Tax and Duty Manual Part 05-01-30

The information in this document is provided as a guide

only and is not professional advice, including legal advice. It

should not be assumed that the guidance is comprehensive

or that it provides a definitive answer in every case.

1

Revenue Guidelines for Determining Employment

Status for Taxation Purposes

Part 05-01-30

Document created May 2024

Tax and Duty Manual Part 05-01-30

2

Table of Contents

1. Introduction ......................................................................................................3

2. Decision-making Framework.............................................................................7

3. Understanding the Decision-making Framework..............................................8

3.1 Work/wage bargain........................................................................................8

3.2 Personal Service ...........................................................................................12

3.3 Control..........................................................................................................15

3.4 All the circumstances of the employment....................................................19

3.5 The legislative context..................................................................................23

4. What does the decision mean for businesses? ...............................................25

4.1 Determination of employment status for taxation purposes.......................25

4.2 Who is an employee? ...................................................................................25

4.2.1 Construction ..............................................................................................26

4.2.2 Part-time, casual and seasonal workers ....................................................27

4.2.3 Workers engaged in a domestic setting ....................................................28

4.2.4 Couriers and other transport providers.....................................................29

4.2.5 Media.........................................................................................................29

4.2.6 Public sector ..............................................................................................30

4.2.7 Platform operators ....................................................................................30

4.3 Provision of workers through a Company ....................................................32

4.4 Provision of workers through an employment agency ................................32

5. Decision Tree...................................................................................................33

6. Examples .........................................................................................................34

Tax and Duty Manual Part 05-01-30

3

1. Introduction

For tax purposes, the treatment of individuals who are engaged as employees

(‘contract of service’) differs to those who are engaged as a contractor/self-

employed (‘contract for service’), although there is generally no difference in the tax

rate which applies

1

.

Where an individual is engaged under a contract of service, i.e., as an employee

taxable under Schedule E, income tax, USC and PRSI should be deducted from his or

her employment income through their employer’s payroll system on or before when

a payment is made. He or she can claim a deduction through MyAccount for

expenses incurred wholly, exclusively and necessarily in carrying out the duties of

the employment. For the avoidance of doubt, “office holders” (e.g., Company

Directors) are always subject to PAYE.

Where an individual is engaged under a contract for service, i.e., as a self-employed

individual taxable under Schedule D, he or she will generally be obliged to register

for self-assessment, to pay preliminary tax and file their own income tax returns

using the Revenue Online Service (ROS). He or she can claim a deduction for

expenses incurred wholly and exclusively for the purpose of his or her trade or

profession.

Each business making payments to individuals needs to correctly determine whether

individuals are employed or self-employed based on the facts and circumstances of

each relationship and payment. While it is usually clear whether an individual is

employed through a ‘contract of service’ or self-employed through a ‘contract for

service’, it has not always been immediately obvious and it has led to confusion in

relation to their employment status. There is no single, clear legal definition of the

terms “employed” or “self-employed” in Irish or EU law.

These Guidelines are being issued to outline the tax implications of the Supreme

Court judgment of 20 October 2023 in ‘The Revenue Commissioners v Karshan

(Midlands) Ltd. t/a Domino’s Pizza’ (“the case”) in making such a determination. The

judgment was delivered by Mr. Justice Murray and when referencing his analysis

throughout this document, it is referred to as “the judgment”. The full text of the

judgment is available at the Court Service website.

These Guidelines set out the key elements of the judgment and its implications for

businesses engaging employees, workers, contractors or sub-contractors. It is

1

There is a 3% USC surcharge on non-PAYE income over € 100,000

Tax and Duty Manual Part 05-01-30

4

important to stress that the case was concerned solely with the proper tax

treatment of the workers concerned. The broader question of employment rights

was not before the Court and was not considered by it.

While Revenue has responsibility for determination of employment status of a

worker for taxation purposes, responsibility for determination of employment status

of a worker for PRSI purposes falls to the Department of Social Protection. In

general, self-employed individuals and certain company directors are liable to pay

Class S PRSI, whereas employees generally pay Class A PRSI, with their employers

also making a PRSI contribution. Each class has different PRSI rates and entitlements.

If an employer or employee is unsure as to the correct PRSI class to apply to

payments made to an employee, the case can be referred to Scope Section in the

Department of Social Protection, Áras Mhic Dhiarmada, Store Street, Dublin 1 D01

WY03 for a determination. Further details can be obtained at Operational

Guidelines: Scope Section - Insurability for PRSI purposes.

Responsibility for a range of employment rights, such as employment equality,

minimum wage rates, holiday pay, sick pay, maternal and paternal leave, sectoral

pay agreements, etc., falls to the Workplace Relations Commission (WRC) under the

aegis of the Department of Enterprise, Trade and Employment. The question of

whether a person is an employee or is self-employed for the purposes of Irish

employment rights legislation depends on the definition contained in each

instrument, for example, the Equality Acts, health and safety legislation, the National

Minimum Wage Act, the Unfair Dismissals Act, etc. The WRC’s Adjudication Service

and the Labour Court (on appeal) determine employment status as a preliminary

issue when adjudicating on employment rights complaints. Information on

employment rights can be obtained from the WRC, O’Brien Road, Carlow. Further

details can be obtained at the Workplace Relations Commission website.

Each State body operates within its own legislative framework and a decision by one

body is non-binding on the other two bodies. While Revenue endeavours to ensure

consistency, occasionally, due to the separate legislative frameworks, differences

arise. As a result, it cannot be assumed that the decision of one State body will be

replicated by either or both of the other two.

The Code of Practice on Determining Employment Status (“the Code”) was originally

developed in 2001 by the Employment Status Group under the Programme for

Prosperity and Fairness to address concerns around the number of individuals

categorised as ‘self-employed’ where ‘employee’ status would have been more

appropriate. It was updated in 2007 by the Hidden Economy Monitoring Group

under the Towards 2016 Social Partnership Agreement.

Tax and Duty Manual Part 05-01-30

5

In 2021, the Code was further updated by an interdepartmental working group

comprising of the Department of Social Protection (DSP), Revenue and the WRC. The

purpose of the Code is to provide a clear understanding of employment status,

taking into account labour market practices and developments in legislation and

caselaw. It aims to be of benefit to employers, employees, independent contractors

and legal, financial and HR professionals, together with staff in the DSP, Revenue and

the WRC.

Following the judgment, Revenue is working with colleagues in DSP and the WRC to

update the Code.

The judgment provides an extensive review of caselaw to date in the area of

determination of employment status, and succinctly summarises it through the

provision of a decision-making framework. The decision-making framework consists

of five questions that should be used to resolve the question of whether a contract is

one of service (employee) or for service (self-employed). This will greatly assist

businesses in determining the employment status of workers, i.e., whether they are

employed or self-employed.

It has restated the position that the terms and conditions of an engagement as set

out in a written contract should be considered when determining the status of the

relationship. However, they may not be the sole determining factor as the facts and

circumstances of that relationship may also have to be considered in the application

of the decision-making framework.

It has also clarified that there does not need to be a continuity of service, in effect, a

worker engaged to carry out one job, gig or shift, will generally be an employee for

tax purposes for that one job, gig or shift.

The judgment was concerned with the tax treatment of delivery drivers who were

treated as self-employed contractors. It is important to note that the judgment also

applies across all sectors and not just delivery drivers. This is considered further in

these guidelines. Revenue’s treatment of services supplied through a Personal

Services Company, or a Managed Services Company, which are common structures

through which contracting services are supplied, has not changed. Revenue do not

look through corporate structures, except in very limited circumstances specifically

provided for in the Taxes Consolidation Act. In that regard, for tax purposes, the

judgment only relates to individuals and there is no change in the tax position for

businesses who engage companies to carry out work on their behalf.

Tax and Duty Manual Part 05-01-30

6

Having considered the full facts and circumstances of the case, and applying the five-

step framework, the Supreme Court unanimously confirmed Revenue’s

determination of the employment status for taxation purposes of the workers in the

case as employees.

Some businesses have relied on previous decisions of Deciding Officers of the

Department of Social Protection, to treat workers as self-employed for the purpose

of tax. With the clarification from the judgment, such previous decisions cannot be

relied upon for determining the correct taxation treatment. The five-step framework

should be applied to each relationship to determine the taxation status of each

worker.

