1

POSB (CBS) Manual

Note:- These rules apply to the Post Office Savings Accounts and, also mutatis, to

(1) Post Office Savings Account

(2) National Savings Recurring Deposit Account

(3) National Savings Time Deposit Account

(4) Public Provident Fund Account

(5) National Savings Monthly Income Account

(6) Senior Citizens Savings Scheme Account

(7) Sukanya Samriddhi Account

(8) Kisan Vikas Patra Account

(9) National Savings Certificates (VIII Issue) Account

Except where separate rules are made with regard to the particular type of accounts, in which

case, such rules relating to the particular type of accounts will apply.

2

Contents

Chapter 1:- POST OFFICE SAVINGS ACCOUNT ................................................................. 9

1. Saving Bank Offices ................................................................................................ 9

2. Duties and Responsibilities of the Supervisor and Tenure ...................................... 9

3. Distribution of Work ............................................................................................. 10

4. CBS Pass Book ...................................................................................................... 10

5. Stock Register For CBS Pass Books In Head Post Offices ................................... 11

6. Stock Register of CBS Pass Books in Sub Offices ............................................... 12

7. Transmission of CBS Pass Books ......................................................................... 12

8. Register Of Undeliverable CBS Pass Books In Deposit In The HOs And SOs .... 13

9. Pay-In-Slip (SB-103) ............................................................................................. 15

10. Preliminary Receipt (SB-26) ................................................................................. 15

11. Receipt for depositor‟s CBS Pass Book (SB-28) .................................................. 16

12. Supply of Savings Bank Account Statement ......................................................... 18

13. Types of Savings Accounts ................................................................................... 18

14. Specimen Signatures and Photograph ................................................................... 21

15. Nomination ............................................................................................................ 22

16. Opening of Savings Account ................................................................................. 23

17. Opening of Account............................................................................................... 29

18. Acceptance of deposit/Funding in Savings, SSA and PPF account. ..................... 30

19. Printing of Passbook .............................................................................................. 30

20. Process in CPC ...................................................................................................... 31

21. Procedure for acceptance of deposit/funding of account when initial deposit is

made by cheque................................................................................................................ 31

22. Procedure for acceptance of deposit/funding of account when initial deposit is

made by transfer of funds ................................................................................................ 31

23. Opening of Account-Procedure in Extra Departmental Branch Post Offices (Non

RICT) ............................................................................................................................... 32

24. Procedure in the Account Office for accounts opened at their Branch Post Offices

(Non RICT) ...................................................................................................................... 33

25. Accounts Opened In Contravention Of Rules ....................................................... 33

26. Subsequent Deposits/Credits-Mode of Deposits/Credits ...................................... 34

27. In case Account Stands at Extra Departmental Branch Post Office ...................... 36

28. Withdrawals/Debits from Savings Account .......................................................... 37

3

29. Presentation and writing up of CBS Pass Book .................................................... 42

30. Withdrawal on the basis of general power of attorney either at HO or SO ........... 43

31. Withdrawal at Branch Offices (Non RICT) .......................................................... 43

32. Withdrawal from any CBS Post Office including Account Office in respect of

accounts standing at EDBO (Non-RICT) ........................................................................ 44

33. Memo of Admission of Payment ........................................................................... 45

34. Attestation of Signature of The Depositor ............................................................. 46

35. Withdrawals from Minor's Accounts ..................................................................... 46

36. Withdrawals from Lunatic‟s Accounts .................................................................. 47

37. Closure of Savings Account .................................................................................. 47

38. List of Transactions, Consolidation and Voucher Bundle ..................................... 49

39. Disposal of List of Transactions (LOT) And List Of Documents In Head Offices

50

40. Sb Slips (SB-27) .................................................................................................... 51

41. Consolidated Journal of Deposits/Withdrawals .................................................... 51

42. Transfer of Accounts ............................................................................................. 51

43. Procedure for Transfer ........................................................................................... 51

44. Issue of Fresh Pass Book In Lieu Of Used Up One .............................................. 54

45. Issue of Duplicate Pass Book ................................................................................ 55

46. Issue of pass book in lieu of spoiled pass book ..................................................... 57

47. Action to be taken by Inspecting/vising officers ................................................... 57

48. Change of Name of Depositor or Change of Agent of Depositor ......................... 57

49. Calculation and posting of annual s.b. Interest and posting of interest in pass

books in head/sub post offices ......................................................................................... 59

50. Verification of Balances ........................................................................................ 61

51. Disposal of Undelivered Pass Books ..................................................................... 62

52. Return of Pass Books To Depositors By Head/Sub Office ................................... 62

53. Interest Short/Excess Passed ................................................................................. 63

54. Accounts Which Are To Be Treated As Silent ...................................................... 64

55. Revival of Silent Account...................................................................................... 64

56. Transfer of Branch Office From One Account Office To Another Under The

Same Head Office ............................................................................................................ 67

57. Conversion of Branch Office into Sub Office ....................................................... 67

58. Amounts defrauded from S.B. Accounts to Departmental Officials and not

accounted for in the books of the Department. ................................................................ 67

4

59. Verification of withdrawals of Rs. 10,000/- and above in savings accounts at

branch offices ................................................................................................................... 69

60. Payment of The Amount Of Savings Bank Accounts In The Name of Deceased

Depositors ........................................................................................................................ 70

61. Settlement of claim of a depositor becoming insane or otherwise incapable of

managing his own affairs. ................................................................................................ 85

62. Settlement of Claims To Balances In Sb Accounts Standing In The Name

Ofpersons Unheard For More Than Seven Years ............................................................ 85

63. Attachment of Money At The Credit of An Account By Civil or Other Court or

Other Competent Authority ............................................................................................. 85

64. Confiscation of Money By The Reserve Bank Of India or Any Other Competent

Authority .......................................................................................................................... 86

Chapter 2 :- NATIONAL SAVINGS RECURRING DEPOSIT ACCOUNT......................... 87

65. Salient features ...................................................................................................... 87

66. CBS Pass Book ...................................................................................................... 87

67. RD Journal ............................................................................................................. 87

68. Nomination ............................................................................................................ 87

69. Type of Accounts................................................................................................... 87

70. Defaults in Payment Of Monthly Installments ...................................................... 88

71. Payment of Defaulted Installments........................................................................ 88

72. Opening of An Account ......................................................................................... 89

73. Modes of Deposit of Subsequent Installments ...................................................... 89

74. Rebate on Deposits Paid In Advance .................................................................... 92

75. Acceptance of Deposits In Absence of The CBS Pass Book ................................ 93

76. Half Withdrawal (RD Loan) .................................................................................. 93

77. Repayment of Withdrawal (RD Loan) .................................................................. 93

78. Closure of Account on Maturity ............................................................................ 94

79. Continuance of deceased depositor‟s accounts ..................................................... 96

80. Payment of amount in accounts in the name(s) of the deceased depositors .......... 96

81. Premature Closure of Rd Accounts ....................................................................... 97

82. List of Transaction and Cosolidation of Deposits and Withdrawas ...................... 97

83. Transfer of Accounts ............................................................................................. 98

84. Submission of Returns to Control Organisation .................................................... 98

85. Protected Savings Scheme ..................................................................................... 98

86. Sanction of Claim .................................................................................................. 99

87. Procedure in Circle Office for registration and verification of claims under the

Protected Savings Scheme in RD accounts ................................................................... 100

5

Chapter 3:-National Savings Time Deposit Account............................................................. 101

