1

ODISHA ELECTRICITY REGULATORY COMMISSION

BIDYUT NIYAMAK BHAWAN

PLOT NO. 4, CHUNOKOLI, SHAILASHREE VIHAR,

BHUBANESWAR-751021

************

Present : Shri G. Mohapatra, Member

Shri S. K. Ray Mohapatra, Member

CASE NOS. 82, 83, 88 & 80 of 2022

DATE OF HEARING : 24.02.2023 at 11.00 A.M (TPSODL),

27.02.2023 at 11.00A.M (TPNODL),

28.02.2023 at 11.00A.M (TPCODL)

04.03.2023 at 11.00 A.M (TPWODL)

DATE OF ORDER 23.03.2023

IN THE MATTER OF: Applications of Distribution Companies namely TPSODL,

TPNODL, TPCODL & TPWODL for approval of their

Aggregate Revenue Requirement (ARR), Wheeling Tariff

and Retail Supply Tariff for the FY 2023-24 under Sections

62,64 & 86 and other applied provisions of the Electricity

Act, 2003 read with relevant provisions of OERC (Terms and

Conditions for determination of Wheeling and Retail Supply

Tariff) Regulations, 2022 and OERC (Conduct of Business)

Regulations, 2004 and other Tariff related matters.

AND

CASE NOs. 86, 87, 89 & 85 of 2022

DATE OF HEARING : 24.02.2023 at 11.00 A.M (TPSODL),

27.02.2023 at 11.00A.M (TPNODL),

28.02.2023 at 11.00A.M (TPCODL)

04.03.2023 at 11.00 A.M (TPWODL)

IN THE MATTER OF: Applications for approval of Open Access Charges for FY 2023-

24 in accordance with OERC (Terms and Conditions of Intra-

State Open Access Charges) Regulations, 2020 for approval of

Wheeling Charges, Cross Subsidy Surcharge, Additional

Surcharge & Standby charges applicable to Open Access

Customers for use of intra-state transmission/ distribution

system in view of Section 42 of the Electricity Act, 2003 of

DISCOMs namely TPSODL, TPNODL, TPCODL & TPWODL.

AND

2

CASE NO. 06 of 2023

DATE OF HEARING : 24.02.2023 at 11.00 A.M (TPSODL)

IN THE MATTER OF: Application for approval of Truing up expenses for the period

of FY 2020-21(3 months) and for FY 2021-22 under Section

62& 86(1) and all other applicable provisions of the Electricity

Act, 2003 read with relevant provisions of OERC (Terms and

Conditions for determination of Wheeling and Retail Supply

Tariff) Regulations, 2022 and OERC (Conduct of Business)

Regulations, 2004 and other Tariff related matters.

AND

CASE NO. 84 of 2022

DATE OF HEARING : 27.02.2023 at 11.00 A.M (TPNODL)

IN THE MATTER OF: Application for approval of Truing up expenses for FY 2021-22

under Sections 62 & 86(1) and all other applicable provisions of

the Electricity Act, 2003 read with relevant provisions of OERC

(Terms and Conditions for determination of Wheeling and

Retail Supply Tariff) Regulations, 2022 and OERC (Conduct of

Business) Regulations, 2004 and other Tariff related matters.

AND

CASE NOs. 90 & 91 of 2022

DATE OF HEARING : 28. 02.2023 11.00 A.M (TPCODL)

IN THE MATTER OF: Application for approval of Truing up expenses for the period of

FY 2020-21 (June, 2020 to March, 2021) and for FY 2021-22

under Sections 62 & 86(1) and all other applicable provisions of

the Electricity Act, 2003 read with relevant provisions of OERC

(Terms and Conditions for determination of Wheeling and

Retail Supply Tariff) Regulations, 2022 and OERC (Conduct of

Business) Regulations, 2004 and other Tariff related matters.

AND

CASE NO. 81 of 2022

DATE OF HEARING : 04.03.2023 at 11.00 A.M (TPWODL)

IN THE MATTER OF: Application for approval of Truing up expenses for the period of

FY 2020-21 (3 months) and for FY 2021-22 under Sections 62 &

86(1) and all other applicable provisions of the Electricity Act,

2003 read with relevant provisions of OERC (Terms and

Conditions for determination of Wheeling and Retail Supply

Tariff) Regulations, 2022 and OERC (Conduct of Business)

Regulations, 2004 and other Tariff related matters.

3

AND

CASE NOS. 12, 10, 11 & 13 of 2023

DATE OF HEARING : 24.02.2023 at 11.00 A.M (TPSODL),

27.02.2023 at 11.00A.M (TPNODL),

28.02.2023 at 11.00A.M (TPCODL)

04.03.2023 at 11.00 A.M (TPWODL)

IN THE MATTER OF: Applications of Distribution Companies namely TPSODL,

TPNODL, TPCODL & TPWODL for approval of their

Business Plan for FY 2023-24 in compliance to OERC (Terms

and Conditions for determination of Wheeling and Retail

Supply Tariff) Regulations, 2022.

O R D E R

The Distribution Companies in Odisha namely TPSODL, TPNODL, TPCODL and

TPWODL are carrying out the business of distribution and retail supply of electricity in

their licensed areas as detailed below:

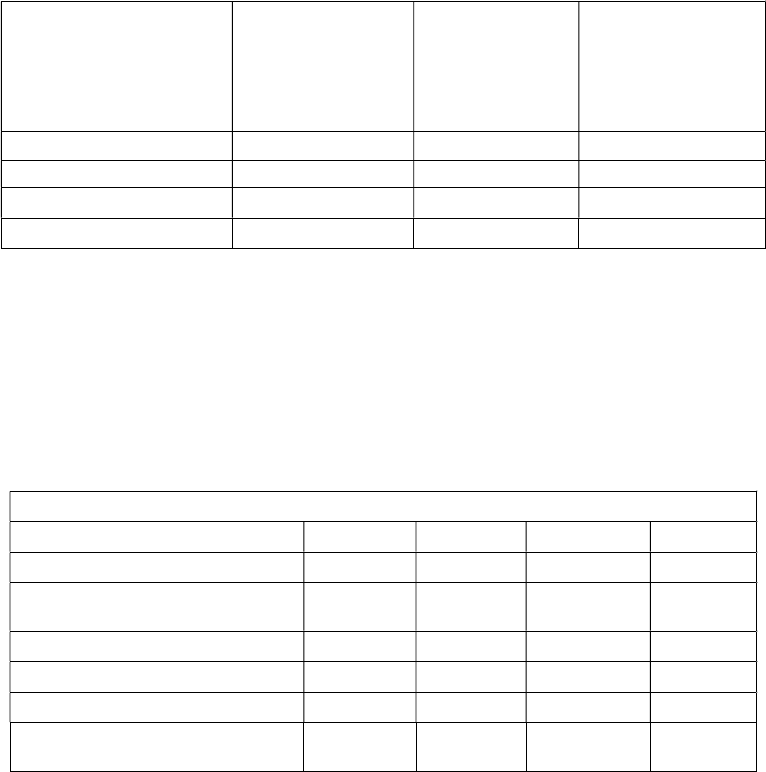

Table – 1

Sl.

No.

Name of

DISCOMS

Licensed Areas (Districts) %age area of

the State of

Odisha

1. TPSODL Ganjam, Gajapati, Kandhamal, Boudh, Rayagada, Koraput,

Nawarangpur and Malkanagiri.

30.8

2. TPNODL Mayurbhanj, Keonjhar, Bhadrak, Balasore and major part

of Jajpur.

18.0

3. TPCODL Puri, Khurda, Nayagarh, Cuttack, Denkanal, Jagatsinghpur,

Angul, Kendrapara and some part of Jajpur.

18.9

4. TPWODL Sambalpur, Sundargarh, Bolangir, Bargarh, Deogarh,

Nuapara, Kalahandi, Sonepur and Jharsuguda.

32.3

Odisha Total 100.0

The Commission initiated proceedings on the filing of Applications in respect of

Aggregate Revenue Requirement (ARR), Wheeling Tariff and Retail Supply Tariff

(RST) for FY 2023-24 of the aforesaid Distribution Companies under Sections 62, 64

& 86 and other related provisions of the Electricity Act, 2003 read with relevant

provisions of the OERC (Terms and Conditions for determination of Wheeling and

Retail Supply Tariff) Regulations, 2022 and the OERC (Conduct of Business)

Regulations, 2004 and other matters related to Tariff. All these above stated

Applications are disposed of by this common Order as follows:

4

A. PROCEDURAL HISTORY (PARA 2 TO 12)

2. After the revocation of licenses of distribution Utilities such as SOUTHCO, NESCO,

WESCO and CESU, the Commission under Section 21 of the Electricity Act, 2003 has

transferred the responsibilities of erstwhile distribution utilities to TPSODL, TPNODL,

TPWODL and TPCODL with effect from 01.01.2021, 01.04.2021, 01.01.2021 and

01.06.2020 respectively through separate vesting orders.

3. As per the OERC (Conduct of Business) Regulations, 2004 and the OERC (Terms and

Conditions for determination of Wheeling and Retail Supply Tariff) Regulations, 2022,

the DISCOMs i.e. TPCODL, TPWODL have filed their Aggregate Revenue

Requirement (ARR), Wheeling Tariff and Retail Supply Tariff (RST) Applications for

FY 2023-24 on 09.01.2023, whereas TPSODL & TPNODL have filed their Aggregate

Revenue Requirement (ARR), Wheeling Tariff and Retail Supply Tariff (RST)

Applications for FY 2023-24 on 10.01.2023.

4. The said Aggregate Revenue Requirement (ARR), Wheeling Tariff & Retail Supply

Tariff applications were duly scrutinized and registered as Case Nos. 82/2022

(TPSODL), 83/2022 (TPNODL), 88/2022 (TPCODL) and 80/2022 (TPWODL)

respectively.

5. As per direction of the Commission, applicants have published the Aggregate Revenue

Requirement (ARR), Wheeling & RST tariff Applications in the prescribed formats in

the leading and widely circulated Odia and English newspapers in their area of

operation in order to invite objections/suggestions from the general public. The above

applications were also posted in the Commission’s website (www.orierc.org) including

the website of the Distribution Utilities. The Commission had also directed the

applicants to file their respective rejoinders to the objections filed by all the objectors.

6. In response to the said public notices, the Commission received objections/ suggestions

from the following persons/ associations/ institutions/ organizations as mentioned

below against each of the respective distribution companies:-

Objections/Suggestions on the Applications of TPSODL:-

(1) Shri Ramesh Ch. Satpathy, Secretary, National Institute of Indian Labour &

President, Upobhokta Mahasangha, Plot No.302(B), Beherasahi, Nayapalli,

Bhubaneswar-751012, (2) M/s. Reliance JIO Infocom Ltd., Wing A&B, First Floor,

Fortune Tower, Chandrasekharpur, Bhubaneswar-751023, (3) Shri Priyabrata sahu, S/o.

