Northern Illinois University Law Review Northern Illinois University Law Review

Volume 9 Issue 2 Article 6

5-1-1989

The Illinois Mortgage Foreclosure Act and Installment Contracts: The Illinois Mortgage Foreclosure Act and Installment Contracts:

Filling in the Gaps Filling in the Gaps

Robert Kratovil

Follow this and additional works at: https://huskiecommons.lib.niu.edu/niulr

Part of the Law Commons

Suggested Citation Suggested Citation

Robert Kratovil, The Illinois Mortgage Foreclosure Act and Installment Contracts: Filling in the Gaps, 9 N.

Ill. U. L. Rev. 349 (1989).

This Article is brought to you for free and open access by the College of Law at Huskie Commons. It has been

accepted for inclusion in Northern Illinois University Law Review by an authorized editor of Huskie Commons. For

more information, please contact [email protected].

The

Illinois

Mortgage

Foreclosure

Act

and Installment

Contracts:

Filling

in

the

Gaps

ROBERT

KRATOVIL*

I.

INTRODUCTION

Drastic

changes

in

Illinois

foreclosure

law were

introduced

into

our

state

effective

July

1,

1987

by

Public

Act

84-1462.'

While

this

law

contains

many

complex

provisions, this

commentary

will

focus

on

one

short

paragraph.

The

paragraph

to

be

examined

is

15-1106(2).

The relevant language

is

as

follows:

Sec. 15-1106.

Applicability

of

Article.

(a)

Exclusive

Procedure.

From

and after

the

effective

date

of

this

amendatory

Act

of

1986,

the

following

shall

be

foreclosed

in

a

foreclosure

pur-

suant

to

this

Article:

(1) any

mortgage

created

prior

to,

on or

after

the

effective

date

of

this

amendatory

Act

of

1986;

(2)

any

real

estate

installment

contract

for

residential

real

estate entered

into

on

or after

the

effective

date

of

this

amendatory

Act

of

1986

and

under

which

(i)

the

purchase

price

is

to

be

paid

in

installments

over

a

period

in

excess

of

five

years

and

(ii)

the

amount

unpaid

under

the terms

of

the

contract

at

the

time

of

the

filing

of

the

foreclosure

complaint,

including

principal

and

due

and

unpaid

interest,

at

the rate

prior

to

default,

is

less

than

80%

of

the

original

purchase

price

of

the

real

estate

as

stated

in

the

contract

....

2

A

problem

arises

when

the

practitioner,

in

pursuing

a

remedy

for

a client,

uses

the current

real

estate

contract

forms.

This

commentary

will

highlight

deficiencies in

present

forms,

while

providing

sample

*

Distinguished

Professor

of

Law,

The

John

Marshall

Law

School,

Chicago,

Illinois.

1.

Illinois

Mortgage

Foreclosure

Law,

Public

Act

84-1462,

ILL.

REV.

STAT.

ch.

110,

paras.

15-1101

to

15-1706

(Supp.

1987)

(effective

July

1,

1987).

2.

Id.

at

para.

15-1106.

NORTHERN

ILLINOIS

UNIVERSITY

LA

W

REVIEW

provisions designated

to

bring the

contracts into

compliance

with

the

Act.

II.

PROCEDURE

PRIOR

TO

NEW

LAW

Prior

to

the enactment

of

this

new

law,

the

typical

remedy

employed

by

the

vendor

when

default

occurred

was

forfeiture

followed

by

forcible

detainer.

3

Briefly,

forfeiture

of

an installment

contract

was

a

procedure

by

which

the

vendor

could

extinguish

all

the

pur-

chaser's

rights

to

the

property

and

to

any

past

monies

paid under

the

contract

upon

an

act

of

default.

This

procedure

was

much

like

the

eviction

of

a

tenant

who

was

unable

to

pay

rent.

This

was

a more

expedient

remedy

than

a

mortgage

foreclosure.

In

order

to

declare

a

forfeiture,

the

installment

contract

must

have

contained

a

forfeiture

clause.

Without

such a clause,

in

the

event

of

an

act

of

default,

the

vendor

could

still

regain

possession

of

the

property

by

utilizing

the

common

law

remedy

of

rescission.

If

held

to

be

a rescission,

the

vendor

would

have

to

return

the

payments

made

by

the

purchasers,

less

a

reasonable

rent,

and

would

therefore

lose

money

that

could

otherwise

be

retained

if

there

were

a

valid

forfeiture

clause.

Assuming

the

installment

contract

did

contain

a

forfeiture

clause,

upon

an

act

of

default

by

the

purchasers

which

under

the

terms

of

the

installment

contract

must

have

entitled

the

vendor

to

declare

a

forfeiture,

the

vendor

was

required

to

give

the

purchasers

notice

that

they

had thirty

days

to

cure

all

defaults

under

the

dontract.

When

that

time

period

had

expired,

the

vendor

was

then

required

to

serve

the

purchasers

with

a

declaration

of

forfeiture

and

a

demand

for

possession.

This

completed

the

forfeiture,

and the

vendor

could

then

oust

the

purchasers

under the

Forcible

Entry

and

Detainer

Act.

The

ease

with

which

this

procedure

could

be

accomplished,

plus

the

resulting

loss

of

equity

accumulated

by

the

buyers,

are

two

reasons

for

the

historical

aversion

of

courts

to

forfeiture

of

any

kind.

They

are

also

the

primary

reasons

why

the

Illinois

General Assembly

changed

the

law.

Unfortunately,

however,

the

contract

forms

com-

3.

The

law

and

practice

are

explained

in

expert

detail

in

a pamphlet

issued

by

the

Chicago

Title

and

Trust

Company,

entitled

P.

HESS,

FoREITusR

OF INSTALLMENT

CONTRACTS

IN

ILLINOIS

(1981).

This

material

originally

appeared

as

Chapter

3

of

the

book,

2

REAL

ESTATE

LITIGATION;

PLEADINGS

AND

PRACTICE,

published

by

the

Illinois

Institute

of

Continuing

Legal

Education.

For

a

more

complete

understanding

of

the

material

in

this

commentary,

careful

reading

of

this

fine

article

by

Peter

Hess

is

advised.

See

also

Kratovil,

Forfeiture

of

Installment

Contracts

in

Illinois,

53

ILL.

B.J.

188

(1964).

[Vol.