88. Categories of accounts ......................................................................................... 101

89. Forms ................................................................................................................... 101

90. Opening of an account ......................................................................................... 102

91. Repayment of deposits and payment of annual interest ...................................... 102

92. Procedure for payment of annual interest ............................................................ 103

93. Procedure for Closure of TD Account ................................................................. 104

94. Reinvestment of Maturity value of Time Deposit in a new T.D. Account .......... 104

95. Post Maturity Interest (over-due) ........................................................................ 104

96. Premature Closure of Time Deposit Accounts .................................................... 104

97. Transfer of Time Deposit Account as Security ................................................... 105

98. Re-investment of amounts payable to depositors ................................................ 106

99. Credit of maturity value of T.D. Account into PO Savings Account .................. 106

100. Payment of maturity value if becomes Rs.20,000/- or above .......................... 106

101. Payment of claims in Time Deposit Accounts of deceased depositors ........... 106

102. Checking of Time Deposit Accounts at branch offices and single handed

departmental sub post offices ......................................................................................... 106

103. Transfer of TD Account from one Post Office to another ............................... 107

Chapter 4:- NATIONAL SAVINGS SCHEME 1987 & 1992 .............................................. 108

Chapter 5:- PUBLIC PROVIDENT FUND ACCOUNT ...................................................... 110

106. Salient features of the Scheme: The following are the salient features of the scheme

........................................................................................................................................ 110

107. Forms ..................................................................................................................... 111

108. Procedure to Be Followed ...................................................................................... 112

109. Transfer of Accounts.............................................................................................. 115

Chapter-6:- NATIONAL SAVINGS MONTHLY INCOME ACCOUNT ........................... 117

115. Salient Features of the Scheme .............................................................................. 117

116. Forms ..................................................................................................................... 118

117. Types of Accounts ................................................................................................. 119

118. Nomination ............................................................................................................ 119

119. Opening of Account At Head/Sub Offices ............................................................ 119

120. Payment of Monthly Interest ................................................................................. 119

121. Closure of Account ................................................................................................ 121

122. Transfer Of Accounts ............................................................................................. 121

123. General ................................................................................................................... 122

6

124. Post-maturity interest ............................................................................................. 123

Chapter-7:- SENIOR CITIZENS SAVINGS SCHEME ACCOUNT ................................... 124

125. Salient Features Of The Scheme ............................................................................ 124

127. Mode of deposit ..................................................................................................... 132

128. List of Transactions (LOT) .................................................................................... 132

129. Type of Accounts ................................................................................................... 132

130. Nomination ............................................................................................................ 132

131. Opening of account ................................................................................................ 134

132. Payment of quarterly interest ................................................................................. 134

133. Payment on maturity .............................................................................................. 134

134. Premature closure of account ................................................................................. 136

135. Transfer of accounts ............................................................................................... 136

136. General ................................................................................................................... 138

137. Senior Citizens Savings Scheme, 2004 (Deduction of TDS) ................................ 138

Chapter-8 :- PROCEDURE FOR PAYMENT OF COMMISSION TO SAS/MPKBY

AGENTS ................................................................................................................................ 139

138. General ................................................................................................................... 139

139. Deposits through SAS and MPKBY Agents ......................................................... 139

140. Procedure to be followed by the Account Branch ................................................. 142

Chapter 9:- SUKANYA SAMRIDDHI ACCOUNT (SSA) .................................................. 143

141. Salient Features of the Scheme .............................................................................. 143

Chapter 10:- NATIONAL SAVINGS CERTIFICATES ....................................................... 148

142. Defination .............................................................................................................. 148

143. Delegation of Duties .............................................................................................. 148

144. Application for Purchase of Certificates ................................................................ 148

145. Modes of Payment for Purchase of Certificates .................................................... 149

146. Procedure for Issue of A Certificate ...................................................................... 149

147. Sale of Certificate through Authorized Agents ...................................................... 150

148. Maintenance of The Application For Purchase/Account Opening Form (AOF) ... 155

149. Preparation of List of Transactions And Consolidation of Certificate Accounts

Opened ........................................................................................................................... 155

150. Encashment Of Certificate ..................................................................................... 155

151. Closure of Certificate Account on maturity or pre-mature closure ....................... 159

152. Journals of Certificates Discharged ....................................................................... 159

153. Memo of Admission of Payment ........................................................................... 161

7

154. Memo of Admission of Transfer............................................................................ 161

155. Nomination ............................................................................................................ 161

156. Change of Name Of Holder of A Certificate ......................................................... 167

157. Transfer of Certificates from One Post Office to Another .................................... 167

158. Transfer of Certificate from One Holder to Another ............................................. 169

159. Pledging of Certificates as Security ....................................................................... 171

160. Issue of Duplicate Certificate ................................................................................. 175

161. Attachment of a Certificate by a Court of Law...................................................... 189

162. CONFISCATION BY CUSTOMS OR EXCISE AUTHORITIES ....................... 190

163. Payment of Proceeds of Savings Certificates Held By Holder(S) To an Authority

Empowered Under the Law to Demand Such Payment ................................................. 190

164. Encashment of Certificates Held By Army and Air Force Personnel ................... 191

165. Payment of the Value Of Certificate In The Name Of Deceased Holder(S) ......... 191

166. Statistical Register ................................................................................................. 205

167. Certificates Voucher List ....................................................................................... 205

168. KISAN VIKAS PATRA ACCOUNT ............................................................................ 206

169. NATIONAL SAVINGS CERTIFICATES (VIII-ISSUE) ACCOUNT ........................ 208

170. 10 years National Savings Certificates .................................................................. 213

Appendix-I ............................................................................................................................. 215

CBS FINACLE working Environment as related to Cheques clearings ................... 215

Appendix- II ........................................................................................................................... 229

Standard Operating Procedure for RICT CBS -Branch Office Transactions ................ 229

Appendix-III .......................................................................................................................... 235

Cheque System in Post Office Savings Bank ................................................................ 235

Cheque Truncation System (CTS) ..................................................................................... 244

Appendix-IV .......................................................................................................................... 249

Preservation Periods for Sb Records.............................................................................. 249

Appendix-V............................................................................................................................ 251

Register of Verification Memos for Withdrawal of Rs 10,000/- and Above At

EDBOs/Single Handed SOs ........................................................................................... 251

Appendix VI........................................................................................................................... 252

Applicattion For The Purpose of Availing The Facilty of Automatic Transfer From SB

Account to RD Account(S) ............................................................................................ 252

Appendix VII ......................................................................................................................... 253

Application for Issue Of Duplicate Pass Book .............................................................. 253

Appendix-VIII........................................................................................................................ 254

8

Incentives Scheme for Branch Postmasters ................................................................... 254

Appendix-IX .......................................................................................................................... 260

Payment of Pension to Postal & Telecom Pensioners through Post Office Savings Bank

........................................................................................................................................ 260

Appendix-X............................................................................................................................ 271

Disbursment of Pension to Railway Pensioners through Post Offices Procedure to Be

Followed By Post Office ................................................................................................ 271

Appendix-XI .......................................................................................................................... 282

Grant of Pension to Freedom Fighters through Post Office Savings Bank ................... 282

Appendix-XII ......................................................................................................................... 285

Know Your Customer (KYC) / Anti Money Laundering (AML)/ Combating of

Financing of Terrorism (CFT) Norms ........................................................................... 285

