2021

FULL-YEAR

RESULTS

FY-2021

OVERVIEW

JEAN-MARIE TRITANT

CEO

Lady Gaga concert, Westfield Les 4 Temps

Westfield Valley Fair

3

2021 FULL YEAR RESULTS2021 FULL YEAR RESULTS

Confirmed recovery in H2 with tenant sales

approaching pre-COVID levels with positive

footfall trajectory

Significant improvement in occupancy

demonstrating retailer demand

Proactive leasing strategy to protect long-

term value as conditions improve

Well-positioned to keep capitalising on

continued growth in 2022

2021 in review

Clear recovery in H2-2021

2021 FULL YEAR RESULTS

4

+190 bps

occupancy improvement

(vs. -60 bps in H1)

+2.2%

MGR uplift for leases

>36 months (vs. +1.3% in H1)

€56.7 Mn

C&E NOI

(vs. -€1.5 Mn in H1)

93%

tenant sales as % of 2019

(vs. 62% in H1)

92%

rent collection

(vs. 73% in H1)

€71.9 Mn

sales based rent

(vs. €34.2 Mn in H1)

2021 financial performance reflects operating conditions and

deleveraging progress

2021 FULL YEAR RESULTS

5

+4.7%

2021 AREPS

restated for disposals

vs. 2020 AREPS

-140 bps

IFRS LTV

improvement

(43.3% vs. 44.7% at FY-2020)

-€1.6 Bn

IFRS net debt

reduction

ESG integrated throughout business thanks to Better Places 2030

strategy

(1) Update from October 2021 2021 FULL YEAR RESULTS

6

Recognised leader

1

st

in RE industry and 5

th

in entire rating universe

(1)

4

th

year in a row

B rating (prime status)

first decile in the industry

ESG AAA rating

8

th

year in a row

Continued progress across all pillars in 2021

Joined Net Zero Initiative

Developing a collective

framework for carbon neutrality

1.5 million

vaccinations administered to

people at URW’s assets

34%

women in leadership vs.

commitment of ≥40% by 2025

Issuance of a €3.1 Bn sustainability-linked revolving

credit facility, the largest by a REIT in Europe

Substantial progress on deleveraging

2021 FULL YEAR RESULTS

7

European disposal programme

(2021/22)

Positioned for radical reduction

of financial exposure to the US

Strict CAPEX control

€2.5 Bn of €4.0 Bn target agreed

or completed

(€0.8 Bn secured at FY-2020)

Several processes ongoing; on

track to complete programme by

year end

€0.5 Bn of debt reduction

through portfolio streamlining

and disposals

Internal strategy exercise

completed, positioned to execute

€1.0 Bn of CAPEX spent in line

with commitment

€0.5 Bn of JV partnerships,

optimising capital allocation

US strategy on track

(1) Green Street Advisors rating, weighted by value

(2) Speciality tenants, excluding Apple and Tesla, weighted by sq. ft. 2021 FULL YEAR RESULTS

8

Radical reduction of financial exposure to the US on track

for 2022/2023

95% of URW’s US shopping centres

are in the “A” rating category

(1)

with

an average sales density

(2)

of $724

per sq. ft.

76% are A+ rated

(1)

or above with an

average sales density

(2)

of $872 per

sq. ft.

Superior Quality

Strong mall operating fundamentals

URW Flagship destinations

competitively stronger following

pandemic

Mall Recovery

Financing market improving

for A-rated malls

Transaction market will

follow

Markets Opening

Macro challenges partially offset by positive consumer trends

Sources: U.S. Bureau of Labor Statistics, Freightos, Dares, OECD 2021 FULL YEAR RESULTS

9

Labour shortages

Unemployment

7.6%

7.7%

3.7%

5.4%

9.7%

6.0%

2019 2020 2021E

+40%

higher retail worker turnover

in the US compared to 2020

118,700

restaurant and hotel workers

resigned in France (Jan-July 2021)

Eurozone US Eurozone 10y av. US 10y av.

Supply chain disruption

Household savings

6.5%

11.1%

7.9%

12.5%

7.0%

8.8%

2019 2020 2021E

Global Supply Chain Pressure

Index hits peak levels and is 4

st. dev. above long-term average

+85%

Shipping time between US

and China (Dec 2021 vs. Dec 2019)

Eurozone US Eurozone 10y av. US 10y av.

2019

2020

2021

COVID-19 restrictions

Retail trade

94

Days of closure in 2021 in Europe,

0 days in the US, 69 days globally

Local rules on capacity limits,

COVID-pass requirements and quasi-

lockdowns for the unvaccinated

107.3

114.2

104.9

121.7

100

Eurozone US Index basis

46%

63%

79%

81%

49%

74%

93%

93%

Q1 Q2 Q3 Q4

Tenant sales in H2-2021 reaching pre-COVID levels

2021 FULL YEAR RESULTS

10

Group figures, as percentage of 2019 levels:

Footfall Sales

US tenant sales now at pre-COVID levels

(1) Excluding Westfield World Trade Center and Westfield San Francisco Centre

(2) Restated for the Westfield UTC & Westfield Montgomery Arclight (Chapter 7) cinema closures,

relet to AMC and opening in February and March 2022, respectively 2021 FULL YEAR RESULTS

11

Category

Sales

Luxury

+42%

Home

+22%

Food Stores & Mass Merchandise

+9%

Fashion

+1%

F&B

-4%

Entertainment

-26%

(2)

77%

97%

102%

98%

83%

104%

108%

104%

Q1 Q2 Q3 Q4

Sales Sales non-CBD Flagships

(1)

