance, benefit plans, and other

1,189,764

1,052,049

By Board

4,390,982

4,160,166

By donors

645,399

598,003

Total assets limited or restricted as to use - noncurrent portion 6,226,145

5,810,218

PROPERTY AND EQUIPMENT - Net

8,832,768

8,846,497

OPERATING LEASE RIGHT-OF-USE ASSETS 574,980

598,938

INVESTMENTS IN UNCONSOLIDATED AFFILIATES 5,600,268

5,165,540

GOODWILL 942,198

848,078

PREPAID PENSION AND RETIREE HEALTH ASSETS 245,772

232,725

OTHER ASSETS

340,075

322,449

TOTAL ASSETS

34,666,728$ 32,280,207$

The accompanying notes are an integral part of the consolidated financial statements.

(Continued)

As of

- 4 -

TRINITY HEALTH

CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(In thous ands)

March 31, June 30,

LIABILITIES AND NET ASSETS

2024 2023

CURRENT LIABILITIES:

Commercial paper 99,388$ 99,538$

Short-term borrowings 599,415 616,335

Current portion of long-term debt 464,073 245,326

Current portion of operating lease liabilities 142,033 150,878

Medicare cash advances 161,366 -

Accounts payable and accrued expenses 1,848,751 1,551,303

Salaries, wages and related liabilities 1,059,726 1,065,904

Payable under security lending agreements 358,247 349,985

Estimated payables to third-party payers 238,224 286,409

Current portion of self-insurance reserves 302,399 303,658

Total current lia bilities 5,273,622 4,669,336

LONG-TERM DEBT - Net of current portion 7,013,801 6,757,159

LONG-TERM PORTION OF OPERATING LEASE LIABILITIES 515,289 535,888

SELF-INSURANCE RESERVES - Net of current portion 1,219,393 1,151,235

ACCRUED PENSION AND RETIREE HEALTH COSTS 73,470 88,859

OTHER LONG-TERM LIABILITIES 830,245 751,728

Total liabilities 14,925,820 13,954,205

NET ASSETS:

Net assets without donor restrictions 18,491,503 17,176,548

Noncontrolling ownership interest in subsidiaries 539,372 493,440

Total net assets without donor restrictions 19,030,875 17,669,988

Net assets with donor restrictions 710,033 656,014

Total net assets 19,740,908 18,326,002

TOTAL LIABILITIES AND NET ASSETS 34,666,728$ 32,280,207$

The accompanying notes are an integral part of the consolidated financial statements. (Concluded)

As of

- 5 -

TRINITY HEALTH

CONSOLIDATED STATEMENTS OF OPERATIONS AND

CHANGES IN NET ASSETS (UNAUDITED)

NINE MONTHS ENDED MARCH 31, 2024 AND 2023

(In thousands)

2024 2023

OPERATING REVENUE:

Net patient service revenue 15,319,533$ 13,710,230$

Premium and capitation revenue 833,872 832,590

Net assets released from restrictions 22,672 23,315

Other revenue 1,583,483 1,380,539

Total operating revenue 17,759,560 15,946,674

EXPENSES:

Salaries and wages 7,920,260 6,929,400

Employee benefits 1,508,370 1,288,751

Contract labor 278,823 683,743

Total labor expenses 9,707,453 8,901,894

Supplies 3,224,805 2,900,025

Purchased services and medical claims 2,250,545 2,148,270

Depreciation and amortization 668,917 666,497

Occupancy 670,019 635,884

Interest 206,051 192,760

Other 961,928 764,459

Total expenses 17,689,718 16,209,789

OPERATING INCOME (LOSS) BEFORE OTHER ITEMS 69,842 (263,115)

Restructuring costs

- (82,259)

Dividend received from cost method investee

- 53,864

Gain on sale of Gateway Health Plan L.P.

- 8,000

OPERATING INCOME (LOSS)

69,842 (283,510)

NONOPERATING ITEMS:

Investment earnings 853,017 457,334

Equity in earnings of unconsolidated affiliates 433,100 295,360

Change in market value and cash payments of interest rate swaps 9,604 18,157

Other net periodic retirement cost (36,477) (56,655)

Inherent contributions - 484,579

Other, including income taxes (16,366) (2,756)

Total nonoperating items 1,242,878 1,196,019

EXCESS OF REVENUE OVER EXPENSES 1,312,720 912,509

EXCESS OF REVENUE OVER EXPENSES ATTRIBUTABLE

TO NONCONTROLLING INTEREST

(51,481) (56,171)

EXCESS OF REVENUE OVER EXPENSES,

NET OF NONCONTROLLING INTEREST 1,261,239$ 856,338$

The accompanying notes are an integral part of the consolidated financial statements.

(Continued)

- 6 -

CHANGES IN NET ASSETS (UNAUDITED)

NINE MONTHS ENDED MARCH 31, 2024 AND 2023

(In thousands)

2024 2023

NET ASSETS WITHOUT DONOR RESTRICTIONS:

Net assets without donor restrictions attributable to Trinity Health:

Excess of revenue over expenses 1,261,239$ 856,338$

Net assets released from restrictions for capital acquisitions 15,522 13,844

Net change in retirement plan related items - consolidated organizations 50,720 66,223

Net change in retirement plan related items - unconsolidated organizations - 13,567

Purchase of noncontrolling interest in subsidiary (18,448) -

Other 5,923 11,592

Increase in net assets without donor restrictions attributable

to Trinity Health 1,314,956 961,564

Net assets without donor restrictions attributable to noncontrolling interest:

Excess of revenue over expenses attributable to noncontrolling interest 51,481 56,171

Noncontrolling interests attributed to acquisitions 60,658 -

Dividends, distributions and other (66,208) (47,211)

Increase in net assets without donor restrictions

attributable to noncontrolling interest 45,931 8,960

NET ASSETS WITH DONOR RESTRICTIONS:

Contributions:

Program and time restrictions 56,437 40,522

Endowment funds 1,851 1,024

Net investment gains:

Program and time restrictions 22,983 12,162

Endowment funds 10,881 1,386

Net assets released from restrictions (38,194) (37,159)

Acquisitions - 69,732

Other 61 255

Increase in net assets with donor restrictions 54,019 87,922

INCREASE IN NET ASSETS 1,414,906 1,058,446

NET ASSETS - BEGINNING OF YEAR 18,326,002 16,897,308

NET ASSETS - END OF PERIOD 19,740,908$ 17,955,754$

The accompanying notes are an integral part of the consolidated financial statements. (Concluded)

- 7 -

TRINITY HEALTH

SUMMARIZED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

NINE MONTHS ENDED MARCH 31, 2024 AND 2023

(In thousands)

2024 2023

OPERATING ACTIVITIES:

Increase in net assets 1,414,906$

1,058,446$

Adjustments to reconcile change in net assets to net cash provided by

(used in) operating activities:

Depreciation and amortization 668,917 666,497

Amortization of right-of-use asset 98,047 106,933

Change in net unrealized and realized gains and losses on investments

(816,577) (

386,054)

Change in market values of interest rate swaps (10,190) (24,743)

Undistributed equity in earnings of unconsolidated affiliates (430,014) (284,217)

Inherent contributions related to acquisitions - (484,413)

Loss on transfer of St. Francis Medical Center - 22,842

Gain on sale of Gateway Health Plan L.P. - (8,000)

Dividend received from cost method investee - (53,864)

Loss on purchase of noncontrolling interest in subsidiary 18,448 -

Increase in noncontrolling interest related to acquisitions (60,658) -

Deferred retirement items (7,007) (27,367)

Restricted contributions acquired - (69,732)

Dividends paid attributed to non-controlling interest 50,850 47,161

Other adjustments (30,854) (40,756)

Changes in:

Patient accounts receivable (903,699) (207,502)

Estimated receivables from third-party payers (245,906) 15,415

Prepaid pension and retiree health costs (13,047) (8,702)

Other assets 6,322 (97,766)

Medicare cash advances 161,366 (409,533)

Accounts payable and accrued expenses 311,333 (214,249)

Estimated payables to third-party payers (45,385) (64,122)

Self-insurance reserves and other liabilities (31,733) (129,049)

Accrued pension and retiree health costs (8,383) (9,701)

Total adjustments (1,288,170) (1,660,922)

Net cash provided by (used in) operating activities 126,736 (602,476)

INVESTING ACTIVITIES:

Net sales of investments

594,654 1,836,667

Purchases of property and equipment

(692,736) (642,151)

Change in investments in unconsolidated affiliates

(3,650) (29,488)

Cash proceeds from sale of Gateway Health Plan L.P.

- 8,000

Dividend received from cost method investee - 53,864

Cash used for disposal of St. Francis Medical Center - (14,500)

Net cash used for acquisitions

(57,503) (530,598)

Change in other investing activities

1,867 (4,151)

Net cash (used in) provided by investing activities

(157,368) 677,643

FINANCING ACTIVITIES:

Proceeds from issuance of debt 49,448

366,620

Repayments of debt

(186,559) (169,761)

Net change in commercial paper

(150) (26)

Draws on lines of credit

600,000 -

Dividends paid

(50,850) (47,161)

Proceeds from restricted contributions and restricted investment income

11,343 6,192

Increase in financing costs and other

(979) (2,328)

Net cash provided by financing activities

422,253 153,536

NET INCREASE IN CASH, CASH EQUIVALENTS, AND

RESTRICTED CASH

391,621 228,703

CASH, CASH EQUIVALENTS, AND RESTRICTED CASH -

BEGINNING OF YEAR

736,085 801,155

CASH, CASH EQUIVALENTS, AND RESTRICTED CASH -

END OF PERIOD

1,

127,706$ 1,029,858$

The accompanying notes are an integral part of the consolidated financial statements.

- 8 -

TRINITY HEALTH

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

NINE MONTHS ENDED MARCH 31, 2024 AND 2023

1. ORGANIZATION AND MISSION

Trinity Health Corporation, an Indiana nonprofit corporation headquartered in Livonia, Michigan, and its

subsidiaries (“Trinity Health” or the “Corporation”), controls one of the largest health care systems in the

United States. The Corporation is sponsored by Catholic Health Ministries, a Public Juridic Person of the

Holy Roman Catholic Church. The Corporation operates a comprehensive integrated network of health

services, including inpatient and outpatient services, physician services, managed care coverage, home

health care, long-term care, assisted living care and rehabilitation services located in 27 states. The

operations are organized into Regional Health Ministries, National Health Ministries and Mission Health

Ministries (“Health Ministries”). The Mission statement for the Corporation is as follows:

We, Trinity Health, serve together in the spirit of the Gospel as a compassionate and

transforming healing presence within our communities.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying unaudited consolidated financial statements have been prepared in accordance with

accounting principles generally accepted in the United States of America (“GAAP”) for interim financial

reporting information. Accordingly, they do not include all of the information and footnotes required by

GAAP for complete financial statements. In the opinion of management, all adjustments considered

necessary for a fair presentation have been included and are of a normal and recurring nature. Operating

results for the nine months ended March 31, 2024 are not necessarily indicative of the results to be expected

for the year ending June 30, 2024.

Principles of Consolidation – The consolidated financial statements include the accounts of the

Corporation, and all wholly-owned, majority-owned, and controlled organizations. Investments where the

Corporation holds less than 20% of the ownership interest are accounted for using the cost method. All

other investments that are not controlled by the Corporation are accounted for using the equity method of

accounting. The equity share of income or losses from investments in unconsolidated affiliates is recorded

in other revenue if the unconsolidated affiliate is operational and projected to make routine and regular cash

distributions; otherwise, the equity share of income or losses from investments in unconsolidated affiliates

is recorded in nonoperating items in the consolidated statements of operations and changes in net assets.

All material intercompany transactions and account balances have been eliminated in consolidation.

Use of Estimates – The preparation of consolidated financial statements in conformity with GAAP requires

management of the Corporation to make assumptions, estimates and judgments that affect the amounts

reported in the consolidated financial statements, including the notes thereto, and related disclosures of

commitments and contingencies, if any.

The Corporation considers critical accounting policies to be those that require more significant judgments

and estimates in the preparation of its consolidated financial statements, including the following:

recognition of net patient service revenue, which includes explicit and implicit price concessions; financial

assistance; premium revenue; recorded values of investments and derivatives; goodwill; evaluation of long-

lived assets for impairment; reserves for losses and expenses related to health care professional and general

liabilities; and risks and assumptions for measurement of pension and retiree health liabilities. Management

relies on historical experience and other assumptions believed to be reasonable in making its judgments and

estimates. Actual results could differ materially from those estimates.

- 9 -

Cash, Cash Equivalents and Restricted Cash – For purposes of the consolidated statements of cash flows,

cash, cash equivalents and restricted cash include certain investments in highly liquid debt instruments with

original maturities of three months or less.

