Real estate reset:

The case for UK

property

Executive summary

Bill Page

Head of Real Estate Research

1. After screening as expensive for several years, UK real

estate valuations now appear to offer fair value on a range

of metrics.

2. UK valuations also better reect current market pricing

than Europe and the US, in our view.

3. That said, sector and segment differentials remain

signicant and require careful navigation.

4. Continuing volatility in rates and potential geopolitical

risk suggest portfolios should still tilt to income resilience

rather than taking a binary ‘bet’ on yield compression.

In our view the latter should be seen as an upside risk

to expected returns, rather than a strategy.

2024

|

Real estate reset: The case for UK property

For professional clients only. Not to be

distributed to retail clients. Capital at risk.

3

2024

|

Real estate reset: The case for UK property

2

2024

|

Real estate reset: The case for UK property

Introduction

Since 2016, many asset classes, and UK real estate in

particular, have been rocked by a succession of events: Brexit,

Covid, spikes in ination, and a historically aggressive policy

rate hiking cycle.

At the midpoint of 2024, we feel the timing is right to look

objectively at pricing and valuation to establish a clear view

on the relative case for UK real estate.

Why now?

In our view UK real estate pricing – and indeed valuations –

have, after two years, reset to levels consistent with where

rates, and other macros drivers, have settled. Therefore, an

informed view on fair value and how pricing might evolve in

the medium term is warranted.

We do not, and should not, have condence in our ability to

forecast ination, interest rates or geopolitics. Although the

probability of a slow reduction in policy and market interest

rates between now and the end of 2025 is reasonably high,

it is not guaranteed. ‘Low probability, high impact’ geopolitical

events may yet impact markets. Such factors can inform

investment choices between resilient sectors and binary

yield plays.

We also reect that, internationally, gaps between transaction

pricing and valuation differ, and differences vary depending

on real estate sectors. Such differences matter for allocation

and deployment decisions.

According to higher frequency MSCI monthly data, UK real

estate values are approximately -25% lower than they were

in June 2022

1

. April 2024’s reading showed almost zero

movement in aggregate, with industrial and residential values

appreciating, retail stable, and oces falling

2

. This slowdown

does not guarantee the next move in values at the all-property

level will be upward, but it does make a discussion of relative

value timely.

Meanwhile, quarterly valuation data from MSCI clearly show

how the UK correction was harder and faster than other

regions.

1. Source: MSCI Monthly Digest, May 2024

2. Source: MSCI Monthly Digest, April 2024. Industrial and retail values were up 0.1% and 0.05% month on month respectively with oce values down -0.5%

Capital value change since June 2022, quarterly, global regions

Source: MSCI Global Quarterly Property Index, Q1 2024. Value changes re in local currency. Note the Europe excl UK is a LGIM Real Assets calculation based on available

data and reweighted. Past performance is not a guide to the future.

3. Source: IPF UK Real Estate Consensus Forecasts, Spring 2024

4. Source: ULI, Emerging Trends in Real Estate 2024

Other investors seem to agree that a change of fortunes is

imminent, with the IPF consensus

3

showing expected capital

growth of 0.8% this year and c. 3% p.a. between 2025 and 2028

inclusive.

At the same time, ULI

4

implies that global investors expect to

see more alignment on pricing and recovering volumes as we

move through 2024.

70

75

80

85

90

95

100

105

Jun

2022

Sep

2022

Dec

2022

Mar

2023

Jun

2023

Sep

2023

Dec

2023

Mar

2024

Europe Global U.S. UK Asia-Pacific Europe excl. UK estimate

In our view UK real estate

pricing – and indeed

valuations – have, after two

years, reset to levels

consistent with where rates,

and other macros drivers,

have settled.

Assumptions, opinions and estimates are provided for

illustrative purposes only. There is no guarantee that any

forecasts made will come to pass.

5

2024

|

Real estate reset: The case for UK property

4

2024

|

Real estate reset: The case for UK property

Global real estate fund raising, overall and by risk style, 2007 - 2024 (estimates)

UK REITS discount to net asset value

Source: Preqin, Data as at 31 March 2024. The light green bar is an estimate of fundraising over the remaining three quarters in 2024, based on average trends over

the last three years. Past performance is not a guide to the future. The value of an investment and any income taken from it is not

guaranteed and can go down as well as up, you may not get back the amount you originally invested. Assumptions, opinions

and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Source: Bloomberg, LGIM Real Assets, May 2024. Past performance is not a guide to the future. The value of an investment and any income

taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally invested.