US tenant sales (vs. 2019) Select category results H2-2021

(vs. H2-2019)

Broad-based recovery in Europe, despite remaining restrictions

2021 FULL YEAR RESULTS

12

Select category results H2-2021

(vs. H2-2019)

Category

Sales

Sport

+5%

Food Stores & Mass

Merchandise

-2%

Health & Beauty

-3%

Fashion

-12%

F&B

-13%

Entertainment

-20%

Footfall Sales

Continental Europe

81% 92%

UK

78%

83%

Europe

81%

90%

H2-2021 (in % of H2-2019)

55% leases +2.2% MGR uplift

44% leases +1.3% MGR uplift

H2

H1

1. Long-term leases (>36 months)

› Standard lease terms with MGR and an SBR top-up

› Demanding on the tenant quality

› Supports value of URW’s assets and generates stable cash flows

56% leases

-12.8% MGR uplift

-13.8% MGR uplift

H2

H1

2. Short-term leases (≤36 months)

› Pragmatic approach to lease terms

› Protect occupancy and optimise short-term cash-flow through

SBR

› Opportunity to convert to long-term leases under better economic

conditions

45% leases

Leasing strategy supports higher activity and long-term rental

value

(1) Excluding airports

NB: All letting figures exclude deals <12 months. 2021 FULL YEAR RESULTS

13

2,399 leases signed

(vs. 2,359 in 2019)

Sales Based Rent (SBR)

(1)

:

2019: €61.8 Mn 2020: €41.5 Mn 2021: €80.2 Mn

URW is the preferred partner for top brands

(1) For above mentioned retailers 2021 FULL YEAR RESULTS

14

Overall GLA

(1)

increased by +12.0% between 2019 and 2021

8 Deals

6 Deals

7 Deals

13 Deals 8 Deals

11 Deals

5 Deals

5 Deals

# deals in 2021

Nike flagship in Westfield London

+194%

in GLA

JD Sports in Westfield La Maquinista

+196%

in GLA

Zara in Westfield Les 4 Temps

+74%

in GLA

Apple in Westfield Valley Fair

+246%

in GLA

Emerging concepts choosing URW Flagship destinations

2021 FULL YEAR RESULTS

15

Pro-active strategy to introduce sustainable

and inclusive brands including second-hand stores

Food Society in Westfield La Part-Dieu

Youseum in Westfield Mall of the Netherlands Thérapie Clinic in Westfield London

Amazon 4-star in Westfield London

+40.8%

vs. 2020

(€33.5 Mn)

-25.0%

vs. 2019

(€62.8 Mn)

Parking: €47.2 Mn

Valet parking in Westfield Century City

Premium parking in Westfield Century City

Ongoing recovery in variable revenue streams

2021 FULL YEAR RESULTS

16

Commercial Partnerships: €76.2 Mn

+16.3%

vs. 2020

(€65.5 Mn)

-35.3%

vs. 2019

(€117.8 Mn)

Dior brand experience in Westfield London

Google Pop-Up in Westfield La Maquinista

Deepscreen technology in Westfield Mall of

Scandinavia

H&M Circular Design Story in Westfield WTC Infiniti car show in Westfield WTC

Netflix Squid Game in Westfield Century City

Trinity, La Défense

Success in office letting: Trinity

(1) Lease incentives in line with typical incentives given in La Défense. Excluding 2 floors for which

part of the rent is variable 2021 FULL YEAR RESULTS

17

% leased

(30,103 sqm)

63

€ Per sqm, weighted

average face rent

office GLA

(1)

Deals signed in 2021

7

559

3,500 sqm of green urban spaces, with 60

trees planted

HQE Exceptional and BREEAM Excellent

Built with low carbon concrete (-30% emissions)

