Recommendations for

Successful Affordable Housing

Program Applications

April 23, 2024

2024 Sponsor Training

Agenda

FEDERAL HOME LOAN BANK OF ATLANTA

2

• AHP General Fund Overview

• Why Apply for AHP General Fund?

• How to Apply

• Application Criteria and Scoring

• The Role of Underwriting

• Compliance and Risk Management

• Online Application

• Helpful Resources

• Questions and Answers

FEDERAL HOME LOAN BANK OF ATLANTA

Disclaimer

3

Federal Home Loan Bank of Atlanta (the Bank) provides training materials to aid

in understanding the requirements of the Affordable Housing Program (AHP).

However, the participants in the AHP remain responsible for reviewing the AHP

regulations, AHP Implementation Plan, AHP agreements and related supporting

documentation (the AHP Requirements), as the same may be updated from time

to time.

In the event there is a discrepancy in the information or conflict between the AHP

Requirements and the training materials, the AHP Requirements shall control and

be applicable to all AHP projects.

It is also the sponsor’s responsibility to ensure that the project information,

including but not limited to the project type, is entered correctly into the

online application system and is consistent with supporting documentation

provided.

AHP General Fund Overview

FEDERAL HOME LOAN BANK OF ATLANTA 4

AHP General Fund Overview

Equity-like Funding for Rental or Ownership Development

• 10 percent of FHLBank Atlanta’s annual net income is committed to affordable

housing and community development

• AHP General Fund is gap funding for the development of affordable owner-

occupied and rental housing for low- to moderate-income households

• AHP General Fund reduces rental project debt service

– Permits a reduction in project rents to enhance affordability

– Makes projects feasible that otherwise may not be feasible

• Projects can be located anywhere in the country, but funds are accessed

exclusively through members of FHLBank Atlanta

• AHP General Fund is a competitive program based on a 100-point scale

FEDERAL HOME LOAN BANK OF ATLANTA 5

New for 2024: Up to $1 Million per Project!

Increase in AHP Subsidy Amount for 2024:

• On April 16, 2024, the Federal Home Loan Bank of Atlanta announced a

record

$55 million in available funds through our 2024 Affordable

Housing Program (AHP) General Fund!

• Applicants may apply for up to $1 million per project maximum direct

subsidy (direct cash payment)

in grant funding to support the acquisition,

construction, or rehabilitation of multifamily and single-family housing

• An increase from $750,000 from last year’s round.

FEDERAL HOME LOAN BANK OF ATLANTA 6

AHP General Fund Overview

What Makes AHP Different from Other Sources of Funds?

• Equity-like funding

• No interest accrues

• No expectation of repayment if project continues to provide the housing as

committed in the application

• Secured with a note and security instrument to ensure compliance

through the affordability period

– 15 years for rental projects

– 5 years for ownership projects that include a transfer of ownership

• Retention (i.e., a mortgage) is not allowed for owner-occupied units that do not include

transfer of ownership (e.g., rehabilitation)

FEDERAL HOME LOAN BANK OF ATLANTA 7

AHP General Fund Overview

• May be used for

– Rental

– Ownership

– New construction

– Rehabilitation

– Supportive housing

– Mixed Use

– Owner-occupied rehabilitation

– Down payment assistance

• May not be used for

– Non-residential costs

– Operating subsidies

– Empowerment activities

– Housing while undergoing medical treatment

– University housing

FEDERAL HOME LOAN BANK OF ATLANTA 8

FEDERAL HOME LOAN BANK OF ATLANTA 9

Examples of FHLBank Atlanta AHP Projects

Toby’s Place for Women and Children

Columbia, SC

Northside Commons

Miami, FL

Ox Fiber Apartments

Frederick, MD

Bickerstaff Crossing

Richmond, VA

AHP General Fund – LIHTC Project Example

Example: 9% LIHTC Deal

Example: 52-unit, Senior Rental Project

Total Sources

AHP

Member First

Mortgage

Other Sources*

Acquisition $180,000

$157,800

$22,200

Construction $5,131,407

$310,200 $180,000

$4,641,207

Soft Costs $706,376 $706,376

Other Costs $1,010,059 $1,010,059

Total Development Budget $7,027,842

$468,000 $180,000

$6,379,842

*Other sources include subordinate and soft debt and equity

Borrowing the Amount

of AHP from the Member

Total Member First

Mortgage

$648,000

AHP $0

Member Loan-to-Value

(LTV)/cost

9.2%

Debt Coverage Ratio 0.56

Using AHP Funds

Total Member First

Mortgage

$180,000

AHP $468,000

Member Loan-to-Value

(LTV)/cost

2.6%

Debt Coverage Ratio 2.14

Making Lending

Possible and

Projects Feasible

FEDERAL HOME LOAN BANK OF ATLANTA 10

AHP General Fund – Non-LIHTC Rental Example

Example: 8-unit, Senior Rental Project, Housing Authority Sponsor

Total Sources

AHP

Member First

Mortgage

Other Sources*

Acquisition $25,000

$25,000

$0

Construction $1,028,578

$83,000 $209,328

$819,250

Soft Costs $52,030

$17,000 $7,950

$44,080

Other Costs $70,000

62,360

$7,640

Total Development Budget $1,175,608

$100,000 $304,638

$870,970

*Other sources include subordinate and soft debt and equity

Borrowing the Amount

of AHP from the Member

Total Member First

Mortgage

$404,638

AHP $0

Member Loan-to-Value

(LTV)/cost

34.4%

Debt Coverage Ratio 1.14

Using AHP Funds

Total Member First

Mortgage

$304,638

AHP $100,000

Member Loan-to-Value

(LTV)/cost

25.9%

Debt Coverage Ratio 1.51

Improves Project

Feasibility

FEDERAL HOME LOAN BANK OF ATLANTA 11

AHP General Fund – Non-LIHTC Rental Example

Example: 8-unit, Homeownership Project, 100% Very Low-Income

Total Sources

AHP

Member First

Mortgage

Other Sources*

Acquisition $50,214

$50,214

$0

Construction $2,131,295

$748,400 $852,568

$530,327

Soft Costs $164,692 $164,692

Other Costs $84,444

$1,600

$82,844

Total Development Budget $2,430,645

$750,000 $902,782

$777,863

*Other sources include subordinate and soft debt and equity

**First Mortgage based on 7.5% interest rate / 30-year amortization

First Mortgage without AHP

Purchase Price $303,831

AHP $0

First Mortgage** $206,598

First Mortgage LTV

(mortgage / purchase price)

