© CENTER FOR AUTOMOTIVE RESEARCH | 2019 i

U.S. Consumer & Economic

Impacts of U.S. Automotive

Trade Policies

Michael Schultz

Kristin Dziczek

Yen Chen

Bernard Swiecki

FEBRUARY

2019

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 i

Table of Contents

Acknowledgments ........................................................................................................................................ iii

Executive Summary ....................................................................................................................................... 1

Introduction .................................................................................................................................................. 3

Trade and the U.S. Automotive Industry ...................................................................................................... 3

Policy Specifics .............................................................................................................................................. 6

Section 232 Tariffs on Imported Light Vehicles & Vehicle Parts ............................................................... 6

USMCA ...................................................................................................................................................... 6

Section 301 Tariffs on Imports from China ............................................................................................... 8

Section 232 Tariffs on Imported Steel & Aluminum ................................................................................. 9

Summary of Methods ................................................................................................................................... 9

Simulation Model ...................................................................................................................................... 9

Simulation Inputs .................................................................................................................................... 10

Section 232 Tariffs on Imported Light Vehicles & Vehicle Parts ............................................................. 10

USMCA .................................................................................................................................................... 10

Section 301 Tariffs on Imports from China ............................................................................................. 11

Section 232 Tariffs on Imported Steel & Aluminum ............................................................................... 11

U.S. Light Vehicle Production Capacity ................................................................................................... 12

Uncertain Impacts on Used Vehicles Prices, Repair, & Maintenance Costs ............................................... 12

Policy Scenarios ........................................................................................................................................... 13

Results ......................................................................................................................................................... 14

Conclusions ................................................................................................................................................. 17

Works Cited ................................................................................................................................................. 18

Methodology Appendix .............................................................................................................................. 21

The Simulation Model ............................................................................................................................. 21

Compliance with USMCA Rules of Origin ................................................................................................ 22

Section 232 and Section 301 Tariffs ........................................................................................................ 24

Known Biases .......................................................................................................................................... 26

Scenario Results Without Capacity Constraints ...................................................................................... 27

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 ii

Lis

t of Figures

Figur

e 1: Sourcing of U.S. Light Vehicle Sales, 2017 ..................................................................................... 4

Figure 2: Sourcing of U.S. Motor Vehicle Parts Imports, 2017 ..................................................................... 5

Figure 3: U.S. Consumer Price Indices for All Items-Except Food & Energy, and New Vehicles, 1994-2018 6

List of Tables

Tab

le 1: USMCA Regional Value Content Requirements .............................................................................. 7

Table 2: Overview of U.S. Automotive Trade Scenarios Analyzed .............................................................. 14

Table 3: Source of Impacts, by Specific Policy, by Scenario ........................................................................ 15

Table 4: Change in U.S. Light Vehicle Sales and Prices Under Various U.S. Automotive Trade Policies ..... 16

T

able 5: Change in Dealership Revenue, Employment, U.S. GDP, and Overall U.S. Employment Under

Various U.S. Automotive Trade Scenarios ................................................................................................. 16

T

able 6: Change in U.S. Light Vehicle Sales, and Prices Under Various U.S. Automotive Trade Policies --

Capacity Unconstrained .............................................................................................................................. 28

Table 7: Change in Dealership Revenue, Employment, U.S. GDP, and Overall U.S. Employment Under

Various U.S. Automotive Trade Scenarios – Capacity Unconstrained ........................................................ 28

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 iii

Acknowledgments

The authors would like to thank Diana Douglass, and Jack Ombry at the Center for Automotive Research

for their assistance with this briefing. This research was sponsored by the National Automobile Dealers

Association.

Fo

r citations and reference to this publication, please use the following:

Schultz, M., Dziczek, K., Chen, Y., and Swiecki, B. (2019). U.S. Consumer & Economic Impacts of

U.S. Automotive Trade Policies. Center for Automotive Research, Ann Arbor, MI.

3005 Boardwalk, Suite 200

Ann Arbor, MI 48108

www.cargroup.org

CAR’s mission is to conduct independent research and analysis to educate, inform and advise

stakeholders, policymakers, and the general public on critical issues facing the automotive

industry, and the industry’s impact on the U.S. economy and society.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 1

Executive Summary

A decision to impose tariffs on U.S. imports of autos and auto parts under Section 232 of the Trade

Expansion Act of 1962, as amended (hereafter, “Section 232 autos and auto parts tariffs”), could far

outweigh the impact of any previous trade action on the U.S. automotive industry, and on related U.S.

consumer prices, sales, and employment. Moreover, this is true even though the implementation of the

new United States Mexico Canada Agreement (USMCA) and other trade agreements will partially

mitigate the effects of these tariffs.

The Center for Automotive Research (CAR) looked at ten different policy scenarios, projecting different

combinations of policies and U.S. trade deals including: Section 232 autos and auto parts tariffs; the

USMCA; the current (as of January 21, 2019) Section 301 tariffs on Chinese imports; and the current

Section 232 steel and aluminum tariffs. Across all these policy scenarios, the impact on the U.S. new

vehicle market and the broader U.S. economy is (1) substantial and (2) nearly entirely determined by the

severity of the potential Section 232 tariffs on imported autos and auto parts.

Worst-case scenario

Under the scenario where (1) the USMCA is implemented in its current form, (2) other tariffs continue

unmodified, and (3) the Section 232 auto and auto parts tariffs are imposed except on Canada, Mexico,

and South Korea, the following will likely occur:

• A total of 366,900 U.S. jobs will be lost;

• U.S. light-duty vehicle prices will increase by USD 2,750 on average;

• U.S. new light-duty vehicle sales will drop by 1,319,700 units per year; and

• Many consumers will be forced into the used car market.

Importantly, in this worst-case scenario, the broad-based Section 232 autos and auto parts tariffs will be

responsible for over 90 percent of the total economic harm.

Other scenarios

A range of current and potential U.S. trade actions will impact the U.S. automotive industry going

forward – from the new USMCA, to current tariffs on imports from China and imported steel and

aluminum products from a wide range of trading partners, to the potential for new tariffs on imported

automobiles and auto parts. No matter how these policies are combined, they operate to raise

consumer prices for new vehicles, while lowering U.S. light vehicle sales, U.S. Gross Domestic Product

(GDP), and total and new vehicle dealership employment.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 2

In every scenario considered new vehicle dealership revenue and employment fall. Dealerships are likely

to experience a decline in revenue totaling between USD 6.1 billion and USD 43.6 billion, with associated

employment losses of between 10,700 and 77,000 employees. For the average dealership, these losses

correspond to a fall in revenue ranging from USD 362,000 to USD 2.6 million, with corresponding

employment losses of 0.6 to 4.6 employees. In the broader economy, U.S. GDP is projected to fall

between USD 6.0 billion and USD 30.4 billion and total economy-wide employment would decline by

between 71,200 and 366,900 jobs. In addition, higher prices for new vehicles will impact the market for

used vehicles as well as raise the price of repair and maintenance parts – thereby raising the overall cost

of vehicle ownership for consumers.

While there are many moving pieces in U.S. trade policy, the range of likely outcomes from (1) the

implementation of the USMCA, (2) continuation of Section 301 China tariffs, (3) the Section 232 steel

and aluminum tariffs, and (4) a range of possible Section 232 auto and auto parts tariffs are all

profoundly negative for consumers, for new vehicle dealership revenue and employment, and for

overall U.S. economic output and employment levels.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 3

Introduction

Since the early days of the 2016 U.S. presidential campaign, President Trump pledged to revamp U.S.

trade policy. The first two years of the Trump Administration have seen dramatic and, at times, rapid

changes as the President seeks to prioritize U.S. manufacturing employment and investment. Many of

the enacted or proposed policy changes have profound impacts on the U.S. and North American

automotive industry, consumer prices for autos and auto parts, and the broader economy.

