OUTDATED

METHODOLOGY

RATING

METHODOLOGY

RESIDENTIAL MBS

OU

ME

RATING

METHODOLOG

Y

Table of Contents:

SCOPE 1

RATING APPROACH 2

ASSET-LEVEL ANALYSIS AND RELATED

MODELING 3

STRUCTURAL ANALYSIS AND LIABILITY

MODELING 6

OTHER CONSIDERATIONS 7

MONITORING 8

APPENDICES 9

MOODY’S RELATED PUBLICATIONS 16

Analyst Contacts:

FRANKFURT +49.69.70730.700

Steven Becker +49.69.70730.939

Vice President – Senior Anal

y

st

steven.becker@moodys.com

LONDON +44.20.7772.5454

Barbara Rismondo +44.20.7772.5448

Senior Vice President/Manager

barbara.rismondo@moodys.com

» contacts continued on the second to last page

CLIENT SERVICES:

Americas: +1.212.553.1653

J

apan: +81.3.5408.4100

EME

A: +

44.20.7772.5454

Asia-Pacific

: +

852.3551.3077

DECEMBER 20, 2022

Reverse Mortgage Securitizations

Methodology

This rating methodology replaces Reverse Mortgage Securitizations Methodology published in

April 2020. We clarified how we apply our home price decline assumptions, and we made

editorial updates to enhance readability.

Scope

This rating methodology applie

s

s to securities backe

d

d b

y

y revers

e

e mortgag

e

e loans.

In this methodology, we explain our approach to assessing credit risks for reverse mortgage

securitizations, including quantitative and qualitative factors that are likely to affect rating

outcomes in this sector.

We discuss the asset and liability analysis, including associated modeling, as well as other

considerations. We also describe our monitoring approach.

This methodology is no longer in effect. For information

on rating methodologies currently in use by

Moody’s Investors

Service, visit ˫˫̭˭

OUTDATED

METHODOLOGY

2 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Rating Approach

I

I

n

n thi

s

s section

,

, w

e

e summariz

e

e ou

r

r approac

h

h t

o

o assessin

g

g credi

t

t risk

s

s fo

r

r securitie

s

s backe

d

d b

y

y revers

e

e

mortgag

e

e loans

,

, includin

g

g quantitativ

e

e an

d

d qualitativ

e

e factor

s

s tha

t

t ar

e

e likel

y

y t

o

o affec

t

t ratin

g

g outcome

s

s i

n

n

thi

s

s sector

.

.

Asset Description

A reverse mortgage is a mortgage loan – usually secured by a residential property – in which the main

source of repayment is the proceeds from the sale of the underlying home or prepayment by the borrower.

The reverse mortgage, which lenders typically market to older borrowers, is typically due and repayable

either upon the death of the borrower or when the borrower moves out of the home. We refer to these as

maturity events. The loans can feature a bullet repayment for the whole loan, or a series of repayments, or

take the form of a revolving credit line. Interest usually accrues until the loan is repaid. For certain product

types, the borrower agrees instead to sell a portion (or all) of the home at a discount in return for a lump

sum payment. The lender or buyer then receives a portion (or all) of the proceeds when the home is sold.

Key Risks

The major risk for investors in a reverse mortgage securitization is a decline in home values such that when

the homes underlying the securitized loans are sold, the proceeds are insufficient to pay off the original loan

amount and any accrued interest. To account for this risk, the main variable that we consider in our analysis

is the future price movement of the underlying homes in the asset pool. Since each loan’s maturity is

uncertain, the interest that can accrue and the exposure to home price movements are also uncertain.

Consequently, we also analyze the factors that can affect the loan maturity dates, such as expected

mortality rates for borrowers and the likelihood of moving out of the home before death.

In addition, cash flows are highly uncertain because reverse mortgages do not have regularly scheduled

payments. Consequently, we assess the extent to which the transaction’s assets or reserve funds provide

sufficient cash to make the required payments on the securities and transaction fees. In our assessment, we

incorporate any additional risk that might arise if the securities have a variable interest rate.

To analyze the risks, we stress each of the related variables to levels we deem consistent with the target

rating on the securities, applying greater stress to the risk variables the higher the rating. We use a cash flow

model of the transaction to determine whether investors would be paid in full in the stress scenario. The

cash flow model generally represents how the transaction allocates cash flows from the assets, credit

enhancement, and hedging vehicles among the various transaction participants, as well as how it allocates

asset losses. It also models how triggers within the transaction change those allocations.

In determining our ratings, we may also consider the results from other stressed combinations of the risk

variables to account for idiosyncrasies in a particular transaction, such as correlations across the variables or

concentrations among the assets. Model outputs derived by our quantitative modeling are important

considerations in our rating committee process. However, the ratings assigned by the rating committee also

incorporate a variety of qualitative factors, including operational, counterparty and legal risks, as well as

underwriting and servicing practices. As a result, the assigned rating may differ from the model output.

This publication does not

announce a credit rating action.

For any credit ratings referenced in

this publication, please see the

issuer/deal page on

ratings.moodys.com for the most

updated credit rating action

information and rating history.

OUTDATED

METHODOLOGY

3 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Asset-level Analysis and Related Modeling

I

I

n

n thi

s

s section

,

, w

e

e explai

n

n ho

w

w w

e

e analyz

e

e th

e

e underlyin

g

g asset

s

s tha

t

t bac

k

k revers

e

e mortgag

e

e securitization

s

s

an

d

d ho

w

w w

e

e estimat

e

e potentia

l

l losse

s

s o

n

n thos

e

e assets

.

.

Home Price Risk

Repayment of a reverse mortgage loan depends on the net liquidation proceeds from the sale of the

property,

1

and thus our home price assumptions play a key role in our approach. In our scenarios, we

generally assume a decline in home prices occurs in the first year of the transaction and no decline for B2

(sf)-rated securities. Furthermore, we typically assume no price appreciation for Aaa (sf)-rated securities. For

outstanding transactions, the decline occurs the year of the review date.

