1666 K Street NW, 9th Floor

Washington, DC 20006

Telephone: (202) 207-9100

Facsimile: (202) 862-8430

www.pcaobus.org

Statement of Daniel L. Goelzer

Acting Chairman

Public Company Accounting Oversight Board

Before the

United States House of Representatives

Financial Services Committee,

Subcommittee on Capital Markets, Insurance and

Government Sponsored Enterprises

Hearing on Accounting and Auditing Standards:

Pending Proposals and Emerging Issues

2128 Rayburn House Office Building

May 21, 2010

Statement of Daniel L. Goelzer

Acting Chairman

Public Company Accounting Oversight Board

Chairman Kanjorski, Ranking Member Garrett, and Members of the Subcommittee:

I appreciate the opportunity to appear before you today on behalf of the Public

Company Accounting Oversight Board ("PCAOB" or the "Board") to testify on the work

of the PCAOB. I want to begin by thanking the Financial Services Committee and this

Subcommittee for their support of the Board’s mission. In light of the extraordinary

events over the past two years, the statutes – and the regulators that implement them –

over which you have jurisdiction could not be more important to the future financial well-

being of the American people. I look forward to discussing with the Subcommittee the

role that the Board plays in protecting investors and fostering confidence in our

securities markets.

More than half of American households invest their savings in securities to

provide for retirement, education, and other goals. The auditor’s job is to protect these

investors’ interest in accurate, complete, and fairly presented financial information by

independently reviewing and reporting on management’s financial statements. Reliable

financial reporting is one of the linchpins on which our capital markets depend. If

investors lose confidence in financial reporting, they may demand prohibitively high

returns as a condition of investing or they may withdraw from the markets altogether.

The result would be to make it more difficult and expensive to finance the businesses on

which our economy depends. Moreover, inaccurate financial reporting can mask poor

business strategies that, if left uncorrected, may result in the misallocation of capital and

in business failures and layoffs.

As the accounting scandals related to Enron and WorldCom demonstrated,

auditors can face strong pressures and incentives to acquiesce in rosy accounting. The

Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act” or the “Act”) was passed in the

wake of the collapse of confidence that resulted from these and other financial reporting

break-downs. Title I of the Act created the PCAOB to serve as a counterweight to

those pressures and incentives. Congress rightly determined in 2002 that rigorous,

independent oversight was essential to the credibility of the auditor’s watchdog function.

In the balance of my testimony, I want to explain how we have sought to translate that

vision into reality.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 2

I. The Responsibilities of the PCAOB

Prior to the creation of the PCAOB, public company auditors were subject to

oversight by their professional association and to peer reviews conducted by other

auditing firms. Title I of the Sarbanes-Oxley Act profoundly changed the environment in

which public company auditors operate by providing for ongoing accountability to the

PCAOB, which is independent of the profession. The Board exercises that oversight

through four basic functions –

• Registration of accounting firms – No accounting firm may prepare, or

substantially contribute to, an audit report for a public company that files

financial statements with the Securities and Exchange Commission (“SEC”

or “Commission”) without first registering with the PCAOB. Since 2009,

securities broker-dealers must also have the balance sheets and income

statements they file with the SEC audited by PCAOB-registered firms.

There are currently 2,484 accounting firms registered with the Board. This

includes 935 non-U.S. firms and 530 firms that registered because they

have broker-dealer audit clients. Beginning this year, all registered firms

must file annual and other reports that provide the Board and the public with

updated information about the firm and its audit practice.

• Inspection of firms and their public company audits – Since 2003, the

Board has conducted more than 1,300 inspections of firms’ quality controls

and reviewed aspects of more than 6,000 public company audits. The audit

engagements we review are not selected at random. To make the most

effective use of its resources, the PCAOB uses a variety of analytical

techniques to help the inspection staff select engagements and audit areas

that are likely to raise challenging or difficult issues.

1

PCAOB inspections

have identified numerous audit deficiencies, including failures by the largest

1

The PCAOB devotes considerable resources to collecting, quality

checking, and analyzing data from public sources, vendors, registered firms and internal

sources. The PCAOB uses this data to monitor financial reporting and auditing risks.

The PCAOB’s screening techniques combine non-public data collected in the inspection

process with publicly-available data to identify those firms, offices, partners,

engagements, and issues that present the greatest audit risks. PCAOB analysts

perform in-depth analysis of these high-risk issuer-audits to provide our inspectors with

actionable intelligence when they go into the field.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 3

U.S. and non-U.S. firms. These findings have led to changes in firm quality

controls, and, in some cases, to corrections of client financial statements.

• Investigation and disciplinary proceedings – The Board has broad

authority to impose sanctions on registered firms and associated persons

that have violated applicable laws and standards. The PCAOB has publicly

announced the resolution of 31 enforcement proceedings, which involved a

combined total of 55 registered firms and individual auditors of those firms.

Among these 55 parties are 32 individual auditors, including partners and

other individuals associated with major accounting firms, who have have

consented to suspensions or bars from working on public company audits.

These proceedings also include 15 settled revocations of firms’

registrations, preventing them auditing public companies in the future.

Sanctions have also included significant monetary penalties. These

settlements do not, however, reflect the full extent of PCAOB enforcement

activity. Under the Sarbanes-Oxley Act, all Board investigations and all

contested proceedings (i.e., cases in which the Board files charges and the

respondent elects to litigate, rather than settle) are non-public. There are a

significant number of matters under active investigation and an additional

number in litigation.

The Board closely coordinates its enforcement efforts with the SEC. In

certain instances, the PCAOB investigates the auditor’s conduct and the

SEC focuses its investigation on the public company, its management, and

other parties. In other cases, the SEC’s Division of Enforcement takes

responsibility for an investigation and requests that PCAOB defer to that

investigation.

