A GUIDE TO WORKING FOR YOURSELF

immigrantsrising.org

Introduction

Most undocumented immigrants face significant barriers to pursuing employment in the

United States. Employers are required to ask for proof of legal status, and it is illegal for

any employer to hire a person knowing that the individual is not lawfully authorized to

work. In this section, we have outlined some legal ways to earn money in the United

States. It is your responsibility to determine whether you may legally pursue these

options based on your immigration status. Be sure to consult with an experienced

immigration lawyer first.

There are multiple ways to work for yourself, including independent contracting (also

called consulting or freelancing) and establishing a formal business. Many individuals,

including professionals, do independent work outside of their regular employment as a

way to boost earnings or lay the foundation for a business. This section will discuss what

it means to be an independent contractor, personal information needed to pursue this

option, tax liability, and independent contractor guidelines.

Basic Facts

● An independent contractor is a self-employed person who produces a specific

type of work product in a determined amount of time.

● The general rule for being an independent contractor is that the payer has the

right to control only the result of the work and not what will be done and how it

will be done.

● An independent contractor receives all profits and is held liable for all losses and

debts.

● All immigrants regardless of legal status are able to earn a living as independent

contractors, or start a business using an ITIN or SSN.

● An independent contractor must pay self-employment tax and income tax. An

independent contractor may use an ITIN to file and pay taxes instead of a SSN.

● As mandated by IRCA, an individual or entity (client) is NOT required to obtain

Form I-9, or otherwise inquire about immigration status from independent

contractors or sporadic domestic workers.

● Independent contractors should submit a W9 From instead of the I-9 Form to

each entity (client) they provide independent contractor services to. The W-9 is

filled out at the start of work by an independent contractor and kept on record by

the payer (client).

● A payer (client) must file a 1099 Form for each independent contractor paid $600

or more. A copy of the 1099 is mailed to the independent contractor at the end

of the year and he or she becomes responsible for paying taxes thereafter.

● Federal Statute 8 U.S. Code 1324a(a)(4) prohibits an individual or entity from

knowingly engaging an unauthorized individual to provide services as a

contractor.

● If a DACA beneficiary were to lose his or her work permit, the company that hired

them would not be able to contract with him or her. In the case of DACA getting

revoked, a DACA beneficiary could pursue independent contract work or start a

business using his or her assigned SSN, as long as he or she contracts with any

other entity other than the one that is aware of the expired work authorization.

● If you obtained DACA and used it to get a SSN you should not continue to use or

renew your ITIN. Regardless of the possible termination of DACA, the assigned

SSN will remain yours even if the individual’s work authorization terminates. You

may continue to use your SSN to work as an independent contractor or start a

business; both options do not require work authorization.

Legal Considerations for Independent Contracting

It is important to consider and be aware of the legal aspects of earning a living as an

independent contractor without legal status. Under federal law, as mandated by the

Immigration Reform and Control Act of 1986 (IRCA)

1

, it is illegal to knowingly employ

unauthorized workers in the United States. This applies to all workers; however, an

employer’s responsibility to verify work authorization is much higher for workers

classified as employees than for workers classified as independent contractors, sporadic

domestic workers, or workers who are hired through contracts with other legal entities.

The IRCA requires employers to verify that every new employee is legally authorized to

work in the U.S., through a two-part federal employment verification system, known as

the “I-9 System”. First, an employee must complete Form I-9, Employment Eligibility

Verification and assert under penalty of perjury that they are legally authorized to work

in the U.S. Second, the employer must review the original documentation from a

specified list (e.g., birth certificates, passports and work permits) to verify both the

worker’s identity and eligibility to work. After review, the employer must certify under

penalty of perjury that they have examined the original documentation.

2

There are exceptions to the I-9 System obligations when not dealing with employees. An

individual or entity is NOT required to obtain Form I-9 from independent contractors or

sporadic domestic workers.

