UNITED STATES DISTRICT COURT

SOUTHERN DISTRICT OF INDIANA

INDIANAPOLIS DIVISION

COMPLAINT FOR PERMANENT INJUNCTION, RESTITUTION, CIVIL

PENALTIES, AND OTHER EQUITABLE RELIEF

INTRODUCTION

The Plaintiff, the State of Indiana, by and through its Attorney General

Theodore E. Rokita

, files

this Complaint

pursuant to statutes as set forth below

against MV REALTY OF INDIANA, LLC, MV REALTY HOLDINGS, LLC, MV

REALTY PBC, LLC, MV REALTY BROKERAGE OF INDIANA, LLC, AMANDA J.

CASE NO. ________________

COMPLAINT AND DEMAND

FOR JURY TRIAL

MV REALTY OF INDIANA, LLC, MV

REALTY HOLDINGS, LLC,

MV REALTY PBC, LLC, MV

BROKERAGE OF INDIANA, LLC, AND

AMANDA J. ZACHMAN F/K/A AMANDA

ZUCKERMAN, ANTONY MITCHELL,

DAVID MANCHESTER,

INDIVIDUALLY

,

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 1 of 103 PageID #: 1

2

ZACHMAN f/k/a AMANDA ZUCKERMAN, an individual, ANTONY MITCHELL, an

individual, and DAVID MANCHESTER, an individual, (collectively “Defendants”).

The State of Indiana brings this action to enjoin the Defendants from further

pursuit of an aggressive and illegal robocalling and telemarketing operation that

targeted Hoosier homeowners offering them cash payments in exchange for a future

interest in the sale of the homeowner’s real property. Defendants' “Homeowner

Benefit Agreement” (“HBA”) is nothing more than a disguised extension of credit with

implicit interest to be paid back by the homeowner at a future date. The HBA is

designed to strip the homeowner’s equity in their real property. Through its

misrepresentations and omissions of information related to the true nature of the

HBA product, Defendants have caused substantial and ongoing harm to Hoosier

homeowners.

The marketing, sale, and servicing of the HBAs by Defendants are illegal,

unfair, deceptive, and abusive under numerous Federal and State consumer

protection statutes. Plaintiff seeks to permanently enjoin this illegal conduct, void

and release all HBA agreements and related liens attaching to real property, obtain

restitution for consumer victims, and seek civil penalties for which Plaintiff is entitled

to obtain on behalf of its residents in its role as parens patriae and by operation of

law. In support thereof, the State of Indiana alleges as follows:

JURISDICTION AND VENUE

1.

This Court has subject matter jurisdiction over this action pursuant

to 28 U.S.C. §§ 1331, 1337(a), 1355, the Telephone Consumer Protection Act

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 2 of 103 PageID #: 2

3

(“TCPA”), 47 U.S.C. § 227(g)(2),

the Telemarketing and Consumer Fraud and Abuse

Prevention Act (“Telemarketing Act”)

, 15 U.S.C. § 6103(e), and the Telemarketing

Sales Rule (“TSR”), 16 C.F.R. § Part 310; the Truth-in-Lending Act, (“TILA”) 15

U.S.C. § 1601

et seq.,

via

12 U.S.C. § 5536(a)(1)(A), and

the

Home Ownership

and Equity Protection Act (

“

HO

EPA

”), 15 U.S.C. § 1639,

§§ 1639a – 1639h,

via

15 U.S.C. § 1640(e)

. T

he Court has pendant jurisdiction over the state law claims

pursuant to 28 U.S.C. § 1367.

2.

Venue is proper in this District under 28 U.S.C. §§ 1391(b), 1395(a),

47 U.S.C. § 227(g)(4), 15 U.S.C. § 6103(e),

12 U.S.C. § 5552(a)(1), and 15 U.S.C.

§ 1640(e)

. A substantial part of the events or omissions giving rise to the claims

alleged in this Complaint occurred in this District.

3.

Plaintiff notified the Federal Trade Commission (“FTC”) of this

civil action prior to instituting such action, as required by 15 U.S.C. § 6103(b).

4.

Plaintiff notified the Federal Communications Commission

(“FCC”) of this civil action prior to instituting such action, as required by 47

U.S.C. §§ 227(e)(6)(B) and (g)(3).

5.

Plaintiff notified the Consumer Financial Protection Bureau (

“

CFPB

”

)

of this civil action prior to instituting such action, as required by 12 U.S.C. § 5552(b)

and 15 U.S.C. § 1640(e).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 3 of 103 PageID #: 3

4

PARTIES

A. PLAINTIFF

6.

Plaintiff, State of Indiana, by and through its Attorney General

Theodore E. Rokita, by undersigned counsel, is authorized by 47 U.S.C. §

227(g)(l) to file actions in federal district court to enjoin violations of, and

enforce compliance with, the TCPA on behalf of residents of the State of

Indiana, and to obtain actual damages or damages of five hundred dollars

($500) for each violation, and up to treble that amount for each violation

committed willfully and knowingly.

The Attorney General

is authorized by

15

U.S.C. § 6103(a) to file actions in federal district court to enjoin violations of and

enforce compliance with the TSR

and to secure remedies allowed under the

15

U.S.C. § 6103.

Section 1036(a)(l)(A) of the Consumer Financial Protection Act of 2010

("CFPA"), 12 U.S.C. § 5536(a)(l)(A), authorizes the Plaintiff to bring actions for

violations of other Federal consumer financial laws set forth in the CFPA, including

TILA, 15 U.S.C. § 1601, et seq. and HOEPA. The Attorney General is authorized by

12 U.S.C. § 5536(a)(1)(A) to file actions in federal district court to enjoin violations of

and enforce compliance with the Truth-in-Lending Act and to secure remedies

allowed under TILA. The Attorney General is authorized by 12 U.S.C. § 5536(a)(l)(A)

to file actions in federal district court to enforce HOEPA and to secure remedies

allowed under that statute.

The Attorney General is an enforcement authority

under Indiana state law and is therefore authorized to bring this action and to

seek injunctive and other statutory relief pursuant to Indiana Code § 24-4.7

et

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 4 of 103 PageID #: 4

5

seq.

(Telephone Solicitation of Consumers), § 24-5-14

et seq.

(Auto-Dialer Act), §

24-5-12

et seq.

(Telephone Solicitation), § 24-5-0.5

et seq.

(Consumer Sales), § 24-

9

et seq.

(Home Loan Practices Act), and § 24-5-10,

et seq.

(Home Solicitation Sales

Act).

B. CORPORATE DEFENDANTS

7.

Defendant MV Realty of Indiana, LLC is an Indiana domestic limited

liability company incorporated November 4, 2021, with a principal office address

of 219 N. Dixie Blvd., Delray Beach, FL, 33444.

8.

Defendant MV Realty Holdings, LLC is a Florida limited liability

company incorporated on August 19, 2019, with a principal office address of 219

North Dixie Blvd., Delray Beach, FL, 33444.

9.

Defendant MV Realty PBC, LLC is a Florida limited liability company

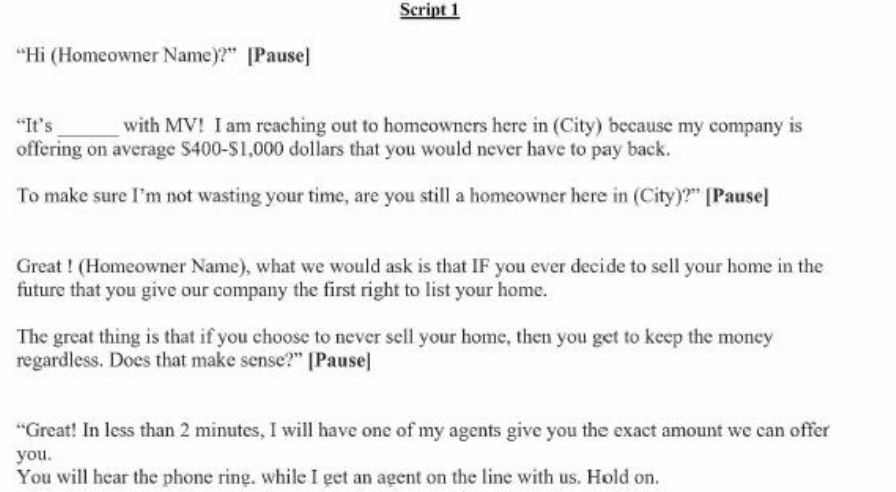

incorporated on August 5, 2014, with a principal office address of

219 N. Dixie Blvd.,

Delray Beach, FL, 33444.