• Establishing auditing, quality control, ethics, independence, and other

standards – The Board is responsible for establishing the auditing and

related standards under which public company audits are performed. Prior

to the Sarbanes-Oxley Act, public company audits were performed

according to standards set by the profession itself. The PCAOB has an

active standard-setting agenda, as I will describe later in my testimony.

All of the Board’s responsibilities are discharged under the oversight of the SEC.

The SEC appoints, and may remove, Board members. The PCAOB’s annual budgets

must be approved by the SEC. The PCAOB’s rules, including its auditing and related

professional practice standards, are not effective unless approved by the SEC. PCAOB

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 4

inspection reports, remediation determinations, and disciplinary actions are appealable

to the SEC. In addition to these formal oversight mechanisms, we work closely with the

Commission on a daily basis. Chairman Schapiro and Chief Accountant Kroeker have

taken a deep interest in the Board’s work, and I am grateful to them for their support

and for the strong working relationship they have fostered between our organizations.

The PCAOB receives no appropriated funds. Once approved by the SEC, the

Board’s budget is funded through an annual accounting support fee assessed on public

companies in proportion to their average equity market capitalizations. As a result,

roughly three-quarters of the PCAOB’s accounting support fee is paid by the largest 500

public companies. The Financial Accounting Standards Board (“FASB”) is funded in a

similar way, and the PCAOB serves as the collection agent for FASB assessments.

II. The PCAOB’s Recent Work in Connection with the Financial Crisis

The Subcommittee asked that I describe how the PCAOB has responded to audit

issues raised by the financial crisis. PCAOB auditor oversight is not intended to assess

financial institution capital adequacy or risk management, which many have suggested

were the proximate reasons for institutions’ failure or need for bail-out funds. Nor does

the PCAOB set accounting and disclosure requirements. That is the purview of the

FASB, the International Accounting Standards Board, in the case of institutions

permitted to use International Financial Reporting Standards, and the SEC. Rather, the

PCAOB focuses on whether auditors have done their job, which is to make sure an

institution’s financial statements and related disclosures fairly present its results – good

or bad – to investors in conformity with applicable accounting and disclosure standards.

Each of our core programs has adjusted its focus to address issues that have

arisen from the financial crisis. I want to briefly summarize these responses.

A. Inspections

The PCAOB’s inspection program is the core of its oversight of registered firms’

public company audit work. The PCAOB conducts annual inspections of firms that

regularly audit the financial statements of more than 100 public companies. In 2009,

the PCAOB inspected ten such firms. Firms that regularly audit the financial statements

of 100 or fewer public companies must be inspected at least once every three years.

The PCAOB inspected 277 such firms in 2009, including 82 non-U.S. firms located in 26

countries. In the course of these inspections, PCAOB inspectors reviewed portions of

more than 350 audits performed by the ten firms subject to annual inspection, and

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 5

portions of more than 730 audits performed by the remaining 277 inspected firms.

During 2009, the PCAOB inspected aspects of audits for some of the largest public

companies in the world, including financial services and other companies with complex

financial instruments and transactions and risks relating to market volatility.

The Board is required to issue a report with respect to each inspection it

conducts. The public portion of an inspection report describes matters that inspectors

have identified as significant audit failures. These findings, presented in Part I of the

report, generally involve situations in which PCAOB inspectors believe that the auditor

failed, in some material respect, to obtain sufficient evidence to support the audit

opinion or failed to identify a material departure from generally accepted accounting

principles. Consistent with restrictions in the Sarbanes-Oxley Act, however, the Board

does not publicly disclose the identity of the companies that are the subject of audits

discussed in an inspection report.

2

Most of the audits that the Board inspected during 2009 were of financial

statements for fiscal years ending in 2008. We are now in the process of evaluating

firms’ responses to questions and comments we have raised and preparing our

inspection reports. So far, 112 reports on 2009 inspections have been released,

including two with respect to firms subject to annual inspection. Because the 2009

reporting cycle is still ongoing, it is not possible to generalize concerning the kinds of

audit problems we found. However, in order to broaden the field of auditors and others

who may benefit from understanding the nature of common audit deficiencies inspectors

identified last year, the Board plans to issue a summary report, under PCAOB Rule

2

The PCAOB discusses any criticism of or potential defects in a firm’s

system of quality control in Part II of its inspection reports. The Act affords inspected

firms one year within which to remediate Board criticisms concerning firm quality

controls. If the Board is not satisfied with a firm’s remediation efforts, the portion of the

report containing the discussion of the quality control deficiencies becomes public.

The Board transmits full inspection reports, including the nonpublic portions of

such reports, to the SEC and appropriate state boards of accountancy. The Board is

also permitted to share full reports with certain other U.S. regulatory and oversight

authorities. In addition, the Board sends a special report to the Commission when, as a

result of information developed in an inspection, the Board believes that financial

statements filed with the Commission, and on which the public is relying, are materially

inaccurate.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 6

4010,

3

on audit issues presented by the financial crisis. I anticipate that this report will

afford those interested in auditing and financial reporting with additional insight

concerning the audit challenges that have emerged from the financial crisis.

In addition, in light of the allegations raised in the Lehman bankruptcy examiner’s

report, the PCAOB has asked certain firms to provide information on their audit

procedures in connection with audit clients in the financial services industry that have

applied sales accounting treatment to repurchase agreements involving financial assets.

Repurchase transactions may not be the only method companies may have used to

dress-up their financial statements at period-end, however. The PCAOB is looking for

other strategies companies may use to manipulate reported debt.