Appendix- XIII....................................................................................................................... 300

Jan Suraksha Schemes ................................................................................................... 300

A. PMJJBY :- ........................................................................................................... 302

B. PRADHAN MANTRI SURAKSHA BIMA YOJNA ............................................... 302

C. Atal Pension Yojna.................................................................................................... 304

Appendix-XIV ....................................................................................................................... 309

Pay Roll Savings Scheme .............................................................................................. 309

Appendix-XV ......................................................................................................................... 310

Schedule Of Fees To Be Charged From The Investors/ Holders Of Savings Certificates

Forvarious Services Rendered By The Post Offices ...................................................... 310

Appendix -XVI ...................................................................................................................... 312

(A) Register of duplicate certificate Passbooks issued in lieu of lost, stolen, destroyed,

mutilated or defaced certificates, which were issued after to 01.07.2016. .................... 312

Appendix-XVII ...................................................................................................................... 313

Intimation of the seizure of National Savings certificates issued by the Post Office. ... 313

Appendix-XVIII ..................................................................................................................... 314

Period of Preservation of Savings Certificates Records in Post Offices ....................... 314

Appendix-XIX ....................................................................................................................... 316

(A) Calender of Returns ................................................................................................. 316

9

Chapter 1:- POST OFFICE SAVINGS ACCOUNT

1. Saving Bank Offices

All Head Offices (H.O.), Sub-Offices (S.O.) and Branch offices (B.O.) with the exception of

those which are not vested with Saving Bank powers or from which the Savings Bank powers

have been withdrawn by the Head of Circle are Savings Bank offices. The facilities of

deposits and withdrawals by cheque are available only in Head and Departmental Sub

Offices. All Department Post Offices are called Service Outlets (SOL) in Core Banking

Solution.

2. Duties and Responsibilities of the Supervisor and Tenure

(1) The term Supervisor used in this chapter includes a Sub-Postmaster, a Deputy Postmaster,

an Assistant Postmaster or Assistant Sub Postmaster.

(2) All the duties of the Supervisor in connection with the Savings Bank Department may be

performed as may be assigned in the memo of distribution of work. The following duties shall

be the personal responsibility of the Head Postmaster: -

Sanctioning claims in respect of savings bank accounts of deceased depositors which lie

within his power of sanction and the safe custody of the records relating to such claims.

(3) The Postmaster will however remain personally responsible for the general functioning of

the S.B. Branch.

(4) If the officer to whom the duties of the S.B. branch have been delegated notices any

erasures or alterations in Pay-in-Slip (SB-103) or applications for withdrawal (Form SB-7) or

account closure form (SB-7A) or Account Opening Form (AOF) or Annexure-I or Annexure-

II or any Know Your Customer (KYC) document or any other suspicious circumstances

attending a S.B. transaction, these will be brought to the personal notice of the Head

Postmaster who will report the matter at once by name to the Divisional Head confidentially,

unless he is under the direct control of the Regional/Circle Office, after taking appropriate

action at his level as laid down in the rules. He should preserve all relevant records which

may have a bearing on the case in his personal custody until they are transferred to the

investigating authorities.

(5)Tenure of SB/SC Counter Assistants: - The following tenure has been fixed for SB/SC

Counter Clerks in various offices: -

Note:- Any Official who has been given training of Finacle End User should not be posted at any

branch other that POSB/SC unless there are compelling circumstances. Otherwise staff can be rotated

within the office on POSB/SC related seats.

Sl.No.

Type of Office

Tenure

(a)

Tenure in single-handed and double handed

offices.

4 years

(b)

Overall tenure in „A‟ Class and bigger offices.

4 years.

(c)

Overall tenure in Head Office and bigger sub

offices having full time SB/SC Assistants.

5 years

10

3. Distribution of Work

The work in the SB Branch of a Head Post Office should be distributed in the following

manner:-

1) The common duties of the SB branch as mentioned below should be assigned to one

person who may be given other duties also so as to utilize him fully.

(i) Receipt and distribution of dak.

(ii) Maintenance of statistics and preparation of statements.

(iii) Maintenance of the register of undelivered pass books.

(iv) Maintenance of the files of instructions and circulars.

(v) Settlement of objections.

(vi) Deceased claim cases.

(vii) Correspondence including complaints.

(viii) Maintenance of Register relating to transfer of accounts.

(ix) Issue of ATM debit cards and maintaining related registers

(x) Delivery of Welcome KIT to the depositors

Note: - Postmaster can assign some of these duties to Counter Assistant.

2) Each of the remaining Assistants should be given rest of the Savings Bank work to be

determined on the average number of transactions, such as: -

(i) Maintenance of Savings Bank Accounts.

(ii) Maintenance of Account Opening Forms (AOF) and KYC documents for accounts opened.

(iii) Transfer of accounts and maintenance of registers as well as KYC documents of accounts

transferred.

(iv) Entry of interest in pass books belonging to EDBOs and Pass Book Printing.

(v) Revival of silent accounts and maintenance of register and separate guard file to keep the

KYC documents of customers of such accounts.

(vi) Issue of fresh/duplicate passes books.

(vii) Maintenance of Index to Preliminary receipts (SB-26) issued by the ED Branch Post

Offices.

(viii) Issue of sanction of withdrawals and closure of accounts of /EDBOs.

Note: -The list given above is not exhaustive and covers some of the salient points only.

3) Statistical Registers: All reports and statistical registers shall be maintained by the

FINACLE CBS Software except those which have been specifically mentioned for manual

maintenance.

4. CBS Pass Book

Two uniform common CBS Pass Books (SB-5) and (SB5A) have been introduced. SB5 will

be used of SB/RD/MIS/SCSS/SSA and PPF schemes whereas SB5A will be used for

NSC/KVP and TD Accounts. The entries in the said CBS Pass Books will be made through

Pass Book printer only. The uniform common CBS Pass Books need to be stitched and not

stapled so that it can be Pass Book printer friendly. Information and entries shown in the CBS

Pass Books is for the information of public and there will be no legal liability of the

department with regard to the balance or transactions shown in the CBS Pass Books. Entries

relating to Penalty Fee charged in case of RD and PPF as well as Rebate paid only should be

made manually by hand by the user. Except these entries, no entry should be made by hand in

the passbooks in any departmental post office.

4.1 For the new accounts opened in CBS post offices, this Pass book should be issued. For,

migrated accounts, as and when old passbook is presented at the counter, first page of

passbook shall be re-printed on right hand side of next blank page and further transactions

happened in FINACLE CBS shall be printed from next page. Blank space left if any, on the

page being used currently before migration, should be cancelled by drawing lines in red ink.

On the title page, word “CBS” is to be printed. Title of passbook will not be printed by

FINACLE CBS application and counter assistant has to fill the information by permanent

marker.

11

5. Stock Register For CBS Pass Books In Head Post Offices

(1) The H.Os., will obtain supply of CBS Pass Books by placing an indent in the first week of

January, April, July, October on the Postal Stores Depot. The stock on hand and the indented

quantity together will be equal to the requirement of six months. The indent will be in

manuscript and in the following form: -

(INDENT FOR THE QUARTER ENDING………..20…………)

Number of CBS Pass

Books used during the last

quarter

Stock in hand

Number required

Remarks

1

2

3

4

The indent will be prepared in duplicate; one copy being retained in the Head Post Office.