Home Price Decline Assumptions

Home price decline is a more critical assumption for reverse mortgage-backed securities than for standard

residential mortgage-backed securities (RMBS) for two key reasons: unlike standard RMBS, where only

defaulted properties are liquidated, all properties with reverse mortgages - if not prepaid - are eventually

sold. In addition, the average life of a reverse mortgage transaction is much longer than an RMBS

transaction.

As a starting point for our Aaa (sf) home price decline assumptions, we apply a stress similar to one

applicable to a portfolio of residential mortgage loans under our country-specific asset modeling approach.

In the US, we typically use a fixed home price decline assumption similar to the one described in our US

RMBS methodology

2

and apply this assumption throughout the transaction’s life. For countries where the

home price decline assumption varies over time, we typically consider a “through-the-cycle” concept, i.e.,

an average stress decline over a long-term period, to maintain stability in that assumption. For B2 (sf)-rated

securities, we typically assume no price decrease in the first year. For securities with ratings ranging from

Aa2 (sf) to Ba2 (sf) as per the tables in Appendix A, the home price decline is typically based on an

interpolation of the stresses applied in Aaa (sf) and B2 (sf) scenarios. Our home price decline assumption

includes foreclosure costs.

We may apply a higher stress (at each rating level) for home price decline assumptions if there are specific

risks in the transaction or unusual concentrations in the reverse mortgage pool, such as geographic

concentrations, which make it more likely that a regional downturn could cause a significant decline in the

overall pool performance.

Our home price decline assumptions for reverse mortgages in a severe stress scenario could be higher than

the assumptions we use to rate standard RMBS transactions because of (1) the higher sensitivity to home

price declines in a reverse mortgage transaction since all of the properties need to be sold - if not prepaid;

(2) the potential selection bias in terms of borrower (borrowers who expect to live longer) and property type

(higher value properties); and (3) the uncertainty regarding the level of property maintenance. However, a

strong mitigant to the above factors is the lack of correlation in reverse mortgages between the timing of a

sale and the home price cycle. This contrasts with the correlation between severe home price declines and

higher defaults and subsequent foreclosures among residential mortgage borrowers. In addition, in reverse

mortgage transactions we conservatively apply the home price decline to the whole portfolio in the first

year of the transaction for the Aaa to Ba2 scenarios.

1

We typically index the property value at the analysis date.

2

For more information, see our methodology for rating US RMBS. A link to a list of our sector and cross-sector methodologies can be found in the “Moody’s Related

Publications” section.

OUTDATED

METHODOLOGY

4 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Home Price Appreciation Assumptions

We set the long-term assumption for home price appreciation at zero for Aaa (sf)-rated securities. For B2

(sf)-rated securities, we typically apply a growth rate which is a stable approximation of our expected long-

term growth rate. For securities with ratings ranging from Aa2 (sf) to Ba2 (sf) as per the tables in Appendix

A, the growth rate is typically based on an interpolation of the appreciation applied in Aaa (sf) and B2 (sf)

scenarios. We may apply lower home price appreciation assumptions (at each rating level) if there are

specific risks in the transaction or in the reverse mortgage pool.

Our home price appreciation assumptions incorporate an expectation that the homes of reverse mortgage

borrowers will appreciate less on average than those of the population as a whole because of the following

factors:

» Reverse mortgage borrowers are relatively unlikely to repair or refurbish their homes given that part or

all of the upside in value will mostly benefit the reverse mortgage provider. A decline in the value of the

home will also not leave the borrower’s estate with unpaid mortgage debt (the debt would be

extinguished).

» In contrast with a traditional mortgage, the balance on a reverse mortgage rises over time, which

increases the likelihood that the homeowner’s equity stake will be wiped out, reducing the incentive to

maintain the home.

See Appendix A for our typical country-specific home price decline and appreciation assumptions. When

relevant, we may also consider alternative home price appreciation assumptions.

Reverse Mortgage Maturity

Reverse mortgages mature when the borrower dies or, in the case of co-borrowers, when both die (mortality

event). When the borrower moves into long-term care (morbidity event) or when the borrower repays the

loan (prepayment or mobility event), the reverse mortgage will also mature. For each mortgage in the pool,

we estimate the probability of maturity in each year after origination, taking these types of events into

account.

Timing of Mortality Events

We establish baseline assumptions for the timing of mortality events using the mortality rates compiled in

the country of the securitization, typically by the life insurance industry, to the extent that they are

available. Typically, the mortality rates are stratified by gender and age, allowing us to distinguish broadly

among types of borrowers in the pool. If data in a particular country are not available, we may use data

from comparable countries and adjust accordingly for possible discrepancies.

In light of their sociodemographics, we assume longer life expectancy for the population of borrowers that

use reverse mortgages than for the general population, but reasonably equivalent to that of a life insurance

annuitant population. Therefore, we may also adjust the data to account for likely differences between the

population reflected in the historical data and the borrowers in the pool.

Another factor that we account for is whether the mortgage has a single obligor or joint obligors. A reverse

mortgage maturity event caused by mortality is triggered by the death of the second individual in a couple.

Therefore, when there are joint borrowers, we calculate the mortality rate for the couple, which is the joint

probability of both obligors’ death. Consequently, near-term mortality rates for couples are considerably

lower than the mortality rates of individuals.

Our analysis of the likely mortality rates of the pool also incorporates expectations of changes in life

expectancies resulting from improvements in living standards and in healthcare technology and availability.

OUTDATED

METHODOLOGY

5 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

We typically assume in our analysis more improvement for higher-rated securities than for lower-rated

securities, resulting in greater longevity and, thus, a higher stress. See Appendix B for more information. In

addition, we may apply different improvement factors if the pool is concentrated in a specific cohort (for

example, in cases where all borrowers have similar ages).