The following table reconciles cash, cash equivalents and restricted cash shown in the statements of cash

flows to amounts presented within the consolidated balance sheets as of March 31 (in thousands):

2024 2023

Cash and cash equivalents $ 924,060 $ 875,451

Restricted cash included in assets limited or restricted as to

use - current portion

Held by trust under bond indenture 222 224

Self insured benefit plans & other 115,890 83,297

By donors 1,681 4,151

Total restricted cash included in assets limited or restricted

as to use - current portion

117,793 87,672

Restricted cash included in assets limited as to use -

noncurrent portion

Self insured benefit plans & other 48,626 27,318

By donors 37,227 39,417

Total restricted cash included in assets limited or restricted

as to use - noncurrent portion

85,853 66,735

Total cash, cash equivalents, and restricted cash shown in

the statements of cash flows

$ 1,127,706 $ 1,029,858

Investments – Investments, inclusive of assets limited or restricted as to use, include marketable debt and

equity securities. Investments in equity securities with readily determinable fair values and all investments

in debt securities are measured at fair value and are classified as trading securities. Investments also include

investments in commingled funds, hedge funds and other investments structured as limited liability

corporations or partnerships. Commingled funds and hedge funds that hold securities directly are stated at

the fair value of the underlying securities, as determined by the administrator, based on readily determinable

market values, or based on net asset value, which is calculated using the most recent fund financial

statements. Limited liability corporations and partnerships are accounted for under the equity method.

Investment Earnings – Investment earnings include interest, dividends, realized gains and losses and

unrealized gains and losses. Also included are equity earnings from investment funds accounted for using

the equity method. Investment earnings on assets held by trustees under bond indenture agreements, assets

designated by the Corporation’s board of directors (“Board”) for debt redemption, assets held for

borrowings under the intercompany loan program, assets held by grant-making foundations, assets

deposited in trust funds by a captive insurance company for self-insurance purposes, and interest and

dividends earned on life plan communities advance entrance fees, in accordance with industry practices,

are included in other revenue in the consolidated statements of operations and changes in net assets.

Investment earnings, net of direct investment expenses, from all other investments and Board-designated

funds are included in nonoperating investment income unless the income or loss is restricted by donor or

law.

Derivative Financial Instruments – The Corporation periodically utilizes various financial instruments

(e.g., options and swaps) to hedge interest rates, equity downside risk and other exposures. The

Corporation’s policies prohibit trading in derivative financial instruments on a speculative basis. The

Corporation recognizes all derivative instruments in the consolidated balance sheets at fair value.

- 10 -

Securities Lending – The Corporation participates in securities lending transactions whereby a portion of

its investments are loaned, through its agent, to various parties in return for cash and securities from the

parties as collateral for the securities loaned. Each business day, the Corporation, through its agent, and the

borrower determine the market value of the collateral and the borrowed securities. If on any business day

the market value of the collateral is less than the required value, additional collateral is obtained as

appropriate. The amount of cash collateral received under securities lending is reported as an asset and a

corresponding payable in the consolidated balance sheets and is up to 105% of the market value of securities

loaned. As of March 31, 2024, and June 30, 2023, the Corporation had securities loaned of $678.5 million

and $698.7 million, respectively, and received collateral (cash and noncash) totaling $695.8 million and

$716.6 million, respectively, relating to the securities loaned. The fees received for these transactions are

recorded in nonoperating investment income in the consolidated statements of operations and changes in

net assets. In addition, certain pension plans participate in securities lending programs with the Northern

Trust Company, the plans’ agent.

The Corporation evaluates the financial condition of its securities lending plan managers and borrowing

institutions to minimize exposure to credit risk. Credit risk is regularly monitored and minimized by Trinity

Health’s managers of the program by selecting borrowers with stringent financial viability standards,

underwriting and approval procedures as set forth by the institution. An established framework is also used

to size borrower credit limits to reduce concentration risk. In addition, the vast majority of parent borrowers

have long-term credit ratings of A or better and short-term ratings of A-1 or better from at least one

nationally recognized statistical rating organization. The Corporation does not expect any credit losses

related to the securities lending arrangement.

Patient Accounts Receivable, Estimated Receivables from and Payables to Third-Party Payers – An

unconditional right to payment, subject only to the passage of time is treated as a receivable. Patient

accounts receivable, including billed accounts and unbilled accounts for which there is an unconditional

right to payment, and estimated amounts due from third-party payers for retroactive adjustments, are

receivables if the right to consideration is unconditional and only the passage of time is required before

payment of that consideration is due. For patient accounts receivable, the estimated uncollectable amounts

are generally considered implicit price concessions that are a direct reduction to patient service revenue and

accounts receivable.

The Corporation has agreements with third-party payers that provide for payments to the Corporation’s

Health Ministries at amounts different from established rates. Estimated retroactive adjustments under

reimbursement agreements with third-party payers and other changes in estimates are included in net patient

service revenue and estimated receivables from and payables to third-party payers. Retroactive adjustments

are accrued on an estimated basis in the period the related services are rendered and adjusted in future

periods, as final settlements are determined.

Assets Limited as to Use – Assets set aside by the Board for quasi-endowments, future capital

improvements, future funding of retirement programs and insurance claims, retirement of debt, held for

borrowings under the intercompany loan program, and other purposes over which the Board retains control

and may at its discretion subsequently use for other purposes, assets held by trustees under bond indenture

and certain other agreements, and self-insurance trust and benefit plan arrangements are included in assets

limited as to use.

Donor-Restricted Gifts – Unconditional promises to give cash and other assets to the Corporation are

reported at fair value at the date the promise is received. Conditional promises to give and indications of

intentions to give are reported at fair value at the date the gift is received. The gifts are reported as support

with donor restrictions if they are received with donor stipulations that limit the use of the donated assets.

When a donor restriction expires, that is, when a stipulated time restriction ends or program restriction is

accomplished, net assets with donor restrictions are reclassified to net assets without donor restrictions and

reported in the consolidated statements of operations and changes in net assets as net assets released from

restrictions. Donor-restricted contributions whose restrictions are met within the same year as received are

reported as contributions without donor restrictions included in other revenue in the consolidated statements

of operations and changes in net assets.

- 11 -

Inventories – Inventories are stated at the lower of cost or market. The cost of inventories is determined

principally by the weighted-average cost method.

Property and Equipment – Property and equipment, including internal-use software, are recorded at cost,

if purchased, or at fair value at the date of donation, if donated. Finance lease right-of-use assets included

in property and equipment represent the right to use the underlying assets for the lease term and are

recognized at the lease commencement date based on the present value of lease payments over the term of

the lease.

Depreciation is provided over the estimated useful life of each class of depreciable asset and is computed

using either the straight-line or an accelerated method and includes finance lease right-of-use asset

amortization and internal-use software amortization. The useful lives of property and equipment range from

2 to 75 years, and finance lease agreements have initial terms typically ranging from 3 to 30 years. Interest

costs incurred during the period of construction of capital assets are capitalized as a component of the cost

of acquiring those assets.