Operable windows offering natural ventilation

FY-2021

FINANCIAL REVIEW

FABRICE MOUCHEL

CFO

Jazz concert in Westfield Chodov

€ Mn

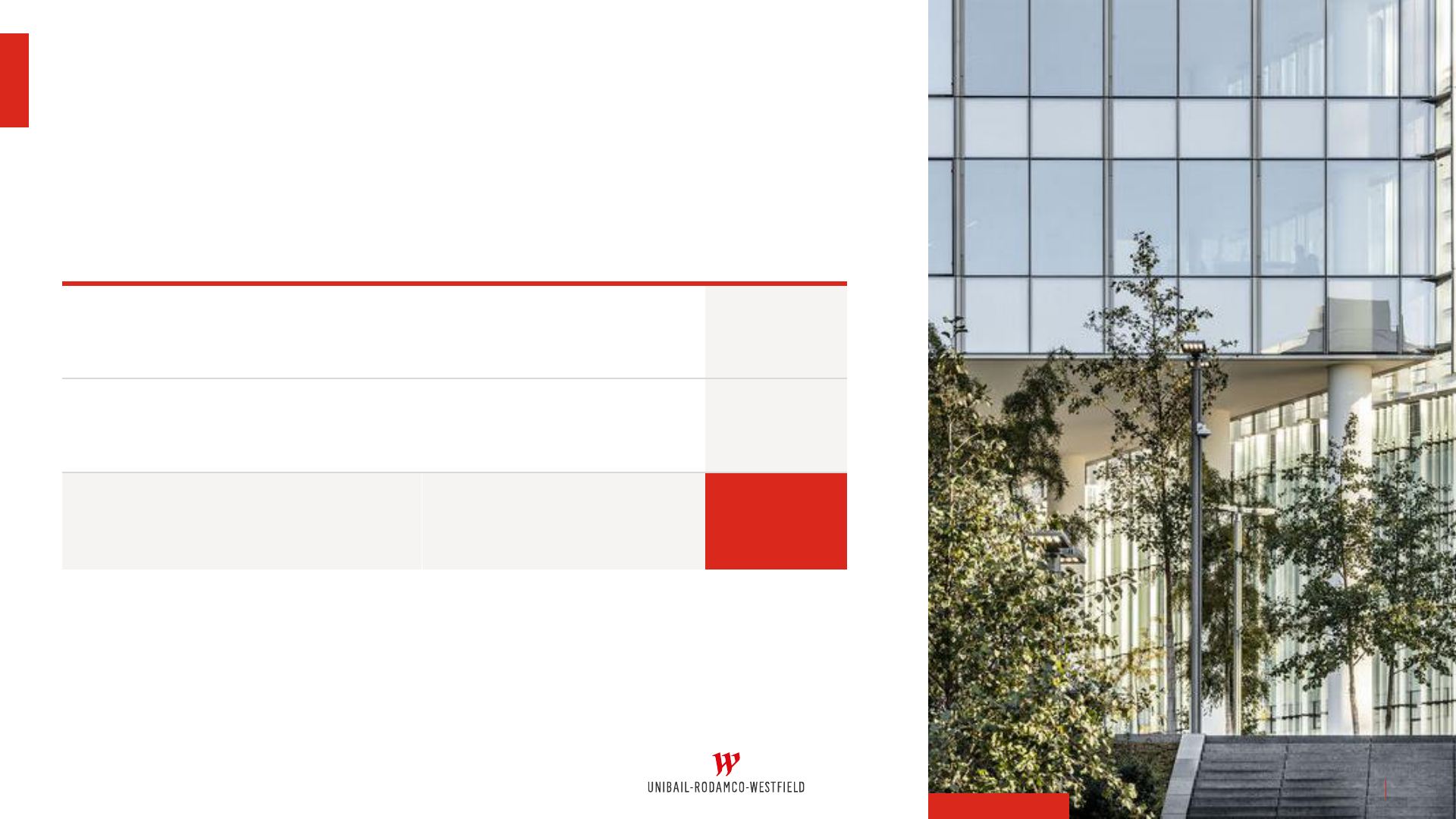

FY-2021 FY-2020 Change Lfl Change

Shopping Centres

1,632 1,699 -3.9%

-1.2%

(1)

Offices & Others

60 86 -29.7%

-6.6%

Convention & Exhibition

32 6 n.m.

n.m.

Net Rental Income

1,724 1,790 -3.7%

-1.6%

(2)

Recurring Net Result (Group share)

1,005 1,057

-4.9%

Recurring EPS 7.26

7.63

-4.9%

Adjusted Recurring EPS

(3)

6.91

7.28

-5.2%

FY-2021 Results

(1) Shopping Centres Lfl NRI excluding airports

(2) Group Lfl NRI including airports

(3) The Adjusted Recurring Earnings are calculated based on the Recurring net result for the period

attributable to the holders of the Stapled Shares minus the coupon on the Hybrid Securities

Figures may not add up due to rounding 2021 FULL YEAR RESULTS

19

FY-2021 AREPS down -5.2%, impacted by disposals

(1) Including taxes, services, airports, administrative expenses and others 2021 FULL YEAR RESULTS

20

€7.28

€6.60

€6.77

€6.91 €6.91

-€0.68

-€0.11

+€0.28

+€0.02

+€0.15

-€0.03

AREPS

2020

Disposals AREPS 2020

restated for

disposals

Financial

expenses

Retail deliveries Operating

performance

Retail & Offices

Convention &

Exhibition

Others AREPS

2021

(1)

+4.7% rebased

(1) XXX

NB: Excluding AIrport

Net closures,

renewals,

relettings and

indexation

COVID-19

rent relief SBR Other Total Lfl

Total

Lfl

excl.

straightlining

(2)

Total Lfl

2020

(3)

Continental Europe

-4.0% -0.3% 0.0% -3.2%

-7.5% -4.3%

-19.1%

United Kingdom

-21.4% +14.4% +5.6% +27.8%

+26.4% +27.0%

-49.3%

United States

-13.8% +1.7% +7.7% +17.1%

+12.7% +9.5%

-29.2%

Total URW Group

-7.2% +0.9% +2.0% +3.0%

-1.2% +0.5% -24.2%

Stable like-for-like retail NRI

(1)

(1) Excluding airports

(2) Excluding reversals, straight-lining and write-off of accruals related to COVID-19 rent relief

(3) Including airports Lfl NRI was -28.0% in the US and -24.0% for the Group 2021 FULL YEAR RESULTS

21

Improving rent collection as centres reopened

(1) Rent collection rate calculated compared to 100% of rents invoiced

(2) Rents invoiced net of adjustments

(3) As reported at the FY-2020 results

(4) On a proportionate basis: €94.8 Mn of receivables provisioned (including Offices & C&E), o/w

€97.3 Mn for shopping centres

NB: retail only, including rents, SBR, service charges and CAM, assets at 100%. Figures may not add up

due to rounding 2021 FULL YEAR RESULTS

22

100%

86% 86% 86%

10%

4%

0%

Invoiced Relief granted Provisioned Remaining

overdue and

not due yet

Collected as at

December 31,

2021

(4)

As at December 31, 2021

Fully provisioned

Collected

Continental

Europe

UK

Q2

(1)

85% 80% 94% 93%

(2)

Q3

(1)