Timing of Morbidity and Mobility Events

In our analysis, we distinguish between two sources of prepayments, which are influenced by different

factors and treated differently in reverse mortgage contracts. Borrowers who move to a long-term care

facility or nursing home due to health reasons (which is usually referred to as a morbidity event) typically do

not incur a prepayment penalty (i.e., properties are sold without additional costs) on a reverse mortgage,

while borrowers who move out for other reasons (usually referred to as a mobility event) can incur a

prepayment penalty. In addition, borrowers who prepay the reverse mortgage outside of these

circumstances can also incur a prepayment penalty. The most important factors determining the likelihood

of a health-related morbidity event are the age of the borrower(s) and whether there is a single borrower or

joint borrowers. For example, older borrowers are more likely to need the services of long-term care

facilities or nursing homes, and there is a higher likelihood that a single person will need those services than

both people in a joint-borrower mortgage. In contrast, older borrowers are less likely to move for non-

health-related reasons.

There is often little incentive for reverse mortgage borrowers to prepay their loans, causing a mobility event.

Typically, prepayments are highest in the early years of a transaction in instances where the borrower

decides that the reverse mortgage product was unsuitable. In addition, borrower mobility typically declines

with age. Higher home price appreciation rates can also result in higher prepayment rates as borrowers look

to withdraw equity from their homes to repay debts. Conversely, prepayments could fall as home prices

decline. Interest rate changes can also affect prepayment rates, with interest rate declines inducing some

fixed-rate borrowers to prepay their loans as they start shopping for lower rates.

We derive the prepayment and morbidity rates, which are typically low single-digit numbers, based on the

portfolio’s characteristics, the rating scenario and available market data. In our analysis, we may reduce the

prepayment and morbidity rates to zero when considering high rating scenarios and in cases where there is

not sufficiently reliable data or prepayment penalties are high.

Interest Rate Risk

Transactions with variable interest rates on either assets or liabilities or both are subject to interest rate risk.

For example:

» For transactions with floating-rate bonds and fixed rates on the mortgages, there is a risk that the

interest rates on the liabilities will rise.

3

» For transactions with variable rates on both assets and liabilities, there is a risk that the spread between

the interest rate on the assets and the rate on the securities will move adversely. In addition, even if the

spread between the rates remains constant, increases or decreases in the overall interest rate can

positively or negatively affect the credit quality of the transaction, depending on how home prices

move and the transaction structure.

» For transactions with variable rates on the assets (mortgages) and fixed rates on the securities, the risk

is that the interest rates on the assets will decline.

3

For more information, see our methodology for assessing counterparty risks in structured finance transactions. A link to a list of our sector and cross-sector

methodologies can be found in the “Moody’s Related Publications” section.

OUTDATED

METHODOLOGY

6 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Consequently, in transactions with variable rates, we review the results of the cash flow model assuming

various levels of interest rates to capture the appropriate risk.

In the base case, we generally assume an interest rate level based on the applicable home price growth rate

for each rating stress, while typically maintaining a fixed differential between long-term interest rates and

home price growth rates after the initial home price decline. For example, in our Aaa scenario where we

assume a severe home price decline with no recoveries, we generally assume a low interest rate of 1%

throughout the transaction’s life. See Appendix A for our typical country-specific interest rate and home

price growth rate stresses.

We use our stress assumptions for home price changes, the timing of maturity events, and interest rates on

the mortgages to estimate the probability-based cash flows that would be generated by each reverse

mortgage in the asset pool. We use the interest rates on the loans to generate the loan balance in each

future period and the timing of maturity events to calculate the probability-based portion of the loan

balance paid down each period. See Appendix C for an example of how we determine the cash flow from a

single hypothetical reverse mortgage.

Data for Collateral Analysis

To perform the collateral analysis described above, we typically receive loan-level data on loan balance,

borrower(s) age, gender, latest available property value, valuation type, property location, property type,

interest on the loan and other information specific to the loan product type.

Structural Analysis and Liability Modeling

I

I

n

n thi

s

s section

,

, w

e

e explai

n

n ho

w

w w

e

e analyz

e

e th

e

e structura

l

l feature

s

s o

f

f revers

e

e mortgag

e

e securitizations

,

,

includin

g

g ho

w

w w

e

e mode

l

l an

d

d allocat

e

e cas

h

h flow

s

s t

o

o differen

t

t classe

s

s o

f

f securities

,

, takin

g

g int

o

o accoun

t

t asse

t

t

cas

h

h flow

s

s an

d

d availabl

e

e credi

t

t support

.

.

Cash Flow Model

We combine the cash flows generated by the reverse mortgages in the asset pool with any cash flows

generated by hedging instruments in the securitization. We then use a model of the transaction that

incorporates how it allocates cash flows and losses, the triggers that change those allocations, the interest

rates on the securities, and the credit enhancement (including guarantees)

4

to determine whether those

cash flows would be sufficient to pay investors in full and on a timely basis. The model output corresponds

to the rating consistent with the most stressful scenario the security could withstand without any losses.

Additionally, we also account for the potential loss severity of a tranche in relation to its thickness when

determining the rating.

Liquidity Risk

There are no regularly scheduled payments on reverse mortgages, but the payments of interest and

sometimes principal on the structured securities are due regularly. Consequently, in our analysis, we assess

the extent to which there will likely be sufficient cash flow from the assets (in the stress scenarios) and from

other sources (such as reserve funds) to pay interest and mandatory scheduled principal when relevant on

the securities. To assess the other sources of cash required in the transaction, we consider the consequences

of missed payments for each class of securities, as well as the likelihood and potential length of interest

payment deferral. In addition, we consider in our analysis whether there are mechanisms in place to

4

For special considerations regarding home equity conversion mortgages (HECMs) guaranteed by the Federal Housing Administration (FHA), see Appendix D.