Gifts of long-lived assets such as land, buildings, or equipment are reported as support without donor

restrictions and are excluded from the excess of revenue over expenses, unless explicit donor stipulations

specify how the donated assets must be used. Gifts of long-lived assets with explicit restrictions that specify

how the assets are to be used and gifts of cash or other assets that must be used to acquire long-lived assets

are reported as support with donor restrictions.

Right-of-Use Lease Assets and Lease Liabilities – The Corporation determines if an arrangement is a lease

at inception of the contract. Right-of-use assets represent the right to use the underlying assets for the lease

term and lease liabilities represent the obligation to make lease payments arising from the leases. Right-of-

use assets and lease liabilities are recognized at the lease commencement date based on the present value

of lease payments over the lease term. The Corporation uses the implicit rate noted within the contract,

when available. Otherwise, the Corporation uses its incremental borrowing rate estimated using recent

secured debt issuances that correspond to various lease terms, information obtained from banking advisors,

and the Corporation’s secured debt fair value. The Corporation does not recognize leases, for operating or

finance type, with an initial term of 12 months or less (“short-term leases”) on the consolidated balance

sheet, and the lease expense for these short-term leases is recognized on a straight-line basis over the lease

term within occupancy expense in the consolidated statements of operations and changes in net assets. The

Corporation’s finance leases are primarily for real estate. Finance lease right-of-use assets are included in

property and equipment, with the related liabilities included in current and long-term debt on the

consolidated balance sheet.

Operating lease right-of-use assets and liabilities are recorded for leases that are not considered finance

leases. The Corporation’s operating leases are primarily for real estate, vehicles, and medical and office

equipment. Real estate leases include outpatient, medical office, ground, and corporate administrative office

space. The Corporation’s real estate lease agreements typically have an initial term of 2 to 10 years. The

Corporation’s equipment lease agreements typically have an initial term of 2 to 6 years. The real estate

leases may include one or more options to renew, with renewals that can extend the lease term from 5 to 10

years. The exercise of lease renewal options is at the Corporation’s sole discretion. For accounting purposes,

options to extend or terminate the lease are included in the lease term when it is reasonably certain that the

option will be exercised. Operating lease liabilities represent the obligation to make lease payments arising

from the leases and are recognized at the lease commencement date based on the present value of lease

payments over the lease term.

Certain of the Corporation’s lease agreements for real estate include payments based on common area

maintenance expenses and others include rental payments adjusted periodically for inflation. These variable

lease payments are recognized in occupancy expense, net, but are not included in the right-of-use asset or

liability balances when they can be separately identified in the contract. The Corporation’s lease agreements

do not contain any material residual value guarantees, restrictions, or covenants.

- 12 -

Goodwill – Goodwill represents the future economic benefits arising from assets acquired in a business

combination that are not individually identified and separately recognized

.

Asset Impairments –

Property, Equipment and Right-of-Use Lease Assets – The Corporation evaluates long-lived assets

for possible impairment whenever events or changes in circumstances indicate that the carrying amount

of the asset, or related group of assets, may not be recoverable from estimated future undiscounted cash

flows. If the estimated future undiscounted cash flows are less than the carrying value of the assets, the

impairment recognized is calculated as the carrying value of the long-lived assets in excess of the fair

value of the assets. The fair value of the assets is estimated based on appraisals, established market

values of comparable assets or internal estimates of future net cash flows expected to result from the

use and ultimate disposition of the assets.

Goodwill – Goodwill is tested for impairment on an annual basis or when an event or change in

circumstance indicates the value of a reporting unit may have changed. Testing is conducted at the

reporting unit level. If the carrying amount of the reporting unit goodwill exceeds the implied fair value

of that goodwill, an impairment loss is recognized in an amount equal to that excess. Estimates of fair

value are based on appraisals, established market prices for comparable assets or internal estimates of

future net cash flows.

Other Assets – Other assets include long-term notes receivable, reinsurance recovery receivables, definite-

and indefinite-lived intangible assets other than goodwill and prepaid retiree health costs. The net balances

of definite-lived intangible assets include noncompete agreements, physician guarantees and other definite-

lived intangible assets with finite lives amortized using the straight-line method over their estimated useful

lives, which generally range from 2 to 20 years. Indefinite-lived intangible assets primarily include trade

names, which are tested annually for impairment.

Short-Term Borrowings – Short-term borrowings include puttable variable-rate demand bonds supported

by self-liquidity or liquidity facilities considered short-term in nature.

Medicare Cash Advances – In April 2020, the Corporation requested and received accelerated Medicare

payments of $1.6 billion for its acute care hospitals, which was provided through the Coronavirus Aid,

Relief and Economic Security Act (the “CARES Act”). Claims for services provided to Medicare

beneficiaries began being applied against the Corporation’s cash advances in April 2021.

During the nine

months ended March 31, 2023, the Center for Medicare and Medicaid Services (“CMS”) recouped $409.5

million of the advances. The remaining balance was fully repaid as of June 30, 2023.

Change Healthcare, a subsidiary of UnitedHealth Group and a major clearinghouse for medical claims,

experienced a cyberattack in February 2024. Although the Corporation’s systems were not directly

impacted by this cyberattack, the event disrupted the billing and collection of patients accounts receivable.

As a result, on March 9, 2024, CMS made available accelerated payments to providers and suppliers

experiencing disruptions due to the incident. These advances have been granted in amounts of up to 30 days

of claims payments and will be repaid through automatic recoupment from Medicare for a period of 90

days. The Corporation received $201.0 million of these cash advances of which $39.6 million has been

recouped, with $161.4 million remaining as of March 31, 2024.

Other Long-Term Liabilities – Other long-term liabilities include deferred compensation, asset retirement

obligations, interest rate swaps and deferred revenue from entrance fees. Deferred revenue from entrance

fees are fees paid by residents of facilities for the elderly upon entering into continuing care contracts,

which are amortized to income using the straight-line method over the estimated remaining life expectancy

of the resident, net of the portion that is refundable to the resident.

- 13 -

Net Assets with Donor Restrictions – Net assets with donor restrictions are those whose use by the

Corporation has been limited by donors to a specific time period or program. In addition, certain net assets

have been restricted by donors to be maintained by the Corporation in perpetuity.

Net Patient Service Revenue – The Corporation reports patient service revenue at the amount that reflects

the consideration it is expected to be entitled to in exchange for providing patient care. These amounts are

due from patients, third-party payers (including commercial payers and government programs) and others

and include variable consideration for retroactive revenue adjustments due to settlement of audits,

reviews, and investigations. Generally, the Corporation bills patients and third-party payers several days

after the services are performed or the patient is discharged from a facility.