Does UK real estate offer fair value?

The UK REIT sector currently trades at a -9.8% discount

to net asset value compared to a long-term average of -4.7%.

This compares favourably to its recent trough of -38%

6

. Asset

valuations (the NAV) have fallen to close the gap with investor

perceptions of pricing, which may have stabilised. Such

high-frequency signals were hugely important in gauging

valuation risks to direct UK real estate as markets evolved

over summer 2022; and they should not be ignored as

sentiment improves.

Global data from Preqin

5

shows how real estate fundraising

was affected by the macro picture in recent years. But more

interesting, we think, is the deviation in fundraising by style.

Two years ago, there was a surge in fundraising activity for

value-add styles. We would interpret this as fund managers

requiring greater risk to deliver investors the return over the

risk-free rate they require.

Furthermore, strategies that combine direct real estate and

indirect and more liquid REIT options have been shown to

outperform

7

. We think the recent performance seen in REITs is

indicative of an ability to capture growth before direct property

valuations do.

More recently, value-add strategies have decelerated from their

cyclical highs, replaced by an increase in core and core+

strategies. We think this shows managers are more

comfortable with current property pricing and see less need

to take additional risk.

5. Source: Preqin Quarterly Updates, May 2024

6. Source: Bloomberg, LGIM Real Assets calculations, May 2024

7. Source: See, for instance, “Blending Public and Private Real Estate Allocations for Dened Contribution Pension Funds: A U.K. Case Study”, Journal of Real Estate

Portfolio Management, Vol. 20, No. 3, 2014

0

50

100

150

200

250

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2023

2022

2024

Capital raised ($bn)

0

10

20

30

40

50

60

70

80

90

2007

2008

2009

2010

2012

2011

2013

2014

2016

2015

2017

2018

2019

2020

2021

2022

2023

2024

Capital raised ($bn)

Core Core-plus

Distressed

Value add Opportunistic

Other

The UK REIT sector currently

trades at a -9.8% discount to net

asset value compared to a long-

term average of -4.7%. This

compares favourably to its recent

trough of -38%.

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

20162014 2018 2020 2022 2024

%

UK average

7

2024

|

Real estate reset: The case for UK property

6

2024

|

Real estate reset: The case for UK property

LGIM Real Assets has several proprietary models it can use to

gauge fair value and we cover two here. The rst is a yield

model which represents where valuation yields should be in

accordance with their historic relationship to rates, corporate

credit, lending activity and rental growth expectations. It

creates an expected yield and compares this to actual

valuation yields. This model showed a gap of 200 bps

immediately after 2022’s LDI crisis, implying signicant value

risk for directly held assets. These risks came to pass and,

following outward yield movement and some amelioration in

rate inputs, the yield model is now at parity with valuation

yields for the rst time in almost three years.

Secondly, LGIM Real Asset’s relative value indicator also looks

at MSCI yields and compares them to their own history and to

other asset classes such as equities and corporate bonds. This

indicator has screened ‘expensive’ since 2019, but – like the

yield model – has recently moved into neutral territory.

LGIM Real Assets yield model

LGIM Real Assets relative value indicator

Source: LGIM Real Assets, May 2024. Past performance is not a guide

to the future. The value of an investment and any income

taken from it is not guaranteed and can go down as well as

up, you may not get back the amount you originally invested.

Source: LGIM Real Assets, May 2024. Past performance is not a guide

to the future. The value of an investment and any income

taken from it is not guaranteed and can go down as well as

up, you may not get back the amount you originally invested.

Source: LGIM Real Assets, MSCI Quarterly Digest, Q1 2024. Past performance is not a guide to the future. The value of an investment and any

income taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally invested.

Source: LGIM Real Assets, MSCI Quarterly Digest, May 2024. Past performance is not a guide to the future. The value of an investment and any

income taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally invested.

Both models evidence our view that UK real estate offers fair

value – although we would emphasise that they do not suggest

the sector is cheap, only that it is no longer expensive. We

would also caveat this by pointing out it is the oce sector that

has done most of the recent work in increasing the all property

yield. Nevertheless, such signals have historically correlated

well with subsequent returns, as shown in the graph on the

next page.