OUTDATED

METHODOLOGY

7 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

replenish such reserve funds, if necessary. For securities with floating interest rates, we incorporate into our

analysis the risk that interest rates may rise over the life of the transaction to test that interest is paid

regularly even if the pool has not generated any cash.

5

Other Considerations

A

Alon

g

g wit

h

h ou

r

r asset

,

, structura

l

l an

d

d liabilit

y

y analysis

,

, w

e

e conside

r

r othe

r

r quantitativ

e

e an

d

d qualitativ

e

e factor

s

s

i

n

n ou

r

r credi

t

t analysi

s

s suc

h

h a

s

s transactio

n

n counterparties

,

, lega

l

l risks

,

, reliabilit

y

y an

d

d completenes

s

s o

f

f

historica

l

l an

d

d portfoli

o

o data

,

, an

d

d environmental

,

, socia

l

l an

d

d governanc

e

e (ESG

)

) considerations

.

.

Counterparty Risks

We consider various counterparty-related risks at different stages throughout our credit analysis. More

specifically, the risks we consider include hedge counterparties and operational risks.

6

Based on our review,

we may adjust our assumptions, inputs or model results. If information is limited, we may also adjust the

rating level.

Hedge Counterparties

We analyze the rating impact of exposures to hedge counterparties including assessing the probability of a

transaction becoming unhedged and deriving additional potential losses. As part of our analysis, we may

conclude that we adjust the ratings to reflect the linkage and additional loss.

Operational Risk

Operational risks can arise from various potential sources, including disruption to cash flows caused by the

financial distress of a service provider to a reverse mortgage securitization. As part of our analysis, we

consider the financial disruption risk and the roles of relevant transaction parties.

Similar to other RMBS asset classes, our servicer quality analysis in reverse mortgage transactions addresses

the impact of servicer practices on the performance of the mortgage pool.

7

Reverse mortgages also pose

unique servicing challenges. Unlike traditional mortgage transactions, reverse mortgage transactions do not

require the servicer to process payments or make collection calls. Its responsibilities instead generally

include determining each property’s occupancy status (to determine if a maturity event has occurred),

updating the property values using a desktop or indexed valuation (generally when the borrower defaults)

and ensuring that payment of insurance is current. We update this assessment as necessary as we monitor

transactions and incorporate our views on the servicer’s quality.

Legal Risks

We assess legal risks that may affect the expected losses posed to investors. In particular, we consider the

potential legal consequences of whether the issuer is bankruptcy remote. We review legal opinions at

closing to inform our views on the key legal risks identified in a transaction.

Our legal analysis focuses on the risks posed by the potential bankruptcy of the transaction originator,

securitization entity, servicer and other relevant parties. We also consider the consumer protection laws and

regulations applicable to the reverse mortgage loans, the obligors and the originators. For example,

5

For more information, see Appendix A.

6

For more information, see our methodology for assessing counterparty risks in structured finance transactions. A link to a list of our sector and cross-sector

methodologies can be found in the “Moody’s Related Publications” section.

7

For more information, see our methodology for assessing counterparty risks in structured finance transactions. A link to a list of our sector and cross-sector

methodologies can be found in the “Moody’s Related Publications” section.

OUTDATED

METHODOLOGY

8 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

borrowers or heirs could challenge mortgage agreements, and aggressive cross-marketing of other financial

products, such as long-term annuities, could pose legal or reputational risks.

Data Quality Evaluation

We assign ratings to securities issued by reverse mortgage securitization when we have sufficient

information from reliable sources. Data quality is also important throughout the life of a reverse mortgage

transaction.

8

Environmental, Social and Governance Considerations

Environmental, social and governance (ESG) considerations may affect the ratings of securities backed by a

portfolio of reverse mortgage loans. We evaluate the risk following our cross-sector methodology that

describes our general principles for assessing these ESG issues

9

and may incorporate it in our analysis.

Monitoring

I

I

n

n thi

s

s section

,

, w

e

e describ

e

e ou

r

r approac

h

h whe

n

n monitorin

g

g transactions.

We generally apply the key components of the approach described in this methodology when monitoring

transactions, except for those elements of the methodology that could be less relevant over time, for

example some elements of a legal risk.

We receive periodic information for the purpose of monitoring the transaction. More specifically, we track

portfolio and loan-level information as well as information relating to the capital structure and credit

enhancement.

10

We may also gather updated information on other factors such as annual life improvement

factors, changes in house prices and foreclosure costs. The starting point is typically the monitoring of the

collateral performance relative to our initial expectations.

Our monitoring analysis may also include ongoing assessment of any entity whose ability to fulfill its

contractual obligation to the transaction could affect the cash flows that investors receive. Typically, those

entities would include the servicer, swap counterparties and credit support providers. Changes in the

financial stability of an entity could affect the credit quality of the securities. As pools season and borrowers

become older, the servicer’s role, in particular, becomes more important; for example, through active

monitoring of the properties’ occupancy status. We will reassess servicer quality as necessary as we monitor

transactions.

We may, at times, ask for additional information to adequately monitor our ratings.

11

8

For more information, see our approach to evaluating date quality in structured finance transactions. A link to a list of our sector and cross-sector methodologies can be

found in the “Moody’s Related Publications” section.

9

For more information, see our methodology that describes our general principles for assessing ESG issues. A link to a list of our sector and cross-sector methodologies

can be found in the “Moody’s Related Publications” section.

10

For example, in methodologies where models are used, modeling is not relevant when it is determined that (1) a transaction is still revolving and performance has not

changed from expectations, or (2) all tranches are at the highest achievable ratings and performance is at or better than expected performance, or (3) key model inputs

are viewed as not having materially changed to the extent it would change outputs since the previous time a model was run, or (4) no new relevant information is

available such that a model cannot be run in order to inform the rating, or (5) our analysis is limited to asset coverage ratios for transactions with undercollateralized

tranches, or (6) a transaction has few remaining performing assets.