93% 94% 93% 93%

(2)

Q1

(1)

83% 80% 80% 91%

(2)

Q4

(1)

90% 91% 93% 87%

(2)

FY

(1)

88% 86% 90% 91%

(2)

US

2020

(1)(3)

80% 85% 79% 70%

As at February 3, 2022

Sector split of bankruptcies:

35%

23%

11%

8%

5%

18%

Food & Beverage Fashion apparel Health & beauty

Bags, Footwear & Accessories Home Other

Cont. Europe UK US URW

# of stores

204 19 58 281

% of total units

2.8% 2.8% 1.5% 2.4%

In place 122 11 27 160

Replaced 53 0 15 68

In place

/ replaced

86% 58% 72% 81%

Vacant

29 8 16 53

Lower bankruptcies in 2021

(1) Revenues (including service charges) of tenants that are in some form of bankruptcy procedure

and currently still in place, as % of 2021 2021 FULL YEAR RESULTS

23

Annualised potential

revenue exposure

(1)

: 1.7%

Bankruptcies down -57% vs. FY-2020

2.5%

7.7%

9.1%

5.4%

4.9%

9.7%

13.1%

8.3%

5.0%

12.2%

14.0%

8.9%

4.0%

10.6%

11.0%

7.0%

Continental

Europe

UK US Group

Vacancy levels decreased in H2-2021

2021 FULL YEAR RESULTS

24

FY-2019 vacancy

FY-2020 vacancy

H1-2021 vacancy

FY-2021 vacancy

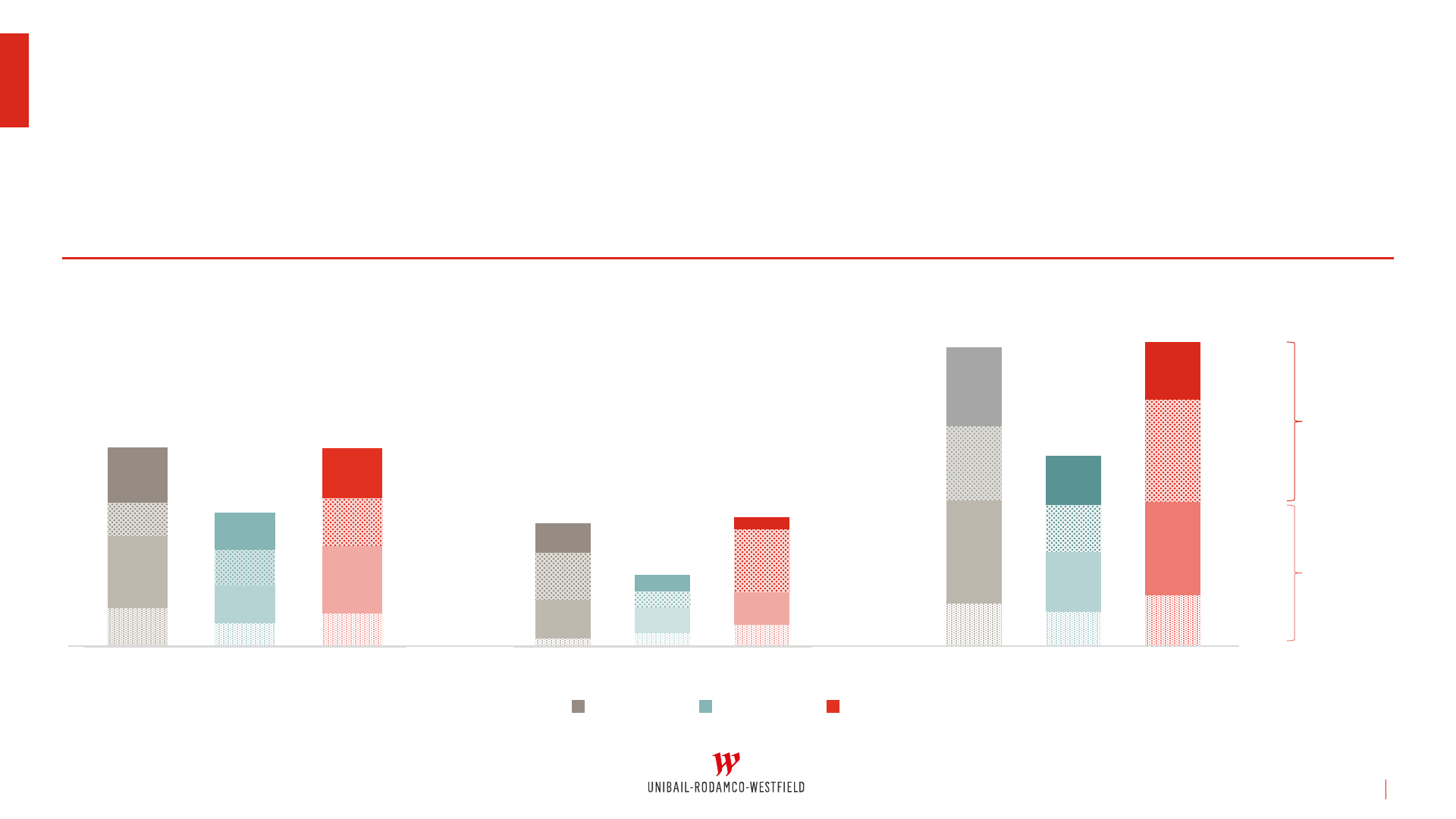

Letting activity back at 2019 levels

(1) Including the UK

NB: All letting figures exclude deals <12 months. Short-term refers to leases between 12 and 36

months inclusive, long-term refers to leases >36 months. Usual 3/6/9 leases in France are included in

the short-term leases 2021 FULL YEAR RESULTS

25

2,399 leases signed

+2% vs. FY-2019

+60% vs. FY-2020

2019 2020 2021

LETTINGS/

RELETTINGS

RENEWALS

0

500

1000

1500

2000

2500

0

500

1000

1500

2000

2500

0

100

200

300

400

500

600

700

800

900

1000

1100

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

2200

2300

2400

2500

Europe

(1)