As outlined throughout these guidelines, there are a number of workers across a

number of sectors who will need to be treated as employees for tax purposes, where

previously they have been treated as self-employed. It is essential that businesses

urgently and comprehensively review arrangements with all workers and determine

their employment status for taxation purposes. Where a business previously treated

a worker as self-employed, rather than as an employee, and the review of these

arrangements by reference to the five-step framework indicates that they are

employees for tax purposes, the business must now rectify that position by treating

the relevant workers as employees and operating PAYE.

Throughout these guidelines, the term ‘business’ is used to describe any recipient of

a service and includes not-for-profit entities (such as sporting organisations and

charities), and ‘worker’ is used to describe the service provider (i.e., the self-

employed individual, or employee, as the case may be).

Tax and Duty Manual Part 05-01-30

7

2. Decision-making Framework

The decision-making framework consists of five questions as follows:

“1. Does the contract involve the exchange of wage or other remuneration for

work?”. This is more commonly known as the ‘Work/Wage bargain’ and is

explained in more detail in Section 3.1.

“2. If so, is the agreement one pursuant to which the worker is agreeing to

provide their own services, and not those of a third party, to the employer?”.

This is more commonly known as ‘Personal Service’ and is explained in more

detail in Section 3.2.

“3. If so, does the employer exercise sufficient control over the putative

employee to render the agreement one that is capable of being an

employment agreement?”. ‘Control’ is explained in more detail in Section 3.3.

“4. If these three requirements are met, the decision maker must then determine

whether the terms of the contract between the employer and worker

interpreted in the light of the admissible factual matrix, and having regard to

the working arrangements between the parties as disclosed by the evidence,

are consistent with a contract of employment, or with some other form of

contract having regard, in particular, to whether the arrangements point to

the putative employee working for themselves or for the putative employer.”.

‘All the circumstances of the employment’ is explained in more detail in

Section 3.4.

“5. Finally, it should be determined whether there is anything in the particular

legislative regime under consideration that require the court to adjust or

supplement any of the foregoing.”. ‘The Legislative Context’ is explained in

more detail in Section 3.5.

The first three questions are to be viewed as a filter. If any of these are answered

negatively, there cannot be a contract of employment. If the first three questions

are answered affirmatively, questions four and five must then be considered to

determine if a contract of employment exists. The Decision Tree at Section 5

provides a visual representation of how the framework should be applied.

Section 3 analyses each of the five questions in more detail.

Tax and Duty Manual Part 05-01-30

8

3. Understanding the Decision-making Framework

The five-question decision making framework is expanded on in this section. As

detailed above, questions one to three must be answered ‘yes’ for there to be a

contract of employment, with questions four and five then considered.

3.1 Work/wage bargain

The Supreme Court reframed the ‘mutuality of obligation’ test as simply being a

reasonable description of the work/wage bargain. It is necessary to establish if there

is an exchange of work for remuneration before a working arrangement could be

categorised as an employment contract.

The judgment considers that there has been unnecessary confusion caused in

determining employment status by using the term “mutuality of obligation”. The

confusion caused is reflected in the judgment as follows:

“The fact is that the term ‘mutuality of obligation’ has, through a

combination of over-use and under-analysis been transformed in

employment law from what should have been a straightforward description

of the consideration underlying a contract of employment, to a wholly

ambiguous label. That ambiguity has enabled it to morph from merely

describing the consideration that must exist before a contract is capable of

being a contract of employment, to its being presented as a defining feature

that in itself differentiates a contract of service from a contract for services.

The consequence has been to assume that the ‘mutual obligations’ that

subtend a contract of employment are in all cases necessarily and

categorically different from those that underlie a relationship of employer

and independent contractor. This is the fundamental error in Karshan’s legal

analysis.”.

The judgment ultimately concludes that the confusion:

“…will be most effectively avoided in future if the use of the phrase in this

arena is discontinued.”.

It remains the position that there must be a wage or other consideration as

otherwise there is no employment contract:

Tax and Duty Manual Part 05-01-30

9

“The phrase [Mutuality of Obligation] should be viewed as doing no more

than describing the consideration that has to be present before a working

arrangement is capable of being categorised as an employment contract.”.

Thus, the first question to consider is whether there is actually a contract (whether

express or implied) in place at all:

“It goes without saying that the first question a decision maker must broach

when determining if the parties have entered into an employment contract,

is whether they have entered into a contract at all. Arrangements lacking an

intention to create legal relations (as may be the case in what are truly casual

or domestic agreements) and/or which are unsupported by consideration (as

may be the case with volunteers) will be immediately out-ruled.”.

Payment of expenses to volunteers solely to reimburse them for expenses incurred,

up to civil service rates, to allow them to undertake their work for an organisation

whose functions and aims are both altruistic and non-commercial, is not

‘consideration’ in the context of this work/wage bargain. Further detail on payments

to volunteers is included on revenue.ie.

Similarly, arrangements that are truly casual or domestic in nature, e.g., where a

family engages a person to attend their home to “mind” their child for a few hours

on an ad-hoc basis would not create a legal relationship. However, where a family

engages a child minder to attend their home for a fixed number of days per week at

set times, etc., this would be indicative of a contract of employment, subject to the

application of the framework.

The judgment outlines different types of arrangements where an employment

contract may arise:

“For as long as a worker is actually undertaking work for which the employer

is liable to pay them, there is consideration that may be characteristic of an

employment contract: a single engagement can give rise to a contract of

employment if work which has in fact been offered is in fact done for

payment, and a contract which provides merely that a worker will be paid for

such work as they perform is capable of being a contract of service.”.

Thus, a contract may consist of a regular wage for work bargain, a series of

agreements governing the discharge of particular tasks, an agreement to complete

one identified task, an ongoing agreement defined by an umbrella contract, or some

combination of the foregoing. It is possible therefore that a worker can be

Tax and Duty Manual Part 05-01-30

10

considered an employee in respect of one “job”, even where there is no continuity of

obligation. This is explained further below.

The judgment clarifies:

“To qualify as an employment contract for the purposes of this initial hurdle,

however, the consideration must involve a promise of some kind by the

worker to work for the putative employer. That promise may be one to work

at defined points into the future, it may be to work if called upon to do so, or

it may be to work starting more or less contemporaneously with the

agreement itself. It may be to work continuously, or over an undefined

period as called upon, or for a defined period(s), or for the purposes of

completing a specific task(s).”.

Turning then to the employer:

“The obligations on the employer may be to provide work, to pay for work, to

retain the worker on the books and/or to confer some benefit on the worker

which is non-pecuniary. These may, but need not necessarily, involve an

ongoing or continuous obligation into the future to provide work.”

It is necessary to determine the terms of the contract to understand the work/wage

bargain:

“In the course of that process, it will be necessary to determine what,

precisely, the terms of the alleged contract are, and whether they derive

from written agreement, oral agreement, are express, implied, or fall to be

inferred from a course of conduct. There will, in some circumstances, be an

issue of characterisation that this case shows can be important: is the

contract a regular wage for work bargain with ongoing obligations to pay and

work, is it a series of employment agreements governing the discharge of

particular tasks, is it an agreement to complete one identified task, is it an

ongoing agreement defined by an ‘umbrella’ contract, is it some combination

of the foregoing and, indeed, is the agreement one for the exchange of

labour for pay at all? In some cases involving a so-called triangular

relationship, it may be necessary to very specifically identify which

obligations are owed by which party to another.”.

However, there is no requirement for there to be an ongoing commitment:

Tax and Duty Manual Part 05-01-30

11

“…the most important issue that arose before this court was the question of

whether it is a sine qua non of such a relationship (i.e. employer and

employee) that there be an ongoing reciprocal commitment extending into

the future to provide and perform work on the part of the employer and

worker respectively.”.

The judgment confirms that it may be important when deciding if there is continuous

employment for the purposes of certain statutory regimes, but it is not a “sine qua

non” (essential condition) of an employment relationship.

In summary, provided there is payment by a business to a worker for a service,

whether agreed in writing or not, and whether the work is carried out on a once off

basis, or on a continuous basis, or anything in between, there is a contract which is

capable of being an employment contract. Indeed, the consideration of the

judgment regarding the work/wage bargain would strongly suggest that the default

position is that, for the purposes of this test, there is likely to be a contract of

employment unless it can be clearly demonstrated otherwise. Examples indicative of

being capable of being a contract of employment (subject to the other elements of

the framework) include:

An individual undertaking a security role at one sporting event for a set fee;

An individual serving at a bar at one concert for a set fee;

A labourer working for a week on a building site on an hourly rate.