More broadly, the PCAOB plans to enhance its focus on the quality control

mechanisms of large firms that participate in global networks as well as on audit work

performed by non-U.S. firms on subsidiaries or other segments of multi-national audit

clients. We will examine firms’ supervision of work performed by affiliated firms,

including by assessing firms’ controls over consultations on accounting and auditing

standards, instructions to affiliates, and evaluation of affiliates’ work.

B. Enforcement

Based on referrals from the PCAOB’s Office of Research and Analysis, from the

inspections program, and from other information sources, the Board’s enforcement staff

is conducting several investigations related to audits of the financial statements of public

companies involved in the financial crisis. As with most regulatory bodies, our

investigations are by statute confidential.

As I noted earlier, unlike most regulators, including the SEC, the Board’s

contested disciplinary proceedings also are, by law, non-public and confidential. As a

result, unfortunately, the facts and circumstances of any matters stemming from the

financial crisis that the Board believes warrant enforcement action are unlikely to

become public for a considerable period of time. Moreover, this feature of the Act

3

Information received or prepared by the Board in connection with any

inspection is subject to certain confidentiality restrictions set out in Sections 104(g)(2)

and 105(b)(5) of the Act. Under the Board's Rule 4010, however, the Board may

publish summaries, compilations, or general reports concerning the results of its various

inspections, provided that no such published report may identify the firm or firms to

which any quality control criticisms in the report relate.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 7

provides respondents with an incentive to litigate, rather than settle, in order to delay

any adverse publicity.

C. Auditing Standard-setting

The Committee has also asked me to address the role of auditing standards in

the financial crisis and in the transparent portrayal of companies’ overall financial health.

Auditing standards do not set forth reporting or disclosure requirements for companies.

Rather, they set forth required procedures for auditors to evaluate whether financial

statements present the company’s financial position fairly in accordance with applicable

accounting standards.

Nevertheless, the Board’s standard-setting program has responded to the

financial crisis by reminding auditors how existing standards apply in the context of

current challenges. The PCAOB has issued Staff Audit Practice Alerts to explain to

auditors how applicable requirements bear on various issues raised by the crisis. For

example, in December 2008, the PCAOB issued Staff Audit Practice Alert No. 3, Audit

Considerations in the Current Economic Environment (December 5, 2008). This alert

helped PCAOB inspectors focus firms on applicable audit requirements in our 2009

inspections. It covered several audit topics relevant to the crisis, including auditing fair

value measurements and accounting estimates, auditing the adequacy of disclosures,

the auditor’s consideration of a company’s ability to continue as a going concern, and

additional audit considerations for selected financial reporting areas.

More recently, in light of the Lehman bankruptcy examiner’s report, as well as

deficiencies PCAOB inspectors have identified in connection with the auditing of

significant unusual transactions, the PCAOB issued Staff Audit Practice Alert No. 5,

Auditor Considerations Regarding Significant Unusual Transactions (April 7, 2010).

This alert reminded auditors of their obligation to evaluate significant transactions that

may be mechanisms to dress up a company’s balance sheet, as opposed to serving a

valid business purpose.

Practice Alerts only remind auditors of existing requirements. The Board also

has the ability to use information that it learns in its inspections and from other sources

to change the underlying auditing standards. The Board’s Office of the Chief Auditor,

which is responsible for PCAOB standard-setting, is reviewing the results of the 2009

inspections program to determine whether there are additional issues that should be

added to the Board’s standards agenda. As explained below, we have an ambitious

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 8

agenda of standards projects, several of which would respond directly to current

auditing challenges.

III. Challenges Facing the PCAOB

I believe that the Board has made excellent progress during the past seven years

in turning the blueprint that Congress provided in Title I of the Sarbanes-Oxley Act into a

functioning organization that is making a meaningful contribution to investor protection.

However, we still face a variety of challenges to realizing fully the audit oversight that

Congress envisioned. I want to touch briefly on four of those challenges.

A. Inspecting Non-U.S. Audits

Approximately 250 non-U.S. firms are subject to regular PCAOB inspection.

4

To

date, the Board has inspected 173 non-U.S. firms in 33 jurisdictions, with some firms

being inspected more than once. As I mentioned earlier, in 2009 the PCAOB inspected

82 non-U.S. firms in 26 jurisdictions. Twenty-nine of these 82 inspections were

performed on a joint basis with the local auditor oversight authority pursuant to

negotiated cooperative arrangements. In each of the joint inspections, as well as most

other foreign inspections not conducted on a joint basis, the PCAOB and its foreign

counterpart have been able to resolve conflicts of law, sovereignty, and other issues

that may arise when we are operating in another country.

Unfortunately, however, we are not currently able to conduct inspections in the

European Union, Switzerland, and China.

5

In previous years, the PCAOB was able to

4

About 930 registered firms are located outside of the United States, in 86

countries. Not all of these firms are subject to regular, periodic PCAOB inspection.

Only a firm that, during a three-calendar-year period, issues an audit report or plays a

substantial role in the preparation or furnishing of an audit report with respect to an

issuer is subject to regular PCAOB inspections. Many of the Board’s foreign registrants

are members of a global network of firms that share a common name and certain

policies, audit methodologies and business interests with firms that operate in the U.S.

5

As a transparency measure, earlier this week, the PCAOB published a list

of more than 400 non-U.S. issuers whose securities trade in U.S. markets, but whose

PCAOB-registered auditors the Board currently cannot inspect because of asserted

non-U.S. legal obstacles. In addition, the PCAOB has previously published a list

identifying each registered firm that has not yet been inspected even though more than

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 9

conduct joint inspections in some EU Member States, but in February 2009, the EU

barred further joint inspections pending resolution of the information-sharing issue

discussed below. As a result, inspections of 20 EU firms scheduled for 2009 did not

occur.