11

For more information on our guidelines for assessing data quality in global structured finance transactions, a link to a list of our sector and cross-sector methodologies

can be found in the “Moody’s Related Publications” section.

OUTDATED

METHODOLOGY

9 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Appendix A: Assumptions for Home Prices and Interest Rates

The following tables illustrate the home price decline, home price growth rate and interest rate assumptions

we typically apply in the US, UK and Australia for different rating categories.

EXHIBIT 1

UK Assumptions for Home Price and Interest Rates

Target Rating Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

Home price decline over 1 year 35%* 25% 20% 15% 10% 0%

Growth rate after 1 year 0% 1.5% 2.0% 2.5% 3.0% 3.0%**

Home price returns to level at the

time of analysis

Never 20.5 years 12.5 years 8 years 5 years N/A

Interest rate level 1% 2.5% 3.0% 3.5% 4.0% 4.0%

* This is based on the country-specific home price decline assumption we use when analyzing residential mortgage loan portfolios, although

considering a “through-the-cycle” concept. The assumed home price decline of 35% over 1 year may be adjusted if deemed appropriate (e.g., to

reflect portfolio concentrations or transaction-specific risks). For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the home price decline is

typically based on an interpolation of the stresses applied in a Aaa (sf) and B2 (sf) scenarios.

** For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the growth rate is typically based on an interpolation of the stresses applied in a Aaa

(sf) and B2 (sf) scenarios.

Source: Moody’s Investors Service

EXHIBIT 2

US Assumptions for Home Price and Interest Rates (Active Reverse Mortgages)

Target Rating Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

Home price decline over 1 year 30%* 25% 20% 15% 10% 0%

Growth rate after 1 year 0% 1.5% 2.0% 2.5% 3.0% 3.0%**

Home price returns to level at the

time of analysis

Never 20.5 years 12.5 years 8 years 5 years N/A

Interest rate level 1% 2.5% 3.0% 3.5% 4.0% 4.0%

* This is based on the country-specific home price decline assumption we use when analyzing residential mortgage loan portfolios. The assumed

home price decline of 30% (for a diversified portfolio) over 1 year may be adjusted if deemed appropriate (e.g., to reflect portfolio concentrations

or transaction-specific risks). For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the home price decline is typically based on an

interpolation of the stresses applied in a Aaa (sf) and B2 (sf) scenarios.

** For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the growth rate is typically based on an interpolation of the stresses applied in a Aaa

(sf) and B2 (sf) scenarios.

Source: Moody’s Investors Service

EXHIBIT 3

Australia Assumptions for Home Price and Interest Rates

Target Rating Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

Home price decline over 1 year 40%* 32% 24% 16% 8% 0%

Growth rate after 1 year 0% 1% 1.5% 2% 2.5% 2.5%**

Home price returns to level at the

time of analysis

Never 40 years 19 years 10 years 4 years N/A

Interest rate level 1% 2% 2.5% 3% 3.5% 3.5%

* This is based on the country-specific home price decline assumption we use when analyzing residential mortgage loan portfolios, although

considering a” through-the-cycle” concept. The assumed home price decline of 40% over 1 year may be adjusted if deemed appropriate (e.g., to

reflect portfolio concentrations or transaction-specific risks). For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the home price decline is

typically based on an interpolation of the stresses applied in a Aaa (sf) and B2 (sf) scenarios.

** For securities with ratings ranging from Aa2 (sf) to Ba2 (sf), the growth rate is typically based on an interpolation of the stresses applied in a Aaa

(sf) and B2 (sf) scenarios.

Source: Moody’s Investors Service

OUTDATED

METHODOLOGY

10 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

When relevant, we may also consider alternative scenarios to determine the sensitivity of our ratings to

various assumptions.

We may also review the results of liquidity stress scenarios assuming higher interest rate levels. In such

scenarios, we assess the extent to which the transaction characteristics and other cash sources can provide

sufficient cash flow to pay interest on the securities.

OUTDATED

METHODOLOGY

11 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Appendix B: Application of Ratings-Based Longevity Improvement Stresses

We established the following approach to estimating future mortality improvements in the US, UK and

Australia from their historical mortality improvement rates and based on the opinion of external longevity

experts. We will develop similar approaches for other countries as the need arises, based on the information

available in those countries.

Base-Case Scenario: Annual Improvement Factor Approach

We apply annual mortality improvement factor stresses based on rating levels and current age. Exhibits 4

and 6 illustrate the typical improvement factor stresses. For the Aaa (sf) scenario, we generally assume a 5%

annual mortality improvement in the US, while in the UK and Australia, we assume a 7.5% mortality

improvement for ages 60-69 and 5% for ages 70 and higher. We also cap the borrower age at 120.

EXHIBIT 4

US: Assumptions for Mortality Improvement Factor Stress

Age Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

60-120 5.0% 4.0% 3.0% 2.0% 1.5% 1.5%

Source: Moody’s Investors Service

EXHIBIT 5

UK and Australia: Assumptions for Mortality Improvement Factor Stress

Age Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

60-69 7.5% 6.5% 5.5% 4.5% 3.5% 3.5%

70-120 5.0% 4.0% 3.0% 2.0% 1.5% 1.5%

Source: Moody’s Investors Service

Sensitivity Scenario: Age-Setback Approach

We may also apply an age-setback approach to determine the reasonableness of our baseline scenario for

future improvement in expected life. In this case, we will not apply any improvement factor stresses. In the

Aaa (sf) scenario, we typically use an age setback of 10 years, which effectively means that a 70-year-old is

assumed to have the mortality rates of a 60-year-old, and hence increases the expected life.