LGIM’s relative value indicator and subsequent returns for UK all-property (three-year annualised)

Risk Premium and subsequent returns for UK all-property (three-year annualised)

Analysis of the risk premium offered by UK real estate (calculated by current yields plus growth expectations less depreciation and gilt

yields) currently shows a risk premium of 3.2%, compared to an average since 1981 of 2.6%. There is a notable range between sectors

on this measure, but the current all-property average is associated with subsequent returns in the region of 9-10% p.a., consistent

with the analysis above.

0%

2%

4%

6%

8%

10%

12%

1989

1994

1999

2003

2004

2009

2014

2019

2024

Predicted Equivalent Yield Actual Equivalent Yield

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

Standard deviations

20 year indicator using equivalent yields

Not expensive

Expensive

-15

-10

-5

0

5

10

15

20

-1.5 -1.0 -0.5 0.00.5 1.

01.5

-

Subsequent 3 yr returns (% p.a.)

Relative value indicator score

Today’s relative value indicator

-10

-5

0

5

10

15

20

25

-10.0 -8.0 -6.0 -4.0 -2.0 0.0 2.0 4.0 6.0 8.0 1

0.0

Subsequent 3-yr returns (% p.a.)

Risk premium, year end

Today’s est. yield premium

9

2024

|

Real estate reset: The case for UK property

8

2024

|

Real estate reset: The case for UK property

Evolution of the risk-free rate

At the time of writing, nancial markets were pricing in two

policy rate cuts in the UK over the remainder of 2024 and three

by May 2025. Our expectations are very similar. Market interest

rates have adjusted to this slower anticipated pace of easing,

with 10-year gilts hovering around 4.2% and expected to reach

3.4% by year end 2025

8

. As mentioned above, analysts should

be humble in both their own predictions and in reading too

much into volatile nancial market signals.

But we can consider scenarios with relevance to the relative

pricing of real estate assets:

.

Rates fall, as implied

by markets

.

Rates fall faster than

markets imply

.

Rates stay at current levels

over the near term

.

Rates increase

We think that real estate yields, as evidenced by the

above metrics, have broadly adjusted to today’s

market interest rates.

Therefore, scenario 1 would allow for modest yield

compression as well as being consistent with a

reasonable economic backdrop supporting rental

growth.

Scenario 2, a faster reduction in rates, may all else

being equal technically allow for a reduction in real

estate yields, but could come at a recessionary cost

with weaker occupation markets.

Should rates stay at current levels – scenario 3 – then

our assumption that real estate values have already

broadly adjusted would suggest future returns are

almost entirely driven by income returns and rental

growth.

Finally, an increase in rates – scenario 4 – would

remove much of the potential for yield compression,

all else being equal, but may also be consistent with

stronger growth which could benet higher beta

sectors such as retail, as well as mitigating oce risk

via additional jobs growth.

Illustrative property equivalent yield in 2025 under various scenarios

Source: LGIM Real Assets, May 2024, based on MSCI Monthly Data as at April 2024 and calculated through LGIM’s yield model. Assumptions, opinions

and estimates are provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

In summary, there are various potential rates scenarios with only one of those considered – increased rates without any rental growth

benet –signicantly detrimental to real estate performance based off today’s valuation yields.

8. Source: Bloomberg as at May 2024

6.

4%

6.

6%

6.

8%

7.

0%

7.

2%

7.

4%

7.6%

Current yield Rates fall 50 bps Rates fall faster,

all else equal

Rates fall faster

and rental growth

flatlines

Rates rise further Rates rise further

and rental growth

improves

Assumptions, opinions and estimates are provided for

illustrative purposes only. There is no guarantee that

any forecasts made will come to pass.