Examples of where there is no work/wage bargain where the individual is not

treated as an employee for tax purposes include:

An individual providing stewarding services at one or a series of matches in

an unpaid capacity;

An individual on a rota working part-time every week in a charity shop as a

volunteer in an unpaid capacity;

A family member minding children full-time in an unpaid capacity.

Whether the agreement between the business and worker in the examples above is

in writing or verbal, whether its terms are express or implied, and whether it’s a

single or ‘umbrella’ contract, will not alter the position. If the business has

determined that the answer to this question is “yes”, it must proceed to examine the

second question of the framework – personal service.

Tax and Duty Manual Part 05-01-30

12

3.2 Personal Service

This question considers whether the worker has agreed to provide their services to

the business personally. This is what is known as the ‘substitution test’. Substitution

concerns a worker’s right to appoint someone else as a substitute if he or she is

unable or unwilling to do all or part of the work, or never intended to do the work

themselves. In other words, it concerns whether the worker can “subcontract” the

work or hire assistants, and whether the agreement provides for personal service or

can the worker independently arrange for someone else (a "substitute”) to provide

the service. An important question to ask when considering this test can be who

does the work when the worker is absent?

The judgment reiterates the importance of this test by saying:

“This is more than just a matter to be ‘taken into account’, as the decision

maker has to make a judgment having regard to the terms of the agreement

and the facts as to whether the agreement is, or is not, one for personal

service. This is the essence of an employment agreement.”.

It was indicated that it would be:

“…helpful to separate out the requirement of personal service so as to make

clear that it is a requirement and not merely a factor to be put into the mix.”.

While some degree of limited substitution is consistent with a contract of service,

the judgment notes that:

“Substitution clauses which impose substantive restrictions on the

circumstances in which a worker can delegate the obligations they have

assumed will thus not be inconsistent with employment status.”.

The judgment further refines the term by saying:

“A right of substitution available only where the worker is unable to carry out

the work is consistent with personal performance. A right of substitution

limited only by the need to show that the substitute is qualified to do the

work is not consistent with personal service, while a right only with the

consent of another person who has absolute and unqualified discretion to

withhold consent will be consistent with personal performance.”.

Tax and Duty Manual Part 05-01-30

13

The judgment summarises the foregoing by saying:

“But, in every case it is necessary to decide if the agreement is just one for

personal services, whether it is an agreement for personal services with a

conditional capacity for delegation, or whether it is an agreement that

enables such unconditional delegation that it is not a contract for personal

services at all.”.

Thus, an important factor in assessing the level of substitution possible includes a

consideration as to whether and to what extent the business has a say in who the

worker hires. Other important factors to consider are whether and to what extent

the substitute is controlled and/or paid by the business or the worker. The judgment,

in referring to Pimlico Plumbers Ltd v Smith [2017] EWCA Civ.51 states:

“An unfettered right to substitute is inconsistent with an undertaking to

provide the workers service personally. A conditional right to substitute may

or may not be inconsistent with personal performance depending on the

conditionality, and in particular on the nature and degree of any fetter: a

limited and occasional right will point to personal service.”.

A typical characteristic of an independent contractor or self-employed person is that

they are free to hire other people, on his or her own terms, to do the work which has

been agreed to be undertaken.

In situations where there are umbrella contracts such as existed in the Karshan case

itself, the judgment states:

“…where the contract of employment is an individual assignment governed in

part by an umbrella agreement, this means that the worker cannot both

accept an offer of work in accordance with the umbrella contract, and then

be permitted to unconditionally delegate it.”.

In summary, the more restrictions imposed on the freedom for a worker to appoint a

substitute, the more indicative the arrangement is that of a contract of employment.

The types of restrictions that may occur which indicate an employment relationship

will be arrangements where prior approval of substitutes is required such that the

business has an unfettered right of refusal, payment of substitutes is made directly

by the business rather than the person they are providing cover for, or where

substitutes are from a pool of preapproved workers.

Tax and Duty Manual Part 05-01-30

14

Examples where the substitution test is indicative of a contract of employment

(subject to the other elements of the framework) include:

No ability to nominate a substitute, i.e., the business arranges someone to

provide cover if necessary;

A worker engaged as a child minder in the home of a family, where the

worker cannot nominate a substitute;

A delivery driver who can only nominate a substitute from a list of candidates

provided by the business.

Examples where the substitution test is indicative of a self-employment contract

include:

A contract to run a bar at a racecourse with no provision included as to who

will serve the drinks;

A contract to install a gas boiler at a residential property without any

specification that the work be undertaken by one named individual;

A contract to provide landscaping services, whether at a private or

commercial setting, without any specification that the work be undertaken

by one named individual.

If the business has determined that the answer to this question is “yes”, it must

proceed to consider the third question of the framework – control.

Tax and Duty Manual Part 05-01-30

15

3.3 Control

Control refers to the ability, authority, or right of a business to exercise control over

a worker concerning what work should be done, and how, when and where it should

be done. The continuing importance of control was noted in the judgment as

follows:

“While the meaning of ‘control’ has, as I have explained earlier, evolved, this

long established feature of the Irish cases has never been questioned, and

indeed Walsh J. in Roche v. Patrick Kelly and Co. Ltd. [1969] IR 100 at p. 108

(with whose judgment Ó Dálaigh CJ and Haugh, Budd and FitzGerald JJ.

agreed) authoritatively restated it: “[w]hile many ingredients may be present

in the relationship of master and servant, it is undoubtedly true that the

principal one, and almost invariably the determining one, is the fact of the

master’s right to direct the servant not merely as to what is to be done but as

to how it is to be done. The fact that the master does not exercise that right,

as distinct from possessing it, is of no weight if he has the right.”.

As the third filter of the decision-making framework, control is described as a

“gateway”. It is not determining the issue of employment status but rather

describing the legally minimum level of control before a relationship is capable of

being an employment contract. The judgment notes that this level of control differs

depending on the engagement:

“What this ‘legally minimum’ element of control is, will depend on the nature

of the employment, and in some cases it may indeed prove to be a wide

gateway. It is well and clearly expressed by MacKenna J. in RMC: the control

involves a lawful authority to command ‘so far as there is scope for it’ (at p.

515). The question is thus directed to whether there is a sufficient framework

of control in the sense of ultimate authority, rather than the concept of day-

to-day control envisaged by the older cases (see Montgomery v. Johnson

Underwood Ltd. [2001] EWCA Civ. 318, [2001] IRLR 269 at para. 19).”.

Tax and Duty Manual Part 05-01-30

16

There must obviously be a minimum level of control before a relationship can be

capable of being an employment contract. The judgment confirms this:

“…if the putative employer does not enjoy the power to direct the type of

work the worker is required to do, the relationship will not be capable of

constituting an employment relationship (Minister for Education v. The

Labour Court and ors. at para. 9.13, and para. 102 of the reported judgment).

Similarly if the service is provided to a person who has no entitlement to

prescribe times by which the work is to be done, no power to determine

where or in what conditions the work is to be done or, within an enterprise,

the persons who were to do particular work, it is difficult to see how this

requirement could be met.”.

When assessing the degree of control held by the business and the degree of

independence held by the worker, it should be borne in mind that the right of the

business to exercise control is more relevant than whether they actually exercise

this right. The judgment states:

“…the decision-maker is concerned to establish a right of control, over what

is to be done, at least generally the way in which it is to be done, the means

to be employed in doing it, the time when and the place where it shall be

done. That must take account of the nature of the employment and the

control an employer would be reasonably expected to exert.”.

The actual degree of control will vary with the type of work and the skills of the

worker. Deciding the degree of control that exists when examining the engagement

of experts can be difficult. Due to their expertise and specialised training, they may

need little or no specific direction in their daily activities. When considering the right

of control over what is to be done and modern working with skilled and unskilled

labour being examined, the judgment notes:

“If unskilled, close direction as to the means and manner by which the work

is to be done is expected. While if skilled, the employer would not be

expected to be in a position to direct the worker as to how to achieve the

prescribed objective.”.

Tax and Duty Manual Part 05-01-30

17

This is expanded on further:

“While in cases involving skilled work, it is to be expected that the employer

will not have the right to direct how the work is to be done, the test requires

that the employer retain some residual authority over it.”.

An example of such residual control would be the expectation to meet clearly

defined deliverables, or meet clearly set targets, within defined deadlines. Control

for skilled workers would generally not extend to how work is undertaken, rather

what is required to be done by when.

An additional test to consider, as a subset of control, is the ‘enterprise test’, which

considers which of the parties to a working relationship bore the economic risk:

“…. it is not possible to separate the question of control from the question of

whether the evidence points to the worker carrying on business on their own

account.”.