5

Late Adikanda Sahu, At-Bijay Bihar, 3

rd

Lane, P.O: Berhampur, Dist.-Ganjam-

760001,(4) M/s. East Cost Railway, Bhubaneswar-751017, (5) Shri R. P. Mahapatra,

Retd. Chief Engineer & Member (GEN), OSEB, Plot No. 775(Pt.), Lane-3, Jayadev

Vihar, BBSR-751013, (6) Shri Akshya Kumar Sahani, Retd. Electrical Inspector, GoO,

B/L-108, VSS Nagar, Bhubaneswar-751007, (7) Shri Soumya Ranjan Patnaik, S/o. Late

Brajabandhu Patnaik, MLA, Khandapada, Plot No.185, VIP Colony, Nayapalli,

Bhubaneswar-751015, (8) Shri Bidyadhar Mohanty, At-Chorda, P.O: Jajpur Road,

Dist.-Jajpur-756019, (9) M/s. Utkal Chamber of Commerce & Industry Ltd.(UCCI), N-

6, IRC Village, Nayapalli, Bhubaneswar-751015, (10) Shri Panchanana Jena, S/o. Late

Bairagi Jena, Working President, Bijuli Karmachari Sangha, Sakti Nagar, 3

rd

Lane,

Engineering School Road, Berhampur-760010, (11) Shri Umakanta Mohapatra, S/O.

Late Prabodha Chandra Mohapatra, At/P.O: Sunhat, P.S;Town, Dist.-Balasore-756002,

(12) M/s. Grinity Power Tech Pvt. Ltd., At-K-8/82,Kalinga Nagar, Ghatikia,

Bhubaneswar-751029, (13) Shri Ananta Narayan Mahanty, S/o. Shri Biswanath

Mahanty, At/P.O: Bamakoyi, P.S: K.Nuagum, Dist.-Ganjam-761042, (14) Shri

Bibekananda Mohanty, Advocate, S/O. Late Harekrushna Mohanty, Civil Society,

Jajpur Road, Dist-Jajpur-755019, (15) Shri Asitananda Biswal, S/o. Late Gobinda

Chandra Biswal, At/P.O: Chorada, Jajpur Road, Dist.-Jajpur-755019,(16) Shri

Prabhakar Dora, Vidya Nagar, 3rd Line, Co-Operative Colony, Rayagada, Dist.

Rayagada-765001,(17) Shri Rajendra Samal, S/o. Shri Nilamani Samal, At-Natapada,

P.O: Jajpur Road, Dist-Jajpur-755019,(18) Shri Subrat Kumar Behera, Advocate, At-

Ranipatna, P.S/Dist.-Balasore-756001, (19) Shri Manoranjan Routray, S/O. Shri Khetra

Mohan Routray, At-Tritha Temple Street, P.S/P.O/Dist.-Koraput, (20) Shri Jayanta

Kumar Jena, S/O. Late Baikuntha Bihari Jena, At-Plot No.40, Bapuji Nagar, P.O:

Ashoknagar, Bhubaneswar-9,Dist.-Khordha, (21) M/s. GRIDCO Ltd., Janpath,

Bhubaneswar-22, (22) All India Weavers Welfare and Charitable Trust, C/O: B.C.

Behera, Om Sai Marga, Manik Nagar-5, P.O: Hinjilicut,Dist.-Ganjam-761102,(23) M/s.

ATCTelcom Infrastructure (P) Ltd.,4

th

Floor Module-A, Fortune Tower,

Chandrasekharpur, Bhubaneswar-751023,(24) M/s. Maa Bana Devi Poultry Pvt. Ltd.,

At/P.O: Nuagoan, Via-Aska, Dist.-Ganjam-761010, (25) Shri Ananda Kumar

Mohapatra, S/O. Jachindranath Mohapatra, Plot No. 799/4, Kotitirtha Lane, Po-OLD

Town, PS-Lingaraj Police Station, Bhubaneswar-751002, (26) M/s. Indian Energy

Exchange, Plot No.C-001/A/1, 9

th

Floor, Max Towers, Sector-16B, Noida, Gautam

Buddha Nagar, U.P.-201301,(27) M/s. OPTCL, Janpath, Bhubaneswar-22,(28) Chief

6

Load Despatcher, SLDC,SLDC Building, GRIDCO Colony, Mancheswar,

Bhubaneswar-751017, ( 29) Grahak Panchayat, Friends Colony, Paralakhemundi, Dist-

Gajapati-761200 (Consumer Counsel), (30) Secretary, PRAYAS, Energy Group,

Amrita Clinic, Athawale Corner, Carve Road, Pune-411004, India (Consumer

Counsel),(31) The Principal Secretary to Govt. Department of Energy, Govt of Odisha

All the above named objectors have filed their objections/suggestions and out of the

above, Objector Nos. 2,4,12,15,22,23,26,28 and both the Consumer Counsel remained

absent during hearing through hybrid mode and also had not submitted their written

notes of submission for consideration by the Commission. All written submissions filed

by objectors were taken on record and considered by the Commission. The Commission

heard the applicant, the Objectors, Consumer Counsel and the representative of Govt. of

Odisha, Department of Energy and others who were present during hearing.

Objections/Suggestions on the Applications of TPNODL:-

(1)

Shri Ramesh Ch. Satpathy, Secretary, National Institute of Indian Labour &

President, Upobhokta Mahasangha, Plot No.302(B), Beherasahi, Nayapalli,

Bhubaneswar-751012, (2) M/s. Relia

nce JIO Infocom Ltd., Wing A&B, First Floor,

Fortune Tower, Chandrasekharpur, Bhubaneswar-

751023, (3)M/s. North Odisha

Chamber of Commerce and Industry (NOCCI), Ganeswarpur Industrial Estate,

Januganj, Balasore-756019, (4) Shri Priyabrata Sahu, S/o. Late Adikanda Sahu, At-

Bijay Bihar, 3rd Lane, P.O: Berhampur, Dist.-Ganjam-760001

,(5) M/s. East Cost

Railway, Bhubaneswar-751017, (6)

Shri R. P. Mahapatra, Retd. Chief Engineer &

Member (GEN), OSEB, Plot No. 775(Pt.), Lane-3, Jayadev Vihar, BBSR-751013, (7)

Shri Akshya Kumar Sahani, Retd. Electrical Inspector, GoO, B/L-

108, VSS Nagar,

Bhubaneswar-751007, (8)

Shri Soumya Ranjan Patnaik, S/o. Late Brajabandhu

Patnaik, MLA, Khandapada, Plot No.185, VIP Colony, Nayapalli, Bhubaneswar-

751015,(9) Shri Bidyadhar Mohanty, At-Chorda, P.O: Jajpur Road, Dist.-Jajpur-

756019, (10) M/s. Utkal Chamber of Commerce & Industry Ltd.(UCCI), N-

6, IRC

Village, Nayapalli, Bhubaneswar-751015, (11) M/s. Sita Ratan International, At-

Ward

No.4,Near M.P.K. Girls High School, Lalbazar, P.O/P.S: Baripada, Dist.-Mayurbhanj-

757001,(12) Shri Panchanana Jena, S/O. Late Bairagi Jena,

Working President, Bijuli

Karmachari Sangha, Sakti Nagar, 3rd Lane, Engineering School Road, Berhampur-

760010, (13) Shri Umakanta Mohapatra, S/O. Late Prabodha Chandra

Mohapatra,

7

At/P.O: Sunhat, P.S;Town, Dist.-Balasore-756002,(14) M/s. Tata S

teel Ltd,

Kalinganagar Industrial Complex, At/P.O: Duburi, JK Road, Dist.-Jajpur-

755026, (15)

M/s. Visa Steel Ltd., Kalinganagar Industrial Complex, At/P.O: Jakhapura, Dist.-

Jajpur-755026, (16) M/s. Grinity Power Tech Pvt. Ltd., At-K-

8/82,Kalinga Nagar,

Ghatikia, Bhubaneswar-751029, (17) Shri Ananta Narayan Mahanty, S/O.

Shri

Biswanath Mahanty, At/P.O: Bamakoyi, P.S:K.Nuagum, Dist.-Ganjam-

761042, (18)

Shri Bibekananda Mohanty, Advocate, S/O. Late Harekrushna Mohanty,

Civil

Society, Jajpur Road, Dist-Jajpur-

755019, (19) Shri Asitananda Biswal, S/o.Late

Gobinda Chandra Biswal, At/P.O: Chorada, Jajpur Road, Dist.-Jajpur-

755019,(20)

Shri Prabhakar Dora, Vidya Nagar, 3rd Line, Co-Operative

Colony, Rayagada, Dist.

Rayagada-765001,(21)Shri Rajendra Samal, S/o. Shri Nilamani Samal, At-Natapada,

P.O:Jajpur Road, Dist-Jajpur-755019, (22) Shri Subrat Kumar Behera, Advocate, At-

Ranipatna, P.S/Dist.-Balasore-756001, (23) Shri Manoranjan Routray, S/O.

Shri

Khetra Mohan Routray, At-Tritha Temple Street, P.S/P.O/Dist.-Korapu

t, (24) Shri

Jayanta Kumar Jena, S/O. Late Baikuntha Bihari Jena, At-

Plot No.40, Bapuji Nagar,

P.O: Ashoknagar, Bhubaneswar-9,Dist.-

Khordha, (25) M/s. GRIDCO Ltd., Janpath,

Bhubaneswar-22, (26) M/s. Balasore Alloys Ltd., Balgopalpur, Balasore-

756020, (27)

Shri Ananda Kumar Mohapatra, S/O. Jachindranath Mohapatra, Plot No. 799/4,

Kotitirtha Lane, Po-OLD Town, PS-Lingaraj Police Station, Bhubaneswar-

751002,(28) Er..(Dr.) P.K. Pradhan, 4-

B, Jayadurga Nagar, Budheswari Colony,

Bhubaneswar-751006, (29) M/s. Indian Energy Exchange, Plot No.C-

001/A/1, 9th

Floor, Max Towers, Sector-16B, Noida, Gautam Buddha Nagar, U.P.-

201301,(30)

Shri Prasanta Kumar Panda, District Executive Member, BJP, At-Goudapada, P.O:

Jamujhadi, Via Simulia, Dist.- Balasore-756126, (31) M/s. O

PTCL, Janpath,

Bhubaneswar-

22, (32) Chief Load Despatcher, SLDC,SLDC Building, GRIDCO

Colony, Mancheswar, Bhubaneswar-

751017,(33) Secretary, PRAYAS, Energy Group,

Amrita Clinic, Athawale Corner, Carve Road, Pune-

411004, India (Consumer

Counsel),(31) The Principal Secretary to Govt.