10.

Collectively MV Realty of Indiana, LLC,

MV Realty Holdings, LLC,

and MV Realty PBC, LLC

will be referred to in this complaint as “MV Realty HBA

Defendants” as the State of Indiana seeks to assert joint and several liability as

to each claim asserted.

11.

Defendant MV Brokerage of Indiana, LLC (“MV Brokerage”) is an

Indiana domestic limited liability company incorporated October 3, 2022, with a

principal office address of 219 N. Dixie Blvd., Delray Beach, FL, 33444.

MV

Brokerage of Indiana, LLC maintains an expired Real Estate Broker Company

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 5 of 103 PageID #: 5

6

License No. RC52200259 and is managed by its Managing Broker, Kenton

Williams, License No. RB14023379.

12.

MV Brokerage of Indiana's Real Estate Broker Company License No.

RC52200259 expired on June 30, 2023. At the time of this filing, MV Brokerage

of Indiana's Real Estate Broker Company License No. RC52200259 remains

expired and renders MV Brokerage unable to engage in the practice of real

estate

1

.

13.

Upon information and belief, MV Realty Holdings, LLC is the entity that

owns one hundred percent of MV Realty PBC, LLC.

14.

Upon information and belief, MV Realty of Indiana, LLC and

MV

Brokerage of Indiana, LLC

are affiliates or wholly owned subsidiaries of MV Realty

PBC, LLC.

15.

MV Realty PBC, LLC operates substantially the same line of

business across at least 32 states using multiple corporate entities. In this case,

it is alleged that each state-specific LLC formed for the purpose of conducting

business there is simply an alter ego of the Florida-based company and its

executives, officers, and agents.

16.

Collectively, this entire enterprise will be referred to as “MV Realty.”

“MV Realty” encompasses all corporate Defendants and individual Defendants.

1

Another broker license was issued in the name “MV Realty,” license no.

RC52100307, also expired, with no clear connection to any of the entities named in

this Complaint.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 6 of 103 PageID #: 6

7

17.

Each corporate Defendant above has transacted business in the

Southern District of Indiana by utilizing a network of Indiana-based sales

associates to engage in consumer transactions, as well as, by placing liens on real

property located in Indiana as a means of securing payment from consumers

related to MV Realty’s disguised credit transactions known as HBAs.

C. INDIVIDUAL DEFENDANTS

18.

Defendant Amanda J. Zachman f/k/a Amanda Zuckerman (“Zachman”)

is an individual residing in Florida. At all times relevant to this Complaint, she was

a manager and lead broker of MV Realty and directly participated in, managed,

operated, controlled, and had the ability to control the operations of MV Realty PBC,

LLC and its affiliates and subsidiaries.

19.

At all times relevant to this Complaint, acting alone or in concert with

others, Zachman formulated, directed, controlled, had the authority to control, or

participated in the acts and practices of MV Realty, including the acts or practices

set forth in this Complaint.

20.

Through her direct participation in, and control over, MV Realty,

Zachman had knowledge of the acts and practices constituting the violations alleged

herein, had control over them, and directly participated in them.

21.

Defendant Zachman personally participated in the design and execution

of Homeowner Benefit Agreements on behalf of Defendant MV Realty of Indiana,

LLC.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 7 of 103 PageID #: 7

8

22.

Defendant Antony “Tony” Mitchell (“Mitchell”) is an individual residing

in Florida. At all times relevant to this Complaint, he was an executive of MV Realty

and directly participated in, managed, operated, controlled, and had the ability to

control the operations of MV Realty PBC, LLC and its affiliates and subsidiaries.

23.

At all times relevant to this Complaint, acting alone or in concert with

others, Mitchell formulated, directed, controlled, had the authority to control, or

participated in the acts and practices of MV Realty, including the acts or practices

set forth in this Complaint.

24.

Through his direct participation in, and control over, MV Realty,

Mitchell had knowledge of the acts and practices constituting the violations alleged

herein, had control over them, and directly participated in them.

25.

Defendant Mitchell is an officer of Defendant MV Realty Holdings, LLC.

26.

Defendant David Manchester (“Manchester”) is an individual residing

in Florida. At all times relevant to this Complaint, he was the Managing Director and

Chief Operating Officer of MV Realty and directly participated in, managed,

operated, controlled, and had the ability to control the operations of MV Realty PBC,

LLC and its affiliates and subsidiaries.

27.

At all times relevant to this Complaint, acting alone or in concert with

others, Manchester formulated, directed, controlled, had the authority to control, or

participated in the acts and practices of MV Realty, including the acts or practices

set forth in this Complaint.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 8 of 103 PageID #: 8

9

28.

Through his direct participation in, and control over, MV Realty,

Manchester had knowledge of the acts and practices constituting the violations

alleged herein, had control over them, and directly participated in them.

29.

Defendants Zachman, Mitchell, and Manchester are officers of

Defendant

MV Realty PBC, LLC.

30.

Defendants Zachman, Mitchell, and Manchester are officers of

Defendant MV Realty of Indiana, LLC.

31.

Defendant Manchester led MV Realty's operations team, which included

Defendant Zachman.

32.

Defendants Manchester and Zachman had access to, could review, and

33.

Defendant Zachman has responded to consumer complaints.

34.

Defendant Manchester was responsible for reviewing and approving MV

Realty's advertising.

35.

As principals, officers, and agents of MV Realty, Zachman, Mitchell, and

Manchester, acting both individually and collectively, have directed the business and

affairs of MV Realty, and are jointly and severally liable for the unfair, deceptive, and

abusive acts and practices as alleged in this Complaint.

36.

As principals, officers, and agents of MV Realty, Zachman, Mitchell, and

Manchester have all transacted business in the Southern District of Indiana.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 9 of 103 PageID #: 9

10

37.

As principals, officers, and agents of MV Realty, Zachman, Mitchell, and

Manchester have so misused to corporate form as to promote fraud, injustice, and

illegal activities as stated herein.

FACTUAL ALLEGATIONS

A. BACKGROUND

38.

MV Realty Holdings, LLC and MV Realty PBC, LLC are both Florida-

based companies operating in Indiana and in at least 32 other states.

39.

MV Realty of Indiana, LLC and MV Brokerage of Indiana, LLC are both

Indiana domestic limited liability companies affiliated with the Florida-based

companies with common ownership and control.

40.

Sometime in 2019, MV Realty designed and began aggressively

marketing a product called the Homeowner Benefit Agreement (“HBA”). MV Realty

began the program in Florida and quickly expanded into multiple jurisdictions,

including Indiana.

41.

MV Realty refers to the entire program of selling HBAs as the

Homeowner Benefit Program. In training and marketing materials, MV Realty uses

the terms “Homeowner Benefit Program” and “Homeowner Benefit Agreement”

interchangeably.

42.

To market HBAs, MV Realty employed “Transfer Specialists,” who were

remote telemarketers, and “Sales Agents,” who were licensed Indiana real estate

agents.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 10 of 103 PageID #: 10

11

43.

As part of its investigation, Plaintiff deposed Todd W. Schneider on

March 17, 2023. Mr. Schneider was a Sales Agent working for MV Realty. A true and

accurate copy of the deposition is attached to this Complaint as Exhibit A. A true

and accurate copy of the exhibits shown to Mr. Schneider as part of the deposition

are attached as Exhibit B.

44.

As of the date of this filing, MV Realty and related entities and

individuals have been sued by Attorneys General in Florida, Ohio, Massachusetts,

North Carolina, Pennsylvania, and New Jersey.

45.