The following parts of the judgment provide detailed analysis of how this is to be

examined:

“The need for this element has not been diminished, nor has the RMC test

been supplanted, by a ‘business on his or her own account’ test as a result of

the decision in Henry Denny”,

” … the issue of whether a person is in business on their own account is

relevant to the question of control, because the degree of control exercised

by the employer over a person in business on their own account will, by

definition, be less than that exercised over an employee.”,

“… if the service is provided to a person who has no entitlement to prescribe

times by which the work is to be done, no power to determine where or in

what conditions the work is to be done or, within an enterprise, the persons

who were to do particular work, it is difficult to see how this (control)

requirement could be met.”.

Tax and Duty Manual Part 05-01-30

18

Integration (the extent to which a worker, and their work, form a coherent part of

the business) was also not considered by the Supreme Court to be a stand-alone test

and rather it can be, but does not always have to be, viewed within the context of

control. The judgment states:

“It should be viewed as doing no more than articulating a possible feature of

some employment arrangements that may negate or support control, and/or

might otherwise suggest that the worker is so divorced from the employer’s

undertaking that they cannot be properly viewed as being employed within

it.”.

The judgment cites Lord Denning in Stevenson, Jordan and Harrison v. MacDonald

and Evans [1952] 1 TLR 101 as first formulating the test:

“…One feature which seems to me to run through the instances is that, under

a contract of service, a man is employed as part of the business and his work

is done as an integral part of the business; whereas under a contract for

services his work, although done for the business, is not integrated into it but

is only accessory to it.”.

Determining this (i.e., the integration test) has its difficulties, which is why it is not

treated as a stand-alone test:

“…the notion of which work is ‘integral’ to a business is not easily applied has

been frequently observed (see for example Deakin and Morris at para. 2.14).

So, a decision maker may be quite right in a particular case to examine the

extent to which the worker and their work form a coherent part of the

employer’s organisation but treating this as a stand-alone ‘test’ (with the

implication that it must be interrogated in all cases) is neither necessary nor

helpful.”.

Additional matters to consider when examining control include elements such as

notice periods, whether and to what extent the business controls the method, and

amount, of payment, and the working hours of the worker.

Tax and Duty Manual Part 05-01-30

19

3.4 All the circumstances of the employment

If the first three “filter” questions on work/wage bargain, personal service and

control are answered affirmatively, consideration then needs to be given to the

entire factual matrix of the engagement. The basis for this ‘filtering’ approach was

set out in the judgment as follows:

“While in many cases decision makers will always end up at the same point –

looking at all relevant factors – I think the prescription of a method should at

least assist in obtaining uniformity of approach, in both clearly identifying

and removing from the inquiry at an early stage those situations which, in

law, are incapable of amounting to a contract of employment and in

describing the ‘pointers’ that suggest one way or another whether an

arrangement between worker and employer should be viewed as consistent,

or inconsistent, with the status of employment.”,

“…. I think the right approach is to view the first three questions I have just

identified as a filter in the form of preliminary questions which, if any one is

answered negatively means that there can be no contract of employment,

but if all are answered affirmatively, allow the interrogation of all of the facts

and circumstances to ascertain the true nature of the relationship. This is

what Keane J. in Henry Denny described as the consideration of ‘all the

circumstances of [the] employment.”.

When reviewing all the facts and circumstances that should be interrogated to

ascertain the true nature of the relationship, the judgment notes that:

“While many ‘tests’ have been formulated around the elements of an

employment relationship, they all lead directly or indirectly to two closely

related (and somewhat unremarkable) conclusions – first, that every case

depends on the particular facts, and second that in distinguishing an

arrangement that is a contract of employment from one that is not, it is

necessary to assess all relevant features of that relationship, identifying those

that are, and those that are not, consistent with an employment contract,

and determining based upon the sum of those parts the correct

characterisation. The role of the various tests is thus, ultimately, not as much

to condition the content of that ‘multi-factorial’ analysis (although of course

as the law has developed various important and helpful indicia that are, and

are not, consistent with an employment contract have been identified in the

cases) as it is to formulate a workable structure within which that analysis

Tax and Duty Manual Part 05-01-30

20

can be conducted while, at the same time, enabling the early elimination of

those arrangements that do not present the legally required minimum

contents of such a contract.”.

The complete wording for this step of the framework is as follows:

“If these three requirements are met the decision maker must then

determine whether the terms of the contract between the employer and

worker interpreted in the light of the admissible factual matrix and having

regard to the working arrangements between the parties as disclosed by the

evidence, are consistent with a contract of employment, or with some other

form of contract having regard, in particular, to whether the arrangements

point to the putative employee working for themselves or for the putative

employer.”.

The judgment expands on four specific matters to be considered at this stage. The

first two are as follows:

1. “First, while RMC looked to ‘the provisions of the contract’, the decision in

Castleisland establishes that the contract itself must be interpreted (as, today,

with all contracts) in the light of the factual matrix in which it was concluded.

There is nothing new in that regard in Irish law, but insofar as the RMC test does

not make this clear, it should be expressly stated.”.

2. “Second, both Henry Denny and Castleisland demand that in conducting that

inquiry, the court must take into account the actual dealings between the

parties. Keane J. thus referred in the first of these cases to the relevance of ‘the

manner in which the work was done’, Murphy J. to ‘the facts or realities of the

situation on the ground’ and (in Castleisland) Geoghegan J. stressed that the

Appeals Officer whose decision was in issue in that case, was bound to examine

‘what the real arrangement on a day to day basis between the parties was’.”.

The judgment concludes that these statements:

“…mean that where an agreement purports to characterise the relationship

between or the status of the parties, that description does not fetter the

function of the court in determining what, as a matter of law, the agreement

actually is. ..[..].. These statements also require that, as a matter of the

general law, an agreement which says one thing when both parties in fact

intend another will not be given effect to under the doctrine of sham, or

perhaps mistake.”.

Tax and Duty Manual Part 05-01-30

21

On that basis, while a detailed written agreement may carry significant weight,

efforts to describe a relationship in a particular way which differs from the day-to-

day reality, in order to circumvent or frustrate the operation of statutory provisions,

will be challenged. Additionally, terms of a written contract, which seek to describe

the legal consequences of rights and obligations or conclusions of law, rather than

defining the rights and obligations of the parties to the contract, may be

disregarded. Phrases such as “as a self-employed contractor you will be responsible

for your own tax” will carry little weight.

However, it is worth noting that the judgment caveated this somewhat as follows:

“As I have alluded to, there may well be cases in which it is found that the

parties elected to describe their relationship in a particular way in order to

circumvent or even frustrate the operation of some statutory provision,

which would engage both questions of statutory intent and the doctrine of

sham. But outside that situation whether, and if so when, it is possible in Irish

law to otherwise allow evidence of the conduct of the parties to override the

consequences of detailed and written contract, have to await a case in which

that question is properly in issue, and is argued in full.”.

The third and fourth elements to be considered are as follows:

3. “Third, the last clause in the RMC test is reframed in this formulation to make

clear that this part of the inquiry does not depend on any presumption arising

from the other parts. It is free standing, the onus of proof being in the ordinary

way on the party who asserts any proposition of fact, law or mixed fact and law

having regard to the statutory process in which the decision is made.”.

4. “Fourth, it is useful to remember that if the contract is not one of employment it

is something else, and the question of whether it is within the former category

cannot in reality be resolved without identifying what it actually is. … the issue

may, for example, be a choice between an employment relationship and one of

copartners (as in DPP v. McLoughlin [1986] IR 355) or joint venturers, or (as in

RMC) a contract of carriage or (as in Cheng Yuen v. Royal Hong Kong Golf Club

[1998] ICR 131) a licence agreement permitting the worker to provide a service

to third parties. Nonetheless, the effect of the Market Investigations case was to

elevate the issue of whether the facts were consistent or not with the worker

carrying on business on their own account, or whether they pointed to the

worker conducting the business of the employer”.

Tax and Duty Manual Part 05-01-30

22

After reviewing the complete factual matrix, consideration should be given as to

whether the evidence is consistent with a contract of employment with the

individual working for the business as an employee or whether the individual is self-

employed. The question to be considered is whether the facts are consistent or not

with the worker providing services on his or her own account, or whether the facts

indicate that the worker is providing the services on behalf of the business. The

judgment notes that:

“… the law makes it clear that the capacity to profit in a material way from

their own skill, the need for the employee to invest significantly in their

ability to undertake the work, and the requirement to bring tools or

equipment to the task all lean against the existence of a contract of

employment.”.