Department of Energy, Govt of

Odisha.

All the above named objectors have

filed their objections/suggestions and out of the

above, Objector Nos.2,5,12,16,20,21,22,23,24,26,28,29,30 & 33 remained

absent

during hearing through hybrid mode. The Consumer Counsel

namely Odisha

Consumers Association, Balasore Chapter, Balasore participated in the hearing

by

8

filing their written notes of submission. All written su

bmissions filed by objectors

were taken on record and considered by the Commission. The Commission heard the

applicant, the Objectors, Consumer Councel, Balasore Chapter, the

representative of

the Govt. of Odisha and others who were present during hearing through hybrid mode.

Objections/Suggestions on the Applications of TPCODL:-

(1)

Shri Ramesh Ch. Satpathy, Secretary, National Institute of Indian Labour &

President, Upobhokta Mahasangha, Plot No.302(B), Beherasahi, Nayapalli,

Bhubaneswar-751012, (2) M/s.

Reliance JIO Infocom Ltd., Wing A&B, First Floor,

Fortune Tower, Chandrasekharpur, Bhubaneswar-

751023, (3) Shri Kamalakanta Das,

S/o. Late Nishakar Das, Flat No.

D/102, Prestige Residence, Mahadev Nagar,

Jharapada, Bhubaneswar-751006, (4) Shri Priyabrata

sahu, S/o. Late Adikanda Sahu,

At-Bijay Bihar, 3

rd

Lane, P.O: Berhampur, Dist.-Ganjam-

760001,(5) Shri Ashok

Kumar Pattnaik, M/s. BRG Iron & Steel Co.Pvt. Ltd., Flat No.1001, Tower-8, Z-

1,Advait, Nandankanan Road, Patia, Raghunathpur, Bhubaneswar-751024,(6)

M/s.

East Cost Railway, Bhubaneswar-751017,(7)

Shri R. P. Mahapatra, Retd. Chief

Engineer & Member (GEN), OSEB, Plot No. 775(Pt.), Lane-3, Jayadev Vihar, BBSR-

751013,(8) Shri Akshya Kumar Sahani, Retd. Electrical Inspector, GoO, B/L-

108,

VSS Nagar, Bhubaneswar-751007, (9)

Shri Soumya Ranjan Patnaik, S/o. Late

Brajabandhu Patnaik, MLA, Khandapada, Plot No.185, VIP Colony, Nayapalli,

Bhubaneswar-751015,(10) Shri Bidyadhar Mohanty, At-

Chorda, P.O: Jajpur Road,

Dist.-Jajpur-756019, (11) Shri Panchanana Jena, S/O. Late Bairagi Jena,

Working

President, Bijuli Karmachari Sangha, Sakti Nagar, 3

rd

Lane, Engineering School Road,

Berhampur-760010,(12) Shri Jyoti Prakash das, S/o.Late Satyabadi Das, Ex-Member-

ELBO, At-Devimandir, Shaiskh Bazar, Cuttack-753008,(13) M/

s. Utkal Chamber of

Commerce & Industry Ltd.(UCCI), N-6, IRC Village, Nayapalli, Bhubaneswar-

751015, (14) Shri Umakanta Mohapatra, S/O. Late Prabo

dha Chandra Mohapatra,

At/P.O: Sunhat, P.S;Town, Dist.-Balasore-

756002,(15) M/s. Grinity Power Tech Pvt.

Ltd., At-K-8/82,Kalinga Nagar, Ghatikia, Bhubaneswar-

751029,(16) M/s. Jindal Steel

& Power Ltd.,Chhendipada Road, SH 63, P.O.Nisa, Angul-759130,(17) Sh

ri Ananta

Narayan Mahanty, S/O.Shri Biswanath Mahanty, At/P.O: Bamakoyi, P.S:

K.Nuagum,

Dist.-Ganjam-761042, (18) Shri Rajendra Samal, S/o. Shri Nilamani Samal, At-

Natapada, P.O:Jajpur Road, Dist-Jajpur-755019, (19)

Shri Bibekananda Mohanty,

Advocate, S/O.Late Harekrushna Mohanty, Civil Society, Jajpur Road, Dist-Jajpur-

9

755019, (20) Shri Asitananda Biswal, S/o.Lat

e Gobinda Chandra Biswal, At/P.O:

Chorada, Jajpur Road, Dist.-Jajpur-755019,(21)

Shri Prabhakar Dora, Vidya Nagar,

3rd Line, Co-Operative Colony, Rayagada, Dist. Rayagada-7

65001,(22) Shri Subrat

Kumar Behera, Advocate, At-Ranipatna, P.S/Dist.-Balasore-7560

01, (23) Shri

Manoranjan Routray, S/O.Shri Khetra Mohan Routray, At-

Tritha Temple Street,

P.S/P.O/Dist.-Koraput, (24) Shri Jayanta Kumar Jena, S/O.

Late Baikuntha Bihari

Jena, At-Plot No.40, Bapuji Nagar, P.O: Ashoknagar, Bhubaneswar-9,Dist.-

Khordha,

(25) M/s. GRIDCO Ltd., Janpath, Bhubaneswar-22, (26)

M/s. Pragati Milk Product

Pvt. Ltd., Plot No.71/A/1 & 71/A, New Industrial Estate, Jagatpur, Cuttack-

754021,

(27) M/s. ATC Telcom Infrastructure (P) Ltd.,4

th

Floor Module-

A, Fortune Tower,

Chandrasekharpur, Bhubaneswar-751023, (28)

Shri Ananda Kumar Mohapatra, S/O.

Jachindranath Mohapatra, Plot No. 799/4, Kotitirtha Lane, Po-OLD Town, PS-

Lingaraj Police Station, Bhubaneswar-

751002,(29) Odish Retired Power Engineers’

Forum, C-7640, Bhoi Nagar, Bhubaneswar-

22, (30) M/s. Indian Energy Exchange,

Plot No.C-001/A/1, 9

th

Floor, Max Towers, Sector-

16B, Noida, Gautam Buddha

Nagar, U.P.-201301, (31) Shri Santosh Kumar Agarwal, A/17,

Ashok Nagar, Market

Building, Bhubaneswar-751009, (32) M/s. OPTCL, Janpath, Bhubaneswar-

22,(33)

Chief Load Despatcher, SLDC,SLDC Building, GRIDCO Colony, Mancheswar,

Bhubaneswar-751017,(34)

Secretary, PRAYAS, Energy Group, Amrita Clinic,

Athawale Corner, Carve Road, Pune-411004, India (Consumer Counsel

), (35)

Secretary, Confederation of Citizen Association, 12/A, Forest Park, Bhubaneswar-

751009(Consumer Counsel),(36) The Principal Secretary to Govt.

Department of

Energy, Govt of Odisha.

All the above named objectors have

filed their objections/suggestions and out of the

above, Objector Nos.2, 5,10,11,12,14,15, 17, 18, 19, 20, 21, 22, 23, 24, 27, 29, 30, 31

& 34 remained absent during hearing through hybrid mode. B

oth the Consumer

Counsel

namely Confederation of Citizen Association, 12/A, Forest Park,

Bhubaneswar-751009 and PRAYAS, Energy G

roup, Amrita Clinic, Athawale Corner,

Carve Road, Pune-411004, India have also remained absent and not filed

their written

note

of submissions for consideration by the Commission. The Commission heard the

applicant, the Objectors, Consumer Counsel and the

representative of Govt. of Odisha,

Department of Energy and others who were present during the hearing.

10

Objections/Suggestions on the Applications of TPWODL: -

(1) Shri Ramesh Ch. Satpathy, Secretary, National Institute of Indian Labour &

President, Upobhokta Mahasangha, Plot No.302(B), Beherasahi, Nayapalli,

Bhubaneswar-751012, (2) M/s. Reliance JIO Infocom Ltd., Wing A&B, First Floor,

Fortune Tower, Chandrasekharpur, Bhubaneswar-751023, (3) M/s. Scan Steels

Ltd.(Unit-III), At-Bai-Bai, Tudalaga, Bargaon, Dist.-Sundargarh-770016, (4) M/s. D.

D. Iron & Steel (P) Limited, H-4/5, Civil Township, Rourkela-769004, Dist-

Sundargarh,(5) M/s. Shree Salasar Castings Pvt. Ltd., Regd. Office-Balanda, Po-

Kalunga, Dist-Sundargarh-770031, (6) M/s. Top Tech Steels Pvt. Ltd., At- Plot

No.972/3634, Hatibari Road, Kuamunda, Dist.-Sundargarh-770031,(7) M/s.Shri Radha

Krishna Ispat Pvt. Ltd., At-Plot No.19 P, Goibhanga, Kalunga, Dist.-Sundargarh-

770031,(8) M/s. Chunchun Ispat Pvt.Ltd.,,At-Usra,P.O: Kaurmunda, Dist.-Sundargarh-

770039,( 9) M/s. Shri Radha Raman Alloys Pvt. Ltd.,At-T-16, Civil Township,

Rourkela, Jharbeda, Kutra, Dist.-Sundargarh-770070, (10) M/s. Scan Steels

Limited,(Unit-I), At- Rambahal, P.O: Keshramal, Near Rajgangpur, Dist.-Sundargarh-

770017,(11) M/s. Puspanjana Alloys Pvt. Ltd., At-Plot No.1562/2565, Balanda, P.O:

Kalunga,Dist.-Sundargarh-770031, (12) M/s. Refulgent Ispat Pvt.Ltd., At-Chikatmati,

Plot No.1437, P.O: Belhidi, Sundargarh-770031,(13) M/s. Arun Steel Industries Pvt.

Ltd.,At-Plot No.373, Jiabahal Road, Kalunga, Dist.-Sundargarh-770031,(14) M/s.