6

In the case of Switzerland, although the PCAOB was on track to conduct two

joint inspections with the Swiss audit regulator, the Swiss informed us in early 2009 that

those inspections could not go forward. The Swiss objections related in large part to

our ability to transfer information gathered during inspections to other U.S. regulators,

such as the U.S. Department of Justice.

7

With regard to China, the objection is based

primarily on national sovereignty. There, inspections of two mainland Chinese firms

were scheduled in 2009 but did not occur, and inspections of eight Hong Kong firms

have been commenced but not completed because we were denied access to

documents relating to companies operating in mainland China.

8

One of the obstacles to reaching an agreement to resume inspections in the EU

Member States has been the Board's inability under the Sarbanes-Oxley Act to share

inspections and investigation information with foreign auditor oversight authorities.

While the Act protects PCAOB inspection and investigative processes from public

disclosure and from discovery in private legal proceedings, it allows the PCAOB to

four years have passed since the firm first issued an audit report while registered.

These lists are available at http://pcaobus.org/Featured/Pages/International.aspx.

6

There are 307 firms from 26 countries in the EU (including Norway)

registered with the PCAOB; 73 of those firms (in 20 countries) are subject to inspection

because they audit, or play a substantial role in auditing the financial statements of a

U.S. public company’s foreign operations or a foreign private issuer listed on a U.S.

exchange.

7

Nine Swiss firms are currently registered with the PCAOB; five of those

firms are subject to inspection because they audit, or play a substantial role in auditing

the financial statements of a U.S. public company’s Swiss operations or a foreign

private issuer listed on a U.S. exchange.

8

There are 53 Chinese firms, and 59 Hong Kong firms, registered with the

PCAOB; 52 (24 in mainland China and 28 in Hong Kong) of those firms are subject to

inspection because they audit, or play a substantial role in auditing the financial

statements of a U.S. public company’s Chinese operations or a foreign private issuer

listed on a U.S. exchange.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 10

us andicap.

share information prepared or gathered during those processes with certain U.S. federal

and state authorities.

9

However, since non-U.S. audit oversight bodies are not

included, the PCAOB is currently unable to enter into agreements to provide information

to non-U.S. regulators. Information sharing is important to many of our foreign

counterparts, and our inability to provide it is a serio h

Thanks to this Committee’s efforts, Section 7602 of the Reform Act, as passed

by the House of Representatives last year, would correct this problem by permitting the

PCAOB to share information with non-U.S. audit oversight bodies. A similar provision

has been included in the Restoring American Financial Stability Act of 2010 in the U.S.

Senate. Final enactment of the information sharing provisions would enable the Board

to proceed with meaningful discussions with its EU counterparts. The Board

understands that this provision enjoys widespread investor and profession support.

B. Auditing Standards

The second area I would like to mention is the setting of auditing standards. The

PCAOB is engaged in several standard-setting initiatives, in consultation with the SEC,

that are intended to modernize, or address weaknesses in, existing standards. Those

standards were originally developed by the profession itself and adopted by the PCAOB

in 2003 as interim standards. I regard this area as a current challenge simply because

of the range and scope of the current projects we have under way.

As I noted earlier, in creating the Board, Congress shifted responsibility for public

company auditing standards from the auditing profession itself to the PCAOB.

9

The list of authorities that may receive such information is limited to the

SEC, the Attorney General of the United States, appropriate Federal functional

regulators (such as bank regulators), State attorneys general in connection with criminal

investigations, and appropriate State regulatory agencies (such as state boards of

accountancy). Section 7608 of H.R. 4173, the Wall Street Reform and Consumer

Protection Act (“Reform Act”), would enable the PCAOB to share confidential

information with the Congress.

The omission of foreign audit oversight authorities from the list of permissible

recipients of confidential information is due to the fact that when the current provisions

were written, very few countries had bodies similar to the PCAOB. Since the

establishment of the PCAOB, more than 30 countries have established or empowered

bodies to inspect public accounting firms.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 11

Nonetheless, in our standard-setting, the Board takes into account initiatives of the

profession, including the International Auditing and Assurance Standards Board

(“IAASB”), which is an arm of the International Federation of Accountants (“IFAC”) and

sets standards known as International Standards of Auditing. The Board is an observer

to the IAASB’s Consultative Advisory Group and monitors various IAASB projects; and

the IAASB is an observer to our comparable advisory body – the Standing Advisory

Group (“SAG”). Most important, though, the PCAOB takes into account information

learned in inspections, investigations and other oversight activities, in order to develop

standards focused on improving investor protection.

The Board has four standards-setting projects that are in various stages of public

exposure. These are –

• Risk Assessment – On December 17, 2009, the Board re-proposed seven

new auditing standards, Proposed Auditing Standards Related to the

Auditor's Assessment of and Response to Risk and Related Amendments to

PCAOB Standards that, collectively, would update the requirements for

assessing and responding to risk in an audit. The re-proposed standards

are intended to provide for more robust risk assessments and more rigorous

procedures to respond to identified risks. The Board is considering

comments received on this proposal and plans to finalize its project later this

year.