However, there are no “static characteristics” indicative of an employment contract,

rather:

“What depends on the particular facts, however, is the place of those

positives and negatives and the weight to be given to them, in the balancing

exercise undertaken in a given case. That is a matter, when the relevant

factors pointing one way or the other are identified, for the assessment of

the decision maker.”.

The judgment states that it is appropriate that control be considered again at this

stage:

“…as there will be cases in which it is so extensive as to point overwhelmingly

in the direction of employment just as there will be cases in which it is so

attenuated as to push the agreement towards another type of relationship.”.

Section 3.3 above contains a detailed narrative on the control test.

Tax and Duty Manual Part 05-01-30

23

3.5 The legislative context

In relation to the legislative context, the judgment states that consideration needs to

be given to any legislation that requires an adjustment or supplement to any of the

foregoing questions in the particular circumstances of the relationship being

considered. This would occur where there are:

“…legislative provisions in which it is intended to carry a different meaning.

This may be evident from the language used in the statute as a whole, or

indeed its overall purpose and context.”.

This question opens the prospect that:

“…particular legislative schemes – in particular those involving the protection

of particular employee rights – might require a modification of either the

test, or (as was decided by the United Kingdom Supreme Court in Uber) to

the approach adopted to the relationship between a written contract of

employment and the practices of the parties in implementing it in a particular

case, must be factored into the analysis.”.

While there was no such legislation requiring application of this part of the

framework in the case, the judgment outlines this as one of the five questions for

cases where it may be relevant.

As an example of how this question of the framework might apply, one could look to

the EU Directive on Platform Workers. On 24 April 2024, the European Parliament

adopted the Directive. The provisions currently provide how employment status will

be determined for individuals working through digital platforms. The Directive aims

to correct the employment status of those who have been misclassified as self-

employed, improve transparency and regulate the use of algorithms and data in

taking decisions about platform workers. Once the Directive is approved by the

European Council and published in the Official Journal of the EU, all EU Member

States have two years to bring their national legislation in line with the Directive.

The Directive obliges EU Member States to establish a rebuttable legal presumption

of employment at national level, aiming to correct the imbalance of power between

the digital labour platform and the person performing platform work. The burden of

proof lies with the platform, meaning that it is up to the platform to prove that there

is no employment relationship.

Tax and Duty Manual Part 05-01-30

24

Another example is the application of PAYE on office holder payments, where no

application of the framework will be required, as application of PAYE on office holder

income is provided for in section 112 of the Taxes Consolidation Act.

Tax and Duty Manual Part 05-01-30

25

4. What does the decision mean for businesses?

4.1 Determination of employment status for taxation purposes.

A worker’s employment status for taxation purposes is not a matter of choice - it

depends on the terms and conditions of the role and whether the practical working

arrangements between the business and the worker are consistent with the express

categorisation of the contract. While it is usually clear whether an individual is

employed or self-employed, it may not always be obvious. The judgment provides

clarity on the determination of employment status of workers for taxation purposes.

Businesses who engage workers now have a clear decision-making model by

reference to the five-question framework set out in the Supreme Court judgment to

determine the employment status of each worker for taxation purposes. It is

essential that businesses urgently and comprehensively review arrangements with

all workers and determine their employment status for taxation purposes. It is clear

that there are a number of workers across a number of sectors who will need to be

treated as employees for tax purposes, where previously they have been treated as

self-employed. For those re-classified as employees for tax purposes, the business

will have an obligation to operate PAYE.

4.2 Who is an employee?

On foot of this judgment, it’s expected that there will be an increase in the number

of workers that will be determined to be employees for tax purposes once the five-

step framework is applied to their facts and circumstances. For example, it is difficult

to envisage how unskilled workers in the retail or hospitality sectors, or any worker

providing labour only services in the construction or transport sectors, would be

anything other than an employee when the framework is applied. Conversely, the

provision of goods or tools together with labour will not always result in the

relationship being classified as self-employment, particularly when the worker is

engaged in the main by one business or a number of connected businesses.

Businesses have been encouraged to review arrangements and apply the framework

to determine if a worker should be treated as an employee. While not being

prescriptive, Revenue would expect evidence of the analysis done to apply the five-

step framework when a worker is engaged, including, where appropriate, looking

beyond the simple wording of the contract between the business and the worker. As

relationships tend to change over time, it’s important that businesses undertake a

Tax and Duty Manual Part 05-01-30

26

regular review of the arrangements to ensure application of the framework at that

later point in time would not result in a different determination.

It is the nature of the engagement that determines the relationship, so it is possible

for a worker to have two or more employers. For example, a student may work as a

food delivery driver two evenings per week and work as a labourer on a construction

site on a Saturday. Having applied the five-step framework, the student can be an

employee in both scenarios.

Also, the fact that there is only one shift/engagement undertaken by a worker does

not in itself mean that a worker is self-employed, he or she can be an employee in

respect of one piece of work, subject to the application of the five-step framework.

Some general commentary on some sectors is included below.

4.2.1 Construction

The construction industry is one industry with a significant number of workers being

treated as self-employed. Since 1970, payments made to these self-employed

workers are subject to Relevant Contracts Tax (RCT) which is operated by the

business paying the worker. Tax is deducted at a rate specified by Revenue, that

being 0%, 20% or 35%. Since 2012, this deduction rate is updated and notified

though ROS in real-time and is determined by the circumstances of the worker with

compliant workers generally seeing 0% deducted, and non-compliant generally being

subject to 20% or 35% deduction. This system reduces potential tax leakage if the

workers fail to file their tax returns and make tax payments. It also operates in the

meat processing and forestry sectors.

Some construction workers are engaged on a full-time, or near full-time, basis by a

single entity or a group of connected entities and have no autonomy as to what work

they do and when they work. On foot of this judgment, subject to the facts and

circumstances and the framework being correctly applied, it is highly likely that such

workers will be determined as employees for taxation purposes.

Other scenarios where a worker is likely to be determined to be an employee for tax

purposes, following the application of the framework, include:

An unskilled worker operating as, for example, a casual labourer paid an

hourly rate, taking direction from the site foreman;

Tax and Duty Manual Part 05-01-30

27

A skilled worker (e.g., electrician, plasterer, roofer) who works alone (i.e.,

does not employ a team to work for him or her), uses material supplied by

the business and is told what, where and when to do work;

An individual fitting windows for one company or a group of connected

entities, on a continuous basis, using equipment supplied by the business,

and travelling in or driving a company vehicle.

There will always be workers in the construction sector who are properly treated as

self-employed and paid through the RCT system. Examples include:

An electrician who has his or her own firm with a team of workers, is engaged

to wire a number of houses for a fixed fee, is free to send anyone he or she

wishes to undertake the work and can profit if it’s done more efficiently, i.e.,

in less time;

Any worker who provides their service through a corporate, i.e., they are not

engaged directly as an individual by the business (construction company),

rather the business engages another company to provide a service, which is

undertaken by the worker. In this case, the worker is an employee of the

service company, rather than the construction company.

It is not unusual for skilled workers in the construction industry to be both an

employee and self-employed, but not for the same or connected businesses. For

example, an electrician who is an employee for the majority of the week but

undertakes ad-hoc work for individual householders at the weekend would likely be

self-employed in respect of the weekend work, subject to application of the

framework.

All construction businesses should ensure they have reviewed all workers by

reference to the framework and treat relevant workers as employees, except where

they are clearly self-employed.

4.2.2 Part-time, casual and seasonal workers

There was a perception that when workers were engaged on a part-time or casual

basis, including specifically for one off shifts, they were not employees as there was

no continuous employment obligation. These engagements are particularly

prevalent in sectors such as agriculture (e.g., fruit pickers, drivers for silage

contractors, relief milkers), retail (e.g., shelf stockers, till operators, fuel pump

attendants), entertainment (e.g., extras on tv shows, ticket scanners in venues,

parking attendants) and catering (e.g., waiters and waitresses, bar tenders,

cleaners). Such workers are generally employed for their own service (i.e., they

Tax and Duty Manual Part 05-01-30

28

cannot provide a substitute) and would be subject to significant control by the

business. On that basis, it is expected that such workers would be determined as

employees for tax purposes when the framework is applied.

All businesses employing such workers should ensure they have reviewed all workers

by reference to the framework and treat relevant workers as employees, except

where they are clearly self-employed.