EXHIBIT 6

Age-Setback Approach for the US, the UK and Australia

Aaa (sf) Aa2 (sf) A2 (sf) Baa2 (sf) Ba2 (sf) B2 (sf)

10 years 8 years 6 years 4 years 2 years 2 years

Source: Moody’s Investors Service

OUTDATED

METHODOLOGY

12 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Appendix C: Illustrative Example of Determining Cash Flow for a Sample Reverse

Mortgage

The following is an example of how we determine the cash flow from a sample reverse mortgage, taking

into account expected improvements in mortality rates. We calculate the maturity event rate which

represents the probability that a loan is repaid in a given year, with repayment triggered by the death of any

remaining obligors.

Define:

»

t

as the number of years since the date of our analysis.

» ݍ

(

ݐ

)

as the one year probability of death t years in the future for an individual who has survived

through year t-1.

In our example below, the individual who is the remaining obligor has lived up to age 60, so q(1) is the

probability of death in the 61

st

year of age (given that the individual has lived to age 60). Likewise, q(2) is the

probability of death in the 62

nd

year of age, conditional on the individual having lived to age 61, and so on.

» ܫܨ as the improvement factor that represents the annual rate of improvement in mortality of an

individual, or equivalently, the reduction in the conditional one year mortality rate q(t).

» ݏ

(

ݐ

)

= ൫1 െݍ

(

ݐ

)

൯כݏ(ݐെ1) as the probability that the individual is still alive after a period of t years

following the date of our analysis, with ݏ

(

0

)

=1.

»

(

ݐ

)

= ݍ

(

ݐ

)

כݏ(ݐെ1) as the maturity event rate, i.e., the probability that the individual will repay (by

way of death) t years following the date of our analysis. We assume that Σ p(t) =1.

» ܳ

(

ݐ

)

= ݍ

(

ݐ

)

כ (1 െܫܨ)^(ݐെ1) as the adjusted conditional one year probability of death ݍ

(

ݐ

)

after

accounting for the improvement factor IF.

» ܵ

(

ݐ

)

= [1െܳ(ݐ)] כܵ(ݐെ1) as the adjusted probability that the individual is still alive after a period

of t years following the date of our analysis, after accounting for the improvement factor IF, with

ܵ

(

0

)

=1.

» ܲ

(

ݐ

)

=

Q(t)*S(t-1)

as the maturity event rate adjusted for the improvement factor IF.

The exhibit below shows how we calculate the maturity event rates p(t) and P(t) using both 0% and 2%

improvement factors:

12

12

For this example, we will use ݍ

(

ݐ

)

based on the years 2015-2017 from the UK Office for National Statistics. We typically use individual annuity mortality tables from the

Society of Actuaries for the US and from the Bureau of Statistics for Australia.

OUTDATED

METHODOLOGY

13 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

EXHIBIT 7

Maturity Event Rates

No mortality improvement:

IF equal to 0%

Adjusted

conditional prob

of death assuming

IF equal to 2%

Mortality improvement:

IF equal to 2%

t

q(t)

s(t) = [1- q(t)] *

s(t-1)

p(t) = q(t) *

s(t-1)

Q(t) = q(t)*

(1-IF)^(t-1)

S(t) = [1 - Q(t)]

*S(t-1)

P(t) = Q(t) *

S(t-1)

1 0.7955% 99.20% 0.80% 0.80% 99.20% 0.80%

2 0.8614% 98.35% 0.85% 0.84% 98.37% 0.84%

3 0.9324% 97.43% 0.92% 0.90% 97.49% 0.88%

4 1.0484% 96.41% 1.02% 0.99% 96.52% 0.96%

5 1.1447% 95.31% 1.10% 1.06% 95.51% 1.02%

6 1.2244% 94.14% 1.17% 1.11% 94.45% 1.06%

7 1.3496% 92.87% 1.27% 1.20% 93.32% 1.13%

8 1.4599% 91.51% 1.36% 1.27% 92.14% 1.18%

9 1.5607% 90.09% 1.43% 1.33% 90.91% 1.22%

10 1.7228% 88.53% 1.55% 1.44% 89.61% 1.31%

Source: Moody’s Investors Service

Assuming the following property and loan characteristics:

» Loan balance on the date of our analysis (LB(0)) = £ 150,000

» Property value on the date of our analysis (PV(0)) = £ 300,000

» Fixed interest rate (r) = 5%

» HPI growth rate (HPI rate) = 2%

The exhibit below shows a simplified example of how we determine the probability-based cash flows from a

reverse mortgage:

EXHIBIT 8

Reverse Mortgage Cash Flow Calculations

t Property Value Loan Balance Cash flow assuming IF 0% Cash flow assuming IF 2%

PV(0) * (1+HPI rate)^t LB(0) * (1+r)^t min(PV(t), LB(t)) * p(t) min(PV(t), LB(t)) * P(t)