9

FILLING

IN

THE

GAPS

monly

used

to

effectuate

such

installment

contracts

have

not

kept

pace

with

the

changes

in

the

law.

III.

FoRMs

CURRENTLY

IN

USE

There

are

many

printed

forms

of

Illinois

installment

contracts,

4

and

while

identification

of

every

potential

problem

is

impossible,

there

are

several

provisions

contract

forms

should

contain

to

comply

with

the

new

law.

For

example,

some

of

these

forms

should,

but

fail

to

include

the

acceleration

clause,

thus

drawing

attention

to

it$

absence.

Without

an

acceleration

clause,

the

remaining

unpaid

balance

does

not

become

due

when

payments

fall

behind,

only

the

amount

actually

in

default.

It

is

important

to

note

that

there

is

no

right

to

accelerate

unless

the

contract

so

provides.'

As

mentioned,

courts

have

a

great aversion

to

forfeiture

of

any

kind.

It

is

also

fairly

clear

that

an

anti-forfeiture

clause

of

the

type

contained

in

the

new

statute

cannot

be

waived.

6

To

understand

the

importance

of

including

an

acceleration

clause

in

an installment

contract,

consider

a

situation

in which

the

contract

is

silent

on

the

issue,

yet

the

vendor,

in

declaring

a

forfeiture,

seeks

to

accelerate

and

demands

payment

of

the

entire purchase

price.

There

appear

to

be

no

decisions

directly

on

point

in

Illinois,

and

the

decisions

outside

of

Illinois

are conflicting.

Under

one

view,

such

a

forfeiture

would

be

void.

In

Rader

v.

Taylor,

7

defendants

had

purchased

real

estate

on

an installment

basis.

When

they later

defaulted,

plaintiffs

attempted

to

accelerate,

although

the installment

contract

contained

no

acceleration

agreement.

8

The

Montana

Supreme

Court

strictly

construed

the

contract,

and

held

that

acceleration

would

not

be

allowed

where

the

contract

does

not

so

provide.

9

The

dissent

in

Rader

cited

Illinois

decisions

it

claimed

support

the

opposite

conclusion.'

0

4.

The

one

often

used

by

many Chicago

lawyers

is

George

E.

Cole

Form

No.

74.

This

form, and a

critique

thereof

are

included

at

the

end

of

this

commentary

as

Appendices

A

and

B,

respectively.

These

I

distribute to

my

classes

at John

Marshall.

The

defects

of

special

interest

are

in

paragraph

11

of

Form

74.

5.

See,

e.g.,

92

C.J.S.

Vendor

and

Purchaser

§

422

(1955);

77

A.L.R.

290

(1932).

6.

See

17

AM.

JUR.

2D

Contracts

§

173

(1964).

7. 134

Mont.

419,

333

P.2d

480

(1958).

8.

Rader

v.

Taylor,

134

Mont.

419,

428,

333

P.2d

480,

486

(1958).

9.

Id.

10.

Montana

Wheat

Land

Co.

v.

Northern

Pac.

Ry.

Co.,

308

Ill. 620,

139

N.E.

876

(1923)

(vendor's

notice

of

intention

to

forfeit

misstated

the

amount

necessary

to reinstate

the

contract);

Forest

Preserve

Real

Estate

Improvement

Corp.

v.

Miller,

1989:349]

NORTHERN

ILLINOIS

UNIVERSITY

LA

W

REVIEW

In

point

of

fact,

the

Illinois

decisions

cited

deal

with

minor

errors

stating

the

amount

due,

and

not

with

acceleration.

The

dissent

also

cited

Iowa,

Washington,

and

California

decisions

as

supporting

its

position

that

if

there

was

any

delinquency,

the

vendor

may

forfeit."

The dissent

is

clearly

wiong.

The

problem

with

the

dissent's

position

is

that

an

unsophisticated

purchaser

may

simply

concede

defeat

if

he

receives

notice

calling

on

him

to

pay

a

vast

sum

of

money.

In

this

age

of

consumerism,

I

believe

that

the

majority

opinion

in

Rader

states

the

law

correctly.

The

wise

practitioner

should

avoid

the

uncertainty

of

how

courts

will

deal

with

forfeiture

where

there

is

no

acceleration

clause.

Such

a

provision,

therefore,

should

be

incorporated

into

every

installment

contract.

The

question

becomes

how

to

go

about

drafting

these

provisions.

IV.

FEDERAL

NATIONAL

MORTGAGE

ASSOCIATION

(FNMA)

PROVISIONS

In

view

of

the

national

approbation

given

FNMA

forms,

it would

seem

desirable

to

follow

their

language

as

much

as

possible

in

drafting

an

acceleration

clause

for

the

installment

contract.

The present

FNMA

Fixed

Rate

Note

for

a single-family

dwelling

provides,

in

part:

6.

BORROWER'S

FAILURE

TO

PAY

AS

REQUIRED

(A)

Late

Charge

for

Overdue

Payments

If

the

Note

Holder

has

not

received

the

full

amount

of

any

monthly

payment

by

the

end

of

-calendar

days

after

the date

it

is

due,

I

will

pay

a

late

charge

to

the Note

Holder.

The

amount

of

the

charge

will

be

_%

of

my

overdue

payment

of

principal

and

interest.

I

will

pay

this

late

charge

promptly

but

only

once

on

each

late

payment.

379

Ill.

375,

41

N.E.2d

526

(1942)

(vendor's

notice

which

was

challenged

as

insuffi-

cient

demanded

payment

for

taxes

which

were

not

due

under

the

contract)

cited

in

Rader

v.

Taylor,

134

Mont.

419,

440-41,

333

P.2d

480,

492-93

(1958)

(Adair,

J.,

dissenting).

11.

See

Rader,

134

Mont.

at

441-42,

333

P.2d

at

493

(Adair,

J.,

dissenting)

(citing

Gibson

v.

Thode,

209

Iowa

368,

228

N.W.

92

(1929))

(notice

of

past

interest

due

was

sufficient

notice

for

possible

forfeiture);

Harris

v.

Seattle

Land

&

Improve-

ment

Co.,

122

Wash.

323,

211

P.

282

(1922)

(notice

of

forfeiture

not

defective

where

it

demands

more

money

than

is

actually

owed);

Adams

&

McKee

Land

Co.

v.

Dugan,

68

Cal.

App.

226, 228

P.

681

(2d

Dist.