68%

Monthly Homebuyer P&I

Payment

$1,291

Using AHP Funds

Purchase Price $303,831

AHP $750,000

First Mortgage** $112,848

First Mortgage LTV

(mortgage / purchase price)

37%

Monthly Homebuyer P&I

Payment

$705

Improves

Homebuyer

Affordability

-45%

FEDERAL HOME LOAN BANK OF ATLANTA 12

AHP General Fund Overview

FEDERAL HOME LOAN BANK OF ATLANTA 13

Getting Started

• Sponsors are housing developers, public entities, contractors, community

builders, and other organizations engaged in development and rehabilitation

of affordable rental or owner-occupied housing

– Sponsors drive the application process and submit applications

– Members review and approve applications

• All applications include a member

– Members are the financial institutions that are part of FHLBank Atlanta

– We can assist you in finding a member

– Visit www.fhlbatl.com

for member locator tool

How to Apply

FEDERAL HOME LOAN BANK OF ATLANTA 14

How to Apply

Application is submitted through AHPBuild

®

by the sponsor

• Log in on the home page of the FHLBank Atlanta website

Sponsor submits application to member for review and approval

• Supporting documents are uploaded through AHPBuild

FHLBank Atlanta member approves application

Webinars are offered to review the actual application content

• One-on-one assistance is also available

FEDERAL HOME LOAN BANK OF ATLANTA 15

How to Apply

FEDERAL HOME LOAN BANK OF ATLANTA 16

General Fund Application and Underwriting Schedule

Initial Monitoring Review (IMR)

Time Limits

FEDERAL HOME LOAN BANK OF ATLANTA

17

Project Timeline

Development

Period

Retention Period

App.

39 mos.

Ownership: 5 Years

Rental: 15 years

Conditions of Funding

Funding Deadline 24

months

December 2026

(except ownership taking down

AHP funds at HB closing)

Report Complete

Project Completion Deadline

39 months

March 2028

Progress Reports

Award Date

December 2024

Long-term Monitoring for Rental Non-LIHTC Projects

Application Criteria Threshold

18

Permanent Sources and Uses Statement

FEDERAL HOME LOAN BANK OF ATLANTA

6

1

2

3

4

5

Site Control

Sponsor Qualifications

Project Specific Thresholds

20 Percent of Funding Committed by an Unrelated Third Party

Application Certification

Application Scoring Criteria

19

FEDERAL HOME LOAN BANK OF ATLANTA

Application Criteria Scoring

FEDERAL HOME LOAN BANK OF ATLANTA

District Priorities Points Type

Member Financial Participation 10 Variable

Project Readiness 5 Variable

Health Care Empowerment 5 Fixed

AHP Subsidy per Unit 7 Variable

Enhanced Broadband Access 4 Variable

Heirs’ Property Resolution 5 Fixed

In-District Application 5 Fixed

Difficult Development Area 5 Fixed

Other Categories

Donated or Conveyed Government-owned or Other Property 5 Variable

Nonprofit or Government Sponsor 5 Variable

Targeting to Lower-Income Households 20 Variable

Underserved Communities and Populations 9 Variable

Creating Economic Opportunity 7 Variable

Community Stability, Including Affordable Housing Preservation 8 Fixed

Total 100

20

Scoring - Member Financial Participation (MFP)

21FEDERAL HOME LOAN BANK OF ATLANTA

Member Financial Participation

• Five points – credit/equity must come from member submitting application

• Minimum five (5) percent of total development costs

• Permanent or construction financing

• Letter of credit

• Debt or equity

• Must demonstrate the member's direct participation in the project

• Must be closed prior to project completion

• Cash collateralized bridge loans are not eligible for points

• Commitments should include:

– Intent to extend credit and/or equity

– Amount and type of funding

– Borrower meets the funder’s credit criteria

– Project has been underwritten and conditionally eligible to receive funder’s credit and/or equity

– Funder’s signature, expiration date, and borrower’s acceptance

Available Points

--------------------------

5 Points / Variable

MFP Collaboration – (MDI, CDFI, LIDCU)

Member Financial Participation (continued)

• 5 points for funding collaboration between a Minority

Depository Institution (MDI), Community Development

Financial Institution (CDFI), or Low-income Designated

Credit Union (LIDCU) and a non-MDI, CDFI or LIDCU

Thresholds

:

– Must encourage collaborations between banks and MDIs,

CDFIs, and/or LIDCUs

– Must be members of FHLB Atlanta as of the application

deadline

– Must be designated as a MDI, CDFI, or LIDCU as of the

application deadline

– Must provide the funding to the project

– Must be unaffiliated and not be in control of, controlled by, or

in common control with the collaborating member

22FEDERAL HOME LOAN BANK OF ATLANTA

Available Points

--------------------------

5 Points / Variable

MFP Collaboration – (MDI, CDFI, LIDCU)

Member Financial Participation (continued)