3

Further, Individuals or entities are generally not obligated

to affirmatively verify the work authorization of individuals whom they engage as

independent contractors. However, Federal Statute 8 U.S. Code 1324a(a)(4) prohibits an

individual or entity from knowingly engaging an unauthorized individual to provide

services as a contractor.

4

This means that if an employer is aware that an employee’s

work authorization has expired, he or she could not then contract with that same

individual as an independent contractor. Therefore, if a DACA beneficiary were to lose

his or her work permit, the company that hired them would not be able to contract with

1

Immigration Reform and Control Act of 1986, Pub. L. No. 99-6603, 100 Stat. 3359 (codified at 8 U.S.C §

1324a). The IRCA amended the Immigration and Nationality Act (“INA”).

https://www.gpo.gov/fdsys/pkg/STATUTE-100/pdf/STATUTE-100-Pg3445.pdf

2

8 CFR § 274a.2(b)(1)(i)(B), https://www.uscis.gov/ilink/docView/SLB/HTML/SLB/0-0-0-1/0-0-0-11261/0-

0-0-28757/0-0-0-28810.html

3

8 CFR § 274a.1, https://www.uscis.gov/ilink/docView/SLB/HTML/SLB/0-0-0-1/0-0-0-11261/0-0-0-

28757.html

4

United States Code, 2006 Edition, Supplement 5, Title 8 - ALIENS AND NATIONALITY

https://www.gpo.gov/fdsys/granule/USCODE-2011-title8/USCODE-2011-title8-chap12-subchapII-partVIII-sec1324a/content-

detail.html

him or her. In the case of DACA getting revoked, a DACA beneficiary could pursue

independent contract work or start a business using his or her assigned SSN, as long as

he or she contracts with any other entity other than the one that is aware of the expired

work authorization. Individuals who fail to comply with Form I-9, or knowingly hire or

contract undocumented individuals may face civil fines, criminal penalties, or debarment

from government contracts.

5

It should be noted that in some instances, engaging in unauthorized employment

(which USCIS has interpreted to include unauthorized self-employment) may adversely

impact the ability of the individual to adjust his or her immigration status at a later time.

However, legal experts who consulted with us could not imagine a scenario in which

prior unauthorized work caused an

additional

adverse impact to adjustment beyond the

adverse impact of having been present without authorization.

5

https://www.uscis.gov/i-9-central/penalties

Independent Contracting

Although employers may not knowingly hire an unauthorized immigrant, federal and

state laws often do not require proof of immigration status for an individual to go into

business for him or herself and receive payment for goods or services. Individuals who

perform services, but are not employees, are sometimes categorized as independent

contractors.

Definition: An independent contractor is a self-employed person who produces a

specific type of work product in a determined amount of time. The difference between

an independent contractor and an employee is discussed below, but the general rule is

that the person paying an independent contractor has the right to control or direct only

the result of the work and not what will be done and how it will be done.

6

The

independent contractor may be paid an hourly rate or a flat fee. A contract

7

is signed

between parties to justify the working relationship, outline services, fees, duration of

contract, and protect intellectual property. Independent contractors generally use their

own name to do business, but they may decide to start their own company by starting a

sole proprietorship and using a business name instead.

Personal Identification Required: The person or company that pays is not required to ask

an independent contractor to fill out an I-9 (used to verify an employee’s identity and to

prove that the individual is able to legally work in the US), or otherwise inquire about

immigration status. They will, however, require a Social Security Number or an Individual

Taxpayer Identification Number (ITIN)

8

to commence work. Please note that if you

obtained DACA and used it to get a SSN you should not continue to use or renew your

ITIN. Regardless of the possible termination of DACA, the assigned SSN will remain your

SSN even if the individual’s work authorization terminates.

Liability: An independent contractor receives all profits and is held liable for all losses

and debts. If you’re a contractor, you may consider getting general liability insurance

6

For further information on independent contractor work and guidelines see

http://www.irs.gov/businesses/small/article/0,,id=99921,00.html

7

This is one example, many contract templates are available online.