1924)

(notice

to

vendee

of

intention

to

enforce

"time

is

of

the

essence"

clause,

and potential

forfeiture

thereunder

was

sufficient

to

revive

the

"time

of

the

essence"

clause).

[Vol.

9

FILLING

IN

THE

GAPS

(B)

Default

If

I

do

not

pay

the

full

amount

of

each

monthly

payment

on

the

date

it

is

due,

I

will

be in

default.

(C)

Notice

Of

Default

If

I

am

in

default,

the

Note

Holder

may send

me

a

written notice

telling

me

that

if

I

do

not

pay

the

overdue

amount

by

a

certain date,

the Note

Holder

may

require

me

to

pay

immediately

ihe

full

amount

of

principal

which

has

not

been

paid and

all

the

interest

that

I

owe

on

that

amount.

That

date

must

be

at

least

30

days

after

the date

on

which

the

notice

is

delivered

or

mailed

to

me.

(D)

No

Waiver

By

Note

Holder

Even

if,

it

a

time

when

I

am

in default,

the Note

Holder

does

not

require

miie

to

pay

immediately

in

full

as

described

above,

the

Note

Holder

will

still

have

the

right

to

do

so

if

I

am

in

default

at

a

later

time.

(E)

Payment

of

Note

Holder's

Costs

and

Expenses

If

the Note

Holder

has

required

me

to

pay immediately

in

full

as

described

above,

the

Note

Holder

will

have

the

right

to

be

paid

back

by

me

for

all

of

its

costs

and

expenses

in

enforcing

this

Note

to

the

extent

not

prohibited

by

applicable

law.

Those

expenses

include,

for

example,

reasonable

attorneys'

fees.

7.

GIVING OF

NOTICES

Unless

applicable

law

requires

a different method,

any

notice

that

must

be

given

to

me

under

this

Note

will

be

given

by

delivering

it

or

by

mailing

it

by

first

class

mail

to

me

at

the

Property

Address

above

or

at

a

different

address

if

I

give

the

Note

Holder

a

notice

of

my

different

address.

Any notice

that

must

be given

to

the Note

Holder under

this

Note

will

be

given

by

mailing

it by

first

class

mail

to

the

Note

Holder

at

the address

stated

in

Section

3(A)

above

or

at

a

different

address

if

I

am

given

notice

of

that

different

address.

1

2

The Illinois

FNMA

Non-Uniform

acceleration

and

foreclosure

covenant

for

residential mortgages

provides:

Non-Uniform

Covenants.

Borrower

and

Lender

further

cove-

nant

and

agree

as

follows:

19.

Acceleration;

Remedies.

Lender

shall

give

notice

to

Bor-

rower

prior

to

acceleration

following

Borrower's

breach

of

any

cov-

12.

Federal

National

Mortgage

Association

(FNMA)

Multistate

Fixed

Rate

Note

Form

3200

(Dec.

1983).

A

copy

of

this form

is

contained

in

Appendix

C

of

this

commentary.

1989:3491

NORTHERN ILLINOIS

UNIVERSITY

LAW

REVIEW

enant

or

agreement

in

this Security

Instrument

(but

not

prior

to

acceleration

under

paragraphs

13

and

17

unless

applicable

law

provides

otherwise).

The

notice

shall

specify:

(a)

the

default;

(b)

the

action

required

to

cure

the

default;

(c)

a

date,

not

less

than

30

days

from

the

date

the

notice

is

given

to

Borrower,

by

which

the

default

must

be

cured;

and

(d)

that

failure

to

cure

the

default

on

or

before

the

date

specified

in

the

notice

may

result

in

acceleration

of

the

sums

secured

by

this

Security

Instrument,

foreclosure

by

judicial

proceeding

and

sale

of

the

Property.

The

notice

shall

further

inform

Borrower

of

the

right

to

reinstate

after

acceleration

and

the

right

to

assert

in

the

foreclosure

proceeding

the

non-existence

of

a

default

or

any

other

defense

of

Borrower

to

acceleration

and

foreclosure.

If

the

default

is

not

cured

on

or

before

the

date

specified

in

the

notice,

Lender

at

its

option

may

require

immediate

payment

in

full

of

all

sums

secured

by

this

Security

Instrument

without

further

demand

and

may

foreclose

this

Security

Instrument

by

judicial

proceeding.

Lender

shall

be

entitled

to

collect

all

expenses

incurred

in

pursuing

the

remedies

provided

in

this

paragraph

19,

including,

but

not

limited

to

reasonable

attorneys'

fees

and

costs

of

title

evidence.

20.

Lender

in

Possession.

Upon

acceleration

under

paragraph

19

or

abandonment

of

the

Property

and

at

any

time

prior

to

the

expiration

Of

any

period

of

redemption

following

judicial

sale,

Lender

(in

person,

by

agent

or

by

judicially

appointed

received)

shall

be

entitled

to

enter

upon,

take

possession

of

and

manage

the

Property

and

to

collect

the

rents

of

the

Property

including

those

past

due.

Any

rents

collected

by

Lender

or

the

received

shall

be

applied

first

to

payment

of

the

costs

of

management

of

the

Property

and

collection

of

rents,

including,

but

not

limited

to,

receiver's

fees,

premiums

on

receiver's

bonds

and'reasonable

attorneys'

fees,

and then

to

the

sums

secured

by

this

Security

Instrument.

13

When

drafting

any

installment

contract,

the

practitioner

should

include

provisions

like

those

listed

above.

However,

when

one

desires

to

comply

with

the

new

Illinois

law,

additional

clauses

should

be

added.

V.