(2) It will be the duty of the Postmaster to ensure proper maintenance of Passbooks and stock of

Passbooks. Immediately when the supply of new CBS Pass Books is received, the Supervisor

should verify that the number of CBS Pass Books noted in the invoice has actually been

received. He should then make an entry of the receipt in the Stock register maintained

manually. He should enter the invoice number and date of the invoice and the balance in hand

in the stock registers maintained separately for both SB5 and SB5A.

(3) The particulars of CBS Pass Books issued to S.Os should be entered in the registers

maintained separately for SB5 and SB5A. The account numbers of the CBS Pass Books

issued for new accounts and in lieu of used up one and the account numbers of all duplicate

CBS Pass Books issued for lost and spoilt CBS Pass Books will be entered in the relevant

columns of stock register and balance will be struck.

(4) At the close of the day, the Supervisor should check the stock registers and see that the

balance of passbooks in hand is the tallied with stock shown in the register.

(5) Postmaster should check the stock of physical passbooks with reference to the stock register

and see that: -

(a) The entries showing the number of pass books issued for new accounts and serial numbers of

the accounts in question are correct by reference to the new accounts opened on that day..

(b) The entries showing the number of pass books issued in lieu of used up and spoilt pass books

and the serial numbers of the accounts in question are correct by reference to the receipts

taken from the depositors in respect of the accounts standing at the H.O. and the entry in the

S.B. Slip or B.O. Slip in respect of accounts standing at a S.O. or its B.Os or at a B.O. in

direct account with the H.O.

(c) The entries showing the number of duplicate pass books issued and the serial numbers of the

concerned accounts are correct by reference to the relative application containing his orders

for the issue of duplicate pass books; and

(d) The balance of passbooks in hand is the same as shown in the Stock Register.

(e) The stock of CBS Pass Books should remain in the Supervisor‟s custody and be verified by

him daily with the balance shown in the stock register.

12

6. Stock Register of CBS Pass Books in Sub Offices

(1) For each sub post office, the Divisional Head will fix the authorized stock of CBS Pass Books

i.e SB5 and SB5A which should be the average requirement of two months.

(2)(a) The S.O. will place an indent on the Head Post Office at the beginning of every month for

replenishment of stock of CBS Pass Books upto the authorized limit fixed. The indent will be

prepared in duplicate in the following form, copy being retained in the SOs.

Stock in Hand

Authorized stock

Number required

The Head Office will make supplies to the Sub Post Office, after proper check over the

quantity indented for with reference to the authorized stock, under separate series of invoice

to each Sub Post Office. The invoice will be prepared in triplicate, serially numbered for each

Sub Post Office and two copies will be sent to the sub post office with the CBS Pass Books.

The serial number of invoices will run consecutively for each financial year. The Sub Office

will return one copy of the invoice to the Head Post Office duly acknowledged. The

acknowledged copy will be filed with the original invoice.

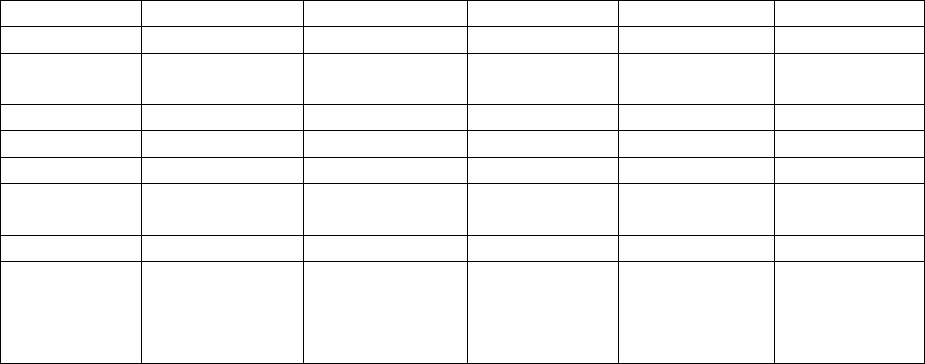

(b) In Sub Post Office stock register of CBS Pass Books in form SB-4(a) will be maintained in the

format given below separately for SB5 and SB5A:-

SPECIMEN OF FORM

SB-4(a)Stock Register of CBS Pass Books of Sub Office

Date

CBS Pass Books

received

CBS Pass Books issued

*Account number should be

mentioned for new accounts.

Balance

in hand

after

each

receipt

or issue

Initials of

sub-

Postmaster

Remarks

Particulars

of the

invoice

(a)

No of

passbooks

(b)

For new

accounts

(a)

In lieu of

used up

passbooks

(b)

Issued

duplicate

1

2

3

4

5

6

7. Transmission of CBS Pass Books

(1) When a CBS Pass Book is made over by a depositor to a Post Office for any purpose, a receipt

will be issued from SB-28.and handed over to the depositor.

(2) When a CBS Pass Book is made over by a depositor to a Post Office for dispatch to another

post office, it should be dispatched by service registered post and the receipt for the registered

article being given to the depositor. The words “CBS Pass Book of Post Office Saving/ RD/

TD/ PPF/NSS/MIS/SCSS/SSA (Account No…………………….. with a balance of

Rs………… should be written on the receipt. When a CBS Pass Book is returned by the post

office to the depositor or sent by one Post Office to another, a similar note should made on the

receipt which should be given to the Saving Bank Assistant who should paste it in his receipt

book or case file.

13

(3) In the following cases, free transmission of CBS Pass Books from one post office to another is

allowed:

(i) As enclosure to a complaint or a deceased claim.

(ii) In response to a call from the post office for presentation of CBS Pass Book.

(iii) From a depositor on active service through the Field Post Office to his near relative for

operating on the account and vice versa..

8. Register Of Undeliverable CBS Pass Books In Deposit In The HOs And SOs

(1) Register of CBS Pass Books in deposits in H.O. :- If a depositor fails to take delivery of his

CBS Pass Book within 30 days from the date of its receipt in the HO or SO, the S.O. will

forward the CBS Pass Book to the H.O. duly entered in the list of documents with remarks

“Undelivered”. Whenever a CBS Pass Book is returned undelivered by a subordinate office

or is received by the H.O. from any other source (e.g. from the depositor himself) and remains

undelivered for any reason, particulars thereof should be entered in the Register of