• Collaborating options include:

23FEDERAL HOME LOAN BANK OF ATLANTA

Non-MDI, CDFI,

or LIDCU

MDI, CDFI, or

LIDCU

Applying Member

Collaborating Funder

MDI, CDFI, or

LIDCU

Non-MDI, CDFI,

or LIDCU

Applying Member

Collaborating Funder

OR

Scoring – Project Readiness

Rental

• Non-LIHTC: 100 percent of non-AHP permanent sources committed

• 9 percent LIHTC: tax credits awarded by state allocating agency

• 4 percent LIHTC: 100 percent of non-AHP permanent sources committed (must have bond

inducement resolution or equivalent)

24FEDERAL HOME LOAN BANK OF ATLANTA

Ownership

New Construction/Rehabilitation

• 75 percent of the units presold to qualifying households

Owner-Occupied Rehabilitation

• 75 percent of the units have been identified, rehab specifications and cost breakdown have been

determined for identified units, and homeowners are income eligible for AHP

Down-payment Assistance

• 100 percent of the homebuyers identified and qualified

Project Readiness – Funding Commitments

• Two (2) points

Available Points

--------------------------

5 Points total / Variable

Project Readiness

25FEDERAL HOME LOAN BANK OF ATLANTA

Project Readiness - Construction Readiness

• Additional three (3) points awarded for construction readiness,

bringing the total Readiness points to five (5)

• Points will be awarded for financing readiness criteria by project

type in combination with

one of the following construction

readiness criteria:

– Construction or rehabilitation-related permit(s) has been issued

– Construction or rehabilitation financing has closed

– Rehabilitation work is in progress

Available Points

--------------------------

5 Points total / Variable

Application Criteria Scoring – Health Care Empowerment

26FEDERAL HOME LOAN BANK OF ATLANTA

Health Care Empowerment

• Health care delivery, referrals, or services

throughout the entire AHP retention period

• On-site, mobile services, and/or accessible off-site

• Offered to all residents

• Structured agreement required

• Examples:

– Primary medical care including vaccinations and

screening programs

– Mental health counseling; and/or

– Alcohol or substance abuse counseling

– Nutritional counseling

• Update for 2024: Health Care Empowerment

services no longer must be new service offerings.

– Sponsor can replicate a service offered at its other

properties

Available Points

--------------------------

5 Points / Fixed

Application Criteria Scoring – AHP Subsidy per Unit

27FEDERAL HOME LOAN BANK OF ATLANTA

AHP Subsidy per Unit

• For this category, projects using fewer AHP subsidy

dollars per AHP-assisted unit will receive more

points than projects using more AHP subsidy

dollars

• Variable score of up 7 points

• Cannot be self-scored

• Based on the weighted average formula, projects

with subsidy per unit of $50,000 or more will not

receive any points in this category

Available Points

--------------------------

7 Points / Variable

Application Criteria Scoring – Enhanced Broadband Access

28

• One (1) point will be awarded to projects in which 100

percent of the units have access to four times the

minimum broadband download speed. This

minimum

threshold requirement

must be met to receive points in

this category

• One additional

point for each of the following, for up to a

maximum of 4 points

– Computers in a quantity equal to the number of

units in the project times 10 percent (1 point)

– Free or reduced cost broadband access devices,

such as computer equipment, tablets, or hotspot

devices (1 point)

– Free Wi-Fi access available within all units (1 point)

FEDERAL HOME LOAN BANK OF ATLANTA

Enhanced Broadband Access

Available Points

--------------------------

4 Points / Variable

Application Criteria Scoring – Heirs’ Property Resolution

29

• Heirs’ property is property without clear title

• To receive the five (5) points in this category, members must submit

documentation evidencing at least one (1)

of the three (3) Heirs’

Property Resolution Categories:

1. Pro bono legal services

2. Local government innovation

3. Developer/contractor driven affordable housing initiatives

Thresholds

• Submit documentation that project includes a solution to an heirs’

property issue. Provide documentation of a resolution plan that

addresses the heirs’ property issue as part of the AHP project.

Heirs’ property resolution plan must

:

– Have committed resources

– Be contemporaneous with the project

– Achieve the intended objectives without negative impact to the

existing owner or the community

– Address heirs’ property in one or more of the three (3) categories

noted above

• Sponsor must offer an ongoing education and/or awareness program

addressing heirs’ property prevention and resolution

FEDERAL HOME LOAN BANK OF ATLANTA

Heirs’ Property Resolution

Available Points

--------------------------

5 Points / Fixed

Application Criteria Scoring: In-district Application

30FEDERAL HOME LOAN BANK OF ATLANTA

In-district Application

• 100 percent of the units in the project are located in

the FHLBank Atlanta district

Available Points

--------------------------

5 Points / Fixed

– Alabama

– District of Columbia

– Florida

– Georgia

– Maryland

– North Carolina

– South Carolina

– Virginia

Application Criteria Scoring – Difficult Development Area

31FEDERAL HOME LOAN BANK OF ATLANTA

Difficult Development Areas

• Five (5) points for projects in which 100 percent

of the units are located in a Difficult Development

Area (DDA)

• Based on the latest documentation available from

the U.S. Department of Housing and Urban

Development (HUD)

• DDAs are designated based on high development

costs relative to income

• https://www.huduser.gov/portal/datasets/qct.html

Available Points

--------------------------

5 Points / Fixed

Application Criteria Scoring – Donated/Conveyed Govt. Owned

Donated or Conveyed Government-Owned or Other

Property

• Federal government property sold for a project

• Property donated by any other party at a small, negligible

amount, most often $10 or less.