• Audit Confirmation Evidence – One of the most widely used substantive

tests for obtaining evidence regarding the existence and, to a lesser extent,

the valuation of various accounts, is direct communication by the auditor

with third parties independent of management, commonly referred to as

confirmation. The Board issued a Concept Release on Possible Revisions

to the PCAOB's Standard on Audit Confirmations in 2009, seeking public

comment on the potential direction of a standard-setting project. The

concept release identified possible changes to the existing standard on

confirmation, including changes that would reflect the prevalence of

electronic confirmation requests and electronic records, as well as changes

related to the risks of management interception or other intervention in the

confirmation process. The Board is considering the comments and plans to

issue a proposal to change the standard in the near future.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 12

• Communications with Audit Committees – The Board recently proposed

a new standard on auditor-audit committee communications. A fundamental

objective of the Sarbanes-Oxley Act is to strengthen the role of the audit

committee by placing it squarely at the center of the relationship between a

public company and its auditor. The proposed new standard is intended to

implement that objective by enhancing and making more concrete the

substance of auditor-audit committee communications. In particular, the

proposal focuses on communications regarding audit risk.

• Engagement Partner Audit Report Signature – The Board issued in 2009

a Concept Release on Requiring the Engagement Partner to Sign the

Audit Report to solicit public comment on whether it should require the

engagement partner to sign the audit report. The partner’s signature

would be in addition to the PCAOB's current requirement for the registered

public accounting firm to sign the audit report. The Board is currently

considering comments.

There are several other projects as to which we intend to publish proposals

within the next few months. These include –

• Cross-border Audits of Multi-national Companies – The Board is

considering revising the PCAOB’s interim standard on the principal, or

signing, auditor’s use of other audit firms in conducting audits of financial

statements of multi-national companies. In addition, because most such

audits are performed by firms that participate in a network of affiliates and

hold themselves out as offering a common brand, the PCAOB is evaluating

the adequacy of its quality control standards and considering whether

changes may be appropriate to enhance networked firms’ controls over

interaction with and use of other firms in their networks.

• Use of a Specialist – The Board is considering enhancing the audit

requirements when the auditor uses someone with expertise outside the

area of accounting and auditing to assist in the audit.

• Related Party Transactions – In light of issues raised in the financial crisis,

the Board is considering revising its standard on auditing related party

transactions, as well as other significant unusual transactions, that may not

be on arms-length terms. Accounting for related party transactions is

sometimes abused to make a company appear to be doing better than it is.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 13

There are other auditing standards projects under consideration. I have attached

a copy of the PCAOB’s most recent standard-setting agenda as Appendix A.

C. Expanding Authority – Broker-Dealer Auditor Oversight

Another challenge the Board currently faces relates to the likelihood that our

jurisdiction will significantly expand this year. Both the Reform Act passed by the House

last year and the Restoring American Financial Stability Act of 2010 in the Senate would

extend the Board’s inspections, enforcement, and standard-setting authority to include

audits of securities broker-dealers. The Board supports this provision, since it would

close the gap that currently exists between the requirement that broker-dealer auditors

register and the absence of any Board authority to oversee the work of these firms.

This authority would, however, require us to add to the expertise of our staff and to

adjust the focus of our programs in order to address this new area of oversight.

In December 2008, in the wake of the revelation of the Madoff Ponzi scheme, the

SEC discontinued the exemption from PCAOB registration previously applicable to

accounting firms that audit the 5,000 or so SEC-registered nonpublic broker-dealers.

10

As a result, more than 500 additional audit firms with broker-dealer audit clients have

been registered by the Board. However, the Sarbanes-Oxley Act does not empower the

Board to inspect, set standards for, or investigate deficiencies in broker-dealer audits.

11

This creates a risk that brokerage firm clients may believe that, because broker-dealer

auditors are registered with the PCAOB, we are exercising oversight of the audit work of

those firms, especially as it relates to the auditor’s review of procedures the broker

employs to protect client cash and securities.

Section 7601 of the Reform Act, and Section 982 of the Restoring American

10

Every SEC-registered broker and dealer is required by Section 17(e)(1)(A)

of the Securities Exchange Act of 1934 (15 U.S.C. 78q(e)(1)(A)), as amended by the

Sarbanes-Oxley Act, to file with the SEC a balance sheet and income statement

certified by a registered public accounting firm. The SEC issued a series of orders

which deferred effectiveness of the PCAOB registration requirement for these auditors.

The last such order expired on December 31, 2008.

11

On January 8, 2009, the Board issued a statement to raise public

awareness that the Sarbanes-Oxley Act does not provide for PCAOB oversight of

brokerage firm audits.

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 14

Financial Stability Act of 2010 in the U.S. Senate, would give the Board full oversight

authority.

12

If this legislation is enacted, the Board would be required to expand its rules

to cover audits of brokers and dealers as well as issuers, develop standards and an

inspection methodology for audits of broker-dealers, and hire and train additional staff

with experience related to broker-dealer audits. The PCAOB would also need to

establish a budget for these new activities, as well as adjust its funding system so that

broker-dealers, like public companies, contribute to the cost of overseeing their auditors.

D. FEF v. PCAOB

Finally, no discussion of challenges facing the Board would be complete without

mentioning the pending challenge to the Board’s constitutionality. In December 2009,

the Supreme Court heard argument in a case challenging the constitutionality of the

Board’s structure.

13

The litigation deals principally with the way in which Board

members are appointed and the circumstances under which Board members could be

removed. The case does not challenge the mission of independent oversight of the

auditing profession, and the Board remains focused on that mission as it awaits the

Court’s decision.

The Board has vigorously defended its constitutionality since the case was

originally filed in 2006, maintaining that its members are properly appointed by the SEC

because Board members are “inferior officers,” and that the SEC’s plenary power over

the Board brings the Board well within separation of powers requirements. The United

States, which joined the case through the Department of Justice and the SEC, has also

argued – through two consecutive Administrations – that the Board’s structure passes

12

The provision passed in Section 7601 of H.R. 4173 and the provision in

Section 982 of S. 3217 contain different approaches to registration. The House bill

would permit the PCAOB to decide, by rule and with SEC approval, whether to inspect

the audits of certain categories of brokers and dealers, and then would grant an

exemption from the requirement to register with the Board to those firms that would not

be inspected. The Senate bill would require auditors of all SEC-registered brokers and

dealers to remain registered with the Board, but would grant the Board discretion,

subject to SEC approval, to determine the inspection cycle for different categories of

firms.