SUGGESTED

PROVISIONS

It

would

seem

desirable

to add

a

rider

to

any

installment

contract

following

roughly

the

following

form:

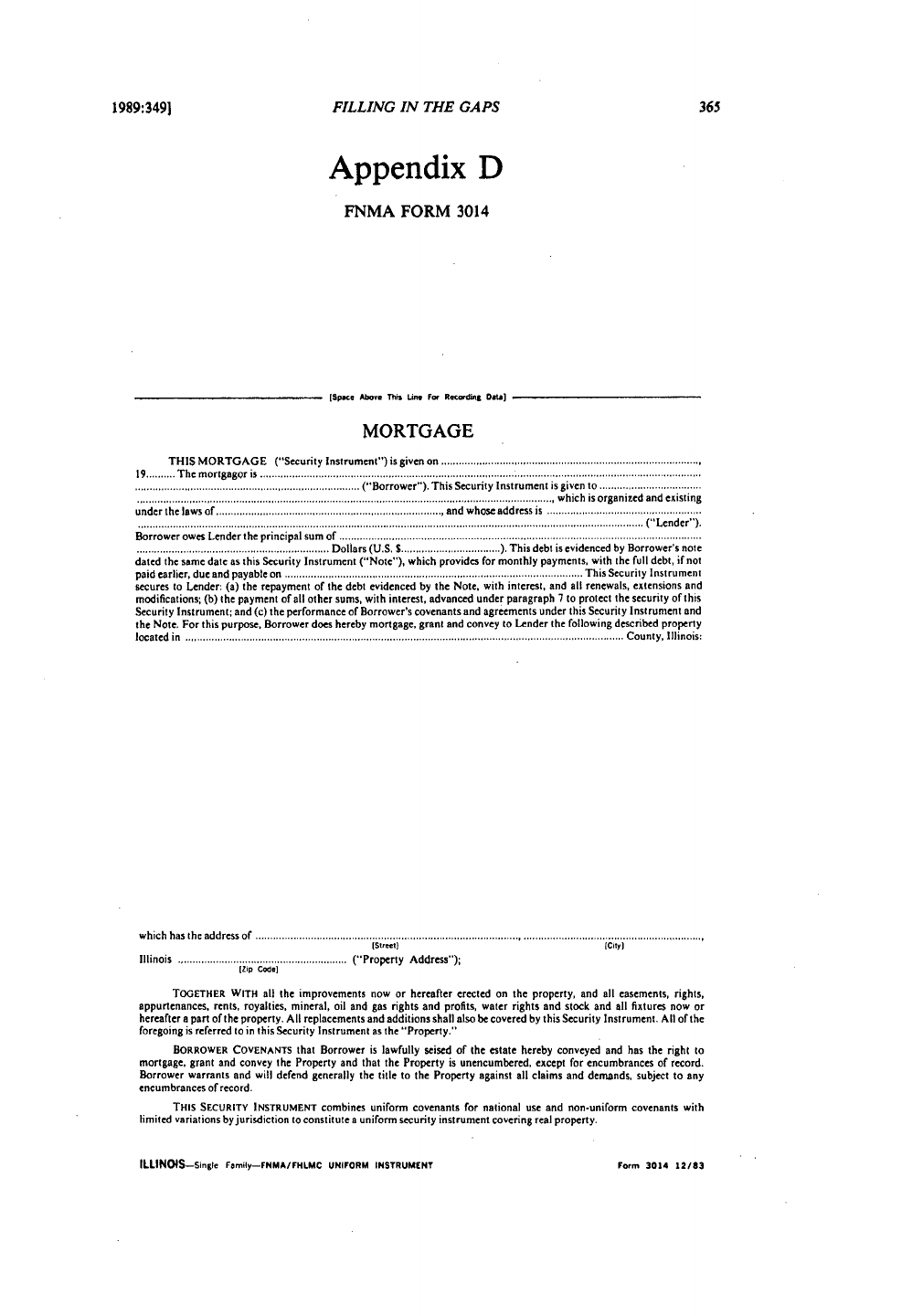

13.

FNMA

Form

3014

(Dec.

1983).

A

copy

of

this

form

is

contained

in

Appendix

D

of

this

Commentary.

[Vol.

9

FILLING

IN

THE

GAPS

In

the

event

of

any

default

in

payment

of

interest

or

principal

hereunder,

or

in

the

event

of

any

breach

of

covenant

herein

contained,

the

vendor

shall

have

as

an

additional

remedy

hereunder,

exercisable

at

his

option,

the

following

remedy:

Vendor

shall

give

notice

to

Purchaser

prior

to

acceleration

following

Purchaser's

breach

of

any

covenant

or

agreement

in

this

contract.

The

notice

shall

specify:

(a)

the

default;

(b)

the

action

required

to

cure

the

default;

(c)

a

date,

not

less

than

thirty

days

from

the

date

the

notice

is

given

to

Purchaser,

by

which

the

default

must

be

cured;

and

(d)

that

failure

to

cure

the

default

on

or

before

the

date

specified

in

the

notice

may

result

in

acceleration

of

the

sums

due

or

to

become

due

under

this

contract

secured

by

this

contract

and

foreclosure

by

judicial

proceeding

and

sale

of

the

property.

The

notice

shall

further

inform

Purchaser

of

any

right

to

reinstate

after

accel-

eration

and

the

right

to

assert

in

the

foreclosure

proceeding

the

non-existence

of

a

default

or

any

other

defense

of

Pur-

chaser

to

acceleration

and

foreclosure.

If

the

default

is

not

cured on

or

before

the

date

specified

in

the

notice,

Vendor

at

its

option

may

require

immediate

payment

in

full

of

all

sums

secured

by

this

contract

without

further

demand

and

may

foreclose

this

contract

by

judicial

proceeding.

Vendor

shall

be

entitled

to

collect

all

expenses

incurred

in

pursuing

the

remedies

provided

in

this

paragraph,

including,

but

not

limited

to,

reasonable

attorneys'

fees

and

costs

of

title

evidence.

In

any

such

foreclosure,

the

procedure

shall

be

as

set

forth

in

Public

Act

84-1462

or

as

hereafter

amended

and

Vendor

shall have

all

the

rights

and

remedies

available

under

a

mortgage

foreclosure

under

that

statute.

This

comprehensive

provision

brings

the

installment

contract

into

compliance

with

the

Act,

and

explicitly

provides

that

the

Act

is

to

govern

in

the

event

of

a

foreclosure.

Such

a clause,

however,

may

not

be

sufficient

if

the

mortgage

in

question

is

one

covering

residential

real

estate.

VI.

RESIDENTIAL

REAL

ESTATE

DEFINED

Residential

real

estate,

which

is

subject

to

this

foreclosure

clause,

is

defined

in

paragraph

15-1219.14

Many

installment

contract

forms,

14.

Residential

Real

Estate.

'Residential

real

estate'

means

any

real

estate,

except

a single

tract

of

agricultural

real

estate

consisting

of

more

than

40

1989:3491

NORTHERN

ILLINOIS

UNIVERSITY

LAW

REVIEW

however,

do

not

identify

the

property

as

residential

real

estate.