• At least 25 percent of the units, land, or land lots

• Score: percentage of units, land or land lots donated to the

project times five points

• Donation must be contemporaneous with the AHP project

• Must be donated by a party not related to the sponsor, project

owner, or member, prior to the disbursement of AHP funds

• A donation from government or quasi-government sellers or

lessors to a related party is allowed

32FEDERAL HOME LOAN BANK OF ATLANTA

Available Points

--------------------------

5 Points / Variable

Application Criteria Scoring – Nonprofit/Government Sponsor

Nonprofit or Government Sponsor

33FEDERAL HOME LOAN BANK OF ATLANTA

Available Points

--------------------------

5 Points / Variable

Rental Projects

1 point: Nonprofit sponsor has or will

have an ownership interest

4 additional points: Nonprofit sponsor

has a controlling interest

• Greater than 50% ownership if non-

LIHTC

• Greater than 50% ownership in GP if

LIHTC, or 50% with “control”

Owner- occupied Projects

1 point each (maximum 5 points):

• Marketing and outreach

• Property acquisition

• Pre-development

• Construction rehabilitation

• Qualifying borrowers for home mortgages,

including AHP

• Providing or arranging permanent mortgage

financing

Application Criteria Scoring – Targeting

Household Income Targeting

• Rental compared to rental. Ownership compared to

ownership

– Income categories:

• Moderate: >65-80 percent of AMI

• Low: >50-65 percent of AMI

• Very low: 50 percent or less of AMI

• Maximum score of 20 points will automatically be

awarded to rental projects that reserve at least

60% of units for very low-income households (50

percent of AMI or less)

34

Income

Targeting

Points

FEDERAL HOME LOAN BANK OF ATLANTA

Available Points

--------------------------

20 Points / Variable

– At least 20 percent of the units in a rental project must be reserved for very low-

income residents

Income Calculator

Expanding Your Eligible Customer Base

• AHP income limit methodology and calculator

• Selects the greatest of four calculation

methodologies

• Point-and-click calculator automatically provides

the highest income limit

• AMIs >80% excluded from AHP funds

• FHLBank Atlanta Income Calculator Tool

https://cis.fhlbatl.com/regsponsor/incomecalculation

FEDERAL HOME LOAN BANK OF ATLANTA 35

Application Criteria Scoring- Underserved Comm. & Population

FEDERAL HOME LOAN BANK OF ATLANTA 36

Underserved Communities and Populations

• Housing for Homeless Households (3 points)

• Native American Tribal areas (3 points)

• Senior Housing (3 points)

Housing for Homeless Households

: At least 20 percent of units must be reserved for

homeless households, or the creation of transitional housing for homeless households

permitting a minimum of six months occupancy

Native American Tribal areas

: Some or all the project must be located in an area

owned or otherwise controlled by a Native American Tribe. Must be federally or state

recognized and located in the Bank’s district.

Sponsor must provide documentation demonstrating that the project is located in

an eligible area.

Senior Housing

: At least 20 percent of units must be reserved for senior households

(62 years and older)

Available Points

--------------------------

9 Points / Variable

Application Criteria Scoring – Creating Economic Opportunity

37

Creating Economic Opportunity – Promotion

of Empowerment

• Up to five (5) points for promotion of empowerment

• Residential Economic Diversity - Two (2) points for projects where one or

more of the project’s affordable housing units is located in a high-income area

https://geomap.ffiec.gov/FFIECGeocMap/GeocodeMap1.aspx

Empowerment Activities Owner (non-OOR)

Owner Occupied

Rehab (OOR)

Rental

Pre-closing Counseling via the Bank-

prescribed counseling

2.5 Points

N/A

N/A

Employment Readiness Program

2.5 Points 2.5 Points

2.5 Points

Onsite Daycare (Child or Adult)

2.5 Points

N/A 2.5 Points

Training and Education Program

2.5 Points

2.5 Points

2.5 Points

Owner/Resident Involvement Program

2.5 Points

2.5 Points

2.5 Points

Counseling Program

(Homeowners and Tenants)

N/A

2.5 Points

2.5 Points

FEDERAL HOME LOAN BANK OF ATLANTA

Available Points

--------------------------

7 Points / Variable

Application Criteria Scoring - Community Stability, including

Affordable Housing Preservation

38

Vacant or Abandoned

1. The redevelopment of vacant

residential where at least 60

percent of the units are vacant at

the time of acquisition by the

property owner, and all vacant or

abandoned units are being

rehabilitated;

2. In the case of existing non-

residential properties, 100

percent of the building is vacant

or abandoned

FEDERAL HOME LOAN BANK OF ATLANTA

Community Stability, Including Affordable Housing Preservation

Neighborhood Stabilization

3. A project that is an integral part

of the community revitalization

or economic development

strategy approved by a unit of

state or local government or

instrumentality thereof

Some or all of the project

must be within the

designated area

Available Points

--------------------------

8 Points / Fixed

The Role of Underwriting

FEDERAL HOME LOAN BANK OF ATLANTA 39

The Role of Underwriting

40

Project Communications

• We only discuss projects with the primary project sponsor and/or

member and will not discuss projects with consultant without member

and/or project sponsor present

Development Budget Guideline Examples

• Sponsor’s acquisition cost or donated value

– Acquisition cost must be supported by the sponsor’s written description with

backup documentation of how the budgeted acquisition cost in the budget

was determined

• Reasonable hard cost based on industry construction cost data

FEDERAL HOME LOAN BANK OF ATLANTA

41

Budget Guideline Examples

• Capitalized reserves:

‒ Maximum nine (9) months operating expenses plus nine months of hard

debt service

‒ Maximum 12 months operating expenses (net of all reserves included in

operating expense) plus twelve (12) months of hard debt service for

projects with 100 percent of units reserved for supportive housing

households

‒ For projects using state-administered funding or rental assistance from a

federal government agency (e.g., HUD or USDA), the Bank may defer to

the requirement published by the state HFA or its equivalent or the federal

government agency

• Items in the development budget typically paid as operating expenses

are included in the reserves calculation

FEDERAL HOME LOAN BANK OF ATLANTA

Budget Guidelines – Capitalized Reserves

42

Budget Guideline Examples

• 100 percent of net proceeds to the seller from the purchase of a

property from a related party seller must become a source of funds for

the subject project

‒ Not applicable for

‒ Governmental or quasi-governmental seller, or when AHP funds are used to

replace short-term debt or equity from the sponsor

‒ A related party’s debt or equity extended for the contemporaneous acquisition of

property

• Total soft cost maximum percentage

FEDERAL HOME LOAN BANK OF ATLANTA

Budget Guidelines

– Soft Cost Contingency & Related Party Property Sales

Project Type Maximum Soft Costs

4% LIHTC with bonds 35 percent

9% LIHTC projects 28 percent

Non-LIHTC 22 percent

Ownership development 25 percent

Owner-occupied rehabilitation 20 percent

43

Developer Fee Guidelines

FEDERAL HOME LOAN BANK OF ATLANTA

Budget Guidelines – Developer Fees

Type Fee

All projects except as listed below 15%

Consultant fee if no change of ownership and 100% owned by nonprofit 5%

Other projects with no change/transfer of ownership 0%

• Calculated as percentage of total development costs net of

– Acquisition

– Reserves

– Developer fee

• Developer fee includes fees paid to consultants for services normally provided by a

developer

• FHLBank Atlanta may defer to state HFA guidelines if using state-administered funding

• Developer fee cannot increase if construction financing has closed and there is not a

proportional increase in hard cost

44

Deferred Developer Fee Guidelines

• If financing has closed on/or before application with deferred developer

fee or other subordinate funding from a related party (e.g., “bridge” funds,

owner equity) as a source of funding:

– Then up to 50 percent of the AHP award can be used to reduce

deferred developer fee or other subordinate funding from a related

party; and

– At least 25 percent of the total developer fee remains deferred

• Must continue to meet Deferred Developer Fee guidelines throughout the

project life cycle

• Not applicable if AHP funds are used to replace short-term debt or equity

from the sponsor or a related party for property acquisition, construction,

or rehabilitation prior to the AHP funding

FEDERAL HOME LOAN BANK OF ATLANTA

Budget Guidelines – Developer Fees (continued)

Proforma Guideline Examples

• Debt coverage ratio: 1.00 minimum, 1.50 maximum at application though

board approval

• 1.75 maximum, after award, if new/additional sources of equity or soft debt

are secured that results in a reduction in hard debt service

• Net cash flow: Maximum 15 percent of effective gross income

– Alternate need for subsidy test may be used for projects with no hard debt, DCR, or net

cash flow outside of stated guidelines

• Management fees: Maximum nine (9) percent of gross rent

• Replacement reserves: Up to $450 per unit per year

• Annual operating expense: Maximum 80 percent of effective gross income (EGI)

in year one (90 percent of EGI in year one for projects receiving maximum

targeting points)

Market Feasibility Guideline Example

• Defer to State approved market feasibility if using state-administered funding

FEDERAL HOME LOAN BANK OF ATLANTA

Application Criteria Underwriting – Debt Service Coverage Ratio

Project Completion

46

Requirements to Report Complete

• Draw down all AHP General Fund subsidies

• Construction must be 100 percent complete

• All requested documents must be received and approved by the Bank

• Project-specific requirements:

– Ownership: all owner-occupied units must be sold and occupied by eligible households

– Rental: projects must have a certificate of occupancy and be at least 75 percent

occupied

FEDERAL HOME LOAN BANK OF ATLANTA

Compliance and Risk Management

FEDERAL HOME LOAN BANK OF ATLANTA 47

Compliance and Risk Management

48

Scoring Commitments

• Owner and Sponsor shall, from project completion through the end of the

AHP retention period, continue to meet scoring and underwriting

commitments in the application, subject to modification as may be approved

by the Bank

Conflicts Between AHP and Other Funders

• It is the project sponsor's responsibility to ensure compliance with all AHP

requirements can be met and are not in conflict with other financing and/or

service providers’ requirements

FEDERAL HOME LOAN BANK OF ATLANTA

Compliance and Risk Management

49

Modifications (Per AHP regulation §1291.29)

• (a) Modification procedure. If, prior to or after final disbursement of funds to a project from all

funding sources, in order to remedy noncompliance or receive additional subsidy, there is or will

be a change in the project that would change the score that the project application received in the

AHP funding round in which it was originally scored and approved, had the changed facts been

operative at that time, a Bank shall approve in writing a request for a modification to the terms of

the approved application, provided that:

– (1) The Bank first requests that the project sponsor or owner make a reasonable effort to cure any

noncompliance within a reasonable period of time, and the noncompliance could not be cured within a

reasonable period of time;

– (2) The project, incorporating any such changes, would meet the eligibility requirements of this part;

– (3) The application, as reflective of such changes, continues to score high enough to have been approved in

the AHP funding round in which the application was originally scored and approved by the Bank, which is as

high as the lowest ranking alternate approved for funding by the Bank if the Bank has a written policy to

approve alternates for funding; and

– (4) There is good cause for the modification, which may not be solely remediation of noncompliance, and the

analysis and justification for the modification, including why a cure of noncompliance was not successful or

attempted, are documented by the Bank in writing.