13

Free Enter. Fund and Beckstead and Watts, L.L.P. v. Pub. Co. Accounting

Oversight Bd., et al., No. 08-861 (U.S. argued Dec. 7, 2009).

Statement of PCAOB Acting Chairman Daniel L. Goelzer

May 21, 2010

Page 15

constitutional muster. Both investors and the accounting profession filed amicus briefs

in the Supreme Court in support of the Board.

We expect the Supreme Court to issue its decision by the end of June. The

PCAOB prevailed in the District Court and the Court of Appeals,

14

and we hope that the

Supreme Court will reach the same result. In the event that the PCAOB does not

prevail – and the decision requires a legislative change – I would urge Congress to act

quickly to fix whatever structural problems the Court identifies. The Board stands ready

to assist Congress in that effort. As recent events have shown, the need for investor

protection through independent oversight of the auditing profession is as urgent today

as it was in 2002 when the Sarbanes-Oxley Act was enacted.

* * *

That completes my overview of the current work of the Public Company

Accounting Oversight Board and of some of the challenges we face. I would be happy

to answer any questions.

14

Free Enter. Fund and Beckstead and Watts, L.L.P. v. Pub. Co. Accounting

Oversight Bd., et al., 2007 U.S. Dist. LEXIS 24310 (D.D.C. Mar. 21, 2007), affirmed,

537 F.3d 667 (D.C. Cir. 2008).

Appendix A

1666 K Street, NW

Washington, D.C. 20006

Telephone: (202) 207-9100

Facsimile: (202)862-8430

www.pcaobus.org

STANDING ADVISORY GROUP MEETING

OCA CURRENT STANDARD-SETTING AGENDA

APRIL 7-8, 2010

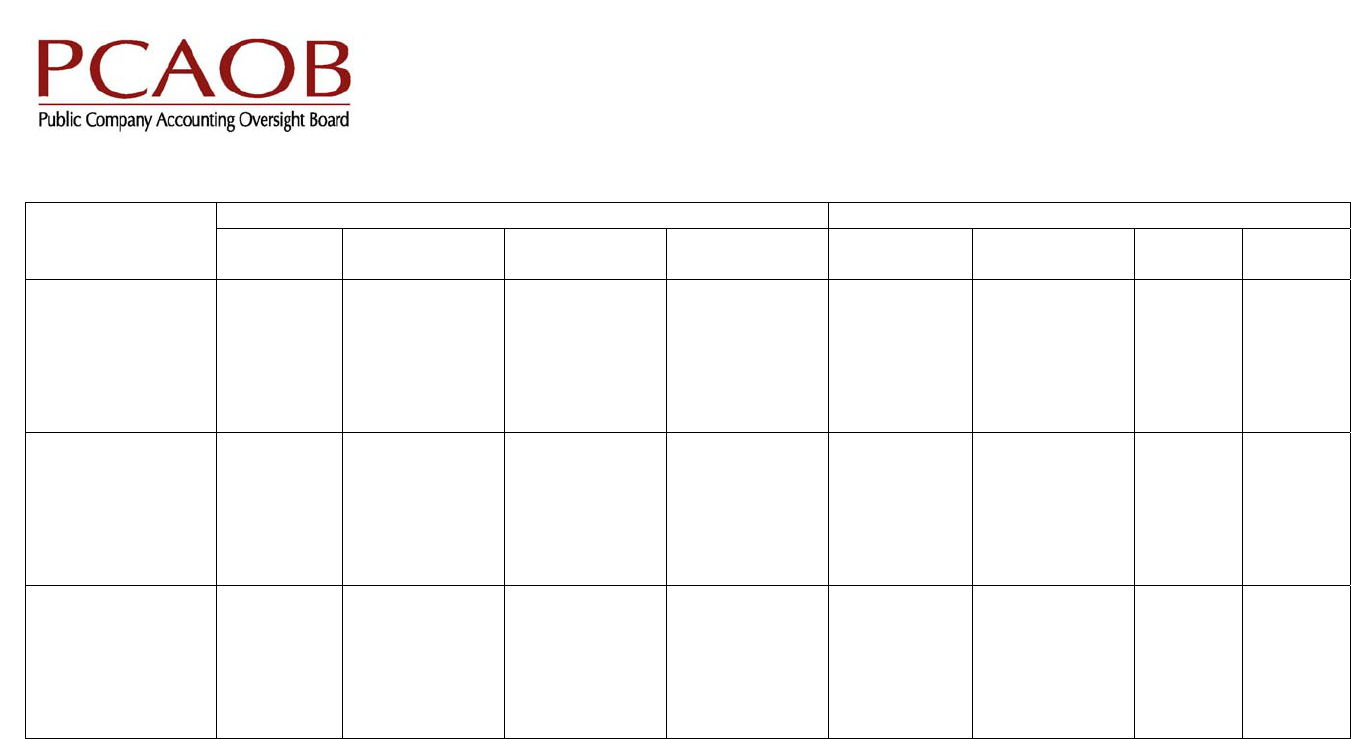

The table, followed by a brief project overview, presents the Office of the Chief Auditor's ("OCA") current standard-setting

agenda with key milestones. Project milestones have been developed for planning and budgeting purposes and may

change due to a variety of reasons. Specifically, the projected project milestones are contingent on the Board determining

that the staff should pursue a standard-setting project in each area. If the Board determines to issue a concept release for

public comment before proposing a standard, the Board will analyze the comments received and determine if it is

appropriate to proceed with a proposed standard. Additionally, after the Board receives public comment on a proposed

standard the Board will determine whether to adopt a final standard or seek additional comment through re-proposal.