The Corporation determines performance obligations based on the nature of the services provided. Revenue

for performance obligations satisfied over time is recognized based on actual charges incurred in relation

to total expected charges. The Corporation believes that this method provides a faithful depiction of the

transfer of services over the term of the performance obligation based on the inputs needed to satisfy the

obligation. Generally, performance obligations satisfied over time relate to patients in hospitals receiving

inpatient acute care services, or receiving services in outpatient centers, or in their homes (home care). The

Corporation measures performance obligations from admission to the hospital, or the commencement of an

outpatient service, to the point when it is no longer required to provide services to the patient, which is

generally at the time of discharge or the completion of the outpatient services. Revenue for performance

obligations satisfied at a point in time is generally recognized when goods are provided to our patients and

customers in a retail setting (for example, pharmaceuticals and medical equipment) and the Corporation

does not believe that it is required to provide additional goods and services related to that sale.

Because patient service performance obligations relate to contracts with a duration of less than one year,

the Corporation has elected to apply the optional exemption provided in Financial Accounting Standards

Board (“FASB”) Accounting Standards Codification (“ASC”) 606-10-50-14(a) and, therefore, the

Corporation is not required to disclose the aggregate amount of the transaction price allocated to

performance obligations that are unsatisfied or partially unsatisfied at the end of the reporting period. The

unsatisfied or partially unsatisfied performance obligations are primarily related to inpatient acute care

services at the end of the reporting period. The performance obligations for these contracts are generally

completed when the patients are discharged, which generally occurs within days or weeks from the end of

the reporting period.

The Corporation has elected the practical expedient allowed under FASB ASC 606-10-32-18 and does not

adjust the promised amount of consideration from patients and third-party payers for the effects of a

significant financing component due to the Corporation’s expectation that the period between the time the

service is provided to a patient and the time that the patient or a third-party payer pays for that service will

be one year or less. However, the Corporation does, in certain instances, enter into payment agreements

with patients that allow payments in excess of one year. For those cases, the financing component is not

deemed to be significant to the contract.

The Corporation determines the transaction price based on standard charges for services provided, reduced

by contractual adjustments provided to third-party payers, discounts provided to uninsured and

underinsured patients in accordance with the Corporation’s policy, and implicit price concessions provided

to uninsured and underinsured patients. The Corporation determines its estimates of contractual adjustments

and discounts based on contractual agreements, discount policies and historical experience. The estimate

of implicit price concessions is based on historical collection experience with the various classes of patients

using a portfolio approach as a practical expedient to account for patient contracts with similar

characteristics, as collective groups rather than individually. The financial statement effect of using this

practical expedient is not materially different from an individual contract approach.

- 14 -

Generally, patients who are covered by third-party payers are responsible for related deductibles and

coinsurance, which vary in amount. The Corporation also provides services to uninsured and underinsured

patients, and offers those uninsured and underinsured patients a discount, either by policy or law, from

standard charges. The Corporation estimates the transaction price for patients with deductibles and

coinsurance and for those who are uninsured and underinsured based on historical experience and current

market conditions, using the portfolio approach.

The initial estimate of the transaction price is determined by reducing the standard charge by any contractual

adjustments, discounts, and implicit price concessions. Subsequent changes to the estimate of the

transaction price are generally recorded as adjustments to patient service revenue in the period of the

change. Subsequent changes that are determined to be the result of an adverse change in the payer’s or

patient’s ability to pay are recorded as bad debt expense in other expenses in the statement of operations

and changes in net assets. Agreements with third-party payers typically provide for payments at amounts

less than established charges. A summary of the payment arrangements with major third-party payers is as

follows:

Medicare (Parts A and B) – Acute inpatient and outpatient services rendered to Medicare program

beneficiaries are paid primarily at prospectively determined rates. These rates vary according to a

patient classification system that is based on clinical, diagnostic, and other factors. Certain items are

reimbursed at a tentative rate with final settlement determined after submission of annual cost reports

and audits thereof by the Medicare fiscal intermediaries.

Medicare Advantage (Part C) – Acute inpatient and outpatient services rendered to Medicare

beneficiaries that chose an Advantage plan are paid primarily at prospectively determined rates. These

rates vary according to a patient classification system that is based on clinical, diagnostic, and other

factors.

Medicaid – Reimbursement for services rendered to Medicaid program beneficiaries includes

prospectively determined rates per discharge, per diem payments, discounts from established charges,

fee schedules and cost reimbursement methodologies with certain limitations. Cost reimbursable items

are reimbursed at a tentative rate with final settlement determined after submission of annual cost

reports and audits thereof by the Medicaid fiscal intermediaries.

Medicaid Health Maintenance Organization (HMO) – Reimbursement for services rendered to

Medicaid program beneficiaries that chose an HMO program where payments are based on

prospectively determined rates per discharge, per diem payments, discounts from established charges,

fee schedules and cost reimbursement methodologies with certain limitations.

Other – Reimbursement for services to certain patients is received from commercial insurance carriers,

health maintenance organizations and preferred provider organizations. The basis for reimbursement

includes prospectively determined rates per discharge, per diem payments and discounts from

established charges.

Cost report settlements under these programs are subject to audit by Medicare and Medicaid auditors and

administrative and judicial review, and it can take several years until final settlement of such matters is

determined and completely resolved. Because the laws, regulations, instructions, and rule interpretations

governing Medicare and Medicaid reimbursement are complex and change frequently, the estimates that

have been recorded could change by material amounts.

Settlements with third-party payers for retroactive revenue adjustments due to audits, reviews or

investigations are considered variable consideration and are included in the determination of the estimated

transaction price for providing patient care. These settlements are estimated based on the terms of the

payment agreement with the payer, correspondence from the payer and historical settlement activity,

including an assessment to ensure that it is probable that a significant reversal in the amount of cumulative

revenue recognized will not occur when the uncertainty associated with the retroactive adjustment is

- 15 -

subsequently resolved. Estimated settlements are adjusted in future periods as adjustments become known

(that is, new information becomes available), or as years are settled or are no longer subject to such audits,

reviews, and investigations.

For the nine months ended March 31, 2024, the Corporation accrued $121.6 million for the 340B remedy

lump sum settlement under the Centers for Medicare & Medicaid Services (“CMS”) November 8, 2023

Final Rule related to underpayments in the drug discount program for calendar years 2018 to 2022.

Financial Assistance – The Corporation provides services to all patients regardless of ability to pay. In

accordance with the Corporation’s policy, a patient is classified as a financial assistance patient based on

specific criteria, including income eligibility as established by the Federal Poverty Guidelines, as well as

other financial resources and obligations.

Charges for services to patients who meet the Corporation’s guidelines for financial assistance are not

reported as net patient service revenue in the accompanying consolidated financial statements. Therefore,

the Corporation has determined it has provided implicit price concessions to uninsured and underinsured

patients and patients with other uninsured balances (for example, copays and deductibles). The implicit

price concessions included in estimating the transaction price represent the difference between amounts

billed to patients and the amounts the Corporation expects to collect based on its collection history with

those patients.