A Massachusetts court has entered a preliminary injunction against MV

Realty,

2

in which the Court found:

“that the Commonwealth is likely to succeed in

proving that MV has engaged in a pattern of unfair

and deceptive conduct . . . by tricking homeowners

into thinking that they would never have to repay

the amounts that MV advanced to them and that

they would owe no interest to MV, hiding the fact

that MV would record a mortgage on the

borrower’s property . . ., falsely representing that

MV would serve as their agent in selling their home

when MV never had any intent of doing so, not

giving the borrower homeowners copies of their

contract with and mortgage to MV until after the

three-day period to rescind the arrangement

expires, . . . and unlawfully closing mortgage loans

without being represented by an attorney.”

Emphasis added.

2

Decision and Order Allowing the Commonwealth’s Motion for Preliminary

Injunction (Ordered February 21, 2023), https://www.mass.gov/doc/20230221-comm-

v-mv-realty-pi-decision/download.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 11 of 103 PageID #: 11

12

46.

A North Carolina court also entered a preliminary injunction against

MV Realty.

3

B. THE DESIGN AND GROWTH OF THE HBA PRODUCT IN INDIANA

47.

As early as January 2022, MV Realty began recording HBA agreements

in county recorders offices across Indiana.

48.

MV Realty rapidly expanded to include, to-date, at least 366 HBAs

recorded across at least 65 Indiana counties.

49.

Defendants marketed the HBA program as a “loan alternative,” offering

between a $300 to $5,000 payment if the homeowner agrees to use MV Realty as their

listing agent should they decide to sell their home in the next forty (40) years.

50.

The amount paid to consumers, as a “Promotion Fee,” was based on a

valuation model designed within Defendants’ proprietary case management system.

Using this system, Sales Agents would offer cash payments totally approximately

0.3% or .003 of the home’s total estimated value.

51.

During the summer of 2022, MV Realty changed the amount offered to

consumers to 0.27% or .0027 of the home’s total value, based on a directive from

investors to respond to changing market conditions and rising interest rates.

52.

Pursuant to the HBA agreement, consumers are purportedly bound by

a forty (40) year contract with MV Realty wherein they are required to retain the

3

Attorney General Josh Stein Wins Preliminary Injunction in MV Realty Case,

Attorney General Josh Stein (Aug. 31, 2023), https://www.mass.gov/doc/20230221-

comm-v-mv-realty-pi-decision/download.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 12 of 103 PageID #: 12

13

company as listing agent should they decide to sell the home any time in the forty

(40) year period.

53.

Upon information and belief, a forty (40) year listing agreement is far

more onerous than the industry standard for real estate listing contracts in the State

of Indiana.

54.

In Indiana, the largest “Promotion Fee” paid to a Hoosier was $2,080 for

a homeowner in Morgan County. The lowest payment was $340 to a homeowner in

St. Joseph County.

55.

The average payment to Indiana consumers in return for signing an

HBA agreement was a mere $635.09.

56.

Sales Agents were paid a $500 commission, as employees, for each

homeowner they were able to sign up for an HBA.

57.

In some circumstances, the Sales Agents received a larger commission

than the homeowner received as an incentive payment in connection with the HBA.

58.

In Indiana, MV Realty paid their Sales Agents more in commission than

118 homeowners were paid to sign an HBA. Thus, MV Realty paid more in

commission for approximately 32% of their Indiana HBAs.

59.

MV Realty actively monitors and strictly enforces the one-sided and

onerous terms of the HBA if the homeowner deviates from contract, requiring an

Early Termination Fee to be paid in an amount equal to 3% of the market value of

the home (as determined by MV Realty at the time the fee is assessed).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 13 of 103 PageID #: 13

14

60.

The market value of the home used in determining the 3% is the greater

of the property's value at the time the HBA was signed or the fair market value of

the property when there is an Early Termination Event or breach. This is determined

by MV Realty.

61.

The HBA agreement grants MV Realty a purported right to receive sales

proceeds from homeowners, resulting in a minimum 10x rate of return for MV Realty

upon repayment. For a token amount of money paid to a homeowner, MV Realty

unfairly stands to gain potentially tens of thousands of dollars in return.

62.

The incentive payment paid to homeowners, described in the HBA as a

“Promotion Fee,” is a disguised credit transaction with an implied rate of interest

that can be quantified when either: a.) the homeowner utilizes MV Realty as their

listing broker and consummates a sale; or b.) the homeowner is subject to an “Early

Termination Event” subjecting them to have to pay an Early Termination Fee. In

either case, the implied rate of interest is usurious, unfair, deceptive, and abusive.

63.

If a homeowner were to pass away during the 40-year HBA term, which

has happened to homeowners subject to the agreements in Indiana, MV Realty has

sought to have their heirs either assume the obligations of the HBA and use MV

Realty as their listing broker or pay 3% of the value of the home (valued at MV

Realty’s discretion) as an Early Termination Fee.

64.

As part of the investigation into the HBAs, Plaintiff sent surveys to

Hoosier homeowners with an HBA attaching to their real property.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 14 of 103 PageID #: 14

15

65.

Seventy percent (70%) of homeowners surveyed reported that they were

not adequately informed that the agreement would last for 40 (forty) years.

66.

Eighty-three percent (83%) of homeowners surveyed reported that they

were not informed that the HBA agreement could possibly be binding on their heirs.

67.

Seventy-eight percent (78%) of homeowners surveyed reported that they

were not informed of their ability or timeline to cancel or rescind the agreement.

68.

Ninety-one percent (91%) of homeowners surveyed indicated that they

were not informed that MV Realty would record a Memorandum of Homeowner

Benefit Agreement in the county recorder’s office where their real property was

located.

69.

At least one targeted homeowner had previously been diagnosed with

dementia and was subject to a power of attorney at the time the HBA agreement was

purportedly executed because he was not able to handle his own financial affairs.

With the assistance of his Power of Attorney, he returned the money to MV Realty in

the form of a check demanding that they release him from his agreement. The

consumer reported that the check remains uncashed and that MV Realty has not

responded to his correspondence.

70.

Another consumer survey respondent indicated that he had been trying

to contact MV Realty to sell his house and that they would not respond to his requests

for a listing.

71.

MV Realty recorded the HBA agreements or a Memorandum of HBA in

the public record of the county recorder’s office where the real property is located.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 15 of 103 PageID #: 15

16

This action, of which 91% of surveyed consumers are not even aware, has created a

lien or cloud on title that restricts homeowners from selling or transferring any

interest they have in the real property without making repayment to MV Realty.

72.

The lien also restricts homeowners from accessing their home equity

without paying a usurious and abusive rate of interest in the form of an Early

Termination Fee to MV Realty.

73.

In sum, the HBA prevents homeowners from selling, refinancing, or

otherwise accessing their home equity without first satisfying the lien.

74.

Mr. Schneider testified that other Sales Agents at MV Realty were

having issues with the HBA being lifted to do a refinance. Ex. A (Schneider

Deposition) at 92:9-16. Further, MV Realty would not lift the HBA in some cases

because the person did not have enough equity. Id at 156:21-157:4.

75.

The language in the HBA relating to public recordings deceptively states

as follows:

76.

This language does not explicitly indicate that MV Realty intends to file

a lien against the homeowner’s property.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 16 of 103 PageID #: 16

17

77.

In fact, it is deceptively inconsistent with the FAQ on MV Realty’

website at the time of filing, which states as follows

4

:

78.

Instead of just directly indicating that the Memorandum of HBA can

and will likely constitute a lien that must be released prior to the homeowner

consummating a sale, refinance of their mortgage debt, or other disposition involving

a homeowner’s real property, MV Realty suggests that the HBA might only be a lien

in the event of a homeowner’s breach of the HBA.

79.

MV Realty’s communications with homeowners regarding the HBA

constituting a lien against their real property are false and misleading and meant to

conceal the fact that the Memorandum of HBA can and will serve as a cloud on a

homeowner’s title to their home from the moment their executed HBA is executed

and subsequently recorded.

80.

In MV Realty’s marketing materials and communications with

homeowners, MV Realty conceals the fact that these memoranda act as liens against

the homeowners’ real property.

4

Frequently Asked Questions, MV Realty, https://homeownerbenefit.com/?src=9#faq

(last visited July 5, 2023).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 17 of 103 PageID #: 17

18

81.