FEDERAL HOME LOAN BANK OF ATLANTA

FEDERAL HOME LOAN BANK OF ATLANTA

Any person who knowingly makes a false statement or

misrepresentation to the Federal Home Loan Bank is subject to

penalties that may include disqualification of application, sponsor

suspension, fines, imprisonment, or both, under the provision of Title

18, United States Code, Sec. 1014, including, but not limited to:

• Members

− Loan Officers

− Processors (Submitters)

− Underwriters (Approvers/Program Managers)

− Closers

• Closing Agents

• Contractors/Inspectors

• Real Estate Agents

50

Compliance and Risk Management

Compliance and Risk Management

Types of false statements include but are not limited to:

• Omitting or not fully disclosing information on the application certification

– Certification must remain true throughout entire underwriting period

• Not having completed work that was represented to the Bank as complete

• Not disclosing if under investigation by a law enforcement agency or

applicable regulator

• Sources and uses submitted are not consistent throughout funders

You have the duty to disclose any material changes to the project to the

Bank in a timely manner

FEDERAL HOME LOAN BANK OF ATLANTA 51

Online Application

FEDERAL HOME LOAN BANK OF ATLANTA 52

Online Application Registration Process

New Project Sponsors

• Registered sponsors do not need to register again

• Visit FHLBank Atlanta website to start a new, one-time registration

– https://cis.fhlbatl.com/regsponsor/

• Previously registered sponsors must review their organization profile to

ensure it is complete and accurate

FEDERAL HOME LOAN BANK OF ATLANTA 53

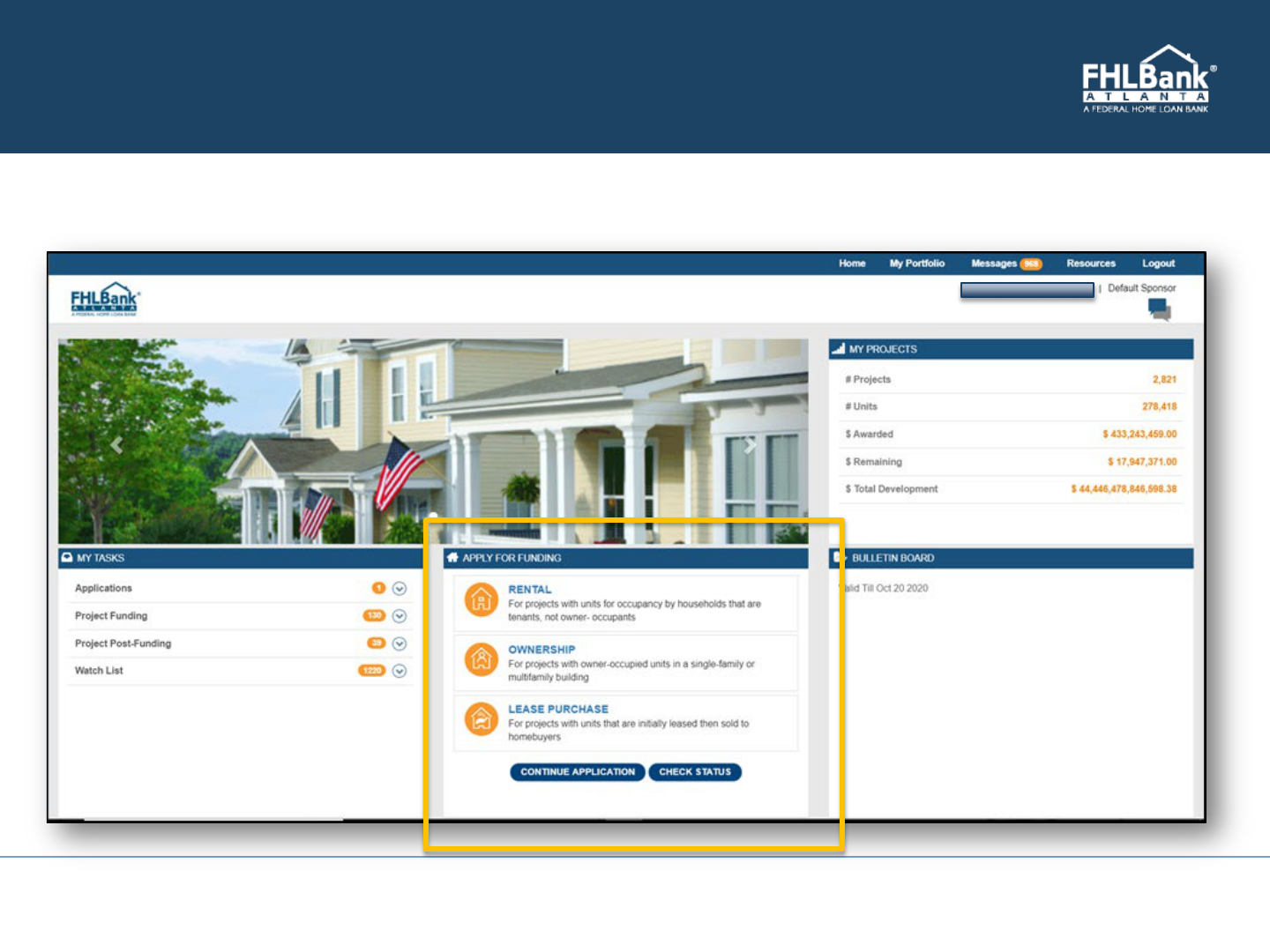

Online Application Components – AHPBuild Portal

Application Home

FEDERAL HOME LOAN BANK OF ATLANTA 55

Online Application Components

FEDERAL HOME LOAN BANK OF ATLANTA 56

Apply for Funding Description

RENTAL Allows you to initiate AHP subsidy application for