This briefing provides a quantitative analysis of current and proposed trade policy impacts on the U.S.

automotive industry and updates CAR’s Trade Briefing: Consumer Impact of Potential U.S. Section 232

Tariffs and Quotas on Imported Automobiles & Automotive Parts that was released in July 2018 (Schultz,

Dziczek, Swiecki, & Chen, 2018). This briefing expands on the July report and considers four specific

policies: The United States-Mexico-Canada Agreement (USMCA), Section 232 national security tariffs on

imported steel and aluminum, Section 301 tariffs implemented against imports from China, and the

potential for Section 232 national security tariffs on imported autos and auto parts. The Center for

Automotive Research (CAR) evaluated ten policy scenarios to estimate the combined effect of adopting

each of these four policies. The scenarios differ by which countries are assumed to be subject to the

potential auto and auto parts tariffs, and whether Canada and Mexico win exemptions from U.S. tariffs

on imported steel and aluminum.

Trade and the U.S. Automotive Industry

The U.S. market relies on imported light vehicles and automotive parts to meet consumer demand.

While the United States produced over 11 million light vehicles in 2018, light vehicle sales were 17.3

million. (IHS, 2018). In 2017, the dollar value of imported light vehicles and parts totaled over USD 340

billion (U.S.A. Trade Online, 2018). That year, 48 percent of all vehicles sold in the United States were

imported – with 25 percent imported from NAFTA partners: Canada (11 percent) and Mexico (14

percent) (IHS Markit).

NAFTA ranks third globally in terms of light- and medium-duty vehicle production and is the second

largest auto parts production region in the world. The North American light- and medium-duty motor

vehicle market is estimated to be worth USD 728 billion annually, which together represents roughly 28

percent of the global market for new vehicles (Ward’s World Motor Vehicle Data, 2017).

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 4

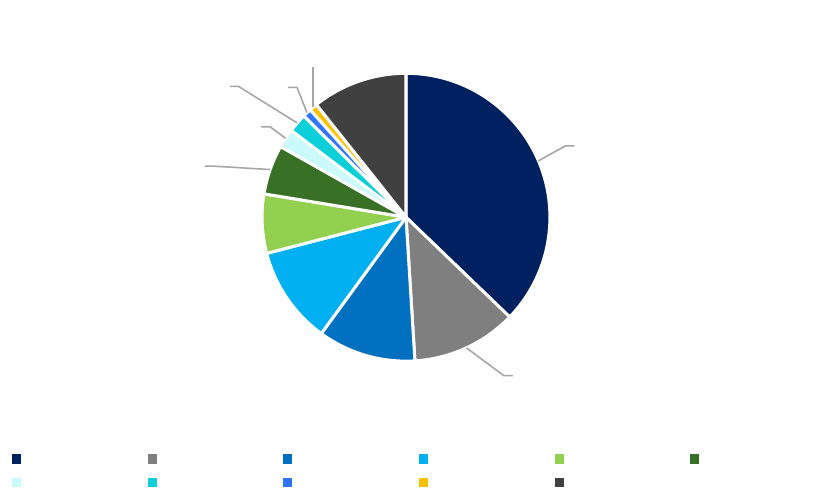

Figure 1: Sourcing of U.S. Light Vehicle Sales, 2017

Source: CAR; U.S. International Trade Administration

Automakers and their suppliers throughout the NAFTA region are very interconnected. No vehicle

assembled in the United States is 100 percent U.S.-made; the average vehicle produced in the United

States relies on 40 to 50 percent imported parts and component content (National Highway Traffic

Safety Administration, 2018).

The share of non-U.S. parts content ranges widely across vehicles – and does not fall neatly across

companies or vehicle brands. Some vehicles assembled in the United States have low North American

and U.S. content, while certain models assembled outside the United States have high U.S. content.

Consider two generalized examples: A vehicle selling for USD 35,000 contains approximately USD 26,000

in value from materials, parts, and components. At 80 percent U.S. content for these inputs, a 25

percent tariff applied to all imported auto parts would add USD 1,300 to the vehicle’s price. For a U.S.

content level of 30 percent, the price increase would surpass USD 4,500. At the vehicle model level,

consumers are very sensitive to relative prices compared to other vehicles within the same class or

segment. Thus, even the relatively small price change experienced by the 80 percent U.S. content

vehicle could drive significant sales losses for a dealership.

The U.S. imported USD 148.8 billion in auto parts in 2017 with NAFTA partners accounting for nearly half

of all parts imports: 11 percent of all U.S. parts imports were from Canada and 37 percent from Mexico

(U.S.A. Trade Online). Canada and Mexico are also the destinations for 62 percent of U.S. motor vehicle

and parts exports (U.S. International Trade Administration, 2017).

Even for vehicles not assembled in the United States, automakers’ decisions on where to build their

products impact U.S. jobs and the economy. Imports from Canada and Mexico support many U.S. jobs

since there is a greater share of U.S. content in the average Canadian- or Mexican-built vehicle than

there is in any vehicle assembled in a non-NAFTA country. According to CAR’s estimates of NAFTA

content in vehicles sold in the United States, the typical Mexican-assembled vehicle includes between 20

and 30 percent U.S. and Canadian content. In contrast, the average vehicle imported from outside the

region has North American content of just 3.5 percent.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 5

Figure 2: Sourcing of U.S. Motor Vehicle Parts Imports, 2017

Source: CAR; U.S. International Trade Administration

Due to the automotive industry’s reliance on complex cross-border supply chains, any new barriers to

trade will have a significant impact on the U.S. automotive industry, consumer prices, and U.S. sales,

employment, and economic output. Trade enables the U.S. automotive and parts industries to be

globally competitive. Because of international commerce, the U.S. industry can specialize in areas where

it has a comparative advantage and achieve greater economies of scale.

U.S. consumers benefit from trade both because there is a greater selection of models in the market,

and because trade helps to keep new vehicles affordable. While only 117 vehicle models were produced

in the United States in 2017, 354 models were available for U.S. consumers to choose from (IHS, 2018).

Among the 237 vehicle models without U.S. production, some models have sales that are just too low to

support local production: 49 of these models see fewer than 1,000 annual U.S. sales, and 95 less than

5,000 (IHS, 2018). U.S. consumers additionally benefit from improved affordability as trade increases

competition between automakers encourages specialization and improves economies of scale.

Figure 3 shows that while consumer prices have risen 86 percent since NAFTA came into being in 1994,

new vehicle prices have only gone up by 7 percent over the same period.

Mexico

37%

China

12%

Canada

11%

Japan

11%

Germany

7%

South Korea

5%

Thailand

2%

Taiwan

2%

India

1%

UK

1%

ROW

11%

Mexico China Canada Japan Germany South Korea

Thailand Taiwan India UK ROW

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 6

Figure 3: U.S. Consumer Price Indices for All Items-Except Food & Energy, and New Vehicles, 1994-

2018

Source: U.S. Bureau of Labor Statistics, 2018

Policy Specifics

Section 232 Tariffs on Imported Light Vehicles & Vehicle Parts

In May 2018, at the direction of President Trump, the U.S. Department of Commerce (DOC) opened an

investigation into whether U.S. light vehicle and parts imports are a threat to U.S. national security,

again using the authority granted Section 232 of the Trade Expansion Act of 1962. The DOC was

expected to issue findings and recommendations in February 2019,

1

after which the President has 90

days to decide whether to impose tariffs or quotas (or both) to adjust imports. President Trump has

frequently mentioned imposing new auto and auto parts tariffs of as high as 25 to 30 percent using

Section 232 as the tool to do so.

As part of the USMCA negotiations, both Canada and Mexico gained commitments from the United

States, which effectively exempt them from any Section 232 tariffs on vehicles or vehicle parts.

USMCA

The renegotiation of NAFTA began in August 2017, and the parties released the draft text of the USMCA

on September 30, 2018. President Trump, Canadian Prime Minister Trudeau, and Mexican President

Peña Nieto signed the agreement on November 30, 2018. Pending approval by each party’s national

legislatures, USMCA is projected to enter into force on January 1, 2020.

Alterations to the rules governing automotive trade are among the most significant changes in the move

from NAFTA to USMCA. The USMCA heavily modifies the automotive Regional Value Content (RVC)

requirement and introduces a North American steel and aluminum purchase requirement and a Labor

1

The report is due within 270 days of opening the investigation.

156.5

257.6

137.6

146.3

100

120

140

160

180

200

220

240

260

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

Consumer Price Index (1982

-1984 = 100)

CPI: All items less food and energy CPI: New vehicles

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 7

Value Content (LVC) requirement, both of which finished vehicles must additionally comply with to

receive tariff-free access to each country.