4.2.3 Workers engaged in a domestic setting

As mentioned earlier, casual arrangements where a family engages a person to

attend their home to “mind” their child for a few hours on an ad-hoc basis would not

create an employment relationship and obligation to apply PAYE. This equally

applies to engaging trades people to do once-off tasks in the home, e.g., fix

appliances, install a boiler, carry out landscaping work, etc.

Aside from those arrangements, other than one domestic employee in the

employer’s private house paid less than € 40 per week

2

, there is no minimum

threshold for the application of PAYE where a worker is engaged to carry out such

services and, following the application of the framework, they are correctly classified

as an employee.

Generally, subject to the application of the framework, if a person is engaged on a

regular or an ongoing basis to care for a person or people in the home of the cared

for, the payer will have obligations to register as an employer and deduct PAYE.

In relation to the exemption from income tax

3

for gross earnings up to € 15,000 per

annum by individuals who provide a child-minding service for up to 3 children in the

childminders own home, this exemption is only available to self-employed

individuals, i.e., if applying the framework the childminder is determined to be an

employee rather than self-employed, PAYE is to be applied to all income.

Carers engaged through corporates would generally not be employees of the family

but of the corporate providing them. In such instances, the corporate agrees to

provide a carer and should apply PAYE to the payments made to the employees.

2

Section 986(6) TCA 1997

3

Section 216C TCA 1997.

Tax and Duty Manual Part 05-01-30

29

Families and individuals engaging such workers should ensure they have reviewed all

workers by reference to the framework and treat relevant workers as employees,

except where they are clearly self-employed.

4.2.4 Couriers and other transport providers

This sector has seen a lot of change with workers generally now generating a

significant portion, if not all, of their income from a single courier firm. In such

instances, workers generally have the logo of the courier firm on their vehicle, wear

a uniform or clothing incorporating the courier firms’ brand, are provided with a

company mobile phone with the number provided to customers, undergo

performance reviews, and undertake deliveries when, where and how (i.e., what

order) as directed by the firm. They are also generally an integral part of the business

of the courier firm. Applying the complete framework, such individuals would

generally be employees rather than self-employed, which they were historically

treated as. Indeed, removal of some elements identified above, e.g., provision of a

company phone or wearing specific clothing, would not generally see a different

determination being made.

It is noted that there are a minority of genuine self-employed couriers still in

existence, providing ad-hoc services to a number of businesses who do not impose

the same level of control over them as set out above. However, every business who

engages couriers should apply the framework to ensure they have correctly

determined the status of their couriers.

All courier firms should ensure they have, following application of the framework,

reclassified appropriate workers as employees, except where they are clearly self-

employed.

4.2.5 Media

Personal service is the essence of the majority of engagements between a media

outlet and its workers such as actors, presenters or journalists. As the business also

generally controls when work is undertaken and where, they would also generally

meet the control test. Due to the skilled nature of the roles, it’s unlikely the workers

will be told ‘how’ to undertake the work, but the level of residual control retained by

the business will result in the control test being met. This is equally applicable to

other workers in the sector such as camera persons, sound engineers and producers.

Free-lance journalists and photographers have been a long-standing feature of the

media industry. Where a worker produces content of his or her own volition and

Tax and Duty Manual Part 05-01-30

30

offers that content for sale to various media outlets, his or her status will, subject to

the framework, generally be that of an independent provider subject to self-

assessment as a self-employed worker. Commissioned work, i.e., where a media

outlet engages a person to produce content, will, subject to the framework,

generally result in the person being an employee of the media outlet in respect of

the work.

It is noted that some workers in this sector provide their services through the use of

personal service companies. Such workers will not be employees of the media outlet

but will be subject to PAYE on payments from their personal service companies.

All media firms should ensure they have applied the framework to workers and

reclassified the relevant directly employed workers as employees, except where they

are clearly self-employed.

4.2.6 Public sector

There are no special rules around determining whether a worker is an employee or

self-employed in the Public Sector. The framework equally applies to public sector

workers as all other workers.

It is expected that there may be some workers engaged by public sector bodies who

were treated as self-employed that will, when applying the framework, need to be

treated as employees.

All Public Sector bodies should ensure they have reclassified their directly employed

workers as employees, except where they are clearly self-employed.

4.2.7 Platform operators

Although the method of engagement of a ‘platform’ worker might be different from

traditional methods because of the use of modern technology, such workers will still

be categorised as being either an employee or self-employed using the same

approach as is taken with workers in other sectors. Each engagement must be

looked at based on the facts and circumstances of the case.

Platforms such as online food delivery platforms, with levels of control over workers

in terms of appearance, delivery, substitution and equipment would suggest control

consistent with employment. Similarly, where a business operating through a

platform can supervise performance, including by electronic means, and exercise

control over the distribution or allocation of tasks, it would be consistent with

Tax and Duty Manual Part 05-01-30

31

employment. Control over working conditions and restrictions on choosing working

hours will also display control consistent with employment.

While the EU Commission is progressing proposals on employment status in relation

to the gig economy

4

, it is clear from the judgment that the Supreme Court has clearly

established that gig workers can be employees for tax purposes. All businesses

employing such workers should ensure they apply the framework and reclassify

appropriate workers as employees, except where they are clearly self-employed.

4

Once domestic legislation is passed to implement the Directive in Ireland, these guidelines will be reviewed and

updated if necessary.

Tax and Duty Manual Part 05-01-30

32

4.3 Provision of workers through a Company

It is open to any worker to incorporate their business, at which point the business is

a separate legal entity. Any engagement of companies by businesses cannot be

contracts of service, or employments, for taxation purposes.

5

This judgment does

not disturb this position.

However, the employment status of workers contracting with those companies will

have to be considered having regard to the decision-making framework, bearing in

mind that those who are office holders will always be subject to PAYE.

4.4 Provision of workers through an employment agency

Revenue does not regard the taxation of workers employed through agencies any

differently to the taxation of workers employed by any other means. PAYE/PRSI/USC

is operated by agencies where the agencies are obliged to pay the person placed

with a business. In contrast, PAYE/PRSI/USC is operated by the business where the

business is obliged to make the payment to the person placed with them.

The PAYE system provides for the concept of a “paying employer”, who may not be

an employer in the strict sense. For example, a person in receipt of a pension can be

an “employee” and the body paying the pension can be an “employer” for the

purpose of operating the PAYE system.

The person who is contractually obliged to make the payment to an employed

agency worker is the employer for the purpose of collecting income tax, USC and

PRSI through the PAYE system. Tax and Duty Manual 05-01-15 explains the tax

treatment in more detail.

5

There are a number of provisions in Chapter 4 of Part 42, for example sections 985C to 985F, which provide for

PAYE liabilities to arise to a person other than the payer.

Tax and Duty Manual Part 05-01-30

33

5. Decision Tree

Figure 1 Decision Tree

Tax and Duty Manual Part 05-01-30

34

6. Examples

The examples included below are included for illustrative purposes only, and do not

have universal application. Each case has to be examined in the light of its own facts

and circumstances to determine the employment status of the worker for taxation

purposes.