11

2024

|

Real estate reset: The case for UK property

10

2024

|

Real estate reset: The case for UK property

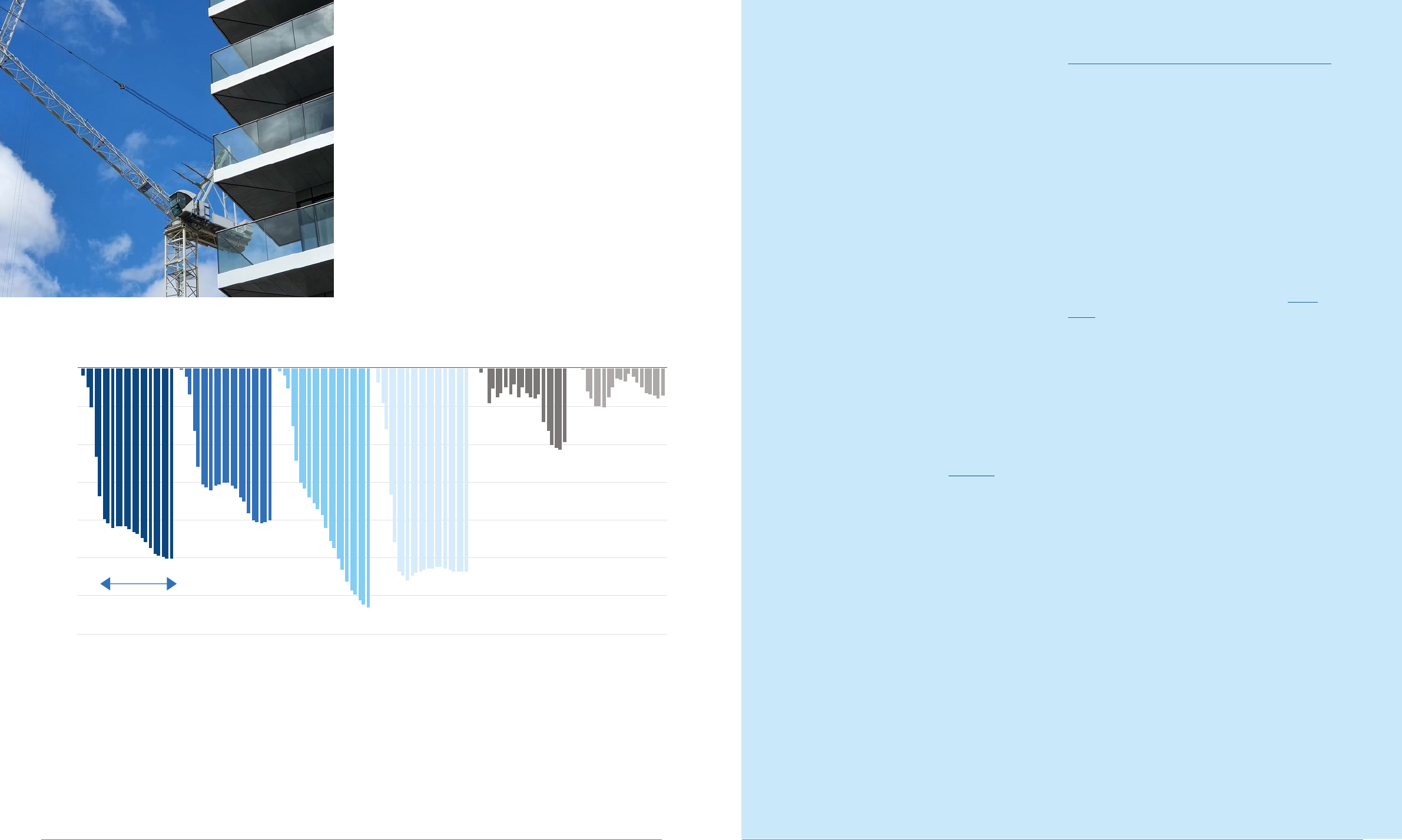

Sector differences

The graphs below show the cumulative value change on the

MSCI monthly index by main sector, with an LGIM Real Assets

estimate for BTR (build-to-rent residential) where most of the

recent deterioration was a direct result of the scrapping of

multiple dwelling relief in this year’s budget). Yields are

commensurately different, with the expansion in oce yields

compared to other sectors historically aggressive.

Compared to an all-property valuation fall of -25% since June

2022, retail values have fallen -20%, industrial 27%

9

and oces

32% with the residential sample within MSCI down around 4%

and a BTR sample around -10%

10

.