Therefore,

if

the

contract

is

used

as

printed,

acceleration

is

impossible.

Thus,

the

contract

should

provide,

if

that

is

the

case,

that

the

land

is

residential

real

estate

as

defined

in

paragraph

15-1219

of

the

Act.

VII.

INSTALLMENT

CONTRACT

AS

MORTGAGE

Another

problematic

provision

is

paragraph

15-1107

of

the

Act,

which

provides

that

a

real

estate

installment

contract

that

must

be

foreclosed

shall

be

deemed

a

mortgage

and

the

vendor

shall

be

deemed

a

mortgagee

and

the

purchaser

a

mortgagor.

This

is

all

well

and

good,

but

there

are

hundreds

of

mortgage

forms

and

notes.

The

problem

is

finding

a form

that

conforms

with

the

provisions

of

the

Act.

It

is

suggested

that

the

current

Illinois

FNMA

Mortgage

and

Mortgage

Note

at

the

time

the

contract

is

made

be

appended

as

exhibits

and

that

the

contract

contain

some

clause

to

this

effect:

Once

foreclosure

has

been

instituted,

the

Vendor

shall

be

treated

as

a

Mortgagee

and

the

Purchaser

shall

be

deemed

a

Mortgagor

just

as

if

the

parties

had

executed

such

document

as

part

of

the

contract

transaction,

and

each

of

the

parties

shall

have

all

the

rights,

duties

and

obligations

as

though

fully

set

forth

in

the

contract.

Where

there

is

a

conflict

between

the

provisions

of

the

installment

contract

and

the

provisions

of

the

appended

mortgage

and note,

the

provisions

of

the

mort-

gage

and note

shall

prevail,

except

to

the

extent

that

they

vary

from

the

provisions

of

said

Act,

in

which

case

the

law

as

set

forth

in

the

Act

shall

prevail.

This

incorporation

shall

include

all

riders

appended

to the

mortgage

and

note.

acres,

which

is

improved

with

a

single

family

residence

or

residential

condominium

units

or

a

multiple

dwelling

structure

containing

single

family

dwelling

units

for

six

or

fewer

families

living

independently

of

each

other,

which

residence,

or

at

least

one

of

which

condominium

or

dwelling

units,

is

occupied

as

a

principal

residence

either

(i)

if

a

mortgagor

is

an

individual,

by

that

mortgagor,

that

mortgagor's

spouse

or

that

mortgagor's

descendants,

or

(ii)

if

a

mortgagor

is

a

trustee

of

a

trust

or

an executor

or administrator

of

an

estate,

by

a

beneficiary

of

that

trust

or

estate or

by

such

beneficiary's

spouse

or

descendants

or

(iii)

if

a

mortgagor

is

a

corporation,

by

persons

owning

collectively

at

least

50

percent

of

the

shares

of

voting

stock

of

such

corporation

or

by a

spouse

or

descendants

of

such

persons.

The

use

of

a

portion

of

residential

real

estate

for

non-residential

purposes

shall

not

affect

the

characterization

of

such

real

estate

as

residential

real

estate.

ILL.

REv.

STAT.

ch.

110,

para.

15-1219

(Supp.

1987)

(effective

July

1,

1987).

[Vol.

9

FILLING

IN

THE

GAPS

The

contract

should

further

provide

that

the

parties

have expressly

agreed

that

if

the

contract

at

the

time

of

foreclosure

is

one

that

must

be

foreclosed

under the

Act,

the

conversion

of

the

contract

into

a

note

and mortgage

cannot

be

reversed,

and

the

transaction

shall

be

governed

by

the

mortgage

law

of

Illinois.

VIII.

RECORD

NOTICE

Lastly,

once

foreclosure

is

filed,

the

practitioner

should

be

sure

to

file

the

recorded

notice

required

by

paragraph

15-1218.11

IX.

PRIORITIES,

PROCEDURE,

POSSESSION

&

INSURANCE

The

contract

should

also

provide

that

once

foreclosure

is

filed,

the

lien

of

the

mortgage

shall

relate

back

to

the date

of

the recording

of

the

contract.

16

Further,

such

lien

shall

be

entitled

to

priority

as

of

such

date, for

the

mortgage

debt and

all

expenses

incurred

by

the

mortgagee

to

maintain

the

security

of

his lien,

including

those

set

forth

in

paragraph

15-1302

of

the

Act.'

7

15.

Recorded

Notice.

"Recorded

notice"

with respect

to

any

real

estate

means

(i)

any

instrument

filed

in

accordance

with

§§

2-1901

or

12-101

of

the

Code

of

Civil

Procedure

or

(ii)

any

recorded

instrument

which

discloses

(a)

the

names

and

addresses

of

the

persons

making

the

claim

or

asserting

the

interest

described

in

the

notice;

(b)

that

such

persons

have

or

claim

some

interest

in

or

lien

on

the

subject

real

estate;

(c)

the

nature

of

the

claim;

(d)

the

names

of

the

persons

against

whom

the

claim

is

made;

(e)

a

legal

description

of

the

real

estate

sufficient

to

identify

it with

reasonable

cer-

tainty;

(f)

the

name

and

address

of

the

person

executing

the

notice;

and

(g)

the

name

and

address

of

the

person

preparing

the

notice.

Id.

at

para.

15-1218.

16.

This

is

standard

mortgage

law.

See

80

A.L.R.2D

191,

196,

199,

217,

219

(1961).

17.

Certain

Future

Advances.

(a)

Advances

Made

After

Eighteen

Months.

Except

as

provided

in

subsection

(b)

of

Section

15-1302,

as

to

any monies

advanced

or applied

more

than

18

months

after

a

mortgage

is

recorded,

the

mortgage

shall

be a

lien

as

to

subsequent

purchasers

and

judgment

creditors

only

from

the

time such

monies are

advanced

or

applied.

However,

nothing

in

this

Section

shall

affect

any

lien

arising

or

existing

by

virtue

of

the

Mechanics'

Lien

Act.

(b)

Exceptions.

(1)

All

monies

advanced

or applied

pursuant

to

commitment,

whenever

advanced

or applied,

shall

be a

lien

from

the

time

the

mortgage

is

recorded.