MV Realty also instructed its Sales Agents not to send homeowners the

HBA contract in advance of the signing of the HBA. Ex. A at 86:4-22; 175:5-7.

82.

In MV Realty marketing and training materials as well as in

communications with borrowers, MV Realty deceptively states that the money they

lend to homeowners does not have to be paid back.

83.

Despite deceptively claiming that the money they were providing to

homeowners in exchange for the HBA was not a loan and not required to be paid back,

MV Realty at various times purchased lead data for those whose purpose in providing

their information was for “Refinance, Cash Out, VA and FHA” as well as “personal

loans” – evidencing a clear intent to target homeowners seeking loans.

84.

At the time of this filing and since June 30, 2023, MV Brokerage of

Indiana has an expired Real Estate Broker License.

85.

MV Brokerage of Indiana and Defendants are currently unable to legally

sell a home for a commission in Indiana.

86.

On August 23, 2023, Defendant Mitchell sent Plaintiff a response to a

consumer complaint. In the response, Defendant Mitchell wrote: “MV stands ready

to assist [consumer] in selling her home in the event that she, in her sole discretion,

ever decides to do so.”

87.

Defendant Mitchell signed the letter as President of MV Realty of

Indiana, LLC.

88.

Defendants are therefore unable to legally perform their agreed duties,

even if ephemeral, pursuant to the HBAs they executed with Indiana consumers.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 18 of 103 PageID #: 18

19

C. FACTS RELATED TO DOCUMENT EXECUTION PROCEDURES

89.

In addition to the foregoing, MV Realty’s document execution

procedures failed to ensure that homeowners had a meaningful opportunity to review

and understand the written terms of the agreement prior to execution.

90.

To execute the HBA, MV Realty sent a third-party notary to meet the

homeowner, typically at his or her home. MV Realty rarely provided a copy of the

HBA prior to the appointment with a notary.

91.

In response to Plaintiff's survey, seventy percent (70%) of respondents

indicated that they were not offered time to review the documents prior to signing.

92.

Further, at the notary signing, the Sales Agent tasked with executing

the 40-year HBA was typically not present, and only available by phone to answer

questions.

93.

MV Realty’s document execution procedures have caused consumer

confusion because the terms hidden in the small type of the HBA materially differ

from the simple deal that MV Realty represented to consumers in MV Realty's

marketing and solicitation calls.

94.

MV Realty fails to disclose critical contract terms in their

communications with homeowners, rarely provides advance copies of the HBA, and

engages in swift document execution, leaving consumers trapped by fine print and

legalese that they had no real opportunity to read and understand.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 19 of 103 PageID #: 19

20

D. FACTS RELATED TO MV REALTY’S ILLEGAL ROBOCALLING AND

TELEMARKETING

95.

MV Realty has boasted: “[t]he company’s Homeowner Benefit Program

has grown from 7,778 contracts in 2021 to 32,000 as of August 2022” and that it “is

on track to expand its portfolio to over 100,000 over the next 12 months.”

96.

To meet these aggressive goals, MV Realty relied on their relentless

illegal robocalling and telemarketing campaign.

97.

MV Realty devised a robocalling and telemarketing scheme that

targeted Hoosiers, including Hoosiers on the Indiana Do Not Call List and National

Do Not Call Registry.

98.

MV Realty's robocalls and telemarketing calls invaded Hoosiers' privacy

and resulted in monetary losses to Hoosiers, including consumers.

99.

MV Realty used telemarketing employees, called Transfer Specialists,

that initiated or made outbound calls, left prerecorded voicemails, and/or sent text

messages to Hoosiers.

100.

MV Realty also used Indiana licensed real estate agents, “Sales Agents”,

to initiate telephone solicitations to Hoosiers. Under this model, Sales Agents

transformed into telemarketers, using their own cell phones and landlines to make

outbound calls to leads that MV Realty required them to call.

101.

If a consumer was interested in learning more and it was a call from a

Transfer Specialist, the Transfer Specialist would transfer the Indiana consumer to

an Indiana Sales Agent to complete the HBA sales process.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 20 of 103 PageID #: 20

21

102.

On several occasions, Indiana consumers complained about receiving

robocalls and prerecorded voicemails to Sales Agents. At times, these Sales Agents

would then bring up complaints during weekly meetings and trainings.

103.

For many of these trainings and weekly meetings, Defendants Zachman

and Manchester would be present.

104.

Internally, MV Realty used Slack so that the Sales Agents, Transfer

Specialists, other employees, and management, including Defendants Zachman,

Mitchell, and Manchester, could communicate.

105.

Upon information and belief, Defendants Zachman, Mitchell, and

Manchester had the ability to view MV Realty Slack messages sent by MV Realty

employees.

106.

Broker Kenton Williams was in an Indiana-specific Slack channel with

other Indiana Sales Agents.

107.

In this Indiana-specific channel, Indiana Sales Agents would discuss

issues, including issues with MV Realty's telemarketing.

108.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester were on notice and/or had knowledge that MV Realty's telemarketing

programs were violating federal and state telephone privacy laws and/or consumer

protection laws.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 21 of 103 PageID #: 21

22

109.

MV Realty's telemarketing program regarding Transfer Specialists was

designed, managed, and implemented by Defendants Zachman, Mitchell, and

Manchester.

110.

MV Realty's telemarketing program regarding Indiana Sales Agents

was designed, managed, and implemented by Zachman, Mitchell, and Manchester.

Transfer Specialists - Robocalls and Telemarketing

111.

Defendants controlled the MV Realty telemarketing and robocalling

operation from their headquarters in Florida. Defendants provided their employees

with sales scripts and telephone numbers (leads) to call. Further, Defendants

monitored and controlled the calls using a customer relations management (“CRM”)

software platform.

112.

Defendants used a third-party platform or platforms to initiate or make

telephone solicitations, and to leave prerecorded messages on Hoosiers' voicemails.

113.

Defendants made, initiated, or caused to be made or initiated telephone

solicitations and/or telephone sales calls to Hoosiers on the Indiana Do Not Call List

and National Do Not Call Registry.

114.

Defendants made, initiated, or caused to be made or initiated telephone

solicitations and/or telephone sales calls to Hoosiers on the Indiana Do Not Call List

and National Do Not Call Registry.

115.

Defendants made, initiated, or caused to be made or initiated telephone

calls, including telephone solicitations, that left a prerecorded message on Hoosier's

voicemails, including Hoosier's cell phones and/or residential lines.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 22 of 103 PageID #: 22

23

116.

Defendants provided false and misleading information to consumers

about the Homeowner Benefit Program in both live calls and on prerecorded

voicemail messages.

117.

The Federal Communications Commission (“FCC”) investigated MV

Realty’s use of PhoneBurner for telemarketing and robocalling. On January 24, 2023,

the FCC ordered all U.S.-based voice service providers to prevent the transmission

on their networks of suspected illegal robocall traffic from MV Realty using the

PhoneBurner platform.

5

118.

The FCC concluded that MV Realty placed nearly 12 million calls to

phone numbers listed on the National Do Not Call Registry.

6

119.

The FCC found:

a. The calls were telephone solicitations;

7

b. Called homeowners “did not give consent to be called and did not

have an established business relationship with MV Realty”;

c. MV Realty “frequently called consumers who repeatedly and

affirmatively asked MV Realty to stop calling them”;

5

Fed. Commc’n Comm’n, Public Notice: FCC Enforcement Bureau Notifies All U.S.-

Based Providers of Apparently Illegal Robocall Traffic from PhoneBurner, Inc. and

MV Realty PBC, LLC, File No. EB-TCD-22-00033721, pp. 2-3,

https://docs.fcc.gov/public/attachments/DA-23-65A1.pdf (Jan. 24, 2023).

6

Id. at 4.

7

Id. at 2.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 23 of 103 PageID #: 23

24

d. MV Realty “[f]ailed to remove homeowners from its calling list

despite being notified by MV Realty’s own employees” that those

homeowners had asked to be removed; and

e. “[T]hat 10,926,635 calls were placed to wireless numbers and

1,022,739 calls were placed to landline phone numbers actively

listed on the DNC Registry.”