(GLI) that can protect you from a variety of claims including bodily injury, property

damage, personal injury and others that can arise from your business operations.

9

Taxes: An independent contractor must pay self-employment tax and income tax. An

independent contractor may use a Taxpayer Identification Number (ITIN) to file and pay

taxes instead of a Social Security Number (SSN).

IRS Forms Required of Independent Contractors W-9: The IRS requires that payers use

Form W-9

10

to obtain taxpayer identification numbers from independent contractors.

The W-9 is filled out at the start of work by an independent contractor and kept on

record by the payer. Note that if, in one calendar year, an independent contractor is paid

anything less than $600 then the payer does not need to request a W-9 Form.

11

1099: The IRS requires that payers use Form 1099

12

to record the total amount of money

paid to independent contractors in any given calendar year. A payer must file a 1099 for

each independent contractor paid $600 or more. A copy of the 1099 is mailed to the

independent contractor at the end of the year and he or she becomes responsible for

paying taxes thereafter.

Recap of Forms Needed to Work as an Independent Contractor

● W-7 Form: Only needed to get an ITIN if you do not have a SSN and are not

eligible to get one.

● W-9 Form: You give a W9 form to each entity you do business with.

● 1099 Form: You get back a 1099 form at the end of year from each entity you

conducted business with that paid you more than $600 in one year. You use this

form to file your taxes.

● Written (and customized) Contract: Given to each entity you do business with to

justify your working relationship, outline your services, fees and duration of

contract, and protect your intellectual property.

9

Contact your insurance provider for more information about GLI.

10

The latest Form W9 may be found here: https://www.irs.gov/pub/irs-pdf/fw9.pdf?portlet=103

11

http://www.mbahro.com/News/tabid/110/entryid/147/W9-Tax-Form-FAQ.aspx

12

The latest Form 1099 may be found here: https://www.irs.gov/pub/irs-pdf/f1099msc.pdf

Basic Guidelines for Independent Contractors

*This section comes from IRS Publication 15-A, 2016 Edition.

14

When discussing independent contracting with potential payers/clients, make sure to

cite the IRS directly and refer them to information posted directly by the IRS. Many

individuals make a living and earn additional income through independent contracting,

so you want to avoid making it seem like these opportunities are only available for

immigrants.

People such as doctors, veterinarians, and auctioneers who follow an independent trade,

business, or profession in which they offer their services to the public, are generally not

employees. The general rule for being an independent contractor is that the payer has

the right to control only the result of the work and not what will be done and how it will

be done. It extremely important for you and your potential payer/client to understand

the rules and differences between an independent contractor and an employee.

Misclassification may result in legal consequences and penalty fees incurred by the

payer/client.

To determine whether an individual is an employee or an independent contractor under

the common law, the relationship of the worker and the business must be examined. In

any employee-independent contractor determination, all information that provides

evidence of

the degree of control and the degree of independence must be considered. Facts that

provide evidence of the degree of control and independence fall into three categories:

behavioral control, financial control, and the type of relationship of the parties. These

facts are discussed next.

Behavioral Control

Facts that show whether the business has a right to direct and control how the worker

does the task for which the worker is hired include the type and degree of:

1. Instructions the business gives the worker. An employee is generally subject to the

business’ instructions about when, where, and how to work. All of the following are

examples of types of instructions about how to do work:

14

For more detailed information, visit https://www.irs.gov/pub/irs-pdf/p15a.pdf

a. When and where to do the work

b. What tools or equipment to use

c. What workers to hire or to assist with the work

d. Where to purchase supplies and services

e. What work must be performed by a specified individual

f. What order or sequence to follow

The amount of instruction needed varies among different jobs. Even if no instructions

are given, sufficient behavioral control may exist if the employer has the right to control

how the work results are achieved. A business may lack the knowledge to instruct some

highly specialized

professionals; in other cases, the task may require little or no instruction. The key

consideration is whether the business has retained the right to control the details of a

worker’s performance or instead has given up that right.