undeliverable CBS Pass Books in deposit in the H.O. in the format given below:-

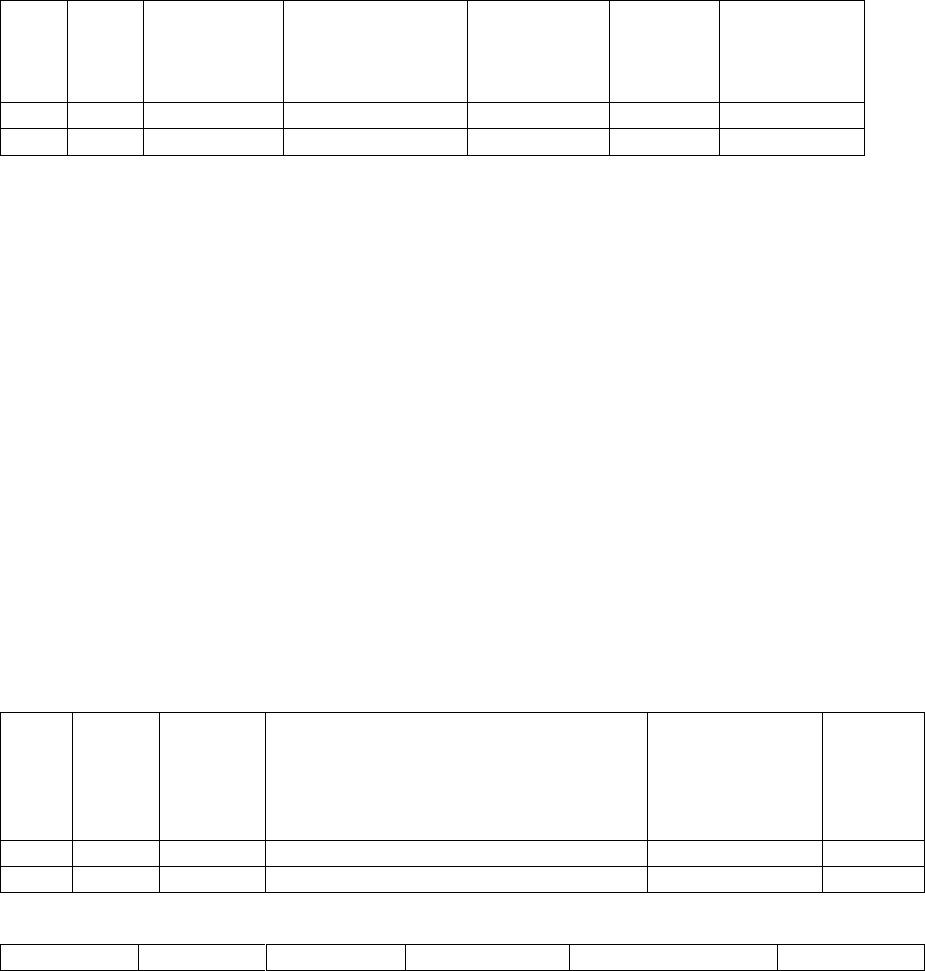

SPECIMEN OF FORM

SB 12(c)Register of undelivered CBS Pass Books in deposit in the Head Post

Office……………………………………

Date of receipt of

undeliverable CBS

Pass Book from sub

or branch post

office or from any

other source.

Account

Number

Balance

Name of Sub

or Branch Post

Office from

which

received or the

person from

whom

received

Particulars regarding

the final disposal of

the CBS Pass Book

with date of its

dispatch from the

HO or delivery to

the depositor

Remarks

1

2

3

4

5

6

2) When a CBS Pass Book which has been brought on the register is returned to the depositor

either directly or through a subordinate office or in any other way, particulars regarding its

final disposal should be entered in the register.

3) The register and the CBS Pass Books entered in it should remain in the personal custody of

the Supervisor.

4) If a CBS Pass Book is not claimed within a period of three months from the date of its

original receipt at the H.O. it should be forwarded to the SBCO for safe custody. The

acquaintance of the SBCO for such CBS Pass Book will be obtained in the remarks column

of the relevant entry in the register.

5) Before the CBS Pass Book is sent to the SBCO, the balance shown therein should be

verified with that shown in the Finacle CBS application using relevant menu and the

remarks “Balance Rs………… verified and Passbook transferred to control organization

for safe custody on………………………….”

14

6) If an application for a CBS Pass Book which has been transferred to the SBCO is received

in the H.O., the CBS Pass Book should be called for from the SBCO by sending a

requisition duly signed by the Postmaster. On receipt of the CBS Pass Book from the

SBCO, a suitable note should be made in the register against the particular entry. A note in

the Register should be made as follows” Recalled and delivered to the depositor

on………/dispatched to SO on……………”

7) Such an application received in a SO should be forwarded to the HO indicating the date on

which the CBS Pass Book was returned to the HO as undelivered.

8) Register of CBS Pass books in deposit in SOs: The CBS Pass Books received from the

head office or any other source for delivery to the depositors will be entered in a

manuscript register to be maintained for this purpose in the form given below in order to

keep their proper account. The date of receipt will be noted on the top in the register. The

serial number in the register will run in an annual series starting from No. 1 in April each

year. The CBS Pass Books should be delivered to the depositors as soon as possible on

their surrendering the receipt (SB-28) granted to them duly signed and date of delivery

noted in the register. The details of CBS Pass Books sent to branch offices will be entered

in the register in the prescribed columns. The date on which the CBS Pass Book is finally

returned as undelivered to the Head Office will be noted in the register under initial of the

SPM in the prescribed column. A summary of the CBS Pass Books in hand showing the

closing balance on a day when there is change in the balance will be prepared in the

remarks column of the register by the sub postmaster under his dated signature. The receipt

should be pasted to the office copy of the receipt in the receipt book (SB-28).

Summary

(a) Opening balance…………………………………………………………………………….

(b) CBS Pass Books received …………………………………………………………………

(c) Total ………………………………………………………………………………………….

(d) CBS Pass Books delivered/returned to H.O. /sent to Branch Office……….………….

(e) Closing balance …………………………………………………………………………….

Date Signature of the Sub Postmaster

The closing balance should be verified with the CBS Pass Books in hand. The register and the CBS

Pass Books entered in it should remain in the personal custody of the Sub Postmaster.

SPECIMEN OF FORM

Proforma for the Register of CBS Pass Books in Deposit in Sub Offices

Sl

No.

Account

No

Type

of

account

SB,RD,

etc.

Name of

branch

office to

which the

CBS Pass

Book sent

Date of

delivery

To the

depositor or

date of

dispatch to

the B.O.

Date on

which

returned as

undelivered

to the Head

Office.

Initial of

the

Supervisor

Remarks

1

2

3

4

5

6

7

8

15

9. Pay-In-Slip (SB-103)

(i) All deposits presented at the counter of Post Office will be accompanied by pay-in-slips with

counterfoil (SB-103) duly filled in by or on behalf of the depositor. The Counter Assistant

accepting the deposit should check the entries in both parts to see that they agree in all

respects and after transaction is done in Finacle CBS Application, note Name of Scheme and

Transaction ID in red ink on the upper right hand corner of the Pay-In-Slip.. The date-stamp

should be impressed at the marked place on both parts. The counterfoil will be signed,

detached and handed over to the depositor or his messenger. The pay-in-slip will serve as a

voucher for deposit. This voucher will be included in the Voucher Bundle along with other

vouchers.

(ii) The pay-in-slip is in two different colours viz. white (SB-103) for

Savings/TD/MIS/NSS/PPF/SSA accounts and yellow (SB-103) (a) for RD accounts.

Note: - The pay-in-slip can be filled in either in English or in Hindi or in the Regional language at the

option of the depositor.

10. Preliminary Receipt (SB-26)

1) Preliminary receipts SB-26are printed in books of 50 receipts in triplicate for Branch Offices

and are machine-numbered.

2) In Extra-Departmental Branch Office, these receipts are to be prepared by the ED-BPM for

the first deposit in triplicate by double sided carbon paper with indelible pencil entering the

name of the person and the amount of deposit. The type of account for which receipt is

issued should be prominently noted at the top on both copies of the receipt, e.g., SB, TD (--

----year/s), RD/SSA, etc. After all three copies of the receipts are signed by the ED-BPM

the pencil copy should be given to depositor after noting the date on which he may attend

the post office to collect the pass book, the second copy to be sent to account office duly

entered in list of documents and third copy being retained in the book as office copy. The

number of receipt issued should be noted in the remarks column of BOSB/RD/TD/SSA

Journal and Specimen Signature book in red ink.