8

120.

Upon information and belief, MV Realty engaged in the same conduct in

Indiana and with Hoosier homeowners.

121.

Defendants purchased, gathered, and received leads from third parties.

122.

Once Defendants obtained a lead, they aggressively telemarketed MV

Realty’s Homeowner Benefit Program.

123.

In several instances, Hoosiers asked to opt-out of MV Realty's

telemarketing campaigns, only to continue being called by MV Realty.

124.

Sales Agents notified Defendants during their weekly calls that MV

Realty was recycling leads that were on MV Realty's internal do not call list.

125.

Effectively, MV Realty did not have or follow an internal do not call

procedure or policy, nor did MV Realty avoid calling Hoosiers on the Indiana Do Not

Call List or the National Do Not Call Registry. Thus, Hoosiers had no effective way

to stop or avoid receiving MV Realty's telemarketing calls.

8

Id. at 4.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 24 of 103 PageID #: 24

25

126.

PhoneBurner

9

produced call detail records to Plaintiff. Based on these

records:

a. MV Realty made or initiated approximately 29,478 telephone

solicitations to telephone numbers with an Indiana area code;

b. MV Realty left approximately 17,288 prerecorded voicemails on

telephones that had an Indiana area code;

c. MV Realty made or initiated approximately 3,121 telephone sales

calls to Hoosiers on the Indiana Do Not Call List;

d. MV Realty made or initiated approximately 1912 telephone sales

calls that left a prerecorded voicemail to Hoosiers on the Indiana

Do Not Call List;

e. MV Realty made or initiated approximately 12,483 telephone

solicitations to Hoosiers on the National Do Not Call Registry;

and

f. MV Realty made or initiated approximately 8,157 telephone

solicitations that left a prerecorded voicemail to Hoosiers on

National Do Not Call Registry.

9

The data produced by PhoneBurner is a conservative estimate of calls initiated by

or on behalf of MV Realty. Plaintiff has not obtained complete call records from

PhoneBurner, MV Realty's Sales Agents, who used their personal phones, and from

MV Realty's telemarketing vendors, who also initiated telephone solicitations on

behalf of MV Realty.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 25 of 103 PageID #: 25

26

127.

MV Realty produced to Plaintiff a set of leads that were purchased from

various sources, including but not limited to, PX Inc. and the Wisdom Co.

128.

The price per lead ranged from $0.05 to $2.

129.

Upon information and belief, MV Realty did not have the requisite

consent to call its leads and/or does not possess the requisite proof consent.

130.

In a contract with PX Inc., MV Realty agreed to following language:

Consumer information may not have been collected from

Consumers who have provided “prior express written

consent” as required under the TCPA and/or Do Not Call

List requirements and any applicable rules, regulations

or guidelines. As a result, PX does not make any claim,

representation or assertion that Client, or any third

party, may: (a) call any telephone or mobile phone

numbers contained within any Lead, without first

scrubbing against the National Do-Not-Call-Registry;

and/or (b) call any telephone or mobile phone numbers

contained within any Lead through the use of an

automatic telephone dialing system, pre-recorded or

artificial voice message, or text message, without first

separately obtaining prior express written consent from

each such Consumer, as required under the TCPA.

131.

In a contract with Wisdom Co., MV Realty agreed to be solely

responsible for compliance with all federal and state laws, including the TCPA and

all regulations regarding the National Do Not Call Registry. MV Realty agreed to

take on all the risk that the leads purchased were not compliant with the TCPA.

132.

MV Realty provided Plaintiff with records of 77,901 third-party leads

(“MV Realty Lead List”) related to Indiana consumers.

133.

The MV Realty Lead List had total of 64,035 unique phone numbers.

134.

Each lead contained a phone number, resident name, and address.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 26 of 103 PageID #: 26

27

135.

MV Realty provided Plaintiff with an internal do not call list (“MV

Realty Internal Do Not Call List”) that contained 1,644 entries.

136.

Of these 1,644 entries, six phone numbers were on the list twice.

137.

Of these 1,644 entries, 140 entries included a date and time the person's

phone number was added to the MV Realty Internal Do Not Call List.

138.

Approximately 12,881 phone numbers on MV Realty Lead List were on

the Indiana Do Not Call List.

Approximately 29,996 phone numbers on the MV Realty Lead List were on the

National Do Not Call Registry.

139.

Approximately 344 phone numbers on the MV Realty Internal Do Not

Call List were on the Indiana Do Not Call List.

140.

Approximately 988 phone numbers on the MV Realty Internal Do Not

Call List were on National Do Not Call Registry.

141.

Approximately 34 phone numbers on the MV Realty Customer List were

on the Indiana Do Not Call List.

142.

Approximately 135 phone numbers on the MV Realty Customer List

were on the National Do Not Call Registry.

143.

Approximately 578 phone numbers on the MV Realty Lead List were on

the MV Realty Internal Do Not Call List.

144.

Approximately 5 phone numbers on the MV Realty Customer List were

on the MV Realty Internal Do Not Call List.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 27 of 103 PageID #: 27

28

145.

Approximately 82 phone numbers on the MV Realty Lead List were on

the MV Realty Customer List.

146.

Upon information and belief, MV Realty used caller IDs with Indiana

area codes so that they could match the area codes with the called party.

147.

This practice is called neighborhood spoofing, and it is intended to trick

the call recipient into thinking the call is coming from a fellow Hoosier compared to

a company based in Florida.

148.

The Transfer Specialists' calls and voicemails were telephone

solicitations and/or telephone sales calls.

149.

To initiate or make outbound telephone calls, a Transfer Specialist

would use MV Realty's CRM platform.

150.

Once a Transfer Specialist was ready to initiate or make a telephone

call, the platform would select the phone number to call and then dial the phone

number.

151.

If a consumer would answer the phone call, the Transfer Specialist

would then follow a script provided by MV Realty.

152.

If the call went to voicemail, the Transfer Specialist would click a button

to leave a prerecorded voicemail.

153.

An example of a prerecorded voicemail was

10

:

10

Actual audio of a Realty Scam exploiting the MV Realty Brand captured by

YouMail Inc., YouTube (Feb. 6, 2023),

https://www.youtube.com/watch?v=O5oq7AdFw7c. See also 704-368-0726, YouMail,

https://directory.youmail.com/phone/704-368-0726 (last visited July 6, 2023).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 28 of 103 PageID #: 28

29

Hi, this is Amanda with MV Realty. We're offering cash

homeowners as a part of our homeowner benefit program

you can receive up to $5000 without selling your home or

paying us back. For more details and to find out how

much money you can get please call us back or dial 866-

770-8587.

154.

When a prerecorded voicemail was left, the call would end for the

Transfer Specialist. MV Realty's system, on its own or in combination with a third-

party, would then leave the prerecorded voicemail on the consumer's voicemail.

Simultaneously, the system would begin calling the next lead.

155.

Upon information and belief, the prerecorded voicemail above and other

voicemails were recorded by Defendant Zachman.

156.

If a consumer answered the phone, MV Realty trained its Transfer

Specialists to use calling scripts.

157.

MV Realty's Script 1 read:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 29 of 103 PageID #: 29

30

158.

Script 2 read:

159.

Script 3 read:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 30 of 103 PageID #: 30

31

160.

In all the scripts, MV Realty instructed its Transfer Specialists to tell

the called person that he or she was not going to be asked to pay MV Realty back.

161.

This is a clear misrepresentation of the HBA program.

162.

Further, all the scripts omitted material provisions of the HBA.

163.

As an example, these omissions included, but are not limited to, that the

HBA would create a lien on their property, that the HBA was a 40-year contract, and

that there would be a strictly enforced and large cancellation fee.

164.

In Scripts 2 and 3, MV Realty instructed its Transfer Specialists not to

use the name of the company.

165.

In training sessions, MV Realty instructed Transfer Specialists to say

they were calling from the Homeowner Benefit Program.

166.

This is a clear violation of the TSR and Indiana law, as the Homeowner

Benefit Program was not the name of the entity making the telemarketing call.

167.