Self-Insured Employee Health Benefits – The Corporation administers self-insured employee health

benefit plans for employees. The majority of the Corporation’s employees participate in the programs. The

provisions of the plans permit employees and their dependents to elect to receive medical care at either the

Corporation’s Health Ministries or other health care providers. Patient service revenue has been reduced by

an allowance for self-insured employee health benefits, which represents revenue attributable to medical

services provided by the Corporation to its employees and dependents in such years.

Premium and Capitation Revenue – The Corporation has certain Health Ministries that arrange for the

delivery of health care services to enrollees through various contracts with providers and common provider

entities. Enrollee contracts are negotiated on a yearly basis. Premiums are due monthly and are recognized

as revenue during the period in which the Corporation is obligated to provide services to enrollees.

Premiums received prior to the period of coverage are recorded as deferred revenue and included in

accounts payable and accrued expenses in the consolidated balance sheets.

Certain of the Corporation’s Health Ministries have entered into capitation arrangements whereby they

accept the risk for the provision of certain health care services to health plan members. Under these

agreements, the Corporation’s Health Ministries are financially responsible for services provided to the

health plan members by other institutional health care providers. Capitation revenue is recognized during

the period for which the Health Ministry is obligated to provide services to health plan enrollees under

capitation contracts. Capitation receivables are included in other receivables in the consolidated balance

sheets.

Reserves for incurred but not reported claims have been established to cover the unpaid costs of health care

services covered under the premium and capitation arrangements. The premium and capitation arrangement

reserves are included in accounts payable and accrued expenses in the consolidated balance sheets. The

liability is estimated based on actuarial studies, historical reporting, and payment trends. Subsequent actual

claim experience will differ from the estimated liability due to variances in estimated and actual utilization

of health care services, the amount of charges and other factors. As settlements are made and estimates are

revised, the differences are reflected in current operations.

- 16 -

Other Revenue – Other revenue is recorded at amounts the Corporation expects to collect in exchange for

providing goods or services not directly associated with patient care and recorded over the time in which

obligations to provide goods or services are satisfied. Other revenue includes revenue from the following

sources: grants, retail pharmacy, operating investment income, assisted and independent living, equity in

earnings of unconsolidated affiliates if the unconsolidated affiliate is operational and projected to make

routine and regular cash distributions, incentive revenue, and gainshare recognized under alternative

payment models and ancillary services.

Grant Revenue – Where grants are determined to be contributions, unconditional grants are recognized as

revenue when received. Conditional grants are recognized as revenue when the Corporation has complied

with and substantially met the conditions associated with the grant. For grants that are not contributions,

the Corporation recognizes revenue at the amount that reflects the consideration it is expected to be entitled

to in exchange for providing services under the term of the grant agreement.

Income Taxes – The Corporation and substantially all of its subsidiaries have been recognized as tax-

exempt pursuant to Section 501(a) of the Internal Revenue Code. The Corporation also has taxable

subsidiaries, which are included in the consolidated financial statements. The Corporation includes

penalties and interest, if any, with its provision for income taxes in other nonoperating items in the

consolidated statements of operations and changes in net assets.

Excess of Revenue Over Expenses – The consolidated statements of operations and changes in net assets

includes excess (deficiency) of revenue over expenses. Changes in net assets without donor restrictions,

which are excluded from excess (deficiency) of revenue over expenses, consistent with industry practice,

include the effective portion of the change in market value of derivatives that meet hedge accounting

requirements, permanent transfers of assets to and from affiliates for other than goods and services,

contributions of long-lived assets received or gifted (including assets acquired using contributions, which

by donor restriction were to be used for the purposes of acquiring such assets), net change in retirement

plan related items, discontinued operations and cumulative effects of changes in accounting principles.

Adopted Accounting Pronouncements –

In June 2016, the FASB issued ASU No. 2016-13, “Financial Instruments – Credit Losses (Topic 326)”.

This guidance is intended to align the needs of the users of financial statements related to credit loss

recognition and also address the potential weakness from the delayed recognition of credit losses, resulting

in an overstatement of assets. The amendments replace the current incurred loss methodology, which delays

recognition until it is probable a loss has occurred, with one that reflects expected credit losses and requires

consideration of a broader range of reasonable and supportable information to inform credit loss estimates.

This guidance was effective for the Corporation beginning July 1, 2023. The adoption of this guidance did

not materially impact the Corporation’s financial position, or results of operations. As required, additional

disclosures have been included.

Forthcoming Accounting Pronouncements –

In October 2021, the FASB issued No. 2021-08, “Business Combinations (Topic 805) – Accounting for

Contract Assets and Contract Liabilities from Contracts with Customers”. This guidance was issued to

address the inconsistency in accounting related to recognition of an acquired contract liability and the

payment terms and their effect on subsequent revenue by the acquirer. The amendments in this update

require that the acquirer recognize, and measure contract assets and contract liabilities acquired in a business

combination in accordance with Topic 606, as if it had originated the contracts, generally consistent with

how they were recognized and measured in the acquiree’s financial statements. This guidance is effective

for the Corporation beginning July 1, 2024. The Corporation will apply this guidance in consideration of

any future business combinations that may occur on or after July 1, 2024.

- 17 -

3. INVESTMENTS IN UNCONSOLIDATED AFFILIATES, BUSINESS ACQUISITIONS AND

DIVESTITURES

Investments in Unconsolidated Affiliates – The Corporation and certain of its Health Ministries have

investments in entities that are recorded under the cost and equity methods of accounting. The Corporation’s

share of equity earnings or losses from entities accounted for under the equity method and the classification

on the consolidated statements of operations and changes in net assets for the nine months ended March 31

are as follows (in thousands):

2024 2023

Other revenue 52,332$ 10,528$

Nonoperating Items 433,100 296,935

Total equity in earnings of unconsolidated affiliates 485,432$ 307,463$

The most significant of these investments include the following:

BayCare Health System – The Corporation holds a 50.4% interest in BayCare Health System Inc. and

Affiliates (“BayCare”), a Florida not-for-profit corporation exempt from state and federal income

taxes. BayCare was formed in 1997 pursuant to a Joint Operating Agreement (“JOA”) among the not-

for-profit, tax-exempt members of the Corporation, Morton Plant Mease Health Care, Inc., South

Florida Baptist Hospital, Inc. and BayCare. The Corporation’s participants in BayCare include St.

Anthony’s Hospital, Inc., St. Joseph’s Hospital, Inc., and St. Joseph’s Health Care Center, Inc.