3) If a preliminary receipt is spoiled, the word “Spoiled” should be written across all the

copies of the receipt under the dated signature of the E.D.B.P.M. First and second copies

should be sent to the Account Office (HO/SO) duly entered in the BO Daily Account with

appropriate remarks.

4) On receipt of the original and duplicate copies of a preliminary receipt from a Branch Post

Office with the remarks “Spoiled”, the Sub/Head Postmaster will, after verification and

counter-signature, return the original to the Branch Office and file the duplicate in his

office. When the receipt is receive back at BO from the Account Office after verification

and counter signature by the Postmaster, it should be pasted to the office copy of the receipt

by the BPM

5) The Account Office of a Branch Office will maintain an Index to Savings Bank preliminary

receipts issued by the Branch Offices in account and keep a watch over the use of the

receipts in serial order. The duplicate copies of the preliminary receipts received from the

Branch Offices should be filed in the Account Office in monthly bundles Branch Office-

wise.

6) A designated Savings Bank Assistant in HO/SO will maintain an index of preliminary

receipts which will have entries for Extra-Departmental Branch offices. The index should

be in the form of index to preliminary receipts (MS-15). On receipt of the vouchers from

BO, he will check that the first serial number is in continuation of the last serial used and

that all serial numbers are in a consecutive order. He will enter the numbers of preliminary

16

receipts issued by each ED Branch Office in the index (MS-15) and initial the entry. He

will put up the index to the Supervisor who will initial the entry with date after satisfying

himself that the prescribed check has been carried out. In case of any discrepancy in

continuity of serial numbers, the SB Assistant should promptly bring the fact to the notice

of the Supervisor for necessary action.

7) The Head Office/Sub Office is responsible for supply of preliminary receipts book to Extra-

Departmental Branch Office in direct account only when the receipts in the book in use are

about to be exhausted. To ensure against double supply, a note with the date of supply of

the receipt book should be made in the index to preliminary receipt books (MS–15). In

case of Branch Offices, in account with the Sub Office, HO on recipt of requisition, will

supply SB-26 to Sub Office for supply to its BOs. The date of supply of receipt book

should be intimated to the Divisional Superintendent for verification at the time of

inspection.

8) When a Branch Office is closed, the Savings Bank preliminary receipt book should be sent

to the Head/Sub Office concerned where the unused receipts will be examined. The unused

receipts will be destroyed personally by the Supervisor after making suitable remarks in the

index to the preliminary receipts.

9) In case the loss of original receipt is reported by the depositor at EDBO, following

procedure is to be adopted:- When a depositor reports the loss of the original receipt, he

should be asked to submit a written application giving full particulars of the first deposit

and stating the circumstances in which the original receipt was lost. If the depositor is

illiterate, his mark or seal on the application should be attested by a respectable person

known to the applicant and known to the post office. The signature and other particulars

mentioned in the application should be carefully verified and when the genuineness of the

application has been established, the following certificate should be recorded on the

application by the GDSBPM under his dated signature:-“Certified that the particulars of the

first deposit and the signature of the depositor have been verified by me and found correct”.

The application should be forwarded to the Account office for verifying the signature of the

depositor and for orders (to be recorded on the application itself) regarding delivery of the

CBS Pass Book to the applicant. After the orders are passed by the Postmaster, the

application with the orders thereon should be pasted to the office copy of the preliminary

receipt. The CBS Pass Book should be delivered to the depositor on obtaining his receipt

on the office copy of the preliminary receipt (PR) on which the following endorsement

should be made by the GDSBPM under his dated signature. “Delivered on proper

identification and after verification vide application dated………………… of the depositor

pasted herewith”. The application will then be pasted along with office copy of PR.

11. Receipt for depositor’s CBS Pass Book (SB-28)

1) A receipt (SB-28) printed and machine numbered in books of 50 receipts will be given to the

depositor when his CBS Pass Book is taken from him and cannot be returned to him

immediately but has to be retained in the office.

2) The receipt is to be prepared in duplicate by carbonic process using double sided carbon

paper with an indelible pencil by the Counter Assistant entering the account number, name

of the depositor and the balance at credit. Both copies should be impressed with the date

stamp and signed by him before the receipt book is placed before the APM/SPM for check.

After the entries are checked and both copies of the receipt signed by the APM/SPM, the

pencil copy will be given to the depositor after noting the date on which he should attend

the post office to collect the CBS Pass Book and the carbon copy retained in the book.

17

3) When the CBS Pass Book is delivered to the depositor, his copy of the receipt (SB-28),

duly signed by him in token of having received the CBS Pass Book, will be taken back

from him and pasted to the office copy of the receipt. The signature of the depositor

appearing on the receipt should be compared with the specimen signature on record before

delivering the CBS Pass Book.

4) The current book of receipts should remain in the personal custody of the APM/SPM at the

close of the day‟s transactions when he should see that the unissued receipts in book are

intact and put his dated signature on the reverse of the last used receipt.

5) The APM/SPM will review the receipt books at the close of each month in order to see that

all the receipts are properly accounted for and that the depositor‟s copies of the receipt

containing acknowledgement for the CBS Pass Books are on record duly pasted to the

office copies before the books are transferred to record.

6) If the receipt is spoilt the word “spoilt” should be written across both the copies of the

receipt under the dated signature of the APM/SPM which may be kept on record. If the

receipt is spoilt in the branch office, the branch office will forward the original copy of the

spoilt receipt to its account office which will return the same to the branch office after

verification and counter-signature.

7) The Head/Sub Post Office will maintain an index of receipts (SB-28) issued by the Branch

offices in account with it in form MS-15 with reference to the relevant entries in the BO

daily account and ensure that the receipts are serially issued.

8) The Head Office is responsible for the supply of receipt books (SB-28) to the sub and

branch post offices. A fresh receipt book will be supplied to the sub and branch office in

direct account on receipt of requisition from SPM/BPM. In case of branch offices in

account with the sub office, a fresh receipt book will be supplied on receipt of requisition

from the sub office. Care should be taken to guard against double supply of receipt book

against the same requisition. The date of supply of the receipt book should be intimated to

the Divisional Superintendent/Inspector of Post Offices, as the case may be, for verification

at the time of inspection.

9) When a branch office or sub office is closed, the receipt book should be sent to the H.O.

where the unused receipts will be examined. The unused receipts will be destroyed

personally by the Supervisor after making a suitable remark in the index receipts (MS-15).

10) When a depositor reports the loss of the original receipt, he should be asked to submit a

written application indicating the account number and last balance in the CBS Pass Book

and stating the circumstances in which the original receipt was lost. If the depositor is

illiterate, his mark or seal on the application should be attested by a respectable person

acquainted with the applicant and known to the post office. The signature and other

particulars mentioned in the application should be carefully verified and when the

genuineness of the application has been established, the following certificate should be

recorded on the application by the APM/SPM under his dated signature.

“Certified that the last balance shown in the application and Signature/L.T.I. of the depositor have

been verified by me and found Correct.”

After the orders are passed, the CBS Pass Book should be delivered to the depositor on obtaining his

receipt on the reverse of the office copy of the receipt on which the following endorsement should be

made by the APM/SPM under his dated signature.

18

“Delivered on proper identification and after verification vide application dated………of the

depositor pasted herewith.

The application with orders thereon should be pasted to the office copy of the receipt.

12. Supply of Savings Bank Account Statement

A depositor may obtain account statement of his Savings Account in Post Office working on

CBS platform in lieu of passbook on payment of such fees specified by the central

government by notification in the official gazette. Balance and transactions shown in the

passbook or statement of accounts shall be for the information of the depositor.