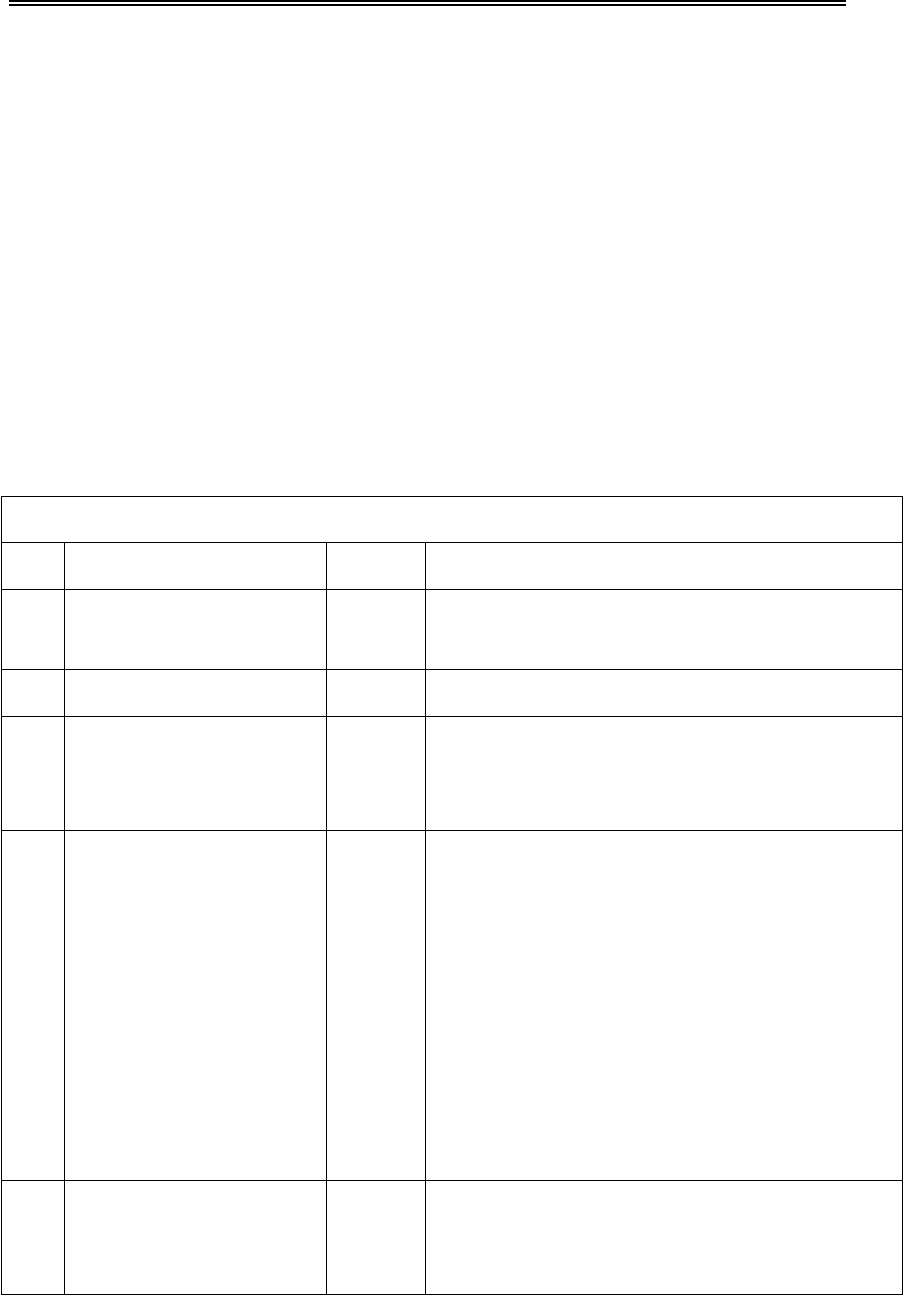

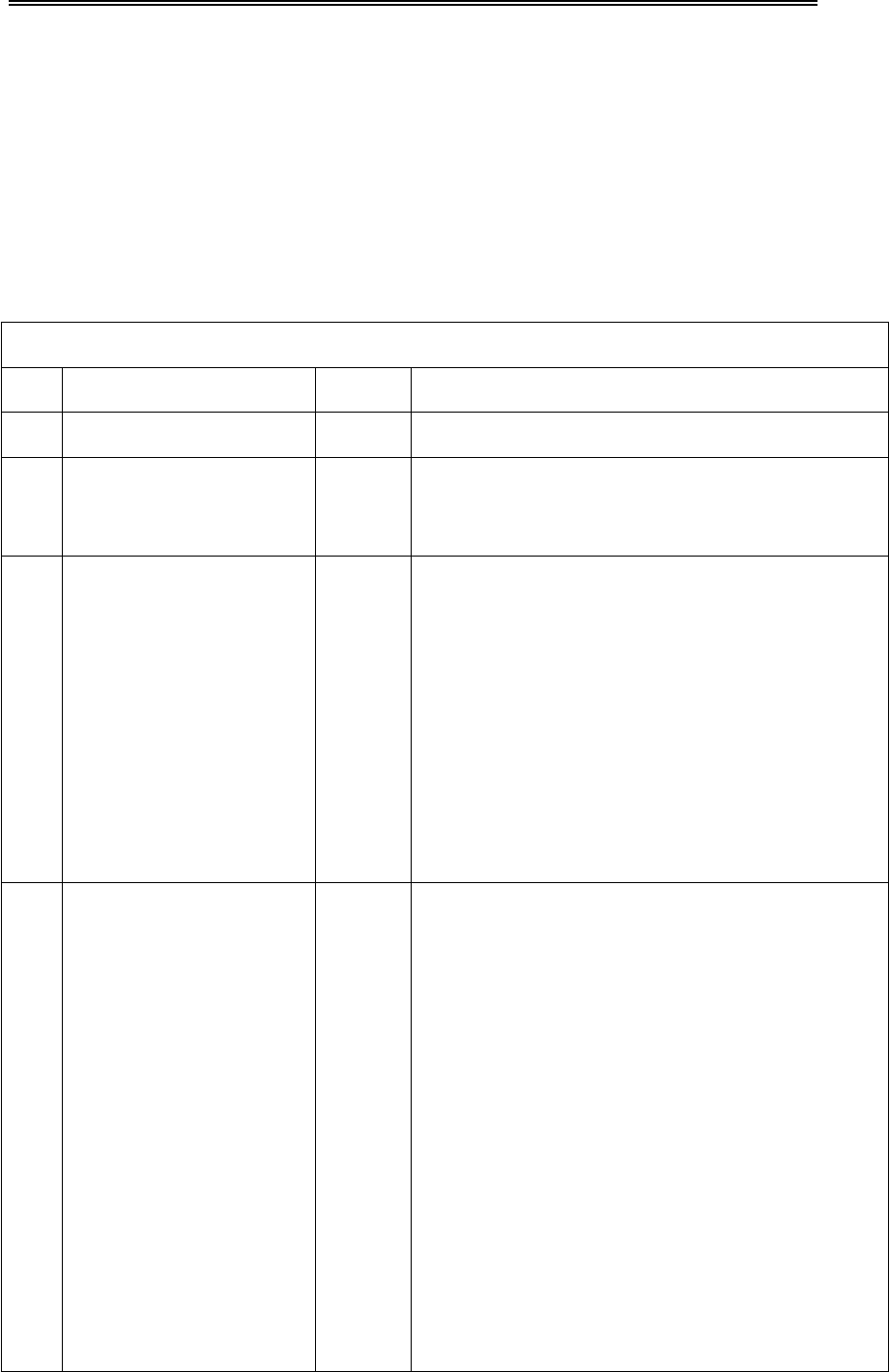

Example 1

A construction company, C Co, engages a general labourer, James, to work on a site.

James is to be paid an hourly rate. James cannot send someone else in his place. C

Co’s foreman determines the hours that will be worked. James does not supply

equipment and supplies labour only.

Five Step Framework

No.

Question

Answer

Explanation

1

Work/wage bargain

Yes

James is paid an hourly rate to undertake

work

2

Personal Service

Yes

James cannot send someone else in his place

3

Control

Yes

The site foreman, on behalf of C Co,

determines how, where, what and when the

work is to be done.

4

All the circumstances of

the employment

Yes

The contract of engagement is drafted as a

self-employment contract with payments

made to James reported through the RCT

portal by C Co. The facts of the case do not

support this position. In addition to the facts

detailed under questions 1 to 3, James cannot

profit beyond his set hourly rate, is told what

he’s being paid by the foreman, uses tools

supplied by C Co and is insured similar to an

employee.

5

Legislative context

N/A

There is no legislation that requires an

adjustment or supplement to any of the

questions above.

James will be an employee based on the relationship and PAYE should be applied by

C Co.

Tax and Duty Manual Part 05-01-30

35

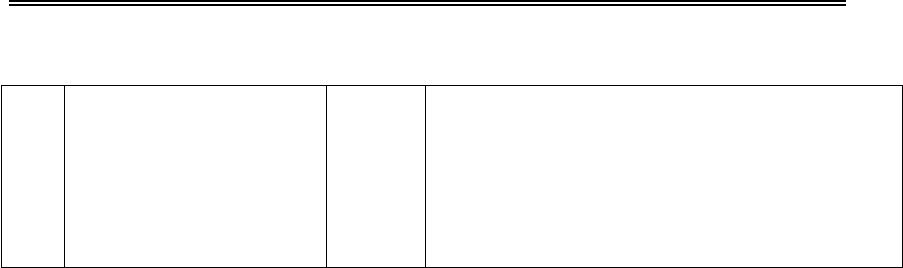

Example 2

Richard works as a plasterer for B Co, a building company, on a labour only basis. He

is paid on a daily basis. He takes his instructions from the site foreman. Richard is not

free to provide someone else to perform his duties.

Five Step Framework

No.