Further, MV Realty and its employees made a false representation

and/or implication as to the identity of the entity making the telephone solicitation.

168.

In other trainings and documents, MV Realty instructed its employees

on how to respond to the most common questions. MV Realty called these questions

and/or comments “objections.”

169.

These objections included misrepresentations or omitted material

provisions of the HBA.

170.

One common objection and response was:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 31 of 103 PageID #: 31

32

171.

MV Realty verbally instructed and trained Transfer Specialists to

continue their pitch to call recipients that wanted put on MV Realty's Do Not Call list

or did not want to be called.

172.

Another common objection and response script was:

173.

And:

174.

These are misrepresentations of the nature of the HBA and how the filed

“memorandum” operates under Indiana law.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 32 of 103 PageID #: 32

33

175.

Transfer Specialists were required to make between 60 and 70 calls an

hour, and up to 400 to 450 calls per day. Transfer Specialists also were required to

hit a goal of a ten percent transfer rate for all answered calls.

176.

Upon information and belief, MV Realty hired third-party telemarketers

that initiated or made telephone calls that played a prerecorded message or used an

artificial voice on behalf and to the benefit of MV Realty.

177.

MV Realty sent, made, or initiated text messages to Hoosiers.

178.

At this time, Plaintiff does not know how many texts were sent to

Hoosiers, including Hoosiers on the Indiana Do Not Call List and the National Do

Not Call Registry.

179.

The text messages produced by MV Realty are indicative of MV Realty's

aggressive, deceptive, and abusive sales strategy.

180.

Some of the texts included but were not limited to:

Own a home? Receive up to $5000 cash today without selling. Find out how much you

can get: {SENDER_PHONE}

Our Homeowner Benefit Program can pay you up to $5000, without selling your home.

Find out how much you can get:{SENDER_PHONE}

Hi, this is Amanda. We pay homeowners for the opportunity to list their home if they

ever decide to sell. Clients never need to sell or pay it back. Reach us at

{SENDER_PHONE} to find out how much you qualify for.

Hi, it's Amanda from the Homeowner Benefit Program. We pay homeowners for

agreeing to use MV Realty if they decide to sell their home in the future. Reach us at

{SENDER_PHONE} to find out how much you qualify for.

We want to sign you up for the Homeowner Benefit program - where the Agent pays you.

{SENDER_PHONE} to find out more.

Get paid today without selling your home. Call {SENDER_PHONE} to find out how

much you can get.

Receive a check from the Homeowner Benefit program today - no need to sell. Call

{SENDER_PHONE} to learn more.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 33 of 103 PageID #: 33

34

Indiana Real Estate Agents - Telemarketing

181.

MV Realty employed licensed real estate agents as Sales Agents.

182.

The Sales Agents' job was to sell HBAs through telemarketing.

183.

This telemarketing included inbound and outbound calling using the

Sales Agent's personal phone.

184.

At this time, Plaintiff does not have access to the Sales Agents' phone

records, as the Sales Agents used their personal phones. Thus, there are likely far

more Hoosiers on the Indiana Do Not Call List and National Do Not Call Registry

that were called by Defendants.

185.

MV Realty trained their Sales Agents in telemarketing the HBAs.

186.

MV Realty did not train their Sales Agents in how to sell the homes of

those clients that had an HBA.

187.

For an example, below is a MV Realty new agent training schedule:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 34 of 103 PageID #: 34

35

188.

The Sales Agents were required to claim a minimum of 30 leads per day,

and 150 leads per week.

189.

To claim a lead, the Sales Agent would use MV Realty's CRM platform.

The platform would identify a lead to call, and the Sales Agent would cold call the

lead. During this process, the Sales Agent would input information about the call into

the CRM platform.

190.

Sales Agents had to receive at least 15 inbound calls per week. Inbound

calls were those calls that a Transfer Specialist transferred to a Sales Agent.

191.

When a Transfer Specialist transferred an Indiana inbound call, every

Indiana Sales Agent's phone would ring. The first person to answer the call would

claim the inbound lead.

192.

At some point in July or August of 2022, MV Realty increased the

number of inbound calls to eight per day. Ex. A at 48:8-16.

193.

Further, the Sales Agent had to have two HBA appointments per week,

which is where the HBA sales process would be closed.

194.

Mr. Schneider testified he did not like inbound calls because, among

other things, “we would start our spiel, and these people had no idea what or why

they were being called.” Id. at 51:1-15.

195.

Further, Mr. Schneider stated: “One gentleman . . . He said he got a call,

left a voicemail to call back, something about a prize, and then he called back. And

then he was routed to me because we live in Indiana.” Id. at 52:2-17.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 35 of 103 PageID #: 35

36

196.

Mr. Schneider received transferred calls where the Indiana resident

thought the MV Realty calls were related to a government program. Id. at 52:18-25.

197.

MV Realty provided their Sales Agents with a script for dealing with

inbound calls from Transfer Specialists:

198.

When making outbound calls, Sales Agents had to claim the lead in MV

Realty's CRM platform. After a Sales Agent claimed a lead, MV Realty had a specific

workflow the agent would have to follow. The purpose of this workflow was to follow

up with the Hoosier until an HBA sale was made. This was the workflow:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 36 of 103 PageID #: 36

37

199.

And:

200.

Even when the first call did not work, MV Realty trained their Sales

Agents to continue calling:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 37 of 103 PageID #: 37

38

201.

Effectively, MV Realty required its employees to continue bothering

Hoosiers, and Hoosiers on the Indiana Do Not Call List and National Do Not Call

Registry, over and over until MV Realty sold an HBA.

202.

If a Sales Agent followed MV Realty's instruction, the call recipient

would receive up to five telephone solicitations and/or telephone sales calls before

being put back in the marketing funnel.

203.

Thus, the total number of telephone calls made to Hoosiers on the

Indiana Do Not Call List and the National Do Not Call Registry could be multiples

more than indicated above.

204.

Further, MV Realty trained their Sales Agents on how many calls the

most successful sellers make:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 38 of 103 PageID #: 38

39

205.

Internally, this was called “smiling and dialing.” Id. at 172:1-7.

206.

During the weekly meetings with the Sales Agents, MV Realty trainers

“would list who did the most that week, and then anybody who got four of them

[HBAs] or above, they were mentioned by name.” Id. at 186:9-17.

207.

Despite all this pressure to make sales, MV Realty's Sales Agents were

instructed not to sell HBAs to friends and family. MV Realty's CRM training guide

specifically stated:

208.

MV Realty provided Sales Agents with calling scripts.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 39 of 103 PageID #: 39

40

209.

For example:

210.

Regarding outbound calls, Mr. Schneider stated: “Most people see the

call, so they don't answer, so I leave a short message like this is Todd with the

Homeowner Benefit Program, blah, blah, blah.” Id. at 54:1-5.

211.

It is a violation of the TSR and Indiana state law to not include the name

of the business in telemarketing and/or telephone sales calls. Homeowner Benefit

Program is not the name of MV Realty.

212.

Again, MV Realty and its employees made a false representation and/or

implication as to the identity of the entity making the telephone solicitation.

213.

Further, MV Realty trained the Sales Agents on common questions

(objections) and provided sample responses. For example:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 40 of 103 PageID #: 40

41

214.

When asked how often call recipients said this sounds like a scam, Mr.

Schneider stated: “Not all of them obviously, but many of them did say this sounds

like a scam.” Id. at 154:3-6.

215.

Further, MV Realty did not want their Sales Agents to use the word

“lien” when discussing the HBA, and they were instructed to say “memorandum.” Id.

at 174:6-21.

216.

Sales Agents were instructed to ask their customers for referrals.

217.

Upon information and belief, Sales Agents would initiate or make

outbound telephone solicitations and/or telephone sales calls to these referred

consumers.

MV Realty's Do Not Call Policy

218.

Defendants were not registered to receive the Indiana Do Not Call List.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 41 of 103 PageID #: 41

42

219.

Defendants were not registered as a telephone solicitor with the

Consumer Protection Division of the Office of the Attorney General.

220.

MV Realty had an internal do not call policy (“Policy”).

221.