projects with units for households that are for

tenant’s occupancy

No owner-occupants

OWNERSHIP Allows you to initiate AHP subsidy application for

projects with owner-occupied units in a single or

multifamily building

LEASE-

PURCHASE

Allows you to initiate AHP subsidy application for

projects with units initially leased and subsequently

sold to the homeowners

Call the Bank for further information if you are

submitting a lease-purchase application

CONTINUE

APPLICATION

Allows you to access incomplete/partially saved

applications

CHECK STATUS Allows you to check the status of your applications

submitted in the current round

Online Application Components

General Information

FEDERAL HOME LOAN BANK OF ATLANTA 57

Online Application Components

General Information

FEDERAL HOME LOAN BANK OF ATLANTA 58

Online Application Components

General Information

FEDERAL HOME LOAN BANK OF ATLANTA 59

Development Team

FEDERAL HOME LOAN BANK OF ATLANTA 60

Online Application Components

Details

Owner of Record

Member

FEDERAL HOME LOAN BANK OF ATLANTA 61

Online Application Components

Details

Online Application Components

Project Targeting

FEDERAL HOME LOAN BANK OF ATLANTA 62

Online Application Components

Building Information

FEDERAL HOME LOAN BANK OF ATLANTA 63

Online Application Components

Financial Feasibility

FEDERAL HOME LOAN BANK OF ATLANTA 64

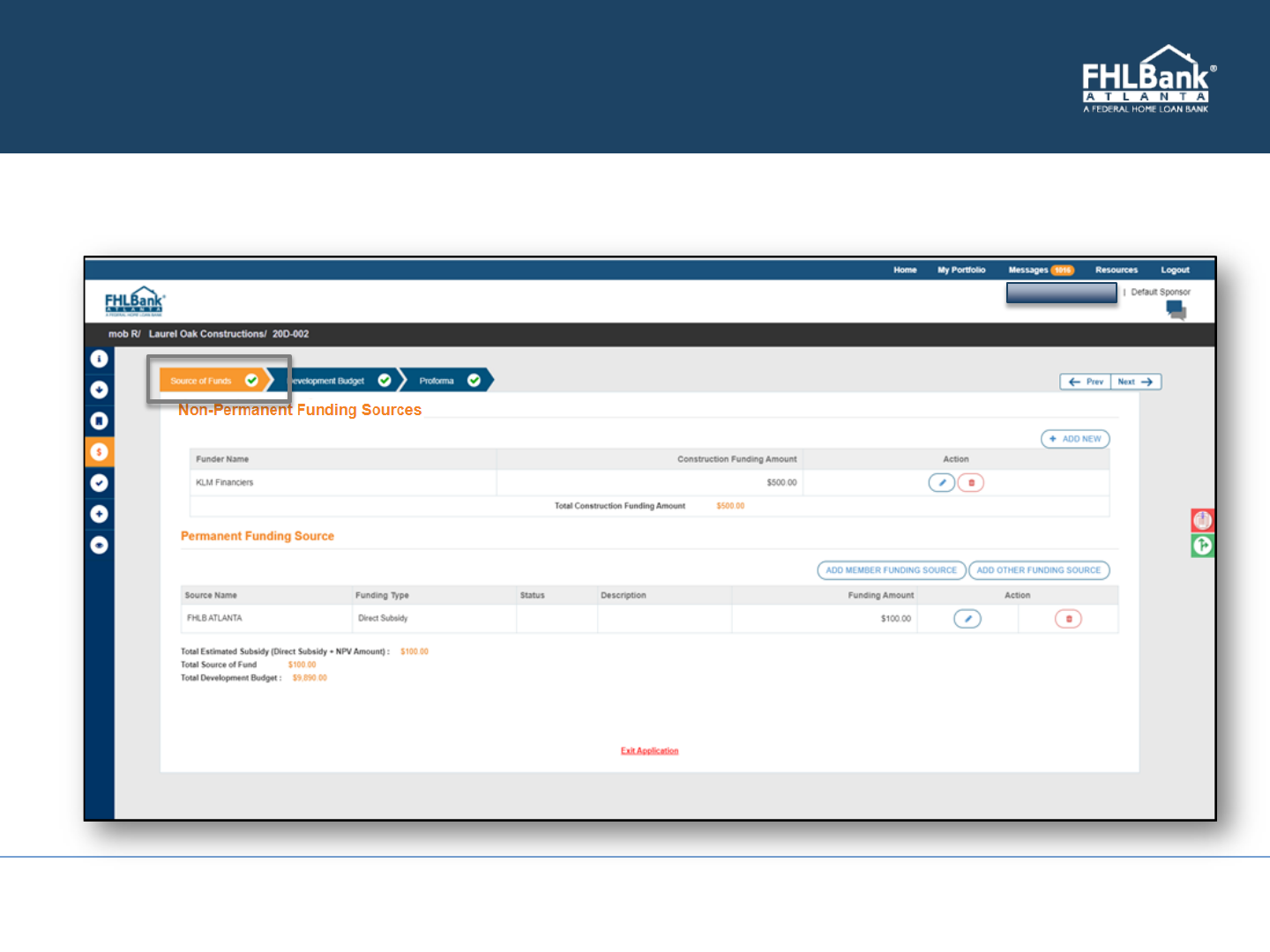

Online Application Components

Sources of Funding – Rental Projects

• Non-permanent funding sources

– Include only short-term sources that will not last past project completion

• Bridge loans

• Construction loans

• Permanent funding sources

– Include only long-term sources that will remain in place past project completion

– Show status of approved only if you have documented firm commitment

– Include the market value of in-kind donations and voluntary professional

labor or services

– Include the value of donated land as a source (land equity)