1,442

US Group

971

1,437

917

532

962

2,359

1,503

2,399

Long-term

Short-term

Long-term

Short-term

Positive uplift on long-term deals and decreasing proportion

of short-term deals

(1) Usual 3/6/9 leases in France are included in the short-term leases. Restated for this, the

percentage of deals between 12 to 36 months in Continental Europe would be 34% in H1 and 32%

in H2 2021 FULL YEAR RESULTS

26

Continental Europe

(1)

UK US Group

12-36

months

>36

months

Total

12-36

months

>36

months

Total

12-36

months

>36

months

Total

12-36

months

>36

months

Total

MGR Uplift

-7.4%

+4.6%

-0.5% -26.2%

-3.7%

-7.6% -17.8%

+1.0%

-11.0% -13.4%

+1.8%

-5.2%

72%

56%

28%

44%

H1-2021 H2-2021

27%

31%

73%

69%

H1-2021 H2-2021

45%

40%

55%

60%

H1-2021 H2-2021

56%

45%

44%

55%

H1-2021 H2-2021

1,181

40798

676

% deals

12-36 months

>36 months

589

555

74

1,218

›

Significant increase in SBR in

2021 on the back of improving

retailer performance

›

Almost equivalent total

revenues with higher weight of

SBR

›

Opportunity to convert to long-

term leases under better

economic conditions

Increase in SBR partly compensates loss in MGR in the US

2021 FULL YEAR RESULTS

27

18.4

18.3

50.1

€ 18

18.8

13.0

21.8

-22.1

2019 2020 2021 Annualised SBR Annualised MGR

reduction

Renewals, relettings

signed in 2021

(1)

Annualised

In € Mn

US SBR (excl. airports)

Renewals, relettings

signed in 2021

(1)

(1) Including full SBR deals

NB: estimated annualised figure, taking into account seasonality effects

Trinity, La Défense

Offices & Others:

NRI impacted by disposals

2021 FULL YEAR RESULTS

28

Net Rental Income

(€ Mn)

FY-2021 FY-2020 Change

Lfl Change

France

35 56 -37.7%

2.4%

Others

25 30 -14.6%

-15.3%

Total

60 86 -29.7%

-6.6%

Convention & Exhibition: strong recovery of activity in H2

(1) Signed as at January 2022

(2) Non-cancellable bookings, signed as at January 2022

NB: all events are required to comply with local guidelines 2021 FULL YEAR RESULTS

29

278

events in H2-2021

vs. 294 in H2-2019

401

pre-bookings 2022

(1

)

o/w 254 bookings

(2)

Strong interest from organisers for 2021-2022

81%

number of events

pre-booked for the

year vs. pre-bookings

as at January 2018

Recovery

Back to “normal”

Paris Olympics

H2-2021 - 2022

H1-2023

From H2-2023

KCorp Experience, Palais des Congrès de Paris

Who’s Next, Paris Expo Porte de Versailles

€ Mn

FY-2021 H1-2021 FY-2020 FY-2019

Change N

vs N-2

Net Rental

Income

32 0 6 95 -66.9%

Property Services

& Other Income

24 -2 6 62 -61.6%

Net Operating Income

55 -2 12 157 -64.8%

Convention & Exhibition: positive results upon reopening

2021 FULL YEAR RESULTS

30

NB: Figures may not add up due to rounding

December 2020 Disposals Lfl revaluation Non Lfl revaluation &

revaluation of shares

CAPEX /

Acquisitions /

Transfers

Currency Effect December 2021

€56,314 Mn

€54,473 Mn

-€196 Mn

+€1,063 Mn

-€1,956 Mn

-€1,939 Mn

+€1,187 Mn

GMV evolution mainly driven by disposals

and like-for-like revaluation

2021 FULL YEAR RESULTS

31

Shopping centre valuations bottoming out in H2 in Continental

Europe

(1) Based on the Lfl revaluation reported

NB: retail only. Figures may not add up due to rounding 2021 FULL YEAR RESULTS

32

-1.3%

-8.5%

-1.6%

-2.0%

-9.1%

-26.3%

-12.6%

-11.3%

-1.7%

-9.1%

-2.7%

-2.5%

-0.3%

-5.2%

-5.5%

-1.9%

Continental Europe

(69% of GMV)

UK

(6% of GMV)

US

(25% of GMV) URW

Lfl revaluation since Dec 31, 2018

(1)

-12%

-42% -21%

-17%

-2.0%

-14.0%

-8.2%

-4.4%

Total revaluation

since 2018:

Revaluation 2019 Revalutation 2020 Revalutation H1-2021 Revalutation H2-2021

URW revenues hedged against inflation through indexation and SBR

2021 FULL YEAR RESULTS

33

(1) Shopping Centre GMV only

(2) Including airports

Sources: ECB

~90% of the leases tied to retailer

sales through SBR clauses

SBR: 15.9% of 2021 NRI

(2)

Continental Europe: 69% of GMV

(1)

UK: 6% of GMV

(1)

US: 25% of GMV

(1)