Bajrang Steel & Alloys Ltd.,Plot No.31,Goibhanga,Kalunga,Rourkela, Dist.-

Sundragarh-770031,(15) M/s. Maa Girija Ispat (P) Ltd., At-BB-2, Ground Floor, Civil

Township, Rourkela-769004, Dist-Sundargarh,(16) Shri Priyabrata sahu, S/o. Late

Adikanda Sahu, At-Bijay Bihar, 3

rd

Lane, P.O: Berhampur, Dist.-Ganjam-760001,(17)

M/s. East Cost Railway, Bhubaneswar-751017, (18) Shri R. P. Mahapatra, Retd. Chief

Engineer & Member (GEN), OSEB, Plot No. 775(Pt.), Lane-3, Jayadev Vihar, BBSR-

751013, (19) M/s. Bajrangabali Sponge & Power Ltd., At-Plot No.82, IDC, Kalunga,

Dist.-Sundargarh-770031, (20) Shri Akshya Kumar Sahani, Retd. Electrical Inspector,

GoO, B/L-108, VSS Nagar, Bhubaneswar-751007,(21) Shri Soumya Ranjan Patnaik,

S/o. Late Brajabandhu Patnaik, MLA, Khandapada, Plot No.185, VIP Colony,

Nayapalli, Bhubaneswar-751015,(22) Shri Bidyadhar Mohanty, At-Chorda, P.O: Jajpur

Road, Dist.-Jajpur-756019,(23) Er.(Dr.) P.K.Pradhan,B-4,Jayadurga Nagar, P.O:

Budheswari Colony, Bhubaneswar-751006,(24) M/s. Utkal Chamber of Commerce &

Industry Ltd.(UCCI), N-6, IRC Village, Nayapalli, Bhubaneswar-751015, (25)

M/s.Greengold Bamboo Foundation, At-Dewansaheb Para, P.O/P.S: Bhawanipatna,

11

Kalahandi-766001,(26) Shri Panchanana Jena, S/O. Late Bairagi Jena, Working

President, Bijuli Karmachari Sangha, Sakti Nagar, 3

rd

Lane, Engineering School Road,

Berhampur-760010,(27) Shri Umakanta Mohapatra, S/O. Late Prabodha Chandra

Mohapatra, At/P.O: Sunhat, P.S: Town, Dist.-Balasore-756002,(28) M/s. Grinity Power

Tech Pvt. Ltd., At-K-8/82,Kalinga Nagar, Ghatikia, Bhubaneswar-751029,(29) M/s.

Romco Alluminate Pvt. Ltd.,(Formerly known as Rourkela Minerals Company Pvt.

Ltd.), At-Bijabahal, P.O: Kaurmunda, Dist.-Sundargarh-770039, (30) Shri Ananta

Narayan Mahanty, S/O. Biswanath Mahanty, At/P.O:Bamakoyi, P.S;K.Nuagum,Dist.-

Ganjam-761042,(31) Shri Bibekananda Mohanty, Advocate, S/O. Late Harekrushna

Mohanty, Civil Society, Jajpur Road, Dist-Jajpur-755019, (32) Shri Asitananda Biswal,

S/o. Late Gobinda Chandra Biswal, At/P.O: Chorada, Jajpur Road, Dist.-Jajpur-

755019,(33) Shri Prabhakar Dora, Vidya Nagar, 3rd Line, Co-Operative Colony,

Rayagada, Dist. Rayagada-765001,(34) Shri Rajendra Samal, S/o. Shri Nilamani

Samal, At-Natapada, P.O: Jajpur Road, Dist-Jajpur-755019, (35) Shri Subrat Kumar

Behera, Advocate, At-Ranipatna, P.S/Dist.-Balasore-756001, (36) Shri Manoranjan

Routray,S/O.Shri Khetra Mohan Routray,At-Tritha Temple Street, P.S/P.O/Dist.-

Koraput, (37) Shri Jayanta Kumar Jena, S/O.Late Baikuntha Bihari Jena, At-Plot

No.40, Bapuji Nagar, P.O: Ashoknagar, Bhubaneswar-9,Dist.-Khordha, (38) M/s.

GRIDCO Ltd., Janpath, Bhubaneswar-22, (39) Shri Ananda Kumar Mohapatra, S/O.

Jachindranath Mohapatra, Plot No. 799/4, Kotitirtha Lane, Po-OLD Town, PS-Lingaraj

Police Station, Bhubaneswar-751002,(40) M/s. Indian Energy Exchange, Plot No.C-

001/A/1, 9

th

Floor, Max Towers, Sector-16B, Noida, Gautam Buddha Nagar, U.P.-

201301, (41) M/s. Shri Jagannath Alloys Private Ltd., At-Plot No.QQQ-14, Civil

Township, Rourkela, Dist.-Sundargarh-769004,(42) M/s. Ritika Ispat Private Ltd., Plot

No.490, Balanda, Kalunga, Dist.-Sundargarh-770031,(43) M/s. Dalmia Cement

(Bharat) Ltd., At/P.O: Rajgangpur, Dist.-Sundargarh-770017, (44) M/s. Subh Ispat

Pvt.Ltd.,At-Jiabahal, Kalunga, Dist.-Sundargarh-770031,(45) M/s. Vedanta Ltd.,1

st

Floor, C-2,Fortune Tower, Chandrasekharpur, Nandankanan Road, Bhubaneswar-

751023, (46) M/s. ATCTelcom Infrastructure (P) Ltd.,4

th

Floor Module-A, Fortune

Tower, Chandrasekharpur, Bhubaneswar-751023, (47) M/s. OPTCL, Janpath,

Bhubaneswar-22,(48) Chief Load Despatcher, SLDC,SLDC Building, GRIDCO

Colony, Mancheswar, Bhubaneswar-751017, (49) Sambalpur District Consumers

Federation, Balaji Mandir Bhavan, Kheterajpur, Dist.-Sambalpur-678003, (50)

Sundargarh District Employee Association, AL-1, Basanti Nagar, Rourkela-

12

769012,(51) Secretary, PRAYAS, Energy Group, Amrita Clinic, Athawale Corner,

Carve Road, Pune-411004, India (Consumer Counsel), (52) M/s. Juggernaut

Association of Entrepreneurs, Plot No.1294, CRP Square, Nayapalli, Bhubaneswar-

751012,(53) Director of Horticulture, Govt. of Odisha, Krushi Bhawan, Bhubaneswar-

751001,(54) The Principal Secretary to Govt. Department of Energy, Govt of Odisha.

All the above named objectors have filed their objections/suggestions and out of the

above, Objector Nos. 39, 40, 41, 42, 43, 44 & 46 and the Sambalpur District Consumers

Federation, Balaji Mandir Bhavan, Kheterajpur, Sambalpur-678003, Sundargarh

District Employee Association, AL-1, Basanti Nagar, Rourkela.- 769012 and PRAYAS,

Energy Group, Amrita Clinic, Athawale Corner, Carve Road, Pune-411004, India

remained absent during hearing through hybrid mode. Beside the above, Shri Ananda

Kumar Mohapatra also participated in the hearing. All the written submissions filed by

the objectors were taken on record and also considered by the Commission. The

Commission heard the applicant, the Objectors, Consumer Counsel and the

representative of Govt. of Odisha, Department of Energy and others who were present

during hearing.

Table – 2

Sl.

No.

Name of the Organisations/persons with address

Name of the Distribution

Utility from where the

Consumer Counsel to

represent

1

Orissa Consumers’ Association, Balasore Chapter,

Balasore

-

756126

TPNODL

2

Sambalpur District Consumers’ Federation, Balaji Mandir

Bhavan, Khetrajpur,

Sambalpur

-

678003

TPWODL

3

Sundargarh District Employee Association, AL-1, Basanti

Nagar, Rourkela

-

769012

TPWODL

4

Grahak Panchayat, Friends Colony, Parlakhemundi, Dist :

Gajapati

-

761200

TPSODL

5

Secretary, Confederation of Citizen Association, 12/A,

Forest Park, BBSR

-

9.

TPCODL

6 The Secretary, PRAYAS Energy Group, Pune-411004

TPCODL, TPNODL, TPWODL

& TPSODL

7. The dates and time for hearing through hybrid mode were fixed and it was duly notified

in the leading English and Odia daily newspaper along with the names of the objectors.

The Commission issued notice to the Govt. of Odisha represented by the Department of

Energy to take part in the hearing.

8. In its consultative process, the Commission conducted public hearings through hybrid

13

mode for TPSODL in its area of supply on 24.02.2023 at 11.00AM.at Rural

Development & Self Employment Training Institute (RSETI) Conference Hall,

Paralakhemundi, Dist.-Gajapati, for TPNODL in its area of supply at “ATRIUM”

NOCCI Business Park Bampada, Chhanpur, Dist.- Balasore-756056 on 27.02. 2023 at

11.00 AM, for TPCODL in its area of Supply at Zilla Parisad Conference Hall, !st

Floor, Zilla Parisad Office, Mahisapat Main Road, NH 55, Near Nirupama Hotel, Dist.-

Dhenkanal on 28.02.2023 at 11.00 AM and for TPWODL in its area of supply at Biju

Patnaik E- Learning Centre Auditorium, VSSUT, Burla, Sambalpur on 04.03.2023 at

11.00 AM. The Commission during hearing heard the Applicants, Consumer Counsel,

World Institute of Sustainable Energy, Pune and the persons/institutions/ organizations

who had filed their written views and participated in the hearing through hybrid mode,

the Objectors present during hearing and the representative of the DoE, Government of

Odisha at length. Parties were directed to file their written note of submission, if any

within 7 days. The applicants were also directed to file their rejoinder/written note of

Submission along with their reply to the queries of the Commission made during

hearings through hybrid mode, if any.

9. DISCOMs have filed their applications relating to Open Access Charges for FY 2023-

24 in accordance with Regulation 22, 23, 24 & 25 of Chapter-5 of the OERC (Terms

and Conditions of Intra-State Open Access Charges) Regulations, 2020 for approval of

Wheeling Charges, Cross Subsidy Surcharge, Additional Surcharge & Stand-by charges

applicable to Open Access Customers for use of intra-state transmission/ distribution

system for FY 2023-24 which were registered as Case Nos. 86, 87, 89 & 85 of 2022 for

TPSODL, TPNODL, TPCODL and TPWODL respectively. TPSODL & TPWODL had

filed their applications for approval of Truing up expenses for 3 months of FY 2020-21

and for the whole financial year 2021-22 which had been registered as Case Nos.6/2023

and 81/2022 respectively. TPCODL had filed truing up application in respect of 10

months for FY 2020-21 and for whole year of FY 2021-22 which had been registered as

Case Nos. 90 & 91 of 2022 respectively. Similarly, TPNODL had filed its truing up

application for FY 2021-22 which had been registered as Case No.84/2022. The above

named DISCOMs of Odisha had also filed their applications for approval of Business

Plan for FY 2023-24 in compliance to OERC (Terms and Conditions for determination

of Wheeling and Retail Supply Tariff) Regulations, 2022 which were registered as Case

Nos.12 of 2023, 10 of 2023, 11 of 2023 & 13 of 2023 for TPSODL, TPNODL,

TPCODL and TPWODL respectively and were taken up for analogous hearing with

14

their ARR & RST applications for FY 2023-24 in compliance to the directions of the

Commission in their vesting orders. The Commission had directed the DISCOMs to

publish the Public Notice regarding their application in widely circulated Odia and

English newspaper inviting views/ suggestion of the public. The Commission had also

posted a copy of their applications in its website.

10. For the sake of addressing the issues involved, the Commission took up hearing of all

the applications of individual DISCOM as stated above through hybrid mode on 24.02.