13. Types of Savings Accounts

From 13.5.2005, only individual accounts can be opened under Rule 4 of Post Office

Savings Account Rules, 1981. Following types of accounts can be opened in the FINACLE

CBS Software:-.

(i) Single/Joint account with Cheque Book or without cheque book.

(ii) Minor account opened through Guardian.

(iii) Lunatic Account opened on behalf of a person of unsound mind through Guardian

(iv) Pension Account.

(v) Sanchayika Account. (discontinued from 1.10.2016)

(vi) Account not bearing interest

(vii) Basic Savings Account (Zero Balance)

A brief detail of each type of account is given below: -

(i).Single and Joint Account with or without cheque book: -

(a) Single accounts can be opened by an adult or a minor of the age of 10 years or more. Joint

account can be opened by two or three adults to be operated by them (a) jointly or by the

survivors/survivor which is called Joint-A type account (b) either of them/any of them or

either of the survivors or survivor which is called Joint-B type account. Any number of

accounts can be opened by the depositor(s) but NOT more than one single, one joint account

and one Minor Account as Guardian can be opened in each post office. A person can open

two joint accounts with two different partners at the same post office. For example, if A,B and

C open a joint account in one post office, A can also open separate joint accounts wirh B & C

respectively. In other words, A can open one separate Joint Account with B and another

separate Joint Account with C. If the applicant applies for cheque book, account can not be

opened with initial deposit of less than Rs.500/-. Otherwise, account can be opened without

cheque book with Rs.20/- as initial deposit.

(b) Any individual of the age between 10-18 years, who opens account in POSB without

guardian, has to submit revised account opening form (AOF) on attaining the age of 18 years

with fresh KYC documents. Revised AOF and KYC documents should be attested by the ex-

guardian. Otherwise, all transactions of such accounts will be frozen from the day he/she

attains the age of 18 years.

(ii) Minor‟s Accounts: - Only guardian can open account on behalf of a minor. Guardian in

relation to a minor means: -

Father or mother, and

19

Where neither parent is alive, or where the only living parent is incapable of acting, a person

entitled under the law for the time being in force to have the care of the property of the minor.

a) If an account is to be opened on behalf of a minor, the application form for opening the account

should be submitted by the guardian of the minor. If only year of birth is known by the

guardian and exact month and date of birth is not known, the 1

st

July of that year will be taken

as Date and month of birth and in case only date is not known, 16

th

of the month will be taken

as the date of birth.

b) The minor, on whose behalf account has been opened by the guardian, on attaining majority

should fill in account opening form (AOF) duly attested by the guardian and present his

Identification/Address proof and photograph to post office where account stands. If he/she

desires to continue the account, a following additional declaration is required to be given on

plain paper in manuscript:-

“I further declare that I have/I shall have, after the expiry of one month from the date of my

attaining majority, not more than one account standing in my own name at any Post Office

Savings Bank. In the event of this declaration proving incorrect, I shall be liable to forfeit

interest from the date of my attaining majority to the date of closure of all such accounts

found open in any Post Office”. The declaration should be attested either by the person who

was operating the account or by a trustworthy person known to the Post Office.

c) The revised AOF alongwith Annexure-I or II and KYC documents including separate

declaration if given should be kept in the post office in A4 size Guard File. Duplicate KYC

Form should be sent to Circle processing Centre (CPC) for further processing.

Note: Once the minor attains majority, the status of account will automatically be shown as “freeze”

in FINACLE CBS Application. During the next transaction, in CMRC menu option, in account

modification option, “mode of operation” to be changed to 012- self to enable the ex-minor to operate

the account independently.

(iii) Lunatic Accounts opened on behalf of persons of unsound mind through Guardian: -

a) An account may be opened on behalf of a person of unsound mind under the conditions

mentioned in rule 4(1)(d) of the Post Office Savings Account Rules, 1981.

b) An account opened on behalf of a person of unsound mind by a manager or guardian

appointed by a Court of Law or the Superintendent of a Mental Hospital, may, in the event

of the court or the Superintendent of Mental Hospital subsequently declaring such person of

unsound mind to be sane, be operated by the ex-lunatic on his/her furnishing the following

additional declaration in addition to a fresh account opening form (AOF) ,“I further declare

that I have/I shall have, after the expiry of one month from the date of my becoming sane,

not more than one account standing in my name at any Post Office Savings Bank. In the

event of this declaration proving in-correct, I shall be liable to forfeit interest from the date

of my being declared sane to the date of closure of all such accounts found opened in any

post office”.

c) The revised AOF along with Annexure-I or II and KYC documents including separate

declaration if given should be kept in the post office in A4 size Guard File. Duplicate KYC

Form should be sent to Circle processing Centre (CPC) for further processing.

(iv) Pension Accounts: -

a) A pension account can be opened by the Pensioners of Railway, Postal, Telecom or any

other Organization (with whom agreement has been signed by the Department) for the

20

credit of monthly pension automatically in their pension account by the Postmaster. Only

one pension account can be opened by the Pensioner. He can also open an ordinary single

and joint account in addition to the pension account in the same post office. In this

account, the amount of pension will be credited by the Postmaster every month and the

pensioner can withdraw the amount from the account at his convenience. The pensioner

cannot deposit any other money in this account. A Pension account can also be opened in

Joint capacity but only with spouse of Pensioner whose name is entered in the PPO.

b) In a pension account, the Head Savings Bank or Sub Savings Bank is authorized to recover

any amount credited in excess of the eligible amount. An application for withdrawal will

be used for the purpose with suitable remarks showing the reasons for the withdrawal. An

intimation to the pensioner should be sent in that case explaining why the balance in his

account is reduced.

(iv) Sanchayika Accounts: - This was introduced by MOF(DEA) from 22.06.1970 and

discontinued for opening of these accounts from 1.10.2016. However, already opened

Sanchayika Accounts shall be treated as normal savings account.

(vi) Accounts not bearing interest:- If at the time of opening an account, the intending depositor

expresses his unwillingness to receive interest on the deposits in his account, he should be

requested to record a statement to that effect under his own signature in the application form

for opening of the account. The words “No interest” should then be written prominently in red

ink across the top left hand side of the application form, on page one of the pass book given to

the depositor and at the head of the depositor's account in the FINACLE CBS Application.

a) If a depositor who has opened an account not bearing interest applies afterwards to get

interest in his account, he should be allowed to change the option midway during the currency

of the account.

b) If a depositor who has opened Savings account(s) bearing interest, declines afterwards to

accept interest, interest will cease to accrue from the year in which the application is made.

The words “No Interest” should be written in the pass book and entered in FINACLE CBS

Application. The depositor should submit a fresh application form (AOF) which should be

kept along with the old form.

Note: - Only Savings accounts can be opened under this option.

(vii) Basic Savings Account:-Ministry of Finance (DEA) has vide its notification issued vide

F.No. 2/6/2006-NS-II dated 20.5.2011 has introduced another category of savings account

called “Basic Savings Account” under newly inserted Rule 4A (1) of Post Office Savings

Account Rules 1981 and renamed all “Workers Wage Accounts” opened under Rule 4A of

POSA Rules 1981 as well as all Old Age/Widow/Disabled Pensioners Accounts opened under

Indira Gandhi National Old Age Pension Scheme, Indira Gandhi National Widow Pension

Scheme and Indira Gandhi National Disabled Pension Scheme vide Rule 4B of POSA Rules

1981 as “Basic Savings Accounts” from 20.5.2013. Rule 4B of POSA Rules 1981 has been

deleted from 20.5.2013. Main features of this type of savings account and the procedure to be

followed for opening and operating this type of account(s) is given below: -

(a) A registered adult member of any Government Welfare scheme can open Basic Savings

Account at any Post Office including EDBO.