~50% of the leases tied to retailer sales

through SBR clauses

SBR: 5.5% of 2021 NRI

All rents indexed

SBR: 2.3% of 2021 NRI

0%

1%

2%

3%

4%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Eurozone inflation Indexation URW NRI N+1

Cap rates protected by high risk premiums

2021 FULL YEAR RESULTS

34

4.3%

0.0%

4.3%

4.4%

2007

08

09

10

11

12

13

14

15

16

17

18

19

20

21

France

+440 bps

4.5%

0.7%

5.7%

5.3%

08 09 10 11 12 13 14 15 16 17 18 19 20 21

UK

+460 bps

4.6%

1.4%

5.8%

4.2%

2007

08

09

10

11

12

13

14

15

16

17

18

19

20

21

US

+280 bps

URW NIY / WFD Estimated Yield (weighted avg.)

10-year gov. bond yield (1-year avg.)

€0 Bn

€5 Bn

€10 Bn

€15 Bn

€20 Bn

€25 Bn

2022 2023 2024 2025 2026

Pro-forma

(1)

proportionate

Net Financial

Debt €23.9 Bn

Annual projection of average hedging amounts and fixed rate debt up to 2026

The Group’s debt is fully hedged

2021 FULL YEAR RESULTS

35

(1) Pro-forma for the receipt of the proceeds from the disposal of Solna Centrum and a 45% stake in

Westfield Carré Sénart

NB: as at Dec. 31, 2021

Debt kept at fixed rate Macro hedges (swaps & caps) Optional

Marginal sensitivity to interest rates evolution

2021 FULL YEAR RESULTS

36

(1) The theoretical impact of a rise or decrease in interest rates is calculated relative to the

applicable rates as at December 31, 2021: 3m Euribor (-0.572%), 3m USD Libor (0.209%) and 3m

GBP Libor (0.262%)

NB: on a proportionate basis; GBP is fully hedged

+€21.4 Mn

-€21.4 Mn

-€32.1 Mn

-€32.7 Mn

+€0.3 Mn

-€0.3 Mn

-€1.2 Mn

-€2.5 Mn

-25 bps +25 bps +100 bps +200 bps

Interest rates:

Impact of increase in rates

(1)

on 2022 recurring financial expenses

100 bps

EUR US

75 bps

EPRA NRV evolution

(1) Hybrid securities are excluded from NAV

(2) Including the capital gain on disposals

(3) Including a positive FX effect, offset by a negative impact of taxes and the fair value of financial

instruments 2021 FULL YEAR RESULTS

37

EPRA Net Reinstatement Value

(1)

(in € per share)

(2)

(3)

December 2020 Lfl Asset Revaluation Non Lfl Asset

Revaluation &

Intangible Assets

Recurring Results Goodwill impairment Other December 2021

€166.80

€159.60

+€7.26

-€12.69

-€0.20

-€0.52

-€1.05

2020

€24.2 Bn

(3)

Disposals &

foreclosures

-€2.3 Bn

Recurring Earnings -€1.0 Bn

Working capital -€0.2 Bn

FX +€0.4 Bn

CAPEX +€1.1 Bn

Others

(4)

+€0.4 Bn

2021

€22.6 Bn

(3)

(1) Pro-forma for the receipt of the proceeds from the disposal of Solna Centrum and a 45% stake in

Westfield Carré Sénart

(2) Excluding goodwill not justified by fee business as per the Group’s European bank debt leverage

covenants

(3) On an IFRS basis

(4) Including deferred payments, rental guarantees paid, the full consolidation of Westfield

Trumbull debt following the acquisition of the JV partners’ interest and other non-recurring

items

NB: All figures excluding the hybrid 2021 FULL YEAR RESULTS

38

Proportionate LTV: 44.9% or 44.2% pro-forma

(1)

(vs. 46.3% as at FY-2020)

(1)

€24.2

€24.2

€22.6

€22.1

38.6%

44.7%

43.3%

42.5%

35%

40%

45%

50%

21.0

22.0

23.0

24.0

25.0

2019 2020 2021 2021 pro-forma

Net Financial Debt in Bn EUR IFRS LTV

(2)

LTV improving on net debt reduction

Net debt to EBITDA

(2)