1 £306,000 £157,500 £1,253 £1,253

2 £312,120 £165,375 £1,413 £1,385

3 £318,362 £173,644 £1,592 £1,530

4 £324,730 £182,326 £1,862 £1,754

5 £331,224 £191,442 £2,113 £1,951

6 £337,849 £201,014 £2,346 £2,125

7 £344,606 £211,065 £2,682 £2,383

8 £351,498 £221,618 £3,005 £2,621

9 £358,528 £232,699 £3,324 £2,847

10 £365,698 £244,334 £3,792 £3,191

Source: Moody’s Investors Service

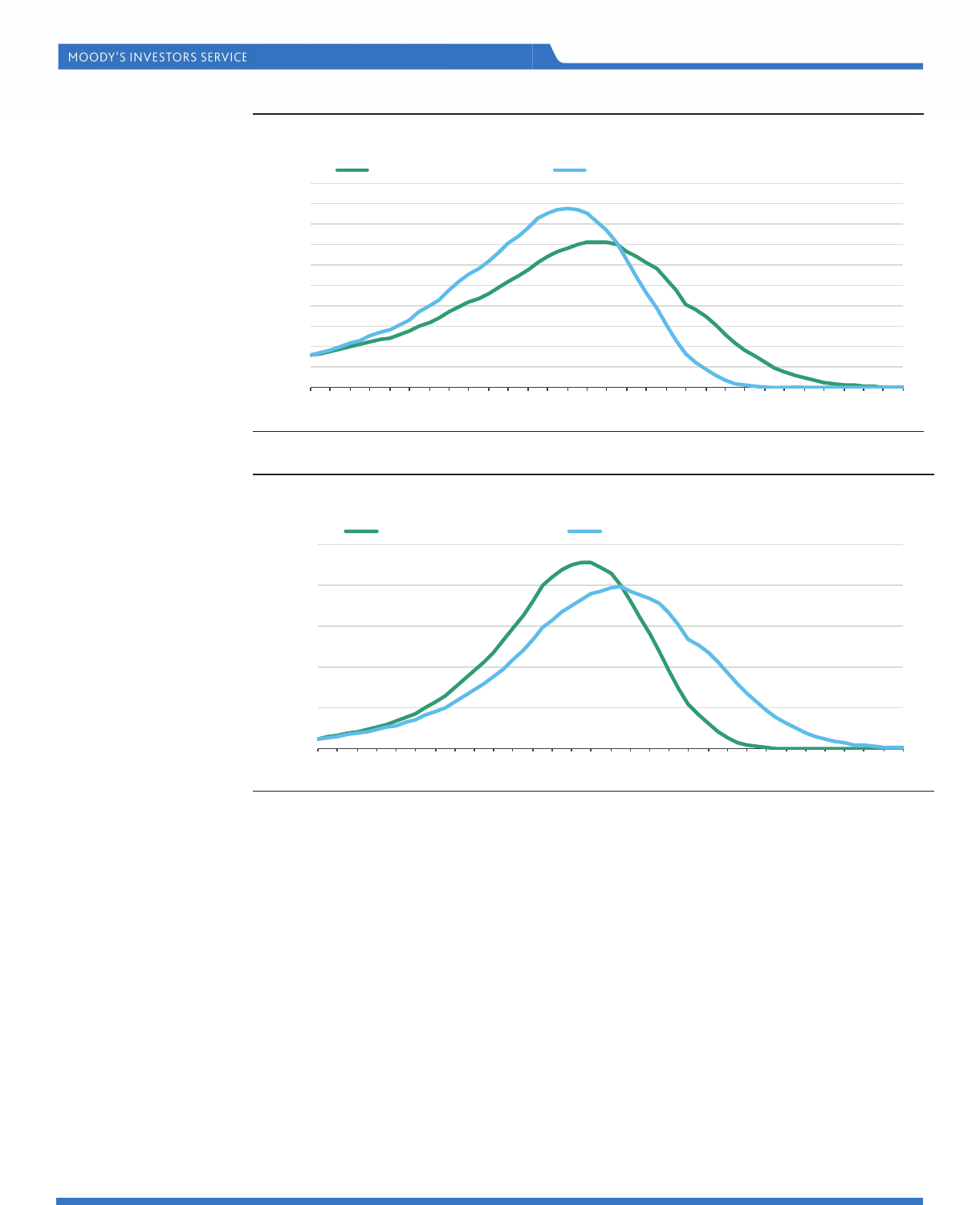

The two exhibits below show the maturity event rates and the cash flow per period, with and without the

improvement factor.

OUTDATED

METHODOLOGY

14 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

EXHIBIT 9

Comparison of Maturity Event Rates (with and without improvement factor)

Source: Moody’s Investors Service

EXHIBIT 10

Comparison of Cash Flow per Period (with and without improvement factor)

Source: Moody’s Investors Service

0. 00%

0. 50%

1. 00%

1. 50%

2. 00%

2. 50%

3. 00%

3. 50%

4. 00%

4. 50%

5. 00%

1 3 5 7 9 1113151719212325272931333537394143454749515355575961

Maturity event rate

Years since the analysis date

Maturity event rate assuming 2% IF Maturity event rate assuming no IF

£0

£5 ,0 00

£1 0, 000

£1 5, 000

£2 0, 000

£2 5, 000

135791113151719212325272931333537394143454749515355575961

Cash flow per period

Years since the anal ysi s date

Cash flow p er perio d assuming no IF Cash Flow per perio d a ssumi ng 2% I F

OUTDATED

METHODOLOGY

15 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Appendix D: Special Considerations for FHA-Guaranteed HECMs in the US

Home equity conversion mortgages are a type of reverse mortgage in the US that is guaranteed by the

Federal Housing Administration (FHA). The FHA guarantees any deficiency between the loan balance and

the home value, as long as the home is sold within six months of entering real-estate-owned (REO) status.

13

If the servicer does not sell the home within six months of it entering REO status, the FHA requires that the

servicers obtain an appraisal of the property from a Department of Housing and Urban Development (HUD)

approved appraiser, and the FHA will only guarantee the deficiency up to the appraisal value. Therefore, if

the home is subsequently sold for less than the appraisal value, the FHA covers the difference between the

outstanding value of the loan and the appraisal value, but the securitization suffers a loss equal to the

difference between the appraisal value and the actual sale price of the home.

Therefore, to analyze the loss potential of HECMs, we assess the following factors:

» The extent to which a home is likely to have positive equity in each period after origination, using our

stress assumptions for the timing of maturity events, home price changes, and the interest rates on the

mortgages

» The likelihood that a home will not sell within six months of entering REO status

» The likely shortfall between the appraisal value (determined in the HUD-mandated appraisal conducted

six months after entering REO) and the sale price of the home

» One-third of the costs of foreclosure that is unreimbursed by HUD

Typically, we assume that 85% of HECMs with negative equity will not be sold within the six-month REO

window and will therefore be subject to the FHA-mandated appraisal. Our assumptions regarding the likely

shortfall between the appraisal value and the sale price of the home is ratings-based, as Exhibit 11 shows.

We also generally assume that the cost of foreclosure on each liquidated property will be close to historical

average values.