2. Type of training provided to the worker. An employee may be trained to perform

services in a particular manner. Independent contractors ordinarily use their own

methods.

Financial Control

Facts that show whether the business has a right to control the business aspects of the

worker’s job include the following:

3. The extent to which the worker has unreimbursed business expenses. Independent

contractors are more likely to have unreimbursed expenses than are employees. Fixed

ongoing costs that are incurred regardless of whether work is currently being performed

are especially important. However, employees may also incur unreimbursed expenses in

connection with the services they perform for their business.

4. The extent of the worker’s investment. An employee usually has no investment in the

work other than his or her own time. An independent contractor often has a significant

investment in the facilities he or she uses in performing services for someone else.

However, a significant investment is not necessary for independent contractor status.

5. The extent to which the worker makes services available to the relevant market. An

independent contractor is generally free to seek out business opportunities.

Independent contractors often advertise, maintain a visible business location, and are

available to work in the relevant market.

6. How the business pays the worker. An employee is generally guaranteed a regular

wage amount for an hourly, weekly, or other period of time. This usually indicates that a

worker is an employee, even when the wage or salary is supplemented by a commission.

An independent contractor is usually paid by a flat fee for the job. However, it is

common in some professions, such as law, to pay independent contractors hourly.

7. The extent to which the worker can realize a profit or loss. Since an employer usually

provides employees a workplace, tools, materials, equipment, and supplies needed for

the work, and generally pays the costs of doing business, employees do not have an

opportunity to make a profit or loss. An independent contractor can make a profit or

loss.

Type of Relationship

Facts that show the parties’ type of relationship include:

8. Written contracts describing the relationship the parties intended to create. This is

probably the least important of the criteria, since what really matters is the nature of the

underlying work relationship, not what the parties choose to call it. However, in close

cases, the written contract can make a difference.

9. Whether the business provides the worker with employee-type benefits, such as

insurance, a pension plan, vacation pay, or sick pay. The power to grant benefits carries

with it the power to take them away, which is a power generally exercised by employers

over employees. A true independent contractor will finance his or her own benefits out

of the overall profits of the enterprise.

10. The permanency of the relationship. If the company engages a worker with the

expectation that the relationship will continue indefinitely, rather than for a specific

project or period, this is generally considered evidence that the intent was to create an

employer-employee relationship.

11. The extent to which services performed by the worker are a key aspect of the regular

business of the company. If a worker provides services that are a key aspect of the

company’s regular business activity, it is more likely that the company will have the right

to direct and control his or her activities. For example, if a law firm hires an attorney, it is

likely that it will present the attorney’s work as its own and would have the right to

control or direct that work. This would indicate an employer-employee relationship.

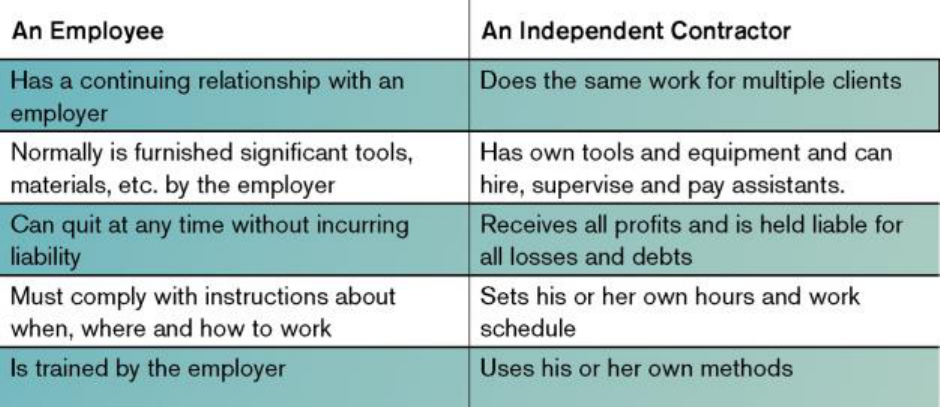

Employees vs. Independent Contractors: Main Differences

Employees vs. Independent Contractors: Examples

*This section comes from “Your Rights As An Independent Contractor, Part 4: Industry

Examples,” About.com.