8.5

8.5

10.5

9.9

14.6

16.6

13.7

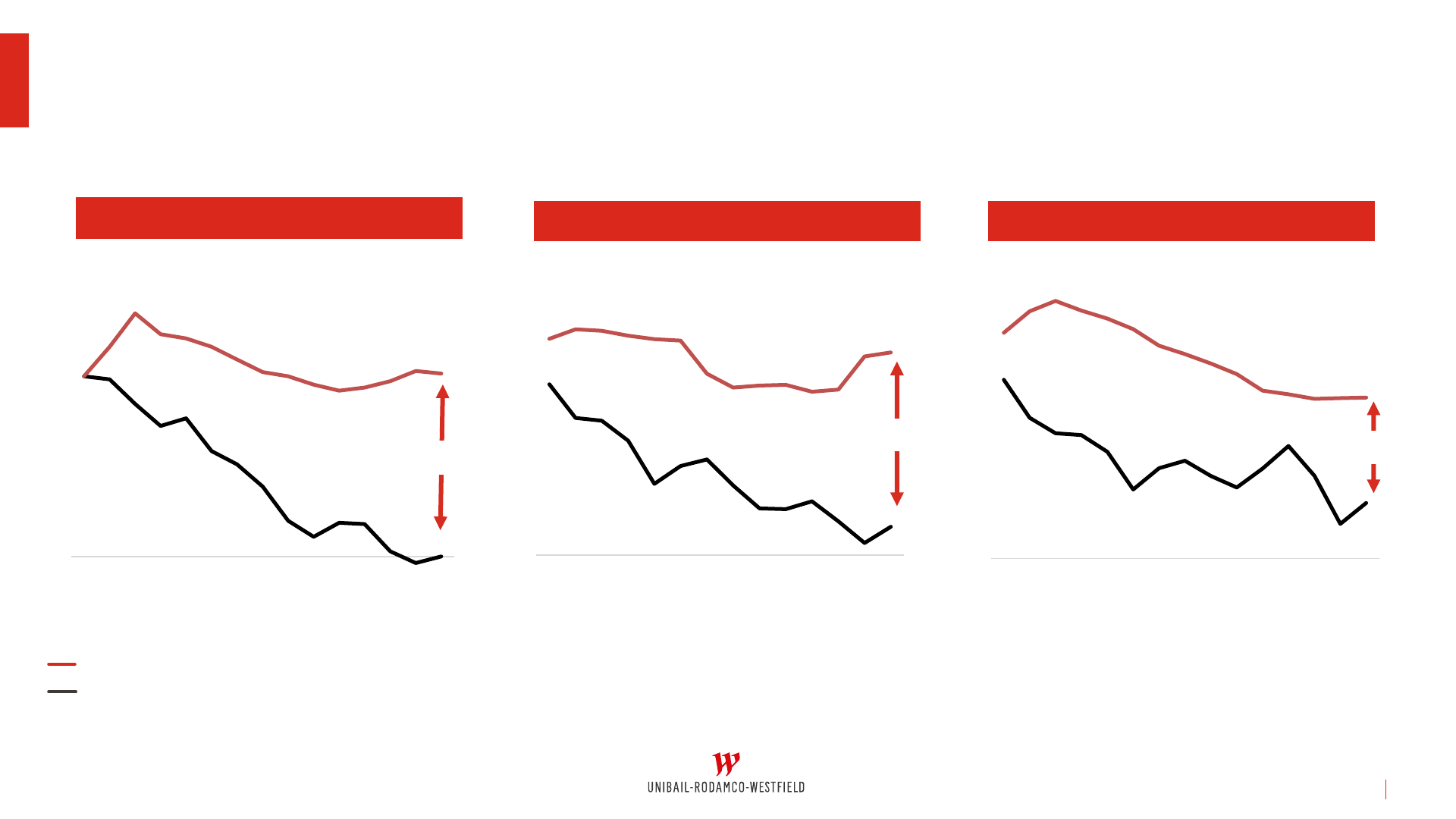

Improving credit ratios still reflect major impact of COVID-19

(1) A waiver of the FFO/Net financial debt ratio test in H1 and FY-2021 has been granted by URW’s

lending banks for its corporate bank debt

(2) On a L12M basis 2021 FULL YEAR RESULTS

39

Interest cover ratio

3.5

4.6

5.9

6.7

6.1

5.7

3.5

2.9

3.3

2.0

Typical covenant level

FFO / NFD

8.7%

9.3%

8.8%

9.7%

7.8%

8.1%

4.8%

4.3%

5.0%

4.0%

(waivers

obtained

(1)

)

Senior Bonds

€699 Mn

0.4 year

residual maturity

2.72%

average coupon

Mortgage debt

(2)

€400 Mn

1.0 year

residual maturity

Sustainability linked

€3,100 Mn

5 year

average maturity

Margin linked to the

Sustainable Target Score of

the Group

Bilateral facilities

€850 Mn

4 year

average maturity

Senior bonds

€1,250 Mn

9.6 year

average maturity

1.05%

average coupon

Mortgage debt

(1)

€494 Mn

6.2 year

average maturity

Favourable credit market access and strong liquidity position

(1) Related to Westfield Shopping City Süd, Aupark and Aquaboulevard & Le Sextant,

included in proportionate debt

(2) Related to Westfield Arkadia and Galeria Mokotow

(3) Taking into account the undrawn credit lines, subject to covenants

(4) On an IFRS basis 2021 FULL YEAR RESULTS

40

Debt

raised

Credit

facilities

Active debt

buy back

€2.3 Bn

cash on hand

(4)

€9.9 Bn

undrawn credit facilities

8.6 year

average debt maturity

(3)

>36 months

liquidity secured

Favourable access to credit markets and ample liquidity underpins strategy

Deleveraging plan on track

2021 FULL YEAR RESULTS

41

Suspend dividend payment

for fiscal

years 2020, 2021

and 2022

Complete €4.0 Bn

European disposal

programme

(2021/2022)

Controlled CAPEX

deployment with

focused development

pipeline and reduced

cost base

Radically reduce financial

exposure

to US in 2022/2023

Objectives

€2.5 Bn in total

agreed/completed

Pipeline reduced

by -€1.2 Bn

€1.0 Bn of CAPEX spent in

line with commitment

Internal strategy exercise

completed, positioned to

execute

Regional asset streamlining

FY-2021 progress

European disposal programme well advanced

Figures may not add up due to rounding

(1) IFRS net debt reduction

(2) Including other classes of asset (land, building rights, projects) for a minor part of the amount

42

2021 FULL YEAR RESULTS

€2.5 Bn

(1)

disposals 4.4% NIY +6.2% vs. last appraisal

2021 FULL YEAR RESULTS

100% sale

of mature offices

crystallising value creation

SHiFT

7 Adenauer

€1.4 Bn

(1)(2)

3.9% NIY

+12.3% vs.