An

advance

shall

be

deemed

made

pursuant

to

commitment

only

if

the

mortgagee

has

bound

itself to

make

such

advance

in

the

mortgage

or

in

an

instrument

executed

contemporaneously

with,

and

referred

to

in,

the

mort-

gage,

whether

or

not

a

subsequent

event

of

default

or

other

event

not

within

1989:349]

NORTHERN

ILLINOIS

UNIVERSITY

LAW

REVIEW

In

addition,

the

installment

contract

should

provide

that,

where

applicable,

the

judicial

process,

judgment,

redemption

and

sale

shall

be

as

set

forth

by

the

Act.

It

may

also

be

necessary

to

include

a

provision

stating

that,

where

applicable,

the

rights

of

possession

shall

be

as

set

forth

in

the

Act

and

in

the

Agreement.

Finally,

since

the

status

of

the

parties

changes

from

vendor

and

purchaser

to

mortgagee

and

mortgagor,

changes

should

be

made

in

the

property

insurance,

and

the

usual

foreclosure

minutes

offered

by

the

title

companies

should

be

employed.

X.

CONCLUSION

Drastic

changes

in

Illinois

foreclosure

law

have

made

current

real

estate

forms

inadequate

to

cover

the provisions

of

that

law.

The

remedies

suggested

here

are

somewhat

makeshift,

and

should

have

been

dealt

with

in

the

comments

to

the

statute.

I

have

drawn

attention

to

this defect

and submit

this

commentary

only

in

the hope

that

it

arouses

the

attention

of

the bar and

produces

better

documentation.

the

mortgagee's

control

has

relieved

or

may

relieve

the

mortgagee

from

its

obligation.

(2)

All

monies

advanced

or

applied,

whenever

advanced

or applied,

in

accordance

with

the

terms

of

a

reverse

mortgage

shall

be

a

lien

from

the

time

the

mortgage

is

recorded.

(3)

All

monies

advanced

or applied

in

accordance

with

the

terms

of

a

revolving

credit

arrangement

secured

by a

mortgage

as

authorized

by

law

shall

be

a

lien

from

the

time

the

mortgage

is

recorded.

(4)

All

interest

which

in

accordance

with

the

terms

of

a

mortgage

is

accrued

or

added

to

the

principal

amount

secured

by

the

mortgage,

whenever

added,

shall

be

a

lien

from the

time

the

mortgage

is

recorded.

(5)

All

monies

advanced

by

the mortgagee

in

accordance

with

the terms

of

a

mortgage

to

(i)

preserve

or

restore

the

mortgaged

real

estate,

(ii)

preserve

the

lien

of

the

mortgage

or

the

priority

thereof

or

(iii)

enforce

the

mortgage,

shall

be a

lien

from

the

time

the

mortgage

is

recorded.

ILL.

REv.

STAT.

ch.

110,

para.

15-1302

(Supp.

1987)

(effective

July

1,

1987)

(footnote

omitted).

[Vol.

9

1989:349]

FILLING

IN

THE

GAPS

359

Appendix

A

COLE

FORM

74**

INSTALLMENT

AGREEMENT

NO.

74

GEORGE

E.

COLE

FOR

WARRANTY

DEED

Febna",

1985

LEGAL

FORMS

(ILLINOIS)

cAunn:

CoNui •

t*kl:

Ware actog

neW

-NOs w4

O0 , to

NW it w

aW

,s N

,nal*

ma

tflnr

Ott ,.t

giantetcwe

enam ,n,,ent

at rctn~mntaatvo

tness

toaact

n~uaa

AGREEMENT,

made

this

day

of

................

19

between

.. .

. Seller.

and

Purchaser:

WITNESSETH.

that if

Purchaser

shall

first

make

the

payments

and

perform

Purchaser's

covenants

hereunder.

Seller

hereby

covenants

and

agrees

to

convey

to Purchaser

in

fee

simple

by

Seller's

recordable

warranty

deed,

with

waiver

of

homestead,

subject

to

the

matters

hereinafter

specified,

the

premises

situated

in the

County

of

__

and State

of_

described

as

follows:

Permanent

Real

Estate

Index

Number(s):

Address(es)

of

premises:

and

Seller

further

agrees

to furnish

to

Purchaser

on

or

before

, 19

-,•

at

Seller's

expense.

the

following

evidence

of

title

to

the

premises:

(a)

Owners

title

insurance

policy

in

the

amount

of

the

price,

issued

by

,

(b)

certificate

of

title

issued

by

the

Registrar

of

Titles

of

Cook

County,

Illinois,

(c)

merchantable

abstract

of

title',

showing

merchantable

title

in

Seller

on

the

date

hereof,

subject

only

to

the

matters

specified

below

in

paragraph

1.

And

Purchaser

hereby

covenants

and

agrees

to

pay

to

Seller,

at

such

place

as

Seller

may

from

time

to time

designate

in

writing,

and

until

such

designation

at

the

office

of

the

price

of

Dollars

in

the

manner

following,

to-wit:

with

interest

at

the

rate

of

per

cent

per

annum

payable

on

the

whole

sum

remaining

from

time

to

time

unpaid.

Possession

of

the

premises

shall

be

delivered

to

Purchaser

on

, provided

that

Purchaser

is

not

then

in

default

under

this

agreement.

Rents,

water

taxes,

insurance

premiums

and

other

similar

items

are

to

be

adjusted

pro

rata

as

of

the

date

provided

herein

for

delivery

of

possession

of

the

premises.

General

taxes

for

the year

19

-.

are

to

be

prorated

from

January

I to

such

date

for

delivery

of

possession,

and

if

the

amount

of

such

taxes

is

not

then ascertainable,

the

prorating

shall

be

done

on

the

basis

of

the

amount

of

the

most

recent

ascertainable

taxes.

It

is

further

expressly

understood

and

agreed

between

the

parties

hereto

that:

1.

The

Conveyance

to

be

made

by

Seller

shall

be

expressly

subject

to

the

following:

(a)

general

taxes

for

the

year

and

subsequent

years

and

all

taxes,

special

assessments

and

special

taxes

levied

after

the

date

hereof;

(b)

all

installments

of

specia

assessments

heretofore

levied

falling

due

after

date

hereof;

(c)

the

rights

of

all

persons

claiming

by,

through

or

under

Purchaser;

(d)

easements

of

record

and

party-walls

and

party-wall

agreements,

if

any;

(e)

building,

building

line

and

use

or

occupancy

restrictions,

conditions

and

covenants

of

record,

and

building

and

zoning

laws

and

ordinances;

(f)

roads,

highways,

streets

and

alleys,

if

any;

2.