According to the Policy, consumers were directed to contact Defendant

Manchester with questions or concerns.

222.

Despite these policies, MV Realty made or initiated calls to Hoosiers who

asked MV Realty not to be call them and Hoosiers on the National Do Not Call

Registry and the Indiana Do Not Call List.

223.

Further, Transfer Specialists were instructed to continue the telephone

solicitation when Hoosiers asked to be placed on MV Realty's internal do not call list.

224.

In a compliance document, MV Realty stated: “Management is routinely

informed of and overseas (sic) the Internal Do Not Call list and its adherence.”

225.

Depending on how the Sales Agents entered or did not enter information

into the CRM when claiming a lead, consumers could become trapped in a never-

ending cycle of MV Realty calls.

226.

For example, Mr. Schneider stated:

[T]ere was one lady that I spoke with in approximately

the August or September time frame. I guess I accepted

her out of the CRM, and then made the call, then sent the

text. And then, I don't know, I got sidetracked or

whatever, and then she got cycled back in because I didn't

fulfill my thing of saying, hey, I reached out again

through the CRM. Because that's the only way I have to

self report. So I didn't do that, she got cycled back in,

somebody picked her up again and called her, and then

they didn't do what they were supposed to do, and then

she get cycled again. And I think she talked to four

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 42 of 103 PageID #: 42

43

different people that called her that day whenever I got a

hold of her. And I think I was like the fourth one on the

same day, and I said that's next to impossible. I said

that's not possible, and I apologized. But she says please

don't call me. I put her on the DNC list. And then I made

an inquiry on the Monday meeting, and they said on the

Monday meeting that -- they explained how that can

happen because you didn't disposition properly. In other

words, you didn't click on it and say, hey, I made contact,

you didn't follow-up, so she cycled back into the system

and kept going, and somebody didn't follow-up and didn't

-- you know.

Id. at 148:13-149:14

D. INDIVIDUAL LIABILITY OF DEFENDANTS ZACHMAN, MITCHELL,

AND MANCHESTER

227.

Defendants Zachman, Mitchell, and Manchester are also individually

liable for the conduct alleged herein.

228.

Defendants Zachman, Mitchell, and Manchester, as officers of MV

Realty, possessed and exercised the authority to control the policies and trade

practices of MV Realty; were responsible for creating and implementing the illegal

policies and trade practices of MV Realty that are described herein; participated in

the illegal trade practices that are described herein; directed or supervised those

employees of MV Realty who participated in the illegal trade practices that are

described herein; and knew or should have known of the illegality of the trade

practices that are described herein and had the power to stop them, but rather than

stopping them, promoted their use.

229.

Defendants Zachman, Mitchell, and Manchester controlled the illegal

conduct of MV Realty and is vicariously liable for its conduct.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 43 of 103 PageID #: 43

44

230.

Defendants Zachman, Mitchell, and Manchester operated through MV

Realty, and their conduct was one and the same.

231.

Defendants Zachman, Mitchell, and Manchester' conduct through MV

Realty has caused harm to consumers.

232.

Treating MV Realty and Defendants Zachman, Mitchell, and

Manchester as separate entities would further sanction a fraud, promote injustice,

and lead to an evasion of legal obligations.

233.

Defendants Zachman, Mitchell, and Manchester are liable for the illegal

conduct alleged herein because they directly participated in the conduct, authorized

and directed others who committed the illegal conduct with knowledge of its illegality,

and in the case of Defendants Zachman, Mitchell, and Manchester, because he/she

controlled the illegal conduct of MV Realty and acted through his/her company to

harm others.

COUNT I

Violations of the TCPA – 47 U.S.C. §§ 227(b)(1)(A)(iii) and (b)(1)(B)

(Prerecorded Calls to Cellular and Residential Telephone Lines)

(As to all Defendants)

234.

Plaintiff incorporates and realleges each of the preceding paragraphs as

if fully set forth herein.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 44 of 103 PageID #: 44

45

235.

In enacting the TCPA, Congress determined that unwanted prerecorded

voice message calls were a greater nuisance and invasion of privacy than live calls

and that such calls delivered to wireless phones can be costly.

11

236.

The TCPA prohibits any person within the United States, or any person

outside the United States if the recipient is within the United States, from making

any call using an artificial or prerecorded voice to any cellular telephone, with

exceptions for certain emergency calls or calls placed with the prior express consent

of the called party. 47 U.S.C. § 227(b)(1)(A)(iii).

237.

The TCPA prohibits any person within the United States, or any person

outside the United States if the recipient is within the country, from initiating any

telephone call to any residential telephone line using an artificial or prerecorded voice

to deliver a message without the prior express consent of the called party, unless the

call is initiated for emergency purposes, or is exempted by rule or order of the FCC.

47 U.S.C. § 227(b)(1)(B)

238.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated 47 C.F.R. § 64.1200(a)(1)(iii) and 47 U.S.C. § 227(b)(1)(A)(iii) by

engaging in a pattern or practice of initiating or making telephone calls to cellular

11

Rules and Regulations Implementing the Telephone Consumer Protection Act of

1991, CG Docket No. 02-278, Report and Order, 18 FCC Rcd. 14014, 14115, para. 165

(2003) (2003 TCPA Order).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 45 of 103 PageID #: 45

46

telephone lines using artificial or prerecorded voices to deliver a message without the

prior express consent of the called party and where the call was not initiated or made

for emergency purposes or exempted by rule or order of the Federal Communications

Commission under 47 U.S.C. § 227(b)(2)(B).

239.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated 47 C.F.R. § 64.1200(a)(2) by engaging in a pattern or practice of

initiating telephone solicitations to cellular telephone lines in Indiana using artificial

or prerecorded voices to deliver a message advertising MV Realty's products and

services without the prior express written consent of the called party.

240.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated 47 C.F.R. § 64.1200(a)(3) and 47 U.S.C. § 227(b)(l)(B) by

engaging in a pattern or practice of initiating telephone calls to residential telephone

lines of Indiana residents using artificial or prerecorded voices to deliver a message

without the prior express written consent of the called party and where the call was

not initiated for emergency purposes or exempted by rule or order of the Federal

Communications Commission under 47 U.S.C. § 227(b)(2)(B).

241.

A telephone solicitation means “the initiation of a telephone call or

message for the purpose of encouraging the purchase or rental of, or investment in,

property, goods, or services, which is transmitted to any person.” 47 C.F.R. §

64.1200(f)(15g).

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 46 of 103 PageID #: 46

47

242.

Defendants' telephone calls were telephone solicitations.

243.

Defendants' HBA is a good or service.

244.

The violative calls include, but are not limited to, prerecorded voicemails

left on Indiana consumers' residential lines and/or cellular phones by MV Transfer

Specialists.

245.

Upon information and belief, Defendants made or initiated

approximately 17,288 violative calls to Indiana residents.

246.

It is believed and averred that Defendants made and/or participated in

additional calls that violated the TCPA; the numbers, dates, and times of said calls

are known to Defendants, but are not known to Plaintiff at this time.

247.

Plaintiff asserts that Defendants may have committed additional

violations of the TCPA arising from their participation in these additional calls.

248.

Defendants' violations were direct and/or vicarious violations.

249.

Defendants’ violations were willful and knowing.

COUNT II

Violations of the TCPA – 47 U.S.C. §§ 227(c) and 47 C.F.R. § 64.1200(c)(2)

(Calls to Telephone Numbers on the National Do Not Call Registry)

(As to all Defendants)

250.

Plaintiff incorporates and realleges each of the preceding paragraphs as

if fully set forth herein.

251.

The TCPA recognized that there is a need to protect residential

telephone subscribers’ privacy rights to avoid receiving telephone solicitations to

which they object. 47 U.S.C. § 227(c)(1). To meet this directive, a single national

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 47 of 103 PageID #: 47

48

database of telephone numbers was compiled of residential subscribers who objected

to receiving telephone solicitations. See 47 U.S.C. § 227(c)(3).

252.

Pursuant to 47 C.F.R. § 64.1200(c)(2), all persons and entities are

prohibited from initiating any telephone solicitation to a residential telephone

subscriber who has registered his or her telephone number on the National Do Not

Call Registry, which registrations must be honored indefinitely, or until the

registration is cancelled by the consumer.