Under NAFTA, a 62.5 percent RVC was the only requirement necessary for vehicles and vehicle parts to

receive tariff-free market access. Before the USMCA, NAFTA automotive rules provided the strictest

rules of origin of any U.S. trade agreement. NAFTA includes extensive rules for calculating content,

provisions to prevent the use of roll-ups,

2

and the use of a tracing list – where the origin of items on the

list had to be traced back often to the raw materials used in their manufacture.

Under USMCA, the content requirement threshold for finished vehicles increases to 75 percent of the

net cost. However, this higher requirement is counterbalanced by provisions which explicitly permit the

use of roll-ups in the calculation of originating content and the abolishment of the tracing list.

The USMCA also extends the requirements for vehicle parts content. Whereas NAFTA had one content

requirement level, the USMCA creates three bins for vehicle parts, each with a different threshold. The

“Core Parts” bin has an RVC of 75 percent, the “Principal Parts” bin has an RVC of 70 percent, and the

“Complimentary Parts” bin has an RVC of 65 percent.

Table 1: USMCA Regional Value Content Requirements

RVC Category

Required

Content

Description of Category and Phase-In Period

Light Vehicles 75%

3-year transition, but automakers can appeal for a 2-year extension for a limited

amount of production (~10%) if they have a “credible plan” to meet the new ROO

Core Parts 75%

Includes engine, transmission, body & chassis, axle, suspension, steering (all 3-year

transition), and advanced batteries (5-year transition). Must be originating for the

vehicle to be originating.

Principal Parts 70%

Includes tires, glass, pumps & compressors, A/C, bearings & bearing housings, electric

motors used as primary source of propulsion, electric motors for electrical variable

transmission, electromagnets, starter motors & generators, bumpers, safety belts,

brakes, road wheels, radiators, mufflers, clutches, airbags, seats, and parts of seats.

Complementary

Parts

65%

Includes dies, locks, catalytic converters, valves, taps & cocks, electric motors &

universal AC/DC motors not exceeding 37.5W, DC motors & generators not

exceeding 750W, other batteries, distributors & ignition coils, electrical lighting,

windshield wipers/defrosters, sound recording/reproducing apparatus, switches,

insulating wiring sets, headlamps, electronic instruments & measurement

equipment.

Steel &

Aluminum

70%

Day 1 rule, no transition.

Source: CAR summary of USMCA provisions on the USTR website

USMCA additionally requires that items in the “Core Parts” bin must be originating content for a finished

vehicle to meet the RVC. To comply with the core parts requirement, either each core part must

2

When roll-ups are employed, any item which meets the relevant content requirement threshold is counted as

wholly originating. For example, consider a car which uses an engine with 75 percent North American content,

facing an RVC threshold of 75 percent. On average, engines account for 11.5 percent of total car content. Without

roll-up, this engine would contribute 8.6 percent (75 percent x 11.5 percent) towards the content requirement. If

roll-up is permitted, however, the full value of the engine is counted as originating content, so it adds 11.5 percent

towards the RVC requirement.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 8

individually meet the 75 percent content threshold or 75 percent of the total content of core parts value

must be originating. Under this second option, which is called the “Super-Core” provision, a vehicle may

contain some non-originating core parts, such as a transmission, and still comply with the core parts

requirement. However, under either option, if a very high-value core part is non-originating, the vehicle

will fail the core parts requirement. For example, if a vehicle is entirely made of North American content

except for its engine (or battery in the case of an EV), the vehicle would fail the core parts requirement

(because the engine is such a large share of core parts content), and therefore the vehicle would fail the

RVC requirement and be subject to tariff.

In addition to the RVC requirements for vehicles and vehicle parts, the USMCA includes a mandate for

North American sourcing of metals used in vehicle manufacturing. For a vehicle to comply, at least 70

percent of an automaker’s expenditures on steel and aluminum purchased to produce vehicles in North

America must be attributable to steel and aluminum products originating in North America.

The USMCA also introduces an innovation in trade policy – the LVC requirement. Under the USMCA, for

tariff-free market access, a minimum portion of the direct manufacturing labor incorporated into the

production of the vehicle must involve a base wage rate of at least USD 16 per hour. For cars, the

minimum is 40 percent, and for light trucks, the minimum is 45 percent. A credit of up to 10 percentage

points towards the 40 or 45 percent LVC requirement is available through the employment of highly-

compensated salaried workers in research & development or information technology. An additional

credit of 5 percentage points applies to vehicles which use an engine, transmission, or battery sourced

from a manufacturing facility with average direct manufacturing pay exceeding USD 16 per hour. In

practice, the LVC is a mandate for U.S. or Canadian manufacturing employment, with additional

incentives for locating salaried workers in the United States or Canada.

Section 301 Tariffs on Imports from China

In August 2017, the United States initiated an investigation into China’s acts, policies, and practices

related to technology transfer, intellectual property, and innovation under Section 301 of the Trade Act

of 1974. The United States Trade Representative (USTR) issued a report in March 2018 and found that

China’s technology-transfer policies, licensing restrictions, outbound investments, and cybercrimes

constitute unfair trading practices. The USTR points to China’s National Medium- and Long-Term Science

and Technology Development Plan, the State Council Decision on Accelerating and Cultivating the

Development of Strategic Emerging Industries, and the Made in China 2025 Notice as evidence of their

claim. The finding enables the United States to pursue trade remedies through bilateral negotiations,

filing disputes at the World Trade Organization (WTO), or initiating additional Section 301 investigations.

The United States published a list of USD 50 billion in Chinese goods that it would target for tariffs, and

China also released a list of USD 50 billion in U.S. goods on which it would impose additional tariffs if the

United States went forward with its tariffs. In July 2018, the United States imposed 10 percent additional

tariffs on the first tranche of USD 34 billion in Chinese imports; China quickly retaliated with tariffs on

USD 34 billion in U.S. imports to China. Also in July 2018, China lowered its bound rate for light vehicle

imports from 25 percent to 15 percent, and then quickly added a 25 percent tariff on U.S. light vehicle

imports only – taking the duty for U.S. autos to 40 percent while the rest of the world pays 15 percent.

In response to China’s retaliatory moves, the United States published a list in July 2018 of USD 200

billion of Chinese imports that it would target for additional tariffs, and China published a list of USD 60

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 9

billion in U.S. goods on which it would raise duties in response. The second tranche of U.S. tariffs on USD

16 billion in Chinese imports went into effect in August 2018, and China quickly followed with tariffs on

USD 16 billion of U.S. imports to China. The third tranche of U.S. tariffs on Chinese goods, which took

effect in September 2018, included substantially all light vehicle parts and components as well as

automotive tooling and molds. The United States set the tariff rate on Chinese imports in the third

tranche at 10 percent, with a threat that the rate would increase to 25 percent if China did not act to

resolve the dispute. In November 2018, the United States and China agreed to a tariff truce and initiated

a series of bilateral talks aimed at addressing the trade dispute. The United States has said it would

automatically raise the third tranche tariff rate to 25 percent if the parties do not make progress in talks

before the end of March 2019. If this comes to pass, the impacts of Section 301 will be far more

significant than CAR has modeled, as this briefing is based on tariff rates in effect as of January 2019.

Section 232 Tariffs on Imported Steel & Aluminum

In January 2018, the DOC completed its investigation into whether imports of steel and aluminum

products constitute a national security threat under Section 232 of the Trade Expansion Act of 1962. As

a result, the United States imposed a 25 percent tariff on steel imports and 10 percent tariff on

aluminum imports on 1 June 2018 (U.S. Customs and Border Protection, 2018). The additional duty

applies to all affected steel and aluminum products from countries except for those the United States

agreed to grant an exemption, including Argentina, Australia, Brazil, and South Korea. As of December

20, 2018, the DOC has issued some 14,301 steel product exclusions out of 44,389 requests filed and 917

aluminum product exclusions out of 6,013 petitions filed (McDaniel & Parks, 2019).