Purchaser

shall

pay

before

accrual

of

any

penalty

any

and

all

taxes

and

installments

of

special

assessments

pertaining

to

the

premises

that

become

payable

on

or

after

the

date

for

delivery

of

possession

to

Purchaser,

and

Purchaser

shall

deliver

to

Seller

duplicate

receipts

showing

timely

payment

thereof.

.

3.

Purchaser

shall

keep

the

buildings

and

improvements

on

the

premises

in

good

repair

and

shall

neither suffer

nor commit

any

waste

on

or

to

the

premises,

and

if

Purchaser

fails

to

make

any

such

repairs

or

suffers

or

commits

waste

Seller

may

elect

to

make

such

repairs

or

eliminate

such

waste

and the

cost

thereof

shall

become

an

addition

to

the

purchase

price

immediately

due

and

payable

to Seller,

with

interest

at

-

per

cent

per

annum

until

paid.

4.

Purchaser

shall

not

suffer

or

permit

any

mechanic's

lien

or other

lien

to

attach

to

or

be

against

the

premises,

which

shall

or

may

be

superior

to

the

rights

of

Seller.

5. Every

contract

for

repairs

and

improvements

on

the

premises,

or

any

part

thereof,

shall contain

an

express,

full

and

complete

waiver

and

release

of

any and

all

lien

or

claim

or

right

of

lien

against

the

pfemises

and

no

contract

or

agreement,

Oral

or written,

shall

be

made

by

Purchaser

for

repairs

or

improvements

upon

the premises,

unless

it

shall

contain

such

express

waiver

or

release

of

lien

upon

the

part

of

the

party

contracting,

and

a

signed

copy

of

every

such

contract

and

of

the plans

and

specifications

for

such

repairs

and

improvements

shall

be

promptly

delivered

to

and

may

be

retained

by

Seller.

6.

Purchaser

shall

not

transfer

or

assign

this

agreement

or

any

interest

therein,

without

the

previous

written

consent

of

Seller,

and

any

such

assignment

or

transfer,

without

such

previous

written

consent,

shall

not

vest

in

the

transferee

or

assignee

any

right,

title

or

interest

herein

or

hereunder

or

in

the premises,

but

shall

render

this

contract

null

and

void,

at

the

election

of

Seller;

and

Purchaser

will

not

lease

the premises,

or

any

part

thereof,

for

any

purpose,

without

Seller's

written

consent.

7.

No

right,

title

orinterest,

legal

or

equitable,

in

the

premises,

or

any

part

thereof,

shall

vest

in

Purchaser

until

the

delivery

of

the

deed

aforesaid

by

Seller,

or until

the

full

payment

of

the purchase

price

at

the

times

and in

the

manner

herein

provided.

8.

No

extension,

change,

modification

or

amendment

to

or

of

this

agreement

of

any

kind

whatsoever

shall

be

made

or

claimed

by

Purchaser,

and

no

notice

of

any

extension,

change,

modification

or

amendment,

made

or

claimed

by

Purchaser,

shall

have

any force

or

effect

whatsoever

unless

it shall

be

endorsed

in

writing

on

this

agreement

and

be

signed

by

the

parties

hereto.

'Stike.

nut all

but one

ofthe

clauses

(a), (b)

and (c).

**

Reprinted

with

permission

of

Boise

Cascade,

Office

Products

Division.

NORTHERN

ILLINOIS

UNIVERSITY

LAW

REVIEW

[Vol.

9

9.

Purchaser

shall

keep

all

buildings

at

any

time

on the

premises

insured

in

Seller's

name

at

Purchaser's

expense

against

loss

by

fire,

lightning,

windstorm

and

extended

coverage

risks

in

companies

to

be

approved

by

Seller

in

an

amount

at

least

equal

to

the

sum

remaining

unpaid

hereunder,

which

insurance,

together

with

all additional

or

substituted

insurance,

shall

require

all

payments

for

oss

to

be

applied

on

the

purchase

price,

and

Purchaser

shall

deliver

the

policies

therefor

to

Seller.

10.

If

Purchaser

fails

to

pay

taxes,

assessments,

insurance

premiums

or

any

other

item

which

Purchaser

is

obligated

to

pay

hereunder,

Seller

may

elect

to

pay

such

items

and

any

amount

so

paid

shall

become

an

addition

to

the

purchase

price

immediately

due and

payable

to

Seller,

with

interest

at

__

per

cent per annum

until

paid.

II.

In

case

of

the

failure

of

Purchaser

to

make

any

of

the

payments,

or

any

part

thereof,

or perform

any

of

Purchaser's

covenants

hereunder,

this

agreement

shall,

at

the

option

of

Seller,

be

forfeited

and

determined,

and

Purchaser

shall

forfeit

all

payments

made

on

this

agreement,

and

such

payments

shall

be

retained

by

Seller

in

full

satisfaction

and

as

liquidated

damages

y

Seller

sustained,

and

in

such

event Seller

shall

have

the

right

to

re-enter

and

take

possession

of

the

premises

aforesaid.

12.

In

the

event

this

agreement

shall

be

declared

null

and

void

by

Seller

on

account

of

any

default,

breach

or

violation

by

Purchaser

in

any

of

the

provisions

hereof,

this

agreement

shall

be

null

and

void

and

be

so

conclusively

determined

by

the

filing

by

Seller

of

a

written

declaration

of

forfeiture

hereof

in

the

Recorder's

office

of

said

County.

13.

In

the

event

of

the

termination

of

this

agreement

by

lapse

of

time,

forfeiture

or

otherwise,

all

improvements,

whether

finished

or

unfinished,

which

may

be

put

upon

the

premises

by

Purchaser

shall

belong

to

and

be

the

property

of

Seller

without

liability

or

obligation

on

Seller's

part

to

account

to

Purchaser

therefor

or for

any

part

thereof.

14.

Purchaser

shall pay

to

Seller

all

costs

and

expenses,

including

attorney's

fees,

incurred

by

Seller

in

any

action

or

proceeding

to

which

Seller

may

be

made

a

party

by

reason

ofbeing

a

party

to

this

agreement,

and Purchaser

will

pay

to

Seller

all

costs

and

expenses,

including

attorney's

fees,

incurred

by

Seller

in

enforcing

any

of

the

covenants

and

provisions

of

this

agreement

and

incurred

in

any

action

brought

by

Seller

against

Purchaser

on

account

of

the

provisions

hereof,

and

all

such

costs,

expenses

and

attorney's

fees

may

be

included

in

and

form

a

part

of

any

judgment

entered

in

any

proceeding

brought

by

Seller

against

Purchaser

on

or

under

this agreement.