– Documentation must show the amount of credit or equity to be extended

– Do not include non-contemporaneous debt

FEDERAL HOME LOAN BANK OF ATLANTA 65

Online Application Components

Sources of Funding – Ownership Development Projects

• Non-permanent funding sources

– Include short-term sources that will not last past project completion

• Bridge Loans

• Construction Loans

• Permanent funding sources

– Include sources that will be identified on the closing disclosure (CD)

– Include non-permanent sources that will be the funding that will allow the

sponsor to extend sponsor-provided first mortgages

• Fundraising

• Grants to the sponsor

– Show status of approved only if you have documented firm commitment

– Include the market value of in-kind donations and voluntary professional

labor or services

– Include the value of donated land as a source (land equity)

– Documentation must show the amount of credit or equity to be extended

FEDERAL HOME LOAN BANK OF ATLANTA 66

Online Application Components

AHP Subsidy Information

FEDERAL HOME LOAN BANK OF ATLANTA 67

Online Application Components

Uses of AHP Funds

• Use of AHP funds here will determine allocation in the development

budget (maximum of three)

– Acquisition

– Hard (construction) cost

– Soft cost

– Other cost

FEDERAL HOME LOAN BANK OF ATLANTA 68

Online Application Components

Development Budget

FEDERAL HOME LOAN BANK OF ATLANTA 69

Online Application Components

Pro Forma (Rental Projects)

FEDERAL HOME LOAN BANK OF ATLANTA 70

Online Application Components

Scoring Criteria

FEDERAL HOME LOAN BANK OF ATLANTA 71

Guidelines

Online Application Components

Additional Information

FEDERAL HOME LOAN BANK OF ATLANTA 72

Online Application Components

Supporting Documentation

FEDERAL HOME LOAN BANK OF ATLANTA 73

Click to upload

supporting documents

Online Application Components

Supporting Documentation

FEDERAL HOME LOAN BANK OF ATLANTA 74

Click to download

templates

Click to browse and

upload documents

Drag and drop

in the box

or

Online Application Components

Variance Questions:

FEDERAL HOME LOAN BANK OF ATLANTA 75

Click to respond to

variance questions

Online Application Components

• Review and Finalize – application deadline 7/29/24, 11:50pm ET

• Please note – technical assistance will not be available after 5pm EST on

7/29/24

FEDERAL HOME LOAN BANK OF ATLANTA 76

Helpful Resources – Connecting with Potential Customers

Lenders Participating in AHP Homeownership Set-aside Program and

Multifamily Housing

• “Find a Member” feature the Bank’s website now includes member

business contacts for multifamily in addition to existing homeownership

contacts

77

Search Options

FEDERAL HOME LOAN BANK OF ATLANTA

• Contact the Bank if you need assistance connecting with a member in your area

Helpful Resources

FEDERAL HOME LOAN BANK OF ATLANTA

Application Resources

Sponsor Registration Instructions

http://corp.fhlbatl.com/files/documents/ahp-sponsor-registration.pdf

Targeted Community Lending Plan https://corp.fhlbatl.com/files/documents/targeted-community-lending-

plan.pdf

AHP Implementation Plan http://corp.fhlbatl.com/files/documents/ahp-implementation-plan.pdf

Income Documentation Requirements

http://corp.fhlbatl.com/files/documents/ahp-income-documentation-

requirement.pdf

Retention Agreement Rider and Instructions Rental: http://corp.fhlbatl.com/files/documents/ahp-retention-

agreement-rider-and-instructions-general-fund-rental-project.pdf

Ownership:

http://corp.fhlbatl.com/files/documents/ahp-retention-agreement-

rider-general-fund-owner-occupied.pdf

MDI, CDFI, and LIDCU Member List 2024 mdi lidcu cdfi list state order.pdf (fhlbatl.com)

FHLBank Atlanta’s AHP Income Limits Calculator https://cis.fhlbatl.com/regsponsor/incomecalculation

Member Locator Registration Form

http://corp.fhlbatl.com/files/documents/ahp-competitive-zip-code-

locator..xlsx

Program Guidelines Links

FHLBank Atlanta Website http://corp.fhlbatl.com/

78

Protocol for Contacting FHLBank Atlanta – Inquiries

• Primary project sponsor and/or member may contact FHLBank Atlanta’s

project analyst and/or Community Investment Services management

regarding project related inquires

• Primary project sponsor and/or member may not contact FHLBank Atlanta’s

board members or any member of the Advisory Council regarding project

related inquires

FEDERAL HOME LOAN BANK OF ATLANTA 79

Diversity, Equity, and Inclusion

FEDERAL HOME LOAN BANK OF ATLANTA 80

Diversity, equity, and inclusion (DEI) is integral to the success of FHLBank

Atlanta. We are committed to embedding DEI principles across all levels

of our organization and into all elements of our internal and external

operations, strategic planning, and decision making.

We know that progress cannot be achieved through symbolic gestures or

complacency; therefore, we challenge ourselves to be self-reflective, hold

each other accountable, and continuously evaluate our practices to

ensure the full integration of DEI into our culture.

We are collectively stronger through an inclusive culture.

TOGETHER WE ACHIEVE

Contact Information

81

Julia L. Brown

Vice President

Multifamily Portfolio Manager

404.888.8093

Technical Assistance:

800.536.9650, Option 3

81FEDERAL HOME LOAN BANK OF ATLANTA

Emmanuel Ankrah

Banking Officer

Multifamily Portfolio Analyst II

404.888.8098

eankrah@fhlbatl.com

Joel Brockmann

Assistant Vice President

Senior Multifamily Portfolio Analyst

404.888.8156

jbrockmann@fhlbatl.com

ShaDonte Butler

Vice President

Relationship Manager

404.888.8416

sbutler@fhlbatl.com

Thank You!