As a result of the tariffs, prices for imported steel and aluminum increased, as did prices for U.S.-

produced metals due to increased demand. U.S. steel and aluminum price increases have increased the

costs of U.S. motor vehicle and parts output due to the usage of steel and aluminum as inputs in the

manufacturing process. The U.S. tariffs have made reportedly made U.S. steel the most expensive,

globally (Naughton & Deaux, 2018). Both Ford and General Motors disclosed in late 2018 that these

tariffs had cost them USD 1 billion each – approximately USD 700 for each vehicle they produced in

North America. Ford and GM’s input costs rose despite already predominantly using U.S.-sourced metals

(Carey & Klayman, 2018) (Carey & Shepardson, 2018).

The steel and aluminum tariffs have also increased the costs of vehicle and parts production in Canada

and Mexico. Due to the integration of the North American market, vehicle parts produced in one

country are often used for vehicle assembly occurring in another. As a result, broad-based cost increases

in one country, such as due to the U.S. tariffs on imported steel and aluminum, and retaliatory measures

enacted by Canada and Mexico, have increased metals prices in all three NAFTA countries.

Summary of Methods

Simulation Model

CAR developed a simulation model of trade in the U.S. automotive industry to evaluate the impact of

imposing additional tariffs on imported autos and auto parts. The analysis examines the substitution

away from imported autos and auto parts as a result of the potential trade action and assumes unitary

demand elasticity (i.e., changes in price yield proportionate changes in sales volumes and the total dollar

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 10

value of the market remains unchanged). The analysis also assumes that producers will fully pass cost

increases along into consumer prices. The simulation provides direct estimates of the impacts on vehicle

prices, sales, dealership revenue, and motor vehicle and parts manufacturing. The direct effects are

used as input values to determine the economy-wide impacts using the Regional Input-Output Modeling

System (RIMS II) – a commercially-available model of the U.S. economy. The appendix presents

additional information on the modeling process.

Simulation Inputs

The impacts of each policy action are required inputs to the simulation model. The potential costs of

each policy were estimated using publicly available data. Where assumptions were required, CAR

utilized best-case scenarios for CAR’s modeling to avoid overstating and compounding potential

negative impacts. A brief discussion of the procedures for estimating changes in trade costs follow, with

additional information available in the methodology appendix.

Section 232 Tariffs on Imported Light Vehicles & Vehicle Parts

While intuitive to assign the tariffs imposed on imported vehicles and vehicle parts as costs to vehicle

sales or vehicle assembly, doing so would overstate the impacts of these tariffs. The reason is that it

would fail to differentiate between original equipment – the production of new vehicles or creation of

vehicle parts – and aftermarket use, such as a consumer purchasing a new muffler from a parts store.

Additionally, many of the goods subject to tariffs are used by multiple industries. CAR researchers

pursued numerous avenues of research to adequately adjust import figures to reflect only the costs

these tariffs would impose on the manufacture and sale of new vehicles.

For imported parts that are specific to light vehicles, an estimated 75 percent of imports (by value) are

destined for original equipment use (Automotive Aftermarket Suppliers Association, 2012) (International

Trade Administration, 2011) (International Trade Administration, 2009) (International Trade

Administration, 2007). Thus, when estimating the impact on the costs of U.S.-assembled vehicles, CAR

considered trade impacts upon 75 percent of imported vehicle parts by value. The total tariff-caused

increase in OEM parts cost is assigned to all vehicles assembled in the United States, with the effects on

the prices of vehicles both assembled and sold in the United States presented in our results. Cost

increases raise the price of U.S. vehicle exports, as well, but this briefing only presents effects on U.S.

consumers. For vehicles assembled outside of the United States, and imported from countries which are

subject to the tariff, the assumed tariff rate of 25 percent is applied to these vehicles as a consumer

price increase.

USMCA

Evaluating the impacts of the new rules of origin requirements present in USMCA requires first

estimating the North American content and the U.S. and Canadian labor content of all vehicles

assembled and sold in North America. While NAFTA content certification data exists, it is not available

for public or research use. CAR developed a method for estimating the required vehicle-model level

content figures using the model year 2018 the American Automobile Labeling Act data, and industry-

level government data available through the U.S. Census Bureau, Statistics Canada, and Instituto

Nacional de Estadística y Geografía. These estimates were cross-checked using trade data and

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 11

proprietary databases. Additionally, one automaker provided limited feedback on the accuracy of CAR’s

estimates for their products.

CAR estimates that 47 vehicle models which are produced and sold in North America do not meet the

USMCA rules of origin requirements. Of these, 20 vehicle models are assembled in the United States,

and the remaining 27 vehicle models are assembled in either Canada or Mexico. Nearly all of the models

assembled outside of the United States met the NAFTA requirements – 24 of the 27 which would not

comply with USMCA do meet NAFTA requirements. Under USMCA, these 24 vehicle models would be

newly exposed to import tariffs assessed by each country. Passenger vehicles entering the United States

would be assessed at the most-favored-nation (MFN) tariff rate of 2.5 percent and cargo vehicles,

including light-duty pickup trucks and vans, are assessed a 25 percent tariff. Across these 24 vehicle

models, the average potential tariff cost for units complying with NAFTA but not USMCA would be USD

635.

Ho

wever, it is unlikely that many of these models will be brought into compliance with USMCA

rules. All non-conforming vehicles fail multiple criteria within the USMCA rules of origin, with the LVC

requirement particularly challenging to meet through supply chain alteration. Instead, the sale of these

vehicles in the U.S. market is likely to cease. Manufacturers have already announced plans to end either

North American production or U.S. sales for 12 of these vehicles.

Although the cost increase for these individual models which could lose tariff-free access is substantial

on a model-by-model basis, weighed against the total volume of vehicles imported from Canada or

Mexico, the average per vehicle imported cost would be far smaller. As a simulation input, the shift from

NAFTA to USMCA is incorporated as a slight increase in the U.S. consumer prices of vehicles assembled

in Canada or Mexico.

Section 301 Tariffs on Imports from China

As previously stated, approximately 25 percent of the value of imported vehicle parts is destined for

aftermarket applications. However, available data suggest that for vehicle parts imported from China,

far more than the typical 25 percent are destined for aftermarket use. To properly incorporate Section

301 tariffs against imports from China, CAR conducted additional research and meticulously reviewed

the most detailed data available. Following this review, where used, remanufactured, and non-

automotive vehicle parts were removed from consideration.

CAR researchers developed boundary conditions, where the full value of those imports which could not

be reliably categorized as relevant or irrelevant to the U.S. light vehicle production were wholly assigned

to use in U.S. light vehicle production or were considered to be entirely unrelated to U.S. vehicle

production. This exercise suggests that between 1 and 3 percent of the value of U.S.-assembled vehicles

is made up of vehicle parts imported from China. To evaluate the impacts of Section 301 tariffs, CAR

used the midpoint of this range – an assumption that 2 percent of the value of U.S.-assembled vehicles

stems from parts imported from China.

Section 232 Tariffs on Imported Steel & Aluminum

For the tariffs in effect against U.S. imports of steel and aluminum, CAR researched the consumption

patterns for steel and aluminum by U.S. industry. The U.S. vehicle and vehicle parts manufacturing

industries account for 26 percent of U.S. steel consumption and 31 percent of U.S. aluminum

consumption (statista) (Bray, 2018) (U.S. Census Bureau, 2015). Using full-year 2017 trade data (the

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 12

latest available), with the exemptions granted to imports from Argentina, Australia, Brazil, and South

Korea, the steel and aluminum tariffs apply to USD 27.8 billion of steel and aluminum imports (U.S.A.

Trade Online). Given current consumption and import patterns and the exemptions granted to imports

from Argentina, Australia, Brazil, and South Korea, the steel and aluminum tariffs represent an indirect

tax of USD 1.4 billion on U.S. light vehicle and vehicle parts manufacturing, increasing costs of U.S.

vehicle assembly by 0.43 percent. Were Canada and Mexico also exempted from the steel and

aluminum tariff, the cost increase for U.S. light vehicle manufacturing would instead be 0.28 percent.

U.S. Light Vehicle Production Capacity

As the U.S. automotive industry does not have sufficient capacity to meet all U.S. consumer demand for

new vehicles, constraints are imposed upon the simulation’s predicted changes to total U.S. light vehicle

production. Open (underutilized) vehicle assembly capacity in the United States currently, as of January

2019, sits at 2.8 million units (Center for Automotive Research, 2018). This open capacity is not evenly

distributed across automakers or regions, does not align with historical production patterns, and mainly

is free due to a mismatch between the products these factories can produce, and those which U.S.

consumers are purchasing.