EXHIBIT 11

Assumed Shortfalls Between Home Sale Prices and Appraisal Values for FHA-Mandated Appraisals

Rating Level Assumed Shortfall Time Horizon

Aaa (sf) 20% Until Maturity

Aa2 (sf) 20% Until Maturity

A2 (sf) 20% 10 years and 0% thereafter

Baa2 (sf) 20% 5 years and 0% thereafter

Ba2 (sf) 20% 3 years and 0% thereafter

B2 (sf) 20% 2 years and 0% thereafter

Source: Moody’s Investors Service

13

A reverse mortgage typically enters REO status if it does not sell in a foreclosure sale, which usually takes place six months after the mortgage becomes due.

OUTDATED

METHODOLOGY

16 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Moody’s Related Publications

Credit ratings are primarily determined through the application of sector credit rating methodologies.

Certain broad methodological considerations (described in one or more cross-sector rating methodologies)

may also be relevant to the determination of credit ratings of issuers and instruments. A list of sector and

cross-sector credit rating methodologies can be found here.

For data summarizing the historical robustness and predictive power of credit ratings, please click here.

For further information, please refer to Rating Symbols and Definitions, which is available here.

OUTDATED

METHODOLOGY

17 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

» contacts continued from page 1

Analyst Contacts:

NEW YORK +1.212.553.1653

Padma Ra

j

a

g

o

p

al +1.212.553.7997

Vice President - Senior Credit Officer/Mana

g

er

padma.rajagopal@moodys.com

Yehudah Forster +1.212.553.7995

Senior Vice President – Structured Finance Legal

Review

y

Karandee

p

Bains +1.212.553.1441

Senior Vice President / Mana

g

er

karandeep.bain[email protected]

UTDATED

ODO

SYDNEY +61.2.9270.8100

J

ac

q

ui Dred

g

e +61.2.9270.1422

A

ssistant Vice President - Anal

y

st

j

Il

y

a Serov +61.2.9270.8162

A

ssociate Mana

g

in

g

Director

OUTDATED

METHODOLOGY

18 DECEMBER 20, 2022 RATING METHODOLOGY: REVERSE MORTGAGE SECURITIZATIONS

RESIDENTIAL MBS

Author

Pier Paolo Vaschetti

Report Number: 1345695

ADDITIONAL CONTACTS:

Frankfurt: +49.69.2222.7847

Madrid: +34.91.414.3161

Milan: +39.02.3600.6333

Paris: +33.1.7070.2229

© 2022 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S CREDIT RATINGS AFFILIATES ARE THEIR CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT

COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MATERIALS, PRODUCTS, SERVICES AND INFORMATION PUBLISHED BY MOODY’S (COLLECTIVELY,

“PUBLICATIONS”) MAY INCLUDE SUCH CURRENT OPINIONS. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL

OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT OR IMPAIRMENT. SEE APPLICABLE MOODY’S RATING SYMBOLS AND

DEFINITIONS PUBLICATION FOR INFORMATION ON THE TYPES OF CONTRACTUAL FINANCIAL OBLIGATIONS ADDRESSED BY MOODY’S CREDIT RATINGS. CREDIT RATINGS

DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS, NON-CREDIT

ASSESSMENTS (“ASSESSMENTS”), AND OTHER OPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S

PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S

ANALYTICS, INC. AND/OR ITS AFFILIATES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE

INVESTMENT OR FINANCIAL ADVICE, AND MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT AND DO NOT PROVIDE

RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS DO

NOT COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS, ASSESSMENTS AND OTHER OPINIONS

AND PUBLISHES ITS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND

EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS,

,

ASSESSMENTS, OTHER OPINIONS, AND PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND

INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS, ASSESSMENTS, OTHER OPINIONS OR PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN

DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER.

ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW, AND NONE OF SUCH INFORMATION MAY BE COPIED OR

OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTED OR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH

PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANY PERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

MOODY’S CREDIT RATINGS,

,

ASSESSMENTS, OTHER OPINIONS AND PUBLICATIONS ARE NOT INTENDED FOR USE BY ANY PERSON AS A BENCHMARK AS THAT TERM IS DEFINED FOR

REGULATORY PURPOSES AND MUST NOT BE USED IN ANY WAY THAT COULD RESULT IN THEM BEING CONSIDERED A BENCHMARK.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as well as other factors,

however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information it uses in assigning a credit rating is

of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However, MOODY’S is not an auditor and cannot in every

instance independently verify or validate information received in the rating process or in preparing its Publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for any indirect, special,

consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information, even if

MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses or damages, including but not limited to:

(a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of a particular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatory losses or

damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for the avoidance of doubt, by

law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers,

arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY CREDIT RATING,

ASSESSMENT, OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (including corporate and

municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any credit rating, agreed to pay to Moody’s

Investors Service, Inc. for credit ratings opinions and services rendered by it fees ranging from $1,000 to approximately $5,000,000. MCO and Moody’s Investors Service also maintain policies

and procedures to address the independence of Moody’s Investors Service credit ratings and credit rating processes. Information regarding certain affiliations that may exist between directors of

MCO and rated entities, and between entities who hold credit ratings from Moody’s Investors Service and have also publicly reported to the SEC an ownership interest in MCO of more than 5%,

is posted annually at www.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s Investors Service Pty

Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intended to be provided only to

“wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, you represent to MOODY’S that you are, or

are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to

“retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer, not on the

equity securities of the issuer or any form of security that is available to retail investors.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’s Overseas

Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a Nationally Recognized Statistical

Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by an entity that is not a NRSRO and,

consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registered with the Japan Financial Services Agency

and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by

MJKK or MSFJ (as applicable) have, prior to assignment of any credit rating, agreed to pay to MJKK or MSFJ (as applicable) for credit ratings opinions and services rendered by it fees ranging from

J

PY100,000 to approximately JPY550,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.