2023 at 11.00 A.M for TPSODL, on 27.02.2023 at 11.00 A.M for TPNODL, & on

28.02.2023 at 11.00A.M. for TPCODL and on 04.03.2023 at 11.00 A.M for TPWODL

with due notice to the applicants and the objectors.

11. Heard the Applicants, Consumer Counsel, the Objectors present in the hearing and the

representative of Department of Energy, Government of Odisha in extenso.

12. In course of hearing of the present Applications, Learned Objectors Shri R. P.

Mahapatra and some others raised the point of competency of this Commission,

functioning with the Officiating Chairperson and another Member, embarking upon the

exercise of determination of tariff and other related areas etc. which were held to be

unsustainable in the orders passed on the different dates of hearing. Thus, that part of

controversy has reached quietus in the wake of the provisions under Section 93 of the

Electricity Act, 2003 read with Section 9(4) of the Orissa Electricity Reform Act, 1995

and Regulation 8(1)(b) of the OERC (Conduct of Business) Regulations, 2004.

B. ARR & RETAIL SUPPLY TARIFF PROPOSAL FOR 2023-24 (PARA 13 TO 21)

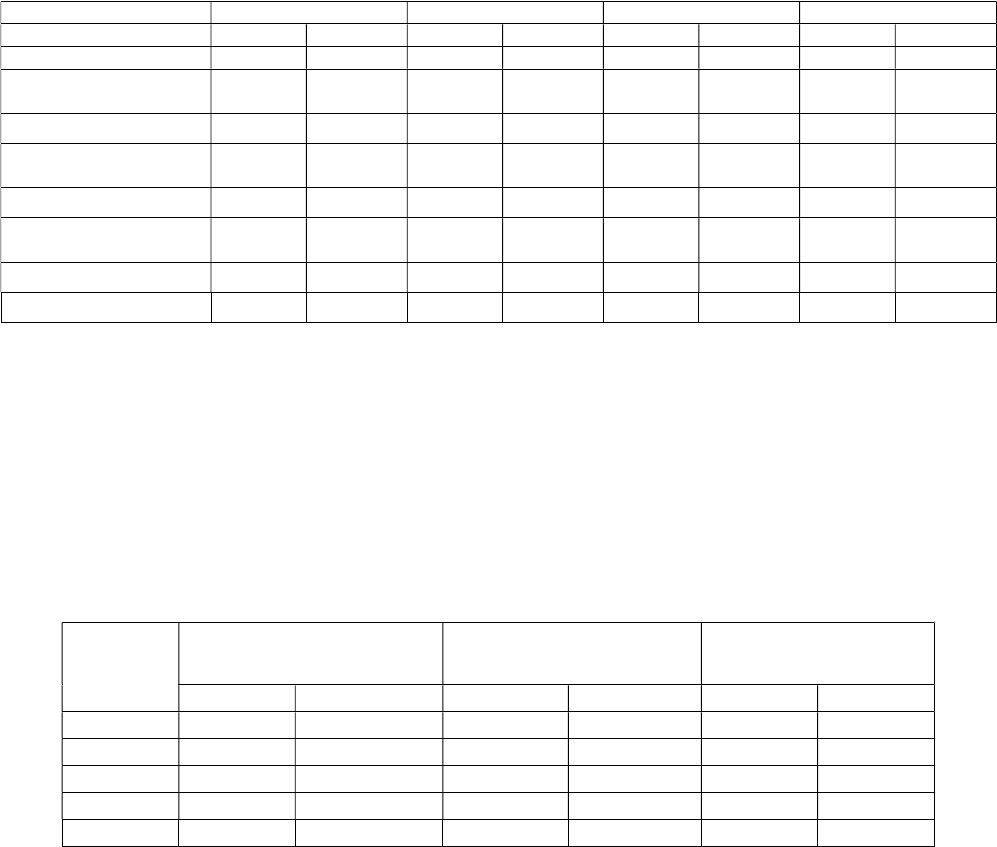

13. Energy Sales, Purchase and Distribution Loss

A statement of Energy Purchase, Sale and Overall Distribution Loss from FY2016-17

to 2023-24 as submitted by DISCOM of Odisha namely TP Central Odisha Distribution

Ltd (TPCODL, erstwhile CESU), TP Western Odisha Distribution Ltd (TPWODL,

erstwhile WESCO Utility), TP Southern Odisha Distribution Ltd. (TPSODL, erstwhile

SOUTHCO Utility) and TP Northern Odisha Distribution Limited. (TPNODL,

erstwhile NESCO Utility) is given below.

Table - 3

15

Energy Sale, Purchase and Loss (Considering railway traction demand)

DISCOMs Particulars

2016-17

(Actual)

2017-18

(Actual)

2018-19

(Actual)

2019-20

(Actual)

2020-21

(Actual)

2021-22

(Actual)

2022-23

(Rev-

Est)

2023-24

(Est)

TPCODL

Energy Sale

(MU)

5488.59 5781.64 6310.92 6273.189 6202.32 6728 7787 8668

Energy

Purchased

(MU)

8139.36 8467.09 8783.92 8160.1 8370.43 8817 10112 10999

Overall

Distribution

Loss %

32.57 31.72 28.15 23.124 25.90 23.69 22.99 21.19

TPNODL

Energy Sale

(M

U)

4077.20 4234.96 4530.91 4722.18 3921.63 4346 5472 6246

Energy

Purchased

(MU)

5329.66 5448.99 5575.60 5439.43 4941.19 5327 6702 7458

Overall

Distribution

Loss %

23.50 22.28 18.74 13.19 20.63 18.40 18.35 16.25

TPWODL

Energy Sale

(MU)

4799.00 5378 5972 6115 5714 7356 10071 10482

Energy

Purchased

(MU)

6969.00 7248 7590 7524 7625 9313 12300 12800

Overall

Distribution

Loss %

31.00 25.81 21.32 18.73 25.07 21.02 18.12 18.11

TPSODL

Energy Sale

(MU)

2141.18 2334.11 2555.88 2619.97 2768.94 3021 3372 3586

Energy

Purchased

(MU)

3273.45 3468.18 3638.94 3468.62 3599.29 3941 4495 4781

Overall

Distribution

Loss %

34.59 32.70 29.76 24.47 23.07 23.34 25 25

14. Sales Forecast

TPCODL has submitted that CAGR is the reasonably common method to project future

sales based on the data of past few years. Due to COVID the sales were not consistent.

Now after normalization of industrial loads, TPCODL is expecting higher sales in HT

and EHT category. TPCODL had projected the sales based on the previous years’

trends and requests for consideration of additional sales in the LT, HT and EHT

consumer categories.

TPNODL has relied on the past ten years’ data with correction for the data during

COVID period while projecting the sales for the year 2023-24. The expected sales for

households being electrified, sales to the new industries reviving their operation after

shutdown during COVID period, consumption of the CGP and steel industries have

been considered on the future projections.

16

TPWODL has submitted that post COVID and after improvement in billing efficiency,

the LT sales is expected to grow at slightly higher rate. However, due to shifting of

electricity consumption through own captive generation by the steel industries and

railways, the EHT sales is expected to grow at very low rate.

TPSODL has submitted that their LT sales is expected to grow at lower rate as the load

in LT segment has already increased post COVID. HT and EHT segment load growth is

expected to be in the range of 6 to 7% on year on year basis.

Table – 4

Sales Forecast

Licensee LT Sales for 2023-24

(Est

imated

)

HT Sales for 2023-24

(Est

imated

)

EHT Sales for 2023-24

(Est

imated

)

Total Sales 2023-24

(Est

imated

)

MU

(MU)

% Rise over

FY22

-

23

(MU)

% Rise over

FY22

-

23

(MU)

% Rise over

FY22

-

23

TPCODL 4902 11% 1908 7% 1858 17% 8668

Remarks

Projected the sales based

on previous years’ trends

and requests in hand.

Higher HT sales projections

due to normalizing of

Industrial Loads post COVID

Higher EHT sales

projections due to

normalizing of Industrial

Loads post COVID.

TPNODL 2607 11.31% 685 8.33% 2953 18.26% 6246

Remarks

Slightly more growth

considered against the

normal growth of 8% due

to various techno-

commercial initiatives to

increase sales and reduce

thefts. Increased sales

due to electrification, agro

industrial activities is

expected to increase LT

sales

Increased consumption by

steel industries and industries

with CGPs will increase

consumption by HT

Consumers

Considering the increasing

fuel costs, increasing open

access tariffs, the CGPs and

OA consumers are again

started availing utilities

power added with few new

consumers licensee is

expecting good growth in

EHT sales

TPWOD

L

3314 7.42% 2123 4.83% 5045 1.69% 10482

Remarks

With improvement in

consumer billing and

increased sales to LT

irrigation consumers, the

LT sales is expected to

grow slightly

Railways consumers shifted

to EHT, significant increase

in agriculture and allied

agriculture consumption

EHT consumption is mainly

by railways, steel industries.

Shifting of consumption by

utilities to their captive

generation has led to less

demand growth in EHT

sector

TPSODL 2553 3.71% 391 6.53% 642 7.04% 3586

Remarks

Load increased post

COVID and hence for FY

2023-24 lower load

growth expected

Load increased in 2022-23

post COVID and further load

growth expected during the

FY 2023-24

Increase in captive

consumption by utilities with

CGPs will lead to lower

growth in this segment

15. System Losses and Collection Efficiency:

17

The System Loss, Collection Efficiency and the target fixed by OERC in respect of

AT&C Loss for the four DISCOMs since FY 2016-17 onwards are given hereunder.

Table - 5

AT&C Loss

DISCOMs Particulars

2016-17

(Actual)

2017-18

(Actual)

2018-19

(Actual)

2019-20

(Actual)

2020-21

(Actual)

2021-22

(Actual)

2022-23

(Rev-

Est.)