The simulation model enforces capacity constraints on a regional basis, using data on current open

capacity at each U.S. vehicle assembly plant and recent historical data on each region’s share of the

nation’s light vehicle manufacturing output. The simulation does not attempt to impose constraints

according to vehicle model, class, brand, or any other criteria beyond the production region’s current

and recent output level. This approach provides a generous accounting of open capacity, such that any

open unit could be used to produce any product regardless of vehicle architecture, the manufacturing

process, or facility ownership. The actual effects of capacity constraints would be more severe, and the

employment and economic outcomes more dramatic than what is shown in these scenarios.

Uncertain Impacts on Used Vehicles Prices, Repair, & Maintenance

Costs

Tariffs on new automobiles and automotive parts will impact the market for used vehicles, as well as

increase the price consumers pay to repair and maintain their existing vehicle due to higher parts prices.

Higher costs for vehicle purchases result in higher valuations of existing vehicles and longer service lives,

yet higher operating costs lower the value of existing vehicles and shorten their service lives. The dearth

of literature presently available makes it impossible to determine which of these effects is likely to

dominate. As an attempt at modeling these effects would rely upon assumed parameters, with little

guidance as to their appropriate values, we exclude the impacts on used vehicles and vehicle repair and

maintenance from our analysis.

Used vehicle prices typically follow a well-behaved and consistent depreciation pattern, with a given

vehicle’s value declining approximately 20 percent per year. Deviations from this generalized

depreciation curve result from macro-level shocks in the economy, such as substantial changes in fuel

prices, or shocks to used vehicle supplies, such as widespread destruction of vehicles due to a natural

disaster (Center for Automotive Research) (Yerger, 2010).

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 13

The relative value of new and used vehicles is influenced by the relationship between used and new

vehicle purchases. The supply of used vehicles is highly inelastic, as additional supply primarily results

from either current vehicle owners bringing in-use vehicles onto the market to reduce their vehicle

holdings or to replace them with newly-manufactured vehicles, thereby expanding the in-use fleet.

Absent a dramatic change to household transportation needs or planned vehicle-ownership downsizing,

sold vehicles must be replaced.

A secondary effect of increasing vehicle prices is an extension of vehicle service lives. Multiple studies

indicate that the typical response to increasing vehicle prices – both for new vehicles, and for used

vehicles – is to extend the length of ownership for currently-held vehicles, resulting in fewer sales of

both new and used vehicles (Copeland, 2013) (Alberini, Bareit, & Martinez-Cruz, 2016) (Bento, Roth, &

Zuo, 2016). However, this effect is offset by the increase in vehicle repair and maintenance costs which a

tariff on imported vehicle parts will cause. Increases in vehicle operating costs have been conclusively

tied to shorter periods of ownership and lower vehicle valuations (Hamilton & Macauley, 1999).

A 25 percent tariff applied to all imports of automotive parts will increase the cost of aftermarket parts

by 8.3 percent. If an exemption were granted to Canada, Mexico, and South Korea, the impact would

instead be a 3.4 percent price increase. Should Canada, Mexico, South Korea, Japan, the United

Kingdom, and the post-BREXIT European Union all receive exemptions, this increase in aftermarket parts

prices declines to 1.7 percent. It is difficult to determine the impact these costs would have on the

providers of automotive repair and maintenance services. Parts and materials account for 100 percent

of the cost of DIY repair and maintenance, and, on average, 33 percent for commercial vehicle repair

and maintenance work. This result suggests that, as the relative cost of DIY would increase against

commercial providers, more consumers would opt for commercial vehicle repair and maintenance

services. However, budget tightening, whether due to price increases or falling incomes, has historically

resulted in a shift towards DIY work. With currently available information, no reliable conclusion can be

drawn as to the impacts of higher parts prices across DIY and “Do It For Me” repair and maintenance

(Automotive Aftermarket Suppliers Association, 2012) (U.S. Bureau of Economic Analysis, 2018) (U.S.

Census Bureau, 2018).

Policy Scenarios

To evaluate the effects of current and potential trade policy, the Center for Automotive Research

developed ten policy scenarios from the four trade policies considered (USMCA, Section 301 China

tariffs, Section 232 steel and aluminum tariffs, and Section 232 auto & auto parts tariffs). In all scenarios,

CAR assumes that the USMCA is ratified and enters into force and that Section 301 tariffs against

imports from China remain unchanged from their January 2019, product coverage and rates. The Section

232 tariffs on imported steel and aluminum are evaluated in either their current form, where Argentina,

Australia, Brazil, and South Korea are exempt or in an alternate form which also provides exemptions for

steel and aluminum imports from Canada and Mexico. This alternative is considered as both countries

had indicated that removal of the steel and aluminum tariffs as a pre-requisite for proceeding with

USMCA, and negotiations towards ending these tariffs or transitioning to a quota system for imports

from Canada and Mexico appear to be ongoing (Rappeport & Thrush, 2018).

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 14

1. A broad-based tariff, where exemptions are granted only to Canada and Mexico, by the existing

and already in-force side letters to the USMCA, and South Korea, because that country has

successfully negotiated exemptions to prior protectionist trade measures;

2. A narrowly-focused tariff that applies only to vehicles and parts imported from the (post BREXIT)

European Union;

3. A narrowly-focused tariff that applies only to vehicles and parts imported from the United

Kingdom;

4. A narrowly-focused tariff that applies only to vehicles and parts imported from Japan; or

5. A broad-based tariff, but with exemptions for Canada, Mexico, South Korea, the EU, the UK, and

Japan

.

Se

ction 232 vehicle and parts Scenarios 2 through 5 are in keeping with the Trump administration’s

history of using tariffs – or the threat of tariffs – as a form of leverage in trade negotiations. Aside from

Canada and Mexico, which have broad exemptions to Section 232 auto and parts tariffs via the USMCA,

and South Korea, which has negotiated exemptions to other U.S. tariffs, the Administration is

negotiating new trade agreements with the E.U., with the U.K., and with Japan.

The ten policy scenarios which result from the combination of the five possible Section 232 auto and

auto parts tariffs, the USMCA, the Section 301 tariffs, and the two scenarios for the Section 232 steel

and aluminum tariffs are summarized in Table 2.

Table 2: Overview of U.S. Automotive Trade Scenarios Analyzed

USMCA

Section

301

China

Tariffs

Section

232

Steel &

Alum.

Tariffs

Potential Section 232 Auto & Parts Tariffs @ 25%

Canada &

Mexico

South

Korea

EU

UK

Japan

All other

countries

1

Implemented in Current Form

In place as of 11 January 2019

Include

Canada &

Mexico

Exempt

Exempt

2

Exempt

Exempt

Exempt

Exempt

Exempt

3

Exempt

Exempt

Exempt

Exempt

Exempt

4

Exempt

Exempt

Exempt

Exempt

Exempt

5

Exempt

Exempt

Exempt

Exempt

Exempt

6

Exclude

Canada &

Mexico

Exempt

Exempt

7

Exempt

Exempt

Exempt

Exempt

Exempt

8

Exempt

Exempt

Exempt

Exempt

Exempt

9

Exempt

Exempt

Exempt

Exempt

Exempt

10

Exempt

Exempt

Exempt

Exempt

Exempt

Results

Across all ten scenarios, average vehicle prices rise and sales fall. New vehicle dealerships – and likewise,

the entire U.S. economy – are always, unambiguously harmed. Of note, the potential Section 232 tariffs

on imported light vehicles and vehicle parts are the single-largest factor in determining the magnitude

of adverse effects. In the worst-case scenario, where a broad-based Section 232 is adopted against

imported light vehicles and vehicle parts, exempting only Canada, Mexico, and South Korea, 90.5

percent of the total economic harm results from this single action. Under the scenario of least-harm,

wherein exemptions to the existent Section 232 steel and aluminum tariffs are expanded to additionally

exempt Canada and Mexico, and Section 232 tariffs on autos and auto parts only affect imports from the

CAR considered five versions of Section 232 tariffs on autos and parts:

© CENTER FOR AUTOMOTIVE RESEARCH | 2019 15

United Kingdom, the vehicle and parts tariffs remain 42.8 percent of the total impact. The source of

impacts, by specific trade policy and scenario, are presented in Table 3.