Retail

Since values peaked in 2015, they have fallen in 23 of the

last 33 quarters, bottoming at -40% below 2015 peaks

(including events since 2022). Rental values are almost

-20% lower. This repositioning has led to the sector rising

up the ranks in many forecasts thanks to its strong

income returns (6.0%

12

) and growth potential, given its

more affordable rental base. We remain more cautious

than consensus, seeing continued risk to the consumer

in the near term, but do recognise opportunities at the

asset level where yields and rents have repriced and

where local demographics support long-term growth.

We feel the most compelling opportunities are in the

supermarket and retail park segments.

Leisure

Leisure now offers an income return of 6.7% from an

equivalent yield of 7.8%. The sector experienced a very

dicult Covid and, although we perceive consumer

expenditure shifting toward experiences from

discretionary purchasers as a long-term trend, the

cost-of-living crisis has also brought challenges.

Going forward, as these risks subside, income growth

on top of generous yields positions the sector well.

Industrial

More extensive views can be found in this paper, but in

short, we see industrial as a repriced sector offering

consistent growth potential for the long term, albeit with

notable segment differences which require careful

navigation. We prefer urban logistics and multi-let

industrials over, say, regional logistics, given different

supply and demand risks – although we think all

industrial segments could outperform the all-property

average over our forecasting horizon.

Residential

As with industrial, multiple segments with different

drivers offer a diversication of income styles within one

sector. We see most growth potential from BtR and

selective purpose-built student accommodation (PBSA),

with ination-linked income streams and the clear social

value upside offered by affordable housing. Despite

lower yields on average, we see the income growth

potential as signicant, potentially supporting

outperforming total returns both over our ve-year

horizon and on a long-term fundamental basis.

Oces

We offered more detailed thoughts in this series of blogs,

but in short we see MSCI valuations (reecting an average

of qualities) as near to fair value, given historic repricing,

but with higher quality oces much closer to this

threshold than lower quality oces, which in our view still

do not adequately compensate investors for known risks.

Although there could be some compelling income

streams on offer at generous yields, we still think it

unlikely that institutional investors will pivot towards the

sector while structural growth remains more convictional

in sectors like residential and industrial.

Other alternatives

We explain our approach to global megatrends in this

paper and this lens informs our long-term positioning in

various sectors within real estate and beyond. One eld

which straddles categories is digital infrastructure, in

particular data centres, where clear demand coincides

with a lack of appropriate built infrastructure.

Income styles: long income versus

operational

Yields available from long income investments with

ination linkage corrected sharply in 2022 and remain

generous relative to recent history. This could allow

institutional investors access to secure income streams

at higher yields than corporate equivalents.

At the other end of the risk spectrum, we are seeing more

operational styles in traditional segments like retail and

oces joining self-storage, hotels, student

accommodation and residential. Given the risks of

ination eroding operational income, caution on asset

and operator selection remains paramount here, but

where successful it can offer performance in real terms

and access to niche parts of the real estate market.

9. Source: -28% at their lowest (Feb 2023) but -27% at the end of April 2024

10. Source: MSCI Monthly Digest, April 2024

11. Source: BTR is our estimate of market build-to-rent residential capital value changes which were affected by the announcement

of the cessation of Multiple Dwellings Tax relief in the 2024 Spring Budget.

Capital value change (cumulative), peak to today, main MSCI sectors

Source: MSCI Monthly Digest, April 2024, LGIM Real Assets calculations

11

. Past performance is not a guide to the future. The value of an

investment and any income taken from it is not guaranteed and can go down as well as up, you may not get back the

amount you originally invested.

12. Source: MSCI Quarterly Digest, Q1 2024

-35

-30

-25

-20

-15

-10

-5

0

All prop Retail Office Industrial BTRMSCI Resi

%

Cumulative monthly, July ‘22

-

April ’24

Assumptions, opinions and estimates are provided for

illustrative purposes only. There is no guarantee that

any forecasts made will come to pass.

Assumptions, opinions and estimates are provided for illustrative purposes only.

There is no guarantee that any forecasts made will come to pass.

13

2024

|

Real estate reset: The case for UK property

12

2024

|

Real estate reset: The case for UK property

Valuations versus pricing: UK and international

By comparing valuation and transaction indices domestically

and internationally we can develop informed views on which

sectors are valued most eciently and which regional

investment destinations offer asset and fund valuations less

likely to be subject to further adjustment.

In the UK, a comparison of MSCI values and completed

transaction prices showed that, by the end of 2023, transaction

prices had moved by more than 7% compared to valuations

13

.