Finally, emerging issues, new accounting developments, and any new legislative initiatives could impact the projected

milestones or could result in other priorities not on the agenda.

Appendix A

OCA Standard-Setting Agenda

April 7-8, 2010

Page 2 of 9

*The projected project milestones are contingent on the Board determining that the staff should pursue a standard-setting

project in each area. If the Board determines to issue a concept release for public comment before proposing a standard,

the Board will analyze the comments received and determine if it is appropriate to proceed with a proposed standard.

Additionally, after the Board receives public comment on a proposed standard the Board will determine whether to adopt a

2010 2011

Project* 1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

1. Risk

Assessment,

including fraud

risk assessment

Adopt final

standards

2.

Communications

with Audit

Committees

Issued

proposed

standard

for public

comment

Adopt final

standard or

re-propose

standard for

public

comment

Adopt final

standard

3. Audit

Confirmations

Issue

proposed

standard for

public

comment

Adopt final

standard

4. Signing the

Auditor's Report

Board to

determine

whether to

proceed with

proposal

Issue

proposed

amendments

to standards

for public

comment

Adopt final

amendments

to standards

final standard or seek additional comment through re-proposal. Finally, emerging issues, new accounting developments,

and any new legislative initiatives could impact the projected milestones or could result in other priorities not on the

agenda.

Appendix A

OCA Standard-Setting Agenda

April 7-8, 2010

Page 3 of 9

*The projected project milestones are contingent on the Board determining that the staff should pursue a standard-setting

project in each area. If the Board determines to issue a concept release for public comment before proposing a standard,

the Board will analyze the comments received and determine if it is appropriate to proceed with a proposed standard.

Additionally, after the Board receives public comment on a proposed standard the Board will determine whether to adopt a

2010 2011

Project* 1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

5. Application of

the Sarbanes-

Oxley Act's

Provision on

"Failure to

Supervise"

Issue release,

including

request for

comment on

possible

related rules

or standards

Board to

consider

whether to

propose

related rules

or standards

Issue

proposed

rules or

standards for

public

comment

Adopt final

rules or

standards

6. Related

Parties

Issue

proposed

standard for

public

comment

Adopt final

standard or

re-propose

standard for

public

comment

Adopt

final

standard

7. Specialists Issue

proposed

standards for

public

comment

Adopt final

standards or

re-propose

standards

for public

comment

Adopt

final

standard

final standard or seek additional comment through re-proposal. Finally, emerging issues, new accounting developments,

and any new legislative initiatives could impact the projected milestones or could result in other priorities not on the

agenda.

Appendix A

OCA Standard-Setting Agenda

April 7-8, 2010

Page 4 of 9

*The projected project milestones are contingent on the Board determining that the staff should pursue a standard-setting

project in each area. If the Board determines to issue a concept release for public comment before proposing a standard,

the Board will analyze the comments received and determine if it is appropriate to proceed with a proposed standard.

Additionally, after the Board receives public comment on a proposed standard the Board will determine whether to adopt a

2010 2011

Project* 1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

8. Fair Value

Measurements

and Other

Accounting

Estimates

Issue

proposed

standards for

public

comment

Adopt final

standards or

re-propose

standards

for public

comment

Adopt

final

standard

9. Principal

Auditor / Multi-

Location Audits

Issue

proposed

standard for

public

comment

Adopt final

standard or

re-propose

standard for

public

comment

Adopt

final

standard

10. Quality

Control

Standards,

Including Quality

Controls Over

the Work of

Affiliated Firms

Issue concept

release for

public

comment

Issue

proposed

standard for

public

comment

Adopt

final

standard

final standard or seek additional comment through re-proposal. Finally, emerging issues, new accounting developments,

and any new legislative initiatives could impact the projected milestones or could result in other priorities not on the

agenda.

Appendix A

OCA Standard-Setting Agenda

April 7-8, 2010

Page 5 of 9

*The projected project milestones are contingent on the Board determining that the staff should pursue a standard-setting

project in each area. If the Board determines to issue a concept release for public comment before proposing a standard,

the Board will analyze the comments received and determine if it is appropriate to proceed with a proposed standard.

Additionally, after the Board receives public comment on a proposed standard the Board will determine whether to adopt a

final standard or seek additional comment through re-proposal. Finally, emerging issues, new accounting developments,

and any new legislative initiatives could impact the projected milestones or could result in other priorities not on the

agenda.

2010 2011

Project* 1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

1

st

Quarter

2

nd

Quarter

3

rd

Quarter

4

th

Quarter

11. Applicability

of SECPS

Requirements to

all Registered

Firms

Board to

determine

whether to

proceed with

a standard-

setting project

Issue

proposed

amendments

for public

comment

Adopt final

standard or

re-propose

standard for

public

comment

Adopt

final

standard

12. Going

Concern

Board to

determine

whether to

proceed with

a standard-

setting project

13. Subsequent

Events

Board to

determine

whether to

proceed with

a standard-

setting project

Appendix A

OCA Standards-Setting Agenda

April 7-8, 2010

Page 6 of 9

Standards-setting Brief Project Overview

1. Risk Assessment – The Board re-proposed the standards for public comment on December 17, 2009. The comment

period ended on March 2, 2010. The staff is analyzing the comments received and will discuss with the Board its views

on how to address the comments.