Table 3: Source of Impacts, by Specific Policy, by Scenario

U

Section

301

China

Tariffs

Section

232 Steel &

Aluminum

Tariffs

Potential Section

232 Auto & Parts

Tariffs @ 25%

Percent of Total Impact Due to Each Policy, by Policy Scenario

S

M

C

A

232 Light

Vehicles & Parts

USMCA 301 China

232 Steel and

Aluminum

Implemented in Current Form

In place as of 11 January 2019

Include Canada & Mexico

Canada, Mexico, & South

Korea Exempt

90.5% 2.2% 3.1% 4.1%

Only applies to EU 74.2% 6.1% 8.5% 11.2%

Only applies to UK 38.9% 14.5% 20.2% 26.5%

Only applies to Japan 76.8% 5.5% 7.7% 10.1%

Canada, Mexico, South

Korea, EU, UK, & Japan

Exempt

73.1% 6.4% 8.9% 11.7%

Exclude Canada & Mexico

Canada, Mexico, & South

Korea Exempt

91.8% 2.3% 3.2% 2.7%

Only applies to EU 77.2% 6.4% 8.9% 7.6%

Only applies to UK 42.8% 15.9% 22.2% 19.1%

Only applies to Japan 79.5% 5.7% 7.9% 6.8%

Canada, Mexico, South

Korea, EU, UK, & Japan

Exempt

76.1% 6.6% 9.3% 8.0%

Source: Center for Automotive Research estimates

Across the ten policy scenarios, the magnitude of trade policy impacts varies meaningfully. The price of

the average vehicle sold in the United States could rise as much as USD 2,750 or by slightly more than

USD 350, depending upon which policies are enacted. These price effects correspond to vehicle sales

losses from 183,000 to 1.3 million. These outcomes are summarized in Table 4.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

16

Table 4: Change in U.S. Light Vehicle Sales and Prices Under Various U.S. Automotive Trade Policies

USMCA

Section

301

China

Tariffs

Section

232

Steel &

Alum.

Tariffs

Potential Section 232

Auto & Parts Tariffs

@ 25%

U.S. Sales

(units)

Overall

Change in

Price/Unit ($

dollars)

Change in

Price/Unit

Imported

Vehicles

($ dollars)

Change in

Price/Unit

Domestic

Vehicles

($ dollars)

Implemented in Current Form

In place as of

11 January 2019

Include Canada

& Mexico

Canada, Mexico, & South

Korea Exempt

(1,319,700) $2,750 $3,700 $1,900

Only applies to EU

(494,000)

$1,000

$1,400

$650

Only applies to UK

(197,600)

$400

$450

$300

Only applies to Japan

(548,700)

$1,100

$1,550

$700

Canada, Mexico, South

Korea, EU, UK, & Japan

Exempt

(425,400) $850 $850 $850

Exclude Canada

& Mexico

Canada, Mexico, & South

Korea Exempt

(1,315,100) $2,750 $3,700 $1,900

Only applies to EU

(482,100)

$950

$1,400

$600

Only applies to UK

(183,800)

$350

$450

$300

Only applies to Japan

(536,900)

$1,050

$1,550

$700

Canada, Mexico, South

Korea, EU, UK, & Japan

Exempt

(408,800) $800 $850 $800

Source: Center for Automotive Research estimates

In every scenario, new vehicle dealership revenue and employment falls, as does U.S. GDP and overall

U.S. employment. Dealerships are likely to experience a decline in revenue totaling between USD 6.1

billion and USD 43.6 billion, with associated employment losses between 10,700 and 77,000 employees.

For the average dealership, these losses correspond to a fall in revenue ranging from USD 362 thousand

to USD 2.6 million, with corresponding employment losses of 0.6 to 4.6 employees. In the broader

economy, U.S. GDP is projected to fall between USD 6.0 billion and USD 30.4 billion and total economy-

wide employment would drop between 71,200 and 366,900 jobs (see Table 5).

Table 5: Change in Dealership Revenue, Employment, U.S. GDP, and Overall U.S. Employment

Under Various U.S. Automotive Trade Scenarios

U

S

M

C

A

Section

301

China

Tariffs

Section

232 Steel &

Aluminum

Tariffs

Potential

Section 232

Auto & Parts

Tariffs @ 25%

Dealership Revenue

Change in U.S.

Dealership

Employment Level

U.S. GDP

($

Billions)

Change

in

Overall

U.S.

Employ-

ment

Level

Total

($

Billions)

Per

Dealershi

p

($1,000s)

Total

Per

Dealershi

p

Implemented in Current Form

In place as of 11 January 2019

Include Canada

& Mexico

Canada, Mexico, &

South Korea Exempt

($43.62) ($2,596) (77,000) (4.6) ($30.40) (366,900)

Only applies to EU

($16.33)

($972)

(28,800)

(1.7)

($10.80)

(131,100)

Only applies to UK

($6.53)

($389)

(11,500)

(0.7)

($7.10)

(83,900)

Only applies to Japan

($18.14)

($1,079)

(32,000)

(1.9)

($12.00)

(145,800)

Canada, Mexico,

South Korea, EU, UK,

& Japan Exempt

($14.06) ($837) (24,800) (1.5) ($18.00) (207,800)

Exclude Canada

& Mexico

Canada, Mexico, &

South Korea Exempt

($43.47) ($2,587) (76,700) (4.6) ($29.80) (360,500)

Only applies to EU

($15.93)

($948)

(28,100)

(1.7)

($9.80)

(119,600)

Only applies to UK

($6.08)

($362)

(10,700)

(0.6)

($6.00)

(71,200)

Only applies to Japan

($17.75)

($1,052)

(31,300)

(1.9)

($11.00)

(134,300)

Canada, Mexico,

South Korea, EU, UK,

& Japan Exempt

($13.51) ($804) (23,900) (1.4) ($16.70) (193,000)

Source: Center for Automotive Research estimates

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

17

Conclusions

CAR expanded its past research into the effects of potential U.S. trade policy actions to consider ten

policy scenarios that combine trade policies implemented as of January 2019 and potential near-term

U.S. trade policy changes. Across these policy scenarios, the variation in impacts on the U.S. new vehicle

market and the broader U.S. economy is substantial, but near wholly determined by the severity of

potential Section 232 tariffs on imported autos and auto parts.

In the worst-case scenario, the price of the average vehicle sold in the U.S. would increase by USD 2,750.

In the least severe case, this average price increase would be a comparatively small USD 350. The

difference between these extremes is almost solely determined by whether automotive Section 232

tariffs are broad-based or highly targeted to only a few countries. Broad-based automotive tariffs

threaten more than 366,000 jobs. While the trade restrictions adopted or under consideration are

intended to assist U.S. workers, these policies are likely to be extremely disruptive to and negative for

the U.S. economy.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

18

Works Cited

Alberini, A., Bareit, M., & Martinez-Cruz, A. (2016). The Impact of Emissions-Based Taxes on the

Retirement of Used and Inefficient Vehicles: The Case of Switzerland. Zurich: Center of Economic

Research at ETH Zurich Economics Working Paper Series.

Armington, P. S. (1969). A Theory of Demand for Products Distinguished by Place of Production. IMF

Staff Papers: Volume 16 No. 1, 159-178.

Automotive Aftermarket Suppliers Association. (2012). Automotive Aftermarket Status Report.

Bento, A., Roth, K., & Zuo, Y. (2016). Vehicle Lifetime Trends and Scrappage Behavior in the U.S. Used Car

Market. Working paper.

Bray, E. L. (2018, January). Mineral Commodity Summaries: Aluminum. U.S. Geological Survey. Retrieved

from https://minerals.usgs.gov/minerals/pubs/commodity/aluminum/mcs-2018-alumi.pdf

Bureau of Industry and Security Office of Technology Evaluation. (2018, January). The Effect of Imports

of Aluminum on the National Security. U.S. Department of Commerce. Retrieved from

https://www.bis.doc.gov/index.php/documents/aluminum/2223-the-effect-of-imports-of-

aluminum-on-the-national-security-with-redactions-20180117/file

Carey, N., & Klayman, B. (2018, July 25). Tariffs ding Detroit automakers' profit forecasts, stocks hit.