In the US, NCREIF has estimated oce cap rates at 6% and

pricing cap rates at 10.3%, with an average of 140 bps seen

across sectors

14

.

USA: Appraisal vs transaction cap rate, Q1 2024

Total forecast returns, 2024-2028

Source: NCREIF, LGIM Real Assets, May 2024. Past performance is not

a guide to the future. The value of an investment and any

income taken from it is not guaranteed and can go down as

well as up, you may not get back the amount you originally

invested.

Source: PMA Global Prime forecasts, Spring 2024. Assumptions, opinions and estimates are provided for illustrative purposes only.

There is no guarantee that any forecasts made will come to pass.

Industrial is a sector that has been more liquid than other

sectors and is therefore in our view more likely to see its

valuations match market pricing. We observe the widest

differential in the US, followed by Europe and then the UK,

where market pricing has now recovered ahead of valuations

15

.

It would seem, therefore, that the UK is further ahead in both

its return to fair value and in ecient pricing signals, although

we acknowledge persistent sector differentiation.

Forecasts and positioning

We expect UK real estate values to adjust -1% over this

calendar year

16

, led by oces, with a total return of around 5%

before modest yield compression and rental growth support

returns of around 7% p.a. between 2025 and 2028 inclusive.

This would equate to a full peak-to-trough value adjustment for

UK real estate of around 25%

17

with almost all of that now in

the past.

13. Source: MSCI transaction backed data. It is only available to the end of 2023 and hence misses further valuation adjustment which we expect

to bring valuations closer to market pricing. It also measures completed deals rather than bidding which can be slower to reect actual market adjustment

14. Source: NCREIF, May 2024

15. Source: Valuation data from MSCI, pricing data for Europe and US is from Green Street’s CPPI service. For UK it is JLL data, unweighted average for

Birmingham, Bristol, Edinburgh, Glasgow, Leeds, London, Manchester

16. Source: Based on MSCI’s UK Annual Digest

17. Source: Using the MSCI Quarterly Digest to reect intra-year movements

18. Source: PMA Global Prime forecasts, Spring 2024. Prime reects the change in estimated values for a high-quality well-located asset

This does, to some extent, rely on a managed path of interest

rate reductions but as we explored above, the market appears

well placed for most rate scenarios. The risk premium analysis

above is suggestive of upside risk to these forecasts, with

unlevered returns closer to 10%.

Forecasts for international performance show the UK is well

positioned, with PMA’s forecast of prime returns

18

showing

outperformance across global averages for all main sectors.

Although history is not guaranteed to repeat, analysis of

subsequent performance after previous downturns can also be

instructive. The graphs on the next page show returns on the

MSCI quarterly digest in the ve and 10 years after a cyclical

low point, assuming an investment is made in the period

immediately before or after a capital value trough. Given our

view that income curation and growth are the best ways to

navigate subsequent performance, with yield compression and

cyclical recovery more dicult to forecast and therefore best

seen as upside risks, we place lower weight on this analysis.

This is, however, illustrative of potential returns – before the

addition of leverage. It also shows that timing the trough of the

market precisely, very dicult in practice, does not make a

signicant difference to subsequent returns.

4.7

6

5.5

3.8

4.3

6.1

10.3

7.2

5

5.2

0

2

4

6

8

10

12

All property

Office

Retail

Industrial

Multifamily

Cap rate (%)

Appraisal cap rate Transaction cap rate

Industrial pricing and valuation around the world

(as at year-end 2023)

Source: MSCI, Green Street, JLL, LGIM Real Assets calculations.

Past performance is not a guide to the future. The value

of an investment and any income taken from it is not

guaranteed and can go down as well as up, you may

not get back the amount you originally invested.

MSCI peak to December 2023

Market pricing peak to today

MSCI Peak to December 2023 Market pr icing pe ak to today

-3

0%

-2

5%

-2

0%

-1

5%

-1

0%

-5%

0%

UK Europe US

0

1

2

3

4

5

6

7

8

9

Multifamily Retail Logistic

sO

ffice

%

Global average UK

0

50

100

150

200

250

2007

2009

2011

2013

2015

2017

2019

2021

2023

Capital raised ($bn)

Assumptions, opinions and estimates are provided for illustrative purposes only.