253.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated 47 C.F.R. § 64.1200(c)(2) and 47 U.S.C. § 227(c) by engaging in

a pattern or practice of initiating telephone solicitations to residential telephone

subscribers in Indiana whose telephone numbers were listed on the National

Do Not

Call

Registry.

254.

The violative calls include but are not limited to the telephone

solicitations initiated by Transfer Specialists and Sales Agents to Indiana consumers

on the National Do Not Call Registry.

255.

Upon information and belief, Defendants made or initiated

approximately 12,483 violative calls to Indiana residents through PhoneBurner.

256.

Upon information and belief, Defendants made or initiated at least one

telephone solicitation to Indiana residents on the MV Realty Lead List.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 48 of 103 PageID #: 48

49

257.

Upon information and belief, Defendants made or initiated

approximately 29,996 telephone solicitations to Indiana residents on the MV Realty

Lead List that were on the National Do Not Call Registry.

258.

In total, Defendants made or initiated approximately 42,479 violative

calls.

259.

It is believed and averred that Defendants made and/or participated in

additional calls that violated the TCPA; the numbers, dates, and times of said calls

are known to Defendants, but are not known to Plaintiff at this time.

260.

Plaintiff asserts that Defendants may have committed additional

violations of the TCPA arising from their participation in these additional calls.

261.

Defendants' violations were direct and/or vicarious violations.

262.

Defendants’ violations were willful and knowing.

COUNT III

Violations of the Telemarketing Sales Rule

16 C.F.R. §§ 310.3-310.4

(As to all Defendants)

263.

Plaintiff incorporates and realleges each of the preceding paragraphs as

if fully set forth herein.

264.

Pursuant to the Telemarketing Act, Congress directed the FTC to enact

rules prohibiting abusive and deceptive telemarketing acts or practices. 15 U.S.C. §

6102(a)(1). In response, the FTC adopted the TSR, 16 C.F.R. § 310 et seq.

265.

The TSR prohibits abusive and deceptive acts or practices by sellers

or

telemarketers and, under 16 C.F.R. § 310.3(b), further prohibits persons from

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 49 of 103 PageID #: 49

50

providing substantial assistance or support to any seller or telemarketer when that

person knows or consciously avoids knowing that the seller or telemarketer is

engaged in any act or practice that violates the TSR.

266.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester are “sellers” and/or “telemarketers,” within the meanings of 16 C.F.R. §

310.2(dd) and 16 C.F.R. § 310.2(ff)

267.

Many of Defendants' telephone calls to Indiana residents were

“telemarketing,” within the meaning of 16 C.F.R. § 310.2(gg),

268.

These telephone calls included calls from Transfer Specialists and Sales

Agents.

269.

Defendants' HBA is a good or service.

270.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated the TSR either directly, or Defendants provided substantial

assistance or support to sellers and telemarketers that were violating the TSR in

contravention of 16 C.F.R. § 310.3(b) when Defendants knew or consciously avoided

knowing that the seller or telemarketer is engaged in any act or practice that violates

the TSR.

271.

Defendants' violations of the TSR include:

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 50 of 103 PageID #: 50

51

a. Misrepresented material restrictions, limitations, or conditions to

purchase, receive, or use goods or services, in violation of 16

C.F.R. § 310.3(a)(2)(ii);

b. Misrepresented material aspects of goods or services, in violation

of 16 C.F.R. § 310.3(a)(2)(iii);

c. Misrepresented material aspects of the nature or terms of the

Defendants' refund, cancellation, exchange, or repurchase

policies, in violations of 16 C.F.R. § 310.3(a)(2)(iv);

d. Made false or misleading statements to induce any person to pay

for goods or services, in violation of 16 C.F.R. § 310.3(a)(4);

e. Initiated or caused the initiation of outbound calls to telephone

numbers of Indiana residents where the person has stated to

Defendants that he or she does not wish to receive an outbound

telephone call by Defendants, in violation of 16 C.F.R. §

310.4(b)(1)(iii)(A);

f. Initiated or caused the initiation of outbound calls to telephone

numbers on the National Do Not Call Registry, in violation of 16

C.F.R. § 310.4(b)(1)(iii)(B);

g. Initiated or caused the initiation of outbound telephone calls that

delivered prerecorded messages, in violation of 16 C.F.R. §

310.4(b)(1)(v);

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 51 of 103 PageID #: 51

52

h. Failed to disclose the identity of the seller of the goods or services

truthfully, promptly, and in a clear and conspicuous manner to

the person receiving the call, in violation of 16 C.F.R. §

310.4(d)(1);

i. Failed to disclose the purpose of the call was to sell goods or

services, in violation of 16 C.F.R. § 310.4(d)(2); and/or

j. Failed to disclose the nature of the goods or services, in violation

of 16 C.F.R. § 310.4(d)(3).

272.

Upon information and belief, Defendants made and/or assisted and

facilitated at least one telemarketing call that violated the TSR to the 64,035 unique

phone numbers on the MV Realty Lead List.

273.

Upon information and belief, Defendants made and/or assisted and

facilitated in the making of 29,478 violative telemarketing calls to Indiana residents

through PhoneBurner.

274.

In total, Defendants made and/or assisted and facilitated in the making

of approximately 93,513 violative calls.

275.

Further, these approximately 93,513 calls include approximately 42,479

violative calls to Indiana residents on the National Do Not Call Registry.

276.

It is believed and averred that Defendants made and/or participated in

additional calls that violated the TSR; the numbers, dates, and times of said calls are

known to Defendants, but are not known to Plaintiff at this time.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 52 of 103 PageID #: 52

53

277.

Plaintiff asserts that Defendants may have committed additional

violations of the TSR arising from their participation in these additional calls.

COUNT IV

Violations of the Telephone Solicitation of Consumers Act (“TSCA”)

Ind. Code 24-4.7

(As to all Defendants)

278.

Plaintiff incorporates and realleges each of the preceding paragraphs as

if fully set forth herein.

279.

The Telephone Solicitation of Consumers Act (“TSCA”) prohibits certain

persons and entities from making, causing to make, or assisting and facilitating in

the making of telephone sales calls to Hoosiers on the Indiana Do Not Call List.

280.

Pursuant to Ind. Code § 24-4.7-3-1, the Office of the Attorney General

quarterly publishes a no telephone sales solicitation listing (“the Indiana Do Not Call

List”). Consumers place their telephone numbers on the Indiana Do Not Call List

when they do not want to receive telephone calls soliciting the sale of a consumer

good or service, as defined in Ind. Code § 24-4.7-2-3.

281.

Defendants MV Realty of Indiana, LLC, MV Realty Holdings, LLC, MV

Realty PBC, LLC, MV Brokerage of Indiana, LLC, Zachman, Mitchell, and

Manchester violated the TSCA when Defendants made, caused to be made, or

assisted and facilitated in the making of telephone sales calls to Indiana consumers

on the Indiana Do Not Call List and/or when Defendants made, caused to be made,

or assisted and facilitated in the making of telephone sales calls where the solicitor

did not use business name or the first and last name of the solicitor.

Case 1:23-cv-01578-MPB-MG Document 1 Filed 09/05/23 Page 53 of 103 PageID #: 53

54

282.

The telephone calls described above were telephone sales calls because

they were made to solicit the sale of a consumer good or service or to obtain

information to be used to solicit the sale of a consumer good or service including,

without limitation, the HBA.

283.

By making or causing to be made telephone sales calls to consumers

residing in Indiana, Defendants are “doing business in Indiana,” within the meaning

of Ind. Code § 24-4.7-2-5, regardless of where the telephone calls originated or where

Defendants are located.

284.

By contacting or attempting to contact subscribers in Indiana by

telephone, Defendants are “callers,” within the meaning of Ind. Code § 24-4.7-2-1.7.

By doing business in Indiana, Defendants are “telephone solicitors,” within the

meaning of Ind. Code § 24-4.7-2-10.

285.

By regularly engaging in or soliciting consumer transactions, whether