Retrieved from Reuters: https://www.reuters.com/article/us-autos-results/tariffs-ding-detroit-

automakers-profit-forecasts-stocks-hit-idUSKBN1KF1FW

Carey, N., & Shepardson, D. (2018, September 26). Trump metals tariffs will cost Ford $1 billion in

profits, CEO says. Retrieved from Reuters: https://www.reuters.com/article/us-ford-motor-

tariffs/trump-metals-tariffs-will-cost-ford-1-billion-in-profits-ceo-says-idUSKCN1M61ZN

Center for Automotive Research. (2018). Analysis based on LMC Automotive production and capacity

data.

Center for Automotive Research. (2018). Book of Deals. Ann Arbor.

Center for Automotive Research. (n.d.). Unpublished, internal research on vehicle values and

depreciation by vehicle age.

Copeland, A. (2013). Intertemporal Substitution and New Car Purchases. Retrieved from

http://copeland.marginalq.com/res_doc/auto_dynamics.pdf

Donelly, W. A., Johnson, K., Tsigas, M., & Ingersoll, D. (2004). Revised Armington Elasticities of

Substitution for the USITC Model and the Concordance for Constructing a Consistent Set for the

GTAP Model. Washington, D.C.: U.S. International Trade Commission Office of Economics.

Donelly, W. A., Johnson, K., Tsigas, M., & Ingersoll, D. (2004). Revised Armington Elasticities of

Substitution for the USITC Model and the Concordance for Constructing a Consistent Set for the

GTAP Model. Washington, D.C.: U.S. International Trade Commission Office of Economics.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

19

Gallaway, M. P., McDaniel, C. A., & Rivera, S. A. (2003). Short-run and long-run industry-level estimates

of U.S. Armington elasticities. The North American Journal of Economics and Finance, 49-68.

Hamilton, B. W., & Macauley, M. K. (1999). Heredity or Environment: Why is Automobile Longevity

Increasing? The Journal of Industrial Economics, 251-261.

IHS|Markit. (2018). North American Automotive Production Forecast.

Instituto Nacional de Estadística y Geografía. (2018). Retrieved from http://en.www.inegi.org.mx/datos/

International Trade Administration. (2007). U.S. Automotive Parts Industry Annual Assessment. U.S.

Department of Commerce Office of Aerospace and Automotive Industries. Retrieved from

https://www.trade.gov/td/auto/domestic/2007Assessment.pdf

International Trade Administration. (2009). U.S. Automotive Parts Industry Annual Assessment . U.S.

Department of Commerce Office of Transportation and Machinery. Retrieved from

https://web.archive.org/web/20150412001450/http://trade.gov/mas/manufacturing/OAAI/buil

d/groups/public/%40tg_oaai/documents/webcontent/tg_oaai_003759.pdf

International Trade Administration. (2011). On the Road: U.S. Automotive Parts Industry Annual

Assessment. U.S. Department of Commerce Office of Transportation and Machinery. Retrieved

from https://www.trade.gov/td/otm/assets/auto/2011Parts.pdf

International Trade Administration. (2018, March). Steel Imports Report: United States Overall

Production and Import Penetration. U.S. Department of Commerce. Retrieved from Global Steel

Trade Monitor: https://www.trade.gov/steel/countries/pdfs/imports-us.pdf

Klayman, B. (2019, January 16). Ford sees weaker-than-expected fourth quarter, uncertainty in 2019.

Reuters. Retrieved from https://www.reuters.com/article/us-autoshow-detroit-ford-motor-

outlook/ford-sees-weaker-than-expected-fourth-quarter-uncertainty-in-2019-idUSKCN1PA1A5

LMC Automotive. (2018). North American Automotive Production Forecast.

McDaniel, C., & Parks, D. (2019). Data compled from Regulations.gov. Mercatus Center.

Morales, R. (2018, August 28). ¿En qué suavizó Estados Unidos sus demandas en el TLCAN? Retrieved

from El Economista: https://www.eleconomista.com.mx/empresas/En-que-suavizo-Estados-

Unidos-sus-demandas-en-el-TLCAN-20180828-0024.html

National Automobile Dealers Association. (2017, June). NADA Data 2017: Annual Financial Profile of

America's Franchised New-Car Dealerships. Retrieved from https://www.nada.org/nadadata/

National Highway Traffic Safety Administration. (2018). American Automobile Labeling Act. U.S.

Department of Transportation. Retrieved from https://one.nhtsa.gov/Laws-&-Regulations/Part-

583-American-Automobile-Labeling-Act-(AALA)-Reports

Naughton, K., & Deaux, J. (2018, October 22). Ford Ratchets Up Rebuke of Trump Tariffs as Steel Costs

Rise. Retrieved from Bloomberg: https://www.bloomberg.com/news/articles/2018-10-22/ford-

says-trump-tariffs-makes-u-s-steel-costliest-in-the-world

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

20

Rappeport, A., & Thrush, G. (2018, November 21). U.S. Weighs Steel Quotas, Instead of Tariffs, on

Canada and Mexico. Retrieved from The New York Times:

https://www.nytimes.com/2018/11/21/us/politics/us-canada-mexico-steel-tariffs.html

Schultz, M., Dziczek, K., Swiecki, B., & Chen, Y. (2018). Trade Briefing: Consumer Impact of Potential U.S.

Section 232 Tariffs and Quotas on Imported Automobiles & Automotive Parts. Center for

Automotive Research. https://www.cargroup.org/wp-content/uploads/2018/07/NADA-

Consumer-Impact-of-Auto-and-Parts-Tariffs-and-Quotas_July-2018.pdf

statista. (n.d.). Steel demand in the United States as of 2017, by sector. Retrieved from statista: The

Statistics Portal: https://www.statista.com/statistics/752484/us-steel-demand-by-sector/

Statistics Canada. (2018). Retrieved from https://www150.statcan.gc.ca/n1/en/type/data?MM=1

U.S. Bureau of Economic Analysis. (2018). National Income and Product Accounts Table 2.4.5U. Personal

Consumption Expenditures by Type of Product. U.S. Department of Commerce. Retrieved from

https://www.bea.gov

U.S. Census Bureau. (2015). 2012 Economic Census. Materials Consumed by Kind of Industry.

U.S. Census Bureau. (2018, July). Annual Survey of Manufacturers, 2016. Retrieved from American

FactFinder: https://factfinder.census.gov/

U.S. Census Bureau. (2018, July). Annual Survey of Manufactures, 2016. Retrieved from American

FactFinder: https://factfinder.census.gov/

U.S. Census Bureau. (2018, July). Business Patterns. Retrieved from American FactFinder:

https://factfinder.census.gov/

U.S. Census Bureau. (2018, July). USA Trade Online. Retrieved from Exports & Imports by NAICS

Commodities : https://usatrade.census.gov/

U.S. Customs and Border Protection. (2018, October). Section 232 Tariffs on Aluminum and Steel.

Retrieved from U.S. Department of Homeland Security Customs and Border Protection:

https://www.cbp.gov/trade/programs-administration/entry-summary/232-tariffs-aluminum-

and-steel

U.S. International Trade Administration. (2017). Automotive Parts Trade Data. Retrieved from

Automotive Statistics: https://www.trade.gov/td/otm/assets/auto/AP_Trade.pdf

U.S.A. Trade Online. (2018). Retrieved from U.S. Census Bureau: https://usatrade.census.gov/

Ward’s World Motor Vehicle Data. (2017).

Yerger, D. B. (2010). Used Car Markets: Reliability Does Matter, But Do Consumer Reports? Applied

Economics Letters, 67-70. Retrieved from

https://www.tandfonline.com/doi/abs/10.1080/135048596356708

Zhang, X.-g., & Verikios, G. (2006). Armington Parameter Estimation for a Computable General

Equilibrium Model: A Database Consistent Approach. Melbourne: The University of Western

Australia Department of Economics.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

21

Methodology Appendix

The Simulation Model

To evaluate the potential economic impacts of trade barriers being imposed upon auto and auto parts

trade, CAR developed a simulation model of the U.S. light vehicle industry. A critical assumption of the

model is that the new vehicle market has a unitary demand elasticity – changes in prices yield

proportionate, opposite changes in sales volumes such that the total dollar value of the market is

unchanged. Additionally, when calculating the effects of tariffs, CAR assumes that these costs are fully

passed along into consumer prices. As not all information required for CAR’s modeling exercise has been

updated through calendar year 2018, CAR’s estimates rely upon 2017 data for vehicle production,

vehicle sales, and trade in vehicles and vehicle parts.