There is no guarantee that any forecasts made will come to pass.

15

2024

|

Real estate reset: The case for UK property

14

2024

|

Real estate reset: The case for UK property

UK all-property returns, unlevered, in the ve and 10 years after a capital value trough

19

Source: MSCI Quarterly Digest, Q1 2024, LGIM Real Assets calculations. Past performance is not a guide to the future. The value of an investment

and any income taken from it is not guaranteed and can go down as well as up, you may not get back the amount you originally

invested.

Conclusion

Analysis suggests the UK is well placed both domestically

and relative to international peers in terms of fair value, sector

relativities and growth potential. Equivalent yields in excess

of 7% with net operating income yields at 5.0% compare

favourably to other asset classes, with UK equities for example

yielding 3.8%

20

.

Real estate assets can provide investors with an income

stream they can potentially access at a cyclically cheaper entry

point that can be managed in an environmentally sustainable

way and can offer social benets.

Volatility in rates and potential shocks suggest portfolios tilt to

income resilience rather than binary yield compression plays,

with the latter seen as an upside risk. After an elongated period

of navigating external shocks, we believe the sector is

positioned for a period of attractive risk adjusted returns.

19. Another caveat to this analysis is that some holding periods coincide with the start of another externally driven downturn

(e.g. historically, the GFC and subsequent Eurozone crisis). Also, the MSCI index was more dominated by higher beta oces and retail historically.

20. Source: MSCI Quarterly Digest, Q1 2024

0

2

4

6

8

10

12

14

16

18

-12

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

5 year total return % p.a

Months before/after trough

Early 90s recession Mid 90s slowdown

Dotcom GFC Eurozone

0

2

4

6

8

10

12

14

16

18

-12

-11

-10

-9

-8

-7

-6

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

10 year return % p.a.

Months before/after trough

Early 90s recession Mid 90s slowdown

Dotcom GFC Eurozone

After an elongated period of

navigating external shocks, we

believe the sector is positioned

for a period of attractive risk

adjusted returns.

Assumptions, opinions and estimates are provided for illustrative purposes only.

There is no guarantee that any forecasts made will come to pass.

2024

|

Real estate reset: The case for UK property

Key risks

The value of an investment and any income taken from it is not guaranteed and can go down as well as up, you may not get back the

amount you originally invested.

It should be noted that diversication is no guarantee against a loss in a declining market. Assumptions, opinions and estimates are

provided for illustrative purposes only. There is no guarantee that any forecasts made will come to pass.

Important information

The views expressed in this document are those of Legal & General Investment Management Limited and/or its aliates (‘Legal & General’, ‘we’

or ‘us’) as at the date of publication. This document is for information purposes only and we are not soliciting any action based on it. The

information above discusses general economic, market or political issues and/or industry or sector trends. It does not constitute research or

investment, legal or tax advice. It is not an offer or recommendation or advertisement to buy or sell securities or pursue a particular investment

strategy. No party shall have any right of action against Legal & General in relation to the accuracy or completeness of the information contained

in this document. The information is believed to be correct as at the date of publication, but no assurance can be given that this document is

complete or accurate in the light of information that may become available after its publication. We are under no obligation to update or amend

the information in this document. Where this document contains third party information, the accuracy and completeness of such information

cannot be guaranteed and we accept no responsibility or liability in respect of such information. This document may not be reproduced in whole

or in part or distributed to third parties without our prior written permission. Not for distribution to any person resident in any jurisdiction where

such distribution would be contrary to local law or regulation.

LGIM Global

Unless otherwise stated, references herein to "LGIM", "we" and "us" are meant to capture the global conglomerate that includes:

Hong Kong: issued by Legal & General Investment Management Asia Limited which is licensed by the Securities and Futures Commission.

Singapore: issued by LGIM Singapore Pte. Ltd. (Company Registration No. 202231876W) which is regulated by the Monetary Authority of

Singapore. The LGIM Stewardship Team acts on behalf of all such locally authorized entities.

© 2024 Legal & General Investment Management Limited, authorised and regulated by the Financial Conduct Authority, No. 119272. Registered in

England and Wales No. 02091894 with registered oce at One Coleman Street, London, EC2R 5AA.

D008321

Contact us

For further information about LGIM, please visit lgim.com or contact your usual LGIM representative