2023-24

(Est)

TPCODL

Dist. Loss

(%)

32.57 31.72 28.15 23.124 25.90 23.69 22.99 21.19

Collection

Efficiency

(%)

96.56 96.6 96.60 90.51 95.09 97.36 99 99

AT&C

Loss (%)

34.89 34.04 30.49 30.42 29.54 25.70 23.76 21.98

OERC

Approved

(AT&C

Loss %)

23.77 23.77 23.77 23.77 23.70 23.70 23.70 22.00

TPNODL

Dist. Loss

(%)

23.50 22.28 18.74 13.19 20.63 18.40 18.35 16.25

Collection

Efficiency

(%)

96.25 93.38 94.10 86.38 94.28 94.20 99.00 99.00

AT&C

Loss (%)

26.37 27.43 23.53 25.01 25.17 23.13 19.17 17.09

OERC

Approved

(AT&C

Loss %)

19.17 19.17 19.17 19.17 19.17 19.17 19.17 17.09

TPWODL

Dist. Loss

(%)

31.22 25.81 21.32 18.73 25.07 21.02 18.12 18.11

Collection

Efficiency

(%)

88.00 88 86.87 87.91 97.71 92.93 97.2 99

AT&C

Loss (%)

39.38 34.80 31.64 28.56 26.78 26.60 20.41 18.93

OERC

Approved

(AT&C

Loss %)

20.40 20.40 20.40 20.40 20.40 20.40 20.40 18.90

TPSODL

Dist. Loss

(%)

34.59 32.70 29.76 24.47 23.07 25.00 25.00 25

Collection

Efficiency

(%)

89.90 91.44 86.95 84.34 91 99 99 99

AT&C

Loss (%)

41.20 38.46 38.93 36.30 29.99 25.75 29.50 29.49

OERC

Approved

(AT&C

Loss %)

26.25 26.25 26.25 26.25 26.25 25.75 25.75 25.75

16. Revenue Gap Proposed by the DISCOMs

The Revenue Requirement, Expected Revenue at existing tariff and Gap as submitted

by Odisha DISCOMs are summarized below:

Table - 6

Proposed Revenue Requirement, Expected Revenue and Gap

18

TPCODL TPNODL TPWODL TPSODL Total

Approved

FY 2022-23

Proposed

FY 2023-24

Approved

FY 2022-23

Proposed

FY 2023-24

Approved

FY 2022-23

Proposed

FY 2023-24

Approved

FY 2022-23

Proposed

FY 2023-24

Approved

FY 2022-23

Proposed

FY 2023-24

Total

Revenue

Requirement

4271.21 5207.02 2700.08 3707.34 4079.34 5771.94 1689.27 2289.89 12739.90 16976.19

Expected

Revenue at

Existing

Tariff

4273.00 5144 2701.03 3503.14 4119.48 6171.82 1694.00 1985.71 12787.51 16804.67

Surplus /

(Gap)

1.79 (63.02) 0.95 (204.20) 40.14 399.88 4.73 (304.18) 47.61 (171.52)

17. Inputs in Revenue Requirement for FY 2023-24

a) Power Purchase Expenses

The Licensees have proposed the power purchase costs based on their current BSP,

transmission charges and SLDC charges. They have also projected their SMD

considering the actual SMD during FY 2022-23 and additional SMD in the coming FY

2023-24 which is as shown in the table given below.

Table - 7

Proposed SMD and Power Purchase Cost FY 2023-24

DISCOMs

Estimated

Power

Purchase

in(MU)

Estimated

Sales(MU)

Distribution

Loss(%)

Current

BSP

(Paise/Unit)

Estimated Power

Purchase Cost (Rs.in

Cr.)(Including

Transmission and

SLDC Charges)

SMD

proposed

MVA

TPCODL

1100

2

8668

21.21%

300

3610

2192

TPNODL

7458

6246

16.25%

321

2604

1500

TPWODL

12800

10482

18.11%

360

5100.06

1850

TPSODL

4781

3586

25.00%

227

1220

800

b) Employees Expenses

TPCODL, TPNODL, TPWODL and TPSODL have projected the employee expenses

for FY 2023-24 and revised estimates for FY 2022-23 based on the six months’ actual

expenses. The projected employee expenses are based on the projected employee

strength and has considered the expenses towards salary for permanent and contractual

employees, PF payment, medical and other incentives, terminal benefits, payment of

arrears etc. Further, the net employee expenses after capitalization are compared with

the current year’s projections and summarized in the following table.

Table -8

Employee Expenses after Capitalization

Employee Expenses after TPCODL TPNODL TPWODL TPSODL

19

capitalization

Employee Expenses in 22-23

773.55

429.29

564.71

517.60

Employee Expenses in 23-24

827.23

484.90

614.97

608.90

% Rise YOY

6.94%

12.95%

8.90%

17.64%

c) Administrative and General Expenses

As per the Wheeling and Retail Supply Tariff (RST) Regulations, 2022, the five year

MYT period starts from FY 2022-23 to FY 2027-28. The regulation permits 7%

escalation YOY for estimating the A&G expenses for the ensuing year. The licensees

have only six months’ data of A&G expenses of the base year i.e. for the period from

April 22 to September, 2022. Due to implementation of different activities for

reduction of AT&C loss and increasing the billing & collection, the licensees are

incurring higher A&G expenses than that approved by the Commission. Accordingly,

the licensees have requested 7% increase over the revised estimates of A&G expenses

for the FY 2022-23. Further over the normal escalation of 7%, the licensees have

projected additional A&G expenses for various activities considered as important and

necessary. The approved A&G expenses for the FY 2022-23, revised estimates of A&G

expenses for the FY 2022-23, A&G expenses proposed for the FY 2023-24, and

additional A&G etc. are summarised in following table:

Table - 9

A&G Expenses

A&G expenses TPCODL TPNODL TPWODL TPSODL

A&G expenses approved by OERC for FY

2022

-

23

132.72 84.23 110.39 77.25

Revised estimated A&G expenses for FY

2022

-

23

- 150.84 173.76 -

Estimated Normal A&G expenses for FY

2023

-

24

142 98.21 185.78 68.04

Additional A&G expenses proposed for FY

2023

-

24

20 101.01 76.37 69.55

Total A&G expenses proposed in ARR for

FY 2023

-

24

163.51 199.22 262.16 137.47

The licensees have submitted that the higher A&G expenses during the current and

ensuing year are on account of meter reading, billing and collection, IT Automation,

AMR related expenses, insurance expenses, professional charges, enforcement

activities, Customer care, compensation towards electrical accidents etc.

TPCODL, TPNODL, and TPSODL have proposed additional A&G expenses for the

undertaking the activities related to metering, billing and Collection. TPWODL has

proposed additional A&G expenses towards Energy Audit, special drive for shifting of

20

meter to outside premises, GIS, SCADA, Communication, OT, Data Charges, special

drive to improve MBC activity, re-establishment of energy police stations, IT

automation, Vigilance and enforcement etc.

Accordingly, TPCODL, TPNODL, TPWODL and TPSODL have estimated the A&G

expenses of Rs.163.51 Cr, Rs 199.22 Cr, Rs.262.16 Cr and Rs.137.59 Cr respectively

for the FY 2023-24.

d) Repair and Maintenance (R&M) expenses

As per the Wheeling & RST Regulations 2022, the R&M expenses are permitted at

specified rate on the opening GFA owned by the licensee and at the rate of 3% for the

assets created through consumer contribution and grants. Accordingly, the licensees

have projected the R&M expenses as per following for the FY 2023-24:

Table - 10

R&M Costs (Rs. in Cr)

R&M expenses TPCODL

TPNODL TPWODL TPSODL

Opening GFA of DISCOMS own assets in

Rs. Cr as on 1

st

April

,

2023

5256.99 2778.83 3009.44 1541

% of GFA on DISCOM’s own assets

approved towards R&M

4.2% 4.5% 4.5% 5.4%

R&M Expenses for DISCOM’s own

assets i

n Rs Cr

220.79 125.05 135.42 83.21

Opening GFA of assets created through

grants in Rs. Cr as on 1 April 2023

2350.04 2033.26 3398.17 2406

% of GFA on assets created through

grants approved towards R&M

3% 3% 3% 3%

R&M Expenses for assets created through

grants in Rs Cr

70.50 60.99 101.95 72.18

Total R&M Expenses for FY 2023-24 as

per Regulation 2022

291.29 186.05 237.37 155.40

TPCODL and TPSODL have proposed the R&M expenses of Rs 291.29 Cr and Rs

155.40 Cr respectively based on the normative R&M permitted under the Regulations

2022.

TPNODL has estimated the R&M expenses for FY 2023-24 as Rs.257.19 Cr. towards

Civil repairs and maintenance, distribution line repairs and maintenance, transformer

repairs, Other R&M work etc. They have submitted that the regulation permits special

R&M for the licensees to undertake critical activities which are not covered under

approved capital investment plan. They have mentioned critical need of 11 and 33 KV

AMC for improvement in reliability. Accordingly, TPNODL has proposed R&M

expenses for FY 2023-24 as Rs 257.19 Cr.

21

TPWODL has submitted that for the current FY 2022-23, as per the Wheeling & RST

Regulations 2014, 5.4% of opening GFA is permitted towards R&M. The licensee has

reported that they have incurred the expenditure of Rs 156.03 Cr towards R&M in first

six months and considering balance six month’s total expenditure towards R&M in FY

2022-23 will be close to Rs. 300 Cr. They have further submitted that FY 2023-24

being the first year of the control period and they have already executed the AMCs for

R&M of the distribution lines and to ensure the proper reliability they have requested to

permit R&M at 5.4% of GFA which is Rs. 346.01 Cr for 2023-24.

e) Provision for Bad and Doubtful Debts

The Regulations 2022, allows provision towards Bad and Doubtful Debt at the rate of

1% of the revenue billed for sale of electricity. This 1% revenue is allowed to pass

through in the ARR. The provision for the bad and doubtful debts proposed by the

licensees is as follows:

Table - 11

Provision for Bad and Doubtful Debt

DISCOMs Total revenue

billed for 2023-

24 (Rs in Cr)

1% Provision

towards Bad and

Doubtful Debt

(Rs in Cr)

Proposed Bad

Debts for 2023-24

(Rs in Cr)

TPCODL

5086.6

50.87

50.87

TPNODL

3503.14

35.03

35.03

TPWODL

6

171.82

61.72

61.72

TPSODL

1985.71

19.86

19.86

f) Depreciation

As per the OERC Tariff Regulations 2022, the depreciation on the assets transferred

through vesting order is calculated on the pre-up valued cost of assets at pre 1992 rate

on the assets base approved by the Commission. For the new created assets, the

depreciation is calculated based on the straight line method by all the licensees at the

rate defined in the Regulations. Accordingly, the depreciation projected for the ensuing

financial year by TPCODL is Rs.81.38 Cr., by TPWODL Rs.97.06 Cr., by TPNODL

Rs.66.88 Cr. and by TPSODL Rs.62.09 Cr.

g) Interest Expenses

TPCODL, TPNODL, TPWODL & TPSODL have submitted the interest expenses

towards interest on capital loan and working capital and the interest earned on security

deposit for the FY 2023-24.