(collectively, the “Trinity Participants”) and certain of their respective Affiliates. BayCare consists of

three community health alliances located in the Tampa Bay area of Florida, including St. Joseph’s-

Baptist Healthcare Hospital, St. Anthony’s Health Care, and Morton Plant Mease Health Care. The

Corporation has the right to appoint nine of the 21 voting members of the Board of Directors of

BayCare; therefore, the Corporation accounts for BayCare under the equity method of accounting. As

of March 31, 2024, and June 30, 2023, the Corporation’s investment in BayCare totaled $4.8 billion

and $4.4 billion, respectively.

Emory Healthcare/St. Joseph’s Health System – The Corporation holds a 49% interest in Emory

Healthcare/St. Joseph’s Health System (“EH/SJHS”). EH/SJHS operates several organizations,

including two acute care hospitals, St. Joseph’s Hospital of Atlanta, and John’s Creek Hospital. As of

March 31, 2024, and June 30, 2023, the Corporation’s investment in EH/SJHS totaled $269.4 million

and $221.5 million, respectively.

Life Flight Network, LLC – The Corporation, through its subsidiary Saint Alphonsus Regional

Medical Center, Inc. holds a 25% interest in Life Flight Network, LLC (“Life Flight”), an Oregon

limited liability company and its affiliates. Life Flight was formed in 2019 pursuant to a JOA. The

members of Life Flight, each owning 25%, are Saint Alphonsus Regional Medical Center, Inc., Legacy

Emmanuel Hospital and Health Center, Oregon Health and Sciences University, and Providence

Health System. Life Flight provides services, including both air and ground ambulance services, in the

Pacific Northwest with 34 bases in Oregon, Washington, Idaho and Montana. The Corporation

accounts for Life Flight under the equity method of accounting. As of March 31, 2024 and June 30,

2023, the Corporation’s investment in Life Flight totaled $78.6 million and $70.5 million, respectively.

Mercy Health Network – The Corporation held a 50% interest in Mercy Health Network, dba

MercyOne, (“MHN”), a nonstock-basis membership corporation with CommonSpirit Health (“CSH”)

,

holding the remaining 50% interest. MHN was the sole member of Wheaton Franciscan Services, Inc.

(“WFSI”) that operates three hospitals in Iowa: Covenant Medical Center located in Waterloo, Sartori

Memorial Hospital located in Cedar Falls and Mercy Hospital of Franciscan Sisters located in

Oelwein. MHN is also the sole member of Central Community Hospital (“CCH”), a critical access

hospital located in Elkader, Iowa. On September 1, 2022, the Corporation completed a transaction

with CSH through which the Corporation acquired CSH’s 50% interest in MHN, and now wholly

owns MHN. See “Acquisitions” subsequently in Note 3 for further information regarding this

transaction. As of March 31, 2024, and June 30, 2023, the Corporation’s investment in MHN totaled

$0, respectively.

- 18 -

Condensed consolidated balance sheets of BayCare, EH/SJHS, and Life Flight are as follows (in

thousands):

Baycare EH/SJHS Life Flight

Total assets 12,629,052$ 965,285$ 400,335$

Total liabilities 2,701,440$ 687,684$ 58,034$

Baycare EH/SJHS Life Flight

Total assets 11,526,730$ 878,549$ 371,904$

Total liabilities 2,616,025$ 603,076$ 61,758$

March 31, 2024

June 30, 2023

Condensed consolidated statements of operations of BayCare, EH/SJHS, Life Flight and MHN are as

follows (in thousands):

Baycare EH/SJHS Life Flight

Revenue, net 4,040,479$ 783,864$ 199,015$

Excess of revenue over expenses 516,976$ 78,018$ 32,155$

Baycare EH/SJHS Life Flight MHN

Revenue, net 3,658,807$ 677,034$ 168,341$ 64,186$

Excess (deficiency) of revenue over expenses 571,666$ 14,510$ 22,370$ (4,236)$

Nine months ended March 31, 2023

Nine months ended March 31, 2024

MHN results are prior to the acquisition date of September 1, 2022, and for the two months ended August

31, 2022.

The following amounts have been recognized in the accompanying consolidated statements of operations

and changes in net assets related to the investments in BayCare, EH/SJHS, Life Flight, and MHN (in

thousands):

Baycare EH/SJHS Life Flight

Other revenue -$ -$ 8,039$

Equity in earnings of

unconsolidated organizations 387,077 47,809 -

Other changes in net assets

without donor restrictions (3,642) - -

Total 383,435$ 47,809$ 8,039$

Baycare EH/SJHS Life Flight MHN

Other revenue -$ -$ 5,593$ (2,077)$

Equity in earnings of

unconsolidated organizations 288,177 6,983 - -

Other changes in net assets

without donor restrictions 15,986 - - -

Total 304,163$ 6,983$ 5,593$ (2,077)$

Nine months ended March 31, 2023

Nine months ended March 31, 2024

MHN results are prior to the acquisition date of September 1, 2022, and for the two months ended August

31, 2022.

- 19 -

Acquisitions:

MercyOne & MHN – On September 1, 2022, the Corporation completed a transaction with CSH through

which (i) the Corporation acquired CSH’s 50% interest in MHN, which is the sole member of WFSI and

the MHN subsidiary that owns and controls CCH, thereby becoming the sole corporate member of MHN,

(ii) MHN became the sole corporate member of Catholic Health Initiatives-Iowa, Corp. d/b/a MercyOne

Des Moines Medical Center (“MercyOne Des Moines”), a regional health care system located in Des

Moines, Iowa, and (iii) Trinity Home Health Services d/b/a Trinity Health At Home, a subsidiary of the

Corporation, acquired certain home care, hospice, and home infusion pharmacy operations from an affiliate

of CSH located in the vicinity of Des Moines (“Iowa Home Care Assets”, and collectively with (i) and (ii),

the “MercyOne Acquisition”). The completion of the acquisition marks a shared commitment to ensuring

access to health care across Iowa. Operating as a part of Trinity Health, MercyOne will retain its name and

brand while enhancing more integrated and unified care in the communities it serves.

The cash paid to CSH in consideration for the MercyOne Acquisition totaled $633.9 million, of which

$613.0 million was paid during the first quarter of fiscal year 2023 and a $20.9 million post-closing

reconciliation adjustment, as stipulated in the definitive agreement, was paid during the third quarter of

fiscal year 2023. Based on final purchase price allocations, goodwill of $27.1 million was recorded on the

consolidated balance sheet as of June 30, 2023.

For the nine months ended March 31, 2024 and 2023, the Corporation’s consolidated statements of

operations and changes in net assets included operating revenue of $1.3 billion and $0.9 billion, operating

losses of $24.6 million and $79.3 million, and deficiency of revenue over expense of $21.1 million and

$62.1 million, respectively, related to the operations of the MercyOne Acquisition.