15.

The

remedy

of

forfeiture

herein

given

to

Seller

shall

not

be

exclusive

of

any

other

remedy,

but

Seller shall,

in

case

of

default

or

breach,

or

for

any

other

reason

herein contained,

have

every

other

remedy

given

by

this

agreement

or

by

law

or

equity,

and

shall

have

the

right to

maintain

and

prosecute

any

and

every

such

remedy,

contemporaneously

or

otherwise,

with

the

exercise

of

the

right

of

forfeiture,

or

any

other right

herein given.

16.

Purchaser

hereby

irrevocably

constitutes

any

attorney

of

any

court

of

record,

in

Purchaser's

name,

on

default

by

Purchaser

of

any

of

the

covenants

and

agreements

herein,

to

enter

Purchaser's

appearance

in

any

court

of

record,

waive

process

and

service

thereof

and

confess

judgment

against Purchaser

in

favor

of

Seller,

or

Seller's

assigns,

for

such

sum

as

may

e

due,

together

with

the

costs

of

such

suit,

including

reasonable

attorney's

fees,

and

to waive

all

errors

and

right

of

appeal

from

such

judgment

or

judgments;

Purchaser

hereby

expressly

waiving

all

right

to

any

notice

or

demand

under

any

statute

in

this

State

with

reference

to

such

suit

or

action.

If

there

be

more

than

one

person above

designated

as

"Purchaser"

the

power

and

authority

in

this

paragraph

given

is

given

by such

persons

jointly

and

severally.

17.

If

there

be

more

than

one

person

designated

herein

as

"Seller"

or

as

"Purchaser",

such

word

or

words

wherever

used

herein

and the

verbs

and

pronouns

associated

therewith,

although

expressed

in

the

singular,

shall

be

read

and

construed

as

plural.

18.

All

notices

and

demands

hereunder

shall

be

in

writing.

The

mailing

ofa

notice

or

demand

by

registered

mail

to

Seller

at

or

to

Purchaser

at

or

to

the last

known

address

of

either

party,

shall

be

sufficient

service

thereof.

Any

notice

or

demand

mailed

as

provided

herein

shall

be

deemed

to

have

been

given

or

made

on

the

date

of

mailing.

19.

The

time

of

payment

shall

be

of

the

essence

of

this

contract,

and

the

covenants

and agreements

herein

contained

shall

extend

to and

be

obligatory

upon

the

heirs,

executors,

administrators

and

assigns

of

the

respective

parties.

20.

Seller

warrants

to

Purchaser

that

no

notice

from

any

city,

village

or

other

governmental

authority

of

a

dwelling

code

violation

which

existed

in

the

dwelling

structure

before

the

execution

of

this

contract

has

been

received

by

the

Seller,

his

principal

or

his

agent

within

10

years

of

the

date

of

execution

of

this

contract.

21.

If

any

provision

of

this agreement

shall

be

prohibited

by

or invalid

under

applicable

law,

such

provision

shall

be

ineffective

to

the

extent

of

such

prohibition

or invalidity,

without

invalidating

or

affecting

the

remainder

of

such

provision

or

the

remaining

provisions

of

this

agreement.

IN

WITNESS

WHEREOF,

the

parties to

this

agreement

have

hereunto

set

their

hands

and

seals

in

duplicate,

the

day

and

year

first

above

written.

Sealed

and

Delivered

in

the

presence

of

(SEAL)

(SEAL)

(SEAL)

(SEAL)

'0K

II'I

, 00

4I,.

FILLING

IN

THE

GAPS

APPENDIX

B

INSTALLMENT

CONTRACTS

-

COLE

FORM

74

CRITIQUE

Because

the

shortage

of

mortgage

money

seems

destined

to

be

with

us

indefinitely,

a

seller

who

must

sell

his

home

at

times

resorts

to

the installment

contract.

Of

the

forms

most frequently

used, George

E.

Cole

Form

74,

revised

February,

1985

seems

to

be

the

most

popular.

It

is

the form

most

frequently

construed

by

the

Illinois

courts.

Hence

its

provisions

and

these

constructions

are

of

interest

to

all

mortgage

attorneys.

This

form

has been

revised

from

time

to

time.

It

is

therefore

necessary

for

you

to

check

the

language

and

date

of

any

decision

to

determine

whether

you

are

dealing

with

the

present

form

or

an

earlier

and

differing

form.

In

an

earlier

version

of

this

form

there

was

no

explicit

requirement

that

the

purchaser

in possession

pay

the

real

estate

taxes. Hence

our

court

found

that

he

was

under

no

obligation

to

pay

such taxes.

Forest

Preserve

Real

Estate

Improvement

Corp.

v.

Miller,

379

Ill.

375,

41

N.E.2d

526

(1942).

The

current

form

in

purchaser's

covenant

two

requires

a

purchaser

in

possessiony

to

pay

taxes.

For

some

mysterious

reason

this

form

contains

no

acceleration

clause.

Obviously

a

vendor's

attorney

will

insert

an

acceleration

clause.

See

paragraph

eleven

of

Form

74.

Of

course,

even

if

there

is

an

acceleration

clause,

a

vendor

who

accepts

tardy

payments

cannot

accelerate

without

giving

a

warning

notice.

Stinemeyer

v.

Wesco

Farms

Inc.,

260

Ore.

109,

487

P.2d

65

(1971).

Where

there

are

two or

more vendors,

obviously

all

must

join

in

declaring

the

forfeiture.

91

C.J.S.

Vendor

and

Purchaser

§

139(3)

(1955).

I

have discussed

this

at

great

length,

along

with

such

kindred

problems

as

the

right

of

less

than

all

lessors

to

forfeit

the

lease

or

less

than

all

owners

of

a right

of

entry

to

forfeit

for

breach

of

a

condition

in

a

deed.

Kratovil,

Divided

Interests

in

Land:

Enforcement

Problems

under

Modern

Concepts

of

Real

Property

Law,

14

HOUSTON

L.

REv.

583

(1977).