22

The major components of the interest expenses of these licensees are as follows:

i) Interest on Capital Loan

TPCODL has estimated the interest on long term debt as Rs.46.61 Cr. Accordingly,

TPNODL has estimated the interest on long term debt as Rs.39.44 Cr. TPWODL has

estimated the interest on long term debt as Rs.58.32Cr. TPSODL has estimated the

interest on long term debt as Rs.28.34 Cr.

ii) Interest on Working Capital

As per the Wheeling and RST Regulations 2022, the components for interest on

Working capital includes O&M for 1 month, Spares 20% of R&M of 1 month, 1month

power purchase cost. The licensees have considered the rate of interest for working

capital as SBI base rate plus 300 basis points. Accordingly, TPCODL, TPNODL,

TPWODL and TPSODL have projected the interest on working capital as Rs.46.87Cr.,

Rs.35.22 Cr., Rs.58.95 Cr. and Rs.20.27 Cr. for FY 2023-24 respectively.

iii) Interest earned on Security Deposit (SD)

TPCODL, TPSODL, TPNODL and TPWODL have projected the interest on SD as

Rs.65.56 Cr., Rs.18.13Cr., Rs.36.03 Cr., and Rs.46.75Cr. for FY 2023-24 respectively.

h) Non-Tariff Income

TPCODL, TPNODL, TPWODL and TPSODL have proposed non-tariff income for FY

2023-24 to the tune of Rs.109.56 Cr, Rs.178.45Cr, Rs.289.33 Cr and Rs.55.65Cr

respectively from the wheeling business and retail supply business which is mainly

through receipts of licensee from meter rent, service connection charges, reconnection

charges, Over Drawl Payment (ODP), Delayed Payment Surcharge (DPS), rebate on

power purchase, interest on Fixed Deposit (FD) etc.

i) Return on Equity and Tax on Income

TPCODL has projected the RoE of Rs.98.75 Cr. and tax on Income of Rs. 33.21 Cr. for

FY 23-24. TPWODL has projected the RoE of Rs.109.44 Cr and tax on Income of Rs.

36.81 Cr. for FY 23-24. TPNODL has projected the RoE of Rs.79.42Cr and tax on

Income of Rs. 26.71Cr. for FY 23-24. TPSODL has projected the RoE of Rs. 54.14Cr

for FY 23-24.

18. Revenue at Existing Tariff

23

The Licensees have estimated the expected revenue from sale of power by considering

the sales projected for FY 2023-24 and by applying various components of existing

tariffs. The total revenue based on the existing tariffs applicable for the projected sales

is estimated at Rs.5144Cr by TPCODL, Rs.3503.14 Cr by TPNODL, Rs.6171.82 Cr by

TPWODL, Rs.1985.71 Cr by TPSODL.

19. Summary of Annual Revenue Requirement and Revenue Gap

The proposed revenue requirement and expected revenue of DISCOMs have been

summarized below:

Table – 12

Proposed Revenue Requirement of DISCOMs for the FY2023-24(Rs in Cr.)

Particulars

TPCODL TPNODL

TPWODL TPSODL Total

Total Power Purchase,

Transmission & SLDC

3610.3 2604.23 5100.06 1219.9 12534.49

Total Operation &

Maintenance and Other Cost

1574.32 1153.95 1545.95 1071.42 5345.64

Return on Equity

98.75

79.42

109.44

54.14

341.75

Tax on ROE

33.21

26.71

36.81

96.73

Total Distribution Cost (A)

5316.58

3864.31

6792.26

2345.46

18318.61

Total Special Appropriation

(B)

0 21.48 (730.99) 0 (709.51)

Total expenditure including

special appropriation (A+B)

5316.58 3885.79 6061.27 2345.46 17609.1

Less: Miscellaneous Receipt

109.56

178.44

289.33

55.57

632.9

Total Revenue Requirement

5207.02

3707.34

5771.94

2289.89

16976.19

Expected Revenue(Full year )

5144

3503.14

6171.82

1

985.71

16804.67

GAP at existing (+/-)

(63.02)

(204.20)

399.88

(304.18)

(171.52)

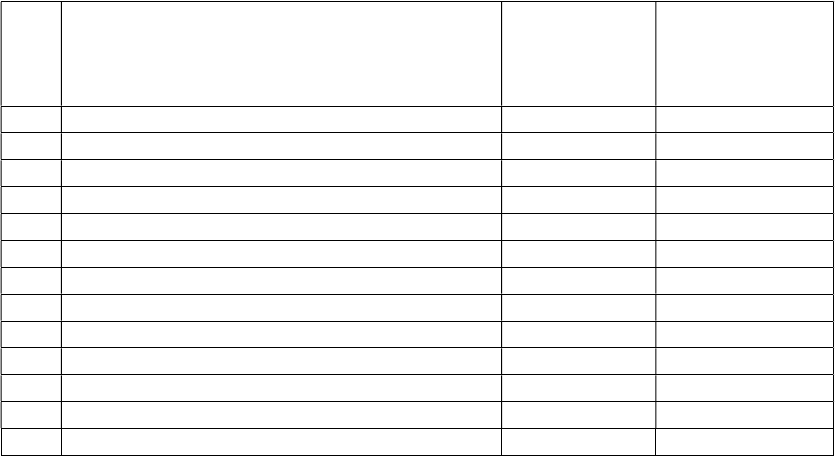

20. Truing Up of expenses for the FY 2020-21 and the FY 2021-22

TPSODL, TPCODL, TPWODL & TPNODL have submitted their true-up expenses for

the FY 2020-21 & FY 2021-22 as provided in the table below:

Table - 13

DISCOM Truing Up requirement Amount in Cr

TPSODL

FY 2020

-

21 ( 3 months)

FY

2021

-

22

Surplus/(Gap)

16.59

4.47

TPCODL

FY 2020

-

21 (10 months)

FY 2021

-

22

Surplus/(Gap)

( 92.89 )

( 213.45)

TPWODL

FY 2020

-

21

(3 months)

FY

2021

-

22

Surplus/(Gap)

29

.52

506.78

TPNODL

FY 2020

-

21

FY 2021

-

22

Surplus/(Gap)

(47.22)

21. Tariff Proposals and Rationalization Measures:

24

The licensees have proposed some tariff rationalization measures to improve the

revenue and recovery the cost of supply. The brief details of their proposal are as under:

(a) Special tariff for drawal of RE power at premium rate (TPNODL,

TPWODL)

TPNODL and TPWODL have submitted that the special green tariff approved by the

Commission for drawal of renewable power by industry at the premium rate i.e. 50

paisa per unit over and above the tariff applicable for that category of consumer has not

attracted many consumers to opt for green energy. The licensees, therefore, propose to

reduce the premium to 25 paisa per unit. The licensees have also proposed methodology

for issuance of Green power certificates to the end users opting for Green Power. Apart

from the green tariff revision,

The Commission had launched premium rate for RE power. Even though provision for

CGP industries was created for fulfilment of 100% of its requirement from renewable

sources is the hurdle. DISCOM power is costlier than their own generation in addition

to that levy of premium rate of 50 paise is on higher side. Therefore, the licensee has

requested the Commission to reduce the premium from 50 paisa to 25 paisa per unit.

Further, certification by DISCOM is another concern. GRIDCO is the obligated entity

on behalf of DISCOM for fulfilment of RE requirement, unless GRIDCO passes

on/allocates RE to DISCOM, it is not possible for DISCOM to provide required

certificate. The licensee has proposed the allocation of RE power across DISCOMs at

GRIDCO level. If Commission permits allocation of RE availability to all the licensees

then DISCOM can provide certificate to the consumer willing to pay premium tariff for

“Green Energy” without recurring consent/approval from GRIDCO Therefore, if RE

power can be assigned (through certification) for industries opting to draw with

premium special rate then it will be a win-win situation for the industries as well as for

other stake holders. The premium price shall be added to the bill. The industry has to

opt in advance for booking of quantum. The licensees propose a premium charge of 25

paise per unit over and above normal charges.

(b) Levy of Cyclone Resilient Network Cess (TPCODL)

Odisha is extremely vulnerable to cyclones with increasing frequency of occurrences.

To restore the system after cyclone, the state government and central government do

extend support to the licensees based on the impact of cyclone. However, the Licensee

25

is of the view to maintain some inventory in order to timely restore the system and

accordingly the petition was also submitted. Further licensee has proposed to levy a

Cess of 2 paisa per unit to all consumers except BPL category to support the DISCOMs

to build inventory so that mitigation / emergency restoration activities can be taken up

faster to tackle such events.

(c) Creation of disaster resilient Corpus Fund

The Licensees i.e. TPNODL & TPWODL have proposed to charge Rs. 2 per month per

consumer to create a corpus fund for meeting the immediate system restoration works

post cyclones.

(d) Amendment to the ToD tariff (TPCODL)

The licensees have observed that there are two peaks in summer and winter at different

times during the day and they have submitted the 15 minutes’ demand profile. At

present the ToD tariff discount of Rs 0.20 per units is offered for the time slot between

10 pm to 6 am to three phase consumers. In view of changing demand licensee has

proposed to change the off-peak period as 1.00 to 6.00 hrs and 16.30 to 18.00 hrs

during summer months. Similarly, they proposed the off-peak period of 00 hrs to 5.00

hrs for winter months for the purpose of extending discounted tariff.

(e) Continuity of Special tariff for Existing industries having CGP if assured

80% LF of existing CD (TPNODL)

Regarding the above matter, TPNODL has submitted that a special mechanism for sale

of surplus power of GRIDCO through tripartite agreement was approved by

Commission as per para 370 of BST order FY 2022-23 & clause (viii) Annexure-B of

RST order. However, in absence of firm power GRIDCO and DISCOMs filed a

separate petition (Case no. 25 of 2022) for approval of price till firm power is available

with GRIDCO. Commission vide order dt.18th May 22, has approved a special price of

Rs.4.75 per kVAh. GRIDCO has to be paid @ Rs.4.26 per kwh for the power consumed

beyond 80% of CD and OPTCL is entitled for 28 paise as transmission charges.

Balance amount is DISCOM share. The intention of such scheme was to sale the

surplus power of the state to the industries inside the state. As a result, industries can

get cheaper/competitive power and may opt to close their CGP or may avoid

undertaking open access of power. The licensee proposed to continue the scheme in the

26

ensuing year also with bucket filling method. In addition, they proposed that an industry

availing this benefit shall not be permitted to avail benefit of another scheme.

Similarly, as per the submission of TPWODL, in FY 2022-23, industry having CGP

with CD up to 20MW willing to avail power from DISCOMs up to double the CD were

allowed to draw power without payment of overdrawal penalty provided they need to

maintain more than 80% LF. Seeing good response, licensee proposed to continue this

benefit for FY 23-24. Industries availing this benefit shall not be permitted to avail

benefit under other scheme. Continuity of Special tariff for Existing industries having

CGP with CD >20 MW with minimum offtake 80% of existing CD (TPWODL) for FY

2022-23, industry having CGP willing to avail power from DISCOMs and operating at

load factor more than 80% were allowed to draw power at the rate not less than

Rs.4.30/kVAh for all incremental energy drawal above 80% load factor without any

overdrawl penalty has been proposed. Licensee requested to continue this scheme for

the ensuing year with bucket filling method. In addition to this an industry availing this

benefit shall not be permitted to avail benefit of another scheme.