North Ottawa Community Health System (“Grand Haven”) – The Corporation’s affiliate, Mercy Health

Partners, completed a transaction with Grand Haven under which Mercy Health Partners became the sole

member of Grand Haven on October 1, 2022. Grand Haven and its affiliates operate an acute care hospital,

urgent care center, long-term care facility and provide hospice services in the communities surrounding

Grand Haven, Michigan. The transaction will provide improved access to specialists, primary care and

health care services, while improving care delivery and access close to home in the Corporation’s West

Michigan market. The fair value of identifiable assets acquired exceeded the fair value of liabilities assumed

by $15.4 million which was recorded as an inherent contribution in nonoperating items in the consolidated

statement of operations and changes in net assets for the year ended June 30, 2023.

For the nine months ended March 31, 2024 and 2023, the Corporation’s consolidated statements of

operations and changes in net assets included operating revenue of $52.8 million and $31.6 million,

operating income of $2.5 million and operating loss of $0.9 million, and excess of revenue over expenses

of $2.5 million and deficiency of revenue over expenses of $1.3 million, respectively, related to the

operations of Grand Haven.

Genesis Health System – On March 1, 2023, the Corporation and its affiliate, MHN, completed a

transaction with Genesis Health System, an Iowa nonprofit corporation and Genesis Health System, an

Illinois not-for-profit corporation (together “Genesis”), under which MHN became the sole member of each

and acquired substantially all assets and liabilities except for certain foundation assets, liabilities and net

assets. Genesis and its affiliates operate four acute care hospitals, including two critical access hospitals,

convenient care centers, physician practices, a long-term care facility joint venture, an independent living

facility for seniors and hospice services in the communities in eastern Iowa and western Illinois. The fair

value of identifiable assets acquired exceeded the fair value of liabilities assumed by $468.1 million that

was recorded as an inherent contribution in nonoperating items in the consolidated statement of operations

and changes in net assets for the year ended June 30, 2023. Based on a revised assessment of assets and

liabilities, a $3.3 million reduction to inherent contribution was recorded during the second quarter of fiscal

year 2024 resulting in total inherent contribution of $464.8 million. As part of the transaction the

Corporation also agreed to a capital commitment as further disclosed in Note 4.

- 20 -

For the nine months ended March 31, 2024 and 2023, the Corporation’s consolidated statements of

operations and changes in net assets included operating revenue of $660.9 million and $66.5 million,

operating income of $45.5 million and operating loss of $1.8 million, and excess of revenue over expenses

of $54.9 million and $0.7 million, respectively, related to the operations of Genesis.

Based on final purchase price allocations the summarized balance sheet information is shown below as of

the respective acquisition dates (in thousands):

MercyOne

Acquisition

Grand Haven

Genesis

Estimated fair value of net tangible assets acquired:

Cash 58,987$ 5,665$ 43,112$

Investments, current 90,277 - 2,064

Patient accounts receivable 174,100 5,620 91,254

Other current assets 56,324 2,972 51,957

Assets limited or restricted as to use - noncurrent portion 56,158 2,320 324,487

Property and equipment - net 436,682 22,864 210,292

Operating lease right-of-use assets 95,707 - 47,704

Investments in unconsolidated affiliates 60,783 - 49,079

Other long-term assets 16,630 1,761 19,139

Goodwill 27,064 - -

Previously held investments in unconsolidated affiliates (111,151) - -

Medicare cash advances (19,648) - -

Other current liabilities (156,811) (11,877) (123,015)

Long-term debt - (11,702) (127,415)

Long-term portion of operating lease liabilities (83,570) - (42,429)

Other long-term liabilities (32,218) (2,001) (47,565)

Noncontrolling ownership interest in subsidiaries - - (433)

Net assets with donor restrictions (35,439) (202) (33,434)

Cash paid 633,875$ - -

Inherent contribution 15,420$ 464,797$

The amount of the Corporation’s pro forma revenue, earnings, and changes in net assets, had the MercyOne,

Grand Haven and Genesis acquisitions occurred on July 1, 2021 are as follows for the nine months ended

March 31 (in thousands):

2023

2022

Total operating revenue 16,685,894$

16,892,255$

Excess (Deficiency) of revenue over expenses net of noncontrolling interest 822,713

(24,147)

Change in net assets without donor restrictions 741,854 57,822

Change in net assets with donor restrictions 17,417 (2,494)

- 21 -

Divestiture:

St. Francis Medical Center (“SFMC”) Trenton, N.J. – On December 22, 2022, the Corporation, through

its subsidiary Maxis Health System (“Maxis”), transferred the membership interest of SFMC and certain

subsidiaries as well as $14.5 million of cash, and certain inventory and equipment, to Capital Health

System, Inc. (“Capital”). As a result of this transaction, restructuring costs of $82.3 million were incurred,

primarily related to loss on sale, asset retirement obligations and transition benefits for colleagues during

fiscal year 2023.

For the nine months ended March 31, 2023, the Corporation’s consolidated statements of operations and

changes in net assets included operating revenue of $59.3 million, operating losses of $99.0 million, and

deficiency of revenue over expenses of $103.0 million (inclusive of restructuring costs), related to the

operations of SFMC.

4. PROPERTY AND EQUIPMENT

A summary of property and equipment is as follows (in thousands):

March 31, June 30,

2024 2023

Land 439,100$ 428,858$

Buildings and improvements 11,592,806 11,287,425

Equipment 7,664,371 7,524,260

Finance lease right-of-use assets 95,071 95,329

Total 19,791,348 19,335,872

Accumulated depreciation and amortization (11,777,068) (11,168,290)

Construction in progress 818,488 678,915

Property and equipment - net 8,832,768$ 8,846,497$

In conjunction with the acquisition of Genesis as described in Note 3, the Corporation and MHN committed

to allocate not less than $450 million of capital to Genesis over seven years with the commitment period

ending March 1, 2030. The capital commitment period may be extended up to 18 months under certain

circumstances. The Corporation’s related capital spending for Genesis through March 31, 2024 is $57.9

million.

5. LONG-TERM DEBT AND OTHER FINANCING ARRANGEMENTS

Obligated Group and Other Requirements – The Corporation has debt outstanding under a master trust

indenture dated October 3, 2013, as amended and supplemented, the amended and restated master indenture

(“ARMI”). The ARMI permits the Corporation to issue obligations to finance certain activities. Obligations

issued under the ARMI are joint and several obligations of the obligated group established thereunder (the

“Obligated Group,” which currently consists of the Corporation). Proceeds from tax-exempt bonds and