2. Communications with Audit Committees – The Board proposed the auditing standard for public comment on March 29,

2010. Comments are due on May 28, 2010.

3. Audit Confirmations – In response to the comments received on the May 29, 2009 concept release, the staff is

evaluating potential revisions to the audit confirmations auditing standard.

4. Signing the Auditor's Report (Advisory Committee on the Auditing Profession to the U.S. Department of Treasury

("ACAP") Recommendation Firm Structure and Finance Recommendation No. 6) – It was recommended that the

PCAOB "[u]ndertake a standard-setting initiative to consider mandating the engagement partner's signature on the

auditor's report." – The staff is analyzing the comments received on the July 28, 2009 concept release and is

discussing with the Board the staff's views on how to address the comments.

5. Application of the Sarbanes-Oxley Act's Provision on "Failure to Supervise" – The staff is currently preparing a draft

release for the Board's consideration relating to the Board's application of Section 105(c)(6) of the Act, which

authorizes the Board to impose sanctions on firms and individuals for failure to supervise. The release would also seek

comment on concepts relating to what, if any, rulemaking or standard-setting might usefully supplement the Board's

application of that provision.

6. Related Parties – In response to comments received at the October 14-15, 2009 SAG meeting, the staff is evaluating

potential revisions to the related parties auditing standard.

7. Specialists – In response to the comments received at the October 14-15, 2009 SAG meeting, the staff is evaluating

potential revisions to the specialist auditing standard.

Appendix A

OCA Standards-Setting Agenda

April 7-8, 2010

Page 7 of 9

8. Fair Value Measurements and Other Accounting Estimates – In response to the comments received at the October 14-

15, 2009 SAG meeting, the staff is evaluating potential revisions to the standards on fair value measurements and

other accounting estimates.

9. Principal Auditor / Multi-Location Audits – The staff is evaluating potential revisions to the principal auditor auditing

standard. The staff will discuss this topic with the Standing Advisory Group at the April 7-8, 2010 meeting.

10. Quality Control Standards, Including Quality Control Over the Work of Affiliated Firms – The staff is evaluating

potential revisions to the quality control standards. This will include an evaluation of Appendix K.

11. Applicability of SECPS Requirements to all Registered Firms – Because registered firms (generally non-U.S. firms and

some smaller firms) that were not members of the SECPS in April 2003 when the Board adopted certain of the SECPS

requirements are not subject to these interim quality control requirements, the staff is analyzing different options to

determine if it is feasible to extend the SECPS requirements to all registered firms. This excludes Appendices E

(superseded by AS No. 7) and K (part of global quality control standards standards-setting project).

12. Going Concern – The staff is monitoring FASB's project and plans to update the timeline when the FASB determines

their action plan for the accounting standard. OCA will assess if any conforming amendments are needed to the

Board's auditing standards to align with the FASB's final standard. The staff will also evaluate any additional issues

and determine whether to pursue a standard-setting project on going concern.

13. Subsequent Events – The staff is evaluating potential revisions to the subsequent events auditing standard in light of

FASB's new accounting standard on subsequent events.

Appendix A

OCA Standards-Setting Agenda

April 7-8, 2010

Page 8 of 9

Other Projects

OCA is also considering the following recommendations relating to standards-setting from the Advisory Committee on the

Auditing Profession to the U.S. Department of Treasury ("ACAP") and the Advisory Committee on Improvements to

Financial Reporting to the U.S. Securities and Exchange Commission ("CiFIR")

1/

–

• ACAP Concentration and Competition Recommendation No. 4(a) – Compile the SEC and PCAOB

independence requirements into a single document and make this document website accessible.

• ACAP, Firm Structure and Finance Recommendation No. 5 – Urge the PCAOB to undertake a standard-

setting initiative to consider improvements to the auditor's standard reporting model. Further, urge that the

PCAOB and the SEC clarify in the auditor's report the auditor's role in detecting fraud under current auditing

standards and further that the PCAOB periodically review and update these standards. The staff will discuss

this topic with the Standing Advisory Group at the April 7-8, 2010 meeting.

• CIFiR Recommendation III.E, Clarifying Guidance on Financial Restatements and Accounting Judgments –

In recognition of the increasing exercise of accounting and audit judgments, we recommend that the SEC

and PCAOB adopt policy statements on this subject.

Interim Professional Auditing Standards adopted by the PCAOB in April 2003

Similar to past practice, OCA continually evaluates the Board's interim standards and takes a priority-based approach in

determining which interim standards need to be amended. As part of developing the standards-setting priorities on an

annual basis, OCA takes into consideration the results of the Board's oversight activities of registered accounting firms,

1/

Final Report of the Advisory Committee on the Auditing Profession to the U.S. Department of the Treasury

(October 6, 2008), available at http://www.treas.gov/offices/domestic-finance/acap/docs/final-report.pdf, and Final Report

of Advisory Committee on Improvements to Financial Reporting to the U.S. Securities and Exchange Commission (August

1, 2008) available at http://www.sec.gov/about/offices/oca/acifr/acifr-finalreport.pdf

.

Appendix A

OCA Standards-Setting Agenda

April 7-8, 2010

Page 9 of 9

the work of other standards setters (e.g. FASB, IAASB), advice from the Standing Advisory Group, emerging issues,

research, and solicitation of public comments. The final set of priorities is determined based on the results of the PCAOB's

oversight of registered public accounting firms, monitoring of the environment, and consultation with the Board's Standing

Advisory Group, among other factors.

* * *

The PCAOB is a private-sector, non-profit corporation, created by the Sarbanes-Oxley Act of 2002, to oversee the

auditors of public companies in order to protect the interests of investors and further the public interest in the preparation

of informative, fair, and independent audit reports.