(f) Billing with Defective Meter (TPNODL, TPWODL):

As per OERC Distribution (Conditions of Supply) Code, 2019, the licensee is permitted

to raise provisional bill for maximum upto three months and during this time the

defective meter has to be replaced with new meter. Thereafter, the provisional bill so

raised shall be revised considering actual meter reading for consecutive six billing

cycle. Further as per OERC Distribution (Conditions of Supply) Code 2019, the billing

is to be done on the basis of average meter reading of past three billing cycles

immediately preceding the meter being found / reported defective. The provisional bill

is required to be revised as per the average of six consecutive billing after the new

meter is installed. Licensees face issues that the consumers are not paying even the

actual bill after replacement of defective meters unless the bill is revised. Further the

consumers are also controlling the consumptions after the installation of new meter. To

improve the collection efficiency licensee also cannot wait for six months. Licensee has

requested for the practice direction for the same in the RST order.

With this mechanism the licensee is facing the following difficulties:

27

a) Consumers are not paying current bill even after replacement of defective meter

unless the bill is revised. The licensee is helpless, as they have to wait for six

consecutive billing cycles for the bill to correct and are not able to release bills.

b) In many cases, consumers are desiring to revise the bill considering past actual

consumption in corresponding period, however, this is not permitted under the

Regulation.

c) Some are insisting for bill revision considering actual metering after one

month’s consumption.

d) Most of the consumers are trying to control the consumption and are tempted to

use through other means with an intention to reduce six month’s average billing

even though they have actually used more and more energy during the meter

defective period.

Licensee has requested the Commission to consider past assessment based on the first

full month’s consumption after the replacement of the meter and issue the direction in

the RST order FY 2023-24. The consumption of subsequent months till 6th month can

be used for correction/ adjustments to the assessment amount which was initially done

basing on first full month’s consumption. The differential amount can be billed to the

consumer at the end of 6 month’s post meter replacement.

(g) Revision of meter rent for Smart Meter Connections (TPCODL)

At present Rs.60 per month and Rs. 150 per month of meter rent for single and three

phase smart energy meters is in force. CEA and MOP have directed to implement smart

meters for all consumers by 2025. Considering the present cost of Rs. 5200/- for single

phase smart meter it is not possible to recover the meter cost at the present meter rent.

Accordingly, the licensee has proposed to revise the meter rent to Rs. 80 per month to

be recovered over a period of 90 months. Licensee has also requested to specify pre-

paid smart meters for all the new connections having consumption above 100 units per

month.

(h) Full recovery of meter rent (TPCODL and TPSODL)

In order to ensure replacement of existing meters by prepaid smart energy meters, the

licensee has requested the Commission to permit recovery of full cost. The cost of

single and three phase meters discovered through competitive bidding by TPSODL is of

Rs. 5197/- and Rs. 8564/- TPSODL proposed the revised meter rent of Rs 84/- and

28

Rs139/- for single and three phase smart meters to be recovered in 7 years or

alternatively Rs. 111/- per month to be recovered over the period of 5 years.

(i) Provision regarding Industries owning Generating Station and CPP

availing Emergency Supply only (TPCODL)

Industries owning CGP consume power for short period with very high demand leading

to increase in SMD of the licensees. In order to avoid such situations, the licensee has

proposed to restrict the drawl at 10% LF or 100% of the highest capacity of generation

unit. In case due to such drawals, if SMD is breached due to overdrawal, then penalty

on excess demand of 10% of the highest generation unit shall be charged to the

consumer at the same rate applicable for the HT and EHT consumers.

(j) Proposal for considering Contract Demand in case of conversion of

connection from Emergency Supply into two-part tariff after continuous

violation for 3 months (TPCODL)

In case of conversion from Emergency Supply to two-part tariff in the event of

continuous violation for 3 months, the licensee has proposed to levy Contract Demand

at 10% of the highest generation unit’s capacity or as per 80% CD or MD whichever is

higher and restricting the consumption of electricity upto 10% of highest generation

capacity.

(k) LT tariff for Consumers with CD<=70kVA (TPCODL)

The licensee has submitted that the consumers, who would have been normally supplied

on LT (i.e. upto 70 kVA), are supplied in HT due to non-availability of as LT supply

and they are billed at HT tariffs. In such cases, the transformer loss is passed on to LT

consumers due to HT metering and this leads to grievances. Therefore, TPCODL

proposes that all consumers with CD<=70 kVA, shall be billed on LT tariff irrespective

of supply voltage and category.

(l) Overdrawl penalty & Demand Charge for all consumers with CD>=110

kVA (TPCODL)

Licensee has proposed to levy overdrawl penalty and the demand charge principle of

80% of CD or MD whichever is higher to LT consumers with CD>=110 kVA.

29

(m) Need for Separate Tariff Category for HT Public lighting (TPCODL)

Public lighting tariff category is available only for LT supply. However, some of the

public lighting connections are provided supply through HT and Licensee has proposed

to have separate HT Public Lighting supply category for such consumers.

(n) Revision of Reconnection Charges with penalty clause (TPCODL,

TPNODL and TPWODL)

Licensees have submitted that the reconnection charges are constant for quite long time

and there is need for upward revision in the reconnection charges considering the rising

costs. further, licensee has proposed double reconnection charges for consumers having

repeated reconnections to avoid such reconnections. Present and proposed charges are

as follows:

Table - 14

Prior to 1

st

April 2012

Continuing since

1

st

April 2012

Proposed

Reconnection Charges

LT Single Phase Domestic

Consumer

Rs.75/- Rs.150/- Rs.300/-

LT Single Phase other

consumer

Rs 200/- Rs.400/- Rs 800/-

LT 3 Phase consumers

Rs.300/

-

Rs.600/

-

Rs.1200/

-

All HT & EHT consumers

Rs.1500/

-

Rs.3000/

-

Rs.6000/

-

(o) Creation of Energy Police Station (TPCODL and TPWODL)

In past during 2008, the State Government had taken anti-theft initiatives and created

29 numbers of Energy Police Stations across all the DSICOMs. Effectiveness of EPS in

the past was not encouraging at that point of time due to nos of factors. Loss Reduction

being one of the key objectives, TPCODL and TPWODL proposed to setup at least 5

EPS each, one in each circles with around 124 staffs. With the change in management

and control of the DISCOMs, re-establishment of Energy Police Stations will definitely

have positive impact in enforcing discipline and accelerating Loss Reduction.

Accordingly, licensee has requested for additional A&G for EPS.

(p) Billing of Public Lighting (TPCODL)

Earlier for many reasons the public lighting connections were not metered. Licensee

proposed to consider 11 hours of supply throughout the year for calculation of average

use of electricity for billing purpose. The Licensee has proposed mandatory installation

of energy meters for new public lighting connections.

30

(q) Demand Charges to HT medium category consumers (TPNODL,

TPCODL)

The HT medium category consumers are now availing supply at demand charges of Rs

150 per kVA as against the GP and SPP category which are paying Rs 250 per kVA as

demand charges. Due to the differential demand charges, consumers under HT medium

category just below 110kVA are always trying to avail demand benefit even though

their actual connected load is more than 110kVA and above. To curb such type of

disparity in demand charges the licensee proposed to revise to Rs 250 per kVA for HT

medium category consumers.

(r) MMFC for LT Category Consumer (TPNODL)

Presently LT category of consumers, except Large PWWs>110kVA & Specified Public

Purposes>110kVA and above are paying Monthly Minimum Fixed Charges (MMFC)

on the basis of their connected load. MMFC for all the LT category of consumers is

proposed to be rationalized with single rate for 1st kW or part thereof as well as

additional kW or part thereof. At present, a Small industry with 10 kW load is paying

Rs.80 for 1st kW and for balance 9kW is paying @ Rs. 35 per kW (Rs.35X9

kW=Rs.315). So the demand charges paid are Rs.395/- instead of Rs.800/- (i.e. Rs.80 X

10kW), similarly in case of LT medium industry it is Rs.100/- for 1st kW or part

thereof and for additional kW it is only Rs.80/- per kW. The minimum load for LT

medium category is >= 22 kVA. Licensee has proposed to levy the MMFC for all the

LT category of consumers with single rate for 1st kW or part thereof as well as

additional kW or part thereof.

(s) Increase in rebate from 3% to 4% for LT Domestic, LT GP single phase &

Single phase irrigation consumers (TPNODL, TPWODL)

The Commission had extended additional rebate of 3% towards digital payment for LT

single phase Domestic & GP category of consumers since FY 2022-23. This is yielding

very good results and the cost of collection is decreasing significantly. Hence, licensee

requested for further increase in the digital rebate from 3% to 4% which would further

motivate digital payment and will help to do away with the culture of door to door

collection.

31

(t) Incremental digital rebate to rural consumers (TPNODL)

The introduction of multiple initiatives of digital collection like My Tata Power App,

Airtel Payment Bank tie-up, Spice Money tie up, tie up with SBI, BBPS & other UPI

facilities, there has been a significant boost in rural digital payments. Hence, Licensee

proposed to extend additional 3% rebate for rural LT domestic consumers for digital

payment.

(u) Considering Actual average LF for the category during assessment of

unauthorized drawl (TPNODL)

As per OERC Supply Code, 2019, the assessment of unauthorized consumption is done

as LxHxF.

Where L=Connected load found in the consumer premises during the course of

inspection in kW: H=No. of hours of the period of assessment, F=Load factor as has

been prescribed for collection of SD in Regulation 52.

The load factor prescribed by the OERC in Supply Code for various categories is found

to be very less which does not reflect the actual probable usage of the various

equipment which results in negative assessment thereby not providing the penal

environment to discourage unauthorized drawls. Hence, it is requested to allow for

taking into consideration the load factor for assessment as average actual load factor for

Domestic category or may consider approving 20% LF for domestic, 25% LF for

commercial and industrial and 50% LF for continuous process industries over a 24

hours’ period.

(v) Levy of CSS on RE power (TPNODL, TPWODL)

The Commission had introduced levy of CSS on RE power with effect from FY 2022-

23. Accordingly, the consumers availing renewable power through open access shall

have to pay the transmission charge, wheeling charge and cross subsidy surcharge as

applicable to consumers availing conventional power. This CSS amount collected by

licensee has helped the licensee to accommodate the BST increase and ultimately has

aided towards non-increase in RST. Hence, the licensee has requested for continuation

of levy of CSS and wheeling charges on RE power for FY 2023-24.

32

(w) Special tariff for existing industries who have no CGP for drawl of

additional power beyond CD of 10 MVA (TPNODL)

After announcement of above special tariff scheme for the industry, few of the other

industries those who have no CGP has started approaching for similar type of scheme