Question

Answer

Explanation

1

Work/wage bargain

Yes

Richard is paid a set daily fee to undertake

work

2

Personal Service

Yes

Richard cannot send someone else instead

3

Control

Yes

The site foreman, on behalf of B Co, tells

Richard where, when and what to do. As a

skilled tradesman, the foreman does not

direct him how to do the work but this is the

only element of the work which is controlled

by Richard.

4

All the circumstances of

the employment

Yes

The contract of engagement is drafted as a

self-employment contract with payments

made to Richard reported through the RCT

portal by B Co. The facts of the case do not

support this position. In addition to the facts

detailed under questions 1 to 3, Richard

cannot profit beyond his set weekly wage if he

does things more efficiently. He is insured as

an employee of B Co who include him in the

CIF pension scheme. The materials used by

Richard are provided by B Co.

5

Legislative context

N/A

There is no legislation that requires an

adjustment or supplement to any of the

questions above.

Richard will be an employee based on the relationship and PAYE should be applied

by B Co.

Tax and Duty Manual Part 05-01-30

36

Example 3

H Co, a company tax resident in Poland (note – similar position arises if H Co were

based in Ireland), provides a team of six scaffolders under contract to B Co on a

labour only basis. The scaffolders will be paid by H Co at a daily rate. The scaffolders

take their instructions from the site foreman of B Co. The individual scaffolders are

not free to provide someone else to perform their duties.

Similar to example 2, although B Co exercises a significant level of control over the

scaffolders, and the contract between H Co and B Co is for the scaffolders’ personal

service, engagements between two corporates can never be under a contract of

service, so B Co pays H Co for the six scaffolders under a contract for service.

We will now consider the contract between H Co and the scaffolders.

Five Step Framework

No.

Question

Answer

Explanation

1

Work/wage bargain

Yes

The scaffolders are paid a set daily fee to

undertake work.

2

Personal Service

Yes

The scaffolders cannot send someone else

instead

3

Control

Yes

The site foreman, on behalf of B Co, tells the

scaffolders where, when and what to do for H

Co. As the work is specialised, the foreman

does not direct them how to do it but this is

the only element of the work which is

controlled by them.

4

All the circumstances of

the employment

Yes

The contract of engagement is drafted as a

self-employment contract with payments

made to the scaffolders reported through the

RCT portal by H Co. The facts of the case do

not support this position. In addition to the

facts detailed under questions 1 to 3, the

scaffolder cannot profit beyond his set daily

wage if he does things more efficiently. The

tools used, including the scaffolding, is

provided by B Co as agreed in the contract

between B Co and H Co.

Tax and Duty Manual Part 05-01-30

37

5

Legislative context

N/A

There is no legislation that requires an

adjustment or supplement to any of the

questions above.

In the first instance, the individual scaffolders will be employees of H Co based on

the relationship and PAYE should be applied by H Co.

However, if B Co is paying the scaffolders, the obligation to deduct PAYE would fall to

B Co in the first instance.

Tax and Duty Manual Part 05-01-30

38

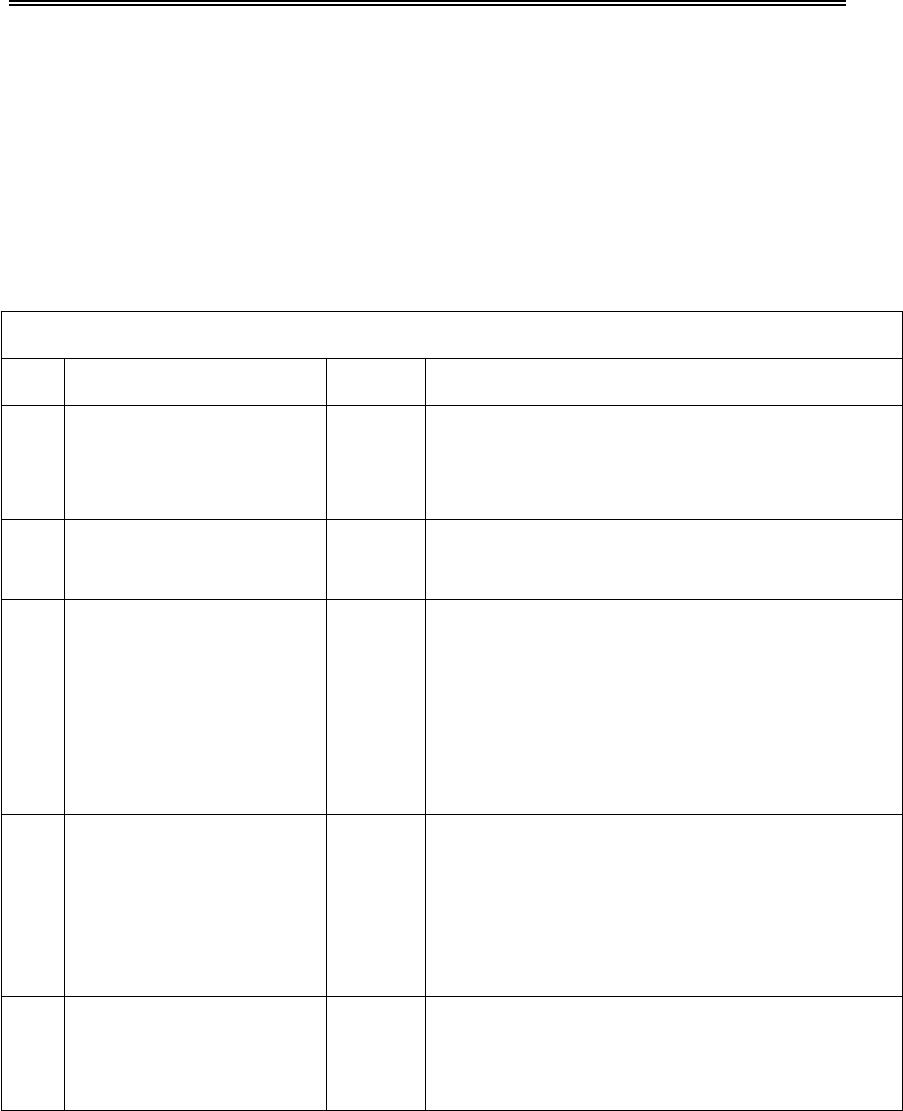

Example 4

Peter works as an electrician for B Co. He supplies labour, materials and his own

tools. He is paid a set fee to wire each house. He takes his instructions on what

house to wire next from the site foreman. There are no restrictions on who

undertakes the work Peter has been contracted to do.

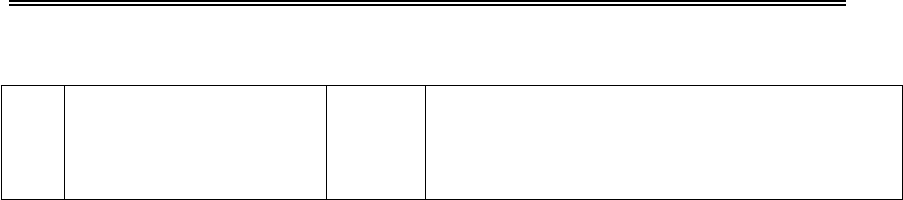

Five Step Framework

No.

Question

Answer

Explanation

1

Work/wage bargain

Yes

Peter is paid a fee to undertake work.

2

Personal Service

No

There are no restrictions on who does the

work so it’s not a ‘personal service’.

3

Control

4

All the circumstances of

the employment

5

Legislative context

As the answer was ‘No’ to one of the first three

questions, the contract is not indicative of an

employment contract, so the remainder of the questions

do not need to be considered.

Peter will be self-employed based on the relationship and PAYE should not be

applied by B Co. Payments made to Peter are reported through the RCT portal by B

Co with RCT deducted as necessary.

Tax and Duty Manual Part 05-01-30

39

Example 5

Michael is engaged by a telecommunications company, T Co, to undertake work,

building and installing new telecoms infrastructure, or repairing existing equipment.

He is paid a fee per project. He provides his own tools and safety clothing and if it is

provided by T Co, it is recharged back to him. He is assigned a body of work and is

free to bring someone else in to do the work on his behalf or assist him in

completing it on time. There are no restrictions on taking on other projects at the

same time or with competitors of T Co.

Five Step Framework

No.

Question

Answer

Explanation

1

Work/wage bargain

Yes

Michael is paid a fee to undertake work.

2

Personal Service

No

There is no personal service as there are no

restrictions on sending someone else to

undertake or assist with the work.

3

Control

N/A

While this test does not need to be examined,