Below you will find examples of the types of work considered to be an independent

contractor or an employee.

Computer Industry

Independent Contractor. Steve Smith, a computer programmer, is laid off when

Megabyte

Inc. downsizes. Megabyte agrees to pay Steve a flat amount to complete a onetime

project to create a certain product. It is not clear how long it will take to complete

the project, and Steve is not guaranteed any minimum payment for the hours spent on

the program. Megabyte provides Steve with no instructions beyond the specifications

for the product itself. Steve and Megabyte have a written contract, which provides

that Steve is considered to be an independent contractor, is required to pay Federal

and state taxes, and receives no benefits (such as health insurance, vacation pay, or

sick pay) from Megabyte. Megabyte will file a Form 1099-MISC. Steve does the work

on a new high-end computer, which cost him $7,000. Steve works at home and is not

expected or allowed to attend meetings of the software development group. Steve is an

independent contractor.

Marketing Industry

Independent Contractor. Lupe Castellanos was contracted by BoostIt Enterprises to

represent a well known coffee brand at the Women’s Nike Marathon in San Francisco. A

signed contract established that this was an independent contractor position, the hourly

rate and duration of promotion. There were no instructions beyond a sample script

provided by client to be used to

learn and talk about the product at the event. Lupe also signed a W-9 form and will

receive a 1099 Form from BoostIt Enterprises if she makes $600 or more working other

events. All communication is done via e-mail or phone with the client. Lupe works from

home using her own computer, phone and car.

Tips to Start Earning a Living as an Independent Contractor

Independent contracting requires a change of mindset, from working for someone to

working for yourself. This means establishing an expertise (through a product or

service), marketing yourself, networking, engaging in continuous learning and most

importantly, believing in yourself! Below are some tips to help you start earning a living

as an independent contractor:

● Make sure the type of work you wish to do follows the independent contractor

guidelines

● Become familiar with the legal aspects of working as an independent contractor

● Think about what it is that you enjoy doing and/or have a natural talent for

● Highlight your assets and skills and be prepared to demonstrate how they meet

the needs of your clients

● Research similar types of work so you know the standard rate for your services

● Become familiar with writing contracts and make sure to sign a contract with

every client

● Promote yourself via social media (LinkedIn, YouTube, Facebook, etc.), blogs, and

websites

● Join an independent consultant network, such as IQ Workforce

● Become active in your local business community

● Attend workshops and watch webinars, lectures, presentations, etc. (available for

free on YouTube) related to consulting/independent contracting

● Research additional tips and resources online

● Become familiar with paying taxes as an independent contractor

About Immigrants Rising

Founded in 2006, Immigrants Rising transforms individuals and fuels broader changes.

With resources and support, undocumented young people are able to get an education,

pursue careers, and build a brighter future for themselves and their community. For

more information, visit immigrantsrising.org.

Acknowledgements

We are grateful for the valuable insight, research, feedback and revisions from the

National Immigration Law Center (Josh Stehlik, Gabrielle Lessard, Ignacia Rodriguez,

Jackie Vimo, Avideh Moussavian and Tanya Broder), Asian Americans Advancing Justice

– Asian Law Caucus (Winifred Kao and Aarti Kohli), the Immigrant Legal Resource Center

(Sally Kinoshita and Jose Magana-Salgado), the The Chavez Foundation (Elena Chavez

Quezada), Prospera Co-ops (Karla Reyes), Family Reunions Project (Alvaro Morales),

Emmanuel Mendoza, Xiuying Li Yu and Alice Matsuda.