(b) A guardian of a minor whose name is registered for any Government Welfare Scheme can

also open Basic Savings Account at any Post Office including EDBO.

(c) Only one account can be opened by the beneficiary.

21

(d) No minimum amount will be required to open such account and no minimum balance needs

to be maintained in such accounts.

(e) Any Government benefit or any other deposit can be made in these accounts.

(f) These accounts will have all the facilities that have been provided for normal Savings

Account except that these will be non cheque accounts.

(g) Only a single account may be opened under this category.

(h) The depositor who desired to open Basic Savings Account under this category has to provide

copy of letter/card issued by a competent authority of any State or Central Government

Department mentioning registration/enrollment number under any welfare scheme. No

account will be opened without providing this information.

(i) The Branch/Sub/Head Postmaster will compare this document with the original under his/her

dated signatures. The depositor has to provide one document as Address Proof from the

documents prescribed for Low Risk Accounts and photograph(s) as required for Low Risk

Category of Accounts.

(j) All other formalities applicable to normal savings account i.e. Specimen Signatures, issue of

PR in EDBO, issue of passbook etc. will be followed.

(k) Interest will be credited in such accounts by following the normal procedure laid down for

savings accounts.

(l) These accounts will not be treated as silent.

(m) All existing Zero Balance Accounts opened either under NREGS module of Sanchaya Post or

opened manually for NREGA Workers or Indira Gandhi National Old Age/Widow/Disability

Pensioners will be renamed as “Basic Savings Accounts”.

14. Specimen Signatures and Photograph

1) For each type of accounts, specimen signatures and photograph of the depositor(s) are

required to be maintained for verifying the signature and their identity. The account opening

forms (AOF) containing specimen signatures and photograph are to be retained in the Post

Office and kept safely in A4 size Binder and KYC Form (Annexure-II) (to be taken only once

unless there is a change in the same) should be sent to CPC which will scan and upload the

same against the relevant account number for future reference.

2) The specimen signature/photograph in the FINACLE CBS Software should be used to verify

the signature or identity of the depositor at the time of withdrawal, closure, transfer or change

of status of the account etc. This can be viewed by using the relevant menu in Finacle CBS

Application.

3) If it is noticed that the signature of a depositor has changed owing to any change in his

handwriting or that a depositor has altered his manner of signing his name, he should be

requested to give fresh specimen of his newly adopted signature and fresh Identity as well as

Address proof in Annexure-II in duplicate. After satisfying that the documents are genuine,

the Supervisor should send one copy of the Annexure-II to CPC for scanning and attaching to

the account and keep the office copy in Guard File.

4) When there is change of incumbent in the case of an account opened by the Superintendent of a

Mental Hospital on behalf of a patient confined in any such hospital, same procedure as

mentioned in (c) above shall be followed.

5) In case of illiterate depositors, left hand thumb impression (LTI) of female and right-hand

thumb impression (RTI) of male depositors are required to be taken instead of signatures.

6) Supervising Officers should make a point of checking at random the specimen signatures

uploaded to Signature Verification System (SVS) in FINACLE CBS Application at the time

of inspection. Head and Sub Postmasters should examine the Signature Verification System in

22

FINACLE CBS Application periodically to see that the signatures are uploaded for all the

accounts opened in their office and ensure that withdrawals in accounts of other SOL IDs

from Savings Bank accounts are not allowed in the absence of specimen signature in SVS.

15. Nomination

1) Individual(s) opening a single or joint account may nominate any person or persons who in

the event of his/their death shall become entitled to receive the payment of the amount due on

the account by filling in the required details in the account opening application form (AOF).

In case of first nomination, the counter PA will enter all the details in the option of

nomination in the FINACLE CBS Software. The depositor(s) of an existing account may also

apply for registration of nomination, its cancellation or variation in the Post office where

account stands at any time after opening the account in form (SB-55) together with the CBS

Pass Book. The depositor has to submit fresh identity as well as Address proof along with

SB-55 form. The depositor has to bring in one witness for registration of nomination whose

ID and Address proof should also be attached. The Counter PA/Supervisor, after satisfying

with the identity of the depositor and accepting of witness, will go to Account Modification

menu and modify the nomination details in the Finacle CBS software and keep relevant

documents in a separate Guard File.

2) No nomination shall be made in respect of an account opened by or on behalf of a minor or a

person of unsound mind.

3) The nomination, its cancellation or variation, when it is registered, takes effect from the date on

which it is entered in the FINACLE CBS Software.

4) The nomination status as „Y‟ for Yes and „N‟ for no will be printed in the Passbook. In case

depositor desires to have name of the nominee or nomination registration number in

Passbook, the same should be entered manually.

5) A nomination made by a depositor under sub-rule (1) may be cancelled or changed by the

depositor. A fee of rupee one shall be chargeable on every application for registration of a

nomination or of any variation in nomination or cancellation thereof; provided that no fee

shall be charged on an application for registration of the first nomination. Whenever depositor

desires to change or cancel a nomination he should fill in the prescribed form of application

(SB-55) and present the same along with the pass book with the prescribed fee in postage

stamps affixed on it. The application will be verified in the same manner as an original

application for nomination. In the account modification menu, the counter PA has to enter the

nomination details with reference to the SB-55 and supervisor has to approve the same.

6) In case of cancellation, a rubber stamp “Nomination cancelled” should be affixed on (a) the

original application for nomination form (SB-3)/AOF/application (SB-55) (b) the pass book.

The application for cancellation should be filed with the original application for nomination

for all types of accounts.

7) In case of change, a rubber stamp “Nomination altered under No……… on (date)……”

should be affixed on (i) the original application in form (SB-3)/AOF/application for

nomination (S.B.-55) (ii) the pass book. In the account modification menu, the counter PA

has to enter the new nomination details with reference to the SB-55 and supervisor has to

approve the same and the new nomination registration number to be entered in the passbook

manually.

8) The postage stamp affixed on the application should be defaced with the date stamp of the

office.

23

9) The application for nomination (Form SB-55) will be kept in a guard file. The application for

cancellation or change (SB-55) should be filed in the guard file along with original

application for nomination or application form (SB-3)/ (AOF).

Note: -If for any reason the application for nomination or change in nomination given by the

depositor is not accepted, he should be informed in writing the reasons for non-acceptance.

10) When a depositor makes a nomination or cancels/changes the nomination already made, using

form SB-55 at the sub office, the Sub Postmaster will make change/cancel/alter the

nomination using Account Modification Menu in Finacle. Sub Postmaster will keep SB-55 in

the guard file in SO.

11) For an account standing at a Branch Office, the Branch Postmaster will send the form SB-55

to the Account office along with Passbook to Account Office. The Account office will deal

with it as it would have tendered at the Account Office. First Page of Passbook should be

printed again from Passbook Printer showing Nomination as “Y” and return the pass book to

the Branch Post Office for delivery to the depositor.

12) When an account is transferred from one SOL ID to another SOL ID, there will not be any

change in already registered nomination details.