CAR’s model provides direct estimates of the output changes for light vehicle sales and manufacturing.

The model explicitly incorporates trade across ten blocks which define U.S. new light vehicle sales by

country of assembly: 1) total U.S. light vehicle sales, 2) U.S. sales of U.S.-assembled vehicles, and U.S.

sales of vehicles assembled in 3) Canada, 4) Mexico, 5) China, 6) South Korea, 7) the United Kingdom, 8)

the Post-BREXIT European Union, 9) Japan, or 10) the remainder of the world.

Application of the simulation model yields the direct impacts of automotive tariffs on three industries:

U.S. motor vehicle dealerships, U.S. light vehicle manufacturing, and U.S. motor vehicle parts

manufacturing. These direct impacts are translated into nationwide economic impacts using the

Regional Input-Output Modeling System (“RIMS II”) available from the U.S. Bureau of Economic Analysis.

The direct impact on dealerships is defined as the change in dealership revenue which results from

changes in the level of new vehicle sales. The direct impact on U.S. light vehicle manufacturing is defined

as the change in the value of U.S. sales of U.S.-assembled vehicles, due to the changes in relative prices

between U.S.-assembled and foreign-assembled vehicles which result from the imposition of tariffs. The

impact on U.S. motor vehicle parts manufacturing is comprised of two, offsetting effects: parts

manufacturing gains from increased U.S. vehicle manufacturing but declines from lowered foreign

vehicle assembly activity. U.S. motor vehicle parts are used in both the production of U.S.- and foreign-

assembled vehicles which are sold in the U.S., particularly those vehicles assembled in Canada and

Mexico. The gain to motor vehicle parts manufacturing from increased U.S.-assembly is encapsulated in

the economy-wide effects estimated from the application of the RIMS II model to the direct impacts on

light vehicle manufacturing. The effects on vehicle parts manufacturing from decreased imports of

vehicles with U.S.-content is incorporated via a combination of the estimated value of U.S.-content in

Canadian and Mexican vehicles with the estimated declines in U.S. imports of vehicles from these

countries.

As the RIMS multipliers are single-region, these estimates do not account for feedback across regional

boundaries, let alone national borders. Instead, CAR explicitly modeled the relationship between U.S.

vehicle parts manufacturing and Canadian and Mexican vehicle manufacturing. This relationship was

evaluated similarly to the “Trade Data Approach” used to estimate foreign content in U.S.-assembled

vehicles, discussed in the section on tariff cost estimates. Vehicles assembled in Canada and Mexico

contain a high degree of U.S. parts content; the value of OEM-destined U.S. vehicle parts exports to

Canada and Mexico are assigned to the value of vehicle production occurring in each country.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

22

Finally, CAR’s simulation model needed to properly incorporate market share shifts across the origins of

vehicles and vehicle parts. As the price of imported goods increase, the amount sourced either

domestically or from an unaffected foreign market increases. Estimated “Armington” trade elasticities

represent this effect. However, estimates of trade elasticities vary wildly. For example, a review of the

literature on U.S. Armington elasticities finds values for automobiles which range from near 1 –

indicating a 1 percent cost increase for imported vehicles results in 1 percent decrease in vehicle

imports, to values greater than 9. Estimates of bilateral trade elasticity values are less consistent, even

when considered for the same country pair. The average of values found for U.S. imports of vehicles is

just below 5 (Donelly, Johnson, Tsigas, & Ingersoll, Revised Armington Elasticities of Substitution for the

USITC Model and the Concordance for Constructing a Consistent Set for the GTAP Model, 2004) (Zhang

& Verikios, 2006) (Gallaway, McDaniel, & Rivera, 2003). A separate review of the pattern of vehicle

imports by vehicle segment, combined with estimates of cross-price elasticities finds, on a sales-

weighted basis, imported vehicles belong to a segment with an elasticity value of 6, based upon 2017

sales and import segmentation. With this finding and considering the Armington elasticity literature,

CAR modeled the sales response of imports and domestic (U.S.-assembled) vehicles to a change in

relative prices such that a 1 percent increase in imported vehicle prices, relative to the prices of

domestic vehicles, results in a market share shift of 5 percent away from imported vehicles and towards

domestic vehicles.

Compliance with USMCA Rules of Origin

To evaluate the potential for USMCA to disrupt existing North American vehicle production, CAR

developed estimates of total North American content, and Canadian and U.S. labor content, for model

year 2018 vehicles assembled in North America. To evaluate the ability of each vehicle to comply with

the other requirements of USMCA rules of origin, CAR additionally cataloged the sources of each

vehicle’s engine, transmission, and for electric vehicles, propulsion battery. Data on the sourcing of steel

and aluminum used in vehicle manufacturing are unavailable, so CAR’s estimates assume all North

American vehicles comply with this requirement.

To develop these estimates, CAR relied upon data from vehicle model-specific data from the American

Automobile Labeling Act (AALA) and industry-wide data for materials and parts purchases, gross output,

and value-added from the U.S. 2012 Economic Census, the U.S. Annual Survey of Manufacturers,

Statistics Canada, and Instituto Nacional de Estadística y Geografía. In calculating NAFTA content, CAR

applied industry-wide averages to individual vehicle models in conjunction with the AALA data. CAR also

relied on trade flow data to contextualize CAR’s content estimates and cross-checked the vehicle,

engine, and transmission sourcing with two commercially-available datasets.

3

Additionally, one

automaker provided limited feedback on the accuracy of CAR’s estimates for their products. CAR

acknowledges the existence of several shortcomings in the use of AALA data for this purpose, but the

AALA data is only publicly-available dataset for analyzing light vehicle content.

4

Due to limitations in

these publicly available data sources, CAR’s content share estimates are imprecise but directionally

correct.

3

LMC Automotive and IHS|Markit

4

NHTSA regulation Part 583 (49 CFR 583)—Automobile Parts Content Labeling.

© CENTER FOR AUTOMOTIVE RESEARCH | 2019

23

Depending upon the assumptions made, between 47 and 120 vehicle models do not comply with

USMCA rules of origin, representing the best and worst cases for compliance, respectively. Considering

only models which are assembled outside of the United States, the most generous assumption set

suggests 27 vehicle models fail to meet USMCA requirements, while under the worst-case scenario for

compliance, 32 models assembled in Canada or Mexico fail to meet USMCA. To avoid overstating the

disruption which USMCA may cause, CAR utilizes the best-case compliance scenario – that only 27

models assembled in Canada or Mexico fail to comply – to estimate impacts of each trade policy

scenario. Additional guidance is provided by a timely statement issued by Mexico – that 32 percent of

2018 vehicle output would not meet USMCA rules of origin requirements (Morales, 2018). This share of

Mexican production failing to meet USMCA is almost perfectly matched by the share indicated under

the “best-case” assumption set.

For the 27 vehicle models which are assembled in either Canada or Mexico and fail to comply under the

most-generous assumption set, 24 met the NAFTA requirements. Adoption of USMCA would see these

models newly exposed to import tariffs – for passenger cars imported into the United States, a 2.5

percent tariff would be assessed, and for cargo vehicles such as pickup trucks and cargo vans, the MFN

tariff rate is 25 percent. Across these 24 models, the average potential tariff is USD 635, but ranges from

USD 321 to USD 7,900. Despite these potentially large tariff costs, automakers are unlikely to bring

production of these models into compliance with USMCA, as each of these models fails to comply with

multiple criteria in the USMCA rules of origin.

For the 24 models assembled in either Canada or Mexico that do not appear to meet USMCA but do

conform with NAFTA rules of origin, CAR estimates that 8 will fail the USMCA core parts requirement. All

8 use an engine imported from outside North America, and 1 uses both an engine and transmission from

outside North America. These 8 vehicle models span 5 manufacturers, and even those models from the

same manufacturer are significantly different in their specifications that the models cannot share a

powertrain. Further, total U.S. sales volumes across these 8 models are just 225,000 units. Even if all of