last appraisal

Offices – 56% of disposalsRetail – 44% of disposals

100% sale

of assets not core to the Group’s

strategy

JV partnerships

with long-term institutional partners,

leveraging on URW management skills

Solna CentrumWestfield Carré Sénart

€1.1 Bn

(1)

4.8% NIY

+1.6% vs.

last appraisal

US regional portfolio streamlining

(1) Speciality sales, 2019 figures, excluding Apple & Auto

(2) FY-2020 figures

€0.5 Bn of disposals and foreclosures with associated debt exiting the portfolio

Debt reduction: €0.4 Bn

Capital gain: €44 Mn

Ownership transfer of Citrus Park, Countryside,

Broward, Sarasota and Palm Desert

Asset quality of foreclosed assets below average

portfolio:

– Sales / sq. ft.: $356 (vs. $606 avg. US portfolio)

(1)

– Occupancy

(2)

: 80% (vs. 87% avg. US portfolio)

2021 FULL YEAR RESULTS

43

Disposal of URW’s 50% stake in Palisade Residential at

Westfield UTC at 15% premium to the latest appraisal

€0.1 Bn proceeds

Palisade at Westfield UTC

Development pipeline reduction through deliveries

and Triangle partnership

(1) Please refer to the MD&A for definitions

Figures may not add up due to rounding 2021 FULL YEAR RESULTS

44

€2.4 Bn

€1.1 Bn

€0.9 Bn

€0.8 Bn

FY-2020 Deliveries Triangle Partnership Project changes FY-2021 Invested to date Remaining to be spent

€3.2 Bn

€1.9 Bn

€4.4 Bn

+€0.2 Bn

-€0.9 Bn

-€1.4 Bn

-€0.5 Bn

Committed

(1)

Controlled

(1)

Focus on two main mixed-used projects

(1) Forward sale, included in Retail GLA in development note

(2) Disposed, not included in development note

(3) Letting / pre-letting: GLA signed, all agreed to be signed and financials agreed 2021 FULL YEAR RESULTS

45

Expected combined stabilised NRI >€110 Mn

Gaîté Montparnasse

Retail GLA

29,287 sqm

URW Ownership

100%

Opening

H2-2021

H1-2022

Hotel GLA

51,835 sqm

Residential GLA

(1)

3,967 sqm

Offices GLA

13,101 sqm

Pre-letting

(3)

100%

Pre-letting

(3)

80%

Management

contract

100%

Total GLA

89,190 sqm

100% TIC

€1,300 Mn

Retail GLA

95,401 sqm

URW Ownership

100%

Opening

H2-2023

Hotels GLA

27,923 sqm

Residential GLA

(2)

42,950 sqm

Westfield Hamburg

Offices GLA

48,326 sqm

Pre-letting

(3)

0%

Pre-letting

(3)

47%

Pre-letting

(3)

100%

Total GLA

214,600 sqm

Outstanding

project

Attractive IRR

URW’s best-in-

class project

management

expertise

Partnership with AXA IM Alts to launch the Triangle project

2021 FULL YEAR RESULTS

46

Tailor-made partnership to optimise capital allocation, paving the way for future growth

Excellent

Exceptional

1,000 sqm of PV panels, supply the

equivalent of lighting for 25,000 sqm

of workspace

Annual carbon emissions >50% lower

than average emissions of existing

tertiary sector

Annual Energy consumptions (conventional)

>66% lower than average consumptions of

existing tertiary sector

Structure and façade designed

to accommodate different uses over time

Optimised

JV set-up

30% remaining

stake for URW

€395 Mn non-

recourse loan

First class JV-

partner

Attractive

returns

for URW

Return through

30% stake and

promote

Limits URW’s

equity

contribution

Triangle

CONCLUSION

JEAN-MARIE TRITANT

CEO

Job Fair at Westfield Forum des Halles

Capitalising on continued growth in 2022 and beyond

2021 FULL YEAR RESULTS

48

Guidance for 2022 – Adjusted Recurring EPS of €8.20 - €8.40

URW will continue to build on improving market conditions and

demonstrated recovery in tenant sales and footfall

The Group benefits from built in protection against inflation and

interest rate increases

Operational improvement will drive strong leasing performance

and lower vacancy in 2022

URW will complete the European disposal programme and is

positioned to radically reduce its financial exposure to the US,

improving the LTV

URW Investor Day

March 30, 2022

10:30 am CET

APPENDIX

Westfield Euralille

Upcoming debt refinancing

Nb: URW’s financial debt profile as at December 31, 2021. On an IFRS basis. Excluding from chart:

€1,250 Mn Hybrid NC 2023 and €750 Mn Hybrid NC 2026 treated as equity under IFRS and undrawn

facilities 2021 FULL YEAR RESULTS

1.5

0.8

1.7

3.1

1.3

16.4

1.2

5.0

16.4

0-1 Y 1-2 Y 2-3 Y 3-4 Y 4-5 Y > 5 Y

50

Without undrawn credit lines and cash on hand With undrawn credit lines and cash on hand

In € Bn

Cost of debt and average debt maturity over time

(1) Including SEK 2021 FULL YEAR RESULTS

51

Average Maturity

(years)

4.3

4.5

4.9

5.4

5.9

6.5

7.0

7.2

7.5

8.2

8.4

8.6

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Average Cost of Debt

3.9%

3.6%

3.4%

2.9%

2.6%

2.2%

1.6%

1.4%

1.6%

1.7%

2.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

EUR

(1)

1.5%

USD & GBP

3.9%

URW.COM

52